Likelihood-ratio inference on differences in quantiles

Evan Miller

Eppo

evan@geteppo.com

Quantiles can represent key operational and business metrics, but the computational challenges associated with inference has hampered their adoption in online experimentation. One-sample confidence intervals are trivial to construct; however, two-sample inference has traditionally required bootstrapping or a density estimator. This paper presents a new two-sample difference-in-quantile hypothesis test and confidence interval based on a likelihood-ratio test statistic. A conservative version of the test does not involve a density estimator; a second version of the test, which uses a density estimator, yields confidence intervals very close to the nominal coverage level. It can be computed using only four order statistics from each sample.

1 Background

Notation follows [3]. Let represent the population quantile of interest, with and representing the true quantile values in control and treatment groups. Suppose that ordered samples and are drawn from control and treatment.

The traditional Price-Bonnet [2] estimator forms a confidence interval on the difference in quantiles as

Donner and Zou [1] noted that this method fails to account for asymmetry in the underlying sampling distributions. They propose instead

where and represent the lower and upper bounds of the one-sample confidence interval for group . Simulations indicate that the Donner-Zou method yields anti-conservative CIs. The method proposed below is similar in spirit to Donner-Zou, but operates in index space rather than value space. It does not involve the quantile estimates themselves, and simulations show that it has better coverage properties than Donner-Zou.

2 Setup

Suppose an unknown distribution has true quantile value . If a sample of size is drawn from , then the probability that the sample contains exactly observations less than is given by the binomial distribution. Then given an ordered sample , a likelihood function may be constructed as

Note that this likelihood function is flat between points in the ordered sample, and so a unique maximum does not exist.

Next consider two samples and and a constraint (hypothesis) of the form . We can test this hypothesis with a likelihood-ratio test, maximizing the joint (two-sample) likelihood with and without the constraint applied.

Figure 1: Constrained and unconstrained MLE estimates of the true median value

The unconstrained likelihoods will be maximized in a region near the sample quantiles. If is an integer, the one-sample likelihood for will be maximized over the open interval . If is not an integer, the one-sample likelihood will be maximized over the open interval . In either case, the maximizing likelihood can be written , and the maximized unconstrained joint likelihood is given by

The constrained problem will maximize the joint likelihood

subject to

or equivalently

The constrained maximization may be performed as a simple line search over between the unconstrained maximizing values (i.e. sample quantiles possibly shifted by ).

Suppose the constrained joint likelihood is maximized at order statistics and . Then a likelihood ratio test statistic can be formed as

Denote this quantity . By Wilks’ theorem,

and thus we have the basis for a hypothesis test and therefore an acceptance region (confidence interval) on :

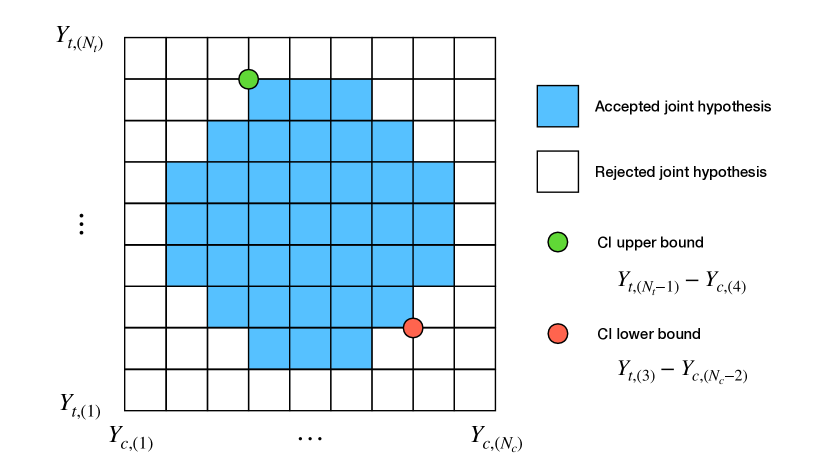

Figure 2: Visualization of the difference-in-quantile acceptance region

The problem may be inverted to simplify computation. Search the acceptance region for extreme values of as

The acceptance region can be visualized as an grid of points; the “tiles” between points represent areas where the joint likelihood is constant. Each cross-sample pair of points represents a potential extreme value in the acceptance region.

Simulations show that a search of the acceptance region for extreme values yields a conservative confidence interval; the conservativeness is likely due to multiple comparisons. In the next section, structure will be added to the problem to permit a single hypothesis test that produces a confidence interval closer to the nominal coverage.

3 Large sample behavior

By the Central Limit Theorem, a binomial converges to a normal distribution and

Thus

and so

To avoid a complete search of the ellipse perimeter, suppose that the true and are each linear inside the elliptical ball:

Then in this region,

A confidence interval can then be found by maximizing and minimizing this expression with respect to and subject to the elliptical constraint. Form the Lagrangian

The first-order conditions are

Solving, we find the optimal indexes to be

And so a confidence interval on is given by

Implementing this method requires knowledge of and . If the treatment effect is constant within the elliptical acceptance region, these can be assumed equal and will drop out of the index equations. But if the treatment effect is (linearly) heterogeneous within the acceptance region, it will be necessary to estimate and from the data.

The following two-step algorithm can be used to form a final confidence interval:

1.

Compute , , , and under the assumption that

2.

Estimate

and

3.

Compute , , , and using the estimated and

In this way, a confidence interval is formed using only four points from each ordered sample, and without a perimeter or region search. Simulations indicate that this confidence interval is less conservative than a full ellipse search, and quite close to the nominal coverage level.

References

[1]

A. Donner G. Y. Zou.

Construction of confidence limits about effect measures: A general

approach.

Statistics in Medicine, 27(10):1693–702, 2008.

[2]

Robert M. Price and Douglas G. Bonett.

Distribution-free confidence intervals for difference and ratio of

medians.

Journal of Statistical Computation and Simulation,

72(2):119–124, 2002.

[3]

Mårten Schultzberg and Sebastian Ankargren.

Resampling-free bootstrap inference for quantiles.

In Kohei Arai, editor, Proceedings of the Future Technologies

Conference (FTC) 2022, Volume 1, pages 548–562, Cham, 2023. Springer

International Publishing.