Continuous Treatment Effects with Surrogate Outcomes

Abstract

In many real-world causal inference applications, the primary outcomes (labels) are often partially missing, especially if they are expensive or difficult to collect. If the missingness depends on covariates (i.e., missingness is not completely at random), analyses based on fully-observed samples alone may be biased. Incorporating surrogates, which are fully observed post-treatment variables related to the primary outcome, can improve estimation in this case. In this paper, we study the role of surrogates in estimating continuous treatment effects and propose a doubly robust method to efficiently incorporate surrogates in the analysis, which uses both labeled and unlabeled data and does not suffer from the above selection bias problem. Importantly, we establish asymptotic normality of the proposed estimator and show possible improvements on the variance compared with methods that solely use labeled data. Extensive simulations show our methods enjoy appealing empirical performance.

Keywords: Continuous treatment effects, surrogate outcomes, double robustness.

1 Introduction

In many causal inference applications, the primary outcomes are missing for a non-trivial number of observations. For instance, in studies on long-term health effects of medical interventions, some measurements require expensive testing and a loss to follow-up is common (Hogan et al.,, 2004). In evaluating commercial online ad effectiveness, some individuals may drop out from the panel because they use multiple devices (Shankar et al.,, 2023), leading to missing revenue measures. In many of these studies, however, there often exist short-term outcomes that are easier and faster to measure, e.g., short-term health measures or an online ad’s click-through rate, that are observed for a greater share of the sample. These outcomes, which are typically informative about the primary outcomes themselves, are refered to as surrogate outcomes or surrogates.

There is a rich causal inference literature addressing missing outcome data. Simply restricting to data with observed primary outcomes may induce strong bias (Hernán and Robins,, 2010). Ignoring unlabeled data also reduces the effective sample size for estimating the treatment effects and inflates the variance. Chakrabortty et al., (2022) considered the missing completely at random (MCAR) setting and showed that incorporating unlabeled data reduces variance. Zhang et al., (2023) generalized the results to missing-at-random (MAR) settings where the unlabeled data has a much larger size than the labeled data. Kallus and Mao, (2020) further examined the role of surrogates in datasets with limited primary outcomes and showed efficiency gains after including surrogates and unlabeled data in the analysis. See also Zhang and Bradic, (2022); Hou et al., (2021); Zeng et al., (2023) for relevant discussions. Previous work, however, has largely focused on binary/discrete treatments. To the best of our knowledge, there are no existing analyses of surrogates with continuous treatments or dose response.

Continuous treatments appear in many applications; e.g., waiting time before follow-up, percent of discount, and drug dosage. Existing estimation procedures include outcome modeling (Newey,, 1994) and treatment process modeling (Galvao and Wang,, 2015). Kennedy et al., (2017) proposed doubly robust methods that model both the outcome and the treatment process, and enjoy appealing robustness properties. Bonvini and Kennedy, (2022) further examined high-order estimators to achieve faster rates.

In this paper we consider estimation of dose response functions with limited primary outcome data. We propose novel doubly robust methods using both labeled and unlabeled data, with the help of surrogates. Our approach avoids the potential selection bias caused by restricting only to labeled data, and provably reduces the variance. Importantly, we study the theoretical properties of the estimator proposed, and establish its asymptotic normality to facilitate statistical inference. Our work serves as a counterpart for Kallus and Mao, (2020) in continuous treatment effects settings and enriches the existing dose response estimation literature (Kennedy et al.,, 2017; Bonvini and Kennedy,, 2022).

The rest of this paper is organized as follows: In Section 2 we introduce the problem setup and notation. Section 3 provides assumptions to identify the continuous treatment effect. Novel methodology and theoretical guarantees are discussed in Section 4. Our simulation study in Section 5 demonstrates the performance of our method. Finally we conclude with a discussion in Section 6. All proofs, additional simulation results and a real data example are included in supplementary materials.

2 Setup and Notation

In this section we introduce the problem of estimating continuous treatment effects with surrogates. We formalize the problem using potential outcomes framework (Splawa-Neyman et al.,, 1990; Rubin,, 1974) and introduce notation to present our results concisely.

2.1 Data Structure

Suppose we have access to two datasets and from a randomized experiment/observational study. The labeled dataset is , where is the set of covariates, is the vector of surrogates, is the continuous treatment, and is the primary outcome. Here is an indicator with if a sample is from the labeled data and otherwise. The unlabeled dataset consists of samples without primary outcomes . Hence the total sample size is and both and contain information on treatment , surrogates and covariates , but the primary outcome is missing in the unlabeled dataset due to, for example, loss to follow-up. Let be the union of covariates and surrogates. Note that we will present the results for , but can be viewed as a special setting where our methodology still applies.

2.2 Estimand and Nuisance Functions

Now we define the continuous treatment effects of interest. We use the random variable to denote the potential (counterfactual) outcome we would have observed had a subject received treatment , which may be contrary to the observed . The continuous treatment effect (or dose response function) is defined as

| (1) |

Without additional causal assumptions introduced in Section 3, involves counterfactual outcome and cannot be identified by observed data. Note that since contains post-treatment surrogate outcomes and may be affected by the treatment, we also use potential outcomes to denote the surrogate under treatment .

We further introduce some nuisance functions that are not of primary interest, but which our estimation method depends on. Let be the regression function of primary outcome in the labeled population and be the function obtained by further regressing on . Denote the conditional density of given as and the marginal density of as . The ratio of the marginal density and conditional density is denoted as . is known as a stabilized weight in the literature (Robins et al.,, 2000; Ai et al.,, 2021). The propensity score for (i.e. the conditional probability that primary outcome is observed) is denoted as .

Let denote the support of . For a (possibly random) function on variables we use or to denote the sample average on a sample of size . The sample over which averages are taken should be clear from context. We use to denote the expectation of where only randomness of is considered and is conditioned on. Finally we use to denote the uniform norm, to denote the -norm with respect to the conditional distribution and to denote the usual -norm.

3 Identification

In this section we discuss sufficient conditions to identify the dose response function (1), summarized as follows:

Assumption 1.

(Consistency) if .

Assumption 2.

(Exchangeability) .

Assumption 3.

(Missing at random) .

Assumption 4.

(Positivity) almost surely.

Assumption 1 is also known as the stable unit treatment value assumption (SUTVA), and requires an absence of interference between different individuals in the study. Assumption 2 is commonly used to identify treatment effects and holds in a randomized experiment or observational study with all confounders measured. Assumption 3 ensures whether the primary outcome is observed only depends on covariates , surrogates and treatment , so that the distributions of labeled and unlabeled data are comparable after conditioning on . Assumption 4 says every subject has some chance to receive treatment and has primary outcome observed. The readers are refered to Gill and Robins, (2001) for detailed discussions on identifying continous treatment effects and Kallus and Mao, (2020) for the role of surrogates in identifying treatment effects. With all these assumptions, the treatment effects of interest can be identified using the observable distribution as summarized in Theorem 1.

The identification formula (2) suggests the following plug-in style estimator of : first regress on in the labeled dataset and obtain an estimator of as , which is further regressed on to get an estimator . Finally we take an average over all the samples to get an estimator of as

| (3) |

The performance of such a plug-in style estimator highly depends on estimation error of . To see this, assume the nuisance estimator is independent of the samples that we average over, then the conditional bias of given is

which solely depends on the estimation error of . When is hard to estimate (e.g., non-smooth/sparse in high-dimensional problems), the plug-in style estimator may inherit the slow convergence rate of and have sub-optimal performance.

4 Doubly Robust Estimation

In this section we present the main results of this paper. We begin with an alternative characterization of the dose response function (1) in Section 4.1, based on which we propose a doubly robust estimator in Section 4.2. Finally, theoretical guarantees of the proposed method are provided in Section 4.3.

4.1 Doubly Robust Characterization

Since treatment is continuous, the function in (2) is not pathwise differentiable (Bickel et al.,, 1993; Díaz and van der Laan,, 2013) and we need a novel way to apply semiparametric efficiency theory. The idea is to find a pseudo-outcome depending on nuisance functions such that , i.e., regressing on yields the target dose response function ideally with second-order dependence on nuisance estimation error. Following Rubin and van der Laan, (2005); Kennedy et al., (2017), we consider the functional , which is pathwise differentiable and admits an efficient influence function. Then the pseudo-outcome is a component in the influence function of . We omit the derivation of the influence function and only present the form of pseudo-outcome. Let be nuisance functions that may not necessarily equal the true , and define

where . The following theorem shows an alternative characterization of the dose response function through .

Proposition 1.

Let be nuisance functions that may not necessarily equal the true . Then

if either or .

Proposition 1 gives the first interpretation of double robustness of our methods. There are two chances to obtain the dose response function by regressing the pseudo-outcome on : we correctly specify either the outcome regression model or both the propensity score of and conditional density of given (although see Proposition 2 for a slightly different parameterization).

4.2 Estimation Procedure

The doubly robust characterization in Proposition 1 motivates a two-stage procedure to estimate : In the first step we model the nuisance functions that appear in the pseudo-outcome with flexible nonparametric or machine learning methods. We then construct estimated pseudo-outcomes and regress these on to obtain an estimator of . We will use the stability framework developed in Kennedy, (2020) to analyze such an estimator, which regresses imputed outcomes on treatment. The formal procedure is summarized in Algorithm 1.

Let denote three independent samples of i.i.d observations of and denote the training set to train the nuisance functions.

-

1.

Nuisance functions training: Construct estimates of using . Then use to get an initial estimator of as

-

2.

Pseudo-outcome regression: Construct estimated pseudo-outcome

for each sample in and regress the pseudo-outcomes on the treatment in using a linear smoother to obtain

where are the treatments in and is the coefficient of -th sample.

-

3.

(Optional) Cross-fitting: Swap the role of and repeat steps 1 and 2. Use the average of different estimates as the final estimator of .

Sample splitting is used in Algorithm 1 to avoid complicated empirical process assumptions that are difficult to justify in practice and simplify our theoretical analysis (Robins et al.,, 2008; Chernozhukov et al.,, 2018; Kennedy et al.,, 2020; Levis et al.,, 2023; Bonvini et al.,, 2023). In Step 1, one can use any appropriate regression/classification algorithms to estimate . However, there are fewer results on estimating stabilized weight . Ai et al., (2021) proposed a method that directly estimates with entropy maximization. Alternatively, one can estimate the conditional density (see, e.g., Colangelo and Lee,, 2020, for discussions on related methods), and then the marginal density can be estimated by

and use their ratio to estimate .

Our analysis in Section 4.3 applies to a wide class of nuisance estimators if the product of convergence rates is fast enough. In step 2 we focus on linear smoother-based estimators since they are relatively straightforward to analyze. We believe similar results hold for a wider class of regression estimators under the stability framework in Kennedy, (2020) and leave theoretical analysis of applying general regression algorithms for future investigation. In applications, researchers can choose suitable parametric methods based on their domain knowledge or flexible nonparametric machine learning methods to avoid model misspecification (or ensembles thereof).

4.3 Theoretical Results

We first present estimation error guarantees of Algorithm 1, for general linear smoothers. Then we focus on a specific type of linear smoother, namely local linear regression, and study the asymptotic distribution of the estimator in Section 4.3.2.

4.3.1 Oracle Estimation Theory

In Algorithm 1 we obtain the estimator by regressing the imputed pseudo-outcome on . It is natural to compare with the “oracle” estimator defined as

which regresses the ground-truth pseudo-outcome on using the same linear smoother. Intuitively it is hard for to have a faster convergence rate than . In the following theorem we summarize the conditions under which enjoys the same rate as and hence is “oracle efficient”.

Theorem 2.

Let denote the doubly robust estimator obtained from Algorithm 1 and denote the oracle estimator with oracle risk at point . Suppose

-

•

for some constants .

-

•

The estimator for nuisance functions in Step 2 is uniformly consistent in the sense that .

Then we have

where is the conditional bias of and . Further assume

then is oracle efficient in the sense that

The conditions in Theorem 2 are mild: is not a function of and hence its conditional variance given should be positive; We do not impose conditions on the convergence rate of but only require its consistency. The key condition for to be oracle efficient is and hence we need a bound on the conditional bias , as summarized in the following proposition.

Proposition 2.

Under the conditions in Theorem 2, further assume the estimated conditional probability and the estimated stablized weight hold for all for some constant . Then we have

where recall . If we further assume the weights of the linear smoother satisfy and there exists a neighborhood around such that if . Then we have

We note that the condition on linear smoothers will be satisfied by Nadaraya–Watson estimators (Nadaraya,, 1964; Watson,, 1964) and local polynomial estimators (Fan et al.,, 1994; Fan and Gijbels,, 1996) when the kernel function used has compact support, e.g., the uniform and Epanechnikov kernel. In the bound for the first two terms depend on the product of the convergence rates of nuisance functions. The additional dependence on convergence rate of (compared with Proposition 1) appears in the bias since we use an agnostic estimator of in Algorithm 1. This is the second interpretation of double robustness: Introducing an extra term to the plug-in style estimator in can correct for the first-order bias and the remainder is second-order and “doubly small”. In most settings we expect the nuisance error rate (with respect to measure ) has the same order as the more common conventional rate (with respect to measure ), which is if belongs to a Hölder class of order and is -dimensional. Alternatively one can always upper bound with at the cost of log factors (Tsybakov,, 2009). The empirical process term would be provided that is bounded. The bound on in Proposition 2 involves

as a coarse bound and for specific estimators tighter bound can be derived. For instance, as we will see in local linear estimation this empirical process term is and asymptotically negligible. Hence we can focus on the first two second-order terms in the conditional bias. Theorem 2 together with Proposition 2 gives conditions under which the estimator has the same rate as the oracle estimator . For instance, assume (no surrogates) and , suppose the dose-response function is -smooth (i.e. belongs to a Hölder class of order ) and and are -smooth, then the rate condition for to be oracle efficient is

or equivalently

4.3.2 Asymptotic Normality

In the following discussions, we will analyze the estimator based on a particular linear smoother (i.e. the local linear regression estimator). For a scalar bandwidth parapmeter , let be the local linear basis, with being a probability density. The local linear regression solves the following weighted least square problem:

which gives the closed-form solution:

where and is the sample average over . Then the local linear estimator of is , i.e. the first component of . We summarize the asymptotic properties of this local linear estimator in Theorem 3, which is the key contribution of our paper.

Theorem 3.

(Asymptotic normality of Local Linear Estimator) Let be an inner point of the compact support of . Assume

-

1.

The bandwidth satisfies and as .

-

2.

The marginal density of the treatment is continuously differentiable, the conditional variance is continuous and the dose response is twice continuously differentiable.

-

3.

For any , the conditional variance the marginal density of treatment the estimated conditional probability and the estimated stablized weight for some constant .

-

4.

is a continuous symmetric probability density with support .

-

5.

All nuisance functions are estimated consistently in norm and the estimated pseudo-outcome also satisfies

Furthermore, the convergence rates of nuisance estimation satisfy

Then we have

where

Assumptions 1-4 in Theorem 3 are standard in the nonparametric kernel regression literature. Assumption 5 guarantees that the contribution of nuisance estimation error is asymptotically negligible compared with the smoothing error. One can also use a symmetric kernel supported on that is square integrable and has finite second-order moment. Then the rate condition would be . Similar to our discussions in Section 4.3.1, the rate conditions in assumption 5 are imposed on the product of nuisance estimation error, since we use a doubly robust estimator and the conditional bias is “second-order small”. The theoretically optimal bandwidth to estimate a twice continuously differentiable function is and yields root-mean-square error of order . With such a choice of the requirement on the convergence rate becomes , which, for example, can be satisfied when is consistent and is estimated with rate . In applications one can select the bandwidth using leave-one-out cross-validation (Härdle et al.,, 1988) due to its computational ease. Specifically, after we obtain the estimated pseudo-outcome, we treat them as known and select by

| (4) |

where . In the setting of Algorithm 1 we can select the bandwidth on to avoid overfitting on .

Similar to most nonparametric inference methods, Theorem 3 shows the estimator is centered around instead of under optimal smoothing, which is known as the “bias problem” in the literature (Wasserman,, 2006). The bias problem can be partially solved by estimating the bias and correcting for it (Takatsu and Westling,, 2022) or undersmoothing (Fan et al.,, 2022) at the cost of suboptimal rates. In this work we simply choose to target since it can be viewed as a smooth version of (Genovese and Wasserman,, 2008) and just characterize the variance of under optimal smoothing as a measure of uncertainty. To construct confidence intervals for one needs to estimate the variance. Define a localized functional (which can be viewed as population version of local linear estimator ) with efficient influence function

Following Kennedy et al., (2017); Takatsu and Westling, (2022), one can show the variance of can be approximated by for

Finally, we compare the asymptotic variance in Theorem 3 with the asymptotic variance in Kennedy et al., (2017), where the unlabeled dataset and surrogates are unavailable. Consider the MCAR setting where is independent of all other variables so that , and for simplicity assume to show how the surrogates and unlabeled data help to reduce the variance in this special setting. Note that since is independent of all other variables, we have and . The asymptotic variance of in our setting (i.e. in Theorem 3) is reduced to

| (5) | ||||

under the MCAR assumption (note the additional factor is omitted since it appears in both settings). In the setting where the unlabeled data is unavailable, the asymptotic variance is shown to be

| (6) |

in Kennedy et al., (2017). By the property of conditional variance

(6) can be re-written as

| (7) | ||||

Comparing (5) with (7) we see the first term is the same since . However the second term in (7) is improved by a factor of in (5). This shows how the variance of the estimator is smaller after introducing unlabeled data and surrogate outcomes. The amount of improvement depends on the missing rate and , which measures the variation of that cannot be explained by .

5 Simulation Study

In this section we use simulations to evaluate the performance of the proposed methods. We will illustrate the advantage of doubly robust estimation over naive plug-in style estimators. Consider the following data generating process: The covariates have a multi-variate Gaussian distribution

Conditioning on , the continuous treatment has normal distribution with

The surrogates has a normal distribution

The indicator of whether the outcome is observed or not is Bernoulli (so we assume a missing completely at random mechanism and ). Finally the outcome conditioning on has a normal distribution with

By direct calculations we have

The dose response function of interest is

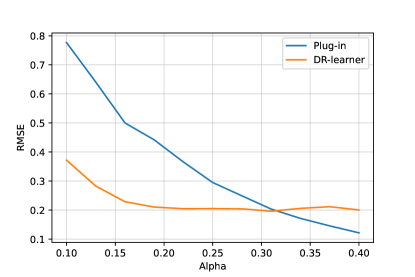

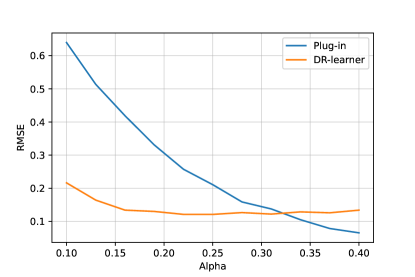

To illustrate the performance of two estimators with different nuisance estimation error we will manually set the estimation error, which is applicable for simulation purposes. For a fixed we let and set , the estimated conditional density of is . Such estimates guarantee the nuisance estimation error is of order . After we generate a sample of size , the plug-in style estimator is defined as . To implement the doubly robust estimator we split the sample into two parts (since the nuisance estimators are given there is no need to split the sample into three parts as in Algorithm 1). We use to construct estimator of the initial estimator , marginal density and select the optimal bandwidth (i.e. construct pseudo-outcomes and run LOOCV as in equation (4) on ). We then construct pesudo-outcomes on and perform local linear estimation using the optimal bandwidth . Finally, the roles of and are exchanged to obtain another estimator and we average the two estimates as the final doubly robust estimator. For sample size and convergence rate , we repeat the data generation and estimation process times. We will aim at estimating and compare the RMSE of plug-in estimator and doubly robust estimator, where is the estimate from -th repetition. The results are summarized in Figure 1.

As we see in Figure 1, if the nuisance estimation error is large ( is small), the doubly robust estimator outperforms the naive plug-in estimator. This can be explained by the second-order bias term of the doubly robust estimator in Proposition 2, i.e., the conditional bias is the product of nuisance estimation errors and is “doubly small”. On the other hand, the plug-in style estimator inherits the slow convergence rate of . As increases, the estimators of nuisance functions are more accurate and plug-in style estimators finally outperform the doubly robust estimator because the doubly robust estimator may suffer from accumulating error in constructing pseudo-outcomes, bandwidth selection and local linear regression, which dominates the conditional bias when nuisance estimation is accurate enough. In real applications, there are typically many covariates and parametric models for nuisance functions may not be accurate. The convergence rate of nonparametric nuisance estimation can be slow when the dimension of covariates is large, and so that the doubly robust estimator with smaller bias is recommended for use. Additional simulation results and a real data example are provided in the supplementary materials.

6 Discussion

In this work, we study the estimation of continuous treatment effects when there is limited access to the primary outcome of interest but auxiliary information on surrogate outcomes is available. We propose a doubly robust estimator that is less sensitive to nuisance estimation error, and hence incorporates flexible nonparametric machine learning methods. Although nonparametric machine learning methods usually suffer from slow convergence rates, they are widely used in nuisance function estimation, especially when practitioners do not have sufficient domain knowledge to justify parametric models. Our doubly robust estimator facilitates the application of nonparametric methods and enjoys optimal estimation rates under mild conditions. Asymptotic normality is further established, which enables researchers to construct confidence intervals and perform statistical inference. We also show how incorporating information on surrogate outcomes improves the variance, compared with methods solely based on labeled data, as in Kennedy et al., (2017). In summary, our methodology provides a robust and efficient approach to leverage surrogate outcomes in continuous treatment effect estimation. However, our method could not deal with the case where only covariate is available in the unlabeled dataset and continuous treatment is also missing (corresponds to the generalizability problem as in Dahabreh et al., (2019)). We leave this setting for future investigation.

References

- Ai et al., (2021) Ai, C., Linton, O., Motegi, K., and Zhang, Z. (2021). A unified framework for efficient estimation of general treatment models. Quantitative Economics, 12(3):779–816.

- Bickel et al., (1993) Bickel, P. J., Klaassen, C. A., Bickel, P. J., Ritov, Y., Klaassen, J., Wellner, J. A., and Ritov, Y. (1993). Efficient and adaptive estimation for semiparametric models, volume 4. Springer.

- Bonvini and Kennedy, (2022) Bonvini, M. and Kennedy, E. H. (2022). Fast convergence rates for dose-response estimation. arXiv preprint arXiv:2207.11825.

- Bonvini et al., (2023) Bonvini, M., Zeng, Z., Yu, M., Kennedy, E. H., and Keele, L. (2023). Flexibly estimating and interpreting heterogeneous treatment effects of laparoscopic surgery for cholecystitis patients. arXiv preprint arXiv:2311.04359.

- Chakrabortty et al., (2022) Chakrabortty, A., Dai, G., and Tchetgen, E. T. (2022). A general framework for treatment effect estimation in semi-supervised and high dimensional settings. arXiv preprint arXiv:2201.00468.

- Chernozhukov et al., (2018) Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68.

- Colangelo and Lee, (2020) Colangelo, K. and Lee, Y.-Y. (2020). Double debiased machine learning nonparametric inference with continuous treatments. arXiv preprint arXiv:2004.03036.

- Dahabreh et al., (2019) Dahabreh, I. J., Robertson, S. E., Tchetgen, E. J., Stuart, E. A., and Hernán, M. A. (2019). Generalizing causal inferences from individuals in randomized trials to all trial-eligible individuals. Biometrics, 75(2):685–694.

- Díaz and van der Laan, (2013) Díaz, I. and van der Laan, M. J. (2013). Targeted data adaptive estimation of the causal dose–response curve. Journal of Causal Inference, 1(2):171–192.

- Fan and Gijbels, (1996) Fan, J. and Gijbels, I. (1996). Local polynomial modelling and its applications: monographs on statistics and applied probability 66, volume 66. CRC Press.

- Fan et al., (1994) Fan, J., Hu, T.-C., and Truong, Y. K. (1994). Robust non-parametric function estimation. Scandinavian journal of statistics, pages 433–446.

- Fan et al., (2022) Fan, Q., Hsu, Y.-C., Lieli, R. P., and Zhang, Y. (2022). Estimation of conditional average treatment effects with high-dimensional data. Journal of Business & Economic Statistics, 40(1):313–327.

- Flores and Flores-Lagunes, (2009) Flores, C. A. and Flores-Lagunes, A. (2009). Identification and estimation of causal mechanisms and net effects of a treatment under unconfoundedness. urn:nbn:de:101:1-20090622213.

- Frölich and Huber, (2017) Frölich, M. and Huber, M. (2017). Direct and indirect treatment effects–causal chains and mediation analysis with instrumental variables. Journal of the Royal Statistical Society Series B: Statistical Methodology, 79(5):1645–1666.

- Galvao and Wang, (2015) Galvao, A. F. and Wang, L. (2015). Uniformly semiparametric efficient estimation of treatment effects with a continuous treatment. Journal of the American Statistical Association, 110(512):1528–1542.

- Genovese and Wasserman, (2008) Genovese, C. and Wasserman, L. (2008). Adaptive confidence bands. The Annals of Statistics, 36(2):875–905.

- Gill and Robins, (2001) Gill, R. D. and Robins, J. M. (2001). Causal inference for complex longitudinal data: the continuous case. Annals of Statistics, pages 1785–1811.

- Härdle et al., (1988) Härdle, W., Hall, P., and Marron, J. S. (1988). How far are automatically chosen regression smoothing parameters from their optimum? Journal of the American Statistical Association, 83(401):86–95.

- Hernán and Robins, (2010) Hernán, M. A. and Robins, J. M. (2010). Causal inference.

- Hogan et al., (2004) Hogan, J. W., Roy, J., and Korkontzelou, C. (2004). Handling drop-out in longitudinal studies. Statistics in medicine, 23(9):1455–1497.

- Hou et al., (2021) Hou, J., Mukherjee, R., and Cai, T. (2021). Efficient and robust semi-supervised estimation of ate with partially annotated treatment and response. arXiv preprint arXiv:2110.12336.

- Huber, (2014) Huber, M. (2014). Identifying causal mechanisms (primarily) based on inverse probability weighting. Journal of Applied Econometrics, 29(6):920–943.

- Huber, (2020) Huber, M. (2020). Replication data for “Direct and indirect effects of continuous treatments based on generalized propensity score weighting”.

- Huber et al., (2020) Huber, M., Hsu, Y.-C., Lee, Y.-Y., and Lettry, L. (2020). Direct and indirect effects of continuous treatments based on generalized propensity score weighting. Journal of Applied Econometrics, 35(7):814–840.

- Kallus and Mao, (2020) Kallus, N. and Mao, X. (2020). On the role of surrogates in the efficient estimation of treatment effects with limited outcome data. arXiv preprint arXiv:2003.12408.

- Kennedy, (2020) Kennedy, E. H. (2020). Towards optimal doubly robust estimation of heterogeneous causal effects. arXiv preprint arXiv:2004.14497.

- Kennedy et al., (2020) Kennedy, E. H., Balakrishnan, S., and G’Sell, M. (2020). Sharp instruments for classifying compliers and generalizing causal effects. The Annals of Statistics, 48(4):2008–2030.

- Kennedy et al., (2017) Kennedy, E. H., Ma, Z., McHugh, M. D., and Small, D. S. (2017). Non-parametric methods for doubly robust estimation of continuous treatment effects. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 79(4):1229–1245.

- Levis et al., (2023) Levis, A. W., Bonvini, M., Zeng, Z., Keele, L., and Kennedy, E. H. (2023). Covariate-assisted bounds on causal effects with instrumental variables. arXiv preprint arXiv:2301.12106.

- Nadaraya, (1964) Nadaraya, E. A. (1964). On estimating regression. Theory of Probability & Its Applications, 9(1):141–142.

- Newey, (1994) Newey, W. K. (1994). Kernel estimation of partial means and a general variance estimator. Econometric Theory, 10(2):1–21.

- Robins et al., (2008) Robins, J., Li, L., Tchetgen, E., van der Vaart, A., et al. (2008). Higher order influence functions and minimax estimation of nonlinear functionals. In Probability and statistics: essays in honor of David A. Freedman, volume 2, pages 335–422. Institute of Mathematical Statistics.

- Robins et al., (2000) Robins, J. M., Hernan, M. A., and Brumback, B. (2000). Marginal structural models and causal inference in epidemiology. Epidemiology, pages 550–560.

- Rubin and van der Laan, (2005) Rubin, D. and van der Laan, M. J. (2005). A general imputation methodology for nonparametric regression with censored data. UC Berkeley Division of Biostatistics Working Paper Series.

- Rubin, (1974) Rubin, D. B. (1974). Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Psychology, 66(5):688–701.

- Schochet et al., (2001) Schochet, P. Z., Burghardt, J., and Glazerman, S. (2001). National job corps study: The impacts of job corps on participants’ employment and related outcomes [and] methodological appendixes on the impact analysis.

- Schochet et al., (2008) Schochet, P. Z., Burghardt, J., and McConnell, S. (2008). Does job corps work? impact findings from the national job corps study. American economic review, 98(5):1864–1886.

- Shankar et al., (2023) Shankar, S., Sinha, R., Mitra, S., Sinha, M., and Fiterau, M. (2023). Direct inference of effect of treatment (diet) for a cookieless world. In International Conference on Artificial Intelligence and Statistics, pages 1869–1887. PMLR.

- Splawa-Neyman et al., (1990) Splawa-Neyman, J., Dabrowska, D. M., and Speed, T. P. (1990). On the application of probability theory to agricultural experiments. essay on principles. section 9. Statistical Science, pages 465–472.

- Takatsu and Westling, (2022) Takatsu, K. and Westling, T. (2022). Debiased inference for a covariate-adjusted regression function. arXiv preprint arXiv:2210.06448.

- Tsybakov, (2009) Tsybakov, A. B. (2009). Introduction to Nonparametric Estimation. Springer, 1st edition.

- Van der Laan et al., (2007) Van der Laan, M. J., Polley, E. C., and Hubbard, A. E. (2007). Super learner. Statistical applications in genetics and molecular biology, 6(1).

- Wasserman, (2006) Wasserman, L. (2006). All of nonparametric statistics. Springer Science & Business Media.

- Watson, (1964) Watson, G. S. (1964). Smooth regression analysis. Sankhyā: The Indian Journal of Statistics, Series A, pages 359–372.

- Zeng et al., (2023) Zeng, Z., Kennedy, E. H., Bodnar, L. M., and Naimi, A. I. (2023). Efficient generalization and transportation. arXiv preprint arXiv:2302.00092.

- Zhang and Bradic, (2022) Zhang, Y. and Bradic, J. (2022). High-dimensional semi-supervised learning: in search of optimal inference of the mean. Biometrika, 109(2):387–403.

- Zhang et al., (2023) Zhang, Y., Chakrabortty, A., and Bradic, J. (2023). Semi-supervised causal inference: Generalizable and double robust inference for average treatment effects under selection bias with decaying overlap. arXiv preprint arXiv:2305.12789.

Appendix A Proofs

A.1 Proof of Theorem 1

Proof.

where the first and fourth equation follow from the property of conditional expectation. The second equation holds since Assumption 2 implies . The third equation follows from Assumption 3. The fifth equation follows from Assumption 2 (specifically ). The last equation follows from Assumption 1. Note that positivity is implicitly assumed to guarantee the conditional expectations are well-defined. ∎

A.2 Proof of Proposition 1

Proof.

If we have

Note that

These two equations imply

and hence

If ,

Note that

By property of conditional expectation, we have

Due to the following equation on the measure:

| (8) |

we can write

Finally we get

∎

A.3 Proof of Theorem 2

Proof.

By Theorem 1 in Kennedy, (2020), the linear smoother is stable if the variance is bounded away from , i.e.

if . ∎

A.4 Proof of Proposition 2

Proof.

For abbreviations we will omit conditioning on in our notation but all the expectations in this part are conditioning on (recall such expectation is denoted using ). Note that

by Proposition 1. By property of conditional expectation

| (9) | ||||

where the first equation follows by conditioning on , the second equation follows from conditioning on and the last equation follows from conditioning on . Further note that and

| (10) |

By equation 8

Add equation 9 and equation 10 together we have

The bound on then follows from Cauchy-Schwarz’s inequality.

For linear smoother , we have

∎

A.5 Proof of Theorem 3

Proof.

We will prove the results with the following decomposition. Let be the oracle estimator. We write

where and .

Step 1: The CLT term. The existing results on local linear estimator (Fan et al.,, 1994; Fan and Gijbels,, 1996) imply

under the conditions stated in the theorem. The conditional variance can be computed as follows:

where the last equation follows since by conditioning on one can show

For the first term in

where the first equation follows from conditioning on and the second equation follows from conditioning on . For the second term in we have

Hence

Step 2: Bounding . Then we proceed to analyze . We first show . Recall . Note that is the kernel density estimator of and standard results in the literature show

which implies . For the element of not on the diagonal

So we have

Since is symmetric around we have and hence

Further notice

Hence we have

which implies . Finally

So we have

One can similarly show

and hence

which implies . Hence we have

This implies . Then we consider . By Lemma 2 in Kennedy et al., (2020) we have for

Note that

This together with implies

We conclude that .

Step 3: Bounding . The last step is to bound . Since we only need to consider

In Proposition 2 we show is equal to

Plug into the equation above we have

Here we slightly abuse the notation and denote as the average over . By boundedness of nuisance estimates and Cauchy-Schwarz’s inequality we have

Similarly we have

For the remaining term , by Lemma 2 in Kennedy et al., (2020) we have

where

This together with implies

| (11) |

By direct calculations (where we assume the outcome is bounded hence is also bounded)

which implies

Combining this equation with (11) yields

Hence under the rate conditions in the theorem we conclude

The asymptotic normality then follows from Slutsky’s theorem. ∎

Appendix B Additional Simulation Results

B.1 Nuisance Functions Estimated by Parametric Methods

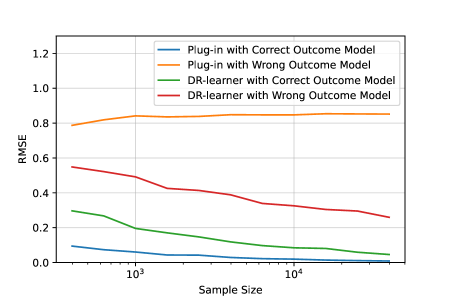

We evaluate the performance of plug-in-style estimator and doubly robust estimator when nuisance functions are estimated using parametric models under the same setting as Section 5. We will fit linear regression models for and separately consider correctly specifying the outcome model or not, where a misspecified model left out the quadratic term in but keeps all other main effects and interactions. The conditional density of given is obtained by first estimating the conditional mean of and plug-in the normal density (i.e., we assume the model for conditional density is always correct). For the plug-in estimator we randomly separate the sample into two parts . The first part is used to fit the regression models for all nuisance functions and we take average on the second part as . The roles of are then exchanged to obtain another estimate and the final estimator is the average of two estimates. The doubly robust estimator is implemented according to Algorithm 1, where the bandwidth is selected on . We generate samples with sample size , apply two estimators to estimate and repeat the process times. The results are summarized in Figure 2.

When the outcome model is misspecified, the plug-in estimator (solely based on outcome modeling) is no longer consistent, as shown in Figure 2. The doubly robust estimator, however, models both outcome and treatment process and has smaller estimation error when the outcome model is misspecified. Estimation with correctly specified outcome model corresponds to in Figure 1, where doubly robust estimator with outcome model and propensity score both correctly specified has larger error compared with the plug-in estimator since slow rate of local linear smoothing dominates the nuisance estimation error .

B.2 Nuisance Functions Estimated by Nonparametric Methods

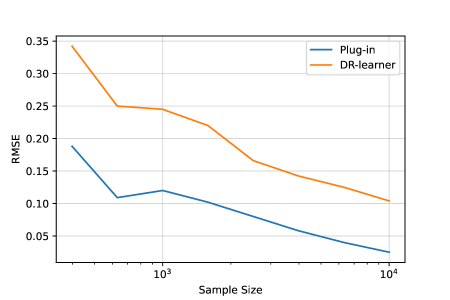

We further evaluate the performance of plug-in-style estimator and doubly robust estimator when nuisance functions are estimated using nonparametric models under the same setting as Section 5. We will fit nuisance functions by superlearner combining generalized linear models and random forests. The conditional density of given is estimated by kernel density estimation. The plug-in estimator is implemented the same way as in Appendix B.1 and the doubly robust estimator is implemented according to Algorithm 1. We generate samples with sample size , apply two estimators to estimate and repeat the process times. The results are summarized in Figure 2.

As shown in Figure 3, the plug-in-style estimator has smaller estimation error when all the nuisance functions are fitted by nonparametric methods. This could be explained by the diffculty in nonparametrically estimating conditional density . Due to curse of dimensionality, large sample size is required for kernel density estimator to estimate well. In our simulations, we find could be small and hence violate the positivity assumption, yielding variation in the construction of pseudo-outcome and larger estimation error of dose response compared with plug-in-style estimator. In applications, prior knowledge on the conditional density, including a reliable parametric model on from domain knowledge or information on the lower bound on due to study design might help us reduce the variation of and estimate the conditional density better, which could improve the performance of doubly robust estimator proposed.

Appendix C Real Data Analysis

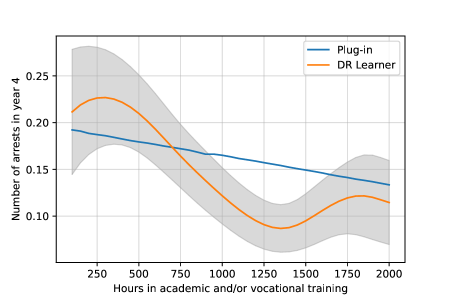

In this section we apply the proposed method to the Job Corps study, conducted in 1990s to evaluate the effects of the publicly funded U.S. Job Corps program. The Job Corps program targets a population between 16 and 24 years old living in the U.S. and coming from low-income households, where participants received an average of 1,200 hours of vocational training over approximately eight months. Schochet et al., (2001) and Schochet et al., (2008) discuss the study design in detail and analyze the effects of Jobs Corps program on various outcomes. They found the Job Corps program effectively increased educational attainment, prevented arrests, and increased employment and earnings. The effects of Job Corps program have been extensively studied under different causal inference frameworks (Flores and Flores-Lagunes,, 2009; Huber,, 2014; Frölich and Huber,, 2017).

However, these previous studies on Job Corps program mainly considered binary treatment definitions. In this work we are interested in estimating the effects of different doses of participation in the program on future involvement in the criminal justice system, namely the number of arrests in the fourth year after the program (outcome ). Specifically, our treatment variable is defined as the total hours spent either in academic or vocational classes of the program. The short-term surrogate outcome is the proportion of weeks employed in the second year after the program. Huber et al., (2020) used generalized propensity score weighting to estimate the continuous treatment effects of time spent in Job Corps program under a mediation analysis framework. We re-analyze their dataset publically available on Harvard dataverse (Huber,, 2020), using the doubly robust estimator proposed as an illustration of our method.

We follow Huber et al., (2020) and focus on samples with a positive treatment (i.e., ). To identify the causal estimand, we invoke the conditional exchangeability in Section 3, where a set of covariates is conditioned on to adjust for confounding bias. The covariate set we adjust for confounding consists of age, gender, ethnicity, education, marital status, previous employment status and income, welfare receipt during childhood and family background (e.g., parents’ education). Missing dummies are created for covariates in containing missing values. The readers are refered to Table 4 in Huber et al., (2020) for descriptive statistics of the pretreatment covariates as well as the treatment, surrogate, and outcome variables in the data. Conditioning on a rich set of covariates is important since it enables us to identify the causal estimand by making the conditional exchangeability assumption plausible. In our analysis, the outcome (number of arrests in year 4) is omitted for 25% of the samples randomly to mimic the setting where the primary outcome is missing and a surrogate outcome is used as auxiliary information. We estimate the treatment effects for each of using both plug-in-style estimator and doubly robust estimator in Algorithm 1, where the nuisance functions are estimated by superlearner (Van der Laan et al.,, 2007) combining generalized linear model and random forests, conditional density is estimated by kernel density estimator. The estimated dose response curve is plotted in Figure 4.

Figure 4 shows that, as participants spend more hours in the program, the expected number of arrests in year 4 has a decreasing trend, which confirms the conclusion that such training programs effectively reduce involvement in the criminal justice system. Importantly, the dose response fitted by the doubly robust estimator is very similar to the results in Huber et al., (2020): the shape of the function is roughly the same to their Figure 2. (Note that the specific values on y-axis are different since they plot a contrast effect and we instead plot the expectation of potential outcome .) As pointed out in Huber et al., (2020), the treatment effect is highly nonlinear, which is further verified by the curve estimated from the doubly robust estimator. By contrast, the curve estimated by simple plug-in-style estimator in (3) fails to capture this non-linearity, possibly because it suffers from large first-order bias.