Set-valued expectiles for ordered data analysis

Abstract

Recently defined expectile regions capture the idea of centrality with respect to a multivariate distribution, but fail to describe the tail behavior while it is not at all clear what should be understood by a tail of a multivariate distribution. Therefore, cone expectile sets are introduced which take into account a vector preorder for the multi-dimensional data points. This provides a way of describing and clustering a multivariate distribution/data cloud with respect to an order relation. Fundamental properties of cone expectiles including dual representations of both expectile regions and cone expectile sets are established. It is shown that set-valued sublinear risk measures can be constructed from cone expectile sets in the same way as in the univariate case. Inverse functions of cone expectiles are defined which should be considered as rank functions rather than depth functions. Finally, expectile orders for random vectors are introduced and characterized via expectile rank functions.

Keywords. multivariate expectile, expectile region, expectile risk measure, expectile rank functions

MSC2020. 62H05, 65C20, 91G70

1 Introduction

Expectile regression and expectiles were introduced in [23] and gained popularity later on, see, for example, [8, 11, 19] and in particular the literature review in [7] with many further references. They also provide a new class of financial risk measures of the type introduced in [2], which has been pointed out in [4] along with dual representation results. Therein, it was also shown that expectile risk measures are basically the only sublinear cash-additive risk measures which are elicitable. In [3, 27], further applications of expectiles to risk management are discussed.

Expectiles were extended from the univariate to the multivariate case in [9, 6] in form of set-valued functions although already Eilers [10] gave a geometric construction for the bivariate case. In [9, 6], one can find the definition of expectile regions as another instance of depth regions whose development started with Tukey [25]. Alternative approaches can be found at different levels of generality in [22, 18, 7].

When passing from the univariate to the multivariate case, the definition of order statistics and quantiles like the median becomes a conceptual obstacle because it is not a priori clear which order relation should replace the ”natural” -relation for real numbers. For this reason, central regions became surrogates for order statistics and quantiles in multivariate statistics. While this was quite successful with respect to characterizing multivariate distributions, it does not really help to answer questions like the following: What are the x% best data points in a cloud of points in ? What is the fraction of them which is better or worse than the median–however the latter is defined? Which data points are in the upper or lower tail of the distribution? The difficulty is that one cannot say which data points are better or worse than others. However, an order relation is often present in applications since decision makers have an understanding which (multi-dimensional) data points are better than others, and they often look for the best alternatives (or the least risky ones etc.). Therefore, new concepts are proposed which start with a vector order for the values of -valued random variables which is not complete in general, i.e., there may exist non-comparable points. The idea is similar to the one in [15], but different types of results are possible due to the convexity properties of expectiles which are not shared by quantiles. In particular, the sublinearity of set-valued expectiles allows a dual representation which also yields a dual description of the expectile region from [9, 6] as a special case. In turn, this leads to new methods for computing cone expectiles, expectile regions and even univariate expectiles for finite data sets which are based on linear programing techniques.

In the next section, cone expectile regions are introduced and basic features established. A dual representation is given in Section 3. This representation opens a straight path to the expectile regions from [9, 6]: it is shown that the cone expectile sets, the expectile region discussed in [6] and families of scalar expectiles all are based on the same dual information. In Section 4, set-valued expectile risk measures are introduced and the differences to the construction in [6] is explained. Section 5 includes the definition of cone expectile rank functions along with their basic properties. Moreover, new order relations for data points and stochastic dominance order random vectors related to expectiles are introduced which can be applied, e.g., in Multi-Criteria Decision Making and for the analysis of ordered data.

2 Definition and basic properties

In this paper, random variables over a probability space are considered. It is assumed that there is a vector preorder for their values present, i.e., a reflexive and transitive relation on , which is compatible with addition and multiplication with non-negative numbers.

Such vector preorders are generated by non-trivial closed convex cones , i.e., via

In particular, furnishes the special case considered in [6]. In this case, points in can only be compared if they are equal which is of course a very poor order relation. The case provides the ”natural” example of component-wise order. On the other end of the spectrum, one can use closed halfspaces which generate complete order relations. A vector order is a vector preorder which is additionally antisymmetric which in turn is the case if , i.e., is pointed.

The presence of such a vector preorder is the feature that sets the developments in this paper apart from earlier contributions like [10, 9, 22, 18, 7, 6] and it also leads to new concepts and perspectives: it might be appropriate to consider the present paper (like [15, 16]) as a contribution to the analysis of ordered data.

The set is called the (positive) dual of the cone (sometimes also the polar cone). As usual, denotes the Banach space of integrable -valued random variables and the component-wise expected value of .

Definition 2.1

Let be an -valued random variable and . The set

| (2.1) |

is called the downward cone -expectile and the set

| (2.2) |

the upward cone -expectile of .

Example 2.2

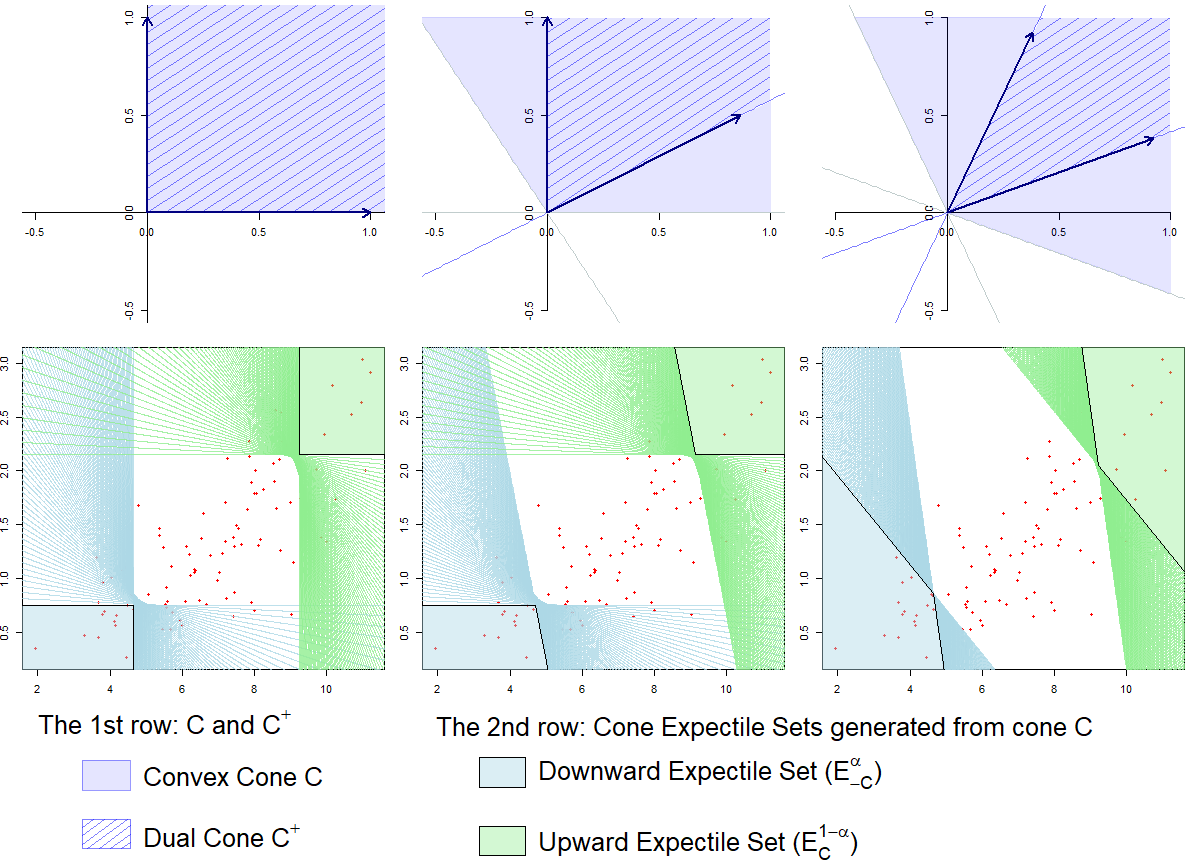

A sample of a bivariate variable simulated from the Gumbel copula in which the two marginal distributions are the normal distribution and the gamma distribution shows the shape of the cone expectiles for different cones . This dataset, plotted as red points in Figure 2.1, will also be used in the later examples.

Figure 2.1 visualizes three different cones along with their duals in (the first row) and how the choice of the cone affects the shape of downward and upward cone expectile sets (the second row).

The computation of univariate sample expectiles for larger data sets in this paper was done in R using the package expectreg [24].

Remark 2.3

A closed convex set is said to be a base of the dual cone if for each there are unique , with . If has a base, then the intersections in (2.1) and (2.2) can be replaced by intersections over since the defining inequalities are positively homogeneous in . The cone has a base if, and only if, has non-empty interior: in this case, the set is a base of where can be chosen arbitrarily.

In the special case and , the dual cone is with base and one has

Another special case is and with dual cone . In this case, it is enough to consider and . One gets as well as . Thus, for and for . This interval is the singleton for . Of course, .

Remark 2.4

One has if . This implies for

as well as

It is an important feature of and that they map into well-defined complete lattices of subsets of , namely into

respectively. It is well-known that and are complete lattices (see [14]). The next results etablish a few elementary properties for the downward cone expectile.

Proposition 2.5

The downward cone -expectiles satisfies:

(1) is a closed convex set with , i.e., ;

(2) If is an invertible -matrix and , then where for a set ;

(3) -a.s. implies ;

(4) It holds for , ;

(5) It holds for , ;

(6) If , then ;

(7) For , one has

Proof. (1) By definition, is an intersection of closed halfspaces and therefore closed and convex. If and , then for all , hence for all which implies .

(2) The set is a closed convex cone with dual (see Lemma A.1 in the Appendix). Now,

where the transformation has been used. On the other hand, the translativity property of univariate expectiles [23, Thm. 1 (iii)], [6, Sect. 2.1, (iii)] gives for all . This implies

for all . Taking the intersection over gives which, together with the linear transformation property, proves (2).

(3) If -a.s., then for all , hence (see [6, p. 3, property (v)]) which in turn implies .

(4) This follows directly from positive homogeneity of the univariate expectiles (see [6, p. 3, property (iv)]).

(5) The function is superadditive for (see [6, p. 3, property (viii)]), hence which in turn implies

for all where the last equality is a consequence of Lemma A.2. Taking the intersection on both sides of the inclusion gives

| (2.3) |

since the intersection of a sum always is a superset of the sum of the intersections.

(6) This is a straightforward consequence of the parameter monotonicity of univariate expectiles: it holds whenever for all (see [4, Proposition 5 (f)], [6, p. 3, property (x)]).

(7) The inclusion is immediate from (6). Assume for all . Then

This implies for all since is a continuous function of the parameter (compare [19, Proposition 1 (ii)]), hence is also true.

Remark 2.6

Properties (4) and (5) mean that the function is positively homogeneous and superadditive for where the order relation in is understood as .

The corresponding result for upward cone -expectiles reads as follows. Its proof runs parallel to the one for Proposition 2.5.

Proposition 2.7

The upward cone -expectiles satisfies:

(1) is a closed convex set with , i.e., ;

(2) If is an invertible -matrix and , then ;

(3) -a.s. implies ;

(4) It holds for , ;

(5) It holds for , ;

(6) If , then .

(7) For , one has

Note that (5) now is subadditivity for the function since the order relation corresponds to in , not .

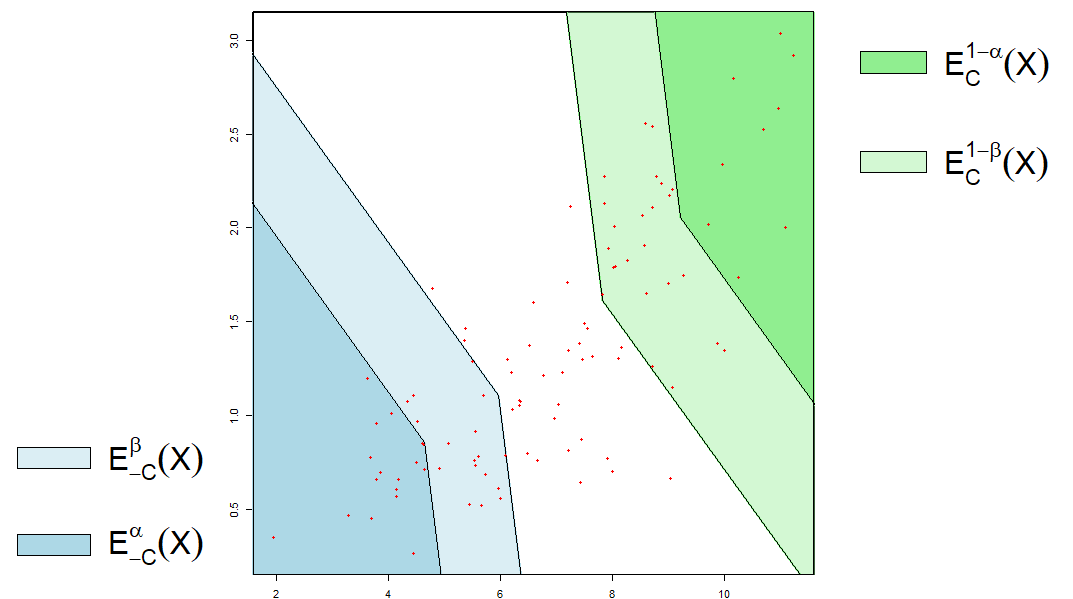

Figure 2.2 provides an example of how the comparison of sets in the complete lattices and works. For the downward cone expectile mapping into , the set is located ”relatively lower” than the set for , i.e., . Therefore, stands for relation in lattice . On the other hand, for the upward cone expectile mapping into the set is located ”relatively lower” than the set , i.e., . In this case, stands for relation in lattice . The cone here is strictly bigger than .

One should also realize that (4) and (5) in Proposition 2.5 are equivalent to the fact that

is a convex cone. Similarly, (4) and (5) in Proposition 2.7 are equivalent to is a convex cone. Compare [14, Def. 4.1, Prop. 4.2] for a more general result of this type which covers the present situation. This cannot be concluded for the expectile region (see below for a definition) from positive homogeneity and (vii) in [6, Sect. 3.1] for which the opposite inclusion in (5) is true. Moreover, while sublinearity in the previous two propositions is quite a natural feature, it turned out to be a serious issue in the geometric expectile approach: compare the involved constructions in [22, Sect 3.2] and [18, Def. 4.4 ff].

The next result is another instance of a feature that is shared by upper/lower expectile sets on the one hand and univariate expectiles on the other hand.

Proposition 2.8

One has

| (2.4) |

Proposition 2.9

The graphs of the two functions and are closed in the product topology on .

Proof. Let be a sequence which converges to . Then for all which is

| (2.5) |

Theorem 10 in [4] gives the Lipschitz continuity of the scalar -expectile for with respect to the Wasserstein distance, i.e., one has for

where and . Thus, is continuous on . This yields the convergence for all . Hence, (2.5) implies

which is . The proof for uses parallel arguments.

This section is concluded with a clarification of the relationship between upward/downward cone expectiles and the expectile region from [9, 6] which is defined as

| (2.6) |

for and . One has if, and only if,

Thus, one also has

which is

In particular, it is always true for any that

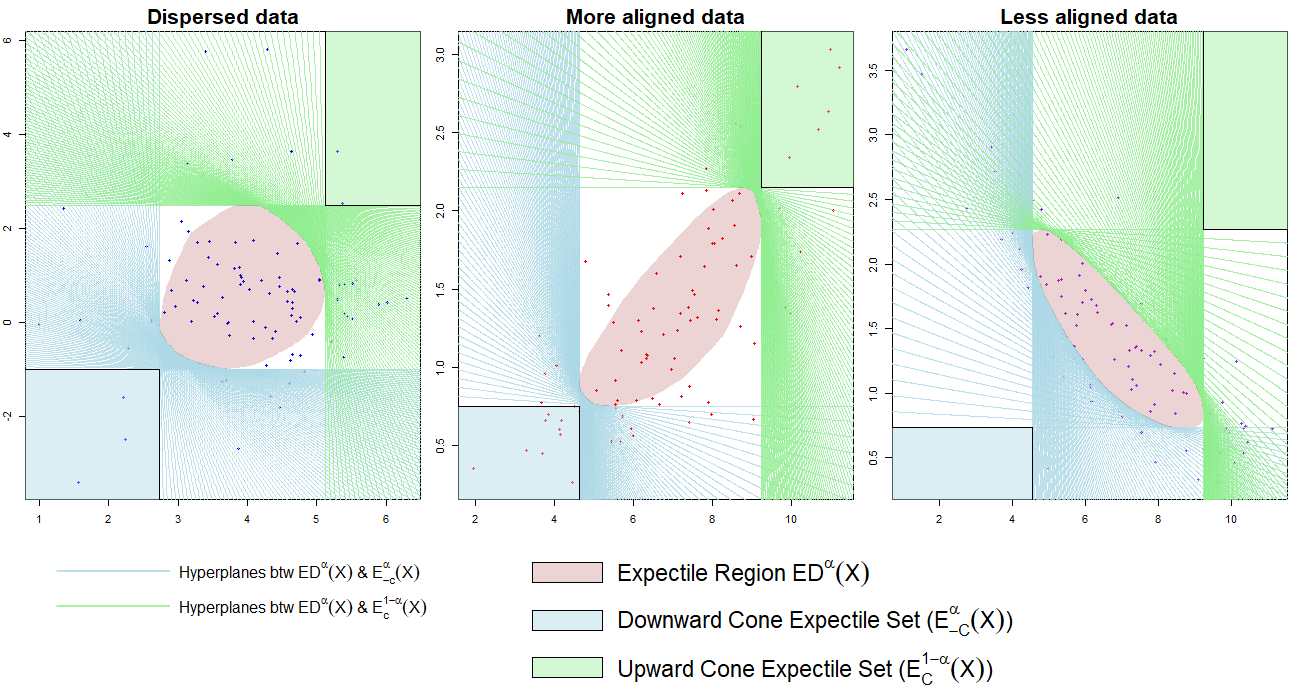

This means that, for , every produces a separating hyperplane for and on the one hand as well as and on the other hand. The subsequent example, complemented by Figure 2.3, exemplifies this idea for various types of bivariate data sets.

Example 2.10

In Figure 2.3, three data samples are shown: the blue points in the left graph are simulated from two independent (univariate) random variables with normal distribution and non-central Student’s t-distribution . The red points in the central graph are the same bivariate data as in Figures 2.1 and 2.2 above (see Example 2.2). The purple points in the right graph are simulated from a rotated bivariate Gumbel Copula with the same parameters as the second one. It might be observed that the three samples can be considered as dispersed and more and less aligned, respectively, with the cone . In all three cases, the expectile region and the upward/downward cone expectiles are distinctly separated by hyperplanes generated from vectors .

From Figure 2.3, it can also be seen that the expectile region captures the central part of the multivariate distribution while downward and upward cone expectiles cover the lower and upper tails of the multivariate distribution, respectively, with respect to the order relation (the latter two may not even include a data point). One might say that the data points in are the ”very bad” points (the lower -expectile tail), the points in the ”very good” ones (the upper -expectile tail); whereas one cannot categorize the remaining points for the given . It should be emphasized that ”good” and ”bad” are understood with maximization in view with respect to the order (vice versa for minimization). When increasing from 0 to 1, the downward cone expectile set moves upward while the upward cone expectile set moves downward.

Both the expectile region and the cone expectiles are set-valued functions of the random variable. Definition 1-2 in [7] shares the same idea of set-valuedness but generalizes it to a family of M-quantiles which are defined as the minimizers of asymmetric loss functions. A different approach in terms of vector-valued expectiles for multivariate random variable can be found in [18] and [22]. Therein, the idea of elicitablility is used to produce (unique) minimizers of certain scoring functions on . While it might seem conceptually easier to consider a single vector as an expectile, this point hardly characterizes the multivariate distribution in a similar way as the scalar -expectile characterizes the univariate distribution because the distribution can be spread out in any direction in the -dimensional space.

In the quoted references, an ordering cone for the values of the random variable is not considered which also leads to conceptual difficulties, for example, with respect to sublinearity as already discussed above (after Proposition 2.7). For this reason, cone expectiles together with the expectile region seem more appropriate since they can characterize the central as well as the tail behaviour with respect to a given vector order of a multivariate distribution.

3 Dual Representation of Set-Valued Expectiles

In this section, dual representation results are given for set-valued expectiles with . The univariate dual representation result from [4, Proposition 8] is used to represent set-valued expectiles as set-valued lower and upper expectations as discussed in [12].

Theorem 3.1

Let . Then

where with and one has

as well as

Proof. The first two formulas follow from [4, Proposition 8] with a straighforward transformation of - density functions into probability measures . The formulas for and are now consequences of the definitions.

Remark 3.2

For fixed , , the function

is an upper -expectation as defined in [12, Sect. 4.7] since, of course, holds true where is understood as the component-wise expectation of with respect to . The previous theorem establishes that the upward cone expectile is a set-valued upper expectation (and the corresponding downward cone expectile is a set-valued lower expectation). This again is a very striking parallelity to the univariate case in [4, Proposition 8].

The dual representations ask for the infimum and supremum of the linear function over the set

| (3.1) |

This raises the question what shape this set has and where it can be found. The following example provides experimental evidence.

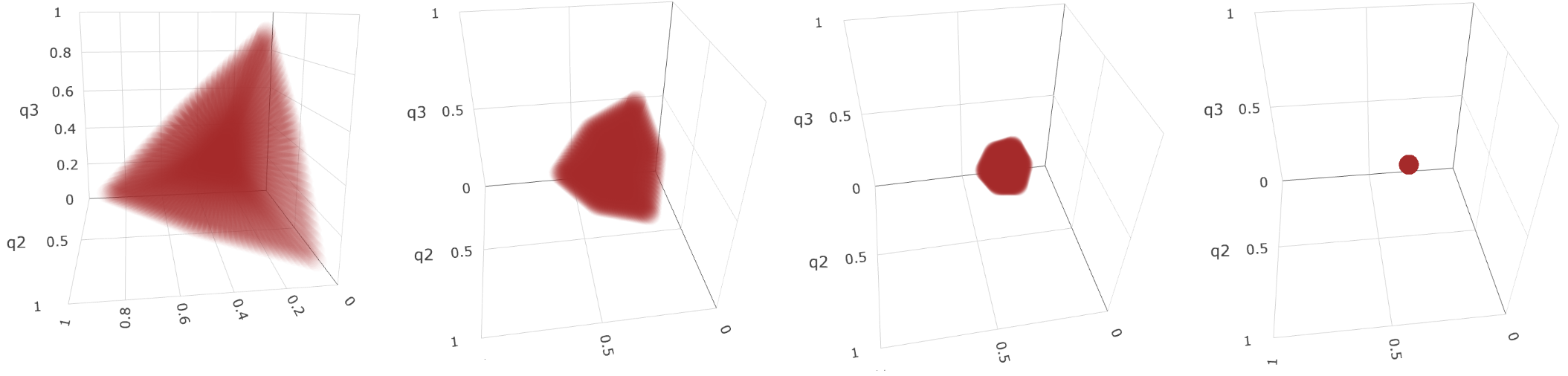

Example 3.3

Let , , . This gives

for . If , then which is the case considered in this example.

Figure 3.1 shows how the set of scenarios looks for four different ’s (). In each case, the shape of the set is filled by 10,000 (maroon) points which will be used for computing the dual representations.

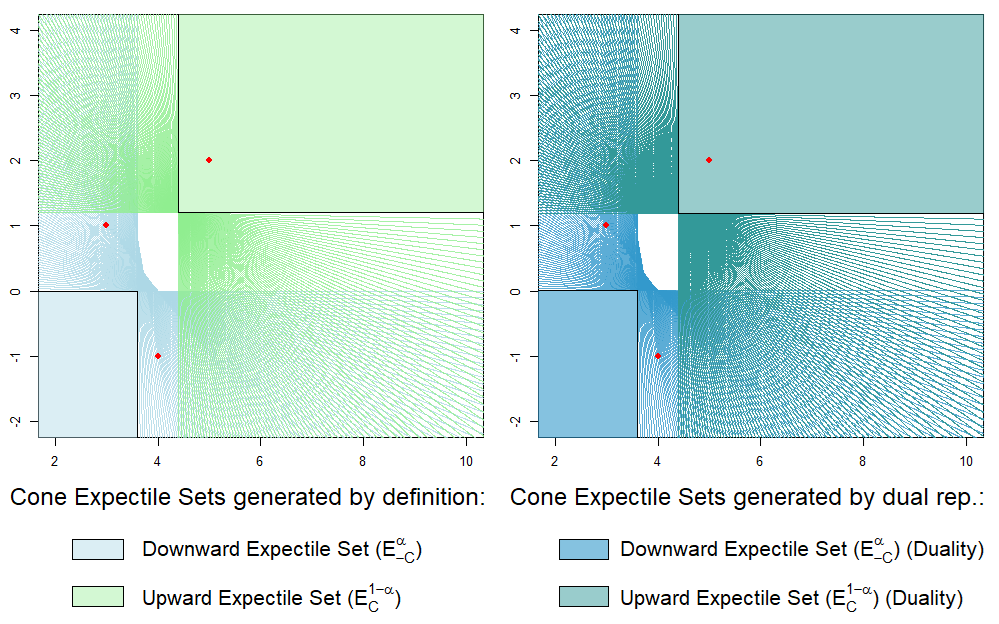

A discrete random variable is given by: . The computations in this simple example are done by brutal force for a fixed . The 10,000 sample points in the set are used to compute the dual representation of the cone expectile sets as per Theorem 3.1. Figure 3.2 depicts the downward and upward cone expectile sets for 3 datapoints which are computed both from the definitions via (2.1), (2.2) (the far left graph), and from the dual representation in Theorem 3.1 (the far right graph). As expected, the definition and the dual representation give the same result.

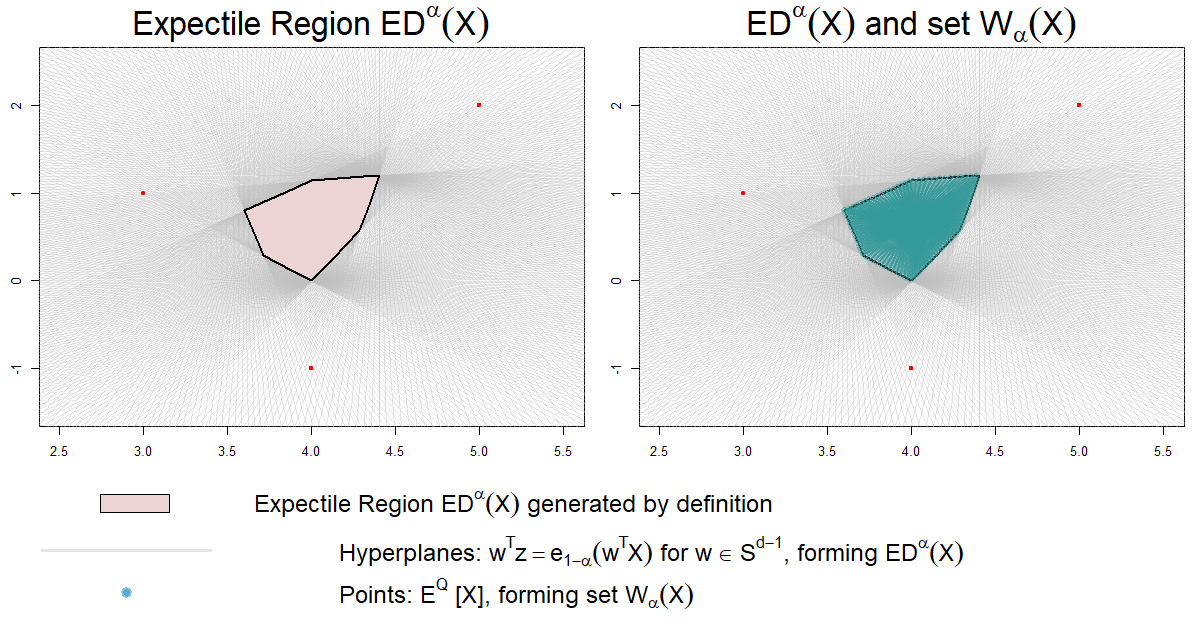

The set is computed in a similar way: for each probability measure (each maroon point in Figure 3.1, the second graph from left), is computed. Then 10,000 points of are plotted on the same plot of expectile region (the blue points in Figure 3.3). These blue points perfectly fill up the shape of the expectile region defined in [9, 6] (or in (2.6) above).

As suggested by Example 3.3, especially Figure 3.3, the following theorem establishes the coincidence of the set with the expectile depth region defined in [9, 6].

Theorem 3.4

For , one has

Proof. By definition,

The dual representation of provides

Now, the function

is the support function of the set . According to a basic duality theorem (see [1, 5.83 Corollary]) one has

since is closed and convex (and compact).

The previous theorem shows that the knowledge of the set admits to reconstruct not only , , but also . This is a dual way of constructing the expectile regions from [6] which also opens a path to use linear programming techniques for computing sample expectiles. Moreover, the set is independent of and while depends on but still not on . This can be seen as structuring the modelling process: if one chooses to use expectiles at some level , one gets set of probability measures from the dual representation. Then, combined with the ”pure” data , one gets –the analyst/decision maker is only interested in the shape of the distribution. Finally, if the analyst/decision maker has a preference for the data points, the cone enters the picture and one can additionally filter out the ”(very) good” and the ”(very) bad” data points with respect to the order .

In [6, Sec. 5], an algorithm for computing the bivariate expectile region is proposed. However, it remains a challenge to compute expectile regions and lower/upper cone expectile sets for dimensions . A general methodology is indicated in the following which draws on the dual representations in Theorem 3.1 and 3.4. More specific and also more effective algorithms will be discussed elsewhere.

The main difficulty when computing expectile regions in for is to sample the vectors in all directions of the unit sphere . This could be overcome by using the dual representation of the expectile region given in (3.1) and Theorem 3.4 in case of finitely many data points, e.g., a sample of a distribution. In this case, will be a polytope in which is–through the dual representation–the projection of another one in where is the number of data points. This means it would be sufficient to compute the vertices of . The following result makes this idea more precise.

Proposition 3.5

Let be a finite set. Then can be identified with a polytope which is a subset of the simplex .

If is a random variable, then is a polytope. Moreover, if is a vertex of , then there is a vertex of such that .

Proof. The identification via for together with the fact that in the finite probability space setting the set is defined by a finite set of linear equations and inequalities verifies the first claim.

Next, assume is a vertex of and is not a vertex of . Then can be written as a convex combination of some elements which are vertices of , i.e., with and . One obtains . Since is a vertex of , this implies , and each of the ’s yields the vertex .

The brutal force idea would be to compute the vertices of in , i.e., get a so called vertex representation, and then use it to compute the vertices of . This is, however, not very efficient since , i.e., the number of data points, is usually much larger than the dimension . Therefore, it might be better to understand the representation as a polyhedral projection problem and solve it either directly or as an equivalent multi-criteria linear programming problem. Efficient algorithms are available for such problems [21, 26].

For cone expectile sets with , the direct computation from Definition 2.1 might be feasible since sampling is no longer an issue if is polyhedral cone. The next theorem gives the key idea.

Theorem 3.6

If is a polyhedral convex cone generated by , i.e., , then one has

for . A parallel formula holds for the downward cone expectile set .

Proof. See Appendix B..

Theorem 3.6 states that, in the polyhedral case, cone expectile sets can be represented by intersections over a finite number of halfspaces instead of the infinitely many generated by all vectors . Therefore, the computation of cone expectile sets is simplified if the preference of the decision maker is given by a polyhedral cone .

4 Expectile risk measures for multivariate positions

In [3], properties of the expectile risk measure defined by

are studied; especially, this risk measure is monotone, cash additive and sublinear for . Moreover, it is known that it is the only coherent risk measure among those which can be written as generalized quantiles [4]. The corresponding result for set-valued expectile risk measure reads as follows. Compare [12, Definition 6] and [14, Definition 7.6] for the definition of set-valued risk measures.

Theorem 4.1

If , then the function defined by with is a sublinear set-valued risk measure, i.e.,

(1) (finiteness at zero),

(2) for all , for all (translativity),

(3) -a.s. implies (monotonicity),

(4) for all (positive homogeneity),

(5) (subadditivity).

(6) has values in and is closed in the product topology.

Proof. One has

(1) since . (2) follows from Proposition 2.5 with the unit matrix. (3)-(5) also follow from Proposition 2.5, (3)-(5). (6) follows from Proposition 2.5 (1) and Proposition 2.9.

The elements of are those deterministic portfolios which can be used as compensation for the risk of at initial time. The assumption ensures in particular that one can add a non-negative portfolio to one that is already risk compensating and still get a risk compensating portfolio. Moreover, (3) applies in particular if -a.s.

For a univariate , one has for . This implies

for the multivariate case. This means that provides the most optimistic risk measure, whereas smaller means more risk aversity since there are potentially less options to compensate the risk. Note that this is right the opposite of the nesting property for expectile (and other depth) regions as stated in [6, Sect. 3.1, (ii)]. Moreover, this also shows that the set is not appropriate as collection of risk compensating portfolios as implied in [6, Sect. 3.1]: it always includes which already in the univariate case is not an appropriate risk compensating quantity. Moreover, the monotonicity property for the expectile region, namely -a.s. implies , would mean that there are less risk compensating portfolios available for the more risky compared to . The same point can be raised for the subadditivity property of expectile regions in [6, Sect. 3.1 (vii)]: it would actually punish diversification. Overall, cannot be considered as an appropriate risk measure, but can which is also a direct generalization of the univariate expectile risk measure.

Finally note that the cone can be understood as a solvency cone at initial time (see Section 2), which also justifies the assumption . It is an obvious question how such a cone (or even more general market models) can be taken into account. General procedures for this can be found in [13, 12]. For expectile risk measures, this will be discussed elsewhere.

The dual representation of the expectile risk measure is an immediate corollary of Theorem 3.1.

Corollary 4.2

For and , one has

Proof. This is a direct consequence of Theorem 3.1 and the definition of .

5 Cone expectile rank functions

Depth functions in multivariate statistics were invented with the idea of centrality: they quantify how close a given point is to the center of the distribution which in turn can be a single point or a (closed convex) set of points, the (most) central region. However, if one understands points as ”good” if they dominate many other points with respect to the order generated by a cone and as ”bad” if they are dominated by many other points, then ”centrality” basically means ”average behaviour” which corresponds to the fact that the expected value is an element of all expectile regions in the sense of [6].

Decision makers are usually not interested in average alternatives, but in ”really good” ones with respect to their preferences where ”good” depends on the goal (maximization or minimization). In such situations, centrality concepts and depth functions are of little use and should be complemented by functions which are monotone increasing with respect to the underlying order . The following definition provides such functions generated by cone expectile sets. They relate to cone expectiles like the expectile depth function in [6, Sect. 4] relates to expectile regions [6, Sect. 3].

Definition 5.1

The functions defined by

are called downward and upward expectile rank function generated by , respectively.

For and , one has which is a direct consequence of Definition 5.1. Here, is the inverse expectile function (see [6, Sec. 2.1]).

Figure 5.1 shows an example of how to spot the downward and upward expectile ranks of a point in generated by for . The downward expectile rank of the ”red” point is and its upward expectile rank is .

The next result characterizes the cone expectile sets as the sublevel and superlevel sets of the downward and upward expectile rank function, respectively.

Theorem 5.2

One has for

Proof. If , then clearly . Vice versa, assume . The definition of the infimum and the monotonicity of the expectile set as in Proposition 2.5 (6) imply for all with . Hence, by Proposition 2.5 (7). The proof for runs parallel using Proposition 2.7 (6), (7).

With the previous result, the first part of the next theorem is immediate.

Theorem 5.3

The expectile ranking functions satisfy:

(1) is lower semicontinuous and quasiconvex, is upper semicontinuous and quasiconcave,

(2) if is an invertible -matrix and , then and for all and all ,

(3) , imply and for all ,

(4) , a.s. imply and for all .

Proof. (1) Extended real-valued functions are lower (upper) semicontinuous if, and only if, all of their sublevel (superlevel) sets are closed, and they are quasiconvex (quasiconcave) if, and only if, all of their sublevel (superlevel) sets are convex. The result follows from Theorem 5.2 and Proposition 2.5 (1), Proposition 2.7 (1).

(2) One has . The result follows from Proposition 2.5 (2) which gives . A parallel argument using Proposition 2.7 (2) works for .

(3) The inequality means . If , then where the last equation is from Proposition 2.5 (1). The definition of gives the result. The inequality for follows similarly with the help of Proposition 2.7 (1).

Note that the monotonicity of the expectile ranking functions with respect to the -variable relies on the image space property of , whereas the monotonicity with respect to the random variable is a consequence of the corresponding monotonicity of the univariate expectiles.

The expectile depth function in [6, Sec. 4] corresponds to the expectile region and is defined as a supremum since shrinks with increasing and thus is a measure of centrality. On the other hand, and ”move outward” with decreasing and increasing in the direction of and , respectively. Thus, a low value of means that the point is a ”bad” one while a high value of means that is a ”good” one if maximality with respect to is the goal (vice versa for minimality). Thus, , can be understood as measures for outstandingness in the direction of and , respectively. Rather than centrality, the expectile rank functions provide information about the tail behavior of the distribution where ”tail” is understood in the direction of and , respectively. Therefore, the term ”outstandingness” is preferred here over ”outlyingness” since the latter does not refer to any order relation for the data points, but is commonly used as the opposite to ”central,” i.e., being away from the center.

It might be noted that the affine equivariance property [6, Sec. 4.1 (i)] is not convincing since it would imply for all , (choose the zero matrix and the zero vector ) which was certainly not the intention of the authors of [6]. Therefore, Theorem 5.3 (2) as well as Proposition 2.5 and 2.7 assume invertible matrices . In particular, Lemma A.1 in the Appendix does not work without this assumption.

The following proposition establishes that the downward and the upward expectile rank of a point generated by and generated by sum up to 1 (and hence it is enough to know one of the two as in Proposition 2.8 for expectile sets). This shows that the expectile rank functions behave similar to the cumulative distribution function and the survival function of a univariate distribution.

Proposition 5.4

For any and , one has

One can define order relations on using the expectile rank functions as follows:

Both and are reflexive, transitive and complete since each is defined via one real-valued function. Figure 5.1 shows that neither one is antisymmetric in general. Moreover, the monotonicity properties in Theorem 5.3 (3) ensure that implies as well as . However, the example depicted in Figure 5.1 shows that both of the above relations do not coincide with in general; they both are complete extensions of the vector preoder and thus may serve as (scalarizing) tools in Multi-Criteria Decision Making in the same way as the lower and upper cone distribution function from [15]: see [17]. Moreover, even the intersection of and does not coincide with in general: the pair in Figure 5.1 satisfies as well as (the ”orange” and the ”red” have the same downward and upward expectile rank), but is not comparable with respect to .

On the other hand, belongs to the symmetric part of as well as that of and thus, a decision maker might consider them as equivalent and not prefer one over the other. This motivates the following definition.

Definition 5.5

The equivalence relations defined by

are called lower and upper expectile rank indifference relation, respectively, with respect to the random variable and the cone . Their intersection

is called expectile rank indifference relation (generated by and ).

Thus, are lower expectile rank indifferent if and and parallel for . Finally, a case is pointed out in which one can draw a conclusion about the comparability of with respect to from the knowledge of , .

Theorem 5.6

Let and satisfy . Then if, and only if, and .

Proof. ”:” This is the monotonicity of the expectile rank functions given in Theorem 5.3 (3) which is true without the additional assumption. ”:” Assume

and hence by assumption. Then and Theorem 5.2 yields . Thus

On the other hand, implies , hence . Thus

Together, this yields for all which means according to the bipolar theorem.

Figure 5.1 provides a counterexample for the remaining case: one has and , thus and the two points are not comparable with respect to .

This section is concluded with a link between new multivariate stochastic orders and expectile rank functions.

Definition 5.7

For two random variables two order relations are defined by

The relation is called lower expectile order, the relation upper expectile order.

One may check that in the special case , both and collapse to the expectile order defined in [5, Def. 6]. In [5, Thm. 8], it is shown that an be characterized through Omega ratios at least for random variables. Instead, the expectile rank functions are used here.

Theorem 5.8

One has

Proof. First, take and assume for all . Then, only two cases are possible:

(i) for all with ; in this case ,

(ii) there exist with ; in this case .

This proves ”” for .

Conversely, fix and take . Theorem 5.2 yields . By assumption, again by Theorem 5.2, hence as desired.

The proof for uses parallel arguments.

6 Conclusion and perspective

In this paper, downward and upward cone expectiles are introduced as set-valued function which capture the tail behavior of a multivariate distribution with respect to an order relation generated by a convex cone instead of its centrality. The cone expectile functions are defined in such a way that they share most of the attractive properties of univariate expectiles such that monotonicity and sublinearity: this is possible since they map into well-defined complete lattices of sets generated by the ordering cone.

As a result, they also facilitate the contruction of coherent set-valued expectile risk measures which captures the idea of risk compensation much better than the expectile region. The incorporation of makret models as in [13] would be the natural next step.

The dual information shared by both cone expectiles in the present paper and the expectile region from [9, 6] opens dual options for computing these sets. The design of efficient algorithms along with convergence properties as well as questions of the asymptotic behaviour of cone expectiles remains a task.

The new downward and upward expectile rank functions correspond to the lower and upper expectile in the same way as the univariate cumulative distribution function corresponds to the quantile function. They admit to quantify the ”outstandingness” of a (data) point with respect to a multivariate distribution.

The new upper and lower cone expectiles as well as the corresponding rank functions can be applied to the analysis of ordered data and especially to the ranking problem in Multi-Criteria Decision Making.

References

- [1] Aliprantis CD, Border KC, Infinite Dimensional Analysis, Springer Publishers, 3rd edition 2006

- [2] Artzner P, Delbaen F, Eber JM, Heath D, Coherent measures of risk, Mathematical Finance 9(3), 203-228, 1999

- [3] Bellini F, Di Bernardino E, Risk management with expectiles, The European Journal of Finance 23(6), 487-506, 2017

- [4] Bellini F, Klar B, Müller A, Rosazza Gianin E, Generalized quantiles as risk measures, Insurance: Mathematics and Economics 54, 41-48, 2014

- [5] Bellini F, Klar B, Müller A, Expectiles, Omega ratios and stochastic ordering, Methodology and Computing in Applied Probability 20, 855-873, 2018

- [6] Cascos I, Ochoa M, Expectile depth: Theory and computation for bivariate data sets, J. Multivar. Anal. 184, 2021

- [7] Daouia A, Paindaveine D, Multivariate Expectiles, Expectile Depth and Multiple-Output Expectile Regression, TSE Working Paper, n. 19-1022, July 2019, revised February 2023

- [8] De Rossi G, Harvey A, Quantiles, expectiles and splines, J. Econometrics, 152(2), 179-185, 2009

- [9] DiGiorgi E, McNeil AJ, On the computation of multivariate scenario sets for the sket-t and generalized hyperbolic families, Comp. Statistics & Data Anal. 100, 205-220, 2016

- [10] Eilers PHC, Expectile contours and data depth, Proc. 25th Intern. Workshop on Statistical Modelling, 167-172, 2010

- [11] Eilers PHC, Discussion: The beauty of expectiles, Statistical Modelling 13(4), 317-322, 2013

- [12] Hamel AH, Heyde F, Set-valued T-translative functions and their applications in finance, Mathematics 9(18), 2021

- [13] Hamel AH, Heyde F, Rudloff B, Set-valued risk measures for conical market models, Math. Financial Economics 5, 1-28, 2011

- [14] Hamel AH, Heyde F, Löhne A, Rudloff B, Schrage C, Set optimization–a rather short introduction, In: AH Hamel, F Heyde, A Löhne, B Rudloff, C Schrage (eds.), Set Optimization and Applications–the State of the Art. From Set Relations to Set-Valued Risk Measures. Springer Science and Business Media, Berlin, pp. 65-141, 2015

- [15] Hamel AH, Kostner D, Cone distribution functions and quantiles for multivariate random variables, J. Multivar. Anal. 167, 97-113, 2018

- [16] Hamel AH, Kostner D, Computation of quantile sets for bivariate ordered data, Computational Statistics & Data Analysis 169, 107422, 2022

- [17] Hamel AH, Kostner D, Cone Ranking for Multi-Criteria Decision Making, arXiv preprint arXiv:2312.03006, 2023

- [18] Herrmann K, Hofert M, Mailhot M, Multivariate geometric expectiles, Scandinavian Actuarial J. 7, 629-659, 2018

- [19] Holzmann H, Klar B, Expectile asymptotics, Electronic J. Statistics 10, 2355-2371, 2016

- [20] Huber PJ, Robust Statistics, John Wiley & Sons, New York 1981

- [21] Löhne A, Weißing B, Equivalence between polyhedral projection, multiple objective linear programming and vector linear programming, Math. Meth. Oper. Res. 84, 411-426, 2016

- [22] Maume-Deschamps V, Rullière D, Said K, Multivariate extensions of expectiles risk measures, Dependence Modeling 5(1), 20-44, 2017

- [23] Newey W, Powell J, Asymmetric least square estimation and testing, Econometrica 55, 819-847, 1987

- [24] Sobotka F, Schnabel S, Waltrup LS, Eilers PHC, Kauermann G, expectreg: Expectile and quantile regression, 2014, https://github.com/cran/expectreg.git, Github read-only mirror of the CRAN R package repository.

- [25] Tukey JW, Mathematics and the picturing of data. In: Proceedings of the International Congress of Mathematicians 2, 523-531, 1975

- [26] Weißing B, The polyhedral projection problem, Math. Meth. Oper. Res. 91, 55-72, 2020

- [27] Zaevski TS, Nedeltchev DC, From BASEL III to BASEL IV and beyond: Expected shortfall and expectile risk measures, Intern. Review of Financial Analysis 87, 102645, 2023

Appendix

A. Lemmas

Lemma A.1

Let be a nontrivial closed convex cone and an invertible -matrix. Then is a closed convex cone with .

Proof. It is straighforward to check that is a closed convex cone. One has

which completes the proof.

Lemma A.2

If and , then

where the addition is understood as element-wise (Minkowski) addition of subsets of .

Proof. Since , there are with and . Then

and the parallel equation is true for . Indeed, if with , then , i.e., belongs to the left hand side. If , then with , i.e., , and therefore, belongs to the right hand side.

B. Proof of Theorem 3.6

The proof is given for the downward cone expectile . The proof for follows similar lines. Define the set

Clearly, , so the opposite inclusion needs to be verified. Since the set generates , every can be represented as with numbers . Since , the univariate expectiles are super-additive and positively homogeneous which yields

In turn, this leads to

| (6.1) |

If one has for all . Therefore,

which gives and consequently

| (6.2) |

The two inclusions (6.1) and (6.2) give

| (6.3) |

Since (6.3) holds for all , one can take the intersection over and obtains which completes the proof.