General spatio-temporal factor models for high-dimensional random fields on a lattice

Abstract

Motivated by the need for analysing large spatio-temporal panel data, we introduce a novel dimensionality reduction methodology for -dimensional random fields observed across a number spatial locations and time periods. We call it General Spatio-Temporal Factor Model (GSTFM). First, we provide the probabilistic and mathematical underpinning needed for the representation of a random field as the sum of two components: the common component (driven by a small number of latent factors) and the idiosyncratic component (mildly cross-correlated). We show that the two components are identified as . Second, we propose an estimator of the common component and derive its statistical guarantees (consistency and rate of convergence) as . Third, we propose an information criterion to determine the number of factors. Estimation makes use of Fourier analysis in the frequency domain and thus we fully exploit the information on the spatio-temporal covariance structure of the whole panel. Synthetic data examples illustrate the applicability of GSTFM and its advantages over the extant generalized dynamic factor model that ignores the spatial correlations.

keywords:

[class=MSC]keywords:

, and

1 Introduction

1.1 Big data on spatio-temporal processes

Many data analysis problems in economics, finance, medicine, environmental sciences, and other scientific areas need to conduct inference on random phenomena observed over time and registered at different locations.

Supervised and unsupervised learning methods for random fields (henceforth, rf) are suitable tools for the statistical analysis of this type of data: they provide an understanding of the key spatial and/or temporal dynamics of the studied phenomena. For instance, rf are routinely applied in medicine for fMRI data analysis (see e.g. Lazar, 2008, Ch.6), in geostatistics for satellite images analysis (see e.g. Cressie, 2015; Cressie and Wikle, 2015), in natural sciences for modeling complex phenomena (see e.g. Vanmarcke, 2010; Christakos, 2017 for applications in physics and engineering), in economics for the analysis of spatial panel data (see e.g. Baltagi, 2008) just to mention few book-length introductions.

In this paper we consider datasets containing records on spatio-temporal rf over a lattice; see e.g. Cressie (2015). We let denote the spatial position in and represent the time index—in principle, the dimension of the spatial lattice can be larger than two. For instance, the points can be: in geostatistics, geographical regions represented as a network with a given adjacency matrix; in image analysis, the position of pixels in an image. At each and time , the object of interest is the -dimensional rf: , for . Typical inference goals for these types of data include e.g. constructing and analyzing generative models, quantifying spatio-temporal dependency, prediction or image restoration.

One key aspect related to the statistical analysis of this data is that is of the order of several hundreds and the number of locations and time points may have the same magnitude. A common approach to analyze the resulting large spatio-temporal rf datasets is to resort on standard time series methods, like e.g. spatio-temporal autoregressive models (see e.g. Cressie and Wikle, 2015). Nevertheless, because of the high-dimensionality, standard parametric approaches are not feasible (e.g. in a vector autoregressive model with one time lag for the time series available at each location , the number of parameters is ) and dimensionality reduction techniques are needed.

To solve the curse of dimensionality, one may look at the literature on high-dimensional time series and think of relying on factor models, which allow for a low-dimensional description of high-dimensional data and a limited number of factors capture the common behaviour of the studied phenomena (see, e.g., Forni et al., 2000; Stock and Watson, 2002; Bai and Ng, 2002; Lam and Yao, 2012; Fan, Liao and Mincheva, 2013, among many others).

Among the existing approaches to factor analysis, the General Dynamic Factor Model (GDFM) of Forni et al. (2000) defines the most general, nonparametric, factor model which is based on a decomposition of the observations into the sum of two mutually orthogonal (at all leads and all lags) components: the common component (driven by a small number of factors) and the idiosyncratic component (mildly cross-correlated). This decomposition looks attractive since it is able to capture not only contemporaneous correlations but all leading and lagging co-movements in time among the components of the the time series.

In the case of a rf the set of correlations among its components is much richer. Indeed, an observation at time and spatial location might depend on observations at time in the same location, or on observations at the same time but at spatial location , but also on observations at time and spatial location . Thus, factor models for spatio-temporal rf have to account for this richer correlation structure.

1.2 Our contributions: the paper in brief

We introduce the General Spatio-Temporal Factor Model (GSTFM), a new a class of factor models which allows us to reduce the dimensionality of a high-dimensional spatio-temporal datasets by capturing all relevant correlations, across both time and space. Our results contribute to different streams of literature on rf theory and inference on high-dimensional data.

(i) We derive the decomposition of a spatio-temporal rf into a common component, which depends on unobservable factors, and an idiosyncratic component, see Theorem 4.1. To obtain this result, we need to tackle an important challenge rooted into probability theory: because of the lack of ordering in , the GDFM results already available in the literature on high-dimensional time series cannot be applied in our setting. Indeed, the extant results are available for discrete time (regularly spaced) time series indexed by and rely on a generalization of the Wold representation to the case of infinite dimensional stationary processes as derived by Forni and Lippi (2001) and Hallin and Lippi (2013). Similar concepts are not readily available for a rf indexed in . As a possible solution, we might specify a notion of spatial past, selecting e.g. the half-plane or the quarter-plane formulation. However, this choice entails the drawback that different versions of the Wold decomposition (see Mandrekar and Redett, 2017) are available, with no obvious indication on which one has to be preferred in our context. To avoid this issue, we resort on the Fourier analysis in the frequency domain. This methodological approach requires a careful extension to rf of the time series notions of canonical isomorphism, dynamic averaging sequences, aggregation space, dynamic eigenvalues and eigenvectors, spatio-temporal linear filters, idiosyncratic variables, and many others. Our theoretical developments would not be justified without these preliminary results. Clearly, our results nest as a special case the GDFM results.

(ii) The mentioned decomposition is at the population level: to apply our methodology we need an estimation procedure of the common component. To this end, we derive a complete and operational estimation theory, which contributes to the literature on the statistical analysis of rf. More in detail, we build on Deb, Pourahmadi and Wu (2017) and, making use of a suitable notion of functional dependence measure for spatio-temporal rf, we derive a consistent estimator of a high-dimensional spectral density matrix. We provide its statistical guarantees, proving consistency (with rate) of the proposed estimator. These general results (which are of their own theoretical interest, see Appendix D) substantially extend the applicability of spectral analysis to non-linear, non-Gaussian, or non-strong mixing rf. Thanks to these novel results, we derive the rate of converge of our estimator of the common component of spatio-temporal rf. The asymptotic regime that we consider is very flexible: it simply requires that the number of locations and the time diverge, but does not need a specification of the type of asymptotics (in-fill or a long-span); see Theorems 6.1 and 6.2 for the mathematical detail.

(iii) The above theoretical developments hinge on a central aspect: the selection of the number of latent factors. We take care of this aspect and state a simple and operational criterion, providing its theoretical underpinning in Theorem 7.1.

(iv) We consider the computational aspects needed to implement our methodology by studying synthetic data examples (see the supplementary material for additional numerical exercices), in which the underlying data generating process involves different types of convolutions over the lattice, which in turn imply different levels of spatio-temporal aggregation.

1.3 Related work

In the literature on panel data and time series, dimensionality reduction is often achieved by factor models, which allow for a low-dimensional description of high-dimensional data. Modern factor models essentially originate in four pioneering contributions: Geweke (1977), Sargent and Sims (1977), Chamberlain (1983), and Chamberlain and Rothschild (1983). The reference factor model for this work is the GDFM introduced by Forni et al. (2000) and Forni and Lippi (2001), where few latent factors capture all leading and lagging main comovements among the observed variables. The GDFM was then studied by Hallin and Liška (2011) in presence of a block structure in the data (where blocks can be seen are spatial locations), and further developed in a predictive context by Forni et al. (2005, 2015, 2017). A criterion for the number of factors is proposed by Hallin and Liška (2007). The GDFM has been successfully applied to many macroeconomic and financial time series problems; see, e.g., Altissimo et al. (2010); Cristadoro et al. (2005); Proietti and Giovannelli (2021); Hallin and Trucíos (2021); Trucíos et al. (2022).

There are many other influential papers on factor models as, e.g., Stock and Watson (2002); Bai and Ng (2002); Lam and Yao (2012); Fan, Liao and Mincheva (2013).

Spatial factor models and related techniques for the analysis of large spatial datasets are also available in the statistical literature. For instance, Christensen and Amemiya (2002) introduce a generalized shifted-factor model for purely spatial data; Wang and Wall (2003) study correlations which are caused by a common spatially correlated underlying factors; Heaton et al. (2018) consider many methods for analyzing large spatial data; Park et al. (2009); Bodelet and La Vecchia (2022) propose a semiparametric (robust) factor model which is connected to the GDFM and achieves dimensionality reduction of spatio-temporal data.

Last, a spatio-temporal dataset can in principle also be modeled as a tensor time series, with some of its modes corresponding to the spatial dimensions. Thus, a spectral approach to the analysis of tensor data represents a possible alternative. Factor models for tensor time series data have recently been studied by many authors, see, e.g., Chen, Yang and Zhang (2022); Chang et al. (2023). However, none of these approaches is dynamic in the sense that it allows for the factors, which might be tensors too, to be loaded by the data with lags.

1.4 Outline

The paper has the following structure. In Section 2 we provide a motivating example for the necessity of introducing a new class of dynamic spatio-temporal factor models. In Section 3 we review main concepts for the spectral analysis of rf. In Sections 4-5 we derive the representation theorem for the GSTFM and we define the spatio-temporal dynamic principal components. In Section 6 we present our estimator and its asymptotic properties. In Section 7 we introduce a criterion to estimate the number of factors. In Section 8 we show numerical results on simulated data. In Section 9 we conclude.

In the supplementary material: we prove all theoretical results (Appendices A, B, C, E, and F), we prove new results for the estimation of a large spectral density of a spatio-temporal rf (Appendix D), we give an algorithm to estimate the number of factors (Appendix G), we apply our methodology to fMRI data (Appendix H), and we provide further numerical results (Appendix I).

1.5 Notation

Given a complex matrix , we denote by the complex conjugate of the transposed of , by its transposed, by its complex conjugate, and for a real matrix we have and . A similar notation holds for complex and real vectors. Given a complex scalar its complex conjugate is denoted as . Given two complex row vectors and we let and is the or Euclidean norm. Real or integer vectors are always column vectors and given two such vectors and we let and . For a complex scalar we have . We use the notation for the Lebesgue measure either on or on or on . When no ambiguity can arise, we use the shortcuts and .

2 Motivating example

To motivate our investigation, we illustrate via numerical examples, the inadequacy of the classical GDFM by Forni et al. (2000) in the spatio-temporal setting. Assume we are given realizations of random variables in spatial locations (therefore, the total number of locations is ) and time points. We organize the data into an -dimensional rf

Under our GSTFM the -th component of is such that , for . The term is called common component and it is a linear combination of latent rf, with , located at the same spatial location and time period as well as at neighbouring spatial points and at various lags. The term is called idiosyncratic component and is assumed to be weakly cross-sectionally correlated. In Theorem 4.1 we show that under the considered setting the presence of an eigen-gap in the eigenvalues of the spatio-temporal spectral density matrix (see Section 3.2 for a definition) is a key distinctive feature. In particular, the largest eigeinvalues of the spatio-temporal spectral density matrix diverge as while the remaining stay bounded if and only if the common component is driven by spatio-temporal factors. As , we can then disentangle the common and idiosyncratic components and, consequently, we can identify the GSTFM. This is the main feature of general factor models, sometimes called blessing of dimensionality, as opposed to the curse of dimensionality typically affecting large dimensional models.

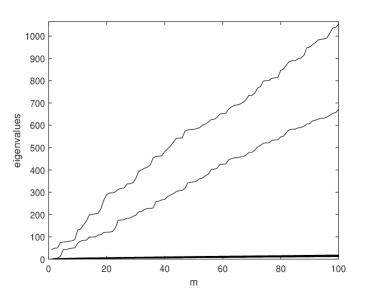

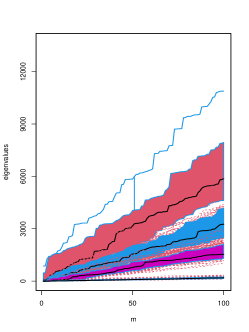

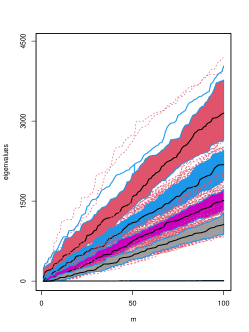

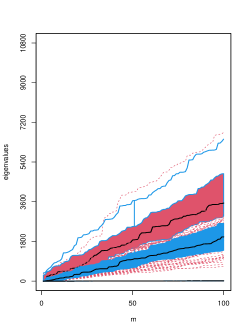

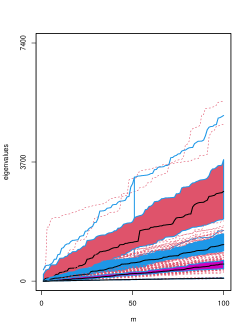

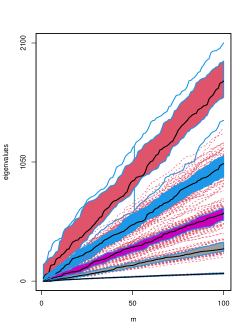

To verify this phenomenon we simulate the common component of the GSTFM with common factors, loaded according to a quite general and commonly encountered configuration (see Model (a) in (23) for details) of the spatio-temporal dependencies. For ease of simulation, the idiosyncratic component is generated from the standard normal distribution. Then, for different subsets of dimension we estimate the spatio-temporal spectral density matrix of and we compute its largest eigenvalues, averaged across all frequencies. In Figure 1, we display these eigenvalues as a function of the cross-sectional dimension : we clearly see that the eigen-gap becomes more and more pronounced as increases, a manifestation of the blessing of dimensionality.

|

|

If instead we decide to resort on the extant GDFM, then the natural thing to do is to stack at each time point the data into an -dimensional time series (the order in which the locations and variables are stacked is irrelevant for this discussion):

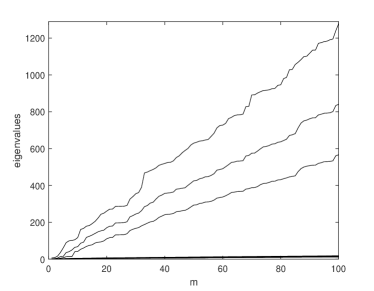

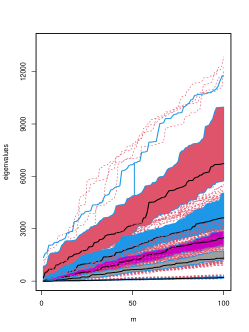

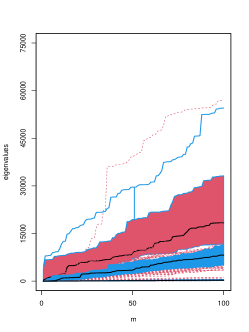

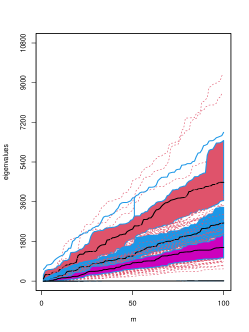

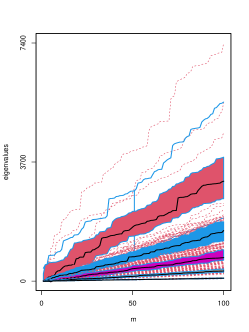

Notice that the rf and the time series contain the same data points but encoded in different ways. Under the GDFM the -th component of is also such that , for , where now is a linear combination of latent time series, with , at the same time period as well as at various lags. Given that the stacking procedure yields a very large dataset, the asymptotic results in Forni et al. (2000) should apply: the eigenvalues of the estimated spectral density of should display an eigen-gap, between the -th and -th eigenvalues, increasing as . In fact, if there is no spatial correlation in the data, then we would expect to have , as the only correlations left would be cross-sectional and temporal and the GDFM is designed precisely to capture them. But, if there are spatial correlations, then the proposed stacking approach is likely to be flawed: ignoring spatial correlations might generate spurious factors. So if the data follows a GSTFM with factors, but instead we fit a GDFM, at best we might find a number of factors . Indeed, if there are ignored spatial correlations, the GDFM might not even be correctly identified. To show this, we consider again the data simulated from the GSTFM and that yield Figure 1. We estimate the spectral density of the stacked vector for and, in Figure 2, we display, as functions of , the ten largest corresponding eigenvalues averaged over all frequencies. Since now , we might expect an eigen-gap even more evident than the one clearly visible in Figure 1. In contrast, in Figure 2 no eigen-gap is detectable at all, even for very large cross-sectional dimensions: this means that the true number of factors cannot be recovered and the GDFM is not identifiable in this setting (for further details on identification of factor models, see Corollary 4.2 and the related discussion).

|

|

The above arguments illustrate a two-fold statistical problem related to the development of a novel theory of general factor models for spatio-temporal rf. On the one hand, there is the need for a representation theory for large dimensional rf, which allows us to capture the common spatio-temporal factors that explain the spatio-temporal co-movements of the process. On the other hand, there is the central need for estimation methods which have statistical guarantees and yield an estimate of the common spatio-temporal component converging to true spatio-temporal common component. In the next sections, we illustrate how to solve this statistical problem.

3 Basic theory of linear random fields

3.1 Random fields

Our object of interest is the infinite dimensional random field (hereafter rf) on a lattice . We index space-time points as , with , and allowed to vary independently. So, for any , we define the infinite dimensional random vector and for any ,we also define the -dimensional column random vector , which is an element of the -dimensional rf . Clearly, is a sub-process of .

Throughout, we let be a probability space and let be the linear space of all complex-valued, square-integrable random variables defined on . Then, if , for any , the process is a complex valued scalar random field with finite variance, and for any fixed the process is a complex valued vector rf with all its elements having finite variance, and the process is an infinite dimensional complex valued rf with all its elements having finite variance. Notice that the space is a complex Hilbert space, thus it possesses the usual inner product given by , where represents the expected value taken w.r.t. the probability .

Last, we define as the minimum closed linear subspace of , containing , i.e., the set of all -convergent linear combinations of ’s. Therefore, a generic element of is of the form with and . Moreover, define , which is such that and it contains also the limits, as , of all -convergent sequences thereof. Hence, both and are Hilbert spaces.

3.2 Spatio-temporal autocovariance and spectral density matrices

A spatio-temporal shift between pairs of points and is defined as a vector such that . We need to set an origin , whose location is arbitrary, but once it has been chosen it remains fix. To make our theory insensitive to origin shifts, we impose space-time homostationarity, which implies that the first two moments (mean and covariance) of a space-time rf are invariant respect to space-time translation, i.e. a homostationary spatio-temporal random field features homogeneity in space and stationarity in time.

To formalize this property, for any and any , we define the autocovariance matrix: Notice that the covariance matrix is non-negative definite; see, e.g., Stein (2012, p.15). Then, we introduce the following assumption of homostationarity.

Assumption 3.1.

For any the random field is such that for any , and, for any : (i) and ; (ii) for any .

A few comments on Assumption 3.1. First, the zero-mean assumption can be made without any loss of generality. Second, since, all elements of the rf are in then for any fixed the covariance matrix is finite and so all autocovariances , are finite too. Third, note that letting , then the following relations holds

which are much weaker requirements than assuming space isotropy—for which we would have , thus imposing that the second-order moments are invariant under all rigid axes motions (Stein, 2012, p.17). Then, we introduce (see Mandrekar and Redett, 2017, p. 45)

Definition 3.1 (Orthonormal white noise rf).

For a given finite integer , let be a -dimensional rf such that and , for any and . Then we call an orthonormal white noise rf if, for any , if and it is otherwise.

To conduct spectral analysis we add the following

Assumption 3.2.

For any , the spectral measure of is absolutely continuous (with respect to on ), so admits an spectral density matrix given by

where and .

For a rf the spectral density matrix depends on a vector of frequencies (Brillinger, 1970), and under Assumptions 3.1 and 3.2, is Hermitian and non-negative definite (Leonenko, 1999, p.13) for all and any . The lag- autocovariance matrix is then given by , for any .

Let denote the infinite matrix having the matrix as its top-left sub-matrix and notice again that as we allow for the possibility of its eigenvalues to diverge (see below), while all its entries are finite by assumption. Moreover, we notice that a -dimensional orthonormal white noise rf has spectral density . Then we have

Definition 3.2 (Spatio-temporal dynamic eigenvalues).

For any and , let be defined as the function associating with the -th eigenvalue in decreasing order of . We call the spatio-temporal dynamic eigenvalues of .

Definition 3.3 (Spatio-temporal dynamic eigenvectors).

For any and let be such that, for any , the row vector satisfies (i) ; (ii) , for ; (iii) . Then, the functions constitute a set of spatio-temporal dynamic eigenvectors associated with the spatio-temporal eigenvalues and the rf .

Hereafter, we also assume strict positive definiteness of

Assumption 3.3.

For any and , and any , .

Remark 3.1.

Following Forni and Lippi (2001, Lemma 3 and 4), one can easily prove that: (i) the real functions are Lebesgue-measurable and integrable in , for any given and ; (ii) is a non-decreasing function of , for any . In particular, from (ii) it follows that, for all , and it is well defined for any .

3.3 Spatio-temporal linear filters

First, for any and , let us consider the three linear operators, , , such that, for any ,

| (1) |

so that when is applied to the vector it shift all its components along the space or time dimension. and act on the (spatial) dimensions of the lattice (see Whittle (1954)), while is the usual time lag operator. We also set and . The operators are commutative, e.g. . In Lemma A.1 in Appendix A, we show that are unitary operators that can be extended to .

Second, consider a generic -dimensional row vector of functions with being measurable for any and such that the following conditions hold: (i) , and (ii) , respectively. The space of such functions is a complex Hilbert space denoted as , obtained from the intersection of two Hilbert spaces each endowed with inner products derived from one of the two norms defined above.

Third, consider the map , such that, for any and ,

| (2) |

where if and if and indicates the map from to such that . Thus, we have

| (3) |

where is an -dimensional vector of ones. In Lemma A.2 in Appendix A we prove that is an isomorphism, also called canonical isomorphism, and it can be extended to the Hilbert space of infinite dimensional functions , with norms and . Notice that is an isomorphism between the measure spaces and (, where and are the Borel -fields on and , respectively. The definition of extends to our setting the classical isomorphism typically applied in time series analysis (see e.g. Brockwell and Davis, 2006, Section 4.8).

Now, for any consider the Fourier expansion

| (4) | ||||

| (5) |

where the equality in (4) holds in the -norm, and are the Fourier coefficients.

Since also , then we apply to it the canonical isomorphism to map it into elements . This defines the filtered processes associated to

| (6) |

Therefore, from (4), (5), and (6), and by linearity of the canonical isomorphism, we have

| (7) |

which defines an -dimensional linear spatio-temporal filter. Note that is the isomorphic map of , that is multiplications become convolutions via the isomorphism and viceversa via . Hereafter, the composition of two linear filters, is denoted as

| (8) |

4 General Spatio-Temporal Factor Model

We show that any dimensional rf , satisfying Assumptions 3.1-3.3, can be summarized by its projection, , on a -dimensional sub-space generated by cross-sectional and spatio-temporal aggregation of the components of and where is a given finite positive integer independent of . The rf is such that as it survives under cross-sectional and spatio-temporal aggregation, i.e., it converges in mean-square to a finite variance rf. The residual rf instead vanishes under cross-sectional and space-time aggregation as . Intuitively, the distinct asymptotic behavior of the two components under aggregation means that if any pervasive signal is present in the rf an aggregation operation should help recovering it in the limit and the signal will appear in the elements of . To make this argument formal we start by introducing

Definition 4.1 (Spatio-temporal aggregation of rf).

For any , consider an -dimensional row vector of functions . The sequence is a spatio-temporal dynamic averaging sequence (STDAS) if

Moreover, we say that is an aggregate if for any there exists a STDAS such that in mean-square and . We denote the set of all aggregates by and we refer to it as the aggregation space of .

Intuitively, the aggregation via a STDAS corresponds to averaging an infinite dimensional rf both in the cross-section and in the space-time dimensions, simultaneously. Notice that, because of the definition of , any aggregate, i.e., any element of , has variance either finite strictly positive or zero. By generalizing to rf the definitions given by Forni and Lippi (2001) and Hallin and Lippi (2013), we have

Definition 4.2 (Idiosyncratic and common components).

We say that an infinite dimensional rf with elements for any and (i) is idiosyncratic if for any and any STDAS , in mean-square; (ii) is common if it is not idiosyncratic, i.e., if for any and any STDAS , in mean-square such that and .

Hereafter, we also refer to the components of as idiosyncratic or common if is idiosyncratic or common, respectively. Note that if is idiosyncratic then , that is it contains only the zero element. Moreover, is idiosyncratic if and only if its largest dynamic spatio-temporal eigenvalue is an essentially bounded function (see Proposition B.7 in Appendix B.2). In contrast, if is common, by aggregating it we get a rf with finite and strictly positive variance, in other words, contains only non-degenerate rf. This yields

Definition 4.3 (Common factors).

Given an -dimensional rf with elements for any and , we say that a scalar rf is a common factor if there exists a STDAS such that in mean-square, , and .

Clearly, by comparing Definition 4.3 with Definition 4.2(ii) we see that the common factors are elements of the aggregation space of the common components.

Denote the sub-space of all components of an idiosyncratic rf (which are scalars) as and the sub-space of all components of a common rf as . Given the above definition we have the decomposition

| (9) |

Moreover, since the set is a closed subspace of , we can also define

Definition 4.4 (Canonical decomposition).

For any and any , the orthogonal projection equation:

| (10) |

is called the canonical decomposition of the rf .

We show that the decomposition (9) and the canonical decomposition (10) are equivalent. In particular, we will show that there exists a -dimensional orthonormal white noise rf with and independent of , such that: (i) , hence, according to Definition 4.3, is a vector of common factors; (ii) is common and has a spectral density of rank ; (iii) is idiosyncratic.

Summing up, given an observed -dimensional rf , common factors are obtained as aggregates of and the common component is obtained by projecting onto such factors. Indeed, projecting onto the aggregation space of or onto the aggregation space of the common component is equivalent, since the aggregation space of the idiosyncratic component contains only the zero element. To formalize the above projection argument, we first state

Definition 4.5 (-General Spatio-Temporal Factor Model).

Let be a non-negative integer. We say that the rf with follows a -General Spatio-Temporal Factor Model (-GSTFM) if contains: (a) an orthonormal -dimensional white noise rf ; (b) an infinite dimensional rf ; both fulfilling Assumptions 3.1 and 3.2 and such that:

-

(i)

for any and any

(11) (12) thus defining an infinite dimensional rf ;

-

(ii)

letting , , , and , it holds that

-

(iii)

for any , , and such that , it holds that .

Furthermore, for any consider the -dimensional sub-processes and with -th largest dynamic spatio-temporal eigenvalues and , respectively, then

-

(iv)

;

-

(v)

, -a.e. in .

We refer to the infinite dimensional rf and as the common and idiosyncratic components of the representation (11). Indeed, part (iv) implies that is idiosyncratic, since, as proved in Proposition B.7 in Appendix B.2, a rf is idiosyncratic if and only if its dynamic spatio-temporal eigenvalues are essentially bounded functions. Moreover, since by part (iii) and have orthogonal elements, then cannot be idiosyncratic and must be common.

The -GSTFM has two main features. First, differently from the GDFM, the common component in (12) accounts for the spatio-temporal dependence. The -dimensional rf of factors is loaded by each element of dynamically in time (possibly in a causal way, see Remark 6.2) and in space, since the filters depend on both dimensions. This means that, being a rf, a common shock to can impact different points in space heterogeneously at the same time and at different points in time and it can impact also the variables observed in a given point in space at different times. Second, we do not impose any specific structure on the second moment of the of vector of idiosyncratic components whose elements can be both cross-sectionally and spatio-temporally cross-auto-correlated, as long as part (iv) is satisfied. By allowing for spatial dependencies we then generalize to rf the representation derived for pure time series by Forni and Lippi (2001), which in turn extended the approximate static factor model by Chamberlain (1983) and Chamberlain and Rothschild (1983) and the exact dynamic factor model by Geweke (1977) and Sargent and Sims (1977), as well as the standard classical exact static factor model for cross-sectional data (see Lawley and Maxwell, 1971).

Remark 4.1.

A sufficient condition for part (ii) to hold is to ask for square summability of the coefficients of the linear filter , i.e., to assume for some finite independent of . Indeed, by definition

Remark 4.2.

Parts (iv) and (v) require some further clarifications. Because of Remark 3.1, the function is the -largest dynamic spatio-temporal eigenvalue of the infinite dimensional rf , and, similarly the function is the largest dynamic spatio-temporal eigenvalue of the infinite dimensional rf . Now, by (v) the former is to be intended as an extended function in the sense that its value is infinite but measurable (Royden and Fitzpatrick, 1988, p. 55), while, by (iv) the latter is instead an essentially bounded function (Rudin, 1987, p. 66).

Remark 4.3.

From (iv) in Definition 4.5 and Remark 4.2, it follows that there exists a finite independent of such that: , . And by the monotone convergence theorem, which holds because of Remark 3.1, we have

This, in turn implies that the idiosyncratic covariance matrix has largest eigenvalue such that

The latter condition is the usual assumption made in the vector static factor model literature to characterize an idiosyncratic component (see, e.g., Forni et al., 2009). Notice, however, that (v) in Definition 4.5 in general does not imply that the common covariance matrix has eigenvalues diverging as , for the effect of common factors might be just lagged and not contemporaneous, in which case only the products for will display diverging eigenvalues. This case has been studied by Lam and Yao (2012) in the vector case.

There are essentially two ways to obtain a -GSTFM. On the one hand, one may assume that the rf spatio-temporal dynamics can be modeled as in (11)-(12), mimicking the approach in Forni et al. (2000). On the other hand, one may find a set of very mild assumptions such that a spatio-temporal rf can be represented as in (11)-(12), extending to the rf setting the results of Forni and Lippi (2001). In what follows, we consider the latter approach, which is more general and powerful than the former one: indeed, (11)-(12) is a representation which holds under Assumptions 3.1-3.3 and it is not a model imposed by the statistician. Our main result of this section is the following

Theorem 4.1.

Theorem 4.1 characterizes the class of rf which admit the -GSTFM in Definition 4.5. First, notice that the same comments of Remark 4.2 apply also to the functions in parts (i) and (ii). It follows that the presence of an eigen-gap in the dynamic spatio-temporal eigenvalues of the infinite dimensional rf is a necessary and sufficient condition for the -GSTFM to hold. To this end no assumption is needed other than Assumptions 3.1-3.3, which are very mild. Notice also that the case is possible, in which case has no common factor and it is purely idiosyncratic. In practice, if for an observed rf , we see evidence of an eigen-gap in the eigenvalues of its spectral density (as e.g. in Figure 1), then admits the -GSTFM.

The proof of the theorem is given in Appendix B and it is rather technical and lengthy. Here, we present only the key aspects of the whole derivation. The necessary condition part (“only if”) is is easy to prove (see Appendix B.3). Indeed, by Weyl’s inequality (see Appendix B.1), it is straightforward to see that if (iv) and (v) in Definition 4.5 hold then (i) and (ii) in Theorem 4.1 hold. The sufficient condition part (“if”) is more difficult to prove and it based on a series of intermediate results. In a nutshell, in the proof we proceed by first constructing a -dimensional orthonormal white noise vector rf, , say (see Proposition B.5). Then, we show (see Proposition B.6). It follows that the canonical projection , is such that is idiosyncratic (Propositions B.7 and B.8), hence , being orthogonal to , is common. The proof is completed by means of the arguments in the following remark on the identifiability of the white noise.

Remark 4.4.

It must be pointed out that, in general, neither the -dimensional orthonormal white noise rf nor the filters in (12) are identified. Indeed, if (11) and (12) hold, then infinitely many other equivalent representations of are obtained by setting for a -dimensional rf such that , , with which is and such that and for all . It follows that is also a -dimensional orthonormal white noise rf. In fact, if were not orthogonal, as assumed, but just invertible, we could still find equivalent representations of where, however, would no more be a white noise rf, but it is a rf autocorrelated in both the spatial and time dimension.

Uniqueness of the -GSTFM follows:

Corollary 4.2.

If follows a -GSTFM as in Definition (4.5), then and Moreover, the number of factors , the common component , and the idiosyncratic component , are uniquely identified.

Notice that this result implies: (i) for any -dimensional white noise rf obtained from as in Remark 4.4, and (ii) for any and . Moreover, no representation with a smaller or larger number of factors fulfilling Definition 4.5 is possible. In other words the -GSTFM is identified. It has to be stressed though that, since the definition of common and idiosyncratic components are only asymptotic ones, i.e., holding in the limit (see Defintion 4.2), identification is achieved only asymptotically. Indeed, as shown later, if is fixed no consistency result can be derived when we estimate the model. This is again an instance of the blessing of dimensionality and it emphasizes that factor analysis is effective in high-dimensions.

5 Recovering the common component - Population results

In this section we prove that among all possible dimensional aggregates which we can project on, the first -dynamic spatio-temporal principal components of are the optimal ones in the sense that they are those with largest variance, and in Theorem 5.1 we prove that by projecting onto such aggregates we can recover the common component in the limit .

The canonical decomposition in Definition 4.4 is optimal in the sense that, by definition of linear projection, it minimizes the variance of the residual idiosyncratic term. However, to achieve such decomposition in practice we need to define a basis for the space of aggregates to project an the elements of onto. Therefore, given a -GSTFM in Definition 4.5 all we need to do is to find a -dimensional rf common factors, which, because of Definition 4.3 belong to , thus have finite and strictly positive variance. Moreover, we shall require this -dimensional rf of factors to be an orthonormal white noise rf.

The definition of common factors holds asymptotically, but in practice we deal with a given fixed , then, for such given and any , we should look for those weights , such that , has maximum variance. In view of the canonical isomorphism in (6), we shall then consider the equivalent maximization problem in the frequency domain, i.e., for any we shall solve:

| (13) |

Notice that the objective function is the variance of the discrete Fourier transform of . For any given , the solution of (13) is clearly given by the eigenvector of the spectral density matrix corresponding to the -th largest eigenvalue , see Definition 3.3. For any , to this solution corresponds a scalar filtered rf which has spectral density and variance . So the first, , dynamic spatio-temporal principal component has largest variance as expected. Moreover, these rf are orthogonal contemporaneously and at any spatio-temporal shift, indeed, for , we have for all . Notice that if then the filtered process should be defined as , hence, they always have zero-mean.

However, the filtered processes defined by solving (13) cannot be directly used as a basis for for two reasons. First, they are not white noise rf. Second, and most importantly, as , their variance is not finite, indeed, under a -GSTFM, we know that for all . Therefore, we need to rescale and whiten those rf. This is accomplished by means of the following (recall the notation in (8))

Definition 5.1 (Normalized dynamic spatio-temporal principal components).

For any and , the filtered rf processes

form a set of normalized dynamic spatio-temporal principal components associated with .

Notice that this definition makes sense since Assumption 3.3 implies that is finite for any and . Now, for any , define the rf . Then, from Definition 5.1 we have:

| (14) |

where the linear spatio-temporal filters and are, respectively, obtained from the diagonal matrix having as entries the dynamic spatio-temporal eigenvalues , for , and the matrix having as rows the corresponding dynamic spatio-temporal eigenvectors. Now, let be the diagonal matrix having as entries the dynamic spatio-temporal eigenvalues , for , and let be the matrix having as rows the corresponding dynamic spatio-temporal eigenvectors. Then, for all , . Therefore, since , from (14) we immediately see that has spectral density , hence it is a -dimensional orthonormal white noise rf as required. By letting , we obtain from the basis for we are looking for. This is formalized by means of the following

Theorem 5.1.

This result is the basis for our estimation approach. It implies that if, for a given , we knew the spectral density matrix of , then, for any and , an estimator of the common component would be:

| (15) |

This is a consistent estimator since as it converges in mean-square to the unobservable common component . Notice that since we are dealing with projections the rescaling by means of the eigenvalues introduced in Definition 5.1 is actually not needed in practice, as we just need the eigenvectors.

Remark 5.1.

For any , let be the matrix having as rows the spatio-temporal dynamic eigenvectors of the spectral density matrix of the common component . Let also the associated linear spatio-temporal filter and for any , denote by the -th -dimensional row of . Then, since for all and -a.e. in , we immediately see that, for any and , we can always write:

| (16) |

because for all . This, together with (15), implies that, as , the coefficients of converge in mean-square to the coefficients of .

Remark 5.2.

In general, the dynamic spatio-temporal eigenvectors are complex vectors. However, for any , we know that , and that the spectral density matrix is Hermitian, i.e., and is a real matrix. Therefore, we can always impose for all . This implies that is always a real number, and, thus, the normalized dynamic spatio-temporal principal components are real rf, see also Hallin, Hörmann and Lippi (2018).

6 Recovering the common component - Estimation

6.1 Estimation in practice

The population results derived in Section 4 show that the spatio-temporal common component can be recovered as from a sequence of projections, see Theorem 5.1. The filters needed to define this projection are given in Definition 5.1 and depend on the dynamic spatio-temporal eigenvalues and eigenvectors of the unknown spectral density matrix.

Let us assume now to observe a finite -dimensional realization of the infinite dimensional rf over points on a 2-dimensional lattice and over time periods. In order to proceed we need to fix the origin of the lattice, because of homostationarity this can be chosen arbitrarily in any location of . Here we adopt the convention that the point corresponds to the South-West corner of the given lattice. Then, index grows by moving East while the index grows by moving North. With this definition of the spatial coordinates, our observations are collected into the -dimensional matrix: .

If the spatio-temporal dynamic eigenvalues of satisfy Theorem 4.1, then, according to the -GSTFM, for all , , , and we can write , where is the common component and is idiosyncratic. For any given , we denote as and the -dimensional rf of the common and idiosyncratic components.

Throughout this section we assume that the number of factors, , driving the common component is known (see Section 7) and we now describe our estimation strategy. Let and , then an estimator of is

| (17) |

with , and being kernel functions and , and being bandwidths, whose properties are discussed later.

In agreement with the population results of Theorem 5.1, the common component is estimated by projecting onto the space spanned by linear filters generated by the leading spatio-temporal dynamic eigenvectors. For all let us denote by the matrix having as rows the spatio-temporal dynamic eigenvectors of and, for any , let the -th -dimensional row of , and, in agreement with (15) define , generating the linear filter .

Now, since is in general infinite and two-sided, but is not available for and , we consider instead a truncated linear filter, whose definition depends on the space-time location in correspondence of which the filter is applied to . Namely, we consider

| (18) |

where, for some integers , and , we defined

| (19) | ||||

For any given and any such that , , and , the common component is then estimated as

| (20) |

Remark 6.1.

In practice all estimated quantities in the frequency domain, as , , and , should be computed only for a finite number of frequencies, defined as , with , , and , for integers , , and . For simplicity, in this and the following sections we implicitly assume the identities , , and .

6.2 Assumptions

For estimation we need to add few more assumptions. First, the GSTFM has two-sided filters as defined in (12), however, it is desirable to have one-sided filters in the time dimension. This can be obtained by imposing the following

Assumption 6.1.

The existence of one-sided time representations in parts (i) and (ii) is a mild one. For the idiosyncratic component, our requirement is for the Wold representation to exist also for an infinite dimensional process. For the common component, which is singular, the existence of the assumed one-sided representation has been investigated by Forni et al. (2015) in the pure time series case (see also Remark 6.2 below). Notice also the Hallin and Lippi (2013) derived an analogous of our Theorem 4.1, where only one-sided filters are used. Such approach, however, does not ensure the existence of a -dimensional white noise rf driving the common component, and its existence is instead assumed. For the common component the two-sided representation in space is implied by the -GSTRF in Definition 4.5, and for the idiosyncratic component we make an analogous assumption but based on an infinite dimensional white noise rf.

By means of parts (i) and (ii) we also strengthen the conditions on the rf and which are now independent along the spatio-temporal dimensions. Note that the independence assumption could be relaxed. For example we could just assume and to be martingale differences in the time dimension so to allow for conditional heteroskedasticity in time (see, e.g., Barigozzi, Cho and Owens, 2023).

Part (iii) implies orthgonality of common and idiosyncratic components at all leads and lags consistently with the GSTFM in Definition 4.5.

Remark 6.2.

If for any fixed the -dimensional vector of common components has a spectral density matrix which is a rational function of , then, from Rozanov (1967, Ch.1, Section 10) it follows that, for all and ,

for some finite positive integers and , which, without loss of generality we can assume to be independent of . Moreover, for all such that , and for all such that . By defining , it follows that

which, by setting , coincides with Assumption 6.1(i). Thus, for all and all , , i.e., is fundamental for . The generalization of this reasoning to the infinite dimensional process is considered in Forni et al. (2015, Lemma 1 and 2) in the case of pure time series, where it is shown that, under rationality of the spectral density, then fundamentalness of is always true for any generically, i.e., for any value of the coefficients such that Assumption 6.1(i) holds with the exception of a zero-measure set (see also Anderson and Deistler, 2008).

The coefficients of the representations in Assumption 6.1 are characterized by

Assumption 6.2.

For all , , and : (i) , for some finite independent of , , and , and some finite independent of and such that , for some finite independent of ; (ii) , for some finite independent of , , and , and some finite independent of and such that and , for some finite independent of and .

This assumption implies square-summability of the coefficients of the filters, which for the common component is a sufficient condition for (ii) in Definition 4.5 to hold, see Remark 4.1. This assumption has two other important implications. First, part (ii) implies that the largest spatio-temporal dynamic eigenvalue of satisfies (see Proposition E.1 in Appendix E)

| (21) |

for some finite . Hence, according to (i) in Theorem 4.1, is effectively an idiosyncratic component. Second, in part (i) we do not require summability of the coefficients along the rows, so that the spatio-temporal dynamic eigenvalues of can be diverging with . Divergence of those eigenvalues is made formal by means of the following assumption which strengthens (ii) in Theorem 4.1:

Assumption 6.3.

For all there exist continuous functions and such that for all

The requirements of distinct and linearly diverging eigenvalues are standard in the factor model literature. While the former requirement is merely technical, the latter implies that here we are dealing only with factors which are pervasive for the whole cross-section, which in turn implies that the ordering of the cross-sectional units is irrelevant for estimation. Both requirements could, in principle be relaxed. For example, the case of local, or group specific dynamic factors, could be considered along the lines of what done by Hallin and Liška (2011) in the purely time series case. We do not make any distributional assumption but we require only the following moment conditions

Assumption 6.4.

For all and , , for some and independent of and .

Two technical assumptions are also required. First, we characterize the kernel functions and bandwidths needed to estimate the spectral density matrix and the truncation levels in (19) by the following

Assumption 6.5.

Part (i) and (ii) are standard. Part (iii) controls the truncation of the linear filter defined in (18) and (19).

Second, we assume that the effect of the linear spatio-temporal filters , as defined in (16), decreases geometrically.

Assumption 6.6.

For any , let , then, for some finite independent of .

6.3 Asymptotic results

To study the asymptotic properties of the estimated spectral density matrix, we generalize to the case of spatio-temporal rf the approaches by Wu and Zaffaroni (2018) and Zhang and Wu (2021) for time series and by Deb, Pourahmadi and Wu (2017) for purely spatial models, which in turn are all are based on the notion of functional dependence originally proposed by Wu (2005) in a univariate time series context. The resulting estimation theory is available in Appendix D and represents a novel contribution to the literature on the inference for spatio-temporal rf.

Letting be the -th entry of the estimator , defined in (17), we prove the following

Theorem 6.1.

Our results are nonstandard in the literature on geostatistics: we do not need to choose between in-fill or long-span asymptotic regime and we simply require that both and diverge, so . With this regard, we emphasize that our estimator of the spectral density matrix entries as in (17) bears some similarities with the tapered estimator of the Fourier transform of the covariance matrix of a spatial rf on a lattice proposed by Dahlhaus and Künsch (1987). Differently from their method, in our approach we replace data tapers with kernels. This yields a two-fold advantage: first, it allows to control for the estimation bias of , taking care of the boundary effects; second, it offers the possibility of using the mentioned flexible asymptotic regime. We refer to El Machkouri, Volnỳ and Wu (2013) for a related discussion; see also Deb, Pourahmadi and Wu (2017) for similar comments.

Remark 6.3.

The rate in Theorem 6.1 depends on the kernel smoothness , and the bandwidths , , and (see Assumption 6.5). Typically the same kernel is used in all dimensions, so we can assume for all . Consider the case in which , then, up to logarithmic terms, the optimal spatial bandwidths are such that , , and . This implies that the optimal rate of consistency for our estimator of the spectral density matrix is . In our applications we used the Epanechnikov kernel for which , hence, the rate of consistency is . In a pure time series model the consistency rate is (Barigozzi and Farnè, 2022), which for a Epanechnikov kernel implies a rate , much slower than what achieved using also the spatial information.

We then prove consistency of the common component estimator defined in (20)

Theorem 6.2.

Theorem 6.2 proves that for consistency of , the number of lags , , and used in (18) should not be too large, while , , and should all diverge to infinity. As it is clear from Theorem 5.1, we need a large to disentangle the common and the idiosyncratic components, while from Theorem 6.1 we see that we need large , , and to consistently estimate the spectral density matrix of the observed rf. We remark that part (i) yields a rate of convergence also when the spatial locations and the time are close to the boundaries: this aspects has been neglected in the literature on factors models.

7 Determining the number of factors

An essential aspect for the implementation of the GSTFM is the correct identification of the number of factors . Theorem 4.1 provides a rough guideline for this: intuitively, one should choose the value of such that the -th dynamic eigenvalue should be “sufficiently large" while the -th one should not be “small". To provide a more precise selection procedure, we define an information criterion (IC) that enables us to estimate consistently. To this end, we propose the use of a criterion which is based on the eigenvalues, , , of .

Letting denote a penalty depending on both and on , and , we consider the information criterion

and we define the estimator of the number of factors

| (22) |

for some a priori chosen maximum number of factors . We assume the following standard divergence rate of the penalty

Assumption 7.1.

As , and

Finally, we establish consistency of

8 Monte Carlo experiments

Before delving into numerical studies, we summarize the estimation procedure in the following

We illustrate how Algorithm 1 works and we provide evidence of our key theoretical results. In Section 2 we already showed the presence of the eigen-gap in finite-samples as predicted by our results in Section 4, further evidence is available in Appendix I; in Section 8.1, we study the performance of the estimator of the common component proposed in Section 6, and we provide a comparison of our GSTFM with the extant GDFM; in Section 8.2, we explain how to select the number of factors following Section 7.

In the whole section we simulate data using , for , with , , and . The case of cross- and serially correlated idiosyncratic components is studied in Appendix I. The idiosyncratic component is i.i.d. from a standard normal distribution and the common component is generated according to two different mechanisms.

-

Model (a)

is an infinite convolution over the lattice:

(23) -

Model (b)

is a finite convolution over the lattice:

(24)

We generate and , from i.i.d. standard normal distributions and from i.i.d. uniform distributions on . The Monte Carlo (MC) experiments are repeated times.

8.1 The common component

Section 6 contains the asymptotics of the proposed estimation methods. A practically relevant question is related to the finite-sample behaviour of the proposed estimators. To investigate this aspect, we set and we study numerically how the mean square error (MSE)

and the standardised MSE

change with and with the spatio-temporal dimensions and .

In the top panel of Table 1, we display the averaged (over all MC runs) and for and . The table clearly shows that the estimation errors decrease as increases: this illustrates the blessing of dimensionality for the estimation of the common component. Interestingly, we remark that already with , and have values that are very similar to the ones obtained for larger sample sizes (e.g. ).

In the bottom panel of Table 1 we report the averaged (over all MC runs) values of and for and with . In line with the theoretical results, the errors decrease as the spatio-temporal dimensions increase.

| Model (a) in (23) | ||||

|---|---|---|---|---|

| 0.389 | 0.346 | 0.339 | 0.331 | |

| 0.066 | 0.060 | 0.059 | 0.058 | |

| Model (b) in (24) | ||||

| 0.251 | 0.193 | 0.175 | 0.164 | |

| 0.047 | 0.036 | 0.031 | 0.030 | |

| Model (23) | ||||

| 0.372 | 0.289 | 0.302 | 0.301 | |

| 0.077 | 0.051 | 0.050 | 0.046 | |

| Model (24) | ||||

| 0.196 | 0.115 | 0.146 | 0.118 | |

| 0.036 | 0.021 | 0.027 | 0.021 | |

To elaborate on the motivating example of Section 2, we compare the performance of the GSTFM and the GDFM in terms of estimation accuracy of the common components. We set , and or . In Table 2, we report the average (over all MC runs) values of and , for the GSTFM and GDFM. The advantage of our approach is evident: the GSTFM produces smaller estimation errors of the common components than the GDFM. We emphasize that of the GDFM displays a sharp rise as increases from to . This aspect illustrates that there is no blessing of dimensionality for the GDFM if the spatial dependencies are ignored: adding more time series does not yield any accuracy improvement and the results of Forni et al. (2000) do not apply. Indeed, when increases, stacking the new observations in a vector, as in Section 2, implies that we are dealing with a larger number of spatially dependent variables: the GDFM ignores these spatial dependencies and, as a result, it becomes less reliable in the estimation of the common component, entailing larger values of —incidentally, this point is not detectable looking at because of its standardisation based on the variance of the true common component.

8.2 Selection of the number of factors

We investigate the finite sample performance of the estimator of defined in Section 7. However, looking at (22), we remark that, if the estimator is consistent, then the estimator obtained via the penalty , , is consistent as well. Hence, in practice, one needs to choose also to estimate consistently. The detailed procedure for the automatic selection of the number of factors is summarized in Algorithm 2 in Appendix G. To evaluate the estimation accuracy of Algorithm 2, we set , , and and we run MC replications. Table 3 shows the under- and over-identification proportions for . The results illustrate good finite-sample performance of the selection procedure of : for Model (b) in (24), the algorithm identifies correctly for all replications and for all values of ; for Model (a) in (23), the over-identification rate is not zero for but it is nevertheless very small.

9 Conclusions and further developments

We develop the theory and provide the complete inference toolkit (estimation of the common component and selection of the number of factors) for the factor analysis of high-dimensional spatio-temporal rf defined on a lattice. Our model accounts for all spatio-temporal common correlations among all components of the rf. We give statistical guarantees of the proposed estimation methods. Our asymptotic theory extends the one available in Forni et al. (2000), whose rates of convergence, which are unavailable in the literature on factor models for time series, can be derived as a special case of our rates in Section 6. Monte Carlo studies illustrate the applicability and the good performance of our GSTFM under many different settings, commonly encountered in data analysis.

We foresee some extensions of our results. For instance, one may define estimators of the common component which involve one-sided filters in time, thus allowing for forecasting. We conjecture that this is possible along the lines of (Forni et al., 2005, 2017). Nevertheless, such extensions cannot be directly obtained within the setting of this paper: they require further assumptions and more involved estimation steps, whose statistical guarantees need to be derived. Therefore, we leave them for further research.

The third author was supported by grants WK2040000055 and YD2040002016.

References

- Altissimo et al. (2010) {barticle}[author] \bauthor\bsnmAltissimo, \bfnmFilippo\binitsF., \bauthor\bsnmCristadoro, \bfnmRiccardo\binitsR., \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmLippi, \bfnmMarco\binitsM. and \bauthor\bsnmVeronese, \bfnmGiovanni\binitsG. (\byear2010). \btitleNew Eurocoin: Tracking economic growth in real time. \bjournalThe Review of Economics and Statistics \bvolume92 \bpages1024–1034. \endbibitem

- Anderson and Deistler (2008) {barticle}[author] \bauthor\bsnmAnderson, \bfnmBrian D. O.\binitsB. D. O. and \bauthor\bsnmDeistler, \bfnmManfred\binitsM. (\byear2008). \btitleProperties of zero-free transfer function matrices. \bjournalSICE Journal of Control, Measurement, and System Integration \bvolume1 \bpages284–292. \endbibitem

- Bai and Ng (2002) {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS. (\byear2002). \btitleDetermining the number of factors in approximate factor models. \bjournalEconometrica \bvolume70 \bpages191–221. \endbibitem

- Baltagi (2008) {bbook}[author] \bauthor\bsnmBaltagi, \bfnmBadi\binitsB. (\byear2008). \btitleEconometric analysis of panel data \bvolume1. \bpublisherJohn Wiley & Sons. \endbibitem

- Barigozzi, Cho and Owens (2023) {barticle}[author] \bauthor\bsnmBarigozzi, \bfnmMatteo\binitsM., \bauthor\bsnmCho, \bfnmHaeran\binitsH. and \bauthor\bsnmOwens, \bfnmDom\binitsD. (\byear2023). \btitleFNETS: Factor-adjusted network estimation and forecasting for high-dimensional time series. \bjournalJournal of Business & Economic Statistics \bpages1–13. \endbibitem

- Barigozzi and Farnè (2022) {barticle}[author] \bauthor\bsnmBarigozzi, \bfnmMatteo\binitsM. and \bauthor\bsnmFarnè, \bfnmMatteo\binitsM. (\byear2022). \btitleAn algebraic estimator for large spectral density matrices. \bjournalJournal of the American Statistical Association \bpages1–13. \endbibitem

- Bodelet and La Vecchia (2022) {barticle}[author] \bauthor\bsnmBodelet, \bfnmJulien\binitsJ. and \bauthor\bsnmLa Vecchia, \bfnmDavide\binitsD. (\byear2022). \btitleRobust sieve M-estimation with an application to dimensionality reduction. \bjournalElectronic Journal of Statistics \bvolume16 \bpages3996–4030. \endbibitem

- Brillinger (1970) {binproceedings}[author] \bauthor\bsnmBrillinger, \bfnmDavid R\binitsD. R. (\byear1970). \btitleThe frequency analysis of relations between stationary spatial series. In \bbooktitleProc. Twelfth Biennial Seminar Canadian Math. Congress (ed. R. Pyke). Canadian Math. Congress, Montreal \bpages39–81. \endbibitem

- Brockwell and Davis (2006) {bbook}[author] \bauthor\bsnmBrockwell, \bfnmP. J.\binitsP. J. and \bauthor\bsnmDavis, \bfnmR. A.\binitsR. A. (\byear2006). \btitleTime series: theory and methods, \beditionSecond ed. \bpublisherSpringer Science & Business Media. \endbibitem

- Chamberlain (1983) {barticle}[author] \bauthor\bsnmChamberlain, \bfnmGary\binitsG. (\byear1983). \btitleFunds, factors, and diversification in arbitrage pricing models. \bjournalEconometrica \bpages1305–1323. \endbibitem

- Chamberlain and Rothschild (1983) {barticle}[author] \bauthor\bsnmChamberlain, \bfnmG.\binitsG. and \bauthor\bsnmRothschild, \bfnmM.\binitsM. (\byear1983). \btitleArbitrage, factor structure and mean– variance analysis in large asset markets,. \bjournalEconometrica \bvolume51 \bpages1305–1324. \endbibitem

- Chang et al. (2023) {barticle}[author] \bauthor\bsnmChang, \bfnmJinyuan\binitsJ., \bauthor\bsnmHe, \bfnmJing\binitsJ., \bauthor\bsnmYang, \bfnmLin\binitsL. and \bauthor\bsnmYao, \bfnmQiwei\binitsQ. (\byear2023). \btitleModelling matrix time series via a tensor CP-decomposition. \bjournalJournal of the Royal Statistical Society Series B: Statistical Methodology \bvolume85 \bpages127–148. \endbibitem

- Chen, Yang and Zhang (2022) {barticle}[author] \bauthor\bsnmChen, \bfnmRong\binitsR., \bauthor\bsnmYang, \bfnmDan\binitsD. and \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. (\byear2022). \btitleFactor models for high-dimensional tensor time series. \bjournalJournal of the American Statistical Association \bvolume117 \bpages94–116. \endbibitem

- Christakos (2017) {bbook}[author] \bauthor\bsnmChristakos, \bfnmG.\binitsG. (\byear2017). \btitleSpatiotemporal random fields: theory and applications. \bpublisherElsevier. \endbibitem

- Christensen and Amemiya (2002) {barticle}[author] \bauthor\bsnmChristensen, \bfnmWilliam F\binitsW. F. and \bauthor\bsnmAmemiya, \bfnmYasuo\binitsY. (\byear2002). \btitleLatent variable analysis of multivariate spatial data. \bjournalJournal of the American Statistical Association \bvolume97 \bpages302–317. \endbibitem

- Conway (1985) {bbook}[author] \bauthor\bsnmConway, \bfnmJohn B\binitsJ. B. (\byear1985). \btitleA course in functional analysis \bvolume96. \bpublisherSpringer Science & Business Media. \endbibitem

- Cressie (2015) {bbook}[author] \bauthor\bsnmCressie, \bfnmNoel\binitsN. (\byear2015). \btitleStatistics for spatial data. \bpublisherJohn Wiley & Sons. \endbibitem

- Cressie and Wikle (2015) {bbook}[author] \bauthor\bsnmCressie, \bfnmN.\binitsN. and \bauthor\bsnmWikle, \bfnmC. K.\binitsC. K. (\byear2015). \btitleStatistics for spatio-temporal data. \bpublisherJohn Wiley & Sons. \endbibitem

- Cristadoro et al. (2005) {barticle}[author] \bauthor\bsnmCristadoro, \bfnmRiccardo\binitsR., \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmReichlin, \bfnmLucrezia\binitsL. and \bauthor\bsnmVeronese, \bfnmGiovanni\binitsG. (\byear2005). \btitleA core inflation indicator for the euro area. \bjournalJournal of Money, Credit and Banking \bvolume37 \bpages539–560. \endbibitem

- Dahlhaus and Künsch (1987) {barticle}[author] \bauthor\bsnmDahlhaus, \bfnmR\binitsR. and \bauthor\bsnmKünsch, \bfnmH\binitsH. (\byear1987). \btitleEdge effects and efficient parameter estimation for stationary random fields. \bjournalBiometrika \bvolume74 \bpages877–882. \endbibitem

- Deb, Pourahmadi and Wu (2017) {barticle}[author] \bauthor\bsnmDeb, \bfnmSoudeep\binitsS., \bauthor\bsnmPourahmadi, \bfnmMohsen\binitsM. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2017). \btitleAn asymptotic theory for spectral analysis of random fields. \bjournalElectronic Journal of Statistics \bvolume11 \bpages4297–4322. \endbibitem

- El Machkouri and Volnỳ (2003) {binproceedings}[author] \bauthor\bsnmEl Machkouri, \bfnmMohamed\binitsM. and \bauthor\bsnmVolnỳ, \bfnmDalibor\binitsD. (\byear2003). \btitleContre-exemple dans le théorème central limite fonctionnel pour les champs aléatoires réels. In \bbooktitleAnnales de l’IHP Probabilités et statistiques \bvolume39 \bpages325–337. \endbibitem

- El Machkouri, Volnỳ and Wu (2013) {barticle}[author] \bauthor\bsnmEl Machkouri, \bfnmMohamed\binitsM., \bauthor\bsnmVolnỳ, \bfnmDalibor\binitsD. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2013). \btitleA central limit theorem for stationary random fields. \bjournalStochastic Processes and their Applications \bvolume123 \bpages1–14. \endbibitem

- Fan, Liao and Mincheva (2013) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmLiao, \bfnmYuan\binitsY. and \bauthor\bsnmMincheva, \bfnmMartina\binitsM. (\byear2013). \btitleLarge covariance estimation by thresholding principal orthogonal complements. \bjournalJournal of the Royal Statistical Society Series B: Statistical Methodology \bvolume75 \bpages603–680. \endbibitem

- Forni and Lippi (2001) {barticle}[author] \bauthor\bsnmForni, \bfnmMario\binitsM. and \bauthor\bsnmLippi, \bfnmMarco\binitsM. (\byear2001). \btitleThe generalized dynamic factor model: representation theory. \bjournalEconometric theory \bvolume17 \bpages1113–1141. \endbibitem

- Forni et al. (2000) {barticle}[author] \bauthor\bsnmForni, \bfnmM.\binitsM., \bauthor\bsnmHallin, \bfnmM.\binitsM., \bauthor\bsnmLippi, \bfnmM.\binitsM. and \bauthor\bsnmReichlin, \bfnmL.\binitsL. (\byear2000). \btitleThe generalized dynamic-factor model: Identification and estimation. \bjournalReview of Economics and statistics \bvolume82 \bpages540–554. \endbibitem

- Forni et al. (2005) {barticle}[author] \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmLippi, \bfnmMarco\binitsM. and \bauthor\bsnmReichlin, \bfnmLucrezia\binitsL. (\byear2005). \btitleThe generalized dynamic factor model: one-sided estimation and forecasting. \bjournalJournal of the American statistical association \bvolume100 \bpages830–840. \endbibitem

- Forni et al. (2009) {barticle}[author] \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmGiannone, \bfnmDomenico\binitsD., \bauthor\bsnmLippi, \bfnmMarco\binitsM. and \bauthor\bsnmReichlin, \bfnmLucrezia\binitsL. (\byear2009). \btitleOpening the black box: Structural factor models with large cross sections. \bjournalEconometric Theory \bvolume25 \bpages1319–1347. \endbibitem

- Forni et al. (2015) {barticle}[author] \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmLippi, \bfnmMarco\binitsM. and \bauthor\bsnmZaffaroni, \bfnmPaolo\binitsP. (\byear2015). \btitleDynamic factor models with infinite-dimensional factor spaces: One-sided representations. \bjournalJournal of Econometrics \bvolume185 \bpages359–371. \endbibitem

- Forni et al. (2017) {barticle}[author] \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmLippi, \bfnmMarco\binitsM. and \bauthor\bsnmZaffaroni, \bfnmPaolo\binitsP. (\byear2017). \btitleDynamic factor models with infinite-dimensional factor space: Asymptotic analysis. \bjournalJournal of Econometrics \bvolume199 \bpages74–92. \endbibitem

- Geweke (1977) {bincollection}[author] \bauthor\bsnmGeweke, \bfnmJohn\binitsJ. (\byear1977). \btitleThe dynamic factor analysis of economic time series. In \bbooktitleLatent Variables in Socio-Economic Models 1 (\beditor\bfnmD. J.\binitsD. J. \bsnmAigner and \beditor\bfnmA. S.\binitsA. S. \bsnmGoldberger, eds.) \bpages365–383. \bpublisherNorth-Holland. \endbibitem

- Hallin, Hörmann and Lippi (2018) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmHörmann, \bfnmSiegfried\binitsS. and \bauthor\bsnmLippi, \bfnmMarco\binitsM. (\byear2018). \btitleOptimal dimension reduction for high-dimensional and functional time series. \bjournalStatistical Inference for Stochastic Processes \bvolume21 \bpages385–398. \endbibitem

- Hallin and Lippi (2013) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM. and \bauthor\bsnmLippi, \bfnmMarco\binitsM. (\byear2013). \btitleFactor models in high-dimensional time series—A time-domain approach. \bjournalStochastic processes and their applications \bvolume123 \bpages2678–2695. \endbibitem

- Hallin and Liška (2007) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM. and \bauthor\bsnmLiška, \bfnmRoman\binitsR. (\byear2007). \btitleDetermining the number of factors in the general dynamic factor model. \bjournalJournal of the American Statistical Association \bvolume102 \bpages603–617. \endbibitem

- Hallin and Liška (2011) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM. and \bauthor\bsnmLiška, \bfnmRoman\binitsR. (\byear2011). \btitleDynamic factors in the presence of blocks. \bjournalJournal of Econometrics \bvolume163 \bpages29–41. \endbibitem

- Hallin and Trucíos (2021) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM. and \bauthor\bsnmTrucíos, \bfnmCarlos\binitsC. (\byear2021). \btitleForecasting value-at-risk and expected shortfall in large portfolios: A general dynamic factor model approach. \bjournalEconometrics and Statistics \bvolume27 \bpages1–15. \endbibitem

- Heaton et al. (2018) {barticle}[author] \bauthor\bsnmHeaton, \bfnmMatthew J\binitsM. J., \bauthor\bsnmDatta, \bfnmAbhirup\binitsA., \bauthor\bsnmFinley, \bfnmAndrew O\binitsA. O., \bauthor\bsnmFurrer, \bfnmReinhard\binitsR., \bauthor\bsnmGuinness, \bfnmJoseph\binitsJ., \bauthor\bsnmGuhaniyogi, \bfnmRajarshi\binitsR., \bauthor\bsnmGerber, \bfnmFlorian\binitsF., \bauthor\bsnmGramacy, \bfnmRobert B\binitsR. B., \bauthor\bsnmHammerling, \bfnmDorit\binitsD., \bauthor\bsnmKatzfuss, \bfnmMatthias\binitsM. \betalet al. (\byear2018). \btitleA case study competition among methods for analyzing large spatial data. \bjournalJournal of Agricultural, Biological and Environmental Statistics \bvolume24 \bpages398–425. \endbibitem

- Lam and Yao (2012) {barticle}[author] \bauthor\bsnmLam, \bfnmClifford\binitsC. and \bauthor\bsnmYao, \bfnmQiwei\binitsQ. (\byear2012). \btitleFactor modeling for high-dimensional time series: inference for the number of factors. \bjournalThe Annals of Statistics \bvolume40 \bpages694–726. \endbibitem

- Lancaster and Tismenetsky (1985) {bbook}[author] \bauthor\bsnmLancaster, \bfnmPeter\binitsP. and \bauthor\bsnmTismenetsky, \bfnmMiron\binitsM. (\byear1985). \btitleThe theory of matrices: with applications. \bpublisherElsevier. \endbibitem

- Lawley and Maxwell (1971) {bbook}[author] \bauthor\bsnmLawley, \bfnmDerrick Norman\binitsD. N. and \bauthor\bsnmMaxwell, \bfnmAlbert Ernest\binitsA. E. (\byear1971). \btitleFactor analysis as a statistical method. \bpublisherButterworths. \endbibitem

- Lazar (2008) {bbook}[author] \bauthor\bsnmLazar, \bfnmNicole\binitsN. (\byear2008). \btitleThe statistical analysis of functional MRI data. \bpublisherSpringer Science & Business Media. \endbibitem

- Lehmann (1999) {bbook}[author] \bauthor\bsnmLehmann, \bfnmErich Leo\binitsE. L. (\byear1999). \btitleElements of large-sample theory. \bpublisherSpringer. \endbibitem

- Leonenko (1999) {bbook}[author] \bauthor\bsnmLeonenko, \bfnmNikolai\binitsN. (\byear1999). \btitleLimit theorems for random fields with singular spectrum \bvolume465. \bpublisherSpringer Science & Business Media. \endbibitem

- Mandrekar and Redett (2017) {bbook}[author] \bauthor\bsnmMandrekar, \bfnmV. S.\binitsV. S. and \bauthor\bsnmRedett, \bfnmD. A.\binitsD. A. (\byear2017). \btitleWeakly Stationary Random Fields, Invariant Subspaces and Applications. \bpublisherChapman and Hall/CRC. \endbibitem

- Park et al. (2009) {barticle}[author] \bauthor\bsnmPark, \bfnmByeong U\binitsB. U., \bauthor\bsnmMammen, \bfnmEnno\binitsE., \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW. and \bauthor\bsnmBorak, \bfnmSzymon\binitsS. (\byear2009). \btitleTime series modelling with semiparametric factor dynamics. \bjournalJournal of the American Statistical Association \bvolume104 \bpages284–298. \endbibitem

- Proietti and Giovannelli (2021) {barticle}[author] \bauthor\bsnmProietti, \bfnmTommaso\binitsT. and \bauthor\bsnmGiovannelli, \bfnmAlessandro\binitsA. (\byear2021). \btitleNowcasting monthly GDP with big data: A model averaging approach. \bjournalJournal of the Royal Statistical Society Series A: Statistics in Society \bvolume184 \bpages683–706. \endbibitem

- Royden and Fitzpatrick (1988) {bbook}[author] \bauthor\bsnmRoyden, \bfnmHalsey Lawrence\binitsH. L. and \bauthor\bsnmFitzpatrick, \bfnmPatrick\binitsP. (\byear1988). \btitleReal analysis \bvolume32. \bpublisherMacmillan New York. \endbibitem

- Rozanov (1967) {bbook}[author] \bauthor\bsnmRozanov, \bfnmYuri Anatolevich\binitsY. A. (\byear1967). \btitleStationary random processes. \bpublisherHolden-Day. \endbibitem

- Rudin (1987) {bbook}[author] \bauthor\bsnmRudin, \bfnmWalter\binitsW. (\byear1987). \btitleReal and complex analysis. 1987. \bpublisherMcGraw-Hill. \endbibitem

- Sargent and Sims (1977) {barticle}[author] \bauthor\bsnmSargent, \bfnmThomas J\binitsT. J. and \bauthor\bsnmSims, \bfnmChristopher A\binitsC. A. (\byear1977). \btitleBusiness cycle modeling without pretending to have too much a priori economic theory. \bjournalNew methods in business cycle research \bvolume1 \bpages145–168. \endbibitem

- Stein (2012) {bbook}[author] \bauthor\bsnmStein, \bfnmMichael L\binitsM. L. (\byear2012). \btitleInterpolation of spatial data: some theory for kriging. \bpublisherSpringer Science & Business Media. \endbibitem

- Stock and Watson (2002) {barticle}[author] \bauthor\bsnmStock, \bfnmJames H\binitsJ. H. and \bauthor\bsnmWatson, \bfnmMark W\binitsM. W. (\byear2002). \btitleForecasting using principal components from a large number of predictors. \bjournalJournal of the American Statistical Association \bvolume97 \bpages1167–1179. \endbibitem

- Sun and Genton (2011) {barticle}[author] \bauthor\bsnmSun, \bfnmYing\binitsY. and \bauthor\bsnmGenton, \bfnmMarc G\binitsM. G. (\byear2011). \btitleFunctional boxplots. \bjournalJournal of Computational and Graphical Statistics \bvolume20 \bpages316–334. \endbibitem

- Trucíos et al. (2022) {barticle}[author] \bauthor\bsnmTrucíos, \bfnmCarlos\binitsC., \bauthor\bsnmMazzeu, \bfnmJoão HG\binitsJ. H., \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmHotta, \bfnmLuiz K\binitsL. K., \bauthor\bsnmValls Pereira, \bfnmPedro L\binitsP. L. and \bauthor\bsnmZevallos, \bfnmMauricio\binitsM. (\byear2022). \btitleForecasting conditional covariance matrices in high-dimensional time series: a general dynamic factor approach. \bjournalJournal of Business & Economic Statistics \bvolume41 \bpages40–52. \endbibitem

- Tzourio-Mazoyer et al. (2002) {barticle}[author] \bauthor\bsnmTzourio-Mazoyer, \bfnmNathalie\binitsN., \bauthor\bsnmLandeau, \bfnmBrigitte\binitsB., \bauthor\bsnmPapathanassiou, \bfnmDimitri\binitsD., \bauthor\bsnmCrivello, \bfnmFabrice\binitsF., \bauthor\bsnmEtard, \bfnmOlivier\binitsO., \bauthor\bsnmDelcroix, \bfnmNicolas\binitsN., \bauthor\bsnmMazoyer, \bfnmBernard\binitsB. and \bauthor\bsnmJoliot, \bfnmMarc\binitsM. (\byear2002). \btitleAutomated anatomical labeling of activations in SPM using a macroscopic anatomical parcellation of the MNI MRI single-subject brain. \bjournalNeuroimage \bvolume15 \bpages273–289. \endbibitem

- Vanmarcke (2010) {bbook}[author] \bauthor\bsnmVanmarcke, \bfnmE.\binitsE. (\byear2010). \btitleRandom fields: analysis and synthesis. \bpublisherWorld scientific. \endbibitem

- Wang and Wall (2003) {barticle}[author] \bauthor\bsnmWang, \bfnmFujun\binitsF. and \bauthor\bsnmWall, \bfnmMelanie M\binitsM. M. (\byear2003). \btitleGeneralized common spatial factor model. \bjournalBiostatistics \bvolume4 \bpages569–582. \endbibitem

- Whittle (1954) {barticle}[author] \bauthor\bsnmWhittle, \bfnmPeter\binitsP. (\byear1954). \btitleOn stationary processes in the plane. \bjournalBiometrika \bpages434–449. \endbibitem