Optimal Order Execution subject to Reservation Strategies under Execution Risk

Abstract

The paper addresses the problem of meta order execution from a broker-dealer’s point of view in Almgren-Chriss model under order fill uncertainty. A broker-dealer agency is authorized to execute an order of trading on client’s behalf. The strategies that the agent is allowed to deploy is subject to a benchmark, referred to as the reservation strategy, regulated by the client. We formulate the broker’s problem as a utility maximization problem in which the broker seeks to maximize his utility of excess profit-and-loss at the execution horizon. Optimal strategy in feedback form is obtained in closed form. In the absence of execution risk, the optimal strategies subject to reservation strategies are deterministic. We establish an affine structure among the trading trajectories under optimal strategies subject to general reservation strategies using implementation shortfall and target close orders as basis. We conclude the paper with numerical experiments illustrating the trading trajectories as well as histograms of terminal wealth and utility at investment horizon under optimal strategies versus those under TWAP strategies.

Keywords: Optimal execution; Execution risk; Reservation strategy; Price impact; Utility maximization

1 Introduction

In financial industry, large position holders such as pension funds or investment banks for various reasons are required to trade in or trade out from their current position to an updated target, possibly subject to a given execution horizon which may vary from days to weeks. The net holdings to be adjusted between the current and the target positions are usually too large to be simply dumped to the market without a priori deliberately assessing the trade’s market impact. Untamed price impact by trading may result in significant transaction cost, potentially turned into a substantial loss. Such an execution risk requires to be properly managed and controlled; otherwise it would eventually influence the position holder’s overall profit and loss (P&L). A common practice is to delegate the execution to the firm’s order execution department or outsource to a broker-dealer agency.

The large position holders, while delegating their tasks to an agency for execution, may have in mind their own preferred strategies or benchmarks that they would like the delegated agent to closely track along. For instance, implementation shortfall (IS) orders [1] are frequently employed by managers for the purpose of short-term alpha pursuit. IS orders are constructed with a pre-trade benchmark price in mind, aiming at executing orders at an average price that remains relatively close to the market price at the beginning of the trade. On the contrary, target close (TC) orders [2], often deployed by index-fund managers for the purpose of minimizing fund risk and tracking error, are formulated with a post-trade benchmark price in order to secure a price in average that remains relatively close to the closing price.Volume weighted average price (VWAP) and Time weighted average price (TWAP) strategies are benchmarks specified for trading sequences with constant trading rate in wall clock time (TWAP) and in volume time (VWAP) respectively. These algorithmic trading strategies are examples of benchmarks that may be imposed as trading constraints to the agent who is missioned to trade in or trade out the position. We shall delve into this type of order execution problems subject to a pre-specified benchmark strategy, which we refer to as the reservation strategy (RS for short), as a stochastic control problem and determine their corresponding optimal strategies in feedback form.

The pioneering works in [3], [1], [4] and [5] are among the first to deal with the problem of order execution under price impact. Since its introduction to the order execution problem, numerous progresses and extensions on the classical Almgren-Chriss framework have been made extensively. For instance, [6] and [7] introduced the notion of transient impact to account for the dissipation of price impacts from the past trades. [8] discusses the objective in the optimization problem, while [9] extends the classical mean-variance framework first considered in [3] to encompass general risk measures as penalty for risk aversion. [10], [11], [12] solve the optimal execution problem in relation to a VWAP benchmark, while [13] asserts the use of the arrival price as a benchmark within the Almgren-Chriss framework. [2] and [14] employ the closed price as a benchmark. Above all, [15] introduces the concept of order fill uncertainty, that pre-scheduled orders may not be fully executed, of which the empirical evidence is confirmed by [16] that the inventory processes of traders invariably contain a Brownian motion term. The aforementioned papers are by no means meant for an exhausting list in literature on this line of active research.

In the current paper, we consider the order execution problem from a broker-dealer’s point of view. Assume that a broker is delegated to reallocate a client’s holdings of a certain stock under the Almgren-Chriss model with order fill uncertainty. The broker is regulated by his client to track a benchmark strategy, i.e., the reservation strategy, to the client’s preference. The broker’s incentive of executing client’s order in this circumstance is to maximize his own expected P&L excess to that of the reservation strategy, marked-to-market. To account for risk aversion, we recast the broker’s order execution problem as a utility maximization problem and, in certain cases, are able to solve the problem in closed form. In particular, when the order fill uncertainty vanishes, or becomes negligible, we show that there exists an “affine structure” among the optimal strategies induced from various reservation strategies. This algebraic structure is supposed to help the broker for concocting and understanding optimal strategies subject to client’s general reservation strategies. We argue that the framework is highly versatile in the sense that it encompasses commonly deployed execution strategies such as IS, TC as well as TWAP and VWAP orders as special cases for benchmarking. As per the algebraic structure, it follows that, for any given continuous reservation strategy which can be approximated by a piece-wise constant function, we show that its corresponding optimal strategy can also be approximated by those induced from the piece-wise constant strategies.

The rest of the paper is organized as follows. In Section 2, we lay out the price impact model of Almgren-Chriss under execution risk and incorporate reservation strategies into the problem of order execution. Section 3 presents the optimal feedback control of the order execution problem in Theorem 1 as one of the main results in the paper. Section 4 focuses and provides detailed discussions on the optimal strategies when the order fill uncertainty vanishes. Reservation strategies and their associated optimal strategies considered in Section 4 include IS and TC orders as well as piece-wise constant strategies. The emphasis is put on an “affine structure” among the trading trajectories induced by general reservation strategies using unit IS and unit TC orders as a basis. Numerical examples illustrating the trading trajectories and the performance analysis under the optimal and TWAP strategies are shown and discussed in Section 5. For the sake of smooth reading, technical proofs of all the theorems, propositions and lemmas are postponed and collected till the end of the paper as an appendix in Section A.

Throughout the paper, denotes a complete probability space equipped with a filtration describing the information structure , where is the time variable and the fixed finite liquidation horizon. Let be a two-dimensional Brownian motion with constant correlation defined on . The filtration is generated by the trajectories of the above Brownian motion, completed with all -null measure sets of .

2 Model Setup

2.1 Price Impact Model

Assume a broker is delegated to reallocate a client’s holdings of a certain stock from shares to shares within a given horizon . Let be the number of shares the broker holds at time during the reallocation process and the transacted price at time . The price dynamic is assumed to follow the Almgren–Chriss model [3] [1] [4]. In the Almgren–Chriss framework, the transacted price consists of the fair price and a slippage. The fair price is driven by the SDE

or equivalently,

where describes the tendency of the stock and is a standard Brownian motion. The term , for , is usually referred to as the permanent impact. Penalized by a price slippage, the transacted price is thus given by

where denotes the broker’s intended trading rate at the instant . The slippage , for , is also referred to as the temporary impact. We remark that in the original setting of Almgren-Chriss and its extensions, the trading rate plays a dual role. On the one hand, it serves as the realized trading rate per the relationship between and . On the other hand, it is regarded as the control variable in the problem of optimal execution. These two seemingly distinct roles coincide if all the scheduled orders are guaranteed fully executed. However, in reality it is well noticed among practitioners that, while executing a sequence of pre-scheduled orders, the orders in the sequence may not be fully executed, resulting in an uncontrollable realized order flow. This introduces an additional risk to the order execution problem, the order fill uncertainty. To account for this uncertainty, we introduce a noise component driven by a correlated Brownian motion into the dynamic of the position as

The diffusion term characterizes the magnitude of the uncertainty of order fills. It worths to reiterate that in a recent work in [16], the authors showed that the presence of a Brownian component in the broker’s inventory during reallocation process is statistically significant. Moreover, because of this uncertainty of order fills, the broker is no longer guaranteed to achieve his intended position at the terminal time , which gives rise to an additional opportunity cost. As a result, the broker is obligated to take a final block trade at time at a worse price. Overall, the realised P&L at the horizon is given by

where the term , for , penalizes the discrepency from a final block trade.

The following proposition shows that the P&L can be written as an Itô process.

Proposition 1.

The realised P&L can be rewritten as

2.2 Reservation Strategy

A common practice in order execution brokerage is that clients may come forward to brokers with their own preferred strategies for benchmarking. These benchmark strategies can be either strategies suggested by elite investors or commonly used ones such as TWAP or VWAP strategies. We shall refer to these pre-specified benchmark strategies as reservation strategies. We consider the reservation strategies that can be represented by a deterministic function with and hereafter.

The broker’s incentive of executing client’s order is thus to maximize his own expected P&L excess to that of the reservation strategy, marked-to-market. Specifically, by disregarding the price impact and slippages incurred from order execution, the stock price reads

The marked-to-market P&L for the reservation strategy is evaluated as

Hence, the broker’s excess P&L , defined by the difference between and , is given by

| (1) | ||||

The broker’s goal is thus to maximize his expected excess P&L in a risk aversion manner which we recast as a utility maximization problem in the section that follows.

3 Optimal Execution as Utility Maximizing

In this section, we recast the problem of order execution as a utility maximization problem as follows. Recall that denotes a complete probability space equipped with a filtration satisfying the usual conditions. We assume that all random variables and stochastic processes are defined on . The set of all real-valued progressively measurable processes are denote by , while the collection of admissible controls is set as

The broker’s problem is to determine an optimal admissible strategy that maximizes his expected exponential utility at the horizon , i.e.,

| (2) |

where the utility function represents the broker’s preference following CRRA (Constant Relative Risk Aversion) preference and is the risk-aversion parameter.

In the following, we solve the utility maximization problem (2) and present solutions in closed form in the cases where the uncertainty of order fill is either a constant or zero. The case of zero uncertainty of order fill is postponed and will be discussed in more details in Section 4.

3.1 Constant Uncertainty of Order Fills

When the uncertainty of order fills is constant, i.e., for some fixed constant , the optimal feedback control can be obtained in closed form. We summarize the result in the following theorem.

Theorem 1.

Let , for some positive constant . The optimal feedback control of the utility maximization problem (2) is given by

| (3) |

where the parameters , , and are

The time dependent function is given in closed form by

and is a solution to the following terminal value problem

The optimal feedback control consists of three parts:

-

•

The first part has the same sign as . Without loss of generality, we assume that , when , which implies the reallocation process has not finished, so the broker should continue to sell the stock. Conversely, when , which implies the strategy is over-shooting, so the broker should buy some shares of the stock back.

-

•

The second part , which is a pre-specified deterministic function in time , does not depend on the state variable .

-

•

The third part has the same sign as , where is the correlation between the stock price process and the execution risk. The discussions in [17] state the fact that the sign of depends on the order type adopted by the trader due to adverse selection: when the trader uses market orders, the correlation is negative while is positive whenever trading with limit orders. In this paper, we regard as a market parameter reflecting whether the market is trader-friendly or not.

-

–

When , the stock price and execution risk tend to increase or decrease together: when the stock price increases, execution risk makes traders buy more or sell less than the amount they submit, which is benefit to the traders; when the stock price decreases, execution risk forces traders to buy less or sell more, which is also benefit to the traders. In such trader-friendly market, like the figure (1), the broker should keep away from the reservation strategy because an overly conservative strategy is not necessary.

Figure 1: A trader-friendly market -

–

On the contrary, implies a trader-harmful market: when the stock price increases, execution risk makes traders buy less or sell more than the amount they submit, which is harm to the traders; when the stock price decreases, execution risk forces traders to buy more or sell less, which is also harm to the traders. In such trader-harmful market, like the figure (2), the broker should keep close to the reservation strategy to attain lower risk.

Figure 2: A trader-harmful market

-

–

Remark 1.

By applying the optimal strategy (3), one obtains the optimal liquidation trajectory as follows. For simplicity, take , satisfies the SDE

which has the closed form solution

| (4) |

where . If we further take and , then and the expression will be neater, in this case,

As , has the limit

Furthermore, when , , the limit of the expression above is

where . It recovers the classical implementation shortfall (IS) strategy (see in section 4.2), which implies the fact that our strategy can be regarded as a version of adaptive IS strategy. Furthermore, we may find that

which is an Ornstein-Uhlenbeck bridge [18]. Therefore, when is small, one may find the approximation to the optimal strategy

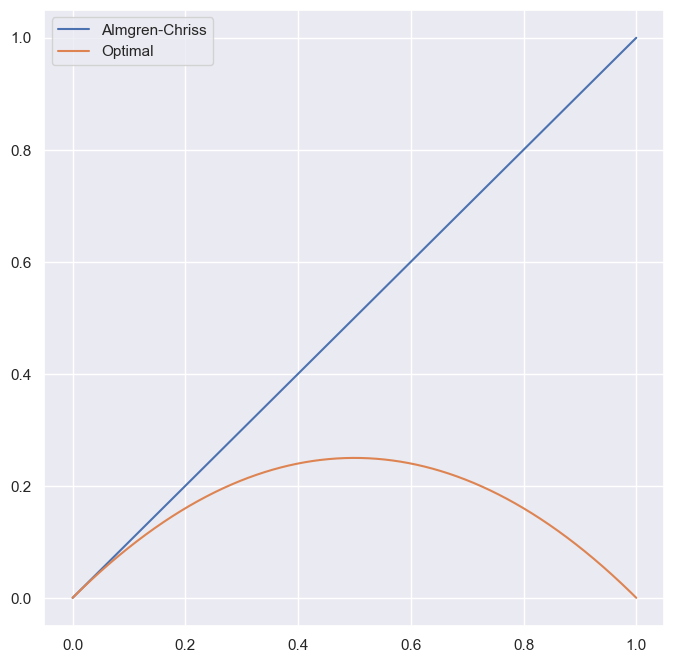

which is a classical IS strategy plus an Ornstein-Uhlenbeck bridge. Figure (3) shows the inventory risk of our optimal strategy and the classical IS strategy, which shows the fact that our optimal strategy has lower inventory risk than the classical IS strategy, especially at the end of the trading process.

4 Zero Uncertainty of Order Fills

For the purpose of better understanding as well as visidualizing the optimal strategy obtained in (3), we present in this section the trading trajectory under optimal strategy in the case when for various reservation strategies. In Section 4.1, we give the optimal strategy for general reservation strategies. In Section 4.2 and 4.3, we present two classic trading strategies: IS order and TC order, both widely used in the market, and show that they are special cases of our model. Next, we consider the case when the reservation strategy is an endpoints-only one in Section 4.4, of which the optimal strategy has a heuristic form. Last but not least, piece-wise constant reservation strategies are studied in Section 4.5.

Notice that in this case the setting of the problem reduces to that of the Almgren-Chriss but subject to a reservation strategy. Furthermore, we shall set the final penalty parameter , indicating that a final block trade at terminal time is strictly prohibited.

4.1 General Reservation Strategy

For a given generic reservation strategy , the following theorem shows a representation for the trading trajectory under optimal control .

Theorem 2.

Let and . The trajectory under the solution to the optimization problem (2) is given by

where the parameter .

A few remarks on the trajectory shown in Theorem 2 are in order.

-

1.

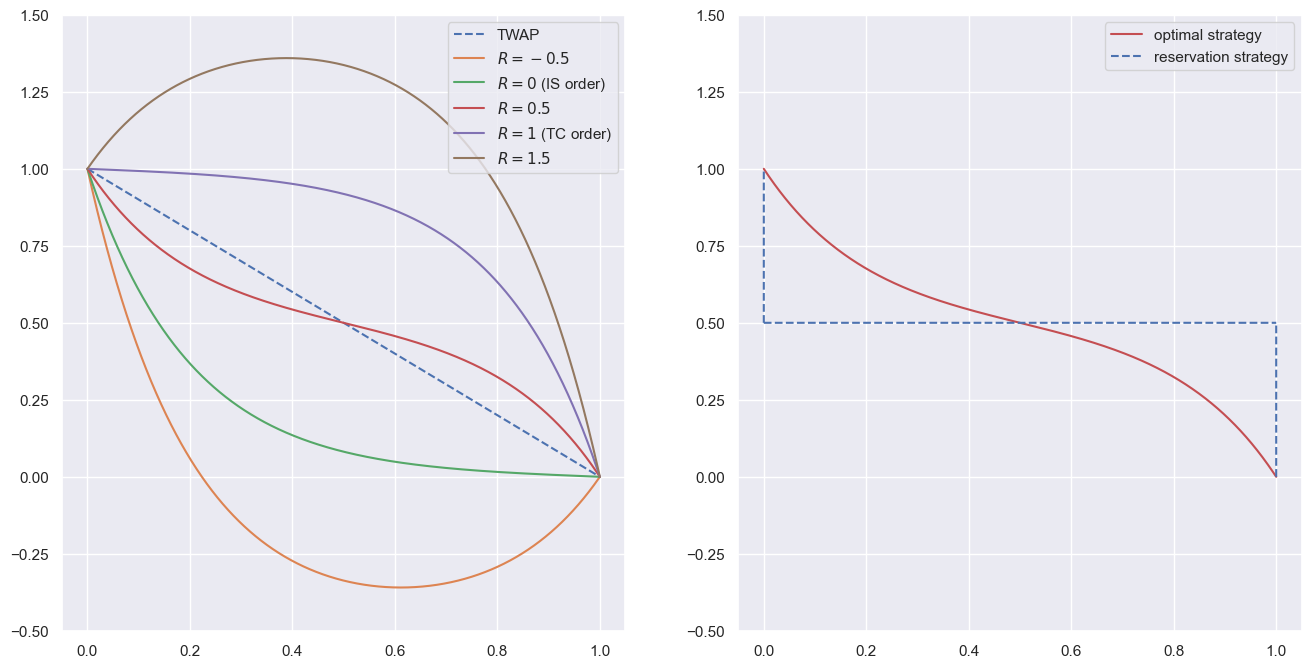

The parameter can be regarded as a tuning parameter between the TWAP and the reservation strategies if . Specifically, in the limit as approaches zero, the optimal strategy converges to the TWAP strategy, i.e., for any , we have

On the other extreme as , the optimal trajectory converges to the reservation strategy itself

for any .

-

2.

The optimal trajectory may also be written as an “affine transformation” as

where

A more detailed discussion on this affine transformation can be found in Section 4.5.

Next, we further specialize the reservation strategies and present their corresponding trajectories in the following sections.

4.2 Implementation Shortfall Order

Assume and the broker is asked to take as the reservation strategy a block trade of size at , i.e.,

The marked-to-market P&L of the reservation strategy is given by

which is equivalent to choosing the initial price as reference price. This model is referred to as an implementation shortfall model in [19], of which the optimal strategy is

| (5) |

where

| (6) |

We shall refer to the strategy as the unit implementation shortfall (IS) order. Hence, the trajectory in (5) can be interpreted as executing unit IS orders if a broker is missioned to make transition of his position from to shares. We remark that, as we will show in Section 4.5, the unit IS orders are used as one of the building blocks for the construction of optimal trajectories for more general reservation strategies.

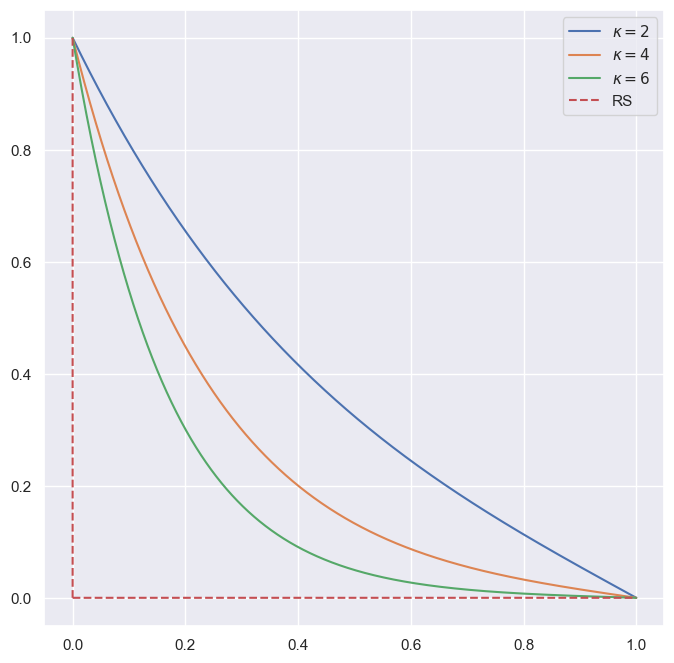

Figure (4) shows examples of the unit implementation shortfall orders under various values of . Notice that, since , as increase or decreases, thus increases, the trajectories suggest the broker trade faster at the beginning and more slowly for the rest of the reallocation process. Indeed, the larger the , the faster the trading at the beginning. The financial rationale is as follows. Recall that is the coefficient of relative risk aversion for the utility function and is the volatility of stock price. Hence, if either of the parameters increases, the broker is more concerned with the price risk than the execution risk, he tends toward trading faster at the beginning and more slowly thereafter. Also, since is the coefficient of slippage, as it decreases, the slippage decreases as well, resulting in lower cost from faster transactions. Therefore, again to mitigate the concern of price risk during reallocation process, the broker should also trade faster at the beginning as well.

4.3 Target Close Order

Assume again that . Here the broker is given as the reservation strategy to take only a block trade of size at terminal time . That is,

The marked-to-market P&L for this reservation strategy is given by

which is equivalent to choosing the stock price at terminal time as the reference price. This model is referred to as an target close model in [19][2], of which the optimal strategy is given by

| (7) |

where

| (8) |

We refer to the strategy in (8) as the unit target close (TC) order. Thus, similar to the case of implementation shortfall order in Section 4.2, the trajectory in (7) can be interpreted as executing unit TC orders if a broker is missioned to make transition of his position from to shares. Likewise as for the unit IS orders, we show in Section 4.5 that the unit TC orders are used as the other building blocks for the construction of optimal trajectories for more general reservation strategies.

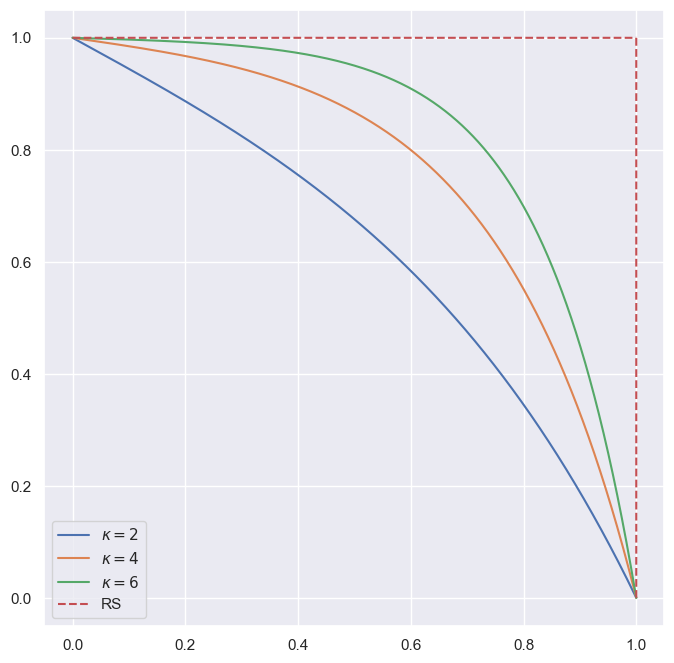

Figure (5) shows examples of plots for unit target close orders in different values of . We observe that the trading trajectories are concave in time as opposed to convex in time as that of the unit IS orders. Also, as increases, the optimal trajectory moves towards the reservation strategy and towards the TWAP trajectory as decreases. In fact, similar to the case for implementation shortfall, in the limit as , the unit TC order (8) converges to the TWAP strategy: for any ,

whereas in the other extreme as , the optimal trajectory converges to a block trade at terminal time :

4.4 Endpoints-only Reservation Strategy

In this section, we consider the following reservation strategy , which we called the endpoints-only.

| (9) |

The strategy is simply to hold shares during the entire reallocation process, except at the initial and terminal times,.

The following lemma will prove itself useful in the determination of the optimal strategy subject to the reservation strategy (9).

Lemma 1.

We have that

In other words, the given integral can be written as the difference between a unit TC and a unit IS order.

We summarize the result for optimal strategies subject to (9) in the proposition that follows.

Proposition 2.

For the reservation strategy in (9), the optimal trajectory is given by an affine combination of a unit IS order and a unit TC order as

| (10) |

Note that when and , the optimal strategy reduces to the following TC strategy as in (7)

whereas when and , the optimal strategy reduces to the following IS strategy as in (5)

Note that for any given reservation level , the optimal trajectory in (10) at any point in time is an affine combination of a unit IS order and a unit TC order. The coefficients represent a trade-off between the two strategies. For example, if is closer to the initial position and further away from the target position , the strategy in (10) suggests we weigh in more on the unit TC order and less on the unit IS order; conversely, one should then weigh in more on the unit IS order. Figure (6) shows the plots of optimal trajectories in different reservation levels , assuming and . Again, we end up with a unit TC order when and a unit IS order when .

As shown in Figure 6, when the optimal strategy suggest overshoot the target, meaning buying more than needed then sell back later and quicker when time approaches the terminal time. On the other hand, if , the optimal strategy suggests undershoots the target. We provide conditions on the parameters under which an overshooting or an undershooting occur in the following proposition.

Proposition 3.

Without loss of generality, assume . Let be the optimal strategy given in (10). We have that, if , then is concave in and it becomes convex in if . It follows that overshoots if and only if

and it undershoots if and only if

It appears that, when is nonzero, the terms in the optimal trajectory (10) that have involved always come in the form of . We provide a financial rationale of this combination of parameters as follows. Note that the combination resembles the Merton ratio in Merton’s optimal portfolio problem in the market consisting of two assets: one risky and the other riskless. The agent is risk averse with power utility and the dynamic of risky asset is governed by a geometric Brownian motion with expected return and volatility . The riskless asset is assumed accruing zero interest. In this setting, the Merton ratio, which represents the percentage of wealth invested in the risky asset, is given by . In our setting, the broker is with exponential utility and the stock price is assumed following an arithmetic Brownian motion with drift and volatility , i.e.,

As in the derivation of the Merton ratio in Merton’s problem, one may show that the “Merton ratio” in this case is given by except that this ratio does not represent the percentage of wealth invested in the risky asset as in the original Merton’s problem. Indeed, this ratio represents the number of shares to be held in the optimal portfolio.

4.5 Piece-wise Constant Reservation Strategy

We consider in this section the reservation strategies that are piece-wise constant across time. The consideration is that, to possibly account for real time market environments during the entire reallocation process, the broker’s strategies may be subject to interval TWAP or VWAP strategies. For example, in an intraday trading activity, it is documented that the market trades much more actively at the times close to opening and closing than that in the middle of common trading days. Also, in the case where trading horizon across multiple days, the broker is most likely treating each trading day individually. In these regards, a piece-wise constant reservation strategy is considered plausible. Theoretically, as we will see in the following, optimal trajectories subject to piece-wise constant reservation strategies have a nice algebraic structure based upon the unit IS and unit TC orders obtained in Sections 4.2 and 4.3, respectively. This structure thus provides, by applying a typical approximation and limiting process for integrable functions, practical and helpful intuitions for the optimal strategies subject to general integrable reservation strategies.

A generic piece-wise constant reservation strategy is defined as

| (11) |

where denotes the indicator function, is the number of periods, and the ’s are fixed constants. The following proposition summarizes the optimal trajectory under the piece-wise constant reservation strategy in (11).

Proposition 4.

The solution to the previous optimization problem under the piece-wise constant reservation strategy given in (11) is of the following form, for ,

| (12) |

where, with ,

and the ’s, for are to be determined.

Notice that the and in Proposition 4 are indeed respectively the unit IS order given in (6) and the unit TC order in (8). Proposition 4 essentially states that, for a given piece-wise constant reservation strategy, its corresponding optimal solution in each subinterval is given by an affine transformation of a unit IS order and a unit TC order. In this sense we may regard the unit IS orders and the unit TC orders obtained in Sections 4.2 and 4.3 respectively as the building blocks or bases for optimal trajectories under piece-wise constant reservation strategies. The algebraic structure of the optimal trajectories is thus depicted by the affine space generated by the unit IS and unit TC orders. What are left to be determined are the coefficients that are subinterval dependent. As an example, Figure (7) shows the plots of a piecewise constant reservation strategy (in dotted red) its optimal trajectory (in blue) with three subintervals , the other parameters are given by , , .

To conclude the section, we show in Theorem 3 a stability theorem for optimal strategies subject to general, smooth enough, reservation strategies.

Theorem 3.

For any given reservation strategies and satisfying

for some . Let and be the corresponding optimal trajectories for and , respectively. We have that, for any ,

The above theorem basically states that when two reservation strategies are close in the sense, their corresponding optimal strategies remain close in the sup norm sense. Note that for any and an almost everywhere continuous bounded RS , there exists a piece-wise constant RS such that

It follows that the optimal trajectory in (12) for , which is an affine transformation of unit IS and unit TC orders in each subinterval, can be applied as an approximation to the optimal trajectory under reservation strategy , with error estimate given in Theorem 3.

5 Numerical Examples

We conduct in this section numerical experiments on the implementation of optimal strategy obtained in Theorem 1 and stress testing the strategy against various parameters. Monte Carlo simulations are implemented to illustrate sample trading trajectories and the performances criteria of the optimal strategy versus those of a related TWAP strategy. The performance of the optimal and TWAP strategies are then stress tested against certain extreme parameters. We remark that the parameters chosen for the numerical examples in this section are for convenience only. In practice, parameters are supposedly calibrated to market data prior to implementation, causing possible issues associated with estimation risk.

5.1 Sample trading trajectories

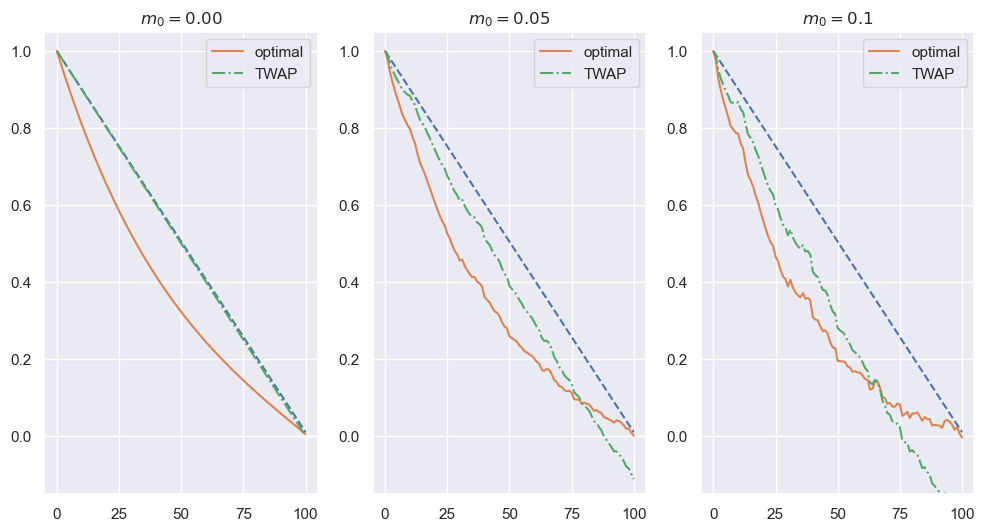

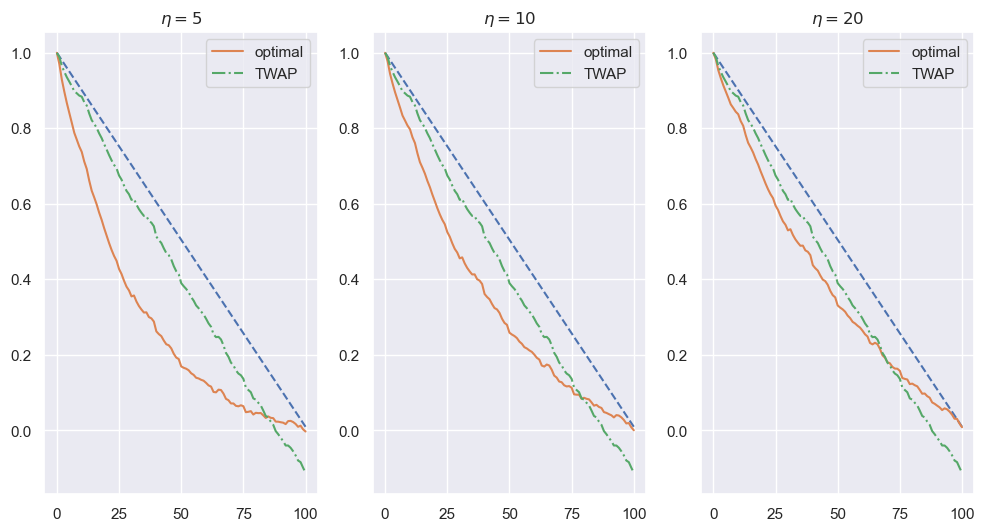

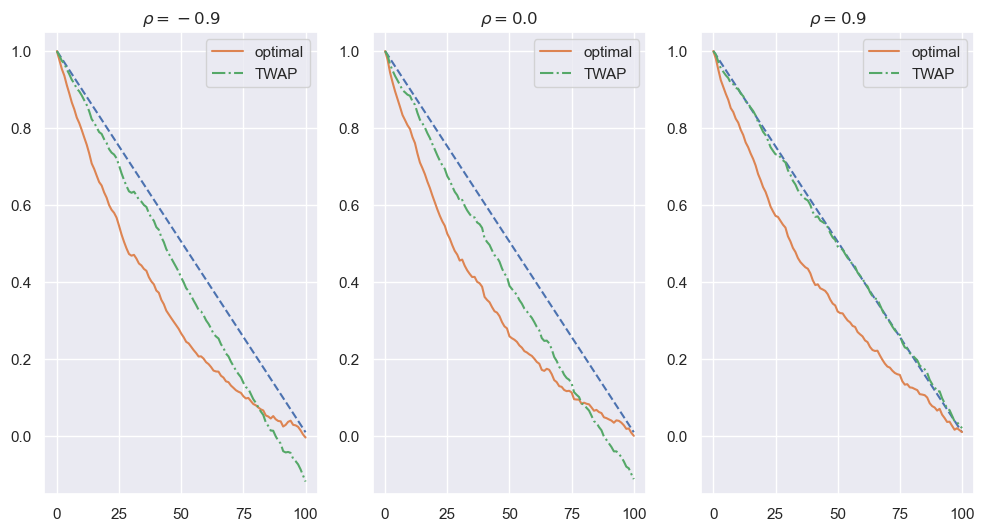

We present in Figures 8 through 13 sample trading trajectories under the optimal and a related TWAP strategies in various parameters. Parameters chosen as base case are . Table 1 summarizes the parameters that vary, while the others are held fixed, in each case and their corresponding figures. The reservation strategy is selected as a block trade at , as shown in Section 4.2.

| Figure number | Parameter | Case 1 | Case 2 | Case 3 |

|---|---|---|---|---|

| Figure 8 | 0.00 | 0.05 | 0.10 | |

| Figure 9 | 5 | 10 | 20 | |

| Figure 10 | -0.9 | 0 | 0.9 | |

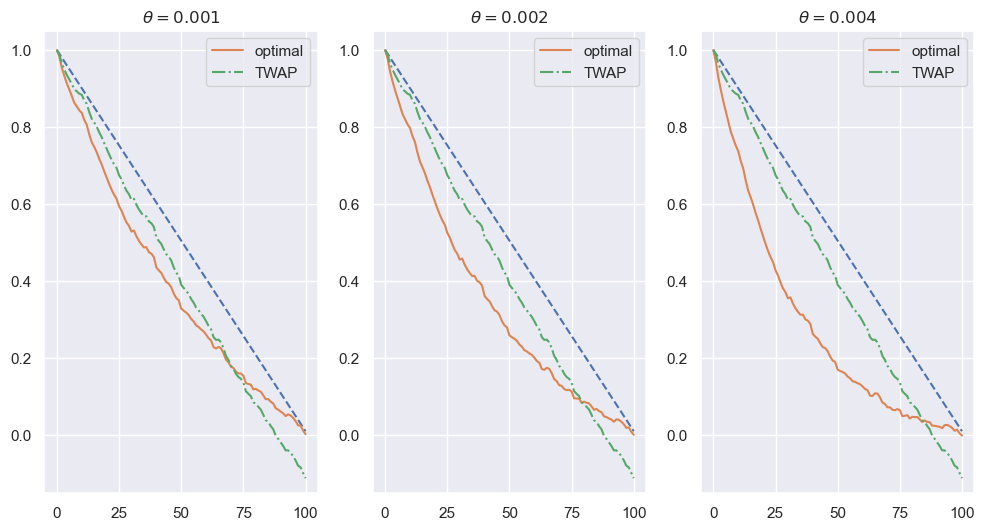

| Figure 11 | 0.001 | 0.002 | 0.004 | |

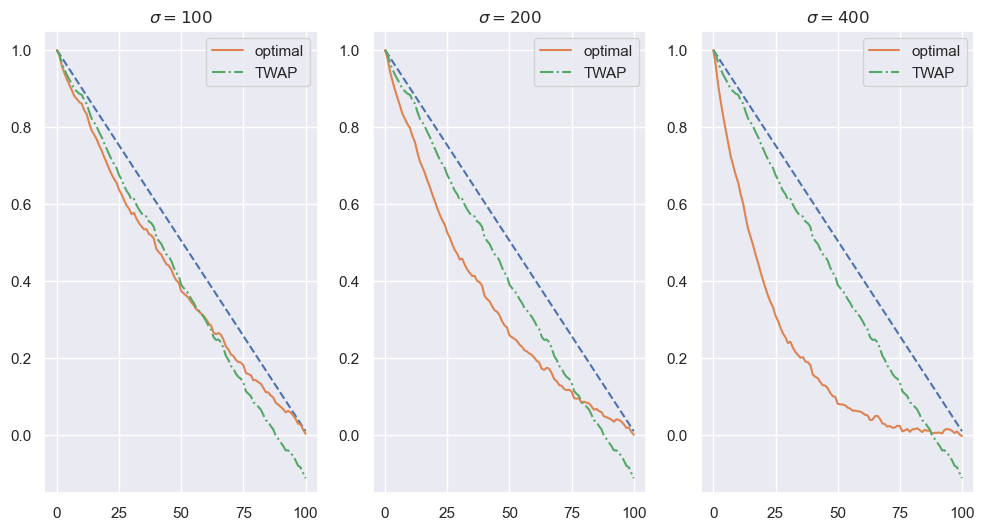

| Figure 12 | 100 | 200 | 400 | |

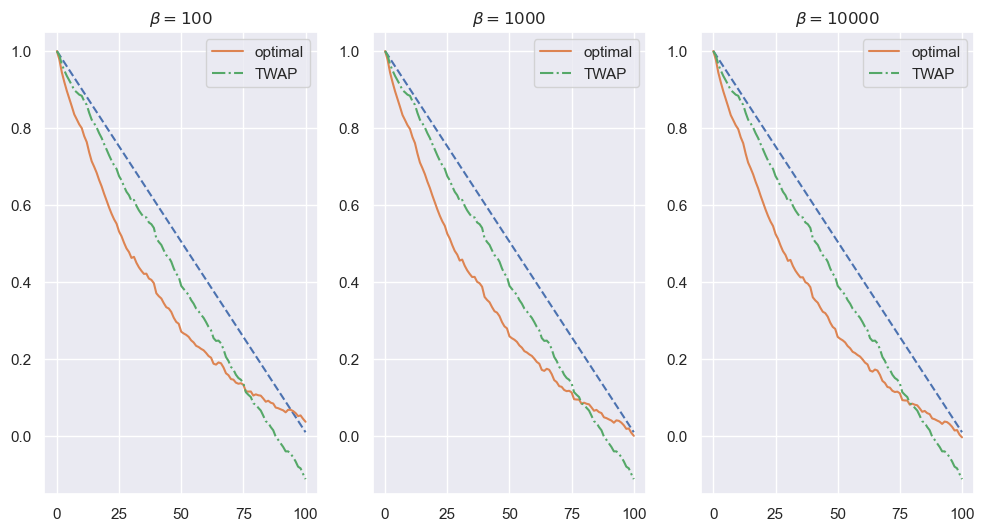

| Figure 13 | 100 | 1000 | 10000 |

Figure (8) illustrates sample trading trajectories for the optimal and the TWAP strategies in different values of . We note that, since quantifies the uncertainty of order fills, as increases both trajectories become more volatile and fluctuating.

Figure (9) exhibits sample trading trajectories in varying values of . It is worth mentioning that, since reflects the level of transaction costs, as the value of increases, transaction cost becomes more significant in the determination of optimal strategies. Consequently, the optimal strategy tends to align more closely with the classical TWAP strategy. In other words, a higher places greater emphasis on minimizing transaction costs, motivating the adoption of a strategy that mirrors the TWAP approach, which aims for consistent execution over time.

Figure (10) shows optimal strategies in the values of . Recall that denotes the correlation between the stock price and the uncertainty of order fills. We note that there seems no significant dependence of the optimal strategies on within this set of parameters.

Figure (11) illustrates the optimal strategies in the values of , which represents the broker’s taste of risk aversion. The larger the value of , the more risk averse the broker tends to be. It follows that the sample trading trajectory under optimal strategy gradually converges towards the reservation strategy as increases, indicating the broker’s inclination to adopt a more conservative and risk-averse approach.

Figure (12) shows sample trading trajectories under optimal strategies with respect to the stock volatility . As increases, the price risk increases. Thus, to mitigate the risk incurred from the price volatility during execution, the optimal strategy tracks more closely to the reservation strategy.

Figure (13) presents the optimal strategies in the values of , which quantifies the penalty of block trade at terminal time. Large indicates that any remaining inventory at terminal time is unfavorable. Therefore, it is seen in the figure that the terminal inventory of the sample trading trajectories under optimal strategy gradually approaches zero. It is thus fathomable that, as approaches infinity, a final block trade at terminal time turns into strictly prohibited.

5.2 Performance analysis and stress test

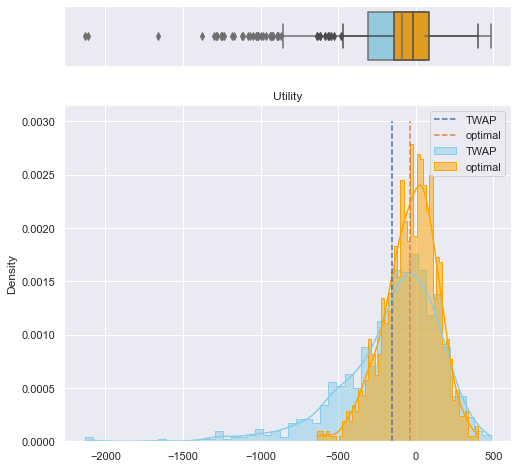

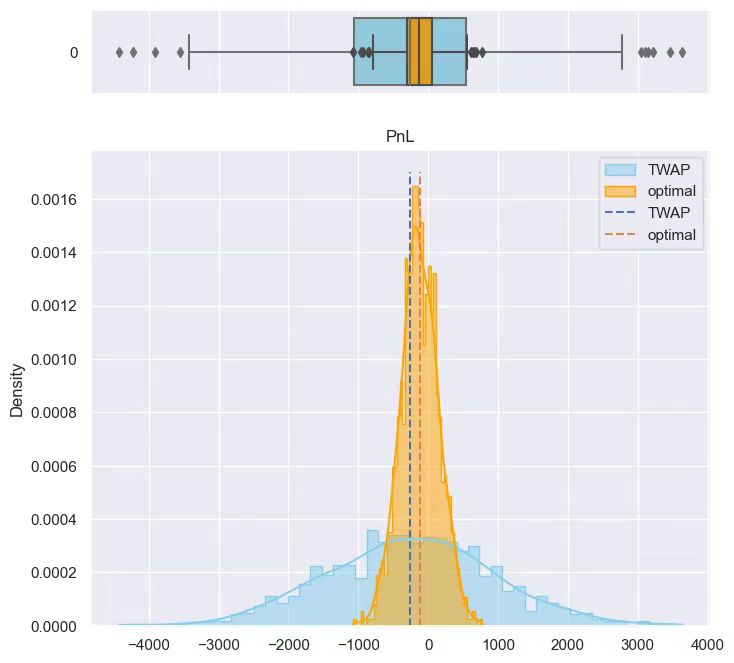

To demonstrate the performance of the optimal strategy against TWAP, we implement the strategies using Monte Carlo simulations and present the resulting histograms and boxplots of the terminal wealths as well as the utilities at the investment horizon. This performance analysis serves to illustrate the optimality and robustness of the optimal strategy.

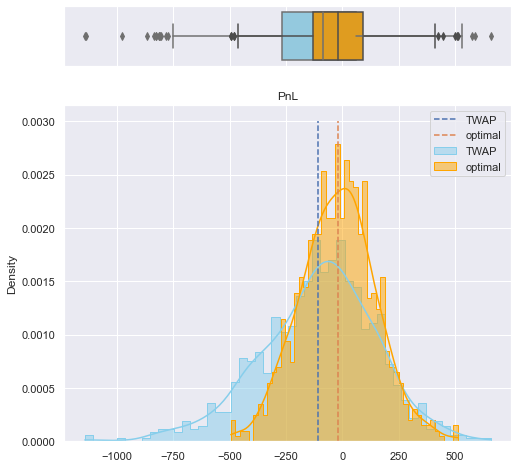

Figure (14) exhibits the histograms and boxplots of the terminal P&L (on the left) and the utility (on the left) at investment horizon for the optimal and the TWAP strategies. We observe that the optimal strategy not only consistently achieves higher average terminal wealth and utility than those under TWAP but also bears lower variability. Furthermore, an intriguing observation is made regarding the tail ends of the distribution. Specifically, the TWAP strategy demonstrates a greater density in these tail regions, indicating a higher likelihood of incurring significant losses when compared to our optimal strategy. This discrepancy in density at the tail end reinforces the notion that the TWAP strategy may accentuate the potential for unfavorable outcomes, thus reflecting a subpar approach to risk management.

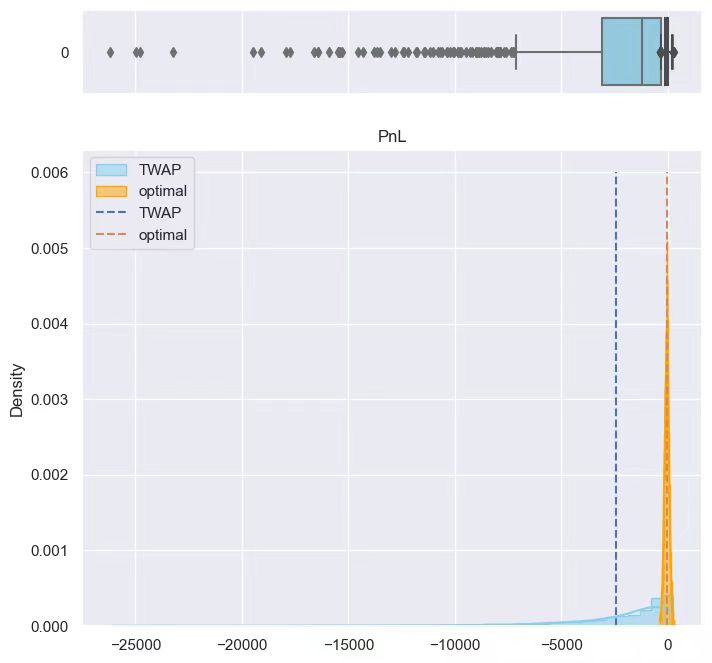

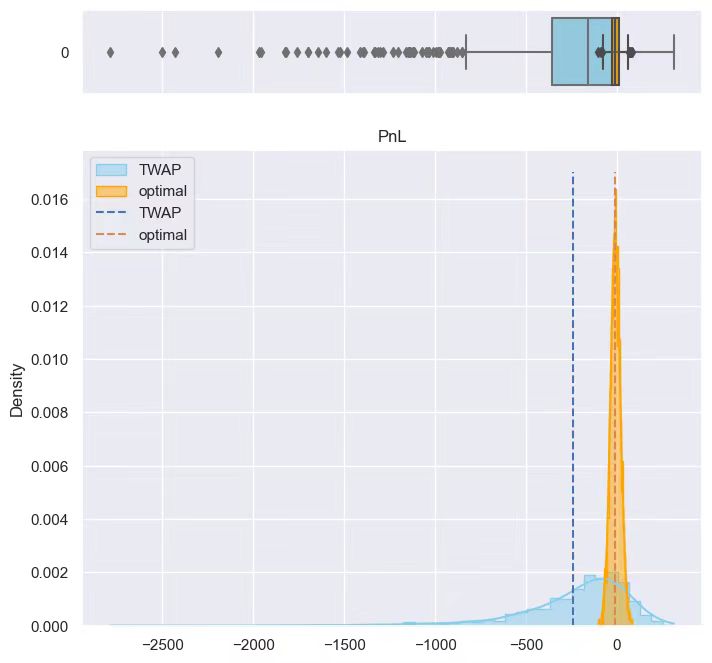

Finally, we stress test the optimal and the TWAP strategies against extreme parameters. While the remaining parameters are held the same as in the benchmark case, the stock volatility is scaled up by ten folds in Scenario 1, the terminal penalty coefficient up by ten folds in Scenario 2, the order fill uncertainty up by a hundred folds in Scenario 3, and lastly in Scenario 4 down by 0.1 hundred folds the temporary cost . Table 2 summarizes the parameters that are stress tested in each scenario and Figure 15 shows the histograms and boxplots of P&Ls at the terminal time under the optimal and the TWAP strategies.

Apparently, in all the scenarios the histograms under optimal strategies are concentrated around zero whereas those under TWAP strategies are much more widely spreading. Also, the sample means under optimal strategies are higher than those of TWAP strategies. We conclude that, even under extreme situations, the optimal strategies outperform TWAP strategies not only in higher averaged P&L but also with lower volatility risk.

| Benchmark | 0.05 | 10 | 0 | 0.002 | 200 | 100000 |

| Scenario 1 (large ) | 0.05 | 10 | 0 | 0.002 | 2000 | 100000 |

| Scenario 2 (large ) | 0.05 | 10 | 0 | 0.002 | 200 | 1000000 |

| Scenario 3 (large ) | 5 | 10 | 0 | 0.002 | 200 | 100000 |

| Scenario 4 (small ) | 0.05 | 0.1 | 0 | 0.002 | 200 | 100000 |

6 Conclusion

In this article, we showed how the broker’s order execution problem under execution risk subject to client’s reservation strategy can be recast as a utility maximization problem. The optimal solution to the utility maximization problem was obtained by solving an associated Riccati differential equation and was presented in feedback form. When execution risk vanishes, the optimal strategies become deterministic and were given in closed form. We showed that trading trajectories subject to the unit IS and the unit TC orders form a basis of an affine structure for trading trajectories under optimal strategies subject to general piece-wise constant reservation strategies. As for general continuous reservation strategies, we proved an approximation and stability theorem for the trading trajectory under the corresponding optimal strategy via the trajectories from piece-wise constant reservation strategies.

Numerical experiments showed that the optimal strategies not only achieve higher expected values but also bear lower variabilities as opposed to those under TWAP strategies. Numerical performance analysis and stress tests confirmed that optimal strategies outperform TWAP strategies, by a wide margin in certain cases. Possible extensions of the framework considered in the paper include (a) a stochastic component to the price evolution reflecting the overall market activity such macroeconomics factors or news; (b) the price impact, rather than permanent, being transient with proper decay kernel. We leave these considerations to a future study.

Acknowledgement

This research is supported by the National Natural Science Foundation of China (Grants No.11971040).

Appendix A Appendix

Proof to Proposition 1

Note that

hence,

Furthermore, note that

in summary,

Proof to Theorem 1

Note that

hence,

Denote

then and are independent standard Brownian motion.

When ,

The optimization problem

is equivalent to

For any admissible , let

where

Denote the value function

where

The integrand of the term is

For some deterministic function and such that , by Ito’s lemma,

hence,

Hence,

where the integrand of the term is

Set the stochastic integral in into zero, we have

The coefficient of is a positive constant

The integrand of the term times is

By completing the squares, we have

Denote

then we have

where and .

We may solve that

where

then we may find that

Denote

We have

Then we may solve

The optimal control is given by

Proof to Theorem 2

When and , , according to Theorem 1, , , , , and

Furthermore, solves the backward ODE

Note that

Integrate on both sides,

Note that now

hence,

Integrate on both sides,

We denote

hence,

Furthermore,

Proof to Lemma 1

Proof to Proposition 2

Proof to Proposition 3

Note that appears as a whole, so WLOG, we may assume that . When the reservation strategy is , the optimal strategy is given by

then

note that , then and , so when , , which represents that the optimal strategy does not contain overshooting. Note that

so when , , which implies that the optimal strategy is a concave function, so

so when

the optimal strategy contains overshooting, and when , the optimal strategy does not contains overshooting. Similarly, when , , which implies that the optimal strategy is a convex function, so

so when

the optimal strategy contains overshooting.

Proof to Proposition 4

It’s crucial to note that the optimal strategy given in Theorem 2 is the solution to the deterministic optimization problem:

Now the objective can be divided into parts, each with a constant RS:

note that if and are fixed,

where

or

In summary,

which implies that is the optimal solution.

Proof to Theorem 3

According to Theorem 2, the optimal strategies and can be given by

and

where are the optimal strategy with respect to reservation strategy and , respectively, hence,

which implies the fact that when , . So we may use the optimal strategy by the piece-wise constant RS to approximate the general RS, with small error

References

- [1] R. Almgren and N. Chriss, “Optimal execution of portfolio transactions,” Journal of Risk, vol. 3, pp. 5–40, 2001.

- [2] O. Guéant, “Target close execution strategies.” [Online]. Available: https://www.oliviergueant.com/uploads/4/3/0/9/4309511/targetclose.pdf

- [3] R. Almgren and N. Chriss, “Value under liquidation,” Risk, vol. 12, no. 12, pp. 61–63, 1999.

- [4] R. F. Almgren, “Optimal execution with nonlinear impact functions and trading-enhanced risk,” Applied Mathematical Finance, vol. 10, no. 1, pp. 1–18, 2003. [Online]. Available: https://doi.org/10.1080/135048602100056

- [5] D. Bertsimas and A. W. Lo, “Optimal control of execution costs,” Journal of Financial Markets, vol. 1, no. 1, pp. 1–50, 1998. [Online]. Available: https://www.sciencedirect.com/science/article/pii/S1386418197000128

- [6] J. Gatheral, “No-dynamic-arbitrage and market impact,” Quantitative finance, vol. 10, no. 7, pp. 749–759, 2010.

- [7] J. Gatheral, A. Schied, and A. Slynko, “Transient linear price impact and fredholm integral equations,” Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, vol. 22, no. 3, pp. 445–474, 2012.

- [8] S. Tse, P. Forsyth, J. Kennedy, and H. Windcliff, “Comparison between the mean-variance optimal and the mean-quadratic-variation optimal trading strategies,” Applied Mathematical Finance, vol. 20, no. 5, pp. 415–449, 2013.

- [9] X. Cheng, M. Di Giacinto, and T.-H. Wang, “Optimal execution with dynamic risk adjustment,” Journal of the Operational Research Society, vol. 70, no. 10, pp. 1662–1677, 2019.

- [10] C. Frei and N. Westray, “Optimal execution of a vwap order: a stochastic control approach,” Mathematical Finance, vol. 25, no. 3, pp. 612–639, 2015.

- [11] Á. Cartea and S. Jaimungal, “A closed-form execution strategy to target volume weighted average price,” SIAM Journal on Financial Mathematics, vol. 7, no. 1, pp. 760–785, 2016.

- [12] O. Guéant and G. Royer, “Vwap execution and guaranteed vwap,” SIAM Journal on Financial Mathematics, vol. 5, no. 1, pp. 445–471, 2014.

- [13] R. Almgren and J. Lorenz, “Adaptive arrival price,” Trading, vol. 2007, no. 1, pp. 59–66, 2007.

- [14] C. Frei and N. Westray, “Optimal execution in hong kong given a market-on-close benchmark,” Quantitative Finance, vol. 18, no. 4, pp. 655–671, 2018.

- [15] X. Cheng, M. Di Giacinto, and T.-H. Wang, “Optimal execution with uncertain order fills in almgren–chriss framework,” Quantitative Finance, vol. 17, no. 1, pp. 55–69, 2017.

- [16] R. Carmona and L. Leal, “Optimal execution with quadratic variation inventories,” SIAM Journal on Financial Mathematics, vol. 14, no. 3, pp. 751–776, 2023.

- [17] R. Carmona and K. Webster, “The self-financing equation in limit order book markets,” Finance and Stochastics, vol. 23, no. 3, pp. 729–759, Jul. 2019.

- [18] A. Mazzolo, “Constraint Ornstein-Uhlenbeck bridges,” Journal of Mathematical Physics, vol. 58, no. 9, p. 093302, 09 2017. [Online]. Available: https://doi.org/10.1063/1.5000077

- [19] O. Guéant, The Financial Mathematics of Market Liquidity: From optimal execution to market making. CRC Press, 2016, vol. 33.