Duality of causal distributionally robust optimization: the discrete-time case

Abstract

This paper studies distributionally robust optimization (DRO) in a dynamic context. We consider a general penalized DRO problem with a causal transport-type penalization. Such a penalization naturally captures the information flow generated by the dynamic model. We derive a tractable dynamic duality formula under mild conditions. Furthermore, we apply this duality formula to address distributionally robust version of average value-at-risk, stochastic control, and optimal stopping.

Keywords: distributionally robust optimization, causal optimal transport, minimax theorem.

1 Introduction

In this paper, we study the duality of the penalized distributionally robust optimization (DRO) problem in a discrete-time setting. Let be the extended real numbers, Polish spaces, the path space of -step processes, the canonical process, a path-dependent function(al), a convex penalization function, a reference probability measure on . We are interested in the following quantity

| (1.1) |

where denotes the set of Borel probability measures on , and denotes the causal transport cost induced by cost function . In particular, taking we obtain the classical DRO problem

| (1.2) |

where is a -neighborhood of corresponding to the uncertainty (ambiguity) about the model . Such quantities gauge the greatest objective value when the actual model deviates from the reference .

This so-called Knightian uncertainty (Knight, 1921) on the model is of fundamental importance and a subject of intense studies in mathematics and economics alike. Mathematical frameworks such as risk measures (Föllmer and Schied, 2008) and sublinear expectations (Peng, 2019) have been developed to take into account the model uncertainty. In mathematical finance, the market model is usually derived from theoretical considerations, possibly combined with some calibration to market data, and typically has nice analytic representation. More recently, numerical data-driven approaches have been developed, often involving deep neural networks and machine learning techniques. In such context, the data – be it market data or generated data – are typically discrete. In both approaches, the misspecification of the postulated measure, i.e, the model, is inevitable. Studying (1.1) leads to a more comprehensive understanding of the model and helps agents make rational decisions in presence of model uncertainty.

The choice of the uncertainty set is subtle and lies in the heart of DRO. Especially, in a dynamic setting the reference model has a natural temporal structure. In this paper, we focus on the case that the discrepancy between models is characterized by the causal transport cost

Here, the infimum is taken over a set of causal couplings which was first systematically studied in Lassalle (2018). Heuristically, the causality constraint means that the transport plan is not allowed to peek into the future of the model dynamic.

It is well-known that the Wasserstein distance intrinsically captures the geometry of the state space, see Lott and Villani (2009) for example. Likewise, the distance induced by (bi)causal optimal transport, the adapted Wasserstein distance, intrinsically captures all the (spatial and temporal) information generated by processes. In the seminal paper Backhoff-Veraguas et al. (2020b), the topology induced by the adapted Wasserstein distance has been shown to be equivalent to various notions of adapted topologies such as Hellwig’s information topology (Hellwig, 1996) and Aldous’s extended weak topology (Aldous, 1981). This notion is also closely related to the pioneering works by Yamada and Watanabe (1971), Rüschendorf (1985), Pflug (2010), Pflug and Pichler (2012) and more recent works by Acciaio et al. (2020), Bion–Nadal and Talay (2019), Backhoff-Veraguas et al. (2017, 2020a, 2022), Pammer (2022), etc. We believe such a discrepancy naturally fits the dynamic setting and is a good candidate to capture the model uncertainty.

Our main result Theorem 3.2 gives a dynamic duality formulation for (1.1). We denote the decomposition of the reference measure by

where are the successive regular disintegration kernels. Under mild conditions, we show that

| (1.3) | ||||

where is the convex conjugate of . We note that a recent work by Han (2023) also derives a duality formula for (1.2). We highlight that our dynamic duality not only works under a more general penalized setting (1.1), but also provides a more tractable formula for the dual problem. In Han (2023), the authors rewrite the causality constraint as an infinite-dimensional linear constraint, which is not numerically tractable. Our approach characterizes the causality through the temporal structure of causal couplings and justifies (1.3) under a measure theoretic framework. In spirit, our proof aligns with the proof in Zhang et al. (2022), while we extend the result to a causal transport-type penalization form. The proof can be split into three steps. The first step is to obtain the duality of (1.2) using the argument in Zhang et al. (2022). We then prove a generalized Fenchel–Moreau duality theorem and rewrite (1.1) as a minimax problem. Finally, we apply dynamic programming principle and analytic selection theorem to reduce the inner maximization to a multistep univariate maximization problem.

We apply the dynamic duality formula (1.3) to several applications. We derive the duality for distributionally robust average value-at-risk (AVaR) in Theorem 4.1. A numerical experiment has been implemented for a two-step exotic option to demonstrate the extra risk induced by model uncertainty. Then we discuss a distributionally robust stochastic control problem in which the objective is subject to model uncertainty. Thanks to the causal DRO duality, we rewrite the original problem into a sequence of subproblems which can be solved by the dynamic programming principle. We derive the Bellman equation for the subproblems in Theorem 5.1 and then work out a linear quadratic stochastic control. Finally, we consider a distributionally robust optimal stopping. In this case, duality (1.3) is not directly applicable. Instead, we consider a relaxed optimal stopping problem for the canonical filtered processes introduced in Bartl et al. (2021a). We reformulate causal optimal transport into a series of weak optimal transports in Theorem 6.2. This allows us to derive the duality for the relaxed problem in Theorem 6.3 from the duality of weak optimal transport-type DRO which has its own interest. Furthermore, we deduce in Theorem 6.5 the value of the relaxed problem coincides with the value of the original problem under mild conditions.

In the literature, the static DRO has been extensively studied and applied to numerous fields, such as statistics (Bartl et al., 2021b), machine learning (Bai et al., 2023, Blanchet et al., 2019), mathematical finance (Bartl et al., 2020, Blanchet et al., 2022), etc. We focus on the discussion of the transport-type DRO and refer interested readers to Rahimian and Mehrotra (2019) for DRO under a broader context. There are two main lines of approaches to tackle DRO: duality and sensitivity. In a static setting, duality has been shown at different levels of generality. Mohajerin Esfahani and Kuhn (2018) proved the duality for data-driven DRO where the reference measure is an empirical measure; Gao and Kleywegt (2022) derived the duality for any Borel measure on a Euclidean state space; Blanchet and Murthy (2019) showed the duality for general Polish spaces through an approximation argument; Bartl et al. (2020) established the duality for the penalized form with the help of a functional duality result; Zhang et al. (2022) derived the duality for a class of spaces with interchangeability, including Polish spaces and Suslin spaces; Kupper et al. (2023) showed the duality for a weak optimal transport-type penalization. On the other hand, sensitivity analysis investigates the first order approximation to (1.2). We refer to Bartl et al. (2021b), García Trillos and García Trillos (2022), Nendel and Sgarabottolo (2022) for a static setting, and Bartl and Wiesel (2023), Bartl et al. (2023) for a dynamic setting.

The rest of the paper is organized as follows. In Section 2, we introduce the basic notations and concepts. In Section 3, we present the proof of the main theorem. As applications, we investigate the distributionally robust version of average value-at-risk (AVaR) in Section 4, stochastic control in Section 5, and optimal stopping in Section 6. Finally, we conclude the paper with a discussion on the relaxed DRO and the original DRO in Section 6.

2 Preliminaries

Notations

Let be the number of steps. For any and an -tuple , we denote the truncation by . All filtrations considered are indexed by , and when there is no ambiguity we write without the index set for simplicity.

For a generic Polish space , we always equip it with its Borel -algebra . Let be the space of Borel probability measures on equipped with its weak topology. For any and an integrable function , we use the shorthand notation

Given and a -algebra , we denote the completion of under by .

Let and be two generic Polish spaces. Given and , the set of couplings between and is defined as

We also denote the set of couplings with a fixed first marginal by

Given and a measurable map , we define the pushforward map by

For any , we write

where is the Borel regular disintegration kernel. Throughout this paper, we adopt the convention that the subscript of a probability kernel denotes the variable it integrates out.

Analytic sets and universal measurability

The analytic sets (also known as Suslin sets) are widely applied to reconcile the measurability issue in dynamic programming principle. We give a minimal introduction here to serve our purpose.

Definition 2.1.

Let be a Polish space. We say a subset of is analytic if is a continuous image of a Polish space, and a function is upper semi-analytic if the level set is analytic for any . The universal -algebra of is defined as

To ease the notation, we will not distinguish any Borel measure and its completion. So, for any universally measurable function , is understood as the integration with respect to the completion of .

Proposition 2.1.

Let be an analytic set. Then is universally measurable, and therefore any upper semi-analytic function is universally measurable.

Proposition 2.2.

Let and be Polish spaces and an analytic set. Then the projection is an analytic subset of .

We also recall the following proposition from Bertsekas and Shreve (1996, Proposition 7.50).

Proposition 2.3 (Analytic selection theorem).

Let and be Polish spaces and an analytic set, and an upper semi-analytic function. Define by

where is the fiber of at . Then for any , there exists an analytically measurable function such that the graph and for any ,

The following result is adapted from Zhang et al. (2022).

Lemma 2.4.

Let be a Polish space equipped with its Borel -algebra, upper semi-analytic and bounded from below. Define as

Then is universally measurable; moreover, it holds that

Proof.

Notice that for any we have

Since is upper semi-analytic, we have is also upper semi-analytic by Proposition 2.2. Moreover, by Proposition 2.1, we know is universally measurable. It follows from the definition that

Now, by Proposition 2.3 there exists an analytically measurable function such that

Moreover, there exists a Borel measurable function such that -almost everywhere. Then we take We derive

As , we conclude

∎

Convex analysis

We recall several basic concepts and results in convex analysis.

Definition 2.2.

Let be a convex function. We define the domain of as

We say is proper if , and is closed if is closed. A function is proper closed concave if and only if is proper closed convex.

Definition 2.3.

Let be a convex function. The convex conjugate of is defined as Similarly, we define the concave conjugate of as

Theorem 2.5 (Rockafellar (1970)).

Let be a closed proper convex (concave) function. Then, we have ().

Proposition 2.6 (Subdifferential).

Let be a convex function. For any , we define the subdifferential of at as

If is proper and closed, then if and only if . And we have the equality .

The following lemma generalizes Fenchel–Moreau theorem. We did not find a direct reference for this lemma, so we include a proof here.

Lemma 2.7.

Let be two closed proper convex functions. Then, we have the following minimax theorem

Remark 2.4.

By taking as a linear function, we retrieve the classical Fenchel–Moreau theorem .

Proof.

By definition, we have

For the other direction, we know

Without loss of generality, we take satisfying and . Otherwise, we have and are monotone and bounded from below, and thus

By the characterization of subdifferential, we have

and

Therefore, we derive

∎

Causal optimal transport

Causal transport is an analogy of the classical transport problem in a dynamic context with the constraint that the transport plan is conditionally independent of the future given the current information. Such a constraint leads to a finer ambiguity set than that of the classical optimal transport and can capture the temporal structure between random processes.

From now on, we refer to as the canonical path space of -step random processes. Let be polish spaces and be the canonical filtered space of -step stochastic processes with paths in where equipped with its Borel -algebra , the canonical filtration, and the coordinate process. We follow the general causal optimal transport framework introduced by Lassalle (2018), Acciaio et al. (2020). Let be a copy of .

Definition 2.5 (Acciaio et al. (2020)).

Given and , we say a coupling is causal from to if for any and

| (2.1) |

is –measurable. We denote the set of causal couplings from to by .

Remark 2.6.

Noticeably, Lassalle (2018) has a slightly different definition of the causal coupling by assuming

is –measurable for any with . Under this definition, we can show is compact under the weak topology. Lassalle proposed a ‘regular’ filtration condition under which two different notions of causality coincide. All the cases of our interest, e.g., the path space equipped with the canonical filtration, are covered by this ‘regular’ filtration condition. We encourage readers to read Lassalle (2018, Lemma 4) for a detailed discussion.

The motivation behind the above definition is that we assume a causal transport plan is generated by a Monge map through . Then is non-anticipative (adapted) in the sense that

It implies that under a causal coupling , given the past of , the past of does not depend on the future of .

Given a nonnegative Borel cost function , we define the causal optimal transport problem as

| (2.2) |

Similarly, we define the bicausal optimal transport problem as

where .

The following proposition shows a dynamic temporal structure of causal couplings.

Proposition 2.8 (Backhoff-Veraguas et al. (2020c)).

The following statements are equivalent:

-

•

is a causal coupling with the first marginal .

-

•

Decomposing in terms of successive regular kernels

then for any and -almost surely , we have

3 Main results

Assumption 3.1.

We assume that is a Borel probability measure, is a nondecreasing closed proper convex function with and , is lower semi-analytic and non-negative with if and only if , is upper semi-analytic and -integrable with for some constant and .

Lemma 3.1.

Under Assumption 3.1, we have closed, proper and concave.

Proof.

The concavity of follows directly from the convexity of the causal couplings . By Assumption 3.1, we know is finite for any , which implies is proper. Consequently, is continuous on the closed set , and hence it is also closed. ∎

Theorem 3.2.

Under Assumption 3.1, we have

| (3.1) |

where is convex conjugate of and is the convex expectation

Moreover, we have the dynamic duality formulation

| (3.2) |

Remark 3.1.

Let be a convex subset of and . We assume is a concave function satisfying for any . Under Assumption 3.1, we have

Remark 3.2.

Proof.

Step 1. We first show the result when . Recall we write

Notice that is closed, proper and concave, and we calculate the concave conjugate of as

By Fenchel–Moreau theorem, we have

Step 2. We notice

On the other hand, since is nondecreasing, we have for any

Hence, we derive . Plugging the result from Step 1, we get

The last equality follows from Lemma 2.7 and the fact that

is proper closed convex.

Step 3. To show (3.2), we first show the following quantities are well-defined:

and for

We claim is upper semi-analytic. We notice

is Borel, and

is upper semi-analytic by Bertsekas and Shreve (1996, Proposition 7.48). By Bertsekas and Shreve (1996, Proposition 7.47), we have is upper semi-analytic. Therefore, is universally measurable and this implies is well-defined. Recursively, we can show is upper semi-analytic for any . By Proposition 2.8, we decompose the optimization problem (3.2) into single step problems as

Under stronger regularity assumptions, we can show the values of DRO under the causal ambiguity and the bicausal ambiguity agree. The strong duality again holds for the bicausal setting even though the set of bicausal couplings with a fixed first marginal is not convex. Such a result has been shown in Bartl and Wiesel (2023) for the standard DRO problem by approximating a causal coupling by a sequence of bicausal couplings with similar marginals.

Corollary 3.3.

Let and suppose Assumption 3.1 holds. We further assume that are continuous and there exist constants , and such that

and

Then we have

Moreover, the same duality holds if we replace the causal transport cost by the bicausal transport cost, i.e.,

Proof.

Let with and . We write which is again causal. By Bartl and Wiesel (2023, Lemma 3.1), for any there exists a bicausal coupling and measurable such that , . By Lebesgue dominated convergence theorem and the regularity condition of , we can take sufficiently small such that

and . Then we have

This implies

Since is arbitrary, we have

The other direction is trivial.

For the strong duality, with the same construction of as above, we can show

Therefore, the strong duality of bicausal case follows directly from the one of causal case. ∎

4 Distributionally robust AVaR

Let be a path-dependent payoff of a contingent claim and . Recall average value-at-risk is given by

We are interested in its distributionally robust counterpart defined by

It is direct to show is again a convex risk measure but not coherent in general. We derive the following dual representation of .

Theorem 4.1.

Let Assumption 3.1 hold. We further assume that is nonnegative and upper semi-continuous, and is lower semi-continuous. Then, we have

Proof.

By DRO duality Remark 3.1, it is direct to show

Now, we show that we can swap the inner and . We fix and consider the case

| (4.1) |

Then we notice

This implies

On the other hand, we take such that goes to infinity. We write and define

By definition is again causal. We further notice

In the last inequality we take . Therefore, we deduce

The second case is that

| (4.2) |

We write

Since , it follows from Fan (1953, Theorem 2) that

Let such that

Since the support of any probability measure on a Polish space is -compact, we may assume is -compact for simplicity. In particular, , where is ascending and compact. We write and . Without loss of generality, we assume

We fix , and define . We take

— it follows from the fact that is causal. Then we derive

On the other hand, is compact under the weak topology, see Lassalle (2018, Theorem 3 (i)). Therefore, we have

Since is arbitrary, we conclude the proof. ∎

Example 4.1.

We consider a two-step exotic option. Let be the underlying asset, the payoff of the option. We set interest rates and dividends to zero for simplicity. Let be a reference pricing measure of the underlying. In this example we assume is the finite marginal of a geometric Brownian motion given by

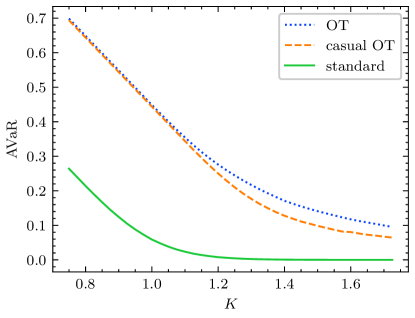

In our numerical experiments, we utilize the dual formulation and take , , , , and . In Figure 4.1, we plot the robust AVaR of the option under a classical transport-type penalization (dotted), a causal transport-type penalization (dashed), and standard AVaR (solid). The gap between the blue and the orange curves corresponds to the reduced risk by considering a non-anticipative perturbation of the reference model.

We emphasize that, in some cases, there is no reduced risk when restricting to a non-anticipative perturbation, for example a calendar spread with any separable cost .

Remark 4.1.

We can also consider robust risk-indifference pricing (Xu, 2006) under model uncertainty. For simplicity, we assume zero initial capital and liability. The robust risk-indifference (sell) price is the minimum price a trader will charge so that the total risk of their portfolio will not increase. It is given by

where is the set of all predictable hedging strategies and is the discrete stochastic integral. By Theorem 4.1, we write

As goes to 0, it is known that the risk-indifference price under converges to the superhedging price. Under the current context, the robust superhedging price is given by

We stress that this is a nondominated framework and is orthogonal to the setting in Bouchard and Nutz (2015). Indeed, we consider all possible reference measure with penalization , whereas in Bouchard and Nutz (2015) authors considered a collection of measures which is stable under the concatenation of kernels. When is compact and is continuous, we can write down pricing–hedging duality as

where denotes the set of martingale measures on . It is unclear if this holds under a more general setting, and we leave it for future work.

5 Distributionally robust stochastic control

Throughout this section, we assume . We set up the framework of distributionally robust stochastic control problems. Let be a probability space, , , Polish spaces, and a random variable with law . Let , , be Borel measurable. We consider the non-Markovian feedback controlled system

with the aim of minimizing

where is a noise independent of taking value in for , and is the set of admissible controls given by

Equivalently, with we can rewrite the objective functional as

| (5.1) |

The objective can be split into two parts: one corresponding to the cost incurred by implementing the control, and the other representing the cost of the system coming from observations. We now consider a case in which precise control on the system is achievable while the observation of the system might be subject to inaccuracies. Mathematically, we are interested in the distributionally robust stochastic control problem:

| (5.2) |

Before the discussion of the robust control problem, we take a short detour to the classical stochastic control problem. By , we denote the law of the conditioned system under control

We define cost-to-go functions by

Under mild conditions, the classical dynamic programming principle yields the following Bellman equation

Then one can solve the Bellman equation by backward induction and find the optimal control (if exists) by

However, such a dynamic programming in general does not hold for the distributionally robust control problem (5.2). The reason is that the distributionally robust control problem has a penalization term which is not compatible with the dynamic programming principle. Even in the case of , the set is not stable under the concatenation of the condition probability kernels. This time inconsistency has been discovered in the context of risk averse multistage stochastic programming Shapiro (2012).

We now utilize the duality formulation and propose a feasible algorithm to solve the robust stochastic control problem (5.2). By duality, we write

Once we obtain , the outside minimization over reduces to a univariate convex optimization, and hence it is efficient to find the minimizer . Moreover, the (sub)optimal control associated with becomes a (sub)optimal control for the original distributionally robust control problem (5.2). Notably, to obtain the robust objective under different penalties, we only need to redo the external univariate convex optimization. Thus, we shift focus to the inner optimization problem and show that it can be effectively solved by dynamic programming. The original time-inconsistent problem is reformulated into a sequence of time-consistent ones. In analogy to the classical case, we define the cost-to-go function as

Theorem 5.1.

We assume , are bounded from below. Let cost-to-go function be defined as above. We write . Then, we can derive from the Bellman equation

| (5.3) |

and . Furthermore, there exists an -optimal control for any satisfying

Proof.

We notice

Therefore, is a classical time-consistent stochastic control problem. By Bertsekas and Shreve (1996, Propositions 8.2 and 8.3), we conclude the proof. ∎

Remark 5.1.

An alternative robust formulation involves considering the misspecification of the cost generated by control, i.e.,

Although it is not covered in the current setup, it can, in some cases, be solved via the same duality result. We have chosen our formulation to provide a simple and clear presentation of how to link the duality and the dynamic programming principle.

Example 5.1.

We consider a finite horizon 1D linear quadratic stochastic control. Let follow

with the aim of minimizing

where are i.i.d. standard normal random variables.

We take and . From the above discussion, we derive

The inner control problem is again a stochastic linear quadratic problem which can be directly solved by a difference Riccati equation.

6 Distributionally robust optimal stopping

In this section, we investigate the distributionally robust optimal stopping problem

| (6.1) |

where is the set of –stopping times and for . We point out that

fails to be concave in general. Hence, Theorem 3.2 is not directly applicable here. We will circumvent this issue and regain concavity by relaxing the problem to a general filtered process setting.

Before we proceed, we first give a concrete example which will shed some light on the relaxation of causal DRO. Take , , and . It is direct to check

To reconcile this, we relax the optimal stopping problem by considering richer filtrations. Heuristically, we can realize a process with law by tossing a fair coin at the first step and then follow the process with law or depending on the outcome of the coin. The value of the optimal stopping problem is exactly , if the admissible stopping time is with respect to the natural filtration augmented by the coin toss. On the other hand, if the admissible stopping time is with respect to the natural filtration, then the value is again . We stress that the value of the optimal stopping problem is not only determined by the law of the process but also the information flow, i.e., the filtration. In order to take all possible filtrations into account, we have to enlarge the canonical path space.

Canonical filtered process space

We formally introduce filtered processes and the canonical filtered space following Bartl et al. (2021a). A filtered process is a 5-tuple , where is –adapted. To prevent confusion between the associated law of and the law of , we call the filtered law of . The set of filtered processes is denoted by . We extend the definition of causality to processes equipped with general filtrations.

Definition 6.1.

Given , we say a coupling is causal from to if for any and

is –measurable. With a slight abuse of notation, we denote the set of causal couplings from to by . The associated causal optimal transport problem is defined as

While such a weak formulation encompasses all possible filtered processes of interest, it lacks a linear structure, and in particular, there is no convex structure on . To this end, the canonical filtered space introduced in Bartl et al. (2021a) serves as a natural ambient space to encode all the information of a filtered process.

Definition 6.2.

We recursively define and for

The canonical filtered space is the tuple , where , , and is the projection map. There is a natural embedding from to . We will not distinguish and as a subspace of .

Definition 6.3.

For a given filtered process , the associated information process is given recursively by and

We define a relation ‘’ on by

The canonical representation of is given by , where . Indeed, one can show .

The following proposition shows that it suffices to consider the canonical filtered processes.

Proposition 6.1.

For any , we have

-

•

if and only if .

-

•

and .

-

•

There exists universally measurable such that

where is the set of –stopping times and is the set of –stopping times.

Proof.

In the sequel, we assume any filtered process is chosen as its canonical representation. Let be a copy of the canonical filtered space, and by we denote the filtered law of respectively. With a slight abuse of notation, we denote the set of the filtered laws of canonical filtered processes by

equipped with the weak topology as a subset of .

As a preparation for the duality of relaxed causal DRO, we present a new dynamic programming principle for causal optimal transport between filtered processes.

Theorem 6.2.

We assume is lower semi-analytic, bounded from below, and semi-separable, i.e., . We recursively define . Let , and for

Here, is the ‘expectation’ of with law . Then, we can rewrite the causal optimal transport problem as a weak optimal transport problem

where . In particular, and are convex in the first argument and jointly lower semi-analytic. Furthermore, if is compact and is lower semi-continuous, then is lower semi-continuous.

Remark 6.4.

The above extends the dynamic programming principle in Backhoff-Veraguas et al. (2017, Theorem 4.2) to general filtered processes. Notably, we do not require the source process to be Markovian.

Proof.

The measurability part follows from similar arguments in Backhoff-Veraguas et al. (2017, Theorem 4.2). For brevity, we skip the discussion and assume the well-posedness of all integrations appearing in the proof.

Let . We write as the disintegration kernel

Similar to Bartl et al. (2021a, Lemma A.1), we have is causal if and only if it has successive disintegration kernels

satisfying for any and -almost surely

Therefore, for any causal coupling we have and for

On the other hand, we write

For any , we construct

It is direct to check such belongs to . Hence, we construct a bijection between and . This implies

The lower semi-continuity of follows from the compactness of and the lower semi-continuity of by Bertsekas and Shreve (1996, Proposition 7.33). ∎

Relaxed causal DRO

We focus on the relaxed distributionally robust optimal stopping

| (6.2) |

or more generally the relaxed causal DRO

Assumption 6.1.

We assume that , is a nondecreasing closed proper convex function with and , is lower semi-analytic and non-negative with if and only if , and is universally measurable with for some constant and any with filtered law .

Theorem 6.3.

Remark 6.5.

As mentioned in Backhoff-Veraguas et al. (2017), we do not expect the semi-separability assumption on can be relaxed. It is because (6.4) relies on a recursive formulation of the causal optimal transport problem which reduces the causal optimal transport to a weak optimal transport problem. A general cost does not admit such a reformulation.

Remark 6.6.

We assume the compactness of in (6.5) to satisfy the conditions for the minimax theorem of Fan (1953). We remark that, even without the compactness assumption, is lower semi-continuous if is separable and lower semi-continuous. However, it remains open if the duality holds without the compactness assumption on .

Proof.

Since is convex, by Remark 3.1 we derive (6.3). We highlight the fundamental distinct between and as derived in (3.2). The difference arises from the constraint on the second marginal of the coupling. To show (6.4), we utilize a weak optimal transport reformulation for causal optimal transport. By Theorem 6.2 there exists such that

Now, we assume the canonical filtered space is compact, is upper semi-continuous, and is lower semi-continuous. As pointed out in Backhoff-Veraguas et al. (2019), we can embed coupling into a nested space by

This yields

On the other hand, is convex by Theorem 6.2. Hence, for any with we have

Hence, we obtain

Since is lower semi-continuous and is compact, we derive is lower-semi continuous from Theorem 6.2. This implies

is concave and upper semi-continuous in and convex in . Combing this with the fact that is compact, we apply Fan (1953, Theorem 2) and obtain

∎

We also consider the relaxed problem under a bicausal transport penalization.

Theorem 6.4.

Proof.

Following the proof of Theorem 3.2, to show (6.6) it suffices to show the convexity of the bicausal cost . As mentioned above, is not a convex set. Hence, the convexity of does not follow from the same line of argument as the causal case. Instead, we reformulate the bicausal optimal transport problem as a classical optimal transport problem which has been shown in Bartl et al. (2021a, Theorem 3.10). We adapt their result to the current setting. Define , and for

Then, we obtain

This implies the convexity of . The rest of the proof is a direct application of Theorem 3.2 in the static setting. ∎

Further discussion on plain processes

It is obvious that the value of (6.1) is not greater than the value of (6.2). We are interested in the case when the two values agree. To this end, by we denote the set of plain processes defined as

For simplicity, we denote the set of the filtered laws of canonical plain processes by .

Theorem 6.5.

Suppose that Assumption 6.1 holds. We further assume that has no isolated points, and , are continuous and bounded. Then, the value of the relaxed problem agrees with the value of the original problem, i.e.,

and

Proof.

Since has no isolated points, Bartl et al. (2021a, Theorem 5.5) implies is dense in . Moreover, since is continuous and bounded, Eckstein and Pammer (2022, Theorem 3.6) implies and are continuous. Hence, for any there exists such that , , and . This concludes the proof.

∎

Corollary 6.6.

Let and be continuous and bounded for . We further assume that has no isolated points. Let be a plain filtered process with law . Then, we have

and

Proof.

Define recursively , for

By Snell envelope theorem, we have

We prove are continuous and bounded by induction. It suffices to show is continuous which follows directly from Prokhorov’s theorem. By Theorem 6.5, we conclude the proof. ∎

Remark 6.7.

In particular, if we take , then is an optimal stopping time and

Hence, we can equip any filtered process with the richest filtration while keeping the same value of the optimal stopping. This implies the value of the relaxed causal problem agrees with the value of the relaxed bicausal problem. Combing this with the above corollary, we conclude the value of the original causal problem agrees with the value of the original bicausal problem. This extends Corollary 3.3 to abstract polish spaces.

Acknowledgement

The author would like to thank Prof. Jan Obłój and Fang Rui Lim for their support and insightful discussions. The author acknowledges support by the EPSRC Centre for Doctoral Training in Mathematics of Random Systems: Analysis, Modelling, and Simulation (EP/S023925/1).

References

- Acciaio et al. (2020) B. Acciaio, J. Backhoff-Veraguas, and A. Zalashko. Causal optimal transport and its links to enlargement of filtrations and continuous-time stochastic optimization. Stochastic Processes and their Applications, 130(5):2918–2953, May 2020.

- Aldous (1981) D. Aldous. Weak convergence and the general theory of processes. Incomplete draft of monograph, July 1981.

- Backhoff-Veraguas et al. (2017) J. Backhoff-Veraguas, M. Beiglböck, Y. Lin, and A. Zalashko. Causal transport in discrete time and applications. SIAM J. Optim., 27(4):2528–2562, Jan. 2017.

- Backhoff-Veraguas et al. (2019) J. Backhoff-Veraguas, M. Beiglböck, and G. Pammer. Existence, duality, and cyclical monotonicity for weak transport costs. Calculus of Variations and Partial Differential Equations, 58(6):203, 2019.

- Backhoff-Veraguas et al. (2020a) J. Backhoff-Veraguas, D. Bartl, M. Beiglböck, and M. Eder. Adapted Wasserstein distances and stability in mathematical finance. Finance Stoch, 24(3):601–632, July 2020a.

- Backhoff-Veraguas et al. (2020b) J. Backhoff-Veraguas, D. Bartl, M. Beiglböck, and M. Eder. All adapted topologies are equal. Probab. Theory Relat. Fields, 178(3-4):1125–1172, Dec. 2020b.

- Backhoff-Veraguas et al. (2020c) J. Backhoff-Veraguas, M. Beiglböck, M. Eder, and A. Pichler. Fundamental properties of process distances. Stochastic Processes and their Applications, 130(9):5575–5591, Sept. 2020c.

- Backhoff-Veraguas et al. (2022) J. Backhoff-Veraguas, S. Källblad, and B. A. Robinson. Adapted Wasserstein distance between the laws of SDEs, Sept. 2022. arXiv:2209.03243.

- Bai et al. (2023) X. Bai, G. He, Y. Jiang, and J. Obłój. Wasserstein distributional robustness of neural networks. In Advances in Neural Information Processing Systems. Curran Associates, Inc., Dec. 2023.

- Bartl and Wiesel (2023) D. Bartl and J. Wiesel. Sensitivity of multi-period optimization problems in adapted Wasserstein distance, Aug. 2023. SIAM J. Financial Math. (forthcoming).

- Bartl et al. (2020) D. Bartl, S. Drapeau, and L. Tangpi. Computational aspects of robust optimized certainty equivalents and option pricing. Mathematical Finance, 30(1):287–309, 2020.

- Bartl et al. (2021a) D. Bartl, M. Beiglböck, and G. Pammer. The Wasserstein space of stochastic processes, Apr. 2021a. arXiv:2104.14245.

- Bartl et al. (2021b) D. Bartl, S. Drapeau, J. Obłój, and J. Wiesel. Sensitivity analysis of Wasserstein distributionally robust optimization problems. Proc. R. Soc. A., 477(2256):20210176, Dec. 2021b.

- Bartl et al. (2023) D. Bartl, A. Neufeld, and K. Park. Sensitivity of robust optimization problems under drift and volatility uncertainty, 2023. arXiv:2311.11248.

- Bertsekas and Shreve (1996) D. Bertsekas and S. E. Shreve. Stochastic Optimal Control: The Discrete-Time Case. Athena Scientific, Dec. 1996.

- Bion–Nadal and Talay (2019) J. Bion–Nadal and D. Talay. On a Wasserstein-type distance between solutions to stochastic differential equations. Ann. Appl. Probab., 29(3), June 2019.

- Blanchet and Murthy (2019) J. Blanchet and K. Murthy. Quantifying distributional model risk via optimal transport. Mathematics of OR, 44(2):565–600, May 2019.

- Blanchet et al. (2019) J. Blanchet, Y. Kang, and K. Murthy. Robust wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857, 2019.

- Blanchet et al. (2022) J. Blanchet, L. Chen, and X. Y. Zhou. Distributionally robust mean-variance portfolio selection with wasserstein distances. Management Science, 68(9):6382–6410, 2022.

- Bouchard and Nutz (2015) B. Bouchard and M. Nutz. Arbitrage and duality in nondominated discrete-time models. The Annals of Applied Probability, 25(2):823–859, Apr. 2015.

- Eckstein and Pammer (2022) S. Eckstein and G. Pammer. Computational methods for adapted optimal transport, Mar. 2022. arXiv:2203.05005.

- Fan (1953) K. Fan. Minimax theorems. Proceedings of the National Academy of Sciences, 39(1):42–47, Jan. 1953.

- Föllmer and Schied (2008) H. Föllmer and A. Schied. Stochastic Finance: An Introduction in Discrete Time. In Stochastic Finance. De Gruyter, Dec. 2008.

- Gao and Kleywegt (2022) R. Gao and A. Kleywegt. Distributionally robust stochastic optimization with wasserstein distance. Mathematics of OR, Aug. 2022.

- García Trillos and García Trillos (2022) C. A. García Trillos and N. García Trillos. On the regularized risk of distributionally robust learning over deep neural networks. Res Math Sci, 9(3):54, Aug. 2022.

- Han (2023) B. Han. Distributionally robust risk evaluation with a causality constraint and structural information, Apr. 2023. arXiv:2203.10571.

- Hellwig (1996) M. F. Hellwig. Sequential decisions under uncertainty and the maximum theorem. Journal of Mathematical Economics, 25(4):443–464, Jan. 1996.

- Knight (1921) F. H. Knight. Risk, Uncertainty and Profit. Boston, New York, Houghton Mifflin Company, 1921.

- Kupper et al. (2023) M. Kupper, M. Nendel, and A. Sgarabottolo. Risk measures based on weak optimal transport, Dec. 2023. arXiv:2312.05973.

- Lassalle (2018) R. Lassalle. Causal transport plans and their Monge–Kantorovich problems. Stochastic Analysis and Applications, 36(3):452–484, May 2018.

- Lott and Villani (2009) J. Lott and C. Villani. Ricci curvature for metric-measure spaces via optimal transport. Annals of Mathematics, 169(3):903–991, 2009.

- Mohajerin Esfahani and Kuhn (2018) P. Mohajerin Esfahani and D. Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Math. Program., 171(1):115–166, Sept. 2018.

- Nendel and Sgarabottolo (2022) M. Nendel and A. Sgarabottolo. A parametric approach to the estimation of convex risk functionals based on Wasserstein distance, Oct. 2022. arXiv:2210.14340.

- Pammer (2022) G. Pammer. A note on the adapted weak topology in discrete time, May 2022. arXiv:2205.00989.

- Peng (2019) S. Peng. Nonlinear Expectations and Stochastic Calculus under Uncertainty: With Robust CLT and G-Brownian Motion, volume 95 of Probability Theory and Stochastic Modelling. Springer, 2019.

- Pflug (2010) G. C. Pflug. Version-independence and nested distributions in multistage stochastic optimization. SIAM J. Optim., 20(3):1406–1420, Jan. 2010.

- Pflug and Pichler (2012) G. C. Pflug and A. Pichler. A distance for multistage stochastic optimization models. SIAM J. Optim., 22(1):1–23, Jan. 2012.

- Rahimian and Mehrotra (2019) H. Rahimian and S. Mehrotra. Distributionally robust optimization: A review, Aug. 2019. arXiv:1908.05659.

- Rockafellar (1970) R. T. Rockafellar. Convex Analysis. Princeton University Press, Princeton, 1970.

- Rüschendorf (1985) L. Rüschendorf. The Wasserstein distance and approximation theorems. Z. Wahrscheinlichkeitstheorie verw Gebiete, 70(1):117–129, Mar. 1985.

- Shapiro (2012) A. Shapiro. Minimax and risk averse multistage stochastic programming. European Journal of Operational Research, 219(3):719–726, June 2012.

- Xu (2006) M. Xu. Risk measure pricing and hedging in incomplete markets. Annals of Finance, 2(1):51–71, Jan. 2006.

- Yamada and Watanabe (1971) T. Yamada and S. Watanabe. On the uniqueness of solutions of stochastic differential equations. Journal of Mathematics of Kyoto University, 11(1):155–167, Jan. 1971.

- Zhang et al. (2022) L. Zhang, J. Yang, and R. Gao. A simple and general duality proof for wasserstein distributionally robust optimization, Oct. 2022. arXiv:2205.00362.