Multiple equilibria in mean-field game models for large oligopolies with strategic complementarities

Abstract.

We consider continuous-time mean-field stochastic games with strategic complementarities. The interaction between the representative productive firm and the population of rivals comes through the price at which the produced good is sold and the intensity of interaction is measured by a so-called "strenght parameter" . Via lattice-theoretic arguments we first prove existence of equilibria and provide comparative statics results when varying . A careful numerical study based on iterative schemes converging to suitable maximal and minimal equilibria allows then to study in relevant financial examples how the emergence of multiple equilibria is related to the strenght of the strategic interaction.

Keywords: Mean-field games; supermodular cost function; optimal production; strategic complementarity; Tarski’s fixed point theorem; fictitious play.

AMS subject classification: 93E20, 91A15, 60H30, 60H10.

JEL subject classification: C61, C62, C73, D24, L11.

1. Introduction

We investigate the presence of multiple equilibria and multiple equilibrium prices as well as their comparative statics in dynamics oligopolies with strategic complementarities. Following [30], we use mean-field game (MFG) models to approximate systems with a large number of firms competing in a market by producing and selling certain goods. Firms can choose investment plans in order to dynamically expand their own production capacity. By doing so, they affect the price of their own good, as well as the price of the goods produced by the other firms. In particular, we focus on the case in which goods are complementary; i.e., goods whose use is related to the use of associated or paired goods, so that the consumption of one good will increase the consumption of others. We model this interdependence among goods with a specific parameter, which also measures the size of such interaction and will be therefore referred to as strength parameter.

Due to the presence of strategic complementarities, the considered model falls into the class of supermodular MFGs. Such class of MFGs has received increased attention in the past few years and several papers study the existence, structure and approximation of equilibria in quite general frameworks (see e.g. [13, 14]). More in general, in the field of game theory, Topkis [28] initially introduced the submodularity property for static -player games. Such a property holds significance in economic and financial applications, as highlighted in [29] and its references. From the mathematical point of view, the main consequence of the supermodularity is that it leads to increasing best response maps, which in turn allows to analyse equilibria using lattice theoretical fixed point theorems.

Despite the generality of [13, 14], several natural questions which are relevant for the model under consideration are left open. Indeed, the presence of strategic complementarities may give rise to multiple equilibria. Thus one would be interested in knowing the structure of the set of equilibria, comparative statics for the set of equilibria and computational methods for (some of the) equilibria.

The main contribution of this paper is twofold. On the one hand, we present some comparative statics result for equilibria and equilibrium prices in terms of the strength parameter. In particular, we show that the minimal and maximal equilibria increase when the strength parameter increases. Moreover, for sufficiently high values of the strength parameter, also the minimal and maximal equilibrium prices manifest the same monotonicity. On the other hand, we investigate numerically the presence of multiple equilibria varying the strength parameter. In particular, while for low and high values of the strength parameter, only one equilibrium can be found, for intermediate values multiple equilibria arise. This is in line with the following interpretation. If the interaction is small, the individual optimization prevails over the interaction, thus companies tends to follow closely their own individual optimal investments plans. For intermediate levels of the strength parameter, the individual optimization and the interaction balance each other, and firms can coordinate at different equilibria. For high values of the interaction, the equilibrium is forced to be unique, which can be intuitively be explained by the fact that the fixed point of a monotone map with sufficiently high slope is necessary unique (see [26]). This experiments are interesting also from the theoretical point of view, as they illustrate the convergence of the numerical schemes related to the Banach iteration without necessarily relying on a contraction theorem.

1.1. Related literature on MFGs

Mean-field games (MFGs, in short) have been proposed independently by [21] and [24] and arise as limit models for non-cooperative symmetric -player games with interaction of mean field type as the number of players N tends to infinity. We refer to [30] for a detailed discussion on mean-field games in dynamic oligopolies. While existence of equilibria has been shown in very general frameworks (see [9]), the general structure of equilibria and their multiplicity is a relevant issue in MFG theory (as well as in game theory). Indeed, uniqueness of the equilibrium is known only for short time-horizon and under the well known (but restrictive) Lasry-Lions monotonicity condition (see [9]) and several works discuss multiple equilibria in MFGs (see, e.g., [4, 6, 11, 12] among others).

The challenge of devising algorithms capable of approximating mean-field game solutions was initially tackled in [8]. In this work, the authors explored the convergence of fictitious play in potential MFGs without common noise using Partial Differential Equation (PDE) methods. Subsequent investigations delved into variations of this algorithm, examining MFGs with stopping and absorbing boundary conditions in [16], and employing machine learning techniques in [18, 27, 32]. An alternative learning approach for approximating MFG equilibria is outlined in [14, 15], specifically for submodular MFGs. This method involves iterating the best reply map and exhibits promise, particularly when combined with reinforcement learning techniques, as demonstrated in the recent works [19, 25].

Within the realm of MFGs, the property of supermodularity (or submodularity for minimization problems) has been previously applied. For instance, in [2] it was exploited for a class of stationary discrete time games. In [31], the property was harnessed for a class of finite-state MFGs with exit, while in [10] it found application in optimal timing MFGs. Moreover, [14] applied the submodularity property to MFGs involving one-dimensional Itô-diffusions. The recent [15] highlights the versatility of the submodularity property in handling qualitatively distinct formulations of MFGs, encompassing scenarios with singular controls, optimal stopping, reflecting boundary conditions, and finite-state problems.

1.2. Organization of the paper

The rest of the paper is organized as follows. Section 2 presents the general mean-field game model and discusses some examples, the properties of equilibria, and some approximation results. In Section 3 we illustrate some numerical experiments for particular instances of the model and we draw economical interpretations of our findings. Concluding remarks are outlined in Section 4, while all the proofs are presented in Appendix A.

2. A general mean-field game model and its properties

In this section we introduce and analyse a model describing large economies of producers of complementary goods. Following [30], we use mean-field game (MFG) models to approximate systems of with large number of firms competing in a market.

2.1. Model formulation

Consider a filtered probability space satisfying the usual conditions of completeness and right-continuity. Assume to be given a standard -Brownian motion and an -measurable square integrable random variable with distribution .

The representative producer of a good chooses an investment plan in order to expand its production. Given , investment plans are elements of the set

Given the investment plan , the resulting production of a firm is described by a stochastic process whose evolution is determined by the stochastic differential equation (SDE, in short):

| (2.1) |

The coefficients and are continuous and satisfy (with no further reference) the following condition.

Assumption 2.1.

and are such that, for any , there exists a unique strong solution to (2.1).

The revenues of the representative firm depend on the production level of the entire population, which is described by a function , where denotes the space of probability measures on . Given such distribution, when choosing an investment plan , the revenue of the representative firm at time is given by

where

| (2.2) |

Here, is a price function to be specified later containing dependence on an exogenous parameter in some interval .

On the other hand, the investment into production is costly and the cost of investing at time is given by , for a convex function .

Thus, assuming that revenues and costs are discounted at a constant rate , for any given and setting as in (2.2), the representative producer maximizes the net profit functional

In our subsequent examples, the parameter measures the size of the interaction among goods, and will be therefore referred to as the strength parameter. See the next subsection and Remark 2.10 for further details.

We introduce the key structural assumption on the model, that will be standing throughout the paper.

Assumption 2.2.

-

(i)

is affine;

-

(ii)

Either is affine or is concave and is nondecreasing in ;

-

(iii)

;

-

(iv)

-

(v)

While conditions (i), (ii) and (iv) above ensure standard concavity property for the maximization problem, condition (v) implies that a marginal increase of increases the marginal profits of the representative firm. Given defined as in (2.2), an investment is said to be optimal for if

When such an investment exists, one refers to a solution to the SDE as to an optimal production (starting at ), and to the couple as to an optimal pair for .

Definition 2.3.

Given the initial distribution of the population, a mean field game equilibrium (MFGE, in short) is a measurable function such that

for the optimal production .

In the sequel, we will address the existence of equilibria, the comparative statics of the equilibria with respect to the strength parameter , and computational methods allowing to find numerically the equilibria.

2.2. Benchmark examples

We now discuss some natural specifications of the model.

Example 2.4 (Mean reverting dynamics and linear demand function).

The first case we consider is the one in which the log-productivity has a mean reverting dynamics

with a linear inverse demand (as in [3], at the end of Section 1)

for and a parameter describing the intensity of the effect of the mean production on the good of the representative player. We further assume a quadratic cost function

Example 2.5.

We next discuss an example with positive price function. We assume that, under no investment, follows a controlled mean reverting dynamics :

so that the dynamics of the unaffected state in levels is given by

Taking with , the effect of an investment on the state is assumed to be additive, so that evolves as

Further, we consider the case of isoelastic inverse demand, which implies price functions of type

| (2.3) |

for parameters and and we take a quadratic cost function

For this model, one can consider the equilibrium condition as in Definition 2.3.

Example 2.6 (Mean reverting log-dynamics and isoelastic inverse demand).

Now want to discuss a similar model as the one in Example 2.5, but with a different notion of equilibrium.

Following [23], we want to rewrite the optimization problem in terms of the state variable , with . First of all, we want a transformation for the controls. If is a process such that then we have, for ,

so that becomes

which is the new admissibility condition. Thus, define the set as

and, for , we can rewrite the optimization problem as

For this problem, we can enforce the equilibrium condition

In terms of the original and , this condition becomes

| (2.4) |

We refer to the Remark 2.9 below for further discussion on this different notion of equilibrium.

Example 2.7.

Similarly to the previous example, we assume , a quadratic cost and an isoelastic inverse demand function giving a price function as in (2.3). However, in this case we assume that follows a controlled geometric Brownian motion process

For this model, one can consider the equilibrium condition as in Definition 2.3.

Example 2.8 (Geometric dynamics and isoelastic inverse demand).

We next consider the model of Example (2.7), but with the equilibrium condition for as in (2.4). We give a reformulation in terms of the state variable . Indeed, for and , we can rewrite the optimization problem as

where the set of controls is defined as

Again, by enforcing the equilibrium condition , we obtain and equilibrium condition for as in (2.4) (see also Remark 2.9 below).

Remark 2.9.

The type of equilibrium used in (2.4) is different from Definition 2.3, and their difference becomes clear in terms of the associated -player game. In particular, in the models with isoelastic inverse demand, consider -firms whose productivity is given by . Denote by the price function for the good produced by fimr . On the one hand, the equilibrium as in Definition 2.3 is the one arising if in the -player game we would take a price function as

On the other hand, the equilibrium as in (2.4) corresponds to the case with price function

We underline that our approach allows to treat both equilibrium types. Moreover, since the two models give qualitatively similar numerical results, we will discuss only the numerics for Examples 2.6 and 2.8 (see Section 4 below).

Remark 2.10.

The previous examples illustrate more explicitly the role of the parameter . First of all, notice that in all of the examples we assume , which is related to the third condition in Assumption (2.2). Secondly, the higher the value of the higher is the relevance of the term in the payoff of the representative player. In this sense, measures the strength of the interaction among players. Thirdly, it is important to underline that negative values of describe the case in which goods are substitute; i.e., goods whose use is related to the use of associated or paired goods, but in which the consumption of one good decreases the consumption of others. In MFG theory, negative values of are related to the Lasry-Lions monotonicity condition (see [9]), which in turn would imply the uniqueness of the equilibrium.

2.3. Existence of MFGE and comparative statics.

We begin by stating an existence result for the individual player’s optimal investment, given an overall mean production level of the firms described by a measurable function .

Lemma 2.11.

For each measurable, there exists a unique optimal response

Since the optimization problem of the individual firm is concave in , the proof of Lemma 2.11 follows standard concavity arguments (see Theorem 5.2 at p. 68 in [33]), and it is therefore omitted.

The crucial point in our analysis is that the game exhibits strategic complementarities; that is, increments of the opponents strategies incentivize increments in the player optimal strategy. This statement is made rigorous in the following lemma.

Lemma 2.12.

Consider two mean productions paths and and define and as the related optimally controlled trajectories. If for any , then for any , -a.s.

Under Assumption 2.2 only, non existence of equilibria is a known issue, as it is discussed in Section 7 in [22]. Intuitively, the reason of this is that the representative player’s optimal answer might be larger and larger when becomes large. Thus, in order to prevent the equilibria to become arbitrarily large, we assume that

| (2.5) | with . |

This conditions allows us to prove the following result.

2.4. Comparative statics at equilibrium

In light of Theorem 2.13, one can find natural sufficient conditions in order to determine the equilibrium providing the maximal reward.

Theorem 2.14.

We next address the comparative statics of the equilibria with respect to the parameter , varying in the set of parameters . In order to do that, we introduce the following assumption.

Assumption 2.15.

We have

| (2.6) |

Theorem 2.16.

Take and let and the related minimal and maximal MFGE, with associated optimal pairs and .

Under Assumption 2.15, if , then:

-

(i)

and ;

-

(ii)

and , -a.s.;

-

(iii)

If, further, is nondecreasing in the variables , then we have monotonicity of optimal rewards at equilibrium; that is,

In the next two subsection, we discuss comparative statics for the examples of Subsection 2.2. Indeed, these examples require some extra arguments, since the assumptions on the monotonicity of in or are not directly satisfied.

2.4.1. Comparative statics for Example 2.4

We begin by observing that, since the production levels are Gaussian, the production can become negative and we cannot expect monotonicity of in or . However, simple observations will allows us to recover some comparative statics.

Notice that, in the specification of the model as in Example 2.4, for , the function satisfy the ordinary differential equation

Assuming , since we have so that for any . Thus, at equilibrium we also have . Hence, for generic and with and , we obtain

which in turn implies

| (2.7) |

From the latter inequality, the same conclusions as in Theorems 2.14 and 2.16 hold.

Further, we can derive comparative statics result for the mean equilibrium prices. In particular, take and let and the related minimal and maximal MFGE, with associated optimal production and . From the equilibrium condition , we can write the related mean equilibrium price as

and similarly for and . Therefore, for , we obtain

giving a comparative statics of the mean equilibrium prices for fixed . Finally, for , with , we obtain

and, if also , we have

which gives us the desired monotonicity.

2.4.2. Comparative statics for Examples 2.6 and 2.8

In both examples, the assumptions of Theorem 2.14 are satisfied, hence the maximal equilibrium is the one associated to the maximal reward.

We now investigate the a comparative statics for the equilibrium prices for Example 2.6. In particular, for generic , and such that , taking the logarithm of the price we obtain

Therefore, for , we have monotone log-price; i.e.,

for the minimal and maximal MFGEs , with associated optimal productions , .

Remark 2.17.

We underline that the comparative statics as in Theorem 2.16 hold even if the (scalar) parameter is replaced by a time dependent function or a stochastic process . In particular, one can consider the case in which a social planner or a exogenous agent can choose the parameter (or some of the parameters of a dynamics for ) in order to optimize some quantities at equilibria. This type of problems appear in contract theory and Stakelberg games involving mean field games (see e.g. the recent [17] or [20] and the references therein) and have received an increasing attention in recent years. For example, a social planner could be interested in keeping the maximal mean price close to a certain target, while incurring in some costs for modifying . Clearly, comparative statics at equilibria can reveal to be extremely useful in this framework.

2.5. Algorithms

We next address the problem of constructing the MFGE. Given an imput , define:

| Algorithm 1 [Banach iteration]: ; | |||

| Algorithm 2 [Fictitious Play]: , and . |

In order to properly initialize the algorithms, we first discuss a priori bounds for the MFGE according to the two cases in Assumption (2.5). On the one hand, if , we can define two trajectories and as the solutions to the SDEs

and via comparison principle we obtain

Thus, we can define

| (2.8) |

in order to obtain

| (2.9) |

Finally, we can state the following convergence result.

Theorem 2.18.

Under Assumptions (2.2) and (2.5), the following statements hold true:

-

(1)

Convergence of Banach iteration:

-

(a)

If , then for any , , and , for any .

-

(b)

If , then for any , , and , for any .

-

(a)

-

(2)

Convergence of Fictitious Play:

-

(a)

If , then for any , , and , for any .

-

(b)

If , then for any , , and , for any .

-

(a)

Remark 2.19.

Notice that, even after showing the convergence of the Banach iteration without necessarily relying on a contraction theorem, its practical implementation could give rise to numerical issues. Indeed, since the whole convergence hinges on the monotonicity of the iteration, a small numerical error when computing the updated distribution could destroy this property, thus preventing the convergence. Analogous issues could arise for the Fictitious Play algorithm. However, we verify in the next Section an accurate performance of the numerical schemes related to the Banach iteration in the Examples of Subsection 2.2.

3. Numerical analysis

In this section we illustrate numerical experiments for some of the examples in Subsection 2.2, choosing (the Dirac’s delta at ) and deterministic. In particular, since the two Examples 2.5 and 2.6 (resp. Examples 2.7 and 2.8) give qualitatively similar numerical results, we will discuss only the numerics for Examples 2.6 and 2.8.

The fixed-point iterations in Theorem 2.18 have a natural numerical counterpart. More in detail, in each iteration from to our implementation of such algorithms goes along the following steps:

-

(1)

Start with the initial guess .

-

(2)

Solve the maximization problem for the given . We implement this step using the dynamic programming approach. In particular, for the given we can write the Hamilton-Jacobi-Bellman (HJB, in short) equation associated to the representative player optimal control problem:

for , with boundary condition for any . Numerically, we solve a discretized HJB equation backward in time on a non-uniform grid over the domain of using a standard finite-difference method. The numerical algorithm follows [1], who discuss how discretization scheme satisfies the monotonicity condition required for convergence [5]. For an interior solution, the first order conditions in the variable allows to find a feedback

Upon a verification theorem (to be shown on a case by case basis), is actually the optimal feedback control.

-

(3)

Compute the distribution of by using the infinitesimal generator . For a one dimensional diffusion as in our case, we have

The evolution of the distribution is given by the associated Kolmogorov Forward equation

where is the adjoint operator of ,

- (4)

-

(5)

Stop if , otherwise go back to (1).

In the next two subsections, we illustrate the numerical results of this scheme in two benchmark examples (see Examples 2.6 and 2.8).

3.1. Mean reverting log-dynamics and isoelastic inverse demand

We now go back to Example 2.6. Recall that the optimization problem writes as

| Maximize | |||

| subject to |

where and are parameters, , and the equilibrium condition is as in (2.4). is an investment that firms can make in order to increase their future production capacity. Enterpreneurs can finance the investment with their own funds, but only up to a limit which captures in a reduced form the fact that entrepreneurs have limited resources.

Since the optimization is over the set , we have

| (3.1) |

and the HJB equation writes as

Moreover, the evolution of the distribution is given by the associated Kolmogorov Forward equation

where is the adjoint operator of

We define a grid with points for between chosen sufficiently large, and set parameters to the following values:

| 0.02 | 1.0 | |||

| 1.0 | 3.0 | |||

| 0.5 | 12.0 | |||

| 3.8 | 1.0 | |||

| 1.2 | 0.1 | |||

In our baseline calibration, we initialize the measure as the Dirac’s delta of the initial condition :

In other words, we assume that all firms start with the same level of capacity .

Given these parameters, we are interested in studying whether different choices for leads to different equilibria. We solve the MFG with the numerical scheme associated to the Banach iteration. We initialize constantly equal to a value of the points in the grid and then we verify the convergence of the resulting sequence to the equilibria, depending on the initial .

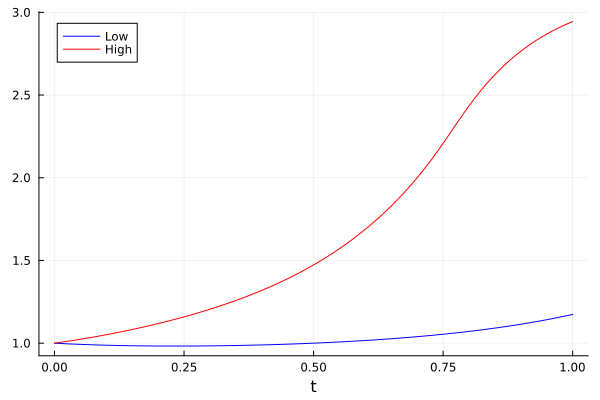

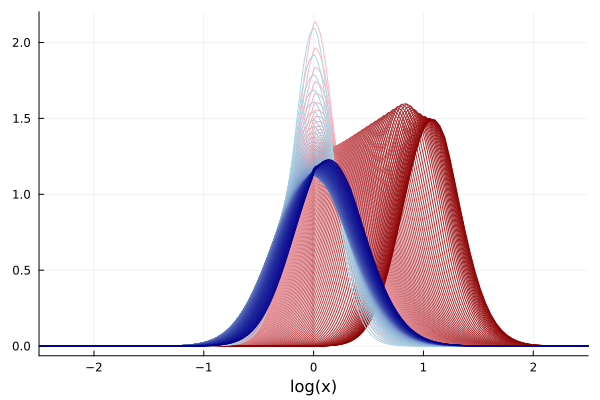

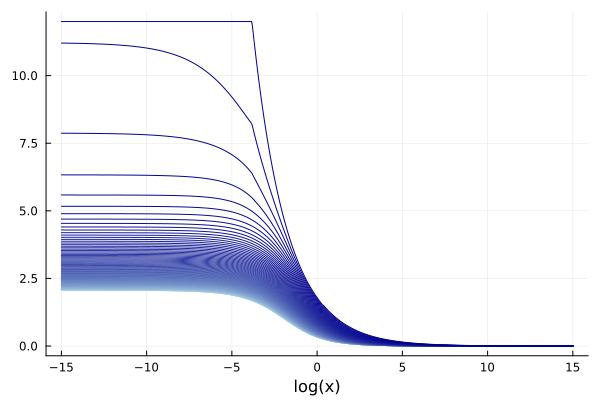

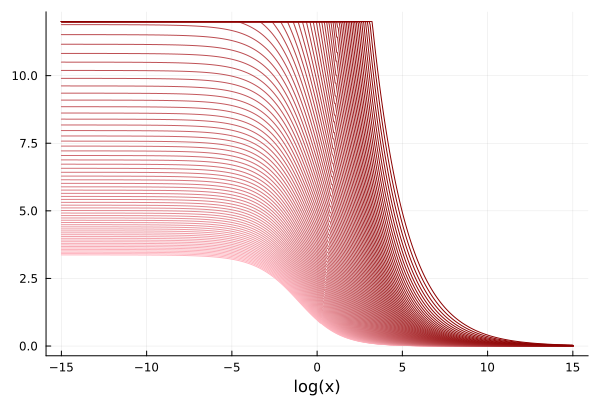

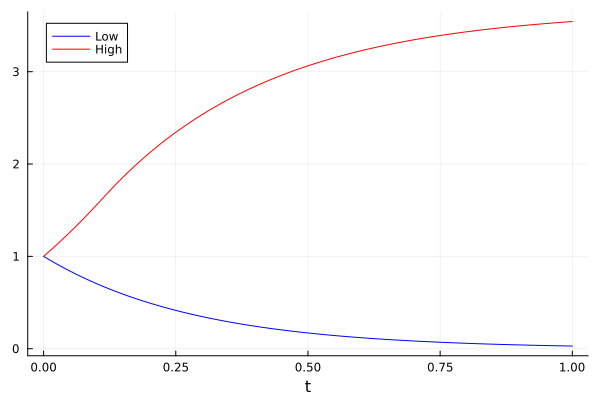

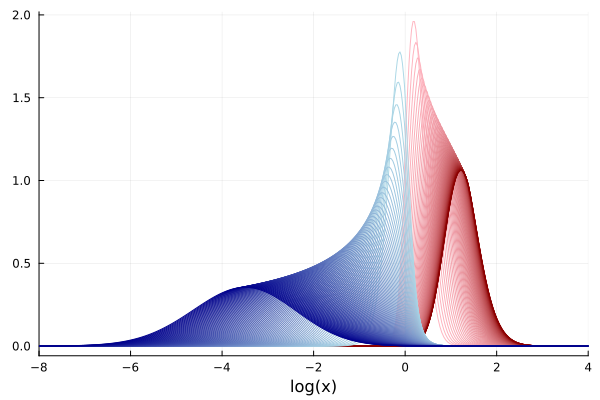

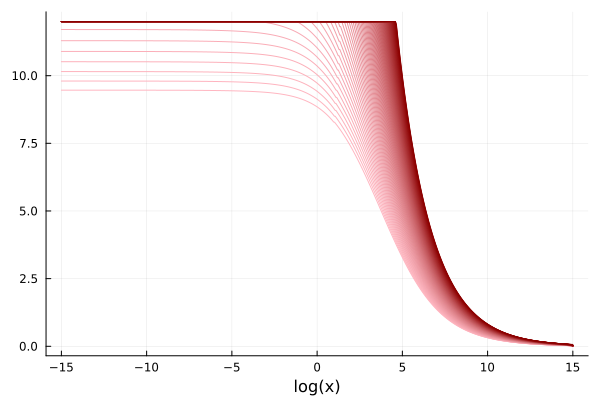

Our numerical analysis shows that there are two equilibria, corresponding to high () and low () values of , as shown in figure 1. Which equilibrium emerges depends on the initialization of . If is set high enough, it acts as a "coordination device", pushing firms to increase their investment as shown in figure 3. As a result of the higher investment, in the high equilibrium firms production capacity increases over time and the distribution shifts to the right (see the red lines in Figure 2). In the low equilibrium instead, investments levels are lower, and so is the resulting capacity distribution.

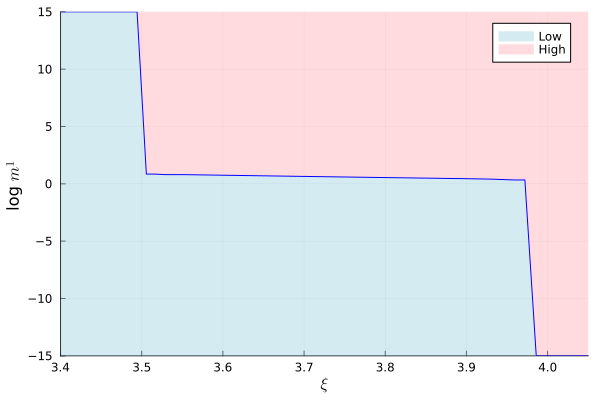

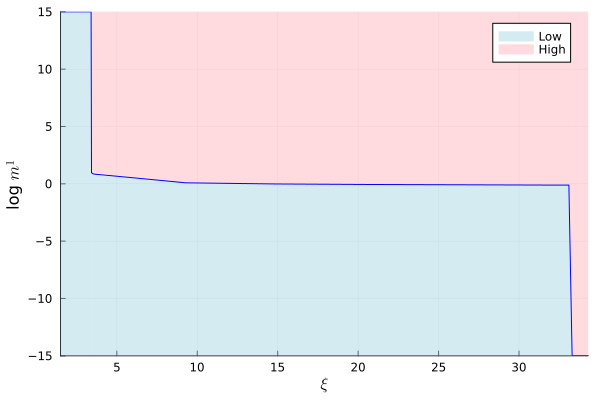

We perform a comparative static exercise to study how equilibria multiplicity depends on the parameter , which regulates the intensity of the strategic interactions among firms. Figure 4 shows that there is range in which there are two equilibria. On the y-axis we present the values of such that the high or low equilibria are selected. When or instead there is only one equilibrium and the choice of is irrelevant.

3.2. Geometric dynamics and isoelastic inverse demand

We now go back to Example 2.8. Recall that the optimization problem writes as

| Maximize | |||

| subject to |

with , and the equilibrium condition as in (2.4). We leave all parameters unchanged and we again initialize to a degenerate distribution with all mass in .

For as in (3.1), we can write the HJB equation as

Moreover, the evolution of the distribution is given by the associated Kolmogorov Forward equation

where is the adjoint operator of

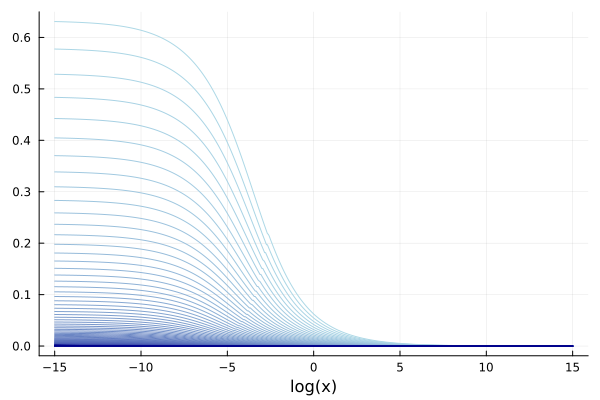

We perform the numerics and illustrate its result using the same parameters as in the previous subsection. Also in this case we find that the model exhibits two equilibria, shown in Figure 5. The absence of the mean reverting component results in a lower minimum equilibrium and in an higher maximal equilibrium . In particular, the minimal equilibrium approximate towards the end of the game. Consistently, we see in Figure 6 that the minimal and maximal distributions move in opposite directions over time. Indeed, while the optimal investments at the lower equilibrium declines to over time, those related to the higher equilibrium rises over time reaching the maximum for low values of the state (see Figures 7).

We perform again a comparative statics in the strength parameter . Similarly to the previous example, we find a range in which there are two equilibria (see Figure 8). However, in comparison to the previous example (cf. Figure 4) we notice that the region with multiple equilibria is significantly wider.

4. Concluding discussion

In this paper, we consider continuous-time mean-field stochastic games with strategic complementarities. The interaction between the representative productive firm and the population of rivals comes through the price at which the produced good is sold and the intensity of interaction is measured by a so-called "strength parameter" . Via lattice-theoretic arguments we first prove existence of equilibria and provide comparative statics results when varying . These give equilibrium-selection criteria depending on the total reward or the price at equilibrium. Moreover, a careful numerical study based on iterative equilibria converging to suitable maximal and minimal equilibria allows then to study in relevant financial examples how the emergence of multiple equilibria is related to the strength of the strategic interaction. This experiments are interesting also from the theoretical point of view, as they illustrate the convergence of the numerical schemes related to the Banach iteration without necessarily relying on a contraction theorem.

Possible extensions of the model could include a common noise, which could be incorporated in a stochastic dynamic strength parameter . The comparative statics results, moreover can be useful when considering the problem of a social planner who can affect the parameter with the intent of optimizing certain quantities related to the minimal or the maximal equilibria and .

Appendix A Proofs

A.1. Auxiliary results

In this appendix we discuss some of the proofs of the results in Section 2. Thanks to Lemma 2.11, for any and there exists a unique optimal investment with related production . We can therefore define the best response map

| (A.1) |

We first show the following auxiliary result, which is a stronger version of Lemma 2.12. For , the symbol denotes the Dirac’s delta at point ; that is, if and if , for any Borel subset of .

Lemma A.1.

Proof.

Take such that and . Let and and set and . Following the the proof of Lemma 3.1 in [13], one can show that the controls defined by

| (A.2) |

are elements of and such that and .

By the admissibility of and the optimality of we can write

Moreover, by (A.2), we easily find

which allows to rewrite the previous inequality as

Next, thanks to conditions (2.2) and (2.15), we obtain

which implies that is a maximizer for . By Lemma 2.11, we conclude that , so that . Thus, we conclude that

from which we obtain

which is the desired monotonicity.

The proof of the first claim simply follows by repeating the argument above for fixed , and by observing that in this case condition (2.15) is not necessary. ∎

A.2. Proof of Theorem 2.13

The aim is to employ Tarski fixed point theorem. Let and be as in (2.8). Define now the set of functions

and define the order relation by

| (A.3) |

Notice that, thanks to (2.9), the map is well defined. Observe that the set of MFGE coincides with the set of fixed points of the map .

The partially ordered set is a complete lattice and the map is nondecreasing (cf. Lemma 2.12). Thus, by Tarski fixed point theorem, the set of fixed points of is a nonempty complete lattice and so is the set of MFGE. In particular, there exists minimal and maximal MFGE.

A.3. Proof of Theorem 2.18

We prove each claim separately.

A.3.1. Proof of Claim 1

We only show the convergence to the minimal equilibrium. The convergence to the maximal equilibrium can be shown with the same arguments.

For , thanks to (2.9) one has

Thus, since is nondecreasing, we have and by a simple induction argument we find

| (A.4) | for any . |

Thus, we can define

and we need to verify that is the minimal MFGE.

We first show that is a MFGE. Define as the optimal pair for . By Lemma A.1 and the monotonicity in (A.4), we have , so that we can define

Using stability properties and comparison principles together with the stochastic maximum principle (for more details, we refer to [13]), one can show that is the optimal production for . Moreover, from the latter limits and the monotone convergesnce theorem, we deduce that

which show that is a MFGE.

We finally show that is the minimal MFGE. If is a MFGE, then we have , and therefore

Thus, by iterating the map , we obtain

Thus, taking limits in we conclude that

which complete the proof.

A.3.2. Proof of Claim 2

Again, we only show the convergence to the minimal equilibrium. The convergence to the maximal equilibrium can be shown with the same arguments.

A.4. Proof of Theorem 2.16

For , and , define by induction the sequences and . Notice that, by monotonicity of in the parameter, we have

and that, if , then

Thus, by induction we obtain that for any , and by Claim 1 in Theorem 2.18 we obtain

as desired.

In the same way, we can show that , thus completing the proof.

Acknowledgements. Funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) - Project-ID 317210226 - SFB 1283.

Disclosure statement. The authors declare that none of them has conflict of interests to mention.

References

- [1] Y. Achdou, J. Han, J.-M. Lasry, P.-L. Lions, and B. Moll, Income and Wealth Distribution in Macroeconomics: A Continuous-Time Approach, The Review of Economic Studies, 89 (2021), pp. 45–86.

- [2] S. Adlakha, R. Johari, and G. Y. Weintraub, Equilibria of dynamic games with many players: Existence, approximation, and market structure, J. Econom. Theory, 156 (2015), pp. 269–316.

- [3] K. Back and D. Paulsen, Open-loop equilibria and perfect competition in option exercise games, The Review of Financial Studies, 22 (2009), pp. 4531–4552.

- [4] M. Bardi and M. Fischer, On non-uniqueness and uniqueness of solutions in finite-horizon mean field games, ESAIM Control Optim. Calc. Var., 25 (2019), p. 44.

- [5] G. Barles and P. E. Souganidis, Convergence of approximation schemes for fully nonlinear second order equations, Asymptotic analysis, 4 (1991), pp. 271–283.

- [6] E. Bayraktar and X. Zhang, On non-uniqueness in mean field games, Proceedings of the American Mathematical Society, 148 (2020), pp. 4091–4106.

- [7] A. Bensoussan, K. C. J. Sung, S. C. P. Yam, and S. P. Yung, Linear-quadratic mean field games, J. Optim. Theory Appl., 169 (2016), pp. 496–529.

- [8] P. Cardaliaguet and S. Hadikhanloo, Learning in mean field games: the fictitious play, ESAIM Control Optim. Calc. Var., 23 (2017), pp. 569–591.

- [9] R. Carmona and F. Delarue, Probabilistic Theory of Mean Field Games with Applications I-II, Springer, 2018.

- [10] R. Carmona, F. Delarue, and D. Lacker, Mean field games with common noise, Ann. Probab., 44 (2016), pp. 3740–3803.

- [11] A. Cecchin, P. D. Pra, M. Fischer, and G. Pelino, On the convergence problem in mean field games: a two state model without uniqueness, SIAM J. Control Optim., 57 (2019), pp. 2443–2466.

- [12] F. Delarue and R. F. Tchuendom, Selection of equilibria in a linear quadratic mean-field game, Stochastic Process. Appl., 130 (2020), pp. 1000–1040.

- [13] J. Dianetti, Strong solutions to submodular mean field games with common noise and related mckean-vlasov fbsdes, arXiv preprint arXiv:2212.12413, (2022).

- [14] J. Dianetti, G. Ferrari, M. Fischer, and M. Nendel, Submodular mean field games: Existence and approximation of solutions, Ann. Appl. Probab., 31 (2021), pp. 2538–2566.

- [15] , A unifying framework for submodular mean field games, Math. Oper. Res., 48 (2023), pp. 1679–1710.

- [16] R. Dumitrescu, M. Leutscher, and P. Tankov, Linear programming fictitious play algorithm for mean field games with optimal stopping and absorption, arXiv preprint arXiv:2202.11428, (2022).

- [17] R. Elie, E. Hubert, T. Mastrolia, and D. Possamaï, Mean–field moral hazard for optimal energy demand response management, Mathematical Finance, 31 (2021), pp. 399–473.

- [18] R. Elie, J. Pérolat, M. Laurière, M. Geist, and O. Pietquin, Approximate fictitious play for mean field games, arXiv preprint arXiv:1907.02633, (2019).

- [19] X. Guo, A. Hu, R. Xu, and J. Zhang, Learning mean-field games, Advances in Neural Information Processing Systems, 32 (2019).

- [20] X. Guo, A. Hu, and J. Zhang, Optimization frameworks and sensitivity analysis of stackelberg mean-field games, arXiv preprint arXiv:2210.04110, (2022).

- [21] M. Huang, R. P. Malhamé, and P. E. Caines, Large population stochastic dynamic games: closed-loop McKean-Vlasov systems and the Nash certainty equivalence principle, Commun. Inf. Syst., 6 (2006), pp. 221–252.

- [22] D. Lacker, Mean field games via controlled martingale problems: Existence of Markovian equilibria, Stochastic Process. Appl., 125 (2015), pp. 2856–2894.

- [23] D. Lacker and T. Zariphopoulou, Mean field and n-agent games for optimal investment under relative performance criteria, Mathematical Finance, 29 (2019), pp. 1003–1038.

- [24] J.-M. Lasry and P.-L. Lions, Mean field games, Jpn. J. Math., 2 (2007), pp. 229–260.

- [25] K. Lee, D. Rengarajan, D. Kalathil, and S. Shakkottai, Reinforcement learning for mean field games with strategic complementarities, in International Conference on Artificial Intelligence and Statistics, PMLR, 2021, pp. 2458–2466.

- [26] C. Mou and J. Zhang, Mean field game master equations with anti-monotonicity conditions, arXiv preprint arXiv:2201.10762, (2022).

- [27] S. Perrin, J. Pérolat, M. Laurière, M. Geist, R. Elie, and O. Pietquin, Fictitious play for mean field games: Continuous time analysis and applications, arXiv preprint arXiv:2007.03458, (2020).

- [28] D. M. Topkis, Equilibrium points in nonzero-sum n-person submodular games, SIAM J. Control Optim., 17 (1979), pp. 773–787.

- [29] X. Vives, Oligopoly Pricing: Old Ideas and New Tools, MIT press, 1999.

- [30] G. Y. Weintraub, C. L. Benkard, and B. Van Roy, Industry dynamics: Foundations for models with an infinite number of firms, J. Econom. Theory, 146 (2011), pp. 1965–1994.

- [31] P. Więcek, Total reward semi-Markov mean-field games with complementarity properties, Dyn. Games Appl., 7 (2017), pp. 507–529.

- [32] Q. Xie, Z. Yang, Z. Wang, and A. Minca, Provable fictitious play for general mean-field games, arXiv preprint arXiv:2010.04211, (2020).

- [33] J. Yong and X. Y. Zhou, Stochastic Controls: Hamiltonian Systems and HJB Equations, vol. 43, Springer Science & Business Media, 1999.