Risk measures based on weak optimal transport

Abstract.

In this paper, we study convex risk measures with weak optimal transport penalties. In a first step, we show that these risk measures allow for an explicit representation via a nonlinear transform of the loss function. In a second step, we discuss computational aspects related to the nonlinear transform as well as approximations of the risk measures using, for example, neural networks. Our setup comprises a variety of examples, such as classical optimal transport penalties, parametric families of models, uncertainty on path spaces, moment constrains, and martingale constraints. In a last step, we show how to use the theoretical results for the numerical computation of worst-case losses in an insurance context and no-arbitrage prices of European contingent claims after quoted maturities in a model-free setting.

Key words: Risk measure, weak optimal transport, neural network, model uncertainty, martingale optimal transport

AMS 2020 Subject Classification: Primary 91G70; 91B05; Secondary 68T07; 91G20; 91G60

1. Introduction

A key component of financial modeling lies in the description of the distribution of underlying risk factors. Since these risk factors typically take values in high-dimensional vector spaces and exhibit complex dependence structures, there is a natural trade-off between simplicity or implementability of a probabilistic model on the one hand and the most accurate description of reality on the other. Since a perfect reflection of reality in a single probabilistic framework is almost never possible, financial modeling is almost always accompanied by model uncertainty. A mathematical framework that allows to include model uncertainty in the assessment of financial contracts is given by the theory of risk measures, cf. [17]. Under appropriate continuity conditions, every convex risk measure admits a robust representation , where the evaluation of a financial position (or loss function) is performed among a family of probability measures, which are penalized according to their plausibility using a suitable penalty function .

In the past decade, a strand of literature has formed around risk measures, where the penalty term is given as a minimal cost of transportation from a given reference measure , cf. [6], or by a suitable function applied to the Wasserstein distance to the reference measure , see [28] and [7, 18] for a dynamic setting. Here, the reference measure might be, for example, a model that is particularly attractive due to its computational simplicity, suggested by some expert, or purely data-driven, e.g., an empirical distribution derived from given data points, cf. [29]. A similar idea is inherent to the discipline of distributionally robust optimization, where an additional optimization over (possibly rescaled versions of) such risk measures is performed, cf. [19, 27, 31]. We also refer to [5, 8, 9] for an analysis of the sensitivity of robust optimization problems with respect to the degree of uncertainty. Moreover, robust versions of risk measures based on uncertainty sets are investigated in [11, 30].

The aim of this article is a theoretical and numerical study of convex risk measures based on weak optimal transport penalties. More precisely, we focus on risk measures, whose penalty functions measure the distance of a probability on a Borel space to a reference probability on a Borel space by means of a weak optimal transport cost of the form

where contains all kernels such that is a coupling between and . The special choice with a cost function results in a standard optimal transport problem as studied, e.g., in [6, 28]. The weak optimal transport problem was initially introduced in [20] and shortly afterwards in [1]. For an overview on basic results of optimal transport theory under weak transportation costs and a collection of applications from different areas, we refer to [4]. For instance, in stochastic optimization and mathematical finance, weak optimal transport appears in the context of martingale transport problems [10], causal transport problems [2], semimartingale transportation problems [33], and stability results for pricing and hedging [3]. In our framework, the weak optimal transport cost allows to consider a wide spectrum of examples, which range from classical optimal transport penalizations, over parametric uncertainty and uncertainty on path spaces in the spirit of [16] to penalties related to càdlàg martingales interpolating between the reference measure as initial marginal and a terminal marginal , see Section 4 for more details.

In a first step, we show that the risk measure

can be expressed in terms of a nonlinear transform of the loss function which is independent of the reference measure . Theorem 2.1 shows that

where is the so-called -transform of and is the extension of to the universal -algebra on .

In a second step, we exploit the fact that the inner expression in the -transform is measure affine and show that, in special yet relevant cases, the computation of the -transform can be reduced to the extreme points. In particular we use a classical representation of the extreme points of sets of probability measures given in terms of generalized moment constraints, cf. [36, 37]. This allows also for a variational formulation of based on an optimization over Borel measurable functions taking values in the set of extreme points, see Proposition 3.6.

In the case of a Wasserstein or martingale Wasserstein penalty, this allows to use a neural network approximation in the spirit of [28]. The idea of using neural network approximations for the computation of risk measures based on classical optimal transport has recently been exploited in [14, 15], see also [13, 22] and the references therein for min-max methods. However, the approach contained in these works relies on duality results, which transform the original problem into the dual superhedging problem. In our approach, we use a neural network to model relevant transformations of the reference measure which are able to approximate the worst-case measure. Therefore, while the approach of [14, 15] provides an approximation from above, and gives as a byproduct the optimal superhedging strategy for the robust hedging problem, our approach provides an approximation from below, and gives as a byproduct the -transform of the loss function. Note that, having the -transform of the loss function at hand, allows for a fast re-evaluation of the risk measure as the reference model changes at the cost of a Monte-Carlo simulation. This makes the approach also appealing for risk management, where the possibility to promptly adjust the evaluation of a risk as the baseline model changes is of great advantage.

An elementary reformulation of the martingale constraint, which is a priori an infinite-dimensional constraint, allows to understand it as a single moment constraint, and allows to consider robust price bounds under no-arbitrage considerations in a model-free setting, see Section 4.4 and Section 4.6. In Section 5.2, we consider European claims with maturities that exceed the last quoted maturity, and model the absence of information after the quoted maturities by penalizing deviations from the last quoted distribution of the underlying assets with a martingale Wasserstein distance. Using the neural network approximation scheme, we compute no-arbitrage bounds for the prices of options written on a possibly large number of underlying assets, see also Section 5.2.3.

The rest of the paper is organized as follows. Section 2 introduces the setup and contains the representation of the risk measure via the -transform of the loss function , see Theorem 2.1. In Section 3, we introduce a specific class of cost functions that allow for more explicit solutions, when the set of extreme points of the ambiguity set is known, see Theorem 3.3. In Section 4, we present a variety of examples that are covered by our approach and indicate possible applications. Finally, in Section 5, we formulate our neural network approximation based on a general approximation result for Wasserstein penalties, see Proposition 5.1. This approximation based on neural networks is then applied to several examples from finance and insurance.

Notation.

Given a topological space , we denote by its Borel -algebra, and by the set of all probability measures on , endowed with the weak topology. Let . Then, we denote by the space of all Borel measurable functions and by the space of all bounded Borel measurable functions . For a probability measure , let , where consists of all sets with for some with . Then, we denote by the -algebra of all universally measurable sets, and by the extension of to for all . For a universally measurable function and , we define

Here and throughout, we use the convention . If , we simply write and instead of and , respectively. For , we denote by the space of all with , where we use the convention . In a similar way, we denote by the space of all universally measurable functions with .

Let be a measurable space. We denote the space of all --measurable functions by . For a probability measure and a function , we define the push-forward by

2. Weak transport penalties

Throughout, let be two Borel spaces, cf. [12, Definition 7.7]. Since is a Borel space, the set of all Borel probability measures on is again a Borel space, cf. [12, Corollary 7.25.1]. We denote by the set of all Borel measurable stochastic kernels from to , i.e., with

-

(i)

for all ,

-

(ii)

the map is Borel measurable for all .

For and , we define

where for all .

In the following, let be a reference measure and be a Borel measurable cost function. We assume that there exists some with for -almost all . For , let

| (2.1) |

where we use the convention . By assumption,

i.e., the kernel can be interpreted as a transform of states in into states in , which is not penalized, or, in other words, incorporates a risk loading w.r.t. the transformed reference measure . Observe that the functional defines a monetary risk measure, i.e.,

-

(i)

for all with ,111For , we write if for all .

-

(ii)

and for all and ,

and that the weak optimal transportation cost for each is a penalty function of the risk measure . We refer to [17, Chapter 4] for a detailed discussion on monetary risk measures.

We define the -transform of by

Since for -almost all , it follows that for -almost all . Moreover, is upper semianalytic and therefore universally measurable, cf. [12, Proposition 7.29] and [12, Proposition 7.47]. In the special case, where for all and with some Borel measurable function , and for all if is not a Dirac measure, the -transform reduces to the well-known -transform for all .

In the following, we restrict the risk measure to the set

Observe that . In particular, contains all constant functions. The following characterization of the risk measure (2.1) is useful for its numerical computation in Section 5.

Theorem 2.1.

The set is convex and defines a convex risk measure, i.e.,

Moreover, for all ,

| (2.2) |

Proof.

Let . Since whenever and for all , we find that

Hence,

| (2.3) |

Now, let and be a universally measurable -selection of , i.e.,

cf. [12, Proposition 7.50]. Then, by [12, Lemma 7.28], there exists some with for -almost all . We thus obtain that

Now, (2.2) follows by passing to the limit .

It remains to show that is convex and that is convex. To that end, let and . By (2.3), it follows that and . Since and are vector spaces, and . Hence, in view of (2.2), both the convexity of and follow as soon as we have shown that

| (2.4) |

Since , there exists a set with as well as

Let and with . Then, and . Hence,

for all . Taking the supremum over all with , it follows that

for all . We have therefore shown the validity of (2.4), and the claim follows. ∎

3. Optimal transport costs with additional constraints

In this section, we consider weak transport costs with constraints given in terms of a convex and Borel measurable set and a family of bijective maps . We assume that both and are Borel measurable maps . Then, by [12, Lemma 7.12 and Proposition 7.25], the maps and are Borel measurable . Moreover, for all , the map is bijective with inverse .

Throughout this section, we consider a weak optimal transport cost of the form

| (3.1) |

where is a Borel measurable cost function. Since , , and the map are Borel measurable, it follows that the cost function is Borel measurable. Again, we assume that there exists some with for -almost all , i.e., and for -almost all . Since the map is bijective with inverse , the -transform of is given by

where, for , we use the notation

The following remark shows how, in the unconstrained case, this setup reduces to a penalty function, which is given in terms of a classical optimal transport problem. For additional examples of penalty functions and the related risk measures covered by this setup, we refer to Section 4 below.

Remark 3.1.

In the unconstrained case, and for all , it follows that , and the weak optimal transport problem

is equivalent to the classical optimal transport problem

where is the set of couplings between and , i.e., the set of all probability measures with and . In fact, on the one hand, for every , the condition implies that the measure given by for all and is a coupling between and . On the other hand, since and are Borel spaces, for each , there exists a Borel measurable stochastic kernel with for all and , cf. [12, Corollary 7.27.2], which is an element of since for all .

In the following, we focus on the general case, where is not necessarily . Recall that a probability measure is an extreme point of , if for and implies . We denote by the set of all extreme points of . The set is endowed with the smallest -algebra on such that , is measurable for all . By [12, Proposition 7.25], coincides with the trace -algebra of on , which is the same as the Borel -algebra of the subspace topology of the weak topology on .

The next result relies on a characterization given in [36, 37]. The set is said to satisfy the integral representation property (IRP) if, for each , there exists a probability measure such that

For the sake of illustration, we provide three examples for sets that satisfy the IRP, and refer to [36] for a more profound study of this property.

Example 3.2.

The IRP is of particular interest in our framework since, for every measure affine functional on , the supremum with respect to probability measures in can be restricted to the supremum over , see [37, Theorem 3.2 and Proposition 3.1]. In fact, for and every probability measure with for all , measure-theoretic induction yields the barycentrical formula222Recall that with the convention .

In particular, if satisfies the IRP and , then for all . Taking the supremum over all , we get

| (3.2) |

In combination with Theorem 2.1, we obtain the following result, which makes the computation of the -conjugate more tractable.

Theorem 3.3.

Assume that the cost function is of the form (3.1), and let . If satisfies the IRP, then

Proof.

We conclude this section with the following proposition, which is another consequence of Theorem 2.1 and is closely connected to [6, Theorem 2.4].

Proposition 3.4.

Suppose that contains all Dirac measures on and that the cost function is of the form (3.1). Then,

Proof.

By [12, Proposition 7.17], every Borel probability measure on a Borel space is regular. Hence, the set of all probability measures on a Borel space has the Dirac measures as extreme points, see [34, Theorem 11.1]. Since contains all the Dirac measures on , it follows that

We have therefore shown that

where the second equality follows from the fact that is bijective for all , and the claim follows again from Theorem 2.1. ∎

3.1. Generalized moment constraints

Theorem 3.3 is particularly useful when the set of extreme points of has a simple and explicit representation. This is, for example, the case if we impose generalized moment constraints in the sense that we consider the set

| (3.3) |

with , Borel measurable functions , and . As already remarked in Example 3.2 c), the set satisfies the IRP. As remarked in the proof of Proposition 3.4, the set of all Borel probability measures on has the Dirac measures as extreme points. This allows us to use the following theorem by Winkler, see [37, Theorem 2.1], which we report here in the special case .

Theorem 3.5 (Winkler, 1988).

The following proposition, which is based on Theorem 3.5, is a helpful tool for the numerical computation of the risk measure using neural networks.

Proposition 3.6.

Proof.

By Theorem 3.3, it follows that

In particular, holds in (3.4). Since the map from to the set of all subprobability measures on , given by , is continuous and is weakly closed, it follows that is closed. Hence, by [12, Lemma 7.28 and Proposition 7.50], for all and , there exists a measurable map with

Taking the supremum over all measurable maps and letting , the claim follows. ∎

While Theorem 2.1 shows that the risk measure can be computed by solving a pointwise optimization that is independent of the reference measure , Proposition 3.6 suggests a variational approach, where the global behaviour of the loss function , the cost , and the reference measure are considered simultaneously. Since the maximization involves an integral with respect to the reference distribution, this optimization aligns with the framework of stochastic gradient descent methods, where tools such as neural networks typically perform very well. In Section 5 below, we will show how a neural network approximation can be formally justified in this context.

We conclude this section with the following corollary for a general set containing all Dirac measures.

Corollary 3.7.

Suppose that contains all Dirac measures on and that the cost function is of the form (3.1). Then,

4. Examples and applications

In this section, we collect several examples that clarify the use of weak transport penalties, and discuss potential applications for the related risk measure.

4.1. Parametric uncertainty

In this subsection, we present a setup that allows to incorporate special forms of parametric uncertainty via a weak optimal transport penalization. To that end, let and be a -compact333Recall that a topological space is -compact if there exists a sequence of compact subsets of with . Hausdorff topological space, endowed with the Borel -algebra. Moreover, we assume that there exists a continuous and injective map , and define . Since is continuous and is -compact, it follows that is Borel measurable and that the inverse is Borel measurable.444This follows directly from the fact that the image of a compact set under a continuous map is compact and therefore is a countable union of compacts for every closed subset . In particular, is a countable union of compacts. We consider a Borel measurable cost function , and assume that there exists a measurable map such that for -almost all . For and , we define

Since , , and are Borel measurable, it follows that is Borel measurable. Then, by Theorem 2.1,

Then, again by Theorem 2.1,

Example 4.1.

Let , be a probability space, and be a random variable with . For , let

Then, the map is continuous, and we define the cost

with nondecreasing cost functions with . Defining for all , it follows that for all .

4.2. Wasserstein uncertainty

In this section, we consider penalties, given in terms of Wasserstein distances. To that end, let be a separable Banach space and denote the set of all probability measures with finite moment of order . We assume that and consider the cost function

Then, the cost is of the form (3.1) with and and for all . Moreover, satisfies for all and we end up with the risk measure

where is the Wasserstein distance of order between and . Different aspects of risk measures based on transport distances have recently been studied in [5, 6, 28]. We also refer [7, 9, 18] for dynamic versions of these risk measures and to [19, 27, 31] for applications in the context of distributionally robust optimization. Since contains all Dirac measures, by Proposition 3.4,

for all .

Now, let and assume that there exist constants and such that

| (4.1) |

Since , it follows that . Using the convexity of the map , it follows that

Now, let such that and . Then,

for all . In particular, and, using Corollary 3.7,

| (4.2) |

where denotes the space of all (-equivalence classes of) functions with .

4.3. Drift uncertainty on the path space

Let be the space of all continuous functions with , endowed with the topology induced by the supremum norm. Let be the Wiener measure, and consider the cost function , given by

with a nondecreasing function . Here, is the Cameron-Martin space, i.e., the space of all with weak derivative , and is the Cameron-Martin norm for . Note that, by definition of , for all , so that the first Poincaré inequality

is valid for all . In particular, the cost function is Borel-measurable.

In this case, the cost function is of the form (3.1) with and for all . Moreover, satisfies for all . The corresponding risk measure is given by

| (4.3) |

for all . By Proposition 3.4, it follows that

If , by [16, Proposition 1] or [16, Proposition 2], it follows that

| (4.4) |

for all , where is the relative entropy of with respect to . Note that, in general, equality in (4.4) only holds if the penalty term in (4.3) is replaced by the Cameron-Martin adapted Wasserstein distance, see [16, Corollary 2] for the details.

4.4. Martingale constraints

We consider the case, where and the ambiguity set is given by all measures that satisfy a martingale constraint with respect to the reference measure . More precisely, we only consider probability measures that admit a martingale coupling with the reference measure , i.e., a coupling with

| (4.5) |

By Strassen [32], the existence of a martingale coupling between two measures and is equivalent to and being in convex order. We consider the risk measure

| (4.6) |

for , where is a Borel measurable cost function and denotes the set of martingale couplings between and .

Then, we can express this risk measure via a weak optimal transport penalty with cost function

with

and for all , i.e., for all .

In fact, let , , and for all . Then, and . On the other hand, every kernel with gives rise to a coupling via for all . Hence,

and therefore .

Observe that the set is defined by a single moment constraint, namely a mean constraint. Hence, Theorem 3.5 implies that

Therefore, by Proposition 3.6, the martingale constraint reduces to the following optimization

| (4.7) |

This means that the martingale constraint, which is an infinite dimensional constraint, on the state space reduces to a -dimensional optimization problem. In Section 5, we will use this representation of the martingale constraint to compute no-arbitrage bounds for prices of financial derivatives after quoted maturities.

4.5. Martingales on the Skorokhod space

Let , and consider the space of all càdlàg functions , endowed with the -algebra generated by the canonical process . Let with . Then, we denote by the set of all martingale measures on with and . Consider the risk measure

where denotes the quadratic variation. Then, by Itô’s formula,

for all . By [21, Remark 2.2 (ii)], we thus find that

As in Section 4.4, we can therefore apply Theorem 2.1, and obtain that

4.6. Matching quoted option prices on a given maturity

Let with , and consider a two-period market consisting of assets. We assume that the distribution of the assets today, i.e., at time , is known and given by a Dirac measure with . We assume that the discounted prices of the assets at time are given by a random vector , whose distribution is not known precisely.

Let be the payoffs of quoted options, e.g., call options with for . The market then gives a set of intervals with representing the bid-ask spread for the option for . If is the law of , it should satisfy , for all . This conditions can be represented as a set of generalized moment constraints. In fact, for each we consider the constraints

Moreover, we require that the measure does not generate an arbitrage opportunity by imposing the constraint on the mean of the distribution at time .

We can then express the upper no-arbitrage price bound for a European option with payoff and maturity using the reference measure and the cost function for and with being the set of all probability measures that satisfy the constraints described above. We may then choose the kernel arbitrarily among all kernels in with , and consider

Here, the second and third equality directly follow from the choice of the reference measure , which implies that for all with .

Using the IRP of the set and Theorem 3.3, together with Theorem 3.5, we can solve this problem by optimizing over Dirac measures. This leads to

where .

In a similar way, we can obtain the lower price bound by considering , see Section 5.2 below.

5. Numerics

In this section, we complement our main result by additional approximation results, which are then applied in a series of numerical examples.

5.1. Wasserstein uncertainty without constraints

Let be a separable Banach space. We start by considering the risk measure from Section 4.2, i.e.,

| (5.1) |

with and . Recall that the risk measure (5.1) corresponds to the weak transport cost for and and that, by (4.2), it can be expressed as

The next proposition provides an approximation from below for this risk measure, based on an optimization over a set which is dense in .

Proposition 5.1.

Proof.

Since , it follows that

To prove the other inequality, let and with

For , consider the probability measure . Then, using the comonotone coupling,

Since is dense in and the Wasserstein distance metrizes the weak topology on , cf. [35, Definition 8.8 and Theorem 6.9], there exists some with

Altogether, we find that

Letting and taking the supremum over all , we obtain that

| (5.2) |

Since for all ,

and the claim follows from equation (5.2). ∎

The previous proposition provides a constructive way of approximating the risk measure (5.1): given an increasing sequence of subsets of , whose union is dense in , we can approximate the risk measure from below by solving a variational problem on the increasing sequence of subsets. From a practical point of view, the previous result allows to approximate the -transform of the loss function by looking at an optimizing vector field instead of solving a pointwise optimization.

Following closely the approach in [28, Section 3], we can apply this result in the case with using the numerical framework of neural networks. For the sake of a self contained exposition, we provide a full description of the framework and restate the approximation result for this explicit choice of increasing subsets. We denote by the set of fully connected feed-forward neural networks from to with hidden layers and neurons per layer, i.e., the set of functions

where are affine transformations of the form with a matrix and a vector , is a nonlinear function, called the activation function, and the composition with the activation function is to be understood componentwise, i.e.,

For a neural network in , is a function from to , are functions from to , and is a function from to . The fact that is dense in for suitable activation functions allows us to state the following corollary. Its proof relies on classical universal approximation results, cf. [23, 24], and follows closely the one of [28, Corollary 3.3].

Corollary 5.2.

For every and every nonconstant Lipschitz continuous activation function ,

for all continuous functions with (4.1).

Proof.

In this framework, the optimization in the space of neural networks can be performed via gradient descent methods minimizing the loss function

where the integral is computed numerically, using either quadrature formulas or a Monte Carlo simulation. Note that, when computing the integral with a Monte Carlo simulation, new samples are drawn at each step of the training, so that gradient descent automatically results in a stochastic gradient descent algorithm.

5.1.1. A two dimensional example with Wasserstein-2 penalization

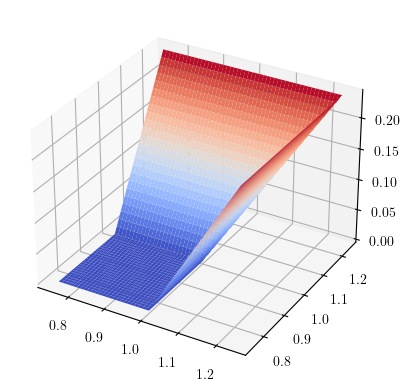

We provide an example for this framework recalling the earthquake example from [28]. We consider a one-period model, where and the reference measure describes an a priori estimate for the location of the epicenter of an earthquake. Suppose an insurance company, selling coverage for the damages caused by earthquakes, estimates a loss function that depends on the location of the epicenter of the earthquake and computes a worst case loss penalizing deviations from the reference model with the Wasserstein-2 distance. We thus consider the risk measure (5.1) with , that is

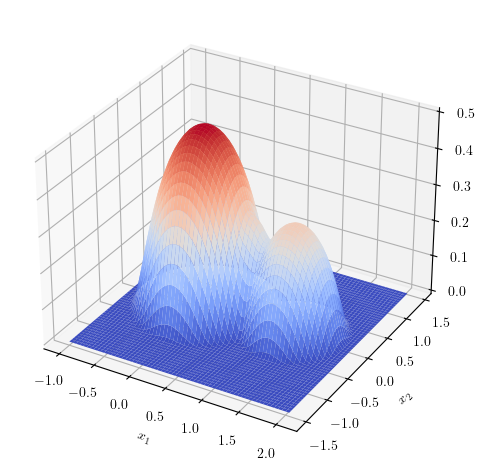

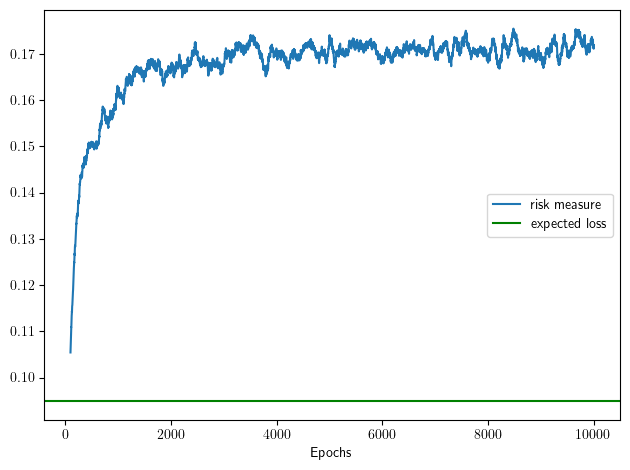

Using Theorem 2.1, one my compute the risk measure by estimating the function and computing its expectation with respect to the reference measure , e.g., via a Monte Carlo simulation. We work with the loss function depicted in Figure 1LABEL:sub@subfig:earth.loss, which models the dependence of the losses on the density of the buildings in a city, or on the distance from two city centers with different exposures. As a reference measure , we choose the law of a two dimensional Gaussian random variable with mean located at and identity matrix as covariance matrix. We estimate this risk measure by approximating with the neural network approach described above.

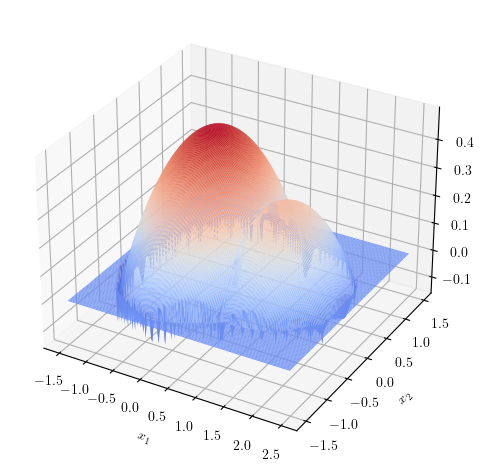

We use a neural network consisting of hidden layers and neurons per layer with ReLU activation function, i.e., . The optimization of the neural network is obtained using the Adam optimizer, cf. [26], with a learning rate of and a batch size of samples, which means that at each iteration only sample points are used to compute the Monte Carlo.555All numerical analyses were performed on a laptop equipped with a 4-Core 3.48GHz CPU and 16GB RAM. The examples were implemented in Python 3.9 and the neural network architecture was handled using the package PyTorch (version 1.11.0). Source codes are available at https://github.com/sgarale/risk_meas_wot. Figure 2 shows the training phase of the risk measure with the neural network approach and Figure 1LABEL:sub@subfig:earth.ctrans depicts the resulting -transform after training epochs. In order to obtain a numerical value for , one only has to perform a final Monte Carlo simulation to integrate the resulting -transform with respect to the reference measure , and this last evaluation can be performed at a low computational cost with a large sample, e.g., one million points.

5.2. Martingale constraint: pricing after quoted maturities

In this section, we apply the framework from Section 4.4 to the pricing of derivatives in a model-free setting. We assume that with , and consider an arbitrage-free market with assets and risk-free rate zero. Suppose that there are many options quoted on a certain maturity , and we therefore know the distribution of the assets at time , and that there are no more quoted options after this maturity. If we want to price a European derivative with maturity , we then have no information for the calibration of a model at that maturity. Using, however, a model-free approach, we can compute bounds on the option price looking at all probability measures which dominate the distribution of the underlying at time in convex order. In fact, even without making rigorous assumptions on the market model, we can assume that absence of arbitrage implies that (discounted) asset processes are martingales.

As a best guess for the distribution at time , we choose the distribution of the assets at time , and we penalize deviations from by means of a martingale optimal transport cost as discussed in Section 4.4.

In order to take into account the length of the time step , we introduce a parameter that controls the level of uncertainty by a rescaling of the penalty term, considering the cost for and . Roughly speaking, the assumption underlying this rescaling is that the uncertainty in the distribution grows proportionally to the square root of time.

We denote by and the upper and lower bound for the option price at time , respectively, i.e.,

Note that corresponds to equation (4.6) with an additional time scaling parameter.

Using the same arguments, it is natural to define the lower bound for the option price considering the infimum over probability measures that dominate in convex order and penalize them with the same cost. This leads to

Numerically, we will solve the reduced problem (4.7) with and with the additional time parameter in the cost function. As in the previous example, we solve this problem using Proposition 3.6, optimizing outside of the integral and reducing the optimization to the space of neural networks with given width and depth, i.e., we consider the optimization

where , indicates a neural network from to , and we denote its components by and . Moreover, we use the transform to map real numbers to probabilities.

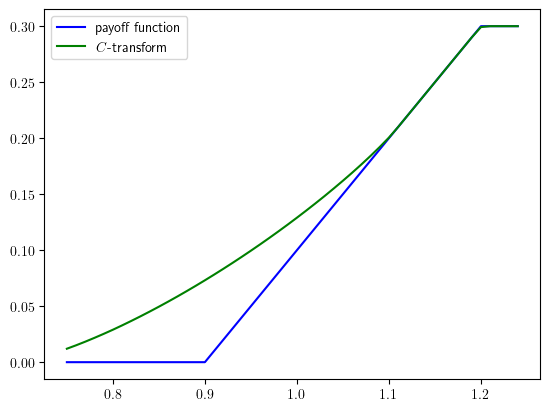

5.2.1. Bull spread option

We consider a bull call spread option, i.e., a European option with payoff given by the sum of a long call option with strike and a short call option with strike . This leads to the payoff function

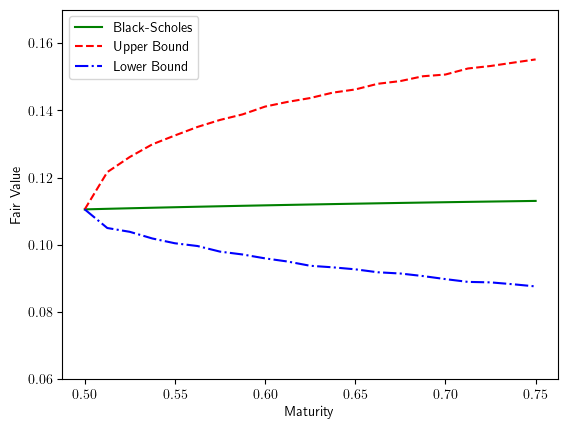

As a reference model, we consider the log-normal distribution corresponding to the marginal at time of a Black-Scholes model with volatility . We set the initial value of the asset to one and the strikes to and .

We work with the cost function , which corresponds to a Wasserstein-3 penalization and compute the upper bound and the lower bound for the arbitrage-free price of the option at different maturities after the quoted maturity . We compare these bounds with the price given by the reference model, i.e., the Black-Scholes price. The output is displayed in Figure 3LABEL:sub@subfig:price.bounds. In Figure 3LABEL:sub@subfig:bull.spread, we depict the payoff function and the resulting -transform for a specific maturity.

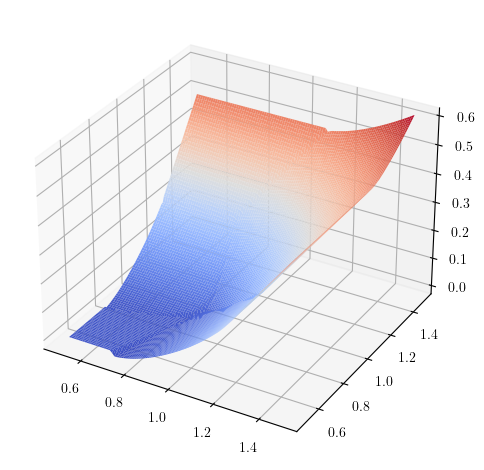

5.2.2. Max call option on two assets

We extend the previous example to a market with two assets. We compute the upper bound for the price of a max call option, which is the European option defined by the payoff

with . As reference measure, we consider the marginal at time of a diffusive model composed by two assets whose dynamics under the equivalent martingale measure is given by the SDE

where is a standard two dimensional Brownian motion under , see [25, Chapter 1]. We fix and penalize deviations from the reference measure with a Wasserstein-3 penalty. As before, we can employ the previously described neural network approach to compute the upper bound for the price of the max call option with strike at the money . Figure 4 displays the payoff function and its -transform.

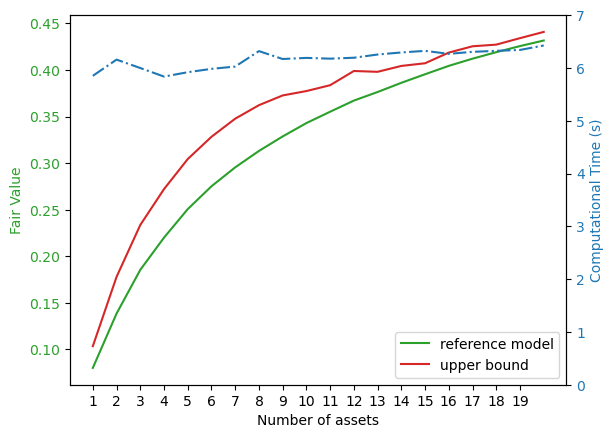

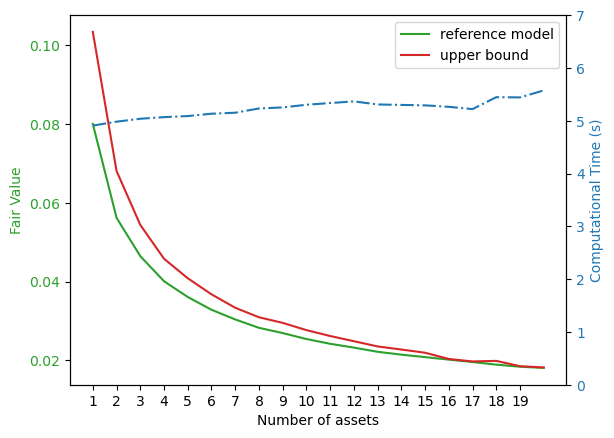

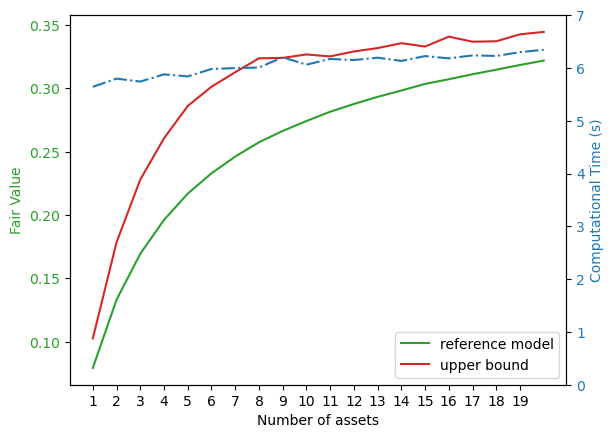

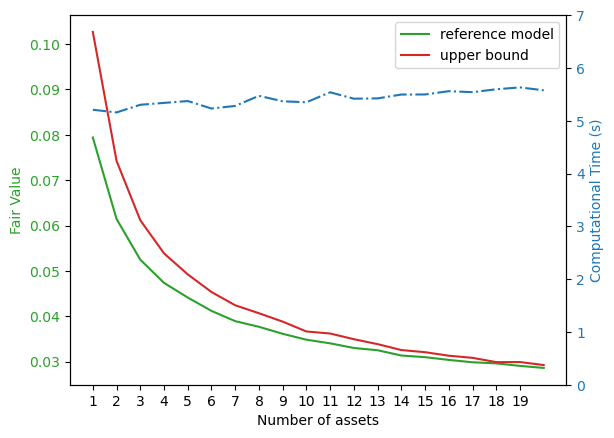

5.2.3. Higher dimensions

We can also work in markets with a higher number of assets. As a matter of fact, the training of the neural network is based on sampling from the reference measure and therefore avoids the curse of dimensionality, which arises in methods based on the discretization of the underlying space. As the number of assets in the market increases, the network reproducing the measurable selection of the optimizers for the -transform of the payoff function becomes larger, but this does not dramatically affect the performance of the method. In Figure 5, we display the result of the evaluation of the upper bound for the price of several options as the number of underlying assets increases, compared with their evaluation time (in seconds). For each value, we train the neural network for epochs. Again, the reference model is a diffusive model in which each asset has volatility and is driven by a standard Brownian motion. Moreover, we assume that the assets start at time zero from the value . Clearly, as in the previous section, it is possible to impose any correlation structure between the assets. We assume that the quoted maturity is (one year) and we compute the upper bound for the price at time with , i.e., one month after the quoted maturity.

We consider four different options, which have the following payoffs:

| max call: | |||

| basket call: | |||

| min put: | |||

| geometric put: |

These options depend on a single strike , which, in the numerical examples, is set to be at the money .

References

- [1] J.-J. Alibert, G. Bouchitté, and T. Champion. A new class of costs for optimal transport planning. European J. Appl. Math., 30(6):1229–1263, 2019.

- [2] J. Backhoff, M. Beiglböck, Y. Lin, and A. Zalashko. Causal transport in discrete time and applications. SIAM J. Optim., 27(4):2528–2562, 2017.

- [3] J. Backhoff-Veraguas, D. Bartl, M. Beiglböck, and M. Eder. Adapted Wasserstein distances and stability in mathematical finance. Finance Stoch., 24(3):601–632, 2020.

- [4] J. Backhoff-Veraguas and G. Pammer. Applications of weak transport theory. Bernoulli, 28(1):370–394, 2022.

- [5] D. Bartl, S. Drapeau, J. Obłój, and J. Wiesel. Sensitivity analysis of Wasserstein distributionally robust optimization problems. Proc. R. Soc. A., 477(2256):Paper No. 20210176, 19, 2021.

- [6] D. Bartl, S. Drapeau, and L. Tangpi. Computational aspects of robust optimized certainty equivalents and option pricing. Math. Finance, 30(1):287–309, 2020.

- [7] D. Bartl, S. Eckstein, and M. Kupper. Limits of random walks with distributionally robust transition probabilities. Electron. Commun. Probab., 26:Paper No. 28, 13, 2021.

- [8] D. Bartl, A. Neufeld, and K. Park. Sensitivity of robust optimization problems under drift and volatility uncertainty. Preprint, arXiv:2311.11248, 2023.

- [9] D. Bartl and J. Wiesel. Sensitivity of multiperiod optimization problems with respect to the adapted Wasserstein distance. SIAM J. Financial Math., 14(2):704–720, 2023.

- [10] M. Beiglböck, P. Henry-Labordère, and F. Penkner. Model-independent bounds for option prices—a mass transport approach. Finance Stoch., 17(3):477–501, 2013.

- [11] C. Bernard, S. M. Pesenti, and S. Vanduffel. Robust distortion risk measures. Preprint, arXiv:2205.08850, 2022.

- [12] D. P. Bertsekas and S. E. Shreve. Stochastic optimal control, volume 139 of Mathematics in Science and Engineering. Academic Press, Inc. [Harcourt Brace Jovanovich, Publishers], New York-London, 1978. The discrete time case.

- [13] L. De Gennaro Aquino and S. Eckstein. Minmax methods for optimal transport and beyond: Regularization, approximation and numerics. Advances in Neural Information Processing Systems, 33:13818–13830, 2020.

- [14] S. Eckstein and M. Kupper. Computation of optimal transport and related hedging problems via penalization and neural networks. Appl. Math. Optim., 83(2):639–667, 2021.

- [15] S. Eckstein, M. Kupper, and M. Pohl. Robust risk aggregation with neural networks. Math. Finance, 30(4):1229–1272, 2020.

- [16] H. Föllmer. Optimal couplings on Wiener space and an extension of Talagrand’s transport inequality. In Stochastic analysis, filtering, and stochastic optimization, pages 147–175. Springer, Cham, 2022.

- [17] H. Föllmer and A. Schied. Stochastic finance. De Gruyter Graduate. De Gruyter, Berlin, 2016. An introduction in discrete time, Fourth revised and extended edition.

- [18] S. Fuhrmann, M. Kupper, and M. Nendel. Wasserstein perturbations of Markovian transition semigroups. Ann. Inst. Henri Poincaré Probab. Stat., 59(2):904–932, 2023.

- [19] R. Gao and A. Kleywegt. Distributionally robust stochastic optimization with Wasserstein distance. Math. Oper. Res., 48(2):603–655, 2023.

- [20] N. Gozlan, C. Roberto, P.-M. Samson, and P. Tetali. Kantorovich duality for general transport costs and applications. J. Funct. Anal., 273(11):3327–3405, 2017.

- [21] G. Guo, X. Tan, and N. Touzi. Tightness and duality of martingale transport on the Skorokhod space. Stochastic Process. Appl., 127(3):927–956, 2017.

- [22] P. Henry-Labordere. (Martingale) Optimal Transport And Anomaly Detection With Neural Networks: A Primal-dual Algorithm. Preprint, arXiv:1904.04546, 2019.

- [23] K. Hornik. Approximation capabilities of multilayer feedforward networks. Neural Networks, 4(2):251–257, 1991.

- [24] K. Hornik, M. Stinchcombe, and H. White. Multilayer feedforward networks are universal approximators. Neural Networks, 2(5):359–366, 1989.

- [25] I. Karatzas and S. E. Shreve. Methods of mathematical finance, volume 39 of Applications of Mathematics (New York). Springer-Verlag, New York, 1998.

- [26] D. P. Kingma and J. Ba. Adam: A method for stochastic optimization. International Confernence on Learning Representations, 2014.

- [27] P. Mohajerin Esfahani and D. Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations. Math. Program., 171(1-2):115–166, 2018.

- [28] M. Nendel and A. Sgarabottolo. A parametric approach to the estimation of convex risk functionals based on wasserstein distance. Preprint, arXiv:2210.14340, 2022.

- [29] J. Obłój and J. Wiesel. Robust estimation of superhedging prices. Ann. Statist., 49(1):508–530, 2021.

- [30] S. Pesenti, Q. Wang, and R. Wang. Optimizing distortion riskmetrics with distributional uncertainty. Preprint, arXiv:2011.04889, 2020.

- [31] G. Pflug and D. Wozabal. Ambiguity in portfolio selection. Quant. Finance, 7(4):435–442, 2007.

- [32] V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36:423–439, 1965.

- [33] X. Tan and N. Touzi. Optimal transportation under controlled stochastic dynamics. Ann. Probab., 41(5):3201–3240, 2013.

- [34] F. Topsøe. Topology and measure, volume Vol. 133 of Lecture Notes in Mathematics. Springer-Verlag, Berlin-New York, 1970.

- [35] C. Villani. Optimal transport, volume 338 of Grundlehren der mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, 2009. Old and new.

- [36] H. von Weizsäcker and G. Winkler. Integral representation in the set of solutions of a generalized moment problem. Math. Ann., 246(1):23–32, 1979/80.

- [37] G. Winkler. Extreme points of moment sets. Math. Oper. Res., 13(4):581–587, 1988.