Wasserstein distributionally robust optimization

and its tractable regularization formulations

Abstract

We study a variety of Wasserstein distributionally robust optimization (WDRO) problems where the distributions in the ambiguity set are chosen by constraining their Wasserstein discrepancies to the empirical distribution. Using the notion of weak Lipschitz property, we derive lower and upper bounds of the corresponding worst-case loss quantity and propose sufficient conditions under which this quantity coincides with its regularization scheme counterpart. Our constructive methodology and elementary analysis also directly characterize the closed-form of the approximate worst-case distribution. Extensive applications show that our theoretical results are applicable to various problems, including regression, classification and risk measure problems.

AMS subject classification: 90C15, 90C17, 90C47

Keywords: Wasserstein discrepancy, Wasserstein distributionally robust optimization, regularized optimization, worst-case loss quantity, data-driven decision making.

1 Introduction

A central question of interest in many machine learning and operations research applications is the selection of an appropriate decision variable from a decision space . This often involves minimizing the expected risk of prediction errors, that is,

where is a random variable in a given space , with the probability distribution , and is a loss function. In practice, the ground-truth distribution is usually unknown. Instead, one only has access to an empirical distribution , where is a training dataset, are nonnegative weights satisfying , and is the point mass at . The associated optimization problem

| (1) |

is often known as the empirical risk minimization (ERM) problem (Vapnik and Chervonenkis 2015).

Robustness approach. One major criticism of the ERM problem is that the empirical distribution might differ from the ground-truth distribution considerably, and might be unreliable due to errors in the data collection. This motivated the study of the corresponding distributionally robust optimization problem. Rather than relying on one single distribution , it hedges against a set of distributions in the space of all probabilities on , denoted as . Formally, the distributionally robust optimization (DRO) problem takes the form of solving a minimax problem

Here, the set is referred to as the ambiguity set or uncertainty set, which is often constructed by imposing some statistical conditions on the set of probability distributions under consideration. For example, the moment-based ambiguity set can be defined via certain moment constraints as in Delage and Ye (2010), Goh and Sim (2010), Wiesemann et al. (2014), or as the confidence region of a goodness-of-fit hypothesis test (Bertsimas et al. 2018). Alternatively, the ambiguity set can be constructed as , where is a nonnegative tuning parameter, and defines a certain discrepancy on , such as the Prohorov and total variation metric (Gibbs and Su 2002, Erdoğan and Iyengar 2006), Kullback-Leibler and divergence (Hu and Hong 2013, Jiang and Guan 2016), or Wasserstein metric (Shafieezadeh-Abadeh et al. 2015, Mohajerin Esfahani and Kuhn 2018, Blanchet and Murthy 2019, Gao 2022). These choices of are often named as discrepancy-based ambiguity sets.

In this work, we focus on the ambiguity set based on the Wasserstein discrepancy. Given two probability distributions and an extended nonnegative-valued function , the Wasserstein discrepancy111In this work, we use the term “Wasserstein discrepancy” instead of the commonly-used “Wasserstein metric” in the literature, since here is not required to be a metric. with respect to and an exponent is defined via the optimal transport problem (Villani 2009, Peyré and Cuturi 2017) as

| (2) |

where (Villani 2009, Definition 1.1) denotes the set of all joint probability distributions between and , that is, by letting denote the set of all measurable sets in ,

Intuitively, the Wasserstein discrepancy (2) can be understood as finding the minimum cost to move the mass of to that of . Accordingly, the Wasserstein distributionally robust optimization (WDRO) problem considers the ambiguity set , where is a nonnegative scalar. Formally, the WDRO problem takes the form as

| (3) |

Regularization approach. Another criticism of the ERM problem is that the resulting estimator might exhibit unsatisfactory out-of-sample performance or overfitting phenomena (Plan and Vershynin 2012, Feng et al. 2014). To overcome this deficiency, a common approach is to modify the objective function in the ERM problem (1) by adding a regularization term. Specifically, the regularization scheme takes the form as

where is a nonnegative tuning parameter, is a regularization function. When , there are some popular options for , such as the ridge penalty (Horel 1962, Hoerl and Kennard 1970), the Lasso penalty or its variant combining with a group or a fused penalty (Belloni et al. 2011, Bunea et al. 2013, Stucky and Van De Geer 2017, Jiang et al. 2021). In addition, it is also a topic of interest to study the appropriate value for the tuning parameter . In certain scenarios such as the Lasso and group Lasso problems (Bickel et al. 2009, Lounici et al. 2011), it has been shown that appropriate values of depend on the noise level of the dataset. In response, several works have shown that the optimal can be made independent of the noise level if the original expectation term is replaced by when is the squared loss function (Belloni et al. 2011, Bunea et al. 2013, Stucky and Van De Geer 2017).

Equivalence interpretation. In both the robustness and regularization approaches, one of the key ingredients is the tuning parameter , which essentially controls how conservative the new scheme is compared to the original ERM problem. While the regularization scheme is more tractable and preferable in terms of computational consideration, the WDRO scheme (3) is more favorable in accommodating the geometric structure of the data space via the cost function and the intuitive understanding of the level of robustness via the radius . In order to draw the connections and take into account the advantages of both of them, the equivalence between the WDRO problem and the regularization scheme has received increasing attention over the last few years. Specifically, let

| (4) |

then it aims to study sufficient conditions under which the following equivalence holds:

| (5) |

where , and acts as a penalty on which might also depend on other factors such as and . In particular, the equivalence (5) gives a probabilistic explanation of the penalty parameter in the regularization model based on the WDRO interpretation. Compared to (4) which involves a minimax problem, solving problem (5) appears to be more tractable and computationally favorable in certain circumstances, thanks to the efficient algorithms studied in Li et al. (2018a, b), Luo et al. (2019), Zhang et al. (2020), Tang et al. (2020), Chu et al. (2022).

There are typically two main streams of works to tackle (5) in the literature. First, the worst-case loss quantity defined in (4) can be viewed as an optimization problem with a single inequality constraint, thus its dual counterpart can be inspected as a univariate optimization problem. In addition, the complications in verifying the interchangeability condition for and also suggest that it might be beneficial to replace (2) with its dual problem. Consequently, to guarantee the equality (5) instead of just the inequality derived from weak duality, many existing works impose relatively strong assumptions on the underlying problem in order to prove/use the strong duality and/or guarantee the existence of the dual optimal variables (Mohajerin Esfahani and Kuhn 2018, Blanchet and Murthy 2019, Blanchet et al. 2019, Chu et al. 2022, Zhang et al. 2022, Gao and Kleywegt 2023, Zhen et al. 2023). Second, when , (5) can be rewritten as . This observation suggests that is related to certain Lipschitz-type properties of the loss function (Shafieezadeh-Abadeh et al. 2015, 2019, An and Gao 2021, Gao 2022). However, the usual Lipschitz condition is not enough to guarantee (5) since the Lipschitz constant can always be chosen arbitrarily large. Thus, one often needs some other conditions such as the tightness at certain points (Shafieezadeh-Abadeh et al. 2019, Gao 2022), the convexity of (Wu et al. 2022) or the differentibility of almost-everywhere with nonexpansive gradients (An and Gao 2021).

In this paper, we study sufficient conditions to establish the equivalence between the worst-case loss quantity in the WDRO problem and its associated regularization scheme. Our proposed sufficient conditions generalize the existing results from various perspectives, particularly by relaxing the required assumptions on the loss function and cost function. Moreover, our constructive approaches and elementary proofs directly characterize the closed forms of the approximate worst-case distributions. The generality of our theoretical results are demonstrated through their applications to various problems, including regression, classification and risk measure problems.

The remaining part of this paper is organized as follows. In Section 2, we summarize our main contributions and compare them with the existing results in the literature. We derive our main theoretical results in Section 3 and present their applications in Section 4 and Section 5. The conclusion is given in Section 6.

Notations. Throughout this paper, or denotes a measurable space, where is a given -algebra on such that for any (Cohn 2013, Section 1.2). In particular, when , where is the Borel -algebra on , then is always understood as . A set is called measurable if ; a function is called measurable if for any (Cohn 2013, Proposition 2.1.1); and denotes the Cartesian product measurable space with -algebra (Cohn 2013, Section 5.1).

In this work, the function is assumed that is measurable for any . A function is a probability if it is countably additive, and ; the space of all probabilities on is denoted by ; and the expectation of a measurable function of a real-valued random variable on is denoted by (Cohn 2013, Section 10.1).

Define the indicator function of a set as if , and otherwise. Define the point mass function (Dirac measure) at point as if , and otherwise, for any measurable set . Given two functions and , we define the function as for any . We adopt the convention of extended arithmetic such that . Denote the inner product on by for any . Let be an arbitrary norm on and be its dual norm defined as . Given matrices , we denote the horizontal concatenation of and by , and the vertical concatenation of and by . Let . For any real number , the sign function is defined as if , and otherwise.

2 Main contributions

In this section, we shall summarize our main contributions and compare them with the existing results in the literature. We first state some notations which will be used. Let be a given dataset and be the corresponding empirical distribution. In addition, let be a scalar and be a measurable function on . Suppose the loss function takes the form as

For notational simplicity, let and (depending on some scalar , which will be discussed in detail later in Section 3) be defined as:

In particular, is well-defined as is assumed to be nonnegative when . It can be seen that defined in (4) satisfies , whose proof can be found in Appendix A.1. Since is a supremum quantity over a feasible set, there exists a sequence of feasible distributions whose expectations converge to as . More precisely, for any , we are interested in characterizing which satisfies and . In particular, when is attainable, one might even characterize satisfying and . Note that, in general, it is not guaranteed that exists, see for example in Mohajerin Esfahani and Kuhn (2018, Example 2). In this work, we call as an approximate worst-case distribution (Gao and Kleywegt 2023).

| Assumptions | Conclusions | References | ||||

| Others | ||||||

| norm | max-of-concave | 1 | convex | Mohajerin Esfahani and Kuhn (2018, Thm 4.2, 4.4) | ||

| extended norm | absolute/logistic | 2 or 1 | Blanchet et al. (2019, Thm 1,2) | |||

| extended semi-norm | absolute | 2 | Chu et al. (2022, Thm 4) | |||

| metric | globally Lipschitz | 1 | tightness at infinity(⨝) | Gao et al. (2022, Col 2) | ||

| lower semicontinuous | upper semicontinuous | positive definite(♢) | Blanchet and Murthy (2019, Thm 1) | |||

| cost function | interchangeability principle | positive definite(♢) | –(♭) | Zhang et al. (2022, Thm 1) | ||

| cost function(♯) | measurable | locally compact(♯) | Gao and Kleywegt (2023, Thm 1, Col 1) | |||

| cost function(†) | smooth | –(♭) | (Shafieezadeh-Abadeh et al. 2023, Thm 3.2) | |||

| extended norm | convex, piecewise linear | Wu et al. (2022, Thm 5,6,7) | ||||

| cost function | -Lipschitz | tightness conditionally(⊛) | this work | |||

| (♯) As commented in Blanchet and Murthy (2019, Section 1), the proof given in Gao and Kleywegt (2023, Lemma 2) implicitly assumes that is locally compact. We also notice from Gao and Kleywegt (2023, Remark 2, Remark 5) that Gao and Kleywegt (2023, Lemma 2, Corollary 2) requires to be a metric. (♮) The analytical formula of (or ) is not given explicitly in the result, but can be constructed directly from the proof. (♭) The analytical formula of (or ) is not a trivial implication from the corresponding result, as far as we understand. (♢) Positive definiteness/point-separating: if and only if . (†) is required to be lower bounded by a metric with compact sublevel set (Assumption 2.1(ii)), hence it must be positive definite. (⨝) See the discussion after Remark 3.1. (⊛) See Theorem 3.2 and Theorem 3.3. | ||||||

In recent years, it has been an emerging topic to study the relationships among , and . Table 1 shows an informal comparison of our results with the existing results in the literature; for detailed discussions, see Section 3. We should note that while is a computationally tractable quantity, is less computationally friendly as its evaluation involves solving a one-dimensional minimization problem with a complicated objective function. Thus the equivalence is much more desirable than the equivalence . Correspondingly, the conditions needed for the equivalence to hold are also stronger.

We summarize our main contributions in this paper as follows.

-

•

We first propose a lower bound for (see Theorem 3.1(a)). Then, we characterize a certain property named as the weak -Lipschitz property and prove that under this condition, we have (see Theorem 3.1(b)). The bounds and are demonstrated to exhibit some characteristics that are consistent with the existing literature (see the discussions after Theorem 3.1).

-

•

We propose sufficient conditions for in the cases where (see Theorem 3.2) and (see Theorem 3.3). Our result is a generalization of many existing results in the literature, which is discussed in detail in Section 3. It is worth noting that our proofs do not involve verifying the validity of interchangeability of and . In particular, we do not use the strong duality result and/or the existence of primal-dual optimizer of the Wasserstein problem , which relaxes the assumptions needed for . As a byproduct, our constructive approach directly characterizes the analytic formulation of .

-

•

Although studying sufficient conditions for is a widely explored topic, we state certain scenarios in which the existing results do not apply. But our results still can cover theses circumstances under suitable conditions, for instance, even when the globally Lipschitz condition fails (see Example 3.1); is not convex (see Example 3.2 and Example 4.6); is not a metric, not positive definite, not convex (see Example 4.4); and is not a locally compact metric space (see Example 4.2).

- •

[caption = (Informal) summary of our applications.,

label = table:supper-long-table,

]

colspec = —l—l—l—,

Application Formulation Remark

Regression loss functions

Higher-order

regression

,

(1)

(2) takes one of

, where

, where

Lower partial

moments

,

,

Higher-order

-insensitive

regression

,

,

Nonparametric

scalar-on-function

linear regression

,

,

(1)

(2)

(3) For , takes one of

, or ,

Parametric

scalar-on-function

linear regression

,

,

,

Log-cosh

loss regression

(1)

(2) takes one of

Huber

loss regression

where

Quantile

loss regression

where

Ridge linear

ordinary regression

(1) ,

(2)

Hard sigmoid

/HardTanh

(1)

(2)

(3) Equivalence holds conditionally

Classification loss functions

Higher-order

hinge loss

binary classification

,

(1)

(2)

Higher-order

support vector

machine classification

,

Log-exponential loss

Smooth hinge loss

with

Truncated

pinball loss

with

Binary

cross-entropy loss

(1)

(2)

(3) Equivalence holds conditionally

Generalization to risk measure

-support

vector

regression

(1)

(2)

(3)

-support

vector

machine

(1)

(2)

(3)

Higher

moment

coherent

risk measures

(1)

(2)

(3)

3 Theoretical analysis of the equivalence

In this section, we will establish our main results for deriving the equivalence between the worst-case loss quantity in the WDRO problem and its regularization scheme counterpart. We first give the following lemma, with the proof in Appendix A.2, to quantify the Wasserstein discrepancy between any distribution and a singleton, which will be used in the subsequent analysis.

Lemma 3.1.

Given any distribution and any point , for any scalar and any extended nonnegative-valued measurable function , we have

Before stating our main results, we need the following definition of the cost function.

Definition 3.1.

The function defined on is called a cost function if it is extended nonnegative-valued, measurable, and vanishes whenever two arguments are the same, that is, for any , and .

Next, we introduce a weak Lipschitz property for functions on with respect to a given cost function , where the weak Lipschitz constant depends on the second input of . Note that it is different from the Lipschitz property used in Shafieezadeh-Abadeh et al. (2015), An and Gao (2021), Gao (2022), as the latter does not depend on the input variables.

Definition 3.2 (Weak Lipschitz property).

Given a function , a cost function on and a subset , is called -Lipschitz at if for any , one has

where is a constant depending on and .

The classical Lipschitz property can be seen as a special case of Definition 3.2 when is a metric space and . In other words, any Lipschitz function is weak Lipschitz, while the reverse is not always true, for example, see Example 3.1.

3.1 Lower and Upper bounds of the worst-case loss quantity

We now derive a lower bound and an upper bound of the worst-case loss quantity for a certain class of loss functions in the following theorem.

Theorem 3.1.

Let be a given dataset and be the corresponding empirical distribution. In addition, let be a scalar and be a cost function on . Suppose the loss function takes the form as

Let be defined as in (4). Then the following statements hold for any .

-

(a)

Let for . Then

-

(b)

Suppose is -Lipschitz at with , then

-

(c)

Suppose is -Lipschitz at , then

Proof. (a) For any collection such that for all . It follows from Lemma 3.1 that for any

Hence we can construct

| (6) |

Then we have , and , since for any measurable sets ,

Therefore, we can see that

Moreover, according to (6), we have

By taking supremum on all possible such that for all , we have

Besides, since by Lemma 3.1, we have that

and hence .

(b) Let be an arbitrary scalar. Fix any such that . By the definition of , there exists such that

Besides, by the definition of the loss function , we have

where the inequality (∗) holds naturally if , and follows from the Minkowski inequality if . Since is -Lipschitz at , it holds that

This means that for any , we have

By letting , we get the desired inequality.

(c) Since is -Lipschitz at , by the convention that , one has for any . In particular, for any . Therefore, is a constant function on , and so is . Thus, we have

This completes the proof.

For better understanding, we give an intuitive explanation of the above theorem. The first conclusion shows that the worst-case loss quantity is lower bounded by the weighted average of worst-case loss quantities with respect to point masses , , which is easier to calculate according to Lemma 3.1. The second conclusion shows that the worst-case loss quantity can be upper bounded by using the weak Lipschitz property of the kernel function . The third conclusion shows that when the weak Lipschitz constant is zero, then the upper bound is met. In addition, from (a) and (b), we have that if , then . That is to say, if is -Lipschitz at and , then . Therefore, in the remaining part of this work, we shall only consider the case when and .

Note that if one fixes the input data while varying , the worst-case loss quantity , the lower bound and the upper bound are all functions of on . A few remarks are in order. First, the lower bound is larger than the trivial lower bound given in Zhang et al. (2022, Lemma 1). Second, the upper bound is continuous on and in particular, right-continuous at . This is similar to the continuity of another existing upper bound (Zhang et al. 2022, Remark 2). Third, if we have for each (for example, when Theorem 3.2 or Theorem 3.3 holds true), then is continuous on . It is worth noting that another sufficient condition for the continuity of has been studied in Zhang et al. (2022, Remark 2), where the loss function is required to be a composition of a non-decreasing concave function and the cost function .

Next, we will analyse various cases on when the lower or upper bound for the worst-case loss quantity provided in Theorem 3.1 is achievable.

3.2 Equivalence in (5) when

We first consider the case when . The following theorem provides a sufficient condition on when the lower and upper bounds in Theorem 3.1 will coincide.

Theorem 3.2.

Let be a given dataset and be the corresponding empirical distribution. In addition, let be a cost function on and be a scalar. Suppose the loss function takes the form as

where the function satisfies the following assumptions:

-

(A1)

is -Lipschitz at with ;

-

(A2)

for any and each , there exists such that and

Then we have that in Theorem 3.1, that is,

| (7) |

Proof. Since is -Lipschitz at , by Theorem 3.1, we have that

Hence, in order to prove (7), it suffices to show that .

Let be an arbitrary scalar. By Assumption (A2), for any , there exists such that and

Let and choose

Then one has

and

Let , we have that for any ,

Therefore, it holds that

This completes the proof.

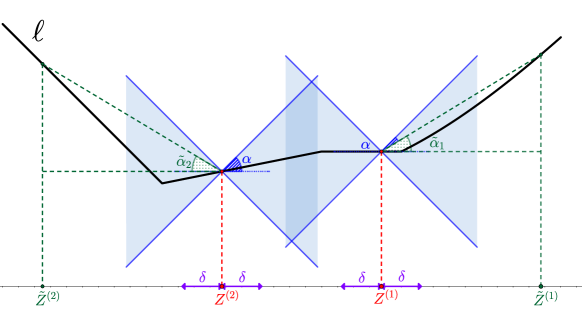

For better illustration, we give a visualization of Assumptions (A1-A2) in Figure 1 under the setting where and . Assumption (A1) says that for any , we have for , which is equivalent to the condition that the graph of must stay inside two blue double cones with the opening angle . Assumption (A2) says that for any and , there exists depending on such that and . This is equivalent to requiring the existence of a point such that the green slope of the line passing through and satisfies , while the distance between and is at least .

Remark 3.1.

In Theorem 3.2, it is required that the condition (A2) holds for any , with respect to the same Lipschitz constant . To relax this condition, one might assume that Assumptions (A1-A2) hold at each with a Lipschitz constant , for . Even though it might not guarantee that the lower bound and upper bound for coincide as in Theorem 3.2, we show in Appendix C that one still has closed forms for the lower and upper bounds given by

It is worth mentioning that our Assumptions (A1) and (A2) are weaker than those made in the literature. First, in the existing works such as Shafieezadeh-Abadeh et al. (2015, Theorem 4), Shafieezadeh-Abadeh et al. (2019, Theorem 9, Theorem 14), An and Gao (2021, Assumption 1) and Gao (2022, Assumption 1(I)), the Lipschitz assumption on the function needs to hold globally, while our Assumption (A1) only requires it to hold when the second argument of the cost function is one of the empirical points. Later, Example 3.1 will provide an instance wherein the loss function lacks the global Lipschitz continuity property, but it satisfies our weak Lipschitz property in certain scenarios. Second, Gao (2022, Assumption 1(II)) requires that the Lipschitz constant is attained at infinity222This means that for any , there exists a sequence such that and ., and Shafieezadeh-Abadeh et al. (2019, Assumption 10, Assumption 21) requires that the Lipschitz constant is attained exactly at a certain point where the derivative also exists, while our Assumption (A2) only requires it to be (approximately) attained at points far enough from the empirical points. Third, we do not assume any convexity of as in Wu et al. (2022). In the subsequent contexts, Example 3.2 will provide an instance where the Lipschitz constant is not attained at infinity and the loss function is not convex but the equivalence (7) holds conditionally according to our Theorem 3.2. Fourth, we do not require to be positive definite (that is, if and only if ) as in Blanchet and Murthy (2019, Assumption (A1)) and Zhang et al. (2022, Assumption 1).

Another important observation of Assumption (A2) is that for any , is required to be at least . That is to say, one requires the knowledge of to tell whether Assumption (A2), and further the equivalence (7), hold or not in practice. At first glance, it seems restrictive, compared with the existing results where the equivalence (7) has been studied with arbitrary . Fortunately, as it will be shown later in Section 4, our Assumption (A2) indeed holds for most of the commonly-used loss functions for any . In particular, Propositions 4.1, 4.2, 4.3, and 4.4 serve as guidance on finding and checking the validity of Assumption (A2) (and Assumption (B) later in Theorem 3.3).

We give the following two examples to show that the two assumptions in Theorem 3.2 are not removable. Specifically, we will see that with the same loss function , the equivalence (7) holds for some values of and fails for some other values, which indicates that the condition in Assumption (A2) is not removable. In addition, Example 3.2 also shows that our weak Lipschitz property in Assumption (A1) needs to depend on the empirical distribution , which provides the evidence that our generalization is essential compared with the existing results which rely on the global Lipschitz property of . Specifically, these two examples illustrate that the classical Lipschitz terminology fails to capture the exact reformulation of certain WDRO problems. Similar to (Kuhn et al. 2019, Remark 3), one can see in Example 3.1 and Example 3.2 that the value of is not simple in general cases. Nevertheless, this notion of the weak Lipschitz constant is better (i.e., lower) than the classical Lipschitz constant, and applicable for more generic class of loss functions. Efficient scheme to compute is an interesting topic to explore, and we leave it for future research. The detailed proofs corresponding to these two examples are given in Appendix B.1 and Appendix B.2.

Example 3.1 (Binary cross-entropy (Yi-de et al. 2004, Scott 2012, Hurtik et al. 2022)).

Let the univariate function be defined as

Define the loss function as . Consider the cost function defined as for any . Then the following statements hold true.

-

(a)

is convex, continuously differentiable, but not globally Lipschitz on .

-

(b)

Given any and . We have that is -Lipschitz at , where . Moreover, for , we have the following two results:

-

(b1)

if , then ;

-

(b2)

if , then .

-

(b1)

Example 3.2 (Hard sigmoid (Howard et al. 2019) / HardTanh (Collobert 2004)).

Let the univariate function be defined as

Define the loss function as . Consider the cost function as . For any , we denote to be a vector in satisfying and .

-

(a)

Given scalars and any vector satisfying . Suppose with , then is -Lipschitz at . Moreover,

-

(a1)

if , then ;

-

(a2)

if , then .

-

(a1)

-

(b)

Given any such that . Suppose with , then is -Lipschitz at . Moreover,

-

(b1)

if , then ;

-

(b2)

if , then .

-

(b1)

3.3 Equivalence in (5) when

Next, we derive a sufficient condition on when the equivalence (5) holds for .

Theorem 3.3.

Let be a given dataset and be the corresponding empirical distribution. In addition, let be a cost function on and be a scalar. Suppose the loss function takes the form as

where satisfies Assumption (A1) in Theorem 3.2 with , and also satisfies the following assumption:

-

(B)

for any and , there exists such that and

where the set is defined as

Then we have in Theorem 3.1, that is,

Proof. Let be a scalar. According to Assumption (B), for any , there exists such that and . We consider two cases.

Case 1.

When , we know that for each ,

Let and . Then it can be seen that , , since for any measurable sets ,

In addition, it can be seen that

Moreover, we have that

where the equality (Δ) follows from the fact that for any , we always have .

Case 2.

When , we have for any . Set for each , and define

Then we can see that and , as for any measurable sets ,

Moreover, we have . Thus, it holds that

The fact that together with the nonnegativity of the function implies that for any , which further indicates that

Therefore, combining the above two cases, for any given , we can construct such that and

By letting and recalling that , we can conclude that

The fact that satisfies Assumption (A1) together with Theorem 3.1 also implies that

which completes the proof.

Note that when the loss quantity at the empirical distribution vanishes, one can see that Assumption (A2) and Assumption (B) are the same. On the other hand, when , if for some , one can always choose for this .

4 Applications to different function classes

In this section, we present the applications of Theorem 3.2 and Theorem 3.3 in various regression and classification problems. We first give the definition of an absolutely homogeneous function, which will be used in the remaining part of this section.

Definition 4.1.

An extended-valued function on a real vector space is called absolutely homogeneous if one has for any and . In addition, is called proper if there exists such that .

From the above definition, we can see that if is absolutely homogeneous, then and is a cone on . Besides, the following two functions

-

•

for all and for ;

-

•

for all ,

are absolutely homogeneous, but not proper.

4.1 Applications to simple piecewise linear regression loss functions

We start from the applications of our results to simple piecewise linear regression loss functions as follows.

Proposition 4.1 (Linear loss).

Let be a (finite or infinite dimensional) real vector space. Suppose that is absolutely homogeneous and proper, is linear, and

Let the cost function be defined as for any . Given any scalar , then the functions , and are -Lipschitz at . Furthermore, they also satisfy Assumptions (A1), (A2) and (B) at for any if .

Proof. In order to prove that , and are -Lipschitz at , by noting the fact that for any ,

we only need to prove that

This can be seen as follows:

-

•

if , then it holds true immediately;

-

•

if , since , one also has ;

-

•

if , then

Thus, , and are all -Lipschitz at .

Suppose that . From the previous discussion, we have that , and satisfy Assumption (A1) at with any . By the definition of , for any , there exists such that and . Since is linear and is absolutely homogeneous, for any , we have and . Hence, one can always choose such that

Next we prove that the functions , and satisfy Assumptions (A2) and (B) at for any .

-

•

For the function , given any and any , by letting , we have and

Therefore, satisfies Assumption (A2) at for any . Using some similar analysis as above, we can also show that satisfies Assumption (B) at .

-

•

For the function , we first prove that satisfies Assumption (A2) at . For any and , let

Then if , we have and

if , we have and

Therefore, satisfies Assumptions (A2) at for any .

Next, we turn to Assumption (B). Fix , , a dataset and the corresponding empirical distribution . For any , we consider the following cases.

-

–

If , then (A2) and (B) are equivalent.

-

–

If and , for any , we can set . Then we have . Therefore, and

-

–

If and , then and one can choose such that (B) holds.

This means that satisfies Assumptions (B) at for any .

-

–

-

•

Finally, we consider the function . For any and , let

Then if , we have and

if , we have and

Thus satisfies Assumptions (A2) at for any .

Fix , , a dataset and the corresponding empirical distribution . For each , since the cases when (1) or (2) and , are easy to check, we only need to consider the case when and . For any , let . Then we can see that

Moreover, we have and

Therefore, satisfies Assumptions (B) at for any .

This completes the proof.

Remark 4.1.

Proposition 4.1 can be viewed as a guidance to find the weak Lipschitz constant when certain properties of the loss and cost functions are given.

Based on Proposition 4.1, Theorem 3.1(c), Theorem 3.2 and Theorem 3.3, we obtain the following corollary stating the equivalence (5) for simple piecewise linear regression loss functions.

Corollary 4.1.

Under the setting of Proposition 4.1, given any scalar and any empirical distribution on , it holds that for any ,

where takes one of the following forms: , or .

Here are some specific examples of the above corollary. Note that some of the following results have been studied in the literature, whereas we have provided a unified framework to study the equivalence between the worst-case loss quantity in the WDRO problem and the regularization scheme for simple piecewise linear regression and scalar-on-function linear regression functions.

Example 4.1 (Linear-type regression).

Let . Given any , and any empirical distribution on . For any and , we have

where , and takes one of the following forms:

-

(a)

;

-

(b)

;

-

(c)

;

and and take one of the following forms:

-

(i)

and ;

-

(ii)

and ;

-

(iii)

and where and ;

-

(iv)

and where is a given matrix.

The proof associated with the above example is given in Appendix B.3. Note that this example covers many commonly-used regression problems. Specifically, we list some of them here.

-

•

Higher-order regression: , . When , the regularized problem is often referred as a variant of the square-root Lasso model, where is a function of which promotes specific structures in , such as smoothness, sparsity, and clustering of coordinates (Belloni et al. 2011, Bunea et al. 2013, Stucky and Van De Geer 2017, Jiang et al. 2021).

- •

- •

In the existing literature, the equivalence between the worst-case loss quantity in the WDRO problem and the regularization scheme for the above problems has been studied for some specific settings. For instances, Blanchet et al. (2019, Proposition 2, Theorem 1) studied variants of the square-root Lasso model when is an extended norm and Chu et al. (2022, Theorem 1) covered the cases when is an extended semi-norm; Kuhn et al. (2019) studied tractable reformulation of the WDRO problem where satisfies certain convex/concave properties; Gao et al. (2022, Corollary 2) investigated more general linear models when is a metric and Wu et al. (2022) explored the piecewise linear convex loss function when is an extended norm. Moreover, when , Montiel Olea et al. (2023) considered a similar model but with the max-sliced Wasserstein ball.

As a natural extension of the ordinary linear regression problem, the scalar-on-function linear regression problem has received increasing attention nowadays, where the feature space is a functional space instead of , endowed with the inner product . We refer the readers to Ramsay and Dalzell (1991), Ramsay and Silverman (2005), Wang et al. (2016) for more details and discussions about the functional linear regression problem. To the best of our knowledge, the equivalence between the worst-case loss quantity in the WDRO problem and the regularization scheme for this class of problems has not been established in the literature. Fortunately, based on our results, we can give the following equivalence for the scalar-on-function linear regression problems, whose proof can be found in Appendix B.4. It is worth mentioning that the nonparametric model (a) has been studied in Cardot et al. (1999), Cai and Yuan (2012) and the regularizer involving has been considered in Tong and Ng (2018, (2)). In addition, the parametric model (b) has been introduced to reduce the degree of freedoms.

Example 4.2 (Scalar-on-function linear regression).

Denote the set of real-valued, square-integrable functions on as . Given any empirical distribution on and any scalar , the following equality holds for any and :

where for any ; , or ; and , take one of the following forms.

-

(a)

(Nonparametric) Given and let defined as

for any . Let .

-

(b)

(Parametric) Let , . Define as

for any . Let .

4.2 Applications to nonlinear regression loss functions

Next, we move on to study nonlinear regression problems.

Proposition 4.2 (Nonlinear regression loss).

Let be a (finite or infinite dimensional) real vector space. Suppose that is absolutely homogeneous and proper, is linear, and

In addition, given , suppose a univariate function satisfies the following assumptions:

-

(H1)

is globally -Lipschitz on with ;

-

(H2)

for any , there exists such that and

Then the function defined by is -Lipschitz at , where the cost function is defined as for any . Moreover, also satisfies Assumptions (A1) and (A2) at with if .

Proof. By Proposition 4.1, one has that is -Lipschitz at . According to (H1), for any , we have

Hence, is -Lipschitz at .

Next, suppose that . Then we have satisfies Assumption (A1) at with . For any , denote , then we have . Let be any scalar. As in the proof of Proposition 4.1, there exists such that and . We know from (H2) that there exists such that

Since is globally -Lipschitz continuous, we have . Thus, we have

which implies that

Let . Then we have

and

Therefore, satisfies Assumption (A2) at with the given . This completes the proof.

Remark 4.2.

Proposition 4.2 characterizes a certain case where is nonlinear but Theorem 3.2 still holds true. In this case, the loss function can be written as a composition of a linear map and a univariate -Lipschitz function , where the Lipschitz constant is approximately attainable on . In particular, if is approximately attainable at infinity, then Assumption (H2) holds regardless of the choice of , as long as is finite.

Thanks to Proposition 4.2, Theorem 3.1(c) and Theorem 3.2, we now can cover a broader class of nonlinear regression loss functions in the following corollary.

Corollary 4.2.

Under the setting of Proposition 4.2, for any empirical distribution on , the following equivalence holds for any given :

where .

We give the following example as an application of Corollary 4.2 to show the equivalence of the worst case loss quantity in the WDRO problem and the regularization scheme for nonlinear regression loss functions, including the log-cosh loss, the quantile loss and Huber loss (Huber 1973, Koenker and Bassett Jr 1978, Koenker and Hallock 2001, Wang et al. 2020), whose proof can be found in Appendix B.5.

Example 4.3.

Given any , and any empirical distribution on , we have

where and takes one of the following forms:

-

(a)

log-cosh loss: ;

-

(b)

Huber loss:

-

(c)

quantile loss: with ;

and and take one of the following forms

-

(i)

and ;

-

(ii)

and .

4.3 A special regression model

In this subsection, we introduce an interesting example wherein our results can be applied to the cases when the cost function is nonconvex, not positive definite and the weak Lipschitz constant is not in the popular form of the norm of the regression vector . In Shafieezadeh-Abadeh et al. (2019, Remark 19), it has been pointed out that the Tikhonov-regularized problem with respect to a Lipschitz loss function can not be explained by a distributionally robust learning problem. In addition, it has been shown in Li et al. (2022) that the Tikhonov-regularized problem with respect to the squared loss has an equivalence interpretation as a martingale DRO problem with respect to the quadratic cost . Nevertheless, according to Example 4.4, whose proof is in Appendix B.6, we show that with the notion of the weak Lipschitz property in Definition 3.2, the Tikhonov-regularized squared loss problem is equivalent to a WDRO problem swith a specifically designed cost function on the sample space. In particular, unlike , our designed cost function is nonconvex and not positive definite.

4.4 Applications to classification loss functions

Next we turn our attention to linear-type classification loss functions. For the detailed proof of the following proposition, see Appendix A.3.

Proposition 4.3 (Linear classification loss).

Let , where is a (finite or infinite dimensional) real vector space. Suppose that is absolutely homogeneous and proper, is linear, , and

Let the cost function be defined as and the function be defined as for any . Then for any , the functions and are -Lipschitz at . Furthermore, they also satisfy Assumptions (A1), (A2) and (B) at for any if .

Together with Theorem 3.1(c), Theorem 3.2 and Theorem 3.3, we have the following corollary on the equivalence (5) for linear-type classification loss functions.

Corollary 4.3.

Under the setting of Proposition 4.3, given any scalars , and any empirical distribution on . We have that for any ,

where or .

Now we give an example of the higher-order hinge loss binary classification and the higher-order support vector machine classification, which is an application of the above corollary. The detailed proof can be found in Appendix B.7. Note that the second conclusion in Blanchet et al. (2019, Theorem 2) can be viewed as a special case of this example with .

Example 4.5 (Higher-order hinge loss /Higher-order support vector machine).

For any , define the cost function . Given any , and any empirical distribution on , we have

where and takes one of the following forms:

-

(a)

;

-

(b)

.

Then, we consider the applications of our results to nonlinear classification loss functions in the following proposition, whose proof can be found in Appendix A.4.

Proposition 4.4 (Nonlinear classification loss).

Let , where is a (finite or infinite dimensional) real vector space. Suppose that is absolutely homogeneous and proper, is linear, , and

Let the cost function be defined as and the function be defined as for any . Given and suppose satisfies Assumptions (H1-H2) in Proposition 4.2, then is -Lipschitz at . Moreover, also satisfies Assumptions (A1) and (A2) at with if .

The following corollary allows us to establish the equivalence of the worst-case loss quantity in the WDRO problem and the regularization scheme for nonlinear classification loss functions, based on Proposition 4.4, Theorem 3.1(c) and Theorem 3.2.

Corollary 4.4.

Under the setting of Proposition 4.4, for any empirical distribution on , the following equivalence holds for any given :

where .

Nonlinear classification loss functions have gained widespread popularity due to their efficacy in handling real-world datasets where the relationships between the variables are intricate and nonlinear. We give the following example to show that our results are applicable in many popular instances, whose proof can be found in Appendix B.8. Here, the log-exponential loss example is equivalent to the first conclusion in Blanchet et al. (2019, Theorem 2) and a tractable reformulation of the worst-case loss quantity with respect to the smooth hinge loss function has also been studied in Shafieezadeh-Abadeh et al. (2019, Corollary 16).

Example 4.6.

For any , define the cost function . Given any , and any empirical distribution on . We have

where and takes one of the following forms.

-

(a)

Log-exponential loss: ;

-

(b)

Smooth hinge loss:

-

(c)

Truncated pinball loss (Shen et al. 2017):

where are two given constants.

5 Generalization to risk measure

In this section, we shall generalize the expectation function in the equivalence (5) to a risk measure, which might be nonlinear in distribution.

Given any cost function and any scalar , it can be easily seen that for any by choosing . In addition, we use the convention that when . Then we can see that is a cost function on . Moreover, one can define the weak Lipschitz property on with respect to the cost function . Inspired by Wu et al. (2022), we propose the following sufficient condition under which a supremum on the Wasserstein neighborhood of and an infimum on are interchangeable.

Theorem 5.1.

Given any empirical distribution on and any given . Suppose that a function satisfies the following conditions:

-

•

on is concavelike in , i.e., for any and , there exists such that for all ,

-

•

is convex, coercive and lower semi-continuous for each ;

-

•

is -Lipschitz at for some which does not depend on .

Then we have that for any ,

Proof. Since is -Lipschitz at , for any such that , we have for any ,

| (8) |

As is convex and coercive, it admits at least one minimizer. Let be a minimizer of , i.e., . Since is coercive, there exists such that for any ,

This together with (8) implies that for any such that and any scalar , it holds that

| (9) |

On the other hand, (8) also implies that

| (10) |

Thus, according to (9) and (10), we have for any such that ,

This further means that

By Sion (1958, Theorem 4.2’), since is a concave-convexlike on and is lower semi-continuous for each on the compact set , we have

Therefore, it holds that

As it is obvious that

we complete the proof.

Based on the above theorem, we give the following corollary, which generalizes the expectation function in the equivalence (5) to a risk measure.

Corollary 5.1.

Given any scalar . Let be a cost function on . Suppose the function is -Lipschitz at with . Let be a given dataset and be the corresponding empirical distribution. Then we have the following conclusions.

-

(a)

Denote . Given , suppose that for all ,

Then it holds that

-

(b)

Given , let . Given , suppose that for any ,

Then it holds that

Proof. (a) Define the function by

By the definition of , we have that

Now we verify that the function satisfies the three conditions in Theorem 5.1. It is easy to verify that the first two conditions hold. Next we turn to the third condition. Fix and any such that . For any , we have

By taking infimum over all , we can see that

which means that is -Lipschitz at . Then according to Theorem 5.1, for any , we have that

Thus, it holds that for any ,

where the third equality following from the fact that for all ,

(b) The proof of this part is similar to the one for part (a). We omit the details here.

As applications of the above corollary, we give the following three examples, stating the equivalence between the worst case loss quantity in the WDRO problem and the regularization scheme for -support vector regression, -support vector machine, and higher moment coherent risk measures. The proof of these examples can be found in Appendices B.9-B.11.

Example 5.1 (-support vector regression (Schölkopf et al. 1998)).

For any , define the cost function . Given , , and any empirical distribution on , we have

Example 5.2 (-support vector machine (Schölkopf et al. 2000)).

For any , define the cost function . Given any , , and any empirical distribution on , we have

Example 5.3 (Higher moment coherent risk measures (Krokhmal 2007)).

For any , define the cost function . Given , , , and any empirical distribution on , we have

6 Conclusion

In this paper, we studied a variety of the Wasserstein distributionally robust optimization problems and proposed certain conditions to quantify the corresponding worst-case loss quantity. Specifically, we drew connections and established the equivalence between the worst-case loss quantity and its associated regularization scheme. Our proposed results generalized the existing results from various perspectives, particularly by relaxing the required assumptions on the loss function and the cost function. Moreover, our constructive approaches and elementary proofs directly characterized the closed forms of the approximate worst-case distributions. Extensive examples demonstrated that our theoretical results can be applied to various problems, including regression, classification and risk measure problems.

Following the presented results, there are some possible topics for future studies on the WDRO problems. For example, by similar arguments as in our proposed weak Lipschitz property, the notion of the growth rate in Gao and Kleywegt (2023, Lemma 2) can be readily extended to be dependent on the cost function and its variables. On the other hand, recent works on the WDRO problems such as Blanchet and Murthy (2019), Zhang et al. (2022), Gao and Kleywegt (2023), suggest that further assumptions might be required when the empirical distribution is not discrete. In summary, we hope our results can inspire more fruitful studies on the behavior of the worst-case loss quantity and the applications of the associated regularization scheme in the machine learning and operations research.

Acknowledgement

Meixia Lin is supported by The Singapore University of Technology and Design under MOE Tier 1 Grant SKI 2021_02_08. Kim-Chuan Toh is supported by the Ministry of Education, Singapore, under its Academic Research Fund Tier 3 grant call (MOE-2019-T3-1-010).

Appendix A Proof of auxiliary results

A.1 Proof of

We can see that

which completes the proof.

A.2 Proof of Lemma 3.1

For any , we have for any measurable sets . In particular, it holds that

| (11) |

This implies that for any measurable set , and hence

Moreover, (11) also implies that

Therefore, one has that

This completes the proof.

A.3 Proof of Proposition 4.3

For any , we have

Moreover, we can see that

where the last inequality holds as follows.

-

•

If , then it holds true;

-

•

If , then and . Since , this implies that ;

-

•

If , then we have , and

Therefore, and are -Lipschitz at .

Suppose that . Then it can be seen that and satisfy Assumption (A1) at for any thanks to previous discussions. By the definition of , for any , there exists such that . For any and , define as

Then we can see that and

Therefore, for any and , by setting or , we can see that satisfies both Assumption (A2) and (B) at .

Finally, we are going to prove that satisfy Assumptions (A2) and (B) when . For any and , define as and

Then if , we have and

if , we have and

This means that satisfies Assumptions (A2) at for any . Next, we turn to Assumption (B). Fix , , a dataset and the corresponding empirical distribution . For any , we consider the following cases.

-

•

If , (A2) and (B) are equivalent.

-

•

If and , one can choose such that (B) holds.

-

•

If and . For any , let be defined as and . Then we have

Moreover, one can see that and

This means that satisfies Assumptions (B) at for any .

A.4 Proof of Proposition 4.4

As the proof of this proposition is similar to that of Proposition 4.2, we only sketch it. For any , we can see that

Hence, is -Lipschitz at .

Next, suppose that . Then we can see that satisfies Assumption (A1) at with . For any , denote , then we have . Let . As in the proof of Proposition 4.1, there exists such that and . By Assumption (H2) and the Lipschitz property of , there exists such that and

Define , then we have

and

Therefore, satisfies Assumption (A2) at with the given . This completes the proof.

Appendix B Proof of examples

We start with the following technical lemma, which will be used later in the proof of Examples 3.1 and 3.2.

Lemma B.1.

Let and be a convex, continuously differentiable function. Given any , let defined as

Then we have that is continuous and non-decreasing on . Moreover,

where and .

Proof. Since is continuously differentiable, we can see that is continuous on . For any such that , we can see

Note that is convex, hence for any , and thus for any . Therefore, is non-decreasing on , and the remaining conclusion follows.

B.1 Proof of Example 3.1

(a) Note that for any , we can easily see that is convex and continuously differentiable. Moreover, we can see that

Thus is not globally Lipschitz on .

(b) For any such that , we have and

where is defined as in Lemma B.1. According to Lemma B.1, we have that is continuous and non-decreasing on . Moreover, we can see that

Together with Lemma B.1, we have that

where the second equality follows from the fact that . Thus, is -Lipschitz at .

(b1) Suppose . For any , since is continuous, non-decreasing on , and also satisfies , there exists such that

Then and

Hence, Assumption (A2) is satisfied. By Theorem 3.2, we have that

(b2) Suppose . Note that is upper bounded by 0. Thus, we have that

On the other hand, if we choose with for each , then by Lemma 3.1, we have for sufficiently large . Moreover, it holds that

as . Therefore, we have

This completes the proof.

B.2 Proof of Example 3.2

(a) For any , we have and

Therefore, we can see that is -Lipschitz at .

(a1) Suppose . For any , let , then we have that and

which means that satisfies Assumption (A2) at for . Therefore, according to Theorem 3.2, we have

(a2) Suppose . We have that for any ,

Hence, . On the other hand, if we choose with , then by Lemma 3.1, we have . Moreover, it holds that

which means

(b) For any , we can see that and

which further implies that

Therefore, we can see that is -Lipschitz at .

(b1) Suppose . For any , let , then and

which means that satisfies Assumption (A2) at for . Therefore, according to Theorem 3.2, we have

(b2) Suppose . Similar to (b1), we have . On the other hand, if we choose with , then by Lemma 3.1, we have . Moreover, it holds that . Therefore,

This completes the proof.

B.3 Proof of Example 4.1

It is obvious that the function is linear on . We are going to apply Proposition 4.1 and Corollary 4.1 to draw the conclusions. Here we will check the conditions in Proposition 4.1 and Corollary 4.1 case by case.

(i) Let , then it can be seen that is absolutely homogeneous on . Then and . In addition,

(ii) Let , then is absolutely homogeneous, and . In addition,

(iii) Let , then we have that is absolutely homogeneous, and . In addition,

B.4 Proof of Example 4.2

It is obvious that the function defined in (a) or (b) is linear on . In addition, let , then we can see that is absolutely homogeneous on , and

B.5 Proof of Example 4.3

(a) We first see that

which means that is globally -Lipschitz on and for any , we have

This is to say, defined in (a) satisfies Assumptions (H1-H2) with . Then the rest of the proof which involves finding is similar to Example 4.1. We omit the details here. Then our conclusion follows from Corollary 4.2.

(b) We have that , which means that is globally -Lipschitz on . For any , we have

which means that defined in (b) satisfies Assumptions (H1-H2) with . The rest of the proof is similar to that of (a).

(c) It is easy to see that defined in (c) is globally -Lipschitz on . Moreover, for any , we can see that

which means that defined in (c) satisfies Assumptions (H1-H2) with . The rest of the proof is similar to that of (a).

B.6 Proof of Example 4.4

We first show that for any satisfies Assumption (A1) with . For any , we have

Hence, is -Lipschitz at .

Next, we show that satisfies Assumption (A2). For any and , let with , then and

as . On the other hand, we have

and

as . Thus, for the given and any , there exists a positive integer such that for , one has

This implies that

Therefore, it satisfies Assumption (A2). By Theorem 3.2, we have the required result.

B.7 Proof of Example 4.5

It is obvious that is linear on . Let , then we can see that is absolutely homogeneous, and . In addition,

According to Corollary 4.3, we have the conclusions.

B.8 Proof of Example 4.6

According to Corollary 4.4 and the proof to Example 4.1, it suffices to show that each defined in this example satisfies Assumption (H1-H2) with . Next, we discuss them one by one.

(a) For , it can be seen that

which indicates that is globally -Lipschitz on . Moreover, given any , we have

(b) Given

It can be easily seen that is globally -Lipschitz on . In addition, for any , we have

(c) Let be defined as

The piecewise linear function is obviously globally -Lipschitz on . For any , we can see that

This completes the proof.

B.9 Proof of Example 5.1

B.10 Proof of Example 5.2

B.11 Proof of Example 5.3

Appendix C A weaker version of Theorem 3.2 with relaxed assumptions

Theorem C.1.

Let be a given dataset and be the corresponding empirical distribution. In addition, let be a cost function on and be a scalar. Suppose the loss function takes the form as

where the function satisfies the following assumptions:

-

(C1)

is -Lipschitz at with for each ;

-

(C2)

for any and each , there exists such that and

Then we have that , where

which means that

References

- An and Gao (2021) An Y, Gao R (2021) Generalization bounds for (Wasserstein) robust optimization. Advances in Neural Information Processing Systems, volume 34, 10382–10392.

- Bawa (1975) Bawa VS (1975) Optimal rules for ordering uncertain prospects. Journal of Financial Economics 2(1):95–121.

- Belloni et al. (2011) Belloni A, Chernozhukov V, Wang L (2011) Square-root lasso: Pivotal recovery of sparse signals via conic programming. Biometrika 98(4):791–806.

- Bertsimas et al. (2018) Bertsimas D, Gupta V, Kallus N (2018) Robust sample average approximation. Mathematical Programming 171:217–282.

- Bickel et al. (2009) Bickel PJ, Ritov Y, Tsybakov AB (2009) Simultaneous analysis of Lasso and Dantzig selector. The Annals of Statistics 37(4):1705–1732.

- Blanchet et al. (2019) Blanchet J, Kang Y, Murthy K (2019) Robust Wasserstein profile inference and applications to machine learning. Journal of Applied Probability 56(3):830–857.

- Blanchet and Murthy (2019) Blanchet J, Murthy K (2019) Quantifying distributional model risk via optimal transport. Mathematics of Operations Research 44(2):565–600.

- Bunea et al. (2013) Bunea F, Lederer J, She Y (2013) The group square-root lasso: Theoretical properties and fast algorithms. IEEE Transactions on Information Theory 60(2):1313–1325.

- Cai and Yuan (2012) Cai TT, Yuan M (2012) Minimax and adaptive prediction for functional linear regression. Journal of the American Statistical Association 107(499):1201–1216.

- Cardot et al. (1999) Cardot H, Ferraty F, Sarda P (1999) Functional linear model. Statistics & Probability Letters 45(1):11–22.

- Chen et al. (2011) Chen L, He S, Zhang S (2011) Tight bounds for some risk measures, with applications to robust portfolio selection. Operations Research 59(4):847–865.

- Chu et al. (2022) Chu HT, Toh KC, Zhang Y (2022) On regularized square-root regression problems: Distributionally robust interpretation and fast computations. Journal of Machine Learning Research 23(1):13885–13923.

- Cohn (2013) Cohn DL (2013) Measure Theory, volume 5 (Springer).

- Collobert (2004) Collobert R (2004) Large scale machine learning. Technical report, Université de Paris VI.

- Delage and Ye (2010) Delage E, Ye Y (2010) Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research 58(3):595–612.

- Drucker et al. (1996) Drucker H, Burges CJ, Kaufman L, Smola A, Vapnik V (1996) Support vector regression machines. Advances in Neural Information Processing Systems, volume 9, 155–161.

- Erdoğan and Iyengar (2006) Erdoğan E, Iyengar G (2006) Ambiguous chance constrained problems and robust optimization. Mathematical Programming 107:37–61.

- Feng et al. (2014) Feng J, Xu H, Mannor S, Yan S (2014) Robust logistic regression and classification. Advances in Neural Information Processing Systems, volume 27.

- Fishburn (1977) Fishburn PC (1977) Mean-risk analysis with risk associated with below-target returns. The American Economic Review 67(2):116–126.

- Gao (2022) Gao R (2022) Finite-sample guarantees for Wasserstein distributionally robust optimization: Breaking the curse of dimensionality. Operations Research .

- Gao et al. (2022) Gao R, Chen X, Kleywegt AJ (2022) Wasserstein distributionally robust optimization and variation regularization. Operations Research .

- Gao and Kleywegt (2023) Gao R, Kleywegt A (2023) Distributionally robust stochastic optimization with Wasserstein distance. Mathematics of Operations Research 48(2):603–655.

- Gibbs and Su (2002) Gibbs AL, Su FE (2002) On choosing and bounding probability metrics. International Statistical Review 70(3):419–435.

- Goh and Sim (2010) Goh J, Sim M (2010) Distributionally robust optimization and its tractable approximations. Operations Research 58(4-part-1):902–917.

- Hoerl and Kennard (1970) Hoerl AE, Kennard RW (1970) Ridge regression: Biased estimation for nonorthogonal problems. Technometrics 12(1):55–67.

- Horel (1962) Horel A (1962) Application of ridge analysis to regression problems. Chemical Engineering Progress 58:54–59.

- Howard et al. (2019) Howard A, Sandler M, Chu G, Chen LC, Chen B, Tan M, Wang W, Zhu Y, Pang R, Vasudevan V, Le QV, Adam H (2019) Searching for mobilenetv3. Proceedings of the IEEE/CVF International Conference on Computer Vision, 1314–1324.

- Hu and Hong (2013) Hu Z, Hong LJ (2013) Kullback-Leibler divergence constrained distributionally robust optimization. Available at Optimization Online 1(2):9.

- Huber (1973) Huber PJ (1973) Robust regression: Asymptotics, conjectures and monte carlo. The Annals of Statistics 799–821.

- Hurtik et al. (2022) Hurtik P, Tomasiello S, Hula J, Hynar D (2022) Binary cross-entropy with dynamical clipping. Neural Computing and Applications 34(14):12029–12041.

- Jiang et al. (2021) Jiang H, Luo S, Dong Y (2021) Simultaneous feature selection and clustering based on square root optimization. European Journal of Operational Research 289(1):214–231.

- Jiang and Guan (2016) Jiang R, Guan Y (2016) Data-driven chance constrained stochastic program. Mathematical Programming 158(1-2):291–327.

- Koenker and Bassett Jr (1978) Koenker R, Bassett Jr G (1978) Regression quantiles. Econometrica: Journal of the Econometric Society 33–50.

- Koenker and Hallock (2001) Koenker R, Hallock KF (2001) Quantile regression. Journal of Economic Perspectives 15(4):143–156.

- Krokhmal (2007) Krokhmal PA (2007) Higher moment coherent risk measures. Quantitative Finance 7(4):373–387.

- Kuhn et al. (2019) Kuhn D, Esfahani P, Nguyen V, Shafieezadeh-Abadeh S (2019) Wasserstein distributionally robust optimization: Theory and applications in machine learning. Operations Research & Management Science In The Age Of Analytics. pp. 130-166

- Lee et al. (2005) Lee YJ, Hsieh WF, Huang CM (2005) -SSVR: A smooth support vector machine for -insensitive regression. IEEE Transactions on Knowledge and Data Engineering 17(05):678–685.

- Li et al. (2022) Li J, Lin S, Blanchet J, Nguyen V (2022) Tikhonov Regularization is Optimal Transport Robust under Martingale Constraints. Advances In Neural Information Processing Systems. 35:17677-17689

- Li et al. (2018a) Li X, Sun DF, Toh KC (2018a) On efficiently solving the subproblems of a level-set method for fused Lasso problems. SIAM Journal on Optimization 28(2):1842–1866

- Li et al. (2018b) Li X, Sun DF, Toh KC (2018b) A highly efficient semismooth Newton augmented Lagrangian method for solving Lasso problems. SIAM Journal on Optimization 28(1): 433–458

- Lounici et al. (2011) Lounici K, Pontil M, Van De Geer S, Tsybakov AB (2011) Oracle inequalities and optimal inference under group sparsity. The Annals of Statistics 39(4):2164 – 2204.

- Luo et al. (2019) Luo Z, Sun DF, Toh KC, Xiu N (2019) Solving the OSCAR and SLOPE models using a semismooth Newton-based augmented Lagrangian method. Journal of Machine Learning Research, 20(106):1–25

- Mohajerin Esfahani and Kuhn (2018) Mohajerin Esfahani P, Kuhn D (2018) Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming 171(1-2):115–166.

- Montiel Olea et al. (2023) Montiel Olea JL, Rush C, Velez A, Wiesel J (2023) The out-of-sample prediction error of the square-root-LASSO and related estimators. arXiv preprint arXiv:2211.07608.

- Peyré and Cuturi (2017) Peyré G, Cuturi M (2017) Computational optimal transport. Center for Research in Economics and Statistics Working Papers (2017-86).

- Plan and Vershynin (2012) Plan Y, Vershynin R (2012) Robust 1-bit compressed sensing and sparse logistic regression: A convex programming approach. IEEE Transactions on Information Theory 59(1):482–494.

- Ramsay and Dalzell (1991) Ramsay JO, Dalzell C (1991) Some tools for functional data analysis. Journal of the Royal Statistical Society: Series B (Methodological) 53(3):539–561.

- Ramsay and Silverman (2005) Ramsay JO, Silverman BW (2005) Functional Data Analysis. Springer Series in Statistics (New York: Springer), 2nd edition, ISBN 978-0-387-40080-8.

- Schölkopf et al. (1998) Schölkopf B, Bartlett P, Smola A, Williamson R (1998) Support vector regression with automatic accuracy control. ICANN 98: Proceedings of the 8th International Conference on Artificial Neural Networks, 111–116 (Springer).

- Schölkopf et al. (2000) Schölkopf B, Smola AJ, Williamson RC, Bartlett PL (2000) New support vector algorithms. Neural Computation 12(5):1207–1245.

- Scott (2012) Scott C (2012) Calibrated asymmetric surrogate losses. Electronic Journal of Statistics 6(none):958 – 992.

- Shafieezadeh-Abadeh et al. (2023) Shafieezadeh-Abadeh S, Aolaritei L, Dörfler F, Kuhn D (2023) New perspectives on regularization and computation in optimal transport-based distributionally robust optimization. ArXiv Preprint ArXiv:2303.03900.

- Shafieezadeh-Abadeh et al. (2019) Shafieezadeh-Abadeh S, Kuhn D, Esfahani PM (2019) Regularization via mass transportation. Journal of Machine Learning Research 20(103):1–68.

- Shafieezadeh-Abadeh et al. (2015) Shafieezadeh-Abadeh S, Mohajerin Esfahani PM, Kuhn D (2015) Distributionally robust logistic regression. Advances in Neural Information Processing Systems, volume 28.

- Shen et al. (2017) Shen X, Niu L, Qi Z, Tian Y (2017) Support vector machine classifier with truncated pinball loss. Pattern Recognition 68:199–210.

- Sion (1958) Sion M (1958) On general minimax theorems. Pacific Journal of Mathematics 8(1):171–176.

- Stucky and Van De Geer (2017) Stucky B, Van De Geer S (2017) Sharp oracle inequalities for square root regularization. Journal of Machine Learning Research 18(67):1–29.

- Tang et al. (2020) Tang P, Wang C, Sun DF, Toh KC (2020) A sparse semismooth Newton based proximal majorization-minimization algorithm for nonconvex square-root-loss regression problem. The Journal Of Machine Learning Research. 21, 9253-9290

- Tong and Ng (2018) Tong H, Ng M (2018) Analysis of regularized least squares for functional linear regression model. Journal of Complexity 49:85–94.

- Vapnik and Chervonenkis (2015) Vapnik VN, Chervonenkis AY (2015) On the uniform convergence of relative frequencies of events to their probabilities. Measures of Complexity: Festschrift for Alexey Chervonenkis, 11–30 (Springer).

- Villani (2009) Villani C (2009) Optimal Transport: Old and New, volume 338 (Springer).

- Wang et al. (2016) Wang JL, Chiou JM, Müller HG (2016) Functional data analysis. Annual Review of Statistics and its Application 3:257–295.

- Wang et al. (2020) Wang Q, Ma Y, Zhao K, Tian Y (2020) A comprehensive survey of loss functions in machine learning. Annals of Data Science 1–26.

- Wiesemann et al. (2014) Wiesemann W, Kuhn D, Sim M (2014) Distributionally robust convex optimization. Operations Research 62(6):1358–1376.

- Wu et al. (2022) Wu Q, Li JYM, Mao T (2022) On generalization and regularization via Wasserstein distributionally robust optimization. arXiv preprint arXiv:2212.05716.

- Yi-de et al. (2004) Yi-de M, Qing L, Zhi-Bai Q (2004) Automated image segmentation using improved pcnn model based on cross-entropy. Proceedings of 2004 International Symposium on Intelligent Multimedia, Video and Speech Processing, 2004., 743–746 (IEEE).

- Zhang et al. (2022) Zhang L, Yang J, Gao R (2022) A simple and general duality proof for Wasserstein distributionally robust optimization. arXiv preprint arXiv:2205.00362.

- Zhang et al. (2020) Zhang Y, Zhang N, Sun DF, Toh KC (2020) An efficient Hessian based algorithm for solving large-scale sparse group Lasso problems. Mathematical Programming, 179(1): 223–263

- Zhen et al. (2023) Zhen J, Kuhn D, Wiesemann W (2023) A unified theory of robust and distributionally robust optimization via the primal-worst-equals-dual-best principle. Operations Research.