Least-Cost Structuring of 24/7 Carbon-Free Electricity Procurements ††thanks: Work partially supported by ARPA-E PERFORM grant DE-AR0001289.

Abstract

We consider the construction of renewable portfolios targeting specified carbon-free (CFE) hourly performance scores. We work in a probabilistic framework that uses a collection of simulation scenarios and imposes probability constraints on achieving the desired CFE score. In our approach there is a fixed set of available CFE generators and a given load customer who seeks to minimize annual procurement costs. We illustrate results using a realistic dataset of jointly calibrated solar and wind assets, and compare different approaches to handling multiple loads.

Index Terms:

CFE score, portfolio optimization, renewable energy scenarios, hourly matching of load profilesI Introduction

We consider the problem of matching a given load profile with a portfolio of renewable generators to achieve a desired 24/7 CFE score. This has become a topical task for many large industrial users, especially data centers and tech companies, who seek auditable (via e.g. ISO settlement hourly reports or renewable energy credit accounts) commitment to reducing their carbon footprint. Corporate customers with the appetite to “do the right thing” procure carbon-free energy sources on a purchasing power agreement (PPA) basis and evaluate their hourly CFE metric, i.e. the ratio of total load to purchased CFE. Crucially, unused CFE does not contribute, while unmatched load is penalized linearly. The goal is then to hit a desired annual target. Due to inherent intermittency, such hourly matching is an essential but technically challenging step to achieving 100% decarbonization [1, 2].

Our work is inspired by the latest generation of probabilistic models for large-scale simulation of renewable electricity generation [3] which provide the critical underpinning for a proper statistical framing of the CFE target problem. These stochastic models of the short term joint behavior of load and renewable production were modified to produce realistic long-term (multi-year) simulations. As a consequence the results here are fundamentally probabilistic in contrast to so-called “8760” analysis of expected volumes which by construction cannot yield distributional results and are, therefore, blunt instruments in transaction structuring. This simulation methodology has been used to structure 24/7 CFE transactions for large data center portfolios in PJM, NYISO and ISONE regions (see [4]).

The structures discussed here are useful for supporting the continued expansion of the renewable generation footprint, providing enhanced revenue streams to those with the foresight and investment appetite to build existing generation, while simultaneously incentivizing new builds with the prospect of enhanced profitability. Two white papers from Google [5, 6] outline potential ways to scaling this market.

Due to the nonlinearity introduced by the capped ratio, probabilistic modeling (including the realistic representation of correlation within the CFE portfolio) is essential. We view the problem at an annual ( = 365 x 24 hours) scale, with hourly matching. The CFE score is taken as a constraint, with the objective of minimizing generation cost.

To handle the intrinsic stochasticity, we work with a collection of scenarios, jointly simulated across loads and generators. These scenarios represent potential fluctuations that render the realized CFE score a random variable. In line with this, we interpret the CFE target probabilistically, so that it must hold for a given (large) fraction of the scenarios.

Our contributions are two-fold: (1) we provide a mathematical framework of optimization with probabilistic constraints for CFE structuring, highlighting the role of the two primary parameters of CFE target and guarantee level; (2) we present two realistic case studies where the underlying scenarios are fully probabilistically coupled and calibrated to a realistic renewable assets. As complement to this article, we provide an interactive online dashboard [7] where the users can themselves explore CFE portfolio characteristics.

II Methodology

We consider a collection of renewable energy assets which we structure into a fixed portfolio with the goal of minimizing the respective energy procurement cost, while guaranteeing that a target CFE score is achieved with a given probability based on a finite set of scenarios.

| Notation Used | |

| : | number of assets (energy sources), |

| : | number of scenarios, indexed by |

| : | number of time periods indexed by |

| : | amount of energy (MW) generated by source in hour . is the -th scenario of |

| : | Load (MW) in hour with scenarios |

| : | CFE target score, |

| : | CFE quantile guarantee level, |

| : | fraction of source procured for the portfolio |

| : | set of feasible portfolio allocations |

| : | cost of energy () from source |

| : | constructed CFE portfolio |

Using the notation below, our problem is translated into building a static portfolio representing an annual PPA that procures throughout the year. Let be the hourly CFE fraction, with the cap indicating that over-generation is not transferable across time. The PPA structure should cover most of the load across hours and achieve a CFE score target of (e.g. , meaning that 95% of the load must be matched with the CFE generators) with a probability of , meaning that the quantile of the CFE score across all scenarios must be higher than . Costs are assessed per MW of energy delivered, which is a random quantity. Our goal is to minimize the expected PPA cost, . This is equivalent to minimizing the average hourly cost where

represents the average generation for asset across all scenarios and time steps .

Note: the vector of the weights is a vector of size , is a 3-d tensor, and is a matrix.

III The optimization framework

The mathematical formulation of the CFE structuring problem is as follows:

| (1a) | |||

| (1b) |

where is the random variable denoting the annual CFE score and is the hourly CFE ratio, reflecting the fraction of load matched, capped at unity.

Remark 1

Our framework is similar to the portfolio management problem in which a manager maximizes expected returns with a quantile constraint guaranteeing that the portfolio return will be above a certain threshold with a given probability level. However unlike that analogue, we face a temporal dimension where surplus energy in one period cannot be utilized to compensate for energy deficits in other periods.

Almost sure constraints are straightforward to handle, since they correspond to separate piecewise-linear constraints . However, in the probabilistic setting with a continuum of potential scenarios, achieving the target in all possible outcomes is not meaningful. Practitioners have thus also considered the average-case constraint which however does not give any control on the distribution of . Our goal is to span this gap by taking . In tandem, allowing a fraction of the scenarios to breach the target lowers the cost, providing another tuning knob for portfolio structuring. Such probabilistic constraints are in general not solvable exactly; for example taking our prototypical case of scenarios and , we require that the CFE target score would be achieved in at least 950 out of the 1000 scenarios. This in principle requires to search over all potential subsets of size 950 and finding the minimal cost for each such subset to achieve .

Such “robust” optimization framework can be solved using mixed-integer programming (MIP)[8]. The idea would be to introduce binary variables to model whether a particular scenario meets the procurement constraint, translating to for auxiliary binary variables, . The introduction of a large number of auxiliary variables significantly increases the computational complexity, leading to very long solution times. The approach we propose considers the constraint in (1b) directly as a black-box, non-convex function of the weight vector . We observe that it is in fact piecewise linear from an hour-by-hour and scenario-by-scenario perspective, for a total of at most pieces. Arguing by the Law of Large Numbers that is approximately Gaussian, one can approximate its quantile by , where and are the estimates of

and is the standard Gaussian CDF. The problem is then reduced to:

| (2) | ||||

| s.t. |

This problem can be linearized and solved by means of linear programming techniques. Following this linearization idea, we consider the constraint as a function of the weights , i.e.,

and use the Sequential Least Squares Programming (SLSQP) algorithm to deal with the constrained minimization problem in (2) The SLSQP algorithm, first proposed by [9, 10], is widely used to solve nonlinear least-squares problems. The algorithm works by iteratively solving a sequence of quadratic programming subproblems. At each iteration, a quadratic approximation of the Lagrangian function is constructed around the current iterate. This quadratic approximation is then minimized subject to the constraints and is used to generate a new iterate. The SLSQP algorithm can be summarized as follows (see [11] for more details):

-

1

Initialize the iterate .

-

2

For

-

a

Construct a quadratic approximation of the Lagrangian function around , .

-

b

Solve the quadratic subproblem given by

to obtain a search direction .

-

c

Update the iterate: where is a step size.

-

a

In step 2.a, the gradient and Hessian at are approximated via finite difference schemes. The algorithm stops whenever or the new iterate does not satisfy the constraints. The step size is selected via a line search according to Wolfe’s condition [12]. To address the potential convergence of the SLSQP algorithm to a local minimum of the objective function, we initialize as the solution to the approximate problem in (2).

IV Illustrative Case Study I

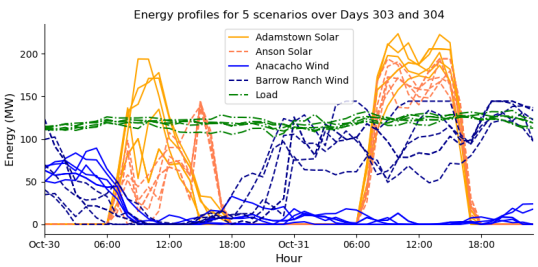

Our first case study features 2 solar assets (Adamstown and Anson), 2 wind assets (Anacacho and Barrow Ranch) and a hydro asset, taken to be fully deterministic. The underlying data and asset names refer to the ERCOT region and the ARPA-E PERFORM Dataset [13]. Figure 1 shows 5 representative scenarios on 2 consecutive representative days for this collection of 4 renewable assets and the desired load. We emphasize that all simulations are fully coupled. The basic structure of high levels of solar CFE production during mid-day and with wind production predominantly at night shows that matching to a much less volatile load is quite challenging. Table I shows that the 2 Solar assets are highly correlated, while the 2 Wind assets are only moderately correlated. As is common, there is a positive dependence between Load and Solar, but a negative one between Load/Solar and Wind generation. These features can be observed in Figure 1 where Barrow Ranch generation is high on Oct 31 (hitting its max capacity around midnight), while Anacacho is barely producing; in contrast there is a strong correlation between Adamstown and Anson.

| Adam. | Anson | Anac. | BaRa | Load | |

|---|---|---|---|---|---|

| Adamstown Solar | 1.00 | 0.91 | -0.38 | -0.39 | 0.15 |

| Anson Solar | 0.91 | 1.00 | -0.40 | -0.40 | 0.15 |

| Anacacho Wind | -0.38 | -0.40 | 1.00 | 0.43 | -0.18 |

| BarrowRanch Wind | -0.39 | -0.40 | 0.43 | 1.00 | -0.22 |

| Load | 0.15 | 0.15 | -0.18 | -0.22 | 1.00 |

| Asset | Capacity | Ave Gen | Cost/MW | |

|---|---|---|---|---|

| Adamstown Solar | 250.0 | 67.6 | 30 | 0.228 |

| Anson Solar | 200.0 | 61.6 | 30 | 0.419 |

| Anacacho Wind | 89.3 | 25.9 | 50 | 1.000 |

| Barrow Ranch Wind | 144.3 | 51.5 | 60 | 0.725 |

| Hydro | 123.7 | 97.8 | 102 | 0.383 |

After optimizing for at -level, we get the portfolio weight vector listed in Table II. Note that the unit costs here were designed to bear some resemblance to the ERCOT marketplace; elsewhere solar RECs are substantially premium, with hydro the least expensive. Our discussion is agnostic to variations in the cost stack used. Observe that Anacacho is fully used, illustrating the common feature that some of the optimal weights bind to the constraints , due to either an asset being not competitive and not getting picked at all, or it being scarce and hence fully procured . The resulting procurement cost per MW of Load is . This is significantly higher than the costs in Table II due to overgeneration: the constructed least-cost portfolio on average procures 125.3% of Load.

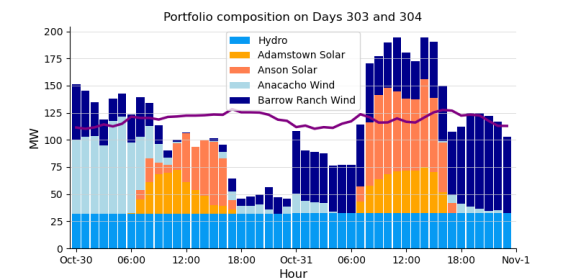

Figure 2 shows the realized generation on the same 2 days based on the above . We observe that in that specific scenario and time period, the constructed portfolio overproduces by up to 70% (see 11am on Oct 31), however it has significant shortfall on the evening of the first day when there is no solar produciton and very little wind.

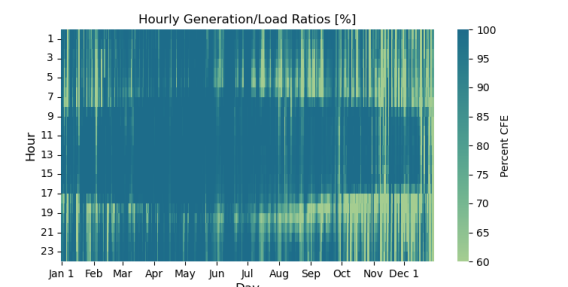

Figure 3 displays the hourly average CFE scores across the entire year. By construction, the time-averaged CFE score is 90% . The reliance on solar energy is clear, as the CFE score is close to 1 between 9-3pm and then is consistently below 0.9 in the late evening.

Stronger CFE targets, i.e. higher are more costly, and so is the higher level of guarantee . Table III shows how these 2 input variables drive the cost. We observe that the guarantee level plays a mild role (less than 0.5% additional cost) in portfolio cost, while costs increase exponentially as CFE target . In the given setting, the maximum achievable average CFE target is 99.34%, so that in most scenarios, even if procuring all available CFE sources, there are hours where load is not fully covered.

IV-1 Marginal Cost of Load

Another way to explore the portfolio construction is to consider the marginal portfolio, i.e. which assets are used to match the next bit of additional load. This is captured by comparing the portfolios when an infinitesimal amount of additional load is added (multiplicatively, to reflect the non-constant temporal profile). In the case study, a marginal increase in load when is met with the marginal showing that at the margin it is mostly Anson Solar and BarrowRanch being used (Anacacho already being completely utilized, see Table II). In contrast, when the marginal portfolio is shifting more into Hydro being the main marginal source of additional generation due to stricter CFE targets.

IV-2 Effect of Diversification

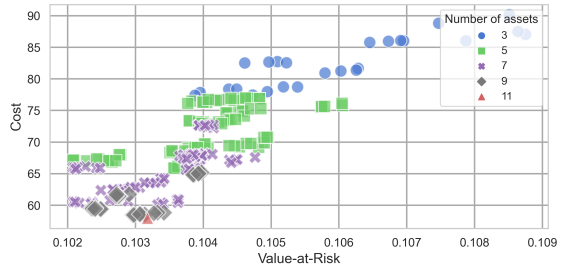

We augment the previous case study with additional renewable assets, for a total of 5 solar (fixed cost 30 $/MWh) and 5 wind farms (50 $/Mwh), We then compare different combinations, i.e. subsets of these 10 assets, comprising Solar, Wind, and Hydro asset, to investigate diversification impact, focusing on cost and downside risk. Our metric for evaluating downside risk is the value-at-risk (VaR) of the energy mismatch between load and CFE generation over the entire year.

We define the relative procurement shortfall , as the summation of the hourly shortfalls between load and constructed portfolio :

For a level , the VaR of the shortfall is . Intuitively, will be around the average fraction of load not met, and measures the downside risk of not meeting the CFE target.

Figure 4 compares various portfolio compositions considering their respective costs and CFE shortfall VaR at level . As expected, the more energy sources are available, the lower the cost. We also see that through more diversified portfolios, the amount of mismatch between the demand and generation gets smaller for a similar cost.

V Multiple Loads

In the multiple loads framework, our goal is to match heterogeneous load profiles with a portfolio of renewable energy generators. Suppose there are Loads, each with their own CFE target and guarantee level and energy sources. When there are multiple loads, cost minimization needs to be defined precisely as it depends on the economic setting; so far CFE contracts have been bilateral with no pooling or netting of multiple contracts. We consider three approaches depending on how the CFE structurer allocates the resources to different Loads.

V-1 Sequential Optimization

In the first approach, the structurer successively addresses the optimization of each Load one at a time. The first Load gets priority and can use any/all of the assets; remaining unclaimed generation then cascades down to become the input for the second optimization for Load 2, and so forth. Mathematically, we solve Problem (P1) for Load with the constraint where , to address that the energy supply for Load has been reduced by the procurement of Loads 1 through .

V-2 Multipartite Optimization

The CFE sources are split equally among the Loads. If there are two Loads, each one will have access to half the generation of each asset. That is, there is no longer any sequencing and we solve Problem (P1) with allocation set , independently for each of Loads.

V-3 Concurrent Optimization

The portfolios are constructed by jointly minimizing the sum of the costs:

| (3) | ||||

where is the CFE score of the -th Load. The joint approach does not provide any preference to one Load over another, focusing on (cooperatively) achieving a minimal total cost while respecting individual Load targets/constraints.

Table IV illustrates the impact of these choices for Case Study II which features 3 stochastic energy sources (“Solar” with cost $50/MWh, “Wind” ($28/MWh) and “Hydro” ($27/MWh)) and 2 Loads representative of Industrial and Commercial profiles. While Load1 is smaller than Load2, it has a higher target with same .

We observe that the Hydro asset is the most desirable among the 3 sources. Without constraints would take 45% of it, while would take 66% of Hydro, creating a competition for this asset, see the first two rows in Table IV. If the assets are arbitrarily split down the middle, then this restriction does not bind for Load1, but hurts Load2 even more, as they can only get at most 50% of Hydro (whereas they could get nearly 55% as “leftovers” after Load1). Finally joint optimization is almost as cheap for Load2 as being first in line, and only hurts Load1 a bit, leading to the lowest sum of procurement costs (right-most column).

VI Conclusion

We have presented initial analysis of structuring portfolios of renewable assets to probabilistically achieve given CFE targets at minimal cost. Our work provides a methodological underpinning to the recent bilateral structures that have been announced in the industry, such as the previously referenced Iron Mountain transaction structured by RPD Energy, as well as the Google data center commitments. Looking ahead, two avenues of research will be explored in follow-up projects. First, concurrently handling multiple loads (e.g. for ) presents a methodological challenge; one seeks a structure that combines features of the sequential, priority-driven allocation (as some Loads might have some sort of preferred status), and the joint cooperative solution that minimizes total procurement costs. Second, one should more explicitly define non-compliance costs, i.e. sustaining a realized CFE score below the target. In practice, the provider might be on the hook for some costs, e.g. to procure in real-time additional CFE credits in order to reach the target when the portfolio is performing below expectations. Properly capturing this cost of shortfall would modify the minimization objective.

References

- [1] G. J. Miller, K. Novan, and A. Jenn, “Hourly accounting of carbon emissions from electricity consumption,” Environmental Research Letters, vol. 17, no. 4, p. 044073, 2022.

- [2] Q. Xu and J. Jenkins, “Electricity system and market impacts of time-based attribute trading and 24/7 carbon-free electricity procurement,” Zero Lab, Princeton University, 2022.

- [3] M. Ludkovski, G. Swindle, and E. Grannan, “Large scale probabilistic simulation of renewables production,” arXiv preprint arXiv:2205.04736, 2022.

- [4] C. Pennington, “Iron mountain implements 24/7 carbon free energy solution,” Tech. Rep., 2023, linkedIn Post. [Online]. Available: https://www.linkedin.com/posts/chris-pennington-b362438_iron-mountain-implements-landmark-247-carbon-activity-7021905239859503105-3BuX/

- [5] Google, “The CFE manager: A new model for driving decarbonization impact,” Tech. Rep., 2022. [Online]. Available: https://www.gstatic.com/gumdrop/sustainability/2022-carbon-free-energy-manager.pdf

- [6] ——, “A policy roadmap for 24/7 carbon-free energy,” Tech. Rep., 2022. [Online]. Available: https://www.gstatic.com/gumdrop/sustainability/policy-roadmap-carbon-free-energy.pdf

- [7] M. Ludkovski and S. Mouti, “CFE portfolio structuring dashboard,” Tech. Rep., 2023, accessed on Nov 20, 2023. [Online]. Available: https://mludkov.shinyapps.io/CFEportfolio

- [8] L. A. Wolsey and G. L. Nemhauser, Integer and combinatorial optimization. John Wiley & Sons, 1999, vol. 55.

- [9] M. Powell, “A new algorithm for unconstrained optimization,” in Nonlinear Programming, J. Rosen, O. Mangasarian, and K. Ritter, Eds. Academic Press, 1970, pp. 31–65.

- [10] R. Fletcher, “An algorithm for solving linearly constrained optimization problems,” Mathematical Programming, vol. 2, pp. 133–165, 1972.

- [11] D. Kraft, “A software package for sequential quadratic programming,” Forschungsbericht- Deutsche Forschungs- und Versuchsanstalt fur Luft- und Raumfahrt, 1988.

- [12] P. Wolfe, “Convergence conditions for ascent methods,” SIAM review, vol. 11, no. 2, pp. 226–235, 1969.

- [13] National Renewable Energy Lab, “ARPA-E’s PERFORM Program Data Plan,” Tech. Rep., 2022. [Online]. Available: https://electricgrids.engr.tamu.edu/electric-grid-test-cases/datasets-for-arpa-e-perform-program/