Robust Inference for Multiple Predictive Regressions with an Application on Bond Risk Premia

Abstract

We propose a robust hypothesis testing procedure for the predictability of multiple predictors that could be highly persistent. Our method improves the popular extended instrumental variable (IVX) testing (Phillips and Lee,, 2013; Kostakis et al.,, 2015) in that, besides addressing the two bias effects found in Hosseinkouchack and Demetrescu, (2021), we find and deal with the variance-enlargement effect. We show that two types of higher-order terms induce these distortion effects in the test statistic, leading to significant over-rejection for one-sided tests and tests in multiple predictive regressions. Our improved IVX-based test includes three steps to tackle all the issues above regarding finite sample bias and variance terms. Thus, the test statistics perform well in size control, while its power performance is comparable with the original IVX. Monte Carlo simulations and an empirical study on the predictability of bond risk premia are provided to demonstrate the effectiveness of the newly proposed approach.

Keywords: Highly Persistent Predictors, Sample Splitting, Bias and Variance, Size Control, Bond Return Predictability.

1 Introduction

Testing the predictability of asset returns is the focal point of financial studies for different stakeholders, including academia, practitioners, and policymakers. However, the commonly used statistical inference suffers from size distortions due to the high persistence of (some) predictors and the contemporaneous correlations between the innovations of predictors and dependent variables (Campbell and Yogo,, 2006). The most popular method to solve this problem is the IVX (Phillips and Lee,, 2013; Kostakis et al.,, 2015), which aims to solve the over-rejection problem of the test statistics based on OLS.

Unfortunately, the IVX-based test (Phillips and Lee,, 2013; Kostakis et al.,, 2015) still has size distortion, which is magnified in empirically relevant finite samples, one-sided hypotheses, and multiple predictors cases. In Section 2, we show explicitly that the root of the oversized IVX statistic is not only the Deformation Effect (DE) and the Displacement Effect (DiE) (Hosseinkouchack and Demetrescu,, 2021; Demetrescu and Rodrigues,, 2022) but also the Variance Enlargement Effect (VEE). In closely related literature, Hosseinkouchack and Demetrescu, (2021) provided a structured approach to control the small sample noncentrality of the IVX -statistic for a given instrumental variable. Demetrescu and Rodrigues, (2022) combined the residual-augmented regression and the recursive demean method to remove the size distortion of IVX caused by higher-order terms. However, Hosseinkouchack and Demetrescu, (2021) did not consider the inference in multiple predictive regressions, while the recursive demean technique applied by Demetrescu and Rodrigues, (2022) would cause the inference to perform worse than our test in terms of power. Additionally, the inference by Hosseinkouchack and Demetrescu, (2021) and Demetrescu and Rodrigues, (2022) still suffers size distortion, as evidenced by their simulations. Xu and Guo, (2022) applied the Lagrange-multipliers principle to the joint test in multiple predictive models. Nevertheless, Xu and Guo, (2022) ignored the higher-order terms that generate the three effects mentioned above, and as a result, their test still suffered size distortions in many cases.

To our knowledge, no existing literature deals with the VEE in IVX test statistics in a single or multiple predictive regression. We show that, as the number of predictors increases, the VEE makes the IVX test statistic grow even bigger compared to its theoretical value. Therefore, ignoring the VEE leads to serious size distortion problems in multiple predictive regressions.

1.1 Main Results and Contributions

Our new three-step procedure (detailed in Section 3) improves the size control of IVX while keeping its good power performance:

-

1.

We entirely eliminate the DE using a novel sample splitting technique without loss of effective sample size. To do so, we use split (evenly from the middle time point) subsamples and obtain three IVX test statistics based on the full sample and two subsamples. The new test statistic is the weighted average of these three test statistics, effectively circumvents the higher-order term causing the DE.

-

2.

We considerably mitigate the DiE, which can cause the finite sample mean of the test statistic to deviate from the expected value of its asymptotic distribution. By subtracting the median of this displacement from the test statistic obtained in the first step, the location of the new test statistic and its asymptotic distribution become very close, thus reducing this displacement effect.

-

3.

The VEE can cause the sample standard deviation of the test statistic obtained in the second step to be greater than its asymptotic standard deviation. We divide the test statistic in the previous step by the ratio of the two (sample and the asymptotic) standard deviations. The standard deviation of the new test statistic and its asymptotic distribution are very close, thereby alleviating this effect.

Under some mild conditions detailed in Section 2, the test statistics converge to a standard normal or Chi-square distribution. For more robust inference in the finite sample, we combine the three steps for size control and the Lagrange-multipliers principle by Xu and Guo, (2022). The easy-to-implement procedure is summarized in Algorithm 1. Intensive simulation studies in the main text and Appendix are provided to demonstrate the effectiveness of the newly proposed approach.

In the empirical research, we revisit the predictability of the bond risk premia. Using forward rates, macroeconomic principal components, and their linear combinations as predictors of bond risk premia, we show that some of the predictors (especially the highly persistent ones) proposed by OLS or IVX (Phillips and Lee,, 2013; Kostakis et al.,, 2015) exhibit no predicting power on bond excess returns based on our test. Additionally, the effective predictors selected by our proposed test have strong economic implications, and these findings are notably different from the IVX test in Kostakis et al., (2015). The empirical results confirm that our newly developed test statistics are more reliable tools to test the predictability of financial returns. Our test should be helpful to practitioners.

The main contributions of the paper are summarized below.

-

1.

We address the distortion effects induced by the higher-order terms of IVX test statistics in a unified approach integrating univariate and multivariate models. We discuss the newly discovered VEE and show its accumulative nature in the finite sample as the number of predictors increases, which explains the lingering size distortion issue in the financial return predictability test literature. Our new test eliminates the DE and significantly reduces the DiE and VEE.

-

2.

The proposed inference procedure performs very well in size control while keeping the good power performance of the original IVX test. Compared to the literature, the proposed method has unique advantages for one-sided tests in the univariate model and joint and marginal tests in the multivariate model.

-

3.

From the empirical study perspective, our test sheds light on the significant variables to forecast one-year-ahead excess returns on bonds. Based on our test, the relatively longer-term forward rates are found to have little predicting power for the short-term bond excess return. The evidence also supports the market segmentation theory, which indicates that the long-term forward rates can not forecast the short-term bond excess return.

1.2 Brief Literature Review

There is a rich literature on the over-rejection problem in the inference of predictive regression with highly persistent predictors. Early literature such as Bonferroni’s method by Campbell and Yogo, (2006) and the conditional likelihood method by Jansson and Moreira, (2006) focused on the inference for the univariate model. Choi et al., (2016) introduced the Cauchy type instrumental variable approach for the test in univariate regression. Zhu et al., (2014) and Yang et al., (2021) proposed the weighted empirical likelihood approach with a good size control to test predictability in univariate and bivariate predictive models. To conduct inference in multiple predictive models, Elliott, (2011) and Breitung and Demetrescu, (2015) proposed the variable addition approach, but the power performance is unsatisfactory. Harvey et al., (2021) used the quasi-GLS demeaned predictor to develop easy-to-implement tests for return predictability in univariate models, displaying attractive finite sample size control and power. The IVX approach is proposed by Magdalinos and Phillips, (2009) and is also studied by Kostakis et al., (2015), Phillips and Lee, (2016), Yang et al., (2020), Demetrescu and Rodrigues, (2022), Hosseinkouchack and Demetrescu, (2021) and Liu and Phillips, (2023). In the studies of forecasting bond risk premia, Bauer and Hamilton, (2018) proposed a bootstrap procedure to test the predictability of bond risk premia with highly persistent predictors. However, it still tends to over-reject and does not offer the asymptotic property of the bootstrap procedure. Fan et al., (2021) proposed an augmented factor model and applied their method to forecast the excess return of U.S. government bonds.

The rest of this paper is organized as follows. Section 2 introduces the higher-order terms causing the distortion effects of IVX test statistics. Section 3 provides the procedures to construct the test statistics and presents the asymptotic theories for the proposed estimators and the test statistics. Section 4 reports the Monte Carlo simulation results. Section 5 presents the empirical application. Section 6 concludes the paper. The online Appendix contains detailed proofs of the theoretical results, extra simulations, and additional empirical results.

Throughout this paper, SD, WD refer to strong and weak dependence, respectively. The symbols , and are used to represent weak convergence and convergence in distribution and in probability, respectively. All limits are for in the limit theories, and is stochastically asymptotically bounded while is asymptotically negligible. For any matrix , is a matrix defined as , in which is the matrix whose th column is the eigenvectors of , and , are the eigenvalues of . It implies that . Also, we define . is a zero vector with dimension K and is a identity matrix.

2 IVX-based Test and the Higher-order Terms

We are interested in testing the predictability of , such as bond or stock returns, in a unified framework with univariate or multivariate predictors. Without loss of generality, we discuss the following multiple predictive regression model

| (1) |

where . The model is also studied by Phillips and Lee, (2013); Kostakis et al., (2015). The highly persistent variables are modeled as follows

| (2) |

where , , , , , and or 1, is the dimension of . We assume no cointegration relationship exists among . Two types of persistence with different values of and are considered: (1) Strong Dependence [SD]: and is a constant; (2) Weak Dependence [WD]: and . 111 We also permit with to have mixed types of persistence; that is to say, could be a function of . In this setting, the theoretical results for the test statistics are almost the same. Define , which is the information set available at time . Here, following Kostakis et al., (2015), a general weakly dependent innovation structure of the linear process on in equations (1) and (2) is imposed as follows.

Assumption 1.

Define as martingale difference sequence222For SD predictors, could be extended from m.d.s. to the linear process. with respect to the natural filtration , which satisfies

| (3) |

for some , where is a positive definite matrix. Assume is a stationary linear process given by

Here, , is the dimension of (), and is a sequence of constant matrices such that is of full rank and . The process is strictly stationary ergodic satisfying

| (4) |

Remark 1.

As specified by Kostakis et al., (2015), the sequence permits the following GARCH(p,q) representation:

| (5) |

where is an i.i.d. (0,1) sequence. is a positive constant. And and are non-negative constants satisfying .

Under Assumption 1, the functional central limit theorem (FCLT) for holds by Phillips and Solo, (1992),

| (8) |

where is a vector of Brownian motions and , and . Under Assumption 1, the following result holds by equation (8), Phillips, (1987) and Kostakis et al., (2015),

| (9) |

for SD predictors, where .

Following Phillips and Lee, (2013), the standard IVX is set to be less persistent than SD predictors to obtain the asymptotic mixture normal distributed estimator . Specifically, we have

| (10) |

where , and

| (11) |

where , and .

In the following, we expand on Proposition 1 of Hosseinkouchack and Demetrescu, (2021), which focuses on univariate models, and point out two higher-order terms in multivariate models. We define the random vector to analyze the DE, DiE and VEE of the original IVX (Kostakis et al.,, 2015; Phillips and Lee,, 2013) in a unified (univariate or multivariate) model,333When , under the null hypothesis , becomes the t-test statistic defined by Hosseinkouchack and Demetrescu, (2021). The three effects exist in univariate models. since the original IVX test statistic is the function of under the null hypothesis , where is a predetermined matrix with the rank , is a predetermined vector with dimension , and .

To show the following proposition, we define the normalized instrumental variable , where for SD predictors and for WD predictors.

Proposition 1.

Under Assumption 1, the following results hold for SD predictors.

| (12) | |||||

| (13) | ||||

| (14) |

| (15) | ||||

where , , is a zero vector with dimension K and is a identity matrix.

Remark 2.

2.1 The DE, DiE and VEE

Three critical points are drawn from Proposition 1. First, similar to Hosseinkouchack and Demetrescu, (2021), the higher-order term comes from the correlation between the terms and in the random vector . Meanwhile, the higher-order term comes from in .

Second, with SD predictors, the higher-order term leads to not only the DiE shown in equation (14) but also the VEE shown in equation (13). The DiE causes the center of the finite sample distribution of to deviate from zero to , which makes the one-sided test of the original IVX to suffer from size distortion (Hosseinkouchack and Demetrescu,, 2021). The VEE causes the covariance matrix of in the finite sample to be enlarged by the higher-order term so that the test statistics is enlarged, which is shown in Theorem 1. Specifically, equation (13) shows that the covariance matrix of in the finite sample is approximately

| (16) |

Therefore, the covariance matrix of in the finite sample is closer to than that of , where and . As a result, the finite sample distribution of the new IVX test statistic

based on is much closer to than that of the original IVX test statistic based on .

The following theorem shows that is positive, and VEE aggravates as K increases.

Theorem 1.

By Theorem 1, as the number of predictors grows, VEE becomes more severe since grows bigger. This causes the original IVX to suffer severe size distortion in multiple predictive models.

Third, equation (15) shows that the higher-order term leads to the DE, meaning that the finite sample distribution of deviates significantly from the normal distribution.

In summary, the DiE, VEE, and DE induced by the higher-order terms and in Proposition 1 explain why the IVX test (Kostakis et al.,, 2015; Phillips and Lee,, 2013) suffers size distortions for one-sided tests and tests in multivariate predictive regression. A straight-forward idea to eliminate the effects of and is to subtract their consistent estimators from . However, it is not an easy task to eliminate the effect of since it arises from which could not be estimated consistently.

3 The Improved IVX Test

3.1 A Sample Splitting Procedure to Eliminate the DE

To eliminate the size distortion induced by the higher-order term in Proposition 1, we apply a sample splitting procedure to remove the term in test statistics, which is the source of DE. Intuitively, we split the full sample into two subsamples and construct the IVX estimators based on the full sample and the two subsamples. By setting appropriate weights, the new estimator, which is the weighted sum of the three estimators (full sample, two subsamples), does not contain . As a result, the DE is eliminated by the following steps.

We split the full sample into two subsamples and , where and is a constant. In practice, we suggest evenly split to subsamples such that , whose reason is further specified by Remark 6 in subsection 3.2. First, we define the IVX estimators based on two subsamples as follows.

| (17) | ||||

| (18) |

where , . Second, we apply equations (1), (10), (17) and (18) to obtain the following equations.

| (19) | ||||

| (20) | ||||

| (21) |

By equations (20) and (21), the following equations hold.

| (22) | ||||

| (23) |

where

| (24) | ||||

By subtracting the sum of equations (22) and (23) from equation (19), the term of in equation (10) is removed as follows.

| (25) | ||||

where , , and

| (26) |

Third, we could utilize another instrumental variable estimator with the IV . Define the IV estimator as follows.

| (27) |

By equations (25) and (27) and that , it follows that

| (28) |

The key and desirable property of the new instrumental variable is

| (29) |

Thus could be deemed the instrumental variable estimator using as IV,

Therefore, the higher-order term vanishes, since the term disappears in .

Theorem 2.

Under Assumption 1, for SD and WD predictors, it follows that

where for SD predictors and for WD predictors and , where for SD predictors and for WD predictors and

| (30) | ||||

Then the test statistic is constructed for the null hypothesis .

| (31) |

where 444We use the heteroskedasticity consistent estimator similar to that of (MacKinnon and White,, 1985). and .

Remark 3.

Following the literature, is estimated by OLS, which has a smaller variance than that of the IV estimator for . Besides the higher-order terms and , Xu and Guo, (2022) argue that the estimation error of also causes the size distortion. Moreover, the variance of unconstrained OLS estimator increases with . To avoid size distortion induced by the uncertainty of the estimators of , we apply the Lagrange-multipliers principle (Xu and Guo,, 2022) to obtain the constrained OLS estimator as follows.

and . Since the procedure to obtain uses the information of the null hypothesis , the estimator is more efficient than the unconstrained OLS estimator. As a result, the size performance of is much better than the case in which the Lagrange-multipliers principle is not applied.

Moreover, we construct the t-test statistic when for right side test vs and left side test vs .

| (32) |

Note that when .

Theorem 3.

Under Assumption 1 and the null hypothesis , one can show that the limiting distribution of the test statistics and are the standard normal and the -distribution with degrees of freedom, respectively.

Then, the local power of with is shown as follows.

Theorem 4.

3.2 Methods to Reduce DiE and VEE

The asymptotically -distributed test statistic still suffers size distortion due to the DiE and VEE in . To analyze these effects, we define the random vector as follows.

Note that

| (33) |

Thus by equations (31) and (33), is the function of under the null hypothesis . Therefore, we can analyze and reduce DiE and VEE in by analyzing and reducing those in .

To analyze the higher-order term of , we define the random vector based on the first subsample as

and the random vector based on the second subsample as

The random vectors and are used to show the property of the higher-order terms of . Since does not contain , it only contains the higher-order terms similar to . Therefore,

| (34) |

where and

| (35) |

where . Also, notice that under the null hypothesis , it follows that

| (36) |

where and

We can apply equation (36) to construct the higher-order terms of by the higher-order terms of and shown in equations (34) and (35). Define the normalized instrumental variable . Then the following proposition holds.

Proposition 2.

Under Assumption 1, for SD predictors, the following equation holds as ,

where And

| (37) | ||||

| (38) |

where and

where , and satisfying and .

Remark 4.

The term could be regarded as the “residual term” of since it is the weighted sum of two terms whose expectation is zero. Therefore, is the main source of DiE induced by rather than the term .

Proposition 2 shows that the higher-order term leads to not only the DiE but also the VEE in multivariate models. Due to the DiE, the center of the distribution of in the finite sample deviates from zero vector, while the covariance matrix of in the finite sample is closer to rather than .

First, we try to reduce the DiE. Although Remark 4 shows that the higher order term ’s term is the main source of size distortion, the operation that subtracting by could not eliminate the size distortion caused by the higher order term . The main reason is as follows. converges to a function of Brownian Motion rather than a constant. So the covariance matrix of the random vector does not vanish even when the sample size goes to infinity. As a result, the finite sample covariance matrix of is non-negligible since its rate converging to zero is very slow. This non-negligible finite sample covariance matrix of leads that the finite sample covariance matrix of significantly deviates from its asymptotic covariance matrix . This deviation causes the size distortion of the test statistic constructed by .

To reduce the size distortion arise from , we subtract by the estimator of , which is equal to . We construct the random vector as follows.

| (39) |

where is the consistent estimator of . Note that , and are the consistent estimators of , and , respectively.

In the following, we illustrate why the DiE is reduced in in the following aspects. First, by equation (39) and Proposition 2, it is straightforward that

| (40) |

where and thus

| (41) |

Second, we show that the distorting effect of for the size is much smaller than that of in the following aspects. By Proposition 2, it follows that is negative definite matrix and . Therefore, the size distortion induced by is smaller than that of . As a result, the size distortion induced by is smaller than .

Remark 5.

The intuition of the size distortion induced by is smaller than that of can be easier to see using an example of a univariate model. First, when , which implies that the median of is approximately 0. Moreover, such that is bounded. It implies that is much smaller than generally, which means DiE is reduced significantly in .

Remark 6.

However, VEE still exists in since

| (42) | ||||

Equation (42) holds since induced by equation (39). To eliminate the VEE, the random vector is constructed as follows.

| (43) |

where , and

By equations (1), (33), (39) and (43), the estimator for is defined as

| (44) |

where and We apply the following estimator for the asymptotic distribution of to reduce VEE of IVX.

| (45) |

Then we define the test statistics for .

| (46) |

Proposition 3.

Under Assumption 1 and the null hypothesis , for SD predictors, it follows that

Thus far, the DE is eliminated for SD predictors in the finite sample, and the DiE and VEE are reduced significantly in .

On the other hand, the asymptotic property of and is the same as that of and by equation (44), which is shown as follows.

Theorem 5.

Under Assumption 1, for SD and WD predictors, it follows that

By Theorem 5, the asymptotic distribution of the test statistic is the same as that of , which is shown as follows.

Theorem 6.

Under Assumption 1 and the null hypothesis , one can show that the limiting distribution of is the -distribution with degrees of freedom.

Although performs well in terms of size with SD predictors in the finite sample, it suffers size distortion with WD predictors since the terms to reduce the DiE and VEE for the case with SD predictors are redundant terms with WD predictors. To avoid size distortion with WD predictors, we construct the test statistics by the following steps. First, the weight is introduced such that for SD predictors555We put in such that the weight is closer to one in the finite sample with more predictors. Therefore, the size control is improved since the DiE and the VEE are reduced sufficiently. while for WD predictors, where is the consistent estimator of for the predictor . Then the proposed estimators and the test statistics are given as follows.

| (47) | ||||

| (48) | ||||

| (49) |

where and .

Since for SD predictors and for SD predictors, we have . By this result and Proposition 3, we have the following proposition.

Proposition 4.

Under Assumption 1 and the null hypothesis , for both SD and WD predictors, it follows that

By Proposition 4, the finite sample property of with SD predictors is similar to that of rather than that of . Thus with SD predictors still has the nice finite sample property of discussed earlier. Meanwhile, the finite sample property of with WD predictors is similar to that of rather than that of . Thus is free of the redundant terms of with WD predictors. Therefore, is free of size distortion for both joint and marginal tests in multiple models with both SD and WD predictors.

Next, we present the one-sided test for , that is constructed by setting the rank of matrix to be one and . So we construct the t-test statistic for right side test vs and left side test vs .

| (50) |

Note that when . By similar arguments for the nice property of , performs well in terms of size for one-sided tests in both univariate and multiple models.

By equation (43) and that , we have

| (51) |

Therefore, the limiting distribution of the t-test statistic with and Wald type test statistic with under the null hypothesis is stated in the following theorem with its detailed proof given in the Appendix.666Our procedure works for univariate models as well since is equal to the t-test statistic for univariate model when .

Theorem 7.

Under Assumption 1 and the null hypothesis , the limiting distribution of the t-test statistic with and those of Wald type test statistic are the standard normal distribution and the -distribution with degrees of freedom, respectively.

We summarize our procedure in Algorithm 1 below.

-

•

Reduce the DiE: Construct the estimator , where .

-

•

Reduce the VEE: Construct the estimator for the asymptotic covariance matrix of as , where .

-

•

Reduce the size distortion induced by the variance of the estimator of : Use Lagrange-multiplier principle to obtain by the constrained OLS estimation .

4 Monte Carlo Simulations

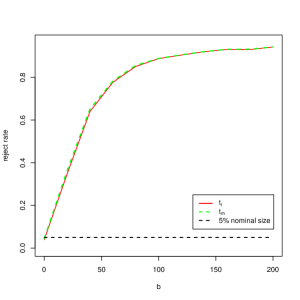

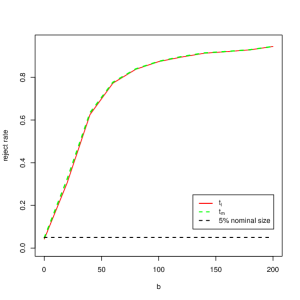

We demonstrate the effectiveness of the proposed procedure using a multivariate case. We report the results for 1) the joint test vs ; 2) the marginal test (two-sided) vs ; 3) the marginal test (one-sided) vs and vs .

The DGP of and is equation (1), (2) and (5), in which and . The DGP of the innovations is as follows: , where . Thus the contemporaneous correlation coefficient between and is , which is the source of the size distortion of the standard IVX test statistics (Kostakis et al.,, 2015; Phillips and Lee,, 2013) and DiE and VEE shown in Proposition 1. We report the simulation results for a GARCH model with , , and the sample with the nominal size . 777To save space, we did not report the simulation results for GARCH model with the sample size and and ARCH and i.i.d. model with the sample size , and in the paper, which is similar to the result of GARCH model with the sample size . The codes and results are available upon request. Simulation is repeated times for each setting. Set in Table 2 and and for all Tables. 888This setting (choice of ) is not exactly the same as the IVX of Phillips and Lee, (2013), in that it makes the instrumental variable become less persistent as the number of predictors K grows bigger. Therefore, in this setting, we can see the advantages of our test even when the predictors are less persistent, but the VEE is nonetheless significant (see discussions after Proposition 1).

First, the results for the size and power performances of the proposed test statistics and for joint test are shown in Table 2 in which and . Second, the size and power performances of the proposed test statistics and for two-sided marginal test vs and right side marginal test vs are shown in Panel A and Panel B of Table 1, in which . The first column of Panel A and Panel B of Table 1 and the third column of Table 2 are the size results while the others are power results. In these models, we set , where . We show the simulation results for , and thus the contemporaneous correlation coefficient between and are and .

We have the following findings from Tables 1 and 2. First, for the joint test , the proposed test statistic still suffers size distortion with multiple predictors () and the size distortion grows bigger as the number of predictors K grows bigger. Meanwhile, the proposed test statistic is almost free of size distortion in different settings. It is because still suffers from DiE and VEE while does not. Second, the size performance of is better than that of although suffers small-scale size distortion for two-sided marginal test vs and right side marginal test vs . Specifically, the size performances of and are comparable for right side marginal test , while the size performance of is much better than that of for two-sided marginal test vs . Third, the power performances of and are comparable and quite well.

We also conduct other experiments (a univariate case and other settings of multivariate cases, e.g., for different ’s) for the robustness of our conclusions. These results are reported in the Appendix. We obtain a similar conclusion there.

| Tests | Panel A: vs | Panel B: vs | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

| i=1 | 7.3 | 59.8 | 83.7 | 89.7 | 93.1 | 93.9 | 94.8 | 95.4 | 96.0 | 8.1 | 67.3 | 86.8 | 91.6 | 94.2 | 94.8 | 95.8 | 96.1 | 96.8 | |

| i=2 | 6.8 | 39.4 | 74.1 | 86.6 | 90.8 | 92.4 | 94.6 | 94.8 | 95.5 | 5.9 | 49.3 | 79.4 | 89.0 | 92.5 | 93.6 | 95.4 | 95.7 | 96.1 | |

| i=3 | 7.0 | 40.8 | 69.3 | 80.2 | 85.9 | 87.0 | 88.8 | 89.7 | 91.0 | 5.5 | 48.3 | 74.2 | 83.7 | 88.1 | 89.0 | 90.6 | 91.7 | 92.4 | |

| i=4 | 6.8 | 48.2 | 82.0 | 90.4 | 94.0 | 95.2 | 95.9 | 96.6 | 96.5 | 5.5 | 57.4 | 85.5 | 92.3 | 95.0 | 96.1 | 96.4 | 97.2 | 97.0 | |

| i=5 | 5.9 | 27.6 | 65.9 | 84.8 | 90.9 | 93.3 | 94.6 | 95.8 | 96.3 | 5.7 | 37.3 | 73.3 | 88.2 | 92.9 | 94.7 | 95.5 | 96.6 | 97.0 | |

| i=6 | 5.7 | 22.8 | 60.0 | 81.0 | 89.3 | 93.2 | 94.3 | 95.7 | 96.5 | 5.5 | 32.2 | 68.4 | 85.5 | 91.5 | 94.7 | 95.5 | 96.5 | 97.1 | |

| i=7 | 5.4 | 15.8 | 45.7 | 71.0 | 84.5 | 90.3 | 93.1 | 94.8 | 95.6 | 4.9 | 23.7 | 56.2 | 77.8 | 88.0 | 92.4 | 94.5 | 95.8 | 96.3 | |

| i=8 | 6.7 | 30.7 | 68.7 | 84.7 | 90.5 | 93.1 | 94.8 | 95.5 | 95.8 | 6.2 | 39.8 | 75.8 | 87.9 | 92.3 | 94.3 | 95.6 | 96.2 | 96.5 | |

| i=9 | 5.6 | 18.1 | 48.8 | 73.7 | 86.1 | 91.3 | 93.9 | 94.8 | 95.9 | 5.4 | 26.8 | 59.0 | 80.3 | 89.5 | 93.2 | 95.0 | 95.6 | 96.7 | |

| i=10 | 6.1 | 20.7 | 54.7 | 76.6 | 87.8 | 91.9 | 94.0 | 95.3 | 96.3 | 5.7 | 29.8 | 64.1 | 82.3 | 90.7 | 93.6 | 95.2 | 96.2 | 96.9 | |

| i=1 | 6.3 | 58.5 | 82.8 | 89.4 | 92.7 | 93.6 | 94.7 | 95.2 | 95.7 | 7.8 | 65.9 | 86.4 | 91.3 | 94.1 | 94.6 | 95.6 | 95.9 | 96.5 | |

| i=2 | 6.0 | 37.7 | 72.8 | 86.1 | 90.2 | 92.0 | 94.3 | 94.6 | 95.3 | 5.5 | 47.5 | 78.4 | 88.5 | 92.1 | 93.3 | 95.3 | 95.5 | 96.0 | |

| i=3 | 6.3 | 38.3 | 67.8 | 79.3 | 85.2 | 86.6 | 88.5 | 89.3 | 90.6 | 5.1 | 46.8 | 73.2 | 82.8 | 87.7 | 88.6 | 90.2 | 91.2 | 92.2 | |

| i=4 | 6.1 | 50.0 | 82.3 | 90.3 | 93.7 | 95.0 | 95.8 | 96.4 | 96.4 | 6.4 | 59.4 | 85.4 | 92.2 | 94.8 | 95.9 | 96.3 | 97.1 | 97.0 | |

| i=5 | 5.4 | 29.0 | 66.4 | 84.5 | 91.0 | 93.0 | 94.5 | 95.7 | 96.2 | 6.6 | 39.1 | 74.0 | 88.1 | 92.7 | 94.4 | 95.5 | 96.4 | 96.9 | |

| i=6 | 5.2 | 24.1 | 61.2 | 81.1 | 89.3 | 93.2 | 94.3 | 95.6 | 96.4 | 6.5 | 34.2 | 69.6 | 85.7 | 91.7 | 94.6 | 95.4 | 96.4 | 97.0 | |

| i=7 | 5.4 | 17.7 | 47.9 | 72.3 | 84.7 | 90.4 | 93.1 | 94.9 | 95.5 | 6.0 | 26.2 | 58.3 | 78.8 | 88.6 | 92.6 | 94.5 | 95.8 | 96.4 | |

| i=8 | 5.8 | 30.0 | 67.8 | 84.4 | 89.9 | 92.8 | 94.7 | 95.3 | 95.6 | 6.1 | 39.6 | 74.9 | 87.5 | 91.9 | 94.1 | 95.6 | 96.0 | 96.4 | |

| i=9 | 5.4 | 18.3 | 48.5 | 73.5 | 85.5 | 90.9 | 93.5 | 94.6 | 95.7 | 5.7 | 27.4 | 59.3 | 79.8 | 89.1 | 93.0 | 94.8 | 95.6 | 96.6 | |

| i=10 | 5.5 | 19.6 | 52.8 | 75.5 | 86.9 | 91.5 | 93.5 | 94.9 | 96.1 | 5.5 | 29.0 | 62.9 | 81.2 | 90.0 | 93.3 | 95.0 | 95.9 | 96.8 | |

To sum up, the proposed test statistics and with perform quite well in terms of both size and power in multivariate models. Thus, we recommend that empirical researchers apply our test statistics and and set .

Statistics 0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 K=2 6.0 23.2 60.9 79.6 88.7 92.2 94.3 95.9 96.6 4.9 19.0 55.3 76.8 87.2 91.3 93.6 95.5 96.4 K=3 6.6 15.8 42.3 67.7 82.4 90.3 93.6 96.1 96.9 4.4 12.4 37.5 63.7 80.1 88.9 92.7 95.6 96.4 K=4 7.1 17.2 51.8 76.9 89.8 95.6 97.7 98.6 99.3 4.6 19.1 55.6 79.0 90.8 96.3 97.7 98.7 99.3 K=5 6.9 16.6 46.6 74.4 87.3 95.5 97.4 98.9 99.6 4.8 18.0 51.3 77.7 89.0 96.1 97.7 99.0 99.6 K=6 7.1 14.3 41.4 67.8 86.0 93.7 97.5 98.4 99.2 4.5 15.6 45.8 72.8 88.3 94.9 97.9 98.5 99.3 K=7 6.4 12.6 34.0 61.9 79.7 90.1 95.2 98.0 99.2 4.5 13.5 39.5 67.3 84.1 91.9 96.2 98.3 99.3 K=8 7.0 12.6 31.8 57.3 77.0 89.1 95.1 97.9 98.8 4.8 12.9 36.1 63.3 81.2 91.3 96.2 98.3 99.0 K=9 7.3 10.6 25.8 49.3 72.3 85.5 92.2 96.6 98.2 5.1 11.0 30.6 56.0 77.0 88.9 94.2 97.4 98.8 K=10 7.5 9.6 21.8 43.5 64.5 79.1 88.4 94.1 97.2 4.4 9.8 25.6 50.2 70.5 83.8 91.4 95.5 97.6

5 Robust Inference for Bond Risk Premia

Prediction of bond risk premia is crucial for monetary policy and investment decisions. Following the literature (Cochrane and Piazzesi,, 2005), we use the excess log return of n-year U.S. discount bond rx(n), where , as the left-hand side variable. We reexamine the predictability of five bond forward rates F1-F5 (Cochrane and Piazzesi,, 2005) and the first eight macroeconomic principal components M1-M8 (the , in Ludvigson and Ng,, 2009) constructed by 132 macro variables in a multiple predictive regression model. Specifically, the forward rate F1 is the log price of the one-year discount bond; and the forward rate Fn of n-year (n=2,…5) bond is the log price difference between (n-1)-year bond and n-year bond.999The dataset used in this section is from the Fama-Bliss database available on CRSP, and the macroeconomic factors are from the Link of Ludvigson and Ng, (2009). Our main sample period is 1964:01-2003:12, which is the same used in the aforementioned literature. We present the test statistics and the corresponding p-values in parenthesis marked with , , implying the rejection of the null hypothesis at the 10%, 5%, and 1% levels. We also conduct empirical studies on A1) reexamining the three linear combinations of F1-F5 and M1-M8, which include CP (Cochrane and Piazzesi,, 2005) constructed by F1-F5 and LN1, LN2 (the F5, F6 in the original paper of Ludvigson and Ng,, 2009) constructed by M1-M8; and A2) evaluating the predictability during the pandemic period 2020:01-2022:12. Due to space limitations, we put the more details of these two studies in Appendix C.

Sample studied in Ludvigson and Ng, (2009) (1964:01-2003:12) Variables F1 F2 F3 F4 F5 CP M1 M2 M3 M4 M5 M6 M7 M8 LN1 LN2 0.996 0.997 0.997 0.996 0.997 0.980 0.760 0.306 0.563 0.458 0.581 0.554 0.185 0.203 0.793 0.900 Sample during the Covid-19 epidemic period (2020:01-2022:12) Variables F1 F2 F3 F4 F5 CP M1 M2 M3 M4 M5 M6 M7 M8 LN1 LN2 0.995 0.993 0.991 0.992 0.992 0.990 0.307 0.257 -0.22 0.531 0.373 0.312 0.092 0.337 0.326 0.371

The predictors’ persistence parameters ’s are reported in Table 3. It shows that F1-F5 and CP are likely the SD predictors, while the rest of the variables are likely to be WD predictors. Therefore, applying our robust testing procedure is necessary to avoid the spurious predictability induced by the size distortion discussed earlier. We show the testing results using F1-F5 and M1-M8 as regressors in Table 4. This is helpful for practitioners to discover which component of CP, the LN1 and LN2 plays a vital part in predicting the bond excess returns.

We discuss the main results as follows. First, our method shows less significance (of predictability) than the original IVX (Kostakis et al.,, 2015; Phillips and Lee,, 2013) and Ludvigson and Ng, (2009). This aligns with the theoretical results in Section 3 that our method improves the size control performance of the original IVX by reducing the distortion effects of the higher-order terms. Our approach does not detect some predictability of F1-F5 and M1-M8 found by IVX and test statistics based on OLS. At the same time, all predictability of F1-F5 and M1-M8 found by our method are also detected by IVX and test statistics based on OLS except for the predictability of F5 for rx(5). Our test also finds that the linear combinations predictors CP, LN1 and LN2 have predicting power for the one-year bond excess returns at all maturities in the main sample period (with higher p-values than the IVX). During the pandemic period of 2020:01-2022:12, our test does not reject the null that CP, LN1 and LN2 have no predictability at all maturities, contrary to the OLS and IVX tests, where the former almost rejects all null hypotheses, and the latter finds CP to have predictability. The details are shown in Table C1 of the Appendix.

| Predictors | IVX | OLS | IVX | OLS | IVX | OLS | IVX | OLS | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| F1 | 0.0*** | 0.0*** | 0.0*** | 0.0*** | 0.0*** | 0.0*** | 16.2 | 0.0*** | 0.0*** | 35.0 | 0.0*** | 0.1*** |

| F2 | 0.0*** | 0.2*** | 0.0*** | 87.1 | 64.2 | 52.1 | 49.7 | 59.0 | 41.6 | 33.4 | 69.7 | 49.1 |

| F3 | 23.4 | 1.42** | 10.4 | 7.8* | 0.0*** | 0.0*** | 88.2 | 0.0*** | 39.5 | 27.0 | 1.1*** | 20.7 |

| F4 | 92.5 | 72.3 | 40.4 | 87.2 | 72.1 | 67.0 | 0.3*** | 8.4* | 0.0*** | 20.1 | 33.8 | 0.7*** |

| F5 | 14.4 | 90.4 | 31.6 | 27.9 | 54.8 | 94.4 | 63.3 | 84.8 | 19.2 | 0.2*** | 15.2 | 0.0*** |

| M1 | 0.0*** | 0.6*** | 0.0*** | 0.5*** | 0.0*** | 0.0*** | 1.4** | 0.4*** | 0.0*** | 0.9*** | 0.4*** | 0.0*** |

| M2 | 12.8 | 28.9 | 38.2 | 26.0 | 92.4 | 20.1 | 37.3 | 97.3 | 24.1 | 49.2 | 86.6 | 21.8 |

| M3 | 3.3** | 0.3*** | 0.0*** | 9.4* | 0.4*** | 0.0*** | 10.7 | 1.7** | 0.0*** | 9.9* | 2.2** | 0.0*** |

| M4 | 0.3 | 0.2*** | 2.6** | 50.5 | 0.9*** | 8.5* | 48.0 | 0.1*** | 1.6** | 34.4 | 0.6*** | 5.1** |

| M5 | 6.8* | 4.8** | 0.2*** | 10.4 | 15.9 | 0.3*** | 5.6* | 21.6 | 0.0*** | 10.4 | 6.3** | 0.0*** |

| M6 | 58.7 | 24.8 | 48.2 | 89.8 | 16.5 | 56.0 | 73.2 | 87.2 | 95.1 | 77.5 | 20.0 | 73.7 |

| M7 | 0.3** | 0.2** | 0.0*** | 0.3*** | 0.0*** | 0.0*** | 0.7*** | 0.1*** | 0.0*** | 2.2** | 0.0*** | 0.0*** |

| M8 | 13.0 | 17.0 | 5.0** | 21.8 | 54.3 | 15.6 | 25.4 | 98.9 | 40.5 | 18.9 | 84.4 | 33.3 |

From the economic perspective, our empirical result in Table 4 supports the market segmentation theory (D’Amico and King,, 2013; Foley-Fisher et al.,, 2016; Greenwood et al.,, 2018). The market segmentation theory points out that short and long-term securities are not perfectly substitutable, and the short-term bond risk premia could only be predicted by the short-term forward rates and, similarly, the long-term forward rates for long-term bond risk premia. In the main sample, our findings parallel the studies of (Ludvigson and Ng,, 2009) that CP, LN1 and LN2 can predict the expected one-year excess return on bonds (see the Appendix for details). However, during the pandemic, the bond return is more likely to be driven by aggressive monetary policies and epidemic shocks (Goldstein et al.,, 2021; Levine et al.,, 2021), which hamper the predicting power of CP, LN1 and LN2. Our test can detect the spurious predictability of CP, LN1 and LN2 in forecasting excess bond returns under different macroeconomic scenarios, while IVX and OLS do not.

6 Conclusion

This paper improves the popular IVX testing (Kostakis et al.,, 2015; Phillips and Lee,, 2013) by addressing not only DE and DiE, pointed out by Hosseinkouchack and Demetrescu, (2021), but also VEE which cannot be ignored, especially in multiple predictive regressions. We introduce a three-step method to deal with all the aforementioned issues regarding finite sample bias and variance-inflating terms. As a result, the size performance of the proposed method for the one-sided test and the test in multiple predictive regressions is improved significantly, while the power performance is comparable with the original IVX. Numerical simulations demonstrate the effectiveness of the newly proposed approach. Moreover, an empirical study of the predictability of bond returns shows that the original IVX rejects the null more often than our method, which supports the theoretical results that our procedure reduces the size distortion induced by the higher-order terms of IVX.

SUPPLEMENTARY MATERIAL OF “ROBUST INFERENCE FOR MULTIPLE PREDICTIVE REGRESSIONS WITH AN APPLICATION ON BOND RISK PREMIA”

A Proofs

To help the readers navigate the testing procedure in the main text, we first explain the names of important test statistics.

- Explanation about test statistics’ subscripts in the main text:

-

Here we use as the general notation of a test statistic. The subscript ‘ivx’ in the random vector (or scalar) is to show is constructed by the method of the original IVX (Kostakis et al.,, 2015). The subscript ‘a’ in the random vector (or scalar) is to show is constructed by time series in the duration of the first subsample, while the subscript ‘b’ in the random vector (or scalar) is to show is constructed by time series in the duration of the second subsample. The subscript ‘l’ in the random vector (or scalar) is to show is constructed after the procedure that DE is eliminated. The subscript ‘n’ in the random vector (or scalar) is to show is constructed after the procedure that DE is eliminated and DiE is reduced. The subscript ‘m’ in the random vector (or scalar) is to show is constructed after the procedure that DE is eliminated and both DiE and VEE are reduced.

Then, we give the proofs of the theoretical results. Then, we give the proofs of the theoretical results. The equation numbers refer to those in the main text. The new numbered equations in this appendix have the prefix A before the numbers, such as ‘A1’.

Proof of equation (29).

Lemma 1.

Under Assumption 1, for SD and WD predictors, it follows that

| (A2) |

Proof of Lemma 1.

First, we consider the case with SD predictors. To begin with, we first prove that follows asymptotically normal distribution. To this aim, we need to prove that

for any real vector and with dimension K and use the Cramer-Wold device. Define

| (A3) |

Then . Note that is a martingale difference sequence. So we need to verify the Lindeberg condition specified by Corollary 3.1 of Hall and Heyde, (1980) as follows

In the following part, we will prove this equation. By equation (A3) and Cauchy-Schwarz inequality, it follows that

| (A4) | ||||

It is straightforward that both events and implies . So we have

| (A5) | |||

| (A6) |

And

| (A7) |

By equations (A4), (A5), (A6) and (A7), it follows that

| (A8) | ||||

By part (ii) of Lemma 5.2 of the proof of the Online Technical Supplement to Phillips and Lee, (2013), we have

| (A9) |

By equations (A8) and (A9), the following Lindeberg condition holds.

| (A10) |

Next, we verify the stability condition for . By equation (11), it is known that

Thus

| (A11) | ||||

The last step of the above equation holds since , and by Online Appendix of Kostakis et al., (2015) and . Similarly,

| (A12) |

By equations (A3), (A11) and (A12), the following stability condition holds.

| (A13) | ||||

By equations (A10) and (A13), Corollary 3.1 of Hall and Heyde, (1980) yields the following results.

| (A14) | ||||

for any real vectors and . By the Cramer-Wold device and equation (A14), for SD predictors, we have

| (A15) |

Similarly, for WD predictors, we also have

| (A16) |

By equation (30), it follows that

| (A17) |

where the joint convergence is guaranteed by that both and are the function of . And by the proof of part (i) of Proposition A1 and Lemma 3.2 of Phillips and Magdalinos, (2009), the joint convergence of and applies. As a result, considering that is the function of , the joint convergence of and holds.

Lemma 2.

Under Assumption 1, for SD and WD predictors, we have

Proof of Lemma 2.

Following the similar procedure for the stability condition shown in equation (A13) for of Proof for Lemma 1, Lemma 2 is proved.

∎

Lemma 3.

Under Assumption A.1 and the condition , by Taylor expansion of matrix (Deadman and Relton,, 2016), we have

| (A18) | ||||

And

| (A19) | ||||

Proof Lemma 3.

By online appendix of Kostakis et al., (2015), it follows that

| (A20) | ||||

Thus

| (A21) |

By equation (A21) and continuous mapping theorem, the equation about determinant holds as follows.

| (A22) |

Additionally,

| (A23) |

where , is the singular value of . By equations (A22) and (A23) and that , it follows that

| (A24) |

On the other hand, following the similar procedure of Hosseinkouchack and Demetrescu, (2021), we have

| (A25) |

By Lemma 3 and (A25), equation (A18) holds. Also, by the similar procedure, equation (A19) is proved.

∎

Proof of Proposition 1.

We consider the higher order terms induced by the SD predictors. By equation (11), it follows that

| (A26) |

where . We define and thus and

| (A27) | |||

Then by equation (A18) in Lemma 3, we have

| (A28) |

where

and

By the online appendix of Kostakis et al., (2015) and the continuous mapping theorem, it is known that .

Since , then

| (A29) | ||||

And

| (A30) | ||||

Let , with and

We work out first. By the proof of Hosseinkouchack and Demetrescu, (2021),

Then for , it follows that

| (A31) | ||||

Thus by the independence of innovations and equation (A27), it follows that

| (A32) | ||||

The last four lines of equation (A32) hold since is a scalar and .

And by equations (S.2)-(S.5) of the appendix of Hosseinkouchack and Demetrescu, (2021), we have

| (A33) |

Then by equations (A32) and (A33), it follows that

| (A34) | ||||

On the other hand,

| (A35) | ||||

Proof of Theorem 1.

By the definitions of and , it follows that

| (A40) |

The last line of equation (A) holds since , and are positive definition. And

| (A41) | ||||

The last line holds of equation (A41) since . By equations (A) and (A41), Theorem 1 holds.

∎

Proof of equation (30).

We first consider the SD case for . By the definition of and and part (i) of Lemma B1 of Online Appendix for Kostakis et al., (2015) , it follows that

| (A42) | |||

Similarly,

Second, by equation (7) of the supplementary material for Kostakis et al., (2015), for WD predictors, we have

| (A43) | |||

By equation (2), it follows that

| (A44) |

So

| (A45) | |||

where . By equations (24), (A43), (A44) and (A45), for WD predictors, we have

Similarly, for WD predictors, by the continuous mapping theorem and the definition of and , it follows that

∎

Lemma 4.

Under Assumption 1, for SD and WD predictors, it follows that

| (A46) |

Proof of Lemma 4.

Proof of Theorem 2.

The proof of equations (34) and (35) is very similar to the proof of Proposition 1, so it is omitted here.

Lemma 5.

Under Assumption 1, for SD and WD predictors, we have

Proof of Lemma 5.

Proof of Proposition 2.

This proof is quite similar to the proof of Proposition 1 of Hosseinkouchack and Demetrescu, (2021).

By equations (34), (35) and (36), it follows that

| (A57) | ||||

The last step holds since and by the proof of Proposition 1 of Hosseinkouchack and Demetrescu, (2021).

Proof of Theorem 4.

Proof of Theorem 5.

Proof of Proposition 3.

Proof of Proposition 4.

B Additional Simulation Results

B.1 Example 1 (univariate models)

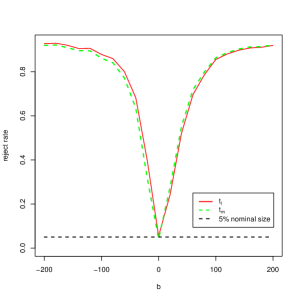

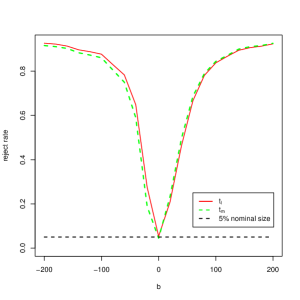

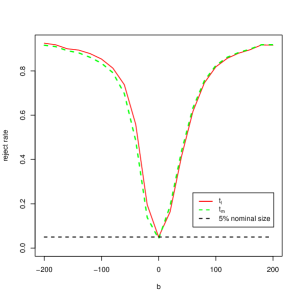

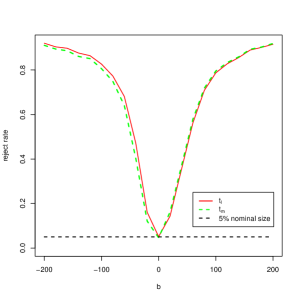

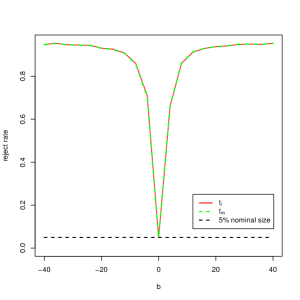

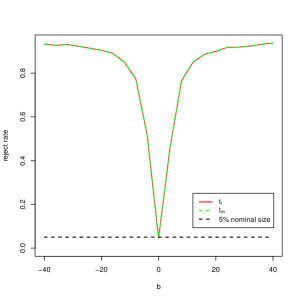

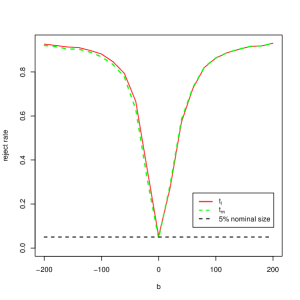

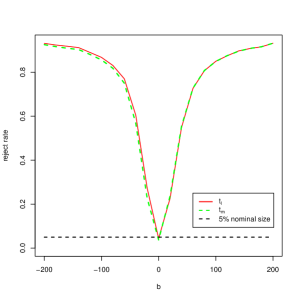

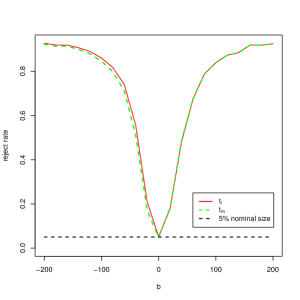

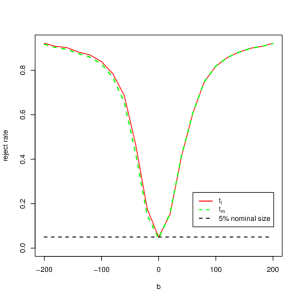

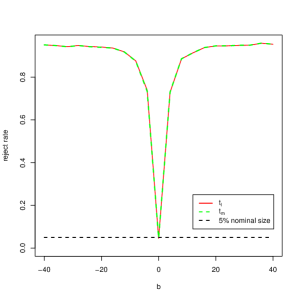

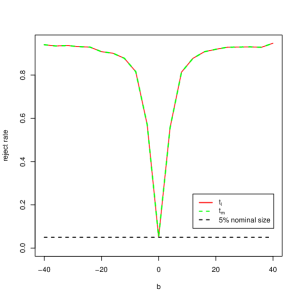

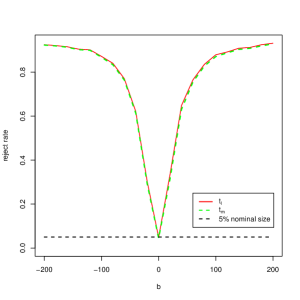

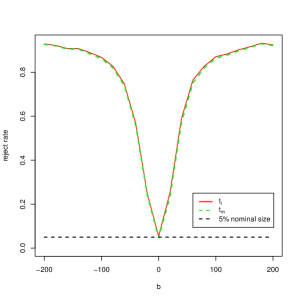

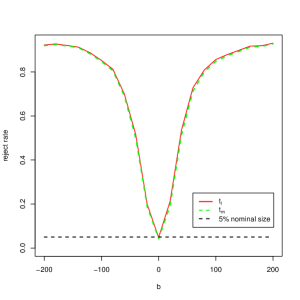

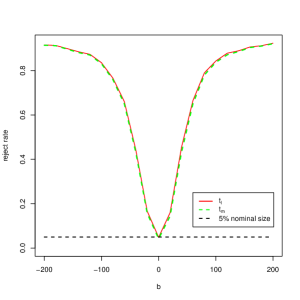

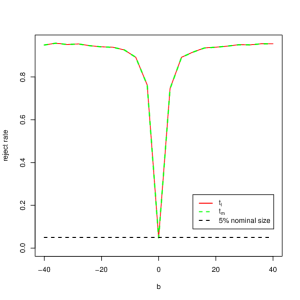

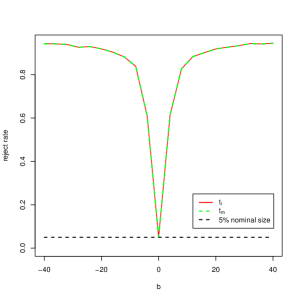

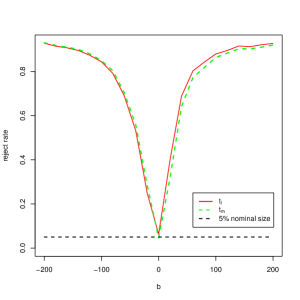

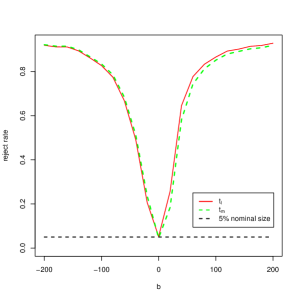

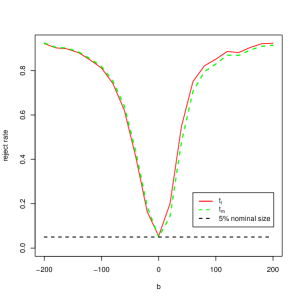

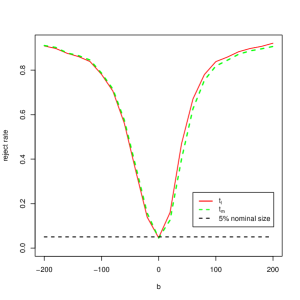

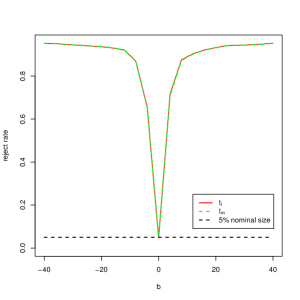

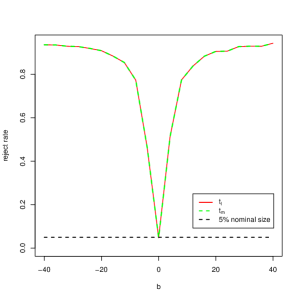

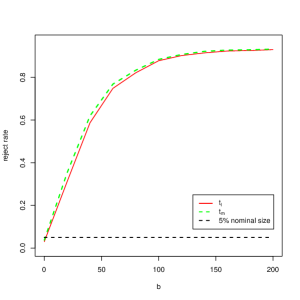

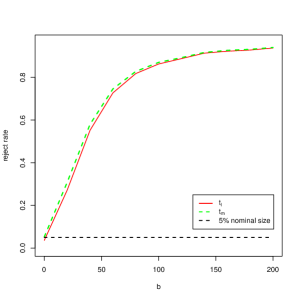

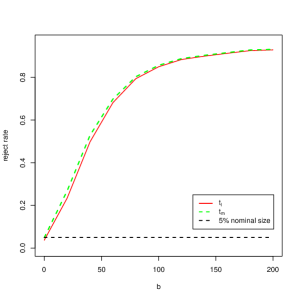

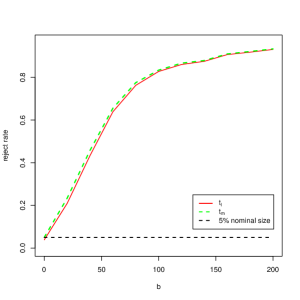

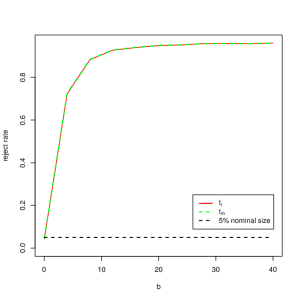

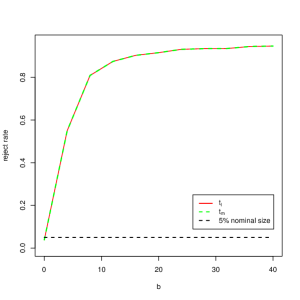

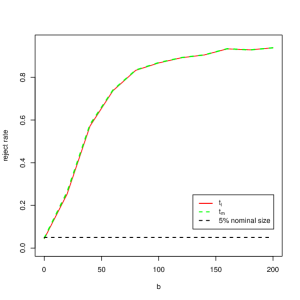

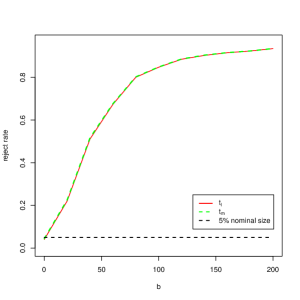

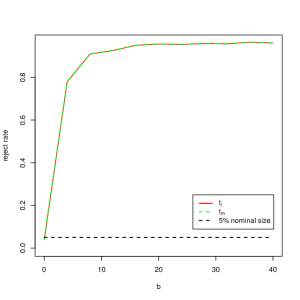

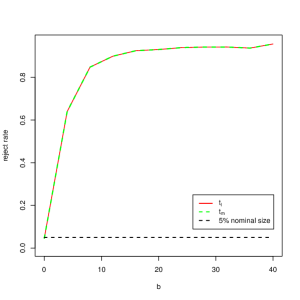

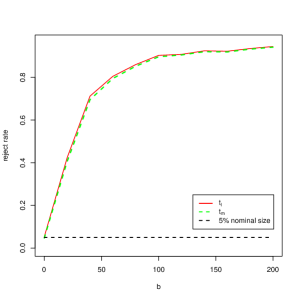

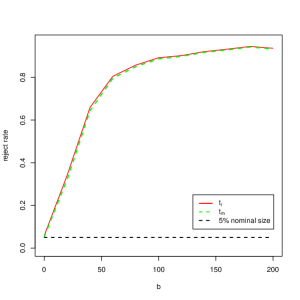

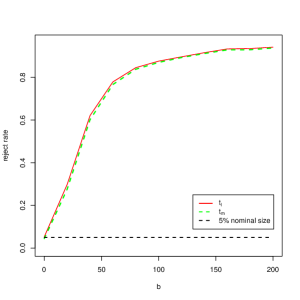

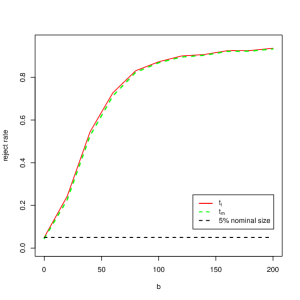

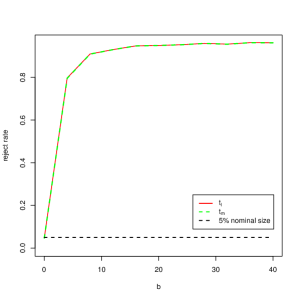

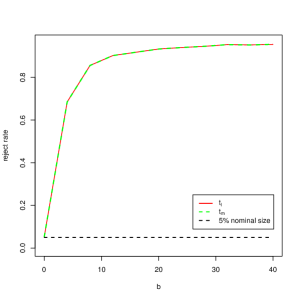

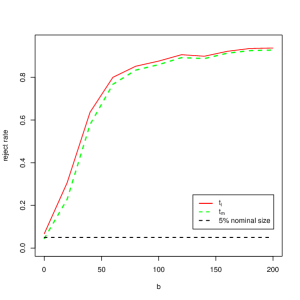

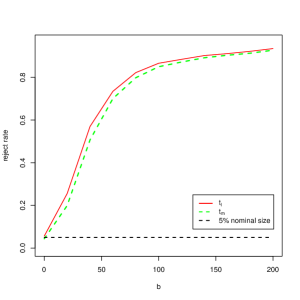

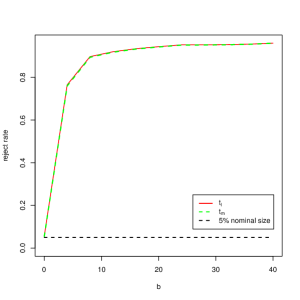

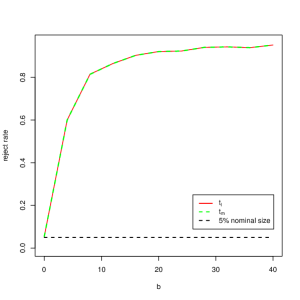

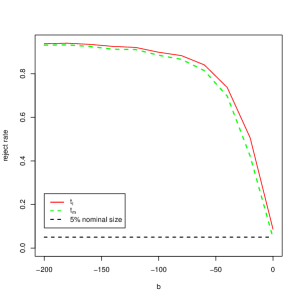

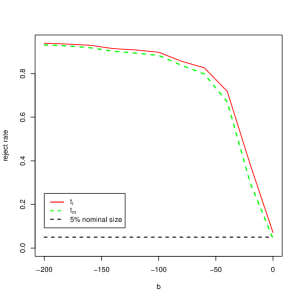

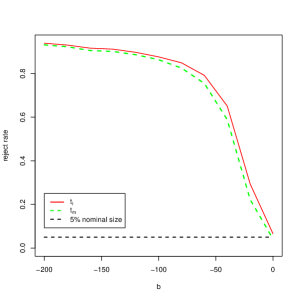

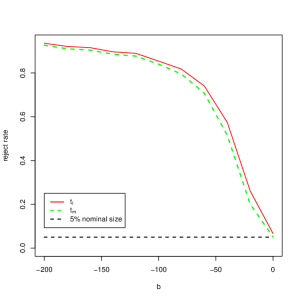

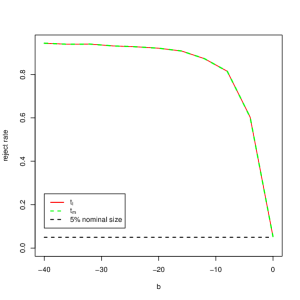

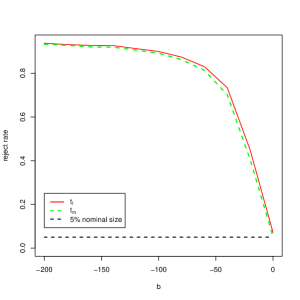

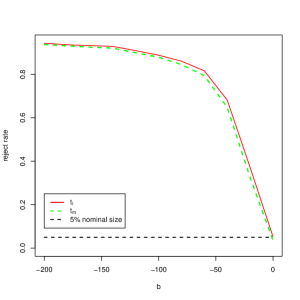

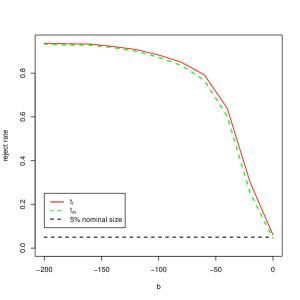

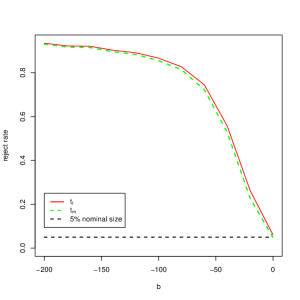

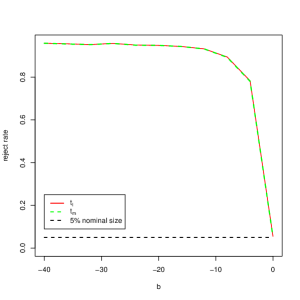

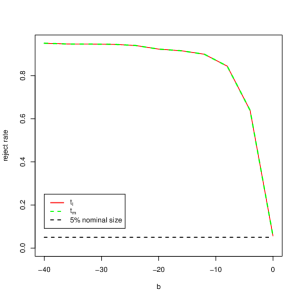

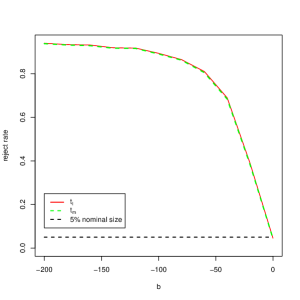

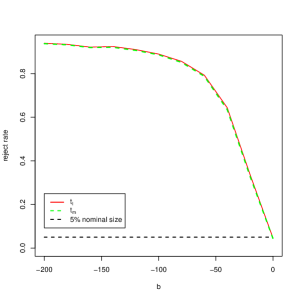

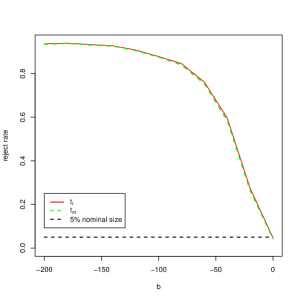

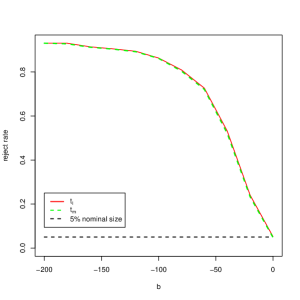

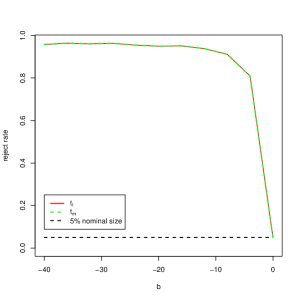

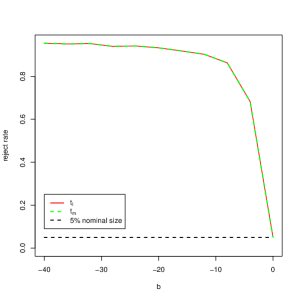

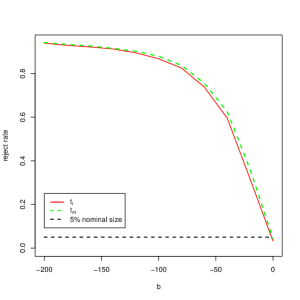

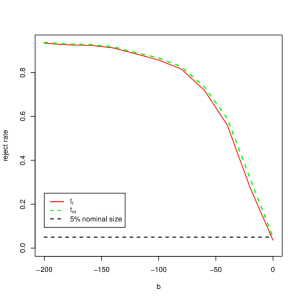

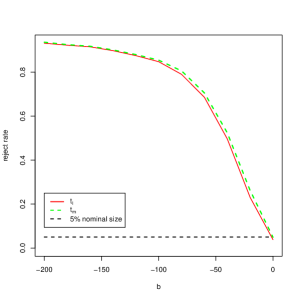

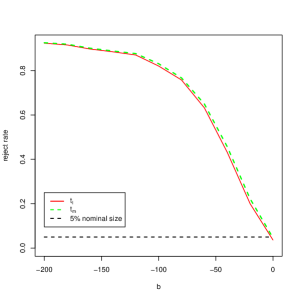

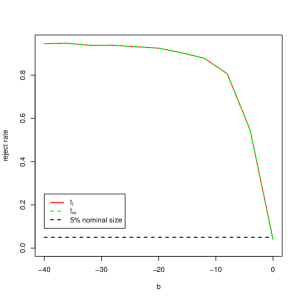

In this example for the univariate model, the DGP is set up by equations (1), (2) and (5), in which , and . In the univariate model, we define the notation and as the t-test statistics and , respectively. To create the embedded endogeneity among innovations, the innovation processes are generated as , where . To save space, we only report the simulation results for GARCH model with the sample . 101010To save space, we did not report the simulation results for GARCH model with the sample size and and ARCH and i.i.d. model with the sample size , and in the paper. Their results are similar to the results of GARCH model with the sample size . The codes and results are available upon request.

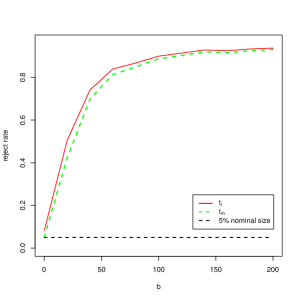

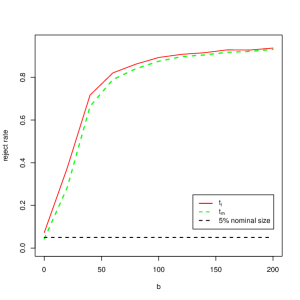

First, the results for the comparison of the size performances of the proposed test statistics and for seven cases in GARCH(1,1) model are shown in Tables B1-B3 while the power performances are shown in Figures B1-B12. The size performance of two-sided test vs and the right side test vs and the left side test vs are shown in Tables B1-B3, respectively. Meanwhile, the power performances of two-sided test vs and the right side test vs and left side test vs are shown in Figures B1-B4, B5-B8 and B9-B12 respectively. In each hypothesis, we show the simulation results for , , and . Additionally, six persistence including two categories are considered in each hypothesis. The first category including case 1 - case 4 is SD with , while respectively. The second category including case 5 - case 6 is WD with , while , respectively. And we set in Tables B1-B3 to compare the size performance with different , to see the local power and in Figures B1-B12, 111111Since the following part states that the proposed test statistics perform the best with , we only show the power performance with . and , , in GARCH(1,1) model and the nominal size to be . Simulations are repeated times for each setting.

| 0.1 | 0.25 | 0.5 | 0.75 | 0.9 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | ||

| Case 1 | 5.8 | 5.6 | 5.1 | 5.7 | 5.9 | 5.2 | 5.0 | 6.2 | 5.8 | 5.3 | 5.1 | 5.9 | 5.7 | 5.4 | 4.5 | 5.6 | 5.7 | 5.6 | 4.7 | 5.5 | |

| Case 2 | 5.5 | 5.4 | 4.4 | 5.5 | 5.3 | 5.1 | 4.8 | 5.4 | 5.7 | 4.9 | 5.0 | 5.4 | 5.6 | 5.3 | 5.2 | 5.5 | 5.3 | 4.9 | 4.9 | 5.6 | |

| Case 3 | 4.8 | 5.1 | 5.0 | 5.4 | 5.3 | 4.9 | 5.0 | 5.0 | 4.5 | 4.9 | 4.6 | 5.0 | 5.1 | 5.3 | 4.8 | 5.1 | 5.6 | 4.5 | 5.0 | 5.1 | |

| Case 4 | 5.0 | 5.0 | 4.5 | 5.4 | 5.1 | 4.9 | 5.1 | 5.0 | 5.1 | 4.8 | 5.0 | 5.2 | 4.8 | 4.7 | 4.9 | 5.0 | 5.4 | 4.8 | 4.7 | 5.7 | |

| Case 5 | 5.0 | 5.0 | 4.8 | 4.6 | 4.8 | 4.7 | 5.2 | 4.5 | 4.6 | 4.7 | 4.8 | 5.1 | 4.8 | 5.0 | 5.3 | 4.8 | 5.0 | 4.9 | 4.8 | 5.1 | |

| Case 6 | 4.5 | 4.5 | 4.9 | 4.5 | 4.3 | 5.2 | 4.9 | 4.8 | 4.8 | 4.9 | 4.6 | 4.5 | 4.7 | 5.0 | 4.6 | 4.6 | 5.2 | 4.7 | 5.0 | 4.3 | |

| Case 7 | 4.6 | 4.6 | 4.5 | 4.5 | 4.6 | 4.9 | 4.7 | 4.9 | 5.0 | 4.8 | 5.0 | 4.6 | 4.9 | 4.8 | 4.7 | 5.1 | 4.3 | 4.5 | 4.3 | 4.4 | |

| Case 1 | 3.8 | 4.3 | 4.0 | 3.6 | 4.3 | 4.2 | 4.3 | 4.3 | 4.2 | 4.3 | 4.4 | 4.2 | 3.9 | 4.4 | 3.9 | 3.6 | 3.6 | 4.4 | 3.8 | 3.8 | |

| Case 2 | 4.6 | 4.2 | 3.6 | 4.3 | 4.5 | 4.3 | 4.2 | 4.6 | 4.8 | 4.3 | 4.2 | 4.5 | 4.5 | 4.7 | 4.6 | 4.5 | 4.1 | 3.8 | 4.1 | 4.5 | |

| Case 3 | 4.3 | 4.3 | 4.2 | 4.7 | 4.8 | 4.2 | 4.3 | 4.4 | 4.2 | 4.4 | 4.0 | 4.3 | 4.6 | 4.5 | 4.1 | 4.3 | 4.6 | 3.9 | 4.3 | 4.3 | |

| Case 4 | 4.9 | 4.3 | 3.9 | 5.1 | 4.8 | 4.4 | 4.4 | 4.7 | 4.7 | 4.4 | 4.3 | 4.9 | 4.3 | 4.1 | 4.3 | 4.5 | 4.9 | 4.2 | 4.2 | 5.1 | |

| Case 5 | 5.2 | 4.9 | 4.7 | 4.8 | 5.0 | 4.7 | 5.1 | 4.7 | 4.8 | 4.6 | 4.7 | 5.2 | 4.8 | 5.0 | 5.1 | 4.9 | 5.1 | 4.8 | 4.7 | 5.2 | |

| Case 6 | 4.5 | 4.5 | 4.9 | 4.5 | 4.3 | 5.2 | 4.9 | 4.8 | 4.8 | 4.9 | 4.6 | 4.5 | 4.7 | 5.0 | 4.6 | 4.6 | 5.2 | 4.7 | 5.0 | 4.3 | |

| Case 7 | 4.6 | 4.6 | 4.5 | 4.5 | 4.6 | 4.9 | 4.7 | 4.9 | 5.0 | 4.8 | 5.0 | 4.6 | 4.9 | 4.8 | 4.7 | 5.1 | 4.3 | 4.5 | 4.3 | 4.4 | |

| 0.1 | 0.25 | 0.5 | 0.75 | 0.9 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | ||

| Case 1 | 3.6 | 4.1 | 5.7 | 8.4 | 3.1 | 3.8 | 5.7 | 9.1 | 3.1 | 3.6 | 5.6 | 8.7 | 2.9 | 3.6 | 4.9 | 9.0 | 2.8 | 4.2 | 5.5 | 8.4 | |

| Case 2 | 4.0 | 4.4 | 4.6 | 7.1 | 4.0 | 4.1 | 5.0 | 6.8 | 3.6 | 4.1 | 5.2 | 7.2 | 3.4 | 4.3 | 5.3 | 7.6 | 3.6 | 3.9 | 5.2 | 7.5 | |

| Case 3 | 4.3 | 4.4 | 5.5 | 6.5 | 4.0 | 4.1 | 4.9 | 6.1 | 3.9 | 4.2 | 5.3 | 7.1 | 3.5 | 4.0 | 5.2 | 6.8 | 3.4 | 4.0 | 5.3 | 7.2 | |

| Case 4 | 4.3 | 4.5 | 5.3 | 6.3 | 3.9 | 4.3 | 5.3 | 6.3 | 3.8 | 4.2 | 5.3 | 6.7 | 3.5 | 4.1 | 5.2 | 6.8 | 3.6 | 3.9 | 5.0 | 7.1 | |

| Case 5 | 4.3 | 4.2 | 5.4 | 5.8 | 4.5 | 4.4 | 5.5 | 5.7 | 4.4 | 4.5 | 5.1 | 6.1 | 3.9 | 4.6 | 5.2 | 6.1 | 3.7 | 4.3 | 5.2 | 6.5 | |

| Case 6 | 4.6 | 4.3 | 4.9 | 5.4 | 4.5 | 4.9 | 5.4 | 5.4 | 4.2 | 4.7 | 4.9 | 5.3 | 4.5 | 4.6 | 5.0 | 5.5 | 4.2 | 4.3 | 5.2 | 5.6 | |

| Case 7 | 4.3 | 4.8 | 5.0 | 5.0 | 4.3 | 4.7 | 5.1 | 5.4 | 4.6 | 4.6 | 5.1 | 5.6 | 4.3 | 4.8 | 5.1 | 5.7 | 4.4 | 4.5 | 4.7 | 5.4 | |

| Case 1 | 4.3 | 4.3 | 4.6 | 4.6 | 4.1 | 4.3 | 4.9 | 5.1 | 4.2 | 4.0 | 4.8 | 5.1 | 4.0 | 4.3 | 4.1 | 5.0 | 3.6 | 4.5 | 4.6 | 4.4 | |

| Case 2 | 5.3 | 4.7 | 3.9 | 4.3 | 5.4 | 4.7 | 4.4 | 4.1 | 4.9 | 4.6 | 4.4 | 4.4 | 4.8 | 4.9 | 4.5 | 4.6 | 5.0 | 4.4 | 4.4 | 4.5 | |

| Case 3 | 5.5 | 4.8 | 4.7 | 4.4 | 5.4 | 4.4 | 4.2 | 4.0 | 5.0 | 4.6 | 4.6 | 4.6 | 4.6 | 4.4 | 4.5 | 4.6 | 4.5 | 4.3 | 4.6 | 4.8 | |

| Case 4 | 5.5 | 4.7 | 4.6 | 4.8 | 5.1 | 4.5 | 4.7 | 4.7 | 4.9 | 4.5 | 4.6 | 4.9 | 4.6 | 4.4 | 4.6 | 5.1 | 4.6 | 4.1 | 4.4 | 5.4 | |

| Case 5 | 4.7 | 4.4 | 5.3 | 5.6 | 4.9 | 4.5 | 5.5 | 5.5 | 4.7 | 4.7 | 5.0 | 5.9 | 4.3 | 4.8 | 5.1 | 6.0 | 4.0 | 4.5 | 5.1 | 6.3 | |

| Case 6 | 4.6 | 4.4 | 4.9 | 5.4 | 4.5 | 4.9 | 5.4 | 5.4 | 4.2 | 4.7 | 4.9 | 5.3 | 4.5 | 4.6 | 5.0 | 5.5 | 4.2 | 4.3 | 5.2 | 5.6 | |

| Case 7 | 4.3 | 4.8 | 5.0 | 5.0 | 4.3 | 4.7 | 5.1 | 5.4 | 4.6 | 4.6 | 5.1 | 5.6 | 4.3 | 4.8 | 5.1 | 5.7 | 4.4 | 4.5 | 4.7 | 5.4 | |

Clearly, the following findings can be observed from Tables B1-B3. First, the proposed test statistics and generally perform well in terms of size for the joint test vs . performs well in terms of size for different while suffers a little bit of size distortion with for SD predictors. Second, the proposed test statistics suffers size distortion for the right side test vs and left side test vs with SD predictors and , while performs well in terms of size, especially with . In one word, with performs well in terms of size for all cases while only performs well in terms of size for the joint test, which is according to the results in Section 3 in the main text.

Next, it is clearly observed from Figures B1-B12 that the power performance of the proposed test statistics and are quite well and comparable. To sum up, with performs well in terms of size and power, which is according to the statements in Section 3 that we reduce DiE and VEE while keeping its power performance.

B.2 Example 2

We observe the following findings from Tables B4-B7, B8-B11, B12-B15 and B16-B20. First, for the joint test , the proposed test statistic still suffers from multiple predictors () and the size distortion grows bigger as the number of predictors K grows bigger. Meanwhile, the proposed test statistic is free of size distortion for different settings with . With and , tends to slightly under-reject the null hypothesis . It is not surprising since still suffers the DiE and the VEE while does not. Second, the size performance of is better than that of for both two-sided and one-sided marginal tests although suffers a little size distortion. In particular, the size performance of and are comparable for right side marginal test . And the size performance of is much better than that of for two-sided marginal test vs and left side marginal test vs . Third, for two-sided marginal test vs , right side marginal test vs and left side marginal test vs , the size performances of and become slightly better as grows bigger while their power performances become worse. Therefore, we recommend the empirical researchers to set . Fourth, the power performances of and are comparable and quite well.

| 0.1 | 0.25 | 0.5 | 0.75 | 0.9 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | 0.95 | 0.5 | -0.1 | -0.95 | ||

| Case 1 | 8.6 | 6.9 | 4.8 | 3.6 | 8.9 | 6.8 | 4.6 | 3.4 | 8.4 | 7.1 | 4.6 | 2.9 | 8.6 | 7.0 | 4.6 | 2.9 | 9.0 | 6.9 | 4.6 | 3.2 | |

| Case 2 | 7.1 | 6.4 | 4.5 | 3.9 | 6.7 | 6.3 | 4.7 | 4.0 | 7.8 | 5.9 | 5.0 | 3.5 | 7.9 | 6.3 | 4.8 | 3.7 | 7.6 | 6.1 | 4.8 | 4.0 | |

| Case 3 | 5.8 | 6.2 | 4.8 | 4.1 | 6.6 | 6.0 | 4.9 | 4.1 | 6.3 | 6.2 | 4.5 | 3.6 | 7.0 | 6.5 | 4.8 | 3.6 | 7.6 | 5.8 | 4.5 | 3.5 | |

| Case 4 | 6.1 | 5.7 | 4.5 | 4.4 | 6.4 | 5.9 | 5.1 | 4.1 | 6.8 | 6.0 | 5.0 | 3.9 | 6.1 | 5.5 | 4.9 | 4.0 | 7.3 | 6.2 | 5.1 | 3.8 | |

| Case 5 | 5.9 | 5.6 | 4.8 | 4.3 | 5.3 | 5.2 | 5.0 | 4.2 | 5.7 | 5.7 | 5.0 | 4.5 | 6.4 | 5.8 | 5.0 | 3.9 | 6.9 | 5.9 | 5.0 | 4.1 | |

| Case 6 | 5.4 | 5.4 | 5.7 | 4.6 | 5.0 | 5.5 | 4.7 | 4.9 | 5.3 | 5.2 | 4.9 | 4.1 | 5.5 | 5.7 | 4.8 | 4.3 | 6.2 | 5.9 | 5.1 | 3.8 | |

| Case 7 | 5.2 | 4.8 | 5.0 | 4.7 | 5.1 | 5.5 | 4.8 | 4.8 | 5.1 | 5.3 | 4.8 | 4.3 | 5.6 | 5.4 | 4.8 | 4.7 | 5.6 | 5.2 | 4.9 | 4.2 | |

| Case 1 | 4.6 | 4.9 | 4.2 | 4.6 | 5.0 | 4.6 | 4.3 | 4.3 | 4.9 | 4.9 | 4.3 | 4.0 | 4.8 | 5.2 | 4.3 | 3.9 | 4.7 | 4.9 | 4.2 | 4.0 | |

| Case 2 | 4.2 | 4.7 | 4.1 | 5.2 | 4.0 | 4.6 | 4.2 | 5.4 | 4.7 | 4.3 | 4.9 | 4.9 | 4.8 | 4.5 | 4.4 | 5.0 | 4.5 | 4.3 | 4.3 | 5.1 | |

| Case 3 | 3.9 | 4.8 | 4.4 | 5.3 | 4.3 | 4.4 | 4.5 | 5.5 | 4.0 | 4.8 | 4.2 | 4.8 | 4.7 | 5.0 | 4.4 | 4.9 | 5.1 | 4.1 | 4.0 | 4.7 | |

| Case 4 | 4.4 | 4.8 | 4.0 | 5.4 | 4.7 | 4.8 | 4.8 | 5.1 | 5.2 | 4.8 | 4.7 | 5.0 | 4.6 | 4.4 | 4.5 | 5.0 | 5.3 | 4.9 | 4.7 | 4.8 | |

| Case 5 | 5.8 | 5.5 | 4.8 | 4.7 | 5.1 | 5.0 | 5.0 | 4.7 | 5.4 | 5.5 | 5.0 | 4.9 | 6.1 | 5.6 | 5.0 | 4.3 | 6.6 | 5.8 | 4.9 | 4.4 | |

| Case 6 | 5.4 | 5.4 | 5.7 | 4.6 | 5.0 | 5.5 | 4.7 | 4.9 | 5.3 | 5.2 | 4.9 | 4.1 | 5.5 | 5.7 | 4.8 | 4.3 | 6.2 | 5.9 | 5.1 | 3.8 | |

| Case 7 | 5.2 | 4.8 | 5.0 | 4.7 | 5.1 | 5.5 | 4.8 | 4.8 | 5.1 | 5.3 | 4.8 | 4.3 | 5.6 | 5.4 | 4.8 | 4.7 | 5.6 | 5.2 | 4.9 | 4.2 | |

| b | 0 | 0.02 | 0.04 | 0.06 | 0.08 | 0.1 | 0.12 | 0.14 | 0.16 | |

|---|---|---|---|---|---|---|---|---|---|---|

| K=2 | 5.8 | 24.0 | 63.2 | 83.5 | 91.3 | 94.3 | 96.2 | 97.0 | 98.0 | |

| K=3 | 6.7 | 15.9 | 43.9 | 70.0 | 83.5 | 91.3 | 95.3 | 97.0 | 98.0 | |

| K=4 | 6.4 | 18.3 | 50.6 | 77.4 | 91.2 | 95.3 | 98.0 | 98.7 | 99.5 | |

| K=5 | 6.7 | 16.4 | 47.2 | 74.5 | 88.6 | 95.2 | 98.4 | 99.1 | 99.6 | |

| K=6 | 6.1 | 14.3 | 40.7 | 68.6 | 86.3 | 93.6 | 97.3 | 98.6 | 99.2 | |

| K=7 | 6.8 | 11.8 | 33.7 | 60.8 | 79.7 | 90.9 | 95.7 | 97.6 | 98.9 | |

| K=8 | 7.2 | 12.0 | 32.3 | 57.9 | 77.6 | 88.9 | 94.9 | 97.5 | 99.0 | |

| K=9 | 7.4 | 10.3 | 26.2 | 50.3 | 71.4 | 85.2 | 91.9 | 96.5 | 98.3 | |

| K=10 | 7.2 | 8.5 | 21.8 | 42.5 | 64.2 | 79.3 | 89.2 | 93.7 | 97.2 | |

| K=2 | 4.3 | 19.0 | 58.3 | 81.1 | 90.2 | 93.5 | 95.5 | 96.6 | 97.7 | |

| K=3 | 4.7 | 12.6 | 39.4 | 65.8 | 80.8 | 89.8 | 94.6 | 96.6 | 97.8 | |

| K=4 | 4.5 | 19.1 | 53.4 | 79.0 | 92.0 | 95.6 | 98.1 | 98.8 | 99.5 | |

| K=5 | 4.4 | 17.6 | 51.0 | 76.8 | 89.7 | 95.8 | 98.5 | 99.1 | 99.7 | |

| K=6 | 3.7 | 15.1 | 44.4 | 72.1 | 87.9 | 94.6 | 97.6 | 98.7 | 99.2 | |

| K=7 | 4.5 | 12.4 | 37.2 | 65.8 | 82.9 | 92.2 | 96.5 | 97.8 | 99.0 | |

| K=8 | 4.8 | 11.9 | 35.2 | 62.5 | 81.3 | 90.8 | 95.5 | 97.9 | 99.2 | |

| K=9 | 4.8 | 9.7 | 30.0 | 55.7 | 76.0 | 88.1 | 93.8 | 97.1 | 98.5 | |

| K=10 | 4.4 | 8.1 | 24.9 | 47.6 | 70.3 | 83.4 | 91.8 | 95.0 | 97.8 | |

-

1

.

| b | 0 | 0.02 | 0.04 | 0.06 | 0.08 | 0.1 | 0.12 | 0.14 | 0.16 | |

|---|---|---|---|---|---|---|---|---|---|---|

| K=2 | 5.7 | 24.9 | 64.8 | 83.7 | 91.6 | 94.4 | 96.0 | 96.7 | 97.5 | |

| K=3 | 7.7 | 17.4 | 44.9 | 69.9 | 84.6 | 91.8 | 95.2 | 96.8 | 97.9 | |

| K=4 | 7.4 | 18.0 | 52.1 | 78.2 | 90.5 | 95.7 | 98.1 | 99.0 | 99.5 | |

| K=5 | 7.7 | 16.0 | 47.4 | 74.2 | 89.0 | 95.3 | 98.0 | 99.0 | 99.5 | |

| K=6 | 7.2 | 14.9 | 41.2 | 68.9 | 86.4 | 94.0 | 97.7 | 98.7 | 99.3 | |

| K=7 | 6.6 | 12.5 | 34.6 | 61.4 | 80.4 | 91.1 | 96.0 | 98.2 | 98.7 | |

| K=8 | 7.2 | 11.8 | 31.5 | 58.6 | 77.0 | 89.3 | 95.3 | 97.7 | 98.9 | |

| K=9 | 6.9 | 10.1 | 26.9 | 51.0 | 71.8 | 85.0 | 93.0 | 96.3 | 98.0 | |

| K=10 | 7.2 | 9.9 | 22.6 | 44.3 | 65.0 | 80.7 | 89.2 | 94.4 | 97.4 | |

| K=2 | 4.3 | 19.9 | 59.9 | 81.5 | 90.3 | 93.7 | 95.7 | 96.5 | 97.3 | |

| K=3 | 5.1 | 13.7 | 40.6 | 66.2 | 82.5 | 90.4 | 94.5 | 96.4 | 97.6 | |

| K=4 | 4.8 | 20.3 | 55.7 | 80.4 | 91.4 | 96.0 | 98.2 | 99.0 | 99.4 | |

| K=5 | 5.3 | 17.4 | 51.4 | 77.2 | 90.1 | 95.9 | 98.4 | 99.1 | 99.6 | |

| K=6 | 4.8 | 16.3 | 45.9 | 73.1 | 89.2 | 95.2 | 98.2 | 98.9 | 99.4 | |

| K=7 | 4.7 | 13.7 | 39.1 | 66.8 | 83.9 | 92.5 | 96.8 | 98.5 | 98.9 | |

| K=8 | 4.9 | 12.4 | 36.6 | 64.0 | 81.4 | 91.4 | 96.4 | 97.9 | 99.0 | |

| K=9 | 4.5 | 10.4 | 31.0 | 57.4 | 77.0 | 88.5 | 94.6 | 97.2 | 98.7 | |

| K=10 | 5.0 | 9.8 | 26.6 | 50.9 | 70.7 | 84.8 | 91.8 | 95.9 | 98.1 | |

-

1

.

| b | 0 | 0.02 | 0.04 | 0.06 | 0.08 | 0.1 | 0.12 | 0.14 | 0.16 | |

|---|---|---|---|---|---|---|---|---|---|---|

| K=2 | 5.8 | 21.7 | 54.7 | 76.1 | 85.2 | 89.5 | 91.8 | 94.1 | 95.2 | |

| K=3 | 6.7 | 15.9 | 40.8 | 65.0 | 79.2 | 88.1 | 91.7 | 94.2 | 96.1 | |

| K=4 | 7.5 | 19.2 | 51.3 | 76.5 | 88.5 | 94.3 | 97.4 | 98.4 | 99.4 | |

| K=5 | 7.2 | 16.7 | 45.3 | 72.8 | 86.9 | 94.6 | 97.5 | 98.8 | 99.2 | |

| K=6 | 7.6 | 14.6 | 41.3 | 65.7 | 85.0 | 93.1 | 97.4 | 98.8 | 99.4 | |

| K=7 | 6.4 | 11.8 | 33.1 | 59.1 | 79.3 | 89.6 | 95.4 | 98.1 | 99.0 | |

| K=8 | 7.7 | 11.9 | 31.0 | 57.1 | 77.1 | 89.2 | 94.7 | 97.6 | 98.6 | |

| K=9 | 6.9 | 11.3 | 25.6 | 48.9 | 69.7 | 85.1 | 91.8 | 96.2 | 97.9 | |

| K=10 | 7.4 | 10.1 | 22.0 | 42.7 | 62.6 | 78.8 | 88.6 | 94.2 | 96.5 | |

| K=2 | 4.7 | 17.4 | 49.7 | 73.5 | 83.4 | 88.4 | 90.6 | 93.5 | 94.9 | |

| K=3 | 4.4 | 12.2 | 36.2 | 60.9 | 76.9 | 86.2 | 90.4 | 93.5 | 95.7 | |

| K=4 | 4.9 | 20.1 | 54.0 | 78.2 | 90.0 | 94.9 | 97.5 | 98.4 | 99.4 | |

| K=5 | 5.0 | 18.0 | 49.6 | 76.0 | 88.6 | 94.9 | 97.7 | 98.8 | 99.3 | |

| K=6 | 5.1 | 15.2 | 45.9 | 70.0 | 87.5 | 94.0 | 98.0 | 98.9 | 99.4 | |

| K=7 | 4.0 | 12.3 | 37.9 | 64.5 | 82.6 | 91.5 | 96.1 | 98.1 | 99.1 | |

| K=8 | 5.2 | 12.4 | 34.9 | 62.6 | 81.3 | 91.2 | 95.5 | 98.0 | 98.9 | |

| K=9 | 4.7 | 11.7 | 29.1 | 54.0 | 74.9 | 88.1 | 93.7 | 96.9 | 98.3 | |

| K=10 | 4.9 | 9.6 | 25.4 | 49.5 | 68.3 | 83.2 | 90.9 | 95.5 | 97.0 | |

-

1

.

| b | 0 | 0.02 | 0.04 | 0.06 | 0.08 | 0.1 | 0.12 | 0.14 | 0.16 | |

|---|---|---|---|---|---|---|---|---|---|---|

| K=2 | 5.6 | 20.6 | 50.9 | 72.3 | 81.6 | 87.3 | 90.8 | 91.8 | 93.3 | |

| K=3 | 6.5 | 14.8 | 39.7 | 61.3 | 78.1 | 86.3 | 91.0 | 93.1 | 95.2 | |

| K=4 | 6.9 | 17.9 | 47.1 | 73.7 | 87.8 | 94.4 | 96.9 | 98.5 | 99.1 | |

| K=5 | 6.9 | 16.3 | 43.5 | 70.0 | 86.7 | 93.5 | 97.4 | 98.4 | 99.2 | |

| K=6 | 7.2 | 13.6 | 39.1 | 65.2 | 83.0 | 92.5 | 96.7 | 98.1 | 99.0 | |

| K=7 | 6.8 | 11.4 | 31.4 | 58.5 | 78.5 | 89.3 | 94.7 | 97.6 | 98.6 | |

| K=8 | 7.5 | 10.9 | 30.2 | 55.5 | 75.2 | 88.1 | 93.9 | 97.1 | 98.7 | |

| K=9 | 7.3 | 11.0 | 25.9 | 47.3 | 68.4 | 82.6 | 91.6 | 95.7 | 97.8 | |

| K=10 | 6.9 | 10.3 | 21.6 | 40.9 | 62.4 | 78.1 | 88.0 | 93.5 | 96.4 | |

| K=2 | 4.2 | 16.4 | 46.2 | 68.8 | 79.5 | 85.6 | 89.6 | 91.0 | 92.3 | |

| K=3 | 4.1 | 10.9 | 35.5 | 57.6 | 75.2 | 84.4 | 89.7 | 92.5 | 94.6 | |

| K=4 | 4.6 | 18.1 | 50.4 | 75.2 | 88.5 | 94.7 | 97.2 | 98.4 | 99.1 | |

| K=5 | 4.9 | 16.3 | 46.7 | 72.3 | 87.5 | 94.0 | 97.4 | 98.5 | 99.3 | |

| K=6 | 4.4 | 14.0 | 42.0 | 68.9 | 85.3 | 93.3 | 97.0 | 98.2 | 99.0 | |

| K=7 | 4.6 | 11.1 | 34.3 | 62.5 | 81.4 | 91.0 | 95.3 | 97.9 | 98.8 | |

| K=8 | 4.5 | 10.7 | 33.0 | 59.3 | 78.6 | 90.5 | 94.9 | 97.3 | 98.8 | |

| K=9 | 4.9 | 10.3 | 28.8 | 52.3 | 72.4 | 85.6 | 93.0 | 96.6 | 98.2 | |

| K=10 | 4.1 | 9.5 | 23.0 | 45.6 | 67.1 | 81.7 | 90.4 | 94.7 | 96.9 | |

-

1

.

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 7.0 | 70.0 | 90.7 | 95.4 | 96.8 | 97.3 | 97.5 | 98.0 | 98.2 | |

| i=2 | 6.9 | 45.8 | 82.7 | 93.0 | 95.5 | 96.6 | 97.6 | 97.9 | 98.2 | |

| i=3 | 6.9 | 53.1 | 83.1 | 90.5 | 93.3 | 94.8 | 95.3 | 96.1 | 95.9 | |

| i=4 | 6.8 | 54.7 | 88.5 | 94.8 | 97.1 | 97.5 | 98.4 | 98.3 | 98.6 | |

| i=5 | 5.9 | 29.5 | 71.2 | 89.7 | 94.6 | 96.4 | 97.3 | 98.1 | 98.2 | |

| i=6 | 5.6 | 24.7 | 64.4 | 85.6 | 93.7 | 95.7 | 97.4 | 97.6 | 98.1 | |

| i=7 | 5.3 | 16.9 | 49.1 | 76.5 | 88.8 | 93.6 | 95.6 | 96.7 | 97.7 | |

| i=8 | 6.2 | 33.6 | 74.4 | 89.8 | 94.4 | 96.7 | 97.5 | 97.7 | 98.3 | |

| i=9 | 5.3 | 19.3 | 52.5 | 78.7 | 89.9 | 94.3 | 96.2 | 96.9 | 97.9 | |

| i=10 | 5.3 | 23.0 | 58.5 | 82.2 | 91.6 | 95.0 | 96.8 | 97.5 | 97.8 | |

| i=1 | 5.8 | 69.2 | 90.2 | 95.2 | 96.4 | 97.1 | 97.4 | 97.8 | 98.1 | |

| i=2 | 5.8 | 43.4 | 81.6 | 92.5 | 95.1 | 96.4 | 97.4 | 97.8 | 98.1 | |

| i=3 | 6.1 | 50.1 | 81.6 | 89.8 | 92.8 | 94.4 | 95.0 | 95.6 | 95.6 | |

| i=4 | 5.7 | 56.6 | 88.9 | 95.0 | 97.1 | 97.4 | 98.2 | 98.2 | 98.6 | |

| i=5 | 5.1 | 30.7 | 71.8 | 89.8 | 94.4 | 96.2 | 97.3 | 98.0 | 98.0 | |

| i=6 | 5.1 | 25.9 | 65.1 | 85.7 | 93.6 | 95.7 | 97.4 | 97.6 | 98.1 | |

| i=7 | 5.1 | 18.5 | 51.2 | 77.5 | 89.0 | 93.7 | 95.7 | 96.8 | 97.7 | |

| i=8 | 5.5 | 32.3 | 73.0 | 89.0 | 94.0 | 96.4 | 97.4 | 97.6 | 98.2 | |

| i=9 | 5.1 | 19.4 | 52.3 | 78.3 | 89.6 | 94.1 | 96.0 | 96.8 | 97.7 | |

| i=10 | 4.8 | 21.7 | 56.5 | 81.2 | 91.0 | 94.6 | 96.6 | 97.2 | 97.7 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

| i=2 | 6.9 | 45.6 | 80.4 | 90.9 | 94.4 | 96.1 | 97.0 | 97.2 | 97.9 | |

| i=3 | 6.8 | 49.3 | 78.7 | 88.2 | 91.6 | 93.8 | 94.3 | 95.0 | 95.4 | |

| i=4 | 6.6 | 53.2 | 86.8 | 94.1 | 96.4 | 97.3 | 97.5 | 98.2 | 98.5 | |

| i=5 | 5.8 | 29.2 | 69.5 | 87.9 | 93.9 | 95.7 | 97.0 | 97.7 | 98.0 | |

| i=6 | 6.1 | 24.4 | 63.5 | 84.9 | 92.5 | 95.4 | 96.4 | 97.4 | 97.6 | |

| i=7 | 5.5 | 16.5 | 48.2 | 74.7 | 87.9 | 93.1 | 95.3 | 97.1 | 97.5 | |

| i=8 | 6.7 | 32.9 | 73.0 | 88.9 | 93.9 | 95.9 | 96.4 | 97.5 | 97.7 | |

| i=9 | 5.4 | 18.9 | 52.1 | 77.5 | 88.9 | 93.5 | 95.8 | 96.8 | 97.7 | |

| i=10 | 5.9 | 21.6 | 58.1 | 82.1 | 91.0 | 94.4 | 96.2 | 97.1 | 97.6 | |

| i=1 | 6.4 | 66.4 | 89.1 | 93.6 | 95.6 | 96.5 | 97.2 | 97.6 | 97.6 | |

| i=2 | 6.0 | 43.4 | 79.2 | 90.4 | 94.1 | 96.0 | 96.9 | 97.0 | 97.7 | |

| i=3 | 6.1 | 46.7 | 77.1 | 87.4 | 91.2 | 93.4 | 93.9 | 94.7 | 95.1 | |

| i=4 | 5.9 | 55.8 | 87.0 | 94.2 | 96.3 | 97.3 | 97.3 | 98.1 | 98.5 | |

| i=5 | 5.4 | 31.0 | 70.3 | 88.0 | 93.8 | 95.7 | 97.0 | 97.6 | 98.0 | |

| i=6 | 5.5 | 26.2 | 64.7 | 85.1 | 92.5 | 95.4 | 96.4 | 97.3 | 97.6 | |

| i=7 | 5.5 | 18.7 | 50.6 | 76.1 | 88.5 | 93.2 | 95.4 | 97.1 | 97.4 | |

| i=8 | 6.0 | 32.0 | 72.0 | 88.3 | 93.7 | 95.6 | 96.2 | 97.3 | 97.7 | |

| i=9 | 5.3 | 18.9 | 51.9 | 76.8 | 88.8 | 93.1 | 95.6 | 96.6 | 97.5 | |

| i=10 | 5.7 | 21.0 | 56.8 | 80.7 | 90.3 | 94.0 | 95.9 | 97.0 | 97.4 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 7.3 | 51.1 | 74.9 | 83.0 | 86.8 | 89.4 | 90.9 | 90.8 | 92.0 | |

| i=2 | 7.4 | 34.6 | 66.1 | 78.9 | 84.1 | 87.2 | 89.6 | 91.2 | 91.7 | |

| i=3 | 7.1 | 33.5 | 58.4 | 69.7 | 75.8 | 79.1 | 81.4 | 82.8 | 84.3 | |

| i=4 | 6.7 | 42.5 | 75.2 | 85.0 | 89.4 | 90.7 | 92.6 | 93.2 | 94.1 | |

| i=5 | 6.3 | 25.2 | 59.3 | 78.0 | 85.7 | 89.3 | 91.9 | 93.0 | 93.0 | |

| i=6 | 6.0 | 21.3 | 53.9 | 76.1 | 85.1 | 89.0 | 91.9 | 92.7 | 93.7 | |

| i=7 | 5.4 | 15.0 | 42.3 | 66.2 | 80.4 | 85.9 | 89.8 | 91.6 | 93.0 | |

| i=8 | 6.6 | 26.8 | 61.9 | 78.2 | 84.7 | 89.4 | 90.6 | 92.2 | 93.1 | |

| i=9 | 5.7 | 16.6 | 44.6 | 68.3 | 80.5 | 86.1 | 89.6 | 91.8 | 93.0 | |

| i=10 | 6.0 | 19.5 | 50.5 | 71.4 | 82.8 | 87.6 | 90.3 | 92.3 | 93.2 | |

| i=1 | 6.3 | 49.5 | 73.4 | 82.2 | 86.1 | 88.9 | 90.4 | 90.3 | 91.3 | |

| i=2 | 6.2 | 32.4 | 64.4 | 78.0 | 83.3 | 86.9 | 89.1 | 90.7 | 91.3 | |

| i=3 | 6.3 | 31.9 | 57.2 | 68.7 | 74.8 | 78.4 | 80.7 | 82.2 | 83.6 | |

| i=4 | 6.0 | 44.0 | 75.1 | 84.5 | 89.0 | 90.6 | 92.4 | 92.7 | 93.7 | |

| i=5 | 5.7 | 25.9 | 59.2 | 77.9 | 85.3 | 88.8 | 91.4 | 92.8 | 93.0 | |

| i=6 | 5.5 | 22.3 | 54.3 | 76.0 | 85.0 | 89.0 | 91.7 | 92.5 | 93.6 | |

| i=7 | 5.1 | 16.5 | 44.2 | 67.2 | 80.7 | 86.0 | 89.8 | 91.4 | 92.8 | |

| i=8 | 5.8 | 25.7 | 60.9 | 77.3 | 83.7 | 88.9 | 90.2 | 92.1 | 92.8 | |

| i=9 | 5.4 | 16.8 | 43.9 | 67.3 | 79.8 | 85.8 | 89.4 | 91.7 | 92.8 | |

| i=10 | 5.6 | 18.6 | 49.2 | 70.0 | 82.1 | 87.0 | 89.8 | 91.6 | 92.9 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 6.8 | 44.2 | 69.0 | 77.2 | 81.8 | 84.2 | 85.1 | 87.0 | 87.3 | |

| i=2 | 6.7 | 30.3 | 60.5 | 72.3 | 78.7 | 82.4 | 84.5 | 86.2 | 88.4 | |

| i=3 | 6.2 | 27.9 | 50.0 | 61.8 | 67.1 | 71.3 | 73.7 | 75.8 | 76.8 | |

| i=4 | 6.8 | 38.3 | 69.2 | 80.2 | 85.3 | 87.5 | 89.4 | 90.2 | 90.9 | |

| i=5 | 6.1 | 22.8 | 54.5 | 73.5 | 81.6 | 85.9 | 87.8 | 90.3 | 91.3 | |

| i=6 | 6.1 | 19.7 | 49.8 | 70.8 | 79.9 | 85.0 | 88.6 | 90.1 | 90.9 | |

| i=7 | 5.8 | 14.5 | 38.2 | 62.8 | 75.1 | 82.1 | 86.1 | 88.7 | 90.6 | |

| i=8 | 6.2 | 24.4 | 56.1 | 73.1 | 80.2 | 84.1 | 86.6 | 89.3 | 90.5 | |

| i=9 | 5.5 | 15.3 | 41.6 | 63.8 | 76.8 | 82.6 | 86.5 | 88.1 | 89.7 | |

| i=10 | 5.8 | 18.2 | 45.9 | 66.8 | 77.8 | 83.3 | 86.9 | 89.4 | 91.0 | |

| i=1 | 5.7 | 42.1 | 66.6 | 76.2 | 80.8 | 83.3 | 84.1 | 86.3 | 86.6 | |

| i=2 | 5.7 | 28.1 | 58.9 | 71.0 | 77.9 | 81.6 | 83.8 | 85.7 | 87.8 | |

| i=3 | 5.5 | 26.2 | 48.4 | 60.3 | 65.8 | 70.0 | 72.7 | 74.8 | 75.8 | |

| i=4 | 5.5 | 38.5 | 68.3 | 79.4 | 84.7 | 86.8 | 88.9 | 89.8 | 90.6 | |

| i=5 | 5.4 | 22.8 | 54.0 | 72.7 | 80.9 | 85.6 | 87.4 | 89.7 | 90.9 | |

| i=6 | 5.3 | 20.1 | 50.0 | 70.8 | 79.5 | 84.6 | 88.2 | 89.8 | 90.4 | |

| i=7 | 5.1 | 14.6 | 39.2 | 63.7 | 75.3 | 82.1 | 85.6 | 88.5 | 90.4 | |

| i=8 | 5.3 | 22.7 | 54.2 | 71.8 | 79.4 | 83.8 | 85.9 | 88.7 | 89.9 | |

| i=9 | 5.1 | 14.9 | 40.9 | 63.0 | 76.0 | 82.2 | 85.9 | 87.5 | 89.2 | |

| i=10 | 5.2 | 17.1 | 43.9 | 65.2 | 76.8 | 82.6 | 86.4 | 88.8 | 90.6 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 7.7 | 76.5 | 92.6 | 96.4 | 97.4 | 97.8 | 98.0 | 98.4 | 98.5 | |

| i=2 | 6.0 | 55.1 | 87.2 | 94.7 | 96.3 | 97.2 | 98.0 | 98.4 | 98.5 | |

| i=3 | 5.1 | 60.9 | 86.3 | 92.1 | 94.4 | 95.5 | 96.1 | 96.7 | 96.6 | |

| i=4 | 5.3 | 63.3 | 91.4 | 96.0 | 97.6 | 98.0 | 98.6 | 98.6 | 98.9 | |

| i=5 | 5.3 | 39.4 | 78.4 | 92.6 | 95.7 | 97.2 | 97.9 | 98.4 | 98.5 | |

| i=6 | 5.1 | 34.7 | 72.3 | 89.6 | 95.5 | 96.8 | 97.9 | 98.1 | 98.4 | |

| i=7 | 4.7 | 25.4 | 59.7 | 82.8 | 91.7 | 95.2 | 96.6 | 97.5 | 98.3 | |

| i=8 | 5.7 | 44.1 | 81.1 | 92.4 | 95.9 | 97.3 | 98.0 | 98.1 | 98.6 | |

| i=9 | 5.1 | 28.0 | 62.7 | 84.5 | 92.9 | 95.8 | 97.2 | 97.6 | 98.4 | |

| i=10 | 5.2 | 31.6 | 68.2 | 86.8 | 93.7 | 96.2 | 97.4 | 98.0 | 98.3 | |

| i=1 | 7.6 | 76.2 | 92.3 | 96.2 | 97.2 | 97.7 | 97.9 | 98.3 | 98.4 | |

| i=2 | 5.3 | 53.3 | 86.0 | 94.2 | 96.2 | 97.1 | 98.0 | 98.2 | 98.5 | |

| i=3 | 4.2 | 58.3 | 85.6 | 91.6 | 94.2 | 95.4 | 95.9 | 96.4 | 96.3 | |

| i=4 | 6.1 | 65.4 | 91.8 | 96.0 | 97.6 | 97.9 | 98.5 | 98.5 | 98.9 | |

| i=5 | 6.0 | 41.0 | 78.3 | 92.5 | 95.8 | 97.1 | 97.8 | 98.4 | 98.4 | |

| i=6 | 5.9 | 36.3 | 73.4 | 89.8 | 95.4 | 96.7 | 97.9 | 98.1 | 98.4 | |

| i=7 | 5.8 | 27.6 | 61.7 | 83.5 | 92.0 | 95.3 | 96.7 | 97.6 | 98.2 | |

| i=8 | 5.4 | 43.1 | 80.1 | 91.9 | 95.5 | 97.2 | 97.9 | 98.0 | 98.6 | |

| i=9 | 5.4 | 28.4 | 62.6 | 84.2 | 92.6 | 95.7 | 97.1 | 97.5 | 98.2 | |

| i=10 | 5.1 | 30.9 | 66.6 | 86.4 | 93.4 | 96.0 | 97.3 | 97.8 | 98.1 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 8.3 | 74.1 | 91.9 | 95.3 | 96.5 | 97.3 | 97.7 | 98.0 | 98.1 | |

| i=2 | 5.7 | 55.0 | 84.4 | 92.7 | 95.6 | 96.8 | 97.6 | 97.7 | 98.3 | |

| i=3 | 5.1 | 57.3 | 83.0 | 90.5 | 93.0 | 94.9 | 95.2 | 96.0 | 96.2 | |

| i=4 | 5.4 | 61.9 | 89.8 | 95.4 | 97.2 | 97.8 | 97.9 | 98.5 | 98.8 | |

| i=5 | 5.7 | 39.4 | 76.9 | 91.0 | 95.3 | 96.5 | 97.7 | 98.2 | 98.4 | |

| i=6 | 5.4 | 33.7 | 72.1 | 88.7 | 94.5 | 96.3 | 97.1 | 97.8 | 98.1 | |

| i=7 | 5.1 | 24.7 | 58.9 | 81.3 | 91.0 | 94.8 | 96.4 | 97.8 | 98.0 | |

| i=8 | 6.4 | 43.2 | 79.6 | 92.0 | 95.3 | 96.8 | 97.2 | 98.0 | 98.2 | |

| i=9 | 5.5 | 26.8 | 62.1 | 83.2 | 92.1 | 95.2 | 96.6 | 97.6 | 98.1 | |

| i=10 | 5.7 | 31.0 | 67.5 | 87.2 | 93.3 | 95.7 | 97.0 | 97.7 | 97.9 | |

| i=1 | 8.1 | 73.5 | 91.4 | 95.0 | 96.3 | 97.1 | 97.6 | 97.9 | 98.0 | |

| i=2 | 5.3 | 53.4 | 84.0 | 92.4 | 95.3 | 96.8 | 97.5 | 97.6 | 98.2 | |

| i=3 | 4.3 | 55.0 | 81.5 | 89.7 | 92.6 | 94.5 | 95.0 | 95.7 | 96.0 | |

| i=4 | 6.7 | 64.6 | 89.9 | 95.6 | 97.0 | 97.7 | 97.8 | 98.4 | 98.8 | |

| i=5 | 6.5 | 41.2 | 77.5 | 91.1 | 95.1 | 96.5 | 97.6 | 98.1 | 98.5 | |

| i=6 | 6.5 | 36.1 | 72.9 | 88.8 | 94.6 | 96.4 | 97.0 | 97.7 | 98.0 | |

| i=7 | 6.3 | 27.6 | 61.5 | 82.2 | 91.3 | 94.9 | 96.5 | 97.8 | 97.9 | |

| i=8 | 6.1 | 42.1 | 78.8 | 91.2 | 95.1 | 96.5 | 97.0 | 97.9 | 98.0 | |

| i=9 | 5.8 | 27.5 | 62.4 | 82.8 | 91.8 | 94.9 | 96.5 | 97.4 | 98.0 | |

| i=10 | 5.7 | 30.2 | 66.6 | 86.3 | 92.9 | 95.6 | 96.8 | 97.6 | 97.8 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 8.3 | 58.9 | 79.1 | 85.8 | 88.9 | 90.9 | 92.3 | 92.2 | 93.4 | |

| i=2 | 6.2 | 42.8 | 71.6 | 82.5 | 86.5 | 89.1 | 91.5 | 92.5 | 93.1 | |

| i=3 | 6.0 | 41.2 | 64.2 | 73.9 | 79.3 | 82.4 | 84.2 | 85.5 | 86.8 | |

| i=4 | 5.3 | 51.0 | 79.8 | 87.5 | 91.0 | 92.2 | 93.8 | 94.3 | 94.9 | |

| i=5 | 5.3 | 34.1 | 67.1 | 82.1 | 88.3 | 91.0 | 93.2 | 94.1 | 94.1 | |

| i=6 | 5.3 | 29.6 | 62.1 | 80.9 | 88.2 | 91.2 | 93.2 | 93.9 | 94.7 | |

| i=7 | 4.8 | 22.7 | 52.1 | 73.2 | 84.9 | 88.9 | 91.9 | 92.9 | 94.2 | |

| i=8 | 5.9 | 35.5 | 68.9 | 82.1 | 86.9 | 91.1 | 92.0 | 93.6 | 94.3 | |

| i=9 | 5.4 | 24.5 | 54.1 | 74.3 | 84.1 | 88.8 | 91.4 | 93.3 | 94.3 | |

| i=10 | 5.8 | 28.1 | 59.7 | 77.0 | 86.3 | 90.0 | 91.8 | 93.4 | 94.5 | |

| i=1 | 7.7 | 57.1 | 77.7 | 85.0 | 88.2 | 90.5 | 91.8 | 91.9 | 93.0 | |

| i=2 | 5.6 | 40.9 | 70.5 | 81.8 | 86.0 | 88.9 | 91.0 | 92.3 | 92.6 | |

| i=3 | 5.6 | 39.7 | 63.3 | 73.3 | 78.4 | 81.7 | 83.8 | 85.1 | 86.3 | |

| i=4 | 6.1 | 52.4 | 79.6 | 87.3 | 90.7 | 92.2 | 93.6 | 94.0 | 94.9 | |

| i=5 | 5.8 | 34.8 | 67.1 | 82.1 | 88.2 | 90.6 | 92.9 | 93.9 | 94.1 | |

| i=6 | 6.1 | 31.3 | 62.9 | 80.9 | 88.0 | 91.0 | 93.2 | 93.9 | 94.6 | |

| i=7 | 5.7 | 24.7 | 53.9 | 73.8 | 84.9 | 88.6 | 91.9 | 92.8 | 94.1 | |

| i=8 | 5.8 | 34.6 | 68.2 | 81.4 | 86.5 | 90.6 | 91.7 | 93.3 | 94.1 | |

| i=9 | 5.7 | 24.6 | 54.4 | 74.1 | 83.7 | 88.6 | 91.2 | 93.1 | 94.2 | |

| i=10 | 5.7 | 27.1 | 58.2 | 76.0 | 85.6 | 89.6 | 91.5 | 93.1 | 94.2 | |

| 0 | 0.05 | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 | 0.35 | 0.4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| i=1 | 7.5 | 51.3 | 73.3 | 81.0 | 84.7 | 86.6 | 87.5 | 88.8 | 89.3 | |

| i=2 | 6.2 | 38.0 | 66.3 | 76.4 | 82.0 | 85.3 | 87.0 | 88.2 | 90.1 | |

| i=3 | 5.4 | 34.9 | 56.8 | 66.9 | 71.6 | 75.5 | 77.2 | 79.3 | 80.5 | |

| i=4 | 5.7 | 46.3 | 74.2 | 83.5 | 87.6 | 89.2 | 91.2 | 91.5 | 92.2 | |

| i=5 | 5.7 | 30.8 | 62.2 | 78.1 | 84.9 | 88.1 | 90.0 | 91.8 | 92.7 | |

| i=6 | 5.6 | 27.9 | 58.7 | 77.0 | 83.4 | 87.4 | 90.5 | 91.8 | 92.3 | |