Semi-parametric local variable selection under misspecification

David Rossell,

Pompeu Fabra University

and

Arnold Kisuk Seung,

University of California at Irvine

and

Ignacio Saez,

Mount Sinai

and

Michele Guindani

University of California at Los Angeles

Abstract.

Local variable selection aims to discover localized effects by assessing the impact of covariates on outcomes within specific regions defined by other covariates. We outline some challenges of local variable selection in the presence of non-linear relationships and model misspecification. Specifically, we highlight a potential drawback of common semi-parametric methods: even slight model misspecification can result in a high rate of false positives. To address these shortcomings, we propose a methodology based on orthogonal cut splines that achieves consistent local variable selection in high-dimensional scenarios. Our approach offers simplicity, handles both continuous and discrete covariates, and provides theory for high-dimensional covariates and model misspecification. We discuss settings with either independent or dependent data. Our proposal allows including adjustment covariates that do not undergo selection, enhancing flexibility in modeling complex scenarios. We illustrate its application in simulation studies with both independent and functional data, as well as with two real datasets. One dataset evaluates salary gaps associated with discrimination factors at different ages, while the other examines the effects of covariates on brain activation over time. The approach is implemented in the R package mombf.

Keywords: local null testing, semi-parametric model, Bayesian model selection, Bayesian model averaging, functional data

Local variable selection, or local null hypothesis testing, is a critical issue in many areas of science. In statistical terms, this problem arises in scenarios where researchers are provided with a set of covariates of interest, denoted as , and are tasked with testing whether they have an effect on an outcome , at specific values indicated by additional covariates . For example, consider evaluating whether

disparities in salary () are associated to covariates such as race and gender () at different career stages (). Although there may be no evidence of such disparities based on race among individuals who have recently entered the workforce (e.g., as a result of newly implemented policies aimed at addressing this matter), there may still exist disparities based on gender and at other career stages.

In another application we discuss here, we test whether patient or experiment covariates () are associated to brain activity () at various time points (). For a broader discussion and further examples, including both independent and dependent data scenarios, we refer to Paulon

et al. (2023). It is important to note that the primary objective in all these examples is testing (multiple) scientific hypotheses indexed by , not merely estimating covariate effects on the outcome. Indeed, our examples illustrate how estimation-focused methods such as tree ensembles, may be prone to considerable false positive inflation.

Semi-parametric models provide a natural framework for analyzing the effect of at various to address local variable selection, particularly when the sample size or computational power are not sufficient for the use of fully non-parametric methods, or one wishes to use simpler models to facilitate interpretation. While semi-parametric models are a standard tool for statisticians (e.g., generalized additive models, Cox proportional hazards model), their application to local variable selection has not been extensively studied. Our research primarily contributes in two significant ways.

Firstly, we offer a theoretical analysis that highlights a critical potential drawback of standard semi-parametric methods. When the model is even slightly misspecified (as is unavoidable in practice), the type I error of most methods that test a precise null hypothesis converges to 1. This raises a significant concern for local variable selection.

Secondly, we propose a strategy to address this pitfall through a simple modification that preserves the interpretability and computational features of semi-parametric models. We give theoretical and empirical evidence that our approach achieves consistent (local) variable selection in scenarios where the model is misspecified. To our knowledge, these results are the first of their kind for high-dimensional local variable selection under misspecification.

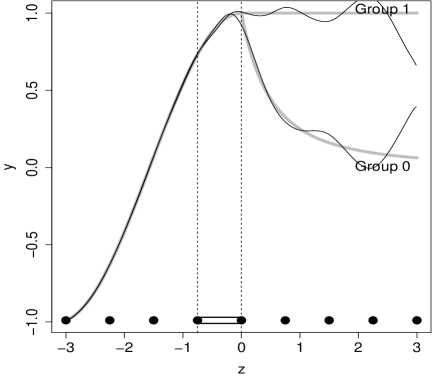

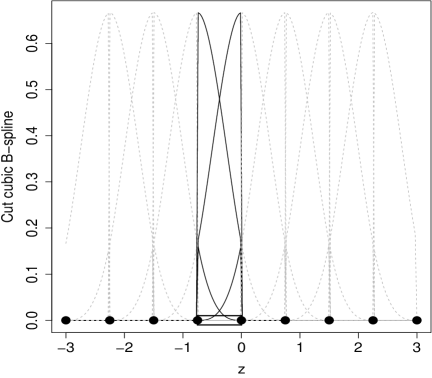

Before discussing related literature, Figure 1 illustrates potential issues that arise when the assumed model misspecifies the true mean structure (see Section 5.1 for details). There is a single binary covariate, , defining two groups. The true group means are equal for and different for . The goal is to identify the set of ’s at which the group means differ, based on observations. Suppose we employ a semi-parametric model based on cubic B-splines, and fit it to the combined data from both groups. The solid black lines in Figure 1 depict the projection of the true group means onto a cubic B-spline basis, i.e. the best approximation that one may recover as . The critical issue emerges when we observe that the projected means are no longer equal for (left panel). As grows, we will erroneously detect differences between the group means for , although truly no differences exist.

Here the sample size is moderate and the projected group means are only subtly different for , nevertheless this suffices to run into significant type I error issues. Specifically, the right panel shows that a near-one posterior probability is assigned to group differences for (similar issues occur when using posterior intervals or P-values). We note that we employed a moderate number of knots, 20 for the baseline mean and 10 for the group differences. Adding knots as grows is standard in estimation and forecasting problems and could mitigate type I error inflation. Alas, in our model selection context, the model space size grows exponentially with the number of knots, and the power to detect local differences diminishes. Therefore, it is desirable to have methods that can effectively operate with relatively few knots.

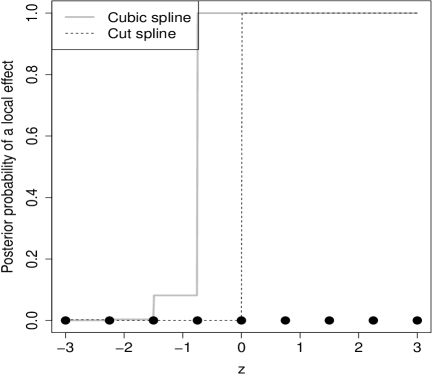

Figure 1. A simulated illustration. True group means and their cubic B-spline projections (left), and posterior probability of local group differences for cubic and cut cubic B-splines based on (right).

This paper considers settings with independent data, where the goal is to perform local variable selection, and some extensions to dependent data. The latter setting received considerable attention in the literature.

For instance, Boehm Vock et al. (2015) addressed local variable selection by combining spike-and-slab priors with latent Gaussian processes, an approach extended by Jhuang et al. (2019) using horseshoe priors. Kang

et al. (2018) applied a soft-thresholding operator to a Gaussian process for local variable selection. For functional data observed over a common grid (e.g., mass spectrometry, images), Morris et al. (2011) and Zhu

et al. (2011) employed basis functions such as wavelets, Fourier transforms, and splines.

These methods test whether covariate effects are near 0, rather than exactly 0 as is our goal here. There is also abundant research in settings where is discrete. For example, Smith and

Fahrmeir (2007) proposed a Bayesian framework for regressions on a lattice, whereas Scheel et al. (2013) and Choi and

Lawson (2018) focused on variable selection over discrete spatial locations.

A work related to ours is the model by Deshpande et al. (2020) , who employed Bayesian additive regression trees (BART) for varying-coefficient models, both with independent and dependent observations, and established near-minimax estimation rates when the number of covariates grows at a rate slower than . However, their work did not provide theory for variable selection. Furthermore, Paulon

et al. (2023) considered a non-parametric framework for time-varying variable selection with discrete covariates, aiming to detect high-order covariate interactions. They established parameter estimation and variable selection consistency for a fixed number of covariates. Here we consider a simpler semi-parametric model that does not require longitudinal data, allows for continuous and discrete covariates and multivariate , and provides high-dimensional theory under model misspecification.

The fundamental aspect of our approach lies in using basis functions that capture covariate effects in a local manner for each neighborhood

and are orthogonal to the basis functions used outside that neighborhood. We refer to this construction as an orthogonal cut basis. It can be viewed as an extension of a piece-wise constant parameterization that maintains certain orthogonality properties and allows including higher-degree terms (e.g., cubic terms, as shown in Figure 1). In settings with dependent data, an additional element is required: a block-diagonal approximation to the covariance that captures local dependence. Combined with the orthogonal cut basis, such a purposedly misspecified dependence model ensures consistent local variable selection as .

We set notation. Let be the observed outcomes,

a vector of covariates for individual , and the “coordinates” of interest. In one example is the salary of individual and the age, in another is the brain activity for a given patient at time .

The goal is to evaluate the effect of on at each possible .

We remark that our theory and methods also hold when is multivariate. However, our examples focus only on univariate for simplicity and clarity. Furthermore, effectively deploying the methodology to multivariate functional data in practice requires thorough work in specifying suitable dependence models that falls beyond our scope. Additionally to , there may be additional adjustment covariates that one includes in the model without undergoing testing. For simplicity we omit said covariates from our exposition, but they are implemented in our software and used in our salary example.

We denote the (unknown) data-generating density of as , which generally lies outside the assumed model class. For purposes of local null testing, it is convenient to partition the support of into a set of regions (e.g., the 9 intervals in Figure 1). We will later discuss that one may consider multiple such sets of regions and obtain combined inference via Bayesian model averaging. However, for ease of exposition we consider a single for now.

The paper is organized as follows. In Section 1, we first discuss a simpler scenario involving a single discrete covariate (group comparisons), which highlights the main issues arising from model misspecification. We then propose a solution based on orthogonal cut bases. In Section 2, we extend these ideas to multiple covariates. Section 3 presents a Bayesian framework for local variable selection, and Section 4 establishes its asymptotic validity.

Specifically, we prove that asymptotically one detects which covariates are conditionally uncorrelated with the outcome (given the remaining covariates) at each considered coordinate (), i.e. one attains consistent local variable selection.

By Slutsky’s theorem, these results imply that our Bayesian model averaging posterior on the parameters converges to the posterior under the optimal model, where only non-zero parameters are included, hence one also obtains accurate point estimates and asymptotically valid posterior credible intervals.

Section 5 shows examples, considering both independent errors and functional data. Finally, Section 6 concludes.

The supplementary material contains all proofs, and R scripts to reproduce our analyses.

Our methods are implemented in the R package “mombf”.

1. Local variable selection in group comparisons

1.1. Local selection in model-based tests

We consider first the case of a single discrete covariate, , which defines distinct groups.

Suppose that the true data-generating process, unbeknownst to the data analyst, is characterized by an expectation given by a baseline function plus an interaction term .

Specifically, we posit that

(1)

where and indicate continuous functions in . An identifiability condition is required in (1), e.g.

a sum-to-zero constraint at each ,

so that

represents the deviation from the baseline mean for group at .

The objective of local variable selection is to assess whether the groups have a zero effect at a specific value of , as indicated by the interaction term . This is expressed by the local null hypothesis:

(2)

In practice, the true data-generating distribution , as well as the functions and , are unknown and need to be approximated.

A common strategy is to model and using basis functions (such as splines) and to assume a specific error model for the outcome , say Gaussian.

More specifically, let us consider the approximation of with and with , where and evaluate the chosen basis at and denote the corresponding coefficient parameters.

Then, (1) is approximated by

(3)

Equation (1) describes a so-called varying coefficient model (Hastie and

Tibshirani, 1993), where the regression coefficients and depend on .

Assuming Gaussian errors, we can express (3) in matrix notation as:

(4)

where is an matrix with row given by , is an matrix with row given by , and represents the error covariance. For instance, one may assume independence and take for some , or consider an appropriate model for dependent data (e.g., autoregressive).

To ensure identifiability, we impose an orthogonality constraint in a manner that represents the baseline mean and represents group deviations from the baseline. This is easily achieved by defining with a standard basis (e.g. splines) and defining to be the residuals from regressing that basis onto , see Section 1.2.

For simplicity, we assume that is non-random, meaning that the covariates and coordinates are fixed, and that any subset of with columns has full column-rank.

Under the model specified in (3), the local null hypothesis can be expressed as

(5)

where is the basis function of evaluated at a specific .

In other words, the local null test at a given assesses whether a particular linear combination (given by ) of the parameters is zero.

To facilitate interpretation, we use a local basis such that conducting the test for any within a given region

is defined by finding zeroes in (rather than in linear combinations ).

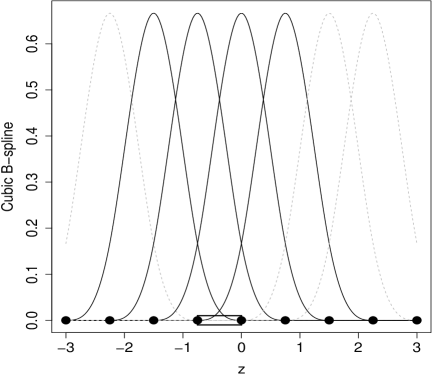

By a local basis, we mean that the value of in each region is defined by a small subset of parameters in . For instance, B-spline bases have minimal support among all spline bases: in an -degree B-spline, each interval between consecutive knots is represented by coefficients.

Figure 5 (left) illustrates a cubic B-spline () in which a local hypothesis is tested for (black square) with groups.

Only bases (marked in black) have nonzero values in this interval, specifically bases 2-5. That is, if it then follows that for all , where we recall that the deviation of group from the baseline is given by , from the identifiability constraint discussed above.

1.2. Model Misspecification and orthogonal cut basis

One of our main messages is that model-based tests, such as (5), can lead to incorrect conclusions when the mean model is misspecified, i.e. the approximation (4) does not perfectly capture the true mean (1).

Under mild conditions, most estimators for the parameters in Equation (4) converge to the optimal values that minimize the Kullback-Leibler divergence.

Consider the independent errors case, with in (4). Then, the asymptotically optimal value minimizes mean squared prediction error under the data-generating truth , and is given by a least-squares regression of on ,

(6)

The issue is that the optimal coefficient values in associated with a specific region may be non-zero even when the group means are equal in that region. In Figure 1,

although the group means are equal for all , the optimal coefficients associated to this region are non-zero.

As , standard frequentist and Bayesian tests provide overwhelming evidence for a group effect at such values, resulting in false positives. This issue remains problematic even when the sample size is moderate, as in Figure 1 where .

Intuitively, the issue arises because the coefficients also play a role in approximating the group means outside the region , e.g. by setting non-zero entries in one obtains a better approximation to the true group means for values .

To address this issue, we introduce the concept of an orthogonal cut basis. This is a basis for that has support only in a region of values and is orthogonal to bases outside that region.

This ensures that the optimal coefficients in (6) contain zeroes when there are truly no group differences in a region, e.g. for in Figure 1.

This occurs because the cut basis only captures the local effects within the region of interest and does not contribute to approximating the group means outside that region. Figure 5 (right) shows a cut cubic B-spline basis.

Specifically, a cut B-spline basis for region is equal to the B-spline basis in and to 0 outside .

Cut bases, similar to tree-based regression methods, can introduce discontinuities in the estimated group differences. It is important to note that the baseline mean, denoted as , can still be assumed to be continuous. Using B-splines for the baseline mean and cut B-splines for the covariate effects combines desirable features of continuous semi-parametric and discontinuous non-parametric methods.

We next describe orthogonal cut basis more precisely and show that the asymptotic solution contains zeroes when there are no local group differences. We partition the support of into regions and select a basis that satisfies two conditions.

Let indicate the rows in that correspond to the observations in region (i.e. ).

The first condition is to employ a cut basis for group effects within each region .

This implies that and the cut basis can be written as

(7)

The second condition is that be orthogonal to , i.e. , and is satisfied as follows. Let be a cut basis (e.g. cut B-splines in Figure 1) such that , then we set

which are the residuals obtained from regressing onto . Consequently, .

We refer to any satisfying (7) and as an orthogonal cut basis.

Lemma 1 below states that the asymptotic , which quantifies the group differences in region , is obtained by regressing the true mean onto (see Section 7 for the proof).

Therefore, if is not linearly associated with in region (the data-generating group means are equal in that region), it follows that .

Lemma 1.

Consider in (6), where , is an matrix and an an orthogonal cut basis as in (7) satisfying .

Let where are the parameters associated to .

Then, .

1.3. Functional data

The presence of dependent observations, as in functional or longitudinal data observed on a dense grid, can introduce additional challenges.

More specifically, when assuming a given , the asymptotic solution becomes

(8)

where is defined as in (6). Unless the second term in the right-hand side of (8) is zero, differs from ,

meaning that the optimal estimator for independent and dependent data are not equal.

Hence, even if contains zeroes – as guaranteed by Lemma 1 when using orthogonal cut basis – may not contain zeroes.

Intuitively, under correlated errors, the optimal parameters for one region depend on those from the other regions. To address this issue, we employ a block-diagonal approximation for that accounts only for within-region dependence.

More in detail, we assume that is equal to some for observations in region and 0 elsewhere.

We also assume independence across functions, i.e. is also block-diagonal, with blocks corresponding to observations for each individual function.

The use of a block-diagonal approximation is reasonable in many functional data applications, as long-range dependence tends to be weak. Related ideas on marginal composite likelihood methods can be found in Caragea and

Smith (2006), and Varin

et al. (2011) (Section 3.1).

In the case of functional data, assuming that the covariates in have zero column means, it can be shown that using such a block-diagonal covariance matrix leads to an asymptotic in (8) that contains zeroes when a covariate has no local effects. The key idea is that Lemma 1 can be extended to , yielding

We refer to Lemma 2 for a precise statement.

If does not differ across groups in region then it is linearly independent of and hence also of ,

and then by Lemma 2.

In our implementation, we adopt an approximation where we assume a common parametric covariance structure across functions. Based on our experience, this allows for a relatively precise estimation of . In particular, we propose obtaining using either a first-order autoregressive or moving average model, selecting the preferred model based on the Bayesian information criterion. Subsequently, we perform inference assuming that is known. This is convenient in that one can take as a working model

(9)

where , and .

This representation enables us to readily apply standard Bayesian independent errors calculations on , including model search and posterior sampling strategies.

We note that our theoretical framework and methodology are applicable to scenarios involving multivariate . However, effectively implementing the approach in a multivariate context would likely require alternatives to the auto-regressive and moving average models we employ here. Therefore, exploring these alternatives and their implementation is left as future work.

2. Extension to multiple covariates

We extend our approach to settings involving a covariate vector . In this case, the data-generating truth in (1) is expanded to

.

Similar to (1), we consider an identifiability constraint so that represent the baseline mean and represents deviations from the mean. Therefore, the local null test for covariate at corresponds to assessing whether depends on or not. To impose this constraint, we orthogonalize the basis used for with respect to that for , as explained below.

As previously discussed in relation to (3), model-based approaches for local variable selection involve approximating using a suitable function class and then expressing the selection in terms of the parameters of that class. While it is possible to model non-parametrically, and assess the effect of at each given , the computational burden increases sharply as or the number of possible values increase (the model space grows exponentially with the number of parameters). Instead, we consider a semi-parametric model that assumes additive covariate effects,

(10)

Analogously to (3), approximates ,

provides an additive approximation to ,

and are basis expansions computed from ,

and are the corresponding parameters.

We denote the total number of parameters as .

Note that the expectation under the data-generating truth may not be additive, e.g. the effect of covariate at may interact with that of covariate . However, the parameters in the assumed model (10) remain interpretable, e.g. is the mean effect of covariate at coordinate , averaged across the values of other covariates. Hence, even in the face of potential model misspecification, testing whether remains a sensible goal.

Note also that if desired one may relax the additivity assumption, e.g., by incorporating interactions and tensor products, and define to be the vector containing all such terms. However we do not pursue that here, rather we focus on providing a model that tests for average local effects and remains easy to interpret.

Assuming a Gaussian distribution for , (10) can be written as

(11)

where is as in (4) and is an orthogonal cut basis as in (7). The only difference relative to (7) is that we extend , the basis for local covariate effects, by multiplying it by the value of each covariate (akin to interaction terms in standard regression).

For brevity we omit details, which are provided in Section 8.

There we also discuss that, since is an orthogonal cut basis, Lemmas 1 and 2 still apply:

if is linearly independent of covariate given the other covariates, then the asymptotic covariate effect in region is (for dependent data, ).

As a practical remark, although our discussion applies to generic basis functions that can be quite flexible, such as cubic splines, the computational burden can become substantial when dealing with many covariates. In our examples, we found that using cubic splines for defining the baseline () and 0-degree splines for the local covariate effects led to faster computations without compromising the quality of inference for local variable selection.

3. A framework for local null testing

Equation (11) defines the likelihood associated to the observed , given the design matrices constructed from the covariates in , the coordinates in , and the corresponding parameters .

As described in (18), under model (11), testing for the effect of covariate in region is equivalent to testing versus , resulting in a total of tests.

Section 3.1 below discusses how to incorporate these tests into a standard Bayesian model selection framework.

Section 3.2 proposes default priors.

In Section 3.3, we explore an alternative approach where instead of pre-defining a fixed set of regions, multiple resolutions are considered. These resolutions can be combined using Bayesian model averaging, providing flexibility and adaptability in capturing the underlying structure of the data.

3.1. Bayesian model selection and averaging

In order to describe any arbitrary model within the local variable selection process, we introduce latent variables , where

and

serve as indicators for variable inclusion across regions and covariates . The model size, i.e. the number of non-zero parameters, is denoted as .

The goal is to select the optimal model , where , with minimizing the mean squared prediction error under the data-generating truth in (6) and (8).

When considering model misspecification, represents the optimal model among those under consideration. Specifically, it is the model with the smallest dimension among those that are Kullback-Leibler closest to (see Rossell (2022)).

The posterior probability of model is obtained as

(12)

where indicates the model’s prior probability and the prior on the parameters under model (see Section 3.2).

Given the posterior distribution for the entire vector , one can assess the local effect of covariate in region using the marginal posterior inclusion probabilities

(13)

As shown in Section 4, under mild regularity conditions, converges to 1 as grows, and thus (13) concentrates on uniformly across the pairs .

This guarantees that, for sufficiently large , using either (12) or (13) leads to consistently selecting and vanishing family-wise type I-II error rates.

We propose including local covariate effects that have high marginal posterior probability in (13). Specifically, we set , for some threshold . In our illustrations, we used . This choice ensures that the model-based posterior expected false discovery proportion (FDP)

remains below 0.05, see Müller et al. (2004).

We point out that this procedure also has a connection with frequentist type I errors. According to Corollary 2 in Rossell (2022), for any true , the frequentist probability of falsely selecting a covariate in region under any data-generating is upper bounded by

.

3.2. Priors for the local effects and model selection

Posterior model probabilities in (12) require setting a prior on the models and a prior on the coefficients under each model.

For the latter, we consider a Normal shrinkage prior

(14)

where is a prior dispersion parameter. By default, we set so that the trace of the prior precision equals that of the unit information prior of Schwarz (1978). Note that (14) can be viewed a imposing a penalty on the norm of ,

and that our multi-resolution analysis (Section 3.3) encourages smoothness across coordinates in the fitted regression.

Although we focus our discussion on (14), in settings with very strong dependence and moderate , we found that replacing (14) by a group pMOM prior with default parameters (Rossell

et al. (2021)) helped prevent type I error inflation. Therefore, for dependent data, we recommend the group pMOM prior as the default choice (see Sections 5.2 and 5.4 for examples).

For the model prior, we consider a Complexity prior akin to Castillo et al. (2015),

(15)

where recall that is the total number of parameters defined after (10), a prior parameter, the normalizing constant,

and we consider that, although possibly , one restricts attention to models with parameters, where is a user-defined bound such as (since models with result in data interpolation).

For the prior probabilities decay exponentially with the model size, , and then equal prior probabilities are set on all models that have the same size.

Setting returns the Beta-Binomial(1,1) prior of Scott and

Berger (2006), i.e. a uniform prior on the model size,

which served as the basis for the extended BIC of Chen and

Chen (2008).

Indeed, while our primary emphasis is on Bayesian methods, the theoretical results shown in Section 4 can be seamlessly adapted to the extended BIC framework by setting and . In our theoretical framework, we consider a general value for . However, in our practical examples we set , since for finite in on our experience this yields a better balance between sparsity and power to detect non-zero coefficients.

3.3. Multi-resolution analysis

So far, to simplify exposition, we assumed that a predefined set of regions is used for performing the local null tests, such as the 8 intervals shown in Figure 1.

In practice, it is often unclear what regions to use, or in other words, what resolution is appropriate for the local variable selection.

To illustrate this point, consider a scenario where there is a single binary covariate that defines two groups, and we are interested in comparing across these groups. If the group differences remain roughly constant across large regions in , it would be advantageous to use a coarse resolution with fewer regions, to increase statistical power. In contrast, if the group differences change rapidly with , a finer resolution with more regions may be preferred, for capturing local variations and detecting smaller-scale differences between the groups.

In practice, the choice of the maximum number of regions is typically guided by computational limitations (as the model space grows exponentially) or because higher resolutions offer limited practical interest. A multi-resolution analysis is instrumental in determining if a coarser resolution might be more suitable.

For example, in our salary application, we consider 2.5- year bins as the highest resolution, since policies or other measures targeting salary discrimination are unlikely to have noticeable effects in shorter time spans. Interestingly, our multi-resolution analysis places most posterior probability on (coarser) 5-year intervals. See Section 5.4 for a related discussion on our brain data.

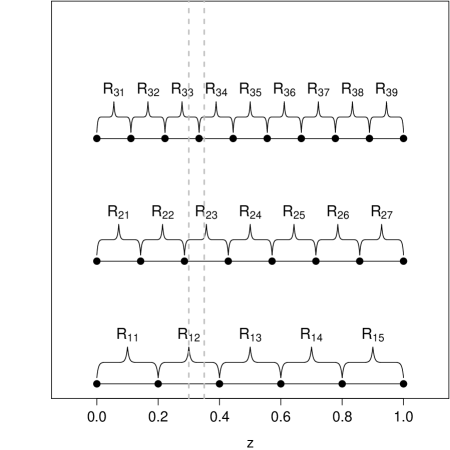

Figure 2. Multi-resolution analysis: an illustration considering 3 resolution levels with , defining 5, 7 and 9 regions respectively.

If we focus on resolutions 1-2, one can note that if and only if (dashed lines), leading to prior dependence across . See Section 3.3 for details.

Bayesian model averaging provides a natural framework for considering multiple resolution levels. We consider resolutions, where each resolution consists of a set of regions . An example with three resolutions and their corresponding regions is shown in Figure 2. Similar to Section 3.2, let and for and represent the set of parameters and models associated with resolution ,

where the latent indicates whether covariate has an effect in region . We consider a joint prior that factorizes as follows,

where is as in (14),

and the model selection prior in (15) is modified to accommodate the multi-resolution setting as follows,

(16)

where is the number of parameters for resolution , and the normalizing constant.

Finally, by default, uniform prior probabilities are assigned to the resolution levels, i.e., .

The multi-resolution formulation induces dependence in the local variable selection across nearby values, as illustrated in Figure 2.

Specifically, the probability of a local effect is ,

where is constant across all values within the same interval at resolution . Hence, nearby and receive similar prior probabilities and .

The corresponding posterior probabilities are

where given a resolution level is given in (13), and

is the marginal likelihood of resolution .

We remark that our multi-resolution strategy is designed to facilitate parallel computation across different resolutions. We define a distinct model for each resolution , obtain separately for each resolution, and then compute their weighted average.

A natural alternative would involve inducing prior dependence across resolutions. This is because, if for example for all at a certain resolution, then also holds true at any coarser resolution. However, we chose not to adopt such more advanced priors here. The primary reason is that computations would no longer be easily parallelizable. Moreover, in our examples, our simpler prior proved sufficiently effective.

4. Theoretical results

We present two main results describing the asymptotic behavior of the proposed cut basis framework. First, we obtain rates at which the Bayes factor favors the optimal model over some other model (Theorem 1). Then, we establish that the posterior model probabilities consistently select (Theorem 2).

These results imply that asymptotically one detects which covariates have an effect at each considered coordinate , and hence attains consistent local variable selection. As discussed in Section 2, since the assumed additive structure in (10) may be misspecified, consistency refers to detecting non-zero marginal effects of each covariate in , averaged across the values of other covariates in .

We consider high-dimensional settings where the total number of parameters can grow with .

The size of the optimal model may also increase with .

We assume that the data-generating has sub-Gaussian tails, specifically satisfies

for some .

This assumption allows for to be dependent. For example, if for some positive-definite , then where is the largest eigenvalue of .

We consider a misspecified setting where the data analyst specifies a model that may not match .

To simplify the exposition and proofs, we assume that the specified model has a fixed covariance, .

Specifically, data analyst specifies the model

(17)

where is a positive-definite matrix, and .

We recall that, when the columns in have zero sample mean and unit variance, in our default choice for the prior in (14), we set and , which is a minimally informative prior. Our theory allows for other and , e.g. letting grow with to enforce sparsity, at the cost of decreased statistical power, see Narisetty and

He (2014); Rossell (2022) for further discussion.

4.1. Bayes factors

The Bayes factor compares a model with the optimal , see Section 10 for its expression, such that when is close to zero then is favored over . We give the rates at which converges to 0 in probability as , assuming the following regularity conditions.

(A1)

The matrix has full column rank .

(A2)

Let be the smallest and largest eigenvalues of .

They satisfy for all and some constants .

(A3)

exists. Its largest eigenvalue satisfies for constants .

(A4)

.

(A5)

Let ,

where ,

.

For some sequence such that ,

The conditions are fairly minimal, for brevity we refer their discussion to Section 11.

A key quantity is in Assumption (A5), it is a non-centrality parameter measuring the sum of squares explained by the optimal but not by model .

Under eigenvalue and beta-min conditions, is lower-bounded by times the smallest square entry in the optimal coefficients (see, e.g., Rossell, 2022, Sections 2.2 and 5.4).

Before stating Theorem 1, we interpret its main implications.

Part (i) indicates that overfitted models, which include all parameters in and some extra, are essentially discarded at a polynomial rate .

Part (ii) states that non-overfitted models, which are missing parameters from , are effectively discarded at an exponential rate in , times a polynomial rate akin to that in Part (i).

In the theorem statement the sequence should be considered as a lower-order term, e.g., , and as a constant close to 0.

Theorem 1.

Let be any sequence such that . Assume (A1)-(A5).

(i)

Overfitted models. If , then

(ii)

Non-overfitted models. If , then for all fixed

where is the sub-Gaussian parameter, the largest eigenvalue of

and is a constant under Assumption (A2).

4.2. Model selection consistency

Theorem 2 below shows that the posterior probability of the optimal model as and provides the associated rate.

The result bounds separately the total posterior probability assigned to the set of overfitted models (),

and to non-overfitted models that are either smaller () or larger () than the optimal . This decomposition helps understand false positive versus power trade-offs.

Theorem 2 requires additional conditions involving the sub-Gaussian parameter of the data-generating , the largest eigenvalue of , the prior dispersion parameter in (14), and the model prior parameter in (15). More specifically,

(B1)

The optimal model has size , where is the maximum model size in (15).

(B2)

.

(B3)

is non-increasing in model size and, for any ,

(B4)

For some ,

(B5)

For any not over-fitted model of size and any fixed ,

where

(B6)

Let . Then,

(B7)

For some ,

.

Assumption (B1) says that the optimal model has positive prior probability. Assumption (B2) is a worst-case scenario, one obtains faster rates in Theorem 2(i) and (iii) if , see the proof for details.

Assumption (B3) is a mild requirement that and are not too small relative to the model size .

(B4) bounds the total number of parameters as a function of , and is satisfied by setting a large (sparse model prior) or (dispersed coefficient prior).

Assumptions (B5) and (B6) are stronger versions of (A5) requiring that the non-centrality parameters are large enough.

Altogether, (B4)-(B6) limit the amount of prior sparsity induced by the model prior parameter and the prior dispersion , relative to and .

Finally, Assumption (B7) is similar to (B2)-(B3) and ensures that the rate in Theorem 2(iii) converges to 0.

(B7) is stronger than needed but simplifies the exposition, please see Assumption (B7’) and Theorem 3 in Section 16 for further details.

Theorem 2.

(i)

Assume (A1)-(A5) and (B2)-(B4). Let .

There exist constants and such that, for all and ,

(ii)

Assume (A1)-(A5), (B1), (B2), (B5) and (B6). Let be the signal strength parameter in (B6),

and .

For and fixed ,

for a constant that may be taken arbitrarily close to 0.

(iii)

Assume (A1)-(A5), (B1), (B2), (B5) and (B7).

Let .

There exist constants and such that, for all and ,

In Theorem 2, should regarded as being close to . Theorem 2 (i) and (iii) state that overfitted and large non-overfitted models (respectively) receive vanishing posterior probability as grows, at a rate that is faster when the prior complexity and the dispersion parameters are large, and slower when either the optimal model is not sparse (i.e., is large) or is large.

In the well-specified case where is Gaussian with independent observations, then . Hence, the condition reflects that under strongly dependent data or model misspecification, convergence rates get slower.

Similarly, Part (ii) states that small non-overfitted models are discarded at an exponential rate in , which gets slower when and when either or are large. Note that if are large, i.e. chosen to favor smaller models, then the convergence rate is slower. This reflects the intuitive notion that, by inducing stronger sparsity, the statistical power to detect truly active coefficients is reduced.

5. Empirical illustration

We assess the performance of our framework through simulations and two examples. Section 5.1 considers a simulation with independent errors to compare our cut orthogonal basis with standard (uncut) cubic splines, the VC-BART of Deshpande et al. (2020) for fitting a varying coefficient model using Bayesian additive regression trees, and a least-squares regression where one obtains Benjamini-Hochberg adjusted P-values for interactions between each covariate and discretized coordinates .

Section 5.2 extends the simulations to functional data with highly dependent errors.

Here, we compare our approach to the LFMM method of Paulon

et al. (2023) and to the interval testing procedure of Pini and

Vantini (2016).

The latter is designed for a single covariate and the former is designed to detect high-order interactions between multiple discrete covariates. Finally, Section 5.3 analyzes a salary survey data from independent individuals,

and Section 5.4 considers functional data from a neuroscience experiment.

For our methodology, we used a cubic B-spline with 20 knots for the baseline and a multi-resolution analysis involving 7, 9 and 11 knots to evaluate the covariate effects.

We considered cut basis of degree 0 (piecewise-constant) and 3 (cubic) but we only report the results from the former, since the results were very similar.

Following our previous discussion, we used the Gaussian shrinkage prior (14) for the independent error settings, whereas we used the group product moment prior of Rossell

et al. (2021) for functional data, in both cases with default parameters.

For our computations, we used Markov Chain Monte Carlo sampling to search over models characterized by different , and to obtain posterior probability estimates for the covariate effects as well as posterior samples for all the model parameters. For this purpose, we used the default specifications in the R package mombf (10,000 Gibbs iterations, with 500 burn-in). Since these are standard MCMC algorithms we do not outline them here for brevity, and refer the reader to Rossell and

Telesca (2017).

5.1. Simulation with independent errors

We illustrate the issues that may arise when employing a standard cubic B-splines for local variable selection, and how these issues are addressed by using a cut orthogonal basis.

We consider two scenarios, with and . In both cases, we consider covariates, and a regular grid of values for . The first covariate is a binary group indicator with equal group sizes. The remaining covariates are generated from a normal distribution with mean , and variance 1, . This results in a mild empirical correlation between and each remaining covariate of 0.43.

The expected outcome is set to depend truly only on the first covariate, and that only when , as depicted in Figure 1 (grey lines).

More in detail, we set the following model

We consider 100 independent replicates of each scenario.

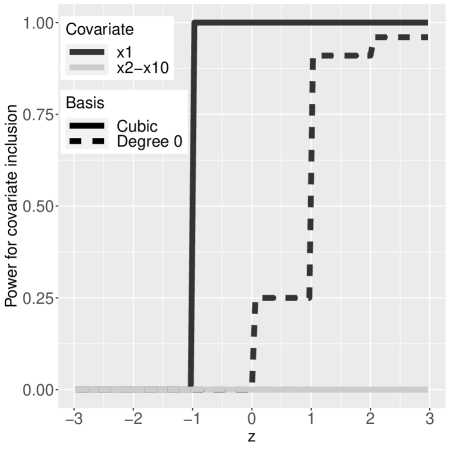

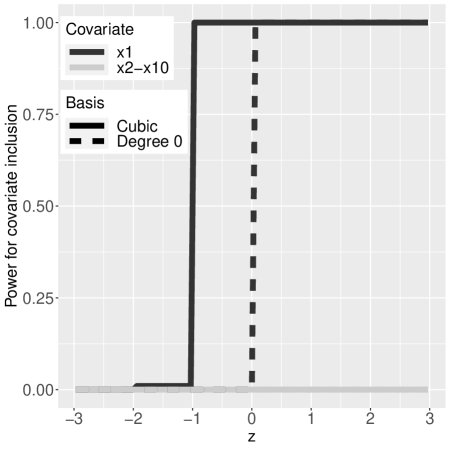

Table 2 shows the type I error and power for the cut and standard B-spline basis, and for the Benjamini-Hochberg P-value adjusted method. The latter exhibits a low type I error, but the power is very low for small . For example, for and , the estimated power for covariate 1 is 0, whereas for the proposed cut basis, it is 0.91. This finding highlights the importance of conducting local variable selection: by learning that covariates 2-10 are unnecessary, the power to detect local effects for covariate 1 increases significantly.

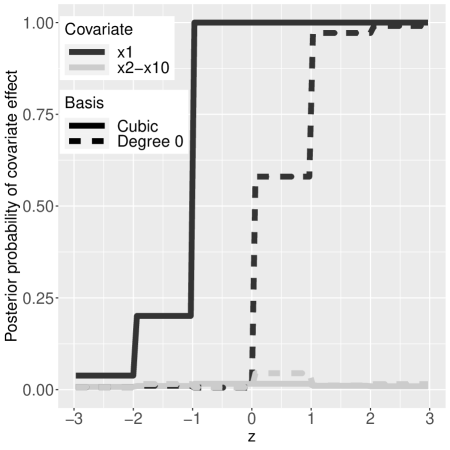

One striking result that strongly supports our theoretical arguments is that when employing cubic splines for the local tests, both the posterior probabilities of rejecting the null hypothesis and the type I error for covariate 1 are near 1 for values . The 0-degree orthogonal cut spline is not affected by these issues. In this example it yields near-perfect inference, except that for , the power to detect for is approximately 0.25.

Figure 6 further illustrates these results. The left panel displays the average posterior probabilities across the simulation replicates while the right panel presents the power function. Both panels once again reveal that standard B-splines run into false positive inflation for covariate 1 at .

We also evaluated the performance of VC-BART. However, we found that VC-BART reported local effects for (truly inactive) covariates 2-10 in all simulations when using a threshold of 0.95 posterior probability inclusion in a tree. Due to this high false positive rate, we chose not to include VC-BART in Table 2 or Figure 6.

Nevertheless, we included VC-BART in Table 3, showing the root mean squared estimation error for the local effects , averaged across covariates and . Standard cubic B-splines achieved a low estimation error, and VC-BART also performed reasonably well. This highlights the fundamental distinction between the two tasks of variable selection and parameter estimation: methods that perform poorly in variable selection may still deliver accurate parameter estimation.

5.2. Functional data simulation

Region

Cut0

LFMM

IT

(-3,-2]

0.02

0.032

0.01

(-2,-1]

0.035

0.032

0.01

(-1,0]

0.047

0.032

0.0131

(0,1]

0.96

0.657

0.389

(1,2]

0.981

0.791

0.964

(2,3]

1

0.800

0.992

Table 1. Functional data simulation. Proportion of rejected null hypothesis for 0-degree cut orthogonal basis, LFMM and the interval testing (IT) procedure. For this is the type I error, for the statistical power

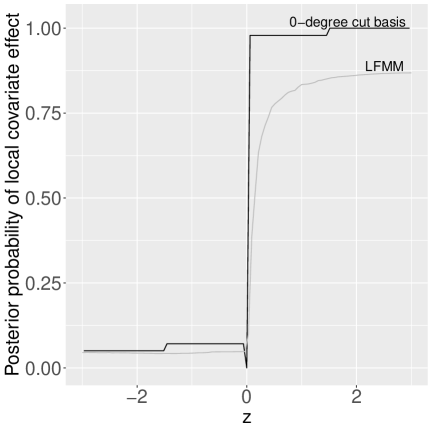

We consider functional data over a grid of time points, with strongly correlated errors. Specifically, we simulate functional data for individuals. For each individual, we consider covariates and functional data over a grid of -values within the interval , extending the scenario in Section 5.1. We further employ the same model for the outcome and covariates as in Section 5.1, that is only covariate 1 truly has an effect (at coordinates ). However, now the errors are drawn from a mean zero, unit-variance, Gaussian process with autocorrelation . We generate independent simulation replicates and report averaged results.

We compare our approach with the longitudinal functional mixed model (LFMM) of Paulon

et al. (2023), and with the interval testing (IT) procedure of Pini and

Vantini (2016). The LFMM has two versions: one designed for a single covariate and another for multiple covariates. The latter version performed poorly, with a type I error rate exceeding 0.5. In addition, the IT procedure can only handle a single covariate. Thus, we first focus on comparing the three methods when considering only the truly active covariate 1.

Table 1 shows that our method has higher power than LFMM (0.96 vs. 0.657 for ), with a similar type I error rate. Similarly, the IT procedure exhibits low power in detecting the covariate effect within the range of . While the procedure controls the family-wise error rate within any specified interval of the domain, this also diminishes its power.

Figure 7 (left) focuses on the two Bayesian methods, and shows the average posterior probability of a local effect for covariate 1 for both the LFMM and our method. At coordinates , where there is truly no covariate effect, these probabilities are close to 0 for both methods. However, for , where the covariate effect truly exists, our method exhibits higher posterior probabilities.

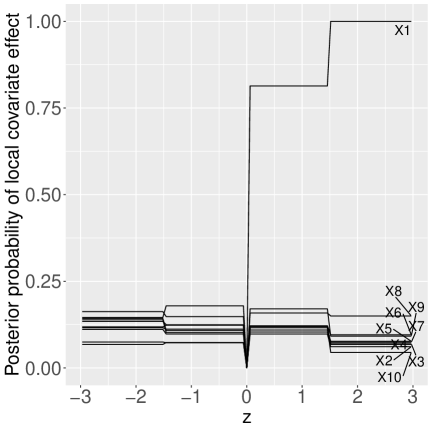

The right panel of Figure 7 and Table 4 present the results only for our method when using all 10 covariates. The results for covariate 1 are overall similar to the single covariate setting, although the posterior probabilities for and the corresponding type I errors are slightly higher. For , the power is also slightly lower (e.g. from to for ). For the truly inactive covariates -, the average posterior probabilities were below at any , and the type I errors ranged from to . In Section 17.2 we show results for a larger sample size, individuals. As illustrated in Table 4, all type I errors are below , and the statistical power is for all .

5.3. Salary gaps versus age

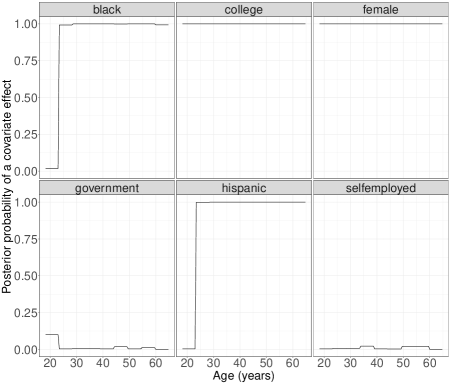

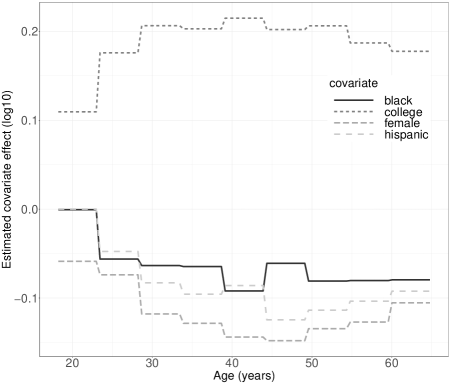

Figure 3. Salary Data, discussed in Section 5.3. Left: posterior probability of a salary gap associated with race, gender and college education versus age, adjusted by occupation and worker class. Right: corresponding estimated effect (log-10 scale)

We used a dataset obtained from the 2019 Current Population Survey (Flood et al., 2020) to investigate the presence of a salary gap associated with potentially discriminatory factors, such as race (binary indicators for black race and Hispanic origin) and gender. The goal was to assess whether said gaps exist at all ages, and specifically for younger individuals who recently entered the workforce. The dataset includes single-race individuals aged 18-65 who were employed full-time (working 35-40 hours per week) and not serving in the military.

The response variable is the log-10 annual work income. Besides assessing the effects of race and gender at various ages ( coordinates), we included the possession of a university degree as a benchmark that is expected to have a positive effect across all ages. We also examined the effects of being government-employed and self-employed. We also included the occupational sector as an adjustment covariate. It is important to note that the inclusion of the occupational sector is predetermined and no testing is performed. The data contain information on 24 occupational sectors, such as architect/engineer, computer/maths, construction, farming, food, maintenance, etc.

We performed a multi-resolution analysis using two different resolutions, defining 10 and 20 local testing regions, respectively. These resolutions roughly corresponded to 5-year and 2.5-year bins, allowing us to examine the data at different age intervals.

Figure 3 summarizes the results.

The existence of gender and college education effect had a posterior probability near 1 at any age (left panel). However, these gaps were estimated to be smaller for younger individuals, aged (right panel).

Specifically, college education was associated with higher salaries, while the female gender was associated with lower salaries at any age.

Interestingly, we did not find evidence of salary gaps associated with black or Hispanic origins among individuals who had recently joined the workforce (aged 18-23). However, strong evidence was found for such gaps at all other ages.

We must emphasize that the lack of evidence against a (local) null hypothesis does not prove its truth, as there may be limited power to detect such differences. However, given the large sample size, it appears that if there were truly a salary gap for individuals aged 18-23, it should not be very large. Finally, we also did not find evidence of salary gaps associated with being self- or government-employed. We remark that these findings should be interpreted conditional on the assumption that two individuals are equal in terms of their occupational sector, college education, and other covariates. Our analysis is not designed to detect discrimination that may hinder individuals from obtaining a certain education or occupation.

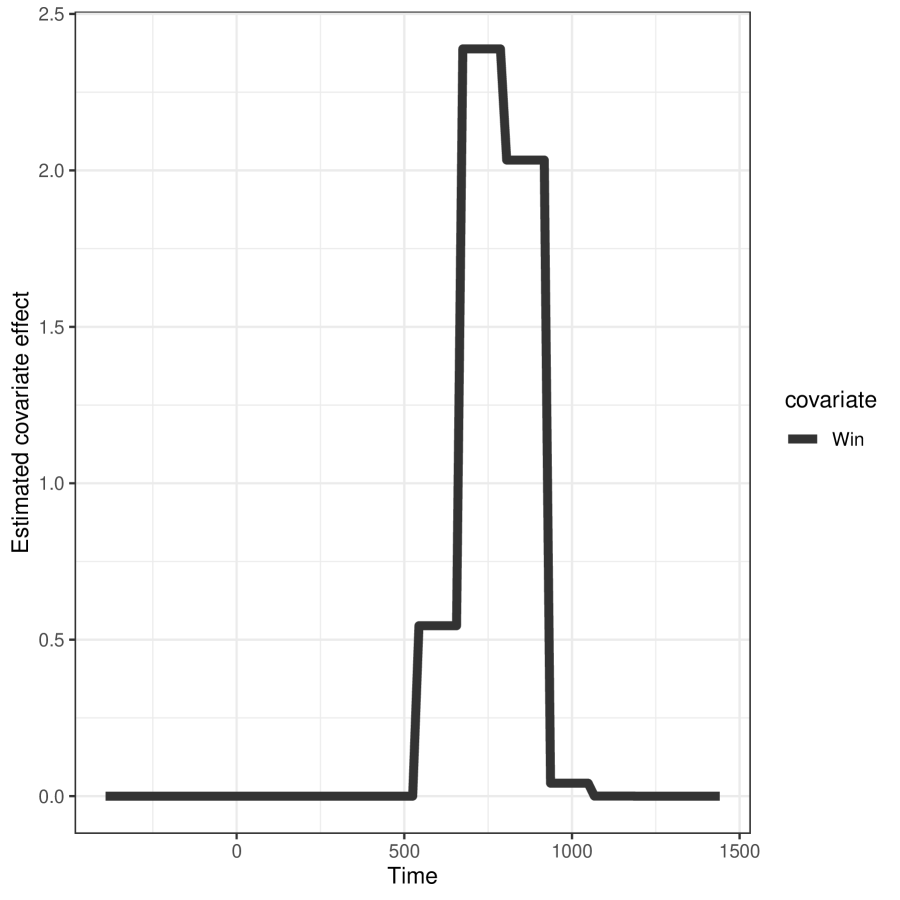

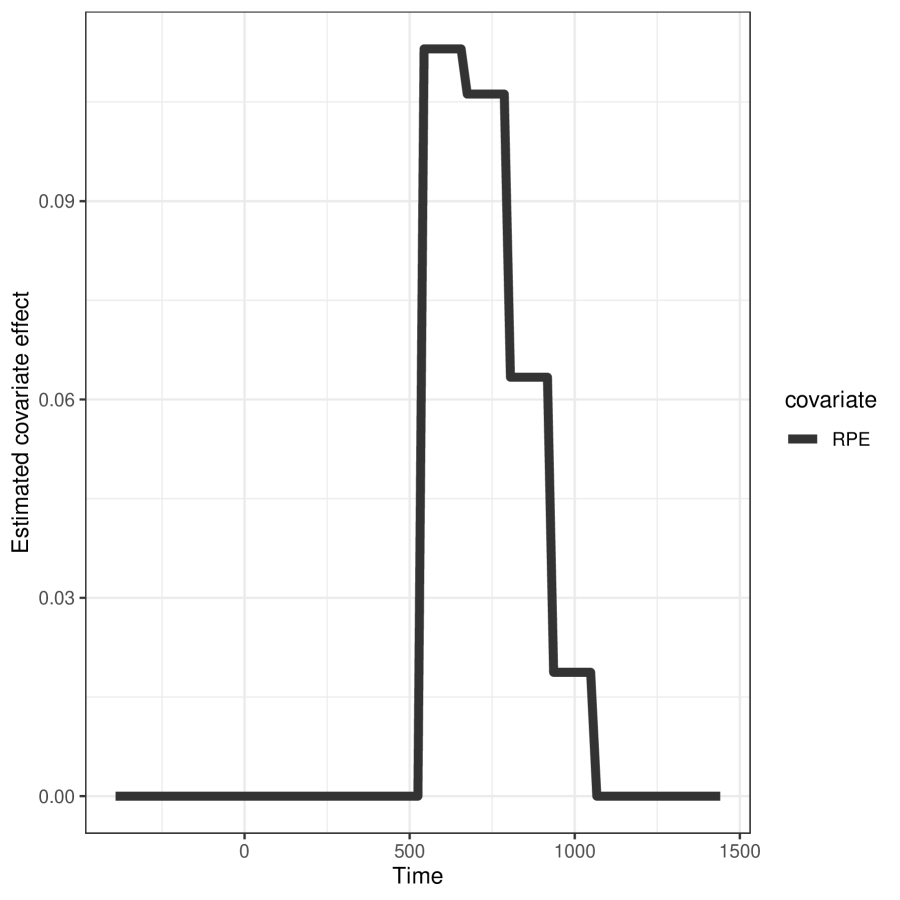

5.4. Local brain activity over time

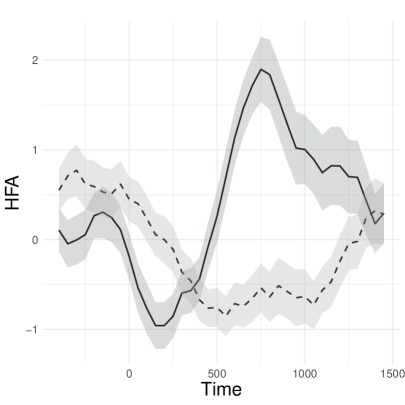

Figure 4. ECoG data. Left: mean high-frequency activity signal averaged across trials where the gamble was won (solid line) or lost (dashed line), and point-wise 80% confidence intervals.

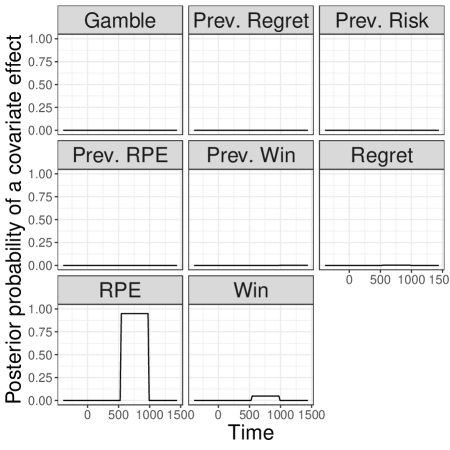

Right: posterior probability of local covariate effects on brain activity

We consider a dataset from Saez et al. (2018) measuring brain activity over time using multi-electrode electrocorticography.

During the experiment, the patients played a game where they chose between a certain prize and a risky gamble, which had varying probabilities of higher winnings. The goal was to assess whether certain game-level covariates were associated with brain activation and, if so, at what specific times.

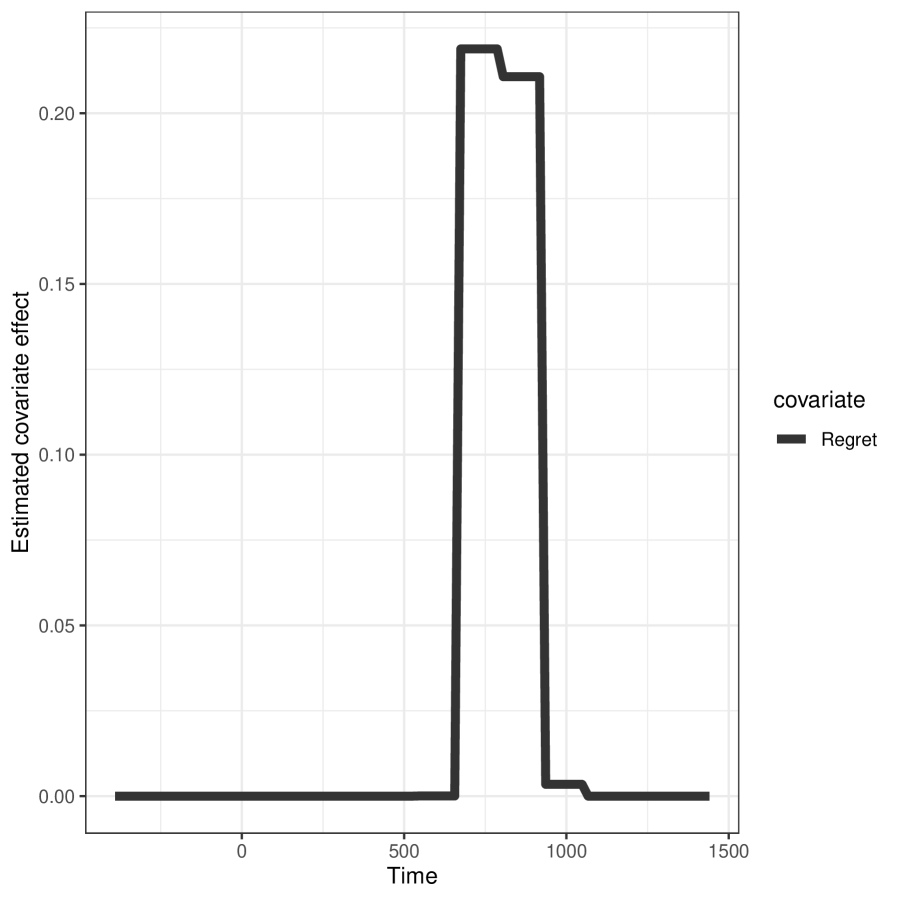

We consider three covariates related to game outcomes: 1) whether the gamble resulted in a win or loss, 2) the reward prediction error (RPE) representing the difference between the obtained reward and the expected value of the gamble, and 3) the additional money that would have been won for the non-chosen option (regret). There was also a dummy covariate indicating whether participants chose to gamble or not and covariates about previous rounds (e.g. losing in the immediately preceding round).

Prior to time participants placed their bets. At exactly time , the game’s outcome (money gained) was revealed to the participants. The researchers recorded the brain activity before and after the outcome revelation. Figure 4 (left) shows the mean high-frequency activity (HFA) signal for an illustrative electrode averaged across 179 trials played by a single patient, split according to whether the game was won (top) or lost (bottom).

See Saez et al. (2018) for further experimental and data pre-processing details.

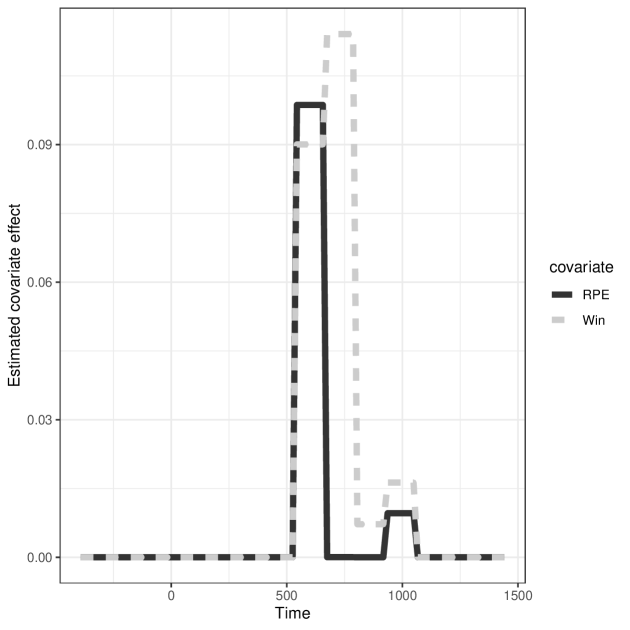

Initially, we examined the local effect of each covariate separately. In this analysis, we focused on a time interval that extended from 450 ms before to 1500 ms after the outcome revelation, with knots placed at every 50-ms interval. This resolution should be sufficient to capture changes in brain activity typically observed in this type of experiment; for example, Saez et al. (2018) consider 50ms increments in a rolling window approach.

We found a significant increase in HFA activity associated with game wins, higher reward prediction error, and regret. Specifically, the posterior probability of an effect for game wins was 0.9797 within the time range of . Similar high probabilities were observed for regret (0.7566) and reward prediction error (0.999). Additionally, these effects displayed temporal variability, gradually decreasing over time, see Figure 8.

Subsequently, we conducted a multivariable analysis that included all eight mentioned covariates. This analysis revealed collinearity among the outcome-related covariates, leading to RPE being the only variable with a significant effect on HFA activity. Specifically, the posterior probability of an effect for RPE on HFA was approximately 0.949 within the time range of . See Figure 4 (right).

Overall, our findings support that HFA activity is associated to outcome-related processes, such as gamble win or loss, RPE and regret, rather than choice-related processes like gamble choice.

Further, that neural activity may be more highly associated with RPE than with wins. Therefore, our method helped disentangle highly correlated covariates and identify which ones can best explain variation in neural activity.

6. Discussion

Our framework is grounded in a semi-parametric model that assumes additive local covariate effects. We believe that this approach can provide more accurate inference compared to non-parametric methods in scenarios with moderate sample sizes or many covariates, while facilitating interpretation and computational efficiency.

In all varying coefficient models such as ours, the evaluation of interactions between and is achieved by assessing changes in the coefficient values. Our approach tests the effect of a covariate in , averaged across the values of other covariates in . Although not done in our examples, to account for higher-order interactions within elements in , one can augment the vector of covariates.

Our work focuses on testing multiple scientific hypotheses, rather than merely estimating the effects of covariates on the outcome. An alternative that a practitioner might consider is the use of credible intervals for covariate selection. However, this approach has several drawbacks.

First, the pathological false positive inflation described here applies equally to confidence/credible intervals, unless one uses a construction ensuring the presence of zeroes in the asymptotic parameter values, e.g. the orthogonal cut basis presented here.

Second, as pointed out by Berger and

Delampady (1987), within a Bayesian framework this does not constitute an efficient testing procedure for a precise null hypothesis. Additionally, it fails to account for multiplicity, especially with dependent hypotheses: even with a small number of predictors, we may expect an increased proportion of falsely rejected null hypotheses.

Finally, with a large number of covariates, a credible interval approach becomes highly inefficient, even in basic linear regression scenarios, compared to the exclusion of inactive covariates.

Our formulation enables the use of standard algorithms for model search and posterior inference. These algorithms were effective in our examples,

but computations become costlier when one considers many covariates, local testing regions or different resolutions.

When many covariate effects are zero (sparse truth) the posterior distribution concentrates on small models, which eases computation, but for non-sparse truths it would be interesting to develop tailored computational algorithms.

It would also be interesting to explore more refined covariance models beyond the simple parametric choices (e.g., auto-regressive and moving averages) considered in our examples. Such dependence models would be particularly relevant for settings with multivariate coordinates ().

However, the challenge lies in proposing statistically and computationally efficient methods despite the larger number of parameters involved.

Beyond our specific framework, we hope to shed light on subtle issues arising in local variable selection under misspecification, and help others put forward alternative solutions.

Acknowledgments

DR was partially funded by Ayudas Fundación BBVA Proyectos de Investigación Científica en Matemáticas 2021, grant Consolidación investigadora CNS2022-135963 by the AEI, Europa Excelencia EUR2020-112096 from the AEI/10.13039/501100011033 and European Union NextGenerationEU/PRT and Huawei Research Grants.

ASK and MG were partially supported by NSF SES Award number 1659921.

Supplementary material

The sections below contain all proofs, Lemma S1, and additional data analysis results.

Additionally, folder 2023_Rossell_Kseung_Guindani_Saez_localvarsel contains data and R scripts to reproduce our results, available at https://github.com/davidrusi/paper_examples.

since .

Now, note that (7) implies that is block-diagonal, i.e.

and hence

and hence , as we wished to prove.

8. Orthogonal cut basis with multiple covariates

Recall that our assumed model is

where is as in (4) and is an orthogonal cut matrix as in (7). Above is obtained by multiplying a local cut basis by each covariate.

Specifically,

where is the cut basis of region , is the column vector comprising the values of covariate for observations in region ,

and denotes the column-wise product obtained by multiplying each column in by , in an entry-wise fashion.

Let where is the coefficient for the effect of covariate in region . Then

the model-based local null hypothesis for covariate in region is

(18)

Since is an orthogonal cut basis, Lemmas 1 and 2 directly apply to (18). In fact, the statement and proof of Lemma 2 are given explicitly multiple covariate case.

This means that if is linearly independent of covariate given the other covariates, then the asymptotic covariate effect in region is (for dependent data, ).

Lemma 2 extends Lemma 1 to dependent data settings where

for each individual one observes data on a grid (e.g. longitudinal or functional data).

Specifically, let be observation , denote the individual and the number of individuals,

and be the covariates for individual (in particular, for group comparisons is a vector coding for group membership).

Suppose that for each individual we have the same number of measurements .

We first recall the notation and setup. Recall that the assumed model is

where are orthogonal cut basis as defined in Section 1.2. Recall that these can be written as

(19)

where is the basis evaluated at region interacted with the covariate effects.

Specifically,

where is the cut basis of region , the column vector with the values of covariate for observations in region ,

and the column-wise product multiplying each column in by , in an entry-wise fashion.

Finally, recall also that is assumed to have a block-diagonal structure across regions, i.e.

Denote by the Kullback-Leibler optimal parameter value under the data-generating truth . That is,

Lemma 2.

Let where is orthogonal cut basis as in (7) satisfying .

Suppose that for each individual one has the same number of measurements ,

and that covariate values add to zero across individuals, i.e. .

Let where are the parameters associated to (i.e. to region ).

Then,

Proof.

Let and , the optimal solution can then be written as

The proof strategy is to show that the conditions of Lemma 1 hold for , which then immediately gives that

The first condition in Lemma 1 is that is a cut matrix. To see that this holds, note that

where .

This proves that has the same structure as in 19, i.e. is a cut basis.

The second condition in Lemma 1 is that is an orthogonal basis to , i.e. . To show that this condition holds, first note that

where are the rows from corresponding to region .

Hence, it suffices to show that for all .

To see this, note that can be computed by summing across individuals . That is,

Since all individuals are observed on the same grid we have that is constant across , and similarly is assumed constant across individuals, hence we may write , where does not depend on the individual .

Similarly,

where is the column vector with the value of covariate for individual , that is constant across observations in region and equal to ,

and does not depend on (since all individuals are observed on the same grid, is constant across individuals indexed by ). Recall that denotes the covariates for individual .

We therefore obtain that

since (the covariates have zero sample mean) by assumption, completing the proof.

∎

10. Bayes factor derivation

The Bayes factor comparing a model with the optimal is

(20)

where .

We derive Expression (20). Recall that the assumed model is

where is an and a positive-definite matrix, and .

The integrated likelihood under model is hence

Denoting by and

, we obtain

Hence the Bayes factor is

as we wished to prove.

11. Discussion of the technical conditions of Theorem 1

Assumption (A1) implies that, although the number of parameters may be larger than , we restrict our attention to full-rank models. This implies that the model size , a common practice in model selection. Assumption (A2) is a mild and can be relaxed, but simplifies our exposition. In our default setting, we assume . Thus (A2) is satisfied when the empirical covariance converges to a fixed positive definite covariance. The assumption is also satisfied by Zellner’s prior, where , so that . Assumption (A3) holds in the homoskedastic independent errors setting where . For dependent data, (A3) is a mild condition that may be relaxed to accommodate cases where is not bounded as grows, see the proof of Theorem 1. Assumption (A4) is minimal and ensures that the prior dispersion does not vanish too fast with (it is satisfied by our default and by the discussed alternatives where may grow with ). In Assumption (A5) the parameter can be interpreted as a non-centrality parameter that measures the sum of squares explained by model but not by model . Assumption (A5) is minimal: otherwise, Bayes factors are not consistent even in finite-dimensional settings with fixed . See also the discussion of Assumption (B6) in Section 4.2 on the relationship between and common beta-min and restricted eigenvalue conditions.

We recall auxiliary results that are helpful in the proofs of our main results.

Lemmas 3-7 are obtained from Sections S6 and S9 in Rossell

et al. (2021).

For brevity we do not reproduce their proofs, please see Sections S6 and S9 in Rossell

et al. (2021).

However, we do prove Lemma 7 here since, although the result in Rossell

et al. (2021) is correct, the proof offered there contains an error.

Lemma 8 is a new result that we prove here bounding tail probabilities for certain differences between quadratic forms of sub-Gaussian vectors.

Lemma 3 is a well-known result. It expresses the difference between the explained sum of squares by two nested models in terms of the regression parameters obtained under the larger model, after suitably orthogonalizing its design matrix.

Definition 1 and Lemmas 4-5 give the definition and two basic properties of

sub-Gaussian random vectors: closed-ness under linear combinations and hat certain quadratic forms of -dimensional sub-Gaussian vectors can be re-expressed as a quadratic form of -dimensional sub-Gaussian vectors.

Lemmas 6-7 give bounds for right and left sub-Gaussian tail probabilities.

Lemma 3.

Let and be an times matrix.

Let

and

the least-squares estimates associated to and , respectively.

Then

where

and .

Definition 1.

A -dimensional random vector follows a sub-Gaussian distribution with parameters and , which we denote by if and only if

for all .

Lemma 4.

Let be a sub-Gaussian -dimensional random vector, and be a matrix.

Then , where is the largest eigenvalue of , or equivalently the largest eigenvalue of .

Lemma 5.

Let be an -dimensional sub-Gaussian random vector.

Let , where is an matrix such that is invertible.

Then , where is -dimensional.

Lemma 6.

Central sub-Gaussian quadratic forms. Right-tail probabilities

Let . Then

(i)

For any ,

(ii)

For any and any such that ,

(iii)

For any ,

where .

Lemma 7.

Non-central sub-Gaussian quadratic forms. Left-tail probabilities

Let and . Then

where the right-hand side follows from Markov’s inequality.

Since where , we obtain

where we used that .

Using the definition of sub-Gaussianity to bound the expectation on the right-hand side gives

The bound above holds for any . The optimal is found by setting the first derivative to zero, which gives

Note that to have , we need that , which holds by assumption. Plugging in the optimal into the upper-bound gives

as we wished to prove.

∎

Lemma 8.

Tail probabilities for differences of sub-Gaussian quadratic forms

Let be a -dimensional sub-Gaussian vector and a -dimensional sub-Gaussian vector, where is finite and .

(i)

Let , then

for any such that

and .

In particular, for where ,

(ii)

Let . Then

for any .

Proof.

of Lemma 8, Part (i).

Let .

The union bound gives that, for any ,

(21)

In particular take , so that and .

Then, using Lemma 7 we have that the second term in (21) is

The proof strategy is as follows. First we show that the first term in (25) is essentially given by (up to lower-order terms). To characterize the second term in (25) we note that the terms in the exponent are

a Bayesian version of the sum of explained squares under model minus that for , show that these are essentially equivalent to the least-squares counterparts. The latter sum-of-squares can be re-written as a quadratic form of sub-Gaussian vectors using Lemma 3, which can be bounded using the inequalities developed in Section 12.

Consider the first term in (25). Under Assumption (A2) the eigenvalues of

lie in , hence

Using that by Assumption (A4), and that are bounded by constants by Assumption (A2),

it is simple to show that

(26)

for large enough , a fixed that can be taken arbitrarily close to 1, and

and

where are finite non-zero constants by assumption.

This concludes the first part of the proof.

Regarding the second term in (25), to ease notation let , ,

and the least-squares estimate when regressing on , which is guaranteed to exist by Assumption (A1).

Then the exponent in (25) features , where

(27)

can be interpreted as the Bayesian sum of explained squares by model .

Under Assumptions (A2) and (A4), is essentially equivalent to the difference between classical least-squares sum of explained squares , where

Briefly, let

so that

which lies in the interval ,

where are the smallest and largest eigenvalues of .

Using Assumption (A2) it is possible to show that both and converge to 1 as , implying that for large enough

(28)

where is a constant that may be taken arbitrarily close to 0 as grows.

The remainder of the proof characterizes the behavior of , separately for the over-fitted case where and the non over-fitted case where .

13.1. Part (i). Case

Let where are the columns corresponding to and the remaining columns.

Lemma 3 gives that

where are the residuals from regressing on , and the projection matrix onto the column span of .

Recall that by assumption, which by Lemma 4 implies that

where and is the largest eigenvalue of .

Now, using that and Lemma 5 gives that

where is a sub-Gaussian vector of dimension .

Combining this result with (26) and (28) gives

Hence, consider any sequence , it follows that

(29)

Since , this is a right-tail probability of a sub-Gaussian quadratic form. Using Lemma 6 with and that are constants by assumption and is bounded by constants by Assumption (A3), said tail probability vanishes for any such that

.

In particular, take , then the condition is that

The latter condition holds for any such that , for any such that .

For these choices of and we obtain

In conclusion,

for any such that , as we wished to prove.

13.2. Part (ii). Case

Let be the union of models and , i.e with design matrix containing all columns in and , so that both and are contained in .

Proceeding similarly to Part (i), Lemmas 3 and 5 give that

where

and , analogously for , and and are the projection matrix defined above.

The key is to bound the two terms and , by noting that they are quadratic forms of sub-Gaussian vectors, which will allow us to use Lemma 8.

Specifically, recall from Part(i) that where and is the largest eigenvalue of .

Using that and Lemma 5 gives that

with dimension .

Regarding the term , since by assumption, by Lemma 5 we have that is a dimensional sub-Gaussian vector with

.

(30) is of the form given in Lemma 8, taking

with and ,

, , and

where to obtain the right-hand side we used that is idempotent, and that .

The expression for can be simplified. First, note that the linear predictor can be decomposed into the contribution from and , where is the subset of corresponding to elements in .

Second, , since is in the column span of and is the corresponding linear projection operator. Hence,

(31)

To conclude the proof we apply Lemma 8 and deduce the smallest one can set so that the tail probability (30) vanishes as .

From Lemma 8, it suffices that diverges to , which holds by Assumption (A5), and that

diverges to infinity as , which happens if and only if its exponential

diverges to infinity. This can be achieved by taking

where satisfies .

The latter condition is equivalent to , and is satisfied by taking

for any that diverges to infinity. Then the expression for becomes

where is any sequence diverging to infinity.

Finally, we argue that may be replaced by in the expression of .

Since and for any ,

and the right-hand side vanishes as , we may replace by

This section derives several auxiliary results used in the proof of Theorem 2.

Lemma 9 is an elementary statement that is useful in carrying out sums of posterior model probabilities over certain model sets.

The remaining results in this section derive bounds on integrals that involve certain tail probabilities for central and non-central sub-Gaussian quadratic forms, which are useful to bound the expected posterior probability assigned to an arbitrary model .

Proposition 1 considers central sub-Gaussians, and is used in the proof of Theorem 2 when considering overfitted models, i.e. models that contain all parameters in the optimal plus some extra spurious parameters.

Theorem 2 uses only Part (ii) of Proposition 1, but for completeness we also provide Part (i), which considers a situation where one obtains faster rates.

Proposition 2 considers the difference between a central and non-central sub-Gaussian quadratic forms. It is used in Theorem 2 to bound the posterior probability assigned to non-overfitted models .

Parts (i)-(ii) are analogous results, the latter corresponding to a more conservative setting where , for defined below.

The proof of Theorem 2 uses Part (ii) to bound the posterior probability for non-overfitted models of size less than .

For these models, the argument as defined below is typically decreasing in : roughly speaking, is a complexity penalty for larger models, which favors over if the latter has larger size. Hence, for posterior probability of to vanish one must rely on the non-centrality parameter to be large enough.

In contrast, when one considers non-overfitted models of size larger than then is typically increasing. For those models one may then either use Proposition 2(ii), or alternatively use 2(iii) which relies solely on being large enough. The latter option leads to slightly simpler arguments when proving Theorem 2.

Lemma 9.

For any two natural numbers it holds that

Further, suppose that is either fixed or a non-decreasing function of . Then

Proposition 1.

Bound on integrated central sub-Gaussian tails.

Let be a -dimensional sub-Gaussian vector, and

where is a constant and .

(i)

Suppose that , where . Then

(ii)

Suppose that and that . Then

for any , where and .

Further, if , then

Proposition 2.

Bound on integrated non-central sub-Gaussian tails.

Let be a sub-Gaussian vector of dimension and be of dimension , where and . Define

for any .

It is easy to show the term for all , hence the integral can be upper-bounded by replacing the power by a smaller quantity.

Now, recall that is an increasing function of and note that is largest when is smallest, i.e. when is smallest, so that

and hence

where to ease notation we defined .

Therefore,

(33)

Note also that

where the right-hand side follows from simple algebra. Hence as grows may be taken arbitrarily close to 0.

To bound (33), note that , since by assumption. Hence the integrand in (33) is and the integral is upper-bounded by taking a smaller power.

Recall that by assumption

hence (33) is upper-bounded by replacing the power by , giving

The proof strategy is to split as the sum of the integral for plus that for . The first integral is then bound using Part (i) of this proposition, and the second integral using Lemma 6(iii).

Take any . Then the integral for is

(34)

since

given that for and that . Applying Part (i) of the current Proposition 1 gives that (34) is

(35)

Next consider the integral for ,

where in the inequality above we used that for .

We may now use Lemma 6(iii) setting , since by assumption, giving that

for .

Combining this expression with (35) gives that

where recall that , as we wished to prove.

As a final remark, note that when the second term is smaller than the first one.

Further note that

The proof strategy is to split the integral into two terms, where the first term is an integral involving a central sub-Gaussian that can be bound using Proposition 1, and the second term involves a inequality that can be bound with Lemma 7.

Denote by and let be an arbitrary number, then the union bound gives

(36)

We shall take so that

and

.

Applying Lemma 7 immediately gives that the second term in (36).

To bound the second term in (37), we first split that integral according to the range of values such that the term inside the log is negative and positive. Note that

where we denoted the right-hand side for convenience, hence the second term in (37) is

(38)

To bound the second term in (38) we use Proposition 1. We do this separately for Part (i) and (ii).

14.4.1. Part (i).

By assumption we have that

where .

To apply Then Proposition 1(i) we also need that

which also holds by assumption.

Then Proposition 1(i) gives that the second term in (38) is

where .

Combining this expression with (37) and (38) and noting that gives that

as we wished to prove.

14.4.2. Part (ii).

By assumption we have that and that

where recall that , which are the two conditions to apply Proposition 1(i) to the second term in (38).

Hence Proposition 1(i) gives that the second term in (38) is

where ,

and

.

Combining this expression with (37) and (38) and noting that gives that

The proof strategy is to note that, since , it holds that