Covariance Function Estimation for High-Dimensional Functional Time Series with Dual Factor Structures

Abstract

We propose a flexible dual functional factor model for modelling high-dimensional functional time series. In this model, a high-dimensional fully functional factor parametrisation is imposed on the observed functional processes, whereas a low-dimensional version (via series approximation) is assumed for the latent functional factors. We extend the classic principal component analysis technique for the estimation of a low-rank structure to the estimation of a large covariance matrix of random functions that satisfies a notion of (approximate) functional “low-rank plus sparse” structure; and generalise the matrix shrinkage method to functional shrinkage in order to estimate the sparse structure of functional idiosyncratic components. Under appropriate regularity conditions, we derive the large sample theory of the developed estimators, including the consistency of the estimated factors and functional factor loadings and the convergence rates of the estimated matrices of covariance functions measured by various (functional) matrix norms. Consistent selection of the number of factors and a data-driven rule to choose the shrinkage parameter are discussed. Simulation and empirical studies are provided to demonstrate the finite-sample performance of the developed model and estimation methodology.

Keywords: Covariance operator, functional factor model, functional time series, generalised shrinkage, high dimensionality, PCA, sparsity.

1 Introduction

A fundamental problem of increasing interest in modelling time series of random functions is to estimate their second-order characteristics, such as the covariance, auto-covariance and spectral density operators (e.g., Bosq, 2000; Hörmann and Kokoszka, 2010; Horváth and Kokoszka, 2012). Understanding these characteristics are not only important for understanding the randomness of the corresponding processes themselves, but also crucial to subsequent down-stream applications such as functional principal component analysis (e.g., Hörmann and Kokoszka, 2010; Horváth and Kokoszka, 2012; Panaretos and Tavakoli, 2013; Hörmann, Kidziński and Hallin, 2015). While most of the existing literature focuses on a fixed number of functional time series, it is increasingly common to collect a large number of them in a diverse range of fields. For example, in climatology, temperature curves are routinely recorded in hundreds of weather stations, while in finance, stock return curves are typically available for thousands of stocks.

The main aim of this paper is to estimate the covariance structure of functional time series, when the dimensionality of the data (the number of functional time series) is comparable to or greater than the sample size (the length of these time series). To overcome the curse of dimensionality arising from this setup, a common practice is to make an approximate sparsity assumption on this structure. Consequently, regularisation methods such as thresholding or adaptive thresholding can be applied (e.g., Fang, Guo and Qiao, 2023). However, the sparsity restriction only works when these functional time series are at most weakly correlated, ruling out many interesting cases where they can be highly correlated. In practice, it is widely recognised that multivariate functional time series are often influenced by common functions over the temporal dimension, leading to strong cross-sectional dependence. For example, the rainfall curves collected in many stations may be affected by the common weather pattern in the region (Delaigle, Hall and Pham, 2019), and the intraday return curves are often driven by latent market and industry factors.

To accommodate cross-sectional dependence, an idea is to use factor models in the context of functional time series. Indeed, the approximate factor model has been extensively studied in the literature for panel time series (Chamberlain and Rothschild, 1983; Bai and Ng, 2002; Stock and Watson, 2002; Fan, Liao and Mincheva, 2013). In recent years, there have been some attempts to extend this model to the functional time series setting, broadly classified into two directions. The first category can be loosely referred to as functional factor models for fixed-dimensional problems. Specifically, Hays, Shen and Huang (2012) and Kokoszka, Miao and Zhang (2015) consider a factor model with real-valued factor loadings and functional factors, whereas Kokoszka et al. (2018) and Martínez-Hernández, Gonzalo and González-Farías (2022) propose a factor model with real-valued factors and functional loadings. These functional factor models are essentially low-dimensional, because the developed methodology is not applicable to large-scale functional time series when the dimension is comparable to the sample size. The second direction is the high-dimensional functional factor model. Gao, Shang and Yang (2019) first apply the classic functional principal component analysis to each functional time series before modelling the component scores via a factor model. However, this method may lead to information loss in the dimension reduction stage, which subsequently may result in inaccurate factor number estimation. To address these, two types of functional factor models with different construction of common components have been proposed in the recent literature. Tavakoli, Nisol and Hallin (2023a, b) introduce a high-dimensional functional factor model with functional loadings and real-valued factors, whereas Guo, Qiao and Wang (2021) propose a different version with real-valued loadings and functional factors.

In this paper, we propose a novel dual functional factor model with functional loadings and functional latent factors, in which the latent factors are modelled through series approximation. Towards this, we relax some restrictive assumptions imposed on existing functional factor models studied in the aforementioned literature. The proposed model includes those in Tavakoli, Nisol and Hallin (2023a, b) as special cases. We allow the covariance functions for the idiosyncratic components to be approximately sparse in a functional sense. Thus, the covariance function (or operator) of the high-dimensional functional process under our setup admits an approximate “low-rank plus sparse” functional covariance structure (e.g., Fan, Liao and Mincheva, 2013), extending the functional sparsity condition assumed in Fang, Guo and Qiao (2023) to allow latent factors.

The main estimation methodology can be seen as a functional analog of the POET method introduced by Fan, Liao and Mincheva (2013). For the factor loadings and common factors, we propose the use of a functional version of principal component analysis (PCA). For the covariance function of the idiosyncratic components, we apply a functional generalised shrinkage to a preliminary estimate of it. Under regularity conditions, we derive the mean squared convergence of the estimated factors, uniform convergence of the estimated functional factor loadings, and convergence of the estimated functional covariance matrices (measured by different matrix norms). These convergence rates depend on the dimension, the length of functional time series, the number of factors, and the error of sieve functional approximation. The Monte-Carlo simulation study shows that the developed methodology has reliable finite-sample performance. An empirical application to the cumulative intraday returns (CIDR) curves of the S&P 500 index data confirms the usefulness of the model and the accuracy of the suggested estimation approach.

After completing a preliminary draft of the paper, we found a recent working paper by Li, Qiao and Wang (2023) who consider a similar problem. It is worth comparing the two papers before concluding the introductory section. First, Li, Qiao and Wang (2023) estimate the large functional covariance matrix based on the high-dimensional functional factor models of Tavakoli, Nisol and Hallin (2023a, b) and Guo, Qiao and Wang (2021), whereas our estimation is built on the dual functional factor model structure. More discussion and comparison between the models are provided in Section 2 below. Second, we allow the number of factors (via the functional sieve approximation) to be divergent and the functional observations from different subjects to be defined on different domains, relaxing some restrictions implicitly imposed in Li, Qiao and Wang (2023). Third, we derive general convergence theory under the flexible model framework and the obtained convergence rates are comparable to those in Li, Qiao and Wang (2023) where the factor number is fixed and the sieve approximation error is zero. Finally, we use a different criterion to consistently estimate the factor number and choose the tuning parameter in functional shrinkage. In particular, we propose a modified cross-validation to select the shrinkage parameter, taking into account the temporal dependence of the functional data over a long time span.

The rest of the paper is organised as follows. Section 2 introduces the dual functional factor model framework. Section 3 describes the main estimation methodology and Section 4 presents the large sample theory for the developed estimators. Section 5 discusses practical issues for implementation and reports the numerical studies. Section 6 concludes the paper. Proofs of the main theorems are given in Appendix A and proofs of some technical lemmas are available in Appendix B. Appendix C briefly reviews the -mixing dependence and the concentration inequality. Throughout the paper, for a separable Hilbert space defined as a set of real measurable functions on a compact set such that , the inner product of is , and the norm of is . Denote by the Cartesian product of and . Let and respectively denote the operator and Hilbert-Schmidt norms for continuous linear operators. Denote the Euclidean norm of a vector by , and the operator, Frobenius and maximum norms of a matrix by , and , respectively. For (the -fold Cartesian product of ), we define . Let , and denote that , and , respectively. Write “with probability approaching one” as “w.p.a.1” for brevity.

2 Dual functional factor models

Let , , with , where is a Hilbert space defined as a set of measurable and square-integrable functions on a bounded set . Throughout the paper, we use to denote the subject index and to denote the time index. We propose the following functional factor model:

| (2.1) |

where , is a bounded set which may be different from , is defined similarly to but replacing by , is a continuous linear operator from to , and . Neither the factor loading operator nor functional factor is observable. The number is unknown but assumed to be finite. Model (2.1) is a natural extension of the conventional factor model to a panel of functional time series. It follows from (2.1) that each functional observation is decomposed into the functional common and idiosyncratic components: and . Write , , and

an matrix of continuous linear operators from to . Then model (2.1) can be written in the following vector/matrix form:

| (2.2) |

To facilitate comparison with the functional factor models proposed in the recent literature, we next consider as a linear integral operator with kernel , i,e.,

Model (2.1) can be re-written as

| (2.3) |

Tavakoli, Nisol and Hallin (2023a) introduce the following model:

| (2.4) |

where is the functional factor loading and is a vector of real-valued factors. It is easy to see that model (2.4) is a special case of (2.3). Letting the matrix of operators in (2.2) be replaced by a matrix of real-valued factor loadings, we obtain the model in Guo, Qiao and Wang (2021):

| (2.5) |

where is the real-valued factor loading and is the functional factor. The factor numbers in (2.3) and in (2.4) are assumed to be fixed positive integers. As in Happ and Greven (2018) and Tavakoli, Nisol and Hallin (2023a, b), we allow the functional observations , , and the latent factors , , to be defined on different domains, i.e., and may vary over and . For instance, the collected high-dimensional functional time series may be a combination of time series with values in spaces with different dimensions (for different subjects). In contrast, Guo, Qiao and Wang (2021) implicitly assume that and are defined on the same domain.

For the model in (2.1)–(2.3), we further impose a low-dimensional functional factor condition on the latent factor by assuming the following series approximation:

| (2.6) |

where is a -dimensional vector of basis functions, is a -dimensional vector of stationary random variables, is the sieve approximation error satisfying Assumption 1(iii), and is a positive integer which may slowly diverge to infinity. Note that the set of basis functions in (2.6) is allowed to vary over . Model (2.6) extends the models studied in Kokoszka et al. (2018) and Martínez-Hernández, Gonzalo and González-Farías (2022) for univariate functional time series to multivariate ones.

Letting

and

the dual functional factor model structure combining (2.3) and (2.6) leads to

| (2.7) | |||||

where and . By Assumption 1(ii)–(iii) in Section 4 below and the Cauchy-Schwarz inequality, we may show that , the common component driven by the series approximation error, converges to zero w.p.a.1. If , model (2.7) reduces to (2.4) as in Tavakoli, Nisol and Hallin (2023a, b) but with a possibly diverging number of factors. Our main interest is to estimate the large contemporaneous functional covariance structure under the general functional factor model framework (2.7).

3 Estimation methodology

Without loss of generality, assume that and all have zero mean. Define , where is the covariance operator between and with the corresponding kernel . Assuming and are uncorrelated, we may decompose as

| (3.1) |

where is the covariance operator between the functional common components and , and is the covariance operator between the functional idiosyncratic components and 111Throughout the paper, we use and to denote the operators, and and to denote their respective kernels.. Let and be matrices of covariance functions (or kernels) corresponding to , and , respectively.

It follows from (2.7) that can be approximated by

| (3.2) |

where is a covariance matrix of latent factors and is defined as in (2.7). Hence can be approximated by , a low-rank functional covariance matrix. On the other hand, since the functional idiosyncratic components are weakly cross-sectionally correlated, it is sensible to impose a functional version of the approximate sparsity restriction on , i.e.,

| (3.3) |

where denotes a positive number which depends on , and “” denotes that is a positive semi-definite matrix of covariance functions, i.e.,

Combining the above arguments, we obtain the functional low-rank plus sparse structure for

| (3.4) |

which may serve as a proxy of . Under some mild conditions such as Assumption 1(iii), we may show converges to (under the matrix maximum norm), using Lemma B.3. With (3.4), we may extend the POET method in Fan, Liao and Mincheva (2013) to estimate in the high-dimensional functional data setting.

Due to the general functional structure for the common components in (2.1)–(2.3), it is practically infeasible to directly estimate the factor loading operators and functional factors in the latent structure. Instead, motivated by (3.2)–(3.4), we may make use of the low-dimensional functional factor model (2.6) and estimate and (subject to rotation) in the latent which approximates . The latter can be done by extending the PCA technique (e.g., Bai and Ng, 2002; Stock and Watson, 2002) to a large panel of functional observations. Assume the number of real-value factors in (2.7) is known for the time being. We will discuss on how to determine this number in Section 5. We estimate the factor loading functions and real-valued factors by minimising the following least squares objective function:

where denotes the norm of elements in , is a -dimensional vector of functions and is a -dimensional vector of numbers. Minimisation of the above least squares objective function can be achieved via the eigenanalysis of

| (3.5) |

Consider the following identification condition in the PCA algorithm:

| (3.6) |

which are similar to those in Bai and Ng (2002) and Fan, Liao and Mincheva (2013). With (3.6), we let as a matrix consisting of the eigenvectors (multiplied by root-) corresponding to the largest eigenvalues of defined in (3.5). The factor loading functions are estimated as

via the least squares, using the normalisation restriction by (3.6). Consequently, the low-rank matrix of covariance functions is estimated by

| (3.7) |

We next turn to the estimation of . Letting be the approximation of , it is natural to estimate by

However, this matrix of conventional sample covariance functions often performs poorly when the number is comparable to or larger than . To address this problem, we adopt the generalised shrinkage and estimate by

| (3.8) |

where is a functional thresholding operator satisfying (i) for any covariance function (or operator) ; (ii) if ; and (iii) , where is a user-specified tuning parameter controlling the level of shrinkage. A modified cross-validation method will be given in Section 5 to determine , taking into account the temporal dependence of high-dimensional functional data. We may further replace the universal thresholding by an adaptive functional thresholding as suggested by Fang, Guo and Qiao (2023) and Li, Qiao and Wang (2023), in which case the theory to be developed in Section 4 remains valid.

Combining and , we finally obtain the estimate of or :

| (3.9) |

4 Large sample theory

In this section, we first give some regularity conditions and then present the convergence properties for the estimates developed in Section 3.

4.1 Regularity conditions

Assumption 1.

(i) Let be a stationary sequence of -dimensional random vectors with mean zero. There exists a positive definite matrix such that

(ii) There exists a positive definite matrix such that

The factor loading operator satisfies that , where is a positive constant.

(iii) The sieve approximation error in (2.6) is stationary (over ), satisfying that , where as .

Assumption 2.

(i) Let be a stationary sequence of zero-mean -valued random elements, independent of and . There exists a positive constant such that

and

(ii) For , any deterministic function defined on , we have

Assumption 3.

(ii) For any and , the joint processes and are stationary and -mixing with , where , and denotes the -th element of .

(iii) There exist positive constants and such that

Remark 1.

Assumption 1 imposes some fundamental conditions on and , which are similar to the assumptions in Bai and Ng (2002), Fan, Liao and Mincheva (2013) and Tavakoli, Nisol and Hallin (2023b). The high-level convergence condition in Assumption 1(i) is essentially a weak law of large numbers for (with diverging size). Assumption 1(ii) indicates that the -dimensional real-valued factors are pervasive. We conjecture that the methodology and theory (with modified convergence rates) may remain valid when some factors are weak. The uniform boundedness condition on the factor loading operators is not uncommon in the literature. For instance, the factor loading vectors are often assumed to be bounded in classic factor models (e.g., Assumption 4 in Fan, Liao and Mincheva, 2013). Assumption 1(iii) implies that the sieve approximation error converges to zero at the -rate, which, together with Assumption 1(ii), indicates that in (2.7) also converges at the -rate.

Assumption 2 contains some high-level moment conditions on the functional idiosyncratic components , indicating that are allowed to be weakly correlated over and . They are similar to the conditions used by Bai and Ng (2002) and Fan, Liao and Mincheva (2013) on the real-valued idiosyncratic components. It is straightforward to verify Assumption 2 when are independent over and .

Assumption 3(i) imposes some mild restrictions on , and . The dimension may diverge at a slow polynomial rate of , whereas can be ultra-large, diverging at an exponential rate of . The -mixing dependence on the stationary processes is introduced by Dedecker et al. (2007) and Wintenberger (2010) for real-valued random variables and further extended by Blanchard and Zadorozhnyi (2019) to Banach-valued random elements. Appendix C gives the concept of -mixing dependence. We refer to Blanchard and Zadorozhnyi (2019) for some examples (such as the functional AR(1) process) satisfying the -mixing dependence. Furthermore, with the sub-Gaussian moment condition in Assumption 3(iii), we may adopt Blanchard and Zadorozhnyi (2019)’s concentration inequality to derive uniform convergence properties in the high-dimensional setting. It is worth pointing out that our sub-Gaussian condition on and is weaker than the uniform boundedness restriction in Assumption (H1) of Tavakoli, Nisol and Hallin (2023b). This relaxation is due to the truncation technique used in our mathematical proofs. A similar sub-Gaussian condition is also assumed by Li, Qiao and Wang (2023).

4.2 Convergence properties

We derive the convergence properties in the so-called large panel setting, i.e., when and diverge to infinity jointly. We start with the convergence property for the PCA estimators of factors and functional factor loadings. Let be a diagonal matrix with the diagonal elements being the first largest eigenvalues of (arranged in the decreasing order), and define the following rotation matrix:

where and . We may show that this random rotation matrix is asymptotically invertible, see Lemma B.2.

Proposition 4.1.

(i) For the PCA estimator of , we have the following mean square convergence:

| (4.1) |

where is defined in Assumption 1(iii).

Remark 2.

The mean square convergence rate in (4.1) is slower than the rates obtained by Bai and Ng (2002) and Tavakoli, Nisol and Hallin (2023b). This is due to a diverging number of factors and the existence of sieve approximation error in (2.6). Similarly, the uniform convergence rate in (4.2) is also slower than some typical convergence rates in the literature. If we additionally assume that is a fixed positive integer and , the rates in (4.1) and (4.2) can be simplified to

respectively, and the involved rates and may disappear when . It is worth pointing out that the -mixing dependence restriction is not required to prove Proposition 4.1(i).

The following theorem gives the convergence rates for the estimated covariance functions for the functional idiosyncratic components.

Theorem 4.2.

Remark 3.

The uniform convergence results in (4.3) and (4.4) can be seen as a natural functional extension of the large covariance matrix estimation theory in the matrix maximum and norms, respectively (e.g. Bickel and Levina, 2008; Fan, Liao and Mincheva, 2013). The uniform convergence rates are comparable to those rates derived in the literature (e.g., Remark 3(b) in Fan, Liao and Mincheva, 2013). As discussed in Remark 2, the divergence rate of and the existence of series approximation error slow down our uniform convergence rates. Note that may disappear if , in which case the large dimension affects the convergence rate in (4.4) via and . Furthermore, if is fixed, and , we may show that can be simplified to

and the uniform convergence rate would be similar to the rates in Theorem 1 of Fang, Guo and Qiao (2023) and Theorem 4 of Li, Qiao and Wang (2023) when is large.

The following theorem states the uniform convergence property for defined in (3.9).

Theorem 4.3.

Remark 4.

Theorem 4.3 shows that uniformly converges to either or in the Hilbert-Schmidt norm. This is due to the fact that

| (4.7) |

or

| (4.8) |

where is the covariance function between and whereas is the covariance function between and . The uniform approximation in (4.7) and (4.8) can be verified using Assumption 1(iii) and Lemma B.3. When is fixed, the uniform convergence rates in (4.5) and (4.6) would be the same as that in (4.3).

Due to the low-rank plus sparse functional matrix structure for and , we cannot derive the uniform convergence property in the functional version of matrix norm as in (4.4). To address this problem, Fan, Liao and Mincheva (2013) recommends measuring the relative error of large low-rank plus sparse covariance matrix estimation for a high-dimensional random vector. However, it seems difficult to directly extend their relative error measurement to the setting of high-dimensional functional data due to the following reasons. First, the inverse of the large covariance matrix is often involved in defining the relative error measurement, but it seems difficult to compute the inverse of the large matrix of covariance operators . Second, although the uniform approximation properties (4.7) and (4.8) hold in the functional version of the matrix maximum norm, it is non-trivial to derive similar approximation properties under the relative error measurement. Although it is difficult to provide a theoretical justification via the relative error measurement, in the simulation study we will report some results on two types of its discrete approximation, illustrating the finite-sample performance of .

5 Numerical studies

In this section, we first introduce an easy-to-implement criterion to consistently estimate the factor number and discuss selection of the tuning parameter in the functional shrinkage. Then, we present Monte-Carlo simulation and empirical studies.

5.1 Practical issues in the estimation procedure

The functional PCA algorithm proposed in Section 3 requires accurate estimation of , the dimension of latent . There have been extensive studies on the factor number selection in the context of high-dimensional real-valued time series. For example, Bai and Ng (2002) introduces some information criteria to consistently estimate the factor number, and Lam and Yao (2012) and Ahn and Horenstein (2013) propose a simple ratio criterion by comparing ratios of the estimated eigenvalues. The factor number is often assumed to be fixed and does not change with the size of data in the aforementioned literature. In this paper, we introduce a modified information criterion to consistently estimate the factor number , which can diverge to infinity slowly222Li, Li and Shi (2017) consider a similar scenario in the factor number selection for real-valued panel time series.. Let be the th largest eigenvalue of with defined in (3.5), and define

| (5.1) |

where in the penalty parameter and is a user-specified positive integer. A similar criterion is also adopted by Aït-Sahalia and Xiu (2017) to determine the number of high-frequency latent factors. The selection criterion in (5.1) amends Bai and Ng (2002)’s information criterion which replaces by summation of over and does not require “-1” adjustment. It is worth pointing out that the amended information criterion (5.1) is easier to implement and its theoretical justification is straightforward. Proposition 5.1 below derives its consistency property.

Proposition 5.1.

The shrinkage estimation of is often sensitive to the choice of the tuning parameter . Bickel and Levina (2008) recommend the cross-validation method to select when the observations are independent and real-valued, see also Fang, Guo and Qiao (2023) for the extension to functional-valued observations. However, since the functional time series observations are serially correlated over time, satisfying the functional factor model structure, the cross-validation method may no longer work well in our setting. We modify the traditional cross-validation as follows.

-

Step 1: Let with . Use a rolling window of size and divide the estimated functional idiosyncratic components within each window into two sub-samples of sizes and by leaving out K observations in-between, where denotes the floor function.

-

Step 2: For the -th rolling window, we compute the shrinkage estimate as in (3.8) using the first sub-sample, where we make its dependence on explicitly, and the conventional estimate (without shrinkage) as in (3.7) using the second sub-sample, with . Determine the shrinkage parameter by minimising

(5.3)

The above selection criterion is introduced by Chen, Li and Linton (2019) for large covariance matrix estimation of weakly dependent real-valued time series. The reason for leaving out observations between the two subsamples in each rolling window is to make these two subsamples have negligible correlation. In practice, for weakly dependent functional time series, we may set .

5.2 Simulation study

We start with the description of the data generating process. For simplicity, let in the fully functional factor model (2.1) or (2.2). The functional factor process is defined by (2.6), i.e.,

where is generated from a Brownian bridge, is a -dimensional vector of Fourier basis functions, follows a VAR model:

with being a coefficient matrix with its element for and being independently generated by a -dimensional standard normal distribution. Each function is generated on a common set of 21 equally-spaced grid points on . The number of real-valued factors, , is set as or . We simulate the factor loadings via

where is independently generated from a standard normal distribution, and is a set of Fourier basis functions.

As in Fang, Guo and Qiao (2023), we simulate the functional idiosyncratic term as

where is the Fourier basis function and with are independently generated from a multivariate Gaussian distribution with mean zero and covariance matrix . Write with being the block, . The functional sparsity pattern on may be characterised by a sparsity structure in . In the simulation study, we define with and

where denotes the binary indicator function.

We apply the developed estimation method to the simulated data and compute the difference between the true and estimated functional covariance matrices over 200 replications. As in Fang, Guo and Qiao (2023), we compute the functional version of and matrix norms for the functional idiosyncratic covariance matrix estimation (see Table LABEL:tab:1), and the matrix maximum norms (see Table LABEL:tab:2), providing the finite-sample justification for Theorem 4.2. These functional , and maximum matrix norms are defined as

We consider four shrinkage functions in the functional shrinkage technique: hard thresholding (Hard), soft thresholding (Soft), SCAD and adaptive lasso (Alasso), and include the sample covariance function estimation (sample) as a benchmark. The tuning parameter involved in the functional shrinkage is selected via the modified cross-validation introduced in Section 5.1. Table LABEL:tab:1 reports the functional - and -norm estimation errors for functional idiosyncratic covariance matrices. Both the - and -norm estimation errors decrease significantly when increases from 100 to 200; the -norm shrinkage estimation errors slightly increase when increases from to 200 but is fixed; whereas the increase of -norm estimation errors is more substantial. The estimation performance is generally stable as increases from 5 to 15. The use of functional shrinkage significantly outperforms the naive sample covariance function without shrinkage. In particular, the adaptive lasso performs best among the four shrinkage functions. Table LABEL:tab:2 further compares the functional max-norm estimation errors between the adaptive lasso333The results are almost the same for the other three shrinkage methods. and sample covariance function. Unlike Table LABEL:tab:1, their estimation performance is very close.

To measure the covariance matrix estimation accuracy of the observed functional observations simulated by the dual functional factor model, due to the existence of spiked eigenvalues, we cannot adopt the functional - and -norm estimation errors both of which are divergent as increases. As discussed in Remark 4, we define the following two relative-error measurements:

whose results are reported in Table LABEL:tab:3. The relative-error measurements increase when increases, but decrease when increases from to . The adoptive lasso again outperforms the other three shrinkage methods, which is consistent with the finding in Table LABEL:tab:1.

We assess the performance of the amended information criterion in Table 4 by reporting percentages of accurately estimating the true number of factors. When and , we achieve perfect accuracy in selecting the factor number; when , the proposed information criterion may occasionally over-estimate the factor number, which has negligible impact on the subsequent covariance function estimation.

| Norm | Shrinkage | |||||||

| 5 | Hard | 6.383 | 6.904 | 7.450 | 4.540 | 4.520 | 4.829 | |

| Soft | 7.045 | 7.582 | 7.991 | 5.754 | 5.976 | 6.500 | ||

| SCAD | 6.932 | 7.518 | 7.954 | 5.248 | 5.517 | 6.154 | ||

| Alasso | 6.442 | 7.010 | 7.511 | 4.657 | 4.688 | 5.079 | ||

| Sample | 26.202 | 52.055 | 104.591 | 19.193 | 37.477 | 75.038 | ||

| Hard | 7.529 | 11.056 | 16.147 | 5.144 | 7.081 | 10.272 | ||

| Soft | 8.344 | 12.366 | 18.126 | 6.277 | 8.991 | 13.246 | ||

| SCAD | 8.134 | 12.171 | 17.970 | 5.598 | 7.993 | 11.939 | ||

| Alasso | 7.401 | 10.823 | 15.789 | 5.126 | 7.012 | 10.153 | ||

| Sample | 19.883 | 39.288 | 78.504 | 14.696 | 28.635 | 56.887 | ||

| 10 | Hard | 6.476 | 6.913 | 7.380 | 4.220 | 4.382 | 4.618 | |

| Soft | 7.118 | 7.598 | 7.970 | 5.571 | 5.993 | 6.309 | ||

| SCAD | 7.003 | 7.527 | 7.932 | 4.997 | 5.503 | 5.908 | ||

| Alasso | 6.584 | 7.057 | 7.492 | 4.423 | 4.710 | 4.983 | ||

| Sample | 25.049 | 49.770 | 99.461 | 18.425 | 35.630 | 70.538 | ||

| Hard | 7.782 | 11.256 | 16.357 | 5.126 | 7.079 | 10.242 | ||

| Soft | 8.632 | 12.680 | 18.488 | 6.366 | 9.190 | 13.489 | ||

| SCAD | 8.413 | 12.461 | 18.322 | 5.641 | 8.144 | 12.098 | ||

| Alasso | 7.743 | 11.195 | 16.221 | 5.173 | 7.131 | 10.274 | ||

| Sample | 19.179 | 37.699 | 75.128 | 14.208 | 27.574 | 54.749 | ||

| 15 | Hard | 6.634 | 7.110 | 7.604 | 4.564 | 4.472 | 4.723 | |

| Soft | 7.221 | 7.691 | 8.021 | 5.834 | 6.058 | 6.379 | ||

| SCAD | 7.084 | 7.621 | 7.981 | 5.300 | 5.582 | 5.979 | ||

| Alasso | 6.777 | 7.250 | 7.669 | 4.767 | 4.824 | 5.103 | ||

| Sample | 24.330 | 48.268 | 96.486 | 18.149 | 35.134 | 69.437 | ||

| Hard | 8.312 | 11.852 | 17.179 | 5.435 | 7.339 | 10.518 | ||

| Soft | 9.112 | 13.197 | 19.120 | 6.659 | 9.476 | 13.832 | ||

| SCAD | 8.871 | 12.964 | 18.917 | 5.947 | 8.431 | 12.430 | ||

| Alasso | 8.356 | 11.878 | 17.151 | 5.492 | 7.443 | 10.659 | ||

| Sample | 18.891 | 36.766 | 73.052 | 14.136 | 27.227 | 53.967 | ||

| Shrinkage | |||||||

| 5 | Alasso | 1.397 | 1.453 | 1.553 | 1.053 | 1.068 | 1.122 |

| Sample | 1.441 | 1.523 | 1.646 | 1.088 | 1.105 | 1.171 | |

| 10 | Alasso | 1.532 | 1.549 | 1.651 | 1.116 | 1.115 | 1.163 |

| Sample | 1.542 | 1.574 | 1.689 | 1.131 | 1.138 | 1.190 | |

| 15 | Alasso | 1.684 | 1.720 | 1.795 | 1.207 | 1.191 | 1.222 |

| Sample | 1.686 | 1.724 | 1.801 | 1.211 | 1.200 | 1.232 | |

| Norm | Shrinkage | |||||||

|---|---|---|---|---|---|---|---|---|

| 5 | RE1 | Hard | 2.162 | 4.283 | 9.218 | 1.685 | 3.453 | 7.390 |

| Soft | 2.464 | 5.386 | 13.373 | 1.880 | 4.199 | 10.306 | ||

| SCAD | 2.202 | 5.070 | 13.055 | 1.232 | 2.728 | 6.836 | ||

| Alasso | 1.517 | 3.111 | 7.361 | 1.247 | 2.475 | 5.311 | ||

| RE2 | Hard | 3.780 | 7.807 | 17.228 | 2.775 | 5.949 | 13.380 | |

| Soft | 5.287 | 11.650 | 29.261 | 3.980 | 9.023 | 22.612 | ||

| SCAD | 4.704 | 10.981 | 28.601 | 2.227 | 5.453 | 14.702 | ||

| Alasso | 2.842 | 6.231 | 15.584 | 1.998 | 4.273 | 10.066 | ||

| 10 | Hard | 1.382 | 3.004 | 6.758 | 0.977 | 2.178 | 4.847 | |

| Soft | 1.574 | 3.715 | 9.401 | 1.180 | 2.921 | 7.433 | ||

| SCAD | 1.394 | 3.445 | 9.105 | 0.704 | 1.747 | 4.729 | ||

| Alasso | 0.983 | 2.112 | 5.192 | 0.688 | 1.454 | 3.335 | ||

| Hard | 2.502 | 5.701 | 13.150 | 1.740 | 4.105 | 9.422 | ||

| Soft | 3.323 | 7.907 | 20.087 | 2.518 | 6.259 | 15.992 | ||

| SCAD | 2.906 | 7.330 | 19.470 | 1.313 | 3.616 | 10.112 | ||

| Alasso | 1.814 | 4.227 | 10.812 | 1.184 | 2.783 | 6.775 | ||

| 15 | Hard | 0.986 | 2.305 | 5.372 | 0.687 | 1.630 | 3.751 | |

| Soft | 1.075 | 2.656 | 6.751 | 0.808 | 2.147 | 5.599 | ||

| SCAD | 0.964 | 2.442 | 6.460 | 0.546 | 1.337 | 3.645 | ||

| Alasso | 0.780 | 1.663 | 4.079 | 0.532 | 1.125 | 2.648 | ||

| Hard | 1.698 | 4.337 | 10.467 | 1.181 | 3.063 | 7.315 | ||

| Soft | 2.184 | 5.639 | 14.469 | 1.684 | 4.611 | 12.062 | ||

| SCAD | 1.893 | 5.158 | 13.845 | 0.939 | 2.715 | 7.730 | ||

| Alasso | 1.318 | 3.228 | 8.391 | 0.848 | 2.111 | 5.336 | ||

| 5 | 99.5% | 100% | 100% | |

| 97.5% | 100% | 100% | ||

| 10 | 100% | 100% | 100% | |

| 98.5% | 100% | 100% | ||

| 15 | 100% | 100% | 100% | |

| 98% | 100% | 100% |

5.3 Empirical application

We apply the developed method to analyse the functional covariance structure of the S&P 500 data containing common stocks traded in the years 2019 and 2020, which are available at the Refinitiv Datascope444https://select.datascope.refinitiv.com/DataScope/. We consider their CIDR curves from 2 January 2019 to 31 December 2020. The S&P 500 index comprises some of the largest companies traded in New York Stock Exchange. After removing the public holidays and half-day trading days (like Christmas Eve), there are trading days in 2019 and in 2020. For each trading day, we consider -minute resolution data between 9:30 and 16:00 Eastern Standard Time, and obtain data points. For asset , let be the intraday 5-minute close price at time on trading day , and construct a sequence of CIDRs (e.g., Rice, Wirjanto and Zhao, 2020):

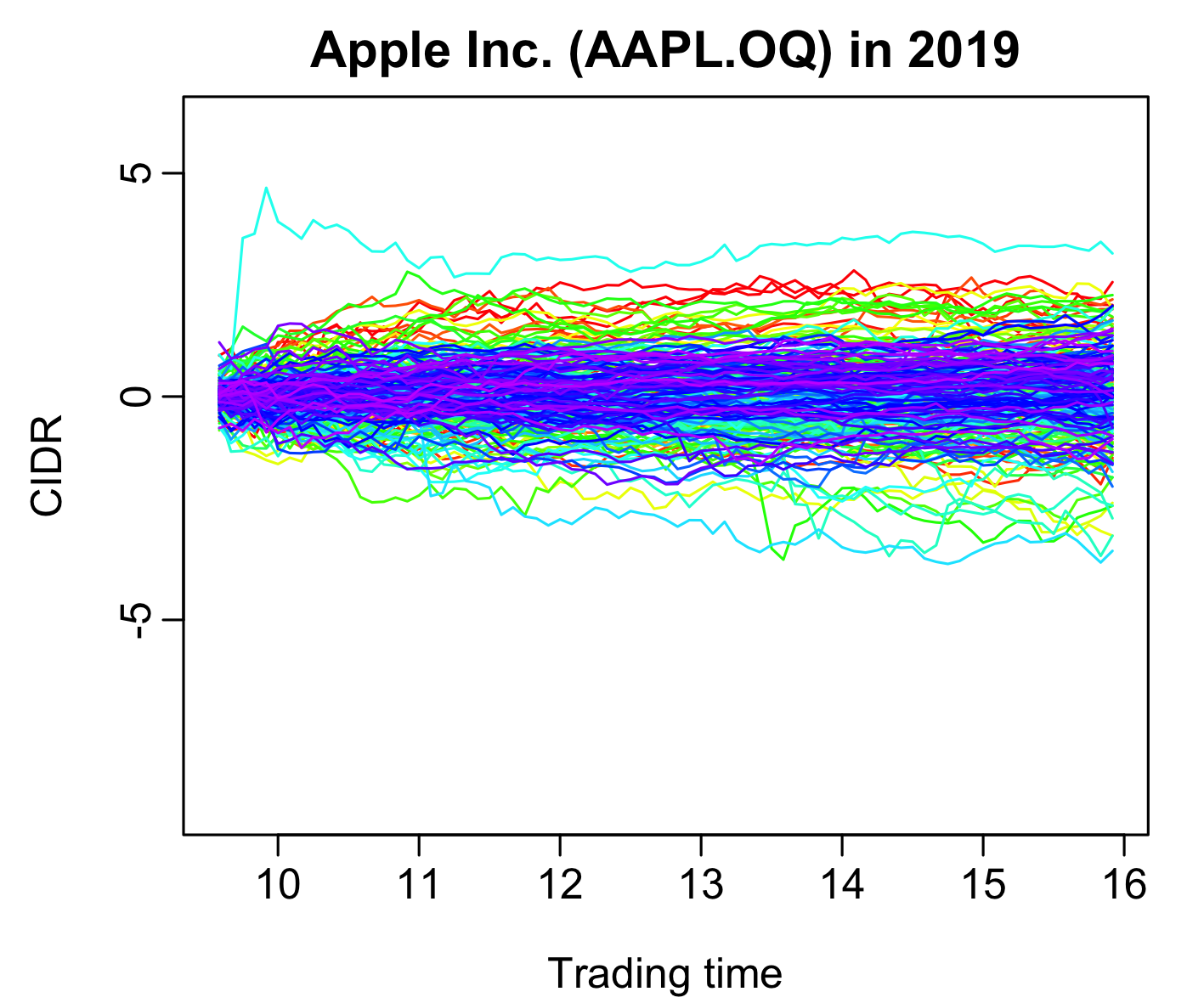

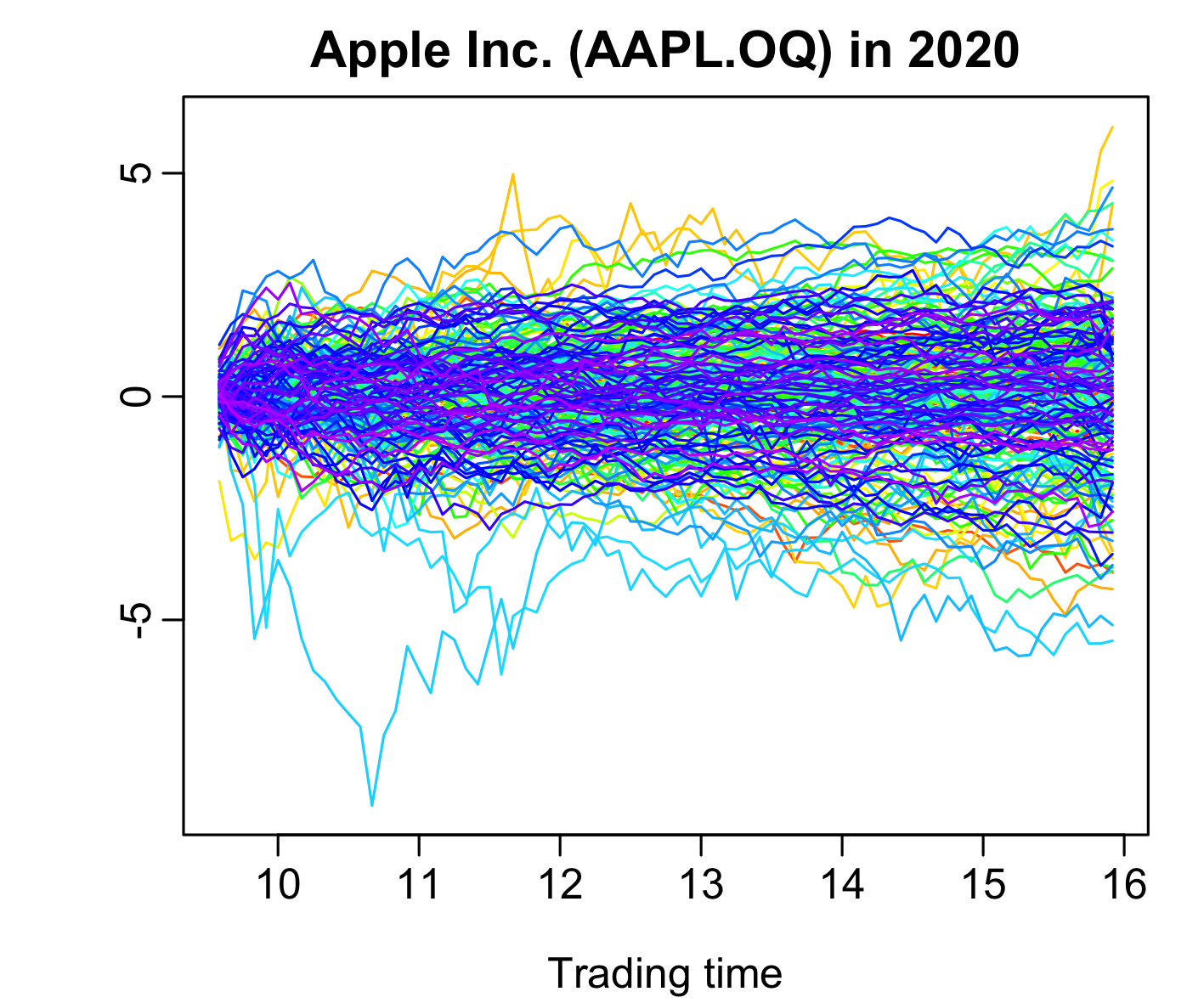

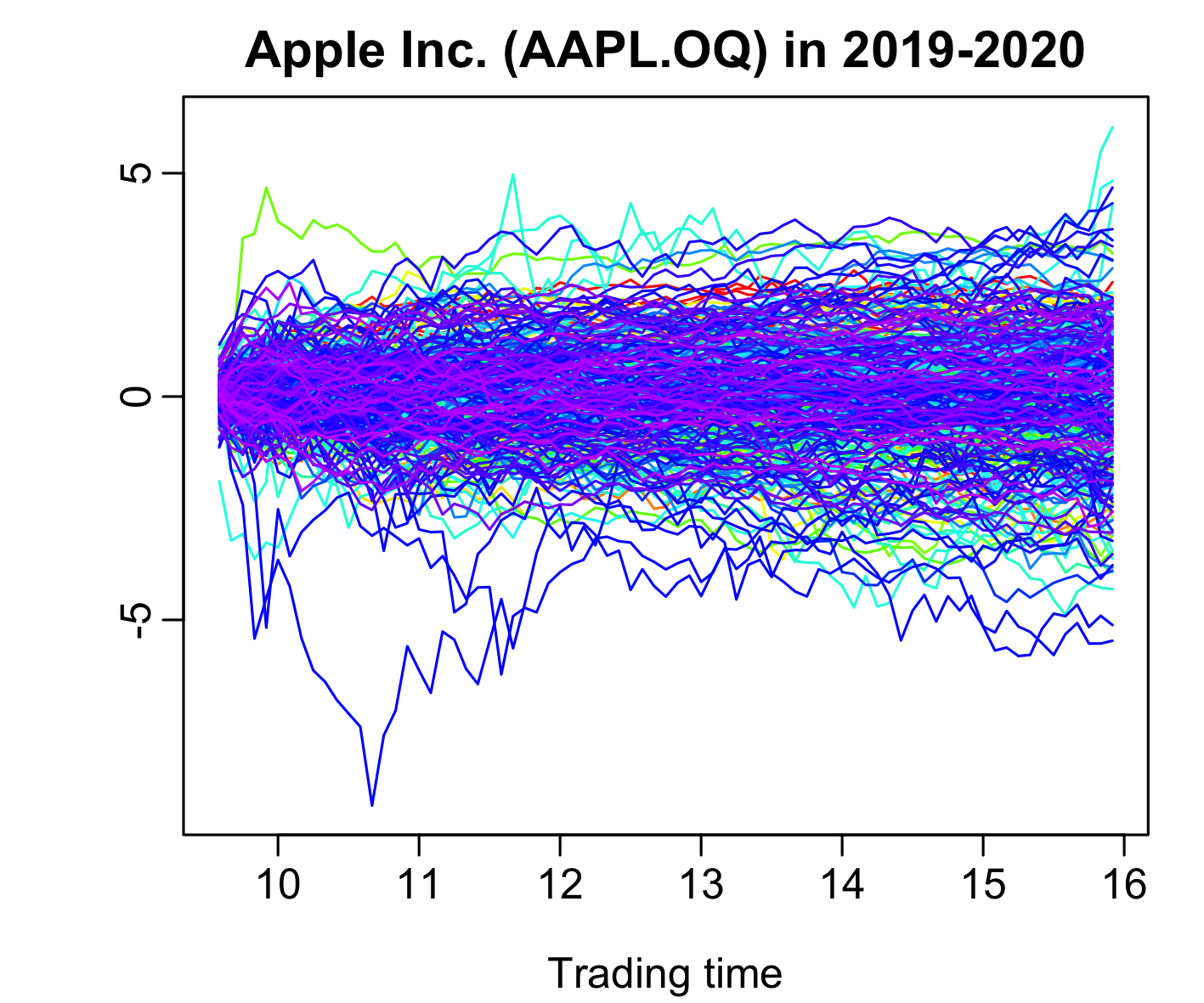

where denotes the natural logarithm, and . The way CIDR is constructed removes the effect of the starting price. The linear interpolation algorithm in Hyndman et al. (2023) is adopted to convert discrete data points into a continuous function. In Figure 1, we display the CIDRs for Apple Inc., one of the most liquid stocks, in 2019 and 2020.

We fit the dual functional factor model to the S&P 500 time series and apply the estimation methodology developed in Section 3. We consider not only the entire time period 2019–2020, but also the two calendar years 2019 and 2020 separately. With the modified information criterion, we select the number of real-valued factors (i.e., ) to be one for 2019, two for 2020, and two for 2019–2020. As recommended in the simulation, we use the functional shrinkage with adaptive lasso to estimate the functional idiosyncratic covariance matrix. With the amended cross-validation in Section 5.1, we select the tuning parameter as 0.160 for 2019, 0.230 for 2020, and 0.114 for 2019–2020.

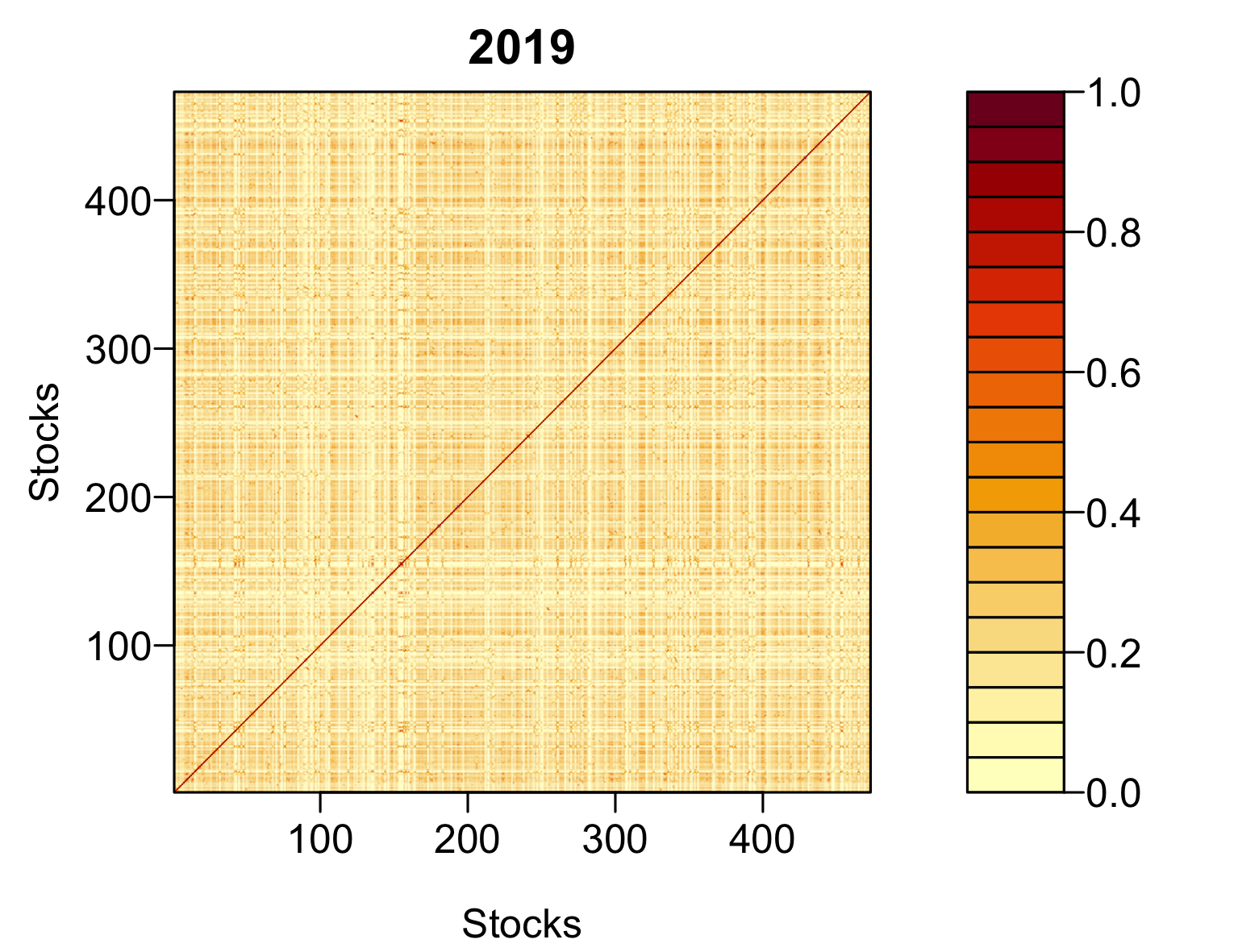

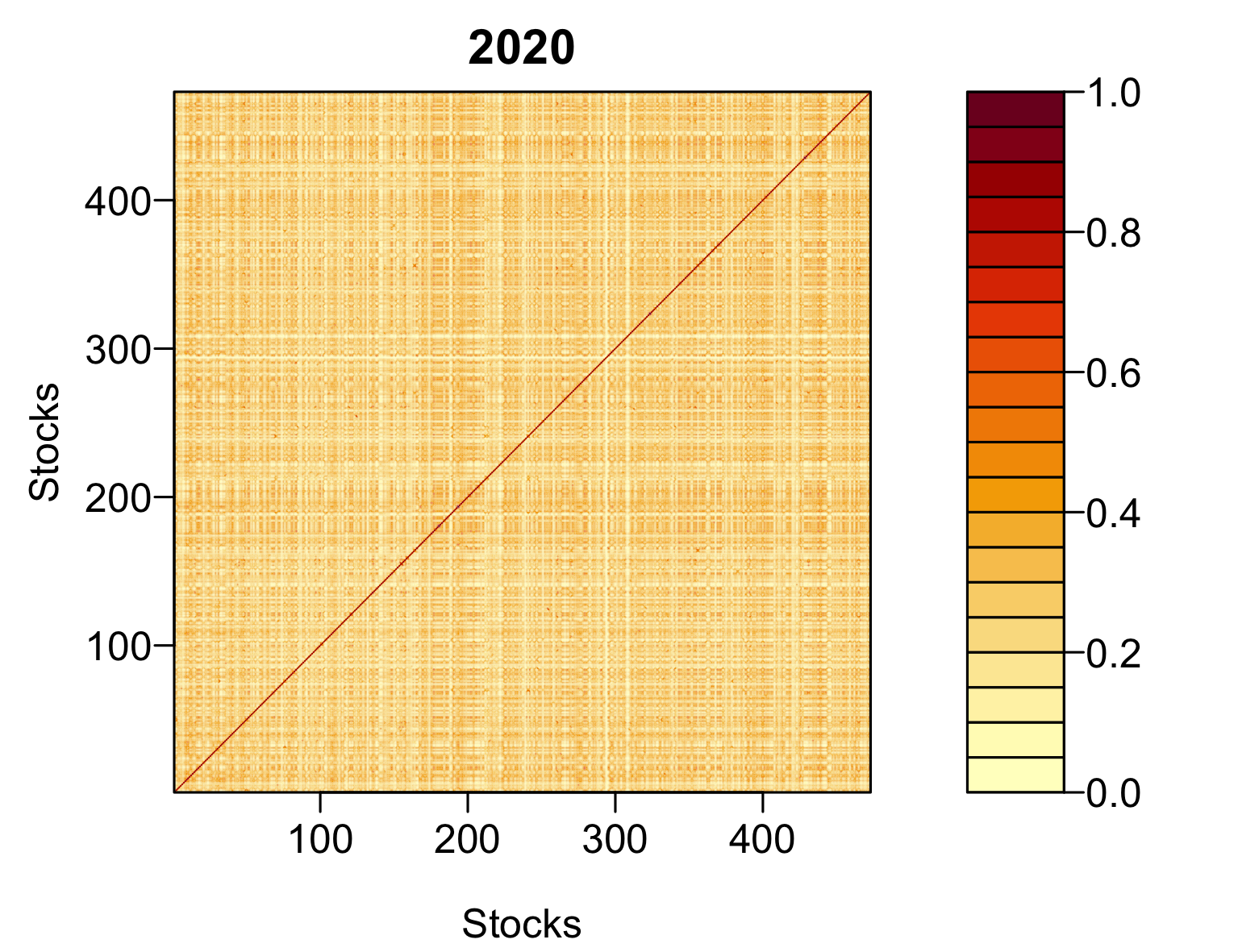

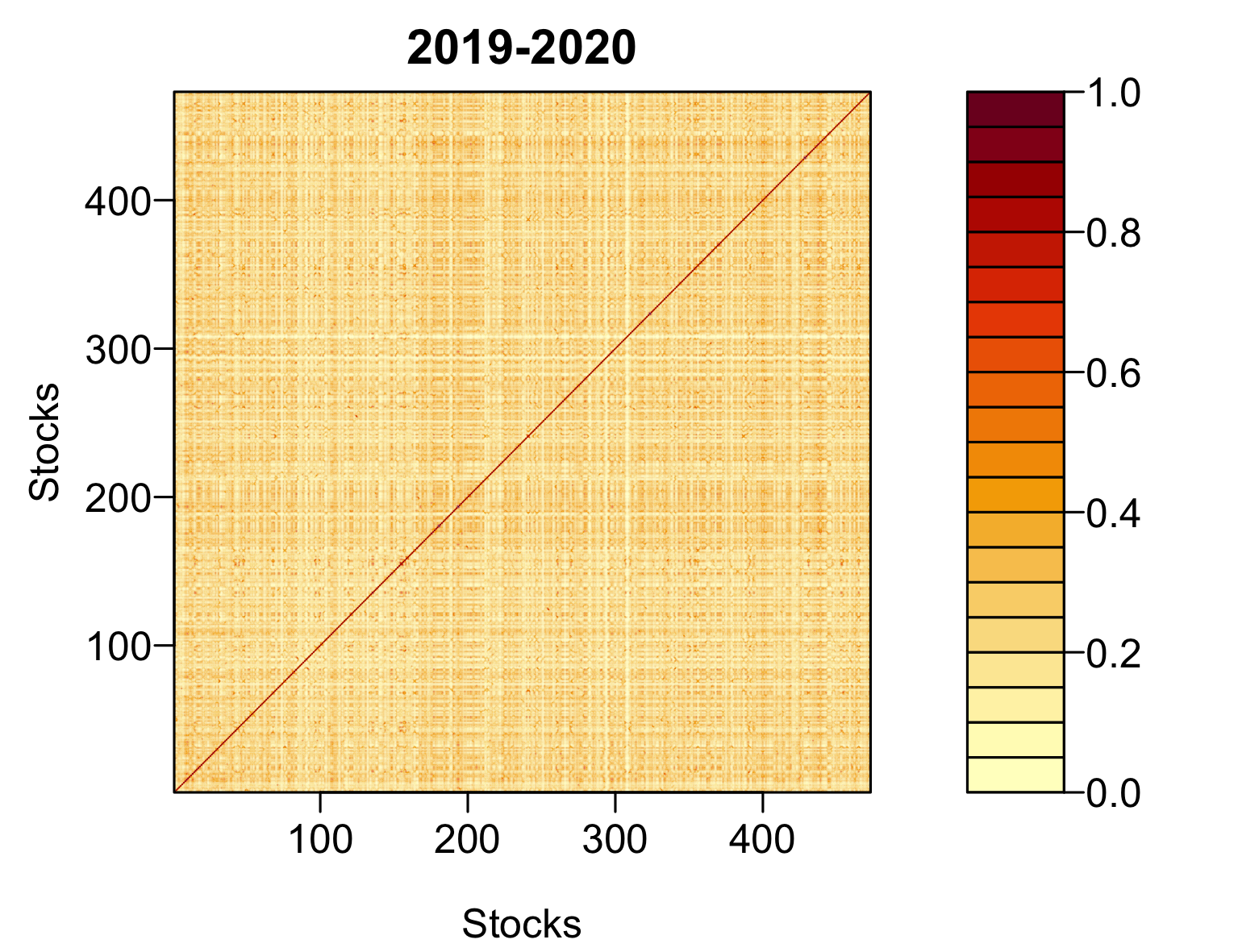

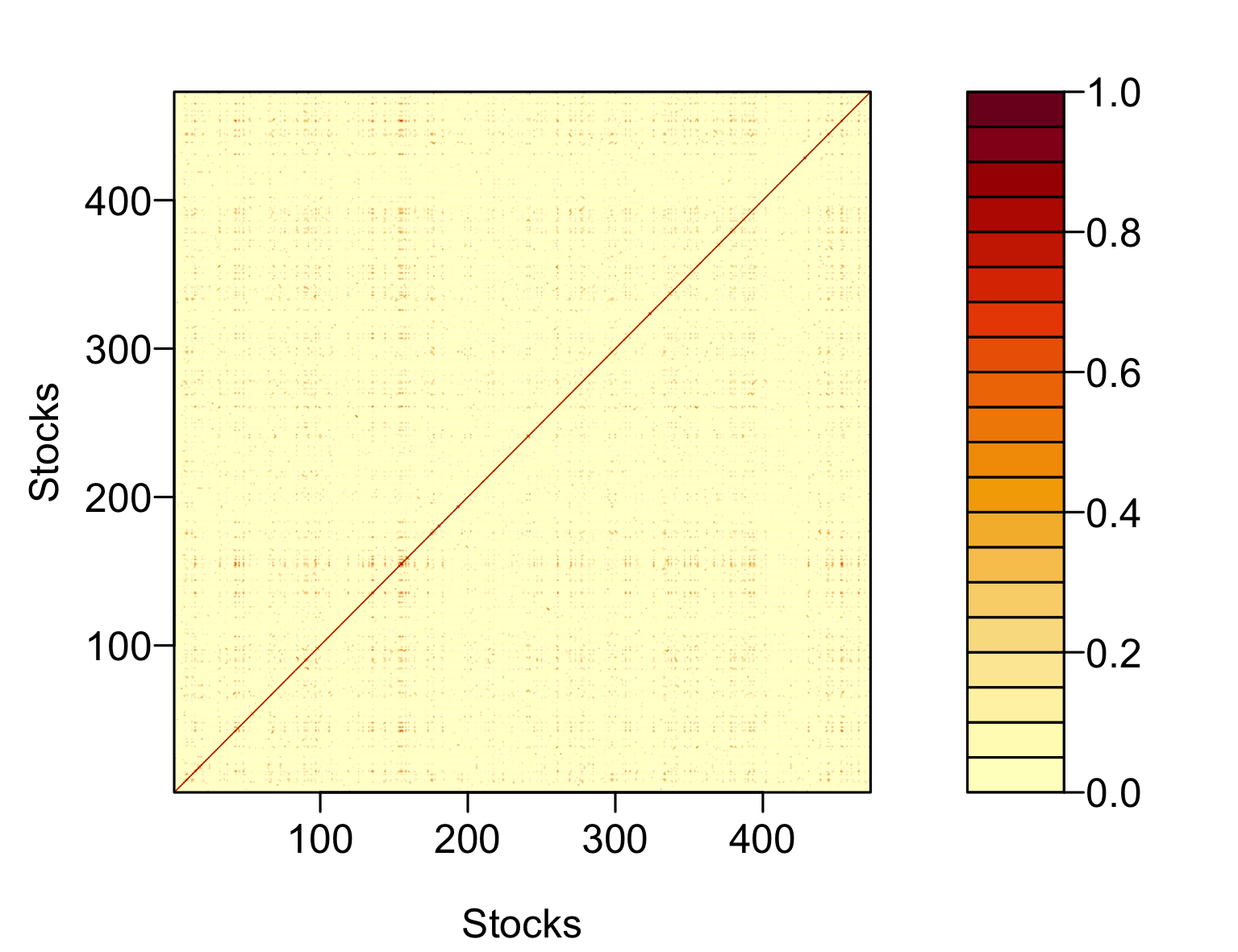

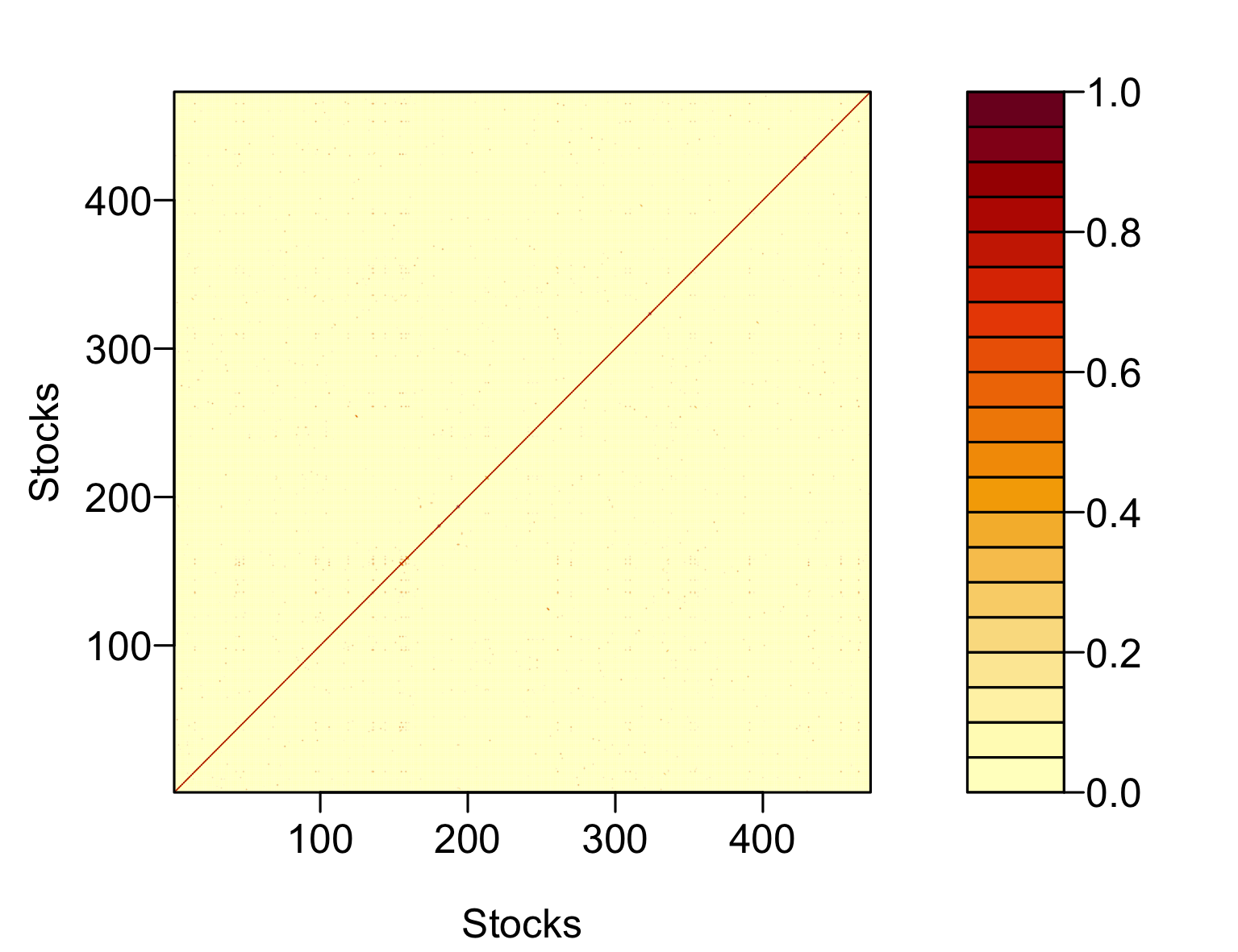

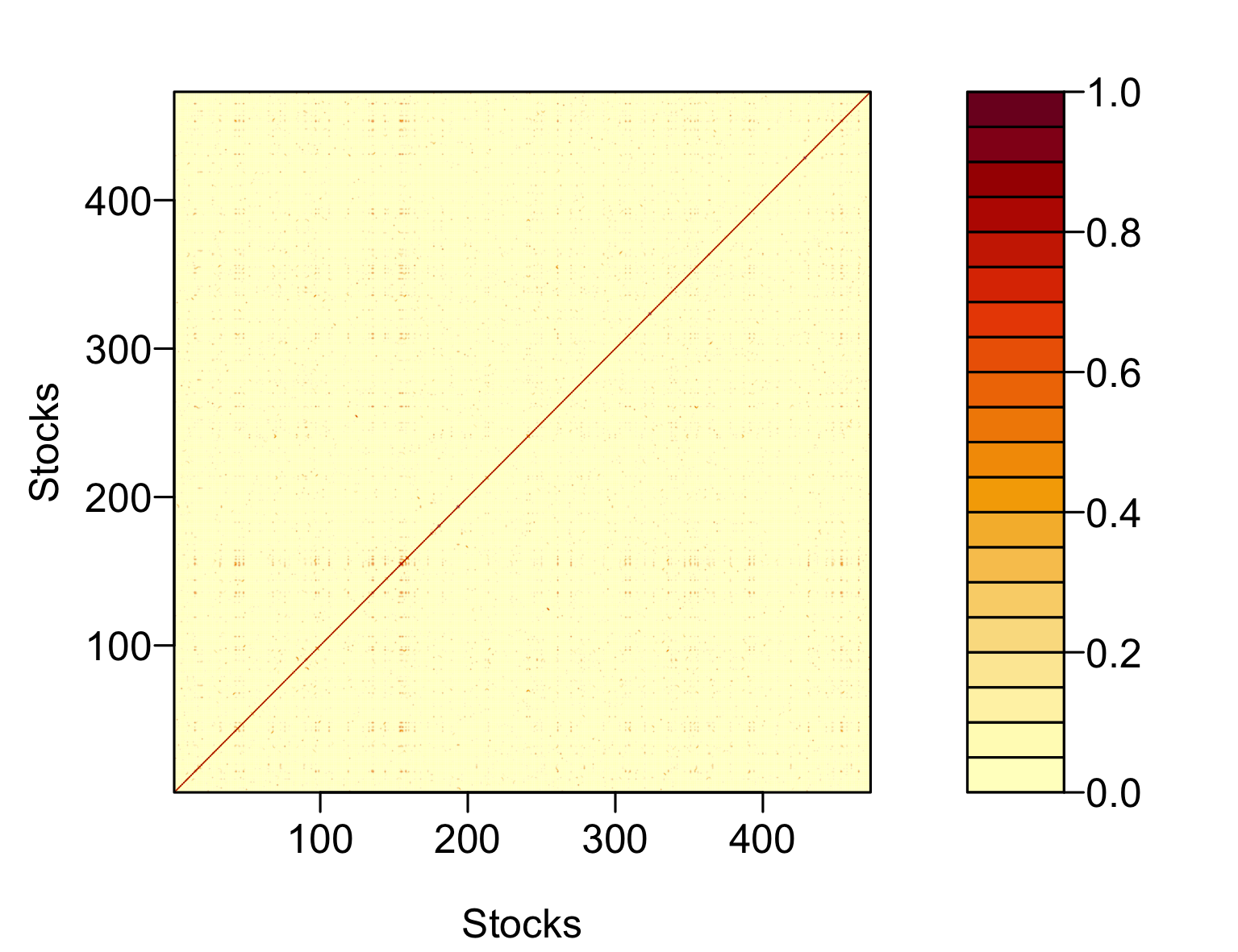

With the estimated covariance functions between stocks, we may further compute the correlation functions whose Hilbert-Schmidt norms are comparable over stocks. Define

where denotes the Hilbert-Schmidt norm of a covariance function (or operator). The correlation functions between the functional idiosyncratic components are computed in a similar way. The Hilbert-Schmidt norms of the estimated correlation functions are used to plot the heat maps displayed in Figure 2. The heat maps show that the functional correlation (or covariance) structure among the stocks is dense whereas that among the functional idiosyncratic components (after removing the common factors) is very sparse, justifying the proposed (approximate) functional low-rank plus sparse structure. Furthermore, we also note that the correlations among the stocks are stronger in 2020 than in 2019, which may be due to a stronger co-movement after the declaration of the COVID-19 pandemic in early 2020.

6 Conclusion

In this paper, we introduce a general dual functional factor model framework to tackle high-dimensional functional time series, extending recent proposals in the literature (Guo, Qiao and Wang, 2021; Tavakoli, Nisol and Hallin, 2023a, b). The main model combines a high-dimensional fully functional factor model for the functional observations and a low-dimensional one for the latent functional factors. Using a sieve approximation for the functional factors, we approximate the large matrix of covariance functions (for the observed functional time series) by the functional low-rank plus sparse structure, making it feasible to extend Fan, Liao and Mincheva (2013)’s POET method to the large-scale functional data setting. A functional version of principal component analysis is proposed to estimate the functional factor loadings and common factors, and a functional shrinkage technique is adopted to estimate the covariance structure of the functional idiosyncratic components. Under some mild assumptions, we establish the convergence properties of the developed estimators. An amended information criterion is proposed to consistently estimate the factor number whereas a modified cross-validation is used to select the shrinkage parameter. Simulation study is provided to demonstrate reliable finite-sample performance of the developed methodology and the empirical application confirms the rationality of adopting the functional low-rank plus sparse covariance (or correlation) structure for CIDR curves of S&P 500 index.

Acknowledgements

Leng’s research is partly supported by EPSRC (EP/X009505/1). Li’s research is partly supported by the Leverhulme Research Fellowship (RF-2023-396), Australian Research Council Discovery Project (DP230102250) and Heilbronn Institute for Mathematical Research. Shang’s research is partly supported by the Australian Research Council Discovery Project (DP230102250). Xia’s research is partly supported by the National Natural Science Foundation of China (72033002).

Appendix A: Proofs of the main results

We next prove the main asymptotic theorems. Throughout the proofs, we let denote a generic positive constant whose value may change from line to line.

Proof of Proposition 4.1. (i) It follows from (2.7) that the -entry of defined in (3.5) can be written as

Then, by the definition of the PCA estimate , we have

| (A.1) |

where and are defined in Section 4.2.

By the triangle and Cauchy-Schwarz inequalities and noting that ,

| (A.2) | |||||

By the identification condition (3.6) and Assumption 1(i), we have

| (A.3) |

By Assumptions 1(ii) and 2(ii),

| (A.4) |

where is the -th element of . By Assumption 1(ii)–(iii), we may show that uniformly over and , which, together with the Cauchy-Schwarz inequality, leads to

| (A.5) |

With (A.2)–(A.5), we readily have that

| (A.6) |

Similarly to (A.2), we have

| (A.7) | |||||

It follows from (A.4) and (A.5) that

| (A.8) |

With (A.3), (A.7) and (A.8), we have

| (A.9) |

By the Cauchy-Schwarz inequality,

| (A.10) | |||||

By Assumption 2(i), we readily have that

| (A.11) | |||||

Since is independent of , by Assumption 2(ii),

indicating that

| (A.12) |

As , we can prove that

| (A.13) | |||||

| (A.14) |

It follows from Lemma B.1 that the matrix is positive definite with the minimum eigenvalue larger than a positive number w.p.a.1. Hence, the inverse of is well defined w.p.a.1. Then, by virtue of (A.1), (A.6), (A.9) and (A.14), we complete the proof of (4.1).

(ii) From the definition of , the factor model formulation (2.7), and the normalisation restriction in (3.6), we have

| (A.15) | |||||

Noting that in Assumption 1(ii), by the definition of , we have

| (A.16) |

With (4.1), (A.3) and (A.16), we can prove that

| (A.17) | |||||

By Lemmas B.3 and B.4 in Appendix B, we have

| (A.18) |

and

| (A.19) |

By (4.1) and Lemma B.5, we may show that

| (A.20) | |||||

By virtue of (A.15) and (A.17)–(A.20), we complete the proof of (4.2).

Proof of Theorem 4.2. Define

and recall that

We first prove that

| (A.21) |

By Lemma B.5 in Appendix B, we have

| (A.22) |

Hence, to prove (A.21), we only need to show

| (A.23) |

Note that

and

By (A.3) and Proposition 4.1, we may show that

| (A.24) | |||||

Combining (A.24) and Lemma B.3, we readily have that

| (A.25) |

By (A.25), Lemma B.5 and the Cauchy-Schwarz inequality, we prove (A.23), which, together with (A.22), leads to (A.21). Using (A.21) and the property (iii) of the shrinkage function and noting that , we may show that

completing the proof of (4.3).

We next turn to the proof of (4.4). Note that

| (A.26) | |||||

Define the event , where is a positive constant. For any small , by (A.22), there exists such that

| (A.27) |

By the sparsity condition (3.3) on , setting with and using the property (iii) of the shrinkage function , we have

| (A.28) | |||||

conditional on .

Note that the events and jointly imply that by the triangle inequality. Hence, conditional on ,

| (A.29) | |||||

By virtue of (A.28) and (A.29), letting in (A.27), we complete the proof of (4.4).

Proof of Theorem 4.3. As , we have , and thus

By Proposition 4.1(ii) and (A.16), we may show that

| (A.30) |

Appendix B: Proofs of technical lemmas

In this appendix, we provide the proofs of the technical lemmas which are involved in proofs of the main theorems in Appendix A.

Lemma B.1.

Proof of Lemma B.1. Letting , we note that

| (B.1) | |||||

As in the proofs of (A.6) and (A.9), we may show that

| (B.2) | |||||

and

| (B.3) |

As in the proof of (A.14), we have

| (B.4) |

Let and denote the -th largest eigenvalue of and , respectively. By Weyl’s inequality and (B.1)–(B.4), we can prove that

for any . By Assumption 1(i)–(ii), is strictly positive. Hence, we may claim that is larger than a positive number w.p.a.1, completing the proof of Lemma B.1.

Lemma B.2.

Suppose that Assumptions 1, 2 and 3(i) are satisfied. Let be a diagonal matrix with the diagonal elements being the eigenvalues of (arranged in the decreasing order) and be a matrix of the corresponding eigenvectors, where and are defined in Assumption 1. Then, we have the following convergence result for the rotation matrix :

| (B.5) |

Proof of Lemma B.2. Write

and define

where denotes diagonalisation of a square matrix. Let

where is defined in (3.5) and is defined in (B.1). By the definition of the functional PCA estimation in Section 3, we have

| (B.6) |

indicating that is a matrix consisting of the eigenvectors of .

Rewrite . By Lemma B.1 and Assumption 1(i)–(ii), in order to complete the proof of the lemma, we only need to show

| (B.7) |

By Lemma B.1, we readily have the first assertion in (B.7). By the triangle inequality, we have

By the definitions of and functional PCA as well as Lemma B.1,

| (B.8) | |||||

completing the proof of the second assertion in (B.7). We next turn to the proof of the third assertion in (B.7). Let be a matrix consisting of the eigenvectors of . By the triangle inequality again and Assumption 1(ii)–(iii), we have

| (B.9) |

By (B.6), the definition of and the theorem in Davis and Kahan (1970), we have

| (B.10) |

Using Assumption 1(i)–(ii) and Proposition 4.1(i), and noting that the rotation matrix is asymptotically non-singular, we may show that . By Lemma B.1, we readily have . Hence, we have , which, together with (B.10), leads to the third assertion in (B.7). The proof of Lemma B.2 is completed.

Lemma B.3.

Proof of Lemma B.3. By the definition of , we have

which indicates that

Hence, to prove (B.11), we only need to show that

| (B.12) |

By Assumption 1(iii) and the Markov inequality, we have, for

completing the proof of (B.12).

Lemma B.4.

Proof of Lemma B.4. We first prove that

| (B.14) |

and

| (B.15) |

In fact, by Assumption 3(iii) and the Bonferroni and Markov inequalities, we may show that

since by Assumption 3(i), and

By (B.14) and (B.15), without loss of generality, we assume that and in the rest of the proof. Hence, we have

It follows from Assumption 3(iii) that there exists such that

By Assumption 3(ii), using the argument in the proof of Lemma S2.13 in Tavakoli, Nisol and Hallin (2023b), we may show that is a stationary sequence of -valued random elements with

We next make use of the concentration inequality in Proposition C.1 to prove (B.13). Setting and replacing and by and , respectively, we have

| (B.16) |

where and are defined in Proposition C.1 and

Then, using Proposition C.1, we have

| (B.17) | |||||

as by Assumption 3(i). Since , the first term on the right side of (B.16) is the leading term of and furthermore,

Lemma B.5.

Suppose that Assumption 3 is satisfied. Then we have

| (B.18) |

where is the covariance function between and .

Proof of Lemma B.5. The proof is similar to the proof of Lemma B.4. By (B.15), without loss of generality, we may assume that uniformly over and throughout the proof, and thus

By Assumption 3(iii), there exists such that

By Assumption 3(ii), following the proof of Lemma S2.13 in Tavakoli, Nisol and Hallin (2023b), is a stationary sequence of -valued random functions with

As in (B.16), we write

| (B.19) |

where we set in Proposition C.1, and

By Proposition C.1, we may show that

| (B.20) | |||||

Appendix C: -mixing dependence and concentration inequality

In this appendix, we introduce the so-called -mixing dependence for random elements defined in a separable Hilbert space with norm , and provide the relevant concentration inequality which plays a crucial role in the main theoretical proofs. The -mixing dependence concept is introduced by Dedecker et al. (2007) and Wintenberger (2010) for real-valued random processes. Blanchard and Zadorozhnyi (2019) extend the concept to Banach-valued random processes and derive some concentration inequalities. We next briefly review some definitions and results closely related to our model setting and assumptions.

Let be the probability space and be a -integrable real function space with being the norm. Consider as a sequence of random elements in . Define the following concept of -mixing coefficient:

where is the -algebra generated by , and

with being a ball. The -valued process is -mixing dependent if as . The following concentration inequality follows from Proposition 3.6 and Corollary 3.7 in Blanchard and Zadorozhnyi (2019).

Proposition C.1.

Suppose that is a stationary sequence of -valued random elements with mean zero, , , and

Then, we have

where , , , and

References

- (1)

- (2)

- Ahn and Horenstein (2013) Ahn, S. and Horenstein, A. (2013). Eigenvalue ratio test for the number of factors. Econometrica, 81, 1203–1227.

- Aït-Sahalia and Xiu (2017) Aït-Sahalia Y. and Xiu, D. (2017). Using principal component analysis to estimate a high dimensional factor model with high-frequency data. Journal of Econometrics, 201, 384–399.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 90, 191–221.

- Bickel and Levina (2008) Bickel, P. and Levina, E. (2008). Covariance regularization by thresholding. The Annals of Statistics, 36, 2577–2604.

- Blanchard and Zadorozhnyi (2019) Blanchard, G. and Zadorozhnyi, S. (2019). Concentration of weakly dependent Banach-valued sums and applications to statistical learning methods. Bernoulli 25, 3421–3458.

- Bosq (2000) Bosq, D. (2000). Linear Processes in Function Spaces. Springer, New York.

- Chamberlain and Rothschild (1983) Chamberlain, G. and Rothschild, M. (1983). Arbitrage, factor structure and mean-variance analysis in large asset markets. Econometrica, 51, 1305–1324.

- Chen, Li and Linton (2019) Chen, J., Li, D. and Linton, O. (2019). A new semiparametric estimation approach for large dynamic covariance matrices with multiple conditioning variables. Journal of Econometrics, 212, 155–176.

- Davis and Kahan (1970) Davis, C. and Kahan, W. M. (1970). The rotation of eigenvectors by a perturbation. III. SIAM Journal on Numerical Analysis, 7, 1–46.

- Dedecker et al. (2007) Dedecker, J., Doukhan, P., Lang, G., León, J.R., Louhichi, S. and Prieur, C. (2007). Weak Dependence: With Examples and Applications. Lecture Notes in Statistics 190. Springer, New York.

- Delaigle, Hall and Pham (2019) Delaigle, A., Hall, P. and Pham, T. (2019). Clustering functional data into groups by using projections. Journal of the Royal Statistical Society Series B, 81, 271–304.

- Fan, Liao and Mincheva (2013) Fan, J., Liao, Y. and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements (with discussion). Journal of the Royal Statistical Society, Series B, 75, 603–680.

- Fang, Guo and Qiao (2023) Fang, Q., Guo, S. and Qiao, X. (2023). Adaptive functional thresholding for sparse covariance function estimation in high dimensions. Journal of the American Statistical Association, in press.

- Fiecas et al. (2019) Fiecas, M., Leng, C., Liu, W. and Yu, Y. (2019). Spectral analysis of high-dimensional time series. Electronic Journal of Statistics, 13, 4079–4101.

- Gao, Shang and Yang (2019) Gao, Y., Shang, H. and Yang, Y. (2019). High-dimensional functional time series forecasting: An application to age-specific mortality rates. Journal of Multivariate Analysis, 170, 232–243.

- Guo, Qiao and Wang (2021) Guo, S., Qiao, X. and Wang, Q. (2021). Factor modelling for high-dimensional functional time series. Working paper available at https://personal.lse.ac.uk/qiaox/qiao.links/research_papers/FMHFTS_v2.pdf.

- Happ and Greven (2018) Happ, C. and Greven, S. (2018). Multivariate functional principal component analysis for data observed on different (dimensional) domains. Journal of the American Statistical Association, 113, 649–659.

- Hays, Shen and Huang (2012) Hays, S., Shen, H. and Huang, J. Z. (2012). Functional dynamic factor models with application to yield curve forecasting. The Annals of Applied Statistics, 6, 870–894.

- Hörmann, Kidziński and Hallin (2015) Hörmann, S., Kidziński, L. and Hallin, M. (2015). Dynamic functional principal component. Journal of the Royal Statistical Society: Series B, 77, 319–348.

- Hörmann and Kokoszka (2010) Hörmann, S. and Kokoszka, P. (2010). Weakly dependent functional data. The Annals of Statistics, 38, 1845–1884.

- Horváth and Kokoszka (2012) Horváth, L. and Kokoszka, P. (2012). Inference for Functional Data with Applications. Springer, New York.

- Hyndman et al. (2023) Hyndman, R. J., Athanasopoulos, G., Bergmeir, C., Caceres, G., Chhay, L., O’Hara-Wild, M., Petropoulos, F., Razbash, S., Wang, E. and Yasmeen, F. (2023). forecast: Forecasting functions for time series and linear models. R package version 8.21.1. https://CRAN.R-project.org/package=forecast.

- Kokoszka, Miao and Zhang (2015) Kokoszka, P., Miao, H. and Zhang, X. (2015). Functional dynamic factor model for intraday price curves. Journal of Financial Econometrics, 13, 456–477.

- Kokoszka et al. (2018) Kokoszka, P., Miao, H., Reimherr, M. and Taoufik, B. (2018). Dynamic functional regression with application to the cross-section of returns. Journal of Financial Econometrics, 16, 461–485.

- Lam and Yao (2012) Lam, C. and Yao, Q. (2012). Factor modelling for high-dimensional time series: Inference for the number of factor. The Annals of Statistics, 40, 694–726.

- Li, Li and Shi (2017) Li, H., Li, Q. and Shi, Y. (2017). Determining the number of factors when the number of factors can increase with sample size. Journal of Econometrics, 197, 76–86.

- Li, Qiao and Wang (2023) Li, D., Qiao, X. and Wang, Z. (2023). Factor-guided estimation of large covariance matrix function with conditional functional sparsity. Working paper available at https://personal.lse.ac.uk/qiaox/qiao.links/FactorCov_2023.pdf.

- Martínez-Hernández, Gonzalo and González-Farías (2022) Martínez-Hernández, I., Gonzalo, J. and González-Farías, G. (2022). Nonparametric estimation of functional dynamic factor model. Journal of Nonparametric Statistics, 34, 895–916.

- Panaretos and Tavakoli (2013) Panaretos, V. and Tavakoli, S. (2013). Fourier analysis of stationonary time series in function spaces. The Annals of Statistics, 41, 568–603.

- Rice, Wirjanto and Zhao (2020) Rice, G., Wirjanto, T. and Zhao, Y. (2020). Tests for conditional heteroscedasticity of functional data. Journal of Time Series Analysis, 41, 733-758.

- Stock and Watson (2002) Stock, J. H. and Watson, M. W. (2002). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association, 97, 1167–1179.

- Sun et al. (2018) Sun, Y., Li, Y., Kuceyeski, A. and Basu, S. (2018). Large spectral density matrix estimation by thresholding. Working paper available at https://arxiv.org/abs/1812.00532.

- Tavakoli, Nisol and Hallin (2023a) Tavakoli, S., Nisol, G. and Hallin, M. (2023a). Factor models for high-dimensional functional time series II: Representation results. Journal of Time Series Analysis, 44, 578–600.

- Tavakoli, Nisol and Hallin (2023b) Tavakoli, S., Nisol, G. and Hallin, M. (2023b). Factor models for high-dimensional functional time series II: Estimation and forecasting. Journal of Time Series Analysis, 44, 601-621.

- Wintenberger (2010) Wintenberger, O. (2010). Deviation inequalities for sums of weakly dependent time series. Electronic Communications in Probability 15, 489–503.