A Nonparametric Bayes Approach to Online Activity Prediction

Abstract

Accurately predicting the onset of specific activities within defined timeframes holds significant importance in several applied contexts. In particular, accurate prediction of the number of future users that will be exposed to an intervention is an important piece of information for experimenters running online experiments (A/B tests). In this work, we propose a novel approach to predict the number of users that will be active in a given time period, as well as the temporal trajectory needed to attain a desired user participation threshold. We model user activity using a Bayesian nonparametric approach which allows us to capture the underlying heterogeneity in user engagement. We derive closed-form expressions for the number of new users expected in a given period, and a simple Monte Carlo algorithm targeting the posterior distribution of the number of days needed to attain a desired number of users; the latter is important for experimental planning. We illustrate the performance of our approach via several experiments on synthetic and real world data, in which we show that our novel method outperforms existing competitors.

1 Introduction

In the context of modern digital interactions, the ability to forecast the initiation of specific activities within a given time-frame holds immense significance. Examples include the number of users who will install a software update, the number of customers who will use a new feature on a website or who will participate in an A/B test. Whether the focus is on estimating the number of individuals initiating an action or predicting the temporal span needed to attain a desired user participation threshold, accurate predictive models play a central role in decision making, resource allocation, and enhancing user experiences. See, e.g., Kohavi et al. (2007) and Bakshy et al. (2014) for further details on online experiments.

While participation data can be formally treated as a time series, the problem of forecasting user participation does not lend itself to time series models (see Richardson et al., 2022, and the references therein). Moreover, intricate dynamics that underlie user engagement patterns. Conventional models often assume that initiation times are identically distributed, ignoring the diverse behaviors and preferences exhibited by individuals. In reality, users demonstrate varying propensities to engage, leading to a multitude of initiation timelines. Recognizing this complexity, Richardson et al. (2022) recently proposed a Bayesian model for the users’ initiation times, which allows different behaviors to be captured, while simultaneously borrowing strength as is typical in hierarchical Bayesian models.

In this work, we extend the framework of Richardson et al. (2022) by proposing a nonparametric Bayesian model for user activity. Contrary to classical (frequentist) nonparametric statistics, in Bayesian nonparametrics (BNP), we still assume a likelihood function belonging to a parametric family, but let the size of the parameters involved in the model be either infinite or increasing with the sample size. Within the context of user prediction, parameters represent the users’ propensity to engage; in this work, we let the pool of potential users be unbounded. However, in any finite period, the number of active users is bounded almost surely (a.s.). Therefore, contrary to Richardson et al. (2022), we do not fix the population size in advance. Beyond the mathematical elegance, this allows us to sidestep the necessity of estimating a key model parameter, either by cross-validation or based on historical data, thus reducing the modeling and computational burden. We study two models: the first one assumes we are given data representing daily activity for each user, while the second assumes that we are provided with the time at which each user is first included in the trial, also called the “first triggering time”. We provide a unified treatment of these two models under the generalized Indian buffet framework of James (2017).

The central contribution of this paper is to use a scaled process (James et al., 2015; Camerlenghi et al., 2022; Beraha and Favaro, 2023) as the prior for the infinite-dimensional parameter involved in the models. Compared to the completely random measure (CRM) priors that have been traditionally employed (Thibaux and Jordan, 2007; Titsias, 2007; Broderick et al., 2014; James, 2017; Masoero et al., 2022), scaled processes offer a richer predictive structure that is well-suited to the problem of activity forecasting. See Section 2.1 for further discussion on the unsuitability of CRMs for forecasting tasks. In particular, we employ the stable Beta-scaled process (Camerlenghi et al., 2022) that offers a sensible trade-off between analytical tractability and richness of the predictive distribution. For the two models under examination, we provide closed-form expression for the posterior distribution of the parameters, as well as the distribution of the number of new users that will be active in a subsequent period of days, . To estimate how many experimental days are needed to reach the desired number of users, we consider two approaches. The first is based on the posterior distribution of such an event, which we show can be computationally burdensome in some cases. The second is a heuristic approach that aims at “inverting” prediction intervals for . This requires building a global (as opposed to pointwise) prediction interval for which we do by exploiting the compound Poisson representation of generalized Indian buffet processes given in James (2017).

Our models are benchmarked on two simulation studies. Moreover, we rank the predictive performance of our models, as well as several other competitors, on 210 real world online experiments that ran on a global e-commerce platform. Our models greatly outperform competitors, ranking first more than twice as often of Richardson et al. (2022).

2 Two BNP Models for Activity Prediction

We present here two models for activity prediction. The first is applicable when data consists of the daily activity of users, that is, if the -th user is active on the -th day and otherwise. We assume that the total possible number of users is infinite, but within any given timespan only a finite number of users are active. In this case, a useful mathematical abstraction is to represent each observation , as a counting measure:

| (1) |

where is the Dirac measure . The measure is supported on an infinite sequence , which can be thought of as the collection of “user-specific labels” (e.g., anonymized user IDs) that play no other role in the subsequent analysis and simply satisfy for .

The second model is useful when the data consists of only the first triggering time for active users, i.e., such that if user is active for the first time on the -th day, and if user is never active in the first days. Also in this case we assume that the potential number of users is a priori infinite, but for any timespan only a finite number of users satisfy and the remaining ones are not detected, i.e., . Again, it is useful to represent the data as a counting measure

| (2) |

We present a unified analysis of both models under the framework of trait allocations (see, e.g., James, 2017; Campbell et al., 2018, and the references therein). In a trait allocation model, each sampling unit displays different traits together with a corresponding level of association. In our setting, the sampling unit is either the day of observation in (1) or directly the entire observation period in (2), with different traits corresponding to unique users, indexed by the user-specific labels. The levels of association are either the indicator that the -th user is active on the -th day ( in (1)) or the first time the –th user is active since the start of the observation period ( in (2)). We emphasize that compared to typical situations where trait allocation models have been considered (see, e.g., James, 2017; Masoero et al., 2022, and the references therein) here we are “flipping” the notion of sampling unit and trait. Indeed, usually the sampling unit corresponds to a user or subject (for instance, taking part in a genomic study) and the trait corresponds to characteristics of the individual (e.g., presence of a genomic variant).

In a trait allocation model, it is assumed that the weights of the random measures representing the data (i.e., the ’s in (1) or the ’s in (2)) follow a common distribution and are further independent given a user-specific parameter , . User-specific parameters and user-specific labels are collected in a measure which is the “only” (nonparametric) parameter in the model and upon which a prior is placed. For notation’s sake, we shall use when referring to the general construction of a trait allocation, when referring specifically to the case of valued weights as in (1) and when the weights take values in as in (2). We will use the notation to denote the conditional law of a trait allocation model.

2.1 Completely Random Measure Priors and their limitations

Completely random measures (CRMs, Kingman, 1975) are the most widely used priors for . An a.s. discrete CRM over is a random measure of the kind such that are the points of a Poisson point process on . It is often assumed that the CRM is homogeneous, i.e., the weights are independent from the atom’s locations and further that , for a (typically diffuse) measure on . In this case, the law of the CRM is specified by its Lévy measure , which is a measure on of the kind where and is the Lévy density. Note that the measure governs only the user-specific labels , and is therefore irrelevant in practice as long as it is diffuse, which ensures that different users are assigned different labels with probability one. Therefore, for simplicity, we will fix to the uniform measure on in the rest of the paper.

In the context of binary observations, notable examples of CRM priors include the Beta process (Hjort, 1990; Thibaux and Jordan, 2007), for which , and the three-parameter (stable) Beta process (Teh and Gorur, 2009) that corresponds to . In the context of integer valued observations, in addition to the Beta process (Heaukulani and Roy, 2016), the Gamma process (i.e., ) and generalized Gamma process have been considered in Titsias (2007) and James (2017). Note that in all the aforementioned processes, so that, almost surely, the CRM has a countable number of support points. In our terminology, this means that the total population of potential users is infinite. At the same time, we also have that for any , . This entails that, in any finite period, we observe a finite number of users with probability one. However, as we allow for longer observation periods, we expect an ever increasing number of active users, diverging to in the infinite-time limit. This is a distinctive feature of Bayesian nonparametric models.

CRM priors offer a great degree of analytical tractability, resulting in a tractable posterior, marginal, and predictive representations for any distribution and prior choice. See James (2017); Broderick et al. (2018) for a detailed account. This enables straightforward estimation of the hyperparameters of the prior via empirical Bayesian procedures (see, e.g., Masoero et al., 2022). However, a fundamental drawback of CRM priors is that they induce a predictive distribution such that the probability of discovering “new users” depends only on the cardinality of the observed samples (i.e., the number of days ). This could be a questionable oversimplification, possibly resulting in poor predictive performance (Camerlenghi et al., 2022), and motivates the study of different prior distributions not based on CRMs. In particular, we advocate for adopting a scaled process as prior for , showing that this choice results in richer predictive distributions while maintaining a high degree of analytical tractability.

2.2 The Stable Beta-Scaled Process Prior

To enrich the predictive distribution of CRM priors, Camerlenghi et al. (2022) proposed the so-called scaled processes (James et al., 2015) as priors for in the context of – valued data. See also Beraha and Favaro (2023) for an extension to the trait allocation setting. In particular, in both papers it is shown how scaled processes derived from the -stable subordinator (Kingman, 1975) provide a reasonable trade-off between analytical tractability and the “richness” of the predictive distribution. We recall their construction next.

First, consider an -stable random measure . That is, is a CRM with Lévy intensity for . Denote by the decreasingly ordered random jumps of . Following Ferguson and Klass (1972) has density , i.e., . Denote by the conditional distribution of given . Then, a scaled process is obtained by marginalizing from the latter distribution. As noted in James et al. (2015), we can gain in flexibility by changing the law of , i.e., marginalizing with respect to for any distribution supported on the non-negative reals. The stable beta-scaled process is obtained by a suitable choice of described below.

Definition 1.

A stable beta-scaled process (SB-SP) prior is a random measure where and is distributed as where

for , , and . We will use the notation .

2.3 Bayesian analysis under the SB-SP Prior

In this section, we consider the following two models:

| (3) |

where the ’s () are random counting measures as in (1), and

| (4) |

where is as in (2) and denotes a discrete distribution over such that

In particular, if , is a truncated geometric distribution that puts to zero all values of greater than .

The two fundamental quantities that we study are the marginal distribution of the data and the posterior distribution of the random measure . Indeed, having a tractable marginal likelihood allows us to adopt an empirical Bayesian strategy to tune the parameters of the prior in Definition 1. The posterior representation of , instead, allows us to develop a conceptually simple Monte Carlo algorithm (and not Markov chain Monte Carlo) to address the activity prediction problem. Below, we derive closed-form analytical expressions for both quantities of interest. These are obtained by specializing the results of Camerlenghi et al. (2022) and Beraha and Favaro (2023).

Theorem 1.

Let be distributed according to (3). Denote by the observed user-specific labels, and let . Then, the marginal distribution of is

where is the beta function and . Moreover, the posterior distribution of coincides with the law of the random measure

| (5) |

such that, given ,

-

•

. In particular, the ’s do not depend on .

-

•

is a completely random measure with Lévy intensity

(6)

In particular, note that the posterior distribution of decomposes as the sum of two parts: the first is a finite measure supported over the previously seen users, while the second is a random measure of the form . Since all the atoms (i.e., user-specific labels) are drawn from a non-atomic probability measure , for any and . That is, is concerned only with the potentially new users that were not active in the first days.

Theorem 2.

Let follow model (4) with the distribution. Denote by the observed user-specific labels. Then the marginal distribution of is

where is as in Theorem 1. Moreover, the posterior distribution of coincides with the law of the random measure

| (7) |

such that, given ,

-

•

,

-

•

is a completely random measure with Lévy intensity as in (6).

3 Activity Prediction

We consider here two related problems: the first one consists in determining the follow-up timespan needed to reach at least active users, while in the second one we aim predicting the number of new users in a (fixed) follow-up observational period of days.

First, observe that under both models (1) and (2) the first triggering time of the -th new user follows a truncated Geometric distribution with parameter and support . Indeed, if the user were to trigger before day , we would have observed them in the original sample. Let denote the measure tracking the first triggering time of all the unobserved users. Denoting by the posterior distribution of as in Theorem 1, the predictive distribution of given the sample is

where the first equality follows from Bayes’ rule, and the second equality follows by observing that the posterior of decomposes as in (7) with depending only on . Moreover, given that we have that the predictive rules on new users are the same under both models.

Let us start by considering the number of new users who will trigger in the period . Exploiting the compound Poisson process representation in Proposition 3.3 in James (2017) we obtain the following distributional characterization for .

Proposition 1.

A straightforward way to estimate is to proceed by “inverse regression”: obtain an estimator of for via the expected value of (8) and estimate with such that .

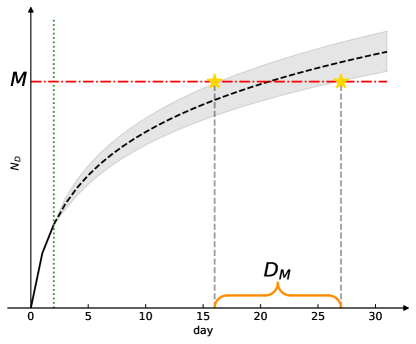

Providing prediction intervals for requires more care. We propose two approaches, one based on Proposition 1 and one based on the direct study of the posterior of . In the former case, we begin by constructing a global credible band, of level , of the form such that

| (9) |

Then, we slice that prediction band at to obtain an interval for . See Figure 1 for further details. To construct such a band, we proceed as follows. First we simulate times from the posterior law of as in Theorem 1 and, conditional on , we sample the values , as in Proposition 1, keeping only the tuples of with highest density. Then, we evaluate the trajectories for , and set and equal to the minimum and maximum of the simulated values for each . We found that the interval for is robust to the chosen value of if this is sufficiently large. In our simulations, we always fix .

The second approach we consider is to study directly the posterior of . Unfortunately, such a posterior has a rather complicated form. Indeed, can be regarded as the -th order statistic of the points of a mixed Poisson process with non-constant rate, for which no closed form expression exists. Hence, we describe next a Monte Carlo procedure that efficiently draws samples from the posterior of .

We start by observing that to sample the first triggering times of the non-observed users , it is “sufficient” to first sample from the corresponding posterior distribution reported in Theorems 1 and 2 and then, conditional on , sample for . This requires truncating to a finite number (say ) of atoms. Simulating the largest atoms in can be achieved by exploiting the Ferguson-Klass representation of completely random measures (Ferguson and Klass, 1972). See Appendix C for further details on how to simulate and an adaptive strategy to set the truncation . Then, the posterior of can be simulated using Algorithm 1.

Unfortunately, we found such an approach unsatisfactory due to the high computational cost. Indeed, sampling each jump in requires computing a non-trivial integral. Moreover, the number of jumps simulated must be sufficiently large to ensure a negligible approximation error. A more efficient approach consists in simulating only those users for which , where is a reasonable upper bound, as in the next theorem.

Theorem 3.

Let . Then

where , and are i.i.d. random variables supported on such that

The proof of Theorem 3 is reported in the Appendix and makes use of the compound Poisson representation for generalized Indian buffet processes in Proposition 3.3 of James (2017). See Algorithm 2 for the pseudocode.

4 Numerical Illustrations

In the following, we will denote by Bernoulli model (BM) the one in (3) and by Geometric model (GM) the model in (4). To fit both models, we adopt an empirical Bayesian approach and estimate by maximizing the marginal likelihood of the data. The negative log-marginal likelihood is not a convex function of the parameters, however we found that standard numerical optimization algorithms perform similarly in terms of the prediction errors. In particular, we have considered gradient descent with linesearch, BFGS, Particle Swarm, and Nelder Mead; the latter two are global optimization algorithms that do not require derivatives. Therefore, we used BFGS as it is usually the fastest to converge. All experiments were performed on a Macbook Pro M1 with 16GB of RAM and 8 threads.

4.1 Comparison between the two models

To highlight the differences between the two models, we begin by considering two simple data generating processes. In the first (DG1) we simulate data from the Bernoulli model using the generative scheme detailed in the Appendix. In the second (DG2) we instead start by simulating data from the Geometric model and construct the daily-activity information , as follows

where . That is, in DG2, after the first trigger, users tend to be less active. This resembles patterns observed, e.g., on e-commerce websites.

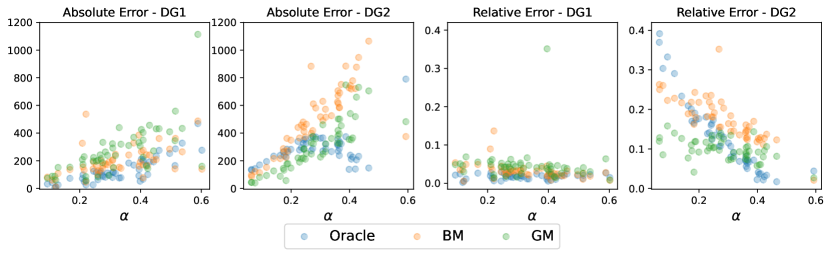

For both data generating processes, we fix , , , and simulate 50 independent dataset that differ only in the value of . Note that these parameters values are used only to generate the synthetic datasets, while prediction are based on estimated values obtained in an empirical Bayesian fashion. We compare the models BM and GM in a prediction task where we estimate the number of newly active users in a subsequent period of days by taking the expected value of the predictive distribution in (8). Since the predictive distribution is the same for both models, we are effectively comparing how well the numerical algorithms can recover the true data generating parameters when maximizing the marginal likelihoods under BM and GM. We report the absolute error as well as the relative error and further compare our models to a Bayesian oracle who knows the data generating parameters and uses the expected value of (8) for her predictions.

Results are summarized in Figure 2. In DG1, the oracle estimator achieves the smallest errors. BM is competitive with the oracle while GM usually yields slightly larger errors. Looking at the relative errors, we can see that these are usually less than and the three prediction yield comparable errors. In contrast, under DG2, GM performs significantly better (improvements are usually greater than 10% for the relative error) than BM across all values of in the data generating process. Surprisingly, GM outperforms the oracle for smaller values of as well.

In summary, it appears clear that when the data follow the assumption of BM (namely, each user is active on each given day with constant user-specific probability), BM is the best model but GM provides competitive estimates. Instead, when the data do not follow such assumptions, as in DG2, BM produces much poorer estimates than GM. Therefore, we will focus in the subsequent analysis only on GM.

4.2 Estimation of

We consider here the estimation of and compare the two approaches outlined in Section 3. For brevity’s sake, we consider only the GM model but analogous results hold for BM.

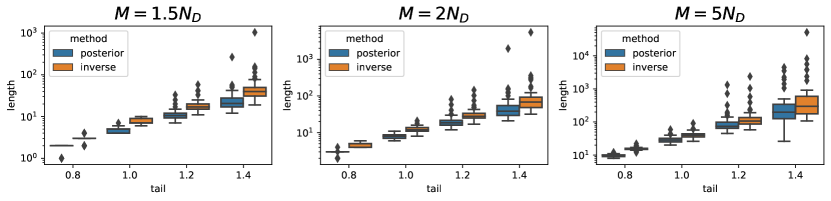

To generate data, we assume that the total pool of possible customers is bounded by 1,000,000 and that each customer has a probability of being active in any given day of , i.e., the frequency of the customers follows a Zipfian law with tail parameter , for . We generate data for days, thus observing users, and we want to estimate the number of days needed to get for .

We compare the estimator and the intervals based on the inversion technique depicted in Figure 1 with the posterior mean and 95% credible intervals obtained from the posterior of , which is approximated using draws from Algorithm 1 in combination with Algorithm 2. As far as the point estimators are concerned, the two estimators give essentially the same results in terms of mean squared error. We report a comparison in the appendix. Focusing instead on the prediction intervals, we observe that the intervals obtained from the inversion techniques are larger than those based on the posterior of , see Figure 3. Moreover, the length of the intervals increases with tail parameter of the data generating process. This is intuitive since for smaller values of we expect to see more users in the first days while if is larger it might require hundreds or thousands of days to reach the desired number of users, resulting in a greater uncertainty. As far as the calibration of the intervals is concerned, when or both types of intervals are misscalibrated, their coverage varying from 60% to 90% depending on the setting. Instead, for and the posterior of produces (almost) perfectly calibrated intervals, while the inversion intervals have a coverage above the nominal level, as expected given that the inversion intervals are larger. Finally, when , the coverage of the inversion intervals is slightly below the nominal level (around 93%) while the posterior inference intervals have a coverage of (when ) and (when ).

Concerning the computational costs of producing the intervals, we note the following. To generate a draw from the posterior of , we use Algorithm 2 to sample the measure . While a big-O analysis of Algorithm 2 eludes us, we can comment that seems to grow linearly with the parameter . Then one needs to sample , , from a discrete distribution over , which requires computing probabilities. In summary, Algorithm 2 can be seen to scale quadratically in . Instead, the inversion approach requires computing the global credible band, that needs to sample repeatedly from the law of , in Proposition 1, compute the density of the samples and evaluate the trajectories for , all of which scales linearly in . Most importantly, the computational cost of estimating the inverse interval for is not affected by the value of . On the other hand, for large values of , the value of in Algorithm 2 can be seen to increase steeply. To test these insights, we performed a small simulation where we generated data from (DG2) for days, with fixed parameters , and . We then tried to compute the inversion and posterior intervals of with . Computing the inversion intervals took around s across all simulations, while for the posterior intervals the cost ranged from s (when ) to almost s (when ).

4.3 Comparison on Real Datasets

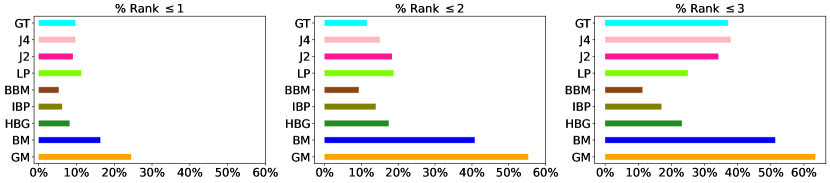

For our experiments on real data, we consider a collection of 210 A/B tests that ran for 28 days in production on a global e-commerce platform. For each experiment, we retain the trigger data from the first days as “training”, and then assess the performance of each method by comparing the model’s prediction with the realized value that occurred at days.

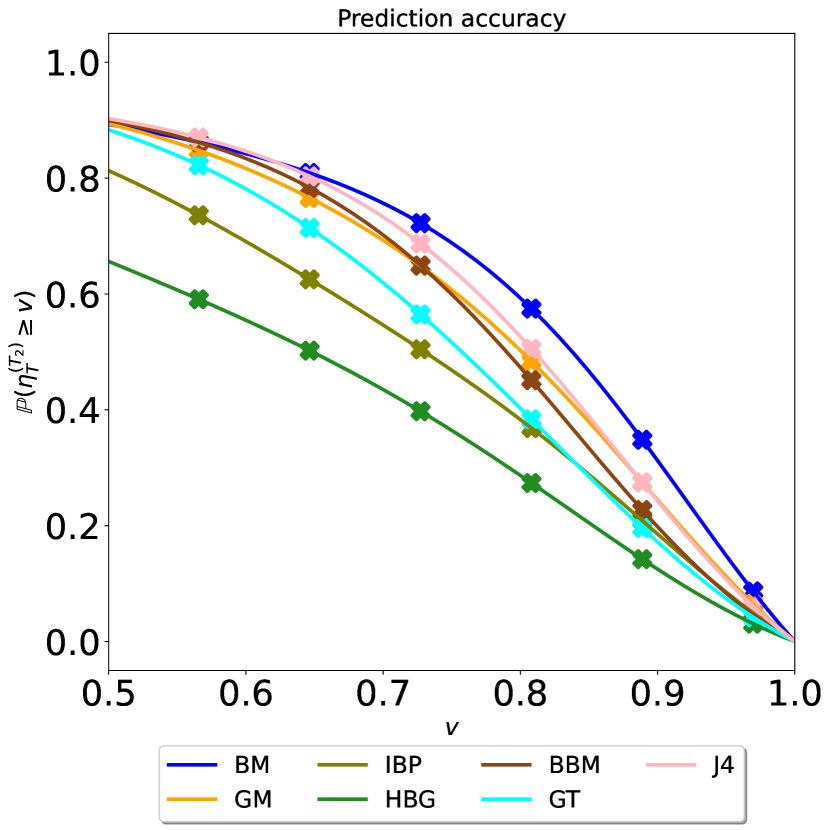

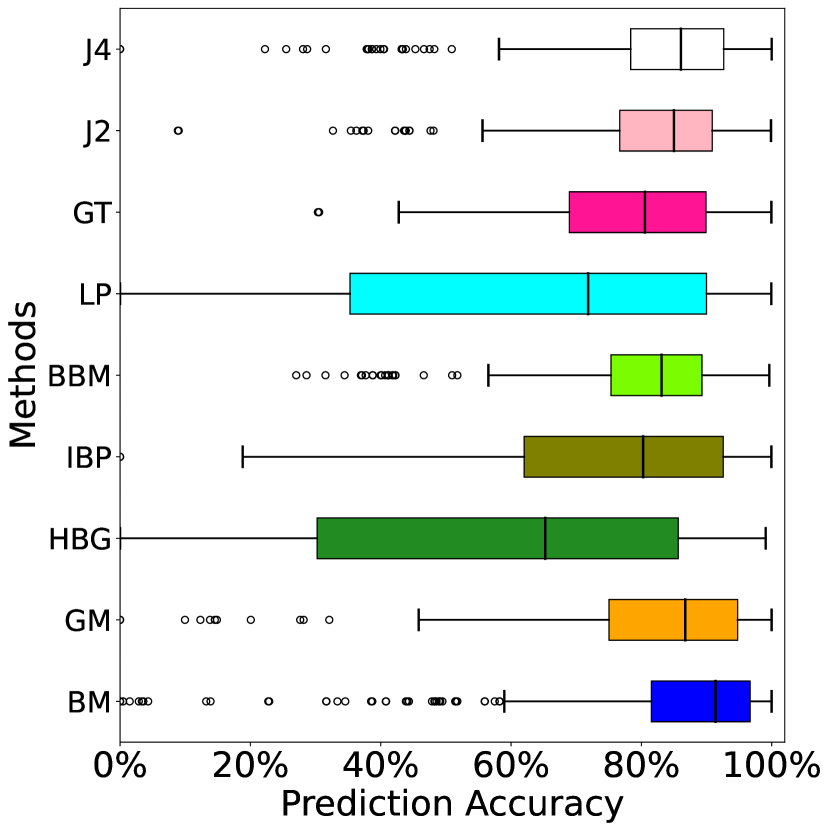

We compare a total of 9 competitors: in addition to our two models (GM and BM) we consider the hierarchical Bayesian model in Richardson et al. (2022) (HGB), the Indian buffet process (IBP), the beta-Bernoulli model of Ionita-Laza et al. (2009) (BBM), the linear programming approach of Zou et al. (2016) (LP) the jackknife estimators of order 2 and 4 (J2 and J4) (Burnham and Overton, 1979), and the Good-Toulmin estimator (Good, 1953). For all the models involving hyperparameters, these are chosen via an empirical Bayesian approach maximizing the marginal likelihood of the data for the first days.

The different experiments feature an extremely diverse number of users, ranging from to less than . Aggregating quantitative performance metrics naively, such as reporting the mean squared error, leads to having a handful of experiments dominating the results. Likewise, as in all real data analysis, making a perfect prediction is unfeasible, especially given the small fraction of data we consider. The user participation can be greatly influenced by online advertisement campaigns, of which unfortunately we have no data. Therefore, we compare the different models based on a more robust metric: their top-k ranking. That is, for each model we report how many times over the 210 experiments the model’s prediction are the top-k best predictions for . Results are reported in Figure 4. We can see that our GM and BM are the best performing ones, and GM consistently outperforms BM, hinting that users preferences may vary after the first trigger. See the appendix for different evaluation metrics that confirm our conclusions.

5 Discussion

We proposed a BNP framework to model online user’s activities with a focus on predicting the number of active users in a given period of days and estimating the time needed to attain a desired level of participation of users . Despite its central importance for experimenters, the estimation of has been overlooked by previous the literature. Our work builds on the recent contributions in Camerlenghi et al. (2022); Beraha and Favaro (2023) where the stable Beta scaled process was proposed as a prior in trait allocation models. Our work complements and extend the analysis and application of scaled process priors, showing how, compared to the use of traditional CRM prior, scaled processes yield greatly improved predictive performances without sacrificing the analytical tractability and computational convenience.

In particular, we derived closed-form expressions for the posterior distribution of , and proposed two strategies to estimate . The first, which “inverts” a global prediction band for , this is computationally cheap but might produce larger intervals. The second strategy simulates directly from the posterior of using Monte Carlo (and not MCMC), which is slightly more demanding from the computational side. These quantities depend crucially on the prior’s parameters, for which an empirical Bayes estimate is easy thanks to the analytical tractability of our models. We tested our approach on several examples, showing good predictive performance especially for the Geometric model, which ranked first out of 9 competitors on a large-scale experiment involving 210 real datasets collected at a global e-commerce platform.

Our Geometric model can be seen as the nonparametric version of Richardson et al. (2022). However, there is a key difference in that our model explicitly accounts (via the prior) for a power-law decay of the user-specific propensities to engage, while in Richardson et al. (2022) such parameters are conditionally i.i.d. As seen in our examples, real data often supports such a hypothesis.

References

- Bakshy et al. (2014) Bakshy, E., D. Eckles, and M. S. Bernstein (2014). Designing and deploying online field experiments. In Proceedings of the 23rd International Conference on World Wide Web, WWW ’14, New York, NY, USA, pp. 283–292. Association for Computing Machinery.

- Beraha and Favaro (2023) Beraha, M. and S. Favaro (2023). Transform-scaled process priors for trait allocations in Bayesian nonparametrics. arXiv preprint arXiv:2303.17844.

- Broderick et al. (2014) Broderick, T., L. Mackey, J. Paisley, and M. I. Jordan (2014). Combinatorial clustering and the beta negative binomial process. IEEE transactions on pattern analysis and machine intelligence 37(2), 290–306.

- Broderick et al. (2018) Broderick, T., A. C. Wilson, and M. I. Jordan (2018). Posteriors, conjugacy, and exponential families for completely random measures. Bernoulli 24(4B), 3181 – 3221.

- Burnham and Overton (1979) Burnham, K. P. and W. S. Overton (1979). Robust estimation of population size when capture probabilities vary among animals. Ecology 60(5), 927–936.

- Camerlenghi et al. (2022) Camerlenghi, F., S. Favaro, L. Masoero, and T. Broderick (2022). Scaled process priors for Bayesian nonparametric estimation of the unseen genetic variation. Journal of the American Statistical Association, 1–12.

- Campbell et al. (2018) Campbell, T., D. Cai, and T. Broderick (2018). Exchangeable trait allocations. Electronic Journal of Statistics 12(2), 2290 – 2322.

- Chakraborty et al. (2019) Chakraborty, S., A. Arora, C. B. Begg, and R. Shen (2019). Using somatic variant richness to mine signals from rare variants in the cancer genome. Nature communications 10(1), 5506.

- Efron and Thisted (1976) Efron, B. and R. Thisted (1976). Estimating the number of unseen species: How many words did Shakespeare know? Biometrika 63(3), 435–447.

- Ferguson and Klass (1972) Ferguson, T. S. and M. J. Klass (1972). A Representation of Independent Increment Processes without Gaussian Components. The Annals of Mathematical Statistics 43(5), 1634 – 1643.

- Ghahramani and Griffiths (2005) Ghahramani, Z. and T. Griffiths (2005). Infinite latent feature models and the Indian buffet process. In Y. Weiss, B. Schölkopf, and J. Platt (Eds.), Advances in Neural Information Processing Systems, Volume 18. MIT Press.

- Good (1953) Good, I. J. (1953). The population frequencies of species and the estimation of population parameters. Biometrika 40(3-4), 237–264.

- Gravel (2014) Gravel, S. (2014). Predicting discovery rates of genomic features. Genetics 197(2), 601–610.

- Heaukulani and Roy (2016) Heaukulani, C. and D. M. Roy (2016). The combinatorial structure of beta negative binomial processes. Bernoulli 22(4), 2301 – 2324.

- Hjort (1990) Hjort, N. L. (1990). Nonparametric Bayes Estimators Based on Beta Processes in Models for Life History Data. The Annals of Statistics 18(3), 1259 – 1294.

- Ionita-Laza et al. (2009) Ionita-Laza, I., C. Lange, and N. M. Laird (2009). Estimating the number of unseen variants in the human genome. Proceedings of the National Academy of Sciences 106(13), 5008–5013.

- James (2017) James, L. F. (2017). Bayesian Poisson calculus for latent feature modeling via generalized Indian Buffet Process priors. The Annals of Statistics 45(5), 2016 – 2045.

- James et al. (2015) James, L. F., P. Orbanz, and Y. W. Teh (2015). Scaled subordinators and generalizations of the Indian buffet process. arXiv: Probability.

- Kingman (1967) Kingman, J. F. C. (1967). Completely random measures. Pacific Journal of Mathematics 21(1), 59 – 78.

- Kingman (1975) Kingman, J. F. C. (1975). Random discrete distributions. Journal of the Royal Statistical Society: Series B (Methodological) 37(1), 1–15.

- Kohavi et al. (2007) Kohavi, R., R. M. Henne, and D. Sommerfield (2007). Practical guide to controlled experiments on the web: listen to your customers not to the hippo. In Proceedings of the 13th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’07, New York, NY, USA, pp. 959–967. Association for Computing Machinery.

- Masoero et al. (2022) Masoero, L., F. Camerlenghi, S. Favaro, and T. Broderick (2022). More for less: predicting and maximizing genomic variant discovery via Bayesian nonparametrics. Biometrika 109(1), 17–32.

- Richardson et al. (2022) Richardson, T. S., Y. Liu, J. McQueen, and D. Hains (2022, 28–30 Mar). A Bayesian model for online activity sample sizes. In G. Camps-Valls, F. J. R. Ruiz, and I. Valera (Eds.), Proceedings of The 25th International Conference on Artificial Intelligence and Statistics, Volume 151 of Proceedings of Machine Learning Research, pp. 1775–1785. PMLR.

- Teh and Gorur (2009) Teh, Y. and D. Gorur (2009). Indian buffet processes with power-law behavior. In Y. Bengio, D. Schuurmans, J. Lafferty, C. Williams, and A. Culotta (Eds.), Advances in Neural Information Processing Systems, Volume 22. Curran Associates, Inc.

- Thibaux and Jordan (2007) Thibaux, R. and M. I. Jordan (2007, 21–24 Mar). Hierarchical beta processes and the Indian buffet process. In M. Meila and X. Shen (Eds.), Proceedings of the Eleventh International Conference on Artificial Intelligence and Statistics, Volume 2 of Proceedings of Machine Learning Research, San Juan, Puerto Rico, pp. 564–571. PMLR.

- Titsias (2007) Titsias, M. (2007). The infinite gamma-poisson feature model. In J. Platt, D. Koller, Y. Singer, and S. Roweis (Eds.), Advances in Neural Information Processing Systems, Volume 20. Curran Associates, Inc.

- Zou et al. (2016) Zou, J., G. Valiant, P. Valiant, K. Karczewski, S. O. Chan, K. Samocha, M. Lek, S. Sunyaev, M. Daly, and D. G. MacArthur (2016). Quantifying unobserved protein-coding variants in human populations provides a roadmap for large-scale sequencing projects. Nature communications 7(1), 13293.

Appendix A Background Material on Bayesian nonparametrics and Random Measures

A completely random measure (CRM) on (with associated -algebra) is a random element taking values in the space of (finite) measures over (with associated Borel -algebra) such that for any and any collection of disjoint subsets of , the random variables are independent. It is well-known (Kingman, 1967) that a CRM can be decomposed as a sum of a deterministic measure, an atomic measure with fixed atoms and random jumps, and an atomic measure where both atoms and jumps are random and form the points of a Poisson point process. As customary in BNP, here we discard the deterministic parts of CRMs and consider measures of the form , where is a Poisson random measure on with Lévy intensity measure . The Lévy intensity characterizes the distribution of via the Lévy-Khintchine representation of its Laplace functional. That is, for measurable

Our focus is on homogeneous Lévy intensity measures, namely measures of the form where is a parameter, is a nonatomic probability measure on and is a measure on such that and for all . These conditions ensure that almost surely. We write . Under a trait allocation model, the law of provides a natural prior distribution for the parameter of the trait process.

We recall below the main results due to James (2017) for the Bayesian analysis of trait allocations under a CRM prior. Consider the trait allocations , . Given we assume that

-

•

for each , where is a distribution over the nonnegative integers such that

-

•

the variables are independent across , given

-

•

is a completely random measure with Lévy intensity .

We use the short-hand notation

| (10) |

and further define

Proposition 2 (Marginal law, Proposition 3.1 in James (2017)).

Let be distributes as (10), such that the sample displays traits and let , . Then, the marginal law of is

Theorem 4 (Posterior law, Theorem 3.1 in James (2017)).

Let be distributes as (10), such that the sample displays traits and let , . Then, the posterior distribution of is equivalent to the distribution of

where

-

1.

are independent positive random variables, also independent of with density

-

2.

is a completely random measure with Lévy intenisty

Appendix B Proofs

We will need the following technical lemma, which follows trivially from Lemma 1 in Camerlenghi et al. (2022)

Lemma 1.

Let . Then, the law of equals the one of a CRM with Lévy intensity

B.1 Proof of Theorem 1

B.2 Proof of Theorem 2

Let us start by focusing on the marginal distribution of . By the tower property of the expectation

where, in the innermost expectation we recognize the marginal law of a trait allocation model endowed with a CRM prior with intensity as in Lemma 1. We can thus apply Proposition 2 (with ) to evaluate such expectation.

In particular, when we have and , leading to

The result follows by marginalizing with respect to .

As far as the posterior is concerned, we argue as above and condition on . Then an application of Theorem 4 yields conditional representation as in the statement. Finally, to determine the posterior law of , observe that an application of Baye’s rule yields that has density

Straightforward computations lead to recognizing the desired law, that is .

B.3 Proof of Proposition 1

Also in this case, the main idea is to first condition of and exploit the general results in James (2017).

Let be the first triggering times of users that are active for the first time in the days . Then, by virtue of Theorem 2, is distributed as

| (11) | ||||

Hence, given , can be represented via Proposition 3 as

where .

Consider now be the triggering times of users first active on days . Arguing as above it is clear that, given and ,

where now . In particular, the law of does not depend on . Taking and reasoning by induction proves verifies the statement regarding .

To obtain the law of , we exploit the closeness of the Poisson family under convolution and write , so that

The results follows by integrating with respect to .

B.4 Proof of Theorem 3

The proof follows arguing as above, so we give here only a sketch. First, conditional to we apply Proposition 3 which yields the representation as a counting measure over a random number of support points. The law of and can be seen to be independent of with the distributions reported in the statement. Finally, follows a Poisson distribution as in Proposition 3, so that marignally it is negative-binomial distributed with parameters as in the statement.

Appendix C Posterior Simulation for via the Ferguson-Klass Algorithm

Using the Ferguson-Klass representation of completely random measures (Ferguson and Klass, 1972) it is straightforward to sample only the largest jumps of . Indeed, we have that conditionally to , is a CRM with Lévy intensity as in (6). Then, if are the jump times of a standard Poisson process of unit rate (i.e., , where is an exponential random variable), we have where is the tail Lévy measure

and is the incomplete Beta function.

The truncation level could be set deterministically, in which case we face a similar challenge as choosing the total number of users in Richardson et al. (2022), or adaptively by simulating until for a reasonable upper bound (e.g., one year). See Algorithm 3 for the pseudocode.

Appendix D Generative Schemes under the Model

We describe below two generative schemes that can be thought of as generalizations of the IBP to our class of prior as well as to deal with non-binary scores. In particular, for the Bernoulli model this scheme is a straightforward consequence of Proposition 5 in Camerlenghi et al. (2022). For the Geometric model, it is a rewriting of Theorem 3.

D.1 Bernoulli Model

-

1.

In the first experiment day, users trigger.

-

2.

After -days suppose we have observed unique users , such that each user has triggered at least once a day for days. Then on day , each of the previously seen user triggers independently of each other according to a Bernoulli distribution with parameter .

Moreover new users (i.e., previously unseen) will trigger for the first time.

D.2 Geometric Model

The triggering times for users active in the period is distributed as the random measure in Theorem 3, where we put and . In particular, the total number of users follows a Negative Binomial distribution with parameters . The triggering times are i.i.d. random variables supported on such that

Appendix E Further details for the real data analysis

E.1 Details on competing predictive methods

HBG Model of (Richardson et al., 2022)

The hierarchical Beta-Geometric model of Richardson et al. (2022) assumes

| (12) | ||||

where is the total population size that would be observed in an infinite time-frame. Conditionally to and , it is possible to exploit the conjugacy of the (truncated) Geometric and Beta distributions and obtain a closed-form expression for the posterior distribution for , that is

We follow Richardson et al. (2022) and set . The posterior distribution of does not belong to a known parametric family, therefore we sample from it using Hamiltonian Monte Carlo (HMC) in Stan. Compared to the rejection sampling algorithm devised in Richardson et al. (2022) we found HMC to have shorter runtimes and give better predictions.

Indian Buffet Process

The IBP model (Ghahramani and Griffiths, 2005) assumes the same likelihood as our BM model in (1) but places a Beta process prior on . I.e., is a CRM with Lévy intensity on . The marginal and predictive laws can be easily deduced by specializing Proposition 2 and 3 to this case. In particular, the distribution of follows

Beta-Binomial Model

Good-Toulmin

We adopted the estimators proposed Chakraborty et al. (2019) for the problem of predicting the number of new genetic variants (in particular, we use the estimators provided in Equation (6) of their supplementary material). Their code is available at https://github.com/c7rishi/variantprobs.

Jackknife

We consider the jackknife estimators developed by Gravel (2014). The -th order jackknife is obtained by considering the first values of the resampling frequency spectrum; that is, by adequately weighting the number of users who appeared exactly times in the experiment. We adapt the code provided in https://github.com/sgravel/capture_recapture/tree/master/software to form our predictions.

Linear Programming

Linear programs have been used for rare event occurrence ever since the seminal work of Efron and Thisted (1976). Here, we adapt to our setting the predictors proposed in Zou et al. (2016) via the UnseenEST algorithm. We adapt the implementation provided by the authors at https://github.com/jameszou/unseenest to perform our experiments.

E.2 Further comparisons

Let and be the true and estimated number of (new) users at the last day of the experiment. We report in Figure 5 the performance of the different models in terms of the following accuracy metric adopted from Camerlenghi et al. (2022)

This metric is equal to when the prediction is perfect and degrades to as its quality worsens.