Bayesian Model Selection via Mean-Field Variational

Approximation

Abstract

This article considers Bayesian model selection via mean-field (MF) variational approximation. Towards this goal, we study the non-asymptotic properties of MF inference under the Bayesian framework that allows latent variables and model mis-specification. Concretely, we show a Bernstein von-Mises (BvM) theorem for the variational distribution from MF under possible model mis-specification, which implies the distributional convergence of MF variational approximation to a normal distribution centering at the maximal likelihood estimator (within the specified model). Motivated by the BvM theorem, we propose a model selection criterion using the evidence lower bound (ELBO), and demonstrate that the model selected by ELBO tends to asymptotically agree with the one selected by the commonly used Bayesian information criterion (BIC) as sample size tends to infinity. Comparing to BIC, ELBO tends to incur smaller approximation error to the log-marginal likelihood (a.k.a. model evidence) due to a better dimension dependence and full incorporation of the prior information. Moreover, we show the geometric convergence of the coordinate ascent variational inference (CAVI) algorithm under the parametric model framework, which provides a practical guidance on how many iterations one typically needs to run when approximating the ELBO. These findings demonstrate that variational inference is capable of providing a computationally efficient alternative to conventional approaches in tasks beyond obtaining point estimates, which is also empirically demonstrated by our extensive numerical experiments.

keywords:

Bayesian inference, Coordinate ascent, Mean-field inference, Oracle inequality.0em1.6em\thefootnotemark

1 Introduction

Variational inference (VI, Jordan et al., 1999; Bishop, 2006a) is an effective computational method for approximating complicated posterior distributions arising in Bayesian statistics. An alternative commonly adopted approach is the Markov Chain Monte Carlo (MCMC) method (Hastings, 1970; Gelfand and Smith, 1990; Hammersley, 2013) based on sampling, where a Markov chain is carefully constructed so that its limiting distribution matches the target distribution. Despite its popularity, MCMC is known to suffer from a number of drawbacks, including low sampling efficiency due to sample correlation and a lack of computational scalability to massive datasets. In comparison, VI turns the integration or sampling problem into an optimization problem, and can be orders of magnitude faster than MCMC for achieving the same approximation accuracy. More precisely, the target distribution in VI is approximated by a closest member in a family of tractable distributions via minimizing the Kullback-Leibler (KL) divergence, which is also equivalent to maximizing a lower bound to the logarithm of the marginal density of data, called evidence lower bound (ELBO). We refer the interested readers to Blei et al. (2017) for a comprehensive review on the history of VI development.

Among various approximating schemes, the mean-field (MF) approximation, which uses the approximating family consisting of all fully factorized density functions over (blocks of) the target random variables, is the most widely used and representative instance of VI that is conceptually simple yet practically powerful. The computation of MF approximation can be realized using the coordinate ascent variational inference (CAVI) algorithm (Bishop, 2006a; Blei et al., 2017), which iteratively optimizes each (block of) components in the factorization while keeping others fixed at their present values (see Section 2.4 for more details). CAVI resembles the classical EM algorithm (Dempster et al., 1977) by viewing the target random variables as the unobserved latent variables. In this paper, we primarily focus on MF approximation, although our development can be analogously extended to other approximation schemes, such as Gaussian approximation and hybrid schemes that further restrict components in MF to be within certain exponential families.

Despite the wide applications of variational inference over the past decades, it is until recent years that some general theory, trying to explain from a frequentist perspective why variational inference works so well, has been developed. Some earlier threads of theoretical research are mostly conducted in a case-by-case manner, by either explicitly analyzing the fixed point equation of the variational optimization problem, or directly analyzing the iterative algorithm for solving the optimization problem. Examples of such include Bayesian linear models (Hall et al., 2011a, b; Ormerod and Wand, 2012), Gaussian mixture models (Titterington and Wang, 2006; Westling and McCormick, 2015), and stochastic block models (Bickel et al., 2013; Zhang and Zhou, 2020). It is a well-known fact that many VI schemes, such as MF approximation, fail to capture the dependence structure and tend to underestimate the estimation uncertainty reflected in the Bayesian posteriors (Wang and Titterington, 2005). This observation is first theoretically illustrated by Wang and Blei (2019b), where under a local asymptotic normality (LAN) assumption, a Bernstein von-Mises type theorem (i.e. asymptotic normal approximation, Van der Vaart, 2000) is proven for the variational (approximated) posterior. However, the crucial LAN assumption used in Wang and Blei (2019b) implicitly assumes the estimation consistency for the model parameter, which still requires a case-by-case verification. In addition, it is not clear that how the asymptotic mean and covariance matrix implied by their LAN assumption relate to characteristics of the statistical model in a general sense. Wang and Blei (2019a) further generalize the results in Wang and Blei (2019b) from well-specified models to mis-specified models.

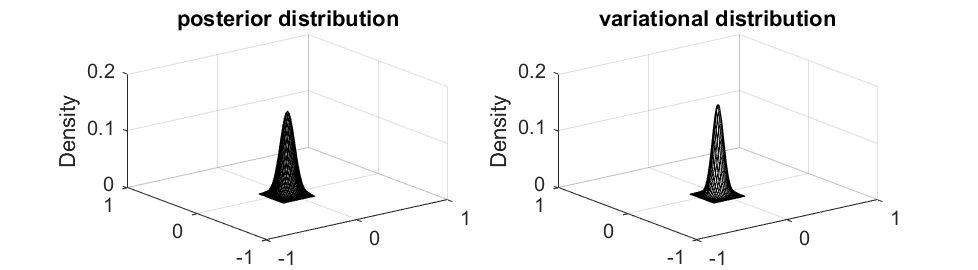

Since VI is generally incapable of accurately approximating the target posterior distributions, another line of research focuses on the estimation consistency of point estimators obtained from variational posteriors (e.g. using the expectation) under general settings. For example, a number of recent works (Alquier and Ridgway, 2020; Pati et al., 2018; Yang et al., 2020; Zhang and Gao, 2020) provide general conditions under which VI leads to consistent parameter estimation; moreover, they derive convergence rates of the point estimators that are often minimax-optimal (up to logarithmic terms) in both regular parametric and infinite-dimensional non-parametric models. In addition, some works (Alquier and Ridgway, 2020; Alquier et al., 2016; Chérief-Abdellatif and Alquier, 2018) derive risk bounds for VI under model mis-specifided settings; while Yang et al. (2020) also studies the risk bounds for VI with fractional posteriors. In a nutshell, this point estimation consistency (first order information) can be attributed to the heavy penalty on the tails in the KL divergence that forces the variational distribution to concentrate around the true parameter at the optimal rate; however, the local shape of the obtained variational posteriors around the true parameter (second order information) can be far away from that of the true posterior (see Fig. 1 for an illustration).

Through a more refined analysis, Han and Yang (2019) show that under some mildly stronger smoothness conditions without assuming consistency, the discrepancy between a point estimator from MF approximation and the maximum likelihood estimator (MLE) is of higher-order compared to the root- estimation error of MLE for regular parametric models. As a consequence, there is essentially no loss of efficiency in using a VI point estimator for parameter estimation, in terms of asymptotically attaining the Cramér-Rao lower bound. In addition, they show that MF variational posterior is close to a multivariate normal distribution centered at MLE with a diagonal precision matrix whose diagonal elements are equal to corresponding elements in the Fisher information at the true parameter. They further propose a consistent variational weighted likelihood bootstrap method for uncertainty quantification for the MF approximation.

The overarching goal of the current paper is to carry out further methodological and theoretical investigations complimenting existing findings by looking into the model selection and algorithmic convergence aspects of MF variational approximation. While there are some existing theoretical results on model selection with variational inference, they either show only an oracle inequality for the selected model (Chérief-Abdellatif, 2019), implying that the estimation performance of the selected model is not much worse than that of the true model, or use an additional aggregation step to combine multiple variational models to achieve an optimal convergence rate (Ohn and Lin, 2021). It remains an open problem to study whether the model selected based on ELBO maximization is consistent; that is, whether the probability of choosing the right model tends to one as sample size tends to infinity. In this paper, we propose ELBO as an alternative criterion for model selection, and show that it is asymptotically equivalent to the Bayesian information criterion (BIC, Schwarz et al., 1978). It is well-known (Yang, 2005) that BIC, derived as an asymptotic approximation to the log-marginal likelihood (a.k.a. model evidence), is consistent in selecting the true model; while another commonly used Akaike information criterion (AIC, Hirotugu, 1974), equivalent to Mallows’s statistic in regression analysis, is minimax-rate optimal for prediction but tends to over-estimate the model size. In this work, we find that ELBO generally leads to a better approximation to the model evidence than BIC due to the full incorporation of prior information and a better dimension dependence in the approximation error. On the other hand, our numerical studies suggest that the proposed ELBO criterion tends to be less conservative than BIC in the presence of weak signals, and can achieve comparable predictive performance as AIC with a much more parsimonious selected model. Furthermore, we study the algorithmic convergence of the CAVI algorithm under regular parametric models by providing generic conditions on the initialization and step size under which CAVI exhibits geometric convergence towards the exact value up to the statistical accuracy of the problem. Specifically, we characterize the algorithmic convergence rate under two commonly adopted updating schemes; and our result provides theoretic guidance on how many iterations one typically needs to run when approximating the ELBO for model selection, so that the numerically selected model coincides with the theoretical one.

The rest of the paper is organized as follows. In Section 2, we review some background on the mean-field variational inference, present some new theoretical results on the mis-specified Bernstein-von Mises theorem, and describe in details the methodology of using MF approximation for model selection and the related computational aspects. Section 3 contains the main theoretical findings of the paper. Section 4 includes the numerical results. We conclude the paper with a discussion in Section 5 and leave the description of motivating examples, their theoretical consequences, high-dimensional extensions and technical proofs to the Appendices.

Notation. We use lower-case letters (e.g. , , ,…) to denote densities, and capital letters (e.g. , , ,…) for the associated probability measures. We use to denote the KL-divergence between two distributions and , and for the Hellinger distance.

2 Model Selection via Mean-Field Approximation and its Computation

In this section, we first set up the modeling framework and review mean-field (MF) variational approximation for Bayesian inference; and then present some new theoretical results, including concentration and distributional convergence under possible model mis-specification. Motivated by the theory, we propose a new criterion based on the evidence lower bound (ELBO) as an alternative to the widely used BIC for model selection. After that, we introduce several common variants of coordinate ascent variational inference (CAVI) algorithms that implement MF for model selection. In Appendix A, we provide some concrete motivating examples and derive the closed form of updating formulas for computing ELBO.

2.1 Variational Inference and Mean-Field Approximation

Let denote i.i.d. random observations from some unknown underlying data generating distribution to be estimated. Consider a parametric family that does not necessarily contain (i.e., we allow model mis-specification). In a general Bayesian framework, the goal is to approximate the posterior density of parameter given data , which is obtained by combining a prior density and data likelihood ,

denoting the normalization constant. In many problems such as the Gaussian mixture modeling, model augmentation with latent variables can greatly simplify the likelihood function evaluation; thereby facilitating posterior calculation. For concreteness, we consider local latent variables where the th latent variable is tied with for . Under this setting, the marginal likelihood function of data can be recovered by integrating the conditional density function with respect to the latent variable distribution , i.e.

In the case where latent variables are of discrete type, we replace the integration above with a summation over . We consider the common setting where the observation-latent variable pairs are conditionally i.i.d. given , that is,

For such a latent variable model, one is typically interested in making inference using the following joint posterior density over parameter and latent variables ,

Unfortunately, in many problems the normalizing constant involving a multivariate integration is analytically intractable and difficult to numerically approximate. Variational inference (VI) instead searches for a closest distribution over from some computationally friendly variational family, denoted by , to approximate the joint posterior distribution by solving the following optimization problem,

| (1) |

The following equivalent description of the objective functional above leads to an alternative way to interpret VI,

| (2) | ||||

where is called evidence lower bound (ELBO) since it bounds the evidence from below, due to the non-positivity of KL divergence. The same identity also illustrates that VI circumvents the need of calculating the unknown normalizing constant since it only contributes to the objective functional as a constant that does not change the optimum.

According to identity (2), ELBO equals to the evidence (i.e. ) if and only if and coincide. As a direct consequence, the following two statistical tasks are equivalent: 1. approximating the joint posterior for conducting statistical inference on ; 2. approximating the evidence for evaluating model goodness of fit or performing model selection. Computationally, we can alternatively maximize the analytically tractable ELBO functional to find the best approximation to the joint posterior within variational family . In this way, we have turned the integration problem into an optimization problem. Although VI is not guaranteed to generate exact samples as MCMC does, the computational efficiency can be considerably improved, as some smart choices of the variational family make the optimization problem numerically solvable and simple. Moreover, the computational speed can be further boosted by taking advantage of modern optimization techniques such as stochastic approximation and distributed computing.

In practice, a popular choice of is the mean-field family that contains all fully factorized densities with the form for all and . As a representative illustrating example, the (closest) MF approximation to the multivariate normal distribution (with being the precision matrix) is , where denotes the diagonal matrix collecting all diagonal elements from a matrix . In other words, the MF approximation keeps all the first-order information, while throwing away second-order interactions encoding the dependence structure, as we have already seen from Fig. 1. A common variant relaxing the fully factorized MF approximation is the block MF approximation of the form , where the dependence within components of or is preserved while that between the two blocks and is neglected. For either the full or the block MF approximation, the corresponding optimization problem can be efficiently solved by a generic coordinate ascent (Wright, 2015), whose specializations to MF will be introduced with more details in Section 2.4.

To interpret and understand different sources of errors due to MF approximation , we may further decompose ELBO into the following three terms (Yang et al., 2020),

| (3) |

where the first term is an integrated marginal log-likelihood function (w.r.t. the variational density ), the second term is the negative KL-divergence between and the prior, and the last term

can be interpreted as a non-negative Jensen gap introduced by approximating the marginal log-likelihood with a lower bound from Jensen’s inequality. In particular, , which collects the first two terms in (3), constitutes the ELBO associated with the objective functional in the variational inference of approximating the (marginal) posterior with variational density ; while the extra gap is due to the presence of latent variables where is approximated by a single distribution for all .

Decomposition (3) also reveals an interesting connection between the optimization of ELBO and the traditional regularized estimation. For example, when there is no latent variable, the Jensen gap term vanishes; and maximizing the ELBO functional (3) over all density functions over becomes finding a KL-divergence-regularized estimator over : the first term in (3) reflects model goodness of fit to the data and encourages to assign all its mass towards the maximizer of log-likelihood function, i.e. the maximum likelihood estimator; while the second regularization term avoids measure collapse as it diverges to infinity as becomes close to a point mass measure.

2.2 Concentration and Distributional Convergence

This subsection presents results about large-sample properties of posterior distributions and their MF variational approximations in terms of concentration towards certain point in parameter space and convergence towards some distribution over , under the frequentist perspective assuming to be i.i.d. from the data generating distribution . These results are direct generalization of Han and Yang (2019) from well-specified parametric models to mis-specified models. They also provide the cornerstone for showing the consistency of model selection based on ELBO in Section 3.1.

For a well-specified model where for some true parameter in parameter space , it is known that the posterior distribution tends to contract towards in view of the BvM theorem (Van der Vaart, 2000). For posterior concentration beyond parametric models, refer to Shen and Wasserman (2001); Ghosal et al. (2000); Ghosal and Van Der Vaart (2007). However, in the context of model selection, we also need to consider candidate models that may not contain . Posterior contraction for mis-specified models is formally studied in Kleijn et al. (2012). More precisely, if we denote

| (4) |

as the parameter associated with the “projection” (relative to the KL divergence) of to a generic (possibly mis-specified) model with parameter space . The BvM theorem under mis-specification (Kleijn et al., 2012) states that the posterior distribution tends to be close to a normal distribution centering at MLE of the assumed model , whose covariance matrix is related as usual to the Fisher information matrix; and the MLE itself is asymptotically normal with asymptotic mean and a sandwiched-form covariance matrix. Since we will fix the model in the following analysis, we will omit the in the subscripts in the rest of this subsection. For example, will be simply denoted as , parameter space as , and prior density as .

To begin with, we make some common regularity assumptions on the prior and log-likelihood function following Han and Yang (2019), with some appropriate generalization to the mis-specified setting.

Assumption 1 (Thickness of prior)

The prior satisfies , and is continuously differentiable in a neighborhood of , with growth controlled as

for any and some positive constants .

Assumption 2 (Regularity of marginal likelihood)

Let be the log-likelihood function at a single data point , then:

-

1.

has continuous mixed derivatives up to order three with respect to components of , and the mixed derivatives have finite fourth moments in a neighborhood of under . Moreover, there exists a measurable function such that

and satisfies for some ;

-

2.

The information matrix is positive definite, and the covariance matrix of the score vector is invertible;

-

3.

The Radon-Nikodym derivative satisfies in a neighborhood of . Moreover, for any there exists a sequence of test functions such that

for some constants and .

Assumption 3 (Regularity of conditional likelihood of latent variable)

The conditional log-likelihood function of the latent variable has continuous mixed derivatives with respect to components of up to order three, and the mixed derivatives have finite fourth moments in a neighborhood of under . Moreover, there exists a measurable function with bounded second moment under such that

Assumptions 1, 2(a), 2(b), and 3 are some standard regularity conditions made on the prior and log-likelihood functions for proving the BvM theorem (for well-specified models). Assumption 2(c) includes some additional regularity conditions and testability assumptions inherited from Kleijn et al. (2012) to address mis-specifed models. We denote the latent variable Fisher information matrix (also called missing data Fisher information matrix in the missing data/EM algorithm literature, e.g. Dempster et al., 1977), of as and denote as the complete data information matrix at . In this work, we only consider non-singular models by assuming the non-singularity of the Fisher information (Assumption 2(b)). The problem of model selection involving possibly singular models (e.g., mixture models, Ho and Nguyen, 2019) is not covered by our theory and will be left to future research. As a result, in Section 4.2 for numerical study on Gaussian mixture model, we only consider a well-specified model. However, we note that our assumptions are satisfied for under-specified Gaussian mixture models, as well as for other commonly used models such as the linear and generalized linear models. In these cases, the Fisher information matrix remains non-singular even when the model is mis-specified, as discussed in Section 4.3.

Theorem 3.1 in Kleijn et al. (2012) states that the posterior distribution of a mis-specified model tends to be close to a normal distribution. In this paper, we find that the MF variational distribution also contracts to a normal distribution under model mis-specification. Following some recently developed techniques, we first include the following two results on the consistency and concentration of the marginal posterior of and its MF approximation. The first result is a non-asymptotic version of Theorem 3.1 in Kleijn et al. (2012) on the contraction of posterior under model mis-specification, which is inherited from Theorem 5.1 in Ghosal et al. (2000).

Lemma 1

Using a similar variational argument as the proof of Lemma 2 in Han and Yang (2019), the sub-Gaussian type concentration property of the posterior is inherited by its MF approximation , as described by the following lemma.

Lemma 2

Intuitively, the concentration of variational distribution is a result of the strong penalty on the tail difference incurred by the log density ratio in the KL divergence objective (1), which forces to concentrate around the same region where the posterior assigns most of its mass. Lemma 2 further leads to the following theorem on the distributional convergence of , which generalizes Theorem 1 in Han and Yang (2019) from well-specified models to mis-specified models. Note that the counterpart of Theorem 1 for well-specified models in Han and Yang (2019) is primarily used for studying the large-sample properties of the variational mean estimator . In contrast, we extend and apply Theorem 1 to mis-specified models to investigate the large-sample properties of the ELBO for model selection.

Theorem 1

As a direct consequence of this theorem, any reasonable point estimator (e.g. by taking expectation) obtained from is asymptotically the same as MLE under the mis-specified model. The KL divergence bound from the theorem implies an bound between the variational mean etimator and the MLE by applying a transportation cost inequality. However, it is noteworthy that our analysis characterizing the updating dynamics of the CAVI iterative algorithm results in an improved error rate of ; see equation (39) in the proof of Theorem 4. This suggests that there is essentially no loss of statistical efficiency by using the MF approximation to obtain a point estimator to the model parameter as compared to the frequentist likelihood based approaches in the mis-specified setting. However, as is common in the MF variational inference, uncertainty quantification from can be misleading as the asymptotic covariance matrix may drastically underestimate the variability in the marginal posterior of , whose asymptotic covariance matrix is (Theorem 3.1, Kleijn et al., 2012). The uncertainty underestimation mainly comes from two sources: 1. ignoring the dependence among components of results in the diagnolization of the covariance matrix; 2. ignoring the dependence between parameter and latent variables results in the inclusion of the extra term in the precision matrix, i.e. the inverse of the covariance matrix. In particular, if there is no latent variable, then matrix appearing in the reduces to .

Remark 1 (Extensions to Block MF)

If we use the block mean-field approximation , which preserves the within-block dependence as described in the previous subsection, instead of the fully factorized one as , then Theorem 1 can be correspondingly extended where the variational posterior tends to be close to a normal with the same mean, but a different non-diagonal covariance matrix. Precisely, we consider the more general case of MF approximation using factorized densities with blocks whose respective sizes are ,

We similarly write the complete data information matrix in the corresponding block form as

where denotes the -th block. Then will be well-approximated by the normal distribution with

In the special case of block MF over parameter and latent variables , or , the approximating normal distribution becomes , where the precision overestimation only comes from the extra latent variable information in decomposition . The probit regression example described in Appendix A uses such a block approximation.

2.3 Bayesian Model Selection via Mean-Field Approximation

In the previous subsection, we discussed the large-sample behaviour of MF variational inference in approximating the posterior. The normal approximation to suggests that we may use , or more precisely, the accompanied ELBO , as a computationally feasible surrogate to the evidence for performing model selection. Concretely, recall that the true data generating distribution is denoted by . We consider a list of candidate models that may or may not contain . Our target is to select a most parsimonious model from that is closest to . In our setting of parameter models, we use and to denote the respective parameter and parameter space associated with model . The size (or complexity) of a model is then the dimension of (i.e. number of parameters).

In the model selection literature, Bayesian information criterion (BIC, Schwarz et al., 1978) is a commonly used criterion function for selecting a best model that balances between goodness-of-fit to data and model complexity, defined as

| (6) |

for a generic model with number of parameters, where denotes the maximal log-likelihood value under model . To employ BIC for model selection, one selects the model with lowest BIC. More specifically, assume a prior distribution is imposed to under model , and denotes the prior probability assigned to model . Using the Laplace approximation, it can be shown (Stoica and Selen, 2004, also see Theorem 2) that provides a large sample approximation to the logarithm of the posterior probability of data given model , i.e. the evidence of model . Therefore, minimizing BIC over all candidate models is asymptotically equivalent to maximizing the posterior probability over all , as the impact from model prior is diminishing as sample size grows.

Since one perspective of variational inference as described in Section 2.1 is finding a best lower bound to the evidence , where denotes the ELBO under a generic model and denotes the MF approximation (i.e. solution of problem (1) that maximizes within ), it is natural to use to approximate model evidence to conduct model selection. Interestingly, we find (c.f. Section 3.1) that as the sample size tends to infinity, model selection via maximizing the ELBO leads to the same model chosen via minimizing the BIC, which is also the highest posterior probability model. Since BIC is capable of consistently selecting the smallest model containing as (Schwarz et al., 1978), a property known as model selection consistency, we can conclude that ELBO inherits the same model selection consistency property.

Specifically, we find a precise characterization of the gap between the exact evidence and the ELBO associated with MF approximation (Theorem 2) under a large sample size , which converges to a model-dependent constant as . In comparison, also provides an asymptotically constant approximation to the evidence, where the limiting constant is (Theorem 2). The empirical results in Section 4 also align well with these theoretical findings. Consequently, approximating the evidence by ELBO does not incur significantly larger error than that by BIC. Moreover, since the discrepancy between the negative half of BIC and ELBO is of constant order while the optimality gap, i.e. the smallest difference in the BIC values between the optimal model and any suboptimal model will be at least of order in order for the true model to be statistically identifiable, they tend to lead to the same selected model as .

More interestingly, a closer inspection of the two limiting constants and reveals that ELBO generally leads to a better approximation to the model evidence than BIC due to the full incorporation of prior information and a better dimension dependence in the approximation error. For example, the definition (6) of BIC completely ignores the prior contribution while ELBO (defined after equation (2)) involves an integration of log-prior, explaining the extra term in the BIC approximation error. In addition, due to the simple Laplace approximation, has an extra term explicitly dependent of model size , making BIC less accurate in approximating the evidence in large or growing dimension problems; also see our numerical study in Section 4.3 on variable selection in GLM. Last but not least, our numerical studies in Section 4 suggest that ELBO tends to be less conservative than BIC in the presence of weak signals, and can achieve comparable predictive performance as AIC (Hirotugu, 1974) with a much more parsimonious selected model. Note that AIC is known to be minimax-rate optimal for prediction in linear regression but tends to over-estimate the model size (Yang, 2005).

We conclude this section with a brief discussion on computation. Variational inference is commonly used when the posterior does not have an explicit form (e.g., in mixture models). In such settings, the MLE required for BIC calculation also does not admit a closed-form solution. In these cases, the MLE can be solved numerically using the EM algorithm or approximated by the expectation of the variational distribution, where the latter incurs an error of order at most (see the remark after Theorem 1). In either scenario, the computational cost for calculating the MLE (or BIC) is comparable to that of variational inference or CAVI, since the EM algorithm can be viewed as a degenerate CAVI in which the parameter component in the mean-field approximation is further restricted to be a point mass measure. Therefore, previous discussions (or Theorem 2) suggest that ELBO tends to achieve better approximation accuracy than BIC with similar computational costs when estimating model evidence. Additionally, a standard implementation of CAVI for computing the variational distribution requires computational cost per iteration due to the necessity of accessing the full data set. In settings where is large, we may consider approximation methods such as stochastic gradient descent to reduce the per-iteration computational cost (Titsias and Lázaro-Gredilla, 2014; Alquier and Ridgway, 2020). We would also like to note that calculating the BIC often requires accurately determining the effective dimension of the model. For some complex models with non-trivial constraints, such as Bayesian factor models (with constraints on the factor loading matrix to enforce identifiability) or latent variable models like Hidden Markov models, counting this effective dimension might not be straightforward. In contrast, calculating the ELBO is a straightforward by-product of implementing the MF variational inference, which automatically incorporates the effective dimension and eliminates the need for case-by-case analysis.

2.4 Computation via Coordinate Ascent

Coordinate ascent is a natural and efficient algorithm for optimizing over densities taking a product form as in MF approximation (1). For illustration, we focus on models without latent variables, where the mean-field family contains all factorized densities of the form for . Otherwise, we may view the latent variables as one (block) coordinate of the parameter and derive the corresponding coordinate ascent algorithms. In general, we may also block approximation where each component is a multi-dimensional density. The key idea of coordinate ascent is to optimize over one component of at a time while fixing the others. Let denote the joint density function of , all components in except for . When optimizing over the component , it would be helpful to express ELBO as a functional of ,

where constant is independent of . From this identify, we may explicitly solve the optimizer as

| (7) |

As is often in practice, one can recognize above as coming from some parametric family, for example, certain exponential family, and determine the normalizing constant of ; otherwise, either particle methods (Saeedi et al., 2017; Wang et al., 2021) can be employed to approximate over , or can be further restricted to some parametric family, resulting in a hybrid variational approximation. To summarize, we can apply coordinate ascent to numerically solve the optimization problem in MF based on formula (7) in an iterative manner; and the resulting method is known as the coordinate ascent variational inference (CAVI, Bishop, 2006b) in the literature. To avoid overly aggressive moves that may lead to periodic oscillation or even divergence, it is customary to introduce a step size parameter and define the next iterate as proportional to the weighted geometric average between and current iterate . In particular, with full step size , the update is most greedy and the coordinate ascent becomes alternating maximization. As we will show in our theoretical analysis in Section 3.2 and some numerical studies in Section 4, the introduction of a partial step size is necessary in some problems to avoid algorithmic non-convergence.

In practice, two common updating schemes are utilized in CAVI, depending on whether the components are sequentially or simultaneously updated. In order to draw a connection with two well-known iterative algorithms for solving linear systems (e.g. Trefethen and Bau III, 1997), we will exchangeably call the followings as the Jacobi scheme and Gauss–Seidel scheme respectively, at iteration :

Parallel (Jacobi) update. We update all components simultaneously based on the last iteration. To be more precise, we run following updates at each iteration.

| (8) |

This algorithm can be run in parallel. However, the ELBO is not guaranteed to be monotonically decreasing in if the full step size is used. To guarantee the convergence, we may need to take a step size , i.e.

| (9) |

This however may lead to a slower convergence.

Randomized sequential (Gauss–Seidel) update. We update one component at each time using the most recent updates of the other components. For simplicity, we focus on the randomized sequential update, where a component is randomly picked to be updated. Concretely, for a random index , we compute

| (10) |

In this way, ELBO value is guaranteed to be monotonically non-decreasing in . However, due to the sequential nature, we cannot utilize parallel computation techniques to reduce the run time. For the sequential update, we may also consider the systematic variant where the components are updated in a pre-specified deterministic order.

Due to the numerical error, the computed ELBO value may differ from the theoretical ELBO value. It is therefore necessary to analyze the convergence of CAVI to guide its implementation in practice, particularly when applied to perform model selection. In Section 3.2, we determine the algorithmic convergence rate of CAVI, and study the impact of various problem characteristics on the rate. Most literature in CAVI convergence studies some special cases such as Gaussian mixture model (Wang and Titterington, 2005; Titterington and Wang, 2006), stochastic block model (Zhang and Zhou, 2020; Mukherjee et al., 2018; Sarkar et al., 2021; Yin et al., 2020) and Ising models (Jain et al., 2018; Koehler, 2019; Plummer et al., 2020). Accessing the convergence and determining the accompanied rate under general settings is still an open problem.

In Section 3.2, we identify a set of suitable conditions under which the -th iteration from CAVI satisfies

as long as initialization is in a constant neighborhood around the true parameter , where is the algorithmic convergence rate depending on the model and the CAVI setup, and is the usual root- statistical error, where the poly- factor in is due to the high probability argument in our proof. This result can be interpreted as that under a warm initialization, the ELBO regret (the difference between the ELBO value at the optimum and ) relative to the theoretical value has a geometric convergence towards zero up to a statistical error of the problem. Since has a trivial bound as , to guarantee the output ELBO value to be within distance away from its theoretical value, our theory suggests that iterations suffice (so that each component is updated times on average). Moreover, under a suitable metric, which will be the Hellinger distance , we show that the iterate at time from CAVI converges towards at a geometric speed up to a statistical error term as

where the convergence rate is expected to be since the KL divergence is locally quadratic when expanded in . This result can be used to determine the number of iterations for obtaining a root- consistent point estimator based on the output of from CAVI.

Another interesting finding implied by our theory is that the randomized sequential update always converges exponentially fast with full step size given a warm initialization. In contrast, in some examples with moderate dependence, the parallel update will converge only when a partial step size (i.e. ) is used. However, for those step sizes under which both schemes converge, they tend to exhibit a similar convergence behavior.

3 Theoretical Results

In this section, we provide the main theoretical results of this paper. In Section 3.1, we derive a non-asymptotic expansion of ELBO under MF approximation, and compare it with that of BIC. We also build an oracle inequality, showing that the model selected by ELBO has prediction performance comparable to the best model, even in the case all candidate models are mis-specified and do not contain . In Section 3.2, we analyze the algorithmic convergence of the CAVI under the two aforementioned schemes, and discuss their consequences.

3.1 Model Selection Consistency Based on ELBO

In this subsection, we show the consistency of model selection based on (penalized) ELBO. Our first result provides non-asymptotic expansions of ELBO and BIC for approximating the model evidence . Recall that defined in (4) denotes the parameter in model such that best approximates the true data generating distribution .

Theorem 2

Suppose the same assumptions of Theorem 1 to hold for a generic model . There exists constants such that for any , it holds with probability at least that

| (11) | |||

| (12) | |||

Note that inequalities (11) and (12) together imply the difference between and ELBO to be asymptotically constant as , which we denote as

| (13) |

As a direct consequence of the theorem, the model selected by maximizing ELBO will lead to the same one that minimizes BIC, as long as the minimal BIC value is at least of order away from the second smallest value. For example, let denote the smallest model containing the data generating distribution . Under the model identifiability condition that any underfitted model not containing has a strictly positive “KL gap” for some , it is not difficult to show (e.g. see Appendix D.5) that the difference between BIC values of and is at least with high probability. On the other hand, for any overfitted model containing and having a larger number of parameters , we have that holds with high probability (see Appendix D.5); this further implies . By combining two cases, we can conclude that maximizing ELBO will consistently select the best model as by minimizing the BIC since for some constant when is sufficiently large.

Note that the same discussion in Remark 1 also applies to Theorem 2 for the block mean-field approximation, where the constant then becomes , which is never larger than the in Theorem 2. This observation suggests that incorporating additional structure in the VI is always beneficial for improving the approximation accuracy given the computation is still tractable. In the other situation with no latent variables, the constant becomes , which is precisely the KL divergence between the two normal distributions and , where the former approximates the posterior distribution under model mis-specification (Kleijn et al., 2012) and the latter approximates the MF solution (Theorem 1 without latent variables), respectively. This limiting gap will vanish if components of are asymptotically independent (e.g. the location-scale normal model in Section 4.1).

Remark 2 (Discussion on model selection criteria)

For a Bayesian model with latent variables, we have another ELBO value to use for model selection, which is the parameter part in decomposition (3), or

where recall that denotes the marginal posterior of and the extra Jensen gap is due to latent variables. In the proof of Theorem 2, it is shown that this Jensen gap asymptotically converges to a non-negative constant . Therefore, the parameter part leads to an improved approximation to the evidence (due to a smaller gap); and model selections based on and are asymptotically equivalent, and equivalent to that based on . However, unlike that can be efficiently computed via CAVI, may not admit a closed form updating formula; and requires Monte Carlo methods to approximate.

Bayesian hypothesis testing can be viewed as a special instance of model selection with two candidate models, denoted as and . Decisions in Bayesian hypothesis testing or model selection between two models are typically based on the so-called Bayes factor, which is defined as

Motivated by our general model selection procedure based on ELBO, we define the ELBO factor as a computationally-efficient surrogate to the log-Bayes factor, by noticing

where the second equality is due to Theorem 2. We summarize the result in the following.

Corollary 1

Previously, we have seen that model selection based on ELBO tends to agree with that based on BIC when at least one of the candidate models contains and it is statistically distinguishable. However, it is often in practice that none of the models in the list contains . Another common situation is when some signals are weak, for example, the -condition (c.f. Yang et al., 2016b) does not hold in linear regression with moderate to large number of variables; then it is information-theoretically impossible to select all important variables. Moreover, using a smaller model may lead to better prediction performance than the true model by excluding those less significant variables; in fact, using the true model with many variables may lead to overfitting. For example, in the numerical study of variable selection in GLM in Section 4.3, we can see from the left two plots in Fig. 8 that both BIC and ELBO tend to select a smaller model which turns out to have better prediction performance than the true model with variables. To theoretically quantify the quality of the model selected via ELBO in the MF approximation in these situations, we prove an oracle inequality, which shows that the model selected by ELBO has prediction performance comparable to the best model in the list, even all candidate models may be mis-specified and do not contain .

Theorem 3

Under the same assumptions as Theorem 2, there exists some constant such that for any , it holds with probability at least that the model selected by satisfies

where is the total number of candidate models.

As mentioned in the introduction, Chérief-Abdellatif (2019) also proves an oracle inequality for the model selected by ELBO maximization in variational inference. However, their results apply only to models that do not contain latent variables, and their risk function is based on the -Rényi divergence, which is generally weaker than the KL-divergence used in our results. Additionally, their result is stated only for -fractional posteriors under , which requires fewer assumptions than our Assumptions 2 and 3. Specifically, they do not require a testing condition such as Assumption 2(c), which is one merit of considering Bayesian fractional posteriors (Bhattacharya et al., 2019).

3.2 Convergence of CAVI Algorithms

In this subsection, we address the theoretical question of analyzing the convergence of CAVI algorithms. The algorithmic convergence analysis provides a theoretical guidance on how many iterations are required to adequately approximate ELBO to achieve model selection consistency; according to Theorem 2 and the related discussions, a constant numerical error approximation to the ELBO would suffice for this purpose. Since in the convergence analysis the model is fixed throughout, we will omit all in the subscripts when no ambiguity may arise. We let be a discrepancy measure between the -th iterate from CAVI and the MF solution . Note that we also have , which is the regret of relative to the theoretical ELBO value achieved by .

Special case: Gaussian posterior without latent variables. We first consider the special case of a Gaussian posterior to help explain the intuition. Specifically, we assume the target posterior to be the density of , which will be denoted by . Since our later analysis concerning a general posterior will have a leading term related to its (asymptotic) normal approximation , we will preserve the notation for the -th iterate in the CAVI, either the parallel or the randomized sequential update depending on the context, of maximizing in the MF variational inference. To simplify the notation, we use the shorthand notation and . Under this notation, the MF approximation is , which is the density of .

To simplify the analysis for the Gaussian posterior, let us assume the initialization to be the density of for some initial mean vector . This assumption is not overly restrictive. It is easy to verify that after each component in is updated at least once with full step size , all future iterates of will follow a normal distribution with covariance matrix . Due to this reason, let us denote as the density of . To describe the two updating schemes of the CAVI described in Section 2.4, let us derive the common step of updating one component from the following rule. Recall that the parallel scheme updates all components with indices in one iteration; while the randomized sequential scheme randomly pick one index . The common updating formula for is

where denotes the step size. Denote the bias at iteration as . Then it is straightforward to translate the preceding display into an updating rule for as

| (14) |

Parallel update applies (14) to components simultaneously, and we may write the equivalent matrix form as for . On the contrary, sequential update applies (14) to one component at each iteration, and we may directly study the decrease in ELBO as it is quadratic (c.f. Appendix D.6 for more details). It is worth noting that the parallel and the randomized sequential schemes using the preceding updating rule respectively coincide with the Jacobi and the Gauss-Seidel methods (with partial step size) for solving the system of linear equations . To analyze the convergence of the algorithm, let us study the evolution of the objective functional , whose convergence implies the convergence of the algorithm. For the Gaussian posterior, we have , which is equivalent to up to some multiplicative constant. We summarize the result in the following lemma, whose proof is deferred to Appendix D.6.

Lemma 3 (Gaussian posterior without latent variables)

Suppose the true posterior is . If the step size is chosen so that the defined below belongs to , then converges exponentially fast to :

for some constant depending on the updating scheme. In particular, we have for the randomized sequential update; and for the parallel update, where

| (15) |

Without parallel computing, the computational complexity of iterations of the sequential scheme is comparable to that of the parallel scheme. Therefore, to fairly compare the overall computational complexities, we may define one iteration in the sequential scheme as updates, whose effective contraction rate is then , which is roughly for a large . Some detailed comparison of the contraction rates is deferred to the end of this subsection.

Remark 3 (Necessity of partial step size)

From Lemma 3, we can see that the randomized sequential update always converges exponentially fast with full step size, i.e. for . In fact, as in randomized sequential update and due to non-singularity of , we may prefer taking to obtain fastest convergence rate. In contrast, the parallel update may require a partial step size to guarantee the convergence. This is not an artifact of our proof technique — consider the following counterexample with : we take , where is the identity matrix and the all-one vector. If initialized at , the parallel scheme leads to , and therefore both and the ELBO diverges.

General case I: non-Gaussian posterior without latent variables. Recall that the CAVI output at -th iteration for a general posterior is denoted as , and the associated CAVI output for its large sample normal approximation (density denoted as ) is . In addition, the MF approximation to is , whose density is denoted as ; and is the MF approximation to . Recall that denotes the regret of relative to the theoretical ELBO value achieved by . We prove the following theorem, describing the convergence of and , by applying perturbation analysis for generalizing Lemma 3 to a general posterior.

Theorem 4 (General posteriors without latent variables)

Under Assumptions 1 and 2, there exist positive constant , such that if the support of initial distribution is in some small neighborhood around , or for some sufficiently small constant , then we have for any it holds with probability at least that

| (16) |

where the contraction rate is given in Lemma 3. Moreover, under the same high probability event, there exists some constant depending on the initialization such that

| (17) |

The proof of the theorem is quite technical and provided in Appendix D.7, where the expression of is also included. As we can see, the general case inherits the same contraction rate from the Gaussian case. However, the convergence is now only up to the statistical accuracy; and only a local geometric convergence can be proved. The local convergence is not an artifact of our proof, as the numerical example in Section 4.4 shows that the fast geometric convergence indeed only occurs after the iterate enters the contraction basin as a local neighborhood around . We note that the in our error bound is larger than the error bound proved in Alquier and Ridgway (2020) for the gradient-based method for MF inference. However, their result is only stated for the MF approximation to -fractional posteriors with , which requires fewer assumptions and tends to be technically less involved to prove. It would be interesting to explore if the same error bound also holds for the MF approximation to the usual posterior without tempering.

In view of Theorem 1, it suffices to run iterations to guarantee model selection consistency by using the approximated ELBO value produced from the CAVI algorithm. The first inequality in the theorem states that converges to exponentially fast up to a statistical error term of order . However, the convergence of to (which is roughly equal to the constant , up to the same statistical error) does not imply the convergence of to . Therefore, we also provide the second inequality that implies the convergence of towards , where the loss function used is the Hellinger distance. We use the weaker Hellinger distance to characterize the convergence of by applying the triangle inequality because KL-divergence is not a metric and hence triangle inequality is not applicable.

General case II: non-Gaussian posterior with latent variables. When there are latent variables, we may apply similar arguments to analyze the convergence of the CAVI algorithm. The (parallel) updating formula in CAVI with latent variables, for example, becomes

We will follow a similar analysis based on Taylor expansions on , first analyzing by utilizing the concentration property of and then plugging it into . This perturbation analysis helps us identify the leading terms in the CAVI updates, resulting in a key updating formula (45) (in Appendix D.8) describing the “noiseless” case dynamic, similar to the updating formula (14) for the Gaussian posterior without latent variables as obtained earlier. With this key updating formula, we can then proceed with the analysis as in the case without latent variables. First, we study the CAVI for the leading “noiseless” Gaussian (or quadratic) case. We then employ perturbation analysis to analyze the CAVI for the original problem. The randomized sequential update can be interpreted and analyzed in a similar way. This leads to the following theorem, whose proof is provided in Appendix D.8. Recall that we used to denote the observed data Fisher information, for the missing data Fisher information, and for the complete data Fisher information. Additionally, and are the diagonal matrices corresponding to the diagonal parts of and , respectively.

Theorem 5 (General posteriors with latent variables)

By comparing the contraction rates of the CAVI algorithm with latent variables (Theorem 5) to those without latent variables (Theorem 4), we can observe that the presence of latent variables generally slows down the convergence of CAVI. Specifically, this reduction in convergence rate is characterized by a factor related to the ratio between the observed data information and the complete data information, or the matrix operator norm of , where diagonalization is due to the mean-field approximation on ; see the sequential update case in Appendix D.8 for a more concrete calculation. Our convergence result for the CAVI algorithm is consistent with existing findings on the algorithmic contraction rate of the EM algorithm (Dempster et al., 1977) — the convergence slows down as the missing data information increases, making the latent variables harder to learn, which in turn affects the algorithmic convergence of the estimation of .

We end this section with a discussion on the efficiency comparison of the two updating schemes using an illustrating example without latent variables. We define an epoch for the sequential scheme to be iterations so that each coordinate is updated once (on average for the randomized sequential update), and an epoch for the parallel scheme as one iteration. We compare the (averaged) decrease in ELBO for the two methods after one epoch. We consider . For the sequential update, has a relative decrease by at least , which will be at after one epoch. For the parallel update, we need to avoid divergence. Taking leads to a largest relative decrease by . When is close to , we can see that the decrease from the parallel update tends to be of that from the sequential update after one epoch. As tends to zero, the relative decrease from the parallel update is about , which is roughly times larger (better) than the decrease from the sequential update when is large. Therefore, efficiency-wise, the parallel update is generally preferred in low dependence situations ( small); while the sequential update is preferred in high dependence and high dimensional situations. Implementation-wise, the parallel update may benefit from parallel computing; the sequential update always converges while the parallel update may need fine tuning the step size.

4 Numerical Study

This section includes numerical experiments on assessing the algorithmic convergence and the performance of using ELBO for model selection. Detailed descriptions about some of the considered examples are provided in Appendix A.

4.1 Location-Scale Normal Model

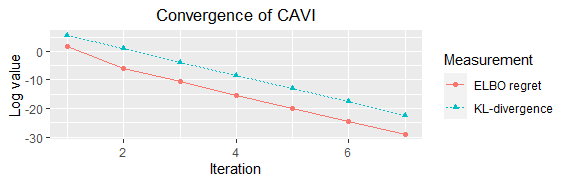

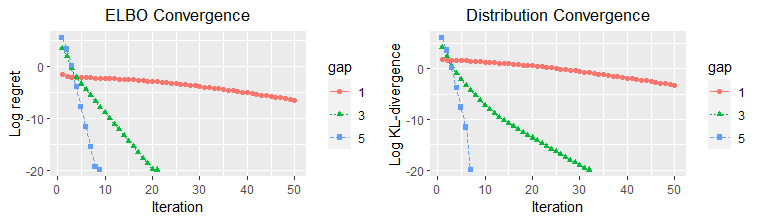

We consider the location-scale normal model with parameter as described in Appendix A. We generate sample from with sample size . We take the prior as and . To assess the convergence of the CAVI algorithm, we plot the logarithms of the ELBO regret and the KL divergence between and respectively versus iteration count . Note that the posterior has asymptotically independent components in this setting, so the two updating regimes lead to similar result, and we present sequential update for illustration. Here the optimal variational distribution is approximately obtained from the CAVI output after sufficiently many iterations. The results in Fig. 2 show that both measurements are nearly linearly decreasing in the log-scale, implying the geometric convergence. The two curves are nearly parallel, which implies the same convergence rate. Note that the Fisher information (equal to without latent) in this example is diagonal. Therefore, the leading constant term of the contraction rate from Theorem 4 vanishes and the remainder term characterizes the contraction rate.

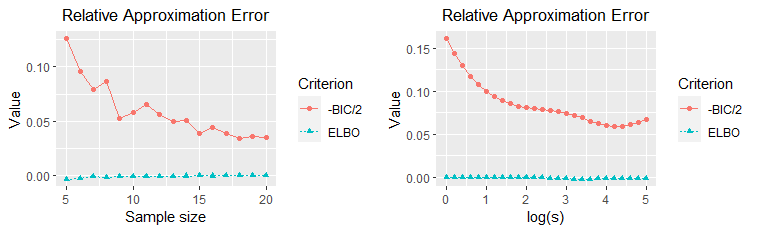

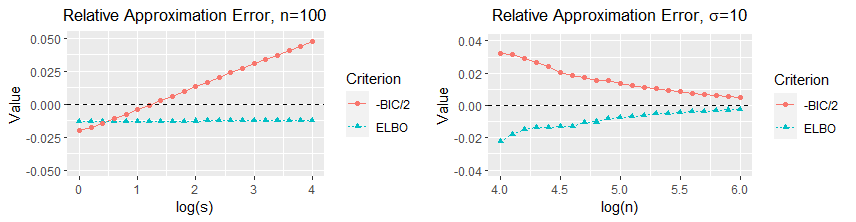

In terms of the approximation accuracy of ELBO and BIC, the diagonal information matrix implies that the limiting constant gap between evidence and ELBO equals 0, and they only differ by a statistical error term. On the other hand, the constant gap between evidence (or ELBO) and is generally non-zero. We can also see this difference via a numerical comparison, by plotting the relative approximation errors of ELBO and BIC under different sample sizes, defined as and respectively. The evidence is calculated based on Monte Carlo replicates. The result is included in the left panel of Fig. 3.

To assess the impact of prior information on the approximation accuracy, we run an extra simulation study by fixing the sample size to be , and taking the prior as and with varying over the grid for . We report the result in the right panel of Fig. 3. As expected, smaller leads to larger approximation error of BIC, as BIC completely neglects the prior contribution in the evidence.

4.2 Gaussian Mixture Model

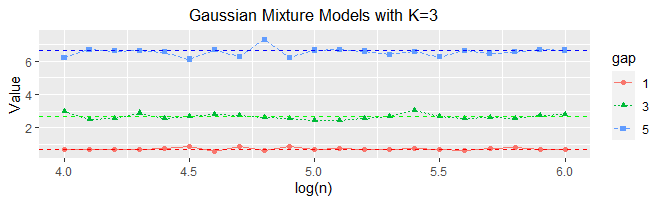

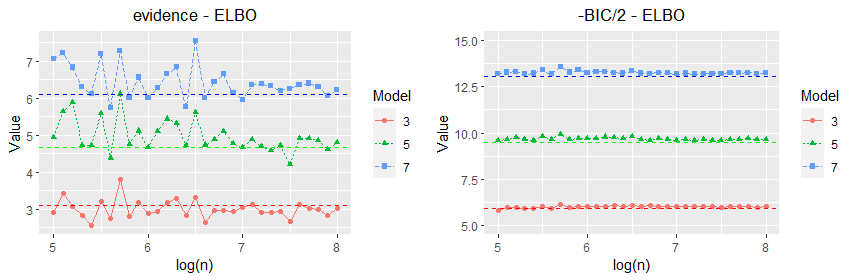

We consider the Gaussian mixture model (GMM) with clusters centered at (a detailed description is provided in Appendix A). We take the gap (or cluster separation) , and the prior parameter in the i.i.d. prior for cluster centers (we choose relatively smaller so that is more distinguishable in the plot for different ). We take the sample size over the grid for , and calculate in comparison with theoretical values . We first focus on the GMM with a correctly specified number of clusters . We can see the simulated values are fairly close to the theoretical limit from Fig. 5.

We also assess the convergence of the sequential CAVI algorithm by plotting the logarithm of the ELBO regret and under , and . The numerical results from Fig. 5 show the geometric convergence of both measurements as they are nearly linearly decreasing in the log-scale, which is consistent to the prediction from Theorem 4. The slopes of two measurements are also close under the same , implying the same convergence rate. Moreover, since a large gap leads to a lower posterior dependence, our Theorem 4 predicts a smaller contraction rate (faster convergence), which is also consistent with the numerical results.

Next, we compare the use of BIC and ELBO for evidence approximation. We consider two settings: 1. prior standard deviation for with under fixed sample size ; 2. sample size with with fixed . We take the gap . As we can see from Fig. 7, the approximation error of BIC is quite sensitive to the prior choice; while the approximation of ELBO is much more accurate and stable. However, both approximations become accurate as we increase the sample size.

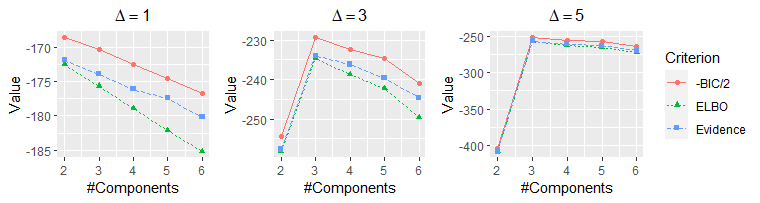

Note that GMM has degenerate Fisher information when the number of clusters is misspecified, which leads to a slower rate of convergence when is over-specified (Chen, 1995). With known mixing weights, the overfitted models are still degenerate. For example, the two component GMM with equal weights is degenerate when true model is a single Gaussian (Dwivedi et al., 2020). Although our theory no longer applies in such a situation, it is still interesting to compare the model selection performance based on BIC, ELBO and the true evidence. For simplicity, we assume the underlying mixing weights to be known and fixed in our simulation setting. We set , sample size and prior with . The results are summarized in the Fig. 7.

As we can see, the three model selection criteria result in the same selected models across all settings. When the gap is relatively small, all criteria select the smaller model with two components. As we increase the gap to , all criteria select the true model. In terms of approximation accuracy for the evidence, we can see that ELBO tends to be more accurate than BIC, particularly for smaller models under stronger signal-to-noise ratios where the Fisher information is non-singular near the mis-specifed MLE.

4.3 Generalized Linear Model

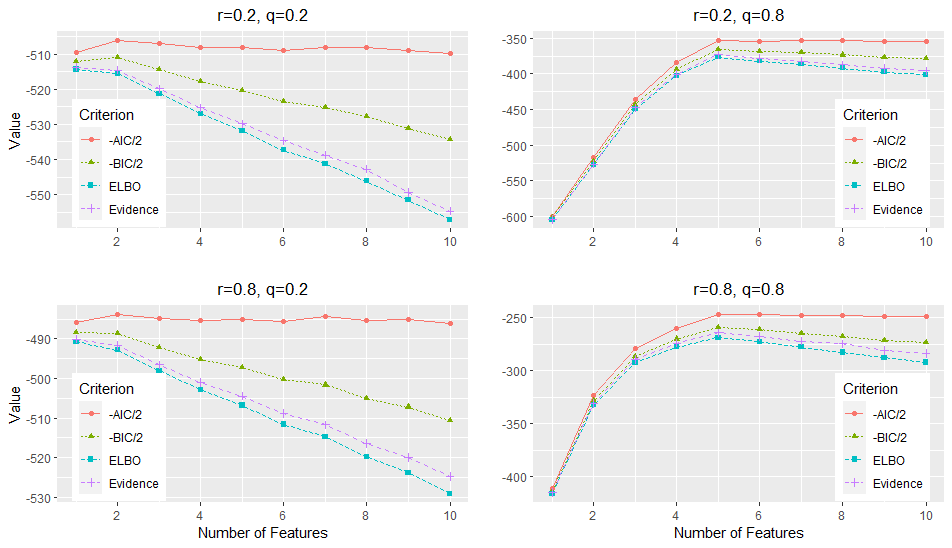

In this section, we consider variable selection in probit regression as a representative instance of generalized linear model (GLM), whose detailed description is deferred to Appendix A. The simulation setting is as follows. We generate -dim feature vectors i.i.d. from . The covariance matrix is of AR(1) structure so that . We take , and the -dim (regression) coefficient has the nonzero terms: . The prior of is the centered multivariate normal distribution with covariance matrix where . To assess the variable selection performance, we compare ELBO with AIC, BIC, and the true evidence (calculated based on Monte Carlo replicates). As we can see from Fig. 8, when the signal is relatively strong (), all methods except AIC correctly select the true model; and AIC selects a larger model (with features) when the dependence is strong (). Moreover, the AIC curve is quite flat and the discrepancy between AIC values under different models are small. Under the weak signal case (), although the proposed criterion and BIC fail to select the true model, they still select the same model as that based on evidence (i.e. highest posterior model). Under all four settings, ELBO is much more accurate than BIC in terms of the approximation for the evidence.

In addition, to compare the numerical gaps with the theoretical constants and (which together also characterize ) in Theorem 2 and (13), Fig. 9 includes their simulated values for the models including , and features (recall the true model contains features), respectively, with the sample size over the grid of for , , …, , . In this study, we set and . We estimate for the underfitted model (with 3 features) based on samples, so that the estimated can be treated as . As we can see from Fig. 9, the simulated values are fairly close to the theoretical ones, which justifies our theory that evidence and are equal to and up to some higher-order terms. We note that the simulated values of have higher fluctuations, which might be partially caused by the high variance of the Monte Carlo approximation to the evidence.

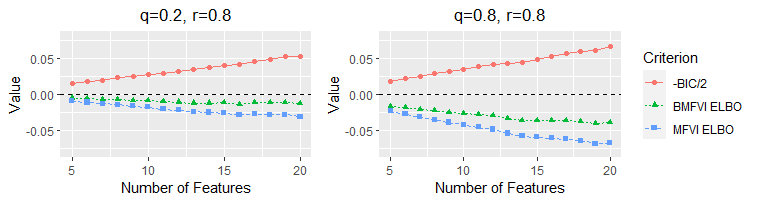

According to Theorem 2, the difference between -BIC/2 and evidence has a term proportional to the dimension , which is consistent with the trend of the gap observed from Fig. 8. On the other hand, as we used block MF (BMFVI) for probit regression, the approximation error of ELBO only comes from the difference between and characterized by , which grows linearly in with slope independent of . To formally demonstrate the impact of on approximation the evidence, we plot the approximation errors of BIC and ELBO for in Fig. 10. In the plot, we also include the results for the fully factorized MF (MFVI), whose limiting approximation error tends to be more sensitive to than BMFVI, as expected.

We can see that ELBO with BMFVI has overall best approximation accuracy, while the approximation error of BIC is largest due to its strong dimension dependence. On the other hand, the ELBO from MFVI has larger approximation error than that from BMFVI, due to the additional independence imposed among parameter components. Therefore, we should take advantage of the block mean field structure and implement BMFVI in practice whenever computationally tractable.

To assess the prediction performance of various criteria in the presence of weak signals (i.e. selection consistency may not be achievable) in the context of Theorem 3, we consider a more challenging setting where , for , and the same covariance matrix with for the random feature vectors. Although now the true model includes all important features, signals decay geometrically fast; as a result, both BIC and ELBO would select much smaller models. Although model selection consistency does not hold under this setting, we use numerical study to compare the prediction performance of model selection based on AIC, BIC and ELBO. In this example, we include AIC as the benchmark corresponding to the theoretically minimax-optimal criterion for prediction (Hirotugu, 1974). We generate data, and randomly select of them as training data, and the remaining as test data. Then we select the model using the training data with AIC, BIC and ELBO, and evaluate their prediction performance on the test data. We compare the classification errors and logistic losses of ELBO and BIC evaluated on the test data. Note that the logistic loss is defined as ], where is the fitted probability on the -th test data with the selected model. The logistic loss is the log-likelihood function evaluated on the test data, and approximates the population-level KL-divergence between the true and the fitted prediction distributions up to some fixed constant. We report the average classification errors along with their standard deviations, and the median of logistic losses from 100 Monte Carlo replicates. From Table 1, the prediction accuracy of ELBO is overall comparable to AIC, and outperforms BIC. However, AIC tends to include more variables than ELBO for slightly reducing its classification error; while due to the tendency of overfitting the data by including too many variables, AIC may incur slightly larger logistic loss on the test data. Overall, ELBO seems to be a better balance between AIC and BIC by selecting a parsimonious model with comparable prediction accuracy as AIC.

classification error in % logistic loss average model size ELBO AIC BIC ELBO AIC BIC ELBO AIC BIC 0.2 200 21.5 (1.6) 20.7 (1.6) 24.1 (2.7) 0.421 0.430 0.451 5.2 (0.9) 7.8 (1.6) 3.6 (0.9) 500 18.8 (0.7) 18.5 (0.8) 20.0 (1.1) 0.363 0.366 0.381 7.4 (0.9) 9.8 (1.5) 5.7 (0.8) 1000 18.0 (0.5) 17.8 (0.5) 18.7 (0.6) 0.346 0.346 0.356 8.7 (0.9) 11.2 (1.4) 7.2 (0.8) 0.8 200 13.3 (1.0) 13.0 (1.0) 14.6 (1.5) 0.276 0.282 0.289 3.8 (0.9) 4.8 (1.2) 2.7 (0.6) 500 11.4 (0.6) 11.2 (0.7) 12.5 (0.9) 0.229 0.227 0.248 5.5 (0.9) 6.9 (1.2) 4.0 (0.6) 1000 10.7 (0.5) 10.5 (0.5) 11.3 (0.5) 0.215 0.211 0.225 7.0 (0.9) 8.6 (1.0) 5.4 (0.8)

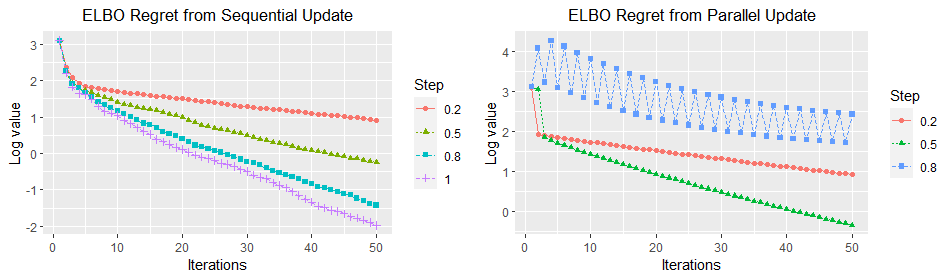

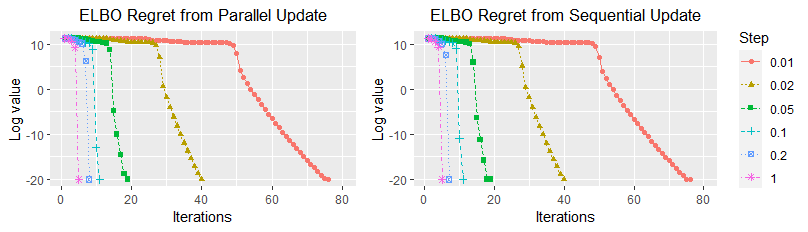

Lastly, we assess the algorithmic convergence of the two CAVI algorithms for implementing MFVI. We take the true model with samples and features with , and feature covariance matrix with . The prior standard deviation is and initialized at . Fig. 11 reports the logarithm of ELBO regret with different step sizes from parallel and randomized sequential updates.

As we can see, the sequential update is always convergent and has faster convergence rate with a larger step size; moreover, the log ELBO regret has a linear decay, imply the geometric convergence of ELBO. On the contrary, the parallel update only converges under smaller step sizes — the ELBO converges extremely slow due to oscillations or even diverges to under larger or full step size (hence not presented), and tends to be the threshold under which CAVI converges fast without oscillations. Consistent with our theory, the parallel CAVI has geometric convergence for small step sizes and . In addition, for both updating schemes, the slope (equal to ) of the log regret is roughly proportional to the step size in absolute value (except for in the parallel update).

4.4 Community Detection

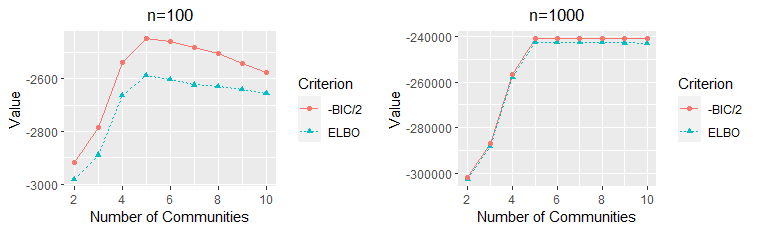

In this example, we consider the model selection problem of selecting the number of communities in the community detection described in Appendix A. We set the true underlying data generating stochastic block model (SBM) to have communities. The five communities have equal number of members. The connectivity matrix is generated as if and . For candidate models, we consider communities. We take the priors on as Beta(1,1) and on as Categorical(). We calculate the ELBO using the parallel update in CAVI with full step size, since we find that the algorithm always converges. In terms of BIC, since we cannot find the exact MLE, we approximate MLE by the variational mean from and obtain the BIC correspondingly.

For SBM the Fisher information is infeasible as is for MLE. However, we can visually find , i.e. the gap between -BIC/2 and ELBO via the numerical differences. Note that it is no longer a “constant” gap since we have growing number of parameters in SBM. We have included the ELBO and BIC values obtained with and 1000 nodes in Fig. 12. Both criteria select the true model under both settings, but the gap between two criteria is comparable to the gap between different models, particularly for the overfitted model. This is due to the growing number of parameters.

We plot in Fig. 13 the regret of ELBO versus iteration counts from both parallel and sequential CAVI algorithms under the true model, with different step sizes.

We can see that two updating regimes have overall similar performance. The ELBO decays slowly in the first several iterations, and converges exponentially fast afterwards. The convergence speed (slope) is roughly proportional to the step size and the two updating regimes have almost identical speed under small step sizes. This is consistent with our findings in Theorem 4 that CAVI has geometric convergence given a good initialization, as the ELBO in SBM starts to converge exponentially fast after entering the local contraction basin around the true parameter.

4.5 Real Data Application

In this section, we apply and compare the three model selection criteria, namely ELBO, AIC and BIC, in four classification datasets: Adult, Taiwan Company Bankruptcy (TRB), Musk and Car Insurance Claims (CIC). The first three are publicly available on the UCI machine learning repository, and the CIC data is available at kaggle.

The original Adult dataset contains 14 features, including 6 continuous and 8 categorical ones. Instead, we use the pre-processed version on the LibSVM repository containing 123 binary features and 32,561 samples. The response variable is a binary one encoding whether the individual has salary 50K. The TRB dataset contains 95 features and 6,819 samples. We remove one constant feature and use the remaining to predict whether the company will go bankruptcy, based on the business regulations of the Taiwan Stock Exchange. Since the data is highly unbalanced as only 220 data points have response one (referring to bankruptcy), we repeat each of them for additional 10 times so the derived dataset contains 9,019 samples. This is equivalent to a weighted probit regression. For the Musk dataset about molecules, we use its second version that contains 6598 samples and 166 features. The goal is to predict whether the molecules are musks or not. The original CIC dataset contains 10,000 samples and 17 features. We remove the samples containing missing values and apply one-hot encoding to the categorical features, and the pre-processed data contains 8,149 samples and 26 features.

We compare the prediction performance in terms of classification error, logistic loss and selected model size, similar to the numerical study in Section 4.3. For each dataset, we randomly select samples as the training data, which is used to conduct model selection with ELBO, AIC and BIC. The selected models are fitted using the same training data and evaluated on the remaining data as the test data. This procedure is repeated times, and we report the average classification errors and median logistic losses, and also the average sizes of the models selected by different criteria. As we can see from Table 2, AIC has the overall best performance in terms of prediction as expected, which is consistent with the optimality of AIC in prediction accuracy (Yang, 2005). On the other hand, the performance of the proposed ELBO criterion tends to be in the between of AIC and BIC, with slightly worse prediction performance than AIC but better than BIC. The model size selected by ELBO also lies between AIC and BIC.

Data classification error in % logistic loss average model size ELBO AIC BIC ELBO AIC BIC ELBO AIC BIC Adult 18.6 (1.3) 18.2 (0.8) 20.0 (1.9) 0.369 0.366 0.384 7.0 (1.3) 11.0 (1.8) 3.7 (0.8) TRB 14.9 (0.7) 14.4 (0.7) 15.5 (0.8) 0.328 0.353 0.317 5.8 (1.7) 8.7 (1.9) 3.4 (0.7) Musk 10.2 (1.1) 8.6 (0.7) 12.2 (1.3) 0.265 0.243 0.290 10.6 (3.1) 17.7 (3.5) 5.5 (1.3) CIC 17.0 (0.8) 16.9 (0.6) 17.9 (1.6) 0.333 0.330 0.349 10.2 (1.2) 11.0 (1.1) 8.0 (1.0)

5 Conclusion

In summary, we proved a non-asymptotic BvM-type theorem for the MF variational distribution, stating that the variational distribution concentrates to a normal distribution centered at MLE with diagonal covariance matrix. Motivated by this normal approximation, we proposed a model selection criterion based on evidence lower bound (ELBO), and studied the model selection consistency. We found that BIC, ELBO and evidence tend to differ from each other by some constant gaps; and ELBO tends to provide a better approximation to evidence than BIC due to a better dimension dependence and the full incorporation of the prior information. To characterize prediction efficiency, we also proved an oracle inequality for the variational distribution from the model selected by ELBO. Lastly, we showed the geometric convergence of two commonly used CAVI algorithms for solving the optimization problem in MF approximation; and the analysis suggested that it suffices to run iterations of CAVI algorithm to approximate the ELBO in order to achieve model selection consistency.