∎

22email: james.bono@microsoft.com 33institutetext: David H. Wolpert 44institutetext: Santa Fe Institute, NM,

Complexity Science Hub, Vienna,

International Center for Theoretical Physics, Trieste,

Arizona State University, Tempe AZ,

44email: david.h.wolpert@gmail.com

Game Mining:

Abstract

It is known that a player in a noncooperative game can benefit by publicly restricting his possible moves before play begins. We show that, more generally, a player may benefit by publicly committing to pay an external party an amount that is contingent on the game’s outcome. We explore what happens when external parties – who we call “game miners” – discover this fact and seek to profit from it by entering an outcome-contingent contract with the players. We analyze various structured bargaining games between miners and players for determining such an outcome-contingent contract. These bargaining games include playing the players against one another, as well as allowing the players to pay the miner(s) for exclusivity and first-mover advantage. We establish restrictions on the strategic settings in which a game miner can profit and bounds on the game miner’s profit. We also find that game miners can lead to both efficient and inefficient equilibria.

Keywords:

commitments contract delegate first-mover advantage bargaining1 Introduction

1.1 How to Mine a Game

That players can benefit in games by entering contracts that distort payoff functions is well-documented in the economic literature [see Schelling (1956); Sobel (1981); Vickers (1985)]. In this paper we focus on a special case of this phenomenon: A player may benefit by publicly committing to pay an external party an amount that is contingent on the game’s outcome. In this paper we explore what happens when external parties discover this fact and seek to profit from it.

To ground the discussion, we present an example.

Example 1

There are two cell-phone manufacturers, Anonymous (A) and Brandname (B). They must simultaneously decide how many cell phones to produce. Each firm has two options, high output (H) or low output (L). Anonymous, like its name suggests, is not well known. Therefore, no matter what level of output Brandname produces, Anonymous prefers to produce high output to gain brand recognition. On the other hand, Brandname’s choice of output does depend on Anonymous’s choice. If Anonymous produces low output, then Brandname prefers to keep prices high by also producing low output. However, if Anonymous produces high output, then Brandname prefers to safeguard its recognized name by also producing high output. The moves and payoffs (in millions of dollars) are summarized by the following matrix.

The NE is , and payoffs are .

A firm called Game Mining Inc. (G) watches this, and just before Anonymous and Brandname declare their output decisions, offers Anonymous the following contract, making sure Brandname sees them do this: “Pay us $1.5 million right now. Then we will pay you back a certain amount after you and Brandname make your decisions. The following matrix shows how much we will pay you, in millions of dollars, for the four possible joint decisions by you and Brandname:”

Note that this matrix does not include the $1.5 million up front payment. So if Anonymous accepts the contract, then the final payoff matrix for the game (including the up front payment) becomes

In this modified game, the unique NE is very close to , where is the probability that chooses . For Anonymous, this results in an average payoff of approximately $1.5 million. This is a $500,000 improvement over its payoff without the contract. On average, makes approximately $160,000 for their trouble. Brandname, on average, makes approximately $333,333. This is a $166,666 decrease in Brandname’s payoff compared to the situation where Anonymous and do not have a contract.

Note that the Coaseian outcome of the game without would be for Anonymous to pay at least $500,001 to Brandname for the outcome [see Coase (1960)]. So is not merely facilitating the Coaseian outcome. Note also that the outcome in example 1 cannot be achieved by a commitment by either player to play or not play either one of their actions. In general, the presence of creates an entirely new strategic setting. However, in this simplest of game mining scenarios, a commitment by to play the mixed strategy would achieve the same equilibrium as the game miner’s outcome-contingent contract. This is not the case for the other game mining scenarios discussed in this paper.

In example 1 makes considerable profit from recognizing that Anonymous benefits from an output-contingent contract. However, Anonymous also benefits from this contract. So game mining can be seen as a natural result of profit-seeking behavior, rather than as the result of economic planning and regulation. It requires no mechanism other than enforceable contracts between players and game miners.

Since profit-seeking behavior creates the game mining setting in example 1, it is natural to think about what other types of game mining settings can arise this way. By studying various structured bargaining games between game miners and players, we find a range of new phenomena. For example, in some cases, it may be that the miner can create a prisoner’s dilemma scenario between the players by offering contracts that each player has an incentive to accept regardless of whether their opponent accepts. If both players accept, the outcome is that they are both worse off than if neither accepts, and the game miner profits considerably. There are also important timing issues in game mining. When players sequentially sign contracts with game miners, there can be a significant first-mover advantage to the first-signing player. This provides the game miner with yet another opportunity for profit; they can charge the players to move first. Finally, game mining has complicated effects on efficiency. The effects depend on the underlying game as well as the bargaining structure between players and the game miner. In this paper, we explore situations where the presence of a game miner can both increase and decrease equilibrium efficiency.

1.2 Related Literature

The ideas underlying the game mining concept are implicit in a large body of economic literature. As an illustration, in the model presented in Jackson and Wilkie (2005) (JW), every player specifies outcome-contingent side-payments that they will make after a non-cooperative strategic form game is played and the payoffs are resolved. These side-payments are binding contracts, so the players are ex ante determining their preferences over the game’s outcomes. In this regard the game that the players actually play is endogenously determined. JW examine whether a mechanism that allows players to make such outcome-contingent side-payments generally results in efficient outcomes and conclude that it does not.

The simplest game mining scenario, e.g., example 1, can be viewed as a variant of JW. In this variant, the only outcome-contingent side-payments are between the players and the game miners and the game miners would be indifferent over outcomes of the game if not for the fact that they will be receiving side-payments dependent on those outcomes. Furthermore, the game miners play no part in the game between the players other than to accept contracts for outcome-contingent side-payments and make the contracts public.

In contrast to JW, we do not assume that a social planner installs a mechanism for players to make side-payments. Instead, we look at a game without formal mechanisms and ask whether external parties will create contracts for outcome-contingent side-payments in pursuit of profit. In addition, we relax the assumption in JW that all side-payments are nonnegative. That is, we allow game miners to pay players for certain outcomes. This will be important when examining optimal contracts as well as the extent to which a monopolist game miner can extract profits from players. Hence, game mining can be seen as the version of JW’s setting that arises as the natural result of profit-seeking in the absence of JW-type regulation. We also consider how outcomes change when the game miner can enter contracts with both players, when mining contracts are offered to players in sequence, and when we change the underlying bargaining structure between the players and the game miner. These considerations do not arise in JW’s setting.

In another related paper, Renou (2009) analyzes what happens when players are able to embed the original game in a new two-stage game. In the second stage of that new game the players play the original game. However before they do so, in the first stage, the players each simultaneously commit not to play some subset of their possible moves in that game in the second stage. These commitment games can be seen as the result of placing three restrictions of the JW setting: (1) player ’s side-payments are only contingent on ’s action (rather than on the full profile of actions), (2) the side-payments are made to external players and (3) the side-payments are effectively infinite. Renou’s restricted setting means that there are fewer commitments available but that there are also fewer deviations available. This means the set of equilibria sustainable in Renou’s restricted setting can differ significantly from the set sustainable in the less restricted JW setting. Renou’s setting and analysis are too restricted to cover the full game mining scenario. This is because there are many circumstances in which both the player and the game miner prefer to make contracts that are fully outcome-contingent and that have non-infinite side-payments. One example can be found in example 1 above, where the player and game miner find it optimal to agree on a contract that results in a unique equilibrium in which the player uses a mixed strategy with full support (and therefore does not make any commitment in the first stage of Renou’s two-stage game).

In Garcia-Jurado and Gonzalez-Diaz (2006) the types of commitments are similar to those studied in Renou (2009). The main difference is that the former studies a repeated game in which commitments to play mixed strategies are possible. They show that when such commitments are available, standard folk theorem results can be obtained with milder assumptions on the stage game. A key difference between our work and that of Garcia-Jurado and Gonzalez-Diaz (2006) is that our settings are all single-shot. Still, it should be possible to make commitments to play mixed strategies in a single-shot game. In the simplest game mining scenario, the set of equilibria is the same as what can be sustained by commitments to play mixed strategies. However, when mixed strategies do arise in our framework, they do so as the result of contracts that produce games with unique mixed NE rather than being required by the commitments themselves. And beyond the simplest game mining scenario, the set of equilibria under commitments to play mixed strategy differ from game mining equilibria. Like Garcia-Jurado and Gonzalez-Diaz (2006), the work of Kalai et al (2010) also obtains a folk theorem for commitments. They study a setting in which players can make commitments that are conditional on the commitments of their opponents. For two-player strategic games, they show that all feasible and individually rational payoffs can be obtained in the equilibrium set of a game with conditional commitments. Such conditional commitments are not explored in the game mining framework but remain of interest for future work.

Another well-studied aspect of commitment in games is the role of timing. Papers such as Hamilton and Slutsky (1990), van Damme and Hurkens (1996) and Romano and Yildirim (2005) concern endogenous timing and Stackelberg-like commitments. Wolpert and Jamison (2011, 2012) introduce the idea that players might also commit to using certain personas before the start of a game. These papers analyze the possibility that experimentally observed non-rationality is in fact rational, because by committing to play the game with a non-rational “persona”, a player may increase her ultimate payoff. This persona has the same effect as a side-payment or commitment, as it is reflected in a temporary change to the player’s utility function. The persona games model has been successful in explaining non-rational behavior in non-repeated traveler’s dilemma and even in versions of the non-repeated prisoner’s dilemma. Timing is also studied in the current paper. Here, the focus is on how the sequence of contracts between the game miner and players determines the outcome. As is the case in persona games, there is often a first-mover advantage in game mining even when players have dominant strategies.

Finally, there is a subset of the principal-agent literature concerning delegation games that is closely related to game mining. In these models, the principal is able to contract with an agent that will engage in a game with the principal’s opponent (or agent of the principal’s opponent). One concern of this literature is detailing the optimal contract for a principal [see Vickers (1985); Fershtman (1985); Sklivas (1987)]. Another concern is whether a mechanism that allows specific types of contracts can lead to Pareto efficiency [see Fershtman et al (1991); Katz (1991)]. Game mining is closely related to a previously unexplored aspect of principal-agent scenarios: the degree to which the agents can profit from delegation contracts.

The important difference between the work here and the related literature is that we concentrate on the potential role of a third party, seeking to make profits by interacting with the players, rather than focus on situations where all relevant decisions are by the original players alone.

1.3 Overview

We start by introducing the game mining model and notation in section 2. Then, in section 3 we assume one player interacts with the game miner and conduct a foundational analysis of the types of contracts and outcomes they can achieve. The properties derived in section 3 serve as the foundation for more in-depth analysis that appears later in the paper. For example, here we derive bounds on the aggregate payoffs that the game miner and player can earn together. We show that they can select a contract to divide these payoffs in any way between them. We also show that outcome-contingent contracts cannot be profitable for both the game miner and contracting player if the other player has a strictly dominant strategy.

In section 4 we consider various market structures, i.e., various structured bargaining games involving the players of the underlying noncooperative game and an external party that tries to mine that underlying game. We begin in section 4.1 with a game based on the assumption that players offer contracts to the game miner and the game miner must choose either one of the offered contracts or neither contract. We show that the game miner can profit by more than the maximal payoff to either player in the game without contracts. This is because players can suffer a loss if their opponent outbids them for the right to contract with the game miner. We derive an upper bound on the game miner’s equilibrium profit. We also characterize the set of equilibria for a simple example and show that the opportunity to make contracts with the game miner can make both players worse off. That is, a Pareto efficient equilibrium of the underlying game is not an equilibrium when game mining is possible. Note that JW find a similar result using their contingent transfers mechanism.

In section 4.2, we allow the game miner to accept both offers if she so chooses. This reduces the game miner’s bargaining power, and we find that the game miner can always do at least as well by restricting herself to accept only one contract.

In section 4.3, we discuss the role of timing and first-mover advantage, establishing that the players may be willing to pay for the right to contract first with the game miner. Therefore, in contrast to the simultaneous contract case in section 4.2, can engage players in a bidding war even when she can accept both contracts. Furthermore, this can happen when one or both of the players have a strictly dominant strategy. Two examples illustrate this and further analyze the difference between game mining and Renou-type commitments.

In section 4.4 we analyze the case where the miner has the bargaining power, i.e., is the one making the offers. We show that this allows the game miner to “play the players against one another” and thereby increase her profit. We also derive an upper bound on this profit. An interesting feature of this scenario is that the game miner moves the players from an inefficient equilibrium to an efficient one. However, as a profit seeker, the game miner is able to capture more profit than the efficiency gain.

In section 5 we briefly discuss several new research areas opened by game mining. These areas include games of more than two players, and risk aversion on the part of the game miner. We briefly consider unstructured bargaining among the players and the miner to determine the contract. We also touch on an “inverted” version of this topic, where the underlying game is itself unstructured, while the miner(s) negotiate with the player(s) via structured bargaining to determine a contract for that underlying game. We end by discussing the idea that one player might sign a contract that obligates him to pay the other player outcome-contingent amounts. This obligation may actually help the payer and hurt the payee.

2 Notation

We study a two-player, one-stage simultaneous-move game of complete information. However, we relax the usual assumption that the two players cannot make outcome-contingent contracts (or simply contracts) with players external to the game.

Specify the two-player pre-contract game as

where is finite and is an -by- matrix for which the entry gives the payoff to when chooses his ’th pure strategy and chooses his ’th pure strategy. Player ’s set of mixed strategies is , , and the set of mixed strategy profiles is . We write all of ’s pure and mixed strategies as -by-one vectors for which the ’th entry gives the probability that assigns to playing ’s ’th pure strategy. Therefore, player ’s expected payoff from as

where superscript indicates matrix transpose.

Player ’s best response correspondence is given by , so that

| (1) |

Therefore, the set of Nash equilibria of game is given by

An outcome-contingent contract between player and the game miner is a matrix that specifies a (possibly negative) transfer from to for every outcome of . We assume is finite. If players use strategies , then under contract player expects to pay to G. Defining , player ’s expected payoff is . Therefore, we can view as a transformation of . We write the post-contract game as for , where the second argument of the post-contract game identifies the player with whom has contracted. Note, that we simplify this notation by dropping this second argument whenever the context makes clear the identity of the player with whom has contracted. We write the set of possible contracts as . The notation denotes the null contract, where all entries are zero.

3 Maximal Mining

Before introducing a formal strategic setting for game mining in the next section, we first explore the way that a player and the game miner can work together to extract gains from . This is the simplest game mining scenario.

The first step is to define the aggregate payoffs from a contract. These are the amounts that the contracting parties can earn in equilibrium and divide among themselves. Suppose and are the contracting parties and is their contract. Then the aggregate payoff that is apportioned between and is given by the payoff that gets at a NE in before pays to the amount specified in .

Definition 1

The aggregate payoff set for and from is:

’s payoffs are the only difference between and the post-contract game . Here distorts , thereby distorting ’s best response function. By varying , we can give any best response function in . This includes best response functions that designate dominant strategies as well as indifferences. Therefore, when exclusively contracts with the game miner, any profile such that chooses a best response can arise as an equilibrium of for some . The same thing can be said for the situation where has the exclusive opportunity to make commitments on mixed strategies.

We denote by the maximum of the aggregate payoff set from . The maximum over all aggregate payoff sets is . It is the maximum that and can possibly have to divide among themselves in any NE of any game in which they sign a contract. We refer to this quantity as the maxagg (maximum aggregate payoff). The maxagg is the subject of our first result.

Proposition 1

| (2) |

Proof

From the definition of maxagg we have:

| (3) |

Recall that the contract does not affect ’s payoffs . This means that . The trouble is to choose so that ’s best response correspondence meets ’s best response function at the maximizers that correspond to , . This problem is solved trivially by choosing such that is indifferent among all strategy pairs. Then every action of is a best response to every action of , including , which, by assumption is in .

Proposition 1 means that to find the maximum aggregate payoffs for and G, we simply search ’s best response correspondences to all of ’s moves for the one giving maximum payoff to . This allows us to restrict our analysis to the values of along ’s best response correspondence. Note that certain outcomes in the aggregate payoff set correspond to profiles in which does not choose a best response to ’s strategy. Only is being forced to make a best-response. So, maxagg is nothing more than an upper bound on what is possible for and G to obtain by making a contract.

In some cases, a game miner might be concerned with maximizing the minimum of the aggregate payoff set as a way of guaranteeing a sufficient minimum payoff. We write the minimum of the aggregate payoff set as . Maximizing over all contracts , we get the maximum minimum aggregate payoff , called the maxminagg:

Trivially, . Comparing maxminagg with maxagg, we also know that . And when there exists a contract such that , we have that . That is, if there exists a contract such that the only NE of yields the maxagg to and G, then the maxagg and maxminagg are the same.

The next example continues from example 1 in the introduction, using maxagg and maxminagg to illustrate a distinction between the equilibrium outcomes in game mining and commitments to play pure strategies. In this example, maxagg is associated with a NE strategy for , , that is a mixed strategy with full support. However in this example, a commitment by to play (or not play) certain pure strategies will never allow and to achieve the maxagg.

On the other hand, contracts that achieve the maxagg may also give rise to a NE with an aggregate payoff lower than the maxagg or the NE aggregate payoff for the original game. So we may expect that a conservative miner would avoid such contracts that achieve the maxagg but also have bad equilibria. To address this, we show that there are contracts that yield a unique mixed NE for which the aggregate payoff is arbitrarily close to the maxagg. Because this NE is unique, the aggregate payoff is also the maxminagg that concerns the conservative game miner. Therefore, a conservative game miner would choose such a contract over one that involves a commitment to play (or not play) a specific strategy.

Example 2

Consider again the game presented in Ex. 1 above:

where is the row player. Write . Then ’s best response correspondence is

If chooses , then will choose , and the payoff to will be . Likewise, if chooses , then will choose , and the payoff will be . If chooses then chooses any combination of and yielding payoffs to between and . Therefore, the maximum payoff for along is when and :

In other words, the maxagg payoff for and is achieved by a mixed strategy. The problem is that there is no contract such that has a unique NE that achieves the maxagg payoff to and that results in a nonnegative payoff for . Moreover, for those ’s such there is a NE of with ’s payoff equaling the maxagg payoff, there are other NE with ’s payoff less than , which is already ’s payoff in every NE of the original game . So it would appear that has no incentive to form a contract with Game Mining, Inc. However, there are contracts that produce a unique NE under which the aggregate payoff is arbitrarily close to the maxagg of . An example of such a contract that gets arbitrarily close to the maxagg is

With this contract ’s payoffs are now given by

There is a unique NE for all . As approaches zero, that NE approaches , so the maxminagg approaches . As mentioned previously, this outcome is also possible if can commit to playing his NE mixed strategy.

The preceding results consider the aggregate payoffs that and can achieve by contracting. We next address the way in which and are able to divide those aggregate payoffs. The following result says that they are able to incorporate any division of the aggregate payoffs directly into the contract without affecting the best response correspondence of or . (Whether and would accept such a division is a different issue.)

Proposition 2

For any and such that , there exists a contract such that:

-

1.

, and

-

2.

.

Proof

By proposition 1 there exists a contract such that . Let stand for a matrix all of whose entries are . So . Therefore there is a scalar such that

This gives us . Since , .

Proposition 2 says that the aggregate payoffs that and G get by mining are not affected by a restriction on the way in which and divide those payoffs. So the way is divided between and in equilibrium will be determined by strategic rather than technical considerations. This will be convenient when we introduce a formal strategic environment in the next section.

In some settings, there is no contract such that and can both benefit in any NE of . This is always the case when has a strictly dominant strategy.111Later we introduce the possibility that and both make contracts with in a sequential structure. Here, there are contracts such that and both benefit in even though has a strictly dominant strategy. The intuition is that ’s contract with will never change ’s payoffs. Therefore, will always play his dominant strategy, no matter what the contract says. Therefore there is nothing that a contract can do to help . This intuition is formalized in the following result.

Proposition 3

If has a strictly dominant strategy, then there is no contract such that and both strictly benefit in any NE of .

Proof

Suppose is a strictly dominant strategy for player . Then for all . Hence the set of NE in is

and the set of NE in is

If benefits by entering contract , then .

But this means that . Since , by combining we have for all . Accordingly, will not benefit by signing .

Proposition 3 puts a restriction on the set of games in which will benefit from the services of a game miner. However, as is shown in later sections, there are ample opportunities for and to benefit from contracts when player has a strictly dominant strategy. In general, such a situation requires that also has an opportunity to make a payoff-contingent contract with the miner.

The next result establishes limits on game mining when one player has a weakly dominant strategy.

Proposition 4

If has a weakly dominant strategy, then there is no contract such that both and strictly benefit in every NE of compared to not signing any contract.

Proof

By contradiction. Suppose is weakly dominant and is a contract such that both and benefit in every NE of . There is a NE of . For every we have that

If is better off in every NE of , then for

which implies

which in turn contradicts the fact that is better off.

Proposition 4 tells us that and cannot eliminate the risk of loss in a NE of if has a weakly dominant strategy in . If and are both conservative and require that they gain in every NE of , then no contract will be made between them.

4 Game Mining Bargaining Structures

4.1 Accepts One Contract

Consider a situation in which players and encounter each other in a simultaneous move game, . There is only one external party, G, that is willing to accept publicly observable outcome contingent contracts. Before and play , they simultaneously offer contracts to G. These contracts are called and respectively.

After observing and , chooses either , or (the null contract). Players and observe this contract and recognize its legally binding nature. and then engage in the simultaneous move game . is the post-contract subgame, where again we simplify the notation by dropping the second argument when the identity of the player with whom has contracted is clear.

Formally, this is an extensive form game with three stages:

- Stage One:

-

Players and simultaneously offer contracts and to G.

- Stage Two:

-

chooses , or the null contract .

- Stage Three:

-

Players and play .

A strategy for in the extensive form game is a pair . The first component, , is the offer that makes to in the first stage. The second component is a function from the space of all possible contracts and contractees, , to the space of probability distributions over ’s action set , i.e. . In other words, gives ’s strategy (pure or mixed) in the post-contract subgame induced by choosing contract from player . Here we also simplify the notation by dropping the second argument when the identity of the player with whom has contracted is clear, e.g. . The profile of strategies of player and player are written as where .

In stage two, selects an element of the choice set . is the function that takes as input the history and returns an element of indicating which player’s contract has been chosen. We let indicate the game miner chooses not to contract with either player.

Given a full strategy profile , G’s payoffs are

is G’s stage two choice given the stage one actions , and is ’s stage three reaction to that choice. For , the payoffs are

if chooses ’s contract and

otherwise. As shorthand, we represent this extensive form game as

Definition 2

A subgame perfect equilibrium (SPE) of is a strategy profile such that:

-

1.

for all contracts .

-

2.

is optimal given for all pairs , i.e.

for all .

-

3.

is optimal given , and , i.e.

for all (mutatis mutandi for ).

We turn our attention to finding the maximum amount that can be mined from . To do so, we introduce a concept that is related to the aggregate payoff set from definition 1:

Definition 3

The aggregate payoff function for and from is:

The aggregate payoff function differs from the aggregate payoff set. Whereas the aggregate payoff set includes payoffs for all NE of , the aggregate payoff function simply returns the sum of and G’s payoffs when is played in . For example, if selects a NE of the post-contract subgame , then the aggregate payoff function selects one element from the aggregate payoff set . We denote by a contract that maximizes ’s aggregate payoff function.

In an SPE, will choose whichever contract yields her the highest payoff as determined by . Given that, ’s should offer more to than ’s offers whenever ’s contract offers less than . The most that will ever be willing to offer is therefore determined by finding the contract of that results in the smallest payoff for , called . Following this logic reveals that, loosely speaking, will contract with the player that has the greatest willingness to pay. In other words, there will not be an SPE in which accepts a contract from one player while the other has a greater willingness to pay. From the players’ willingness to pay, we get the maximum SPE payment to in the following proposition.

Proposition 5

The upper bound SPE payment to is

Proof

First, let . That is, is the contract that minimizes ’s payoff given . Also let

be the change in ’s payoff by going from to . Similarly define

as the change in ’s payoff by going from to .

The proof follows from the strategic considerations of the players. Either (1) neither player pays G, or (2) player pays G. In the case of (2), will offer no more than necessary, which is the minimum increment above what would get by accepting ’s offer, . Player will only be willing to pay this amount if it is less than the amount that she gains by changing the game from to , i.e., This difference is maximized by choosing to minimize ’s payoff in and choosing to maximize ’s payoff in . Given , these arguments are and respectively. So we have that the maximum will pay in an SPE of given is .

Maximizing ’s payoff over all functions and contracts we get the maxagg . Minimizing ’s payoff over all functions we get where the minimizer yields . However, we know that since is part of an SPE, that is a NE of . Therefore, . In other words, the only requirement in constructing is that is always playing a best response. This is because can be such that is a best response to . Therefore,

Putting this together with ’s maxagg and choosing we get the result.

Proposition 5 gives an upper bound on the amount that the monopolist game miner can extract from a game between and . This is achieved when player chooses the contract that minimizes ’s payoff given the strategies for the resulting post-contract game, . At the same time, the amount offered to the game miner by the contract is equal to the maximum amount that is willing to pay to change the game from to . The amount paid to the game miner in this situation is bounded by the players’ payoff functions. So a monopolist game miner cannot, in this situation, extract arbitrary profits.

The SPE concept here allows for some behavior that is unreasonable from a trembling hand perspective. For example, in order for to achieve her maximum payment, must choose contract . However, might actually prefer the outcome under to the outcome under . That is, to support the equilibrium in which offers her maximum willingness to pay, offers quite a bit of money to for a deal she wants not to take effect. ’s offer is only a best response to ’s slightly greater offer because will choose ’s contract, so that this unreasonable offer by , , will never be accepted by G. But, if trembled and chose , the outcome could be disastrous for . In short, for some , there exist SPE in which achieves her maximum payoff only if one of the players acts in a manner that seems unreasonable.

Instead of considering all possible equilibria, perhaps a more reasonable set of outcomes is one in which players only offer contracts () that maximize the aggregate payoff function, . It is reasonable to restrict the analysis to this set of contracts because at least one aggregate payoff maximizer, , is a best response to every and . Note that in some games, this restriction on players’ choice of contracts can reduce G’s maximum SPE payoff.

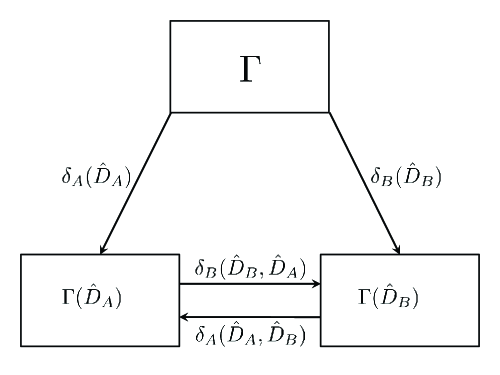

Figure 3 is a flow diagram that illustrates how the aggregate payoff maximizing contracts translate into the monopolist miner’s payoffs. Positive quantities represent movements in the direction of the associated arrow. So if , we know that is willing to pay to change the game from to . Hence, will not be the post-contract subgame in an SPE. Next, if , then is willing to pay more to change the game from to than is willing to pay to change it from to . will offer a contract such that G’s payment is just greater than is willing to pay to change the game from to .

Another implication of proposition 5 is that G’s payoff can be greater than . In other words, the winning contract may pay more than the maxagg for either player. The following example illustrates how a monopolist miner can make both players worse off than they were without the opportunity to mine. We demonstrate that this is the case even when players are restricted to choosing contracts that maximize aggregate payoff functions.

Example 3

Consider the game :

where is the row player. The unique NE of is . Calculating ’s aggregate payoff function for , and as well as ’s willingness to pay, we get:

By symmetry the quantities for are the same as the corresponding quantities of .

The fact that for means that both players are willing to pay to change the game from to , so will not be the outcome. Next, because for , we know that will get a payoff of in equilibrium. This payoff is greater than . In other words, if ’s contract is accepted, then the contract between and pays more than the increase in aggregate payoffs . The reason is that is paying to avoid having become the equilibrium game.

We also observe that . This says that gets less by having the equilibrium contract with than would get if neither player had the opportunity to offer contracts. For , the player that does not win the equilibrium contract, the SPE payoff is also . Therefore, the both players are worse off with the opportunity to mine.

4.2 G Accepts Both Contracts

We now relax the assumption that must choose between and . After all, if is a true monopolist game miner and there are gains to be made by simultaneously contracting with both parties, then will certainly want to do this.

The strategies in must be modified to accommodate this new possibility. First, a strategy for selects an element of G’s choice set after the history . Since can now choose to accept both contracts if she wishes, the choice set is now given by:

This induces the game where () is the contract between and and () is the contract between and G. Therefore, the game is one in which ’s preferences are and ’s preferences are . This means that the stage three strategy profile is defined on so that (). In other words, players select a strategy for every possible post-contract subgame of the form .

We refer to the stage three game that is played in equilibrium of as the equilibrium game. If accepts only , then the equilibrium game is . If accepts and , then the equilibrium game is and so on. The game was not possible when could only accept a single contract. However, when can accept both contracts it is possible.

This raises the issue of determining how chooses given that is choosing . Given a function , ’s contract and G’s decision , chooses a contract in order to maximize his payoff.

| (4) |

This gives rise to a best response correspondence for .

Definition 4

Player ’s best contract response correspondence given is a set valued function that gives all of the contracts that maximize equation 4 when makes contract given .

By requiring that selects a NE of every post-contract subgame, we guarantee that is a best response to and vice versa. When meets this requirement, the best contract response correspondence amounts to a best response correspondence for the extensive form game. The following result uses the concept of a best contract response correspondence to categorize a monopolist game miner’s payoffs when able to accept both contracts.

Proposition 6

The monopolist game miner’s equilibrium payoffs under the restriction that can only accept one contract are always as good and sometimes better than her payoffs without that restriction.

Proof

Suppose and/or and , then with the restriction, gets . However, without the restriction, there is the possibility that for some and , and both prefer to and . If and given , then this will be an equilibrium. When the equilibrium game is , neither player is paying for exclusivity, so G’s payoff is zero instead of .

Further, the threat of an outcome can never induce to pay more than for exclusivity. This is because is the value for of going from to . Given that pays for exclusivity, there is no payment that can make to change the game from to because ’s contract is contingent on exclusivity.

Proposition 6 says that a monopolist game miner cannot be made worse off by restricting herself to accept a single contract. The reason is that when does not restrict herself, then she does not give up in order to accept . Therefore, if accepts , then her best response is to accept any contract for which her payoff under is at least her payoff under . Knowing this, will choose such that G’s payoff under is exactly what it is under . The same holds for . Therefore, is made worse-off by the ability to make contracts with both players. Put differently, the threat of an equilibrium game never induces the players to pay more, and it is sometimes better for the players.

The above suggests that the one-contract restriction might be the result of payoff maximizing behavior. That is, G’s payoff in equilibrium of the one-contract game might be equivalent to a payment not to contract with the other player. Hence, the restricted game is equivalent to a game in which and submit two-element stage-one offers, , where is the matrix of strategy-contingent transfers and is a payment not to make a contract with . If , then places no exclusivity restriction on G’s acceptance of . Therefore, G’s payoff from accepting ’s contract is . If then G’s payoff from accepting both contracts is .

4.3 Sequential Contracts

We now examine the role of timing on game mining outcomes. The game is exactly as previously described, except that first selects a contract to be observed by before selects a contract. In this setting we find that may have a first-mover advantage and also that contracts are not equivalent to the pre-commitments of Renou (2009). Both points are demonstrated in the following example.

Example 4

Consider the game

| x | y | z | |

|---|---|---|---|

| x | 2,5 | 0,0 | 5,4 |

| y | 1,3 | 1,2 | 2,0 |

| z | 0,3 | 0,1 | 2,0 |

where is the row player. The unique NE of this game is . Note that is a strictly dominant strategy for . By proposition 3, there is no contract such that gets a better payoff in a NE of than in a NE of . Despite this fact, there is a contract such that

where is a best contract response to given . In other words, there is a contract such that when chooses his best contract response to , gets a higher payoff in than in any NE of . To illustrate, suppose signs a contract with to pay whenever the outcome is , then the unique NE of is . The post contract game, , is given by:

| x | y | z | |

|---|---|---|---|

| x | 0,5 | 0,0 | 5,4 |

| y | 1,3 | 1,2 | 2,0 |

| z | 0,3 | 0,1 | 2,0 |

Then ’s best contract response is a contract that promises to pay if the outcome is and if the outcome is . This will make the unique NE of .

| x | y | z | |

|---|---|---|---|

| x | 0,5 | 0,0 | 5,4 |

| y | 1,-1 | 1,-1 | 2,0 |

| z | 0,3 | 0,1 | 2,0 |

The final outcome gives his highest payoff from , and it gives his maxagg. gets zero in the equilibrium of , , and . Therefore, this outcome is the unique SPE of .

Note that if was the first to select a contract, then would choose to which ’s best contract response is . Both players would be willing to pay for the right to move first. would pay the difference between his payoff in and , which is . However would only be willing to pay the difference between his payoff in and , which is just .

This example draws a sharp distinction between game mining and pre-commitments to play or not play certain strategies. Suppose instead selected a contract that made a never-best-response. Then ’s best response is , and the outcome is , which is worse for . does not want to commit to not playing because is the ultimate goal. He rather wants to commit to not being the outcome, so that will commit to and not being the outcome.

Exploiting contract timing is yet another way that game miners game miners can extract profits from players even when players are making the offers. Since has a first-mover advantage, and has a second-mover disadvantage, both are willing to pay to move first. Suppose recognizes this advantage before and approaches with his desired contract . could potentially put on hold and notify to start a bidding war over the first-mover advantage. The first-mover advantage is worth more to than it is to , five versus one, so would end up paying ’s maximum willingness to pay for the first-mover advantage. In contrast to the discussion above where players make simultaneous offers and accepts one contract, this type of bidding war can happen even though is free to accept both contracts.

4.4 G Makes Offers

Until this point we have assumed a particular bargaining structure in which and make take-it-or-leave-it offers to G. This implies that G’s only bargaining power is in rejecting contracts that result in negative payoffs. Suppose now that we change the game so that makes publicly observable offers to and . Then and simultaneously accept or reject the offers has made. So and will now accept any contract that does not make them worse off, given the other’s choice. This clearly places more power in the hands of G.

To accommodate the new structure of the game, we alter the definition of strategies. Now G’s stage one strategy is . and have binary stage two strategies and stage-three strategies (), which we sometimes shorten to be and . So selects a contract for each player, . Then each player chooses to accept or reject the contract they are offered, . Finally, the players play the post-contract game according to .

We want to characterize G’s payoffs in an SPE. To do so, consider the following devious plan where can sometimes create a high-order prisoner’s dilemma between and . This is illustrated in the example below.

Example 5

Consider the game where is the row player and both players have a strictly dominant strategy to choose .

The unique NE is , and both players get a payoff of . Then if offers the following contract to

the unique NE of is . ’s payoff in is , so would accept , getting rather than . ’s payoff in is . If offers to , then the equilibrium of is . The payoff to is . Therefore, would accept given that accepts because he will get rather than . By the symmetry of , and , we know that each player prefers to accept regardless of whether accepts or rejects his offered contract.

This is very similar to a prisoner’s dilemma game because each player has an incentive to accept regardless of whether accepts . This moves the players from , where the unique NE gives them , to , where the only NE gives them . By playing against the game miner gets .222Of course, the game miner could reduce the contract payoffs for () from 2.01 to , where is an arbitrarily small number, and the game miner’s payoff would strictly increase without changing any of the equilibria. The number 2.01 is used here for simplicity. The situation can be visualized alternatively as the following PD game where is the row player and is the column player, and the payoffs are given by the unique NE of the resulting post-contract games:

Note that once again moves the game from an inefficient equilibrium to an efficient one. However, as a profit maximizer, the game miner captures the efficiency gains.

The example above shows that can potentially do better for herself by selecting contracts that both and will accept than by contracting with one player exclusively. The intuition for why this is possible is that relies on the fact that and will never obtain in equilibrium. Therefore, is free to offer contracts and such that she loses money in the unique NE of and . This allows her the flexibility to make sure the NE of is in her favor. Note that this result does not rely on the fact that both players have strictly dominant strategies. It is simple to construct examples for games in which only one player has a dominant strategy or neither player has a dominant strategy.

The following proposition provides an upper bound on the game miner’s payoff when she extracts profits according to this scheme.

Proposition 7

The maximum that a monopolist game miner can profit by offering contracts such that and have weakly dominant strategies to accept is

Proof

The first term is the maximum amount that and can earn in any outcome of . The second term is the minimum amount that can force to get by designing such that is a best response to . This is because is constrained so that must lie on ’s best response correspondence for . The third term is the equivalent of the second term for rather than .

Suppose earns more than this maximum, then

| (5) | |||

but because and each have a weakly dominant strategy to accept, we know that

and

Together, these inequalities imply

The left-hand-side is G’s profit, and the maximum of the right-hand-side is given by the right-hand-side of inequality 5. Therefore, we have a contradiction.

This result is important because it says that the game miner cannot make an arbitrary profit from the players by giving each a dominant strategy to accept her offer. Therefore, the game miner’s profit and any efficiency loss for the players are always limited.

5 Discussion

As mentioned in the introduction, the game mining analysis opens up several new research areas. One natural extension is to consider game mining situations in which there are more than two players or even with multiple game miners. With multiple players simultaneously choosing contracts, the blocking and exclusivity concerns we address above are likely to become much more complicated. An open question is how the market structure affects the game miner’s opportunity to profit.333An earlier version of this paper analyzes perfect competition and duopoly competition among game miners

Yet another research question is whether replacing the structured bargaining between players and game miners with unstructured bargaining will change the profitability of game mining. One might also consider the reverse situation in which the stage game is a game of unstructured bargaining between and , but the negotiations between players and game miners follow structured bargaining. Here, we would have that players sign contracts through structured bargaining in an attempt to gain an advantage in the unstructured bargaining that follows. The question is how would players design contracts to distort their utility possibilities set in such a way that benefits them in the ensuing unstructured bargaining. An interesting technical issue arises in deciding whether to allow players to sign contracts that lead to utility possibility sets that are nonconvex. If so, then a solution concept other than the Nash Bargaining Solution is needed [see Nash (1950); Kalai and Smorodinsky (1975)].

All of this raises a crucial question: Why aren’t real game mining firms wreaking havoc on real markets? Game mining appears to be very possible according to basic game theory, so if it is not generally possible in the real world, what assumptions are being violated?

There are many potential answers to this question. One tempting explanation is that the payoff structure of most real world games makes them unable to be mined. This seems a strange assertion because, as shown, even games in which both players have strictly dominant strategies can be mined for profit depending on the market structure. Other potential answers are that the calculations are too difficult in practice, that the time frame in real world games is too short, that game mining could be considered illegal, that imperfect information limits game mining opportunity, or that some kind of strategic uncertainty makes game mining impractical. These explanations should be explored in future work because they might shed light on the way game theory applies to real world strategic settings.

There are other questions to explore. For instance, does game mining imply that certain games should never exist because the minute they appear they will be mined into an alternate game? In some sense this gives rise to a meta-game whereby a player that finds himself involved in an easily mineable game might assume that the game will be mined and therefore conclude that he is actually playing a different game. Or, in a game with multiple equilibria, one equilibrium might make the game susceptible to mining by an outside party that ultimately makes both parties worse off (like what happens when a game miner makes offers that give players strictly dominant strategies to accept). Therefore, that susceptible equilibrium might become less likely than an equilibrium that is more robust. In this way game mining introduces an equilibrium refinement: choose the equilibrium that makes game mining least profitable.

These questions and others are not only interesting for their ability to shed light on game mining concepts, but also more generally for their ability to shed light on the noncooperative theory.

References

- Coase (1960) Coase R (1960) The problem of social cost. Journal of Law and Economics 3(1):1–44

- van Damme and Hurkens (1996) van Damme E, Hurkens S (1996) Endogenous stackelberg leadership. Games and Economic Behavior 28(1):105–129

- Fershtman (1985) Fershtman C (1985) Managerial incentives as a strategic variable in a duopolistic environment. International Journal of Industrial Organization 3:245–253

- Fershtman et al (1991) Fershtman C, Judd KL, Kalai E (1991) Observable contracts: Strategic delegation and cooperation. International Economic Review 32(3)

- Garcia-Jurado and Gonzalez-Diaz (2006) Garcia-Jurado I, Gonzalez-Diaz J (2006) The role of commitment in repeated games. Optimization 55:1–13

- Hamilton and Slutsky (1990) Hamilton JH, Slutsky SM (1990) Endogeneous timing in duopoly games: Stackelberg or cournot equilibria. Games and Economic Behavior 2:29–46

- Jackson and Wilkie (2005) Jackson MO, Wilkie S (2005) Endogenous games and mechanisms: Side payments among players. The Review of Economic Studies 72(2):543–566

- Kalai et al (2010) Kalai A, Kalai E, Lehrer E, Samet D (2010) A commitment folk theorem. Games and Economic Behavior 69:127–137

- Kalai and Smorodinsky (1975) Kalai E, Smorodinsky M (1975) Other solutions to nash’s bargaining problem. Econometrica 43(3):513–518

- Katz (1991) Katz ML (1991) Game-playing agents: Unobservable contracts as precommitments. The RAND Journal of Economics 22(3):307–328

- Nash (1950) Nash J (1950) The bargaining problem. Econometrica 18(2):155–162

- Renou (2009) Renou L (2009) Commitment games. Games and Economic Behavior 66(1):488 – 505

- Romano and Yildirim (2005) Romano R, Yildirim H (2005) On the endogeneity of cournot-nash and stackelberg equilibria: Games of accumulation. Journal of Economic Theory 120:73–107

- Schelling (1956) Schelling TC (1956) An essay on bargaining. American Economic Review 46:281–306

- Sklivas (1987) Sklivas S (1987) The strategic choice of management incentives. The Rand Journal of Economics 18:452–458

- Sobel (1981) Sobel J (1981) Distortion of utilities and the bargaining problem. Econometrica 49:597–617

- Vickers (1985) Vickers J (1985) Delegation and the theory of the firm. Economic Journal (supplement) 95:138–147

- Wolpert and Jamison (2011) Wolpert D, Jamison J (2011) The strategic choice of preferences: the persona model. Berkeley Electronic Journal of Theoretical Economics

- Wolpert and Jamison (2012) Wolpert DH, Jamison J (2012) Evolution and Rationality: Decisions, Cooperation, and Strategic Behavior, Cambridge University Press, chap Schelling Formalized: Strategic Choices of Non-Rational Behavior. In press