Displaying risk in mergers: a diagrammatic approach for exchange ratio determination

Abstract

This article extends, in a stochastic setting, previous results in the determination of feasible exchange ratios for merging companies. A first outcome is that shareholders of the companies involved in the merging process face both an upper and a lower bounds for acceptable exchange ratios. Secondly, in order for the improved ‘bargaining region’ to be intelligibly displayed, the diagrammatic approach developed by Kulpa is exploited.

Keywords— Mergers and acquisitions, exchange ratio determination, synergy, risk-adjusted performance, diagrammatic representation

1 Introduction, literature review and motivation

Mergers and acquisitions have been, and still are a widely studied topic in financial literature under both a theoretical and an empirical point of view. A concise summary of contributions in this field is virtually impossible; recent attempts are King et al. [1] and Risberg et al. [2].

Companies merge for various reasons, but with a unique goal: the creation of synergy, that is a, hopefully positive, change in the behavior of the equity of the resulting company (here denoted by ) when compared to those of the equities of the preexisting ones, namely the acquiring, , and the acquired, or target, .

Relevant contributions to the financial evaluation of synergies are due to Gupta and Gerchak [3], Leland [4], and are broadly summarized in Chapter 15 of Damodaran [5].

This paper focuses on the impact of synergy for shareholders of the merging companies and extends, in a stochastic environment, known results (Larson and Gonedes, [6] and Yagil [7]; in what follows, this approach is referred to as LG-Y).

The attention of this article resides on stock-for-stock agreements, where shareholders of the target company swap, if the merger is finalized, stocks of company for each share of company they own. Shareholders of the acquiring company receive, instead, one stock of for each share they own. Stockholders of either company or become shareholders of company .

A topic that has been almost totally neglected in financial research is the fair determination of the exchange ratio (ER) . In a deterministic framework, the LG-Y setting is the only known contributions. Here, companies are evaluated using the the dividend discount model (Gordon and Shapiro, [8]). The result is the explicit determination of the bargaining region (BR), that is the range for exchange ratios that do not reduce shareholders’ wealth.

A generalization with a dynamical extension of the LG-Y setting is due to Cigola and Modesti [9] while a recent contribution, that encompasses a number of accounting observations, is in Taliento [10].

As noted by Amihud and Lev [11], risk reduction can be a driver pushing companies to merge. An attempt to introduce risk in the determination of the exchange ratio has been proposed by Moretto and Rossi [12]. This contribution, though, does not identify a BR; it provides, instead, a unique risk-corrected ER.

More recently, Toll and Hering [13] analyze, in a stochastic context, the effects of a merger for shareholders by means of expected utility theory.

Entering the realm of randomness in financial markets requires a solid theory for risk measures. The fundamental contribution in this context is provided by Artzner et al. [14]; here riskiness is measured by means of functions that translate random variables into a cash amount that, if positive, has to be paired to the risk in order to make it acceptable.

In this contribution, no specific risk measure is chosen. Our analysis starts by mimicking results in LG-Y replacing the deterministic result with expected values of random stock prices and measures changes in risk the merger grants to stockholders.

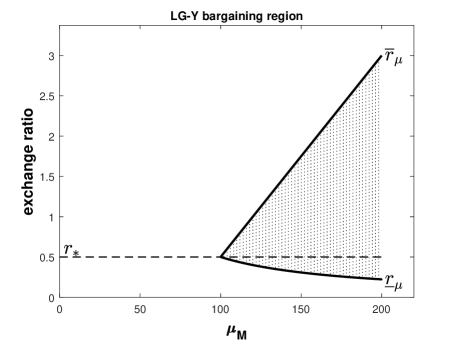

In the LG-Y setting, in terms of ER determination shareholders of the acquiring and acquired companies have clear-cut and opposite interests: the larger , the larger the stake of company ’s shareholders own, and the larger the portion of synergy they receive. This is the reason why stockholders of company aim at keeping as small as possible. Our contribution shows that, when a risk measure is introduced, something completely different and less straightforward occurs.

As a matter of fact, imposing bounds on expected values and risk measure leads to more accurate and realistic BRs.

In finance, nothing comes for free. Adding a second dimension embeds into the stochastic framework a drawback: BRs cannot be easily depicted, unless some appropriate methodology is applied. Luckily, the ‘diagrammatic’ representation of intervals developed by Kulpa (see [15], [16], and [17]) permits to transform intervals into points on a two-dimension Cartesian plane and solve the issue.

The paper is organized as follows: Section 2 describes the theoretical framework on which the extension in a stochastic fashion of the LG-Y model abides. Section 3 introduces Kulpa’s diagrammatic representation, translates BRs in legible and easy-to-understand plots, and provides some financial insights. Section 4 concludes

2 Arithmetic for merger agreements

2.1 The deterministic benchmark: Larson and Gonedes, and Yagil setting

For the reader’s sake, in this subsection we summarize the main findings of contributions from Larson and Gonedes, and Yagil (LG-Y from now on). Their approach is deterministic and highlights conditions under which shareholders of the acquiring () and acquired () companies are better off once the merger agreement is settled, leading to the birth to the resulting company . The LG-Y setting assumes that, in a stock-for-stock agreement, each stock of company translates into one stock of company while each stock of company becomes stocks of company , where is the exchange ratio (ER).

Stock-for-stock refers to the exchange of stocks of the resulting with stocks of the acquired company at a predetermined conversion rate. Companies that pay for their acquisitions with stock share both the value and the risks of the transaction with the shareholders of the company they acquire. Nevertheless, as mentioned above, the LG-Y settingis purely deterministic, and stockholders share only the value of the transaction.

Let , , and be, respectively, the stock price, the number of outstanding stocks, and the equity value for companies . The number of ’s outstanding stocks is

A merger creates some positive synergy when the equity value of corresponds at least to the sum of equity values of and :

A relevant quantity is ratio

| (1) |

which represents the relative value of a stock of company when compared with the value of one stock of company .

The LG-Y approach provides an explicit expression for the bounds of the bargaining region (BR), that is the interval containing all ERs for which shareholders of companies and simultaneously experience an increase in their equity values and, thus, might accept to conclude the merger.

Existence and magnitude of this interval depend on synergy created by the merger.

Company ’s stockholders enjoy a benefit from this agreement when the price of stocks they own after the merger is equal, at least, to the price of stocks they previously owned, that is

Simple algebra yields an upper bound for :

| (2) |

Condition (2) denotes the largest ER company ’s shareholders accept.

Company’s shareholders, instead, obtain an increment in their wealth when

This condition is equivalent to a lower bound for :

| (3) |

Bounds (2) and (3) depend on the equity value of . Further, it is immediate to see that, if , then . In this case, the above bounds identify set

| (4) |

The absence of synergy (i.e. ) shrinks set

into a singleton: . This expression highlights the importance of ratio (1).

2.2 A stochastic extension

As mentioned above, in a stock-for-stock merger companies not only share the change in expected equity values but, also, the change in risk created by this transaction.

In order to expand the LG-Y results in a stochastic environment, we need to introduce and measure risk.

Randomness is represented by (non-negative) random variables , , that describe stock prices. We make no a priori choice on their distribution, as long as expected values assumed to be a measure of performance and homogeneous measures of risk , in the sense of Artzner et al. (see [14]), for , exist. We also assume that so that stocks are considered a non- acceptable risk and shareholders might be interested in reducing it.

For the sake of notational simplicity, we decide to set so that formulas (2) and (3) are recovered. This claim is easy to justify; the deterministic approach corresponds to the one presented in this subsection if expected values only are considered.

Similarly to expression (1), we stress the importance of ratio

| (5) |

that expresses the relative risk of a share of company w.r.t. riskiness of a stock of company .

Introducing a risk measure for equities allows to define ratio , that is the coefficient of variation of random variable as well as a relative value that expresses a stock’s risk-corrected measure of performance.

Condition (respectively ), that is the risk-corrected performance of stock is better (respectively worse) than ’s, is equivalent to (respectively ).

Let . Shareholders of company benefit of a smaller risk after the merger when

| (6) |

This inequality yields a lower bound for ERs:

| (7) |

Here, to prevent from becoming negative, condition must hold.

Stockholders of company obtain a reduction in their equity risk when

| (8) |

This inequality leads to an upper bound for exchange ratios:

| (9) |

where imposing forbids to become negative.

Bounds (7) and (9) yield positive ERs when . This constraint implies that the reduction in riskiness a merger can achieve reduces the risk of company at most up to the largest risk of the merging ones.

Inequalities (7) and (9) identify a second bargaining region that is non empty whenever and contains positive ERs if . These conditions lead to

| (10) |

while this second set is

| (11) |

for . Interval (11) collapses into a singleton when the merger does not reduce riskiness, that is . In fact, .

A comparison between inequalities (2) and (7), that relate to company ’s stockholders, and between inequalities (3) and (9), that identify which exchange ratios are acceptable for company ’s stockholders, leads to a counterintuitive as well as interesting outcome.

If bound (2) suggests that stockholders of company want the exchange ratio to be as small as possible as this would grant them a large stake of expected synergy, bound (7) indicates that, if the number of ’s outstanding stocks is not large enough, the risk each stock ends up carrying is not less than the risk of each ’s stock.

A similar line of reasoning can be done for company ’s stockholders. Bound (3) implies that shareholders of the acquired company want to fix the exchange ratio as large as possible because, in this case, they seize a large portion of expected synergy. Bound (9), though, reveals that acceptable ERs cannot exceed a given threshold. If this happens, the stocks these stockholders obtain in exchange of each share they owned carry larger risk111The trivial arithmetic explanation of this claim is in Appendix A.1..

The existence of exchange ratios upper and lower bounds for both categories of shareholders permits to introduce two more sets that we call consistency region (CR). These intervals, when non-empty, contain all ERs that simultaneously grant both an increase in expected equity values and a reduction in equity risk for both groups of shareholders.

These sets are defined as

| (12) |

with and for shareholders of company , and

| (13) |

with and for those of company .

Assuming a merger yields an improvement in terms of both larger expected wealth and smaller risk might seem a rather ‘too-good-to-be-true’ requirement. Still, the key financial notion of diversification is based on better performance paired with less risk.

Interval (12) is non-empty when

To proceed with this analysis, let be the expected synergy and the reduction in risk, so that and . The above condition becomes

Consider, at first, the limit case where and (that is, the merger carries no benefit whatsoever). Interval (12) is non-empty if

that is when company is preferable to in terms of risk-corrected performance. Shareholders of company are favourable to complete the merger regardless of its positive synergy creation and/or risk reduction because company has an improved risk-corrected performance when compared ’s one.

The trivial algebra that explains the above claim, and the one regarding company below, is relegated in Appendix A.3.

This, of course, holds also when and/or as, if ,

Further, if (that is )

Consider case . Here, the no improvement due to synergy case yields

The resulting company the merger creates has a risk-corrected performance which is smaller than . Company A’s shareholders agree on the merger only if they receive some compensation that offsets their reduction in risk-corrected performance. This occurs if

that is the condition for non-emptiness of set . Here, for each there exists a threshold that linearly decreases w.r.t. . The above inequality indicates that the larger the reduction in risk, the smaller the minimum expected synergy that provides company ’s stockholders with a range of acceptable ERs.

A similar analysis can be carried out for interval (13). This set is non-empty when

Limit case , yields so that company ’s shareholders agree on the merger even if there is no synergistic effect if company has a better risk-adjusted performance.

In this case

When, instead, , set is non-empty when expected synergy fulfills condition

The bargaining region in the stochastic setting is the bivariate set

Set can be in one of six different cases, summarized in Table 1; four of them are non-empty. Each case corresponds to one of the sets and defined above. A detailed description of such cases is in Section 3.

| case 1 - | case 2 - | ||

| NA | case 3 - | case 4 - | |

| NA | NA |

Along the lines of [7] and [6], the issue is now the geometric representation of the bargaining region corresponding to the stochastic setting, , by varying and . Its representation is a subset of the space. However, to display this set in a more intelligible way, we decide to eliminate one dimension, and represent the bargaining region in the plane.

Fortunately, Kulpa does the trick, as he provides a methodology for representing intervals as points on the plane. His results are summarized and applied in the next section.

3 Diagrammatic representation of the bargaining region

In his diagrammatic approach, Kulpa (see, for example, [15], [16], and [17]) develops a useful methodology for representing bounded intervals as points on a plane. This is done, as Kulpa writes, citing [18], in [15], with the idea that “solving a problem simply means representing it so as to make the solution transparent”.

Based on this approach, each non-empty interval of the form is set in a one-to-one correspondence with point

where the two coordinates represent, respectively, the mid-point and the radius, or half-length, of . An interval which collapses to the singleton corresponds, according to Kulpa’s representation, to the point , and lies on the horizontal axis.

Consider now intervals

| (14) |

which, as described in Section 2, are the sets of exchange ratios accepted by both kinds of shareholders that guarantee, respectively, an increase of the value and a decrease of the overall risk of the transaction.

According to the diagrammatic approach, they are represented, respectively, by the points

| (15) |

and

| (16) |

The positions of and in the plane vary with the admissible values of and 222Recall that and are admissible when and ., thus defining two parametric curves, that we analyze in the next subsection.

We observe that, consistently with and , the corresponding points become

that is, the two curves intersect the horizontal axis at the points and , since they represent the singletons and .

The points and , depending respectively on and describe the curves and .

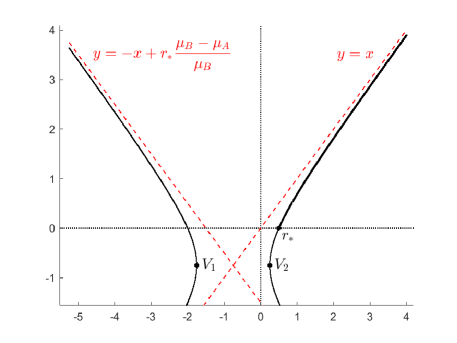

In the next subsection (see also Appendix A.2) we show that and represent two hyperbolas.

The explicit equations of these two curves allow us to represent the intersection of intervals in (14). This achievement allows to make readable and intelligible the set of exchange ratios on which an agreement is possible.

The points of each hyperbola, restricted to those satisfying the conditions imposed on and , represent the set of exchange ratios accepted by all the shareholders with respect to one of the two aspects (i.e., expected wealth or overall risk). Since we eliminate one dimension, it becomes easier and more intuitive to determine the accepted exchange ratios by varying and , as well as those belonging to the bargaining region.

3.1 Analysis of the curves and

Consider point in (15). As proved in Appendix A.2, observing that

| (17) |

using trivial algebra, and removing for the sake of simplicity the dependence from , the parametric curve is described by hyperbola

where

We restrict this curve to those points that satisfy . This condition, together with formula (17), implies that

Therefore, the set of points in the plane that represent the exchange ratios through which stockholders of both parties share an improvement in their expected wealth is

The condition is strict because is an asymptote of the hyperbola

A graphical depiction of these curves is provided in Figure 2.

Along the same lines, using the fact that

the parametric curve is described by

where

Again, we restrict the curve to the points satisfying . This condition yields

Therefore, the set of points that represent the exchange ratios on which shareholders agree because of the associated reduction of risk is

3.2 The bargaining region under Kulpa’s perspective

We choose now an admissible level of post-merger risk, , or, in other words, we fix a point along the curve , which represents all the exchange ratios to which correspond the amount of risk :

We now try to address the following questions. Under which conditions does there exist an interval of exchange ratios that makes an agreement among all the shareholders acceptable? In such a case, what is the shape of this set? Is it possible to describe its shape? To answer these questions, we consider the points of intersection between the interval represented by , and the admissible intervals on which there is an agreement with respect to the expected wealth, that is, those intervals represented by the points along the curve , with . Following Kulpa, the intersection between intervals and is non-empty if

In such a case, Kulpa’s representation of the intersection set is given by the point , where

Therefore, according to Kulpa’s approach, the intersection between the intervals represented by and is non-empty if the condition

| (18) |

is satisfied, and each point belonging to the bargaining region has -coordinate

and -coordinate

We now consider all the cases that may arise from condition (18). For each possible scenario, we explicit what condition (respectively ) has to satisfy, and describe the type of intersection accordingly to Table 1. We refer to Appendix A.4 for the details.

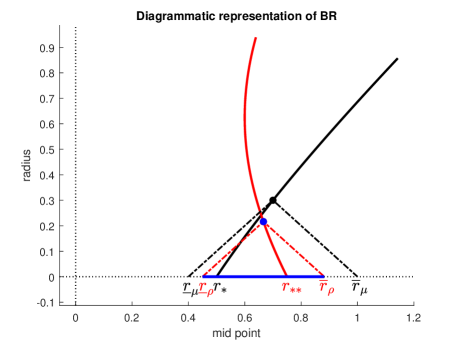

Case 1: Consistency region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of expected synergy, becomes

The set of exchange ratios on which all shareholders agree, represented, according to Kulpa, by the points

lies on the straight line of equation

which corresponds to the region in Table 1.

The diagrammatic representation for this case is in Figure 3.

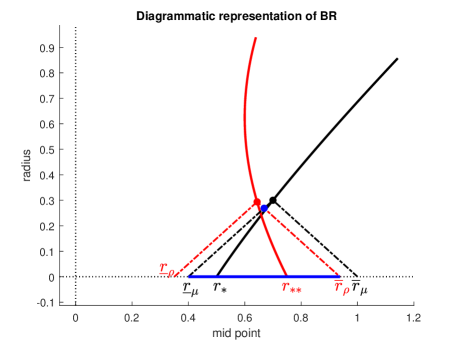

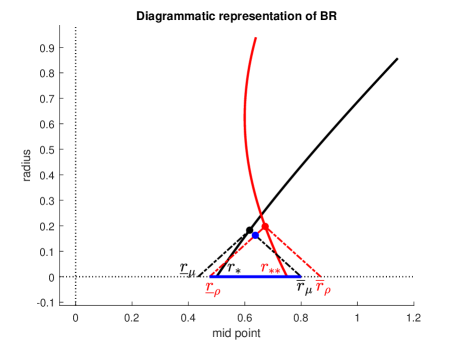

Case 2: Bargaining region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of expected synergy, becomes

The set of exchange ratios on which all shareholders agree on lies on the curve , and corresponds to the region in Table 1.

The diagrammatic representation for this case is in Figure 4.

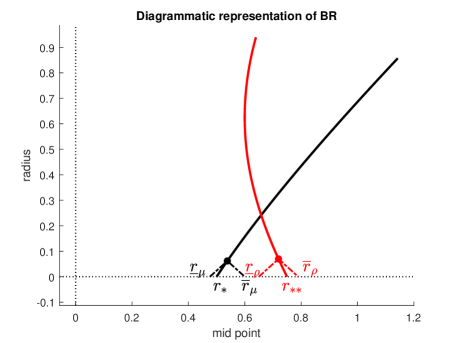

Case 3: Bargaining region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of expected synergy, becomes

The (unique) interval of exchange ratios on which all shareholders agree on corresponds to a point on the curve , represented by

and corresponds to the region , which shrinks to a singleton, in Table 1.

The diagrammatic representation for this case is in Figure 5.

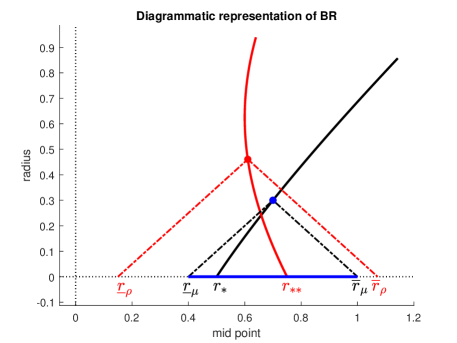

Case 4: Consistency region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of expected synergy, becomes

The set of exchange ratios on which all shareholders agree, represented, according to Kulpa, by the points

lies on the straight line of equation

which corresponds to the region in Table 1.

If we fix instead , we can consider the point , corresponding to the bargaining region . Recall that the intersection of the sets is not empty if (18) holds, then, again, this represents the starting point for the analysis of the possible scenarios. The details can be found in Appendix A.4.

The diagrammatic representation for this case is in Figure 6.

Case 1: Consistency region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of reduction of the overall risk, becomes

The set of exchange ratios on which all shareholders agree, represented, according to Kulpa, by the points

lies on the straight line of equation

which corresponds to the region in Table 1.

Case 2: Bargaining region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of overall risk, becomes

The (unique) interval of exchange ratios on which all shareholders agree on corresponds to the point on the curve

representing the region in Table 1.

Case 3: Bargaining region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of overall risk, becomes

The set of exchange ratios on which all shareholders agree on lies on the curve , and corresponds to the region in Table 1.

Case 4: Consistency region

Assume that and . This situation is consistent, together with , with the condition

The same condition, written in terms of reduction of the overall risk, becomes

The set of exchange ratios on which all shareholders agree, represented, according to Kulpa, by the points

lies on the straight line of equation

which corresponds to the region in Table 1.

Two more cases are displayed in this Table: in both, sets is empty. Figure 7 shows one of them. As it is clear from the above presentation, this set is empty due to the limited increase in expected equity value and/or limited reduction in overall risk.

The last case resembles the one just presented, with the only difference that . For sake of paucity, its diagrammatic representation is omitted.

4 Conclusions

In this article, we present an attempt to extend, in a stochastic setting, deterministic models for exchange ratios determination for merger agreements.

Under a financial point of view, an important result we achieve is that the introduction of a risk measure changes the attitude shareholders of the merging companies have toward the agreed exchange ratio. For shareholders of the acquiring company, smaller exchange ratios result in both larger expected equity value and equity risk. For shareholders of the acquired company, larger exchange ratio yield both a larger expected equity value and equity risk. This introduces a trade-off that makes the negotiation for settling on the definitive exchange ratio more fitting to a risky environment.

As far as the bargaining region is concerned, being here dependent on two quantities, its effective representation is obtained exploiting the Kulpa’s diagrammatic technique as it transforms bounded intervals into points in a bi-dimensional plane and allows to plainly represent all possible cases.

Even if it can be argued that, in real financial markets, imposing that a merger creates both a positive expected synergy and a reduction in the overall equity value risk rarely occurs, our contribution can be intended as a theoretical framework under which mergers can be analyzed, a result that lacks in financial literature.

To conclude, results presented here must be intended as a first step further research development in this field. For instance, ranges of acceptable exchange ratios might be determined following an expected utility approach, where a trade-off between expected value and risk of an investor’s wealth can be established.

Acknowledgments

The idea of exploiting the diagrammatic approach was suggested by Nicolae Popovici, wonderful friend, excellent researcher, and highly esteemed professor at the Department of Mathematics of the Faculty of Mathematics and Computer Science, Babeș-Bolyai University in Cluj-Napoca, Romania. Sadly, Nicolae suddenly passed away in June 2022. Without Nicolae’s help, this article would lack its best part.

La revedere, Nicolae; și mulțumesc pentru tot!

Appendix A Appendices

A.1 Appendix 1

To justify the claim about Company ’s stockholders in subsection 2.2, consider at first what happens in the left-hand side of (8) if : company ’s shareholders receive no stock, carry no risk, and experience a reduction in their riskiness.

As

the left-hand side of expression (8) is strictly increasing with respect to so that the larger , the larger the risk for ’s stockholders.

Finally, being, in accordance with (10), ,

Then, it results that sufficiently large values for bring about larger risk to company ’s stockholders when compared to the risk level they bore before companies merged.

A.2 Appendix 2

Consider point in (15). The difference between its coordinates is

| (19) |

from which (removing the dependence from for the sake of simplicity) we get

Recalling that

and replacing the expression of found above, we obtain

and multiplying by the following equation is obtained

so that is given by

| (20) |

This is the equation of the quadratic curve

with , , , , , and .

As , equation (20) identifies a hyperbola whose eccentricity is and that can be rewritten as

| (21) |

Its two vertices are

and

The abscissa of is smaller then the abscissa of . In terms of diagrammatic representation (see Figure 2), the relevant branch of hyperbola (21) is the one whose vertex is . This is the case as there exist points on the hyperbola’s branch that contains with negative abscissas, a condition that is not compatible with the fact that points belonging to must have positive values.

Focusing on , its abscissa is surely positive if . If, instead, then the abscissa of is positive as long as .

As far as the ordinate of is concerned, it is positive (respectively negative) when .

The asymptotes of (21) are

Similarly, consider point in (16). The sum of its coordinates is

from which (removing the dependence from for the sake of simplicity) we get

Recalling that

and replacing the expression of found above, we obtain

and multiplying by the following equation is obtained

so that is given by

| (22) |

which is, again, a hyperbola with equation

Its vertices are

and

while the asymptotes are

The abscissa of is smaller then the abscissa of . In terms of diagrammatic representation (see Figure 2), the relevant branch of hyperbola (22) is the one whose vertex is . This is the case as there exist points on the hyperbola’s branch that contains with negative abscissas, a condition that is not compatible with the fact that points belonging to must have positive values.

Focusing on , its abscissa is surely positive if . If, instead, then the abscissa of is positive as long as .

A.3 Appendix 3

In terms of risk-adjusted performance, the resulting company performs better then the pre-existing ones when

and

Recalling the notation for expected synergy and risk reduction introduced in Subsection (2.2), these inequalities are respectively equivalent to

and

If, now, and , the first inequality becomes

while the second reads

These expressions explain why, in the absence of any improvement in terms of either positive expected synergy or risk reduction, stockholders of company experience an improvement in the risk-corrected performance of the shares they own if company better behaves, in terms of risk-corrected performance.

A.4 Appendix 4

Consider . In Case 1, the intersection is the set . This interval is represented, under Kulpa’s approach, by the point

that is,

The sum of its coordinates is

that is, on varying we move along the straight line of equation

The conditions under which this situation is possible are

that is,

which can be summarized as follows:

To obtain the condition about the expected synergy, we subtract :

that is,

In Case 2, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

which, varying , leads to the curve (see A.2). The conditions under which this situation is possible are

that is,

which can be summarized as follows:

To obtain the condition about the expected synergy, we subtract :

that is,

In Case 3, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

This point is unique, that is, the bargaining region does not depend on . The conditions under which this situation is possible are

that is,

which can be summarized as follows:

To obtain the condition about the expected synergy, we subtract :

that is,

In Case 4, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

that is,

The difference between its coordinates is

that is, on varying we move along the straight line of equation

The conditions under which this situation is possible are

that is,

which can be summarized as follows:

To obtain the condition about the expected synergy, we subtract :

that is,

Consider now . In Case 1, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

that is,

The difference between its coordinates is

that is, on varying we move along the straight line of equation

The conditions under which this situation is possible are

that is,

which can be summarized as follows:

or, equivalently,

To obtain the condition about the overall risk, we sum :

that is,

In Case 2, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

This point is unique, that is, the bargaining region does not depend on . The conditions under which this situation is possible are

that is,

which can be summarized as follows:

or, equivalently,

To obtain the condition about the overall risk, we sum :

that is,

In Case 3, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

which, varying , leads to the curve (see A.2). The conditions under which this situation is possible are

that is,

which can be summarized as follows:

or, equivalently,

To obtain the condition about the overall risk, we sum :

that is,

In Case 4, the intersection is the interval . This is represented, under Kulpa’s approach, by the point

that is,

The sum of its coordinates is

that is, on varying we move along the straight line of equation

The conditions under which this situation is possible are

that is,

which can be summarized as follows:

or, equivalently,

To obtain the condition about the overall risk, we sum :

that is,

References

- [1] D. R. King, F. Bauer, and S. Schriber, Mergers and acquisitions: A research overview. Routledge, 2018.

- [2] A. Risberg, D. R. King, and O. Meglio, The Routledge companion to mergers and acquisitions. Routledge, 2015.

- [3] D. Gupta and Y. Gerchak, “Quantifying operational synergies in a merger/acquisition,” Management Science, vol. 48, no. 4, pp. 517–533, 2002.

- [4] H. E. Leland, “Financial synergies and the optimal scope of the firm: Implications for mergers, spinoffs, and structured finance,” The Journal of finance, vol. 62, no. 2, pp. 765–807, 2007.

- [5] A. Damodaran, Damodaran on valuation. John Wiley & Sons, 2008.

- [6] K. D. Larson and N. J. Gonedes, “Business combinations: an exchange ratio determination model,” The Accounting Review, vol. 44, no. 4, pp. 720–728, 1969.

- [7] J. Yagil, “An exchange ratio determination model for mergers: a note,” Financial Review, vol. 22, no. 1, pp. 195–202, 1987.

- [8] M. J. Gordon and E. Shapiro, “Capital equipment analysis: the required rate of profit,” Management science, vol. 3, no. 1, pp. 102–110, 1956.

- [9] M. Cigola and P. Modesti, “A note on mergers and acquisitions,” Managerial Finance, vol. 34, no. 4, pp. 221–238, 2008.

- [10] M. Taliento, “The valuation of the share exchange ratio in stock for stock transactions. allocation of synergies and financial implications,” Economia Aziendale Online-, vol. 14, no. 3, pp. 669–683, 2023.

- [11] Y. Amihud and B. Lev, “Risk reduction as a managerial motive for conglomerate mergers,” The bell journal of economics, pp. 605–617, 1981.

- [12] E. Moretto and S. Rossi, “Exchange ratio determination in a market equilibrium,” Managerial Finance, vol. 34, no. 4, pp. 262–270, 2008.

- [13] C. Toll and T. Hering, “Valuation of company merger from the shareholders’ point of view,” Amfiteatru Economic, vol. 19, no. 46, p. 836, 2017.

- [14] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath, “Coherent measures of risk,” Mathematical Finance, vol. 9, no. 3, pp. 203–228, 1999.

- [15] Z. Kulpa, “Diagrammatic representation of interval space in proving theorems about interval relations,” Reliable Computing, vol. 3, no. 3, pp. 209–217, 1997.

- [16] Z. Kulpa, “Diagrammatic representation for interval arithmetic,” Linear Algebra and its Applications, vol. 324, no. 1-3, pp. 55–80, 2001.

- [17] Z. Kulpa, “A diagrammatic approach to investigate interval relations,” Journal of Visual Languages & Computing, vol. 17, no. 5, pp. 466–502, 2006.

- [18] H. A. Simon, The sciences of the artificial. MIT press, 1996.