remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim

On Data-driven Wasserstein distributionally robust Nash equilibrium problems with heterogeneous uncertainties††thanks: Submitted to the editors DATE. \fundingThis work has been partially funded by the ERC under project COSMOS (802348).

Abstract

We study stochastic Nash equilibrium problems subject to heterogeneous uncertainty on the cost functions of the individual agents. In our setting, we assume no prior knowledge of the underlying probability distributions of the uncertain variables. To account for this lack of knowledge, we consider an ambiguity set around the empirical probability distribution under the Wasserstein metric. We then show that, under mild assumptions, finite-sample guarantees on the probability that any resulting distributionally robust Nash equilibrium is also robust with respect to the true probability distributions with high confidence can be obtained. Furthermore, by recasting the game as a distributionally robust variational inequality, we establish asymptotic convergence of the set of data-driven distributionally robust equilibria to the solution set of the original game. Finally, we recast the distributionally robust Nash game as a finite-dimensional Nash equilibrium problem. We illustrate the proposed distributionally robust reformulation via numerical experiments of stochastic Nash-Cournot games.

keywords:

Distributionally robust games, Stochastic programming, Statistical Learning1 Introduction

1.1 Uncertain Games

A variety of applications in smart-grids [28], communication [29] and social networks [1] include self-interested interacting decision makers. An efficient analysis of such systems is typically achieved via game theory [3]. While the study of deterministic games can prove useful in various cases [29], [24], in the majority of applications, the decision problems are affected by uncertainty, which needs to be explicitly incorporated into the models. A number of results in the literature have addressed uncertainty in a gaming set-up, on the basis of specific assumptions on the probability distribution [6], [32] and/or the geometry of the sample space of the uncertainty [2, 19]. However, the uncertainty affecting the system might not exactly follow the imposed probabilistic model. Without an accurate knowedge of the underlying probability distributions that characterize the model uncertainty, sampling-based or data-driven techniques have shown the potential to provide satisfactory solutions.

In [13, 14, 23] the so-called scenario approach was leveraged for the first time to obtain data-driven Nash equilibria with robustness certificates. The framework of these works was extended in [25] and [26], where guarantees for the entire feasibility region were provided, thus also for the entire set of Nash equilibria. Following an approach similar to [25], the works [10, 11] focus solely on sets of variational equilibria. The authors in [27] propose a methodology that provides tunable robustness certificates for a set of strategic deviations around a randomized generalized Nash equilibrium. Based on a different approach, the works [17, 18] propose equilibrium seeking algorithms for stochastic Nash equilibrium problems, formulating the cost functions with expected values.

The aforementioned works do not take into account ambiguity in the probability distribution. From a mathematical standpoint, without any knowledge of the probability distributions and a small amount of available data, a robust Nash equilibrium can hardly be computed without resorting to a worst case set-up. This challenge becomes more pronounced in multi-agent settings with heterogeneous uncertainties affecting the agents’ costs, where the consideration of a collection of (possibly) unknown probability distributions is often required. To circumvent this challenge, our work follows a different line of research from the works above, based on distributionally robust optimization (DRO) [4, 5, 31] approaches. Specifically, DRO considers an ambiguity set of candidate probability distributions aiming to make a decision that is robust with respect to variations of the probability distribution within this set. This work establishes a mathematical framework that connects DRO with game theory.

Bridging DRO techniques with a general gaming set-up with heterogeneous ambiguity in the distributions, allows one to leverage the advantages of DRO over other approaches. Compared to the scenario approach, which requires a significant number of samples to provide sensible robustness guarantees, DRO approaches can work even without a large amount of available data. This is because their robustness is based not only on the number of samples available, but additionally on tuning the size of the ambiguity set through additional parameters. Furthermore, DRO admits as special cases sample average approximation (SAA), where only an adequate estimate of the probability distribution is considered, and robust optimization (RO), where all possible probability distributions defined over a given support set are taken into account. DRO techniques are usually less conservative than RO, while they provide superior out-of-sample performance compared to SAA. Distributionally robust approaches are particularly useful in data-driven applications, where the uncertainty and their corresponding set of distributions are inferred based on a finite amount of available data. In such cases, the appropriate choice of structure on the ambiguity set is of uttermost importance.

In recent years, optimal-transport based ambiguity sets [33] such as the so-called Wasserstein ambiguity set, have attracted substantial attention. Wasserstein ambiguity sets are usually formulated by harnessing available data to construct an empirical probability distribution. Subsequently, they use the so called Wasserstein metric, a measure of distance between two distributions, to define a region that encompasses possible deviations from the empirical distribution. There are several reasons for favouring the Wasserstein distance over alternative metrics when quantifying the distance among distributions. First, the Wasserstein ambiguity set penalizes horizontal dislocations between two distributions. Furthermore, it provides finite-sample certificates on the probability that the true distribution will lie within the constructed ambiguity set. To this end, many works have been dedicated on establishing convergence of empirical estimates in the Wasserstein distance [8, 22, 7, 34, 35, 15].

1.2 Contributions

Despite the considerable body of literature on DRO with Wasserstein ambiguity sets, the exploration of data-driven Wasserstein distributionally robust Nash equilibrium problems with heterogeneous uncertainty in the cost functions represents a notably underexplored topic, which highlights a significant gap in the existing literature: Related works mainly consider ambiguity in the constraints, such as the recent work [36], which studies a game with deterministic cost for each agent and distributionally robust chance constraints with the centre of the Wasserstein ambiguity set being an elliptical distribution; [9] reformulates an equilibrium problem with a deterministic cost and distributionally robust chance-constraints as a mixed-integer generalized Nash equilibrium problem. Differently from previous works, our paper focuses on data-driven Wasserstein distributionally robust Nash equilibrium problems with heterogeneous ambiguity affecting the cost function of each agent. To the best of our knowledge, this is the first time that this class of equilibrium problems is studied and key properties are established. In particular, our contributions are as follows:

-

1.

Robustness guarantees for games with heterogeneous ambiguity: We provide finite-sample guarantees on the probability that, with high confidence, the distributionally robust Nash equilibrium is also robust against the true but unknown probability distribution.

-

2.

Bound on the distance between distributionally robust and true mapping: To account for distributional uncertainty, we consider that each agent constructs a heterogeneous Wasserstein ambiguity set on the basis of samples. We then recast this problem in the form of a Wasserstein distributionally robust variational inequality and bound the distance between the distributionally robust equilibria and the equilibria of the original stochastic Nash equilibrium problem.

-

3.

Asymptotic consistency of distributionally robust Nash equilbria: Based on that, we establish asymptotic consistency of distributionally robust Nash equilibria, i.e., the distance between the set of distributionally robust equilibria and the set of equilibria of the stochastic problem over the true probability distribution converges to zero almost surely as the number of samples increases, under appropriate conditions on the radii of the ambiguity sets and the confidence parameters. As such, our work provides conditions for asymptotic consistency, in similar spirit to [22], that can be applied to the broader setting of multi-agent distributionally robust Nash equilibrium problems with heterogeneous uncertainties.

-

4.

Computational tractability: Adapting the methodology used in [22, Theorem 4.2], we show that this result can in fact be generalized for multi-agent games that admit (possibly) different probability distributions. As such, a seemingly infinite-dimensional game can successfully be transformed into a finite-dimensional generalized Nash game.

Since the resulting finite-dimensional game is in general hard to solve, we propose a variant of the algorithm presented in [18] to empirically calculate equilibria of such problems. Extensive simulation studies show how the choice of the agents’ Wasserstein radii and number of samples affect the resulting distributionally robust equilibria. We illustrate this behaviour through an illustrative example with multiplicative uncertainty and via a data-driven Wasserstein distributionally robust Nash-Cournot game.

2 Problem formulation

2.1 Background on operator theory and distributionally robust optimization

In this section we introduce some basic notation and results required for the subsequent developments. To this end, consider the index set . The decision vector of each agent is denoted by , where , denotes an element; let be the decision vector of all other agents’ decisions except for that of agent and be the collective decision vector.

We denote by the -th norm in , with . The projection operator of a point to the set is given by . A function is -Lipschitz continuous if for all . A mapping is -strongly monotone on if for all . is monotone on if for all . is a function on if for all pairs of distinct vectors and in , there exists such that and , where is the -th component of , i.e., ). The natural mapping of on is given by , where denotes the identity operator. The partial conjugate of a function with respect to its second argument is the function defined as . Finally, denotes the golden ratio parameter.

The symbol means that has probability distribution . The so called dirac measure is given by . Furthermore, let us denote as the set of all probability distributions with support the set and define as

In other words, considers the sets of all distributions defined on with a bounded first-order moment. We are now ready to define the Wasserstein metric to quantify the distance between two probability distributions.

Definition 2.1.

The Wasserstein metric between two distributions is defined as

where represent the set of joint probability distributions of the random variables and with marginals , , respectively.

The Wasserstein metric can be viewed as the optimal transport plan to fit the probability distribution to [33]. An alternative dual interpretation can be derived by the so-called Kantorovich-Rubinstein theorem:

Theorem 2.2.

For two distributions , we have that

where is the space of all 1-Lipschitz continuous functions on .

2.2 Distributionally robust Nash equilibrium problems

Consider a game where each agent selects a decision , and given , minimizes the following local expected loss function:

where

The parameter denotes the uncertainty affecting the cost of each agent . The collection of the local stochastic optimization programs in (G) constitutes a stochastic Nash equilibrium problem (SNEP). For the special case where the probability distributions of the uncertainties affecting each agent are known, a solution to (G) can be calculated on the basis of the following solution concept, known as a stochastic Nash equilibrium (SNE).

Definition 2.3.

A decision vector is a SNE of (G) if

The probability distributions of the uncertainties affecting each agent are unknown in general. This renders the computation of SNE a rather challenging task. Furthermore, possible deviations from the nominal probability distribution are not taken into account. As such, the formulation of (G) and its corresponding solution concept SNE has to be adapted to account for (possible) ambiguity in the probability distributions. To this end, we consider a set of possible probability distributions that each agent’s uncertainty might follow, that contains the true probability distributions with high confidence (see Lemma 3.1), the so called ambiguity set.

To construct an heterogeneous ambiguity set for each agent , we follow a data-driven approach and calculate the empirical distribution from i.i.d. samples based on the relation

Finally, we construct the Wasserstein ambiguity set with radius and centre the empirical probability distribution . We then consider the following data-driven distributionally robust (DR) game

| (DRG) |

For this general class of problems, the equilibrium concept needs to be extended to account for the ambiguity in the probability distributions of the uncertain parameters. Thus, the concept of data-driven Wasserstein distributionally robust Nash equilibrium is proposed.

Definition 2.4.

For a drawn multi-sample for each , a point with , is a data-driven Wasserstein distributionally robust Nash equilibrium of game (DRG) if it holds that

For simplicity we will refer to the data-driven Wasserstein distributionally robust Nash equilibrium as DRNE, where it is implied that the radius of the ambiguity set is according to the Wasserstein metric and its centre is obtained through data. The notation and denotes the dependence of the solution on the multi-sample . Definition 2.4 is a generalization of a saddle-point solution, as obtained in standard DRO, where a single agent makes a decision so as to minimize the expected loss, while nature selects a probability distribution to maximize the expected loss, thus acting as an adversarial agent.

In our case, a DRNE can be written equivalently as:

At a DRNE, given and nature’s decision , each agent cannot further decrease their expected loss by unilaterally deviating from the decision . Respectively, each agent’s perception of nature (viewed as an adversarial agent) at the DRNE cannot increase this cost by unilaterally choosing another probability distribution, given the decision of all agents . We now impose the following standing assumption. {assumption} The set of DRNEs of (DRG) is non-empty. Under this assumption, we establish the equivalence between 1) stochastic Nash equilibrium problems and stochastic variational inequality problems and 2) distributionally robust Nash equilibrium problems and distributionally robust variational inequality problems. To this end, consider the following variational inequality (VI) problem:

where is the so-called pseudogradient mapping and is the collection of true distributions that each uncertainty with follows. {assumption} For each , is measurable on and continuously differentiable in for any given and . The measurability of for each ensures that the corresponding expected values are well-defined. Differentiability of for each is required for the interchange of the expected value operator and the gradient operator, a property that is leveraged in the subsequent developments. Moreover, we have some convexity requirements for the set of decision variables and for the cost functions. {assumption} For each , is closed, compact and convex and is convex. Then, the following lemma establishes a connection between the set of SNE and the solution set SOL() of VI().

Proof: By Assumption 2.2 and the first order optimality condition for NE, the proof follows by adapting Proposition 1.4.2. in [12].

Consider now the following data-driven Wasserstein distributionally robust VI (DRVI)

where denotes the total number of drawn samples, and is the collection of probability measures, each of which belongs to its own distinct Wasserstein ball, i.e., , and is chosen so as to maximize the expected loss of each agent . Then, similarly to the connection of SNEPs and stochastic VIs, we can establish the equivalence of SOL() and the solution set of DRNE of (DRG).

Lemma 2.6.

Proof: Taking the optimality condition for the distributionally robust NE we have that:

| (1) | |||

| (2) |

Concatenating each of the inequalities above across agents we obtain

| (3) | |||

| (4) |

where denotes the collection of all probability distributions at the equilibrium.

Since, is continuously differentiable for each agent we have that

thus retrieving . Conversely, we start from problem

Then, by selecting for each , such that the -th element is , while for all other elements we set , one obtains the optimality conditions for the distributionally robust NE.

The equivalence of SNEPs and DRNEPs with their corresponding VIs as established through Lemmas 2.5 and 2.6 allows to establish fundamental properties of distributionally robust Nash equilibria and provides a connection with the theoretical framework of sensitivity analysis of variational inequalities.

3 Properties of distributionally robust Nash equilibria

In this section, we establish fundamental properties of DRNE. First, we provide finite-sample probabilistic guarantees such that any obtained DRNE evaluated over the ambiguity sets for each is also robust with respect to the true probability distributions with high confidence, which depends on the Wasserstein radii and the number of samples for each . Subsequently, we provide a bound between the mappings of the nominal VI problem and that of the DRVI, which we leverage to show the asymptotic consistency of the set of distributionally robust Nash equilibria to the set of stochastic Nash equilibria of the nominal stochastic Nash equilibrium problem.

3.1 Finite sample probabilistic robustness certificates for DRNE

Let us impose the following assumption which is an adaptation of [22, Assumption 3.3] for heterogeneous uncertainties affecting each agent : {assumption} For any considered probability distribution in the ambiguity set of agent , we have that . Furthermore, there exists such that

The following lemma then holds:

Lemma 3.1.

Under Assumption 3.1, the following confidence bound holds for the true probability distribution of agent :

| (5) |

where

| (6) |

, and where are positive constants that only depend on and .

Proof: The result follows by direct application of Theorem 2 in [16] for each agent . The explicit bound in (6) relates the confidence that the true probability is contained in the Wasserstein ball , with the radius of that ball, as well as the number of drawn samples by each agent . Note that the bound exponentially decays as the number of samples increases. For the case where , the decay with respect to is slower the larger the dimension of the support set .

Solving with respect to , we obtain:

As such, for a drawn multi-sample and a confidence level for each agent , the Wasserstein radius can be tuned accordingly so that the desired finite-sample probabilistic guarantees are satisfied. The following result provides finite-sample probabilistic guarantees that, with high confidence, any DRNE will also be robust against the true underlying distributions.

Lemma 3.2.

Consider a solution of (DRG). Then, for a drawn multisample it holds that

where is the cartesian product of the agents’ probability distributions .

Proof: It holds that

The first inequality is a result of applying Bonferroni’s inequality, while the second inequality follows immediately from Lemma 3.2, thus concluding the proof.

As a particular case, the following result considers the case where the agents share the same samples and distributions.

Lemma 3.3.

Consider a solution of (DRG) and assume that all agents’ uncertain parameters follow the same probability distributions and share the same multi-sample, i.e., and for all . Then, it holds that

Proof: This result is a special case of Lemma 3.2 for a common multi-sample among agents and a common probability distribution . Note that considering the same multi-sample and probability distribution results in the confidence parameter , thus concluding the proof.

Treating the confidence as a function of the number of samples and the Wasserstein radius for each , one has to increase or for each individual agent in order to provide a confidence bound close to 1. From Lemmas 2.5 and 2.6, the equivalence of the SNE set of () and the solution set of , as well as that of the DRNE set of (DRG) and the solution set of , allows to focus solely on variational inequalities. Thus, we show that as the number of samples for each agent increases, the solution set of VI() converges to the solution set of VI(), under appropriate conditions on the Wasserstein radii and the confidence parameters . This property, known in the DRO literature as asymptotic consistency [20], [22], is extended in our work to account for equilibrium problems. To establish such convergence results, as the formulated DRVI can be viewed as a perturbation of the original VI, we first obtain a bound on the distance between the mapping of VI( ) and the original, but unknown, mapping of VI(). Since we are interested in the conditions for convergence of to , we first define the notion of functional convergence.

Definition 3.4.

We say that a sequence of continuous mappings converges to the mapping on if

where , that is for every , there exists a positive integer such that, for all we have that .

We then impose the following regularity assumption on the agents’ cost functions. {assumption} For any and any it holds that

for any and any . Assumption 3.4 is standard in the DRO literature (see [20] and references therein) and allows to invoke Theorem 2.2 as an intermediate step towards the provision of an upper bound on the distance between the two mappings and .

Proposition 3.5.

Proof: For any in an open set and any , where it holds that

The third equality is due to Assumption 2.2. The fourth equality is a direct application of Theorem 2.2. The second inequality is obtained by applying the triangle inequality, while the last inequality holds because for any . The first inequality is obtained as follows: By Assumption 3.4, we have that is Lipschitz continuous with Lipschitz constant . Furthermore, is the set of all Lipschitz continuous functions with Lipschitz constant less than 1. Thus, we have that

where the last line is due to Theorem 2.2.

The following result shows that under appropriate assumptions on the confidence parameter and radius for each agent , the distance between the DR mapping and the original mapping converges to 0 almost surely. This result is then used to show asymptotic consistency of the DR solutions.

Lemma 3.6.

Proof: By adapting Lemma 3.7 in [22] and considering a sequence that satisfies the conditions of the statement, we have that

| (8) |

Then, the following hold:

3.2 Asymptotic consistency of locally unique distributionally robust equilibria

We initially consider the case where the Nash equilibria of VI are isolated, i.e., they are locally unique.

Theorem 3.7.

Consider an isolated point of the nominal VI() defined on the neighbourhood and the perturbed solution set of VI() in this neighbourhood , where . For a sequence of radii and confidence parameters as in Lemma 3.6, every sequence of vectors converges to an accumulation point that is also a solution of VI().

Proof: Note that for any , any sequence is bounded, since is a closed and bounded set for any . Since every bounded sequence has a convergent subsequence, let be the accumulation point of that subsequence. Then, due to the continuity of , with respect to we have that is the accumulation point of the sequence . Considering the mapping , where is the perturbation of in the cartesian product of Wasserstein balls and constructing a sequence of confidence parameters for each in accordance to Lemma 3.6, we have that for any the sequence converges to -almost surely as goes to infinity for each . Since , considering that converges to and that satisfies the variational inequality VI() and taking the limit as tends to infinity for each yields As such, the accumulation point is the unique isolated solution of VI( on .

Though interesting per se, asymptotic consistency for the case of distributionally robust isolated equilibria is useful for cases when is -strongly monotone or satisfies the so called weak sharpness condition [12]. However, it cannot be used in cases where the mapping satisfies a weaker property such as monotonicity. In the next subsection instead, the asymptotic convergence is generalized for the case of solution sets under the assumption that the nominal mapping is [12], a condition that is weaker than monotonicity.

3.3 Asymptotic consistency of distributionally robust variational solution sets

We now extend the results of Section 3.2 to compact solution sets. To this aim, we impose the following technical assumption.

is a mapping on X. Note that a monotone mapping is a function but the vice versa does not necessarily hold [12]. We then have the following result:

Theorem 3.8.

Proof: Under Assumption 3.3 we have from [12, Theorem 3.6.6] that if SOL() is a compact set then there exists such that the level set is bounded. Consider now a perturbation of the nominal probability distribution . Then, applying Proposition 3.5, we have that for any taking values in , where is an open set,

If it holds that:

where the first inequality is due to the non-expansiveness of the projection operator. Denote the ball of mappings defined on based on the maximum norm, i.e., . We now wish to show that the set

is bounded. Taking by selecting appropriate values for for each agent as in Lemma 3.6, the set above is a subset of , which by [12, Theorem 3.6.6] is bounded. Hence, is also bounded. As such, we have that

thus concluding the proof.

Now that we have established the asymptotic constistency of solution sets of distributionally robust games, we aim at reformulating the original game as a simpler and possibly tractable Nash equilibrium problem.

4 Computational tractability

In this section, we show that (DRG) is equivalent, under some assumptions, to a generalized Nash equilibrium problem (GNEP) with individual coupling constraints. First, we impose the following assumption adapted from [22]. {assumption} The uncertainty set is convex and closed. For each and for all , can be written as the pointwise maximum of functions, i.e., , where is convex, proper and lower semi-continuous (in ) for all . Furthermore, for each , is not identically on for all .

Proof: The proof is an adaptation of the proof of Theorem 4.2 [22] and for the ease of presentation is deferred to the Appendix.

The decision variable represents the dual variable of the Wasserstein ball constraint imposed on each probability distribution for each . Note that the problem can be further simplified by following steps similar to [22]. Specifically, the following lemma is an extension of Theorem 4.2 in [22] to account for the more general class of distributionally robust equilibrium problems.

Lemma 4.2.

Proof: See Appendix.

In Lemma 4.2, denotes the epigraphic variable associated with a particular sample , while are auxiliary variables indexed by , related to the elements of the pointwise maximum as per Assumption 4. For clarity of presentation of the following results, we denote , , , , and

| (DRG’) |

From the reformulation of (DRG) to (DRG’) under Assumption 4, the decision variable, corresponding to each agent’s adversarial nature, is no longer an infinite dimensional probability distribution but a finite collection of decision variables, thus substantially simplifying the original game (DRG). In light of the reformulation (DRG’) of (DRG), let us adjust the definition of equilibrium for the reformulated version.

Definition 4.3.

A point is a GNE of (DRG’) if and only if

for all .

Lemma 4.4.

If is a GNE of (DRG’) , then is a DRNE of (DRG).

Proof: For all it holds that:

where the first and last equalities hold due to Theorem 4.1 and Lemma 4.2, while the inequality is obtained by applying Definition 4.3.

The following lemma focuses on the case where the support set is polytopic and known and allows to obtain an explicit form for the conjugate function in each agent’s constraints.

Lemma 4.5.

Suppose that each agent’s support set is a polytope, i.e., , where and . If for all for all . Then, a DRNE of (DRG) can be obtained by solving the GNEP

where and .

5 Numerical simulations

In this section, we provide some numerical examples to show how the radii and the number of samples can affect the equilibrium. The first set of simulations is on an academic example, while in the second we consider a distributionally robust Nash-Cournot game. We calculate a DRNE of (DRG) by leveraging the reformulation of Section 4. To this end, we propose Algorithm 5.1, a variant of Algorithm 1 in [18], in turn inspired by the results in [21]. In the setting of Lemma 4.5, for ease of presentation of Algorithm 5.1, let us introduce the notation

where, with some abuse of notation, and the multiplier vector corresponds to the coupling constraint . Finally, is an appropriately chosen stepsize in according to [18, 21]. The decision , coming from all agents but , can be viewed from agent ’s perspective as an external perturbation to which they have to adapt by changing their decision. Each agent does not have access to the other agents’ constraints. As such, the proposed algorithm does not have theoretical convergence guarantees and is rather used as a heuristics to empirically obtain an equilibrium solution. Developing Nash equilibrium seeking algorithms with theoretical convergence guarantees for such problems, though an interesting avenue for future research, is outside the scope of this work. Due to the presence of a relatively large number of epigraphic constraints, a large number of oscillations is usually expected before an equilibrium can be reached. Furthermore, the epigraphic reformulation that leads to a tractable game renders the corresponding mapping merely monotone, i.e., the definition of monotonicity is satisfied with equality. As such, inertia update terms in the decision variables can often be important for convergence to a solution, which motivates the choice of Algorithm 5.1.

5.1 Illustrative example

Consider a set of two agents , whose decision vectors and are scalar, taking values in . The cost function of each agent is affected by a multiplicative uncertainty , where . Due to lack of knowledge of the probability distribution of the random variables we consider heterogeneous data-driven ambiguity set based on the Wasserstein distance for each agent. Agent then solves the following optimization program,

| (9) |

while Agent 2 solves

| (10) |

We consider drawn samples and a support set and for the heterogeneous uncertainties.

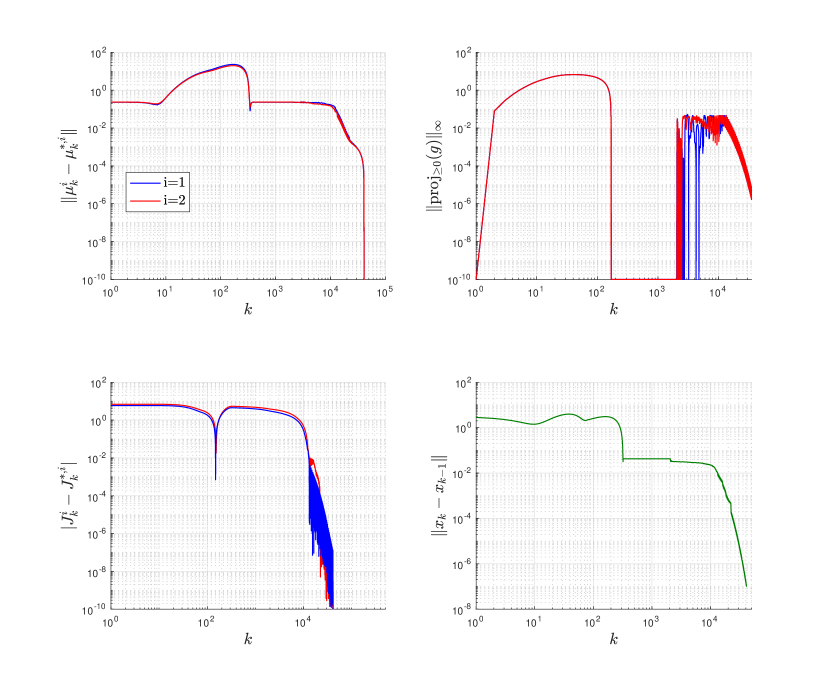

Figure 1 shows the behaviour of Algorithm 5.1. Specifically, the top left corner of Figure 1 shows the convergence of the Lagrange multipliers to their limit point, while the top right corner illustrates the satisfaction of all coupling constraints. To better capture the behaviour of Algorithm 5.1, a logarithmic grid is used. As such, to ensure that only non-negative values are admitted, we illustrate only the non-negative pointwise maximum among the collection of all coupling constraints. The bottom left figure shows convergence of the costs to their corresponding equilibrium, while the bottom right figure illustrates the error bound between the current and previous iterate, which diminishes to zero. Note that satisfaction of the coupling constraints involves a considerable amount of oscillations that decay to zero due to reasons mentioned in the introduction of this section.

5.2 Distributionally robust Nash-Cournot games with heterogeneous ambiguity

We consider an oligopoly Nash-Cournot game involving three companies () producing similar products. Each company wishes to maximize their profits by determining the quantity of products they plan to produce for the market. Furthermore, the market specifies a lower threshold on the demand of product quantity to be satisfied collectively by the companies, expressed in our model as a coupling constraint . However, the price of the product is affected by uncertain factors, whose relation to the price might not be amenable to an explicit formulation. Even if that was the case, the distribution of such factors might be unknown. Thus, it is more suitable to model them as an external uncertain parameter affecting the system. The distribution of the uncertain parameter is in general not known to the companies and using only the empirical probability distribution to estimate it might result in poor future performance. Since companies are concerned about their future profits, they wish to hedge against distributional variations by constructing ambiguity sets of possible distributions that the uncertainty might follow. Thus, the optimization problem of company , given the product quantity chosen by the other companies , is

| (11) |

where is the production cost and is the product price, with and are considered fixed. The coupling constraint is assumed to be affine. Note that both the samples drawn and the radius can be different among agents, thus allowing us to study more general cases, where there is heterogeneity in the ambiguity set.

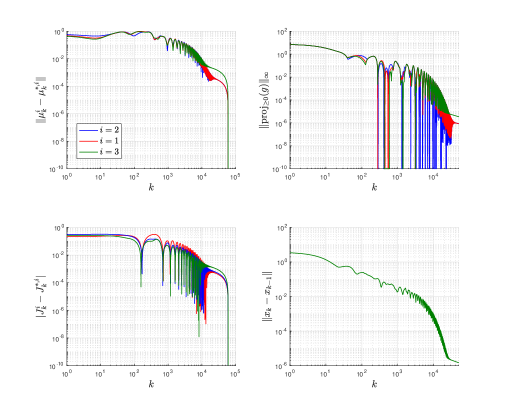

Figure 2 shows the convergence of Algorithm 5.1 for the same radius and different number of samples per agent. Specifically, the Lagrange multipliers (top left) ensure that the coupling constraints, originating either from the reformulation or the additional coupling constraint , on the top right figure are satisfied.

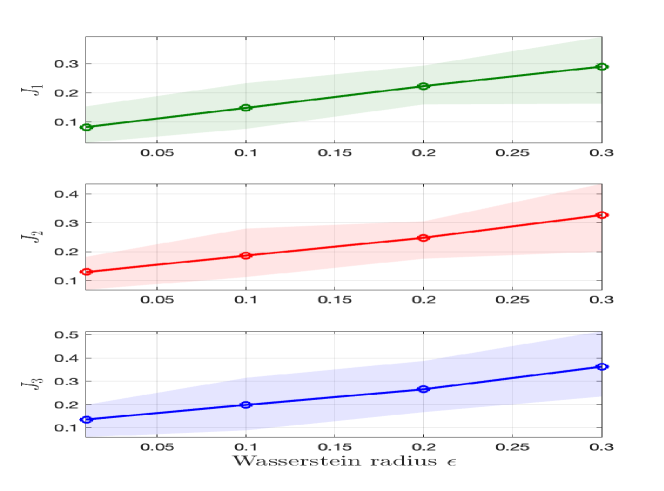

Figure 3(a)) illustrates the agents’ cost at the DRNE for different values of the Wasserstein radius for a common number of samples . Agents follow different normal distributions, assumed to be unknown. For each selection of radius value , 50 simulations are used. The thick line for each agent corresponds to the mean values across these simulations while the transparent stripes correspond to different max and min ranges of values among all realizations. Note that with larger Wasserstein ball there is an increase in the value of the each cost function, as the increase in radius implies that more distributions are taken into account for the construction of the ambiguity set used for risk-averse decision making. Note also that the presence of the coupling constraints related to the product demand from the market can lead to agents sharing the burden of this constraint in a different manner. This can lead to different cost values per agent at the equilibrium, depending on how agents choose to split this constraint.

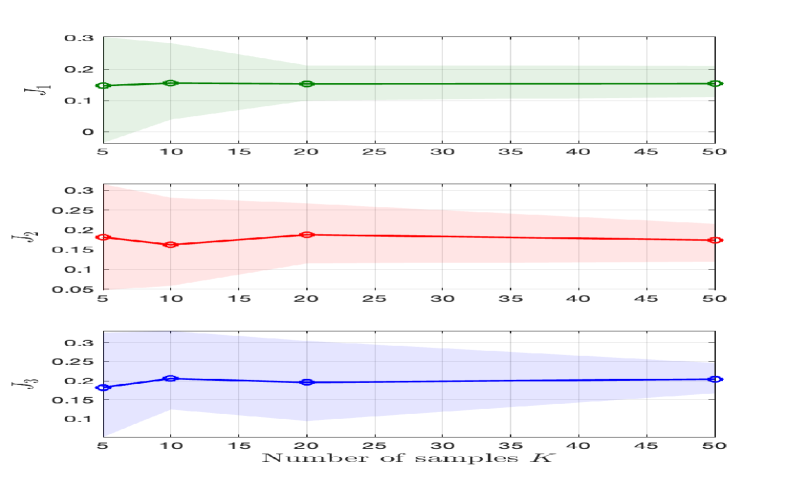

Figure 3(b)) illustrates the agents’ cost at the DRNE for a different number of samples for a common radius . Agents are assumed to follow different distributions and for each radius, 50 simulations are again used. The thick line for each agent corresponds to the mean values across simulations, while the transparent stripes correspond to different values for each realization with the boundaries defining the maximum and minimum cost realizations for some given multi-sample. Note that the larger the number of samples the thinner the stripe corresponding to the maximum and minimum value across simulations. We conjecture that this is because as the number of samples increases, the empirical probability distribution which acts as the centre of the Wasserstein ball becomes more accurate, leading to smaller variations for the same radius size.

3(b)) Agents’ cost for a different number of samples for a common radius . Agents follow different distributions and for each chosen number of samples 50 simulations are used. The thick lines correspond to the mean values across these simulations, while the transparent stripes correspond to different values for each simulation.

6 Conclusion

In this work we propose a distributionally robust approach for the study of stochastic Nash equilibrium problems, where different probability distributions affect the agents’ cost functions. We establish fundamental properties of data-driven Wasserstein distributionally robust equilibria such as out-of-sample certificates, asymptotic convergence of the set of data-driven distributionally robust equilibria and implement an algorithm to calculate such equilibria. Future work will focus on designing algorithms for the solution of distributionally robust Nash equilibrium problems with provable theoretical convergence guarantees and on considering more general cases, where the agents’ costs are nonlinear functions of the probability distribution, thus allowing the use of a richer family of risk measures. An interesting research direction is the study of chance-constrained Nash equilibrium problems with ambiguity both in the cost functions and in the constraints.

7 Appendix

Proof of Theorem 4.1: The proof follows by an adaptation of the proof of Theorem 4.2 in [22]. Specifically, we have that, given , each agent solves

where is the conditional distribution of given that , . Using a duality argument it holds that

The claim about replacing inequality with equality as mentioned in [22], also holds in this more general case under Assumption 4. In fact for this holds due to [30, Proposition 3.4], while for , the Wasserstein ball of agent is reduced to the singleton and, thus, the sample average is obtained.

Proof of Lemma 4.2: Using an epigraphic reformulation it holds that for any and given :

The first equality is derived by leveraging the dual norm, while in the second one we replace maximization with minimization of the negation of the function. In the third inequality we make use of the minmax inequality, which is tight under Assumption 4. Finally, in the last two lines we make use of the existential operator which is in this case equivalent to the min operator to recast as a decision variable.

References

- [1] D. Acemoglu and M. K. Jensen, Aggregate comparative statics, Games and Economic Behavior, 81 (2013), pp. 27–49.

- [2] M. Aghassi and D. Bertsimas, Robust game theory, Math. Program., 107 (2006), pp. 231–273.

- [3] T. Başar and G. Olsder, Dynamic non-cooperative game theory, (1999).

- [4] A. Ben-Tal, L. Ghaoui, and A. Nemirovski, Robust optimization, Robust Optimization, (2009).

- [5] J. Blanchet and K. Murthy, Quantifying Distributional Model Risk via Optimal Transport, Mathematics of Operations Research, 44 (2019), pp. 565–600.

- [6] P. Couchman, B. Kouvaritakis, M. Cannon, and F. Prashad, Gaming strategy for electric power with random demand, IEEE Transactions on Power Systems, 20 (2005), pp. 1283–1292.

- [7] J. Dedecker and F. Merlevède, Behavior of the empirical wasserstein distance in under moment conditions, Electronic Journal of Probability, 24 (2019).

- [8] S. Dereich, M. Scheutzow, and R. Schottstedt, Constructive quantization: Approximation by empirical measures, Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 49 (2011).

- [9] F. Fabiani and B. Franci, On distributionally robust generalized nash games defined over the wasserstein ball, Journal of Optimization Theory and Applications, 199 (2023), pp. 298–309.

- [10] F. Fabiani, K. Margellos, and P. J. Goulart, On the robustness of equilibria in generalized aggregative games, 2020 59th IEEE Conference on Decision and Control (CDC), (2020), pp. 3725–3730, https://doi.org/10.1109/CDC42340.2020.9304348.

- [11] F. Fabiani, K. Margellos, and P. J. Goulart, Probabilistic feasibility guarantees for solution sets to uncertain variational inequalities, Automatica, 137 (2022), p. 110120.

- [12] F. Facchinei and J.-S. Pang, Finite-dimensional variational inequalities and complementarity problems, (2003), https://doi.org/10.1007/b97543.

- [13] F. Fele and K. Margellos, Probabilistic sensitivity of Nash equilibria in multi-agent games: a wait-and-judge approach, (2019), pp. 5026–5031.

- [14] F. Fele and K. Margellos, Probably approximately correct Nash equilibrium learning, IEEE Transactions on Automatic Control, 66 (2021), pp. 4238–4245.

- [15] N. Fournier, Convergence of the empirical measure in expected wasserstein distance: Non-asymptotic explicit bounds in , (2023).

- [16] N. Fournier and A. Guillin, On the rate of convergence in Wasserstein distance of the empirical measure, Probability Theory and Related Fields, 162 (2015), pp. 707–738.

- [17] B. Franci and S. Grammatico, A distributed forward–backward algorithm for stochastic generalized nash equilibrium seeking, IEEE Transactions on Automatic Control, 66 (2021), pp. 5467–5473, https://doi.org/10.1109/TAC.2020.3047369.

- [18] B. Franci and S. Grammatico, Stochastic generalized nash equilibrium-seeking in merely monotone games, IEEE Transactions on Automatic Control, 67 (2022), pp. 3905–3919, https://doi.org/10.1109/TAC.2021.3108496.

- [19] S. Hayashi, N. Yamashita, and M. Fukushima, Robust Nash equilibria and second-order cone complementarity problems, Journal of Nonlinear and Convex Analysis, 6 (2005).

- [20] D. Kuhn, P. M. Esfahani, V. A. Nguyen, and S. Shafieezadeh-Abadeh, Wasserstein Distributionally Robust Optimization: Theory and Applications in Machine Learning, Operations Research & Management Science in the Age of Analytics, (2019), pp. 130–166.

- [21] Y. Malitsky, Golden ratio algorithms for variational inequalities, Mathematical Programming, 184 (2020), pp. 383–410.

- [22] P. Mohajerin Esfahani and D. Kuhn, Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations, Mathematical Programming, 171 (2018), pp. 115–166.

- [23] D. Paccagnan and M. C. Campi, The scenario approach meets uncertain game theory and variational inequalities, in 2019 IEEE 58th Conference on Decision and Control (CDC), 2019, pp. 6124–6129, https://doi.org/10.1109/CDC40024.2019.9030247.

- [24] D. Paccagnan, B. Gentile, F. Parise, M. Kamgarpour, and J. Lygeros, Nash and wardrop equilibria in aggregative games with coupling constraints, IEEE Transactions on Automatic Control, 64 (2019), pp. 1373–1388.

- [25] G. Pantazis, F. Fele, and K. Margellos, A posteriori probabilistic feasibility guarantees for Nash equilibria in uncertain multi-agent games, IFAC-PapersOnLine, 53 (2020), pp. 3403–3408. 21st IFAC World Congress.

- [26] G. Pantazis, F. Fele, and K. Margellos, On the probabilistic feasibility of solutions in multi-agent optimization problems under uncertainty, European Journal of Control, 63 (2022), pp. 186–195.

- [27] G. Pantazis, F. Fele, and K. Margellos, A priori data-driven robustness guarantees on strategic deviations from generalised nash equilibria, 04 2023.

- [28] W. Saad, Z. Han, H. V. Poor, and T. Basar, Game-theoretic methods for the smart grid: An overview of microgrid systems, demand-side management, and smart grid communications, IEEE Signal Processing Magazine, 29 (2012), pp. 86–105.

- [29] G. Scutari, F. Facchinei, J. Pang, and D. P. Palomar, Real and complex monotone communication games, IEEE Transactions on Information Theory, 60 (2014), pp. 4197–4231.

- [30] A. Shapiro, On Duality Theory of Conic Linear Problems, Series Title: Nonconvex Optimization and Its Applications, 57 (2001), pp. 135–165.

- [31] A. Shapiro, Distributionally Robust Stochastic Programming, SIAM Journal on Optimization, 27 (2017), pp. 2258–2275.

- [32] V. V. Singh, O. Jouini, and A. Lisser, Existence of nash equilibrium for chance-constrained games, Operations Research Letters, 44 (2016), pp. 640 – 644.

- [33] C. Villani, Topics in optimal transportation, (2016).

- [34] J. Weed and F. Bach, Sharp asymptotic and finite-sample rates of convergence of empirical measures in wasserstein distance, Bernoulli, 25 (2017).

- [35] J. Weed and Q. Berthet, Estimation of smooth densities in wasserstein distance, (2019).

- [36] T. Xia, J. Liu, and A. Lisser, Distributionally robust chance constrained games under wasserstein ball, Operations Research Letters, 51 (2023), pp. 315–321.