figuret

\floatsetup[figure]capbesideposition=top,right,capbesidesep=quad,facing=yes

Accounting for Financing Risks improves

Intergenerational Equity of Climate Change Mitigation

Christian P. Friesa,b * and Lennart Quante c,d *

-

a

Department of Mathematics, Ludwig Maximilians University, Munich, Germany

-

b

DZ Bank AG Deutsche Zentral-Genossenschaftsbank, Frankfurt a. M., Germany

-

c

Potsdam Institute for Climate Impact Research (PIK), Member of the Leibniz

Association, Potsdam, Germany -

d

Institute of Mathematics, University of Potsdam, Potsdam, Germany

-

*

These authors contributed equally to this work.

-

Correspondence to: email@christian-fries.de

December 12th, 2023

(version 1.0 [v1])

Abstract

Today’s decisions on climate change mitigation affect the damage that future generations will bear. Discounting future benefits and costs of climate change mitigation is one of the most important components of assessing efficient climate mitigation pathways. We extend the DICE model with stochastic discount rates to reflect the dynamic nature of discount rates. Stochastic rates give rise to a mitigation strategy, resulting in all model quantities becoming stochastic. We show that the classical calibration of the DICE model induces intergenerational inequality: future generations have to bear higher costs relative to GDP and that this effect worsens under stochastic discount rates. Accounting for additional financing risks, we investigate two modifications of DICE. We find that allowing financing of abatement costs and considering non-linear financing effects for large damages improves intergenerational effort sharing. We propose a modified optimisation to keep costs below 3% of GDP, resulting in more equal efforts between generations.

Introduction

Climate change is one of the most significant risks of the next centuries 1, as demonstrated by its manifold impacts on society 2. Due to the persistent nature - on human time scales - of the main greenhouse gas carbon dioxide3, a transition to (net) zero emissions is necessary to limit global warming to any constant level. A diverse set of approaches have been developed to find the optimal pathway towards such an emission-neutral world. One traditional method for the assessment of transition pathways are integrated assessment models (IAMs) of the climate and economic systems; for an overview of the developments on IAMs see 4; 5.

We focus on the DICE model 6; 7 as a simple IAM, which is used to demonstrate the impacts of modifications to the original model due to its simplicity 8; 9; 10; 11; 12. While IAMs were first set up as deterministic, stochastic shocks have been included to consider the risk of tipping points 13; 14; 15; 16; 17; 18; 19, natural feedback processes such as permafrost 9 or abstract catastrophic risks 20; 21. Since most damages of climate change will occur over long time scales, value-based decisions on the discount rate and optimisation function have a strong influence on the resulting optimal pathways 22; 23; 24; 25; 26. Stochastic approaches also require more advanced risk evaluations than Monte Carlo averaging to capture the full extent of tail risks 13 or inequalities in the distribution of damages 27.

Most of these contributions aim to provide an estimate of the societal costs of emitting one additional ton of carbon dioxide, the so-called social cost of carbon (SCC), which is an important determinant for benefit-cost analysis of climate mitigation. Model extensions updating IAMs 11; 12; 19; 28 show a wide range of potential SCC, while also econometrics-based SCC estimates for single impacts such as mortality 29 or energy consumption 30, but also general SCC 31 emphasise the need to improve the precision of the estimated SCC, especially by including, so far ignored, additional impact channels. Discount rates, in particular, are an essential component of IAM modelling. Thus, the discussion between proponents of a descriptive approach based on observation of market returns like in DICE 7 versus a normative approach to discounting as in the Stern review 22 continues. The assumptions on discounting have already been discussed in the context of intergenerational 32 and intragenerational inequality 33. Recent studies 34; 35 show that dynamic modelling of discount rates might allow a more precise assessment of the costs of damages and abatement.

We examine the calibration of the DICE model with respect to intergenerational equity. Measuring the costs per GDP of the optimal (calibrated) climate emissions path in the standard model, we find that these costs are unequally distributed across generations. We use an implementation of the DICE model with a flexible time discretisation 36 and couple this model with a comprehensive modelling toolbox for financial markets 37 to enable the integration of valuation methods for complex financial products in IAMs. We add stochastic interest rates to the model and introduce a stochastic abatement policy. The stochastic abatement policy mimics the process of reacting to changes in the interest rate level by repeated (over time) re-calibration of the model. Since intergenerational inequality is related to the sensitivity of the utility and the discount factor, we introduce two model extensions related to these two parts that will significantly improve intergenerational equity: Financing of abatement costs and non-linear discounting of costs, 38. As abatement is a planned investment process, we assume that these costs may be financed by loans with stochastic interest rates. Furthermore, as large projects and investments often incur additional costs 39; 40, we introduce increasing financing costs for large payments via a non-linear discounting. These higher costs for high damages can be viewed as (additional) financing risks. We provide an overview of the extensions in fig. 1. More background is provided in our extensive model description 36.

Results

Intergenerational Inequality

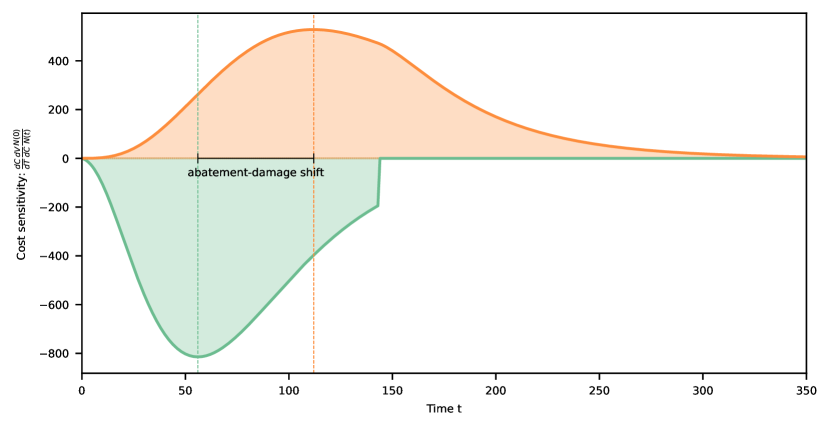

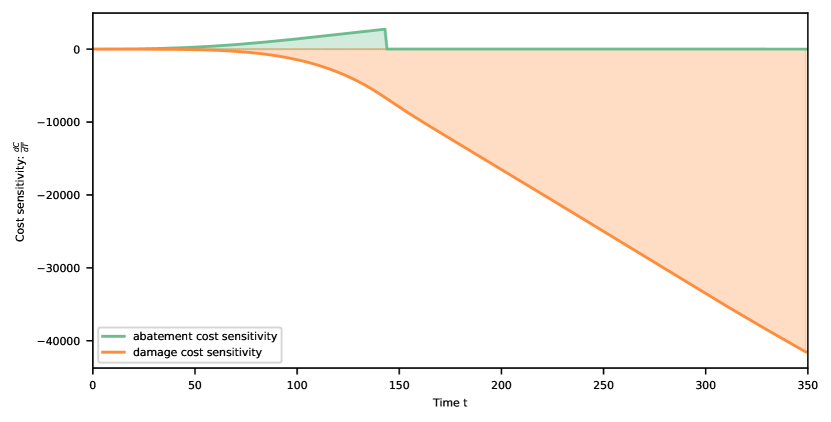

The standard DICE model equates the increment of the cost of damage to the increment of the cost of abatement, both weighted by the value-to-cost-sensitivity and the discount factor.

| (1) |

Here denotes the total welfare, and and denote the damage and abatement cost, respectively, and denotes a parameter representing the abatement policy. The formula presented here is for a reduced model parameterised by the parameter , the time by which 100% abatement is achieved.

The criterion eq. 1 is plausible if a single agent optimises its cost but may be problematic if the costs are distributed between different generations. Note that the two individual contributions in eq. 1 occur at different magnitudes at different times, even different generations. fig. 2 shows the temporal distribution of the weighted functions and .

Hence, marginal gains of one generation are equated to marginal losses of another generation. The calibration does not equalise the burden but the weighted marginal burden. In this sense, the calibration likely introduces intergenerational inequality.

Including stochastic interest rates into DICE

We see in eq. 1 that both the welfare cost sensitivity and the numeraire ratio (i.e., the discount factor) are important to determine the intertemporal optimal pathway. Including a stochastic rate model, the numeraire ratio becomes stochastic. Allowing for (stochastic) adaptation of the abatement policy to the interest rate level, all model quantities become stochastic.

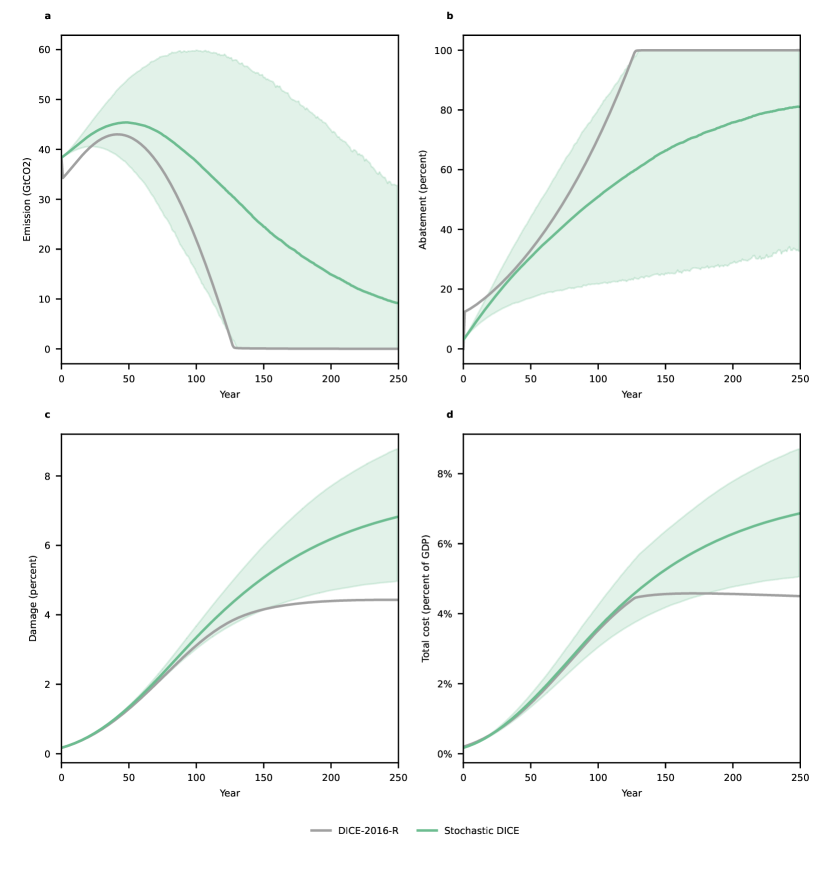

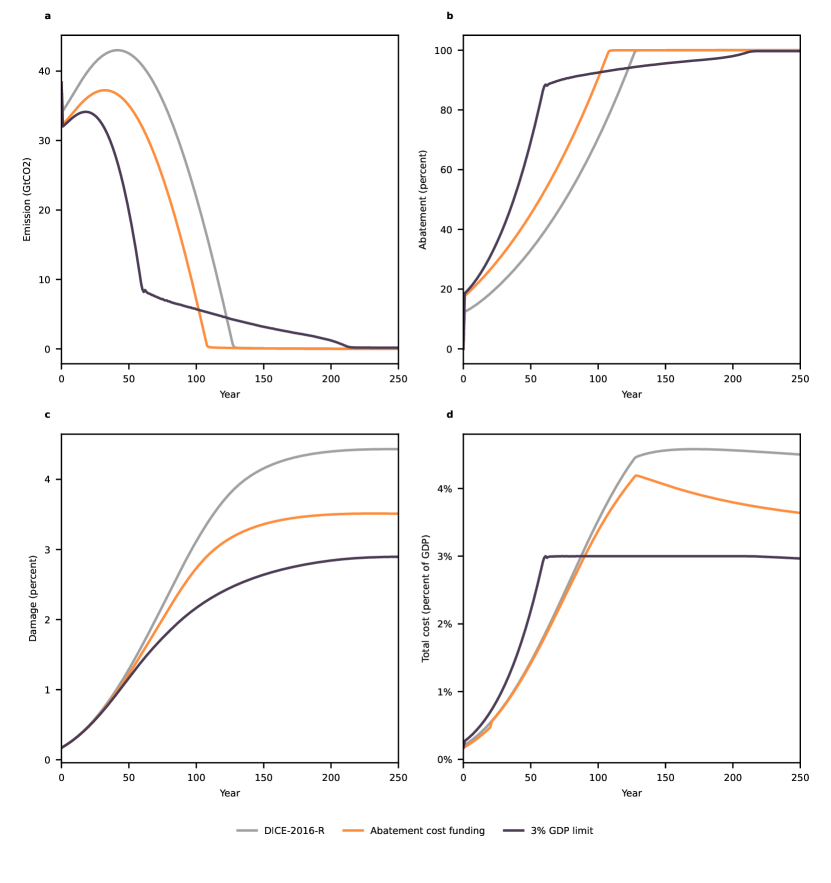

We show that under the stochastic interest rate and stochastic abatement model, the optimal policy will increase intergenerational inequality and, in addition, exhibit the risk of further increases in intergenerational inequality. fig. 3 depicts the impact of stochastic interest rates, both in average and in a quantile measure, on emissions, optimal abatement, damage and total cost-per-GDP. These quantities are depicted for the classical DICE model (grey) and for the DICE model with stochastic interest rates and stochastic abatement policy (green), where we also show the 10 % and 90 % quantile values.

Including funding of abatement and funding risks of damage into DICE

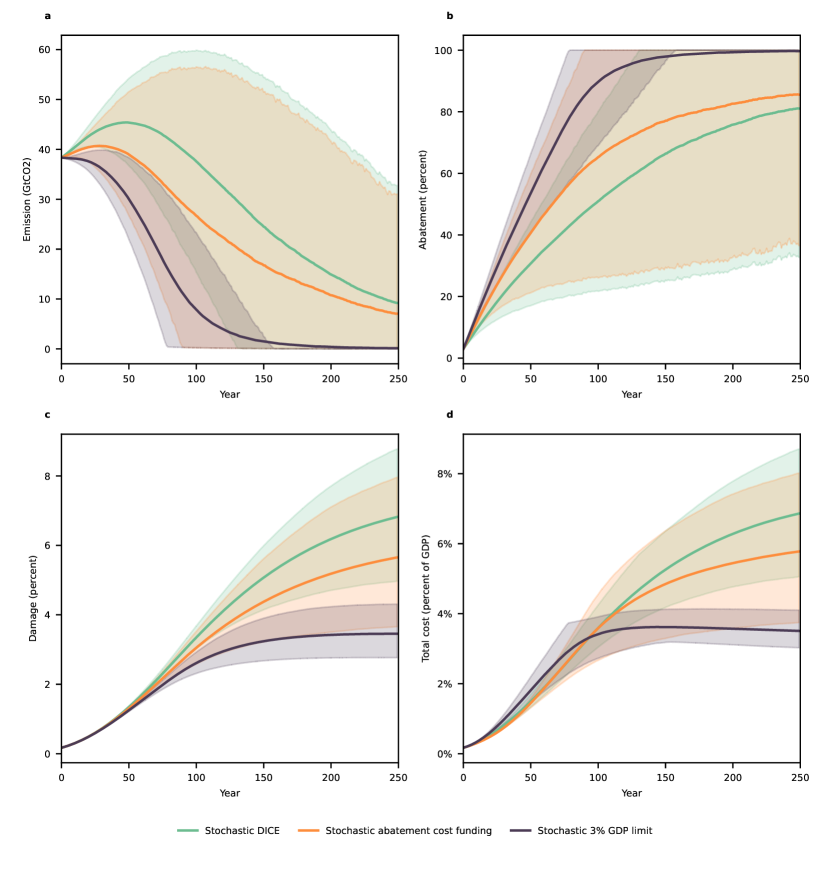

We endow the model with two model extensions: First, we modify the abatement costs by allowing these to be funded over time for interest that has to be paid. Second, we include a non-linear dependency of discounting of the damage cost on the magnitude of the cost. This can be viewed as the additional cost associated with financing risk of very large amount 38.

We find that both modifications allow to improve intergenerational equity (in expectation and risk) in the respective optimal emission pathway. fig. 4 shows the effects of the two modifications on the DICE model with stochastic interest rates. Similar results for the DICE model with deterministic interest rates are shown in LABEL:supfig:pathways_deterministic_with_extension.

Shaded area shows the 10 % to 90 % percentiles.

As shown in fig. 3, costs are distributed unevenly across generations, with higher total costs relative to GDP for generations in the far future. fig. 3 shows that the trade-off between early abatement costs and later damages can be balanced by the constraint that total costs are limited to a certain share of GDP. This measure is already used to assess national debt 41 and results in a more equal distribution of damages between generations. Due to the limits of scaling up abatement immediately and the inherent preference for current generations in the DICE model, present generations still face the lowest costs. Appropriate parameters of the non-linear discounting of the damage cost can be used to limit the costs per GDP.

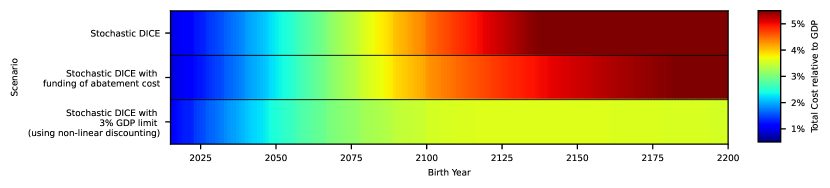

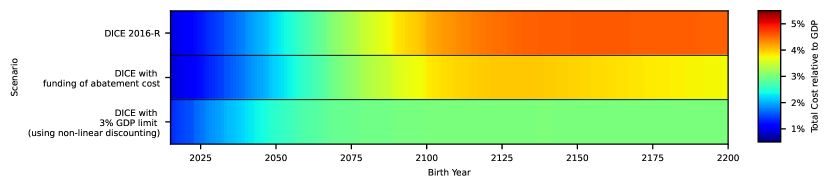

To illustrate the unequal burdens between generations, we use population projections from 2015 to 2100 42 to calculate burdens experienced during the projected lifetime. We measure the burden in percentage-of-GDP, where we choose 3 % as the neutral level (green). While differences are small for the time covered by population projections (fig. 5 and LABEL:supfig:generational_burden_deterministic), extrapolation using the fixed 2100 life expectancy shows a clear divergence at the end of the century. Notably, the stochastic variant does not stay exactly below 3% of GDP on average since high-risk scenarios are not fully offset. The deterministic model keeps the 3% limit and illustrates the equal burden between generations enabled by imposing GDP relative cost limits.

Discussion

We extend the DICE integrated assessment model and compare several extensions for their effect on intergenerational equity. Our analyses apply to integrated assessment models in general and could also be extended to benefit-cost analysis of climate mitigation. We provide a complete open-source implementation of the model illustrating all our extensions, utilising (stochastic) algorithmic differentiation to efficiently calculate sensitivities of model quantities against each other.111The code and data is available at https://gitlab.com/finmath/finmath-climate-nonlinear.

Our first observation is that the DICE model can significantly increase the policy cost measured in terms of cost-per-GDP. This is because the calibration does not consider any intergenerational equity but balances the marginal cost changes induced by a policy change. Absolute cost and its distribution over time are irrelevant to the objective function. This effect is driven by the aggregation of discounted welfare into intergenerational welfare. Considering stochastic interest rates, this effect is amplified when the stochastic adaptation of the abatement strategy generates a significant risk of increased cost. This indicates that a repeated re-calibration of the DICE model to current interest rate levels will amplify intergenerational inequality. We use a more applied scenario by considering the funding of abatement cost and non-linear damage costs to show that these additional aspects would increase the incentive for early mitigation, reducing the burden on later generations. More importantly, the non-linear damage cost allow to effectively limit the generational cost to a specific percentage of the GDP.

Using a simple IAM includes several caveats. First, the representation of damages could be improved 43; 11; 12. Second, the lack of regional resolution compared to, e.g., econometric damage estimates 44; 45 ignores regional inequalities in exposure and potential distributional effects of projected costs 46. Since our study aims to introduce methods such as limiting total costs of climate change by a proportion of GDP to the debate on mitigation pathways, these limitations could be addressed by including the presented concepts in more complex assessments of mitigation pathways 31; 47.

Modifying the DICE model in a modular way, we address the issue that the classical model does not consider equity between generations. The proposed extensions accounting for the funding cost of abatement and increased financing cost of large damages can improve this aspect of the intertemporal optimisation. This is amplified when considering stochastic interest rate risk. Constraining total costs of mitigation and damages relative to GDP could be used as a simple heuristic to ensure intergenerational equity of climate mitigation.

Methods

Derivation of intergenerational inequality in the standard model eq. 1

We consider the one-parameter deterministic abatement model

where the parameter represents the time for reaching 100% abatement. We note that the calibration of a model with the full parameter set is close to the calibration of the model reduced to one parameter 36. As the calibration is maximising the total discounted value, we find that the optimal parameter , representing the equilibrium state of the model, fulfils

| (2) |

where and denote the abatement cost and damage cost, respectively.

Equation 2 allows us to interpret a change in a parameter of the abatement policy as a change in the cash-flow structure of a financial product. Here corresponds to the time- cash-flow, to a weight (like a notional) and to the discount factor.

From eq. 2, we see that the optimisation across generations may result in intergenerational inequality: Since and , the calibration is equating the marginal cost changes of abatement and damage. However, these changes occur at different times, maybe even at different generations. Note that eq. 2 implies eq. 1.

Details on different extensions of DICE-2016-R

We endowed the classical DICE model with several extensions. These are not specific to the DICE model and can also be applied to other IAMs. They are also independent and parameterised in a way that allows to recover the classical model for a specific parameter choice.

Stochastic Discount Rates

The interest rate is modelled with a classical interest rate model. The results depicted here were produced with a Hull-White model with a constant mean-reversion and volatility. The implementation allows to replace this model with a general term structure model.

Stochastic Abatement Policy

It is well understood that the optimal abatement policy depends on the interest rate level. Hence, postulating stochastic interest rates, the abatement policy should be allowed to adapt to the interest rate level. This can also be interpreted as illustrating the effect of a repeated re-calibration of the model to changed interest rate levels. We assume a simple, functional model that depends on the spot interest rate, namely

| (3) |

The simplicity of the models allows us to interpret the parameters. We have that in (3) describes the change of the abatement speed by interest rate change,

Obviously, the stochastic abatement models may achieve a larger-or-equal welfare or lower-or-equal welfare-risk than the corresponding deterministic model simply due to the additional degree of freedom in the abatement optimisation.

Funding of Abatement Cost

Let denote the cost that occur in time due to the abatement policy . In the classical model, the total cost that occur in time are

where are the damage costs and are the abatement costs.

We alter the model by allowing a funding period, such that abatement costs become effective after a period . For the funding, interest has to be paid such that

| (4) |

For the case of no funding, i.e. , , and we recover the original model.

Since damages occur instantaneously, we do not consider funding of these. However, we consider a kind of non-linear discounting.

Non-Linear Discounting of Damage Cost

The idea behind non-linear discounting is that the discount factor depends on the level of the amount to be discounted. This can be justified by a model where one has to attribute for the higher default risk of excessively large future cash-flows. The mechanics are that the compensation of this default risk lowers the return (the interest rate) and hence increases the discount factor38.

Put differently, this adds an increasing weight to large or very large damages.

Let denote the damage cost of the classical model, i.e. the quantity that was formerly denoted by . We then re-define the effective damage costs as

where is the default compensation factor. It is somewhat similar to the inverse of a discount factor, describing the over-proportional cost of funding large projects.

In our experiment, we can specify this weight as a function of the damage or as a function of the fraction of the GDP, i.e., .

The latter approach allows us to penalise damages that exceed a certain percentage of the GDP.

Supplementary Material

Supplementary material is available online.

Code and Data availability

The model code for the stochastic DICE model including the proposed extensions, as well as the experiments generating the data and figures is available in the following Git repository https://gitlab.com/finmath/finmath-climate-nonlinear.

References

- 1 Masson-Delmotte, V. et al. (eds.) Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. IPCC (Cambridge University Press, 2021).

- 2 Pörtner, H.-O. et al. (eds.) IPCC, 2022: Climate Change 2022: Impacts, Adaptation, and Vulnerability. Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press. (Cambridge University Press, 2022).

- 3 Solomon, S. et al. Persistence of climate changes due to a range of greenhouse gases. Proceedings of the National Academy of Sciences 107, 18354–18359 (2010). DOI 10.1073/pnas.1006282107.

- 4 Weyant, J. Some Contributions of Integrated Assessment Models of Global Climate Change. Review of Environmental Economics and Policy 11, 115–137 (2017). DOI 10.1093/reep/rew018.

- 5 Nordhaus, W. Evolution of modeling of the economics of global warming: changes in the DICE model, 1992–2017. Climatic Change 148, 623–640 (2018). DOI 10.1007/s10584-018-2218-y.

- 6 Nordhaus, W. The climate casino: Risk, uncertainty, and economics for a warming world. The Climate Casino: Risk, Uncertainty, and Economics for a Warming World 1–378 (2013). DOI 10.1080/14697688.2014.887853.

- 7 Nordhaus, W. D. Revisiting the social cost of carbon. Proceedings of the National Academy of Sciences of the United States of America 114, 1518–1523 (2017). DOI 10.1073/pnas.1609244114.

- 8 Faulwasser, T., Nydestedt, R., Kellett, C. M. & Weller, S. R. Towards a FAIR-DICE IAM: Combining DICE and FAIR Models. IFAC-PapersOnLine 51, 126–131 (2018). DOI 10.1016/j.ifacol.2018.06.222.

- 9 Wirths, H., Rathmann, J. & Michaelis, P. The permafrost carbon feedback in DICE-2013R modeling and empirical results. Environmental Economics and Policy Studies 20, 109–124 (2018). DOI 10.1007/s10018-017-0186-5.

- 10 Grubb, M. & Wieners, C. Modeling Myths: On the Need for Dynamic Realism in DICE and other Equilibrium Models of Global Climate Mitigation. Institute for New Economic Thinking Working Paper Series 1–29 (2020). DOI 10.36687/inetwp112.

- 11 Glanemann, N., Willner, S. N. & Levermann, A. Paris Climate Agreement passes the cost-benefit test. Nature Communications 11, 1–11 (2020). DOI 10.1038/s41467-019-13961-1.

- 12 Hänsel, M. C. et al. Climate economics support for the UN climate targets. Nature Climate Change (2020). DOI 10.1038/s41558-020-0833-x.

- 13 Crost, B. & Traeger, C. P. Optimal climate policy: Uncertainty versus Monte Carlo. Economics Letters 120, 552–558 (2013). DOI 10.1016/j.econlet.2013.05.019.

- 14 Lemoine, D. & Traeger, C. Watch Your Step: Optimal Policy in a Tipping Climate. American Economic Journal: Economic Policy 6, 137–166 (2014). DOI 10.1257/pol.6.1.137.

- 15 Jensen, S. & Traeger, C. P. Optimal climate change mitigation under long-term growth uncertainty: Stochastic integrated assessment and analytic findings. European Economic Review 69, 104–125 (2014). DOI 10.1016/j.euroecorev.2014.01.008.

- 16 Cai, Y., Judd, K. L., Lenton, T. M., Lontzek, T. S. & Narita, D. Environmental tipping points significantly affect the cost-benefit assessment of climate policies. Proceedings of the National Academy of Sciences 112, 4606–4611 (2015). DOI 10.1073/pnas.1503890112.

- 17 Cai, Y., Lenton, T. M. & Lontzek, T. S. Risk of multiple interacting tipping points should encourage rapid CO2 emission reduction. Nature Climate Change 6, 520–525 (2016). DOI 10.1038/nclimate2964.

- 18 Lemoine, D. & Traeger, C. P. Economics of tipping the climate dominoes. Nature Climate Change 6, 514–519 (2016). DOI 10.1038/nclimate2902.

- 19 Dietz, S., Rising, J., Stoerk, T. & Wagner, G. Economic impacts of tipping points in the climate system. Proceedings of the National Academy of Sciences 118, e2103081118 (2021). DOI 10.1073/pnas.2103081118.

- 20 Ackerman, F., Stanton, E. A. & Bueno, R. Fat tails, exponents, extreme uncertainty: Simulating catastrophe in DICE. Ecological Economics 69, 1657–1665 (2010). DOI 10.1016/j.ecolecon.2010.03.013.

- 21 Ikefuji, M., Laeven, R. J. A., Magnus, J. R. & Muris, C. Expected utility and catastrophic risk in a stochastic economy–climate model. Journal of Econometrics 214, 110–129 (2020). DOI 10.1016/j.jeconom.2019.05.007.

- 22 Hepburn, C. & Beckerman, W. Ethics of the discount rate in the Stern Review on the economics of climate change. World Economics 8, 187–211 (2007).

- 23 Gollier, C. & Weitzman, M. L. How should the distant future be discounted when discount rates are uncertain? Economics Letters 107, 350–353 (2010). DOI 10.1016/j.econlet.2010.03.001.

- 24 van der Ploeg, F. & Rezai, A. Simple Rules for Climate Policy and Integrated Assessment. Environmental and Resource Economics 72, 77–108 (2019). DOI 10.1007/s10640-018-0280-6.

- 25 Van Der Ploeg, F. Discounting and Climate Policy. CESifo Working Papers (2020). DOI 10.2139/ssrn.3657977.

- 26 Wagner, G. & Hoggan, W. H. Carbon Prices, Preferences, and the Timing of Uncertainty (2020).

- 27 Adler, M. et al. Priority for the worse-off and the social cost of carbon. Nature Climate Change 7, 443–449 (2017). DOI 10.1038/nclimate3298.

- 28 Taconet, N., Guivarch, C. & Pottier, A. Social Cost of Carbon Under Stochastic Tipping Points. Environmental and Resource Economics (2021). DOI 10.1007/s10640-021-00549-x.

- 29 Carleton, T. A. et al. Valuing the Global Mortality Consequences of Climate Change Accounting for Adaptation Costs and Benefits. Working Paper 27599, National Bureau of Economic Research (2020). URL https://www.nber.org/papers/w27599. Series: Working Paper Series. DOI 10.3386/w27599.

- 30 Rode, A. et al. Estimating a social cost of carbon for global energy consumption. Nature 598, 308–314 (2021). DOI 10.1038/s41586-021-03883-8.

- 31 Rennert, K. et al. Comprehensive Evidence Implies a Higher Social Cost of CO2. Nature 1–3 (2022). DOI 10.1038/s41586-022-05224-9.

- 32 Padilla, E. Intergenerational equity and sustainability. Ecological Economics 41, 69–83 (2002). DOI 10.1016/S0921-8009(02)00026-5.

- 33 Emmerling, J. Discounting and intragenerational equity. Environment and Development Economics 23, 19–36 (2018). DOI 10.1017/S1355770X17000365.

- 34 Bauer, M. D. & Rudebusch, G. D. The Rising Cost of Climate Change: Evidence from the Bond Market. The Review of Economics and Statistics 1–45 (2021). DOI 10.1162/rest_a_01109.

- 35 Newell, R. G., Pizer, W. A. & Prest, B. C. A Discounting Rule for the Social Cost of Carbon. Journal of the Association of Environmental and Resource Economists 9, 1017–1046 (2022). DOI 10.1086/718145.

- 36 Fries, C. P. & Quante, L. Intergenerational Equity in Models of Climate Change Mitigation: Stochastic Interest Rates introduce Adverse Effects, but (Non-linear) Funding Costs can Improve Intergenerational Equity (2023). URL https://papers.ssrn.com/abstract=4005846. DOI 10.2139/ssrn.4005846.

- 37 Fries, C. P. finmath-lib: Mathematikcal Finance Library: Algorithms and metholodgies related to mathematical finance (2019). URL http://finmath.net/finmath-lib/.

- 38 Fries, C. P. Non-Linear Discounting and Default Compensation: Valuation of Non-Replicable Value and Damage: When the Social Discount Rate may become Negative (2021). URL http://arxiv.org/abs/2007.06465. ArXiv:2007.06465 [q-fin]. DOI 10.48550/arXiv.2007.06465.

- 39 Hallegatte, S., Hourcade, J.-C. & Dumas, P. Why economic dynamics matter in assessing climate change damages: Illustration on extreme events. Ecological Economics 62, 330–340 (2007). DOI 10.1016/j.ecolecon.2006.06.006.

- 40 Shane, J. S., Molenaar, K. R., Anderson, S. & Schexnayder, C. Construction Project Cost Escalation Factors. Journal of Management in Engineering 25, 221–229 (2009). DOI 10.1061/(ASCE)0742-597X(2009)25:4(221).

- 41 Daniel, B. C. & Shiamptanis, C. Pushing the limit? Fiscal policy in the European Monetary Union. Journal of Economic Dynamics and Control 37, 2307–2321 (2013). DOI 10.1016/j.jedc.2013.06.003.

- 42 World Population Prospects - Population Division - United Nations. URL https://population.un.org/wpp/Download/Standard/MostUsed/.

- 43 Burke, M., Hsiang, S. M. & Miguel, E. Global non-linear effect of temperature on economic production. Nature 527, 235–239 (2015). DOI 10.1038/nature15725.

- 44 Kotz, M., Wenz, L., Stechemesser, A., Kalkuhl, M. & Levermann, A. Day-to-day temperature variability reduces economic growth. Nature Climate Change 11, 319–325 (2021). DOI 10.1038/s41558-020-00985-5.

- 45 Kotz, M., Levermann, A. & Wenz, L. The effect of rainfall changes on economic production. Nature 601, 223–227 (2022). DOI 10.1038/s41586-021-04283-8.

- 46 Andreoni, P., Emmerling, J. & Tavoni, M. Inequality repercussions of financing negative emissions. Nature Climate Change 1–7 (2023). DOI 10.1038/s41558-023-01870-7.

- 47 van der Wijst, K.-I. et al. New damage curves and multimodel analysis suggest lower optimal temperature. Nature Climate Change 1–8 (2023). DOI 10.1038/s41558-023-01636-1.

Acknowledgements

We thank Max Singhoff for exploring the calibration of the DICE model with the ADAM solver used in our numerical experiments.

L.Q. received funding from the German Federal Ministry of Education and Research (BMBF) under the research projects QUIDIC (01LP1907A) as well as by Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH on behalf of the Government of the Federal Republic of Germany and Federal Ministry for Economic Cooperation and Development (BMZ).

Author Contribution

C.F. and L.Q. developed the research idea together. C.F. lead the re-implementation of the DICE model and extensions as well as the experiments with input from L.Q. L.Q. lead the plotting implementation with input from C.F. C.F. and L.Q. analysed and interpreted results. C.F. derived the analytic expression for generational inequality. C.F and L.Q. wrote the manuscript.

Competing Interests

The authors declare that they have no competing interests.

Supplementary information for

Accounting for Financing Risks improves

Intergenerational Equity of Climate Change Mitigation

Christian P. Fries and Lennart Quante

figure \cftpagenumbersofftable

figureSupplementary figures

supfigure]supfig:pathways_deterministic_with_extension

supfigure]supfig:generational_burden_deterministic