Estimation of conditional average treatment effects on distributed data: A privacy-preserving approach

Abstract

Estimation of conditional average treatment effects (CATEs) is an important topic in various fields such as medical and social sciences. CATEs can be estimated with high accuracy if distributed data across multiple parties can be centralized. However, it is difficult to aggregate such data if they contain privacy information. To address this issue, we proposed data collaboration double machine learning (DC-DML), a method that can estimate CATE models with privacy preservation of distributed data, and evaluated the method through numerical experiments. Our contributions are summarized in the following three points. First, our method enables estimation and testing of semi-parametric CATE models without iterative communication on distributed data. Semi-parametric or non-parametric CATE models enable estimation and testing that is more robust to model mis-specification than parametric models. However, to our knowledge, no communication-efficient method has been proposed for estimating and testing semi-parametric or non-parametric CATE models on distributed data. Second, our method enables collaborative estimation between different parties as well as multiple time points because the dimensionality-reduced intermediate representations can be accumulated. Third, our method performed as well or better than other methods in evaluation experiments using synthetic, semi-synthetic and real-world datasets.

Keywords— Statistical causal inference; Conditional average treatment effect; Double machine learning; Distributed data; Privacy-preserving method; Collaborative data analysis

1 Introduction

The Neyman–Rubin model (Imbens and Rubin, 2015) or potential outcomes framework is one of the main causal inference methods for estimating average treatment (intervention) effects and has been developed and applied in many studies since its establishment by Rubin. In recent years, there have been innovations that enable the estimation of individual or conditional average treatment effects (CATEs) by adapting not only statistical but also machine learning methods. (e.g., Künzel et al. (2019); Athey et al. (2019)) Most methods for estimating CATEs assume that the data can be centralized in one place. However, if the distributed data contains confidential or private information, it is difficult to centralized them in one place.

Conversely, in the field of machine learning, a privacy-preserving analysis method called federated learning has been developed in recent years. (Konečnỳ et al., 2016; McMahan et al., 2017) Data collaboration (DC) analysis (Imakura and Sakurai, 2020; Bogdanova et al., 2020; Imakura et al., 2021b, 2023), one of federated learning systems, is a method that allows collaborative analysis with privacy preservation by sharing dimensionality-reduced intermediate representations instead of raw data. DC analysis was originally proposed to construct regression and classification models from distributed data. Recently, Kawamata et al. (2024) proposed data collaboration quasi-experiment (DC-QE), that extends DC analysis to allow estimation of average treatment effect (ATE). In this paper, we propose data collaboration double machine learning (DC-DML) as a method to estimate CATEs while preserving the privacy of distributed data by incorporating double machine learning (DML) (Chernozhukov et al., 2018), a machine learning-based treatment effect estimation method, into DC-QE. Moreover, through numerical experiments, we evaluate the performance of our method compared to existing methods.

The effects of policy interventions by governments or medical treatments by hospitals are likely to differ across people. It is possible to improve the overall performance of the treatment if one knows which individuals should be treated. For example, by concentrating scholarship support on those whose future income increases will be higher owing to the treatment, the limited budget can be used more efficiently. In addition, by concentrating medication on those who are more likely to improved or have fewer side effects from the treatment, medication can be more effective and safer to use. One approach to estimating CATEs for these situations with a high accuracy is to centralize data from many parties, but this is difficult owing to privacy concerns. Our method enables to estimate CATEs with high accuracy while maintaining the privacy of distributed data across many parties.

Our contributions are summarized in the following three points. First, our method enables estimation and testing of semi-parametric CATE models without iterative communication on distributed data. Semi-parametric or non-parametric CATE models enable estimation and testing that is more robust to model mis-specification than parametric models. However, to our knowledge, no communication-efficient method has been proposed for estimating and testing semi-parametric or non-parametric CATE models on distributed data. Second, our method enables collaborative estimation between different parties as well as multiple time points because the dimensionality-reduced intermediate representations can be accumulated. Third, our method performed as well or better than other methods in evaluation experiments using synthetic, semi-synthetic and real-world datasets.

The remainder of this paper is organized as follows. In Section 2, we present related work. We describe the basics of causal inference and distributed data in Section 3. We describe our method in Section 4. In Section 5, we report the numerical experiments and discuss the results in Section 6. Finally, we conclude in Section 7.

2 Related works

The field of treatment effect estimation has advanced significantly in recent years through the incorporation of machine learning methods as well as statistics. However, studies that take into account privacy preservation, which is our aim, are limited. Here, we briefly review existing methods.

DML is an innovative method proposed by Chernozhukov et al. (2018) that allows estimation of ATE using any machine learning methods. DML is a semi-parametric method that uses machine learning to estimate nuisance parameters for estimating target parameters. More specifically, DML first estimates nuisance parameters using machine learning, and then estimates the target parameters using the estimated nuisance parameters. DML resolves influences of regularization bias and over-fitting on estimates of target parameters through Neyman–orthogonal scores and cross-fitting, respectively. As shown in Section 3, DML can be extended easily to allow estimation of CATE. DML is a useful method for estimating treatment effects, but using centralized data. To achieve our goal, we need to develop DML to address distributed data. In Section 3, we describe DML in detail.

As representative methods that utilize machine learning for CATE estimation, generalized random forest (GRF) (Athey et al., 2019) and X-Learner (Künzel et al., 2019) have been proposed, but these methods cannot be applied to distributed data. GRF is a non-parametric method for estimating treatment effects by solving local moment equations using random forests. GRF first constructs a random forest, then calculates weights for each sample from the random forest, and finally derives the treatment effect by solving a moment equations using the calculated weights. X-Learner is a non-parametric method that can estimate treatment effects from any machine learning model. X-Learner uses propensity scores (Rosenbaum and Rubin, 1983) to resolve performance degradation that occurs when controlled or treated group is much larger than the other group.

Conversely, Secure regression (SR) (Karr et al., 2005) and FedCI (Vo et al., 2022) are methods that can estimate CATEs from distributed data. SR is a parametric method for estimating linear regression models. In SR, statistics necessary to compute least squares estimates are calculated in each local party, and these statistics are shared. SR is communication-efficient because it enables estimation of a linear model by sharing statistics only once. However, in SR, bias owing to mis-specification can occur if the assumptions of the linear model are incorrect. FedCI is a non-parametric method that constructs a potential outcome model based on Gaussian processes through federated learning approach. In FedCI, the communication between the clients and the server is iterated: each client sends the model gradient calculated from its local data to the server, then the server averages the aggregated gradients, updates its own model parameters, and returns those parameters to the clients. In the case where local data is stored in a location isolated from the Internet or synchronization of communications is not possible, FedCI is difficult to execute.

While the purpose of our method is to estimate CATEs, ifedtree (Tan et al., 2022), Federated MLE, IPW and AIPW (Xiong et al., 2023), and DC-QE (Kawamata et al., 2024) are methods that have been proposed for different estimation targets. Those methods can address distributed data. ifedtree is a tree-based model averaging approach to improve the CATE estimation at a specific party by sharing models derived from other parties instead of raw data. Our method aims to estimate CATEs on aggregated whole data, rather than on specific party data. Federated MLE, IPW and AIPW are a parametric methods that aggregates individually estimated gradients for estimating propensity scores and treatment effects. Federated MLE, IPW and AIPW estimate the ATE not conditioned on covariates.

DC-QE is a semi-parametric method for estimating ATE and ATT based on a DC analysis framework. As shown in Algorithm 1, DC-QE first construct collaborative representations based on dimensionality-reduced intermediate representations collected from all parties instead of raw data, second estimates propensity scores, finally estimates ATE or ATT using the estimated propensity scores. Our method extends DC-QE to address DML for CATE estimation.

Table 1 summarizes five of those described in this section that are particularly relevant to our method. In Section 4, we propose a method for estimating CATEs in a semi-parametric model while preserving privacy of distributed data. Although DML, GRF and X-Learner are methods for centralized data, our method address distributed data. Moreover, our method is more robust than SR for model misspecification and more communication-efficient than FedCI.

| Methods |

|

|

|

||||||

|---|---|---|---|---|---|---|---|---|---|

|

No | Semi-parametric | - | ||||||

|

No | Non-parametric | - | ||||||

|

No | Non-parametric | - | ||||||

|

Yes | Parametric | No | ||||||

|

Yes | Non-parametric | Yes | ||||||

|

Yes | Semi-parametric | No |

3 DML with the linear CATE model

In this section, we describe the DML method with the linear CATE model. Under the Neyman–Rubin causal model, let variables for subject as , , and , where is the -dimensional covariates vector, is the treatment, is the outcome that subject would have if they were treated (), and is that if not (controlled; ). Moreover, we denote . With this definition, the CATE is defined as

| (1) |

In DML, we make the following structural equation assumptions on the data generating process as

| (2) | ||||

| (3) |

is the function that represents the effect of the treatment conditional on the covariate . The covariates affect the treatment via the function and the outcome via the function , where and are defined as functions belong to convex subsets and with some normed vector space. and are disturbances such that , and . In this data generating process, the function of our interest is because obviously , while and are not functions of our interest. Note that, Chernozhukov et al. (2018) assumed that is constant, i.e., independent of . However, as we discuss below, we can estimate similarly to Chernozhukov et al. (2018) even when that linearly depends on .

In this paper, we derive by a partialling-out approach as follows: we can re-write the structural equations as

| (4) |

Here, define , where belongs a convex subset with some normed vector space. Then, the residuals for and are

| (5) | ||||

| (6) |

So we can obtain

| (7) |

Note that because and .

To derive , consider the following score vector:

| (10) |

Define the moment condition

| (11) |

and Neyman–orthogonality (Chernozhukov et al., 2018)

| (12) |

where , and . The Neyman–orthogonality implies first-order insensitivity to perturbations of the nuisance functions and . Then, we have Theorem 1, whose proof is in Appendix A.

Theorem 1.

Given and , can be obtained by solving (11) empirically from dataset as:

| (13) |

(13) indicates that is the solution of the regression problem from to . That is

| (14) |

The DML uses machine learning models to estimate and , and cross-fitting is applied to reduce the effect of over-fitting on the estimation of parameter . In this paper, we conduct cross-fitting by splitting the data into two folds (). To derive the variance of , re-write (10) as

| (15) |

where

| (16) |

From Theorem 3.2 in Chernozhukov et al. (2018), the asymptotic variance of is

| (17) |

Here, and are the functions, and is the set of subjects for fold . Moreover,

| (18) |

Then, the variance of is

| (19) |

In summary, the DML procedure can be expressed as the following two steps. First, and are estimated from the two folds using machine learning models to obtain the estimated residuals: and . Second, is estimated by regressing to .

4 Method

We describe our method in this section. Prior to that, we explain the data distribution that our method focuses on. Let be the numbers of subjects (samples) in a dataset. Moreover, let , and be the datasets of covariates, treatments, and outcomes, respectively. We consider that subjects are partitioned horizontally into parties, as follows:

| (23) | ||||

| (27) | ||||

| (31) |

The th party has a partial dataset and corresponding treatments and outcomes, which are , where is the number of subjects for each party in the th row ().

In the following, this section proceeds as: we first describe our method in Section 4.1, second analyze the correctness of our method in Section 4.2, third propose a dimension reduction method for DC-DML in Section 4.3, and finally the advantages and disadvantages in Section 4.4.

4.1 DC-DML

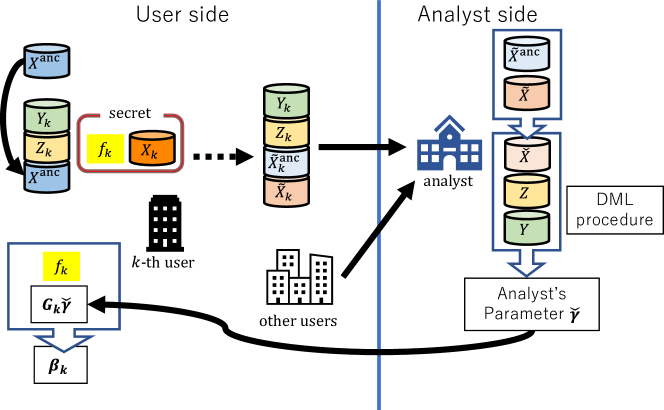

Our method DC-DML is based on DC-QE (Kawamata et al., 2024) and DML (Chernozhukov et al., 2018), and enables to estimate CATE with privacy preservation of distributed data. As in Kawamata et al. (2024), DC-QE operates in two roles: user and analyst roles. Each user have private covariates , treatments and outcomes . DC-QE is conducted in three stages: construction of collaborative representations, estimation by the analyst, and estimation by the users. In the first stage, each user individually constructs intermediate representations and shares them with the analyst instead of the private dataset, then the analyst constructs the collaborative representations. In the second stage, the analyst estimates its own coefficients and variance using DML, and shares them with all users. In the final stage, each user calculates its own coefficients and variance. Each stage is described in turn from Section 4.1.1 to 4.1.3. The pseudo-code of DC-DML, described below, is given in Algorithm 2. Fig. 1 shows an overall illustration of DC-DML.

4.1.1 Construction of collaborative representations

In the first stage, construction of collaborative representations, we use the aggregation method proposed in Imakura and Sakurai (2020). First, users generate and share an anchor dataset , which is a shareable dataset consisting of public or randomly constructed dummy data, where is the number of subjects in the anchor data. The anchor dataset is used to compute the transformation matrices (described below as ) required to construct the collaborative representations. Second, each user constructs intermediate representations using a linear row-wise dimensionality reduction function such as principal component analysis (PCA) (Pearson, 1901), locality preserving projection (LPP) (He and Niyogi, 2003) and factor analysis (FA) (Spearman, 1904). is consisting of a transformation matrix and a shift vector . is the reduced dimension. is a mean vector in with centering such as PCA and FA, or a zero vector in without centering such as LPP. Then, the dimensionality reduction function is applied as

| (32) | ||||

| (33) |

Moreover, is private and can differ from other users. To consider the constant term in the linear CATE model, we combine to and . Formally, we can represent those as

| (34) | ||||

| (35) |

where

| (36) |

Finally, each user shares the intermediate representations and , treatments and outcomes to the analyst.

Next, the analyst transforms the shared intermediate representations into an common form called collaborative representations. To do this, the analyst computes the transformation functions for all such that

| (37) |

where and is the dimension of collaborative representations. Then, we have the collaborative representation for as

| (38) |

Let

| (39) |

be a low-rank approximation based on singular value decomposition of the matrix combining , where is a diagonal matrix whose diagonal entries are the larger parts of the singular values and and are column orthogonal matrices whose columns are the corresponding left and right singular vectors, respectively. Matrix is then computed as

| (40) |

where denotes the Moore–Penrose inverse. Then, the collaborative representations are given by

| (41) |

4.1.2 Estimation by the analyst

In the second stage, estimation by the analyst, the analyst estimates their own CATE model based on the DML procedure that we described in Section 3. The analyst considers the data generation process as

| (42) | ||||

| (43) |

and the linear CATE model as

| (44) |

where and is the collaborative representation of . The score vectors for the analyst are defined as

| (45) | ||||

| (46) |

where and are the analyst’s functions, and is the analyst’s estimates.

The analyst’s purpose in the second stage is to obtain . To accomplish this, first, the analyst constructs and from , and using machine learning models to estimate residuals and . The estimated residuals are expressed as

| (47) | ||||

| (48) |

Second, the analyst calculates and . is the least squares solution of the following regression equation:

| (49) |

That is

| (50) |

The analyst can calculate the variance of in (17), (18) and (19), replacing , and with , and , respectively.

4.1.3 Estimation by the users

In the final stage, estimation by the users, the users estimates their own CATE model based on parameters that the analyst returns. The analysts’s CATE model is written as

| (51) | ||||

| (52) |

Then, for user , subject ’s estimated CATE based on the analyst’s parameter is written as

| (53) | ||||

| (54) | ||||

| (55) |

where

| (56) |

and

| (57) |

For user , is a constant term and are coefficients for in their CATE model. Thus, user ’s coefficients are expressed as .

The variance of is

| (58) |

Then, the variance of is

| (59) |

User can statistically test their CATE model if they obtains , and . To accomplish this, the following procedure is conducted in the final stage. First, the analyst returns and to user . Then, user calculates and as

| (60) | ||||

| (61) |

Moreover, user calculates and using (57) and (59), respectively. Then, user obtained , and , and can test statistically .

4.2 Correctness of DC-DML

In this section, through a similar approach to Imakura et al. (2023), we discuss the correctness of DC-DML. Now, we consider the following subspace depending on ,

| (64) |

where denotes the range of a matrix. Define centralized analysis (CA) as collecting and analyzing the raw data, i.e., , and , in one place. This is an ideal analysis, but not possible if the raw data contains private information. Then, we have Theorem 2, whose proof is in Appendix B.

Theorem 2.

Let and be the coefficients computed in the CA, and that of user computed in DC-DML, respectively. Moreover, and are functions computed in the CA. If , , , and for all , then .

4.3 A dimension reduction method for DC-DML

In this section, we propose a dimensionality reduction method for DC-DML with reference to Theorem 2. The dimensionality reduction method strongly affects the performance of DC-DML. In DC-DML, the coefficients is obtained from the subspace . If we could estimate close to , the coefficients in the CA, we can obtain close to . To accomplish this, the subspace should contain .

Using an approach similar to Imakura et al. (2023), we consider a dimensionality reduction method for DC-DML as shown Algorithm 3. The basic idea of the approach is that each user constructs based on estimates of obtained from their own local dataset. The estimate of obtained by each user could be a good approximation of . Thus, a bootstrap-based method can be a reasonable choice to achieve a good subspace. Let be a parameter for sampling rate. In Algorithm 3, first, through the DML procedure by a random samplings of size , user obtains estimates of as . Then, user constructs , where is a vector excluding the first element of . The reason of excluding the first element of is that should be a transformation matrix for -dimensional covariates. However, since the first column of is as in (36), the subspace contains the full range that the first element of can take.

In addition, as with Imakura et al. (2023), the subspace can be constructed by combining multiple dimensionality reduction methods. Let and be the transformation matrices of the bootstrap-based and other methods, respectively, where . Then, is

| (65) |

4.4 Advantage and disadvantage

In this section, we describe the advantages and disadvantages of DC-DML. Those are attributed to DC-QE or DML with the linear CATE model described in Section 3.

There are four advantages. First, dimensionality reduction preserves the privacy of covariates. It is impossible to completely restore the raw data from the intermediate representations because of the dimensionality reduction. Moreover, by not sharing the dimensionality reduction function among users, even if others obtain a user’s intermediate representations, they cannot infer the user’s raw data. For more discussion for privacy preservation, refer to Imakura et al. (2021a). Second, since DC-DML enables to collect a larger number of samples from distributed data, it is possible to obtain better performance than in individual analysis. Third, as shown in Algorithm 2, DC-DML does not require repetitive communication (communication efficient). Finally, DC-DML is less susceptible to model mis-specification because it assumes a semi-parametric model.

Conversely, there are three disadvantages. First, DC-DML cannot be used directly if privacy information is included in the treatments or outcomes. Solutions to this issue include, for example, transforming treatments or outcomes into a format that preserves privacy through encryption and so on. Second, the performance of the resulting model may deteriorate because the dimensionality reduction reduces the information in the raw data. However, obtaining more samples from the distributed data can improve performance more than the deterioration caused by dimensionality reduction. Finally, if the linear CATE model is not valid, i.e. non-linear, DC-DML may obtain incorrect conclusions.

5 Experiments

In this section we describe three experiments we conducted to demonstrate the effectiveness of DC-DML. 111We performed the experiments using Python codes, which are available from the corresponding author by reasonable request. Through the experiments, we show that DC-DML performs better than individual analysis (IA), the analysis performed by the user using only their own dataset. We will also investigate through the experiments how closely DC-DML performs to a CA. In Experiment I using, that uses synthetic data, we show that DC-DML is useful in the setting of data distributions that would be incorrectly estimated by individual analysis. In Experiment II, that uses semi-synthetic data generated from the infant dataset, we compare the performances between DC-DML and the other methods. In Experiment III, that uses real-world data from the financial assets and jobs datasets, we investigate the robustness of DC-DML performance in the presence of heterogeneous numbers of subjects or treatment group proportions per party.

In Experiment II, the methods to be compared to DC-DML are as follows. First are the DMLs in IA and CA, that we denote for convenience as IA-DML and CA-DML, respectively. As described above, IA-DML and CA-DML are, respectively, targets that DC-DML should perform better and closer to. Second, GRF and X-Learner in IA and CA, denoted for convenience with the prefixes IA- and CA-: IA-GRF, CA-GRF, IA-XL, and CA-XL. Finally, the distributed data analysis methods SR and FedCI.

In the experiments, we set up the machine learning models used in DML and X-learner as follows. First, both machine learning models used to estimate and in the DML methods (IA-DML, CA-DML and DC-DML) in the Experiment I are random forests. Second, the settings of the machine learning models used in Experiments II and III are as follows. We selected the machine learning models used to estimate in the DML methods by our preliminary experiments from among five regression methods: multiple regression, random forests, K-nearest neighbor, light gradient boosting machine (LGBM) and support vector machine (SVM) with standardization. In the preliminary experiments for , we repeated the regression of the outcomes on the covariates for the candidate methods in the CA setting 50 times and set the criterion of selecting the one with the smallest root mean squared errors (RMSE) average. For , similarly, we selected by preliminary experiments among five classification methods: logistic regression, random forests, K-nearest neighbor, LGBM and SVR. In our preliminary experiments for , we followed the similar procedure as for , where we set the criterion of selecting the one with the smallest average Brier score. Here, Brier Score is a mean squared error measure of probability forecasting. (Brier, 1950) The hyperparameters for the candidate methods were the default values shown in Appendix C. As a result of our preliminary experiments, we chose SVM as the machine learning models to be used in the estimation of and , both in Experiment II. For the financial data set in Experiment III, we set and to multiple regression and logistic regression, respectively. For the jobs dataset, we set and to multiple regression and random forest, respectively. We use the same models for the outcome and propensity score in X-Learner (IA-XL and CA-XL) as in DML in all experiments. The results of the preliminary experiments are in Appendix D.

The settings used in DC-DML are as follows. As the intermediate representation construction methods, we used six: PCA, LPP, FA, PCA+B, LPP+B, and FA+B. Here, +B represents the combination with the bootstrap-based dimensionality reduction method. The intermediate representation dimension and collaborative representation dimension were and , respectively. In combination with the bootstrap-based dimensionality reduction method, the BS dimension was set to three in Experiment I and in Experiment II and III. Here, is the ceiling function. Anchor data were generated from uniform random numbers of maximum and minimum values for each covariate and thier subject number was the same of the original dataset .

As described below, in Experiment II, we used the five methods described in Section 2 as comparison methods: DML, GRF, X-Learner, SR and FedCI. Also, in Experiment III, we used DML and SR as comparison methods. See Appendix E for the detailed settings of those methods.

In Experiments II and III, the evaluation measures used were how close the estimates were to the benchmarks. The benchmarks in Experiments II and III were the true values and the average values of 50 trials of CA-DML, respectively. In this study, we consider four evaluation measures: the RMSE of CATE, the consistency rate of significance of CATE, the RMSE of coefficients, and the consistency rate of significance of coefficients.

The RMSE of CATE

The RMSE of CATE is a measure of how much the predicted CATE matched the benchmark CATE as

| (66) |

where is the benchmark CATE and is the estimated CATE. The lower this measure, the better.

The consistency rate of significance of CATE

The consistency rate of significance of CATE is the rate where the estimated CATE obtained a statistical test result of “significantly positive,” “significantly negative,” or “not significant” in 5% level when the benchmark CATE is positive, negative, or zero, respectively. For Experiment III, we set the benchmark CATE is positive, negative, or zero when the estimate in CA-DML is significantly positive, significantly negative or not significant, respectively, in 5% level. The higher this measure, the better. This measure was not calculated in X-Learner and FedCI, because statistical testing methods for CATE are not provided in those methods.

The RMSE of coefficients

The RMSE of coefficients is a measure of how much the estimated coefficients matched that of the benchmark as

| (67) |

where is the benchmark coefficient. The lower this measure, the better. Since GRF, X-Learner and FedCI are not models that estimate linear CATE, this measure was not calculated in those models.

The consistency rate of significance of coefficients

The consistency rate of significance of coefficients is the rate where the estimated coefficient obtained a statistical test result of “significantly positive,” “significantly negative,” or “not significant” in 5% level when the benchmark coefficient is positive, negative, or zero, respectively. For Experiment III, we set the benchmark coefficient is positive, negative, or zero when the estimate in CA-DML is significantly positive, significantly negative or not significant, respectively, in 5% level. The higher this measure, the better. As with the RMSE of coefficients, this measure was not calculated in GRF, X-Learner and FedCI.

5.1 Experiment I: Proof of concepts in synthetic data

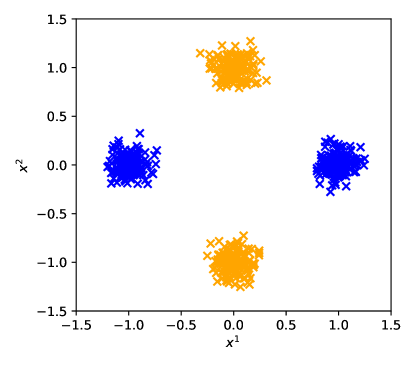

In Experiment I, we considered the situation where two parties () each had a dataset consisting of 300 subjects () and 10 covariates (). The covariates and were distributed as in Figure 2, where blue and orange markers represent that of party 1 and 2, respectively. The other covariates were drawn from a normal distribution .

The setting of the data generation process in Experiment I was

| (68) | ||||

| (69) | ||||

| (70) | ||||

| (71) | ||||

| (74) |

whre w.p. is “with probability”. In this setting, the constant term and the coefficients of and should be estimated to be significantly one.

Party 1 has the dataset with the broad distribution for covariate 1 and the narrow distribution for covariate 2. Thus, party 1 would be able to estimate the coefficient of covariate 1 relatively correctly in IA-DML, but would have difficulty estimating the coefficient of covariate 2. For party 2, the opposite of party 1 can be said.

The result of Experiment I is shown in Table 2. In CA-DML, the constant term and the coefficients of and are significant and close to their true values, and the coefficients of the other covariates are not significant. Thus, CA-DML obtained reasonable estimation results. Conversely, IA-DML obtained some wrong estimation results in both parties.

| Covariates | CA-DML | IA-DML | DC-DML(PCA+B) | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Party 1 | Party 2 | Party 1 | Party 2 | |||||||

| const. | 1.0283 | ** | 0.6300 | ** | 1.0068 | ** | 0.9563 | ** | 1.0207 | ** |

| 1.0610 | ** | 0.9952 | ** | 0.6950 | 1.0578 | ** | 1.0119 | ** | ||

| 1.1290 | ** | 2.0799 | 1.0359 | ** | 0.9042 | ** | 0.9761 | ** | ||

| -0.1628 | -0.1161 | -0.3211 | * | -0.0961 | -0.1269 | |||||

| -0.1595 | -0.0220 | -0.0021 | -0.1489 | -0.1264 | ||||||

| 0.0566 | -0.0924 | 0.1679 | 0.0147 | 0.0190 | ||||||

| 0.0905 | 0.3367 | * | -0.2482 | 0.1608 | 0.1354 | |||||

| -0.0434 | 0.0771 | -0.1849 | -0.0317 | -0.0960 | ||||||

| -0.0494 | -0.0397 | -0.1370 | -0.0336 | -0.0065 | ||||||

| 0.0607 | -0.0955 | 0.1867 | 0.0418 | 0.0536 | ||||||

| -0.1773 | -0.2022 | -0.0543 | -0.1270 | -0.1391 | ||||||

| ** , * | ||||||||||

DC-DML conducted by the PCA+B dimensionality reduction method obtained estimation results similar to CA-DML. This result suggests that even in situations where it is difficult to make valid estimates using IA-DML, DC-DML can produce more valid estimates than that.

5.2 Experiment II: Comparison with other methods in semi-synthetic data

In Experiment II, we evaluate the performance of DC-DML on semi-synthetic data generated from the infant health and development program (IHDP) dataset. The IHDP dataset is “a randomized experiment that began in 1985, targeted low-birth-weight, premature infants, and provided the treatment group with both intensive high-quality child care and home visits from a trained provider.” (Hill, 2011) 222The IHDP dataset is published as the supplementary file (https://www.tandfonline.com/doi/abs/10.1198/jcgs.2010.08162). The IHDP dataset is consisting of 25 covariates and a treatment variable and does not include an outcome variable. Thus, the outcomes needs to be synthetically set up for the experiment. Hill (2011) removed data on all children with nonwhite mothers from the treatment group to imbalance the covariates in the treatment and control groups. We followed this as well, and as a result, the dataset in Experiment II consisted of 139 subjects in the treatment group and 608 subjects in the control group.

In Experiment II, we considered the situation where three parties () each had a dataset consisting of 249 subjects () and 25 covariates (). The ratios of treatment groups were equal in all parties. The outcome variable in Experiment II we set as

| (75) | ||||

| (76) | ||||

| const. | (77) | |||

| (78) | ||||

| (79) |

where and are the average of and standard deviation of covariate , respectively, in the dataset. Note that, and were not defined because the treatments were included in the dataset.

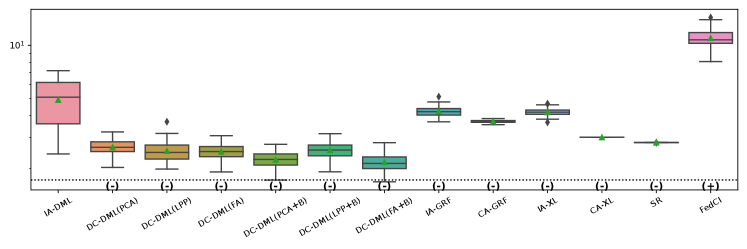

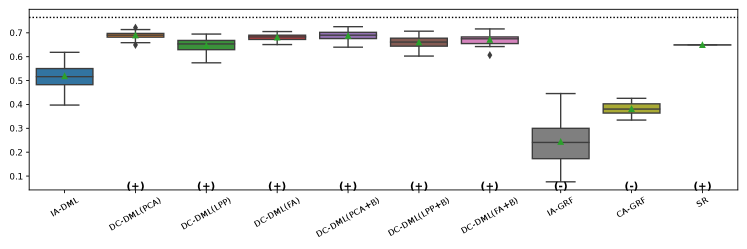

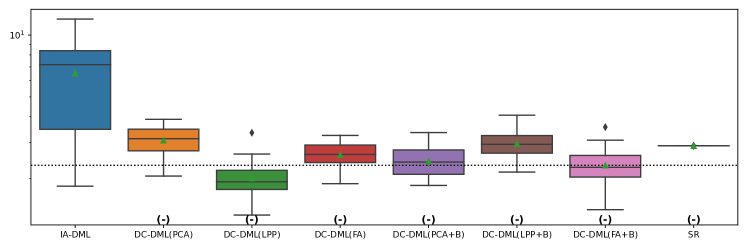

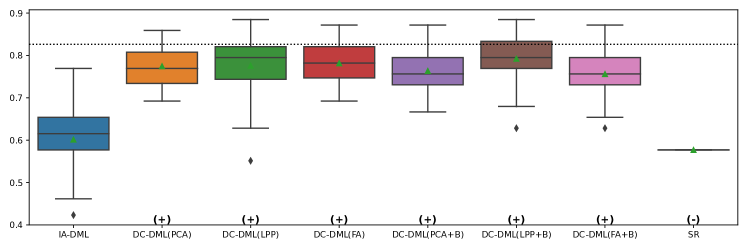

The results of the four evaluation measures in Experiment II is shown in Figures 3-6. In this experiment, we conducted 50 simulations with different random seed values for data distributing and machine learning. The symbols and in parentheses in the figures represent significant positive and significant negative differences from the IA-DML results, respectively, in -test. There were no methods that were not significantly different from DC-DML. The dashed line is the average of the CA-DML results. The triangle markers represent their average values.

As described below, Figures 3-6 show that DC-DML performs well for each of the evaluation measures in Experiment 2. First, as shown in Figure 3, the result for the RMSE of CATE shows that DC-DML significantly outperformed IA-DML. Moreover, DC-DML obtained better result than the existing methods. Second, as shown in Figure 4, the result for the consistency rate of significance of CATE shows that DC-DML significantly outperformed IA-DML. Moreover, DC-DML obtained better result than the existing methods. Third, as shown in Figure 5, the result for the RMSE of coefficients shows that DC-DML significantly outperformed IA-DML and are comparable to CA-DML and SR. Finally, as shown in Figure 6, the result for the consistency rate of significance of coefficients shows that DC-DML significantly outperformed IA-DML. Moreover, DC-DML obtained better result than SR. These results in Experiment II suggests that DC-DML can outperform IA-DML and obtain equal or better results than the existing methods.

5.3 Experiment III: Robustness to distribution settings in real-world data

Based on real-world datasets of financial assets and jobs, in Experiment III, we investigate the robustness of DC-DML performance in the case where the number of subjects or rate of treatment group across institutions is imbalanced. As the financial assets dataset, we focused on a sample of households from Wave 4 of the 1990 survey of income and program participation (SIPP). The SIPP dataset was used in Chernozhukov et al. (2018) to estimate the effect of 401(k) eligibility on accumulated assets. 333This dataset is avaiable from the repository for Chernozhukov et al. (2018) (https://github.com/VC2015/DMLonGitHub/). The SIPP dataset consists of 9915 observations and includes nine individual information (age, inc, educ, fsize, marr, twoearn, db, pira, hown) as covariates, 401(k) offerings as treatments, and net financial assets as outcomes. As the jobs dataset, we focused on employment data obtained from the national supported work (NSW) demonstration project and the panel study of income dynamics (PSID). The jobs dataset was used in Dehejia and Wahba (1999) to estimate the treatment effects of work experience and counseling on incomes. 444This dataset is avaiable from Rajeev Dehejia’s website (https://users.nber.org/~rdehejia/nswdata.html). The jobs dataset consists of 2675 observations and includes eight individual information (age, black, hispanic, married, no degree, re74) as covariates, trainings as treatments, and real earnings in 1978 as outcomes.

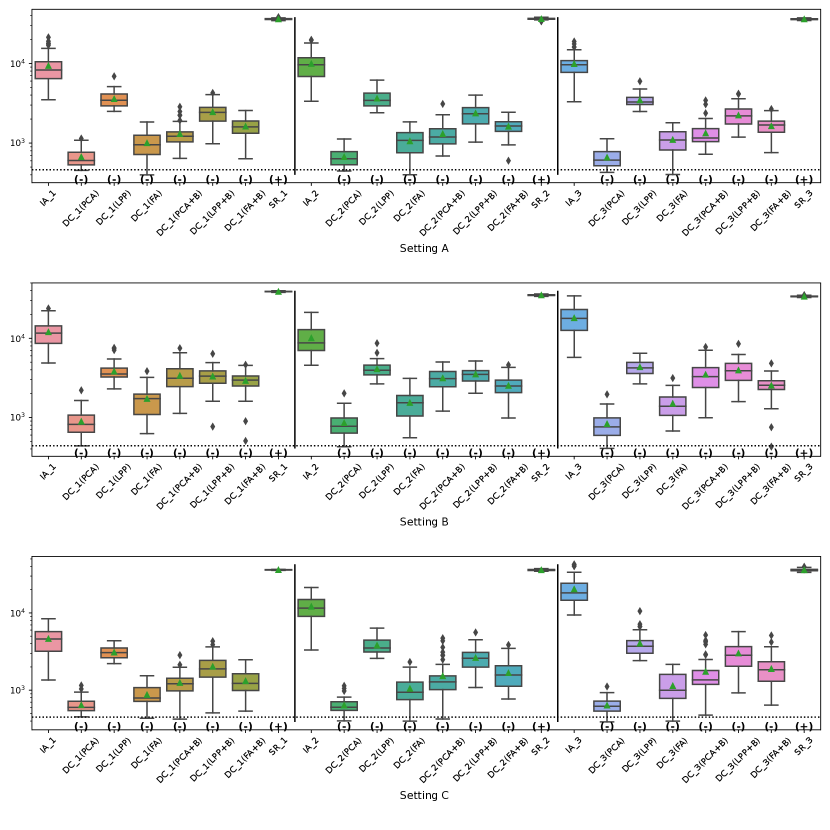

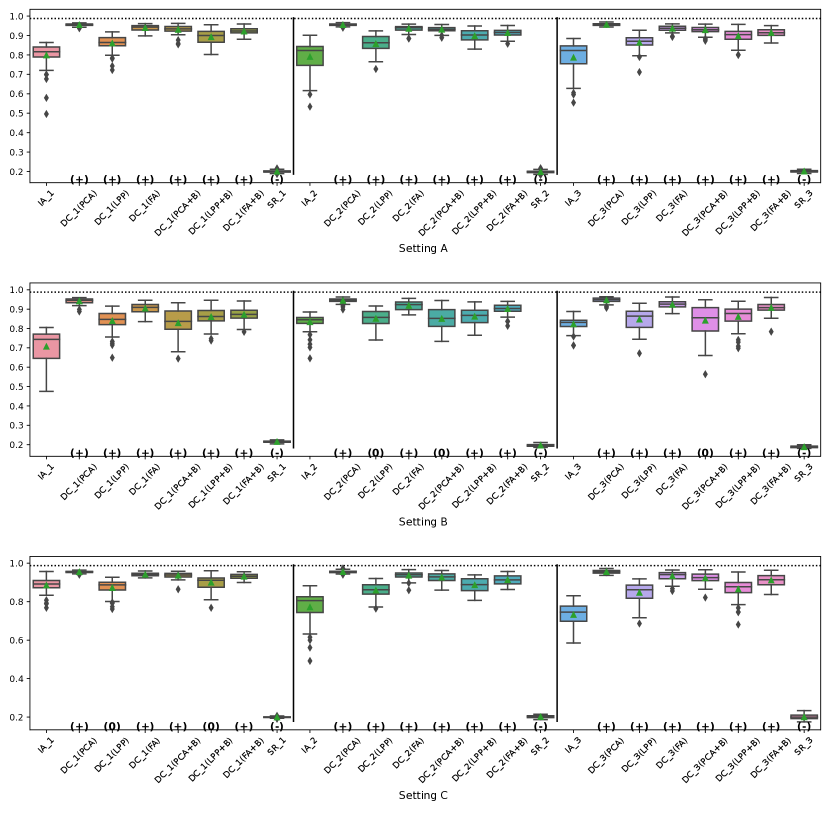

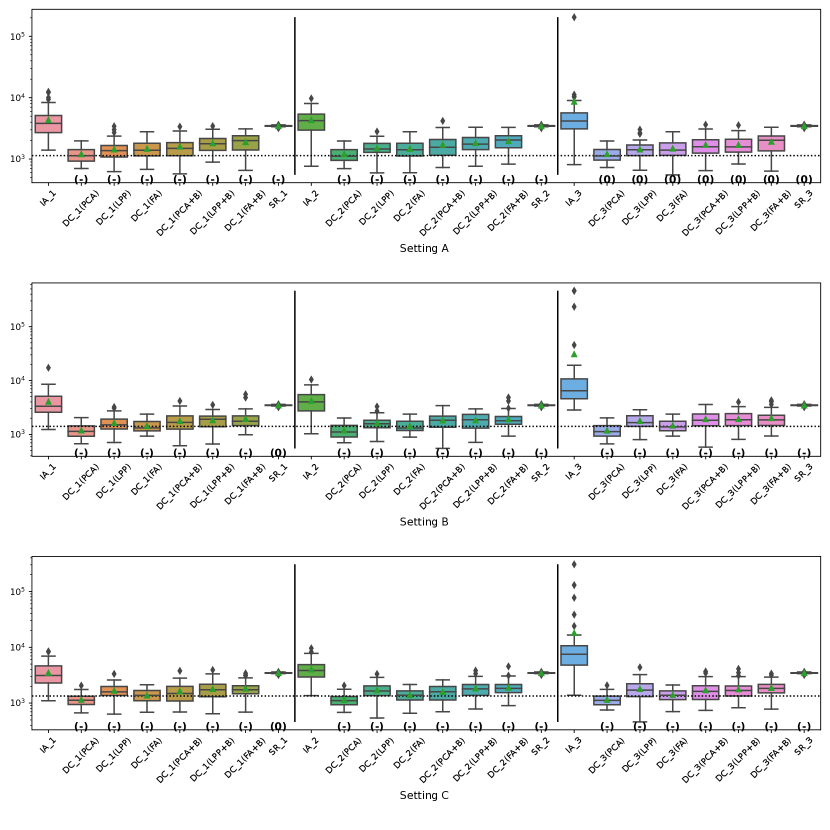

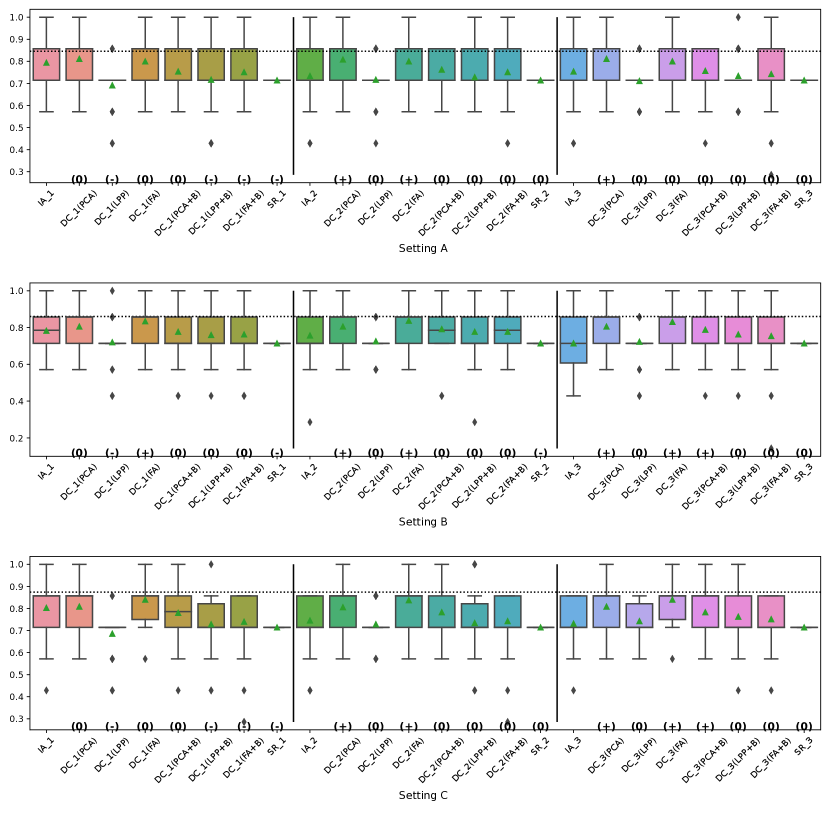

In Experiment III, we considered three parties () and three settings for data distribution where the rate of treatment group and the number of subjects are even or uneven, as shown in Table 3. In setting A, all parties have the same number of subjects and the same rate of treatment groups. In setting B, the number of subjects is even, but the rate of treatment groups differs across parties. In setting C, the number of subjects differs, but the rate of treatment groups is even across parties.

| setting A | setting B | setting C | ||||||||

| subjects | even | even | uneven | |||||||

| treatment rate | even | uneven | even | |||||||

| dataset | party | all | treated | controlled | all | treated | controlled | all | treated | controlled |

| financial assets | 1 | 3304 | 1227 | 2077 | 3304 | 2549 | 755 | 6864 | 2549 | 4315 |

| 2 | 3304 | 1227 | 2077 | 3304 | 849 | 2455 | 2287 | 849 | 1438 | |

| 3 | 3304 | 1227 | 2077 | 3304 | 283 | 3021 | 762 | 283 | 479 | |

| jobs | 1 | 891 | 61 | 830 | 891 | 92 | 799 | 1337 | 92 | 1245 |

| 2 | 891 | 61 | 830 | 891 | 61 | 830 | 891 | 61 | 830 | |

| 3 | 891 | 61 | 830 | 891 | 30 | 861 | 445 | 30 | 415 | |

In Experiment III, the result of CA-DML is used as the benchmark. Table 4 shows the average results of 50 trials of CA-DML. Note that, comparisons with GRF, X-Learner, and FedCI do not make sense because those assume the non-linear CATE model. Thus, only CA-DML, IA-DML and SR were considered as comparison with DC-DML.

| financial assets | jobs | ||||

|---|---|---|---|---|---|

| covariate | coefficient | covariate | coefficient | ||

| const. | -9705.1794 | const. | -7533.7519 | ||

| age | 172.0307 | age | 226.4912 | * | |

| inc | -0.1297 | black | 2493.7939 | ||

| educ | 642.9040 | hispanic | 1519.3141 | ||

| fsize | -1003.0686 | married | -2215.7011 | ||

| marr | 1102.9090 | no_degree | -858.5624 | ||

| twoearn | 5607.3989 | re74 | -0.3354 | ||

| db | 5657.7264 | * | |||

| pira | -1032.3599 | ||||

| hown | 5324.2854 | * | |||

| * | |||||

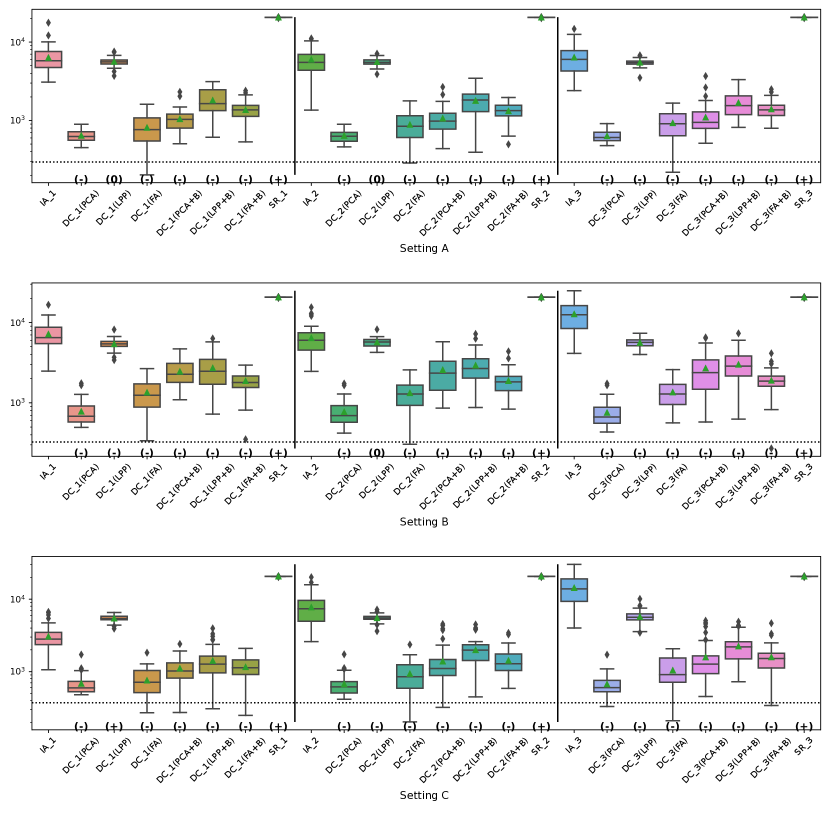

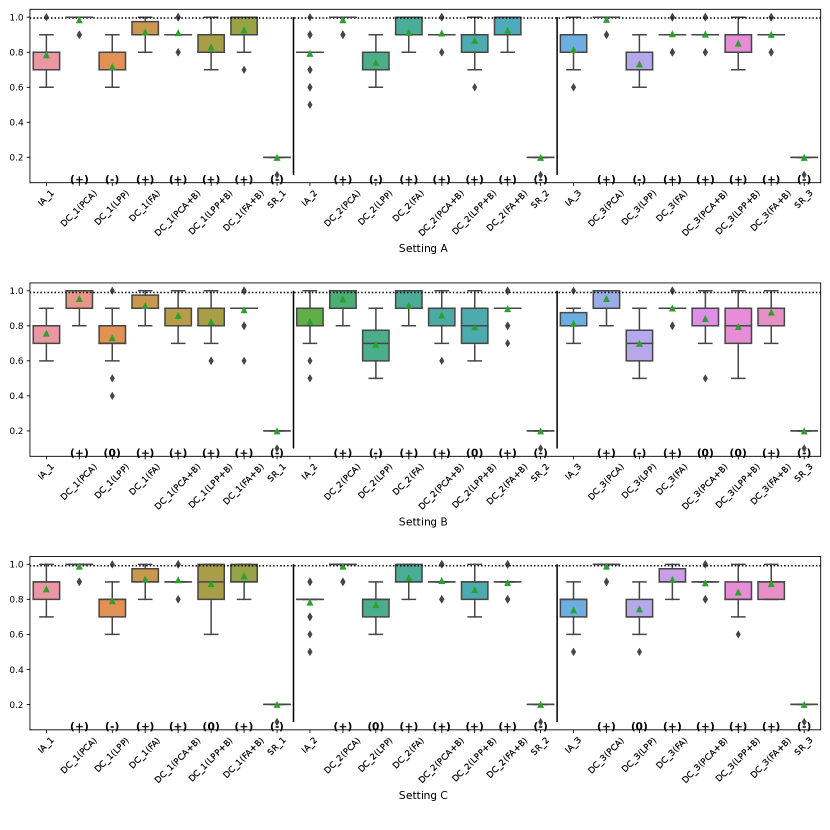

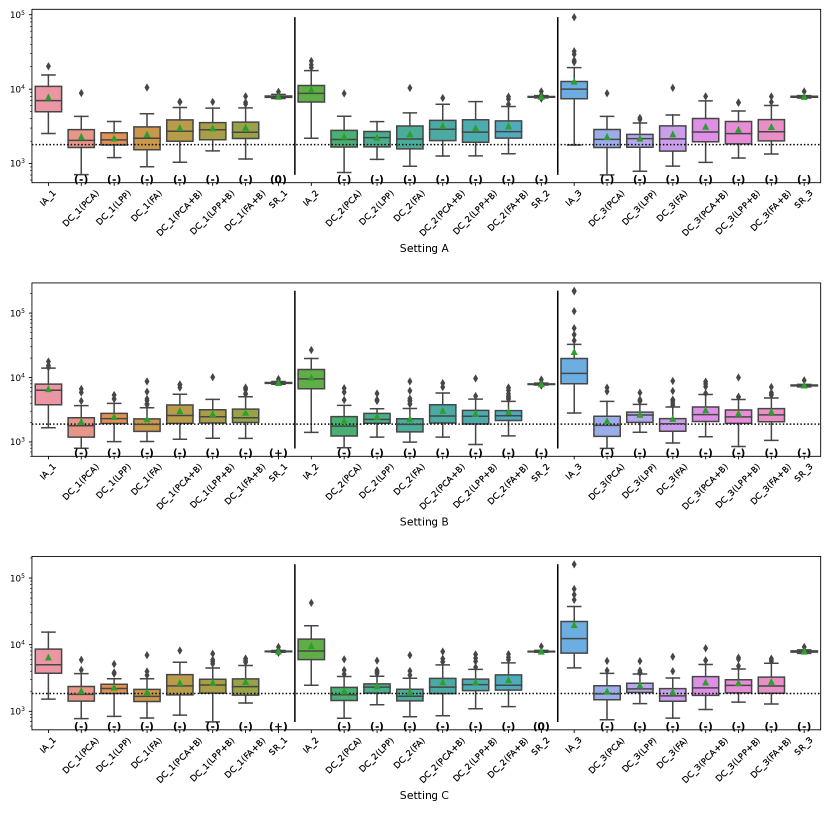

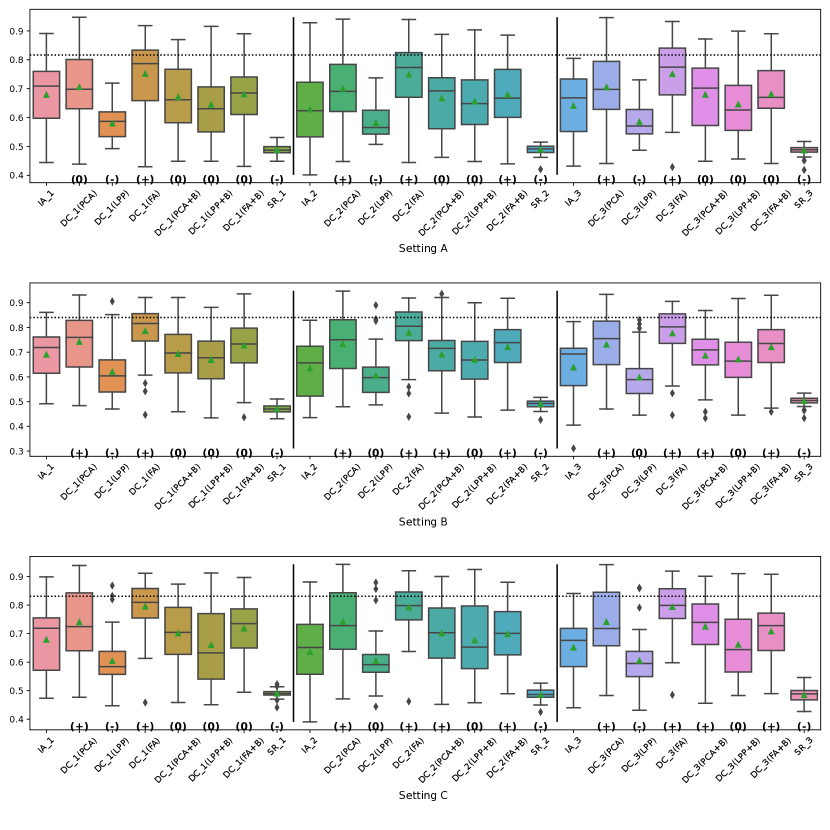

Figures 7-10 represent the results of Experiment III for the financial assets dataset. The symbols , and 0 in parentheses in the figures represent significant positive, significant negative and not significant differences from the IA-DML results, respectively, in -test. The results for parties 1, 2 and 3 are shown on the left, middle and right sides, respectively, in the figures.

In the RMSE of coefficients and the consistency rate of significance of coefficients shown in Figures 9 and 10, DC-DML results for party1 using LPP are worse than for IA-DML in some cases. However, in most other cases DC-DML results are better than IA-DML. In addition, the dimensionality reduction method combined with bootstrapping shows robust results. No SR results are better than IA-DML.

Figures 11-14 represent the results of Experiment III for the jobs dataset. DC-DML results are worse than IA-DML when using LPP for the consistency rate of significance of CATE, and using LPP, LPP+B or FA+B for the consistency rate of significance of coefficients. However, DC-DML results are often better than IA-DML. DC-DML performs better than IA-DML particularly in the RMSEs of CATE and coefficients in most cases. Moreover, as with the financial assets dataset, the dimensionality reduction method combined with bootstrapping shows robust results. SR results are often worse than IA-DML.

In Experiment III with two datasets, DC-DML achieved better results than IA-DML, although not in all cases. Those results suggest that DC-DML can obtain comparable results to CA-DML in various data distribution settings than in IA-DML.

6 Discussion

In this study we proposed DC-DML, a method for estimating CATE models with privacy preserving distributed data. Our method enables flexible estimation of CATE models from distributed data through a semi-parametric approach and does not require iterative communication. To our knowledge, there is no other semi-parametric CATE estimation method for distributed data. Through the experiments, our method outperformed individual analyses in many cases and performed as well as other existing methods.

Our study has some limitations. First, our method assumes the linear CATE model. As mentiond in Section 4.4, the linear CATE model may obtain incorrect conclusions in data where the assumption is not valid. To address this issue, it is necessary to extend our method to a method that can assume a non-linear CATE model, which is a future challenge. Second, the experiments have shown that the method of dimensionality reduction has a significant effect on performance. Which dimensionality reduction method should be used is likely to depend on the data. Thus, a proposal on how to select a dimensionality reduction method is an issue for the future.

7 Conclusion

Utilizing distributed data across multiple institutions is a very important topic in data analysis, but dealing with privacy concerns is a large issue. In this study, we proposed DC-DML as a method that can estimate conditional treatment effects while preserving the privacy of distributed data. We have demonstrated the effectiveness of DC-DML through numerical experiments on synthetic, semi-synthetic and real-world data. In the future, we aim to develop a software implementation of our method.

Acknowledgement

This work was supported in part by the New Energy and Industrial Technology Development Organization (NEDO) (No. JPNP18010), Japan Science and Technology Agency (JST) (No. JPMJPF2017), Japan Society for the Promotion of Science (JSPS), and Grants-in-Aid for Scientific Research (Nos. JP19KK0255, JP21H03451, JP22H00895, JP22K19767).

References

- Athey et al. (2019) S. Athey, J. Tibshirani, and S. Wager. Generalized random forests. The Annals of Statistics, 47(2):1148, 2019.

- Bogdanova et al. (2020) A. Bogdanova, A. Nakai, Y. Okada, A. Imakura, and T. Sakurai. Federated learning system without model sharing through integration of dimensional reduced data representations. In Proceedings of IJCAI 2020 International Workshop on Federated Learning for User Privacy and Data Confidentiality, 2020.

- Brier (1950) G. W. Brier. Verification of forecasts expressed in terms of probability. Monthly weather review, 78(1):1–3, 1950.

- Chernozhukov et al. (2018) V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 01 2018. ISSN 1368-4221. doi: 10.1111/ectj.12097. URL https://doi.org/10.1111/ectj.12097.

- Dehejia and Wahba (1999) R. H. Dehejia and S. Wahba. Causal effects in nonexperimental studies: Reevaluating the evaluation of training programs. Journal of the American statistical Association, 94(448):1053–1062, 1999.

- He and Niyogi (2003) X. He and P. Niyogi. Locality preserving projections. Advances in neural information processing systems, 16, 2003.

- Hill (2011) J. L. Hill. Bayesian nonparametric modeling for causal inference. Journal of Computational and Graphical Statistics, 20(1):217–240, 2011.

- Imakura and Sakurai (2020) A. Imakura and T. Sakurai. Data collaboration analysis framework using centralization of individual intermediate representations for distributed data sets. ASCE-ASME Journal of Risk and Uncertainty in Engineering Systems, Part A: Civil Engineering, 6(2):04020018, 2020.

- Imakura et al. (2021a) A. Imakura, A. Bogdanova, T. Yamazoe, K. Omote, and T. Sakurai. Accuracy and privacy evaluations of collaborative data analysis. In The Second AAAI Workshop on Privacy-Preserving Artificial Intelligence (PPAI-21), 2021a.

- Imakura et al. (2021b) A. Imakura, H. Inaba, Y. Okada, and T. Sakurai. Interpretable collaborative data analysis on distributed data. Expert Systems with Applications, 177:114891, 2021b.

- Imakura et al. (2023) A. Imakura, R. Tsunoda, R. Kagawa, K. Yamagata, and T. Sakurai. Dc-cox: Data collaboration cox proportional hazards model for privacy-preserving survival analysis on multiple parties. Journal of Biomedical Informatics, 137:104264, 2023.

- Imbens and Rubin (2015) G. W. Imbens and D. B. Rubin. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- Karr et al. (2005) A. F. Karr, X. Lin, A. P. Sanil, and J. P. Reiter. Secure regression on distributed databases. Journal of Computational and Graphical Statistics, 14(2):263–279, 2005.

- Kawamata et al. (2024) Y. Kawamata, R. Motai, Y. Okada, A. Imakura, and T. Sakurai. Collaborative causal inference on distributed data. Expert Systems with Applications, 244:123024, 2024.

- Konečnỳ et al. (2016) J. Konečnỳ, H. B. McMahan, F. X. Yu, P. Richtárik, A. T. Suresh, and D. Bacon. Federated learning: Strategies for improving communication efficiency. In NIPS Workshop on Private Multi-Party Machine Learning, 2016. URL https://arxiv.org/abs/1610.05492.

- Künzel et al. (2019) S. R. Künzel, J. S. Sekhon, P. J. Bickel, and B. Yu. Metalearners for estimating heterogeneous treatment effects using machine learning. Proceedings of the national academy of sciences, 116(10):4156–4165, 2019.

- McMahan et al. (2017) B. McMahan, E. Moore, D. Ramage, S. Hampson, and B. A. y Arcas. Communication-efficient learning of deep networks from decentralized data. In Artificial intelligence and statistics, pages 1273–1282. PMLR, 2017.

- Pearson (1901) K. Pearson. Liii. on lines and planes of closest fit to systems of points in space. The London, Edinburgh, and Dublin philosophical magazine and journal of science, 2(11):559–572, 1901.

- Rosenbaum and Rubin (1983) P. R. Rosenbaum and D. B. Rubin. The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1):41–55, 1983.

- Spearman (1904) C. Spearman. “general intelligence,” objectively determined and measured. The American Journal of Psychology, 15(2):201–292, 1904.

- Tan et al. (2022) X. Tan, C. H. Chang, L. Zhou, and L. Tang. A tree-based model averaging approach for personalized treatment effect estimation from heterogeneous data sources. In International Conference on Machine Learning, pages 21013–21036. PMLR, 2022.

- Vo et al. (2022) T. V. Vo, Y. Lee, T. N. Hoang, and T.-Y. Leong. Bayesian federated estimation of causal effects from observational data. In The 38th Conference on Uncertainty in Artificial Intelligence, 2022. URL https://openreview.net/forum?id=BEl3vP8sqlc.

- Xiong et al. (2023) R. Xiong, A. Koenecke, M. Powell, Z. Shen, J. T. Vogelstein, and S. Athey. Federated causal inference in heterogeneous observational data. Statistics in Medicine, 42(24):4418–4439, 2023.

Appendix A The proof of Theorem 1

Proof.

Denote . First, we can prove the moment condition as

Second, for the Neyman–orthogonality, consider

where and . Then,

Here,

The first term is

and the second term is

Thus,

∎

Appendix B The proof of Theorem 2

Proof.

From Theorem 1 in Imakura et al. (2021a), if

then we have

where . Let and be the coefficients compute in CA and that of user computed in DC-DML, respectively. Then,

where is the th row in . We used the assumptions and to transform the equation from line 2 to 3. It is obvious that and are equal in all but the first element. However,

where is the first element in . Then, . ∎

Appendix C Hyperparameters for candidate methods

Most hyperparameters of candidate methods for and are default parameters in scikit-learn (V1.2.2) and LightGBM (V3.3.5). The hyperparameters for estimation are as follows.

- LinearRegression (scikit-learn)

-

fit_intercept: True, positive: False

- RandomForestRegressor (scikit-learn)

-

bootstrap: True, ccp_alpha: 0.0, criterion: squared_error, max_depth: None, max_features: 1.0, max_leaf_nodes: None, max_samples: None, min_impurity_decrease: 0.0, min_samples_leaf: 1, min_samples_split: 2, min_weight_fraction_leaf: 0.0, n_estimators: 100, oob_score: False, warm_start: False

- KNeighborsRegressor (scikit-learn)

-

algorithm: auto, leaf_size: 30, metric: minkowski, metric_params: None, n_neighbors: 5, p: 2, weights: uniform

- LGBMRegressor (LightGBM)

-

boosting_type: gbdt, class_weight: None, colsample_bytree: 1.0, importance_type: split, learning_rate: 0.1, max_depth: -1, min_child_samples: 20, min_child_weight: 0.001, min_split_gain: 0.0, n_estimators: 100, num_leaves: 31, objective: None, reg_alpha: 0.0, reg_lambda: 0.0, subsample: 1.0, subsample_for_bin: 200000, subsample_freq: 0

- SVR (scikit-learn)

-

C: 1.0, cache_size: 200, coef0: 0.0, degree: 3, epsilon: 0.1, gamma: scale, kernel: rbf, max_iter: -1, shrinking: True, tol: 0.001

The hyperparameters for estimation are as follows.

- LogisticRegression (scikit-learn)

-

C: 1.0, class_weight: None, dual: False, fit_intercept: False, intercept_scaling: 1, l1_ratio: None, max_iter: 100, multi_class: auto, n_jobs: None, penalty: none, solver: lbfgs, tol: 0.0001, warm_start: False

- RandomForestClassifier (scikit-learn)

-

bootstrap: True, ccp_alpha: 0.0, class_weight: None, criterion: gini, max_depth: None, max_features: sqrt, max_leaf_nodes: None, max_samples: None, min_impurity_decrease: 0.0, min_samples_leaf: 1, min_samples_split: 2, min_weight_fraction_leaf: 0.0, n_estimators: 100, oob_score: False, warm_start: False

- KNeighborsClassifier (scikit-learn)

-

algorithm: auto, leaf_size: 30, metric: minkowski, metric_params: None, n_neighbors: 5, p: 2, weights: uniform

- LGBMClassifier (LightGBM)

-

boosting_type: gbdt, class_weight: None, colsample_bytree: 1.0, importance_type: split, learning_rate: 0.1, max_depth: -1, min_child_samples: 20, min_child_weight: 0.001, min_split_gain: 0.0, n_estimators: 100, num_leaves: 31, objective: None, reg_alpha: 0.0, reg_lambda: 0.0, subsample: 1.0, subsample_for_bin: 200000, subsample_freq: 0

- SVC (scikit-learn)

-

C: 1.0, break_ties: False, cache_size: 200, class_weight: None, coef0: 0.0, decision_function_shape: ovr, degree: 3, gamma: scale, kernel: rbf, max_iter: -1, probability: True, shrinking: True, tol: 0.001

Appendix D The results of the preliminary experiments

In the preliminary experiments, RMSE was calculated for the estimation of and Brier score for the estimation of using a two folds cross-validation with raw data. Table 5 shows the averages of 50 trials.

| Experiment II | |||

|---|---|---|---|

| RMSE | Brier score | ||

| Multiple regression | 2.5613 | Logistic regression | 0.2579 |

| Random forests | 2.5308 | Random forests | 0.1532 |

| K-nearest neighbor | 2.8690 | K-nearest neighbor | 0.1665 |

| LGBM | 2.5734 | LGBM | 0.1733 |

| SVM | 2.2333 | SVM | 0.1488 |

| Experiment III for the financial assets dataset | |||

| RMSE | Brier score | ||

| Multiple regression | 55827.4190 | Logistic regression | 0.2014 |

| Random forests | 58048.7840 | Random forests | 0.2151 |

| K-nearest neighbor | 57861.6099 | K-nearest neighbor | 0.2339 |

| LGBM | 56665.7031 | LGBM | 0.2047 |

| SVM | 65450.8516 | SVM | 0.2080 |

| Experiment III for the jobs dataset | |||

| RMSE | Brier score | ||

| Multiple regression | 10963.5250 | Logistic regression | 0.1699 |

| Random forests | 12058.0681 | Random forests | 0.1628 |

| K-nearest neighbor | 11981.2699 | K-nearest neighbor | 0.1751 |

| LGBM | 11503.7386 | LGBM | 0.1719 |

| SVM | 15613.6765 | SVM | 0.1912 |

Appendix E Settings for the existing methods

To conduct the exsting method, we used EconML (V0.14.1) and FedCI (https://github.com/vothanhvinh/FedCI). All hyperparameters of GRF (CausalForest) and FedCI are default values as follows.

- CausalForest (EconML)

-

criterion: mse, fit_intercept: True, honest: True, inference: True, max_depth: None, max_features: auto, max_samples: 0.45, min_balancedness_tol: 0.45, min_impurity_decrease: 0.0, min_samples_leaf: 5, min_samples_split: 10, min_var_fraction_leaf: None, min_var_leaf_on_val: False, min_weight_fraction_leaf: 0.0, n_estimators: 100, subforest_size: 4, warm_start: False

- FedCI

-

n_iterations:2000, learning_rate:1e-3

For X-Learner, candidate methods for estimation of the outcome and propensity score have the hyperparameters described in Appendix C. For SR, we considered the regression model to consist of a constant term and a cross term between the covariates and the treatment as