A Diffusion Model of Dynamic Participant Inflow Management

Baris Ata, Booth School of Business, University of Chicago,

5807 S. Woodlawn Ave, Chicago, IL 60637, USA, baris.ata@chicagobooth.edu, p:773-834-2344, ORCID:0009-0001-4793-4607

Deishin Lee, Ivey Business School at Western University, 1255 Western Rd, London, ON N6G0N1, Canada, dlee@ivey.ca, p:519-661-3288, ORCID:0000-0002-6335-2877

Mustafa H. Tongarlak, Boğaziçi University, Bebek, 34342 Beşiktaş/Istanbul, Türkiye, tongarlak@boun.edu.tr, p:+90 212 359 6503, ORCID:0000-0002-4812-2539

October 30, 2023

Abstract

This paper studies a diffusion control problem motivated by challenges faced by public health agencies who run clinics to serve the public. A key challenge for these agencies is to motivate individuals to participate in the services provided. They must manage the flow of (voluntary) participants so that the clinic capacity is highly utilized, but not overwhelmed. The organization can deploy costly promotion activities to increase the inflow of participants. Ideally, the system manager would like to have enough participants waiting in a queue to serve as many individuals as possible and efficiently use clinic capacity. However, if too many participants sign up, resulting in a long wait, participants may become irritated and hesitate to participate again in the future. We develop a diffusion model of managing participant inflow mechanisms. Each mechanism corresponds to choosing a particular drift rate parameter for the diffusion model. The system manager seeks to balance three different costs optimally: i) a linear holding cost that captures the congestion concerns; ii) an idleness penalty corresponding to wasted clinic capacity and negative impact on public health, and iii) costs of promotion activities. We show that a nested-threshold policy for deployment of participant inflow mechanisms is optimal under the long-run average cost criterion. In this policy, the system manager progressively deploys mechanisms in increasing order of cost, as the number of participants in the queue decreases. We derive explicit formulas for the queue length thresholds that trigger each promotion activity, providing the system manager with guidance on when to use each mechanism.

Keywords: Participant inflow management, dynamic control, service operations

1 Introduction

This paper studies a diffusion control problem motivated by challenges faced by public health agencies who run clinics to serve the public. Examples include mass vaccination clinics and blood donation clinics. A key challenge for these agencies tasked with serving the public is to motivate individuals to participate in the services provided. Public health officials cannot control whether and when individuals arrive at the clinics. They can use promotion activities to increase public awareness and thus the participant inflow at clinics, but deploying such mechanisms can be costly. These activities can range from simple email communications and public health advertisements to speaking events for public health officers. If participation turnout is low, there is a negative impact on public health and wasted clinic capacity.

We use a diffusion model to analyze such a service organization where a system manager can deploy costly participant inflow mechanisms to increase the rate at which participants sign up. Ideally, the system manager would like to have enough participants waiting in a queue to serve as many individuals as possible and efficiently use clinic capacity. However, if too many participants sign up, resulting in a long wait, participants may become irritated and hesitate to sign up again in the future (e.g., for the next vaccine dose or giving blood in the future). This is captured by a holding cost in our model. The system manager must use these promotion activities judiciously to balance the inflow of participants, with the risk of overspending on promotion if too many participants sign up.

We show that a nested threshold policy is optimal for the deployment of promotion activities. In this policy, the system manager should progressively deploy these mechanisms in increasing order of cost, as the number of participants in the queue decreases. We derive the explicit queue length thresholds that trigger each promotion activity, providing the system manager with guidance on when to use each mechanism.

The methodological contribution of the paper lies in its solution of a drift-rate control problem on an unbounded domain with state costs. The associated Bellman equation involves boundary conditions at the origin and at infinity. The former is a Neumann type boundary condition whereas the latter is a linear growth condition for the derivative of the value function. Our solution approach proceeds by solving a family of initial value problems starting at the origin parameterized by the average cost rate (defined below), initially ignoring the aforementioned growth condition. We develop an approach to pin down the unique value of the average cost rate that ensures the linear growth condition, which is the technical novelty of the paper.

Literature Review.

Our problem can be viewed as controlling the arrival rate of a queueing system. Such problems have often been tackled by either heavy traffic approximations or Markov decision process formulations in the literature. The heavy traffic approach, pioneered by Harrison (1988), approximates the original control problem for a queueing system with a diffusion control problem, which is easier to analyze; see Harrison and Wein (1989, 1990) for early examples of this approach. For problems similar to ours, heavy traffic approximations often result in drift rate control problems. A closely related paper to ours is Ata et al. (2005), which considers a drift rate control problem on a bounded interval under a general cost of control but no holding costs. Ata (2006) builds on Ata et al. (2005) and approximates a multi-class make-to-order production system with a drift rate control problem on a bounded interval with a piecewise linear convex cost of control. Methodologically, our paper relates to Ata (2006) but it extends it in two important ways. First, its state space is unbounded. Second, it incorporates holding costs. Incorporating these two important model features leads to a significantly more complex analysis. Another closely related paper is Ata et al. (2023). This paper differs from Ata et al. (2023) in that the participants (in the public health setting) are unlikely to abandon. Thus, we do not incorporate abandonments in our model. This modeling difference leads to a different type of Bellman equation, namely, one that involves a growth condition; and its solution requires a different approach.

Ghosh and Weerasinghe (2007) extends Ata et al. (2005) by incorporating holding costs and allowing the system manager to choose the bounded interval on which the process lives endogenously. Ghosh and Weerasinghe (2010) extends this work by introducing abandonments; also see Rubino and Ata (2009), Ghamami and Ward (2013), Ata and Tongarlak (2013), and Sun (2020) for similar formulations with abandonments. In other related work, Ata et al. (2019) approximates a gleaning operation using a drift rate control problem, and derives a nested threshold policy as an optimal staffing policy. The authors derive an approximation in the many server asymptotic regime. The authors derive an approximation in the many server asymptotic regime. Consequently, the drift rate of their control problem has a different structure. This makes their analysis inapplicable in our context.

Recent work by Ata and Barjesteh (2019) studies dynamic pricing, scheduling and outsourcing decision for a make-to-stock manufacturing system. They approximate this problem by a drift-rate control problem with a quadratic cost of control. Leveraging the elegant structure of the Riccati equation that arises as the Bellman equation, the authors derived a closed form solution for the optimal dynamic prices in terms of Airy functions. Several researchers established the asymptotic optimality of their proposed policies in the heavy traffic limit. For example, Budhiraja et al. (2011) studies the service rate and admission control for a queueing network and derives policies that are asymptotically optimal; also see Bell and Williams (2001, 2005), Ata and Kumar (2005), Ata and Olsen (2009, 2013) for asymptotically optimal policies in other related settings.

Many researchers have used Markov decision process formulations to study admission control or service rate problems; see for example Crabill (1972, 1974). Stidham and Weber (1989) studies monotone control policies for dynamic control of service and arrival rates to a queueing network. George and Harrison (2001) considers the dynamic service rate control problem for an M/M/1 queue and derives the optimal policy essentially in closed form. Similarly, Ata and Shneorson (2006) considers a dynamic arrival and service rate control problem for an M/M/1 queue. Ata (2005) and Ata and Zachariadis (2007) consider related service rate control problems for queueing systems arising in wireless communications applications and solve them explicitly; also see Adusumilli and Hasenbein (2010) and Kumar et al. (2013) for studies of other related questions.

2 Model

All stochastic processes live on a filtered probability space that satisfies the usual conditions; see Harrison (2013). In the absence of control, we model the participant queue as a reflected Brownian motion with drift parameter and variance parameter . At any point in time, the system manager can engage in activities . Activity increases the drift rate by , (i.e. it increases the participant arrival rate) but costs per unit of time. We assume , and model the system manager’s control by a K-dimensional process , where

| (3) |

The system manager’s problem can then be expressed as follows: Choose adapted to so as to

| (4) | |||

| such that | |||

| (5) | |||

| (6) | |||

| (7) | |||

| (8) | |||

| (9) |

where is a Brownian motion with almost surely. Moreover, is a martingale with respect to the filtration .

Constraint (7) relaxes the requirement that to allow . As the reader will see below, this relaxation is immaterial to our results because the optimal policy we propose sets for all . But, it simplifies the analysis.

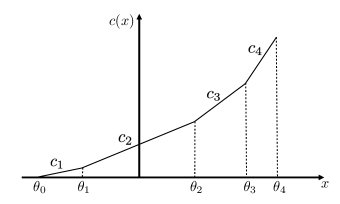

To simplify the formulation further, let , and define for ,

Letting , and for , it is straightforward to show that

| (12) |

Figure 1 shows an illustrative function with .

Using this cost function, consider the following formulation: Choose the drift rate process taking values in A so as to

| (13) | |||

| such that | |||

| (14) | |||

| (15) | |||

| (16) | |||

| (17) |

Proposition 1

Formulations (4)-(9) and (13)-(17) are equivalent in the following sense: For any feasible policy of formulation (4)-(9), there exists a feasible policy of formulation (13)-(17) whose average cost is less than or equal to that of . Similarly, for any feasible policy of formulation (13)-(17), there is a feasible poligy of formulation (4)-(9) that has the same average cost. Moreover, the two formulations have the same average cost.

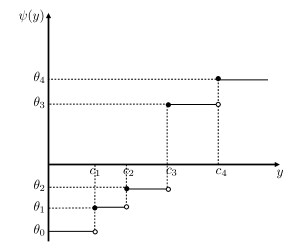

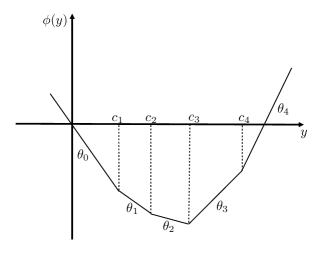

Henceforth, we shall focus attention on formulation (13)-(17). To facilitate the analysis, define the convex conjugate of as follows:

| (18) |

Note that is Lipschitz continuous, as stated in the following lemma.

Lemma 1

The function is Lipschitz continuous with Lipschitz constant .

It is straightforward to argue that is well-defined and finite for all , and that there is a smallest achieving the maximum. That is, the following is well defined, too.

It is straightforward to show that

| (22) |

and

| (26) |

Figures 2(a) and 2(b) display illustrative and functions, respectively. It is immediate from (22) and (26) that for .

3 Solution to the Diffusion Control Problem

In what follows, we restrict attention to stationary Markov policies. Namely, the drift rate chosen at time depends only on the current queue length . Therefore, an admissible policy is a function . As a preliminary to introducing the Bellman equation, we define as the space of functions that are twice continuously differentiable up to the boundary. Similarly, we define as the space of functions that are continuously differentiable up to the boundary.

Consider the Bellman equation associated with formulation (13)-(17): Find a constant and a function that jointly solve the following:

| (27) | |||

| (28) |

To simplify the Bellman equation, let . Substituting this into Equations (27)-(28) and rearranging the terms gives the following:

| (29) | |||

| (30) |

Note that the Bellman equation does not involve the unknown function itself. So it is really a first-order differential equation. Letting and using , we can rewrite the Bellman equation more succinctly as follows: Find a constant and a function that jointly solve the following:

| (31) | |||

| (32) |

The solution to the Bellman equation is derived in Subsection 3.1. Next, we propose a candidate policy given that solution and prove its optimality in Section 3.2. This policy will be characterized further in Section 3.3.

As the reader will see below, the function efficiently captures all aspects of the cost function that are relevant for our purposes. Moreover, the optimal policy will be characterized as follows:

| (33) |

which can be expressed as a nested-threshold policy; see Subsection 3.2.

As a preliminary to proving that this candidate policy is optimal, next we define the class of admissible policies. This definition simply ensures that the system workload is stable under an admissible policy.

Definition (Admissible Policies).

Let . Clearly, . A policy is admissible if it is stationary Markov and if there exists such that for .

Recall that , which ensures there exists an admissible policy.

3.1 Solution to the Bellman Equation

To facilitate the analysis to follow, let and for , consider the following initial value problem, denoted by IVP(), that is closely related to the Bellman equation:

| (34) | ||||

| (35) |

The following lemma establishes the existence and uniqueness of the solution to the IVP(). Its proof is standard, and thus, omitted; see for example Theorem of Keller (2018) for a version of this result on a bounded interval, which can easily be extended to the positive real line.

Lemma 2

In what follows, we denote the solution to the IVP() by and study its properties as varies. Ultimately, we show that there exists a unique such that satisfies the growth condition in Equation (32) and thus, () solve the Bellman equation. Indeed, much of the technical subtlety of the analysis stems from verifying this growth condition, which is crucially used in the proof of optimality of the candidate policy given in Equation (33).

Lemmas 4 and 5 are auxiliary results for the analysis to follow. Lemma 3 is the Gronwall’s Inequality, which is used in establishing the continuity part of Lemma 4. It is stated for completeness; for a proof, see, for example, Ata et al. (2019). Lemma 4 helps us study how the solution of IVP() varies with and is proved in Appendix A.

Lemma 3

Let be a non-negative function such that

for some constants . Then .

Lemma 4

For , is increasing and continuous in .

To facilitate the analysis, define the following two subsets of :

Lemma 5

For each , we have either or , i.e. and . Moreover, for , if , then .

Lemma 6

The sets , are nonempty. That is, , . Moreover, .

Letting , the next lemma shows .

Lemma 7

We have that .

Proof. Suppose not. Then is first increasing and then decreasing. Let and fix such that , and let . Because is continuous and increasing in , there exists such that and

| (36) |

Once again, because is increasing in , we also have

| (37) |

Combining (36) and (37) gives

,

which contradicts that , in particular, that is increasing.

The following is a corollary of Lemmas 5, 6, and 7.

Corollary 1

We have that .

The next result establishes the desired growth condition, paving the way to solving the Bellman equation.

Lemma 8

The function grows linearly. In particular, .

Proof. First note that because as for , there exists such that for . Thus,

Fix such an and note that Equation (34) simplifies to the following:

Rearranging terms, we write

Multiplying both sides by and integrating over give the following:

That is, the following holds:

| (38) |

where . We calculate by integration by parts:

Substituting this into Equation (38) gives

Rearranging the terms gives

That is, we have that

| (39) |

We claim that is such that

| (40) |

so that

| (41) |

which proves the statement. Suppose that (40) does not hold. Then we must have

| (42) |

Otherwise, i.e., if the left-hand side of Equation (42) is negative, then as , which contradicts that . However, Equation (42) implies by continuity that there exists sufficiently small such that (42) holds for , which, in turn, implies that

i.e., that . Thus, we must have , which contradicts that . Therefore, (40) - (41) holds.

The following corollary is then immediate.

Lastly, to provide a solution of the Bellman equation, define

| (43) |

3.2 The candidate policy and its optimality

This subsection first establishes the optimality of the candidate policy introduced above. Recall that the proposed policy is given as follows:

| (44) |

Theorem 1 below verifies the optimality of this candidate policy. As a preliminary to its proof, the following lemma proves useful properties of the function defined in Equation (43); see Appendix A for its proof.

Lemma 9

Under any admissible policy, we have that

Theorem 1

The candidate policy for is optimal, and its long-run average cost is .

Proof. Note from Equations (27)-(28) and (33) that the candidate policy satisfies the following:

| (45) |

Similarly, for an arbitrary admissible policy , we have

| (46) |

Also, for any admissible policy , applying Ito’s lemma to gives

| (47) |

see Chapters 4 and 6 of Harrison (2013). By taking the expectations of both sides of Equation (47), it follows from Lemma 9 that

| (48) |

For any admissible policy , combining Equations (46) and (48) gives

Rearranging the terms gives

Combining this with Lemma 9 gives

Similarly, for candidate policy , combining Equations (45) and (48) gives

Then it follows from Lemma 9 that

Therefore, the candidate policy is optimal and its long-run average cost is .

3.3 Further Characterization of the Optimal Policy

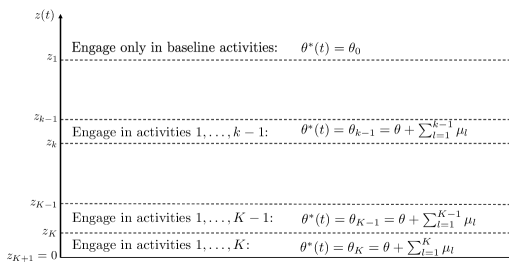

This subsection characterizes the optimal policy as a nested threshold policy and the corresponding thresholds. Recall from Corollary 2 that is strictly increasing, and hence, invertible. Denoting that inverse by and letting for notational convenience, we define the thresholds:

| (49) |

It follows from the monotonicity of that . Defining for notational convenience, it follows from Equation (22) and (44) that the candidate policy satisfies the following:

| (50) |

In other words, the candidate policy is a nested-threshold policy, see Figure 3. The following corollary is immediate from Theorem 1.

Corollary 3

The nested-threshold policy is given in Equation (49) is optimal.

In order to facilitate the computation of the thresholds , we next provide a closed-form formula for ; and the characterization of amounts to inverting this function, cf. Equation (49). For notational brevity, we define for as follows:

which implicitly assumes . The following proposition characterizes .

Proposition 3

We have the following:

| (53) |

for , where . Moreover, for and , we have that

| (56) |

where .

Proof. First, we prove (53). For , using (26), the IVP() in Equation (34) can be written more explicitly as follows:

| (57) |

If , then this simplifies to the following:

Integrating both sides of this and using the boundary condition yields the result:

Now, consider the case . Recall and , and note that is given as follows:

Then, it suffices to show that . To this end, rearranging the terms in Equation (57) yields the following:

Multiplying both sides of the equation with the integrating factor gives the following:

Then, integrating both sides and using the boundary condition gives that

Rearranging the terms on the right hand side and dividing both sides of the equation with gives the desired result:

Next, consider for . Then, as above, using (26), the IVP() given in Equation (34) can be written more explicitly as follows: The function solves the following

| (58) | |||

If , then this simplifies to the following:

Integrating both sides of this over and using the boundary condition that gives the desired result.

Now, consider the case . It suffices to show that . Proceeding as above and using Equation (58) yields:

Rearranging the terms and using the boundary condition give

Further rearranging the terms gives

which then yield the desired result, completing the proof.

4 A Numerical Example

We compare the performance of the dynamic policy with benchmark static policies using a numerical example. In particular, we consider static policies that set for . Under a static policy, the queue length process is a reflected Brownian motion. As such, the following holds (see Harrison 2013):

Then letting denote the long-run average cost of the static policy for , we have that

| (59) |

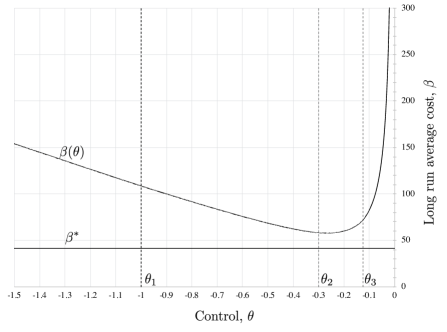

For the following numerical example, let , , , , , , , , , , , , and . Recall that the values correspond to the cost rate of increasing the level of promotion activities. For example, suppose the promotion activities in increasing order of cost were: (i) sending mass emails, (ii) advertising online, (iii) advertising on television and radio, and (iv) outreach activities by public health officials. The static policy of sending mass emails () would incur cost rate , the static policy of advertising online () would incur cost rate , etc.

We compare the long run average cost of each static policy, , , given by (59), with the long run average cost of the dynamic policy ( in Theorem 1). Figure 4 shows that the optimal static policy is , which corresponds to always using the promotion activities of sending mass emails and advertising online. The long run average cost of this static policy is , whereas the long run average cost of the dynamic policy is only . Thus, the cost savings of the dynamic policy over the best static policy is 29%.111An alternate “randomized” static policy that combines static policy with probability 0.85 and static policy with probability 0.15 would achieve a long run average cost of 57.9. This is slightly lower than simply consistently using policy , but the difference is negligible – the dynamic policy still achieves a cost savings of 28.5%.

5 Concluding Remarks

Motivated by a public health service context, we studied a diffusion control problem where a system manager can deploy costly promotion activities to increase the rate of participant inflow. We developed a threshold policy and derived explicit queue length thresholds for progressively deploying these promotion activities. Using a numerical study, we showed the potential cost savings of the dynamic policy relative to the optimal static policy can be significant (i.e., in our example, the cost savings was 29%). Our research makes a methodological contribution by deriving the solution of a drift-rate control problem on an unbounded domain with state costs.

References

- Adusumilli and Hasenbein (2010) Adusumilli, K. M. and J. J. Hasenbein (2010). Dynamic admission and service rate control of a queue. Queueing Systems 66(2), 131–154.

- Ata (2005) Ata, B. (2005). Dynamic power control in a wireless static channel subject to a quality-of-service constraint. Operations Research 53(5), 842–851.

- Ata (2006) Ata, B. (2006). Dynamic control of a multiclass queue with thin arrival streams. Operations Research 54(5), 876–892.

- Ata and Barjesteh (2019) Ata, B. and N. Barjesteh (2019). Dynamic Pricing of a Multiclass Make-to-Stock Queue. Available at SSRN: https://ssrn.com/abstract=3464763 or http://dx.doi.org/10.2139/ssrn.3464763.

- Ata et al. (2005) Ata, B., J. M. Harrison, and L. A. Shepp (2005). Drift rate control of a brownian processing system. The Annals of Applied Probability 15(2), 1145–1160.

- Ata and Kumar (2005) Ata, B. and S. Kumar (2005). Heavy traffic analysis of open processing networks with complete resource pooling: Asymptotic optimality of discrete review policies. Annals of Applied Probability 15, 331–391.

- Ata et al. (2019) Ata, B., D. Lee, and E. Sonmez (2019). Dynamic volunteer staffing in multicrop gleaning operations. Operations Research 67, 295–314.

- Ata and Olsen (2009) Ata, B. and T. L. Olsen (2009). Near-optimal dynamic lead-time quotation and scheduling under convex-concave customer delay costs. Operations Research 57(3), 753–768.

- Ata and Olsen (2013) Ata, B. and T. L. Olsen (2013). Congestion-based leadtime quotation and pricing for revenue maximization with heterogeneous customers. Queueing Systems 73(1), 35–78.

- Ata and Shneorson (2006) Ata, B. and S. Shneorson (2006). Dynamic control of an m/m/1 service system with adjustable arrival and service rates. Management Science 52(11), 1778–1791.

- Ata and Tongarlak (2013) Ata, B. and M. H. Tongarlak (2013). On scheduling a multiclass queue with abandonments under general delay costs. Queueing Systems 74(1), 65–104.

- Ata et al. (2023) Ata, B., M. H. Tongarlak, D. Lee, and J. Field (2023). A dynamic model for managing volunteer engagement. Operations Research, forthcoming.

- Ata and Zachariadis (2007) Ata, B. and K. E. Zachariadis (2007). Dynamic power control in a fading downlink channel subject to an energy constraint. Queueing Systems 55(1), 41–69.

- Bell and Williams (2005) Bell, S. and R. Williams (2005). Dynamic scheduling of a parallel server system in heavy traffic with complete resource pooling: Asymptotic optimality of a threshold policy. Electronic Journal of Probability 10(33), 1044–1115.

- Bell and Williams (2001) Bell, S. L. and R. J. Williams (2001). Dynamic scheduling of a system with two parallel servers in heavy traffic with resource pooling: asymptotic optimality of a threshold policy. The Annals of Applied Probability 11(3), 608–649.

- Budhiraja et al. (2011) Budhiraja, A., A. P. Ghosh, and C. Lee (2011). Ergodic rate control problem for single class queueing networks. SIAM Journal on Control and Optimization 49(4), 1570–1606.

- Crabill (1972) Crabill, T. B. (1972). Optimal control of a service facility with variable exponential service times and constant arrival rate. Management Science 18(9), 560–566.

- Crabill (1974) Crabill, T. B. (1974). Optimal control of a maintenance system with variable service rates. Operations Research 22(4), 736–745.

- George and Harrison (2001) George, J. M. and J. M. Harrison (2001). Dynamic control of a queue with adjustable service rate. Operations research 49(5), 720–731.

- Ghamami and Ward (2013) Ghamami, S. and A. R. Ward (2013). Dynamic scheduling of a two-server parallel server system with complete resource pooling and reneging in heavy traffic: Asymptotic optimality of a two-threshold policy. Mathematics of Operations Research 38(4), 761–824.

- Ghosh and Weerasinghe (2007) Ghosh, A. P. and A. P. Weerasinghe (2007). Optimal buffer size for a stochastic processing network in heavy traffic. Queueing Systems 55(3), 147–159.

- Ghosh and Weerasinghe (2010) Ghosh, A. P. and A. P. Weerasinghe (2010). Optimal buffer size and dynamic rate control for a queueing system with impatient customers in heavy traffic. Stochastic Processes and Their Applications 120(11), 2103–2141.

- Harrison (1988) Harrison, J. M. (1988). Brownian models of queueing networks with heterogeneous customer populations. In Stochastic differential systems, stochastic control theory and applications, pp. 147–186. Springer.

- Harrison (2013) Harrison, J. M. (2013). Brownian Models of Performance and Control (1st ed.). Cambridge University Press.

- Harrison and Wein (1989) Harrison, J. M. and L. M. Wein (1989). Scheduling networks of queues: Heavy traffic analysis of a simple open network. Queueing Systems 5(4), 265–279.

- Harrison and Wein (1990) Harrison, J. M. and L. M. Wein (1990). Scheduling networks of queues: Heavy traffic analysis of a two-station closed network. Operations research 38(6), 1052–1064.

- Keller (2018) Keller, H. B. (2018). Numerical Methods for Two-Point Boundary-Value Problems. Dover Publications.

- Kumar et al. (2013) Kumar, R., M. E. Lewis, and H. Topaloglu (2013). Dynamic service rate control for a single-server queue with markov-modulated arrivals. Naval Research Logistics (NRL) 60(8), 661–677.

- Rubino and Ata (2009) Rubino, M. and B. Ata (2009). Dynamic control of a make-to-order, parallel-server system with cancellations. Operations Research 57(1), 94–108.

- Stidham and Weber (1989) Stidham, S. and R. R. Weber (1989). Monotonic and insensitive optimal policies for control of queues with undiscounted costs. Operations research 37(4), 611–625.

- Sun (2020) Sun, X. (2020). Scheduling queues with customer transfers. Working Paper.

Appendix A Proofs

Proof of Proposition 1.

Let be a feasible policy for formulation (4)-(9) and set for . Clearly, and is feasible for for . Similarly, given a feasible policy for formulation (13)-(17), we set

| (60) |

Clearly, for all . Thus, is feasible for formulation (4)-(9). Also, it is easy to see from Equation (12) that for . These imply that the two formulations have the same long-run average cost.

Proof of Lemma 4.

First, we prove that for and . Fix . Define and note that is a decreasing function. Then substituting in Equation (34) and rearranging the terms, we arrive at the following: For ,

| (61) |

We argue by contradiction. Suppose for some . Let . If , then by continuity of , we conclude that

| (62) |

Multiplying both sides of Equation (61) with and integrating over give the following:

| (63) |

Considering Equation (63) for and and taking the difference give

| (64) |

where the inequality follows from Equation (63) and the monotonicity of . The contradiction reached in Equation (64) show when .

Next, we consider the case of . If , then there exists a sequence such that as and . In particular,

| (65) |

Because , taking the limit in Equation (65) as gives . Combining this with Equation (34) gives

or, , which is a contradiction, proving for .

Second, we prove that is continuous in on . To this end, fix and note from Equation (34) that

Integrating both sides of this on , we have that

Taking the difference gives

Take the absolute value of both sides and using the Lipschitz continuity of (see Lemma 1), we conclude that

Note that letting , we have for that

Proof of Lemma 5.

We proceed in several steps. First, we prove that for all , strictly increases its maximum. Suppose not. Then by continuity of and its derivative, there exists such that

Then we write by Equation (34) that

| (66) | ||||

| (67) |

Subtracting (66) from (67) yields:

which is a contradiction.

Second, we show that is either strictly increasing or it is first increasing then decreasing. Because strictly increases to its maximum, if it never reaches to its maximum, then we are done. Otherwise, let denote the maximizer of . It suffices to show that is decreasing on . Suppose not. Then there exists , such that

It also follows from Equation (34) that

| (68) | ||||

| (69) |

Subtracting (68) from (69) yields:

which is a contradiction.

Third, we show that for , if is increasing, then . Suppose not, i.e., is bounded. Then as . Recall from Equation (34) that

which implies that for . This is possible only if for large and that as . That is,

which contradicts that is bounded.

So far, we proved that for each , it belongs to either or . Thus, . Clearly .

To conclude the proof, it remains to show that if , then for all . Let and suppose that there exists such that . That is, is first increasing, then decreasing. Then because as , there exists such that , which contradicts that is increasing in (see Lemma 4).

Proof of Lemma 6.

We first prove that and . That is, for , is strictly increasing in and that as . Recall from Equation (34) that

| (70) | ||||

| (71) |

Also note that for all . Thus,

| (72) |

Rearranging the terms, we write

| (73) |

Multiplying both sides by gives the following

Integrating both sides and using Equation (71) give the following:

That is,

| (74) |

where the last term can be integrated by parts as follows:

Substituting this into Equation (74) gives the following:

Therefore, we conclude that

| (75) |

Thus, for , we have that as . Moreover, note from Equation (73) that

| (76) |

Because by assumption, substituting (75) into (76) gives

where the last inequality follows because and . This proves that is strictly increasing for , proving the claim.

Next, we prove by contradiction. As a preliminary, define and note that , is decreasing and increasing on . We have the following three cases to consider:

Case 1. . In this case, is decreasing on and .

Case 2. and . In this case, and .

Case 3. and . In this case, and .

Suppose , i.e., increases strictly to for all by Lemma 5. In particular, its inverse is well defined and strictly increasing. We will illustrate a in each case that contradict this. To this end, for , let

Next, we consider each of the above cases.

Case 1. In this case, because and . Moreover, for , we have that

| (77) |

Recall from Equation (34) that

| (78) | ||||

| (79) |

For , let . Then substituting (77) into (78) gives

because . Rearranging the terms further gives

Multiplying both sides by gives

Integrating both sides from 0 to gives:

| (80) |

As done earlier in the proof, the last term on the right-hand side of (80) can be integrated by parts to give the following:

Substituting this into Equation (80) gives

Thus, we have that

Differentiating both sides gives

Rearranging the terms, we can rewrite this as follows:

| (81) |

Next, we verify that for ,

| (82) |

Recall that . Note by definition of that

| (83) |

Also note from Equation (34) that

| (84) |

where the first inequality follows because for , and the second inequality follows because we restrict attention to . Integrating both sides of Equation (84) on gives

Consider the derivative of the second term of the product on the right-hand side of Equation (81):

Thus, we conclude from Equation (82) that

In particular, combining this with Equation (81) gives

Letting , we conclude that , where , which contradicts that is strictly increasing.

To conclude the proof, we consider cases 2 and 3 and treat them simultaneously. Recall that , i.e., . Also note from Equation (34) that

In particular,

| (85) |

where . This follows because for in cases 2 and 3. Integrating both sides of (85) on gives

from which it follows that

| (86) |

where the last inequality follows because we restrict attention to .

Proof of Lemma 9.

To establish part i), it suffices to show the following (see Harrison 2013):

| (88) |

To verify (88), recall that and consider the following:

| (89) |

Recall that has linear growth. Thus, there exists exists such that

| (90) |

Substituting this into Equation (89) yields

It is straightforward to show that the right-hand side is finite, proving part i).

To establish part ii), recall that under an admissible policy , such that for . Fix an admissible policy and the associated . Also, let be a Brownian motion, and let be the associated reflected Brownian motion. It is straightforward to argue that is stochastically larger than the (scaled) queue-length process under . Moreover, note that

In particular, we have

Because has linear growth (see Equation (90)), we conclude that

Thus, we have that

| (91) |

where the last inequality follows is stochastically larger than .