The geometry of multi-curve interest rate models

Abstract.

We study the problems of consistency and of the existence of finite-dimensional realizations for multi-curve interest rate models of Heath-Jarrow-Morton type, generalizing the geometric approach developed by T. Björk and co-authors in the classical single-curve setting. We characterize when a multi-curve interest rate model is consistent with a given parameterized family of forward curves and spreads and when a model can be realized by a finite-dimensional state process. We illustrate the general theory in a number of model classes and examples, providing explicit constructions of finite-dimensional realizations. Based on these theoretical results, we perform the calibration of a three-curve Hull-White model to market data and analyse the stability of the estimated parameters.

Key words and phrases:

Term structure modeling; spreads; interest rate benchmarks; Heath-Jarrow-Morton model; consistency problem; finite-dimensional realization; model calibration.MSC2020 classification: 60H15, 91G30.

The authors are grateful to the participants to the XXIV Workshop on Quantitative Finance (Gaeta, Italy, 2023) for useful comments on an earlier version of this work. The first author gratefully acknowledges financial support from the Europlace Institute of Finance and the University of Padova (research programmes STARS StG PRISMA and BIRD190200/19).

1. Introduction

In dynamic models for the term structure of interest rates, two fundamental problems concern the consistency between a forward rate model and a parameterized family of forward curves and the existence of finite-dimensional realizations (FDRs) for the model. More specifically, consistency between and means that, if the initial term structure belongs to , then model will only generate forward rate curves belonging to , at least for a strictly positive time. The existence of finite-dimensional realizations corresponds to the existence of a finite-dimensional Markov state process driving the evolution of the inherently infinite-dimensional term structure. These problems have been addressed and solved in a remarkable series of works by T. Björk and co-authors (see [Bjö04] for an overview), exploiting the geometric properties of interest rate models and revealing the deep connections between the two problems.

Up to now, the geometric theory of interest rate models has remained restricted to the classical single-curve setup, where a single term structure provides a complete description of the interest rate market. However, starting from the 2008 global financial crisis, the emergence of credit, liquidity and funding risks in interbank transactions has led to multi-curve interest rate markets. The multi-curve phenomenon refers to the coexistence of multiple term structures, each of them associated to an interest rate benchmark for a specific tenor (i.e., the time length of the underlying loan). While overnight rates (such as the recently introduced SOFR in the US, SONIA in the UK, €STR in the Eurozone) can be considered risk-free rates, other interest rate benchmarks (such as Euribor and Libor rates, or the newly proposed Ameribor rates) are risk-sensitive rates associated to distinct term structures, with a specific behavior depending on the tenor.111After the cessation of Libor rates, market participants have expressed the need of risk-sensitive rates embedding credit, funding and liquidity risk components. In the US, this has led to the proposal of BSBY and Ameribor rates. In the Eurozone, Euribor rates represent risk-sensitive rates. Therefore, even after the cessation of Libor rates, global interest rate markets continue to be multi-curve interest rate markets. The mathematical analysis of multi-curve interest rate markets is made complex by the fact that all interest rate benchmarks are quoted in the same financial market, thereby introducing a strong dependence among the multiple term structures. Hence, multi-curve interest rate markets cannot be adequately described by a naive juxtaposition of several single-curve interest rate models. We refer the reader to [GR15] for an overview of multi-curve interest rate models and, closer to the modeling approach adopted in the present work, to [CFG16, FGGS20] for general multi-curve models of Heath-Jarrow-Morton (HJM) type.

In this paper, we address the problems of consistency and of the existence of finite-dimensional realizations for multi-curve interest rate models, extending the geometric approach first proposed by T. Börk and co-authors. This objective is made easier by the fact that several foundational results of [BC99, BS01] are formulated at an abstract level, which facilitates their application beyond the classical single-curve setting. We work in a Heath-Jarrow-Morton model driven by a multi-dimensional Brownian motion and we adopt the convenient parameterization of [FGGS20] of multi-curve interest rate markets in terms of spreads and fictitious zero-coupon bond prices. This parameterization highlights the analogy between multi-curve interest rate markets and foreign currency markets. By exploiting this analogy, we can adapt to our setting the methodology of [Sli10] for characterizing finite-dimensional realizations of a two-economy HJM model. We study in detail the classes of constant volatility models and constant direction volatility models, providing explicit constructions of finite-dimensional realizations. We also study the possibility of including directly the spread processes in the state process determining the finite-dimensional realizations. Finally, we propose a calibration methodology that computes the parameterized manifold that achieves the best fit to market data.

The problems of consistency and of the existence of finite-dimensional realizations have relevant practical applications. Indeed, as explained in [Bjö04, Section 3.1], the consistency problem is related to parameter recalibration. Forward rate curves are typically described through a parameterized family of functions (such as the popular Nelson-Siegel family of [NS87]) and, once a forward rate curve has been obtained, an interest rate model can be calibrated to it. On the next day, a new forward rate curve is computed and the model recalibrated to it. If consistency holds between model and the parameterized family of functions , then generates forward rate curves that belong to . Concerning the existence of finite-dimensional realizations, it has to be noted that Heath-Jarrow-Morton models are in general infinite-dimensional. However, if a finite-dimensional realization can be found, then the model becomes significantly easier to handle and can be described by an underlying Markovian factor process.

We close this introduction by briefly discussing some related literature. The problem of consistency was first addressed in [BC99], while the existence of FDRs was studied in [BG99], [BS01] and [BL02]. The inclusion of stochastic volatility process has been addressed in [BLS04]. These results are based on the interpretation of the realization of a forward rate model as a curve living on suitable Hilbert space. In [FT03, FT04], finite-dimensional realizations are studied in the context of forward rate models living on Fréchet spaces. For simplicity of presentation, in this work we shall only consider the case of Hilbert spaces, also because the conditions obtained by [BS01] continue to hold in that more general setting. Geometric properties related to the problem of consistency and the existence of FDRs for Lévy models are studied in [FT08, Tap10, Tap12].

The paper is structured as follows. In Section 2, we introduce the main modeling quantities of multi-curve interest rate models and the general mathematical framework of our work. In Section 3, we address the consistency problem, while Section 4 contains the study of finite-dimensional realizations. In Section 5, we propose and characterize an alternative notion of invariance. Finally, in Section 6, we describe a calibration algorithm that determines the parameterized manifold that achieves the best fit to market data of a multi-curve interest rate market.

Notation

We introduce some general notation that is going to be used in the paper:

-

•

We denote by the transpose of a matrix and by the scalar product between two vectors and in . The Euclidean norm of a vector is denoted by .

-

•

For a differentiable function we introduce the functionals

-

•

For a Fréchet-differentiable function we denote by its Fréchet derivative at .

-

•

We denote by the identity map on a vector space . Moreover, if , for , we denote by the identity map.

2. The modeling framework

In this section, we describe the general framework of multi-curve interest rate models. In Section 2.1, we introduce the generic types of interest rates considered in our analysis and the key modeling quantities. The mathematical setup of our work is then described in Section 2.2.

2.1. Interest rates and spreads

We consider a generic interest rate market with a numéraire given by the savings account associated to a risk-free rate (RFR). As mentioned in the Introduction, the RFR can represent one of the recently introduced overnight interest rate benchmarks. As usual, we parametrize the RFR term structure by means of zero-coupon bond (ZCB) prices, denoting by the price at time of a ZCB with maturity , for all . The simply compounded forward RFR for the time interval evaluated at time is given by , for .

Besides the risk-free rate, we consider risk-sensitive rates (RSR) that reflect the presence of credit, funding and liquidity risk in interbank transactions. As mentioned in the Introduction, RSRs can play the role of Libor/Euribor rates as well as of the newly proposed credit-sensitive rates (e.g., Ameribor). Since risk-sensitive rates exhibit a distinct behavior depending on their reference tenor (i.e., the length of time of the underlying loan), we consider a family of RSRs associated to a set of tenors , with , for some . The simply compounded forward RSR for tenor is denoted by , for all .

The multi-curve setup consists in the coexistence of the RFR together with the family of RSRs. In line with [CFG16, FGGS20], instead of modeling RSRs directly, we consider multiplicative spreads between RSR and RFR, defined as follows:

| (2.1) |

The spread can be regarded as a spot measure at time of the credit, funding, liquidity risks of the interbank market over a time period of length . Under typical market conditions, spreads are greater than one and increasing with respect to the tenor’s length.

For modeling purposes, we introduce fictitious ZCB prices, defined as follows:

| (2.2) |

Observe that (2.2) ensures the terminal condition , for all and . We point out that we do not assume that the fictitious bonds introduced above are traded in the market. Rather, fictitious bonds serve as a particularly convenient parametrization of the term structures associated to risk-sensitive rates (compare with [FGGS20, Section 2]).

Remark 2.1 (FX analogy).

The quantities and admit a natural interpretation in the context of foreign exchange (FX) markets. Indeed, for each , one can associate to the tenor a foreign economy denominated in a specific currency. The spread acts as the spot exchange rate at time between the -th foreign economy and the domestic economy, while represents the price (denominated in units of the foreign currency) at time of a ZCB with maturity in the -th foreign economy. It can be shown that the quantity represents the value at time of the floating leg of a single-period swap referencing . The FX viewpoint on multi-curve interest rate models goes back to the work of [Bia10] and has been further discussed in [CFG16, FGGS20, MM18]. In our context, the FX analogy will enable us to rely on and extend the approach of [Sli10] when studying finite-dimensional realizations of multi-curve interest rate models (see Section 4).

2.2. Term structure dynamics

Let be a filtered probability space, endowed with a -dimensional Brownian motion and where is a risk-neutral probability. In order to describe the RFR and RSR term structure dynamics, we adopt the Heath-Jarrow-Morton methodology, referring to [FGGS20] for additional details on the general framework.

Adopting the Musiela parametrization, we represent risk-free and fictitious ZCB prices as

| (2.3) |

For , the quantity represents the risk-free instantaneous forward rate at time for maturity . Similarly, for each and , the quantity represents the risk-sensitive instantaneous forward rate at time for maturity relative to tenor . The savings account numéraire associated to the RFR is given by .

Risk-free and risk-sensitive instantaneous forward rates are assumed to satisfy

| (2.4) |

where and are progressively measurable stochastic processes satisfying suitable integrability requirements to ensure the well-posedness of (2.3) and (2.4).

The spreads introduced in (2.1) are modelled as exponentials of Itô processes:

| (2.5) |

for all , where and are suitable progressively measurable processes ensuring the existence of a unique strong solution to (2.5). We shall refer to the process as the log-spread process associated to tenor , for .

In the classical single-curve setting, the HJM drift condition implies that the drift term in (2.4) is determined by the volatility (see, e.g., [Bjö04, Proposition 1.1]). In the present multi-curve setup, risk-neutrality of implies that, for each , the drift term in (2.4) is determined by the volatility as well as by the covariation between and the log-spread process . Moreover, the drift term in (2.5) turns out to be endogenously determined. This is the content of the following proposition, which follows as a special case of [FGGS20, Theorem 3.7]. For convenience of notation, we set and in the following.

Proposition 2.2.

Under a risk-neutral probability measure , the following holds:

for every and .

Remark 2.3.

(i) The drift conditions stated in Proposition 2.2 are equivalent to the local martingale property under of the processes and , for all and . This property is taken as the defining property of a risk-neutral probability. As clarified in [FGGS20], this suffices to ensure absence of arbitrage in the financial market composed by all risk-free ZCBs and single-period swaps referencing the risk-sensitive rates , for all and . Single-period swaps represent the basic building blocks of interest rate derivatives having risk-sensitive rates as underlying.

As a consequence of (2.4)-(2.5), our modeling framework is described by stochastic differential equations (SDEs), since we consider forward rates and spreads. In addition, the SDE (2.4) depends on the time-to-maturity variable . In line with [Bjö04], for each , we view (2.4) as an SDE taking values in a function space . More specifically, we assume that each forward rate process takes value in the space

with . By [BS01, Proposition 4.2], the space is an Hilbert space for every .

We denote by the solution to (2.4)-(2.5), with drift terms determined as in Proposition 2.2. As explained below, existence of a unique solution to (2.4)-(2.5) is guaranteed under Assumption 2.4. The process takes values on the space , where denotes the Cartesian product of copies of . We shall also adopt the notation , where represent the forward rates and the log-spreads.

We introduce some technical assumptions on the volatility coefficients of (2.4) and (2.5). In the following, this will always be assumed to be satisfied without further mention.

Assumption 2.4.

(i) For all and , it holds that

| (2.6) |

where and are deterministic functions.

(ii) For each , the functions and appearing in (2.6) are smooth functions in the Fréchet sense (i.e., they admit continuous -th order Fréchet derivative, for every ). In addition, the functions

are smooth in the Fréchet sense.

Under Assumption 2.4, we can compactly write as follows the dynamics of the process :

| (2.7) |

where and is an element of collecting all drift terms of equations (2.4)-(2.5). Proposition 2.2 together with Assumption (2.4) and the boundedness of the operator in implies that is a smooth vector field in . This ensures the (local) existence of a unique strong solution to (2.7) in the function space , for every initial point (see for instance [DPZ92]).

In the following, it turns out to be convenient to rewrite (2.7) in terms of the Stratonovich integral (see, e.g., [KS12, Definition 3.3.13]), the reason being that in Stratonovich calculus Itô’s formula takes the form of the usual chain rule of ordinary calculus. Denoting by the Stratonovich integral of a semimartingale with respect to a semimartingale , we then have

| (2.8) |

where, for every , the drift term can be explicitly written as follows:

| (2.9) |

Remark 2.5 (On the relation to stochastic volatility models).

For multi-curve interest rate models, the problems of consistency and existence of FDRs cannot be addressed by adapting the techniques used in [BLS04] for stochastic volatility models, replacing the stochastic volatility process with the log-spread processes. Indeed, in [BLS04] the stochastic volatility dynamics do not depend on the forward curves. On the contrary, in a general multi-curve interest rate model, the dynamics of the log-spread processes cannot be separated from the forward curves, also as a consequence of the drift conditions stated in Proposition 2.2.

3. The consistency problem

In this section, we study the consistency between a multi-curve interest rate model and a parameterized family of forward curves222In this section, with some abuse of terminology, we shall refer to as a parameterized family of forward curves even if, strictly speaking, only the first components of represent forward curves, the last components (corresponding to the log-spreads) being real-valued. An alternative approach will be presented in Section 5.. In Section 3.1, we provide a general characterization of consistency, extending to the multi-curve setting the geometric approach first introduced by [BC99]. In Section 3.2, we provide a detailed analysis of an example, addressing the consistency between Hull-White multi-curve models and a modified Nelson-Siegel family of forward curves.

3.1. Characterization of consistency

We consider a mapping defined on an open subset , for some . The mapping determines a manifold defined by the image . More specifically, in this section we shall work under the following assumption.

Assumption 3.1.

The mapping is an injective function such that is injective, for all . As a consequence, is a submanifold of .

For each parameter value , the mapping produces a curve . The value of this curve at the point is denoted by , so that can also be viewed as a mapping . The mapping formalizes the idea of a finitely parameterized family of forward curves. The manifold represents the set of all curves that can be generated by .

In the following, we denote by a multi-curve interest rate model as defined in Section 2.2. We recall that, as a consequence of Proposition 2.2, a multi-curve interest rate model is entirely determined by the volatilities and , for , which satisfy Assumption 2.4. A model and a submanifold are said to be consistent if model generates forward curves that belong to , at least for a strictly positive time interval. The notion of consistency is precisely defined through the following concept of local invariance (see [BC99, Definition 1.1]).

Definition 3.2.

A manifold is said to be locally invariant under the action of if, for each point , there exists a stopping time such that almost surely

If a.s. for all , the manifold is said to be globally invariant.

In the following, we give a necessary and sufficient condition for local invariance (and invariance will always be meant in a local sense). To this effect, following the approach of [BC99], we exploit the equivalence between the notion of invariance and the notion of .

Definition 3.3.

A parameterized family is said to be (locally) -invariant under the action of if, for every , there exists an a.s. strictly positive stopping time and a stochastic process , taking values in and with Stratonovich dynamics

| (3.1) |

such that for all it holds that

As in the classical single-curve setup considered in [BC99] and [Bjö04], the process represents an underlying factor process. The notion of -invariance is therefore equivalent to the existence of an underlying finite-dimensional factor model. This concept will turn out to be intimately related to the existence of finite-dimensional realizations (see Section 4 below).

Under Assumptions 2.4 and 3.1, it can be easily shown that -invariance is equivalent to invariance. By relying on this fact, a straightforward adaptation of the proof of [BC99, Theorem 4.1] leads to the following characterization of invariance in terms of the vector fields and .

Theorem 3.4.

The manifold is invariant under the action of if and only if the following conditions hold for all :

| (3.2) |

where denotes the tangent space of at the point .

Condition (3.2) is equivalent to require that the distribution generated by and (i.e., the subspace of the tangent bundle of generated by and , for ) is a subset of , where denotes the tangent bundle of .

Differently from the single-curve case, in the present multi-curve setup the study of the consistency between a model and a manifold depends on the relations among the components of the function , representing forward rates and log-spreads associated to different tenors. This is illustrated in the next section in the case of a Hull-White multi-curve model.

Remark 3.5.

Even if the log-spread processes are inherently finite-dimensional, it is in general not possible to consider the consistency problem for the forward rate components alone, separately from the log-spread processes. This is due to the fact that the forward rate dynamics can depend on the log-spreads. For this reason, we consider a parameterized family providing a joint representation of forward rates and log-spreads. In Section 5 we will present an alternative approach that allows including the log-spreads explicitly in the state process.

3.2. Example: Hull-White model and modified Nelson-Siegel family

For simplicity of presentation, let us consider the case (the results of this section can be extended in a straightforward way to the case of a -dimensional Brownian motion, see [Lan19, Section 2.3.8]). We suppose that, for each , the forward rate equation (2.4) takes the form

| (3.3) |

Since the Hull-White forward rate equation has constant volatility, we naturally assume that also the volatilities of the log-spread processes are constant. Hence, the volatility of our Hull-White multi-curve model is given by .

We aim at determining a manifold such that the conditions of Theorem 3.4 are satisfied. Already in the single-curve setting, it is well-known that the Nelson-Siegel family is inconsistent with the Hull-White model (see [BC99, Proposition 5.1]). Therefore, we consider the following modified Nelson-Siegel family:

| (3.4) |

denoting , for each . We then introduce the function

| (3.5) |

where the elements , for , are given as in (3.4) and , for , are suitable real-valued functions to be determined later, corresponding to the log-spread components of the multi-curve model . For every , letting

| (3.6) | ||||

we can easily check that conditions and are satisfied, with denoting the drift term of (3.3). Therefore, the vector fields

| (3.7) |

satisfy the first components of the invariance conditions (3.2). This ensures consistency between the forward rate components of the model and the parameterized manifold .

However, we still have to consider the log-spread processes, corresponding to the last components of the function in (3.5). To this effect, we can follow two alternative approaches:

-

(i)

Exploiting the fact that the log-spread processes are inherently finite-dimensional, we can enlarge the parameter space by introducing additional variables corresponding to the log-spread processes themselves. We therefore consider the enlarged state space and define , for every and each . With this approach, the conditions of Theorem 3.4 are always satisfied. Indeed, to verify that (3.2) holds, it suffices to take and

for all and . In this way, we obtain that the parameterized family

(3.8) defined for any , generates a manifold that is consistent with the Hull-White multi-curve model under analysis.

-

(ii)

Instead of enlarging the parameter space , we can look for conditions that ensure that the last components of conditions (3.2), corresponding to the log-spread processes, are automatically satisfied by the vector fields and introduced in (3.6)-(3.7), thereby determining implicitly the components of the function in (3.5).

Approach (ii) requires the validity of some internal relations among the volatilities of the forward rates and of the log-spread processes, as clarified by the next result.

Proposition 3.6.

Let the manifold be given by the image of the function , with given as in (3.4), for each , and defined as follows:

| (3.9) | ||||

for each . If , for all , then the manifold is consistent with the Hull-White multi-curve model considered in this section.

Proof.

By Theorem 3.4, we must verify that the following two conditions

| (3.10) | ||||

| (3.11) |

are satisfied by and given in (3.6)-(3.7), for all . Observe first that

By relying on this identity, differentiating (3.9) and making use of (3.6), it can be checked that condition (3.10) holds (we refer to [Lan19, Section 2.3.5] for the detailed computations). Similarly, to check that condition (3.11) holds, we differentiate (3.9) and make use of the specification , together with the hypothesis that , for all . ∎

Remark 3.7.

Approach (i) leads to a parameterized family whose domain is , without any further requirement on the model. Approach (ii) leads to a parameterized family whose domain lies in and is therefore more parsimonious, but requires the validity of a specific relation. It can be shown that the condition implies that the log-spread process is an affine transformation of the spot rates . If this is the case, a parameterized family that is consistent with the forward rates automatically determines a parameterized family for the log-spread process . This explains why it is not necessary to enlarge the parameter space if , for all .

4. Finite-dimensional realizations

In this section, we study the existence and the construction of finite-dimensional realizations (FDRs) for a multi-curve interest rate model as described in Section 2.2. In Section 4.1, we characterize the existence of FDRs by relying on the geometric approach of [BS01] and we outline a general procedure for the construction of FDRs. Section 4.2 illustrates the methodology in the simple case of constant volatility models, while Section 4.3 considers the more complex case of constant direction volatility models. In Section 4.4, we show that the state variables of an FDR can be chosen as an arbitrary family of forward rates and log-spreads.

4.1. Existence and general construction of FDRs

We start by defining the notion of an -dimensional realization for a multi-curve interest rate model (see [BS01, Definition 3.1]).

Definition 4.1.

Model has an -dimensional realization if, for each , there exist a stopping time a.s., a point , smooth vector fields , defined on a neighborhood of , and a function satisfying Assumption 3.1, such that

almost surely, where is an -dimensional state process given as the strong solution to

We say that model has a finite-dimensional realization (FDR) if it has an -dimensional realization, for some .

In the above definition, corresponds to the initially observed term structures of risk-free and risk-sensitive forward rates, together with the vector of log-spreads. Definition 4.1 is intimately related to the concept of -invariance (see Definition 3.3). Indeed, it is apparent that the existence of an FDR is equivalent to the existence of an -invariant parameterized family . Therefore, in view of Theorem 3.4, given a multi-curve interest rate model , the existence of an FDR amounts to the existence of a submanifold such that , for each , where is a neighborhood of and . In other words, we are looking for the tangential submanifold of the distribution .

By [BS01, Theorem 2.1], a tangential submanifold for a smooth distribution exists if and only if is involutive, i.e., if and only if the Lie bracket between two vector fields in lies in . We recall that the Lie bracket between two vector fields and on is defined as

[BS01, Theorem 2.1] is an infinite-dimensional version of the Frobenius theorem and gives the existence of a tangential submanifold when the distribution generated by and is involutive. However, in general is not involutive. Therefore, we must consider the smallest involutive distribution that contains . Such distribution is called the Lie algebra of . Since [BS01, Theorem 2.1] is an abstract result, it can be immediately applied to our multi-curve framework, leading to the following statement (see [Lan19, Theorem B.3.2] for additional details).

Theorem 4.2.

A model has an FDR if and only if there exists a finite-dimensional tangential submanifold for . In turn, this is equivalent to

| (4.1) |

where denotes the Lie algebra generated by .

As long as condition (4.1) is satisfied, an FDR can be constructed. To this end, we outline the general construction strategy provided in [BL02], proceeding along the following three steps:

-

I.

choose a finite number of independent vector fields which span ;

-

II.

compute the invariant manifold

(4.2) where denotes the integral curve of the vector field passing through ;

-

III.

define the state process taking values in such that , making the following ansatz for the Stratonovich dynamics of the process :

(4.3) where the vector fields and are determined by the following conditions:

(4.4) The uniqueness of the vector fields and , for , satisfying (4.4) is guaranteed since satisfies Assumption 3.1, hence it is a local diffeomorphism.

The above methodology will be illustrated in Sections 4.2 and 4.3 in the case of constant volatility models and constant direction volatility models, respectively. In both cases, we will make use of the FX analogy discussed in Remark 2.1, which enables us to adapt some arguments first used in [Sli10] in the context of an HJM model comprising a domestic and a foreign economy.

4.2. Constant volatility models

Let us first consider the case where the volatility does not depend on , so that are constants in , while are elements of (where is the dimension of the driving Brownian motion). In this case, it holds that

| (4.5) |

To determine the Lie algebra of , we compute the successive Lie brackets between and . This can be easily done by observing that , while

| (4.6) |

Therefore, the Lie bracket of and , for each , is given by

which is constant on . Hence, the only vector field in that is not constant is . Therefore, to determine explicitly it suffices to compute the Lie bracket between and the successive Lie bracket between and . These arguments lead to

| (4.7) |

where (see [Lan19, Section 3.2] for full details)

To state a necessary and sufficient condition for the validity of (4.1) in constant volatility models, we need to recall the concept of quasi-exponential function (see [Bjö04, Definition 2.2]).

Definition 4.3.

A function is said to be quasi-exponential (QE) if it is of the form

where , , are real numbers and , real polynomials.

We recall that QE functions can be characterised as follows (see, e.g., [Bjö04, Lemma 2.1]).

Lemma 4.4.

A function is if and only if it is a component of the solution of a vector-valued linear ODE with constant coefficients, i.e., it holds that , where denotes the i-th order derivative of .

4.2.1. Existence of FDRs

In view of the FX analogy discussed in Remark 2.1, a straightforward adaptation of [Sli10, Proposition 3.2] yields the following characterization of the existence of FDRs in the constant volatility case (see also [Lan19, Theorem 3.2.3] for a detailed proof).

Proposition 4.5.

A multi-curve interest rate model with constant volatility admits an FDR if and only if the function is QE, for every and .

If is QE, for all , , the Lie algebra satisfies

| (4.8) |

where , for each . As a consequence of Lemma 4.4, for each , there exists an annihilator polynomial

| (4.9) |

such that for all . By (4.7), the tangential manifold of dimension is obtained by the composition of the integral curves of , , , for and .

In the following, we will use this notation for a generic element of the state space :

| (4.10) |

4.2.2. Construction of FDRs

In order to construct explicitly an FDR, we apply the three-step procedure outlined at the end of Section 4.1. In view of Theorem 4.5, it suffices to compute the integral curve of every vector field generating the Lie algebra given in (4.7). Then, in step II, we compose the integral curves, thus obtaining the tangential manifold. Finally, in step III, we invert the consistency condition and obtain the following result, which generalizes to the multi-curve setting [BS01, Proposition 5.2] and [Sli10, Proposition 3.5] (see [Lan19, Section 3.2.1] for a detailed proof). We make use of the notation , for .

Proposition 4.6.

Suppose that a multi-curve interest rate model with constant volatility admits an FDR. In this case, the invariant manifold generated by is parameterized as follows:

where denotes the Kronecker delta between indexes and . In addition, the coefficients of the dynamics of the state process in (4.3) are given by

| (4.11) |

according to the notation introduced in (4.10). In (4.11), the term denotes the -th coefficient of the annihilator polynomial given in (4.9), for and .

4.3. Constant direction volatility models

In this section, we consider a more general class of multi-curve interest rate models with non-constant volatility, exploiting the analogy with the two-economy HJM setup analysed in [Sli10] (see Remark 2.1). We aim at providing conditions ensuring the existence of FDRs for a model determined by a volatility of the following form:

| (4.12) |

for , where and and are smooth (in the Fréchet sense) scalar vector fields on , for every and . We introduce the following assumption.

Assumption 4.7.

For all and , it holds that and , for every .

As a first step, we need to compute explicitly the drift term in the Stratonovich dynamics (2.8) of the joint process . To this effect, we notice that, for each ,

We denote by the Fréchet derivative of with respect to the variable computed at , acting on the vector , for each and . We also define

| (4.13) |

Hence, the Stratonovich dynamics of the components of (2.8) are given by

Therefore, the Stratonovich drift term can be explicitly written as follows:

The complexity of the Stratonovich drift arises from the fact that, for a multi-curve interest rate model with volatility as in (4.12), each component of the volatility function can depend on the whole vector of forward rate and log-spread processes.

4.3.1. Existence of FDRs

Differently from Section 4.2, in the case of constant direction volatility the computation of the integral curve of turns out to be more difficult. To overcome this obstacle, we will derive conditions ensuring that a distribution larger than is finite-dimensional. This will provide a sufficient condition for the existence of FDRs.

As a preliminary, we denote by the -th element of the canonical basis of , for each , and introduce the following family of vector fields:

| (4.14) |

where

Making use of this notation, we can write

| (4.15) | ||||

| (4.16) |

for , where

It is easily seen that (4.15)-(4.16) directly imply that , where

| (4.17) |

Consequently, if is finite-dimensional, then also is finite-dimensional. Moreover, the Lie algebra has a much simpler structure than . Similarly to the case of constant volatility models analysed in Section 4.2, it can be proved that is finite-dimensional if and only if is a QE function, for every and (compare with Proposition 4.5 and see also [Lan19, Section 3.2.1] for additional details). We have thus obtained the following result, which in particular provides an extension of [Sli10, Proposition 4.2] to the multi-curve setting.

Proposition 4.8.

If is a QE function, for every and , then the Lie algebra is finite-dimensional.

4.3.2. Construction of FDRs

In view of Theorem 4.2, the result of Proposition 4.8 provides a sufficient condition for the existence of an FDR. We now turn to the construction of FDRs. In this section, to guarantee the existence of FDRs, we shall work under the following assumption.

Assumption 4.9.

For every and , the function is QE.

Under Assumption 4.9, it can be easily verified that the functions given in (4.13) are QE. By Lemma 4.4, there exist and , for all and , such that

for suitable constants and . In this case, due to the definition of the Lie algebra , the dimension of is bounded by .

We introduce the following notation for a generic vector , obtained by concatenating all elements of the vectors , and :

| (4.18) |

As explained in Section 4.2.1, the tangential manifold of can be constructed as follows:

| (4.19) |

for an arbitrary initial point . In the following, we denote by the -th component of , for . The components of the function introduced in (4.19) are given by

| (4.20) | ||||

At this point, we can determine the coefficients and of the state process by requiring that condition (4.4) holds. For simplicity of notation, we shall omit to denote the dependence on in the functions and and adopt a notation consistent with (4.18):

where , for each , has the same representation of the vector . To determine and , we must invert the consistency condition between the coefficients of the model and tangential manifold, as described in step III of the procedure outlined in Section 4.1. In this way we obtain

We follow the same procedure in order to determine . We obtain, for each ,

In conclusion, under Assumption 4.9, an FDR for a model defined by a volatility of the form (4.12) can be determined by the immersion defined in (4.20) and by the finite-dimensional state process , whose drift and volatility coefficients have been explicitly computed above.

Remark 4.10.

Assumption 4.9 only represents a sufficient condition for the existence of FDRs. In the more specific case where , for all and , necessary and sufficient conditions can be obtained for the existence of FDRs. We refer the interested reader to [Lan19, Section 3.3.2] for a detailed analysis of this situation.

4.3.3. An example: Hull White model with non-constant volatility of the log-spread processes

To exemplify the construction of FDRs for constant direction volatility models described above, we consider a simple model with (i.e., we consider two distinct tenors for risk-sensitive rates, together with the risk-free rate) and , with the following volatility structure:

where are positive constants, for and . This volatility specification is consistent with the empirically observed fact that large values of the spreads are typically associated with high volatility, as large values of the spreads tend to occur in periods of financial turmoil. Moreover, we allow for correlation between forward rates and log-spread processes.

We aim at constructing explicitly an FDR for this three-curve model. We assume that the initial point is such that . By continuity of , we can therefore assume that for all , for some stopping time a.s. In this case, Assumption 4.7 holds true and the Lie algebra generated by the coefficients of the model is finite-dimensional. Since the volatility functions of the forward rate processes are QE functions, Proposition 4.8 can be applied. We therefore obtain that the Lie algebra

is finite-dimensional and contains . In view of Proposition 4.8, this ensures the existence of FDRs for the model considered in this example.

To construct the FDRs, we first compute the dimension of . For each , the polynomial annihilator of is trivially for , while it is for . Analogously, since

and otherwise, the polynomial annihilator of is for , while for it is given by , for . Therefore, we have that

Referring to the family of vector fields introduced in (4.14), we have that and , for all and . Hence, these vectors do not contribute to generate the Lie algebra , which has dimension . In analogy with notation (4.18), we denote a generic vector by .

The tangential manifold is given by the image of the function introduced in equation (4.19). In the present example, the latter is given by

4.4. Realizations through a set of benchmark forward rates and log-spreads

Let us consider a model admitting an -dimensional realization. In general, the state process of the FDR has no economic interpretation. In this section, we show that it is possible to construct another FDR of the same dimension determined by forward rates associated to a fixed set of benchmark maturities together with the log-spreads. This result is interesting in view of applications, where it is useful to find realizations for which the state process admits an economic interpretation and, in particular, can be readily deduced from market observables.

Given the existence of an -dimensional realization, considering a point , we aim at constructing an FDR through the linear functional

| (4.21) |

where is a fixed set of maturities and and are constants. The problem is equivalent to prove that is a local system of coordinates for , for a suitable choice of the constants and . The following proposition provides a positive answer to this problem, generalizing [BS01, Theorem 3.3] to the multi-curve setup. We remark that, differently from the classical single-curve case, in the multi-curve setup each component of the FDR determined by (4.21) is given by a linear combination of forward rates and log-spreads.

Proposition 4.11.

Let be a multi-curve interest rate model admitting an -dimensional realization. Then, for any vector , where each is arbitrarily chosen except for a discrete subset of , the realization can be described by the inverse of the function (4.21), for suitable constants and , for and .

Proof.

We need to prove that the function introduced in (4.21) is a diffeomorphism between and its image. We denote by the Fréchet derivative of , where is the tangent space of at . Since has dimension , is an -dimensional subspace of . Let us consider a basis for , where we adopt the notation , for . Then, for a generic element , there exists such that . By linearity, the Fréchet derivative of can be written as

where

and

| (4.22) |

Therefore, the function is a local system of coordinates if is invertible. Since is composed by analytic functions (see, e.g., [BS01, Proposition 4.2]), a non-null element of has isolated zeroes and we can find a discrete subset such that for all and . Since is a polynomial function of , we can always find a set of vectors , defined as in (4.22) and dependent on , such that for every , where is arbitrarily chosen in except for a discrete set. ∎

5. An alternative formulation of invariance

In the previous sections, the log-spread processes , for , have been treated jointly with the forward rate curves. However, since the log-spread processes are inherently finite-dimensional, we can aim at a formulation of invariance that treats the log-spreads differently from the forward rate components. More specifically, in this section we aim at understanding if the log-spread processes can be directly included in the state process of an FDR.

5.1. The role of log-spreads in the consistency problem

Theorem 3.4 characterizes the consistency between a multi-curve interest rate model and a manifold , which provides a joint representation of forward rates and log-spreads. As explained in Remark 3.5, in a multi-curve setting consistency cannot be addressed for the forward rate components alone. Motivated by this remark, in this section we investigate an alternative formulation of invariance, which directly includes the log-spreads in the state variables. More specifically, adopting the notation , we investigate under which conditions there exist a stopping time a.s., a process taking values in and a function such that

| (5.1) |

This is equivalent to the notion of -invariance (Definition 3.3), for the immersion given by

We can rewrite as follows the Stratonovich dynamics (2.8) of the joint process , distinguishing explicitly the forward rate components from the log-spread processes:

| (5.2) |

We define as follows the alternative notion of invariance considered in this section.

Definition 5.1.

Similarly to the equivalence between Definition 3.2 and Definition 3.3, it can be easily shown that Definition 5.1 is equivalent to Definition 3.2 with . As a consequence, the following result can be proved analogously to Theorem 3.4, characterizing the validity of (5.1).

Proposition 5.2.

Let be a parameterized family such that satisfies Assumption 3.1. Then is -invariant under the action of if and only if, for every :

where and denote the Fréchet differentials of with respect to and , respectively.

5.2. Existence of FDRs in the form of Definition 5.1

In this subsection, we address the issue of the existence of FDRs that can be realized in the form (5.1). We start by observing that, if a multi-curve interest rate model admits an FDR (in the sense of Definition 4.1), then it is always possible to construct another FDR in the form (5.1). Indeed, let us consider an FDR given by a function and a finite-dimensional process such that . We can obviously obtain an FDR of the form (5.1) by considering and the joint process with dynamics

However, the above strategy of adding the whole vector of log-spreads to the state variables of an FDR might yield a joint process with redundant components. It is therefore of interest to determine conditions under which a more parsimonious FDR can be found (to this effect, compare also the two approaches described in Section 3.2 and see Remark 3.7).

We start by noting that the embedding introduced in (4.2) can be decomposed as

for , where takes values in and in . The following assumption ensures the possibility of replacing some components of the state vector by log-spreads.

Condition 5.3.

There exists a subspace , for , that is diffeomorphic to a subspace of the state space through the function .

Under Condition 5.3, we denote by the elements of the diffeormophic subspace of the state space , while denotes a generic element of . For , we write . Without loss of generality, we assume that represents the first components of the log-spread vector , while denotes the last components, so that . Writing , invariance implies that is invertible in , for every . Hence, there exists an inverse mapping such that . Let us remark that Condition 5.3 does not impose additional requirements on the model. Indeed, if a diffeomorphic subspace does not exist, then we can just assume that Condition 5.3 holds with .

To construct an FDR under Condition (5.3), we first recall that FDRs are obtained by a set of generators of the Lie algebra (see Section 4). We denote the generators by . To construct an FDR including the log-spreads among the state variables, it suffices to add the last elements of the canonical basis of to the set of generators . Using notation (4.14), we denote by the -th vector of the canonical basis, for . In line with Theorem 4.2, a parsimonious FDR that includes the vector of log-spreads among the state variables can then be constructed under the following assumption.

Assumption 5.4.

The Lie algebra generated by is finite-dimensional.

Note that Assumption 5.4 does not necessarily hold even if is finite-dimensional. We now aim at obtaining necessary and sufficient conditions for the validity of Assumption 5.4. As a preliminary, we recall the notion of multi-index (see, e.g., [Bjö04, Definition 7.4]).

Definition 5.5.

A multi-index is any vector of dimension with nonnegative integer elements. For a multi-index , the differential operator is defined as

Proposition 5.6.

If the Lie algebra

is finite-dimensional, then

| (5.3) |

Conversely, if commutes with and for every and , then the Lie algebra is finite-dimensional.

Proof.

The Lie algebra contains all Lie brackets of the form

Hence, all the differentials are contained in , for every multi-index . We first notice that coincides with and we observe that the vectors commute with each other, so that their Lie bracket is null. Therefore, in order to have that , it is necessary that and , for , do not generate an infinite-dimensional distribution, for every . This implies the necessity of condition (5.3).

On the other hand, assuming that commutes with and is equivalent to requiring that

for every . By the Jacobi identity, successive Lie brackets commute with : indeeed, it holds that . This implies that the commutativity of with and is a sufficient condition for to be finite-dimensional. ∎

Remark 5.7 (Constant direction volatility models).

In Section 4.3, to prove the existence of FDRs for constant direction volatility models, we studied the Lie algebra , defined in (4.17), that is larger than the Lie algebra . In Proposition 4.8, we provided conditions ensuring that . Under these conditions, we can construct FDRs for which the log-spreads are included in the state variables. Indeed, Assumption 5.4 holds under the conditions of Proposition 4.8, since already contains all the vector fields .

6. Calibration of finite-dimensional realizations to market data

In this section, we study the calibration of a multi-curve interest rate model to market data, relying on the theoretical results presented in Section 4. More specifically, we consider a model admitting FDRs and depending on a parameter vector . The calibration procedure aims at determining the parameter vector that achieves the best fit to the market data. As a result of this procedure, the FDR associated to will represent the submanifold of that gives the best representation (in terms of mean-squared error) of the data under analysis.

We consider a three-curve Hull-White model driven by a one-dimensional Brownian motion, for simplicity of presentation. The model is fully specified by the volatility

where are positive constants, for . This specification is a special case of the constant volatility models studied in Section 4.2 and satisfies the conditions of Proposition 4.5. Indeed, the volatility functions are QE, since , for all . For the model under analysis, the parameter vector is given by . The algorithm described below for calibrating is based on the works of [AH02], [AH05] and [Sli10].

6.1. Construction of the FDRs

We first study the vector fields generating . The annihilator polynomial of the forward rate components of the volatility is given by

By equation (4.8), is the dimension of the FDRs. Accordingly, we consider a state vector in , denoted by , in line with notation (4.10). By following the arguments of Section 4.2, we can construct the tangential manifold determined by the composition of the integral curves of the generators of . The generators are , and

The composition of the integral curves of these vector fields yields the tangential manifold , that can be explicitly computed as follows:

| (6.1) |

The state process is the solution to the SDE , where are vector fields on , respectively defined by the coefficients and introduced in system (4.11). By (4.11), the first component of is simply given by , so that we write . While the dynamics of can be derived explicitly, they are not needed in the following.

6.2. Initial families

The FDRs depend on the initial term structures. For the representation of the initial term structures of the forward rates, for , we adopt the widely used Nelson-Siegel family (see [NS87]), given here in the following form:

| (6.2) |

where and . Observe that in (6.2) we directly use the parameter in the exponents. The Nelson-Siegel family has been also adopted in [Sli10], thus facilitating the comparison of our methodology with that work. As a consequence of (6.2), the initial families of the forward rate components of the model depend linearly on the common vector , the only difference being in the exponent that is specific to each forward rate.

6.3. The calibration procedure

We consider market data at daily frequency . For each day , we extract from market data (by means of standard bootstrapping techniques, see below for more details) risk-free ZCB prices, prices of fictitious ZCBs associated to the risk-sensitive rates, for a set of maturities , and the log-spreads:

| (6.3) |

For every , we minimize the squared error between the yields computed on the market data (6.3) and the yields generated by the FDR (6.1), for all maturities in and for all tenors. We denote by the FDR, highlighting the dependence on the parameter vector to be estimated. The argument represents the realization of the components of the state process, which need to be estimated at each date. We denote by the residual at date , given as follows:

| (6.4) |

The properties of the FDR derived in (6.1) and the choice of the initial family made in (6.2) imply that the yields generated by the FDR are affine in . Similarly as in [AH02], this represents a significant advantage in the calibration algorithm, which is structured as follows:

-

P.1

For each , we minimize with respect to the parameters . Exploiting the affine structure of the yields, the SVD algorithm can be used to obtain and , depending on the parameter vector :

-

P.2

The (time-independent) parameter vector is estimated by minimizing the sum of the squared residuals obtained in the previous step along the entire dataset:

To compute the minimizer , we adopt a reflective trust-region algorithm.

6.4. Market data

For the risk-free rate we rely on OIS rates, while as risk-sensitive rates we consider 3M and 6M Euribor rates, corresponding to the most liquidly traded tenors. The dataset used in our analysis is given by daily market quotes from until . Table 1 presents a snapshot of the market instruments included in our dataset.

| Interest rate curve | Market instrument | Quoted maturities |

|---|---|---|

| Risk-free curve | OIS | 1W - 2W - 3W - 1M - 2M - 3M - 4M - 5M - 6M - 7M - |

| 8M - 9M - 10M - 11M - 1Y - 15M - 18M - 21M - 2Y - | ||

| 3Y - 4Y - 5Y - 6Y - 7Y - 8Y - 9Y - 10Y | ||

| 3M | FRA | 1Mx4M - 2Mx5M - 3Mx6M - 4Mx7M - 5Mx8M - 6Mx9M - |

| 7Mx10M - 8Mx11M - 9Mx12M | ||

| IRS | 18M - 2Y - 3Y - 4Y - 5Y - 6Y - 7Y - 8Y - 9Y - 10Y | |

| 6M | FRA | 1M+7M - 2Mx8M - 3Mx9M - 4Mx10M - 5Mx11M - 6Mx12M - |

| 9Mx15M - 12Mx18M | ||

| IRS | 2Y - 3Y - 4Y - 5Y - 6Y - 7Y - 8Y - 9Y - 10Y |

On the basis of this market data, we compute the risk-free and risk-sensitive term structures, making use of the bootstrapping technique described in [GL20]. The resulting term structures include the following maturities: 1M, 2M, 3M, 4M, 5M, 6M, 9M, 1Y, 2Y, …, 10Y.

6.5. Calibration results

To assess the performance of the calibration algorithm, we compare the market data with the calibrated parameterized family at the end of the considered time window. More precisely, the calibrated parameterized family makes use of the parameter vector calibrated as explained in Section 6.3, while the time-dependent parameters are estimated on the basis of the market data at the end of the time window.

By means of a stability analysis (see Section 6.5.2 below), we have determined that a time window of four months yields the most stable results. We therefore consider a time window of four months, starting at 01/04/2021. The initial guesses for the parameters are given in Table 2. The parameters in Table 2 are randomly chosen in the interval , while is randomly chosen in the interval . The calibrated values are reported in Table 3.

| OIS | / | ||

| Libor - 6M | |||

| Libor - 6M |

| OIS | / | ||

| Libor - 6M | |||

| Libor - 6M |

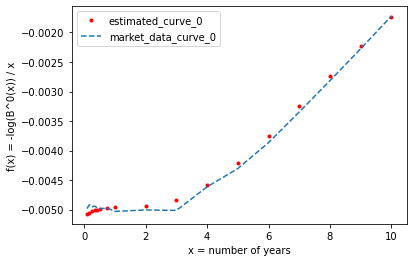

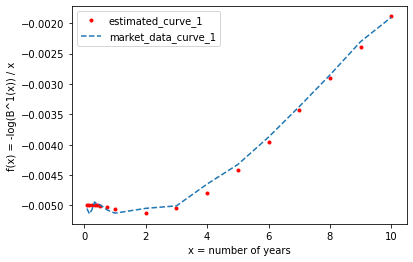

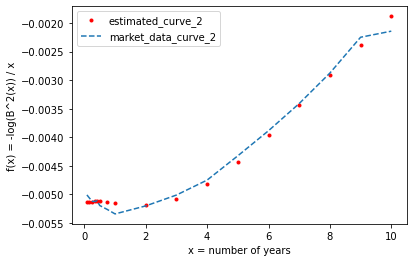

The quality of the fit of the calibrated parameterized family to the market data at the end of the considered time window is illustrated in Figure 1. Apart from the shortest maturities, the quality of the fit appears satisfactory. We can also notice that, due to the unusual monetary policy conditions of 2021, the yields are negative for all maturities. Since the spreads are spot processes, we can compare the calibrated log-spreads with respect to the log-spreads obtained from market data on the whole time window. This comparison is illustrated in Figure 2.

In Table 4, the relative errors are given. The errors have been computed as follows:

-

(1)

if is the calibrated -th yield curve and is the -th yield curve obtained from market data, both considered at the end of the time window, then

(6.5) -

(2)

if is the estimated value of the -th log-spread over the entire time window used for the calibration and is the market value of the -th log-spread in the considered time window, the relative error is

(6.6)

| OIS | 3M | 6M | |

|---|---|---|---|

| yields | 0.01917 | 0.01705 | 0.02385 |

| spread | - | 6.92929e-07 | 8.491172e-07 |

6.5.1. Stability with respect to the length of the time window

When calibrating the model, it is essential to choose in a suitable way the length of the time window. Indeed, a too short time window does not convey sufficient information for a reliable estimation. On the contrary, a too long time window can also be problematic, since consistency is a local property by definition.

In Table 5 we report the relative errors obtained using time windows of different lengths. For the yield curves, we report the error as defined in equation (6.5). For the spreads, we report the relative error between the estimated spread and the market data at the end of the time window. The calibration procedure is always initialized at as given in Table 2. We consider time series of market data ending in 30/07/2021, with lengths 1M, 2M, 3M, 4M, 5M and 6M. This analysis reveals that, for the dataset under consideration, the time length that achieves the best performance is four months, as shown in Table 5.

| length of | Yield curve | Spread curve | |||

|---|---|---|---|---|---|

| months | RFRs | Euribor 3M | Euribor 6M | Spread 3M | Spread 6M |

| 1 | 0.0520 | 0.0524 | 0.0368 | 2.5736e-07 | 2.4474e-07 |

| 2 | 0.0557 | 0.0489 | 0.0371 | 5.6650e-08 | 1.6761e-10 |

| 3 | 0.0213 | 0.0218 | 0.0387 | 4.4926e-07 | 3.8488e-07 |

| 4 | 0.0191 | 0.0171 | 0.0239 | 1.1579e-06 | 9.6982e-07 |

| 5 | 0.0159 | 0.0163 | 0.0334 | 3.1638e-08 | 3.4686e-08 |

| 6 | 0.0213 | 0.0214 | 0.0393 | 1.2390e-07 | 6.3183e-08 |

6.5.2. Stability of the time-independent parameters

In practice, the stability of the calibrated parameters represents an important property. We test this stability through the following procedure, where at each step the length of the considered time window is kept fixed at four months, on the basis of the findings reported in Section 6.5.1:

-

A.1

apply the calibration algorithm with a time window starting at day ;

-

A.2

perform the calibration over a time window starting at day , using as initial guess the parameter values estimated at step A.1;

-

A.3

repeat the previous step, rolling the time window by one day for 50 consecutive steps.

Table 6 reports the results of this procedure, giving the standard deviation of the calibrated parameters. This remarkable stability can be partly explained by the procedure employed. Indeed, in line with the parameter recalibration procedure widely adopted in market practice, the initial guess for the calibration at iteration is chosen as the value estimated at iteration . Since the time window is kept fixed at a length of four months, shifting the time window by one day at each step does not alter significantly the market information, thus explaining the stability of the calibrated parameters.

| avg | 0.371948 | 0.164252 | 0.372120 | 0.159068 | 0.372732 | 0.159813 | 0.481433 | 0.882557 |

| std | 0.000004 | 0.000006 | 0.000003 | 0.000006 | 0.000004 | 0.000004 | 0.000002 | 0.000003 |

References

- [AH02] F. Angelini and S. Herzel. Consistent initial curves for interest rate models. Journal of Derivatives, 9(4):8–17, 2002.

- [AH05] F. Angelini and S. Herzel. Consistent calibration of HJM models to cap implied volatilities. Journal of Futures Markets, 25(11):1093–1120, 2005.

- [BC99] T. Björk and B. J. Christensen. Interest rate dynamics and consistent forward rate curves. Mathematical Finance, 9(4):323–348, 1999.

- [BG99] T. Björk and A. Gombani. Minimal realizations of interest rate models. Finance and Stochastics, 3:413–432, 1999.

- [Bia10] M. Bianchetti. Two curves, one price. Risk Magazine, August:74–80, 2010.

- [Bjö04] T. Björk. On the geometry of interest rate models. In R. A. et al. Carmona, editor, Paris-Princeton Lectures on Mathematical Finance 2003, pages 133–216. Springer, Berlin - Heidelberg, 2004.

- [BL02] T. Björk and C. Landén. On the construction of finite dimensional realizations for nonlinear forward rate models. Finance and Stochastics, 6:303–331, 2002.

- [BLS04] T. Björk, C. Landén, and L. Svensson. Finite-dimensional Markovian realizations for stochastic volatility forward-rate models. Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences, 460(2041):53–83, 2004.

- [BS01] T. Björk and L. Svensson. On the existence of finite-dimensional realizations for nonlinear forward rate models. Mathematical Finance, 11(2):205–243, 2001.

- [CFG16] C. Cuchiero, C. Fontana, and A. Gnoatto. A general HJM framework for multiple yield curve modelling. Finance and Stochastics, 20(2):267–320, 2016.

- [DPZ92] G. Da Prato and J. Zabczyk. Stochastic Equations in Infinite Dimensions. Cambridge University Press, Cambridge, 1992.

- [FGGS20] C. Fontana, Z. Grbac, S. Gümbel, and T. Schmidt. Term structure modelling for multiple curves with stochastic discontinuities. Finance and Stochastics, 24(2):465–511, 2020.

- [FT03] D. Filipović and J. Teichmann. Existence of invariant manifolds for stochastic equations in infinite dimension. Journal of Functional Analysis, 197(2):398–432, 2003.

- [FT04] D. Filipović and J. Teichmann. On the geometry of the term structure of interest rates. Proceedings of the Royal Society of London A, 460(2041):129–167, 2004.

- [FT08] D. Filipović and S. Tappe. Existence of Lévy term structure models. Finance and Stochastics, 12(1):83–115, 2008.

- [GL20] C. Gerhart and E. Lütkebohmert. Empirical analysis and forecasting of multiple yield curves. Insurance: Mathematics and Economics, 95:59–78, 2020.

- [GR15] Z. Grbac and W. J. Runggaldier. Interest Rate Modeling: Post-Crisis Challenges and Approaches. Springer, Cham, 2015.

- [KS12] I. Karatzas and S. Shreve. Brownian Motion and Stochastic Calculus. Springer, New York, 2nd edition, 2012.

- [Lan19] G. Lanaro. The geometry of interest rates in a post-crisis framework. Master thesis, University of Padova - Dept. of Mathematics, available at https://hdl.handle.net/20.500.12608/24253, 2019.

- [MM18] A. Macrina and O. Mahomed. Consistent valuation across curves using pricing kernels. Risks, 6:1–39, 2018.

- [NS87] C. R. Nelson and A. F. Siegel. Parsimonious modeling of yield curves. Journal of Business, 60(4):473–489, 1987.

- [Sli10] I. Slinko. On finite dimensional realizations of two-country interest rate models. Mathematical Finance, 20(1):117–143, 2010.

- [Tap10] S. Tappe. An alternative approach on the existence of affine realizations for HJM term structure models. Proceedings of the Royal Society A, 466(2122):3033–3060, 2010.

- [Tap12] S. Tappe. Existence of affine realizations for Lévy term structure models. Proceedings of the Royal Society A, 468(2147):3685–3704, 2012.