Parallel Affine Transformation Tuning of Markov Chain Monte Carlo

Abstract

The performance of Markov chain Monte Carlo samplers strongly depends on the properties of the target distribution such as its covariance structure, the location of its probability mass and its tail behavior. We explore the use of bijective affine transformations of the sample space to improve the properties of the target distribution and thereby the performance of samplers running in the transformed space. In particular, we propose a flexible and user-friendly scheme for adaptively learning the affine transformation during sampling. Moreover, the combination of our scheme with Gibbsian polar slice sampling is shown to produce samples of high quality at comparatively low computational cost in several settings based on real-world data.

1 Introduction

A variety of methods in probabilistic inference and machine learning relies on the ability to generate (approximate) samples from a high-dimensional probability distribution. But methods generating samples of high quality tend to be slow, so that the sampling can pose a severe computational bottleneck. Here we develop a new approach to address the general black-box sampling problem on for arbitrary dimensions .

Let us start with the concrete formulation of the aforementioned problem. Whenever random variables are introduced in the following, we implicitly require them to be defined on a sufficiently rich common probability space . The target distribution on is given through a potentially unnormalized density , meaning

| (1) |

We may evaluate at any given point, but we generally cannot evaluate and do not even know the normalization constant of (the denominator in (1)). The task is to sample – approximately – from , i.e. to generate realizations of random variables on such that the distribution of is close to in some sense, at least for large enough .

A powerful approach for solving the sampling problem is Markov chain Monte Carlo (MCMC). An MCMC sampler generates a truncated realization of a Markov chain with some initial distribution and a transition kernel111For basic knowledge regarding the definitions and properties of transition kernels see e.g. Rudolf (2012). on that leaves invariant. For commonly used MCMC methods, there are theoretical results ensuring that converges to , meaning

under weak assumptions on and , where TV denotes the total variation distance.

In real-world applications of MCMC methods, information about essential properties of the target distribution, such as the covariance structure or the number, location and relative importance of modes, is often not available. Therefore, MCMC users typically resort to generic off-the-shelf samplers like random walk Metropolis (RWM) (Metropolis et al., 1953), the Metropolis-adjusted Langevin algorithm (MALA) (Roberts & Tweedie, 1996), Hamiltonian Monte Carlo (HMC) (Neal, 1996) or hybrid uniform slice sampling (Neal, 2003). Although these methods are in principle able to address sampling problems with very little a priori information about the target, their performance is often suboptimal, especially in high dimensions, resulting in slow convergence and long-lasting autocorrelations. If some information about the target is available, “informed” MCMC methods that can explicitly incorporate this knowledge into their transition mechanisms often vastly outperform the generic uninformed methods. Instances of informed MCMC samplers include independent Metropolis-Hastings (IMH) (Tierney, 1994), the preconditioned Crank-Nicolson Metropolis-Hastings algorithm (pCN-MH) (Cotter et al., 2013), elliptical slice sampling (Murray et al., 2010) (ESS) and Gibbsian polar slice sampling (GPSS)222As GPSS does not have a user-specified proposal distribution, it is not immediately obvious how it can make use of information about the target. We will clarify this later on. (Schär et al., 2023).

Related to that, adaptive MCMC (Roberts & Rosenthal, 2009) provides a general framework to iteratively acquire knowledge about the target distribution during sampling, and incorporate this information into the transition mechanism. At any iteration the transition mechanism may change depending on the whole “past”, for instance transitioning from to can be performed by a kernel , where may depend on . Numerical experiments indicate that this may improve the sample quality.

In this paper, we consider affine transformation tuning (ATT), a general principle of performing MCMC transitions via a latent space that is connected to the sample space by a bijective affine transformation. In particular, we discuss how to construct adaptive MCMC methods based on ATT, where the adaptivity is used to iteratively learn a “good” affine transformation. When learning the affine transformation, say , the goal is to bring the pushforward of the target distribution under the inverse transformation as close as possible to isotropic position (i.e. mean zero and identity covariance, or a suitable analogue in very heavy-tailed settings). We can then exploit the approximate isotropy of the transformed target distribution to enhance the performance of informed MCMC samplers.

Our framework is very general and can be applied to a large variety of informed MCMC methods, such as IMH, pCN-MH, ESS or GPSS. Nonetheless, we focus on applying ATT to GPSS. This is motivated by the fact that GPSS is able to effectively acquire information about the target distribution at early stages of a run (unlike IMH which early on performs poorly while acquiring information about the target), and known to work well for various types of targets in isotropic position, including both light-tailed and heavy-tailed ones (unlike pCN-MH and ESS that are designed for settings with Gaussian priors). As the application of an affine transformation to the target distribution does not change the tail behavior (e.g. Gaussian tails will stay Gaussian, heavy tails will stay heavy), this makes GPSS uniquely well-suited for ATT. We refer to Appendix G.1 for an explanation of GPSS.

The empirical evidence for the good performance of GPSS in isotropic settings is complemented by theoretical results (Rudolf & Schär, 2024; Schär, 2023) regarding the underlying “ideal” method polar slice sampling (PSS) (Roberts & Rosenthal, 2002), in conjunction with a theoretical result (Schär & Stier, 2023) regarding geodesic slice sampling on the sphere (GSSS) (Habeck et al., 2023). Essentially, Schär & Stier (2023) demonstrated that the use of GSSS within the GPSS transition does not prevent GPSS from achieving the dimension-independent performance of PSS established in the two former works.

The remainder of our paper is structured as follows. Section 2 introduces ATT as a general principle for MCMC transitions. In Section 3, we propose parallel ATT (PATT), a flexible framework for setting up samplers that run multiple parallel ATT chains and let them share information to more quickly learn a suitable transformation. In Section 4, we present a theoretical result that justifies the use of PATT. The results of several numerical experiments with PATT are presented in Section 5. We conclude the paper’s main body with some final remarks in Section 6.

In addition, we offer complementary information on ATT and related topics in the supplementary material: Appendices A, B and C provide detailed considerations and guidelines regarding the choices of the adjustment types, transformation parameters and update schedules defined in Sections 2 and 3. Theses appendices may serve as a “cookbook” for implementing and/or applying ATT or PATT. In place of a related work section, we give a detailed overview of connections between our method and various others in Appendix D. In Appendix E, we prove that in certain cases a simple adaptive MCMC implementation of ATT is equivalent to other, more traditional adaptive MCMC methods, in that the respective transition kernels coincide. The proof of our theoretical result from Section 4 is provided in Appendix F. In Appendix G we elaborate on the models and hyperparameter choices for the experiments behind the results presented in Section 5, and provide some further results. Appendix H presents a series of ablation studies demonstrating that each non-essential component of PATT can, in principle, substantially improve its performance. Appendix I offers more plots illustrating the main experiments as well as the ablation studies.

2 Affine Transformation Tuning

2.1 Formal Description

For the sake of a systematic formalization, let us name two copies of , the sample space and the latent space . Suppose we have an affine transformation

with a shift and an element of the general linear group (over in dimension ),

By the invertibility of , this transformation has the inverse

| (2) |

The transformation and its inverse therefore establish a one-to-one correspondence between points in and .

Suppose now that we are given a target distribution on via an unnormalized density (as in (1)), then the corresponding transformed distribution on is the pushforward measure . This results in the following intuitive relation between and : Let , , then

meaning and have the same distribution.

This simple construction is the basis of what we call an affine transformation tuning (ATT) transition. An ATT transition works by moving to the latent space via the inverse transformation, taking a step in the latent space and then moving back to the sample space. To express this formally, denote by the transition kernel of an MCMC method on the latent space that leaves the transformed target distribution invariant. In the following, the MCMC method taking this role will be referred to as the base sampler (of the resulting ATT sampler). Now an ATT transition for target , based on transformation and auxiliary kernel , from the current state to a new state , is implemented by Algorithm 1.

Input: transformation , inverse transformation , transition kernel on targeting transformed target , current state

Output: new state

The transition kernel corresponding to the transition performed by Algorithm 1 is given by

| (3) | ||||

for any , .

A key observation regarding ATT is that the map has constant Jacobian , hence the distribution has unnormalized density

so that

is also an unnormalized density of . In particular, an evaluation of the target density on the latent space is only as computationally costly as one of the untransformed target density plus one of the transformation .

What are the roles of the parameters and of the transformation ? Clearly, the parameter controls the center of the distribution. Specifically, if is centered around , then the point to which corresponds in the latent space is (for arbitrary ), so that is centered around the origin. The parameter on the other hand affects the covariance structure of the target distribution. Specifically, if has covariance matrix with Cholesky decomposition , then has covariance matrix

Thus, is the identity matrix whenever is orthogonal, the simplest case being .

2.2 Connections to Traditional Adaptive MCMC

A straightforward way to deploy ATT in practice is to implement it as an adaptive MCMC method that uses the adaptivity to learn a suitable transformation during the run, and performs each iteration by calling Algorithm 1 with the latest version of . Intuitively, the resulting method adaptively learns how best to transform the target distribution in order to simplify it in the eyes of its base sampler. This is in contrast to “traditional” adaptive MCMC approaches, where the adaptivity is typically used to adjust the parameters of an underlying sampler’s proposal distribution, thereby adjusting this sampler to better suit the target distribution.

Nevertheless, there are cases in which the transition kernels of an adaptive ATT chain coincide with those of a corresponding traditional adaptive MCMC chain, where the latter uses a parametrized version of the former’s base sampler as its underlying sampler. In Appendix E, we introduce ATT-friendliness as a property that precisely encapsulates which methods produce such an equivalence when used as the underlying/base sampler. We then consider several samplers in detail, namely RWM, IMH (with Gaussian proposal) and ESS, and verify for each of them that it is ATT-friendly.

2.3 Adjustment Types

Motivated by considerations regarding the computational overhead introduced by ATT, we examine ways to restrict our previous specification of as an a priori arbitrary bijective affine transformation. We frame these restrictions by the type of adjustments to the target distribution that they permit. To this end, we introduce the following terms.

Centering is performed by transformations that shift the origin, which – in absence of other adjustments – are of the form for some . Variance adjustments are made by transformations that alter the target’s coordinate variances without affecting the correlations between variables, which – in absence of centering – are transformations of the form for some with . Covariance adjustments are the unrestricted analogue to variance adjustments, meaning that – again in absence of centering – they encompass all transformations with . Of course both variance and covariance adjustments can also be combined with centering, leading to transformations of the form , with and either or . Note that the latter combination recovers the original generality, in that it allows to be an arbitrary bijective affine transformation.

For some considerations on how to decide on adjustment types for a given problem, we refer to Appendix A. The question of how to choose the transformation’s parameters for a given adjustment type will also be considered later.

3 Parallelization and Update Schedules

3.1 Parallelized ATT

Since ATT uses samples to approximate global features of the target distribution, we can use non-trivial parallelization to improve its performance by running parallel chains , that all rely on the same transformation . Whenever the parameters and are to be updated, say in iteration , their new values can be computed based on all samples generated up to this point. For , this should lead to a substantially faster (in terms of iterations per chain) convergence of the transformation parameters to their asymptotic values than with independent chains.

However, if not used with caution, this parallelization approach can substantially reduce the method’s iteration speed333By iteration speed we mean the number of iterations a method completes per time unit, e.g. per second of CPU time.: For example, an iteration of our default base sampler GPSS involves a stepping-out procedure and two shrinkage procedures (see Appendix G.1 or Schär et al. (2023) for details), each involving a random number of target density evaluations. Moreover, this number depends not only on the target distribution and the choice of GPSS’s hyperparameter, but also (and often predominantly) on the random threshold drawn in each iteration to determine a slice. The computing time required for an iteration of GPSS is therefore also random and may vary substantially. Running the parallelized ATT approach with parameter updates in every iteration would require a synchronization of the chains for each update, meaning that all chains have to first terminate the current iteration before the parameters can be updated. Because each chain requires a random and largely varying amount of computing time to complete the iteration, the slowest chain will generally take far longer than an average chain to complete the iteration. In other words, the parallel scheme would spend a substantial amount of computing time waiting for the slowest chain to complete the iteration.

3.2 Update Schedules

A simple remedy is to update the transformation parameters not after a single iteration, but only after a larger number of iterations has been completed. The chains still need to be synchronized before every parameter update. But, if the number of iterations between updates is large enough (w.r.t. both and the variance of the runtime of a base sampler iteration in the given setting), the variance of the accumulated runtimes of individual chains will be quite small compared to the total runtime, so that comparatively little time is spent idling. To formalize the approach of only occasionally updating the parameters, we introduce the following notions.

Definition 3.1.

An update schedule is a strictly increasing sequence of positive integers , where , and either or for some . For a given update schedule , we call an update time if and only if there exists such that . We write if is an update time and otherwise.

The idea is now to define a suitable update schedule and then run the parallelized ATT approach, while updating the transformation parameters only in those iterations that are update times. This general approach will in the following be referred to as PATT (for parallel ATT). In order to enable a concrete description of PATT, we require the following auxiliary definitions.

Definition 3.2.

We define to be the family of bijective affine transformations on , i.e. of all , with .

Definition 3.3.

We define an ergodic base sampler for a given target distribution to be a family of transition kernels on , where for each , the kernel is ergodic towards , meaning that one has

| (4) |

Note that (4) is a relatively weak assumption on and that there are a number of easily verified assumptions on and that imply it, see for example Tierney (1994), Section 3.

Input: ergodic base sampler for the target distribution , number of parallel chains , initial states , update schedule

Output: samples

Based on these definitions, we can formulate PATT as Algorithm 2. It is not immediately clear how exactly one should choose the parameters of the transformations (line 11 of Algorithm 2), even if one has already decided on which adjustment types to use. We therefore provide detailed suggestions on how to specify and efficiently update these parameters in Appendix B. It is also not obvious how to choose a good update schedule. On the one hand, a large delay between updates will reduce the overall waiting time. On the other hand, more frequent updates will reduce the number of iterations to reach a specific sample quality, so there is a trade-off between these two choices. How the transformation parameters , themselves are chosen (e.g. as sample mean and sample covariance, we refer to this as parameter choice in the following) should also be considered when designing an update schedule. Specifically, returning to the notation of Section 2 for the moment, if the parameter choice does not permit incorporating a new sample in a complexity independent of the number of previously incorporated samples , then update schedules not designed to take this into account may result in computational costs that continue to grow in an unlimited fashion with increasing number of iterations. An example is the coordinate-wise sample median as a choice for updating the center parameter , see Appendix B.4 for details. We provide some guidelines for choosing the update schedule in Appendix C. For an exemplary analysis of how the use of interacting parallel ATT chains (rather than independent parallel ones) and update schedules (rather than updates after every iteration) affects sample quality and run time of the resulting sampler, we refer to the ablation study in Appendix H.2.

3.3 Initialization Burn-In

The main purpose of PATT is to allow samplers to work better in the long run. In particular, it is not very helpful (and can even be detrimental) in the early stages of sampling, where each chain needs to find a region of high probability mass, starting from a potentially poorly chosen initial state. Therefore, unless the user is very confident in the initialization of the parallel chains, they should first let the base sampler run them for a reasonable number of iterations. After this initialization burn-in phase, the user can apply PATT by using the final state of each burn-in chain as the initial state of the corresponding PATT chain. To avoid further complicating our description of PATT, we consider this early stage a process entirely separate from the remaining sampling.

Although asymptotically irrelevant, the use of such an initialization burn-in period can have a substantial positive impact in the short- and mid-term of the sampling procedure, see also the ablation study on this effect in Appendix H.3.

4 Theoretical Justification

In this section, we examine the convergence of PATT with finite update schedules where . Our motivation for this is twofold. First, we will demonstrate below that a finite update schedule necessitates only a weak assumption on the underlying base sampler to guarantee convergence of the corresponding PATT sampler. Second, after a sufficiently large number of iterations, the transformation parameters will be close to their optimal values. It may then be more economical to stop updating the parameters to rid oneself of the computational cost incurred from the update itself (which can be quite substantial, particularly in the case of covariance adjustments in high dimensions).

In order to properly express this section’s result, we require some new notation encoding a PATT sampler’s choice of the transformation parameters. Suppose in the following that the dimension of the sample space and the number of parallel chains are both known and fixed.

Definition 4.1.

We define a centering scheme to be a family of functions where maps , and a (co)variance adjustment scheme to be a family of functions where maps .

Intuitively, and take as input all the samples the PATT sampler has generated up to iteration and output the new transformation parameters and . Note that the option not to use centering is encoded in the above definition by for all and the option not to use (co)variance adjustments is encoded by for all .

We now state a general result on the ergodicity of PATT for finite update schedules. Note that in our analysis we ignore the initialization burn-in period entirely.

Theorem 4.2.

Let with for some be an arbitrary finite update schedule. Then for any collection of

-

•

a target distribution on given by an unnormalized density as in (1),

-

•

a number of parallel chains,

-

•

a centering scheme ,

-

•

a (co)variance adjustment scheme , and

-

•

an ergodic base sampler for ,

the resulting PATT sampler is ergodic in the sense that the samples generated by it satisfy

as , for any -integrable function and any choice of the initial states .

Proof.

See Appendix F. ∎

Of course, also theoretical results for PATT schemes with infinite update schedules are desirable. One way to establish such results would be to utilize the AirMCMC framework (Chimisov et al., 2018): It applies to those adaptive MCMC methods that are adapted increasingly rarely (rather than changing the transition kernel in every iteration), which for PATT corresponds to using an update schedule for which the sequence is strictly increasing. The advantage of the AirMCMC framework is that it imposes signficantly weaker conditions than the general adaptive MCMC framework to arrive at the same theoretical guarantees. However, the conditions imposed in theorems on AirMCMC are stronger than the corresponding ones for homogeneous MCMC. Therefore, we expect any theoretical results on PATT based on AirMCMC to rely on more restrictive assumptions than Theorem 4.2.

5 Numerical Experiments

In this section we give a brief overview over the results of a number of numerical experiments in which we let PATT samplers compete with several other methods. Our experiments are in large part inspired by Nishihara et al. (2014) and Hoffman & Gelman (2014).

5.1 Methodology

The main purpose of these experiments is to showcase the potential of PATT-GPSS (by which we denote any variant of PATT with base sampler GPSS) as a well-performing, user-friendly black-box sampler444By the term black-box sampler we refer to any sampling method that does not require its target distribution to have a particular structure (e.g. being a posterior resulting from a Gaussian prior, as in Murray et al. (2010)) and in particular does not explicitly rely on the probabilistic model underlying the target.. To this end, we always deployed PATT-GPSS with the default update schedules defined in Appendix C, thereby eliminating the need to devise setting-specific schedules. Moreover, all but one of our experiments used PATT-GPSS with centering (via sample means) and covariance adjustments (via sample covariances), showing these adjustment types to be a versatile default choice.

Although PATT-GPSS appears to work well for all targets that are not too misshapen, we note that, under certain conditions, PATT with other base samplers can achieve the same sample quality at even lower computational cost. To demonstrate this, we also considered PATT-ESS, meaning PATT with general-purpose ESS (GP-ESS, cf. Example E.5) as its base sampler, in our experiments.

As competitors for the PATT samplers, we found it natural to choose methods that were themselves proposed as user-friendly black-box samplers. From the class of non-adaptive MCMC methods, we chose hit-and-run uniform slice sampling (HRUSS) (MacKay (2003), Section 29.7). Among the traditional adaptive MCMC methods, we chose the adaptive random walk Metropolis algorithm (AdaRWM) (Haario et al., 2001), in the formulation proposed by Roberts & Rosenthal (2009). We implemented both HRUSS and AdaRWM in a naively parallelized fashion, allowing us to run the same number of parallel chains for each of them as for PATT (while not letting these chains interact with one another). Finally, as a sophisticated parallelized scheme of similar complexity as PATT, we chose (two-group) generalized elliptical slice sampling (GESS) (Nishihara et al., 2014). We emphasize that these three methods and the two PATT samplers are all essentially tuning-free, and that, accordingly, the amount of effort we spent on hand-tuning their parameters to each experiment was negligible. For a brief explanation of the inner workings of GPSS and each of the three competitor methods, we refer to Appendix G.1, and for an explanation of GP-ESS to Example E.5.

When numerically analyzing the sampling performance of PATT and its competitors, we were more interested in their respective long-term efficiency than in their behavior in the early stages. We therefore used a generous burn-in period, in that we considered only those samples generated in the latter half of iterations for this analysis. To assess the performance of each method, we computed a cost metric, two sample quality metrics and one aggregate of the former and the latter.

To measure sampling costs, we let each sampler count the number of target density evaluations (TDE) it required in each iteration of each chain and used these figures to compute the average number of TDE it required per (single-chain) iteration (TDE/it). Taking TDE/it to represent a sampler’s cost is common practice (see e.g. Nishihara et al. (2014); Schär et al. (2023)) and well-motivated by the observation that, in real-world applications, the sampler’s remaining overhead is typically negligible compared to the amount of resources it expends on TDE.

To measure sample quality, we relied on two different quantities. On the one hand, we considered the mean step size (MSS), that is, the Euclidean distance between two consecutive samples, averaged over all pairs of consecutive samples under consideration. Supposing that a sampler has already reached (empirically) stable behavior and is no longer moving through the sample space erratically, the MSS gives an indication as to how quickly it traverses the target’s regions of high probability mass (with a higher MSS meaning larger steps and therefore suggesting a quicker exploration of these regions). It has previously been considered by Schär et al. (2023) and is closely related to the often used mean squared jump distance, but more intuitive in its concrete values (since Euclidean distances are much closer to our real world experiences than squared Euclidean distances).

On the other hand, we considered the mean integrated autocorrelation time (mean IAT), which, for a given set of samples from a multi-chain sampler, is obtained by computing the IATs of each univariate marginal of the samples in each individual chain and then averaging these values over both the marginals and the chains. The IAT is commonly considered in the analysis of sampling methods because it is mathematically well-motivated to view the quotient of nominal sample size and IAT as the number of effective samples (ES) (see e.g. Gelman et al. (2013), Section 11.5).

This means that the IAT can be viewed as the number of (single-chain) iterations required to produce one ES, which gives rise to a natural performance metric that weighs cost and sample quality against one another: The product of TDE/it and IAT represents the number of TDE required for one ES (TDE/ES). Although we always provide TDE/it and IAT individually, we use TDE/ES as the primary metric to judge the overall performance of the samplers.

The source code for our numerical experiments is provided as a github repository555https://github.com/microscopic-image-analysis/patt_mcmc/. In the interest of reproducibility, all our experiments are designed to be executable on a regular workstation (rather than requiring a cluster).

5.2 Results

Here we briefly summarize the key parameters and results of our experiments. For details on the models, the resulting target densities, the data and the samplers’ settings (number of iterations etc.), we refer to Appendix G.

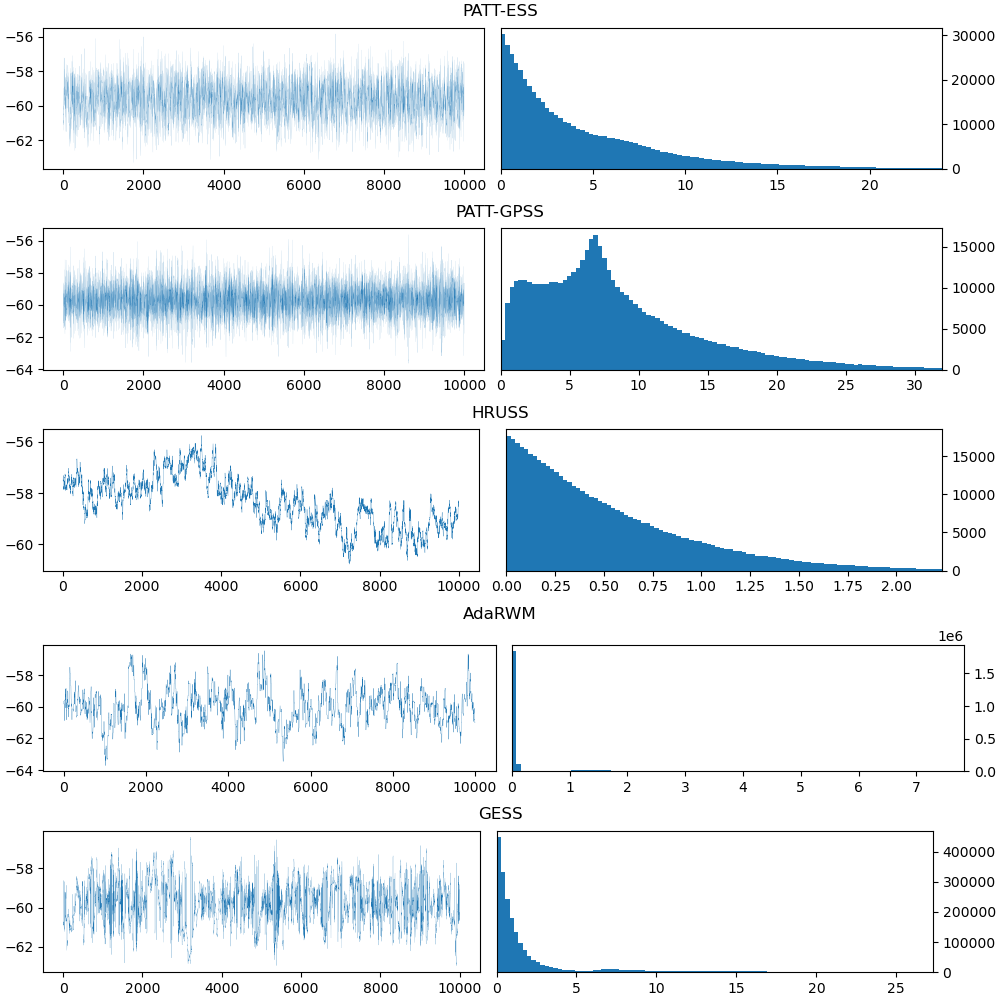

In our first experiment, we performed Bayesian inference on a model in which both prior and likelihood were given by multivariate exponential distributions (i.e. distributions whose densities have elliptical level sets and tails like for some ). We set the sample space dimension to and worked with synthetic data. The resulting sampling statistics are shown in Table 1. Moreover, trace plots of the first univariate marginal and histograms of the step sizes are presented in Appendix I, Figure 4.

| Sampler | TDE/it | mean IAT | MSS | TDE/ES |

|---|---|---|---|---|

| PATT-ESS | 3.28 | 7.87 | 4.53 | 25.84 |

| PATT-GPSS | 6.29 | 1.05 | 8.50 | 6.62 |

| HRUSS | 5.20 | 4476.90 | 0.52 | 23261.68 |

| AdaRWM | 1.00 | 115.89 | 0.67 | 115.89 |

| GESS | 5.02 | 32.43 | 2.43 | 162.75 |

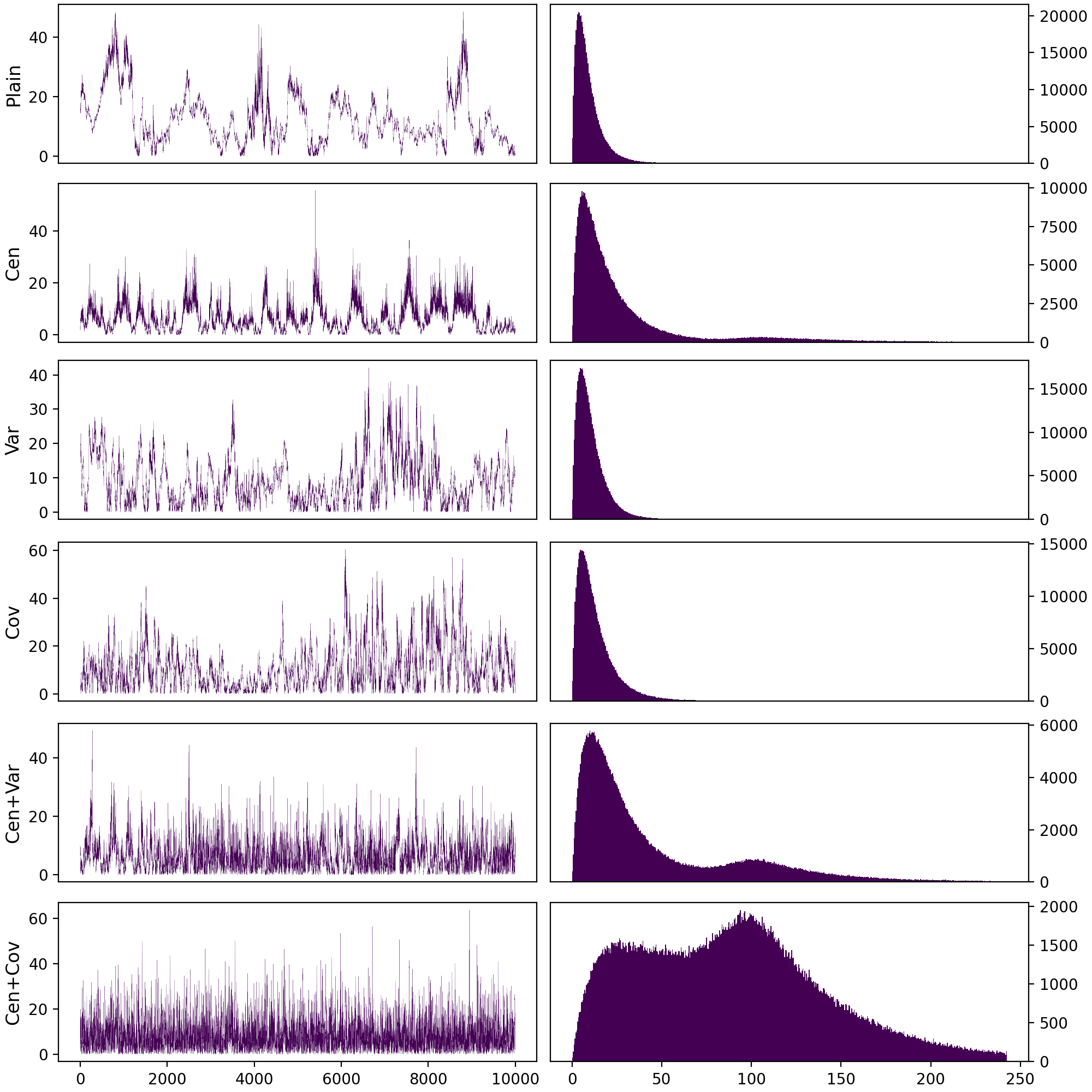

Next we conducted a series of experiments on Bayesian logistic regression (BLR) with mean-zero Gaussian prior for different data sets varying in the number of data points and features. In each of these experiments we added a constant feature to the data to enable an intercept. In some cases, we also performed feature engineering (FE) by augmenting the data with the two-way interactions between the given features. The resulting sample space dimensions were (Credit), (Breast), (Pima, with FE) and (Wine, with FE). For the sake of brevity, we only state the TDE/ES values for each experiment here, see Table 2. The complete sampling statistics are presented in Appendix G.4, Tables 4, 5, 6 and 7. Moreover, Figures 5, 6, 7 and 8 in Appendix I show the final covariance/scale matrices used by the adaptive samplers, thereby giving some insights into the intricate covariance structure the samplers had to learn to perform well.

| Sampler | Credit | Breast | Pima | Wine |

|---|---|---|---|---|

| PATT-ESS | 1.7 | 40.2 | 5.7 | 12.6 |

| PATT-GPSS | 7.6 | 73.2 | 18.9 | 28.0 |

| HRUSS | 2191.9 | 17083.8 | 2804.7 | 27133.7 |

| AdaRWM | 158.3 | 149.9 | 481.2 | 2677.5 |

| GESS | 468.3 | 580.0 | 11365.9 | – |

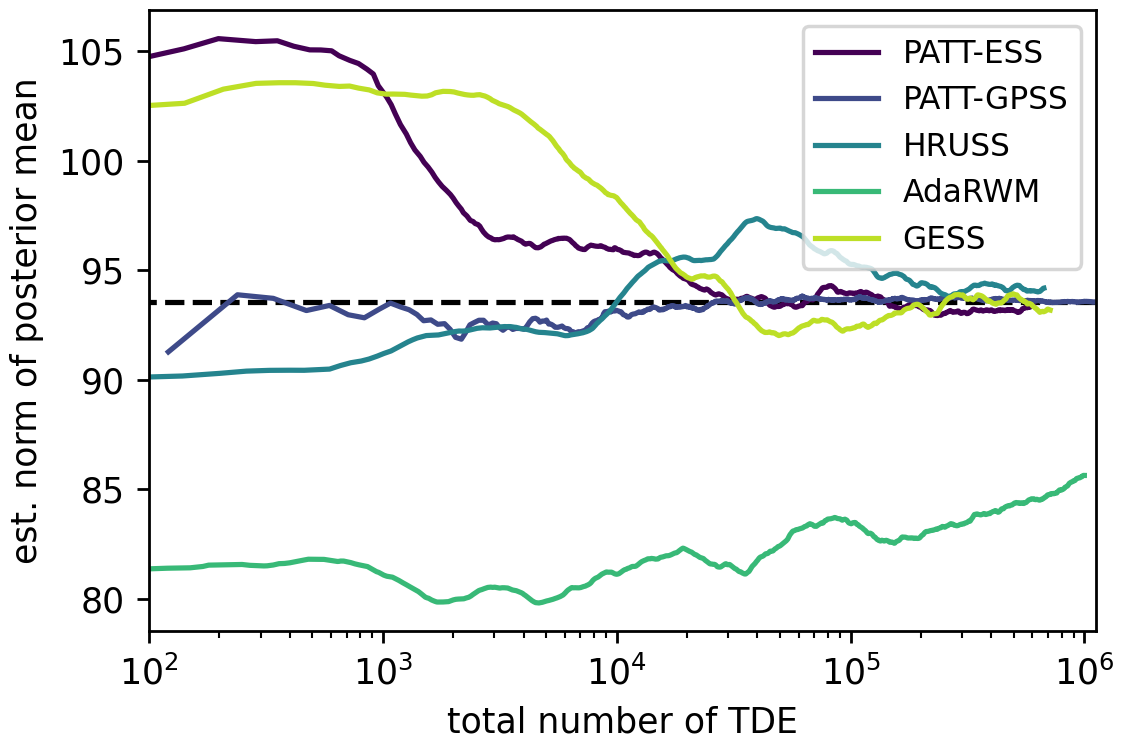

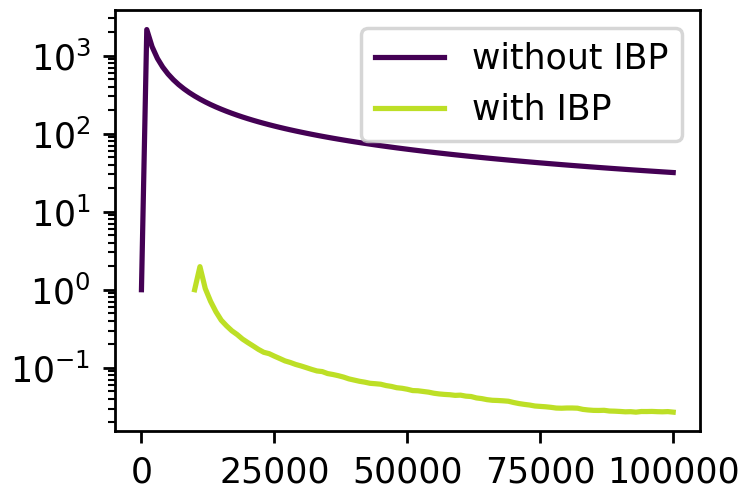

Finally, we conducted an experiment on Bayesian hyperparameter inference for Gaussian process regression of US census data in dimension . The results are shown in Table 3. As the mean IAT failed to properly convey the samplers’ performances in this experiment, we also estimated a target quantity from each run and visualized how quickly the estimates stabilized (for details see Appendix G.5). The result is shown in Figure 1. Judging by this plot, PATT-GPSS appears to have a substantial advantage over all its competitors, with PATT-ESS, HRUSS and GESS requiring perhaps an order of magnitude more TDE to reliably achieve the same precision and AdaRWM performing incomparably worse (which seems to be the result of its inability to efficiently explore the target’s tails, as shown by more detailed plots in the github repository).

| Sampler | TDE/it | mean IAT | MSS | TDE/ES |

|---|---|---|---|---|

| PATT-ESS | 6.06 | 45.62 | 13.16 | 276.52 |

| PATT-GPSS | 11.43 | 37.71 | 21.66 | 424.69 |

| HRUSS | 6.71 | 244.62 | 6.13 | 1641.75 |

| AdaRWM | 1.00 | 503.26 | 1.21 | 503.26 |

| GESS | 7.14 | 184.59 | 8.05 | 1318.77 |

We emphasize that across all of these experiments, the two PATT samplers consistently exhibited the highest sample quality in terms of both TDE/it and MSS (to see this for the BLR experiments, cf. the tables in Appendix G.4), at a cost low enough that they usually also require by far the fewest TDE/ES, often outperforming their nearest competitor in this regard by an order of magnitude or more. Even in the one case where they performed about evenly with AdaRWM in terms of TDE/ES (see Table 3), further analysis suggests that PATT-GPSS nevertheless delivered by far the best performance among the five methods (see Figure 1).

6 Concluding Remarks

We propose parallel affine transformation tuning (PATT), a general framework for setting up a computationally efficient, adaptively self-improving multi-chain sampling method based on an arbitrary base sampler, i.e. a single-chain, non-adaptive MCMC method. PATT provides the user with plenty of freedom in choosing adjustment types, update schedules and the base sampler, while at the same time offering reasonable default choices for all of these parameters. Moreover, with the default update schedules we propose, PATT is expected to scale well with the hardware it runs on, adapting suitably to every architecture from low-end personal workstations to large clusters.

Particularly noteworthy is the synergy of PATT with Gibbsian polar slice sampling (GPSS) (Schär et al., 2023) as the base sampler, in short denoted PATT-GPSS. As we demonstrated through a series of numerical experiments, PATT-GPSS is often able to produce samples of very high quality at a reasonable computational cost.

We wish to emphasize that this is not only the result of GPSS being well-suited to adaptively learning affine transformations like we do in PATT. Rather, PATT-GPSS manages to benefit from the extremely high performance ceiling GPSS has under optimal conditions, namely for target distributions that are rotationally invariant around the origin and unimodal along rays emanating from it. In fact, there is strong theoretical (cf. our remarks on this in Section 1) and numerical (cf. the experiments of Schär et al. (2023)) evidence that GPSS generally performs dimension-independently well in such rotationally-invariant settings. Importantly, through PATT, various challenging targets can be brought close enough to rotational invariance so that the underlying GPSS base sampler starts to approach the remarkably good performance it is known to exhibit under optimal conditions (cf. our numerical results in Section 5 and Appendices G and H).

We would like to stress one important limitation of PATT-GPSS. Although its performance ceiling under optimal conditions – say, for target densities whose level sets are elliptical – does, by all indications, not deteriorate with increasing dimension, the same cannot be said of the speed at which PATT-GPSS learns the affine transformation necessary to transform such a target into one that is rotationally invariant around the origin. While this deterioration in speed is quite moderate, it nevertheless means that in very high dimensions, PATT-GPSS may require a large number of iterations to begin approaching its asymptotic performance. This issue is not unique to PATT. For example, slowly converging empirical covariances in high dimensions had already been observed for AdaRWM by Roberts & Rosenthal (2009).

Acknowledgements

PS and MH gratefully acknowledge funding by the Carl Zeiss Foundation within the program “CZS Stiftungsprofessuren” and the project “Interactive Inference”. Moreover, the authors are grateful for the support of the DFG within project 432680300 – CRC 1456 subprojects A05 and B02.

Impact Statement

This paper presents work whose goal is to advance the field of probabilistic inference. There are many potential societal consequences of our work, none which we feel must be specifically highlighted here.

References

- Blum et al. (1973) Blum, M., Floyd, R. W., Pratt, V., and Rivest, R. L. Time bounds for selection. Journal of Computer and System Sciences, 7(4):448–461, 1973.

- Cabezas & Nemeth (2023) Cabezas, A. and Nemeth, C. Transport elliptical slice sampling. In Proceedings of the 26th International Conference on Artificial Intelligence and Statistics, volume 206 of Proceedings of Machine Learning Research, pp. 3664–3676. PMLR, 2023.

- Chimisov et al. (2018) Chimisov, C., Latuszynski, K., and Roberts, G. O. Air Markov chain Monte Carlo. arXiv preprint arXiv:1801.09309, 2018.

- Cortez et al. (2009) Cortez, P., Cerdeira, A., Almeida, F., Matos, T., and Reis, J. Modeling wine preferences by data mining from physicochemical properties. Decision Support Systems, 47(4):547–553, 2009.

- Cotter et al. (2013) Cotter, S. L., Roberts, G. O., Stuart, A. M., and White, D. MCMC methods for functions: Modifying old algorithms to make them faster. Statistical Science, 28(3):424–446, 2013.

- Craiu et al. (2009) Craiu, R. V., Rosenthal, J., and Yang, C. Learn from thy neighbor: Parallel-chain and regional adaptive MCMC. Journal of the American Statistical Association, 104(488):1454–1466, 2009.

- Gelman et al. (2013) Gelman, A., Carlin, J., Stern, H., Dunson, D., Vehtari, A., and Rubin, D. Bayesian Data Analysis (3rd ed.). Chapman and Hall, 2013.

- Giordani & Kohn (2010) Giordani, P. and Kohn, R. Adaptive independent Metropolis-Hastings by fast estimation of mixtures of normals. Journal of Computational and Graphical Statistics, 19(2):243–259, 2010.

- Grenioux et al. (2023) Grenioux, L., Durmus, A. O., Moulines, E., and Gabrié, M. On sampling with approximate transport maps. In Proceedings of the 40th International Conference on Machine Learning, volume 202 of Proceedings of Machine Learning Research, pp. 11698–11733. PMLR, 2023.

- Haario et al. (2001) Haario, H., Saksman, E., and Tamminen, J. An adaptive Metropolis algorithm. Bernoulli, 7(2):223–242, 2001.

- Habeck et al. (2023) Habeck, M., Hasenpflug, M., Kodgirwar, S., and Rudolf, D. Geodesic slice sampling on the sphere. arXiv preprint arXiv:2301.08056, 2023.

- Hasenpflug et al. (2023) Hasenpflug, M., Natarovskii, V., and Rudolf, D. Reversibility of elliptical slice sampling revisited. arXiv preprint arXiv:2301.02426, 2023.

- Hird & Livingstone (2023) Hird, M. and Livingstone, S. Quantifying the effectiveness of linear preconditioning in Markov chain Monte Carlo. arXiv preprint arXiv:2312.04898, 2023.

- Hoffman & Gelman (2014) Hoffman, M. D. and Gelman, A. The No-U-Turn sampler: Adaptively setting path lengths in Hamiltonian Monte Carlo. Journal of Machine Learning Research, 15:1593–1623, 2014.

- Hofmann (1994) Hofmann, H. Statlog (german credit data). UCI Machine Learning Repository, 1994.

- Li & Tso (2019) Li, S. and Tso, G. K. F. Generalized elliptical slice sampling with regional pseudo-priors. arXiv preprint arXiv:1903.05309, 2019.

- Lie et al. (2023) Lie, H. C., Rudolf, D., Sprungk, B., and Sullivan, T. J. Dimension-independent Markov chain Monte Carlo on the sphere. Scandinavian Journal of Statistics, 2023.

- Lovász & Vempala (2007) Lovász, L. and Vempala, S. The geometry of logconcave functions and sampling algorithms. Random Structures and Algorithms, 30(3):307–358, 2007.

- MacKay (2003) MacKay, D. Information Theory, Inference and Learning Algorithms. Cambridge University Press, 2003.

- Metropolis et al. (1953) Metropolis, N., Rosenbluth, A., M., R., and A., T. Equation of state calculations by fast computing machines. The Journal of Chemical Physics, 21(6):1087–1092, 1953.

- Murray et al. (2010) Murray, I., Adams, R. P., and MacKay, D. Elliptical slice sampling. In Proceedings of the 13th International Conference on Artificial Intelligence and Statistics, volume 9, pp. 541–548. PMLR, 2010.

- Müller (1991) Müller, P. A generic approach to posterior integration and Gibbs sampling. Technical report, Purdue University, 1991.

- Neal (1996) Neal, R. M. Bayesian Learning for Neural Networks, volume 118 of Lecture Notes in Statistics. Springer, New York, 1996.

- Neal (2003) Neal, R. M. Slice sampling. The Annals of Statistics, 31(3):705–767, 2003.

- Nishihara et al. (2014) Nishihara, R., Murray, I., and Adams, R. P. Parallel MCMC with generalized elliptical slice sampling. Journal of Machine Learning Research, 15:2087–2112, 2014.

- Parno & Marzouk (2018) Parno, M. D. and Marzouk, Y. M. Transport map accelerated Markov chain Monte Carlo. SIAM/ASA Journal on Uncertainty Quantification, 6(2):645–682, 2018.

- Rasmussen & Williams (2006) Rasmussen, C. E. and Williams, C. K. Gaussian Processes for Machine Learning. Adaptive Computation and Machine Learning. MIT Press, 2006.

- Roberts & Rosenthal (2002) Roberts, G. O. and Rosenthal, J. S. The polar slice sampler. Stochastic Models, 18(2):257–280, 2002.

- Roberts & Rosenthal (2009) Roberts, G. O. and Rosenthal, J. S. Examples of adaptive MCMC. Journal of Computational and Graphical Statistics, 18(2):349–367, 2009.

- Roberts & Tweedie (1996) Roberts, G. O. and Tweedie, R. L. Exponential convergence of Langevin distributions and their discrete approximations. Bernoulli, 2(4):341–363, 1996.

- Rudolf (2012) Rudolf, D. Explicit error bounds for Markov chain Monte Carlo. Dissertationes Mathematicae, 485:1–93, 2012.

- Rudolf & Schär (2024) Rudolf, D. and Schär, P. Dimension-independent spectral gap of polar slice sampling. Statistics and Computing, 34(article 20), 2024.

- Rudolf & Sprungk (2022) Rudolf, D. and Sprungk, B. Robust random walk-like Metropolis-Hastings algorithms for concentrating posteriors. arXiv preprint arXiv:2202.12127, 2022.

- Schär (2023) Schär, P. Wasserstein contraction and spectral gap of slice sampling revisited. Electronic Journal of Probability, 28(article 136), 2023.

- Schär & Stier (2023) Schär, P. and Stier, T. A dimension-independent bound on the Wasserstein contraction rate of geodesic slice sampling on the sphere for uniform target. arXiv preprint arXiv:2309.09097, 2023.

- Schär et al. (2023) Schär, P., Habeck, M., and Rudolf, D. Gibbsian polar slice sampling. In Proceedings of the 40th International Conference on Machine Learning, volume 202 of Proceedings of Machine Learning Research, pp. 30204–30223. PMLR, 2023.

- Smith et al. (1988) Smith, J. W., Everhart, J., Dickson, W., Knowler, W., and Johannes, R. Using the ADAP learning algorithm to forecast the onset of diabetes mellitus. In Proceedings of the Annual Symposium on Computer Applications in Medical Care, pp. 261–265, 1988.

- Street et al. (1995) Street, N., Wolberg, W., and Mangasarian, O. Breast cancer Wisconsin (diagnostic). UCI Machine Learning Repository, 1995.

- Tibbits et al. (2014) Tibbits, M. M., Groendyke, C., Haran, M., and Liechty, J. C. Automated factor slice sampling. Journal of Computational and Graphical Statistics, 23(2):543–563, 2014.

- Tierney (1994) Tierney, L. Markov chains for exploring posterior distributions. The Annals of Statistics, 22(4):1701–1728, 1994.

- Yang et al. (2022) Yang, J., Latuszyński, K., and Roberts, G. O. Stereographic Markov chain Monte Carlo. arXiv preprint arXiv:2205.12112, 2022.

Appendix A Choosing the Adjustment Type(s)

In this section we provide some general considerations on the potential advantages and downsides of the three adjustment types (cf. Section 2.3) in an ATT or PATT sampler and try to give recommendations for when to use each of them.

Generally speaking, base samplers can be divided into those whose transition kernel is affected by centering with a fixed parameter , which we call location-sensitive, and those that are unaffected by it, which we call location-invariant. Some examples of location-sensitive base samplers are IMH, pCN-MH, ESS and GPSS, and some examples of location-invariant ones are RWM, MALA, HMC and all variants of uniform slice sampling.

Naturally, it only makes sense to use centering when one is working with a location-sensitive base sampler. On the other hand, as we will see in the next subsection, the computational overhead associated with centering is minimal, so that small gains in performance already justify its use. Furthermore, the improvement in sample quality due to centering is often large, particularly if the sample space is high-dimensional. We therefore recommend to use centering per default when working with a location-sensitive base sampler. Of course even with such base samplers there are some scenarios where centering is ill-advised, for example those where the target distribution is known to be centered around the origin (as is the case in our experiment on Bayesian hyperparameter inference for Gaussian process regression, see Appendix G.5 for details).

Variance adjustments can improve the performance, in terms of computational cost per iteration and/or sample quality, of virtually all base samplers. Such performance gains can be expected as soon as the target distribution has a substantial variation among its coordinate variances (i.e. the diagonal entries of its covariance matrix) and should grow alongside any increases in this variation. Moreover, like with centering, the computational overhead associated with the adjustments is minimal. We therefore recommend using variance adjustments pretty much whenever covariance adjustments are ill-advised or infeasible and the variation among the target distribution’s coordinate variances is not known to be small.

Covariance adjustments are a sort of double-edged sword. On the one hand, they constitute a powerful way of reducing the complexity of a given target distribution with non-trivial correlation structure, thereby improving the sample quality of virtually all base samplers. This even includes some which are unaffected by both other adjustments, such as random-scan uniform slice sampling (RSUSS) (Neal, 2003). On the other hand, covariance adjustments are far more computationally costly than centering and variance adjustments, particularly if the sample space is high-dimensional. We therefore find it difficult to give far-reaching recommendations regarding the use of these adjustments, though a good rule of thumb may be to always consider their use and only refrain from it if it proves computationally infeasible or mixing-wise unhelpful.

Some exemplary numerical evidence on the advantages of using the different adjustment types, both individually and in combination, can be found in the ablation study on adjustment types in Appendix H.1.

We conclude this section with some general considerations on potential demerits to using the different adjustments. Specifically, we wish to emphasize that the use of a given adjustment type is likely to be detrimental to a PATT sampler’s performance if the feature of the target density that it modifies (e.g. the extent to which it is centered around the origin) is already in its optimal configuration in the untransformed target. This is intuitively clear: If is already in its optimal configuration, an affine transformation of it cannot possibly be in a better one and is, for virtually all choices of the transformation , actually in a worse one.

Moreover, even if the feature modified by an adjustment type is entirely irrelevant to the base sampler (e.g. centering for variants of uniform slice sampling), allowing PATT to modify that feature may still be somewhat detrimental to the PATT sampler’s performance, simply by virtue of introducing instability into the sampling procedure (since, from the base sampler’s point of view, the target changes at every update time). On the other hand, we note that this detrimental effect is only relevant in the short- to mid-term. Asymptotically (assuming an infinite update schedule), the affine transformation learned by PATT will leave the feature in question as is and thus no longer be detrimental to the sampler’s performance.

Nonetheless, if one seeks to apply PATT in real world applications, one should take care to avoid adjusting both those features for which one knows the target distribution to already be in the optimal configuration (though we imagine such knowledge is seldom available in practice) and those that are irrelevant to the base sampler one wishes to use.

Appendix B Choosing and Updating the Parameters

Here we examine, for each of the three adjustment types, one or more ways to choose the transformation parameter associated with it, based on a given set of samples. Moreover, as promised earlier, we elaborate on efficient ways of updating the chosen parameters and the associated computational complexities.

As ATT can be retrieved from PATT as a special case, we work within the PATT framework in the following. That is, we examine the parameter choices for a sampler that runs parallel ATT chains according to some update schedule , meaning that at each update time all the samples up to that time are pooled and new transformation parameters are computed based on them. For and , we denote by the (sample space) state of the -th chain in the -th iteration.

B.1 Sample Mean

For centering, one needs to choose the parameter . As outlined in Section 2.1, for the transformed distribution to be centered around the origin, would need to be the center of the untransformed target . Supposing that is not too misshapen, and light-tailed enough to have a well-defined mean (a very weak assumption), it is reasonable to view this mean as its center. Since the mean of an intractable target distribution is generally not known to the user, it needs to be approximated based on the available samples. The natural way to do this is by using the sample mean , which in iteration of our multi-chain setting is given by

| (5) |

In order to update the sample mean in a computationally efficient manner at each update time , one may rely on the recursion

| (6) |

to utilize the old sample mean in computing the new one.

Using (6), we can incorporate the new samples into the sample mean in just operations (recall that each sample is a -dimensional vector). If we amortize this cost across the (multi-chain) iterations these samples were generated in, we obtain an amortized cost of per iteration for the parameter updates. Since this complexity is already reached by just storing the corresponding samples, the computational overhead associated with the use of this adjustment type is negligible.

B.2 Sample Variance

The goal of variance adjustments is to transform the target distribution in such a way that the covariance matrix of the transformed target distribution has only ones on its diagonal. Analogously to centering, actually reaching this goal would require knowledge of the target distribution that is generally unavailable. Specifically, one would need to know the coordinate variances

where we write , use them to generate the vector of standard deviations and use as the matrix parameter of . To deal with the values being unknown, we may estimate them by the coordinate-wise sample variances of the available samples. This corresponds to estimating the vector by

| (7) |

where for any vector we denote

Again we may greatly improve the computational efficiency of performing these adjustments by relying on recursive computations. By setting

we obtain

| (8) | ||||

The above recursions, together with (6), allow us to incorporate the new samples into in the same (amortized) complexity as for the sample mean, so that this use of ATT can also be implemented with negligible computational overhead.

We emphasize that in practice one would not actually compute and maintain the full matrices , but rather make use of the fact that the matrix-vector product coincides with , where denotes element-wise multiplication of -dimensional vectors, i.e.

In other words, the evaluation of (and analogously also that of ) can also be implemented to only use operations per evaluation (note that this does not change when combining these adjustments with centering). In particular, the remaining overhead of variance adjustments (i.e. aside from maintaining the transformation’s parameters) is also of the same negligible computational complexity as the one for centering.

B.3 Sample Covariance

As we saw in Section 2.1, the canonical way to transform the target distribution into having the identity matrix as its covariance is to use the Cholesky factor of , meaning , as the matrix parameter of , that is, to set . Analogously to the variance adjustments, a natural way of approximating this optimal choice is to first approximate the true covariance by the sample covariance , then compute its Cholesky decomposition and use as the matrix parameter of .

Again we may use recursive computations. With

we obtain the recursions

Again together with (6), these recursions allow for the incorporation of the new samples into in operations. If we amortize this over the (multi-chain) iterations, we obtain a cost of per iteration, which is optimal for PATT schemes with chains and non-sparse covariance matrix parameter. Recall however, that updating an ATT scheme based on the sample covariance also necessitates computing the sample covariance’s Cholesky factor and that factor’s matrix inverse (to evaluate , cf. (2), which is necessary when translating a state from sample space to latent space), both of which has complexity . We therefore recommend to suitably scale covariance adjustments with the dimension , e.g. by using parallel chains or by choosing an update schedule such that is at least of order , either of which makes it so that the complexity of the aforementioned computations no longer dominates that of the overall method.

We also note that by using a non-diagonal (more precisely non-sparse) matrix in the transformation , one necessarily incurs an evaluation overhead of at least per iteration, because evaluating in a given point involves evaluating at , which in turn necessitates computing the matrix-vector-product , which has complexity .

B.4 Sample Median

If the target distribution is heavy-tailed, any MCMC-style sampler for it will occasionally make trips far into the tails. The samples from these trips will (at least temporarily) have an enormous impact on the sample mean, perturbing it far from the true mean and consequently hindering efficient sampling. Furthermore, if the tails are heavy enough, will not even have a well-defined mean, so that the sequence simply would not converge. Consequently, whenever one is faced with a substantially heavy-tailed target distribution, it is advisable to estimate the target’s center by something other than the sample mean. Possible choices include trimmed means, Winsorized means and the coordinate-wise sample median. In the following, we focus on the latter option and elaborate on how it could be implemented in practice.

As the name suggests, we define the coordinate-wise sample median of a set of samples to be the vector whose -th entry is given by the median of the -th entries of the vectors ,

The naive approach to computing is to simply sort these -th entries (separately for each ) and find the median as the middle element (or the arithmetic mean of the two middle elements, if is even) of the sorted sequence. Because the distribution of the -th vector entries will, in the settings we consider, usually be far from uniform, efficient sorting schemes (such as bucket sort) are out of question, and so the complexity of the aforementioned sorting-based median computation is .

Similarly, one can maintain the median of a growing sequence of values by explicitly maintaining the two sorted half-sequences of elements that are smaller, respectively larger, than the median in two instances of a suitable data structure (e.g. binary search trees). In the present case, supposing that the method has already been running for iterations, this approach would require operations to update all medians based on a batch of new samples . In other words, because the cost of inserting an element into a sorted data structure increases logarithmically in the size of the data structure, maintaining the sample median in this way would lead updates to become arbitrarily expensive if the method is run for sufficiently many iterations. Naturally, we would like to avoid this sort of degeneration of our method.

Though this appears to be infeasible if one requires the median to be updated in each iteration, it can still be accomplished if one is satisfied with occasional updates: It turns out that by using an update schedule that offsets the steadily increasing update cost by performing updates less and less frequently as the sampling goes on, we can achieve an amortized cost per iteration that does not depend on the number of iterations up to that point. To this end, we note that the first approach we mentioned (simply sorting a given set of samples) does not have optimal complexity: It was shown by Blum et al. (1973) that the median of a given set of values can actually be computed in (deterministic) linear complexity. Thus an update of the sample median after iterations with parallel chains can be performed in complexity . Now consider the update schedule with for some and . Since we may amortize the cost of updating at iteration over the iterations since the last update, we obtain an amortized cost of

per iteration, which no longer depends on . Note that with integer choices of and the rounding becomes unnecessary, but that a choice may be preferable performance-wise because it can allow significantly more updates within a finite number of iterations than even the minimal integer choice .

B.5 Well-Definedness Issues

In this section we discuss possible discrepancies between the transformation parameter choices outlined in Section B and the implicit requirement (made somewhat more explicit in Definition 4.1) that the parameter choices one makes should always lead to a well-defined, bijective transformation . For centering this is generally not an issue, regardless of which parameter choice one uses.

For variance adjustments, one already needs to be a bit more careful: Because the sample variance of a set of identical values is zero, if the available samples all coincide in some coordinate, the resulting vector will have a zero entry, so that the transformation is not actually bijective. Of course when using PATT with parallel chains this pathological case is easily avoided by initializing the different chains with coordinate-wise distinct states , (e.g. independently drawn from some Gaussian). However, if one only wants to use a single chain or if one insists on initializing all parallel chains with the same initial state (for whatever reason), some care may need to be taken to ensure well-definedness.

Whether such a setup is problematic actually comes down to the base sampler one wishes to use: For various slice sampling methods, e.g. ESS, GPSS and hit-and-run uniform slice sampling (HRUSS), it is clear that two consecutive samples , produced by any of these methods differ almost surely in all components, so that computing the sample means based on any number of iterations suffices to ensure their well-definedness. On the other hand, any method based on random-scan Gibbs sampling, i.e. on updating the state only in one randomly chosen coordinate per iteration, is at risk of violating the well-definedness, because for any there is a positive (albeit very small) probability that one of the coordinates was never chosen for updating throughout the first iterations, so that all of the available samples coincide in that coordinate. Accordingly, this issue can even affect methods that are rejection-free overall, most notably RSUSS. Of course Metropolis-Hastings (MH) methods are, in regards to this well-definedness, even more problematic than random-scan Gibbs sampling. Because in each iteration they may reject the proposal with some positive probability, it is entirely plausible for an MH method to produce a decently sized sequence of states that all coincide.

In summary, in order to ensure well-definedness of ATT transformations based on the sample variance, one must either use multiple parallel chains, initialized in coordinate-wise distinct states, or use a method that is coordinate-wise rejection-free (in particular no random-scan Gibbs sampling, no MH methods), or slightly modify the variance estimator one uses, e.g. by incorporating a “dummy state” into the computations.

For covariance adjustments based on the sample covariance, well-definedness is an even larger issue: For these adjustments to be well-defined, the sample covariance must be positive definite (since it must have a Cholesky decomposition), for which the samples it is computed from must span the entire sample space . In other words, while the cases that break the well-definedness of variance adjustments do the same for covariance adjustments, there are some additional cases that break only the latter. Moreover, these additional cases, while extremely rare in practice, cannot simply be precluded by choosing a suitable base sampler.

Therefore, if one must be absolutely certain that the covariance adjustments are well-defined, one should replace the sample covariance by a regularized version of itself, i.e. by for some , where is the identity matrix. By choosing large enough (depending on the given ), the resulting matrix can always be made positive definite, which suffices to ensure well-definedness overall.

Appendix C Choosing an Update Schedule

Here we summarize our findings regarding update schedules from Section 3 and Appendix B and add some more general considerations.

When using the PATT framework, it is not advisable to update the transformation parameters in every iteration, even if the computational overhead from the parameter updates themselves is negligible. Rather, one should always run the chains for a reasonable number of iterations in between updates, in order to reduce the total time spent waiting for the slowest chain before each parameter update.

Moreover, it is usually not advisable to begin the tuning right away, i.e. to compute the first set of transformation parameters based on very few samples, as at least the canonical parameter choices we discussed in Appendix B are not particularly robust towards such situations, so that transformation parameters computed from an overly small set of initial samples may well lead to such bad transformations that the method’s medium-term sampling efficiency is significantly hampered.

For the simplest parameter choices, in particular the sample mean from (5) and the sample standard deviation from (7), we conjecture it reasonable to use a linear update schedule, i.e. with for some , chosen according to the above considerations ( being the delay between consecutive updates and being the initial tuning burn-in, i.e. the number of iterations before the first transformation is chosen). Nevertheless, we think it may be slightly more efficient overall to use an update schedule that slowly increases the delay between consecutive updates, particularly because the effect of a fixed number, say , of new samples on statistics like the sample mean and sample standard deviation diminishes as the total number of samples increases.

For slightly more extravagant parameter choices, for which efficient updates have amortized costs per iteration that can depend on the dimension , but not on the number of iterations , a good general guideline appears to be that a linear update schedule for these choices may be used, but that its parameters should be scaled with (powers of) in order to yield an amortized update cost per iteration that is dominated by other tasks. Specifically, with sample covariances, the computational overhead associated with the sampling itself is per iteration, whereas updating the parameters costs . Thus, to achieve good amortization, the guideline suggests using an update schedule for which is of order . A natural way to achieve this would be for some , where consecutive update times are a fixed multiple of apart.

Finally, for even more costly parameter choices like the sample median, for which an update after iterations costs , it seems advisable to use an exponential schedule, as this leads to an amortized cost per iteration independent of (see our analysis in Appendix B.4).

Though the parameter choices should play an important rule in deciding for an update schedule, some characteristics of the target distribution may also be considered in this process. For instance, in cases where is known (or strongly suspected) to be heavy-tailed or very misshapen, update times for ATT should tend to be further apart than in analogous settings with light-tailed and well-shaped targets. This is because in the former settings the base sampler is much more likely to get into situations that require many target density evaluations to get out of (e.g. walking far into the tails in a heavy-tailed setting), which, at least for base samplers using a random number of target density evaluations per iteration, increases the variance of the runtime of each chain for a given number of iterations, and therefore the time spent waiting for the slowest chain when synchronizing them for an update.

Although we expect that such nuanced considerations can enable posing even better-tuned samplers, in our experiments with PATT we have found it easier to always rely on default schedules that are parametrized solely by the selected adjustment types, the dimension of the problem at hand and the number of parallel chains to be used. These default schedules are defined as follows: Each of them is a priori infinite and only truncated by the finite number of iterations to be performed. If the PATT-sampler is to use centering with sample medians, the default schedule is

(note that ). Otherwise, if the sampler is to use covariance adjustments with sample covariances, the default schedule is

Finally, for all choices of adjustment types and parameter choices that fall into neither of these two categories, the default schedule is

Appendix D Connections to Other Works

Since ATT and PATT are simple concepts, expectedly they are related, in one way or another, to various other approaches. On the one hand, adaptive MCMC as a general principle was first popularized with its application to methods that use the adaptivity to (among other things) find a representation of the target distribution’s covariance structure, see Roberts & Rosenthal (2009) and references therein. In contrast to ATT, these methods used the covariance information to adjust their proposal distribution, rather than transform the target. Though the two approaches can in principle lead to equivalent transition mechanisms (cf. our analysis in Appendix E), they usually differ and for some underlying samplers (e.g. GPSS) there is no proposal distribution to be tuned and so no traditional adaptive MCMC methods equivalent to their ATT versions exist.

On the other hand, there are a number of sampling approaches that, like ATT, proceed by moving back and forth between the sample space and a latent space. Most notably, Müller (1991) proposed adaptively transforming the target distribution to adjust its covariance structure (by the same principle as the covariance adjustments of ATT), for the purpose of improving the performance of an underlying Metropolis-within-Gibbs sampler. Similarly, Lovász & Vempala (2007) suggested affinely transforming a log-concave target distribution with the aim, just like in ATT, of bringing it into isotropic position, for the purpose of improving the performance of an underlying MCMC method (for which they have two particular choices in mind). Despite this idea appearing very similar to that of ATT on the surface, the two approaches’ relation is not actually that strong because Lovász & Vempala’s assumption on the target to be log-concave actually leads to substantial differences between their settings (e.g. by enabling a method for learning the affine transformation that is inapplicable without the assumption). Recently, some effort has been made (Hird & Livingstone, 2023) to quantify how linearly preconditioning the target distribution (as a one-time action, i.e. non-adaptively) affects the theoretical properties (e.g. mixing time, spectral gap) of an MCMC method when applying it to the transformed target instead of the untransformed one. Their considerations cover both variance and covariance adjustments (cf. Section 2.3), but no centering (i.e. their transformations are actually linear, not just affine linear). Although Hird & Livingstone (2023) interpret transforming the target as an alternative viewpoint to adjusting some proposal distribution (since the MCMC methods they are interested in all have such a proposal component), many of the conclusions they draw about what types of target distributions are simplified by linear transformations, as well as some of their analysis on which transformation parameter choices are optimal for certain types of models, should apply to ATT and PATT as well.

In a slightly different direction, Yang et al. (2022) proposed to use the -sphere as a latent space for sampling from target distributions on , specifically by transforming back and forth between the spaces with a generalized stereographic projection and using, for example, a simple RWM sampler to make steps in the latent space. Conversely, Lie et al. (2023) suggested a latent space based sampling scheme for sampling from target distributions on (possibly infinite-dimensional) spheres, by relying on samplers that are well-defined on Hilbert spaces (such as pCN-MH and ESS).

Most contemporary latent space based sampling schemes, however, make use of approximate transport maps. That is, they learn (sometimes adaptively) a highly non-linear bijective transformation that aims to transform the given target distribution into a simple reference distribution, typically the standard Gaussian. Whereas the seminal work that first proposed such a scheme (Parno & Marzouk, 2018) built its transformation with triangular maps, nowadays most such schemes instead rely on normalizing flows, see Grenioux et al. (2023) for a recent overview. Most notable among such approaches (in terms of their similarity to this work) Cabezas & Nemeth (2023) proposed to employ the normalizing flows scheme with ESS as the underlying base sampler and even rely on parallelization and a type of update schedule in their learning of the transformation. Clearly, transforming the target distribution into a specific reference distribution is a much more challenging task than just bringing it into isotropic position (the latter being the goal of ATT). Accordingly, the transformations the approximate transport map approach relies on are costly to learn and to evaluate. Moreover, it is known that the approach itself does not scale well to high dimensions (Grenioux et al., 2023).

To the best of our knowledge, in the present adaptive MCMC literature the focus is on samplers that rely on Metropolis-Hastings algorithms. Very few efforts have been made to harness the power of adaptive MCMC for slice sampling. Since we focus on applying PATT to slice samplers (specifically GPSS and ESS), we find it appropriate to briefly cover these related efforts. Firstly, Tibbits et al. (2014) devised an adaptive MCMC scheme to tune deterministic scan uniform slice sampling (DSUSS) (Neal, 2003), by letting it perform its one-dimensional updates along lines spanned by the elements of an adaptively learned basis of (derived from an estimate of the target’s covariance structure) rather than by those of the standard basis. We surmise that this should be equivalent (in the sense discussed for other cases in Appendix E) to applying ATT with covariance adjustments to DSUSS. Secondly, Li & Tso (2019) proposed a scheme in which the target distribution is approximated by an adaptively learned mixture model and approximate samples from the target are generated by applying different versions of ESS to it, depending on the mixture model and the current state of the chain.

Furthermore, we want to comment on the relations to generalized elliptical slice sampling (GESS) (Nishihara et al., 2014). In contrast to the two previous references, the authors of GESS did not opt for an adaptive MCMC, but rather a sophisticated MCMC method. Within their approach they choose those parameters of their sampler that would usually be chosen adaptively based just on the chain’s current state, which they made feasible by introducing both parallelization and a “two-group” component into the method (while still viewing it as a single Markov chain overall). Though founded on entirely different principles, the resulting method has some significant parallels to PATT, in that both methods maintain a number of parallel sub-samplers on the sample space and occasionally pool the information they gather to update their parameters, for the purpose of better adapting them to the target and thereby improving their performance. We mention that PATT may have an advantage compared to GESS, since it is easier to scale to small numbers of parallel chains (e.g. to accomodate users that wish to run a sampler on hardware with relatively few CPU cores). Regarding numerical comparisons between GESS and PATT, we refer to Section 5 and Appendix G.

We also wish to point out two earlier works that PATT shares certain mechanims with. Firstly, Craiu et al. (2009) suggested several adaptive MCMC methods that share PATT’s basic parallelization approach, i.e. each of these methods runs a number of parallel chains on the sample space and uses the samples generated by all chains to update the adaptively learned parameters. In contrast to PATT, Craiu et al. (2009) did not consider any kind of update schedule, instead synchronizing the chains and updating the parameters in every iteration. This is feasible for them because they only considered choosing their underlying sampler as a Metropolis-Hastings method, and these methods are easy to synchronize since they only require a single target density evaluation per iteration.

Secondly, Chimisov et al. (2018) proposed a new framework for adaptive MCMC, called AirMCMC, that differs from the commonly used one by only allowing the adaptively learned parameters to be updated at a predetermined sequence of iterations. Furthermore, the sequence of differences is itself required to be strictly increasing, so that over time an AirMCMC method updates its parameters increasingly rarely. Obviously, the idea to only update the parameters at predetermined times has a large overlap with our concept of an update schedule. Moreover, for Chimisov et al. (2018) the main motivation for using such update times is that it eases theoretical analysis (compared with the general adaptive MCMC framework). The main results of Chimisov et al. (2018) might therefore be of use in proving theoretical guarantees, such as ergodicity, of certain types of PATT samplers with infinite update schedules.

Appendix E ATT-friendly adaptive MCMC schemes

Some classical adaptive MCMC schemes can be interpreted in terms of ATT. More generally, consider an adapation scenario w.r.t. a family of transition kernels with covariance and shift parameters. For this let be the set of all positive definite matrices in , recall that is the set of bijective affine transformations on , c.f. Definition 3.2, and is the pushforward measure of under . We introduce the following property.

Definition E.1.

Let be a family of probability measures on that is closed under affine transformations in the sense that

| (9) |

A family of transition kernels on that satisfies

| (10) |

is called ATT-friendly, if for any there is an such that

| (11) |

for all , where is the zero-vector and the identity matrix.

Observe that, by (3), the identity (11) can be interpreted as saying that is the transition kernel of ATT for target distribution with fixed transformation and the base sampler with transition kernel on the latent space. Moreover, an adaptive MCMC scheme based on an ATT-friendly family of transition kernels can, by (11), be interpreted as updating a linear transformation whenever the pair of parameters is updated.

In the following, we establish the ATT-friendliness of a number of classical MCMC schemes in an exemplary, case-by-case fashion. This allows us to formally establish equivalences between adaptive implementations of ATT and certain adaptive MCMC versions of these classical schemes.

Example E.2 (Random walk Metropolis).

Let be the family of distributions on that admit a strictly positive Lebesgue density. Note that this trivially satisfies (9). Let and denote by its density. The transition kernel of the random walk Metropolis (RWM) algorithm for with covariance parameter and fixed step size is given by

The family is one of the standard families of transition kernels that serve as building blocks for adaptive MCMC, c.f. Roberts & Rosenthal (2009). For example, multiple classical adaptive MCMC methods (e.g. Haario et al. (2001); Roberts & Rosenthal (2009)) follow the basic idea to perform the -th iteration by , where is the sample covariance of the first samples (usually is slightly regularized to enable better theoretical guarantees).

By introducing a dummy index that the kernels do not actually depend on, we obtain the family that fits the format of the class in Definition E.1. As it is well-known that for all , this also satisfies the invariance requirement (10). We may therefore examine the ATT-friendliness of .