Further Education During Unemployment111We are grateful for insightful comments from the co-editor and four anonymous reviewers. We also thank Burt Barnow, Damon Clark, Rajeev Darolia, Sue Dynarski, Nathan Grawe, David S. Lee, Mike Lovenheim, Jordan Matsudaira, Doug Miller, Olivia Mitchell, Ronni Pavan, Ceci Rouse, Haiyuan Wan, Abbie Wozniak, and participants at AASLE, APPAM, CEU, CIRANO-CIREQ, Duke, IZA ed workshop, Northwestern, NTA, Princeton, UC Davis, UVA, and Zurich for suggestions and discussions. Lexin Cai, Amanda Eng, Rebecca Jackson, Hyewon Kim, Suejin Lee, and Katherine Wen provided excellent research assistance. We are indebted to Lisa Neilson and the staff members at the Center for Human Resource Research at Ohio State University, the Ohio Department of Jobs and Family Services, and the Ohio Department of Higher Education for providing the data and answering our many questions. We thank Jeff Smith for generously sharing the National JTPA Study data. Financial support from the Cornell Institute of Social Sciences is gratefully acknowledged. All errors and opinions are our own.222The Ohio Longitudinal Data Archive is a project of the Ohio Education Research Center (oerc.osu.edu) and provides researchers with centralized access to administrative data. The OLDA is managed by The Ohio State University’s Center for Human Resource Research (chrr.osu.edu) in collaboration with Ohio’s state workforce and education agencies (olda.ohio.gov), with those agencies providing oversight and funding. For information on OLDA sponsors, see https://chrr.osu.edu/projects/ohio-longitudinal-data-archive.

Pauline Leung111Email: pleung@cornell.edu

Cornell University

Zhuan Pei222Email: zhuan.pei@cornell.edu

Cornell University

December 2023

Evidence on the effectiveness of retraining U.S. unemployed workers primarily comes from evaluations of training programs, which represent one narrow avenue for skill acquisition. We use high-quality records from Ohio and a matching method to estimate the effects of retraining, broadly defined as enrollment in postsecondary institutions. Our simple method bridges two strands of the dynamic treatment effect literature that estimate the treatment-now-versus-later and treatment-versus-no-treatment effects. We find that enrollees experience earnings gains of six percent three to four years after enrolling, after depressed earnings during the first two years. The earnings effects are driven by industry-switchers, particularly to healthcare.

Keywords: Training, Unemployment, Community College, Dynamic Treatment Effect

JEL codes: J24, J68, I26

1 Introduction

The U.S. labor market has become increasingly polarized in recent decades, as high- and low-skilled jobs grow at the expense of middle-skilled jobs that traditionally employ workers with moderate levels of education (AutorEtAl2006; Autoretal2008). These trends continued through the Great Recession, resulting in disproportionately high unemployment among workers without a college degree (Katz2010; Hoynesetal2012). A long line of research shows that job displacement, especially during economic downturns, is associated with large and persistent earnings losses, adverse health outcomes, and negative impacts on the children of the unemployed (JacobsonEtAl1993; CouchPlaczek2010; Krolikowski2018; SullivanandVonWachter2009; DavisvonWachter2011; Oreopoulosetal2008; StevensandSchaller2011). To mitigate these social and economic costs, economists and policymakers across the political spectrum have advocated for new skill acquisition through further education. At the peak of the Great Recession, for example, the U.S. Departments of Labor and Education created the website opportunity.gov and encouraged state governments to contact unemployment insurance (UI) claimants and inform them of resources (e.g., federal financial aid) and institutions (e.g., community colleges) for reskilling.

Much of our knowledge about the effects of further education for unemployed workers in the U.S. comes from evaluations of government-sponsored training programs (e.g., the Workforce Investment Act program, or WIA, now replaced by the Workforce Innovation and Opportunity Act, or WIOA), even though these programs only constitute one narrow avenue through which unemployed workers upgrade their skills. In reality, many more workers enroll directly in a local postsecondary institution such as a community college. For instance, in the fall of 2017, 4.5 million nontraditional (i.e., 25 years old or above) undergraduate students were enrolled nationwide, compared to 1.6 million participants in the largest U.S. training program in 2016-17 (WIOA Adult and Dislocated Worker programs), of which only a minority received training services (NCES_Digest2018; WIA_Databook_2016). While a large literature analyzes the effects of community college education (see KaneRouse1999 and BelfieldBailey2011 for reviews), few studies focus on unemployed workers, a policy relevant group that differs from other community college attendees. Unemployed workers tend to be older and more experienced, but they have different opportunity costs, face different labor market barriers, and therefore may see different returns to further education. The only studies that directly examine unemployed workers enrolled in community colleges are Jacobson_etal2005_JE; Jacobson_etal2005_ILR, which focus on long-tenured Washington state workers laid off in the early 1990s. This leaves a nearly twenty-year research void on this important topic.

Our study seeks to fill this void. We estimate the labor market effects of retraining among unemployed workers, where retraining is broadly defined as enrollment in a postsecondary institution.111We use the word “retrain” in accordance with its meaning by the Cambridge Dictionary: to learn new skills so you can do a different job, or to teach someone a new skill so that they can do a different job. Workers can “retrain” irrespective of their educational background. We link together high quality administrative data from the state of Ohio, which include UI claims, quarterly wage records, course enrollment and credential data from all in-state public higher education institutions (including community colleges and technical centers), and WIA records. By following unemployed workers who filed a UI claim between 2004 and 2011, we observe that indeed the majority of retraining does not occur within the context of a narrowly defined training program: in our data, nearly 88,000 workers enroll in public postsecondary institutions following a layoff, compared with 27,000 workers who retrain through WIA.

We also tackle methodological issues along the way of our empirical inquiry. To estimate the effects of retraining, we use a matching method that compares the labor market outcomes of unemployed workers who pursue further education (enrollees) versus observably similar workers who do not (matched non-enrollees) within two years after layoff. Because workers enroll at different times, a standard matching estimand will only identify the effect of enrolling now versus potentially enrolling later (e.g., Sianesi2004), but not the effect of enrolling versus not enrolling that we are interested in. We show that, with a testable additional assumption regarding the selection into training that is consistent with AshenfelterandCard1985 and HeckmanandRobb1985JOE; HeckmanandRobb1985book, we can identify a lower bound of the latter effect with a simple modification of the standard estimand. The estimated lower bound appears to be tight in our empirical context.

Our matching specification is informed by the large literature that uses selection-on-observables designs to evaluate training programs in both the U.S. and international contexts (see McCalletal2016_Handbook for a comprehensive review). Moreover, to support our specification, we have conducted our own validation analysis in the spirit of LaLonde1986, using data from the National Job Training Partnership Act Study (NJS) (details can be found in our previous working paper LeungandPei2020). This analysis, which builds on the influential work by Heckman_etal1997, Heckmanetal1998_ECMA, and HeckmanSmith1999, evaluates the ability of various models and specifications (including those based on machine-learning) to recover a causal effect. We find that when we have a sample of workers recently attached to the labor market and incorporate detailed earnings histories linearly into the covariate set, conventional (logit-based) propensity score matching performs well, indicating the plausibility of the underlying conditional independence assumption.

We graphically present the average earnings trajectories of enrollees and matched non-enrollees in the five years before and four years after enrollment. The trajectories reveal little difference in earnings pre-enrollment, followed by temporarily depressed earnings of enrollees while they are in school (the “lock-in” effect), and sustained positive effects thereafter. Overall, we estimate that the lower bound earnings effect among enrollees is $348 per quarter, or about six percent, in the third and fourth years after enrolling. A decomposition of this earnings gain reveals that retraining affects earnings mostly at the extensive margin. While the magnitudes of enrollment effects are heterogeneous across various subgroups, we consistently observe positive earnings gains four years after enrolling. Following an early subset of workers for a longer period, we find that the retraining effect persists and widens to 13 percent at the end of a ten-year horizon.

Another advantage of our study relative to existing training program evaluations is our ability to look into the “black box” of retraining. That is, we observe the courses taken and credentials received by enrollees in our sample, which allows us to explore the types of training underlying our estimates. A simple accounting suggests that the enrollment effects are driven by workers who train and subsequently find employment in new industries post-layoff, particularly the healthcare sector.

This paper makes the following contributions. First, it bridges two largely separate strands of empirical literature on training programs and on community colleges by studying the policy-relevant unemployed worker population that intersects with both. As mentioned above, the U.S. training literature focuses mainly on evaluating government sponsored programs, which finds mixed results.222For WIA, recent experimental and non-experimental evaluations find zero to long-lasting negative effects of training for dislocated workers (Heinrichetal2008; Anderssonetal2013; McConnelletal2016; Fortsonetal2017). For the Trade Adjustment Assistance (TAA) program, which provides training to workers affected by trade, one non-experimental evaluation finds initially large negative effects that fade to zero over a four-year period, while another study utilizing quasi-random variation on TAA petition approvals finds positive effects, though the two studies present estimates of different quantities that are not directly comparable (Schochet2012; Hyman2018). In the community college literature, recent studies that use administrative earnings and transcript data show that associate degrees yield earnings gains of about 18 to 26 percent relative to no degree, mixed effects of other credentials, and positive effects of healthcare-related programs (see review by Belfield_Bailey2017a). As noted above, Jacobson_etal2005_JE; Jacobson_etal2005_ILR are the only studies that look at the community college effects on unemployed workers. Their preferred regression model suggests that enrollment increases earnings between six and eight percent (their main earnings effect finding of nine to thirteen percent is for one year of full-time enrollment, and we scale it based on the average course load in their data), but their estimates are sensitive to the model used.333Most of the community college research using similar administrative earnings data rely on a fixed effects model. In our setting, we find differential pre-trends between enrollees and non-enrollees that would render estimates from fixed effects models biased, similar to Jacobson_etal2005_JE. We also find that fixed effects specifications yield biased estimates in our validation exercise (see LeungandPei2020).

Second, we contribute methodologically to the dynamic treatment effect literature by connecting the studies that estimate the treatment-now-versus-later and treatment-versus-no-treatment effects of training. In particular, by modifying the treatment-now-versus-later estimand per Sianesi2004, we can use "static" propensity score matching to bound the treatment-versus-no-treatment effects on the treated that are typically identified with dynamic estimands as in Lechner2009JBES and LechnerandMiquel2009. Our simple estimator can be implemented with off-the-shelf software commands and avoids the inferential challenges their dynamic counterparts encounter.

Finally, this paper sheds light on the effects of retraining for a recent period, which includes the Great Recession and covers a wide range of economic conditions, and in a Rust Belt state characterized by movement away from declining manufacturing industries. Recency of data is important: labor market trends such as the rise in automation and trade in past decades (Autoretal2013; Autoretal2014; AcemogluRestrepo2020) may have impacted training effects particularly in former manufacturing centers, which makes our estimates more informative for current policy-making relative to those by Jacobson_etal2005_JE; Jacobson_etal2005_ILR from Washington state in the early 1990s. The economic boom and bust in our sample period allow us to speak to the literature examining the dependence of educational returns on labor market conditions. Consistent with previous studies (LechnerWunsch2009; Kahn2010; Oreopoulosetal2012), we find retraining leads to larger average earnings gains for those enrolled during the Great Recession, who sought jobs afterwards in a thawing labor market.

2 Institutional Background

2.1 Unemployment Insurance

In this paper, we identify unemployed workers as those who claim unemployment insurance. To be eligible for UI, workers must have lost a job through no fault of their own and have sufficient earnings and work weeks prior to job loss. In Ohio, workers must have worked at least 20 weeks and have an average weekly wage of about $200 per week in the one-year period that begins five calendar quarters prior to job loss. As a result, our study population consists of UI claimants previously attached to the labor force.

While workers generally need to actively search for jobs and be available to work in order to continue receiving benefit payments, they can pursue “approved training” opportunities without losing UI eligibility. States vary in their definitions of approved training, though it generally includes vocationally-oriented or basic education training. According to NASWA2010, the Ohio unemployment agency automatically approves all training through workforce programs and has 7,000 courses listed as approved. It also approves academic courses that do not lead to a specific occupation on a case-by-case basis.

2.2 Postsecondary Institutions

Our study focuses on the impact of classroom training, which can take place in different settings. First, workers may choose to attend community colleges and enroll in courses that may lead to an associate degree or sub-associate credentials such as certificates. Alternatively, workers may enroll at technical centers. Technical centers typically offer occupation-specific programs that may lead to a state license or other credentials. Examples include state license for practical nursing or professional certification in welding.

The cost of attendance varies by institution and program. According to the Integrated Postsecondary Education Data System (IPEDS), the average tuition and fees across Ohio institutions were approximately $6,400 per year in 2010. However, since unemployed workers are often financially constrained, they are likely to be eligible for and rely on several forms of financial assistance. First, workers may be eligible for federal financial aid such as Pell grants, subsidized loans, and tuition tax credits.444Although the amount of federal aid typically depends on income from about two years prior, UI claimants may qualify for simplified needs tests or automatic zero expected family contribution starting in 2009. Second, they may obtain training funding from workforce programs like WIA or TAA. In WIA, eligible participants may receive an Individual Training Account (ITA) voucher that can be used towards approved training (fewer than 20 percent of WIA participants receive training services, while the others only receive “core” or “intensive” services such as assistance in job search, placement, employment and career planning). The TAA program provides tuition assistance to workers affected by import competition. To understand the relative sizes of the various sources of financial assistance, BarnowSmith2016 report that in 2014, Pell Grants for those who pursued vocational education totaled $8.2 billion. In contrast, the expenditures for the WIA Dislocated Worker program and TAA were only $1.2 and $0.3 billion, respectively.

3 Data, Analysis Sample, and Descriptive Statistics

Our analysis primarily draws on several administrative data sources from Ohio: 1) UI claim records, 2) student records from public postsecondary institutions, including community colleges and technical centers, 3) quarterly wage records, and 4) WIA participant records.

For our analysis of labor market effects, we study workers who file an eligible UI claim between 2004 and the third quarter of 2011. To focus on workers who seek further education after unemployment, we exclude those who enroll at any point within two years prior to layoff.555This restriction eliminates roughly 147,000 claims. The excluded claimants are younger with lower tenure and lower pre-layoff earnings. Our analysis sample contains 1.9 million claims, coming from 1.3 million unique individuals (see Appendix A for details on sample construction and data elements). The UI records contain the claim date, demographics (gender, race, number of dependents, age, and zip code), and prior job information (industry and occupation).666The number of dependents is recorded because the maximum UI benefit amount is higher when a claimant has more dependents. However, only workers with high enough prior earnings receive the maximum UI amount. Since many workers’ UI benefits do not change with dependents, this measure likely understates the true number of dependents.

Our schooling data cover all public postsecondary institutions in Ohio. The Higher Education Information system (HEI) records contain enrollment information for 37 public two- and four-year institutions, though we focus on those who first enroll in a two-year institution in this analysis. In the HEI data, we observe terms enrolled, courses taken, and degrees or other credentials obtained (i.e., graduate or professional, bachelors, associate, or less than two-year awards). We also have student records from 53 publicly funded technical centers through the Ohio Technical Centers (OTC) database. In the OTC data, the courses offered range from one-day courses to certificate programs that last several years. We observe the dates of enrollment in courses as well as any credentials obtained. Despite the expansive coverage of the HEI and OTC data, we do not know whether a worker enrolls in a private institution. While we acknowledge this to be a limitation of our paper as our “non-enrollees” may in fact enroll in a program we do not observe, many studies in the training literature also suffer from similar issues. For example, a survey of trainees in the WIA Gold Standard Evaluation reveals that 28 percent of the training was not funded by WIA (Fortsonetal2017).777Specifically, Fortsonetal2017 find that while 43 percent of workers assigned to the “full WIA” experiment arm self-reported to have trained, only 31 percent in the experiment arm received WIA funding. This implies that percent of the trainees sought training outside WIA. In comparison, the share of observed non-enrollees in our data enrolling in a private institution is likely to be smaller. According to IPEDS, among students 25 or older at two-year or lower institutions in the fall of 2007, less than 10 percent were enrolled in private institutions, of which 94 percent were in for-profit institutions. The unobserved private school enrollment is likely to lead us to understate the effect of training if there is private enrollment in our matched comparison sample—CelliniTurner2019 show that attending for-profit institutions leads to a positive, but statistically insignificant, earnings gain.

We construct our main outcome variables using quarterly earnings data from the state’s UI system (we discuss how out-of-state earnings may impact our estimates in Appendix A). In addition to earnings, we also observe, through the third quarter of 2017, number of weeks worked from 2003 and industry for each private sector employer from 1995 (unlike the UI claim records, the quarterly wage data contain no information on occupation). The long earnings history allows us to observe at least three years of pre-layoff earnings. We also use this data to construct measures of pre-layoff job tenure and outcomes like industry switching.

Finally, we observe whether a worker in our analysis sample is in the WIA Standardized Record Data, which cover participants of WIA Adult, Youth, and Dislocated Worker programs. We use information on the dates of WIA training to identify the subset of enrollees observed in the HEI and OTC data who received WIA training services. Next we state our definition of an enrollee and provide descriptive statistics on enrollee demographics, the timing of enrollment, and enrollment characteristics.

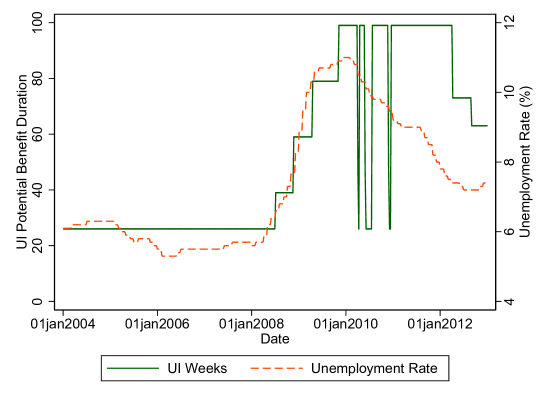

Definition of an enrollee We define an enrollee as a worker who enrolls in a community college or a technical center within two years of layoff.888Since we observe enrollment term rather than date of enrollment in the HEI data, we approximate enrollment terms winter, spring, summer, and fall to the first, second, third, and fourth calendar quarters, respectively. Since enrollment typically occurs in the fall and spring terms, and those terms are likely to begin earlier than the corresponding fourth and second calendar quarters, we are likely to report an enrollment start date that is on average later than when workers actually begin schooling. In 2013, all Ohio public colleges switched to the semester system, which eliminates the corresponding winter quarter. The two-year window is motivated by the fact that UI benefits were available for up to 99 weeks during the Great Recession, which our analysis period covers. We choose to have a consistent definition of treatment by using the same two-year window throughout the entire sample, even though UI is only available for 26 weeks under normal economic conditions. One may be concerned as to whether workers receiving 26 weeks of UI are still unemployed two years after layoff, but as we show in Section 5, enrollees on average have continuously depressed earnings between layoff and enrollment regardless how soon they enroll.

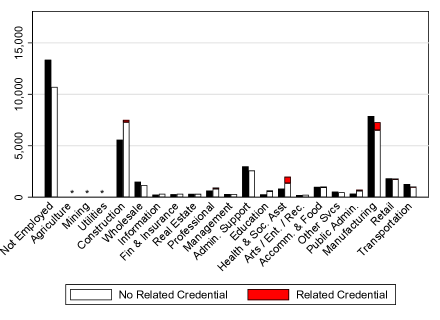

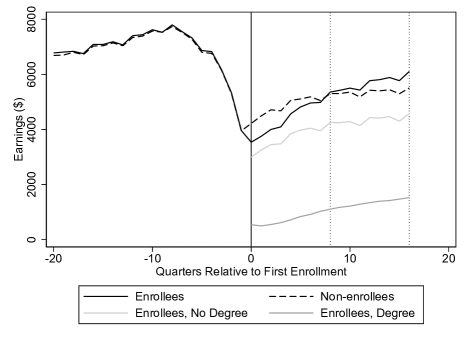

Who enrolls? Panel A of Table 1 presents descriptive statistics for our UI claimant sample by enrollment status. Of the 1.9 million claims in our data, 71,745, or 4 percent, are followed by enrollment in a public postsecondary (two-year or less) institution. While women make up only 34 percent of UI claimants, they are better represented among enrollees, at 44 percent. Compared with 13 percent among non-enrollees, African Americans make up 18 percent of the enrollee population. In terms of prior job characteristics, enrollees are less likely to have worked in manufacturing and transportation, have lower job tenure, are younger, and have lower prior earnings (all earnings are expressed in 2012 dollars).

When do workers enroll, and what are their enrollment characteristics? Table 2 shows that workers take time to enroll—on average 3.7 quarters after layoff—and the mean enrollment length is 4.5 terms. Enrollees in our UI claimant sample mostly attend community colleges (87 percent). 90 percent of enrolled workers take at least one occupational course, and the average proportion of occupational courses is 60 percent, where courses are classified as occupational based on their Classification of Instructional Program (CIP) code following the taxonomy by the National Center of Education Statistics. The overall credential receipt rate within four years of enrollment (including sub-baccalaureate awards, licenses, and industry credentials) is 26 percent. The majority of degrees or credentials obtained are associate degrees or lower: sub-associate credentials account for 58 percent of total credential receipts, associate degrees for 40 percent, and bachelor’s and graduate degrees make up the remaining 2 percent (while we focus on workers who begin enrollment in a community college or technical center, some eventually go on to four-year institutions).

4 Identification, Estimation, and Empirical Implementation

The empirical challenge in estimating labor market effects of enrollment stems from the differences in the characteristics of workers who do and do not enroll that relate to their future earnings potential. Following a long line of research in training program evaluation as reviewed by McCalletal2016_Handbook, we adopt a selection-on-observables research design to measure the causal effects of retraining. Because enrollment timing relative to layoff varies across workers, we rely on a dynamic framework for partial identification, with our main proposition providing a treatment effect lower bound. We discuss the underlying assumptions and define the treatment effect parameters of interest in Section 4.1 below.

Before we proceed, we highlight several rationales for why matching may “work” in our context, given the (often justified) skepticism towards it. First, our sample construction helps to mitigate the “Ashenfelter’s dip” problem, a major challenge in training program evaluation. The Ashenfelter’s dip refers to the phenomenon in most evaluations of U.S. training programs wherein trainees experience (on average) an earnings dip prior to training, while non-trainees do not. This is likely because the decision to retrain is often a reaction to transitory shocks (Ashenfelter1978). A prime example of such shocks is the loss of employment. By starting from the set of recently unemployed workers in Ohio, we shut down job loss as a channel that triggers training, as both enrollees and non-enrollees in our sample have experienced it.

Second, in our matching specification we take advantage of the information available on past labor market histories from our rich administrative data, which makes the selection-on-observables assumption plausible as recent studies have argued. As Anderssonetal2013 succinctly state, “[m]otivated workers, and high ability workers, should do persistently well in the labor market; if so, conditioning on earlier labor market outcomes will remove any selection bias that results from motivation and ability also helping to determine training receipt.” Anderssonetal2013 also find that adding firm fixed effects does not change causal estimates relative to specifications which incorporate detailed labor market histories. Similarly, in extensive empirical Monte Carlo simulations based on German administrative data, LechnerWunsch2013 find that including variables on firm characteristics, industry- and occupation- specific experience, health, program compliance, desired job characteristics, and detailed regional information does not further reduce bias relative to only using basic demographics and labor market histories. Finally, Caliendoetal2017 find that controlling for typically unobserved non-cognitive traits adds little beyond past labor market histories.

Third, our matching specification is guided by a validation exercise in the spirit of LaLonde1986, Heckman_etal1997, and Heckmanetal1998_ECMA. As described in detail in a previous version of this paper (LeungandPei2020), we use data from the NJS to assess whether more flexible machine-learning-based specifications offer better performance than a conventional (logit) propensity score model where the terms enter linearly. We find that conventional propensity score matching methods perform competitively even without the use of machine learning algorithms, and is able to recover a causal effect in subsamples that more closely resemble our Ohio study population—namely workers with previous labor market attachment, for whom past earnings are likely to be predictive of future prospects.

Fourth, the specification informed by our validation study leads to high quality of matching. In Section 4.4, we show overlapping support in the propensity score distributions (except for outliers that amount to one percent of the enrollee sample) and covariate balance across enrollees and matched non-enrollees.

Finally, we believe matching to be better suited than other empirical methods for our setting. In Appendix C, we explore the possibility of adopting alternative research designs—which may identify different causal parameters than matching—including fixed effects models, the use of a distance instrument, and a regression discontinuity design based on layoff timing. We discuss why we cannot use them for our analysis.

Despite these reasons in favor of using matching for our analysis, doubts may still linger over the validity of the selection-on-observables assumption. Chief among them is the possibility that even within a matched pair with the same labor market history, the non-enrollee chooses not to enroll because she expects to be recalled to her previous employer or has a job offer in hand to start in the future (Sianesi2004; FredrikssonJohansson2008). As we show next, our main identification result provides a lower bound on a dynamic treatment effect parameter, and the presence of such “forward-looking” workers may further bias our estimate downward against us finding an enrollment effect.

4.1 Parameters of Interest, Identification and Estimation

The main assumption underlying our method is the conditional independence assumption (CIA), or “unconfoundedness”. For expositional purposes, we begin with the simple static case where enrollment decision takes place at one point in time for all laid-off workers. Let denote whether a worker enrolls in school, with if the worker enrolls and if she does not. Let denote the potential post-enrollment earnings of the worker: is the worker’s potential future earnings if she enrolls, and is her potential future earnings if she does not enroll. The observed outcome is .

The static unconfoundedness assumption standard in the matching literature is

| (1) |

where is a vector of observed covariates realized at or prior to enrollment. Together with a common support condition—the propensity score is less than one (almost) everywhere on the support of —CIA implies the identification of the treatment effect on the treated (TOT) parameter via propensity score matching:

| (2) |

In our study, the “treatment” (enrollment) is allowed to occur over a period of two years, a complication that necessitates a dynamic variant of the framework above. An important consideration in the dynamic setting is the treatment effect parameter of interest. Several earlier studies (Sianesi2004; FredrikssonJohansson2008; Biwen_etal2014) rely on the dynamic counterpart of the conditional independence assumption and use an estimand similar to that in equation (2) to identify the treatment effect of enrolling in one period versus not enrolling in that period but possibly later in the two-year window (the “treatment-now-versus-later” effect). This is different from the dynamic version of the TOT parameter we are interested in, which is the effect of enrolling versus not enrolling in the two-year window (the “treatment-versus-no-treatment” effect). As McCalletal2016_Handbook point out, the “treatment-versus-no-treatment” parameter may be more useful than the “treatment-now-versus-later” parameter, as the former can be more easily incorporated into a cost-benefit analysis.999The “treatment-now-versus-later” effect may be the more relevant parameter such as in the analysis of the earnings impact of job displacement (Krolikowski2018).

In this paper, we modify the method used by studies that estimate the “treatment-now-versus-later” effect. This modified method preserves the simplicity of static propensity score matching and can partially identify the dynamic TOT parameter under an additional testable assumption. In the remainder of this subsection, we state our assumptions and identification results. We discuss the connection between our method and alternatives in the dynamic treatment effect literature in the next subsection.

For ease of exposition, we focus on a two-period case here and leave the more general multi-period case to Appendix B (we have an enrollment window of eight quarters in our empirical setting). In the two-period case, equals one if a worker starts training either in the first or second period post-layoff. We use the binary variable to denote whether a worker begins enrollment in period 1, and to denote whether she begins enrollment in period 2. It follows that with two implications. First, implies that and (a worker who never enrolls does not start training in either period). Second, at most one of and can equal one, meaning that implies (a worker who already enrolls in period 1 is no longer “at risk” for starting enrollment in period 2), and vice versa (a worker who starts enrollment in period 2 cannot have enrolled in period 1).

We use and to denote the vectors of conditioning covariates available at the beginning of the first and second period and before the realization of and , respectively. The superscript notation, consistent with AbbringandHeckman2007, indicates that the covariates incorporate cumulative information up to the beginning of a time period before the training decision for that period. More concretely, we think of as incorporating the relevant covariates available at the beginning of period 1 and before the realization of ; includes all the variables in , and also additional variables realized after but prior to .101010The conditioning set notation in Lechner2009JBES and LechnerandMiquel2009 is similar: our and correspond to their and . Denoting earnings of period by , which realizes at the end of the period, the additional variables in but not typically include . In summary, the sequence of variable realizations is:

Note that because training can only take place during period 1 or 2 in the two-period case, it is not necessary to include the conditioning set and treatment when in the sequence above.

Finally, we use and to denote the potential earnings at the end of period . Our main identification result uses the following observation rule: for a worker who begins enrollment in period (), the observed post-treatment () outcome is ; for a worker who enrolls in neither period, for all . Missing from the observation rule is the relation between observed and potential pre-treatment outcomes among the treated population. While it is tempting to write for a period- enrollee when , doing so requires an additional assumption of no anticipation. No-anticipation is not needed for our main identification result, but we do invoke it to derive testable implications of our assumptions—more details below and in Appendix B.1.

Here are the assumptions for our main identification result. The first is a dynamic CIA assumption

Assumption 1.

a) for and b) for .

Assumption 1 and variations thereof are standard in the literature—they are referred to as “sequential randomization” (e.g., Robins1997) or “weak dynamic conditional independence” (e.g., Lechner2009JBES). In our context, it says that within the “at-risk” set of workers who have not yet enrolled and are therefore able to begin enrollment at the start of period (), the potential future outcome is independent of a worker’s enrollment decision conditional on the information available. Following an argument analogous to the static case, Assumption 1 allows for the identification of the training effect for period-2 enrollees when conditioning on and (i.e., the effect of ). By simply conditioning on , it also allows for the identification of the effect of enrolling in period 1 versus not enrolling in period 1 but possibly in period 2 (i.e., the effect of ) with the estimand:

| (3) |

for . However, it is more complex to identify the TOT parameter of training versus no-training (i.e., the effect of ) for period-1 enrollees. We invoke an additional assumption to bound it from below:

Assumption 2.

Assumption 2 says that among workers who have the same observable characteristics at the beginning of period 1, those who begin enrollment in period 2 have lower average potential future earnings absent training than their never-enrolled counterparts. It reflects the idea that workers who select into training tend to have lower opportunity costs in doing so. As we discuss in Appendix B.1, under additional conditions that are not substantively more restrictive, this assumption is consistent with models of selection into training by AshenfelterandCard1985 and HeckmanandRobb1985JOE; HeckmanandRobb1985book (henceforth, AC and HR, respectively). The AC and HR frameworks also lead to testable implications: To the extent that the earnings process has positive serial dependence, the observed period-1 earnings among period-1 non-enrollees can proxy for their future potential outcome (as mentioned above, this test requires an additional no-anticipation assumption, but we point out in Appendix B.1 that AC and HR’s specifications of the earnings process implicitly maintains this assumption). Thus, we can test Assumption 2 by comparing the of period-2 enrollees and never-enrolled workers with similar . The test can be implemented via propensity score matching, and we present evidence in support of Assumption 2 in Section 5.1.

Assumption 2 allows us to bound the TOT effect for period-1 enrollees from below with a simple modification of the treatment-now-versus-later estimand in (3):

| (4) |

The only difference between (3) and (4) is the comparison group: the comparison group in (3) consists of workers who did not enroll in period 1 (, while the comparison group in (4) consists of workers who did not enroll in either period (). Intuitively, it is impossible to identify the TOT with the treatment-now-versus-later estimand (3) because we do not observe of the later-enrollees (i.e., workers in its comparison group who enroll in period 2). By going from (3) to (4), we replace the later-enrollees by non-enrollees with similar , for whom is the observed . Assumption 2 says that these non-enrollees have a higher average , allowing (4) to provide a lower bound for the TOT parameter.

Directly implementing estimand (4) is subject to the curse of dimensionality when contains many covariates. The use of a propensity score is the usual remedy for overcoming this challenge. However, we are not willing to make a strong CIA assumption for the estimand (i.e., ), and, therefore, we do not have a standard propensity score theorem at our proposal. Fortunately, as we show in Appendix B.2, propensity score matching preserves inequality.111111By similar reasoning, propensity score matching also preserves inequality in the simple static setting. Specifically, if selection into treatment is negative conditioning on covariates: , then selection into treatment is also negative conditioning on the propensity score: . This is a useful result, as it can help sign the population bias when propensity score matching.

Formally, define the propensity scores and , and our main identification result is

All proofs are in Appendix B. Part (a) of Proposition 1 consists of identification results for and , the TOTs at time among period-1 and period-2 enrollees, respectively. Part (b) aggregates across the two enrollee populations and provides a lower bound for , the overall TOT parameter at time . For expositional ease, , our time index here, refers to time relative to layoff. But we can also define with an alternative time index, such as time relative to the beginning of enrollment. Concretely, to obtain the overall TOT quarters after enrollment, we take an average of and weighted by the shares of period-1 and period-2 enrollees. Since enrollment is our treatment variable of interest, we use this alternative time indexing in most of our empirical analyses, which is consistent with the convention in event studies.

The identification results in Proposition 1(a) lead to standard propensity score matching estimators for the lower bound of and for the value of . We can compute their corresponding asymptotic variances by following Abadie_Imbens2016. To estimate the lower bound of the overall TOT , we simply take an average of the two estimators weighted by the shares of period-1 and period-2 enrollees and compute its asymptotic variance accordingly (details in Appendix B.2).

A natural question that arises is how conservative the lower bounds from Proposition 1 are. It is easy to see that the tightness of our bound for depends crucially on the share of later-enrollees, i.e., . When this share is zero, the lower bound estimand point identifies . Intuitively, if no one enrolls in period 2, the treatment-now-versus-later effect for becomes the treatment effect of enrolling in period 1 versus not enrolling in either period. The bounds are likely to stay informative when this share of later-enrollees is small, which is indeed the case in our empirical context.

More concretely, we can empirically assess the tightness of the bound in two ways. First, we can also construct an upper bound of (and therefore ) via propensity score matching. The construction uses the non-negativity of earnings, allowing us to bound the of later-enrollees by zero from below. We can easily estimate this upper bound and apply standard inference procedures (details in Appendix B.2). The second way is to recognize that is actually point identified under Assumption 1, per results by Lechner2009JBES and LechnerandMiquel2009. While the associated estimator from Lechner’s identification result is more complex to implement and comes with inferential challenges, we can use it to generate a point estimate and compare to our estimated lower bound. In the next section, we discuss the connection of our method to Lechner’s and the broader dynamic treatment effect literature.

4.2 Relation to the Dynamic Treatment Effect Literature

This is certainly not the first paper to consider identification of treatment effects in a dynamic context. As mentioned above, previous studies (e.g., Sianesi2004) have estimated treatment-now-versus-later effects. But many other studies aim to estimate alternative causal parameters. We review relevant research in this latter category below with a particular focus on Lechner’s work, providing more context for our method.121212A recent study by vandenBergVikstrom2019 analyzes dynamic treatment effects on earnings in a setting where training eligibility hinges on a worker remaining unemployed. The closest connection of vandenBergVikstrom2019 to our paper is their treatment effect parameter: they are also interested in the TOT effect of training versus not training. Since workers in our setting are not subject to the eligibility criterion they consider, our methodology is more closely related to the work by Lechner.

In a series of influential studies (e.g., Robins1986; Robins1997; GillandRobins2001), James Robins extends the static potential outcomes framework to consider identification of dynamic treatment effects. Specifically, Robins studies identification of potential outcomes under alternative treatment sequences. These treatment sequences are related to but distinct from our treatment variable defined in Section 4.1: Whereas our treatment variable is whether a worker begins training, each element in Robins’s sequence corresponds to whether a worker receives training in a given period. Under a sequential-randomization assumption and a no-anticipation assumption, the distributions of potential outcomes under alternative treatment sequences are identified in the Robins framework. In Appendix B.4.1, we formally discuss Robins’s assumptions and results by adapting the excellent summary in AbbringandHeckman2007 to our two-period setting.

Two important studies by Lechner2009JBES and LechnerandMiquel2009 extend the work by Robins. They focus on the identification of average effects such as the TOTs and propose estimators based on sequential propensity score matching (LechnerandMiquel2009) and sequential inverse probability weighting (Lechner2009JBES). The estimators offer an advantage over those by Robins as they require no functional form assumptions for potential outcomes.

A remarkable implication of the elegant results by Lechner2009JBES and LechnerandMiquel2009 is that , the TOT for period-1 enrollees from Section 4.1, is point identified under dynamic CIA (Assumption 1). Consequently, the aggregate TOT parameter is also identified under dynamic CIA. Using our notation, the estimand that identifies takes the form:131313Like Robins, Lechner2009JBES and LechnerandMiquel2009 define potential outcomes for various treatment sequences. Using their potential outcome notation (reviewed in Appendix B.4.1), the second term in estimand (7) identifies the mean potential outcome in the counterfactual scenario where period-1 enrollees do not enroll in either period.

| (7) |

In (7), the propensity score for is defined as , which differs from by not conditioning on , i.e., period-2 enrollees are in the at-risk set when computing .

We now provide an intuitive account of Lechner’s identification result and how it relates to ours. For ease of understanding, we focus on identification results with estimands that directly match on covariates—that is, replace the propensity scores , , and in Proposition 1 and (7) by the covariates , , and , respectively. Constructing the Lechner estimand entails two steps in a two-period setting. The first step is equivalent to the treatment-now-versus-later matching of Sianesi2004, for which the matched control set consists of period-1 non-enrollees () with similar . This matched control set can be broken down into two groups of workers: i. those who enroll later () and ii. the “never-enrollees” (). The second step updates the matched control set: it replaces group i by their never-enrolled counterparts with similar (since contains all the covariates in , matching on is equivalent to matching on both and ).

To make sense of these two steps, first note that Assumption 1(a) ensures that the average in the matched control set in step one is the average for the population. The problem is that is not observed for group i, so we need to replace it with observable quantities. This is what step two accomplishes. Under Assumption 1(b), the average among group i’s replacements is equal to the average of group i, which implies that the average of the updated matched control set at the end of step two identifies .

To compare our method with Lechner’s, it is useful to recast our estimand construction also as a two-step process. The first step is identical to Lechner’s, resulting in a matched control set consisting of groups i and ii. In the second step, we also replace group i by their never-enrolled counterparts. But unlike Lechner, these replacements share similar with group i, rather than . Under our Assumption 2, the observed mean among these replacements is a lower bound for the mean of group i. Because we only use covariates , we can merge the two steps and directly look for matches with similar among the never-enrollees.

The point identification of the Lechner estimand is quite appealing, but its implementation is complex especially with many periods. Specifically, an -period setting requires matching steps and involves the estimation of propensity scores. For the two-period case, implementing the estimand (7) involves matching twice: first matching on the estimated propensity score , and then matching on the estimated propensity score vector . We have eight periods for our Ohio analysis, as we allow for an enrollment window of eight quarters post-layoff. As such, we need to perform matching eight times, and each time, the corresponding propensity score vector increases in length by one. LechnerandMiquel2009 sensibly use Mahalanobis matching when matching on multiple propensity scores in their four-period analysis, but concerns with the curse of dimensionality become more relevant with more periods, thereby limiting the general applicability of the estimator.

Furthermore, the complexity with the LechnerandMiquel2009 estimator creates inferential challenges. As with all propensity score matching papers at the time, sampling variation in estimating the propensity score was ignored when computing analytical standard errors. With the advent of Abadie_Imbens2016, it became standard to account for the uncertainty in propensity score estimation. Thus, should we choose to rely on LechnerandMiquel2009, extending Abadie_Imbens2016 to the complex case of Mahalanobis matching on a vector of estimated propensity scores seems warranted, but doing so would distract from the substantive analysis of this paper. Similarly, further investigation on inference is also needed for the inverse propensity weighting (IPW) estimator of Lechner2009JBES, which we discuss in more detail in Appendix B.4.2.

For these reasons, we rely on the partial identification result in Proposition 1 (and the corresponding estimator) to generate our main estimates. Its advantage is simplicity, as the estimation and inference procedures can be implemented using off-the-shelf Stata commands. Its disadvantage is the loss of point identification, but we do not view it as a threat to the empirical substance of our analysis. As mentioned above, we can also construct an upper bound, and together, the two bounds indicate an informative range for the TOT effect. Moreover, we can produce the TOT point estimate by following LechnerandMiquel2009, which is only slightly above our estimated lower bound. We report these estimates in Section 5.1.

Finally, while this section focuses on research that assumes selection on observables, another strand of the dynamic treatment effect literature explicitly models unobserved heterogeneity. Examples include AbbringandvandenBerg2003; AbbringandvandenBerg2004, HeckmanandNavarro2007, and Baetal2017. We provide an overview of these studies in Appendix B.4.3.

4.3 Matching Specification

This section describes our matching specification. As discussed above, the specification is informed by our own validation exercise, described in LeungandPei2020. In particular, we find that in another training context, where detailed earnings histories exist for a sample of recently employed workers, modelling the propensity score as a simple logit where the terms enter linearly performs well against more flexible models. However, the validation exercise sample is quite small relative to the Ohio sample. Since we have a large sample, we use both exact and propensity score matching to ensure that our matched comparison group is as similar as possible to the enrollees.

As described in Section 3, we define enrollees as those who start school within eight quarters after filing a UI claim. Proposition 1 (more precisely, its many-period generalization, Proposition 3) suggests that we can estimate the TOT lower bound separately for those who enroll in the first through eighth quarter after layoff and aggregate them to obtain a lower bound for the overall TOT. The Proposition also states that, for all eight enrollee cohorts, we should construct the corresponding matched comparison group by drawing from the pool of workers who do not enroll within the two-year post-layoff period.

We perform exact matching along three dimensions. First, we require that enrollees be exactly matched to non-enrollees laid off in the same quarter. This is motivated by the fact that economic conditions and policies varied widely over our study period. Workers laid off in 2004 may differ from those starting unemployment at the peak of the Great Recession and face dramatically different labor market landscapes.141414Although Heckmanetal1998_ECMA stress the importance of matching workers from the same local labor market, evidence from Michalopoulousetal2004 and Mueser_etal2007 suggests that this is less important when comparison groups are drawn from a single state. Since our data come from (moderately sized) Ohio, temporal rather than geographic variation capture most of the variation in labor market conditions within our sample. That said, we also include the unemployment rate in the month and county of layoff in the propensity score model, which accounts for geographic differences. Furthermore, policies enacted to help workers overcome challenges during the Great Recession, such as UI extensions and information campaigns about resources for retraining, may have influenced workers’ decisions to enroll (BarrTurner2015; BarrTurner2016). By comparing workers that were laid off around the same time, we attempt to control for the influence of time-varying labor market conditions and policies.

Second, following the training evaluation literature, we require that workers be exactly matched on gender, as decisions to enroll may differ between men and women. As argued by HeckmanSmith1999, men’s decisions to enroll may be more heavily influenced by economic prospects, while women’s decisions may depend more on family responsibilities. The different motivations for enrolling may translate into different training effects across gender.

Finally, we exactly match enrollees and non-enrollees based on whether they were working in manufacturing at layoff. The manufacturing sector is of particular interest to policymakers, as it has been in rapid decline over the past decades (Autoretal2013), particularly in “rust belt” states like Ohio.

Within the (exactly matched) layoff quarter, gender, and manufacturing cells for each of the eight enrollment timing cohorts, we estimate a separate propensity score model. As we demonstrate in the validation study in LeungandPei2020, it is crucial to include pre-enrollment earnings, and we use three years of pre-layoff quarterly earnings as (linear) inputs into the model.151515While the literature also favors including indicators for zero earnings in each quarter, we do not include these to minimize the number of perfect prediction and overlap problems within the exact-matching-cells. However, as discussed later, we find that the inclusion of these indicators do not meaningfully change the estimates in a robustness check. In addition to pre-layoff earnings, we also include quarterly earnings between layoff and enrollment per our identification result (we illustrate the importance of incorporating these earnings with empirical evidence in Section 5.1). Finally, we include in our propensity score model demographic and prior job characteristics to the extent that our data allow it.161616Out of the 980 propensity score models, 27 do not converge to a solution with the full set of covariates. In these cases, we estimate the model by eliminating one covariate (i.e., one industry dummy, demographic variable, or quarter of earnings). Specifically, we include race indicators (white, African American, other, or unknown), pre-layoff sector indicators (construction, wholesale trade, administrative support and waste management, healthcare and social assistance, accommodation and food services, retail trade, transportation, and other), job tenure categories (less than one year, one to six years, and more than six years), age indicators (age below 19, each year from age 19 and 59, and older than 59), whether a worker has a dependent at the time of UI claim, and county unemployment rate during the month of layoff.

We use the estimated propensity score to pair each enrollee with her nearest neighbor from the comparison sample, where each comparison worker may be matched to more than one enrollee (i.e., matching with replacement). Choosing a larger number of neighbors may further reduce variance in the estimated treatment effect, but the quality of the match may deteriorate as we allow for larger propensity score differences between the enrollee and comparison workers. Since we have a large enough sample size to attain precise estimates and are more concerned with bias, we use only one neighbor in our main specification. We do, however, explore the sensitivity of our results with respect to the number of neighbors in Section 5.1.

After each logit propensity score regression, we estimate the (cell-specific) TOT with the average difference in outcomes between each enrollee and its match, and the standard error is computed following Abadie_Imbens2016. We then aggregate the TOTs across the enrollment-timing layoff-quarter gender sector cells to obtain the overall treatment effect, where the weights are proportional to the number of enrollees in each cell.

Given that we match workers along the dimensions discussed above, the question of residual differences between enrollees and matched non-enrollees remains. We argue that these remaining factors that compel workers to enroll are unlikely to be related to future earnings potential, conditional on the covariates used for matching. The empirical literature documents several potential sources of variation. First, research has shown that distance to a community college affects whether a worker ultimately enrolls (Card1993). While distance is not a strong instrument in our setting (Appendix C), it is indeed negatively associated with enrollment. Second, information and nudges appear to influence students’ decision-making. For example, in our context, BarrTurner2016 show that a letter targeted to UI claimants informing them of financial aid resources affects enrollment. Relatedly, complexity in UI rules (such as what constitutes as “approved training” that allow workers to continue receiving benefits) may introduce additional variation in whether workers decide to pursue training opportunities. Third, in the context of training programs, there may be variation in who can access training resources based on requirements set by local job centers (Fortsonetal2017). Finally, there has been evidence of capacity constraints in community colleges and programs within community colleges (e.g., Grosz2020), which may generate exogenous variation in who can enroll.

4.4 Matching Design Quality Check: Overlapping Support and Covariate Balance

As emphasized by Smith_Todd2005, we need to assess the validity of the overlapping support assumption. We first point out that some observations indeed appear to violate this assumption, but they are a tiny fraction of the sample. Specifically, when we use the trimming threshold from the algorithm by Imbensandrubin2015 (p. 367-368), we find that only 842 observations out the nearly 72,000 enrollees are dropped—841 observations are dropped due to perfect prediction within exact matching cells, and one observation has a propensity score that is too close to 1.171717The remaining difference in the enrollee sample size between Panels A and B of Table 1 is due to the elimination of the winter quarter of 2013 in the HEI data mentioned in Section 3. We do not estimate the propensity score and enrollment effect for (OTC only) enrollees who start in that quarter, which eliminates an additional 24 enrollees.

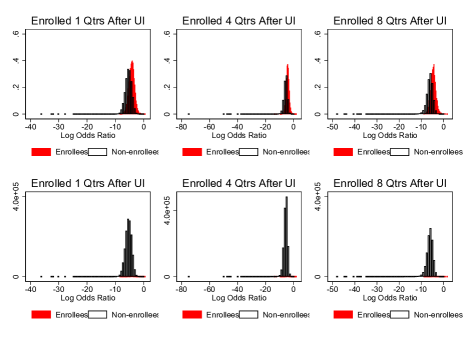

We show the overlap of the enrollee and non-enrollee distributions in Appendix Figure A.1. Because many of the propensity scores are close to zero, for ease of visual inspection, we overlay the histograms of the log odds ratio () of the two groups— is a monotone transformation of the propensity score (i.e. ). In the top row, we plot the estimated log odds ratio distributions for workers who enroll one, four and eight quarters post layoff, and overlay the corresponding distributions for the non-enrollees. We see that the distributions have little support on the positive range, indicating that the propensity score is below 0.5 for the vast majority of observations, and not surprisingly enrollees tend to have a higher propensity to pursue further education. We show the frequency plots of for the two groups in the bottom row, which are more relevant for assessing overlapping support. Because the number of observations in the non-enrollee group is far larger than that in the enrollee group, there appears to be sufficient overlap even in the higher range of the .

To compare covariate values across samples, we follow the literature (e.g., Imbens2015) and report in Panel A of Table 1 the normalized differences between enrollees and non-enrollees for each covariate. That is, for each covariate , we report , where and are the respective sample means of among enrollees and non-enrollees, and and are the corresponding sample standard deviations. The denominator can be interpreted as an average standard deviation (ASD), allowing the normalized difference to be interpreted in percentage terms of the ASD. The covariate that exhibits by far the largest difference is age: Enrollees are younger by 58 percent of ASD. The contrasts are less stark for the other 21 covariates: Nine have a normalized difference below 5 percent of ASD, two between 5 and 10 percent, eight between 10 and 20 percent, and two just above the 20 percent threshold of what RosenbaumRubin1985 consider a large difference (Imbens2015 suggests a higher rule of thumb threshold of 30 percent). In Panel B of Table 1, we show the average characteristics of the matched enrollee and non-enrollee samples. Indeed, covariates are balanced across the two groups: normalized differences are very small, and all -tests fail to reject equality despite the large sample size. We proceed to present our main empirical results on the effects of retraining in the next section, where we also provide additional graphical evidence in support of balance in pre-enrollment earnings trajectories.

5 Empirical Results: Effects of Further Education During Unemployment

5.1 Overall Effects

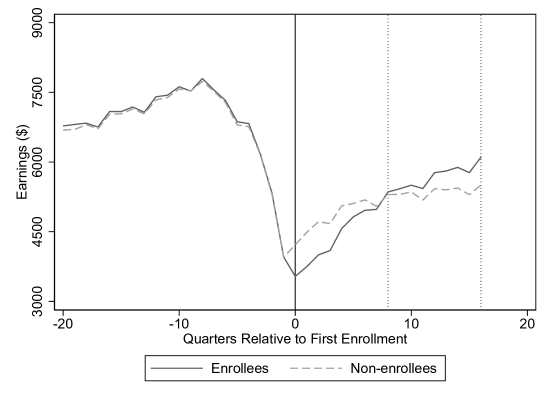

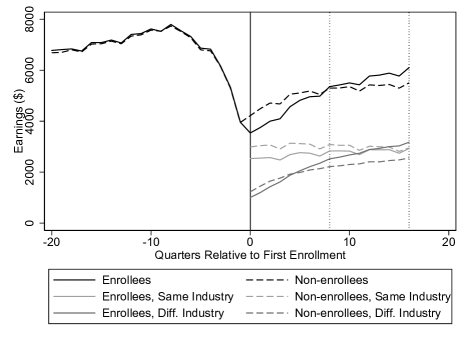

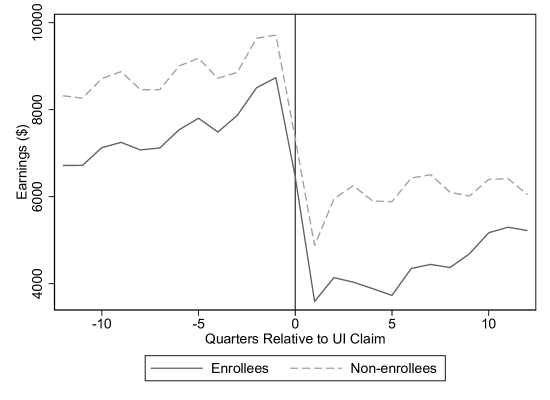

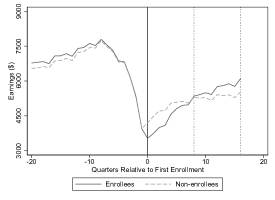

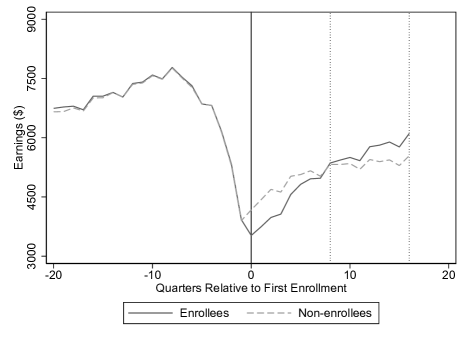

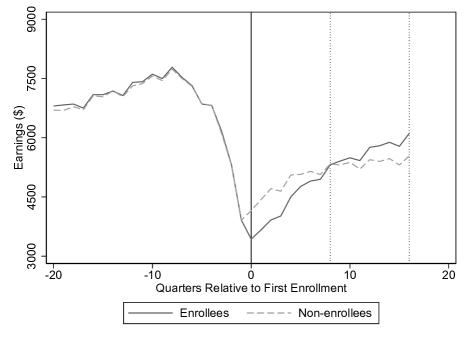

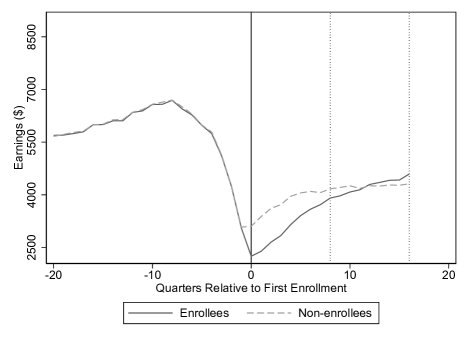

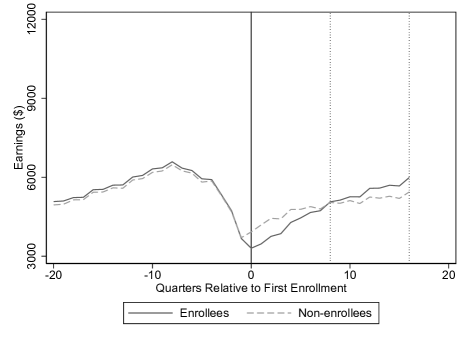

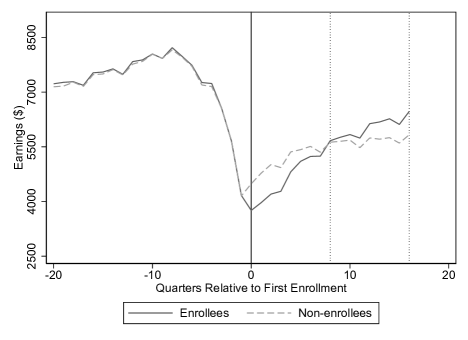

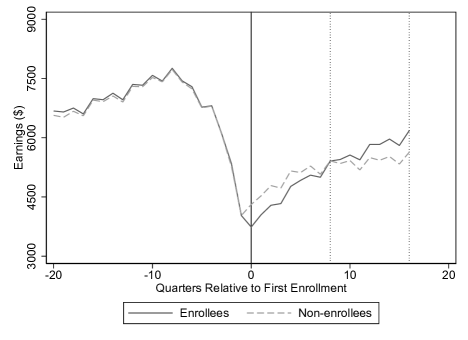

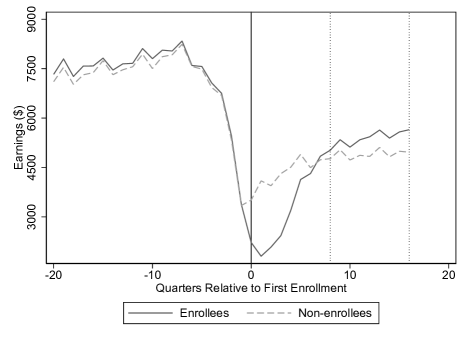

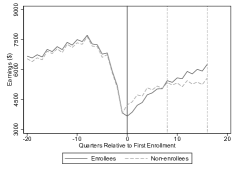

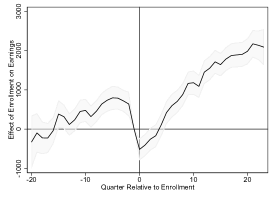

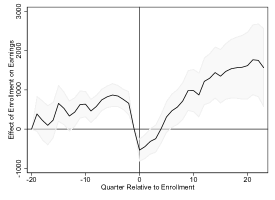

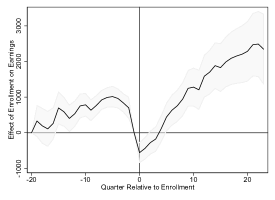

We begin by graphically presenting the average earnings of the full sample of enrollees and their matched non-enrollees. In Figure 1, the solid line shows the average earnings of enrollees over time, from 20 quarters before until 16 quarters after enrollment begins. The dashed line shows the earnings averaged across each enrollee’s nearest neighbor in the non-enrollee sample (see Appendix Figure A.2 for a comparison of earnings trajectories for enrollees and unmatched non-enrollees). Prior to enrollment, both enrollees and their closest comparison workers have similar earnings trajectories, increasing in the period from five years prior to enrollment to approximately two years prior, before dropping to 50 percent of the peak by the time of enrollment. The seemingly slow decline in earnings is due to the fact that we are averaging the earnings of workers who enroll at different times post-layoff, and not because of a drawn-out earnings reduction process for all workers. The close alignment of the pre-enrollment trajectories signifies high match quality and is not mechanically guaranteed just because the earnings enter the logit model for propensity score estimation (see Figure 2 of LeungandPei2020). After enrollment, the two lines begin to diverge. Enrollees have lower earnings for approximately two years before surpassing their comparison group. This “lock-in” effect, which may come about because enrollees are more constrained in their ability to search for jobs and work while in school, is consistent with the finding in Heinrich_etal2013 for the WIA Dislocated Worker program.181818Although the mean (median) enrollment duration is 4.5 (4) quarters in the sample, the average duration between first and last enrollment quarters is closer to 6 quarters due to the fact that workers are not always “continuously” enrolled. Furthermore, it may take some time post-training for earnings to recover: Fortsonetal2017 note that there were about two quarters between when WIA trainees completed training and began post-training employment. The gains appear to grow after the lock-in period while the earnings of non-enrollees flatten. In the third and fourth years post-enrollment, enrollees earn $348 more per quarter than non-enrollees as reported in Table 3, a gain of about six percent. It is notable that even at more than four years after layoff, both enrollees and non-enrollees do not catch up (on average) to their pre-layoff earnings.

As discussed in Section 4.1, these estimates are lower bounds of the enrollment effect, under the assumption that those who enroll in later periods have lower counterfactual earnings than those who never enroll (Assumption 2 and its many-period generalization Assumption 4). We first present evidence in support of this assumption using the test proposed in Section 4.1 and Appendix B.1. Specifically, for an enrollment quarter and a later-enrollee cohort enrolling quarters later (), the test compares their earnings during each of the quarters (before the later-enrollees enroll) against non-enrollees with similar characteristics at the beginning of quarter . We should find lower earnings among later-enrollees under Assumptions 2 and 4 if these interim earnings positively correlate with future potential earnings . We implement the test using propensity score matching and present the earnings differences between later-enrollees and matched non-enrollees for all seven values of (we aggregate across for concise presentation) in Appendix Table A.1. Indeed, all earnings differences are negative, lending credibility to the assumption underlying the lower bound result.

Second, we show that the lower bound is informative in our setting. As discussed in Section 4.2, results from Lechner2009JBES and LechnerandMiquel2009 imply the point identification of the TOT. We implement the sequential propensity score matching estimator of LechnerandMiquel2009 and find that enrollees earn $351 more than non-enrollees in the third and fourth years post-enrollment. Our lower bound estimate of $348 is remarkably close and its 95 percent confidence interval comfortably contains $351. We also construct an upper bound using Proposition 4 in Appendix B.3. Its estimate is $488, or nine percent; together, the two bounds pinpoint an informative range for the earnings effects. The tightness of the bounds results from the small number of later-enrollees relative to non-enrollees, so replacing the later-enrollees’ potential earnings with other values will not have a major impact. The fact that the point-identified estimate is much closer to our lower bound than upper bound suggests that the counterfactual earnings of the later-enrollees are better approximated by the earnings of their non-enrollee replacements than by zero.

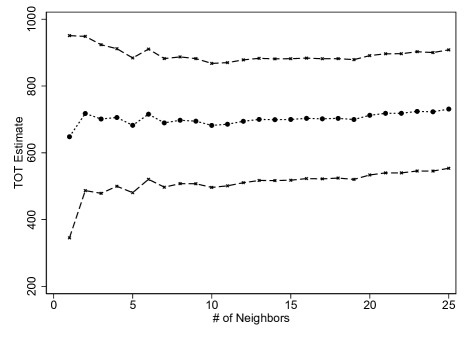

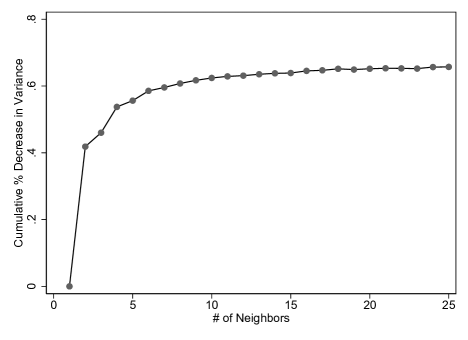

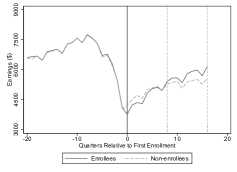

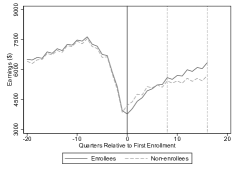

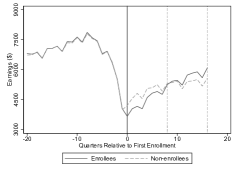

Because our lower bound is very close to the point estimate of the TOT effect, we refer to the lower bound simply as “the effect” in the remainder of this paper for brevity. Next, we conduct several sensitivity checks on our average effect estimates. While the set of non-enrollees in Figure 1 is selected by using 12 quarters of pre-layoff earnings in the propensity score formulation, Panels A and B of Appendix Figure A.3 show that earnings patterns are robust to alternative matching specifications that include fewer quarters of earnings (one pre-enrollment quarter and four pre-enrollment quarters, respectively). However, when we match without earnings between layoff and enrollment in Panel C, the patterns are quite different: the enrollees in this panel have much lower earnings than their matched comparison group heading into enrollment.191919The estimates of enrollment effects in the third and fourth year after enrollment are $378 (seven percent), $366 (seven percent), and -$219 (-4 percent) for Appendix Figure A.3 Panels A, B, and C, respectively. Appendix Figure A.3 highlights the importance of controlling for the most recent information just before enrollment. In contrast, including dummies for zero earnings (on top of the full set of quarterly earnings) in the propensity score model does not appear to affect estimates substantially—effects for the third and fourth year post-enrollment remains at six percent ($339 per quarter, Panel A of Appendix Figure A.4). We also probe the robustness of our results to dropping counties that border another state, as workers from these counties are more likely to be employed in another state post-layoff (which we would not be able to observe). We find that the omission of these counties also do not change our effect estimates much—in the third and fourth year post-enrollment, enrollees earn $324 more per quarter (six percent, Panel B of Appendix Figure A.4). In the last robustness check, we explore the sensitivity of our findings to using more neighbors. We show in Panel A of Appendix Figure A.5 the estimated treatment effect against the number of neighbors used.202020For this exercise, we only use the cell with the largest number of claims (male non-manufacturing workers laid off in the first quarter of 2009). We focus on this subsample to ease the significant computational burden of running the matching analysis 25 times with the full sample. The estimated treatment effect tends to shift upward as we increase the number of neighbors, and the variance is reduced by up to six percent as we show in Panel B of the same figure. An estimate using the full sample with five neighbors follows this general pattern, but since our sample size allows for precise estimates, we use the lowest bias one-neighbor specification.

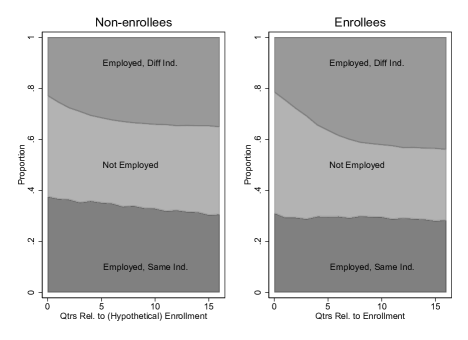

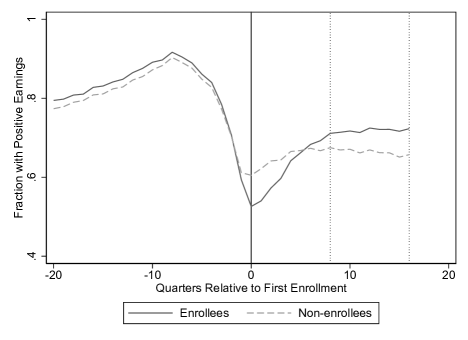

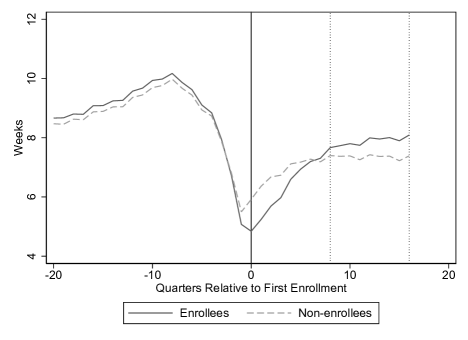

Finally, the two panels of Appendix Figure A.6 plot the probability of having positive earnings and weeks worked per quarter, respectively. Prior to enrollment, we see a similar pattern of a rise and drop in employment for both groups. After enrollment begins, enrollees are less likely to be employed initially but eventually overtake the comparison group at approximately the two-year mark. A natural question that arises is whether or not the gain in employment can explain all of the gains in earnings, or whether enrollment increases both employment and wage rates. One way to answer this question is to note that in Panel B of Appendix Figure A.6, non-enrollees work for 7.3 weeks and earn $5354 per quarter on average three to four years after enrollment, implying a weekly wage of approximately $730. Enrollees, on the other hand, are employed 7.9 weeks and have a weekly wage of approximately $722. Although the differences in weekly wage rates are not causal effects, this indicates that increased wage rates are not driving the enrollment effects.212121Since Appendix Figure A.6 shows a small gap in weeks worked between enrollees and non-enrollees in the pre-period, the weeks “effect” may be overstated. To see how this affects our conclusion, consider the following decomposition of the earnings effect: where Earnings and Weeks are average quarterly earnings and average weeks worked in a quarter, respectively, for enrollees () and non-enrollees (), and denotes the difference between enrollees and non-enrollees. If we adjust the weeks “effect” downward by 0.22 weeks (the gap in the pre-period), the first term of this decomposition still accounts for 70 percent of the total earnings effect. Another way to see this is to examine the earnings distributions of enrollees and matched non-enrollees, shown in Appendix Figure A.7. While the top panels of the figure document similar earnings distributions before enrollment, the bottom panels show that the distributions start to diverge eight quarters after enrollment and further widens at the end of quarter 16, where the gains are concentrated at the extensive margin. Therefore, we conclude training mainly affects employment and likely has minimal effect on wage rates four years after enrolling.

5.2 Effects By Subgroup

We now present the enrollment effects by subgroup. For subgroups that have exactly matched participants (i.e., enrollment timing, layoff quarter, gender, and sector), we estimate the enrollment effect by restricting to enrollees within the subgroup and examine the difference in outcomes compared to their matched non-enrollees. For subgroups that are not exactly matched (age, tenure, and race groups), we first restrict the analysis sample to the subgroup and then re-match enrollees to non-enrollees using the estimated propensity score described in Section 4.3.222222We cannot simply compare enrollees within a certain subgroup to their original matched comparison groups because this compares the outcomes of enrollees within a subgroup to non-enrollees that are potentially not in the subgroup. A simple way to see this is to consider a randomized experiment: if a population is randomly assigned to a treatment or control group with a coin flip, the propensity to be treated is 50 percent for the entire population. If we wanted to estimate the treatment effect for women only, we cannot simply compare the outcomes of treated women with the entire control population, even though their propensity scores are the same at 0.5. That is, we do not implement another matching procedure with re-estimated propensity scores conditional on the subgroup, which is computationally expensive and could bring in workers not included in the set of matched non-enrollees in Section 5.1, resulting in inconsistencies across samples.

A potential challenge is that the nearest neighbor for an enrollee in the subgroup analysis may differ from that in the full sample analysis and may be a worse match. But as we show in Appendix Table A.2, our method still achieves balance in most of the 28 subgroups, as measured by estimates of TOT on earnings one to two years and three to four years pre-enrollment, respectively. After adjusting for multiple hypotheses testing with the Holm method, pre-enrollment earnings from three subgroups (workers under 40, workers with job tenures greater than six years, and Black workers) remain statistically unbalanced at the 5 percent level.232323Note that, because the nearest neighbor may change from the full sample to a particular subgroup, balance in the full sample and one subgroup does not imply balance in the complement of that subgroup. But even for these three groups, the imbalance goes away in the most recent year immediately preceding enrollment as seen in Appendix Figures A.12, A.13, and A.14. This is reassuring as the most recent pre-enrollment earnings are possibly most predictive of future potential outcomes. To alleviate any remaining concerns with this imbalance, which manifests in seemingly parallel trajectories between enrollee and matched non-enrollees before earnings start to decline, we also report estimates using difference-in-differences matching in Table 3. These estimates are obtained by first differencing future earnings with (symmetrically timed) pre-enrollment earnings within person, and then comparing the resulting differences between enrollees and matched non-enrollees.242424The differencing step does not materially affect estimates. This is consistent with ChabeFerret2017, who finds that when conditioning on many periods of pre-treatment earnings as we do here, the bias of matching with or without differencing is similar. The reported standard errors in Table 3 are from testing whether the average pairwise difference between enrollees and matched non-enrollees is different from zero, and we abstract away from the sampling variation in forming these matched pairs. This abstraction is inconsequential for the full sample where we also have available the standard errors that account for the sampling variation in forming matched pairs per Abadie_Imbens2016: compared with their counterparts in Table 3, the two standard errors in columns (1) and (6) of the first row in Table 3 are only slightly larger.

For each of these subgroups, the effects may vary due to differences in “types” and intensity of schooling (e.g., types of courses taken, duration of enrollment, and whether a credential was obtained), differences in enrollee composition, or other factors such as labor market conditions. While we cannot tease out the exact reasons for why we find different effects for some subgroups, we discuss in turn likely explanations.

By Enrollment Timing

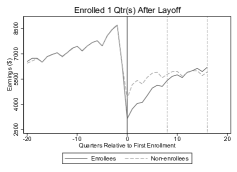

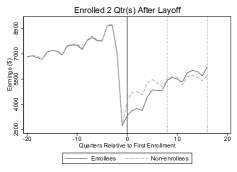

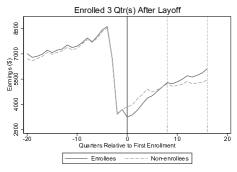

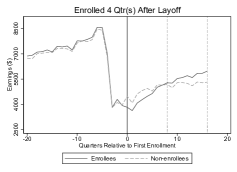

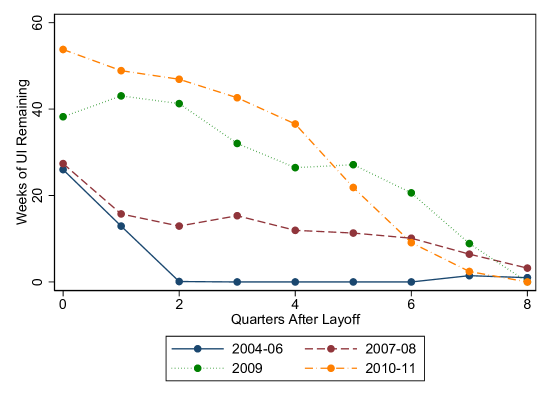

As discussed in Section 3, workers typically do not enroll immediately after layoff, and some take longer to go back to school than others. In Appendix Figure A.8, we show the impacts of enrollment by the quarter in which workers go back to school within two years after layoff. Examining the pre-enrollment period, we see a sharp drop in earnings that is similar across all eight panels, each corresponding to enrolling in a certain quarter (one through eight) since job loss. By comparing the matched non-enrollees’ earnings trajectories in each graph, it is clear that the groups differ in the extent to which their earnings recover post-enrollment, with larger earnings gains for those who enroll later relative to layoff. As reported in Table 3, we find that workers who enroll later have a smaller “lock-in” effect in the first two years after enrolling, and larger gains from enrollment (up to 12 percent) in the third and fourth years.

There are several potential explanations for these patterns. First, it is possible that the larger lock-in effects are due to a higher “treatment dosage” for those who enroll earlier. Consistent with the lock-in effects, those who enroll one quarter after layoff have a mean enrollment duration of 4.7 quarters, while those who enroll eight quarters after layoff are only enrolled on average for 4.2 quarters (and the pattern is monotonic for those who enroll in the second through seventh quarters). It is also true that these longer durations of enrollment correspond to higher rates of credential receipt: For those who enroll within the first quarter post-layoff, about 27 percent receive a credential, while for those who enroll in the eighth quarter after layoff, the credentialing rate is about 20 percent (the pattern is roughly monotonic in between, though it peaks for those who enroll in the second quarter). However, we also see that earlier enrollees have lower post-enrollment gains, which seems inconsistent with the fact that they have more “intensive” schooling (though it is possible that we simply have not looked at a long-enough post-period to observe the full gains).