Counterfactuals in factor models

Abstract

We study a new model where the potential outcomes, corresponding to the values of a (possibly continuous) treatment, are linked through common factors. The factors can be estimated using a panel of regressors. We propose a procedure to estimate time-specific and unit-specific average marginal effects in this context. Our approach can be used either with high-dimensional time series or with large panels. It allows for treatment effects heterogenous across time and units and is straightforward to implement since it only relies on principal components analysis and elementary computations. We derive the asymptotic distribution of our estimator of the average marginal effect and highlight its solid finite sample performance through a simulation exercise. The approach can also be used to estimate average counterfactuals or adapted to an instrumental variables setting and we discuss these extensions. Finally, we illustrate our novel methodology through an empirical application on income inequality.

Keywords: counterfactuals, average marginal effects, panel data, factor models, high-dimensional data

JEL codes: C32, C33, C38

1 Introduction

The goal is to infer the causal effect of a possibly continuous treatment variable on an outcome variable in a panel data setting. Let be the potential outcome under treatment status of unit at date . The realized outcome of unit at time is given by . Our main parameters of interest are the unit-specific and time-specific average marginal effects (AME) of the treatment. The unit-specific AME of unit is

where is the derivative of and denotes the expectation over , for fixed formally, . Note that, when we introduce derivatives or probability limits, we implicitly assume that they exist. Similarly, the time-specific AME at date is defined by

where denotes the expectation over , for fixed , formally, We are also interested in the AME over the whole population, that is

Other important parameters such as average counterfactuals and treatment effects are also discussed in the paper.

To estimate the AMEs, we assume that the potential outcomes are related through a set of random factors such that

| (1) |

where is the number of factors, is a vector of nonrandom loadings and is a random error term. We have

| (2) |

where is the derivative of , so that knowledge of and is sufficient to identify . When is continuous, we only observe for each with probability , so that and cannot be estimated from data on . To overcome this issue, we leverage a panel that loads on the factors. That is, there exists (deterministic) loadings and random error terms such that

| (3) |

the factors can then be estimated from this panel using principal components analysis (or any other method such as cross-section averages). The loadings can then be estimated by linear regression of on the estimated factors interacted with powers of and additional controls.

The proposed approach allows for treatment effects heterogenous across and and leverages the very common modelling assumption of factor models. This set-up can model high-dimensional time series when and both (number of variables in the time series) and are large. For instance, in a macroeconomic application, could correspond to the US federal funds rate, while is the unemployment rate and the panel corresponds to the well-known FRED-MD dataset of McCracken & Ng (2016). Another interesting context corresponding to our set-up is that of a large panel. For instance, suppose that we observe a set of countries at dates. On top of the outcome and the treatment, for each country we observe variables at each of the dates. These variables then constitute the panel , with .

Contributions. As mentioned above, we formulate an estimation procedure for , and . Initially, we estimate the factors from the panel using principal components analysis (PCA). Subsequently, we perform a linear regression of on the estimated factors interacted with powers of and additional controls. This approach enables the estimation of and facilitates the recovery of the AMEs through plug-in methods. We establish the asymptotic properties of the estimator for in the high-dimensional time series case, where while can remain fixed. Additionally, we demonstrate the asymptotic normality of the estimators of and of in the large panel case, where . The finite sample performance of the estimators is evaluated through simulations. An empirical application on income inequality using a large panel illustrates our novel methodology.

This paper introduces a comprehensive approach to model counterfactuals using a factor model. While our focus in this work centers on estimating AMEs due to their importance in nonlinear panel data models (Fernández-Val & Weidner, 2018), our methodology is versatile. It readily extends to estimating various average counterfactuals such as , or for fixed , as well as implementing instrumental variables estimation. Section 4 delves into these extensions and provides corresponding estimators. To maintain conciseness, we refrain from explicitly deriving the asymptotic distributions of these additional estimators. However, similar proof techniques to those employed in establishing the asymptotic normality of the estimators of the average marginal effects can be applied.

Related literature. Modeling potential outcomes of a binary treatment using a factor structure is a well-established approach in the literature (Gobillon & Magnac, 2016; Athey et al., 2021; Bai & Ng, 2021; Fan, Masini & Medeiros, 2022). These papers use a factor model for the untreated potential outcome but do not model the “treated” counterfactual. Specifically, Athey et al. (2021); Bai & Ng (2021) delve into the realm of causal matrix completion, employing a panel denoted as . Given the binary nature of the treatment in their study, they are able to observe numerous entries of the panel . By assuming a factor structure on , they successfully recover for all pairs of and by effectively “completing” the matrix using the information from . However, it is crucial to note that this strategy is not applicable in our current study, which involves a continuous treatment. In this scenario, with probability , none of the entries in the matrix for a given treatment level will be observed, making it impossible to successfully complete the matrix (the same type of issues would arise with the approaches of Gobillon & Magnac (2016), Fan, Masini & Medeiros (2022), since we would also almost never observe the untreated potential outcome). To address this challenge, we propose (i) assuming that the factors are shared across all potential outcomes and (ii) leveraging their learnability from the panel .

Another related strand of literature is that of panel data models with interactive fixed effects (Pesaran, 2006; Bai, 2009; Greenaway-McGrevy et al., 2012). In this set-up it is assumed that , where is a set of controls, are nonrandom loadings and is an error term. Similarly to us, some approaches also assume that follows a factor model with as common factors (Pesaran, 2006; Greenaway-McGrevy et al., 2012). Translated to potential outcomes, panel data models with interactive fixed effects assume that Comparing with our model, we see that in our case the effect of directly interacts with the factors. Thanks to that, the treatment effects can be heterogenous across time and units in our framework. Instead, in panel data models with interactive fixed effects, although it is possible to let depend on (this is called the “heterogenous slopes case”, see Pesaran, 2006), one cannot have treatment effects heterogenous across both dimensions. Moreover, since this approach assumes that the regressors follow a factor model, we argue that it is more natural to also assume that the potential outcomes also load on the same factors and that affects the loadings as we do rather than assuming that the effect of on the potential outcomes is just linear. Note also that if one factor is a constant, our model directly generalizes the panel data models with interactive fixed effects of (Pesaran, 2006; Greenaway-McGrevy et al., 2012).

Next, as mentioned earlier, our approach allows us to estimate treatment effects with high-dimensional time series. A leading approach to estimate treatment effects in time series is local projections (Jordà, 2023). Local projection is a linear regression of the outcome on the treatment and some controls and this approach has been extended to high dimensional data (Babii et al., 2022; Adamek et al., 2022). The standard local projection methodology does not allow for time-varying treatment effects. We improve on local projections in this dimension, at the cost of having to assume that the data follows an approximate factor model.

Finally, this paper is related to the literature on characteristics-based factor model (Connor & Linton, 2007; Connor et al., 2012; Fan et al., 2016). This literature considers a large N,T panel and assumes that follows a factor model. The loadings are modelled as nonparametric functions of some time-invariant characteristics . The loadings and factors can they be estimated by either a semiparametric least squares approach or a projection strategy. The present paper differs from this strand of research in at least two respects. First, we consider a causal inference problem with counterfactuals. Second, in our case the loadings are functions of a time-varying variable . Since the approach of the aforementioned papers crucially relies on the fact that the loadings are functions of time-invariant characterustics, we cannot build up on their estimation procedure. For this reason, we developed a new methodology, where the factors are first estimated from the panel . We note that Fan et al. (2016) provide a theory where the loadings are estimated nonparametrically using series. This is in the spirit of our approach, but to simplify the exposition of the current paper, we do not let the number of series terms go to in theory.

Outline. The paper is organized as follows. Section 2 introduces the estimation procedure. Then, we expose the asymptotic theory in Section 3. Extensions are discussed in Section 4. Section 5 contains simulations. The methodology is illustrated through an empirical application in Section 6. Finally, we conclude in Section 7.

Notation. For an integer , we let . For a matrix , its singular value is and is the singular value decomposition of , where is a family of orthonormal vectors of and is a family of orthonormal vectors of . The operator norm is and the Euclidian norm is . For an integer , and are, respectively, the vectors with all coefficients equal to 0 and 1. Moreover, is the identity matrix of size . For integers and , and are, respectively, the matrices with all coefficients equal to 0 and 1. For a random variable , we let and , when the latter quantities exist.

2 Estimation

In this paper, we estimate the factor by principal components analysis (PCA) applied to the matrix X such that . Note that (3) becomes

in matrix form, where is , is and is the matrix such that . Formally, we first obtain an estimate of applying to one of the estimators of the number of factors available in the literature (Bai & Ng, 2002; Onatski, 2010; Ahn & Horenstein, 2013; Bai & Ng, 2019; Fan, Guo & Zheng, 2022, see for instance). Then, we let the columns of be the eigenvectors corresponding to the leading eigenvalues of . The estimate of corresponds to the colmun of . We note that an alternative estimation procedure for the factors would be to use cross-section averages as in Pesaran (2006).

Once, we obtained an estimate of the factors, the idea is to leverage the fact that to estimate . To simplify estimation, we assume that

| (4) |

where are known non constant functions of and are unknown and need to be estimated. For instance, one can pick and , which yields , allowing for nonlinearity of the effect of on . We note that is identified without imposing (4) and the latter is only useful for estimation. In the spirit of the literature on series estimation, it would be possible to let grow with the sample size and to assume instead that is only approximated by . We do not do so in the present paper in order to simplify the exposition and the methodology.

We obtain

where . Thanks to this, we could estimate by regressing linearly on and . Such an approach would only be valid under the exogeneity assumption . This assumption may not always be credible. To weaken it, we include observed controls , such that , with and . The controls can belong to as is standard in panel data models with interactive fixed effects where the variables used to estimate the factors also act as controls (Pesaran, 2006; Greenaway-McGrevy et al., 2012). The second step regression model can then be written

where and

is . A natural estimator of is then the linear regression of on

| (5) |

a -dimensional vector. Formally,

| (6) |

Note that, by (2) and (4), we have , where

is and is the derivative of . By plug-in the final estimator of is

| (7) |

where

| (8) |

is a -dimensional vector. When is large, we can also estimate by

| (9) |

where

is an estimator of To conclude, we estimate by the sample average of the , that is

| (10) |

Algorithm 1 summarizes the estimation procedure.

3 Theory

We place ourselves in an asymptotic regime where . When we derive the properties of and , we additionally assume that . The number of factors is fixed with . It would be possible to let it grow and/or allow for nonstrong factors, see, for instance, Beyhum & Gautier (2019, 2023); Freeman & Weidner (2023); Bai & Ng (2023). In this section, as is standard in the literature, we suppose that we know , that is almost surely. Our results would nevertheless stay valid as long as .

3.1 Assumptions

We make different types of assumptions. First, there are some standard assumptions for factor models on and . These assumptions correspond to that made in Bai & Ng (2023) and are therefore not new. These are stated in Section 3.1.1. Additional assumptions, not directly imposed on the factor model consisting in and are then outlined in Section 3.1.2

3.1.1 Standard assumptions on

We let and

Assumption 1

Let not depending on and define . The following holds:

-

(i)

Mean independence: a.s.

-

(ii)

Weak (cross-sectional and serial) correlation in the errors.

-

(a)

-

(b)

For all , . For all , .

-

(c)

For all , . For all , .

-

(d)

-

(a)

Assumption 2

-

(i)

, .

-

(ii)

, .

-

(iii)

The eigenvalues of are distinct.

Assumption 3

For each t, (i) , (ii) , for each i, (iii) , (iv) , (v)

3.1.2 New assumptions

Let , with . The next assumption allows us to show asymptotic normality of .

Assumption 4

Uniformly in , the following holds:

-

(i)

For all , is differentiable.

-

(ii)

There exists a constant independent of and such that, for all , and almost surely.

-

(iii)

For all ,

-

(a)

,

-

(b)

and ,

-

(c)

and

-

(d)

-

(e)

-

(f)

-

(a)

-

(iv)

.

-

(v)

-

(a)

,

-

(b)

-

(c)

-

(a)

Assumption 4 (iii) contains mild regularity conditions. The rate condition in Assumption 4 (iv) is the same as the one used in the literature on factor-augmented regression to show that the error made in estimating the factors is asymptotically negligible (Bai & Ng, 2006). Assumption 4 (v) states that certain law of large numbers and central limit theorems hold. Let

where

We leverage the next assumption only to derive the asymptotic distribution of .

Assumption 5

The following holds:

-

(i)

For all ,

-

(a)

,

-

(b)

-

(a)

-

(ii)

.

-

(iii)

-

(a)

,

-

(b)

,

-

(c)

and are independent.

-

(a)

Assumption 6 (ii) can only be satisfied when both and go to infinity. If consists of variables for each unit, we have and the condition simplifies to . Let

The next assumption is only used to establish asymptotic normality of .

Assumption 6

The following holds:

-

(i)

For all ,

-

(a)

,

-

(b)

-

(c)

-

(a)

-

(ii)

.

-

(iii)

-

(a)

,

-

(b)

,

-

(c)

and are independent.

-

(a)

3.2 Asymptotic distributions

To state the asymptotic distribution of our estimators, we need more notation. Let

be the diagonal matrix consisting in the ordered square-root of the eigenvalues of . Moreover, we introduce , where consists in the eigenvectors of the matrix . We also let be the matrix defined by

Next, we define the matrix whose diagonal is the singular value of and introduce We also denote by the matrix defined as but replacing the matrices by . Finally, define the vector

We show in the Appendix that, under our assumptions, and that , and estimate consistently , and , respectively. This allows to derive the asymptotic distributions of our estimators.

The following theorems give the asymptotic distributions of our estimators. First, considering an asymptotic regime with , we have the following result.

Next, we consider an asymptotic regime with all jointly going to infinity.

Theorem 2

In Theorem 2, we assume that just to have a well defined limiting variance. Note that can be equal to , so that can be negligible with respect to .

3.3 Estimation of the variance

Let us now discuss estimation of and . This is crucial to use the theorems for inference.

Estimation of . We can estimate by

It remains to estimate First, we can define where . There are different potential estimators of . If the are not serially correlated, one can use the “standard” heteroscedasticity consistent (HC) estimator:

However, in case of autocorrelation in (which may be caused by serial correlation of the factors), one should use an heteroscedasticity and autocorrelation consistent (HAC) estimator à la Newey & West (1987):

where , is a kernel function and is a bandwidth. The final estimate of is given by

where is either or .111An alternative approach is to use fixed-b critical values as in Lazarus et al. (2018). This would require working out the asymptotic distribution of the test statistic under fixed-b asymptotic, which seems challenging in the present context.

Estimation of . Our estimator of is the matrix . We also let be our estimator of . These are the standard PCA-based estimators. The estimators of , and are then respectively,

Let us denote by

the estimator of .222This estimator will be consistent when are uncorrelated across . This will happen if the are uncorrelated across and independent of the loadings. This is an assumption that could be considered natural in factor models, and the results should not be too sensitive to mild violations of this assumption. To avoid such an assumption, one could use a cross-section consistent estimator as in Bai & Ng (2006). We can estimate by

The final estimator of is then

Estimation of . The variable can be estimated by

where

A natural estimator of is

where estimates , and is either

or, in case of serial correlation,

where , is a kernel function and is a bandwidth.

4 Extensions

In this section, we discuss extensions of our approach to other target parameters and IV estimation. This showcases the flexibility of our modelling strategy.

Average counterfactuals. Let us now discuss other interesting parameters. First, one may want to know what would be the average outcome if the treatment was fixed at . The following parameters answer this question:

The mappings , and are functional parameters and they can be estimated as follows:

where

The mappings , and can also be differentiated to obtain average marginal effects at fixed d and also integrated (possibly after differentiation) with respect to some relevant distibution of .

IV estimation. Suppose now that is endogenous even after including the controls, that is for some . A remedy to this problem is to rely on an IV . Let us define To estimate one can then use the IV estimator

The estimators of the other parameters of interest can then be obtained by plug-in. This approach relies on the exogeneity assumption: .

5 Simulations

In this section, we provide a Monte Carlo study which sheds light on the finite sample performance of our proposed inference procedures. We start by analyzing in Section 5.1 before studying and in Section 5.2.

5.1 Single unit

To analyze , we restrict ourselves to a sample with a single unit , that is . We consider and . We generate samples with factors. The loadings are i.i.d. such that . The factors are generated as for and , where are i.i.d. . The stationary distribution of is , we initialize as such. The quantity controls the level of serial correlation and we let . The idiosyncratic components are i.i.d. . We have two controls, . We let where . The treatment is such that , where . The outcome is generated as

where is i.i.d. . We estimate for , which is equal to when and when . We use the growth ratio estimator of Ahn & Horenstein (2013) to estimate the number of factors. Following Section 3.3, we consider three possible estimators of the covariance matrix . First, there is the standard estimator , second, there is a HAC estimator with quadratic spectral kernel and third a HAC estimator with Parzen kernel. For the HAC estimators, we pick the bandwidth equal to , which corresponds to the recommendation of Lazarus et al. (2018).333The choice in Lazarus et al. (2018) is for linear regression and fixed-b critical values, that is a different context than ours. For each estimator of the covariance matrix, we then construct 95% confidence intervals based on the Gaussian approximation of Theorem 1.

Tables LABEL:tab.singJ1 and LABEL:tab.singJ2 present the results for and , respectively. These are averages over 8,000 replications. We report the bias, variance, mean-squared error (MSE) of our estimator along with the average radius of confidence intervals built using the three different estimators of the covariance matrix and the Gaussian approximation of Theorem 1. We see that our estimator has low bias, variance and MSE, although they worsen when or the level of autocorrelation in the factors increase. The coverage of the confidence intervals is close to nominal when the factors are not serially correlated . In this case, the differences in radius and coverage between the three types of confidence intervals is minimal. When the coverage worsens for all three types of CI, but the decrease is much steeper for the standard CI not taking into account time series dependence. This suggests than one should indeed use HAC estimators of the covariance matrix in practice, since they greatly improve the results when there is autocorrelation at little cost in the absence of the latter. The CIs based on the Quadratic Spectral and the Parzen Kernel seem to have similar performance.

5.2 Large panel

Now, we study and . To do so we consider a panel data with units and dates. We set , which mimicks the case where the panel consists in auxiliary variables (corresponding to and ) for each unit at each date . We generate the factors and idiosyncratic errors as in Section 5.1. There are two controls . We let where and . The treatment is such that , where is i.i.d. . The outcome is generated as

where is i.i.d. .

First, we estimate for . It is equal to when and when . The results are presented in Tables 1 and 2 and are, again, averages over 8,000 replications. The variance is not affected by autocorrelation in the factors and therefore we only report 95% confidence intervals built using and Gaussian approximation. The results confirm that the performance of the estimator is indeed not affected by autocorrelation. The bias, variance and MSE of the estimator is again low and the coverage of the confidence intervals close to nominal.

| Bias | Var | MSE | Av. R. CI | Cov. CI | ||

| Design 1: , | ||||||

| 50 | 50 | -0.0093 | 0.0203 | 0.0204 | 0.2640 | 0.93 |

| 50 | 100 | -0.0081 | 0.0199 | 0.0200 | 0.2649 | 0.93 |

| 50 | 200 | -0.0087 | 0.0203 | 0.0204 | 0.2659 | 0.94 |

| 100 | 50 | -0.0029 | 0.0103 | 0.0103 | 0.1882 | 0.94 |

| 100 | 100 | -0.0030 | 0.0102 | 0.0102 | 0.1893 | 0.94 |

| 100 | 200 | -0.0043 | 0.0098 | 0.0098 | 0.1901 | 0.95 |

| 200 | 50 | 0.0003 | 0.0051 | 0.0051 | 0.1337 | 0.94 |

| 200 | 100 | -0.0030 | 0.0051 | 0.0051 | 0.1349 | 0.94 |

| 200 | 200 | -0.0010 | 0.0051 | 0.0051 | 0.1359 | 0.95 |

| Design 2: , | ||||||

| 50 | 50 | -0.0094 | 0.0203 | 0.0204 | 0.2638 | 0.93 |

| 50 | 100 | -0.0080 | 0.0200 | 0.0200 | 0.2647 | 0.93 |

| 50 | 200 | -0.0087 | 0.0204 | 0.0204 | 0.2658 | 0.93 |

| 100 | 50 | -0.0029 | 0.0103 | 0.0103 | 0.1881 | 0.94 |

| 100 | 100 | -0.0032 | 0.0102 | 0.0102 | 0.1892 | 0.94 |

| 100 | 200 | -0.0042 | 0.0098 | 0.0099 | 0.1901 | 0.94 |

| 200 | 50 | 0.0003 | 0.0051 | 0.0051 | 0.1336 | 0.94 |

| 200 | 100 | -0.0031 | 0.0051 | 0.0051 | 0.1348 | 0.94 |

| 200 | 200 | -0.0011 | 0.0051 | 0.0051 | 0.1359 | 0.94 |

-

Note: “Av. R. CI” (respectively “Cov. CI”) stand for the average radius (respectively, coverage) of the 95% confidence intervals.

| Bias | Var | MSE | Av. R. CI | Cov. CI | ||

| Design 1: , | ||||||

| 50 | 50 | -0.0044 | 0.2771 | 0.2771 | 0.8814 | 0.94 |

| 50 | 100 | -0.0084 | 0.2904 | 0.2905 | 0.8745 | 0.94 |

| 50 | 200 | -0.0101 | 0.2807 | 0.2808 | 0.8761 | 0.94 |

| 100 | 50 | -0.0069 | 0.1374 | 0.1374 | 0.6229 | 0.94 |

| 100 | 100 | -0.0021 | 0.1356 | 0.1356 | 0.6162 | 0.94 |

| 100 | 200 | -0.0008 | 0.1431 | 0.1431 | 0.6179 | 0.94 |

| 200 | 50 | -0.0024 | 0.0677 | 0.0677 | 0.4361 | 0.94 |

| 200 | 100 | -0.0007 | 0.0668 | 0.0668 | 0.4383 | 0.95 |

| 200 | 200 | -0.0042 | 0.0747 | 0.0747 | 0.4459 | 0.94 |

| Design 2: , | ||||||

| 50 | 50 | -0.0047 | 0.2763 | 0.2763 | 0.8813 | 0.94 |

| 50 | 100 | -0.0084 | 0.2912 | 0.2913 | 0.8746 | 0.94 |

| 50 | 200 | -0.0103 | 0.2816 | 0.2817 | 0.8760 | 0.94 |

| 100 | 50 | -0.0073 | 0.1364 | 0.1364 | 0.6228 | 0.94 |

| 100 | 100 | -0.0026 | 0.1350 | 0.1350 | 0.6160 | 0.94 |

| 100 | 200 | -0.0008 | 0.1429 | 0.1429 | 0.6179 | 0.94 |

| 200 | 50 | -0.0026 | 0.0677 | 0.0677 | 0.4359 | 0.94 |

| 200 | 100 | -0.0011 | 0.0668 | 0.0668 | 0.4382 | 0.95 |

| 200 | 200 | -0.0041 | 0.0742 | 0.0742 | 0.4458 | 0.94 |

-

Note: “Av. R. CI” (respectively “Cov. CI”) stand for the average radius (respectively, coverage) of the 95% confidence intervals.

Then we estimate . In this design, we have when and when . The results are displayed in Tables LABEL:tab.panelJ1 and LABEL:tab.panelJ2 and are, again, averages over 8,000 replications. As in Section 5.1, we find that aucocorrelation or increasing worsen the results but HAC estimators of the covariance matrix can mitigate the decrease in coverage of the CIs.

6 Empirical application

To illustrate our methodology, we revisit Voigtländer (2014). This paper considers a panel data with sectors of the U.S. economy observed yearly from 1958 to 2005, that is dates. It investigates if increasing skill intensity of the economy is a cause of increasing wage inequality in the United States. To this end, Voigtländer (2014) builds an input skill intensity measure and evaluate its effect on , the logarithm of the ratio of the average wage of low-skilled workers in sector at time , , over the average wage of high-skilled workers in that sector at the same date. The goal is to assess if skill intensity in a given sector causes wage inequality in that sector.

This data has recently been analyzed by Yin et al. (2021) and Juodis (2022) using common correlated effects approaches. We use the dataset of Yin et al. (2021) available at https://www.tandfonline.com/doi/abs/10.1080/07350015.2019.1623044?casa_token=Jmzhpt-330cAAAAA:MrhnmhaKnNDF1uWAl6jwO09Nz6S8Mx1oONJ7OHWmdLEagE0TeZ8pL60jSYL97XcXRjGwPaqYpkY, it corresponds to a balanced version of the original data of Voigtländer (2014), where some sectors with missing data have been deleted.

We let and . For the panel we use 7 variables for each sector at each date including the logarithm of the ratio of high skilled workers over low-skilled workers, capital equipment per worker. These corresponds to the control variables used in Yin et al. (2021) and Juodis (2022). This leads us to in the panel . The control variables correspond to these variables along with a constant.

Table 3 reports the estimates and confidence intervals of for . The various confidence intervals are built as in the simulations and the growth ratio estimator finds one factor. The estimates and associated confidence intervals are not very sensitive to the choice of . The results are significant and the coefficient is negative: increasing skill intensity increases wage inequality. Our estimates are much more negative than that of Yin et al. (2021) (ranging from to ) and Juodis (2022) (ranging from to ).

| 1 | 2 | 3 | |

|---|---|---|---|

| -1.71 | -1.78 | -1.75 | |

| CI | [-2.08, -1.34] | [-2.15,-1.41] | [-2.18,-1.31] |

| CI QS ker. | [-2.09, -1.33] | [-2.15,-1.41] | [-2.38,-1.11] |

| CI Parzen ker. | [-2.09, -1.33] | [-2.15,-1.41] | [-2.31,-1.18] |

-

Note: ‘ “CI”, “CI QS ker.” and “CI Parzen ker.”’ stand for the 95% confidence intervals computed using, respectively, the standard estimator, the HAC estimator with quadratic spectral kernel and the HAC estimator with Parzen kernel of the covariance matrix.

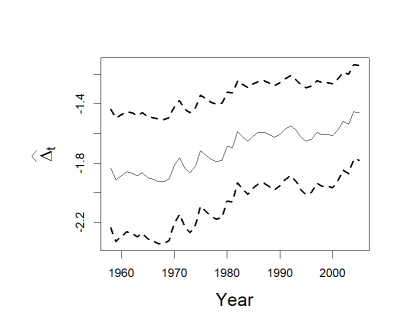

Next, we explore the time trend of the time-specific average marginal effect . In Figure 1, we plot along with its (pointwise) confidence intervals estimated with . We see that the average marginal effect of skill intensity tends to increase over time, suggesting that the wage premium of skilled workers (for a fixed value of the skill intensity measure) is decreasing with time.

7 Conclusion

In this paper, we present a novel factor model for potential outcomes, outlining the methodology for estimating various key parameters within the model. Notably, our approach accommodates both temporal and unit-specific variations in treatment effects. We further establish the asymptotic distribution for several pivotal estimators, paving the way for statistical inference. To enhance the simplicity of inference procedures, the development of a bootstrap technique for constructing confidence intervals across a broad spectrum of estimators in our model would be beneficial. This avenue remains open for exploration in future research endeavors. Another interesting extension is the case where the controls are high-dimensional and lasso is used for estimation. Fan, Masini & Medeiros (2022) demonstrates the importance of such high-dimensional controls in counterfactual analysis with factor models and a binary treatment.

Acknowledgments

Jad Beyhum gratefully acknowledges financial support from the Research Fund KU Leuven through the grant STG/23/014. He thanks Andrii Babii, Geert Dhaene and Jonas Striaukas for useful comments.

References

- (1)

- Adamek et al. (2022) Adamek, R., Smeekes, S. & Wilms, I. (2022), ‘Local projection inference in high dimensions’, arXiv preprint arXiv:2209.03218 .

- Ahn & Horenstein (2013) Ahn, S. C. & Horenstein, A. R. (2013), ‘Eigenvalue ratio test for the number of factors’, Econometrica 81(3), 1203–1227.

- Athey et al. (2021) Athey, S., Bayati, M., Doudchenko, N., Imbens, G. & Khosravi, K. (2021), ‘Matrix completion methods for causal panel data models’, Journal of the American Statistical Association 116(536), 1716–1730.

- Babii et al. (2022) Babii, A., Ghysels, E. & Striaukas, J. (2022), ‘High-dimensional granger causality tests with an application to vix and news’, Journal of Financial Econometrics p. nbac023.

- Bai (2009) Bai, J. (2009), ‘Panel data models with interactive fixed effects’, Econometrica 77(4), 1229–1279.

- Bai & Ng (2002) Bai, J. & Ng, S. (2002), ‘Determining the number of factors in approximate factor models’, Econometrica 70(1), 191–221.

- Bai & Ng (2006) Bai, J. & Ng, S. (2006), ‘Confidence intervals for diffusion index forecasts and inference for factor-augmented regressions’, Econometrica 74(4), 1133–1150.

- Bai & Ng (2019) Bai, J. & Ng, S. (2019), ‘Rank regularized estimation of approximate factor models’, Journal of Econometrics 212(1), 78–96.

- Bai & Ng (2021) Bai, J. & Ng, S. (2021), ‘Matrix completion, counterfactuals, and factor analysis of missing data’, Journal of the American Statistical Association 116(536), 1746–1763.

- Bai & Ng (2023) Bai, J. & Ng, S. (2023), ‘Approximate factor models with weaker loadings’, Journal of Econometrics .

- Beyhum & Gautier (2019) Beyhum, J. & Gautier, E. (2019), ‘Square-root nuclear norm penalized estimator for panel data models with approximately low-rank unobserved heterogeneity’, arXiv preprint arXiv:1904.09192 .

- Beyhum & Gautier (2023) Beyhum, J. & Gautier, E. (2023), ‘Factor and factor loading augmented estimators for panel regression with possibly nonstrong factors’, Journal of Business & Economic Statistics 41(1), 270–281.

- Connor et al. (2012) Connor, G., Hagmann, M. & Linton, O. (2012), ‘Efficient semiparametric estimation of the fama–french model and extensions’, Econometrica 80(2), 713–754.

- Connor & Linton (2007) Connor, G. & Linton, O. (2007), ‘Semiparametric estimation of a characteristic-based factor model of common stock returns’, Journal of Empirical Finance 14(5), 694–717.

- Fan, Guo & Zheng (2022) Fan, J., Guo, J. & Zheng, S. (2022), ‘Estimating number of factors by adjusted eigenvalues thresholding’, Journal of the American Statistical Association 117(538), 852–861.

- Fan et al. (2016) Fan, J., Liao, Y. & Wang, W. (2016), ‘Projected principal component analysis in factor models’, Annals of statistics 44(1), 219.

- Fan, Masini & Medeiros (2022) Fan, J., Masini, R. & Medeiros, M. C. (2022), ‘Do we exploit all information for counterfactual analysis? benefits of factor models and idiosyncratic correction’, Journal of the American Statistical Association 117(538), 574–590.

- Fernández-Val & Weidner (2018) Fernández-Val, I. & Weidner, M. (2018), ‘Fixed effects estimation of large-t panel data models’, Annual Review of Economics 10, 109–138.

- Freeman & Weidner (2023) Freeman, H. & Weidner, M. (2023), ‘Linear panel regressions with two-way unobserved heterogeneity’, Journal of Econometrics 237(1), 105498.

- Gobillon & Magnac (2016) Gobillon, L. & Magnac, T. (2016), ‘Regional policy evaluation: Interactive fixed effects and synthetic controls’, Review of Economics and Statistics 98(3), 535–551.

- Greenaway-McGrevy et al. (2012) Greenaway-McGrevy, R., Han, C. & Sul, D. (2012), ‘Asymptotic distribution of factor augmented estimators for panel regression’, Journal of Econometrics 169(1), 48–53.

- Jordà (2023) Jordà, Ò. (2023), ‘Local projections for applied economics’, Annual Review of Economics 15, 607–631.

- Juodis (2022) Juodis, A. (2022), ‘A regularization approach to common correlated effects estimation’, Journal of Applied Econometrics 37(4), 788–810.

- Lazarus et al. (2018) Lazarus, E., Lewis, D. J., Stock, J. H. & Watson, M. W. (2018), ‘Har inference: Recommendations for practice’, Journal of Business & Economic Statistics 36(4), 541–559.

- McCracken & Ng (2016) McCracken, M. W. & Ng, S. (2016), ‘FRED-MD: a monthly database for macroeconomic research’, Journal of Business & Economic Statistics 34(4), 574–589.

- Newey & West (1987) Newey, W. K. & West, K. D. (1987), ‘A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix’, Econometrica 55(3), 703–708.

- Onatski (2010) Onatski, A. (2010), ‘Determining the number of factors from empirical distribution of eigenvalues’, Review of Economics and Statistics 92(4), 1004–1016.

- Pesaran (2006) Pesaran, M. H. (2006), ‘Estimation and inference in large heterogeneous panels with a multifactor error structure’, Econometrica 74(4), 967–1012.

- Voigtländer (2014) Voigtländer, N. (2014), ‘Skill bias magnified: Intersectoral linkages and white-collar labor demand in us manufacturing’, Review of Economics and Statistics 96(3), 495–513.

- Yin et al. (2021) Yin, S.-y., Liu, C.-a. & Lin, C.-C. (2021), ‘Focused information criterion and model averaging for large panels with a multifactor error structure’, Journal of Business & Economic Statistics 39(1), 54–68.

Appendix

Appendix A Preliminaries

We introduce further notation which will prove useful in the current section of the appendix. Let

be matrices of true and estimated regressors. We also define , and . The following equality, corresponding to (13) in Bai & Ng (2023),

| (11) |

will be useful in the proofs. Recall also that .

Appendix B Useful lemmas on the factors

We prove some useful lemmas on the estimated factors.

Proof. Statements (i), (ii), (iii), (iv) and (vi) correspond to the results of Proposition 1 and Lemmas 1, 2 and A.1 in Bai & Ng (2023). Statement (v) is shown in the proof of Lemma 3(i) in Bai & Ng (2023). Finally, (vii) is a direct consequence of (iv).

Proof. Let us first show (i). The result follows from

where the second inequality follows from Assumption 4 (ii) and we used Lemma B.1 (i). The proof of (ii) is similar to that of (i), and is, therefore, omitted.

Then, we consider (iii). First, notice that

| (12) |

where for . By (11), we have

| (13) |

Let us now bound each term. We have first

| (14) | ||||

where we used Lemma B.1 (v) and (vi) and Assumptions 1 (ii) (d), 2 (i), and 4 (iii) (a), (b) to obtain the bounds in (14). By (13), (14) and Lemma B.1 (ii), we get The result then follows from (12).

Next, we show (iv). First notice that

| (15) | ||||

where . By (11), it holds that

| (16) |

We bound each term. It holds that

| (17) | ||||

where we used Lemma B.1 (v) and (vi) and Assumptions 1 (ii) (d), 2 (i), and 4 (iii) (c), (d) to obtain the bounds in (17). By (16), (17) and Lemma B.1 (ii), we get

| (18) |

Let us now bound. By (11), we have

| (19) |

We bound each term.

| (20) | ||||

where we used Lemma B.1 (v) and (vi) and Assumptions 1 (ii) (d), 2 (i), and 4 (iii) (b), (c) to obtain the bounds in (20). By (19), (20) and Lemma B.1 (ii), we get

| (21) |

The result then follows from (18), (21) and (15). The proof of (v) is a direct consequence of statements (i) and (iv) and it is therefore omitted.

Then, we prove (vi). First, notice that

| (22) | ||||

where . By (11), we have

| (23) |

Let us bound each term:

| (24) | ||||

where we used Lemma B.1 (v) and (vi) and Assumptions 1 (ii) (d), 2 (i), and 4 (iii) (e), (f) to obtain the bounds in (24). By (23), (24) and Lemma B.1 (ii), we get The result then follows from (22). Statement (vii) is a direct consequence of (i) and its proof is therefore omitted.

Appendix C Proof of Theorem 1

Note that Plugging this in (6), we obtain

This leads to

where we used that by Lemma B.1 (vii) and B.2 (v) and (vii) and Assumption 4 (v). Using Lemmas B.1 (vii) and B.2 (vi) and (vii), we also have

which yields

| (25) |

Next, recall that This yields

| (26) | ||||

By Lemma B.2 (iii) and the fact that (from (25) and Assumption 4 (iv) and (v) (a), (b)), it holds that

| (27) | ||||

By (25), (26) and (27), we get

| (28) | ||||

where in the second equality, we used Lemma B.1 (vii) and Assumption 4 (v) (c). By Assumption 4 (d), we obtain and the asymptotic distribution follows from Assumption 4 (v) (b).

Appendix D Proof of Theorem 2

Proof of (i)

From , we have

| (29) | ||||

Notice that, by (25),

| (30) | ||||

where we used Assumption 5 (i) (a) and (ii). Then, remark that

| (31) |

by Lemma B.2 (viii) and (25). Next, by Lemma B.2 (viii) and Assumption 5 (i) (b) and (ii), we have

| (32) | ||||

Combining (29), (30), (31), (32), we obtain

The asymptotic distribution is a consequence of Assumption 5 (iii).

Proof of (ii)

From , we have

| (33) | ||||

where we used (28) (which holds uniformly in i since Assumption 4 is imposed uniformly). By Assumption 6 (i) (a), it holds that

| (34) |

Moreover, note that

| (35) | ||||

where we used Assumption4 (i) (b). Additionally, remark that, for all , we have

where we used Assumption 6 (i) (c). By definition of and , this yields

| (36) |

Combining (33), (34), (35) and (36), and using Assumption 4 (ii), we obtain

The asymptotic distribution then follows from Assumption 6 (iii).