Graphical models for cardinal paired comparisons data

2Department of Statistics and Insurance Science, School of Finance and Statistics, University of Piraeus, 80 Karaoli and Dimitriou str., 18534 Piraeus, Greece

E-mail: wrahulsingh@gmail.com (R Singh), geh@unipi.gr (G Iliopoulos), davidov@stat.haifa.ac.il (O Davidov))

Abstract

Graphical models for cardinal paired comparison data with and without covariates are rigorously analyzed. Novel, graph–based, necessary and sufficient conditions which guarantee strong consistency, asymptotic normality and the exponential convergence of the estimated ranks are emphasized. A complete theory for models with covariates is laid out. In particular conditions under which covariates can be safely omitted from the model are provided. The methodology is employed in the analysis of both finite and infinite sets of ranked items specifically in the case of large sparse comparison graphs. The proposed methods are explored by simulation and applied to the ranking of teams in the National Basketball Association (NBA).

Key-Words: Graph Laplacian, High dimensional inference, Large sample properties, Least square ranking, Linear models, Regression.

1 Introduction

There are many situations in which ranking a set of items is desired. Examples include the evaluation of political candidates, sports, information retrieval, and a variety of modern internet and e-commerce applications (e.g., Cremonesi et al., 2010, Buhlmann and Huber 1963, Govan 2008, Barrow et al. 2013, Xu et al. 2014, Cururingu 2015). The theory and methodology of ranking methods have been extensively studied from a variety of perspectives by researchers in the fields of mathematics (Langville and Mayer 2012), economics and social choice theory (Sen 1986, Slutzki and Volij 2005), machine learning (Ailon et al. 2008, Furnkranz and Hullermeier, 2010), psychology (Davis-Stober 2009, Regenwetter et al 2011) as well as many other disciplines. The focus of most of the existing literature, both old and new, has been procedural rather than inferential. For a statistical perspective on ranking methods, of a somewhat different flavor ours, see the books by Marden (1995) and Alvo and Yu (2014).

A ranking of a set of items can be inferred from different types of data including scores (Balinski and Lariki, 2010) and ranked lists (Marden, 1995). In particular, paired comparison data (PCD) is obtained if all comparisons involve only two items (David, 1988). Suppose that there are items labelled which we would like to rank. Let denote the outcome of the comparison among items and . The random variable (RV) may be binary, ordinal or cardinal. In this paper we consider cardinal, i.e., continuous PCD. We assume that the observations for and satisfy

| (1) |

where

and are independent zero mean RVs. The parameters are refered to as the merits or scores. If we further assume that are IID RVs then (1) is a specially parameterized homoscedastic normal linear model. Clearly this parametrization results in a global ranking referred to as a total linear ranking, cf. Oliveira et al. (2018) and the references therein, in which the merits quantify the degree of preference. We refer to such models as linear models on graphs or more compactly as graph–LMs. It is useful to note that we may view as the outcome of the “game” between team and team where team scored points while team scored points. Then naturally and and thus . Each item is viewed as a vertex of a graph and the set of vertices is denoted by . Let denote the number of comparisons between item and item . We do not assume that for all or even most pairs . If , then items and are connected by an edge denoted by . Let denote the set of edges. The structure is called a graph (Gould, 2012). We note that some authors consider each individual comparison between items and as an edge. Thus would imply multiple edges connecting items and . Such a structure is sometimes referred to as a multigraph. The distinction between a graph and a multigraph is inconsequential from our perspective. With each edge we associate a random sample of comparisons; the set of all samples is denoted by . We call the pair

| (2) |

a pairwise comparison graph (PCG).

Least square estimators for the model (1) have a long history and have been studied in diverse fields (cf. Mosteller 1951, Kwiesielewicz 1996, Csato 2015). Surprisingly, despite the simplicity of model (1), the extensive associated literature, including the many papers on least square estimators, the statistical properties of the least squares estimator have not been properly studied. This paper fills this gap by developing a graph–based statistical theory necessary for conducting inference on the vector of merits. As shown model (1), as well as its extensions, exhibit unique features which complicate and enliven their analysis. In particular our contributions are:

-

1.

The large sample properties of the least square estimator are established using novel necessary and sufficient graph–based conditions. The relationship between the topology of the comparison graph and the quality of the resulting estimators is emphasized. The derived rankings are shown to converge at an exponential rate.

-

2.

Although some papers on graph-LMs with covariates exist, e.g., Harville (2003) who considered a single binary covariate, to the best of our knowledge this is the first paper to rigorously examine such models. In particular, conditions under which models with covariates can be analyzed are provided and the corresponding theory is established. Situations in which covariates can be omitted from the model are emphasized.

-

3.

Finally, an analysis of graph-LMs when the number of items compared grows to infinity is provided. It is shown that up to a logarithmic factor connectivity is sufficient for ensuring that asymptotic normality and uniform consistency.

The paper is organized as follows. The least square estimator is introduced and its elementary properties are explored in Section 2. Section 3 investigates the large sample properties of the LSE. Section 4 and 5 extend model (1) in two directions. In Section 4 models with covariates are analyzed and in Section 5 the number of items compared is allowed to grow to infinity. Simulation results are presented in Section 6 and an illustrative example is discussed in Section 7. We conclude in Section 8 with a brief summary and discussion. All proofs are collected in an Appendix.

2 Least squares on graphs: estimation and elementary properties

Model (1) is the simplest possible graphical linear model (graph–LM) in which a global linear ranking is assumed. Although this model has been widely studied in diverse fields (cf. Mosteller 1951, Kwiesielewicz 1996, Csato 2015) it is surprising that a variety of very basic statistical questions have not been adequatly addressed.

Consider the objective function

| (3) |

which is nothing but a sum of squares over the PCG (2) where is the vector of merits. Clearly, if for all and we have then (3) is the kernel of the likelihood for a normal linear model. Further note that for any where and consequently is not estimable unless a constraint is imposed. Therefore, we define the least squares estimator (LSE) by

| (4) |

where is a preselected vector satisfying , i.e., is not a contrast, cf. Remark A.1. We require the following notations. For any let and Further define,

and

The matrix is the Laplacian of the graph , the diagonal element of the Laplacian is which is the degree of vertex . The total number of paired comparisons is denoted by . Laplacians play an important role in graph theory (Bapat 2010). It is easy to verify that they are symmetric positive semidefinite with rows and columns that sum to .

The vertices and are said to be connected if there exists a sequence of edges . Such a sequence is called a path. If all pairs of vertices are connected then is a connected graph.

Theorem 2.1

The vector of scores can be uniquely estimated if and only if is connected. If so the LSE defined in (4) is given by

| (5) |

where is the Moore–Penrose inverse of .

The proof of Theorem 2.1 shows that if is not connected then there are at least two distinct collections of items and , say, that can not be directly compared, i.e., the difference is not estimable for and . Surprisingly, formula (5) has not been previously derived; however it was mentioned by Ghosh and Davidov (2020) who studied alternatives to the least square estimator. Typically, it has been implicitly assumed that , e.g., Csato (2015), in which case (5) reduces to . It is also worth noting that most papers on the LSE end here, i.e., they make no attempt at studying the statistical properties of (5). Further note that

The second term on the right–hand–side above equals zero for all ; the third term is zero if and only if is in the kernel of However, if is connected then (Bapat, 2010). Thus is the minimum norm solution to the unconstrained minimization problem given in (3). Another common choice for the constraint is where is first standard basis vector for , or equivalently , which leads to the solution where is the row of In particular if for all and then . The choice of the constraint in (4) is not of great importance since the estimated values of are invariant with respect to the chosen constraint:

Corollary 2.1

Let and where and . Then for all we have

Therefore, for simplicity and unless explicitly stated otherwise we henceforth assume that .

Remark 2.1

Some authors consider a weighted objective function, i.e., . The weighted model is used to handle heteroscedasticity, i.e., different comparisons carry different levels of information. The analysis of the weighted and unweighted sum of squares is similar. The only difference is that in equation (5) we replace by and by where the element of is and is the weighted Laplacian with elements when and otherwise. Since the analysis of the weighted and unweighted cases is similar we shall henceforth consider only the unweighted model.

We will assume:

Condition 2.1

The errors are IID with zero mean and a finite variance .

Next, we address the statistical properties of (5). Since it follows that

so . The matrix is symmetric and idempotent therefore it is a projection onto . Moreover, since and by assumption, it follows that and therefore . Hence is unbiased. Further note that under Condition 2.1, and so

| (6) |

It is clear from (6) that the precision of the LSE is a function of and therefore depends on the properties of the comparison graph. The following example shows that even when the total number of paired comparisons is fixed, the structure of the graph has a powerful effect on the precision of the estimators.

Example 2.1

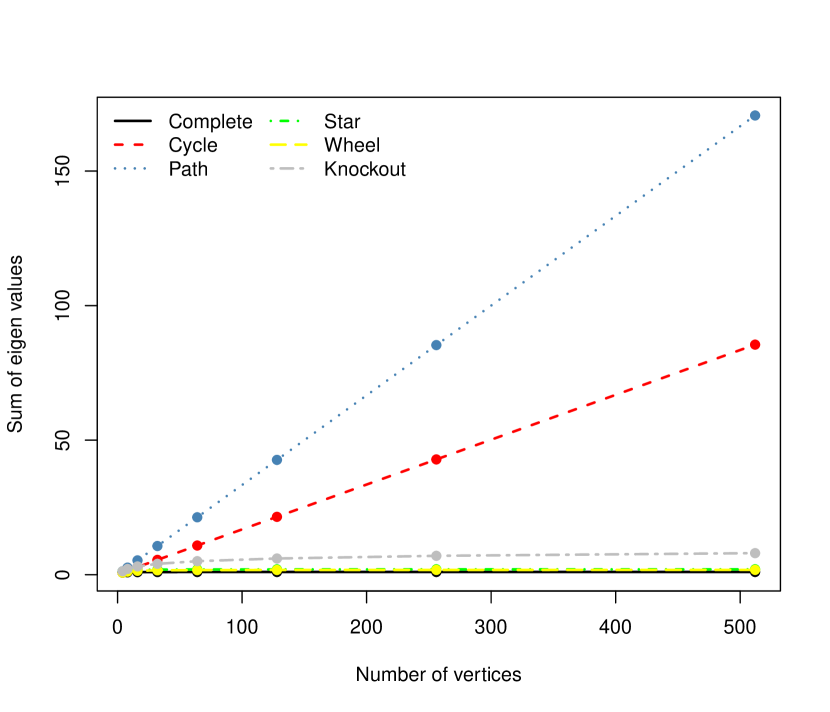

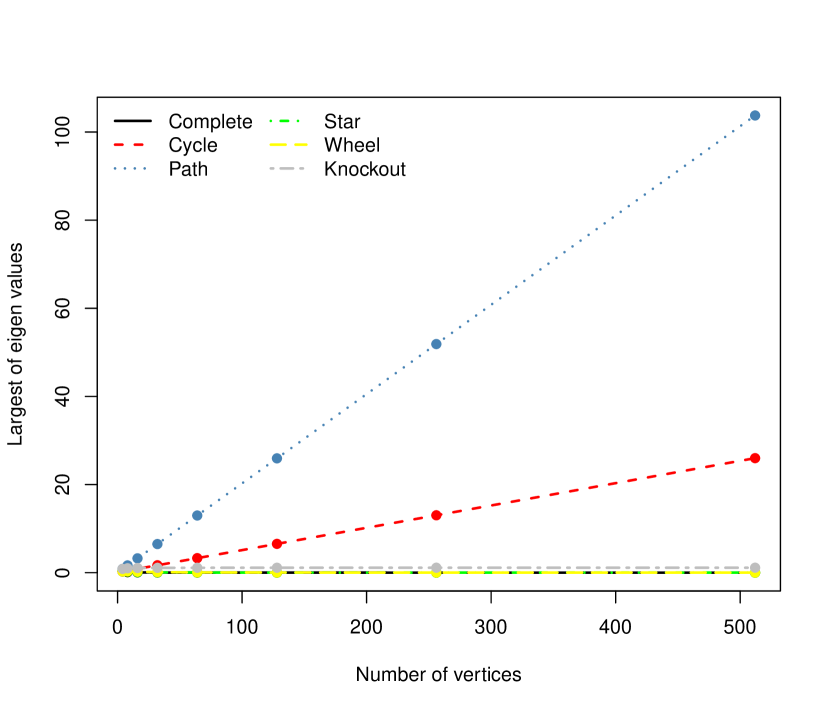

We evaluate the precision of the LSE on several types of graphs. These include the complete, cycle, path, star, wheel and (knockout) tournament graphs as displayed in Figure 1. In the context of the tournament graph we assume, without any loss of generality, that the item with the smaller index moves up the tournament graph.

Figure 1 Comes Here

In a complete graph with items there are paired comparisons whereas in a path graph there are only paired comparisons. Therefore a meaningful comparison among the graphs requires that all Laplacians be scaled so that the total number of paired comparisons, which is equal to , is common to all graphs. For convenience we choose to scale up to the complete graph. Since, the standard tournament graph has vertices, where , we choose . We are interested in the overall precision of which can be assessed, c.f., Atkinson et al. (2007), by various functions of the (positive) eigenvalues of such as their sum, product, largest and smallest value. In Figure 2(a) and 2(b), we display the sum of the eigenvalues and the maximum eigenvalues of the complete, cycle, path, star, wheel and (knockout) tournament graphs as a function of the number of items we are comparing. Larger values indicate higher variability.

Figure 2 Comes Here

Each type of graph is associated with a line in Figures 2(a) and 2(b). The top line corresponds to the path graph on which the estimators are most variable and the bottom line is associated with the complete graph which generates the most precise estimators; the performances of (the scaled) star, wheel and knockout graphs are close to those of the complete graph. Thus, graphs with high connectivity (Cvetković et al. 2009) result in more precise estimators. Among the displayed graphs, the path graph shows the fastest increase in variability as a function of . This is due to its low connectivity. As an example consider comparing the difference between the first and last items in a path graph. Obviously these items are not directly compared. In fact,

i.e., the variance of their difference is compounded over a long path. In high connectivity graphs the paths between any two items is short and therefore comparisons among items are more precise. The performance of the knockout tournament graph is better than the path and cycle graph. It is also interesting to note that all lines in Figures 2(a) and 2(b) are increasing except for the line associated with the complete graph. Finally, in symmetric graphs in which all vertices have the same degree, the components of are estimated with the same variance, e.g., complete graph, cycle graph. If the vertices of the graph have different degrees then the components of are estimated with different variances. The merits of central items (cf., Cvetković et al. 2009) are also estimated with more precision. For example, the merit of the item in the center of the path graph is estimated more precisely than items at the periphery of the graph. Similarly for the central item of the star graph and the wheel graph.

We introduce further notations. The graph is a subgraph of the graph , denoted , if and . The latter notion extends to PCG where whenever and . A matrix is said to be smaller than a matrix , in the Loewner order, if is non–negative definite. This relationship is denoted by . For more on the Loewner order see Pukelsheim (2006). In particular if and are the variances of two (asymptotically) unbiased estimators (of the same quantity) then implies that the estimator associated with is more efficient than the estimator associated with . This means, as an example, that the volume of the confidence ellipsoid associated with is smaller than the volume of the confidence ellipsoid associated with .

Proposition 2.1

Let and be comparison graphs with unique LSEs and whose variances are and respectively. If then

| (7) |

Moreover, for any continuously differentiable function we have where and are the asymptotic variances of and respectively.

Proposition 2.1 shows that the variance of the LSE or any function thereof decreases when the number of paired comparisons on each edge increases.

3 Large sample theory

The asymptotic theory for the LSE requires some additional graph based notions. A graph is called a tree if any two distinct vertices in are joined by a unique path. If is a subgraph of which connects all vertices in then it is called a spanning tree. Moreover, if is connected then has subgraph which is a spanning tree (Gould, 2012).

Condition 3.1

There exists a spanning tree such that as .

Condition 3.1 ensures that the minimum number of comparisons along some spanning tree increases to infinity. More concretely, for any pair , either or there exists a path such that . That is, all pairs of items are compared infinitely many times either directly or indirectly. The rate at which where grows to infinity is left unspecified; in fact the rate may be edge specific. It is easy to see that if at least one , then Condition 3.1 does not hold. However, the fact that all for all does not imply that Condition 3.1 holds. For example, consider a complete graph with four vertices. Suppose that and where is fixed and . It is easy to verify that all ’s tend to infinity but Condition 3.1 is not satisfied.

Theorem 3.1

Theorem 3.1 establishes that the LSE is consistent provided a graph–based condition, i.e., Condition 3.1, holds. Next note that the Laplacian is symmetric and non–negative definite so its spectral decomposition is where is an orthogonal matrix and with Since is connected and . Furthermore where . Using graph decomposition arguments, and Weyl’s inequality (Horn and Johnson, 2007) it can be shown that if Condition 3.1 holds then . In spectral graph theory the value of is referred to as the algebraic connectivity of (Cvetkovic et al. 2009). Further note that the mean squared error of is

which converges to zero at the rate at which . Several authors (e.g., Shah et al. 2015) have also noted that bounds on the mean square error in binary PCD also depend on the algebraic connectivity. The relationship (8) implies that we can estimate the merit at a rate proportional to the smallest element of and the constant in (8) is a function of the algebraic connectivity. This is somewhat surprising and different from what is observed in the usual sample case. Finally, it is worth noting that the condition that for all is not sufficient to guarantee that in probability. For example consider the graph with and where and . Clearly each as , however is bounded for all and it is easy to verify that the variance matrix does not converge to . Next, strong consistency without a variance is established.

Theorem 3.2

Thus, provided the errors have mean zero, the merits converge to their true value with probability one. The rate of convergence is explored by simulation in Section 6. The proof of Theorem 3.2 is rather involved. In addition to the usual probabilistic arguments the proof relies on specialized results in linear algebra (Satorra and Neudecker, 2015) and graph theory. In particular we use the all minors matrix tree theorem (Chen 1976, Chaiken, 1982) and various properties of Laplacians (Chebotarev and Shamis 1998, and Bapat 2013).

Condition 3.2

There exists a spanning tree such that

It is clear that Condition 3.2 is stronger than Condition 3.1. Condition 3.2 implies that for all pairs and in . It can be further shown that Condition 3.2 implies that for any two items , i.e., the total number of paired comparisons for all items grows at the same rate. Formally this means that for all and for all . However for all does not imply that Condition 3.2 holds as demonstrated by the following example.

Example 3.1

Consider a line graph with four vertices such that and . Clearly Condition 3.2 does not hold for this example however for . Moreover, and

does not converge.

Condition 3.2 results in well behaved variance matrices for the LSE.

Lemma 3.1

If Condition 3.2 holds then exists and . Moreover as where all diagonal elements of are positive and .

We are now ready for a CLT.

Thus the LSE, properly standardized and scaled, approximately follows a normal distribution in large samples. One consequence of Theorem 3.3 is that the asymptotic variance of the LSE is determined only by the limit of the graph Laplacian, i.e., by connectivity properties of . In particular the limiting variance depends only on only those for which , all others are awash.

Next, we focus on the associated ranks. Recall that corresponding to the vector of merits we have a vector of ranks where . Clearly belongs to the permutation group of . Note that if then the score is the largest score, if then the score is the second largest and so forth.

Theorem 3.4

Theorem 3.4 shows that the ranks can be identified with probability one at an exponentially fast rate if the tails of the error distribution decay fast enough. Let be any metric on ranks such as the Kendall, Caley and the Footnote distances (cf. Marden 1995). Theorem 3.4 insures that is exponentially small as grows to .

Remark 3.1

In fact, since: with probability one; and the function is continuous on the set where ; it follows by the continuous mapping theorem that with probability one.

We conclude this section with a selection of hypothesis testing problems which can be addressed using the theory developed thus far.

-

1.

Consider the hypothses versus . Thus, under the null all items are equivalent whereas under the alternative they are not. Hotelling’s statistic for this problem is

(9) where , is a natural estimator of and the last equality above follows from Lemma 4.3 in Bapat (2010). Furthermore, by combining Theorem 3.3 with Theorem 2 of Moore (1977) we find that under local alternatives, i.e., when the vector of merits equals , we have

Therefore the null is rejected if the right–hand–side of (9) exceeds the quantile of . This procedure can be modified for testing the equality among any subset of merits. For example, when testing against where and is a strict subset of then (9) reduces to and under local alternatives, where is the submatrix of corresponding to items . In particular if then

where and are element of and , respectively.

-

2.

Next, consider an ANOVA type hypothesis of the type against for some . This system can be reformulated as versus where is a matrix whose row is a contrast comparing the and elements of . The natural test statistic is

(10) which converges in distribution (under local alternatives) to a RV. In particular if , i.e., items and are being compared then (10) reduces to

where is the element of .

-

3.

In some circumstances it is of interest to test whether all items have different merits. Formally, this amounts to testing against . Clearly this is an intersection–union type test (Casella and Berger, 2021), in which the null is the union of and the alternative is of the form . An appropriate test statistic is

It is not hard to see that the least favorable configuration under the null hypothesis is attained at . Let be an matrix of pairwise contrasts, e.g., its first row is of the form comparing the first and second items. The limiting distribution of is equal to the distribution of where is a RV. Hence can be tested by comparing with the quantile of the distribution of which is easily computed by simulation.

-

4.

Many questions regarding the ranking of items are of interest. For example one may be interested in testing whether a specific item, the first say, is better than all others. Nettleton (2009) studied such a problem for multinomial cell probabilities. The complement of the latter testing problem is for all against for some ; clearly under the null item is associated with the smallest merit whereas under the alternative it is not. Note that the null can be expressed as and the alternative as . A natural test statistic is for this problem is

Clearly the least favourable configuration under the null is attained when . Let be matrix whose rows are contrasts with respect to the first item, i.e., in row first element is , element is and other elements are zero. The limiting distribution of is equal to where . The critical value can be easily obtained by Monte–Carlo methods.

There are many other related problems involving inference on item ranks (Xie et al. 2009). Unlike the classical theory PCGs induce a dependence among the estimated merits which complicates the analysis. See also Hung and Fithian (2019) for a related problem.

4 Incorporating covariates

There are situations in which it is advisable and effective to incorporate covariates into models for paired comparisons. For example, Harville (2003) modeled the expected outcome of NCAA basketball league games between teams and by where for a home game and otherwise. Clearly, if then and vice versa. Therefore equals if the game is played on the home–court of team and if the game is played on the home–court of team . The parameter measures the effect of playing on ones own turf. More generally each paired comparison is associated with a pair of covariates. The resulting data structure which we denote by

| (11) |

is a PCG with covariates. Note that and are as before while .

There are numerous ways of modeling the effect of covariates on the outcomes. We adopt the following model:

| (12) |

which is a natural, ANCOVA type, extension of (1). Covariates are incorporated by setting for some function . For example a simple and reasonable choice is in which case mimicking the modelling choice of Harville (2003) and mirroring the relationship . Implicitly this choice of corresponds to the very natural situation in which the merit of the item in the presence of a covariate is . Many other options are possible including models in which each item is associated with an individual regression parameter. However, for the simplicity of the exposition we will not venture beyond the relatively general model (12). Furthermore, we will not address model selection with respect to , which is of course an important problem, and assume that is given a priori. We shall refer to as the covariate and emphasize that its value may vary across comparisons even among the same two items. It is assumed here that where is a given positive integer. The covariates may be fixed constants or stochastic; if so they are assumed, as usual, to be independent of the errors.

The parameters in (12) may be estimated by

| (13) |

where is the parameter of interest, was defined earlier, and

| (14) |

is a sum of squares. We will refer to the resulting estimator as the LSE. It will be useful to view (12) as the following multiple linear regression model:

| (15) |

where is the vector of outcomes arranged by their lexicographical order, i.e.,

is the corresponding vector of errors and is the design matrix. The matrix is a matrix whose elements . Specifically if the element of is where , then the elements of the row of are and for all . The matrix is a matrix whose column corresponds to the covariates arranged by their lexicographic order. With these notations it is easy to verify that

| (16) |

To fix ideas an example is provided.

Example 4.1

Consider a PCG where is a line graph with three vertices, and , and . Here,

Further, and

Condition 4.1

The matrices and satisfy

By Theorem 5 in Puntanen et al. (2011) Condition 4.1 is equivalent to . Now if and only if is connected, which is the sufficient condition for the existence of the LSE without covariates. It is not difficult to show that Condition 4.1 holds provided: (i) ; (ii) ; and (iii) , i.e., the columns of and span different non–null subspaces. In particular, if is comprised of a single covariate, i.e., , then verifying Condition 4.1 is exceptionally simple.

Proposition 4.1

Let then if and only if for some constants in which case Condition 4.1 does not hold.

The following theorem extends Theorem 2.1 to the situation where covariates are present.

Theorem 4.1

Note that the expression for appearing in (18) is reminiscent of the weighted LSE in a linear regression model, whereas is the LSE of a graph–LM without covariates with (adjusted) outcomes . In the proof of Theorem 4.1 a general expression for the LSE for any constraint vector is provided see (38). Observe that the normal equations associated with (15) are which can also be written as

| (19) |

The Laplacian appearing above highlights the dependence of the estimators on the structure of the graph. Proposition 4.1 indicates that the LSE is well defined and unique for all reasonable design matrices. In particular, if the covariates are random variables the the LSE exists with probability one as .

Let

denote the smallest principal angle between the subspaces spanned by columns of the matrices and where the index on emphasizes its implicit dependence on the total sample size.

Condition 4.2

The smallest eigenvalue of diverges and for all large we have for some .

It is well known, e.g., Fahrmeir and Kaufmann (1985), that consistent estimation in standard regression problems requires that the smallest eigenvalue of diverges. The latter together with Condition 4.2 guarantee that the norm of the residual of projected onto the span of does not vanish as . Otherwise the second smallest eigenvalue of may not diverge. Two relevant examples are provided.

Example 4.2

Consider a PCG where satisfies Condition 3.1, , so the matrix is just a vector , and is large. Suppose that for the first observations we have . Next assume that for all we set , i.e., we equate the elements of and the first column of . Clearly, and . Since the orthogonal projection is the nearest point to in , we have

| (20) |

Further, the angle between and is

Consequently, Condition 4.2 does not hold. Note that (20) implies that does not diverge; however does diverge. Consequently, the second smallest eigenvalue of is finite as .

Example 4.3

Consider a PCG with and . Clearly, Condition 3.1 is satisfied. The first and second columns of the matrix are and respectively. We choose such that if for some and otherwise. Clearly, , and as . Next, the orthogonal projection of onto is

Therefore,

Consequently, as . However, the second smallest eigenvalue of is

With some algebra, it can be shown that as so Condition 4.2 is not necessary for the divergence of the second smallest eigenvalue of .

Condition 4.2 is trivially satisfied when the spaces spanned by the columns of and are orthogonal. In such situations the matrix on the LHS of (19) reduced to and the conclusion of Lemma 4.1 is immediate. Interestingly it can also be shown that if where is the Fiedler vector of the graph (i.e., is the eigenvector associated with the second smallest eigenvalue of ) then Condition 4.2 holds as well. Finally, we note that Condition 4.2 is unlikely not to hold in practice. For if it were so at least one column of , or a linear combination thereof, would need to at least approximately satisfy the conditions of Proposition 4.1. This seems very unlikely. Further support for the assertion that Condition 4.2 will hold in applications is given in Lemma 4.2 appearing below.

Lemma 4.2

If the columns of are independent and components in each column of are IID with zero mean and finite variance then as the smallest eigenvalue of diverges and with probability one.

Thus, if the covariates are centered and random then Condition 4.2 holds with probability one.

Condition 4.3

The smallest eigenvalue of is positive and for all large we have for some .

If Condition 4.3 holds then all eigenvalues of grow at the same rate. Clearly Condition 4.3 implies Condition 4.2 and is an analogue of Condition 3.2 for PCGs without covariates.

Consequently the conditions in Lemma 4.3 guarantee the existence of an asymptotic variance of the corresponding LSEs. Note that implies that the second smallest eigenvalue of diverges, however the converse is not true, cf., Example 4.3.

Remark 4.1

Condition 4.2 essentially generalizes the usual condition for consistency in standard regression models of the form , i.e., that to the case of partitioned matrices. That is if then consistent estimation is guaranteed if for and that for all large . Similarly, Condition 4.3 extends the standard condition for asymptotic normality of in regression models, i.e., that to the case of partitioned matrices. That is if then the asymptotic normality of the LSE is ensured if for , for all large .

Condition 4.4

Let

where is the row of .

Condition 4.4 is essentially a Hajek–Sidak type condition. It ensures that the contribution of any finite set of observations is negligible as .

Theorem 4.2

We have:

Theorem 4.2 shows that under mild conditions the LSE and the derived rank vector are consistent and that the LSE is asymptotically normally distributed for graph–LMs with covariates. The asymptotic variance is easily estimated so inference on is readily carried out.

Next we examine the situation where the true model is (12) but a model without covariates, i.e., model (1), is fit to the data. Note first that the LSE given in (4) is generally biased and not consistent if the columns of and are not orthogonal (c.f., Zimmerman 2020). However, orthogonality among and may arise. For example, consider a round–robin tournament where the covariate indicates whether the game was played on the home court or not, cf. Harville (2003). If the tournament is completely balanced, i.e., teams and compete on both home courts the same number of times, then it is easy to verify that columns of and are orthogonal. Therefore the merits can be unbiasedly and consistently estimated. Furthermore, it turns out that the LSE for the model without covariates is often consistent when true model does include covariates. This, and related themes, are explored in the next theorem for which we introduce the following notation. Let , indexed by the parameters , denote the density associated with the true model, i.e., the model with covariates. Similarly let , indexed only by the parameter , denote the density of the misspecified model, i.e., the model without covariates. Let

denote the conditional average Kullback–Leibler (AKL) divergence between the two models.

Theorem 4.3

We have the following:

In the proof of Part of Theorem 4.3 an expression for , under normality, is found and shown to be minimized at when , i.e., when and are “nearly” orthogonal. This is a distributional result which suggests that under near orthogonality the merit parameters in the true and misspecified model have asymptotically similar values. Implications for estimation are explored in Parts and of Theorem 4.3. Part of Theorem 4.3 explores the limiting distribution of the LSE when the true model holds. In particular the form of the bias term is found. The bias can be shown to vanish when . However removing the bias from the asymptotic distribution requires that which is a stronger form of near orthogonality. See section 5.2.2 in Claeskens and Hjort (2008) for related analyses. Finally, in Part of Theorem 4.3 a stochastic representation of the LSE when the covariates are centered RVs is found. In essence it is shown that random covariates enable decoupling the estimation of the merits and regression coefficients. This phenomenon is a consequence of the geometry of high–dimensional spaces (Vershynin 2020).

5 Infinite number of items

So far we have treated as fixed. In this section graph-LMs are extended to the case where . For simplicity we will first assume that no covariates are present. In this setting one can imagine a sequence of nested comparison graphs , . A common practice in such settings is to choose a reference item, denoted by , and set . In this way the merits of all other items are fixed. However, we will continue with the assumption that which is fully justified by Corollary 2.1 but implies that the value of any merit may vary with .

There are numerous comparison regimes to consider when . Although it is possible that some when such scenarios are less likely; moreover, as will become evident, such situations are much easier to analyze. Therefore in this section we shall assume that for all pairs . The following theorem describes the behavior of the vector of estimated merits in a round–robin tournament in which the number of items grows to infinity.

Theorem 5.1

Consider the model (1). Let for all . If then for every finite subset of indices the elements of the LSE satisfy

| (21) |

Consequently, the maximum estimation error satisfies

| (22) |

Equation (21) shows that the CLT holds for any finite collection of items. Note that the independence among the estimated scores is a consequence of the fact that for all and . Moreover, for convenience, the scaling factor in (21) is the square root of the number of items and not the total number of comparisons as in Theorems 3.3 and 4.2. Since , (21) holds also when scaled by instead of . Further note that (21) implies that the RVs where behave as a sequence of independent standard normal RVs the largest of which is of order . Thus (22) holds and can be understood as the rate at which the largest converges to . Theorem 3.4 can also be used in conjunction with Theorem 5.1 to show that the probability of correct ranking converges exponentially fast for any finite subset of indices.

Simons and Yao (1999) proved a theorem similar to 5.1 in the context of Bradley–Terry models, which is a model for binary PCD. Their conditions for consistency and asymptotic normality are much more complicated than those appearing here. In fact no restrictions on the parameters is required in Theorem 5.1 whereas for binary PCDs various regularity conditions on the parameter space must be imposed. For example, it is well known that the merit vector in Bradley–Terry models can not be estimated if there exists a partition of the items into two nonempty sets in which every item in one set is preferred to all items in the other. Simons and Yao (1999) show that if

then such a partition does not exist with probability one while more elaborate conditions are required for consistency and asymptotic normality.

In a complete graph there are distinct comparisons. Next, we consider sparse graphs in which the number of comparisons is much smaller than . One way of doing so is by letting the topology of the comparison graph be determined randomly. To this affect we employ Erdos–Reyni random graphs in which the comparison (edge) is present with probability , independently from every other edge (Janson et al., 2000). Concretely, consider the PCG where the graph is a Erdos–Reyni graph with parameters . Its Laplacian is the random matrix

where are IID RVs. The number of paired comparisons on an Erdos–Reyni graph is of the order and it is well known that such graphs are connected with probability one, as , if and only if for some (Erdos and Renyi 1961). Clearly, the merits can not be estimated unless the comparison graph is connected.

Condition 5.1

For all large assume that for some .

Then,

Theorem 5.2

Theorem 5.2 shows that the LSE is consistent and asymptotically normal provided (only) that the Erdos–Reyni graph is connected as . The proof is based on writing as the random sum . Note that

Since is a binomial RV with parameters , it is now clear that both and are consistent for . Furthermore the relation (24) holds even if is replaced with which is an alternative simple estimator for the merit. In fact this is a randomized version of the so–called row–sum method (Huber, 1963). Moreover, the computation of ’s does not involve inversion of the Laplacian matrix, which is an advantage. Han et al. (2020), who generalized the work of Simmons and Yao (1999) for large sparse graphs, established that for the Bradley–Terry model for some is required for asymptotic normality. In addition they also required some conditions on the parameter space. On the other hand, the linear model requires only that for some as to ensure asymptotic normality, cf. Theorem 5.2. Thus, compared with Bradely–Terry models graph-LMs allow for much sparser comparison graphs.

Next we note that Han et al. (2022) found that if for some then the merit vector in the Bradley–Terry models satisies the following uniform bound

with probability at least . Observe that when , equation (24) and Markov’s inequality imply that

| (25) |

Substituting for some shows that the RHS of (25) converges to , which implies in turn that the LSE in sparse random comparison graph is uniformly consistent. The bound within the probability statement on LHS of (25) is satisfied with probability larger than . Thus compared with Bradley–Terry models we obtain much tighter bounds on sparser graphs. We conclude with a remark.

Remark 5.1

Theorem 5.2 can be extended to situations where is a random graph with varying edge probabilities (cf. Janson et al., 2000) and to the general case where are arbitrary independent RVs. Such a graph may arise when the degree of an item is dependent on its merit, i.e., more popular items are compared more than less popular ones. Examples include IMDB, a movie rating website and Amazon, an online retailer. In such a case, we believe that consistency of the LSE will hold if the graph is connected and degrees of all items increase to infinity as . However, we do not attempt to establish such a result in the current article.

6 Numerical experiments

We evaluate the performance of the LSEs on graph-LMs by simulation in three different settings:

- 1.

-

2.

Graph–LMs with covariates: Next, we investigate the properties of LSEs in PCGs with covariates. Our focus is on assessing the influence of covariates on the accuracy of the estimators described in Theorem 4.3.

- 3.

6.1 Simple graph-LMs

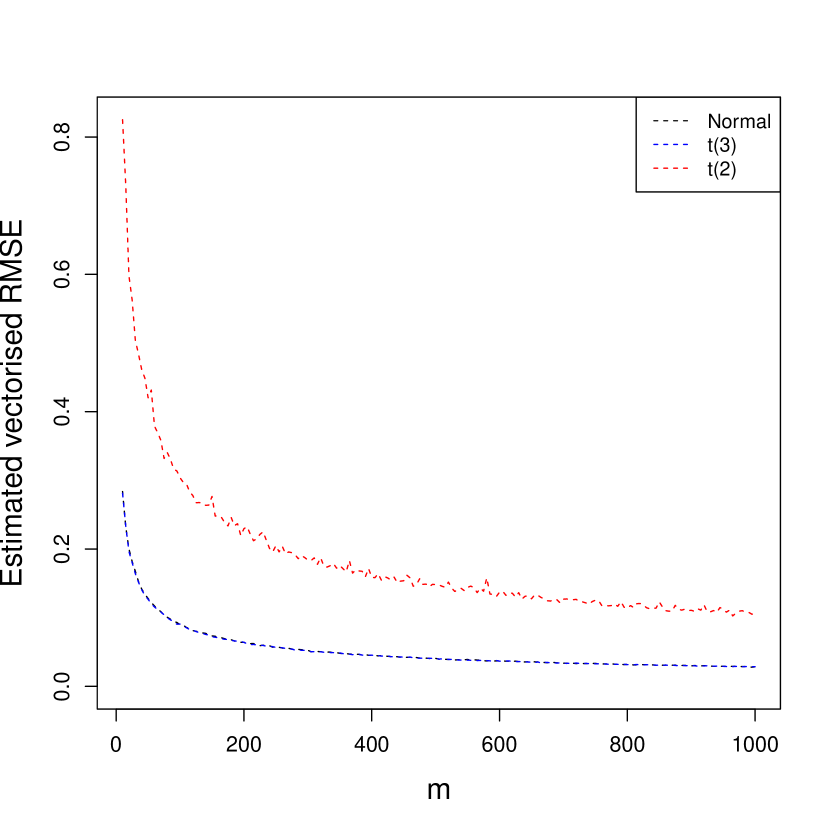

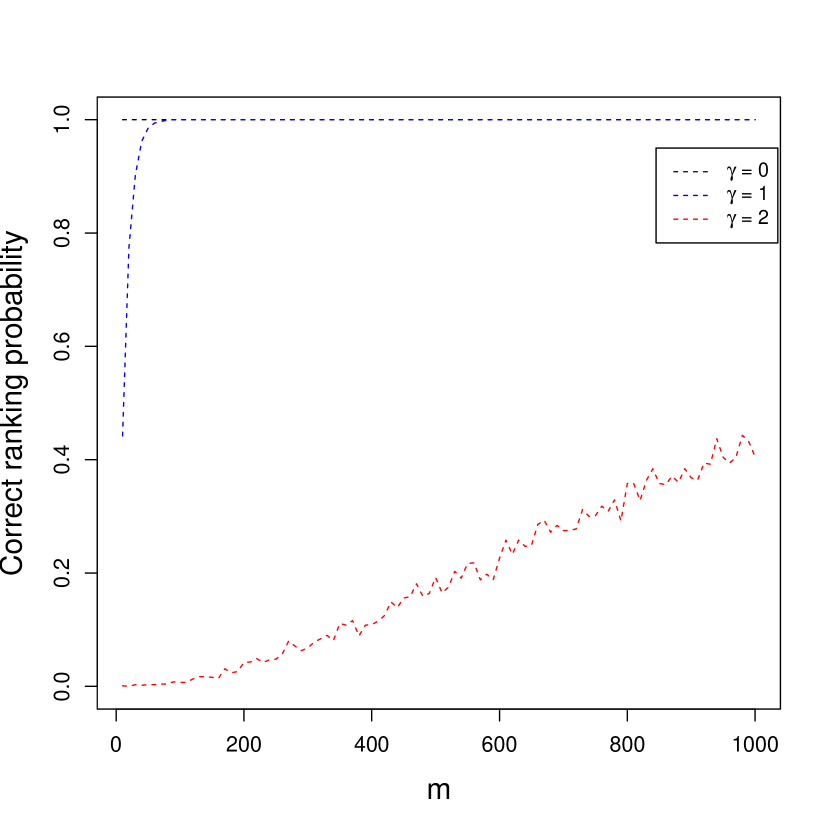

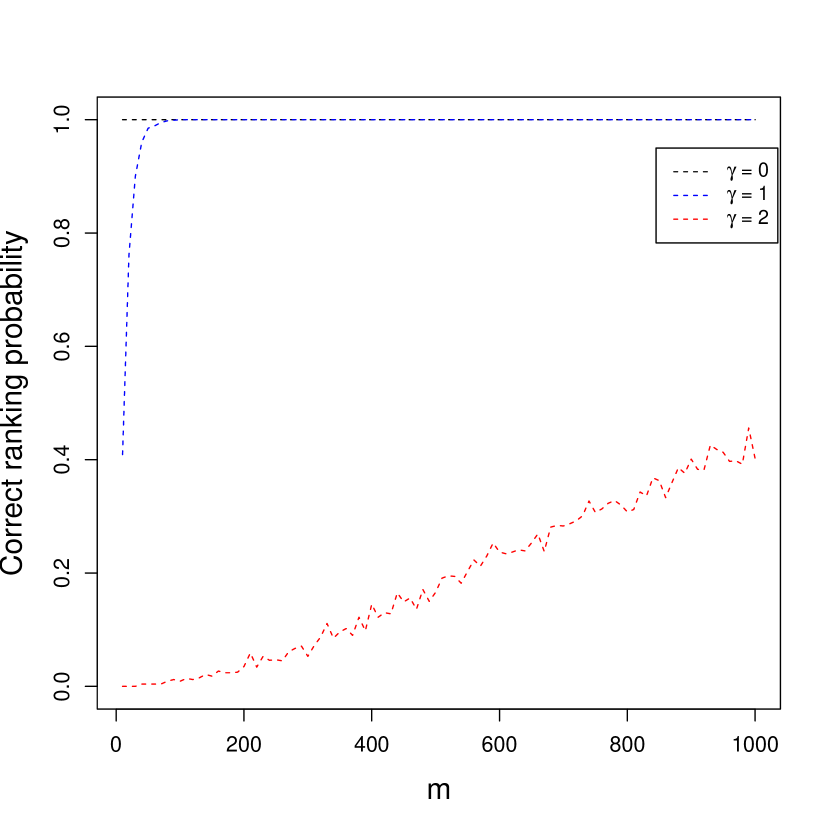

In our simulation study of model (1) we assume a complete graph with and where and . The number of paired comparisons . We experimented with three error distributions, namely , a t–distributed RV with two degrees of freedom, and . Note that a t–distributed RV with two degrees of freedom has a mean but does not have a variance. The variance of the RV is one. In Figure 3(a) we plot the empirical mean squared error (MSE), i.e., , against , where is the LSE computed at the simulation run and is the number of runs. In Figure 3(b) we plot the probability of correct ranking, i.e., , against for three values of assuming the errors are .

Figure 3 Comes Here

It is clear from Figure 3(a) that in all three cases the MSE decreases as increases. The MSEs when the errors are either or seem similar. Nevertheless the MSEs associated with are always smaller than those associated with errors; the difference among the aforementioned MSEs is most pronounced for small values of . In both cases the MSE decays at the expected rate. The MSEs associated with errors behaves quite differently. They seem to decrease at a much slower rate and the empirical MSE curve is not smooth. This is caused by occasional very large errors. In fact since RVs do not have a finite variance the theoretical MSE, i.e., does not exist. This means that once in a while the value of the empirical MSE will shoot up. Nevertheless by Theorem 3.2 the LSE is consistent even in this case. Figure 3(b) provides a complementary view. Note that the probability of correct ranking increase with . When the spacing’s among the means is large this probability is very close to unity. Clearly, it is difficult to rank correctly when the spacing’s are small.

The simulation experiments described above were also carried out for path and cycle graphs with qualitatively similar results.

6.2 Graph–LMs with covariates

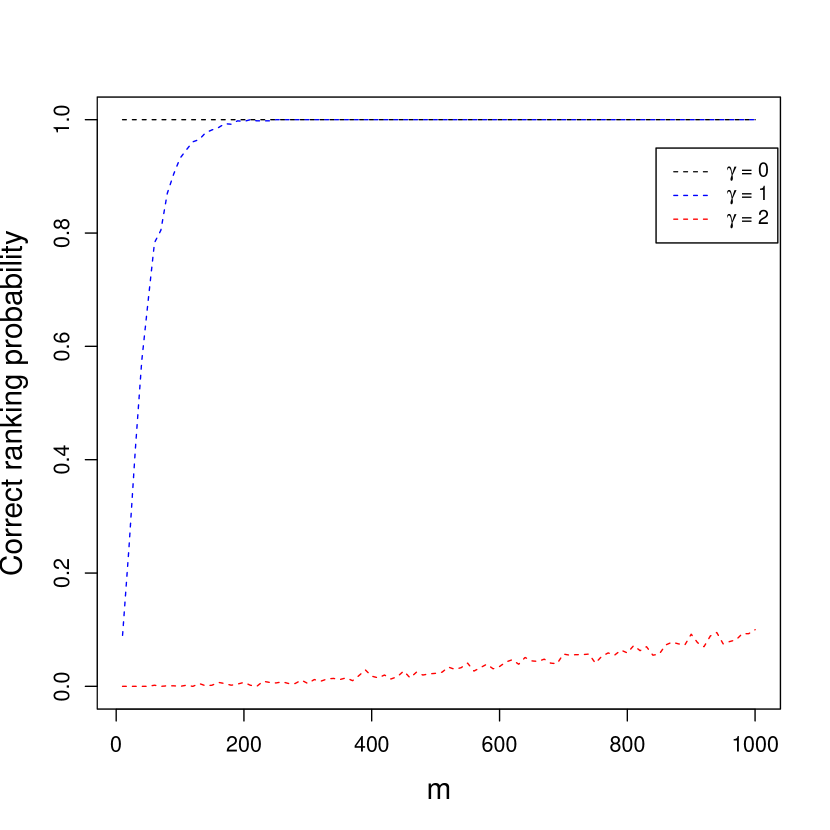

We assume the same graph topology, , and ’s used in Section 6.1. We set and let the bivariate covariate be independent Rademacher RVs, i.e., for . Data was simulated from model (12) assuming the error distribution is .

We fit the model with and without covariates. When fitting the model with covariates we observe, as expected from Theorem 4.2 that the LSE is consistent and converges at the expected rate. Next we fit the model ignoring the covariates. Recall that By Theorem 4.3 the LSE for the vector of merits is also consistent when the covariates are ignored.

Probabilities of correct ranking are presented in Figure 4. Observe that the derived ranks are estimated correctly with high probability even after ignoring covariates, although less efficiently. For example, when and the probability of correct ranking when covariates are included in the model is close to and only when the covariates are omitted.

Figure 4 Comes Here

The simulation experiments described above were also carried out for other distributions of covariates, e.g., the distribution, as well as correlated covariates with similar qualitative results.

6.3 Large graph-LMs

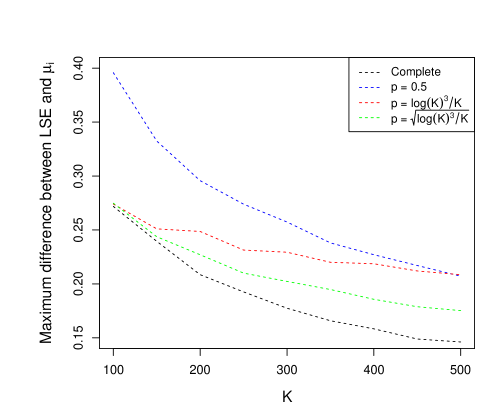

We consider model (1) with . We set and the errors are IID RVs. The ’s are IID Bernoulli RVs with parameter for . Clearly when we have for all , i.e., the graph is complete graph. The other values of are the same as those in Han et al. (2022)

The value of against is plotted, for the aforementioned values of , in Figure 5. Clearly for any fixed the estimation error is decreasing in . Similarly for every fixed the estimation error decreases as increases. We also experimented with a value which is slightly above the theoretical threshold required for convergence, cf. Theorem 5.2. We have found that the convergence of the LSE for this value of to be very slow.

Figure 5 Comes Here

7 Illustrative example

Ranking sports teams is of general public interest and an active application area for ranking methodologies. For illuminating details see the book by Langville and Meyer (2012).

Here, we illustrate the proposed methodology by consider the ranking of NBA teams in 2022–2023 season. The data were obtained from the Basketball Reference Website (https://www.basketball-reference.com/leagues/) and is comprised of regular season games played by the teams comprising the league. In addition to the score and the point–spread, our outcome variable, we record whether the game was played at home or away, and the ranking of the teams in the past two seasons, i.e., seasons 2020–21 and 2021–22. We fit the model

| (26) |

Here for a home game, otherwise, and denote the expanded standings of the team in seasons 2020–21 and 2021–22 respectively. Note that the first regressor the second regressor , as is the third regressor. The parameter quantifies the effect of playing at home, whereas and quantify historical effects.

Table 1 list the rankings derived by fitting four nested submodels of (26) referred to as Models I–IV. Model I, corresponds to a model without any covariates, subsequent models incorporate the covariates, as they appear in (26), culminating in Model IV which includes all three covariates. Teams are listed from left to right according to their expanded standing for the 2022–23 season. Observe that Models I and II yield identical rankings, whereas Models III and IV also yield similar rankings which differ quite substantially from those given by the models without covariates.

Table 1 Comes Here

Table 2 provides the Cayley distance among the different models. We note that the full model is highly significant so there is clear evidence that Model IV should be adopted. The fact that rankings derived from Model I and Model IV are different indicates that and are not orthogonal and the Conditions in Theorem 4.3 do not hold in this example and omitting the covariates may result in an improper ranking.

Table 2 Comes Here

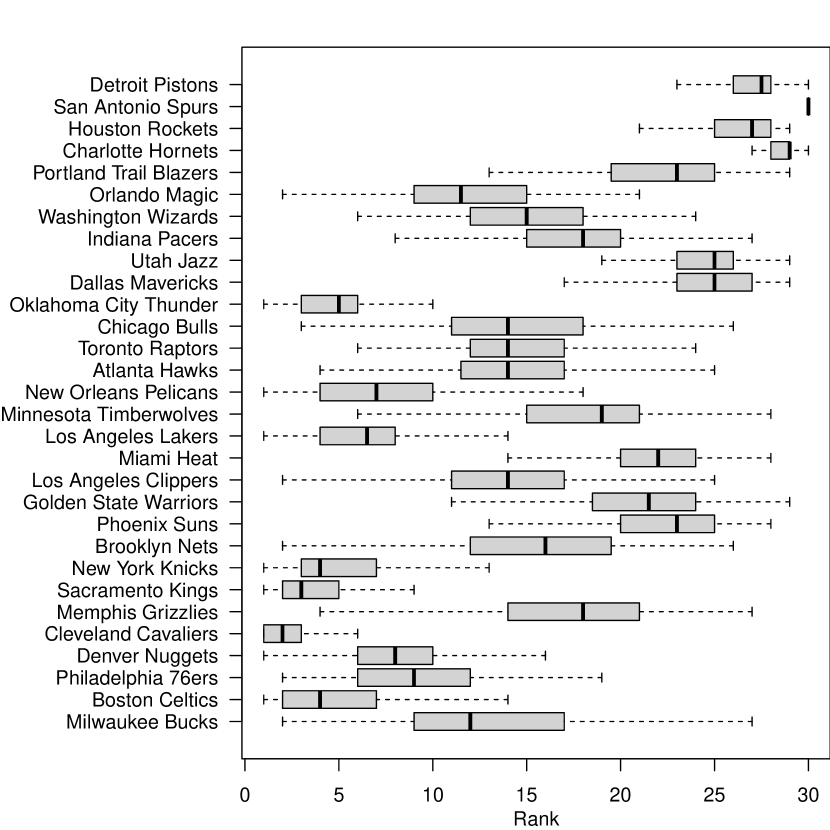

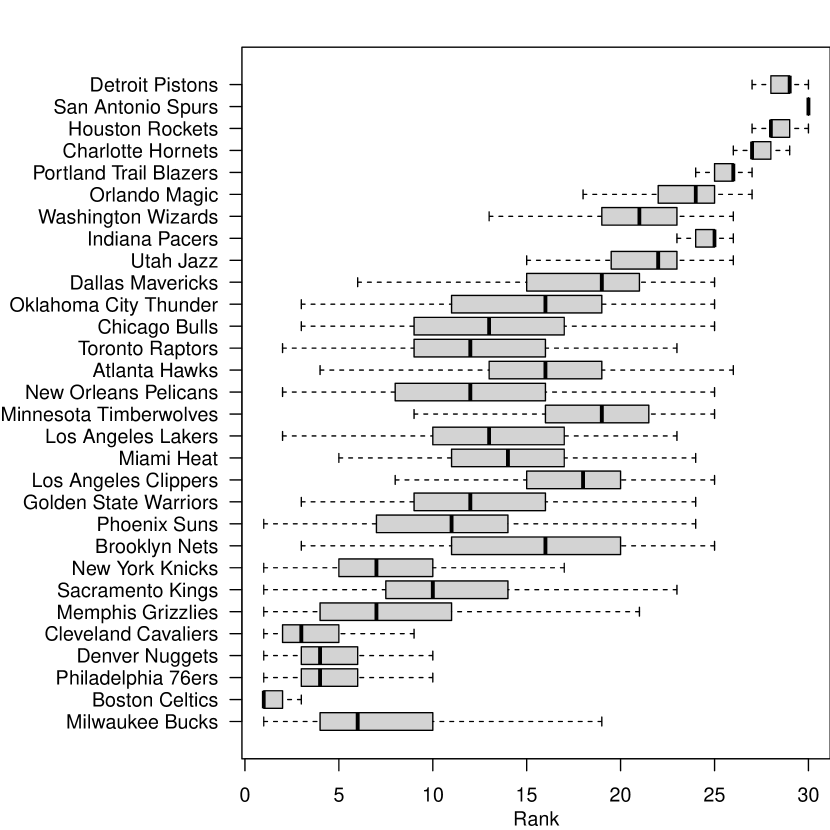

The accuracy and variability of the estimated ranks were assessed by nonparametric bootstrap. Concretely, rankings were estimated in bootstrap samples and the resulting boxplots of ranks are given in Figure 6.

Figure 6 here.

Figure 6 reveals several interesting features. First, variability is not even among all teams. The interquartile (IQR) range for the rank of the Boston Celtics is in Model I and in Model IV. This is a team whose ranking exhibits little variability. In contrast, the corresponding IQRs for the Oklahoma City Thunders are in Model I and in Model IV. It is also clear that overall variability is high for middle ranked teams and less so for the best and worst teams. We also observe that the variability in Model IV is somewhat smaller than the variability in Model I although the difference is not very large.

8 Discussion

Despite the simplicity of models for cardinal PCDs and the extensive literature on the LSE, the statistical properties of the LSE have not been been well studied. Consequently, and surprising, methods for conducting inference were not sufficiently grounded. This paper fills this gap by developing a graph–based, rigorous statistical theory, that enables the conduct of inference for such models.

Our investigation starts with model (1). We find explicit necessary and sufficient graph–theoretic conditions that guarantee consistency, rates of convergence and a central limit theorem. Next, we analyzed PCGs with covariates. To the best of our knowledge this paper is the first to do so in any generality. Conditions for consistency and asymptotic normality are provided. It is also shown that in many situations arising in practice the merits can be estimated consistently even if covariates are omitted from the model. This surprising result is a consequence of the geometry of high–dimensional spaces. Note also Remark 4.1 where the connection between PCGs with covariates and standard regression problems with two disjoint sets of explanatory variables is made. Another extension provided is to situations in which the number of items compared is large, i.e., and the number of paired comparisons between and any two items is small, i.e., or . Such situations have been analyzed for binary PCD, e.g., Simon and Yao (1999), Han et al. (2020) and the references therein, but not for cardinal PCD. Our analysis, like theirs, assumes an Erdos–Reyni random graph and establishes consistency and asymptotic normality provided for some . Uniform consistency requires that for some . Thus, in contrast with binary models no restrictions on the parameter space are necessary and, in addition, limit theorems are available on sparser graphs.

Our work can be extended in many possible directions. For example, our results strictly apply to homoscedastic errors; their extension to hetroscedatic errors is straightforward. In this section we focus on more substantive extensions five of which are listed. There are many more. The first two arise within the modelling framework discussed here. Each of these can be addressed in various fashions. Then, we outline three other more general problems which are, in our view, of significant importance.

-

1.

Robust methods for cardinal PCD: Our simulation results indicated that even when the errors are the merits can be estimated consistently but at a slower rate compared to the situations when the variance of the error is finite. For error distributions without a mean, e.g., the Cauchy distribution, the estimator is not consistent. Thus there is a need for suitably modified robust estimators which can handle heavy–tailed error distributions. Huber–type estimators, or least absolute deviation type estimators are possibilities which require a detailed investigation.

-

2.

Optimal design for PCD: The planning of experiments for PCD is another area which has not received adequate attention. In the context of cardinal PCDs one can use the form of to construct optimal experimental designs for eliciting information on . There is some work in this area (Grasshoff, 2004) but not for cardinal PCD. It would be interesting to examine A–optimal, D–optimal and other optimality criteria (cf. Pukelsheim, 2006) for sequential and non–sequential designs for estimating . It is also clear that different experimental objectives, e.g., finding the best item, the –best and so forth, will yield different designs.

-

3.

Non–transitive and cyclical PCD: Model (1) imposes, what is called a linear transitive ordering, cf. Latta (1979), Oliveira et al. (2018), on the items . However the model may not fit the data, i.e., the expected value of may not equal for all pairs . In such cases the model where must be adopted. The most general model imposes no restrictions on the vector of means . It is important to note that the model indexed by captures a much broader range of preference relations compared to the model indexed by . In particular it may capture a variety of transitivity relations as well as preference relations which are not transitive. Such relations are called cyclical preference relations. The problems of non–transitivity and cyclicality are, unresolved, long standing problems in the field. We have made progress towards a principled resolution of the aforemantioned problem, which will be published separately.

-

4.

Graphical generalized linear models: This paper focuses graph–LMs, i.e., graphical linear models. Some of our theoretical results rely on linear algebraic tools. A natural question arises as to whether, and how, the methodology developed here can be used to model situations in which the outcome of a paired comparison follows a generalized linear model. The resulting class of generalized graphical linear models, i.e., graph-GLMs, are eminently worthy of study. These include of course, binary and ordinal outcomes. Clearly there is a lot to do within this area.

-

5.

Order restriced inference for PCD: Finally we note that many scientific questions arising in the context of paired comparison data are questions about order. Such problems are best formulated and addressed within the context of order restricted statistical inference (cf. Silvapulle and Sen 2005). Very little work in this direction has been carried out. For example, by an specifying orderings on subsets of items for all where the set is a set of prespecified partial ranking (i.e., a ranking of a subset of items) there is a potential of improving the overall accuracy. This is especially true for large sparse graphs where unstable rankings (e.g., Hsieh et al. 2011) are common. The power of tests on the merits and ranks can be also improved by imposing order restrictions. The relations with the classical problems of selection of the best population(s) is obvious.

Acknowledgments

The work of Rahul Singh was conducted while a post doctoral fellow at the University of Haifa. The work of Ori Davidov was partially supported by the Israeli Science Foundation Grants No. 456/17 and 2200/22 and gratefully acknowledged.

References

- [1] Atkinson, A., Donev, A., and Tobias, R. (2007). Optimum experimental designs, with SAS (Vol. 34). OUP Oxford.

- [2] Ailon N, Charikar M and Newman A (2008). Aggregating inconsistent information: ranking and clustering. Journal of the ACM, 55: 23–49.

- [3] Alvo M and Yu PLH (2014). Statistical Methods for Ranking Data. Springer.

- [4] Balinski M and Lariki R (2010). Majority Judgement: Measuring, Ranking and Electing. MIT Press.

- [5] Bapat RB (2013). On minors of the compound matrix of a Laplacian. Linear Algebra and its Applications, 439: 3378–3386.

- [6] Bapat RB (2010). Graphs and Matrices. Springer.

- [7] Barrow D, Drayer I, Elliott P, Gaut G and Osting B (2013). Ranking rankings: an empirical comparison of the predictive power of sports ranking methods. Journal of Quantitative Analysis in Sports, 9: 187–202.

- [8] Bozzo, E. (2013). The Moore–Penrose inverse of the normalized graph Laplacian. Linear Algebra and its Applications, 439(10), 3038-3043.

- [9] Bradley RA and Terry MA (1952). Rank analysis of incomplete block designs. Biometrika, 39: 324-345.

- [10] Buhlmann H and Huber PJ (1963). Pairwise comparisons and ranking in tournaments. The Annals of Mathematical Statistics, 34: 501-510.

- [11] Casella, G., and Berger, R. L. (2021). Statistical inference. Cengage Learning.

- [12] Chaiken S (1982). A combinatorial proof of the all minors matrix tree theorem. SIAM Journal of Algebraic Discrete Methods, 3: 319–329.

- [13] Chebotarev PV and Shamis EV (1998). On proximity measures for graph vertices. Automation and Remote Control, 59: 1443–1459.

- [14] Chen WK (1976). Applied Graph Theory, Graphs and Electrical Networks, 2nd ed. North-Holland, New York.

- [15] Claeskens, G. and Hjort, N. L. (2008). Model selection and model averaging (Vol. 330). Cambridge University Press.

- [16] Cremonesi P, Koren Y and Turrin R (2010). Performance of recommender algorithms on top-n recommendation tasks. Proceedings of the fourth ACM conference on Recommender systems, ACM, 39–46.

- [17] Csato L (2015). A graph interpretation of least squares ranking method. Social Choice and Welfare, 44: 51–69.

- [18] Cururingu M (2015). SYNC–RANK: Robust ranking, constrained ranking and rank aggregation via eigenvectors and SDP synchronization. arXiv preprint arXiv:1504.01070.

- [19] Cvetkovic D, Rowlinson P and Simic S (2009). An Introduction to the Theory of Graph Spectra. Cambridge University Press.

- [20] David HA (1988). The Method of Paired Comparisons. Hodder Arnold.

- [21] Davis–Stober CP (2009). Analysis of multinomial models under inequality constraints: applications to measurement theory. Journal of Mathematical Psychology, 53: 1–13.

- [22] Erdos, P. and Renyi, A. (1961). On the strength of connectedness of a random graph. Acta Mathematica Hungarica, 12(1), 261-267.

- [23] Fahrmeir, L. and Kaufmann, H. (1985). Consistency and asymptotic normality of the maximum likelihood estimator in generalized linear models. Annals of Statistics, 13(1), 342-368.

- [24] Finkelstein, M., Kruglov, V. M., and Tucker, H. G. (1994). Convergence in law of random sums with non-random centering. Journal of Theoretical Probability, 7, 565-598.

- [25] Furnkranz J and Hullermeier E (2010). Preference Learning. Springer.

- [26] Ghosh, S. and Davidov, O. (2020). Graph-based estimators for paired comparison data. Journal of Statistical Planning and Inference, 209, 1-11.

- [27] Gould R (2012). Graph Theory. Dover.

- [28] Govan AY (2008). Ranking Theory with Application to Popular Sports. Applied Mathematics Ph.D. Thesis, North Carolina State University.

- [29] Grasshoff U, Grossmann H, Holling H and Schwabe R (2004). Optimal designs for main effects in linear paired comparison models. Journal of Statistical Planning and Inference, 126: 361–376.

- [30] Han, R., Xu, Y., and Chen, K. (2022). A general pairwise comparison model for extremely sparse networks. Journal of the American Statistical Association, 1-11.

- [31] Han, R., Ye, R., Tan, C., and Chen, K. (2020). Asymptotic theory of sparse Bradley–Terry model. Ann. Appl. Probab. 30(5), 2491-2515.

- [32] Harville DA (2003). The selection or seeding of college basketball or football teams for postseason competition. Journal of the American Statistical Association, 98: 17–27.

- [33] Horn RA and Johnson CR (2007). Matrix Analysis. Cambridge University Press.

- [34] Hsieh F, McAssey MP and McCowen B (2011). Computing a ranking network with confidence bounds from a graph based Beta random field. Proceedings of the Royal Society, doi: 10.1098/rspa.2011.0268.

- [35] Huber, P. J. (1963). Pairwise comparison and ranking: optimum properties of the row sum procedure. The annals of mathematical statistics, 511-520.

- [36] Hung, K., and Fithian, W. (2019). Rank verification for exponential families. Annals of Statistics. 47(2) 758-782.

- [37] Janson S, Luczak T and Rucinski A (2000). Random Graphs. Wiley.

- [38] Jiang, T. (2012). Low eigenvalues of Laplacian matrices of large random graphs. Probability Theory and Related Fields, 153, 671-690.

- [39] Juhasz, F. (1991). The asymptotic behaviour of Fiedler’s algebraic connectivity for random graphs. Discrete mathematics, 96(1), 59-63.

- [40] Kwiesielewicz M (1996). The logarithmic least squares and the generalized pseudoinverse in estimating ratios. European Journal of Operations Research, 93: 611–619.

- [41] Langville AM and Meyer CD (2012). Who’s #1?: The Science of Rating and Ranking. Princeton University Press.

- [42] Li, J., Guo, J. M., and Shiu, W. C. (2014). Bounds on normalized Laplacian eigenvalues of graphs. Journal of Inequalities and Applications, 2014(1), 1-8.

- [43] Marden JI (1995). Analyzing and Modelling Rank Data. Chapman and Hall.

- [44] Matsaglia, G., and PH Styan, G. (1974). Equalities and inequalities for ranks of matrices. Linear and multilinear Algebra, 2(3), 269-292.

- [45] Meng, L., and Zheng, B. (2010). The optimal perturbation bounds of the moore–penrose inverse under the frobenius norm. Linear algebra and its applications, 432(4), 956-963.

- [46] Milliken, G. A., and Akdeniz, F. (1977). A theorem on the difference of the generalized inverses of two nonnegative matrices. Communications in Statistics-Theory and Methods, 6(1), 73-79.

- [47] Moore, D. S. (1977). Generalized inverses, Wald’s method, and the construction of chi-squared tests of fit. Journal of the American Statistical Association, 72(357), 131-137.

- [48] Mosteller F (1951) Remarks on the method of paired comparisons: The least squares solution assuming equal standard deviations and equal correlations. Psychometrika, 16: 3–9.

- [49] Nettleton, D. (2009). Testing for the supremacy of a multinomial cell probability. Journal of the American Statistical Association, 104(487), 1052-1059.

- [50] Oliveira, I. F. D., Zehavi, S., and Davidov, O. (2018). Stochastic transitivity: Axioms and models. Journal of Mathematical Psychology, 85, 25-35.

- [51] Osei, P. P., and Davidov, O. (2022). Bayesian linear models for cardinal paired comparison data. Computational Statistics & Data Analysis, 172, 107481.

- [52] Pukelsheim F (2006). Optimal Design of Experiments. SIAM.

- [53] Puntanen, S., Styan, G. P., and Isotalo, J. (2011). Matrix tricks for linear statistical models: our personal top twenty.

- [54] Rakočević, V. (1997). On continuity of the Moore-Penrose and Drazin inverses. Matematichki Vesnik, 49, 163-172.

- [55] Regenwetter, M., Dana, J., and Davis-Stober, C. P. (2011). Transitivity of preferences. Psychological review, 118(1), 42.

- [56] Satorra A and Neudecker H (2015). A theorem on the rank of a product of matrices with illustration of its use in goodness of fit testing. Psychometrika, 80, 938–948.

- [57] Sen A (1986). Social choice theory. Handbook of mathematical economics.

- [58] Sen, P. K., and Singer, J. M. (1994). Large sample methods in statistics: an introduction with applications (Vol. 25). CRC press.

- [59] Serfling, R. J. (2009). Approximation theorems of mathematical statistics. John Wiley & Sons.

- [60] Shah NB, Balakrishnan S, Bradley J, Parekh A, Ramchandran K and Wainwright MJ (2015). Estimation from pairwise comparisons: sharp minimax bounds with topology dependence. Journal of Machine Learning Research, 17: 1–47.

- [61] Silvapulle MJ and Sen PK (2005). Constrained Statistical Inference. John Wiley & Sons.

- [62] Simons G and Yao YC (1999). Asymptotics when the number of parameters tends to infinity in the Bradley–Terry model for paired comparisons. The Annals of Statistics, 27: 1041-1060.

- [63] Slutzki G, and Volij O (2005) Ranking participants in generalized tournaments. International Journal of Game Theory, 33:255–270

- [64] Vershynin, R. (2020). High-dimensional probability. University of California, Irvine.

- [65] Xie M, Singh K and Zhang CH (2009). Confidence intervals for population ranks in the presence of ties. Journal of the American Statistical Association, 104: 775–787.

- [66] Xu Q, Xiong J and Huang Q (2014). Robust statistical ranking: theory and algorithms. arXiv preprint arXiv:1408.3467.

- [67] Zimmerman, D. L. (2020). Linear model theory: With examples and exercises. Springer Nature.

Figures and Tables:

| Teams |

Milwaukee Bucks |

Boston Celtics |

Philadelphia 76ers |

Denver Nuggets |

Cleveland Cavaliers |

Memphis Grizzlies |

Sacramento Kings |

New York Knicks |

Brooklyn Nets |

Phoenix Suns |

Golden State Warriors |

Los Angeles Clippers |

Miami Heat |

Los Angeles Lakers |

Minnesota Timberwolves |

New Orleans Pelicans |

Atlanta Hawks |

Toronto Raptors |

Chicago Bulls |

Oklahoma City Thunder |

Dallas Mavericks |

Utah Jazz |

Indiana Pacers |

Washington Wizards |

Orlando Magic |

Portland Trail Blazers |

Charlotte Hornets |

Houston Rockets |

San Antonio Spurs |

Detroit Pistons |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model I | 5 | 1 | 4 | 3 | 2 | 7 | 8 | 6 | 17 | 9 | 10 | 19 | 15 | 14 | 21 | 11 | 18 | 12 | 13 | 16 | 20 | 22 | 25 | 23 | 24 | 26 | 27 | 28 | 30 | 29 |

| Model II | 5 | 1 | 4 | 3 | 2 | 7 | 8 | 6 | 17 | 9 | 10 | 19 | 15 | 14 | 21 | 11 | 18 | 12 | 13 | 16 | 20 | 22 | 25 | 23 | 24 | 26 | 27 | 28 | 30 | 29 |

| Model III | 11 | 5 | 9 | 7 | 1 | 19 | 2 | 3 | 17 | 24 | 22 | 12 | 23 | 6 | 20 | 8 | 13 | 16 | 14 | 4 | 26 | 25 | 18 | 15 | 10 | 21 | 29 | 27 | 30 | 28 |

| Model IV | 11 | 5 | 9 | 8 | 1 | 19 | 2 | 4 | 17 | 24 | 21 | 15 | 23 | 6 | 20 | 7 | 14 | 13 | 12 | 3 | 25 | 26 | 18 | 16 | 10 | 22 | 29 | 27 | 30 | 28 |

| Model I | Model II | Model III | Model IV | |

|---|---|---|---|---|

| Model I | 0 | 0 | 23 | 23 |

| Model II | 0 | 0 | 23 | 23 |

| Model III | 23 | 23 | 0 | 8 |

| Model IV | 23 | 23 | 8 | 0 |

Appendix A Appendix: Proofs

Proof of Theorem 2.1:

Proof. Let

| (27) |

where is given by (3). Since is a positive unbounded quadratic a minimizer must exist. Now, if is not connected then we may decompose it as where for each the graph is a connected subgraph of . It follows that

where is the score vector and is the sum of squares associated with the vertices in and . Let be a vector of ones of the same dimensions as . Let be a minimizer of (27). Define

Clearly satisfies and thus it follows that where . Hence for every satisfying we find that solves (27). Thus the LSE is not unique if the graph is not connected.

Hence, from this point on we will assume that is connected. The proof will be completed once we explicitly find and show that it is unique. By Lemma 2 in Osei and Davidov (2022) the function can be expressed as a quadratic form in , i.e.,

where is some function of the data but not of . The Lagrangian associated with (27) is

It follows that

where because . Therefore, setting we obtain the system

| (28) | |||||

| (29) |

It is easy to see that and ; in addition by assumption. Thus by premultiplying (28) by we find that . Thus we get

| (30) |

where is the Moore–Penrose inverse of and is arbitrary. The rows of , like those of , sum to (Bapat, 2010). Thus . The matrix is a projection onto Since is connected, and , therefore equals for some where if and only if Thus if we premultiply (30) by we have

so which we substitute back in (30) to obtain

The uniqueness of follows from the uniqueness of This concludes the proof.

Proof of Corollary 2.1:

Proof. Note that

is independent of . Thus as required.

Proof of Proposition 2.1:

Proof. By assumption . Let where and let . Clearly is a comparison graph. Let and be the Laplacians of , and respectively. Clearly is a nonnegative definite matrix so . Furthermore the uniqueness of the LSEs implies that and are connected graphs and therefore the matrices and have rank . Therefore using Theorem 3.1 in Milliken and Akdeniz (1977) we get . This proves the first claim. The second claim follows immediately by using the first order approximation for the variance of (see for example, page 122, in Serfling 2009).

Proof of Theorem 3.1:

Proof. Suppose that Condition 3.1 holds. If so the LSE is given by and its variance is given by . The Laplacian is symmetric and non–negative definite; its spectral decomposition is where is an orthonormal matrix and with where are the eigenvalues of . Since is connected and Furthermore where .

Let be the tree satisfying Condition 3.1. Let be the subgraph of for which for all edges in where . Further define so by construction . Let and be the Laplacians of and respectively. It is easy to see that

By Weyl’s inequality (Theorem 4.3.1, Horn and Johnson, 2007) we have

where is the Laplacian of a tree with muliplicity one on the vertices of and . Moreover, a spanning tree is a connected graph so . It follows that as . Furthermore and consequently as for all . Now

where are the orthonormal columns of . The orthonormality implies that the absolute value of all elements of must be bounded by . Consequently the display above shows that , the zero matrix. Therefore . We have already shown that and it now follows that is consistent, i.e., as required. Next for part (ii), for each we have

where is the element of the matrix . Let

where is the adjacent matrix of . The matrix is called the normalized Laplacian and from Theorem 2 in Bozzo (2013),

The eigenvalues of are bounded (Li et al. 2014) and therefore the entries of are also bounded. A bit of algebra shows that the diagonal entry of is

and therefore

as required.

Next, suppose that Condition 3.1 does not hold. If so

| (31) |

where the maximization is over all spanning trees of . Let be the subgraph of for which for all edges in . Define , and as before. Now is either a connected or disconnected graph. If is disconnected then by Weyl’s inequality we have

Since is disconnected so . Further note that for some finite constant and thus is finite even if . This shows that does not converge to and consequently . If, however, is connected, then using the same procedure we can extract a tree from and denote the remainder by . This procedure can be repeated until the remainder graph is disconnected. Since is finite, must be finite. Thus applying Weyl’s inequality times find that is finite as . Consequently as . This completes the proof.

Proof of Theorem 3.2:

The proof of Theorem 3.2 requires additional notation and preliminary lemma’s. In what follows denote by and the submatrices arising from by deleting the row and column and the and rows and and columns, respectively. The entry of is denoted by . The determinant of matrix is denoted by . The diagonal matrix with main diagonal is denoted by . It will be convenient to label the rows and columns of this and every other matrix having rows and/or columns using double labels which are ordered lexicographically as are the ’s in . Let be the vector of sample means , where If for some pair then set . Let be the contrast matrix each row of which contains a unity, a negative unity and zeros, such that

Then we have the following.

Lemma A.1

(a) ; (b) ; (c) ; (d) .

Proof. (a), (b) and (c) are easy to see. For (d) use (b) and the fact that to get .

Lemma A.2

If the graph is connected we have

| (32) |

Proof. Chebotarev and Shamis (1998) showed that if the graph is connected then where is the matrix of ones. By doing the required algebraic manipulations it can be verified that the entry of this matrix is as in (32).

Lemma A.3

Let , . Then, for any we have

| (33) |

Proof. When , (33) coincides to the equation given in Bapat (2013, Lemma 2). The proof for the cases and follows among the same lines.

Lemma A.4

Let , . The entry of matrix is while that of is .

Proof. It is easy to verify that the entry of equals . Note that

which by using (33) with becomes

On the other hand,

Hence,

Similarly, we get . Next, write

and apply once more (33) with to re-express it as

Since

we get that

which is equivalent to the stated result. The result for is now straihtforward.

Let be the set of all spanning trees and the set of spanning trees containing edge . For any let be its weight. Then we have the following:

Lemma A.5

All entries of have absolute value bounded by one.

Proof. By the all minors matrix tree theorem (Chen, 1976, Chaiken, 1982) we get that and , where is described in (Chaiken 1982) and is some sign. Thus,

.

Assume now that and Condition 3.1 holds. Note that there may exist ’s which don’t go to infinity and even if they do they may go to infinity at different rates. For a spanning tree let be the rate at which goes to infinity with if . Let be the maximum rate over . Let and be the set of edges which belong to some . Let , where if and zero otherwise. Set finally and let be its Moore-Penrose inverse. Note that is also the Laplacian of a multigraph. Then, we have the following.

Lemma A.6

.

Proof. By Lemma A.4, the entries of and are and , respectively. By applying once more the all minors matrix tree theorem we get and by construction. Since for we may write and . Thus,

which converges to zero since the numerator is and the denominator .

Proof of Theorem 3.2:

Proof. Let . By applying Lemma A.1(c) with and in the place of and we conclude that is consistent for if and only if is consistent for .

By the strong law of large numbers, if (at whatever rate) then almost surely. Therefore, we may write where or according to if or not.

Suppose first that Condition 3.1 is satisfied. By applying Lemma A.1 with instead of we get . However, if then the th column of contains only zeros. Since for all we conclude that . Thus,

since the first term and second terms go almost surely to : the first by Lemma A.6 and the almost sure boundedness of while the second by the strong law and the fact that is bounded as shown in Lemma A.5.

Suppose finally that Condition 3.1 does not hold. In this case the set can be partitioned into two subsets , so that the limiting vector contains the differences only if both belong to or to . This means that no difference with , can be consistently estimated and thus can not be consistent.

Proof of Lemma 3.1:

Proof. Let be the comparison graph obtained from by retaining the edges only if . Let and be their corresponding Laplacians. Condition 3.2 implies that there is a spanning tree in whose edges represent paired comparisons and consequently is a connected graph. Let and where . By construction the relations and hold as .

Let be the cardinality of and let be the matrix whose rows correspond to the items and column correspond to the edges in arranged lexicographically. If the edge in joins the vertices and then

where is the element of . Following the arguments in the proof of Lemma 2.2 in Bapat (2006, p. 12), it is easy to see that . Further and consequently as claimed. Now, the relation follows immediately by applying Theorem 4.2 in Rakoĉević (1997).

Remark A.2

The matrix appearing in the proof of Lemma 3.1 can be obtained from the incidence matrix (Bapat 2010) of the multigraph by dividing by and taking the limit.

Proof of Theorem 3.3:

Proof. Under Condition 3.2, using Lemma 3.1 we have which implies that or equivalently that Let be a random vector of dimension whose components , are arranged by their lexicographical order. Clearly if and then by the one dimensional CLT

| (34) |

where If then the LHS of converges to in probability, in which case and (34) remains valid. Since the components of are independent it follows that as

where is a diagonal matrix with elements arranged by their lexicographical order. Since and there exist a matrix where such that . It follows that

which, by matching moments, can be rewritten as

Premultiplying the above by and using Lemma 3.1 we find that

Proof of Theorem 3.4:

Proof. Without loss of generality assume that whenever . Note that if and only if for some the event occurs. It follows that

Under the stated conditions for each and therefore where by assumption. Consequently,

as . Since is finite we have establishing the first claim.

Next observe that

where is the row of the matrix . A bit of algebra shows that

where the sum is taken over pairs for which . Observe that

where and . By construction since the expectation of is . Note that the collection of RVs where are independent. Using the fact that weighted sums of independent subgaussian RVs are also subgaussian and the form of the moment generating functions of subgaussian RVs we find that

Note that under Condition 3.2, using Lemma 3.1 for all pairs we have that and

where is the element of the matrix . If then

This can be rewritten as

for some constants and . The result follows by taking and .

Proof of Proposition 4.1

Proof. If for then it is easy to see that

Thus . Next let then there exists such that

where is the column of . Therefore for .

Proof of Theorem 4.1:

Proof. The Lagrangian associated with (13) is

Its derivatives with respect to and equated to zero yield

| (35) | |||

| (36) |

Premultiplying (35) by , and recalling that we find that . Therefore a solution to equation (35) is given by

| (37) |

where is arbitrary. If the graph is connected and Condition 4.1 holds, then . Consequently and spans . Thus for some where if and only if . Premultiplying (37) by and using (36) we obtain

Therefore . Thus the unique solution to (35) and (36) is given by

| (38) |

The uniqueness of the LSE follows from the uniqueness of the Moore Penrose inverse.

Conversely, let . Then, we have and consequently . Suppose where . Then can be expressed as a linear combination of orthogonal vectors in . Therefore premultiplying (37) by and using (36), we get a linear equation in variables, so the associated solution is not unique. Consequently the estimator given by (37) is not unique. For example if , then , where and . Therefore premultiplying (37) by and using (36), we get

This is a linear equation in two variables, so the associated solution is not unique. This proves the first part.

Now, substituting into (38) we find that . An explicit solution is facilitated by noting that we can rewrite

where and

Note that is the projection of onto the orthogonal complement of , and consequently in terms of the normal equations are

| (39) |

Here is a full column rank matrix and is an idempotent matrix. Therefore by Proposition 5.4 in Puntanen et al. (2007, p. 132) is a full rank matrix. It now follows from (39) that

Substituting the value of in (39) and solving for , we obtain

Proof of Lemma 4.1:

Proof. Let and note that . Consequently for every there exists a such that . Therefore, the second smallest eigenvalue of diverges if and only if the second smallest eigenvalue of diverges. Next, the second smallest eigenvalue of diverges if the second smallest eigenvalue of diverges and the smallest eigenvalue of diverges. Condition 3.1 guarantees that the second smallest eigenvalue of diverges, cf., Theorem 3.1.

Let and . Then, . If , then and

Using Pythagoras theorem, . Next, for all amounts to saying that

| (40) |

Thus, diverges if diverges. Note that diverges for any if and only if the smallest eigenvalue of diverges. Similarly, the minimum eigenvalue of diverging is equivalent to diverging for any .

Proof of Lemma 4.2