∎

xt990221@stu.xjtu.edu.cn 33institutetext: Jia Liu, 44institutetext: School of Mathematics and Statistics, Xi’an Jiaotong University, Xi’an, 710049, P. R. China

jialiu@xjtu.edu.cn 55institutetext: Zhiping Chen 66institutetext: School of Mathematics and Statistics, Xi’an Jiaotong University, Xi’an, 710049, P. R. China

zchen@mail.xjtu.edu.cn

A dynamical neural network approach for distributionally robust chance constrained Markov decision process

Abstract

In this paper, we study the distributionally robust joint chance constrained Markov decision process. Utilizing the logarithmic transformation technique, we derive its deterministic reformulation with bi-convex terms under the moment-based uncertainty set.To cope with the non-convexity and improve the robustness of the solution, we propose a dynamical neural network approach to solve the reformulated optimization problem. Numerical results on a machine replacement problem demonstrate the efficiency of the proposed dynamical neural network approach when compared with the sequential convex approximation approach.

Keywords:

Markov decision process, Chance constraints, Distributionally robust optimization, Moment-based ambiguity set, Dynamical neural network1 Introduction

Markov decision process (MDP) is an important mathematical framework used to find an optimal dynamic policy in an uncertain environment. The randomness in an MDP often comes from two perspectives: reward varagapriya2022constrained and transition probabilities mannor2016robust ; ramani2022robust . MDPs have been widely used in various fields, including autonomous driving brechtel2014probabilistic , portfolio selection liu2023continual , inventory control klabjan2013robust , power systems wang2020mdp and so on.

For many applications with strong safety requirements (healthcare goyal2022robust , autonomous vehicles you2019advanced etc), one needs to adopt the MDP model with safe constraints. Many variations of constrained MDP have been extensively investigated, for instance, robust constrained MDP delage2010percentile , risk constrained MDP with semi-variance yu2022zero , Value-at-Risk ma2019state , or Conditional Value-at-Risk prashanth2014policy , etc.

As a typical extension, chance constraints are used in MDPs to ensure a high probability of constraints being satisfied. They are important in situations with high safety requirements where the violation of a random constraint might bring severe outcome kuccukyavuz2022chance . Delage and Mannor delage2010percentile studied reformulations of chance constrained MDP (CCMDP) with random rewards or transition probabilities. Recently Varagapriya et al. varagapriya2022joint applied joint chance constraints in constrained MDP and find its reformulations when the rewards follow an elliptical distribution.

However, in many real-world applications of chance constrained MDP, the true probability distribution of rewards or the transition probability is unknown. The decision-maker may only know partial information of the true distribution. It might lead to sub-optimal decisions or even failures of the decision-making system if the estimated distribution biased the true distribution. The distributionally robust optimization (DRO) approach handles such ambiguity by making decisions against to the worst-case distribution in a set of all possible distributions, namely ambiguity set, rather than a single estimated distribution. There are two major types of ambiguity sets: the moments-based ones and the distance-based ones. In moments-based DRO wiesemann2014distributionally ; delage2010distributionally ; rahimian2019distributionally , the decision-maker knows some moments information of the random parameters. In distance-based DRO hu2013kullback ; gao2022distributionally ; xie2021distributionally , the decision-maker has a reference distribution and consider a ball centered at it with respect to a probability metric (say, Kullback-Leibler divergence, Wasserstein distance and so on), given that she/he believes that the true distribution of random parameters is close to the reference distribution. Applying the DRO approach to chance constrained MDP, we have the distributionally robust chance constrained MDP (DRCCMDP) problem. As far as we know, only Nguyen et al. nguyen2022distributionally studied the individual case of DRCCMDP with moments-based, -divergence based and Wasserstein distance based ambiguity sets, respectively. However, the joint case of DRCCMDP has not been studied, which has important applications to guarantee the satisfaction of a complex system with multiple safety constraints in terms of a joint chance constraint.

Different optimization techniques have been widely used to find the optimal policy of an MDP problem, such as interior-point methods wright1997primal , simplex method nelder1965simplex . In practice, many solvers like GUROBI, MOSEK, CVX can be used to solve the resulting optimization problem directly. For instance, Delage and Mannor delage2010percentile transformed the chance constrained MDP into a second-order cone programming (SOCP) and used a gradient descent algorithm to solve the SOCP to find the optimal policy. Varagapriya et al. varagapriya2022constrained reformulated three kinds of constrained MDP problems into the linear programming (LP), SOCP and semi-definite programming (SDP), respectively, and solve them by CVX. Nguyen et al. nguyen2022distributionally transformed the individual DRCCMDP into an SOCP or a mixed-integer SOCP when the ambiguity sets are moment-based, K-L divergence based or Wasserstein distance based, respectively. However, as for the joint DRCCMDP, it cannot directly be solved by an optimization solver due to the non-convexity of the joint chance constraint. And when the transformed optimization problem is large scale, the common optimization algorithms cannot find an accurate enough solution in a reasonable time. Therefore we choose dynamical neural network (DNN) as our solving approach to the joint DRCCMDP.

In this paper, we propose a dynamical neural network (DNN) approach to solve the joint DRCCMDP. The DNN approach is a typical AI based technique that has been employed to solve optimization problems. Using DNNs to solve optimization problems was initiated by Hopfield and Tank hopfield1985neural . Since then, the DNN approach has been extensively applied to solve different optimization problems, such as linear programming (LP) wang1993analysis ; xia1996new , second-order cone programming (SOCP) ko2011recurrent ; nazemi2020new , quadratic programming xia1996new1 ; nazemi2014neural ; feizi2021solving , nonlinear programming forti2004generalized ; wu1996high , minimax problems nazemi2011dynamical ; gao2004neural , stochastic game problems wu2022dynamical , and geometric programming problems tassouli2023neural , etc. All of the work mentioned above adopts an ODE system to model the optimization problem, and then the optimal solution is obtained by solving the ODE system. The ODE systems have been shown to have global convergence properties, meaning that the state solutions converge to the optimal solution of the original optimization problem as the independent variable comes to infinity. In fact, Dissanayake et al. dissanayake1994neural were the first to use a neural network to approximate the solution of differential equations, where the loss function contains two terms that satisfy the initial/boundary condition and the differential equation, respectively. Lagaris et al. lagaris1998artificial developed a trial solution method that ensures initial conditions are always satisfied. Flamant et al. flamant2020solving treat the parameters of ODE system models as an input variable to the neural network, allowing a neural network to be the solution of multiple differential equations, namely solution bundles. Neural networks nowadays have a large number of applications in computer vision, natural language processing, pattern recognition, and other fields dong2023adversarial ; amiri2023novel . It is certain that with the help of studies of ODE, the performance of DNNs, which transform the optimization problem into an ODE, can be continuously improved in the future. To the best of our knowledge, there is no study in the literature that uses a DNN approach to solve CCMDP problems.

After deriving a non-convex reformulation of the moment-based joint DRCCMDP problem, we apply the DNN approach to solve the obtained reformulation. As a comparison, we also apply the sequential convex approximation (SCA) algorithm hong2011sequential ; liu2016stochastic to solve the joint DRCCMDP problem, which decomposes the non-convex reformulation problem into a series of convex sub-problems. The main contributions of this paper can be summarized as follows:

-

•

For the first time, we study the joint DRCCMDP under a moments-based uncertainty set.

-

•

To the best of our knowledge, this is the first attempt to apply the dynamic neural network approach to solve the CCMDP problem.

-

•

Numerical experiments validate the pros and cons of the dynamical neural network approach compared to the traditional sequential convex approximation approach.

The structure of this paper is as follows. In Section 2, we introduce the DRCCMDP model. In Section 3, we study the reformulation of the moments-based joint DRCCMDP. In Section 4, we apply the dynamical neural network approach to solve the moments-based joint DRCCMDP problem. We transform the reformulated optimization problem into an equivalent ordinary differential equation (ODE) system, and then solve it using a neural network way. In Section 5, we apply the proposed DNN approach to a machine replacement problem and compare it with the SCA algorithm. In the last section, we conclude the paper.

2 Distributionally robust chance constrained MDP

2.1 MDP

We consider an infinite horizon Markov decision process (MDP) as a tuple where:

-

is a finite state space with states whose generic element is denoted by .

-

is a finite action space with actions and denotes an action belonging to the set of actions at state

-

is the distribution of transition probability which denotes the probability of moving from state to when the action is taken.

-

denotes a running reward, which is the reward at the state when the action is taken. is the running reward vector.

-

is the probability of the initial state .

-

is the discount factor which satisfies

In an MDP, the agent aims at maximizing her/his cumulative value with respect to the whole trajectory by choosing an optimal policy. We know from sutton1999policy that there are two ways of formulating the agent’s objective function. One is the average reward formulation and the other is considering a discount factor We assume that the agent cares more about current rewards than future rewards, and thus consider the discounting value function in this paper.

We consider a discrete time controlled Markov chain defined on the state space and the action space , where and are the state and action at time , respectively. At the initial time the initial state is and the action is taken according to the initial state’s probability Then the agent gains a reward based on the current state and action. When the state moves to with the transition probability The dynamics of the MDP repeat at state and continue in the following infinite time horizon.

We assume that running rewards and transition probabilities are stationary, i.e., they both only depend on states and actions rather than on time. We define the policy where denotes the probability that the action is taken at state , and , the whole historical trajectory by time Sometimes the decisions made by the agent may vary at different time accordingly, thus the policy may vary depending on time. We call this kind of policy the history dependent policy, denoted as When the policy is independent of time, we call it a stationary policy. That is, there exists a vector such that for all Let and be the sets of all possible history dependent policies and stationary policies, respectively. When the reward is random, for a fixed we consider the discounted expected value function

| (1) |

where is the given discount factor. The object of the agent is to maximize the discounted expected value function

| (2) |

We denote by the -discounted occupation measure altman1999constrained such that

As the state and action spaces are both finite, by Theorem 3.1 in altman1999constrained , the occupation measure is a well-defined probability distribution. By taking the occupation measure into (1), the discounted expected value function can be written as

where .

It is known from Theorem 3.2 in altman1999constrained that the set of occupation measures corresponding to history dependent policies is equal to that corresponding to stationary ones. We thus have:

Lemma 1 (varagapriya2022constrained ; altman1999constrained )

The set of occupation measures corresponding to history dependent policies is equal to the set

| (3) |

where is the Kronecker delta, such that the expected discounted value function defined by (2) remains invariant to time .

With Lemma 1, the MDP problem (2) with history dependent policies is equivalent to the following optimization problem:

| (4a) | |||||

| (4b) | |||||

Remark 1

In a constrained MDP (CMDP), on the basis of the MDP defined above, we consider both running objective rewards in the objective function (denoted by introduced pre-ahead) and some running constraint rewards in some safe constraints. Let be the running constraint rewards and be the running constraint rewards vector. Let be the bounds for the constraints. A CMDP is defined by the tuple where

Considering the natural situation that more attention is paid on optimizing current rewards than future ones, we apply the discount factor in the expected constrained value function and define

| (5) |

to be the -th constrained expected value function. Combined with Lemma 1, the object of the agent in a CMDP can be written as the following optimization problem

| (6a) | |||||

| (6c) | |||||

2.2 Distributionally robust chance constrained MDP

In many applications, the reward vectors are random. It’s reasonable for us to consider the MDP with random rewards. We use the expected value of the objective rewards as the objective function. To ensure a high satisfaction probability of safe constraints, we use a chance constraint for the safe constraints in the CMDP. We denote such an MDP problem as the chance-constrained MDP (CCMDP).

Let denote the joint probability distribution of and denote the confidence level for the constraints. Then, the joint CCMDP (J-CCMDP) can be defined as the following optimization problem

| (7a) | |||||

| (7c) | |||||

on a tuple , where .

When the satisfactions of different constraints are considered separately, we obtain the following individual CCMDP,

| (8a) | |||||

| (8c) | |||||

where is the probability distribution of and is the confidence level of the th constraint.

If the distribution information of rewards are not perfectly known, we can apply the distributionally robust optimization approach to handle the ambiguity of or . Then we consider a distributionally robust chance constrained MDP (DRCCMDP). The joint DRCCMDP (J-DRCCMDP) can be defined as the tuple , where , is the ambiguity set for the unknown distribution and is the ambiguity set for the unknown joint distribution of . The resulting J-DRCCMDP can be formulated as

| (9a) | |||||

| (9c) | |||||

As a speical case, the individual DRCCMDP (I-DRCCMDP) can be written as the following optimization problem:

| (10a) | |||||

| (10c) | |||||

where is the ambiguity set for the distribution and is the confidence level of the th constraint.

3 moment based J-DRCCMDP

In this section, we consider the reformulation of the J-DRCCMDP problem when we only know information about the first two order moments of the joint distribution.

3.1 Reformulation of moment based J-DRCCMDP

We first consider the ambiguity of the marginal distribution. Applying the Mahalanobis distance, we define the ambiguity of the mean vector through an ellipsoid of size centered at for each . And we specify the covariance matrix of the reward vector lies in a positive semi-definite cone, which gives a one-side estimation on the covariance. In detail, we define

| (11) |

where , and for . Here, is the reference value of the expected value of , and is the reference value of the covariance between and , . We assume that is a positive semidefinite matrix, are two nonnegative parameters controlling the size of the uncertainty sets. means , where is the -dimensional positive semidefinite cone.

We assume that different rows in the joint chance constraint are independent of each other and consider the following ambiguity set for the joint distribution

| (12) |

where is the joint distribution for random vectors with marginals and are all defined in (11). Then we have the following proposition.

Proposition 1

Proof

Given the ambiguity set as defined in (11), we find that (9a) has the same structure as (7) in liu2022distributionally , so by Theorem 1 in liu2022distributionally , (9a) has the following equivalence

| (14) |

Given the ambiguity set defined in (12), a joint DRO chance constraint is equivalent to the product of DRO counterparts of individual marginal distributions shapiro2021lectures . This means that

By introducing the auxiliary variables , (9c) is equivalent to the following reformulation:

| (15a) | |||

| (15b) | |||

We can see that (15a) exhibits the same structure as the individual distributionally robust chance constrained geometric program with moments-based ambiguity set in liu2022distributionally . Then, by Theorem 1 in liu2022distributionally , (15a) has the following equivalent reformulation:

| (16) |

Combining with the reformulations (14), (15a), (15b) and (16) gives us (13).

Remark 2

By liu2016stochastic ; liu2022distributionally ; bartlett1946statistical , we know that the logarithmic transformation is a common method to convert a nonconvex optimization problem into a convex one. After introducing with the assumption that , we have a reformulation of (13)

| (17a) | |||||

| (17e) | |||||

where

| (18) |

It is worth mentioning that the optimization problem (17) is still nonconvex due to (17e), though (17a)-(17e) have a convex form. This can be illustrated as follows.

For any , and , we have

| (19a) | |||||

| (19b) | |||||

| (19c) | |||||

| (19d) | |||||

There exists some and such that , thus the set is nonconvex and the optimization problem (17) is a nonconvex one.

3.2 Sequential convex approximation algorithm for J-DRCCMDP

Like hong2011sequential and liu2016stochastic , we can use the sequential convex approximation approach to deal with the nonconvexity of (13). The basic idea of the sequential convex approximation consists in decomposing the original problem into subproblems where a subset of variables is fixed alternatively. For problem (13), we first fix and update by solving

| (20a) | |||||

| (20c) | |||||

and then we fix and update by solving

| (21a) | |||||

| (21d) | |||||

where and is a given searching direction for , . The detailed procedure of the sequential convex approximation algorithm for solving problem (13) is given in Algorithm 1.

Algorithm 1 can be seen as a specific relization of the alternate convex search or block-relaxation methods gorski2007biconvex . By Theorem 2 in liu2016stochastic , we know that Algorithm 1 converges in a finite number of iterations and the returned value is an upper bound of problem (13). When these sub-problems are all convex, the objective function is continuous, and the feasible set is closed, the alternate convex search algorithm converges monotonically to a partial optimal point (Theorem 4.7 gorski2007biconvex ). When the objective function is a differentiable and biconvex function, is a partial optimal point if and only if is a stationary point (Corollary 4.3 gorski2007biconvex ). As is positive semi-definite, is a convex function for any . Thus both problems (20) and (21) are convex programs and Algorithm 1 converges to a stationary point.

4 Dynamical neural network approach for J-DRCCMDP

Different from the current methodology, we consider in this section using the DNN approach to solve problem (13). We show that the equilibrium point of the DNN model corresponds to the KKT point of problem (13). Then we study the stability of the equilibrium point by analyzing the Lyapunov function. Figure 1 shows how we apply the DNN approach to solve the J-DRCCMDP problem.

Firstly, we apply the log-transformation to problem (13) and we get the following reformulation.

| (22a) | |||||

| (22e) | |||||

Lemma 2

The optimization problem (22) is a biconvex optimization problem with respect to and .

Proof

4.1 KKT conditions

Let , , , , , , and . We can then rewrite problem (22) as follows:

| (23a) | |||||

| (23g) | |||||

Definition 1

is called a partial optimum of problem (23) if and .

Lemma 3 (jiang2021partial )

In biconvex optimization problems, there always exists a partial optimal solution.

Now we derive the KKT conditions of problem (23). Let , if there exist , , , , , , and , such that

| (24a) | |||

| (24b) | |||

| (24c) | |||

| (24d) | |||

| (24e) | |||

| (24f) | |||

| (24g) | |||

| (24h) | |||

| (24i) | |||

then is called a partial KKT point of problem (23), where , , , , , and are the Lagrange multipliers associated with the constraints with respect to the two sub problems with fixed or respectively. Furthermore, we have the following lemma which gives the optimal KKT conditions of problem (23).

Lemma 4 (jiang2021partial )

4.2 Neural network model

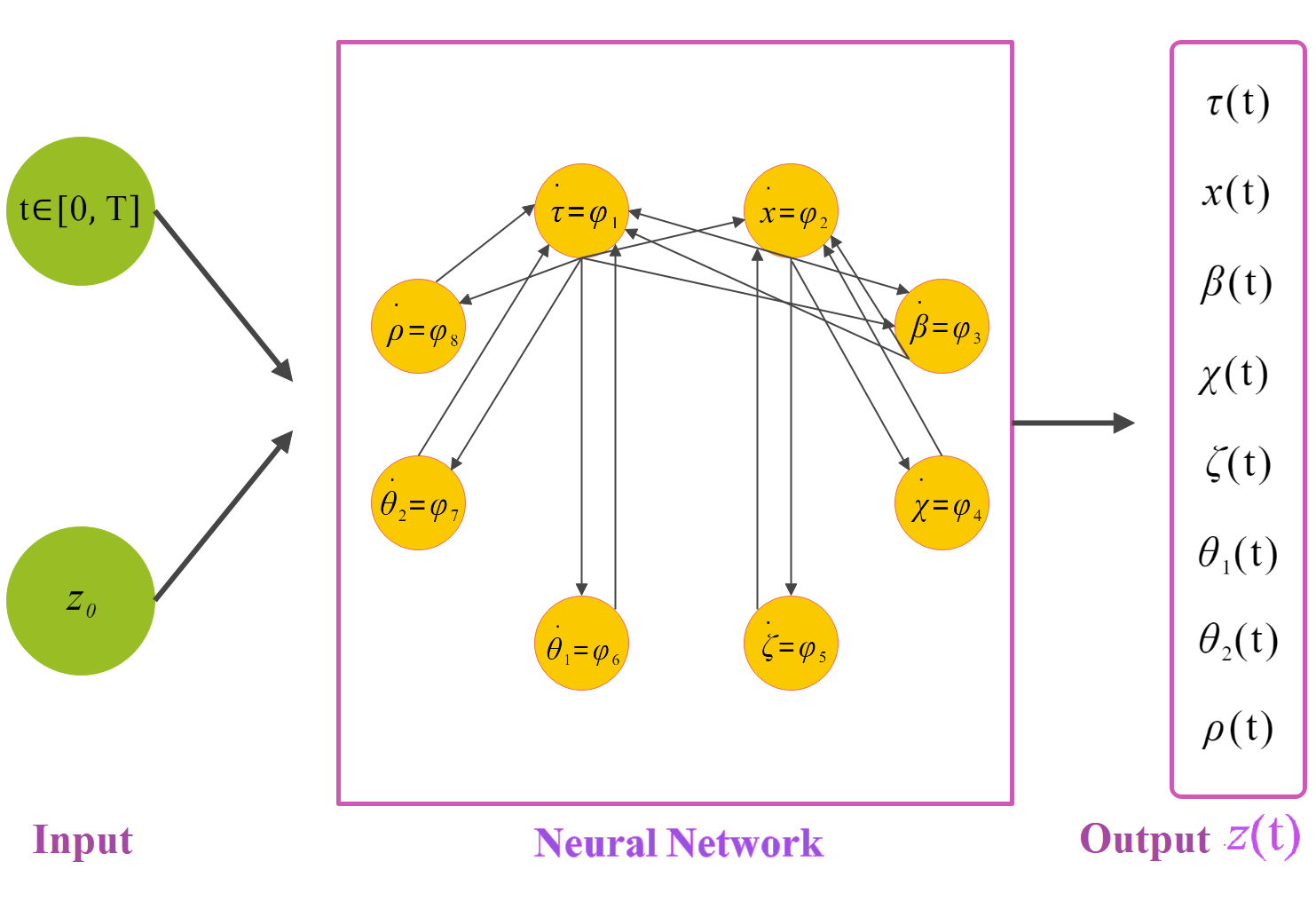

In this section, we introduce a DNN model to solve problem (23). Let and we define the dynamical equations of the DNN as

| (26) | ||||

Let , then the dynamical system can be written as

| (27) |

where

is a given initial point and is a scale parameter that indicates the convergence rate of the DNN model (26). For the sake of simplicity, we set . Figure 2 shows the structure of our proposed DNN model, where the frame in the middle illustrates the cyclic structure of the neural network. For example, the arrow from to means that the in-process solution which is generated by will be used to update by . These arrows among eight differential equations constitute the cyclic structure of the neural network.

Theorem 4.1

Proof

Let be an equilibrium point of the neural network (26), then . Thus we have

Notice that if and only if and . Following the same way, we have , , , , , , , , , , which implicates (26). Thus we obtain the partial KKT system (24) with =. By Lemma 4, is the KKT point. The converse conclusion is straightforward.

Theorem 4.2

For any initial point , there exists a unique continuous solution for (26).

Proof

As are all continuously differentiable, then all terms of (26) are locally Lipschitz continuous. Therefore is locally Lipschitz continuous with respect to . For any given closed interval , by the local existence theorem of ODE (Picard–Lindelöf Theorem hu2005theory ), the neural network (26) has a unique continuous solution when . As for any bounded closed interval, is bounded. Then we know from the continuation theorem hu2005theory that the unique continuous solution in can be extended to interval , which completes this proof.

4.3 Stability analysis

In this section, we study the stability of the proposed DNN model. To prove our DNN model’s stability and convergence, we first show that the Jacobian matrix is negative semidefinite.

Lemma 5

The Jacobian matrix is a negative semidefinite matrix.

Proof

For any , we assume that there exist index sets such that

Then we have , , and . For the sake of simplicity, we define , , , , , , and . Without loss of generality, we consider the case with . We represent the Jacobian matrix as follows

| (28) |

where

where if , if , if , if and all other elements in are equal to .

Since is twice differentiable, by Schwarz’s theorem, we have . Then we get , so becomes

| (29) |

It is clear that are negative semidefinite. Thus

is negative semidefinite.

Since the function is convex and twice differentiable, is positive semidefinite. Furthermore, is biconvex, are convex and are all twice differentiable. Thus by gorski2007biconvex , we have that , , , , are all positive semidefinite. It follows that are negative semidefinite and then is negative semidefinite.

Let , then can be written as . Since are both negative semidefinite, it is then known from foias1990positive that is negative semidefinite. This establishes the desired result. The proof when or follows similar lines.

Before showing the stability of the DNN model, we introduce the following definition and lemma.

Definition 2 (rockafellar2009variational )

A mapping is said to be monotonic if

Lemma 6 (rockafellar2009variational )

A differentiable mapping is monotonic if and only if the Jacobian matrix is positive semidefinite.

Theorem 4.3

Proof

Let be an equilibrium point of (26). We define the following Lyapunov function:

We have that

Since by (27), we have and thus

By Lemma 5, is negative semidefinite, then we have , . By Theorem 4.1, the equilibrium point satisfies . Then by Lemma 5 and Lemma 6, is monotonic. Therefore, we have . This means that . Therefore the DNN model (26) is stable at in the sense of Lyapunov.

Since , there exists a convergent subsequence such that . Let . By slotine1991applied , using LaSalle’s invariance principle, we have that any solution starting from a given converges to the largest invariant set contained in . Notice that

It follows that is an equilibrium point of (26).

Next we consider a new Lyapunov function defined by . Since is continuously differentiable, and , then we have . Furthermore, by , we have and . It can then be deduced that the DNN model (26) is convergent in the sense of Lyapunov to an equilibrium point where is a KKT point of (23). Then we finish the proof.

5 Numerical experiments

In Section 5.1, we give the setup for the numerical experiments. In Sections 5.2-5.5, we will carry out a series of numerical tests to compare the DNN approach and the SCA algorithm, including optimal policy results, convergence results, accuracy results and the generalization ability. In Section 5.6, we give a conclusion of the numerical experiments.

5.1 Experimental setup

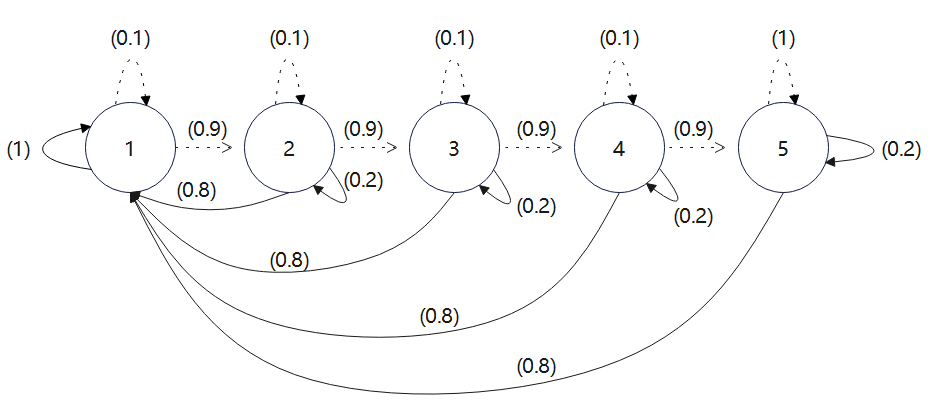

In order to evaluate the performance of our DNN approach, we consider the machine replacement problem, which was studied in delage2010percentile ; varagapriya2022constrained ; wiesemann2013robust ; goyal2022robust ; ramani2022robust . In the machine replacement problem, we consider an opportunity cost in the objective function along with two kinds of maintenance costs and in the constraint. The opportunity cost comes from the potential production losses when the machine is under repair. The maintenance cost comes from two parts: is the operational consumption of machines, such as the required electricity fee and fuel costs when the machine is working; is the cost occurred from production of inferior quality products. We set the states as the used age of a machine. At each state, there are two possible actions: is to repair and is not to repair. Three considered costs introduced above are incurred at each state. We assume that there are 5 states in all. The transition probabilities are given in Figure 3, where the solid lines denote the case when the decision maker chooses the action “repair” and the dashed lines denote the case when the decision maker chooses the action “do not repair”. The numbers along with the lines denote the transition probabilities. For example, at states - , if the repair action is taken, the machine moves to state 1 with probability 0.8 and stays in the current state with probability 0.2. At state , it stays in the state with probability 1 under the repair action. If the “do not repair” action is taken, the machine moves to the next state with probability 0.9 and stays in the current state with probability 0.1; whereas in the last state, it remains there with probability 1. For the above problem, we consider the corresponding moment-based J-DRCCMDP problem (22). The objective of the MDP is to maximize the discounted value function (minimizing the corresponding cost function), while keeping the two maintenance costs not exceeding the tolerance levels with a large probability.

For the MDP, we choose the discount factor and assume that the initial distribution is a uniform distribution. The mean values of the three costs are shown in Table 1. For example, at state 1, if the “repair” action is taken, the mean values of are , respectively; if the “do not repair” action is taken, the mean values of three costs are respectively. The last two states are risky states for which the mean values of costs are much larger. We assume that the reference covariance matrices of the three costs are diagonal and positive definite. Concretely, for both actions, the reference covariance matrix of are , and respectively. In our experiment, We set , , and .

| States | Maintenance cost | Operation consumption cost | Inferior quality cost | |||

|---|---|---|---|---|---|---|

| 1 | 1 | 0 | 1.5 | 8 | 0 | 5 |

| 2 | 1 | 0 | 1.5 | 8 | 0 | 5 |

| 3 | 1 | 0 | 1.5 | 8 | 0 | 8 |

| 4 | 4 | 30 | 5 | 100 | 1.5 | 30 |

| 5 | 4 | 70 | 5 | 200 | 3 | 50 |

All numerical experiments are run on a PC with AMD Ryzen 7 5800H CPU and 16.0 GB RAM. We use Python 3.11 as our programming language to implement our DNN model. We solve the ODE systems corresponding to the DNN model with solveivp from the scipy.integrate package. We notice that the complexity of solving the ODE system depends on the number of variables. In our test, the numbers of variables are respectively, and so 37 in total. We set the initial point as . For comparison, we also use the sequential convex approximation (SCA) algorithm (Algorithm 1) to solve the problem (22), where we set the initial points , , and . We conduct Algorithm 1 in MATLAB and solve the sub-optimization problems by the MOSEK solver. The detailed numerical results are shown in the following 4 parts from different perspectives.

5.2 Optimal policy

We solve the moment-based J-DRCCMDP problem (22) corresponding to the above machine replacement problem by using the DNN approach and SCA algorithm respectively, and especially derive the optimal solutions of problem (22). Then by Remark 1, we can compute the optimal policy of the machine replacement problem. For the DNN, we choose the optimal solution when . Table 2 shows the optimal policies at each state found by the two approaches. As there are only two actions at each state, the sum of probabilities of the two actions is 1, thus we denote the probability of one action when the probability of the other action is very close to 0.

| State | 1 | 2 | 3 | 4 | 5 | |

| DNN | repair | 1.7576e-08 | 2.8942e-08 | |||

| do not repair | 3.2052e-08 | 4.4931e-07 | 2.7283e-07 | |||

| SCA | repair | 3.5698e-10 | 4.8275e-10 | |||

| do not repair | 2.1067e-11 | 2.2559e-10 | 5.0490e-10 | |||

From Table 2, we can see that the optimal policy for each state derived by two approaches are nearly the same. For two approaches, the probability of “repair” at last three states are all , which is consistent with the fact that the machine gets aging with the state moving forward.

5.3 Convergence quality

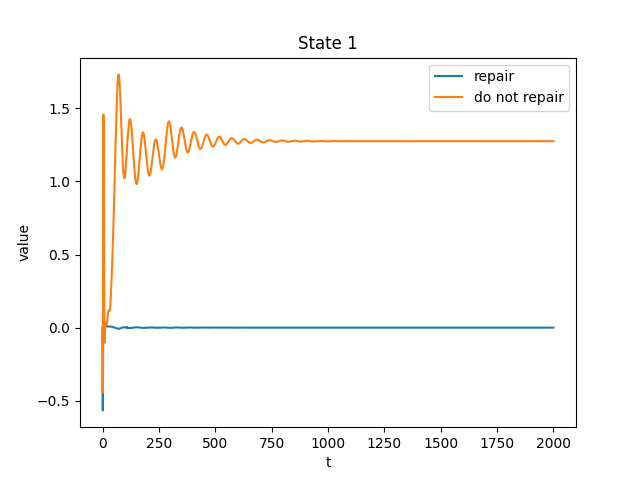

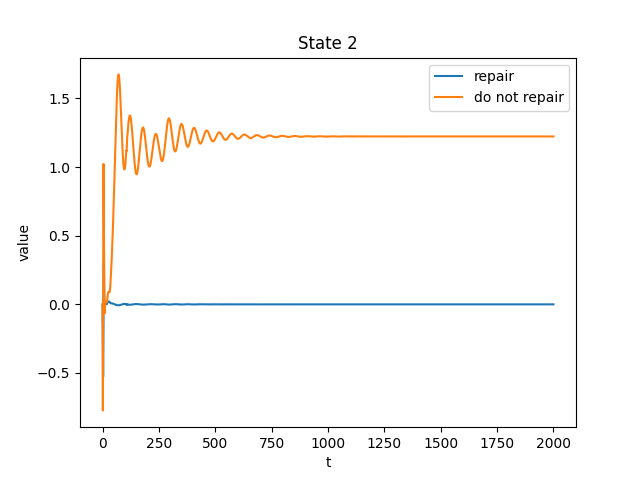

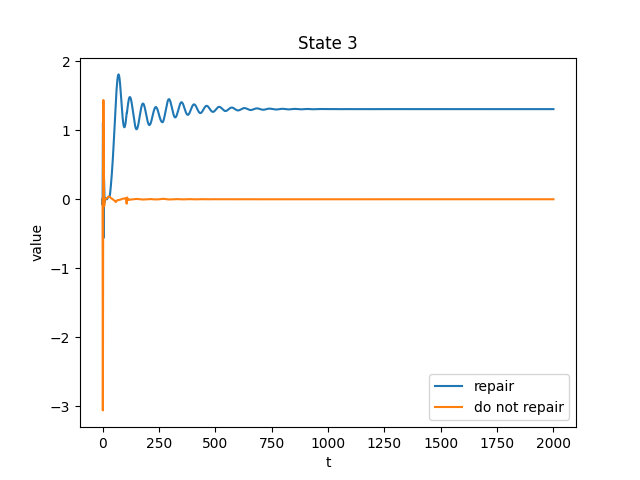

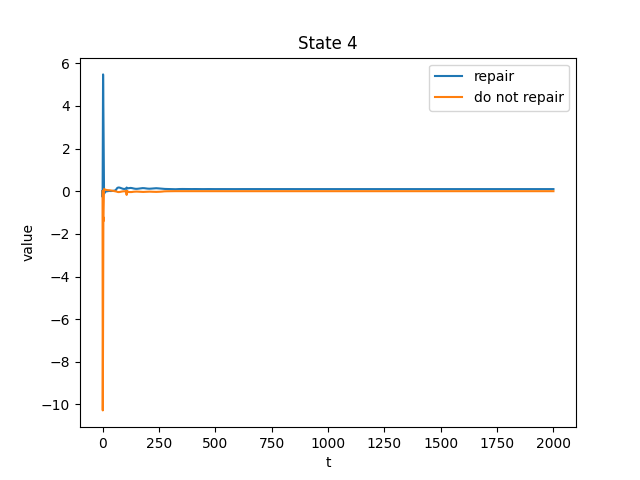

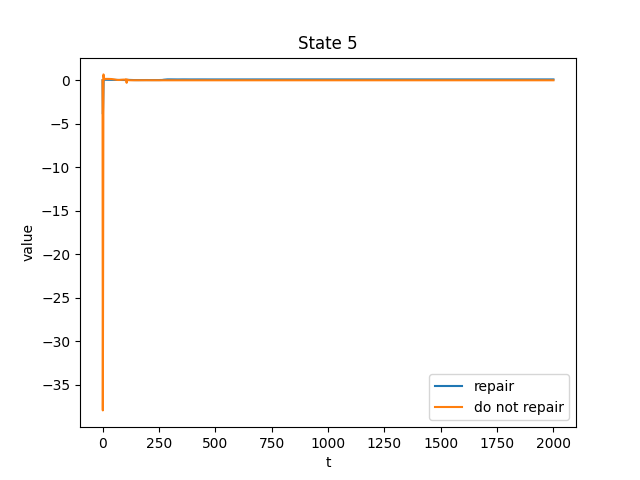

For the DNN model, we choose the interval of to observe the convergence performance. Figure 4 shows the values of optimal solutions at the five states. For instance, in (a), the blue curve denotes the value of and the orange curve denotes the value of , where correspond to the actions “repair” and “do not repair”, respectively. We see from these figures that the solution converges at each state.

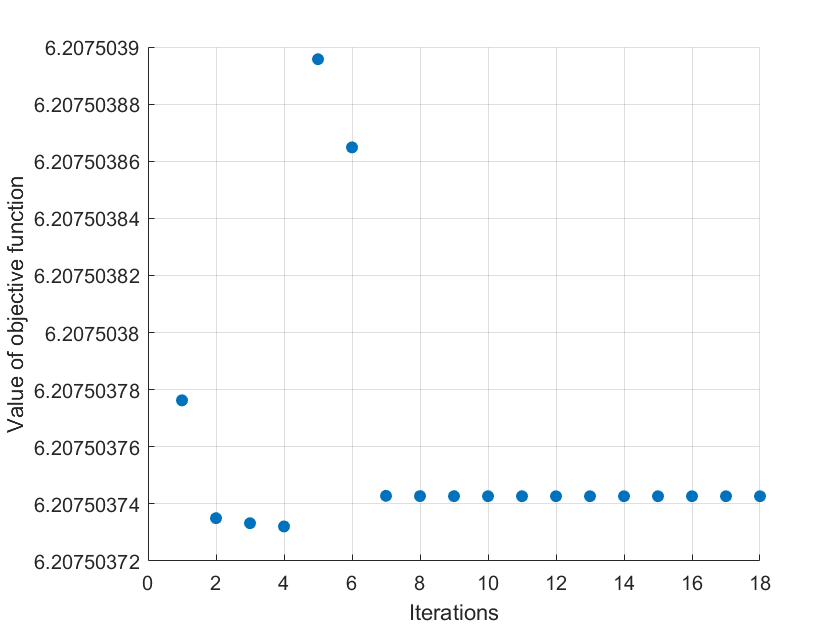

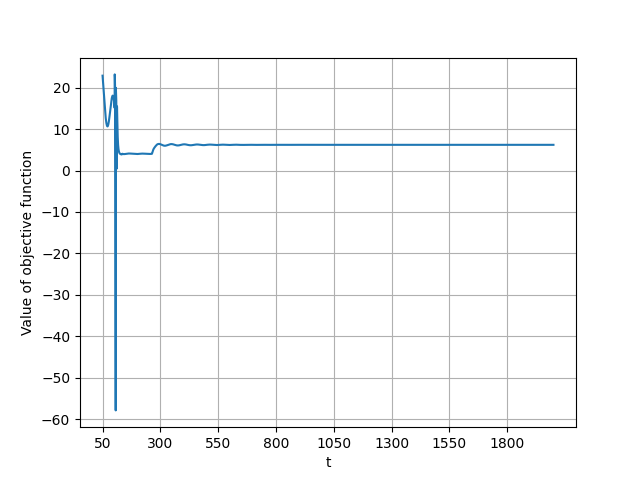

We also use the SCA algorithm to solve the problem (22). Figure 5 shows the value of optimal objective function of problem (22) at each iteration of the SCA algorithm. Figure 6 shows the value of optimal objective function of the DNN approach with in . When is between , the objective value varies intensely up to 7250 which is far from the convergence value, so we do not plot that part in the figure.

Comparing Figure 5 and Figure 6, we find that a key feature of the DNN approach is time-continuity, while the SCA algorithm is with finite steps. The time-continuity of the DNN approach provides more information about how the objective function move towards the optimal value. We also see that the convergence speed of two approaches are both fast. For the SCA algorithm, the objective function converges within a relative small bound at the 7th iteration. For the DNN approach, the objective function converges within a relative small bound when .

5.4 Accuracy of solutions

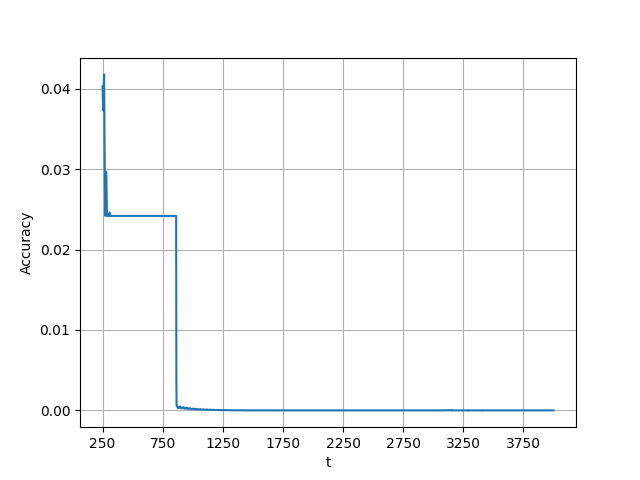

We know from Theorem 4.1 that the equilibrium point of the DNN model (26) is equivalent to the KKT point of (23). Thanks to the Lyapunov stability of (26) by Theorem 4.3, the solution of DNN is guaranteed to converge to the equilibrium point when . Based on the definition of the equilibrium point, the samller the value of where , the closer the solution of (26) to the equilibrium point. Thus we introduce the following measure to evaluate the accuracy of the solution of our DNN model.

Definition 3

The accuracy of a solution to the DNN model is the gap between the solution to the DNN model and the KKT point of (23). We can compute the accuracy by finding the minimal such that

Figure 7 shows the solution accuracy of the DNN model when solving the machine replacement problem in terms of Definition 3. For example, when , the accuracy . When , the accuracy value may reach nearly 90. Thus we only show the values in the interval to observe the final convergence.

It can be observed from Figure 7 that the accuracy could be extremely low when . However, for the SCA algorithm, we could not relate its accuracy of solutions with KKT conditions of the original problem. The only way to ensure its accuracy is to set a very low error bound in Algorithm 1 to force the solutions of two separated optimization problems as close as possible.

5.5 Generalization performance

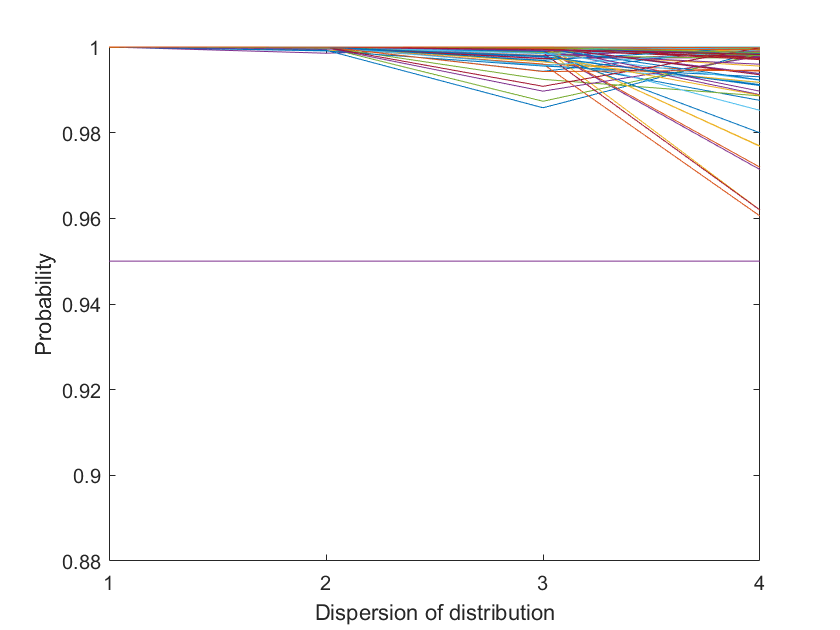

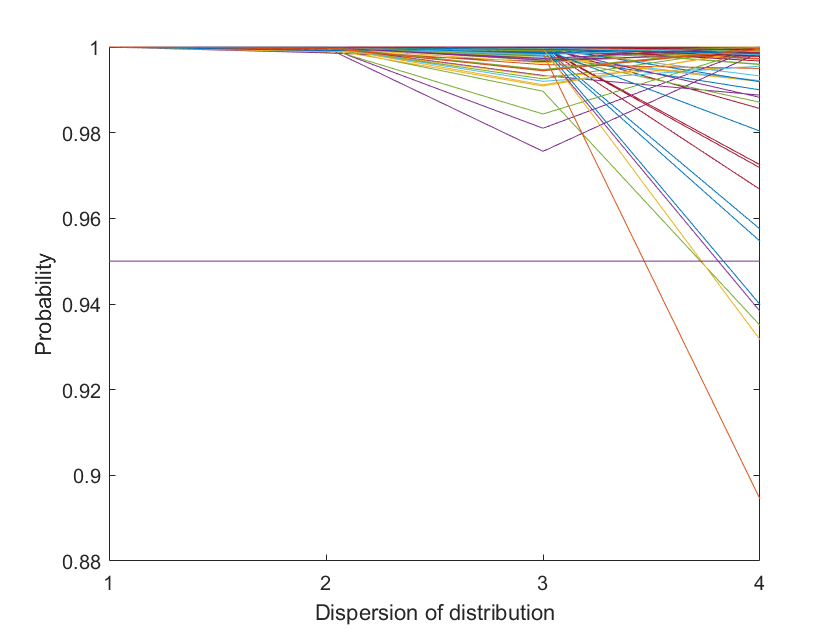

To evaluate the generalization ability of the two solution methods, we examine the out-of-sample performance of the optimal solutions under some randomly generated distributions. We assume that the reference distribution is a conservative estimation of the true distribution, and randomly generate the mean vector of the simulated distribution related to the center of the moments-based ambiguity set. We use the “rand” function in MATLAB to generate 4 groups of out-of-sample distributions, which represent different levels of dispersion. In each group, we randomly generate 100 Gaussian distributions. In particular, in the first group, the randomly generated Gaussian distributions are , , where , denotes the number of the reward vector and denotes the number of generation. In the second group, the randomly generated Gaussian distributions are , where . In the third group, the randomly generated Gaussian distributions are , where . In the forth group, the randomly generated Gaussian distributions are , where .

With the above setting, we use 100 randomly generated distributions in each group and the optimal solutions obtained by the DNN approach and the SCA algorithm to compute the satisfaction probability

where is the standard Gaussian cumulative distribution function. The concrete results are depicted in Figure 8.

It can be found from Figure 8 that there are 5 out-of-sample distributions in the forth test group, under which the solution found by SCA algorithm fails to guarantee the satisfaction of the chance constraint, while the solution obtained by DNN approach can guarantee the satisfaction in all of the 4 groups. Furthermore, comparing their out-of-sample performance, we can observe that the solution obtained by the DNN approach in complex situations, i.e., 100 randomly generated distributions, is more robust than that derived by the SCA algorithm.

5.6 Conclusion of numerical experiments

Based on a series of numerical experiments above, our conclusions of the DNN model in solving the moment-based J-DRCCMDP problem compared with the SCA algorithm are as follows.

Firstly, we can find by Table 2 that the numerical solutions of DNN approach and SCA algorithm are nearly the same in this problem, and they both consistent to the aging effect to the machine replacement. Secondly, through convergence results, we can see the objective values obtained by DNN approach change continuously. However the objective values obtained by SCA algorithm are dispersed, and we cannot capture the whole changing trend. Thirdly, with the Lyapunov stability in Theorem 4.3 and the equivalence between the equilibrium point and the KKT point in Theorem 4.1, the solutions obtained by DNN approach are surely converging to an equilibrium point which corresponds to a KKT point of the original optimization problem. Therefore we can depict the accuracy of DNN approach in correspondence to KKT conditions. While for the SCA algorithm, the level of accuracy cannot be reduced continuously w.r.t. KKT conditions. Lastly, in out-of-sample experiments, we compare the solutions obtained by two approaches. We find that the solution obtained by DNN approach in complex simulation environment performs more robustly than the solution obtained by SCA algorithm, which indicates that the generalization ability of solutions obtained by DNN approach are better than those obtained by SCA algorithm.

6 Conclusion

In this paper, we study the moment-based joint DRCCMDP and derive its deterministic reformulation. We propose a dynamical neural network approach to solve the resulting nonconvex optimization problem. In the numerical experiment, we examine the pros and cons of the DNN approach and the SCA algorithm in a machine replacement problem.

For the future research, using the DNN approach to solve the DRCCMDP with other kinds of ambiguity sets or studying the DRCCMDP with joint ambiguity on the distribution of rewards and the transition probabilities are promising topics.

Acknowledgements.

This research was supported by National Natural Science Foundation of China (No. 11991023 and 11901449) and National Key R&D Program of China (No. 2022YFA1004000)References

- (1) Varagapriya V, Singh V V, and Lisser A. Constrained markov decision processes with uncertain costs. Operations Research Letters, 50(2):218–223, 2022.

- (2) Mannor S, Mebel O, and Xu H. Robust mdps with k-rectangular uncertainty. Mathematics of Operations Research, 41(4):1484–1509, 2016.

- (3) Ramani S and Ghate A. Robust markov decision processes with data-driven, distance-based ambiguity sets. SIAM Journal on Optimization, 32(2):989–1017, 2022.

- (4) Brechtel S, Gindele T, and Dillmann R. Probabilistic decision-making under uncertainty for autonomous driving using continuous pomdps. In 17th international IEEE conference on intelligent transportation systems (ITSC), pages 392–399. IEEE, 2014.

- (5) Liu S, Wang B, Li H, and et al. Continual portfolio selection in dynamic environments via incremental reinforcement learning. International Journal of Machine Learning and Cybernetics, 14(1):269–279, 2023.

- (6) Klabjan D, Simchi-Levi D, and Song M. Robust stochastic lot-sizing by means of histograms. Production and Operations Management, 22(3):691–710, 2013.

- (7) Wang C, Lei S, Ju P, and et al. MDP-based distribution network reconfiguration with renewable distributed generation: Approximate dynamic programming approach. IEEE Transactions on Smart Grid, 11(4):3620–3631, 2020.

- (8) Goyal V and Grand-Clement J. Robust markov decision processes: Beyond rectangularity. Mathematics of Operations Research, 2022.

- (9) You C X, Lu J B, Filev D, and et al. Advanced planning for autonomous vehicles using reinforcement learning and deep inverse reinforcement learning. Robotics and Autonomous Systems, 114:1–18, 2019.

- (10) Delage E and Mannor S. Percentile optimization for markov decision processes with parameter uncertainty. Operations Research, 58(1):203–213, 2010.

- (11) Yu Z H, Guo X P, and Xia L. Zero-sum semi-markov games with state-action-dependent discount factors. Discrete Event Dynamic Systems, 32(4):545–571, 2022.

- (12) Ma S and Yu J Y. State-augmentation transformations for risk-sensitive reinforcement learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 4512–4519, 2019.

- (13) Prashanth L A. Policy gradients for CVaR-constrained MDPs. In International Conference on Algorithmic Learning Theory, pages 155–169. Springer, 2014.

- (14) Küçükyavuz S and Jiang R W. Chance-constrained optimization under limited distributional information: a review of reformulations based on sampling and distributional robustness. EURO Journal on Computational Optimization, page 100030, 2022.

- (15) Varagapriya V, Singh V V, and Lisser A. Joint chance-constrained markov decision processes. Annals of Operations Research, pages 1–23, 2022.

- (16) Wiesemann W, Kuhn D, and Sim M. Distributionally robust convex optimization. Operations Research, 62(6):1358–1376, 2014.

- (17) Delage E and Ye Y Y. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research, 58(3):595–612, 2010.

- (18) Hamed R M and Sanjay M. Distributionally robust optimization: A review. arXiv preprint arXiv:1908.05659, 2019.

- (19) Hu Z L and Hong L J. Kullback-leibler divergence constrained distributionally robust optimization. Available at Optimization Online, pages 1695–1724, 2013.

- (20) Gao R and Kleywegt A. Distributionally robust stochastic optimization with wasserstein distance. Mathematics of Operations Research, 2022.

- (21) Xie W J. On distributionally robust chance constrained programs with wasserstein distance. Mathematical Programming, 186(1):115–155, 2021.

- (22) Nguyen H N, Lisser A, and Singh V V. Distributionally robust chance-constrained markov decision processes. arXiv preprint arXiv:2212.08126, 2022.

- (23) Wright S J. Primal-dual Interior-Point Methods. SIAM, 1997.

- (24) Nelder J A and Mead R. A simplex method for function minimization. The computer journal, 7(4):308–313, 1965.

- (25) Hopfield J J and Tank D W. “Neural” computation of decisions in optimization problems. Biological cybernetics, 52(3):141–152, 1985.

- (26) Wang J. Analysis and design of a recurrent neural network for linear programming. IEEE Transactions on Circuits and Systems I: Fundamental Theory and Applications, 40(9):613–618, 1993.

- (27) Xia Y S. A new neural network for solving linear programming problems and its application. IEEE Transactions on Neural Networks, 7(2):525–529, 1996.

- (28) Ko C H, Chen J S, and Yang C Y. Recurrent neural networks for solving second-order cone programs. Neurocomputing, 74(17):3646–3653, 2011.

- (29) Nazemi A and Sabeghi A. A new neural network framework for solving convex second-order cone constrained variational inequality problems with an application in multi-finger robot hands. Journal of Experimental & Theoretical Artificial Intelligence, 32(2):181–203, 2020.

- (30) Xia Y S. A new neural network for solving linear and quadratic programming problems. IEEE transactions on neural networks, 7(6):1544–1548, 1996.

- (31) Nazemi A. A neural network model for solving convex quadratic programming problems with some applications. Engineering Applications of Artificial Intelligence, 32:54–62, 2014.

- (32) Feizi A, Nazemi A, and Rabiei M R. Solving the stochastic support vector regression with probabilistic constraints by a high-performance neural network model. Engineering with Computers, pages 1–16, 2021.

- (33) Forti M, Nistri P, and Quincampoix M. Generalized neural network for nonsmooth nonlinear programming problems. IEEE Transactions on Circuits and Systems I: Regular Papers, 51(9):1741–1754, 2004.

- (34) Wu X Y, Xia Y S, Li J M, and et al. A high-performance neural network for solving linear and quadratic programming problems. IEEE transactions on neural networks, 7(3):643–651, 1996.

- (35) Nazemi A. A dynamical model for solving degenerate quadratic minimax problems with constraints. Journal of Computational and Applied Mathematics, 236(6):1282–1295, 2011.

- (36) Gao X B, Liao L Z, and Xue W M. A neural network for a class of convex quadratic minimax problems with constraints. IEEE Transactions on Neural Networks, 15(3):622–628, 2004.

- (37) Wu D W and Lisser A. A dynamical neural network approach for solving stochastic two-player zero-sum games. Neural Networks, 152:140–149, 2022.

- (38) Tassouli S and Lisser A. A neural network approach to solve geometric programs with joint probabilistic constraints. Mathematics and Computers in Simulation, 205:765–777, 2023.

- (39) Dissanayake M and Phan-Thien N. Neural-network-based approximations for solving partial differential equations. Communications in Numerical Methods in Engineering, 10(3):195–201, 1994.

- (40) Lagaris I E, Likas A, and Fotiadis D. Artificial neural networks for solving ordinary and partial differential equations. IEEE transactions on neural networks, 9(5):987–1000, 1998.

- (41) Flamant C, Protopapas P, and Sondak D. Solving differential equations using neural network solution bundles. arXiv preprint arXiv:2006.14372, 2020.

- (42) Dong H Y, Dong J L, Yuan S, and et al. Adversarial attack and defense on natural language processing in deep learning: A survey and perspective. In International Conference on Machine Learning for Cyber Security, pages 409–424. Springer, 2023.

- (43) Amiri M, Jafari A H, Makkiabadi B, and et al. A novel un-supervised burst time dependent plasticity learning approach for biologically pattern recognition networks. Information Sciences, 622:1–15, 2023.

- (44) Hong L J, Yang Y, and Zhang L W. Sequential convex approximations to joint chance constrained programs: A monte carlo approach. Operations Research, 59(3):617–630, 2011.

- (45) Liu J, Lisser A, and Chen Z P. Stochastic geometric optimization with joint probabilistic constraints. Operations Research Letters, 44(5):687–691, 2016.

- (46) Sutton R S, McAllester D, Singh S, and et al. Policy gradient methods for reinforcement learning with function approximation. Advances in neural information processing systems, 12, 1999.

- (47) Altman E. Constrained Markov Decision Processes: Stochastic Modeling. Routledge, 1999.

- (48) Liu J, Lisser A, and Chen Z P. Distributionally robust chance constrained geometric optimization. Mathematics of Operations Research, 47(4):2950–2988, 2022.

- (49) Shapiro A, Dentcheva D, and Ruszczynski A. Lectures on stochastic programming: modeling and theory. SIAM, 2021.

- (50) Bartlett M S and Kendall D G. The statistical analysis of variance-heterogeneity and the logarithmic transformation. Supplement to the Journal of the Royal Statistical Society, 8(1):128–138, 1946.

- (51) Gorski J, Pfeuffer F, and Klamroth K. Biconvex sets and optimization with biconvex functions: a survey and extensions. Mathematical Methods of Operations Research, 66(3):373–407, 2007.

- (52) Jiang M, Meng Z Q, and Shen R. Partial exactness for the penalty function of biconvex programming. Entropy, 23(2):132, 2021.

- (53) Hu J S and Li W P. Theory of Ordinary Differential Equations. Existence, Uniqueness and Stability. Publications of Department of Mathematics. The Hong Kong University of Science and Technology, 2005.

- (54) Foias C and Frazho A E. Positive definite block matrices. In The Commutant Lifting Approach to Interpolation Problems, pages 547–586. Springer, 1990.

- (55) Rockafellar R T and Wets R J B. Variational Analysis, volume 317. Springer Science & Business Media, 2009.

- (56) Slotine J J E, Li W P, and et al. Applied Nonlinear Control, volume 199. Prentice hall Englewood Cliffs, NJ, 1991.

- (57) Wiesemann W, Kuhn D, and Rustem B. Robust markov decision processes. Mathematics of Operations Research, 38(1):153–183, 2013.