Asymptotic Theory of the Best-Choice Rerandomization using the Mahalanobis Distance

Abstract

Rerandomization, a design that utilizes pretreatment covariates and improves their balance between different treatment groups, has received attention recently in both theory and practice. There are at least two types of rerandomization that are used in practice: the first rerandomizes the treatment assignment until covariate imbalance is below a prespecified threshold; the second randomizes the treatment assignment multiple times and chooses the one with the best covariate balance. In this paper we will consider the second type of rerandomization, namely the best-choice rerandomization, whose theory and inference are still lacking in the literature. In particular, we will focus on the best-choice rerandomization that uses the Mahalanobis distance to measure covariate imbalance, which is one of the most commonly used imbalance measure for multivariate covariates and is invariant to affine transformations of covariates. We will study the large-sample repeatedly sampling properties of the best-choice rerandomization, allowing both the number of covariates and the number of tried complete randomizations to increase with the sample size. We show that the asymptotic distribution of the difference-in-means estimator is more concentrated around the true average treatment effect under rerandomization than under the complete randomization, and propose large-sample accurate confidence intervals for rerandomization that are shorter than that for the completely randomized experiment. We further demonstrate that, with moderate number of covariates and with the number of tried randomizations increasing polynomially with the sample size, the best-choice rerandomization can achieve the ideally optimal precision that one can expect even with perfectly balanced covariates. The developed theory and methods for rerandomization are also illustrated using real field experiments.

Keywords: potential outcome; randomization-based inference; optimal rerandomization; diverging number of covariates; Berry–Esseen bound

Introduction

Fisher (1925) advocated randomization in experimental design since it can eliminate bias and permit valid test of significance (Hall 2007). Since then, randomized experiments have become the gold standard for studying causal effects in many research areas, such as randomized clinical trials in medical research, randomized field experiments in social science, and online experiments in technology companies. The completely randomized experiment (CRE) has become one of the most popular designs due to its simplicity in both implementation and analysis. In addition, the CRE can balance all potential confounding factors, no matter observed or unobserved on average, and can justify simple and intuitive comparison between different treatment groups. For example, the difference between outcome means in two treatment groups, often called the difference-in-means estimator, is unbiased for the true average treatment effect (Neyman 1923).

However, as commented by Fisher (1926), most experimenters carrying out random assignments of plots will be shocked to find out how far from equally the plots distribute themselves, and more recently by Morgan and Rubin (2012), with mutually independent covariates and at significance level, the usual covariate balance test will be significant for at least one covariate with probability about . Note that the covariate balance test has become a common practice when reporting randomized experiments nowadays. When chance imbalances are observed, researchers may worry about the results from the experiment, since the difference between the treatment groups in comparison may be to due to the difference in pretreatment covariates. Technically speaking, this is related to the variability of the treatment effect estimation, and, as we demonstrate later, we can reduce the variability of the treatment effect estimator or equivalently enhance its precision by improving the balance of pretreatment covariates.

The classical solution to avoiding chance imbalance of pretreatment covariates is blocking (Fisher 1935; Box et al. 2005), which, however, works mainly when we only have a few discrete covariates. Through a survey of leading researchers carrying out randomized experiments in developing countries, Bruhn and McKenzie (2009) discovered several rerandomization methods that are used in practice to improve covariate balance but are not well discussed in print. Rerandomization turns out to provide a general solution to the covariate balance issue, which can easily accommodate many covariates of various types. Although its idea has existed for a long time in the literature tracing back to Fisher (Savage 1962, Page 88), Gosset Student (1938), Cox Cox (1982) and etc., the rerandomization design is formally proposed until recently by Morgan and Rubin (2012), who also adopted and advocated the Fisher randomization test to analyze such a design. As discussed in Bruhn and McKenzie (2009), there are at least two types of rerandomization: the first specifies a certain covariate balance criterion and keeps drawing treatment assignments until getting an acceptable one, and the second draws, say, , randomizations and chooses the one with the best covariance balance based on a certain covariate imbalance measure. Both of them are intuitive designs and have been commonly used in practice, but their analysis is not straightforward compared to the classical and well-studied CRE. Recently Li et al. (2018) studied the large-sample theory for the first type of rerandomization, revealing a general non-Gaussian asymptotic distribution for the usual difference-in-means estimator; see, e.g., Li and Ding (2020); Li et al. (2020); Yang et al. (2021); Zhao and Ding (2021); Wang et al. (2021); Lu et al. (2022); Cohen and Fogarty (2022); Branson et al. (2022); Wang and Li (2022) for related extensions.

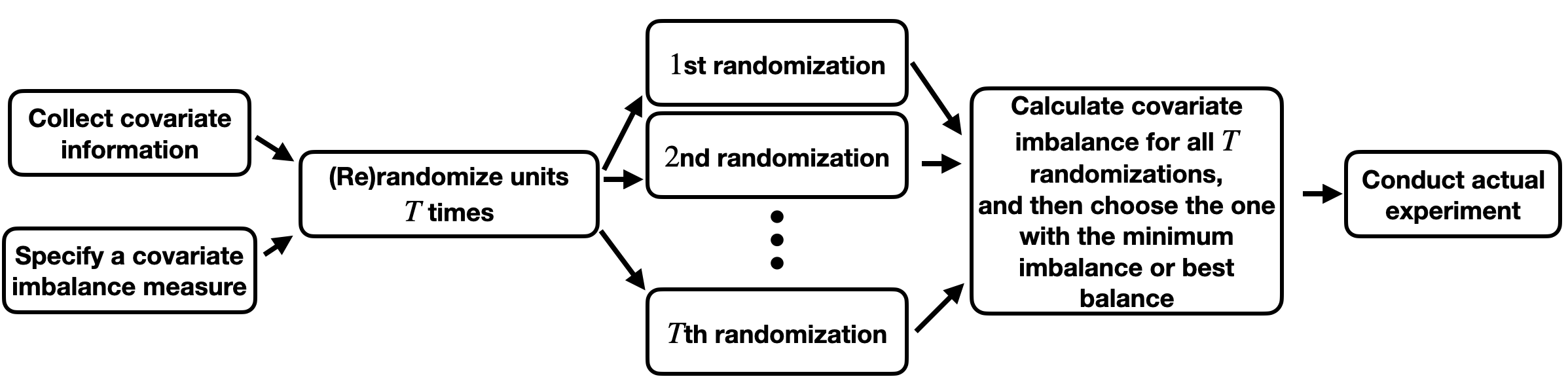

In this paper we will focus on the second type of rerandomization, which randomizes the treatment assignment multiple times and chooses the one with the best covariate balance, and, to distinguish it from the first type, we will call it the best-choice rerandomization. The best-choice rerandomization has received less attention in theory, despite its popularity in practice. Our goal is to address this theoretical gap by developing the large-sample theory and inference for the best-choice rerandomization. Specifically, we will consider the best-choice rerandomization design that draws complete randomizations and chooses the one with the smallest covariate imbalance measured by the Mahalanobis distance, which is one of the most popular imbalance measure for multivariate covariates. A general procedure of a best-choice rerandomization is illustrated using the diagram in Figure 1, in parallel with Morgan and Rubin (2012, Figure 1) for the first type of rerandomization. Specifically, we first randomly and independently draw treatment assignments times, then calculate the covariate balance for each of these assignments based on some prespecified measure, and finally choose the one with the best balance and use that to conduct the actual experiment.

Compared to the first type of rerandomization that discards assignments with bad covariate balance, the best-choice rerandomization has at least two salient features that can overcome some drawbacks of the first type. First, when the prespecified covariate balance criterion is too stringent, it is possible that no assignment will be acceptable under the first type of rerandomization. Second, even if there are acceptable assignments, it may take a long, random, and thus uncertain computation time to get an acceptable assignment for the first type of rerandomization. In contrast, the best-choice rerandomization can always produce a feasible assignment, and can always get that in a prespecified time. Despite these, it is not clear from the existing literature that how a proper statistical inference can be conducted for the best-choice rerandomization. Note that, following Morgan and Rubin (2012), we can still use Fisher randomization test, but it will work only for sharp null hypotheses that generally requires constant-effect-type assumptions or more broadly bounded null hypotheses that typically focus on the extreme individual effect (Caughey et al. 2023). In this paper, we will instead focus on Neyman (1923)’s large-sample repeated sampling inference for the average treatment effect, allowing unknown individual effect heterogeneity, and demonstrate the advantage of rerandomization over complete randomization. We also want to point out that the main purpose of this paper is not to compare the two types of rerandomization, but rather to provide large-sample inference tools for practitioners that design and analyze experiments from the second type of rerandomization.

Another question that will receive special attention in our paper is the choice of , the number of tried complete randomizations. Intuitively, larger can provide greater covariate balance and seems an attractive option for practitioners. However, when is overly large and in particular is infinite in the extreme case, all possible treatment assignments will be enumerated and the best-choice rerandomization will essentially choose the one with the best balance from all possible assignments. When some covariates are continuous, this will generally lead to an almost deterministic design where there is no randomness in the treatment assignment. This apparently violates Fisher’s principle of experimental design. A natural question to ask is then: how large can and should be so that (i) there is still sufficient randomness in the treatment assignment for robust causal inference and (ii) rerandomization can achieve an “optimal” efficiency for treatment effect estimation? To the best of our knowledge, the choice of has been theoretically investigated only recently by Banerjee et al. (2020), from an ambiguity-averse decision-making perspective. Specifically, the authors considered an -contamination-type model (Huber 1964), which essentially allows model or prior misspecification, to facilitate the discussion on the trade-off between subjective expected performance and robust performance guarantees. They found that the loss in robustness due to rerandomization is of order , with denoting the number of tried complete randomizations and denoting the number of experimental units, and suggested choosing less than the sample size , ensuring the loss is on the order of . We will also study the same issue on the choice of , but from a different perspective. In particular, we will focus on the feasibility of a large-sample randomization-based robust inference for treatment effects. In addition, we will also investigate the role of the number of covariates in rerandomization.

The paper proceeds as follows. Section 2 introduces the framework and notation. Section 3 studies the asymptotic properties of the best-choice rerandomization. Section 4 investigates whether the best-choice rerandomization can achieve its ideally optimal precision that one can expect even with perfectly balanced covariates. Section 5 proposes large-sample valid inference for the best-choice rerandomization. Section 6 conducts simulations to illustrate our theory, and Section 7 concludes with a short discussion.

Framework and Notation

2.1 Potential outcomes, covariates and treatment assignments

Consider an experiment with units, where of them will receive some active treatment and the remaining will receive control. We invoke the potential outcome framework to define treatment effects (Neyman 1923; Rubin 1974). For each unit , let and denote the treatment and control potential outcomes, and be the corresponding individual treatment effect. We are interested in inferring the average treatment effect , where and denote the average treatment and control potential outcomes, respectively. The fundamental difficulty of causal inference is that we can observe at most one potential outcome for each unit and thus half of the potential outcomes will be missing. Specifically, for each unit , let be the treatment assignment indicator, where if the unit receives treatment and otherwise. The observed outcome for each unit is then , one of the two potential outcomes.

Throughout the paper, we will conduct the randomization-based inference (Neyman 1923; Li and Ding 2017), also called the design-based or finite population inference, where all the potential outcomes (as well as the pretreatment covariates introduced shortly) for the experimental units are viewed as fixed constants or equivalently being conditioned on. The finite population inference has the advantage of avoiding any model or distributional assumptions on the potential outcomes and covariates (as well as their dependence structure). The randomness in the observed data comes solely from the random treatment assignment. Therefore, the distribution of the treatment assignment vector , also called the treatment assignment mechanism (Rubin 1978), governs the data generating process and is crucial for statistical inference. In a randomized experiment, the experimenter can generate the treatment assignment vector from a carefully prespecified or designed distribution, based on which units will be allocated into treatment and control groups.

The completely randomized experiment (CRE) is one of the most commonly used treatment assignment mechanism, under which the treatment assignment vector takes a particular value with probability if and zero otherwise.

2.2 Covariate imbalance and rerandomization

Let denote the available pretreatment covariate vector for each unit , denote the average covariate vector for all units, and denote the finite population covariance matrix of covariates. We further introduce

| (1) |

to denote the difference-in-means of covariates, where and denote the average covariates in treated and control groups, and denote its covariance matrix under the CRE by .

In practice, it is often a routine to check the imbalance of the pretreatment covariates when conducting randomized experiments. In this paper we will focus on the Mahalanobis distance imbalance measure, which is one of the most commonly used imbalance measure for multivariate covariates, enjoys the affine invariant property, and has the following form:

| (2) |

When the covariates, especially those likely to have strong associations with the potential outcomes, are imbalanced, we may worry about the results from the experiment. In particular, we may worry that the difference in outcomes between treated and control groups is due to the difference in baseline covariates, instead of the treatment effects. Moreover, as discussed earlier, covariate imbalance is not rare even under the intuitive and commonly used CRE (Morgan and Rubin 2012). Therefore, a design that can mitigate or avoid unlucky and bad chance covariate imbalance will be highly desirable.

Rerandomization is a general design that can improve the balance of pretreatment covariates, by checking covariate balance prior to conducting the actual experiment. This is feasible, since the covariate balance depends only on the treatment assignment and pretreatment covariates, without involving any post-treatment variables. Throughout the paper, we will focus on the best-choice rerandomization using the Mahalanobis distance. Specifically, we first completely randomize the units or equivalently draw treatment assignments from the CRE times, where is a prespecified integer, then calculate the Mahalanobis distance in (2) for each of these complete randomizations, and finally choose the treatment assignment with the minimum Mahalanobis distance to conduct the actual experiment; see also Figure 1 for a general best-choice rerandomization. In this paper we aim to develop the large-sample theory and inference for the best-choice rerandomization under the randomization-based inference framework.

2.3 Difference-in-means of the outcome and covariates under the CRE

Throughout the paper we will focus on the inference of the average treatment effect under the best-choice rerandomization. Moreover, we will focus on the intuitive difference-in-means estimator:

| (3) |

which is the difference between the average observed outcomes in treated and control groups. As discussed shortly, the joint distribution of the difference-in-means of the outcome and covariates in (3) and (1) under the CRE plays an important role in studying the property of the best-choice rerandomization. Below we discuss its first two moments, i.e., mean and covariance matrix.

Recall that denotes the finite population covariance matrix of the covariates. For , let be the finite population variance of potential outcomes, and be the finite population covariance between potential outcomes and covariates. Define analogously as the finite population variance of individual effects and as the finite population covariance between individual effects and covariates. From Li et al. (2018), under the CRE, the difference-in-means of the outcome and covariates has mean , indicating that the difference-in-means estimator is unbiased for the true average effect and the covariates are balanced on average between the two treatment groups, and covariance matrix

| (4) |

Below we further introduce an important measure for the association between potential outcomes and covariates, which will play an important role in studying the asymptotic properties of the best-choice rerandomization. Specifically, we will consider the squared multiple correlation between the difference-in-means of the outcome and covariates under the CRE as an -type measure for the association between potential outcomes and covariates:

| (5) |

where the equivalent forms follow from Li et al. (2018). In (5), denotes the finite population variance of the linear projections of potential outcomes on covariates, for , and analogously denotes the finite population variance of the linear projections of individual effects on covariates. When treatment effects are additive, in the sense that is constant across all , reduces to , the squared multiple correlation between control potential outcomes and covariates (i.e., the proportion of variability in the control potential outcomes that can be linearly explained by the covariates).

2.4 Finite population asymptotics and Berry–Esseen-type bounds

Because the exact distribution of the difference-in-means estimator is generally intractable under the best-choice rerandomization, we will invoke large-sample approximations. Specifically, we will conduct the finite population asymptotics that embeds the finite population of size into a sequence of finite populations with increasing sizes; see Li and Ding (2017) for a review with an emphasize on applications to causal inference. Importantly, as pointed out by Neyman (1923) in his seminal paper, under the CRE and when the sample size is large, the distribution of the difference-in-means of the outcome in (3) (and analogously of covariates in (1)) can be well approximated by an Gaussian distribution; see, for example, Hájek (1960) for a rigorous proof and Li and Ding (2017) for extension to vector outcomes with multivariate Gaussian approximation.

Furthermore, in our large-sample analysis for the best-choice rerandomization, we will allow both the number of tried complete randomizations and the number of covariates to vary (say, increase) with the sample size. Specifically, we will view and as and in the remainder of the paper; for descriptive convenience, we will keep such dependence on the sample size implicit. In order to deal with the sample size dependent and , we need a more delicate characterization of the multivariate Gaussian approximation under the CRE. In particular, we will consider the following Berry–Esseen-type bound for the Gaussian approximation of the joint distribution of the difference-in-means of the outcome and covariates under the CRE:

| (6) |

where denotes the collection of all measurable convex sets in , is a dimensional standard Gaussian random vector, and is defined as in (4). Based on Raič (2015)’s conjecture, there exists an absolute constant such that with

| (7) |

where , and denote the finite population mean and covariance of the ’s, and denotes the inverse of the positive semidefinite square root of . Wang and Li (2022) recently proved that ; see also Wang and Li (2022, Theorem 2) and Shi and Ding (2022) for other forms of Berry-Esseen-type bounds on . We will then assume the following regularity condition along the sequence of finite populations, which can guarantee the Gaussian approximation for the difference-in-means of the outcome and covariates (or equivalently that converges to zero as ).

Condition 1.

As the size of the finite population , in (7) converges to zero.

Condition 1 implicitly requires that the potential outcomes and covariates are not too heavy-tailed, and that the number of covariates does not increase too fast with the sample size. Specifically, Condition 1 implies that (Wang and Li 2022).

In addition, we impose the following condition that the number of tried complete randomizations does not increase too fast with the sample size. This will be discussed and emphasized in detail later.

Condition 2.

As , , or equivalently .

Asymptotic theory for the best-choice rerandomization

3.1 The best-choice rerandomization using the Mahalanobis distance

To formally introduce the best-choice rerandomization design, we first introduce several notations. Let and denote mutually independent treatment assignment vectors from the CRE with and units receiving treatment and control, respectively. For each , let be the difference-in-means of covariates as in (1) under the treatment assignment , and be the corresponding Mahalanobis distance for covariate imbalance as in (2).

With a slight abuse of notation, we use to denote the minimum Mahalnobis distance, with the subscript representing the index in that achieves this minimum. If there are multiple treatment assignments achieving the minimum at the same time, we will then randomly choose one from them. Consequently, will be the treatment assignment with the minimum covariate imbalance (measured by the Mahalanobis distance) among all the complete randomizations. Under the best-choice rerandomization, as illustrated in Figure 1, we will use the “best” assignment to conduct the actual experiment (or more precisely to conduct the actual treatment allocation). We emphasize that the best-choice rerandomization depends the number of tried complete randomizations; for descriptive convenience, we will make such dependence implicit, unless otherwise stated.

3.2 Difference-in-means estimator under the best-choice rerandomization

We consider the intuitive difference-in-means estimator in (3) to estimate the average treatment effect under the best-choice rerandomization. Specifically, recalling that is the treatment assignment actually implemented under the best-choice rerandomization, we will denote the corresponding difference-in-means estimator by , where we use the subscript to emphasize that it is the estimator under the treatment assignment with the minimum covariate imbalance. Below we will study the asymptotic distribution of under the best-choice rerandomization.

By the construction of the best-choice rerandomization design, the distribution of relies on the joint distribution of the differences in means of the outcome and covariates for the mutually independent complete randomizations. From Section 2.4, under certain regularity conditions, these differences in means are approximately Gaussian distributed. Thus, intuitively, we can approximate the distribution of by the corresponding part implied by the multivariate Gaussian approximations. As demonstrated below, such an intuition can be made rigorous under Conditions 1 and 2.

Let , , be mutually independent Gaussian random vectors with mean zero and covariance matrix in (4), which can be viewed as Gaussian approximations for the differences in means of the outcome and covariates from the mutually independent completely randomizations. Define analogously as in (2) for , and let be the minimum among the ’s. With a slight abuse of notation, we use the subscript to denote the index in achieving this minimum; when there are multiple indices (i.e., ties) achieving the minimum at the same time, we randomly choose one from them. Consequently, is one of the ’s that corresponds to the minimum value of the ’s. By construction of the best-choice rerandomization, corresponds to under the Gaussian approximation. The theorem below characterizes the difference between the distributions of and .

Theorem 1.

Theorem 1 justifies the asymptotic approximation for the difference-in-means estimator under the best-choice rerandomization. Below we consider simplifying the distribution of . Let , for , be independent and identically distributed (i.i.d.) -dimensional standard Gaussian vectors, i.e., . We further define the following constrained Gaussian variable:

| (9) |

Recall the squared multiple correlation in (5).

Theorem 2.

Remark 1.

For the first type of rerandomization using the Mahalanobis distance, Wang and Li (2022) showed that, under Condition 1, the supremum distance between the distribution functions of the standardized difference-in-means estimator under rerandomization and the corresponding constrained-Gaussian approximation as in (8) is of order , with being the approximate acceptance probability under the given imbalance threshold.222In Wang and Li (2022), the approximate acceptance probability is defined as , where is the chi-squared random variable with degrees of freedom and is the given imbalance threshold. This is because under Condition 1, the distribution of the Mahalanobis distance is approximately , so that . Thus, the first and second types of rerandomization share similar approximation error (at least in terms of the derived upper bounds) when and are of the same order. This is not surprising from their implementation. Under the first type of rerandomization, in expectation, we will draw about assignments to get an acceptable one; while under the second type, we will deterministically draw assignments to get an acceptable one, which is the one with the best balance. Nevertheless, the technical derivation for these error bounds is considerably different for these two types of rerandomization.

3.3 Representation for the asymptotic distribution under rerandomization

From Theorems 1 and 2, the asymptotic distribution of the difference-in-means estimator under the best-choice rerandomization can be approximated by the distribution in (10), which involves the constrained Gaussian random variable in (9). Below we will give a representation of , which can facilitate its simulation.

Let be the first coordinate of a -dimensional random vector uniformly distributed on the -dimensional unit sphere, be a random sign with probability being and , be a Beta random variable that degenerates to when . Let and be i.i.d. chi-squared random variables with degrees of freedom , and be the minimum of these i.i.d. chi-squared random variables. Define further the following constrained chi-squared random variable:

| (11) |

where denotes the quantile function for the chi-squared distribution with degrees of freedom , and denotes a Beta random variable with parameters and ; see the supplementary material for a proof of the equivalence in (11).

Proposition 1.

The representation in Proposition 1 is analogous to that in Li et al. (2018) for the first type of rerandomization using the Mahalanobis distance. Both of them have similar forms, except that our representation in (12) involves the order statistic of chi-squared random variables while that in Li et al. (2018) involves truncated chi-squared random variable. This is not surprising given the implementation of the design: the best-choice rerandomization chooses the best one among multiple randomizations, while the first-type rerandomization chooses only those assignments with covariate imbalance below a certain threshold.

More importantly, from Proposition 1 and (11), we can easily simulate the constrained Gaussian random variable using the multiplication of the three random variables in (12), which can be more efficient than using the form in (9). Consequently, we can also efficiently simulate from the asymptotic distribution of in (2). This can be useful when conducting inference for the average treatment effect under the best-choice rerandomization, as discussed in Section 5.

3.4 Improvement from the best-choice rerandomization

In this subsection we will compare the asymptotic properties of the classical CRE and the best-choice rerandomization. Note that the CRE can be viewed as a special case of the best-choice rerandomization with , under which reduces to a standard Gaussian random variable and the asymptotic distribution of the standardized difference-in-means estimator reduces to a standard Gaussian distribution. Below we essentially compare the asymptotic distribution in (2) to the standard Gaussian distribution .

First, both the standard and constrained Gaussian random variables and are symmetric and unimodal around zero. These properties will also be maintained under scaling and convolution. We can then immediately derive the following corollary, which implies that the difference-in-means estimator is asymptotically unbiased under both the CRE and the best-choice rerandomization.

Corollary 1.

The asymptotic distribution for the standardized difference-in-means estimator in (10) is symmetric and unimodal around zero.

Second, we compare the asymptotic variance of the difference-in-means estimator under the two designs. Let denote the variance of the constrained Gaussian random variable in (9) and (12). Note that as implied by (11) and (12). We may use expressions from Nadarajah (2008) for moments of chi-squared order statistics. However, these expressions involves Lauricella functions that are not available in standard software. For simplicity, we will mainly consider Monte Carlo approximation for .

Corollary 2.

Under the best-choice rerandomization, the asymptotic variance of the standardized difference-in-means estimator is smaller than or equal to that under the CRE. Specifically, the percentage reduction in asymptotic variance is , which is nonnegative and nondecreasing in both and .

Intuitively, the covariates can be viewed as potential outcomes that are unaffected by the treatment. Thus, by the same logic, the covariates will be more balanced (or more precisely have smaller asymptotic variances) under the best-choice rerandomization than under the CRE. Moreover, the percentage reduction in asymptotic variance of any linear combination of covariates is , enjoying the “equal percent variance reducing” property (Morgan and Rubin 2012).

Third, we compare the asymptotic quantile ranges of the difference-in-means estimator under the two designs, because the asymptotic distribution under the best-choice rerandomization is generally non-Gaussian and its variability cannot be fully characterized by the variance. Moreover, we will focus on the symmetric quantile range, which will be the shortest at any given coverage level due to the unimodality in Corollary 1 (Casella and Berger 2002). This is also related to the two-sided confidence intervals discussed later in Section 5. For any , let be the th quantile of the standard Gaussian distribution, and be the th quantile of the distribution in (10).

Corollary 3.

Under the best-choice rerandomization, for any , the asymptotic symmetric quantile range is narrower than or equal to that under the CRE. Specifically, the percentage reduction in length of the asymptotic symmetric quantile range is , which is nonnegative and nondecreasing in both and .

From Corollaries 2 and 3, the best-choice rerandomization improves the estimation precision compared to the usual CRE. Moreover, the gain from rerandomization increases with the squared multiple correlation in (5), which characterizes the strength of the association between potential outcomes and the covariates. This is intuitive. When the covariates have stronger association with the potential outcomes (or equivalently can explain more variability in the potential outcomes), the best-choice rerandomization can provide more precision improvement by balancing these covariates.

Corollaries 2 and 3 also imply that the gain from rerandomization increases with the number of tried complete randomizations. However, this does not mean that we should use as many complete randomizations as possible for the best-choice rerandomization. The is because Condition 2 requires that cannot be too large. If is too large, the asymptotic approximation in Theorem 1 may fail, which will further invalidate the results in Corollaries 2 and 3. We will focus on this issue regarding the choice of in the following section.

Optimal best-choice rerandomization

Condition 2 and Corollaries 2 and 3 show the trade-off when choosing the number of tried complete randomizations for the best-choice rerandomization. On the one hand, we want to be small so that the regularity condition is more likely to hold and the asymptotic approximation can be more accurate. On the other hand, we want to be large so that we can gain more improvement in precision from the best-choice rerandomization. In particular, the asymptotic distribution in (10) becomes most concentrated around zero when , under which it reduces to the Gaussian distribution . This is the ideally optimal precision that we can expect from rerandomization, since comes from the variability in potential outcomes that cannot be explained by the covariates. These then naturally lead to the following question: Can we increase at a proper rate of the sample size so that the asymptotic theory for the best-choice rerandomization still holds and it achieves the ideally optimal precision?

Below we first study the asymptotic properties of the constrained Gaussian random variable when both and vary and possibly diverge to infinity. We then study the optimal best-choice rerandomization that can achieve the ideally optimal precision. We finally discuss some practical guidance for the choice of as well as the number of covariates .

4.1 Asymptotic properties of the constrained Gaussian random variable

We study the asymptotic behavior of the constrained Gaussian random variable in (9) and (12) along a sequence of varying ’s. In particular, we will allow both and to diverge to infinity along the sequence, and consider sufficient and necessary conditions for the constrained Gaussian random variable to be asymptotically ignorable. Note that the ’s for any set of ’s are uniformly integrable; see the supplementary material for details. This then implies that if and only if its variance . Moreover, from Corollary 2, is also closely related to the precision gain from the best-choice rerandomization. Therefore, in the following, we will consider mainly the asymptotic behavior of , which turns out to depend critically on the ratio between and . We summarize the results in the following theorem. We use and to denote limit superior and limit inferior, respectively.

Theorem 3.

Along any given sequence of ’s,

-

(i)

if , then ;

-

(ii)

if , then ;

-

(iii)

if , then ;

-

(iv)

if , then .

Theorem 3 has several implications regarding the impact of the relative magnitude of the number of tried complete randomizations and the number of covariates . First, if grows at a super-exponential rate of , in the sense that for , then the constrained Gaussian random variable becomes asymptotically negligible. This indicates that the best-choice rerandomization obtains its ideally optimal efficiency, under which the covariates are also asymptotically exactly balanced. We emphasize that this, however, does not mean we should use as large as possible, because the asymptotic theory in Section 3 may fail when is too large; see the next Section 4.2 for more detailed discussion regarding this issue.

Second, if grows at a sub-exponential rate of , in the sense that for , then the variance of the constrained Gaussian random variable becomes asymptotically the same as that of the unconstrained standard Gaussian random variable. From Corollary 2, the best-choice rerandomization then provides no gain on the precision of the treatment effect estimation. This reminds us that we should not use too many covariates and should try an appropriate number of complete randomizations for the best-choice rerandomization.

Third, if grows at an exponential rate of , in the sense that for bounded away from zero and infinity, then the variance of the constrained Gaussian random variable will be bounded strictly between and . In this case, the best-choice rerandomization still provides precision gain compared to the complete randomization, although there is a gap from the ideally optimal one.

Remark 2.

The asymptotic behavior of the constrained Gaussian random variable is similar to the truncated variable studied in Wang and Li (2022, Theorem 4) with being the th quantile of the chi-squared distribution with degrees of freedom . This is not surprising due to similar reasons as in Remark 1. By their representation in Proposition 1 and Li et al. (2018, Proposition 2), the difference in and comes mainly from the component of the constrained chi-squared random variable. Specifically, involves the minimum order statistic from i.i.d. random variables, while involves the random variable given that it is bounded by the th quantile. Intuitively, both of these constrained random variables are from the smallest proportion of distribution. This intuition may help explain their similar asymptotic behavior. However, an obvious difference between them is that always has a bounded support, while can take value on the whole real line. Moreover, the proof of Theorem 3 relies on the characterization of the order statistics of multiple chi-squared random variables, which is different from its analogue in Wang and Li (2022) that focuses on analyzing a single truncated random variable.

4.2 Optimal best-choice rerandomization with diverging number of tries

We now consider the question at the beginning of this section: Can we let increase at a proper rate of the sample size so that the best-choice rerandomization can achieve the ideally optimal precision asymptotically? From Theorems 1, 2 and 3, such an optimal rerandomization exists if we can find such that Condition 2 holds (i.e., ) and the condition in Theorem 3(i) holds (i.e., ), where the former guarantees the asymptotic approximation and the latter guarantees the optimal precision. We summarize the results below.

Condition 3.

As , .

Theorem 4.

In Theorem 4, we additionally assume that is bounded away from , which is reasonable since in practice we generally do not expect the covariates to perfectly explain all the variability in potential outcomes. Importantly, from Theorem 4, the difference-in-means estimator under the best-choice rerandomization becomes asymptotically Gaussian distributed, and achieves the ideally optimal precision with remaining variation due solely to variability in potential outcomes that cannot be linearly explained by the covariates. In addition, it has the same asymptotic distribution as the linearly regression-adjusted estimator under the CRE (Lin 2013; Li and Ding 2017). Therefore, the best-choice rerandomization is essentially the dual of covariate adjustment, where the former is at the design stage while the latter is at the analysis stage. Moreover, rerandomization has the advantage of being blind to outcomes and can thus avoid data snooping, and the difference-in-means estimator is a more intuitive and transparent estimator for the average treatment effect (Lin 2013; Rosenbaum 2010; Cox 2007; Freedman 2008).

From Theorem 4 and the discussion before, a proper choice of such that Conditions 2 and 3 hold is crucial for designing the optimal best-choice rerandomization. On the one hand, should be small in the sense that to ensure the asymptotic approximation; on the other hand, should be large in the sense that with to ensure the optimal efficiency. Below we investigate under what conditions such a choice of exists. We summarize the results in the following theorem.

Theorem 5.

Under the best-choice rerandomization, assume Condition 1 and .

- (i)

- (ii)

- (iii)

- (iv)

From Theorem 5, under our asymptotic theory, the feasibility of the optimal best-choice rerandomization depends crucially on whether the ratio between and can diverge to infinity. This is similar to that for the first-type of rerandomization studied in Wang and Li (2022); see Remark 3. From Wang and Li (2022, Theorem 2), it is not difficult to see that a sufficient condition for is . To get more intuition, similar to Wang and Li (2022), we consider the asymptotic rate of assuming that units are i.i.d. samples from a certain superpopulation, Specifically, we invoke the following regularity condition for the sequence of superpopulations that generate the finite populations. Recall that for .

Condition 4.

Each finite population consists of i.i.d. ’s from some superpopulation distribution, with being the corresponding standardized vector. Moreover, for some constant and all , the inner product of the standardized vector and any constant unit vector has its -th absolute moment uniformly bounded by an absolute constant, i.e., .

From Lei and Ding (2020, Proposition F.1), a sufficient condition for Condition 4 is that all coordinates of are mutually independent and their -th absolute moment is uniformly bounded. From Wang and Li (2022), under Condition 4, we have

| (14) |

In (14), the lower bound of always hold regardless of Condition 4, and it implies that the upper bound in (14) is precise up to an factor. Suppose that both and are strictly bounded away from zero and one, which is reasonable in practice so that there is nonnegligible proportions of units receiving both treatment arms. Below we will consider three cases for the rate of such that Condition 1 holds with high probability, and the resulting “largest” choice of (ignoring subpolynomial terms) such that Condition 2, as well as the asymptotic approximation, for rerandomization holds with high probability. Let (or if the conjecture in Raič (2015) holds).

-

(i)

[.] In this case, , and we can choose with . Consequently, as implied by Theorem 3(i), and the best-choice rerandomization achieves the ideal optimal efficiency.

-

(ii)

[.] In this case, , and we can choose with . Consequently, as implied by Theorem 3(ii) and (iii), and the best-choice rerandomization has nonnegligible gain over the complete randomization, although there is still a gap from the ideally optimal precision.

-

(iii)

[ with .] In this case, , and we can choose with . Consequently, as implied by Theorem 3(iv), and the best-choice rerandomization provides no gain over the CRE.

The above theoretical results suggest that we should use at most number of covariates in rerandomization. Importantly, we should use those covariates relevant for the potential outcomes (measured by the corresponding as in (5)). In addition, we can try multiple complete randomizations with the number of tries increasing polynomially with the sample size, in order to maximize the efficiency gain while maintaining the robustness. Note that, when some covariates are continuous, is infinitely large and we can enumerate all possible treatment assignments, the best-choice rerandomization will generally become almost deterministic with only one or two (if the two treatment groups have equal sizes) realized assignments; in such cases, robust randomization-based inference is generally infeasible, and inference has to rely on random sampling of units from some (hypothetical) superpopulation (Johansson et al. 2021).

Interestingly, as discussed in the introduction, Banerjee et al. (2020) recently also studied the best-choice rerandomization from an ambiguity averse decision making perspective, and discovered that appropriately diverging number of tried complete randomizations will lead to asymptotically negligible loss on robustness. However, under their framework with a fixed number of covariates, they allow faster growing rate of , which only needs to satisfy that . Note that we generally require to increase at most polynomially with the sample size, in order for our asymptotic theory to work. We do want to emphasize that our requirement on the growing rate of is only sufficient for the asymptotic theory of rerandomization. Whether it is possible to relax such a requirement for studying large-sample randomization-based properties of rerandomization is still an open question.

Remark 3.

Additionally, the condition for achieving the optimal precision under both types of rerandomization are actually equivalent when , where denotes the approximate acceptance probability for the first type and denote the number of tried complete randomizations for the second type. This is actually a direct consequence of the similarity discussed in Remarks 1 and 2.

4.3 Practical guidance

The discussion in Theorem 4.2 focuses mainly on how to achieve the optimal best-choice rerandomization in the asymptotic regime. It hints that the number of covariates should not be too large and increase at most logarithmically with the sample size, and the number of tried complete randomizations can increase polynomially with the sample size, with the exponent being sufficiently small. However, the design of best-choice rerandomization with finite sample size can still be challenging. In the supplementary material, we provide some useful guidance when designing a best-choice rerandomization in practice.

Statistical inference under the best-choice rerandomization

We now consider the statistical inference for the average treatment effect under the best-choice rerandomization. From the asymptotic approximation in Theorem 1 and (10), it suffices to estimate and . By their definition in (4) and (5), we essentially need to estimate the finite population variances of potential outcomes and their linear projections on covariates. We estimate these quantities by their sample analogues. Specifically, for , let be the sample variance of the observed outcomes for units receiving treatment arm , and be the corresponding sample covariance between observed outcomes and covariates. We further define as a sample analogue of , and as a sample analogue of . Let for . We can then estimate and by:

| (15) |

By the asymptotic approximation in Theorem 1 and (10), for any , we then propose the following confidence interval for the average treatment effect :

| (16) |

Importantly, the quantile can be efficiently estimated by the Monte Carlo method using the representation in Proposition 1.

As demonstrated in the theorem below, under certain regularity conditions, we can derive the probability limits of the estimators in (15) and prove the asymptotic validity of the confidence interval in (16). Let denote the finite population variance of the residuals from the linear projection of individual effects on covariates. We then invoke the following condition.

Condition 5.

As ,

| (17) |

Below we give several remarks regarding Theorem 6. First, by the same logic as Corollary 3, the confidence interval is always shorter than or equal to Neyman (1923)’s one for the CRE, while still being asymptotically conservative. This demonstrates the gain in inference from rerandomization.

Second, in addition to Conditions 1 and 2, the large-sample inference in Theorem 6 requires additionally Condition 5. From Wang and Li (2022, Corollary 2(iii)), this additional condition can be guaranteed by moderate conditions on the moments of the potential outcomes.

Third, Theorem 6(i) implies that the estimators in (15) are consistent for their population analogues. Intuitively, is consistent for , while itself is only conservative for , due to the individual treatment effect heterogeneity that cannot be linearly explained by the covariates. This is a feature of the finite population inference (Neyman 1923).

Fourth, Theorem 6(ii) shows the asymptotic validity of the confidence interval in (16). The confidence intervals are generally conservative, due to the conservativeness in estimating as discussed before. From Theorem 6(iii), when the effect heterogeneity is asymptotically negligible, the confidence intervals will become asymptotically exact.

Fifth, and are almost equivalent to the sample variances of the residuals from the linear regression of observed outcomes on covariates in treatment and control groups, respectively. Similar to Lei and Ding (2020) and Wang and Li (2022), we can consider rescaling the residuals as in usual regression analysis (MacKinnon 2013) to improve its finite sample performance. These strategies will be denoted as HC0, HC1, HC2 and HC3; see, e.g., Wang and Li (2022) for a detailed illustration. We will evaluate their performance in the simulation studies in Section 6.

If additionally Condition 3 holds and , then, from Theorem 4, the difference-in-means estimator under rerandomization will become asymptotically Gaussian distributed. In this case, it is also intuitive to use the usual Wald-type confidence interval. This is indeed true, as rigorously stated below. Let denote the th quantile of the standard Gaussian distribution.

Theorem 7.

In practice, we generally suggest using the confidence interval in (16), since it requires weaker regularity conditions. In addition, when Condition 3 holds and , the constrained Gaussian random variable is , and, intuitively, the confidence interval in (16) will be asymptotically equivalent to the Wald-type confidence interval .

Numerical illustration

6.1 The Student Achievement and Retention Project

To illustrate the performance of the best-choice rerandomization using various numbers of covariates and tried complete randomizations, we conduct a simulation using the Student Achievement and Retention Project project (Angrist et al. 2009) in a similar way as in Wang and Li (2022). This also facilitates the comparison between the best-choice rerandomization and the first type of rerandomization studied there. To avoid the paper being too lengthy, we relegate the simulation details and results to the supplementary material.

6.2 Mobile Banking in Bangladesh

We now illustrate the gain of the best-choice rerandomization using an actual rerandomized experiment recently conducted by Lee et al. (2021), which aims to study the effect of mobile technology on reducing inequality through the modern ways of money transfer. Specifically, the experiment involves rural household-urban migrant pairs at two connected sites: Gaibandha district in Northwest Bangladesh and Dhaka District at the capital of Bangladesh, where each pair can be viewed as an experimental unit. Lee et al. (2021) randomized the pairs into treatment and control following the rerandomization procedure as described in Bruhn and McKenzie (2009), and the treated pairs would receive training about how to sign up for and use the mobile banking service provided by bKash, which is the largest provider of such services in Bangladesh. The actual randomization is more complicated than simple treatment-control allocations and uses imbalance measure other than the Mahalanobis distance, and its exact implementation is not clearly described in the paper. Nevertheless, we can use the data from this experiment to illustrate the potential gain of rerandomization over the complete randomization.

We consider the best-choice rerandomization using the Mahalanobis distance in (2) with ; such a value is used in Bruhn and McKenzie (2009). Similar to Bai (2022), we include six pretreatment covariates for migrants: household size, age, gender, whether completed primary school, and total remittance in the past seven months and expenditure in the past month (in taka) from a baseline survey right before the intervention, where missing values are imputed in the same way as Bai (2022). We focus on two post-treatment outcomes: total remittance in the past seven months and expenditure in the past month from an endline survey one year after the intervention. To make the simulation realistic, we compute the average treatment effect estimate using difference-in-means, and pretend that the treatment effects are constant across units and equal to the average effect estimate. In this way, we are able to impute all the missing potential outcomes from the observed ones.

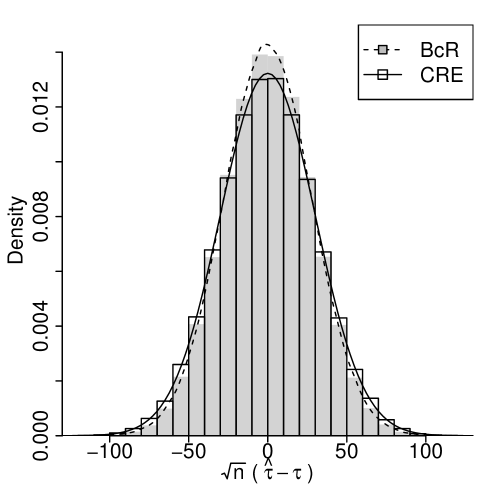

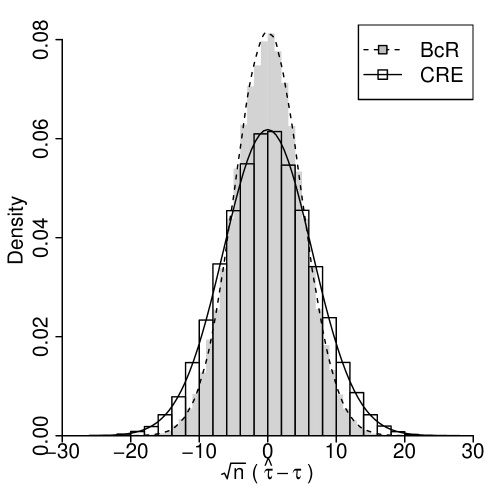

Figure 2 shows the histograms of the difference-in-means estimator under the best-choice rerandomization and the CRE, based on simulated assignments from both designs. Obviously, the treatment effect estimator under the best-choice rerandomization is more concentrated around the true average treatment effect, and the improvement for the expenditure outcome is notably larger. The reason is that the pre-treatment covariates have stronger association with the potential expenditures. Specifically, both the baseline expenditure and household size have considerable associations with the potential expenditures, and the corresponding defined in (5) for measuring the strength of association between covariates and potential outcomes is . However, for the remittance outcome, only the baseline remittance has a substantial predictive power for the potential remittances, and the corresponding is . Nevertheless, it is worth mentioning that rerandomization can improve the precision of treatment effect estimation for multiple outcomes at the same time. In other words, the same rerandomization can benefit multiple outcome analyses.

We then consider the performance of the proposed confidence confidence intervals. For the remittance analysis, averaging over simulated assignments, the coverage probabilities of our confidence interval for the best-choice rerandomization and Neyman (1923)’s one for the CRE are both about . Analogously, for the expenditure analysis, the coverage probabilities of ours and Neyman’s confidence intervals are, respectively, and . All of the coverage probabilities are close to the nominal level. This is coherent with our theory since the treatment effects are constant across all units in our simulation, under which these confidence intervals will be asymptotically exact. Moreover, our confidence intervals under the best-choice rerandomization is considerably shorter than Neyman’s one under the CRE, which demonstrates the gain in inference efficiency from rerandomization. In particular, the percentage reduction in average length of confidence intervals under the best-choice rerandomization, compared to that under the CRE, is for the the remittance analysis and for the expenditure analysis. These essentially lead to and increase in effective sample size, respectively.

Discussion

We studied the large-sample analysis for the best-choice rerandomization using the Mahalanobis distance and its optimality, allowing sample-size-dependent number of covariates and number of tried complete randomizations. We showed that (i) rerandomization can outperform usual complete randomization in terms of both estimation precision and length of confidence intervals, (ii) it should incorporate appropriate number of pretreatment covariates that are relevant for the potential outcomes, and (iii) the number of tried complete randomizations should be large but not overly large, increasing at most by a polynomial order of the sample size.

In this paper we focus mainly on the best-choice rerandomization based on the completely randomized experiments and using the Mahalanobis distance measure. Like the existing literature on the first type of rerandomization, it will be interesting to further extend it to other covariate imbalance measure (e.g., Branson and Shao 2021; Zhang et al. 2021; Zhao and Ding 2021; Liu et al. 2023) and other randomized experiments (e.g., Branson et al. 2016; Li et al. 2020; Johansson and Schultzberg 2022; Wang et al. 2021). We leave these for future study.

REFERENCES

- Angrist et al. [2009] J. Angrist, D. Lang, and P. Oreopoulos. Incentives and services for college achievement: Evidence from a randomized trial. American Economic Journal: Applied Economics, 1:136–163, 2009.

- Bai [2022] Y. Bai. Optimality of matched-pair designs in randomized controlled trials. American Economic Review, 112:3911–40, 2022.

- Banerjee et al. [2020] A. V. Banerjee, S. Chassang, S. Montero, and E. Snowberg. A theory of experimenters: Robustness, randomization, and balance. American Economic Review, 110:1206–30, 2020.

- Box et al. [2005] G. E. P. Box, J. S. Hunter, and W. G. Hunter. Statistics for experimenters: design, innovation, and discovery, volume 2. Wiley-Interscience New York, 2005.

- Branson and Shao [2021] Z. Branson and S. Shao. Ridge rerandomization: An experimental design strategy in the presence of covariate collinearity. Journal of Statistical Planning and Inference, 211:287–314, 2021.

- Branson et al. [2016] Z. Branson, T. Dasgupta, and D. B. Rubin. Improving covariate balance in 2K factorial designs via rerandomization with an application to a New York City Department of Education High School Study. The Annals of Applied Statistics, 10:1958 – 1976, 2016.

- Branson et al. [2022] Z. Branson, X. Li, and P. Ding. Power and sample size calculations for rerandomized experiments. arXiv preprint arXiv:2201.02486, 2022.

- Bruhn and McKenzie [2009] M. Bruhn and D. McKenzie. In pursuit of balance: Randomization in practice in development field experiments. American Economic Journal: Applied Economics, 1:200–232, 2009.

- Casella and Berger [2002] G. Casella and R. L. Berger. Statistical Inference. Pacific Grove: Duxbury, 2002.

- Caughey et al. [2023] D. Caughey, A. Dafoe, X. Li, and L. Miratrix. Randomization inference beyond the sharp null: Bounded null hypotheses and quantiles of individual treatment effects. Journal of the Royal Statistical Society, Series B (Statistical Methodology), in press, 2023.

- Cohen and Fogarty [2022] P. L. Cohen and C. B. Fogarty. Gaussian prepivoting for finite population causal inference. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 84:295–320, 2022.

- Cox [1982] D. R. Cox. Randomization and concomitant variables in the design of experiments. In P. R. Krishnaiah G. Kallianpur and J. K. Ghosh, editors, Statistics and Probability: Essays in Honor of C. R. Rao, pages 197–202. North-Holland, Amsterdam, 1982.

- Cox [2007] D. R. Cox. Applied statistics: A review. The Annals of Applied Statistics, 1:1 – 16, 2007.

- Dharmadhikari and Joag-Dev [1988] S. Dharmadhikari and K. Joag-Dev. Unimodality, Convexity, and Applications. San Diego, CA: Academic Press, Inc., 1988.

- Fisher [1925] R. A. Fisher. Statistical Methods for Research Workers. Edinburgh by Oliver and Boyd, 1st edition, 1925.

- Fisher [1926] R. A. Fisher. The arrangement of field experiments. Journal of the Ministry of Agriculture of Great Britain, 33:503–513, 1926.

- Fisher [1935] R. A. Fisher. The Design of Experiments, 1st Edition. Edinburgh, London: Oliver and Boyd, 1935.

- Freedman [2008] D. A. Freedman. On regression adjustments to experimental data. Advances in Applied Mathematics, 40:180–193, 2008.

- Hájek [1960] J. Hájek. Limiting distributions in simple random sampling from a finite population. Publications of the Mathematics Institute of the Hungarian Academy of Science, 5:361–74, 1960.

- Hall [2007] N. S. Hall. R. a. fisher and his advocacy of randomization. Journal of the History of Biology, 40:295–325, 2007.

- Huber [1964] P. J. Huber. Robust Estimation of a Location Parameter. The Annals of Mathematical Statistics, 35:73 – 101, 1964.

- Johansson and Schultzberg [2022] P. Johansson and M. Schultzberg. Rerandomization: A complement or substitute for stratification in randomized experiments? Journal of Statistical Planning and Inference, 218:43–58, 2022.

- Johansson et al. [2021] P. Johansson, D. B. Rubin, and M. Schultzberg. On optimal rerandomization designs. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 83:395–403, 2021.

- Lee et al. [2021] J. N. Lee, J. Morduch, S. Ravindran, A. Shonchoy, and H. Zaman. Poverty and migration in the digital age: Experimental evidence on mobile banking in bangladesh. American Economic Journal: Applied Economics, 13:38–71, 2021.

- Lei and Ding [2020] L. Lei and P. Ding. Regression adjustment in completely randomized experiments with a diverging number of covariates. Biometrika, 108:815–828, 2020.

- Li and Ding [2017] X. Li and P. Ding. General forms of finite population central limit theorems with applications to causal inference. Journal of the American Statistical Association, 112:1759–1769, 2017.

- Li and Ding [2020] X. Li and P. Ding. Rerandomization and regression adjustment. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82:241–268, 2020.

- Li et al. [2018] X. Li, P. Ding, and D. B. Rubin. Asymptotic theory of rerandomization in treatment–control experiments. Proceedings of the National Academy of Sciences, 115:9157–9162, 2018.

- Li et al. [2020] X. Li, P. Ding, and D. B. Rubin. Rerandomization in factorial experiments. The Annals of Statistics, 48:43 – 63, 2020.

- Lin [2013] W. Lin. Agnostic notes on regression adjustments to experimental data: Reexamining Freedman’s critique. The Annals of Applied Statistics, 7:295–318, 2013.

- Liu et al. [2023] Z. Liu, T. Han, D. B. Rubin, and K. Deng. Bayesian criterion for re-randomization. arXiv preprint arXiv:2303.07904, 2023.

- Lu et al. [2022] X. Lu, T. Liu, H. Liu, and P. Ding. Design-based theory for cluster rerandomization. arXiv preprint arXiv:2207.02540, 2022.

- MacKinnon [2013] J. G. MacKinnon. Thirty years of heteroskedasticity-robust inference. In Recent advances and future directions in causality, prediction, and specification analysis: Essays in honor of Halbert L. White Jr, pages 437–461. Springer, Berlin, 2013.

- Morgan and Rubin [2012] K. L. Morgan and D. B. Rubin. Rerandomization to improve covariate balance in experiments. The Annals of Statistics, 40:1263–1282, 2012.

- Nadarajah [2008] S. Nadarajah. Explicit expressions for moments of order statistics. Bulletin of the Institute of Mathematics Academia Sinica (New Series), 3:433–444, 2008.

- Neyman [1923] J. Neyman. On the application of probability theory to agricultural experiments. Essay on principles (with discussion). Section 9 (translated). reprinted ed. Statistical Science, 5:465–472, 1923.

- Raič [2015] M. Raič. Multivariate normal approximation: permutation statistics, local dependence and beyond. 2015.

- Rosenbaum [2010] P. R. Rosenbaum. Design of Observational Studies. New York: Springer, 2010.

- Rubin [1974] D. B. Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Psychology, 66:688–701, 1974.

- Rubin [1978] D. B. Rubin. Bayesian inference for causal effects: the role of randomization. The Annals of Statistics, 6:34–58, 1978.

- Savage [1962] L. J. Savage. The Foundations of Statistical Inference. Methuen and Co. Led., London, 1962.

- Shi and Ding [2022] L. Shi and P. Ding. Berry–esseen bounds for design-based causal inference with possibly diverging treatment levels and varying group sizes. arXiv preprint arXiv:2209.12345, 2022.

- Student [1938] Student. Comparison between balanced and random arrangements of field plots. Biometrika, 29:363–378, 1938.

- Wang et al. [2021] X. Wang, T. Wang, and H. Liu. Rerandomization in stratified randomized experiments. Journal of the American Statistical Association, (just-accepted):1–25, 2021.

- Wang and Li [2022] Y. Wang and X. Li. Rerandomization with diminishing covariate imbalance and diverging number of covariates. The Annals of Statistics, 50:3439 – 3465, 2022.

- Wintner [1936] A. Wintner. On a class of Fourier transforms. American Journal of Mathematics, 58:45–90, 1936.

- Yang et al. [2021] Z. Yang, T. Qu, and X. Li. Rejective sampling, rerandomization, and regression adjustment in survey experiments. Journal of the American Statistical Association, page in press, 2021.

- Zhang et al. [2021] H. Zhang, G. Yin, and D. B. Rubin. PCA Rerandomization. arXiv preprint arXiv:2102.12262, 2021.

- Zhao and Ding [2021] A. Zhao and P. Ding. No star is good news: A unified look at rerandomization based on -values from covariate balance tests. arXiv preprint arXiv:2112.10545, 2021.

Supplementary Material

Practical guidance for designing the best-choice rerandomization

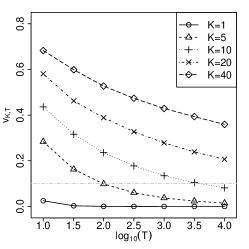

In this section, we present the details for Section 4.3 regarding the practical guidance for designing the best-choice rerandomization with a given finite set of experimental units. In general, the asymptotic gain from the best-choice rerandomization increases with , but the additional gain from increasing typically decreases with ; see, e.g., Figure A1 below. Thus, we suggest using large but not overly large , say, . In addition, we should choose moderate number of covariates , trying to make their association with potential outcomes, measured by , large. We should avoid excessively large value of that provides little increment on but substantially increase the variance of the constrained Gaussian random variable, which will ultimately diminish the gain from rerandomization, as implied by Corollary 2. Below we provide some useful practical guidance when designing a best-choice rerandomization.

First, we can check the efficiency improvement from a specific choice of for the best-choice rerandomization. From Corollary 2 and Theorem 4, the difference between a best-choice rerandomization with a particular choice of and the optimal one is . Thus, the variance of the constrained Gaussian random variable, , actually gives an upper bound on the gap between a particular rerandomization design and the optimal one. In practice, we can choose such that this gap is reasonably small, say, below or . Figure A1 shows the value of when ranges from to and ranges from to . Obviously, the value of increases with and decreases with . Below we investigate the choice of such that is bounded by . When , is about when ; when , is about when ; when , is about when is about ; when , we need to be greater than in order to make bounded by . These indicate that in practice we should not include too many covariates into rerandomization, since they would require much larger in order to make the best-choice rerandomization close to the optimal one; intuitively, this will also lead to higher computation cost and less accurate asymptotic approximation.

Second, we can evaluate the trade-off between the potential gain and the worst-case loss from the best-choice rerandomization, as suggested in Wang and Li [2022]. As demonstrated before, the best-choice rerandomization can asymptotically improve the precision of the difference-in-means estimator compared to the CRE. With finite sample size, the CRE is actually the minimax optimal in terms of the mean squared error of the difference-in-means estimator, when we considering the worst-case scenario over all possible configurations of the potential outcomes [see, e.g., Wang and Li, 2022, Proposition A1]. Note that this does not contradict with our asymptotic theory, since, in the worst case with , the asymptotic distribution of the difference-in-means estimator under the best-choice rerandomization is the same as that under the CRE. These two observations then provide a quantitative way to characterize the trade-off when designing rerandomization. Intuitively, we can use Corollary 2 to characterize the potential gain, and the worst-case mean squared error, which can be estimated by the Monte Carlo method, to characterize the worst-case loss. We can then consider these trade-offs when comparing multiple rerandomization designs. We will discuss this in more detail in Section A2.

Simulation using the student achievement and retention project

In this section, we provide the details for Section 6.1. The Student Achievement and Retention (STAR) project aims to evaluate the effect of academic services and incentives for college students. We focus on the comparison between two treatment arms, where the treated students would receive an array of support services and cash awards for meeting a target GPA and the control students received only standard support services.

We preprocess the data in the same way as Wang and Li [2022]. We remove units with missing covariates, resulting in treated units and control units, and generate pretreatment covariates for these units. Specifically, the first covariates are from the STAR project, including high-school GPA, age, gender and indicators for whether lives at home and whether rarely puts off studying for tests, and the remaining covariates are generated independently from the distribution with degrees of freedom . We use the first year GPA from the STAR project as the outcome and let both treatment and control potential outcomes be the same as the observed ones, so that we are able to evaluate the repeated-sampling properties of various designs. Once generated, the potential outcomes and covariates will be kept fixed during the simulation, mimicking the finite population inference. Table A1 shows the empirical bias, root mean squared error and coverage probabilities based on draws from the best-choice rerandomization using the first covariates and number of tried complete randomizations, for various choices of . Surprisingly, we find that the best-choice rerandomization performs relatively well even when and are large, although the confidence intervals become slightly under-covered when is large. These show the robustness of the best-choice rerandomization design in the presence of high-dimensional covariates and large number of tried complete randomizations. Note that these do not contradict with the intuition from our theory, which implies the potential danger of large and . As shown below, for some potential outcome configurations, the performance of rerandomization can deteriorate significantly as and increase.

| Bias | RMSE | HC0 | HC1 | HC2 | HC3 | Bias | RMSE | HC0 | HC1 | HC2 | HC3 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

We now consider another way of generating potential outcomes. We first use Monte Carlo method to estimate the propensity scores of each unit averaging over the best-choice rerandomization designs under investigation, and then take a Gaussian quantile transformation to generate both potential outcomes, where the treatment and control potential outcomes for each unit are the same. With this potential outcome configuration, Table A1 shows analogously the empirical bias, root mean squared error and coverage probabilities under the best-choice rerandomization designs with various choices of . Obviously, as and increases, both the bias and mean squared error tend to be larger, and the coverage probabilities become much smaller than the nominal level. Thus, the performance of the best-choice rerandomization can be sensitive to the potential outcome configuration when and are large. Below we present two practical ways to tackle this issue.

First, we can check the worst-case behavior of the best-choice rerandomization using the formula derived in Wang and Li [2022, Proposition A1]. As shown in Table A2, both the worst-case bias and root mean squared error increase notably as and increases. It is worth mentioning that there is considerable Monte Carlo error even when we use simulated assignments to estimate the worst-case root mean squared error; for example, the estimated worst-case bias and root mean squared error for the CRE is about and , whose true values are known to be and . We can increase the number of simulated assignments to make the Monte Carlo estimation more accurate, but the trend in Table A2 already illustrates the potential drawback of large and . As discussed in Section A1, in practice, we can also combine this with the potential gain that rerandomization can bring as shown in Corollary 2 to guide our design of rerandomization. For example, similar to Wang and Li [2022], we can use the geometric mean of the worst-case mean squared error and the ideal-case mean squared error implied by the asymptotic theory as a measure for comparing different best-choice rerandomization designs. Note that the asymptotic mean squared error (or equivalently the asymptotic variance since is asymptotically unbiased under rerandomization) depends on the association between potential outcomes and covariates, measured by in (5), which needs to be determined by domain knowledge or prior studies.

| Original covariates | Trimmed covariates | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Second, we can perform trimming to effectively improve the worst-case performance of the best-choice rerandomization, a strategy that has also been used by Lei and Ding [2020] and Wang and Li [2022]. Note that under our randomization-based inference without any model assumptions, we have the flexibility to conduct arbitrary pre-processing of the covariates. The intuition of trimming is similar to that discussed in Morgan and Rubin [2012] with small sample size. When a unit has extreme covariates, it is more likely to be allocated to the group of larger size under rerandomization, which can help balance the covariates between the two groups. The extremeness of covariates also appears on the Berry-Esseen bound in (7), which depends crucially on the leverages scores of the covariate matrix [Wang and Li, 2022]. Trimming can help us mitigate the extreme covariates, thereby improving the robustness of the best-choice rerandomization. For example, we trim each covariate at its and quantiles, and analogously calculate the worst-case performance as shown in Table A2. Obviously, the performance of the best-choice rerandomization enhances after trimming. Indeed, the propensity scores of units under these rerandomization designs with the original covariates range from to , while that with trimmed covariates range from to , which are much more stable and concentrate around .

Remark A4.

We finally comment on the comparison between the best-choice rerandomization and rerandomization based on a prespecified imbalance threshold. Comparing Table A2 and Table A1 in Wang and Li [2022], given the same number of covariates, the worst-case mean squared errors under the best-choice rerandomization trying complete randomizations are comparable to the first-type rerandomization with acceptance probability . This echos the intuitive and theoretical comparisons in Remarks 1–3. However, the best-choice rerandomization can be more stable in practice, because it can always produce “acceptable” randomizations. Besides, its implementation is intuitive, convenient, and has already been used frequently in practice.

Proof for the asymptotic distribution of the difference-in-means estimator under the best-choice rerandomization

To prove Theorem 1, we need the following three lemmas.

Lemma A1.

Proof of Lemma A1.

Lemma A1 follows directly from the definition of and the fact that the sets and are convex for any . ∎

Lemma A2.

Under the same setting as Lemma A1, let be any random vectors that are independent of and ; Define

Then for any ,

Proof of Lemma A2.

By the law of iterated expectation,

| (A1) |

where

is an event that becomes deterministic once conditioning on and . By the union bound,

Note that both and are independent of . From Lemma A1, we then have

where the second last equality holds because is a continuous random variable and consequently the measure of the intersection of the two events there is zero, and the last equality holds by the same logic as (A3). Therefore, Lemma A2 holds. ∎

Lemma A3.

Under the same setting as Lemma A2, for any ,

Proof of Lemma A3.

By the law of iterated expectation,

| (A2) |

where

is an event that becomes deterministic once conditioning on and , and the last equality holds because the two events there are disjoint. Note that both and are independent of . From Lemma A1, we then have

where the last equality holds by the same logic as (A3). ∎

Proof of Theorem 1.

Recall the definition of ’s, ’s and in Section 3. Define further as the difference-in-means estimator under the treatment assignment , for . By the construction of the best-choice rerandomization, for any ,

| (A3) |

where the inequality in (A3) comes mainly from the fact that there may be multiple treatment assignments achieving the minimum covariate imbalance. Recall also the definition of ’s and ’s in Section 3.2. Furthermore, without loss of generality, we assume that ’s and ’s are independent of ’s and ’s. Obviously, for all , follows the chi-squared distribution with degrees of freedom .

First, we consider the upper bound of . For , define

Obviously, and differ only in the th element, for . This allows us to apply Lemma A2 to get that, for any ,

where in the above inequality we take and as and ; and take and as and . Armed with the above inequality, we have

Second, we consider the lower bound of . By the same logic as the proof of the upper bound and applying Lemma A3, we have

Third, we prove that, for any ,

| (A4) |

By the same logic as (A3), the left-hand side of (A4) is bounded from above by , which is further bounded from above by the right-hand side of (A4). Furthermore, the right-hand side of (A4) is also bounded from above by the left-hand side:

where the last equality holds because ’s are mutually independent continuous random variables. These facts then imply that (A4) must hold.

To prove Theorem 2, we need the following lemma.

Lemma A4.

Let be mutually independent -dimensional standard Gaussian random vectors. Then, for any constant unit vector ,

where is the first coordinate of .

Proof of Lemma A4.

For any given unit vector , we can always construct an orthogonal matrix whose first row is . Then will be the first coordinate of , and for all . By the property of standard Gaussian distributions, follows the same distribution as . This then implies Lemma A4. ∎

Proof of Theorem 2.