Golden parachutes under the threat of accidents

Abstract

This paper addresses a continuous-time contracting model that extends the problem introduced by Sannikov [47] and later rigorously analysed by Possamaï and Touzi [44]. In our model, a principal hires a risk-averse agent to carry out a project. Specifically, the agent can perform two different tasks, namely to increase the instantaneous growth rate of the project’s value, and to reduce the likelihood of accidents occurring. In order to compensate for these costly actions, the principal offers a continuous stream of payments throughout the entire duration of a contract, which concludes at a random time, potentially resulting in a lump-sum payment. We examine the consequences stemming from the introduction of accidents, modelled by a compound Poisson process that negatively impact the project’s value. Furthermore, we investigate whether certain economic scenarii are still characterised by a golden parachute as in Sannikov’s model. A golden parachute refers to a situation where the agent stops working and subsequently receives a compensation, which may be either a lump-sum payment leading to termination of the contract or a continuous stream of payments, thereby corresponding to a pension.

Key words: principal–agent problem, random horizon, integro-differential Hamilton–Jacobi–Bellman equation

1 Introduction

Risk naturally emerges in various interactions across all sectors of the economy and is well-known to be closely linked to the concept of uncertainty. It involves the potential occurrence of unexpected shocks that could lead to harm or loss, thus exerting a significant—and usually negative—influence on the considered economic scenario. Here, one is naturally led to consider situations such as accidents during the production process in a company, injuries in an health insurance context, or even the devaluation of financial assets in specific corporations, due to the bankruptcy of a subsidiary. Although various other instances could be mentioned, they all have in common the potential for certain adverse events that can be categorised as accidents. It is therefore natural to study risk prevention in contract theory, specifically within principal–agent problems.

The principal–agent paradigm addresses the optimal contracting problem in the presence of information asymmetry between two economic actors: a principal (‘she’) and an agent (‘he’). In the typical scenario, the principal designs a contract to hire the agent, who can accept or reject it based on whether it provides sufficiently adequate incentives to ensure that his reservation utility is attained. The primary challenge is that the principal designs this contract to optimise her utility while having imperfect information about the efforts provided by the agent. This problem originated in the 1970s within a discrete-time framework and was subsequently reformulated in a continuous-time model by Holmström and Milgrom [26]. This seminal work initiated the study of moral hazard problems in continuous-time, providing important insights into formulating an optimal contract between a principal and an agent whose effort influences the drift of the output process. Following this, numerous results have been established to explore more general models and derive tractable solutions, thereby expanding the scope of this initial work. A comprehensive analysis of the related literature can be found in the survey paper of Sung [55] or in the book of Cvitanić and Zhang [18].

It has nowadays been universally acknowledged that Sannikov [47] achieved a substantial breakthrough in the field. In this work, the author studied an infinite horizon principal–agent model, in which the principal provides continuous payments to the agent, who exclusively controls the drift of the output process until a random retirement time. The significance of this work lies in its pioneering approach, which enables the transformation of the original bi-level optimisation problem between the principal and the agent into a standard stochastic control problem, whose solution can be described through an Hamilton–Jacobi–Bellman equation. This approach led to numerous follow-up works that rigorously formalised Sannikov’s ideas. Particularly noteworthy are the PhD thesis of Choi [13] and, more recently, the contribution of Possamaï and Touzi [44], which extended the principal–agent model introduced by Sannikov by considering potentially different discount rates for both parties. Their primary focus was on technical rigour, ultimately providing a complete characterisation of the solution to the contracting problem. Another significant extension was introduced by Cvitanić, Possamaï, and Touzi [19], presenting a comprehensive mathematical approach to solve principal–agent problems that allow control over both the drift and diffusion of the output process. While this analysis focused on a finite deterministic horizon setting, Lin, Ren, Touzi, and Yang [33] subsequently addressed principal–agent problems over random horizons.

It is nonetheless important to point out that the Brownian framework considered in all the previously mentioned works fails to capture sudden and unpredictable events, and consequently it becomes necessary to consider principal–agent problems involving a jump component in the output process. There exists a vast literature that adopts jump processes to replicate negative shocks, with an early influential contribution from Sung [54]. This work extended Holmström and Milgrom’s model, addressing a corporate insurance problem driven by a multi-dimensional point process, where each component represents a specific type of accident, less likely to occur when the agent exerts effort. More recently, Zhang [56] explored efficient allocations in a Mirrleesean economy influenced by persistent shocks that transition according to a continuous-time Markov chain that is beyond the control of the agent. Similarly, Sannikov and Skrzypacz [48] investigated the dynamic interaction among economic actors in a scenario where the information process is characterised by a discontinuous uncontrolled Poisson component associated to bad news. In contrast, Biais, Mariotti, Rochet, and Villeneuve [9, 10] simulated accidents and large and unfrequent losses, respectively, using a Poisson process whose intensity can be influenced by the agent’s actions. Additionally, Pagès and Possamaï [40], later extended by Hernández Santibáñez, Possamaï, and Zhou [24] to include adverse selection, explored the optimal securitisation of a pool of long-term loans exposed to Poisson default risk, where the default intensity can be reduced through the monitoring activity of a bank. Furthermore, Martin and Villeneuve [36] modelled a large insurable risk capable of halting production entirely using a single jump process. However, it is worth noting that in existing literature, a jump process is not exclusively associated with negative events. El Euch, Mastrolia, Rosenbaum, and Touzi [21] linked a Poisson process with market orders to investigate a contract offered by an exchange to a market-maker, aiming to reduce the bid–ask spread for a single risky asset. Subsequently, this model was extended to consider multiple market participants by Baldacci, Possamaï, and Rosenbaum [4] and to enable trading on dark liquidity pools by Baldacci, Manziuk, Mastrolia, and Rosenbaum [5].

All the previously mentioned works adopt jump processes with a constant jump size to simulate sudden shocks. To the best of our knowledge, the first study to consider accidents of different random sizes is by Capponi and Frei [12]. The authors examined a principal–agent model where the agent can exert both effort and accident prevention, aiming to decrease the likelihood of negative events that are described by an exogenous loss distribution. Later on, Bensalem, Hernández Santibáñez, and Kazi-Tani [8] employed a similar jump–diffusion framework in their investigation of an insurance demand model, enabling the protection buyer to exert prevention effort to reduce his risk exposure. An extension of all the aforementioned principal–agent models can be found in the work of Hernández Santibáñez [23]. Here, the author studied a general contracting problem between the principal and a finite number of agents, where each agent has control over the drift of the output process and the compensator of its associated jump measure. Additionally, Mastrolia and Zhang [37] formulated an energy-optimal demand–response model where the principal hires an infinite number of agents, incorporating accidents by introducing a Lévy process.

Principal–agent models with jumps that go beyond simple Poisson process lead to Hamilton–Jacobi–Bellman equations with an additional integral term. Consequently, the notion of viscosity solution introduced by Crandall and Lions [16] and Lions [35] requires particular attention as the equations become non-local. The first works in this direction are to be attributed to Soner [52, 53] for bounded measures and Sayah [49, 50] for unbounded measures. Subsequently, Alvarez and Tourin [2] proved a general existence and uniqueness result for viscosity solutions to integro-differential equations characterised by a bounded integral operator, while Pham [42] achieved a similar result for a special case involving singular measures. In recent years, there has been a surge of interest in extending the theory of viscosity solutions to integro-differential equations. This growth in the literature is largely due to the dependence of the results on the integrability of the singular measure characterising the integral operator. Among these advancements, Jakobsen and Karlsen [28] presented a first version of a non-local maximum principle, which allowed the deduction of a comparison principle for viscosity sub-quadratic solutions. Subsequently, Barles and Imbert [7] and later the PhD thesis of Hollender [25] generalised their uniqueness result by considering solutions with arbitrary growth at infinity.

In this paper, we examine the model introduced by Sannikov [47] in the presence of accidents, thereby making the model suitable for investigating contracting problems between a principal and an agent in an economic environment that might experience unpredictable and negative shocks of unknown size. Specifically, we explore optimal contracts offered by a risk-neutral principal to a risk-averse agent aimed at executing a project. To maximise the project’s value, which is described by an underlying jump–diffusion process, the agent can employ two distinct actions simultaneously, influencing both the drift of the process and the likelihood of accidents occurring. We model the impact of accidents using a compound Poisson process, in line with the approach outlined by Capponi and Frei. However, a slight issue arises in the derivation of optimal contracts in the mentioned work, particularly in the application of the martingale representation property in [12, Lemma 3.1]. This issue inevitably imposes a restriction on the set of the admissible contracts. Consequently, our contribution can be seen as an extension to this model, not only due to this concern but also because we assume that the principal offers compensation to the agent not solely at the random termination time but consistently throughout the entire duration of the contract.

The main objective of this paper is to verify whether the rigorous study by Possamaï and Touzi [44] regarding Sannikov’s contracting problem remains valid within our framework that incorporates accidents. More specifically, we aim to test the robustness of the economic conclusions drawn by these authors by studying the economic implications resulting from these unpredictable events that negatively impact the principal–agent interaction. Our focus is particularly on examining the concept of a ‘golden parachute’ in the context of accident risk. This term refers to a situation where the agent ceases to work at a random time—or refrains from working completely—and subsequently receives a positive compensation. This compensation may take the form of a lump-sum payment, leading to termination of the contract, or a continuous stream of payments, indicating retirement. Therefore, our investigation aims to determine whether economic conditions exist that could lead to the existence of these two distinct instances of golden parachutes, similarly to what was observed in the problem without accidents. To conduct this analysis, we need to consider different regimes based on the impatience levels of both parties:

-

when the principal is significantly more impatient than the agent, a golden parachute does not exist. This scenario depends only on the impatience of both economic actors and the agent’s level of risk aversion, completely mirroring the case without accident risk. Indeed, the problem degenerates because the principal can achieve her maximum reward regardless of the agent’s participation level. However, optimal contracts do not exist;

-

when the principal is more impatient than the agent but still above the threshold mentioned above, a golden parachute can correspond to either of the previously described situations. Unlike the analysis not involving accidents, if the agent stops working, this means that he is either fired or retired. This difference is due to the impact of accidents on the economic scenario, leading the principal to prefer terminating the contract over retiring the agent for a sufficiently small continuation utility of the agent. This decision is influenced by the expenses associated with potential future losses outweighing the immediate cost of compensating the agent. This is in stark contrast with the analysis excluding accidents, where termination is never considered the optimal choice;

-

when the principal is as impatient as the agent, the analysis closely aligns with that conducted without considering accidents. In other words, we know that a golden parachute is likely to exist, and it corresponds to a lump-sum compensation;

-

when the agent is strictly more impatient than the principal, a golden parachute can be associated with both distinct compensation schemes, which further depends on the average loss per accident. When the size of potential accidents is not significant, contract termination is never an optimal choice, analogously to the model without accidents. However, when the impact of an accident grows significantly, resulting in higher associated costs, the principal prefers either firing the agent or retiring him, based on the continuation utility of the agent. Hence, we observe that the nature of a golden parachute is deeply linked to the average accident size. In case of large accidents, it translates to either a lump-sum payment or a continuous stream of payments. Conversely, as the accident size decreases, it corresponds to the retirement scenario, mirroring the situation in the absence of accidents.

We emphasise that the economic features of the model are closely related to the specific regime under consideration and thus rely on the impatience levels of both parties, exactly as in the problem without accidents. However, despite the unchanged structure of the problem, the introduction of unpredictable and adverse events allows for the possibility of both golden parachute scenarii. In other words, when the agent is not as impatient as the principal, a golden parachute can be associated with both retirement and termination, while retirement is always the preferred choice in the absence of accidents. This different characterisation stems from the different nature of an appropriate face-lifted version of the agent’s inverse utility function, which is defined through an obstacle problem. While in the accident-free framework, this problem simplifies to the study of an ordinary differential equation, in our model, the analysis of this face-lifted utility function is significantly more involved due to its significant correlation with the average accident size. We also mention that even with relatively small potential accidents, the impact on the principal is significant, and can result in a 50% reduction of the value of the principal for an accident size which represents only 2.5% of the average value of the project.

Another important difference with the reference model without accidents is obvious in the study of the first-best problem, which is no longer directly solvable, except in the scenario where the principal and the agent are equally impatient. Despite the difficulty in fully characterising the first-best solution for every regime, we can still replicate similar economic considerations. However, the most challenging aspect of investigating the model incorporating accidents lies in describing the second-best problem in order to address the economic question of whether a golden parachute is optimal. Unfortunately, we cannot provide a definitive answer to this question due to the complexity arising from the integral term appearing in the Hamilton–Jacobi–Bellman equation associated with the contracting problem. We will discuss this in more detail in Section 5.2. Nonetheless, we are able to characterise the solution to the problem as the unique viscosity solution of the aforementioned equation through a generalisation of Tietze’s extension theorem that allows to overcome the obstacles posed by the limited liability constraint.

The rest of the paper is structured as follows. In Section 2, we formulate the principal–agent model and provide a comprehensive explanation of the criteria of the agent and the principal. We then discuss the two notions of a golden parachute along with the definition of the face-lifted utility function that combines these concepts. In Section 3, we completely characterise the face-lifted utility in all the various cases , , and outlined above. In Section 4, we study the first-best contracting problem, which offers insights into the subsequent analysis of the second-best contracting problem in Section 5. We defer technical proofs to the appendices.

Notation. Let be the set of positive integers, and the set of non-negative real-numbers. For any , we write and . Consider a probability space carrying a filtration . We use the convention and . For , we write for the conditional expectation of a random variable with respect to . For any –stopping time , we denote by the set of –stopping times such that , –a.s., and by (resp. ) the stochastic interval . The notation (resp. ) refers to the predictable (resp. optional) -algebra on . For a random measure on , we denote by (resp. ) its -compensator (resp. -compensated random measure). We introduce the spaces

where is an –Brownian motion. For an –local martingale in the sense of Jacod and Shiryaev [27, Definition I.1.45], we denote its stochastic exponential by , that is,

where is the quadratic variation of the continuous martingale part of and denotes the jump process of (as in [27, Theorem I.4.61]).

2 Model and assumptions

We investigate a continuous-time contracting problem in which a risk-neutral principal hires a risk-averse agent to manage a project over a possibly infinite time horizon. During this period, the agent can exert effort to increase the instantaneous growth rate of the project’s value, that is, the principal’s profit, while simultaneously reducing the likelihood of accidents that negatively impact the total profit. It is important to emphasise that in the model considered here, the agent is unable to reduce the impact of accidents on the project’s value as he has no control over their size, which is an exogenous factor.

2.1 The setting

Let be a probability space carrying the following jointly –independent objects: a one-dimensional Brownian motion , a Poisson process with -intensity (see [27, Definition I.3.26]), and a collection of bounded and positive –i.i.d. random variables . Let , and let denote a given initial investment. The dynamics of the project’s value, referred to as the output process hereafter, under no exertion of effort by the agent is given by

where denotes the compound Poisson process

Here, represents a source of randomness, and models the losses that can occur throughout the lifetime of the project at random times. The Poisson process represents the total number of accidents, while the respective cumulative losses since, for , each random variable quantifies the size of the -th accident. The average loss per accident is denoted by

| (2.1) |

where is the common distribution function associated to all the , . Note that is positive since is assumed to be positive. Finally, we let be the -augmentation of the filtration generated by the Brownian motion and the compound Poisson process . Note that satisfies the usual conditions under by Protter [45, Theorem I.31].

In this setting, a natural question to ask is whether the predictable martingale representation property with respect to and holds. This can indeed be achieved by introducing the associated jump measure of as follows. Let

where denotes the Dirac measure, the -compensator (see [27, Theorem II.1.8] for the definition) is then given by

To ease the notation, we write for the compensated random measure . Furthermore, for any and , we denote by

| (2.2) |

the stochastic integral of with respect to and the compensated stochastic integral of with respect to the random measure , respectively, in the sense of [27, Chapter 1 & 2]. Having collected the necessary ingredients, we can now state the following martingale representation theorem, which is derived from Cohen and Elliott [14, Theorem 14.5.7] combined with [27, Observation I.4.1].

Lemma 2.1.

Let be an –local martingale. Then, there exist unique and such that

Moreover, this property is preserved under an equivalent change of measure, see for instance [27, Theorem III.5.24].

2.2 Actions and contracts

We assume that through specific costly efforts, the agent can influence the distribution of the output process , that is, he can affect the probability measure under which the problem is described in its weak formulation. For this, we introduce a compact subset of containing and bounded by , for some , representing the possible effort values that the agent can exert on the drift of the output process. Additionally, we define another compact subset of bounded by . This set denotes all possible accident frequencies, which is why it needs to satisfy the technical condition of being bounded away from zero. Specifically, there exists some such that and for any . Note that the fact that is positive implies that accidents are less likely to happen if the agent exerts effort, but he cannot eliminate them completely. We denote for simplicity .

The collection of admissible controls for the agent consists of all -predictable processes with values in such that the following stochastic exponential

is a –uniformly integrable -martingale. It is well-known that this implies the existence of an -measurable random variable such that is still a –uniformly integrable -martingale.

For any , we define as the probability measure on whose density with respect to is given by

| (2.3) |

While the agent can control the growth rate of the output process and reduce the intensity at which accidents occur through costly effort, the objective of the principal is to design a contract that incentives the agent to increase the overall value of the project. The execution of the contract starts at time 0 and terminates at the random time . Throughout that period, the agent receives a remuneration for his work in the form of a continuous stream of payments and a lump-sum payment at termination. We assume that is an –stopping time, is an -predictable non-negative process, and is a non-negative -measurable random variable. We denote by the collection of contracts .

Remark 2.2.

-

To be precise, we only need the process to be a –uniformly integrable -martingale, where represents the termination of the contract between the principal and the agent. However, it is straightforward to notice that we are not asking for more by requiring that is a –uniformly integrable -martingale since we can simply redefine the process as for all if is finite.

-

By [14, Theorem 15.2.6], for any , the process is an –Brownian motion, and the compound Poisson process and the Poisson process have -intensity given by and , respectively. Moreover, the measure has -compensator . Notice that we highlight the dependence on the probability measure with the superscript . Accordingly, for any , the output process can be expressed as

2.3 The problem of the agent

The preferences of the agent are determined by a utility function , which is supposed to be increasing, strictly concave and twice continuously differentiable. Moreover, we assume and the condition . The function satisfies the following growth condition:

| (2.4) |

Now, we introduce the opposite of its inverse that we will be using throughout the paper. Precisely,

| (2.5) |

The required conditions on the agent’s utility function immediately imply that is twice continuously differentiable, strictly concave, and that . Furthermore,

| (2.6) |

Given a contract offered by the principal, the agent’s optimisation problem is

| (2.7) |

In order to simplify notations in the subsequent discussion, it is convenient to rewrite the criterion of the agent as follows

Here, we have denoted and , respectively. Henceforth, we indifferently identify as a contract the triplet or the triplet due to the one-to-one correspondence between them.

The agent chooses the effort that maximises his utility from remuneration subject to the corresponding cost . Here, we abuse notation and indifferently identify the one-argument function with the two-arguments function . We assume the cost function to be twice continuously differentiable, strictly convex, and satisfying . This latter assumption captures the fact that there is no cost for exerting no effort. Moreover, we suppose that is increasing for any , and that is decreasing when . This description of the cost function mathematically reflects the idea that exerting effort to increase the instantaneous growth rate of the value of the project and to decrease the likelihood of negative events causes discomfort to the agent as his utility is reduced. Finally, in order to consider the time-value of money, the agent exponentially discounts future income at the constant discount rate .

A control is considered an optimal response to the contract if . We denote by the set of all optimal responses of the agent to the contract . In addition, as usual in contract theory, we suppose that the agent has a reservation utility , for some , meaning that he is only willing to accept the contract if his participation constraint is satisfied, that is, . Consequently, the agent only accepts contracts in

where the set denotes the collection of admissible contracts that will be introduced at the end of Section 2.5, as we need to impose some additional integrability requirements first.

2.4 The problem of the principal

Anticipating the optimal response of the agent, a risk-neutral principal seeks to design the contract which best serves her objective under his participation constraint. Specifically, her problem is

| (2.8) |

where

| (2.9) |

as a consequence of Doob’s optional sampling theorem. With the notation introduced in the previous section and using the utility function given in (2.5), we can rewrite the criterion of the principal to

It is worth noting that the future rewards of the principal are discounted with a constant discount rate , which may differ from the one of the agent. Additionally, we adopt the convention that implies that the principal has an interest in only offering contracts which induce an optimal response from the agent, that is, contracts for which the set is not empty.

2.5 Golden parachute and reformulation

A golden parachute is a situation where the agent ceases to exert any effort but receives a compensation from the principal. Within the framework presented here, there are two ways in which a golden parachute can occur

-

•

retirement: the agent is retired by the principal at some non-negative random time, and continues to receive a stream of positive payments;

-

•

termination: the contract is terminated at some non-negative random time, and the agent receives a lump-sum compensation.

As pointed out in [44], we will prove that although the agent is unconcerned by the two scenarii, the discrepancy between the two discount rates and can lead to a situation where the principal can improve her reward by retiring the agent rather than firing him, and thus terminating the contract. More precisely, for any given state , the agent is indifferent between receiving at some non-negative random time or a continuous stream of payments over the interval for some , with subsequent termination of the contract postponed to time with a lump-sum compensation verifying the following condition

On the contrary, the principal may prefer retiring the agent in this case since her criterion compared to the termination scenario can be improved by the quantity informally expressed as

Therefore, it is evident that the problem of the principal exhibits the so-called face-lifting phenomenon, as her reward can be improved by the introduction of the face-lifted utility , which is defined by the following deterministic mixed control–stopping problem

| (2.10) |

where the function is introduced in (2.5), denotes the set of Borel-measurable maps from to , and for all , the state process is defined by the controlled first-order ODE

| (2.11) |

which is given explicitly by

It is important to emphasise that we need to restrict our attention to the subset . This results from the fact that the agent cannot receive negative payments as he is protected by limited liability, and represents the utility he gets from the lump-sum payment for every time .

After having introduced the face-lifted utility , it would be natural to define what is known as the relaxed criterion of the principal in [44]. However, before proceeding with this, we first need to define the set of admissible contracts. We denote by the collection of contracts satisfying the integrability condition

| (2.12) |

for some and .

Remark 2.3.

-

Note that the value function of the agent is finite for any , that is, for any contract that verifies the integrability condition (2.12). Additionally, the value function of the principal is locally bounded; it is trivially bounded from above by and locally bounded from below since there exists at least a contract such that the set is not empty.

-

The requirement in the integrability condition (2.12) is necessary in order to apply Kruse and Popier [29, Proposition 2] in the reduction argument in Appendix C. Specifically, this condition is crucial for the application of the Burkholder–Davis–Gundy inequality for non-continuous local martingales.

Analogously to [44], we can introduce the collection of admissible contracts where

for some , -measurable with values in , and . Since it can be easily shown that the two sets and coincide, we have the following equivalent formulations of the problem of the principal

where the relaxed reward of the principal is given by

| (2.13) |

Consequently, the introduction of the face-lifted utility and its corresponding relaxed reward for the principal plays a crucial role as it combines both notions of a golden parachute in the termination scenario.

Definition 2.4.

The relaxed contracting problem exhibits a golden parachute if on the event set , for any optimal contract .

It is worth noticing that in the definition of a golden parachute, the optimal termination of the contract can be null, indicating that the agent receives some remuneration without starting to work. This scenario is a consequence of the formulation of the problem, as the principal cannot choose not to hire the agent, and thus may simply decide to hire him and terminate the contract simultaneously.

3 On the face-lifted utility

We first start by investigating the problem to provide an explicit characterisation of the face-lifted utility . The associated Hamilton–Jacobi equation is given by

| (3.1) |

where , and denotes the concave conjugate of defined as

It is straightforward to verify that is null on , and it is negative on . Furthermore, the growth condition (2.4) imposed on the utility function of the agent results in

| (3.2) |

The subsequent sections are dedicated to the analysis of the aforementioned Hamilton–Jacobi equation to compute the face-lifted utility in closed-form. We prove that when the agent and the principal are equally impatient, namely when , the principal never benefits from delaying the termination of the contract and allowing the agent to exert no effort for a while. Only this particular scenario corresponds exactly to the analogous one without accidents studied in [44]. Indeed, when the two discount factors differ, the possibility of accidents may lead the principal to consider termination as a more favourable option. However, this decision is never optimal when , unless the continuation utility reaches the value .

If the agent is more impatient than the principal, and thus , we need to divide the analysis into two cases based on the size of possible accidents. When the average size per accident is small, precisely , we show that nothing differs from the results in [44] because the face-lifted function is always strictly above , meaning that the retirement scenario is always preferred by the principal. This decision originates from the principal’s relatively limited concern for accidents, given that the potential losses she might face are not significant.

However, when the size of the accidents becomes larger, specifically when is above the aforementioned threshold, the decision to retire the agent is no longer optimal in general because the two functions and coincide for small values of the continuation utility of the agent. This difference can be attributed solely to the principal’s concern regarding accidents since the occurrence of an accident now significantly impacts the value of the project. Consequently, the principal chooses to terminate the contract by firing the agent when his continuation utility decreases sufficiently. This is in stark contrast with the results of [44], where termination is never optimal for .

When the principal becomes much more impatient than the agent, namely , the problem degenerates exactly as in [44] since coincides with until the latter reaches the value , after which it stays identically equal to . Consequently, for small values of the continuation utility of the agent, the presence of accidents leads the principal to prefer dismissing the agent rather than risking the occurrence of an accident that is more costly for her. Conversely, when the continuation utility of the agent increases sufficiently, the principal chooses not to terminate the contract, and the cost of retiring the agent is given exactly by the average loss incurred in case of an accident.

Finally, in case where the principal is still more impatient than the agent but , there is one point at which the concavity of breaks, a feature which never occurred in [44], where is always concave. In fact, the face-lifted utility coincides with up to this point, and is then a non-trivial majorant of . This implies that the principal can prefer dismissing the agent or retiring him based on the actual level of his continuation utility, owing to the combined effect of her impatience and her concerns regarding possible accidents. Surprisingly, this decision is independent of the size of the potential losses, unlike in the case where . For every positive value of , termination of the contract is a possibility, which never arises in the analysis without accidents, namely when .

3.1 The equally impatient case

Here we examine the case where , or equivalently, .

Proposition 3.1.

When , we have on .

Proof.

Let us fix some . The definition of the control–stopping problem in Equation 2.10 easily implies that . To show the reverse inequality, we fix some and . If , the fundamental theorem of calculus implies that

given that the state is determined by the ODE (2.11) and the fact that . Accordingly, it holds that

due to the concavity of the function . On the other hand, if , similar computations as before lead to

Thus, we can conclude that by arbitrariness of and . ∎

3.2 Different discount rates

In general, the Hamilton–Jacobi equation corresponding to the mixed control–stopping problem cannot be simplified into an ODE as presented in [44, Equation A.1]. Nonetheless, with the following assumption, we can verify whether the function can be a solution in the case where the two discount factors and differ.

Assumption 3.2.

If , the function defined by

| (3.3) |

is decreasing and such that .

The assumption naturally implies the existence of the following point

| (3.4) |

and we will implicitly assume this throughout the paper. We show below that 3.2, which is introduced for mathematical convenience, also holds in a simple and reasonable example.

Remark 3.3.

It is important to highlight that within the accident-free framework examined by [44], 3.2 is unnecessary. Specifically, when (and ), the function is strictly negative on due to the strict concavity of over the same interval. Consequently, the latter is a sub-solution, not a solution, to the ODE in (3.1). This observation is also confirmed by [44, Proposition 2.1], which establishes that, under these conditions, the face-lifted utility is a strict majorant of .

Example 3.4.

Suppose and consider the utility function , for . Then,

It is straightforward to verify that 3.2 holds. Indeed,

The factor in front of the positive power function is negative when , which implies that the map is decreasing with . In particular, we find that

3.2.1 A more impatient agent

Throughout this section, we characterise the face-lifted reward function in the case where .

Proposition 3.5.

Let us assume that . We introduce the function

where . Then, the face-lifted utility function is such that

-

if , we have , for

-

if , we have , for .

In particular, is continuously differentiable with . Moreover, it is decreasing and strictly concave, and satisfies the following growth condition:

The proof is postponed to Appendix A.

Remark 3.6.

Proposition 3.5 distinguishes between two cases based on the size of the average loss per accident. When this value is small, specifically less than , the point introduced in (3.4) becomes zero, and therefore the function cannot be a solution of the Hamilton–Jacobi equation (3.1). Conversely, when is strictly above the aforementioned threshold, solves the equation on the non-degenerate interval .

Example 3.7.

In the specific positive power utility setting of Example 3.4, only the second scenario described in Proposition 3.5 occurs, as . Consequently, the face-lifted utility coincides with on , and then it is described by the concave conjugate of , which is given by

Unfortunately, providing an explicit expression for the face-lifted reward on is hindered by the presence of the two different powers that characterise the above formula. Nevertheless, we can approximate using numerical techniques, as it is shown in the graphs at the end of this section.

3.2.2 When the principal becomes strictly more impatient

In our current scenario where , our aim is to provide a comprehensive characterisation of the solution to the Hamilton–Jacobi equation (3.1). Initially, we observe that the point , as defined in (3.4), is positive due to the fact that . This observation suggests the possibility of the solution coinciding with the function in a right-neighbourhood of zero. We will prove that it indeed agrees with , at least until the latter reaches the value of . However, prior to presenting this main result, we derive some key features of .

Lemma 3.8.

If , then it holds that .

Proof.

It is sufficient to prove that since due to continuity. To achieve this, consider as the maximiser in the definition of , which is the unique value such that when , otherwise . In the first case, the fact that implies that allowing us to conclude that

In the second case, it follows that as . This completes the proof. ∎

Hence, we introduce

| (3.5) |

It is now fundamental to distinguish between two distinct cases, depending on or . Specifically, when , the problem (2.10) degenerates, leading to the face-lifted utility coinciding with the function up to the point , after which remains constant at the value of . Conversely, if and , we will show that the two aforementioned functions coincide up to some point within the interval . Beyond this point, referred to as in Lemma 3.9, takes the form of an affine transformation of the face-lifted reward introduced in [44, Proposition 2.1], which we denote as and which is given by

| (3.6) |

Furthermore, [44, Proposition 2.1] proves that is twice-continuously differentiable, decreasing with , and

| (3.7) |

Consequently, we deduce that both the function and its first derivative are negative on the interval .

Lemma 3.9.

Let and . There exists a unique that satisfies .

Proof.

We show that the function , for , has a unique zero on the interval . To achieve this, we assert that is decreasing on ; however, the proof is postponed to the end for the sake of clarity. As a result, the statement follows directly because and . The former inequality arises from the definition of the point in (3.5), given that . To prove that , we first observe that the definition of the point stated in (3.4) and the Equation 3.7 satisfied by lead to the following:

where , for . By noticing that is decreasing on and , we can conclude that . The proof is complete once we verify the claim that on . We proceed by contradiction by assuming there exists some such that . Then, by differentiating the ODE satisfied by and the function , combined with 3.2, we can observe that

Given that , we deduce that

where we have used the fact that as . It follows that . Now, let us define the set of sets

It holds that for some . We have ; otherwise, the same argument as before would lead to the existence of some such that . Consequently, , and on . As a result, the function is strictly concave and decreasing on , implying that . However, this contradicts the fact that dominates on (see [44, Lemma A.3]). ∎

Proposition 3.10.

Let us assume that . Then, the face-lifted utility function can be described as follows:

-

if , we have , for

-

if , we have , for ,

where is defined in Equation 3.5, whereas is introduced in Lemma 3.9. It holds that is twice-continuously differentiable, except at a single point. Furthermore, when , it is decreasing and exhibits the following growth:

This result is proved in Appendix A.

Example 3.11.

Within the specific framework of the positive power utility as described in Example 3.4, we find that

Consequently, if , then

3.3 Numerical simulations

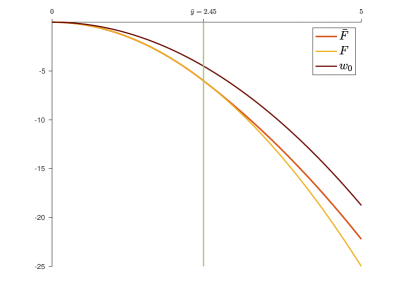

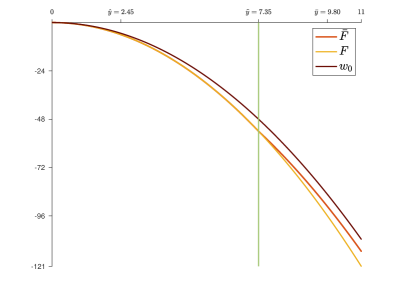

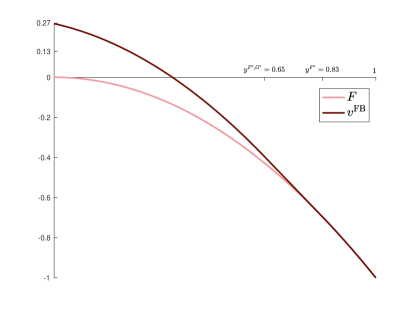

In order to gain a deeper insight into the implications stemming from the accidents incorporated in Sannikov’s contracting problem explored by [44], we perform some numerical simulations. Initially, we consider the specific positive power utility setting outlined in Example 3.4, which we elaborate on in Example 3.7 and Example 3.11, depending on the value of the ratio . For this analysis, we set and . Specifically, in the two graphs provided in Figure 1, we illustrate the face-lifted utility and compare it with its barrier and the face-lifted utility that characterises the problem without accidents. As expected, the latter is always a strict upper bound, particularly since termination is never optimal when but becomes an option for small values of the continuation utility of the agent when . However, as the continuation utility exceeds either or (depending on ), the principal prefers retiring the agent since her reward starts to deviate from the barrier . This results from the requirement to ensure that the agent receives a sufficiently high utility, leading the principal to prefer the risk of potential future losses.

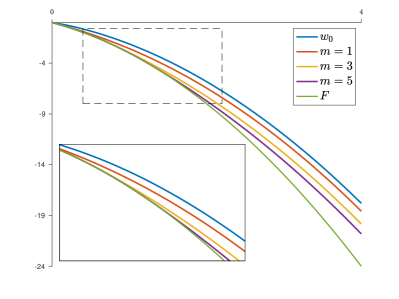

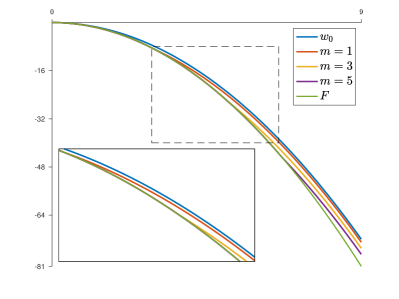

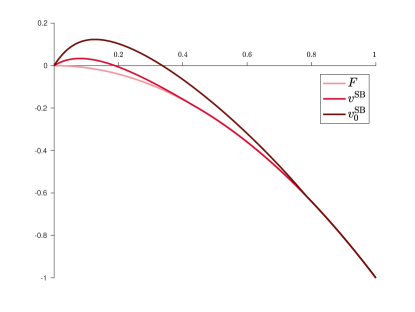

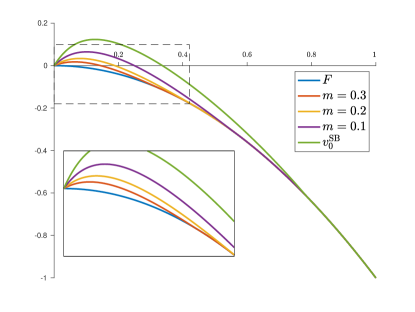

As discussed in Example 3.7, the positive power utility exhibits only a singular scenario when . Consequently, we slightly modify the utility function by considering , for . It is important to note that since this function is injective, it corresponds to a specific utility , which cannot be expressed analytically. However, this is unnecessary for our analysis; what is significant is that since this condition ensures that both scenarios in Proposition 3.5 are feasible. We proceed by illustrating the face-lifted utility in the case when as before, but for different values of . The plot in Figure 2a highlights a continuous dependence between the value of and the value of , and therefore a continuous dependence between the average size of accidents and the length of the interval where termination is the preferred choice. Specifically, it is evident that, as the size of the potential losses reduces, the value of also decreases, while the function increases until converging to the accident-free reward . A similar analysis can be carried out for ; however, for numerical convenience, we consider the standard positive power utility setting , for , where we set . The results are plotted in Figure 2b. Analogously to the case , we can observe a correlation between the value and . The only difference is that the latter is null only in the absence of accidents, that is, when .

4 The first-best problem

In this section, we analyse the first-best contracting problem, which represents the benchmark situation without moral hazard. Indeed, in this case, the principal has all the bargaining power, in the sense that she actually chooses both the contract and the effort of the agent under the constraint that his utility is above the reservation utility:

| (4.1) |

Note that this equality directly follows from the analysis in Section 2.5 as . To characterise the solution to this contracting problem, we introduce the notation to represent the maximal reward obtained by the principal when maintaining the utility of the agent at the level . This function is referred to as the first-best value function, and it holds that By introducing a Lagrange multiplier associated to the participation constraint of the agent and applying the classical Karush–Kuhn–Tucker method, we can always rewrite the first-best value function, for any , as

Clearly, the above expression can be expressed in a more compact form as follows:

| (4.2) |

where we have introduced Notice that this function is clearly non-decreasing and convex. In particular, for all .

In the subsequent analysis, the study of the first-best problem (4.1) is divided into two separate investigations depending on the ratio . Namely, when , the problem can be easily tackled with the aforementioned Karush–Kuhn–Tucker method, while this classical method is not successful to provide a complete characterisation of the first-best value function when . Nevertheless, under the additional condition , we can identify the first-best value function as the unique viscosity solution of the following obstacle problem:

| (4.3) |

for the operator

| (4.4) |

Here, the initial value is given by the expression (4.2), that is,

| (4.5) |

Remark 4.1.

-

Notice that the value is not attainable. Achieving this value would require choosing , , and , but the contract does not satisfy the participation constraint of the agent for any choice of the lump-sum payment which is -measurable.

Despite the apparent differences emphasised previously, we get analogous results to those in [44, Theorem 3.1]. Specifically, we can prove that when , the first-best value function touches the barrier and, when this occurs, the two functions coincide forever. Conversely, when , it can be shown that either the two aforementioned functions coincide in a right-neighbourhood of the origin or they never touch. Unfortunately, in the case where , we are unable to proceed with the analysis; it is possible only when , as we can demonstrate that the problem degenerates. In fact, analogously to [44, Theorem 3.1], it can be shown that the principal can achieve her maximal value , motivating the agent to exert maximal effort continuously and promising him a substantial lump-sum payment at a large retirement time.

Theorem 4.2.

-

Let . Then on and an optimal contract does not exist.

-

Let , and introduce .

-

-

If , then on

-

-

otherwise if , we have that for any . Additionally, the first-best value function is continuously differentiable and, defining 333Notice that as by definition of ., determined by

-

-

-

Let and . We have that the first-best value function is the unique continuous viscosity solution of Equation 4.3 in the class of functions such that for any , for some .

-

-

Let . If , then there exists such that on . Moreover, it is true that on if

-

-

otherwise if , and , then it holds that on . Furthermore, it is twice continuously differentiable, and with such that

-

-

Let , and assume that for any and for any . We can define , recalling that represents the face-lifted reward in the problem without accidents as introduced in (3.6). If for some , then on .

-

-

The proof of the first result follows; we show the remaining items in the subsequent sections and in Appendix B.

Proof of Theorem 4.2..

The fact that the first-best value function is constantly equal to on follows directly from Theorem 5.7.. Furthermore, this value can only be achieved by selecting the effort and the contract with and . However, as highlighted in Remark 4.1., this contract fails to meet the participation constraint of the agent. ∎

Remark 4.3.

-

Definition 2.4 can be readily translated into the first-best setting. Specifically, we say that the first-contracting problem (4.1) exhibits a golden parachute if an optimal solution satisfies on the event set . Based on Theorem 4.2., we can conclude that when and , a first-best golden parachute always exists, and it represents a termination scenario. In other words, the agent stops working at a finite time null if the reservation utility of the agent exceeds leading to the termination of the contract, and the principal paying a positive lump-sum payment. The same holds if and the agent has a positive reservation utility. In this case, the termination time is always zero, signifying that the contract does not start, and the agent receives his reservation utility as payment.

-

Theorem 4.2.- directly implies analogous conclusions when , and . In fact, if the reservation utility of the agent is positive, the first-best problem exhibits a golden parachute. However, since in this case the face-lifted function is strictly above , the contract does not terminate immediately. Instead, the agent does zero effort right from the beginning of the contract, he is immediately retired, and receives a continuous stream of payments. This scenario is never possible in the absence of accidents. In fact, according to [44, Theorem 3.1], there is no golden parachute whenever . This is because the initial value is always positive when , as the function is non-negative.

-

The same result as in the case without accidents holds when and . Theorem 4.2.- states that a first-best golden parachute does not exist since the first-best value function never touches its barrier on .

-

The case of and is the only one that we are unable to analyse in detail. Given the explicit form of the face-lifted utility expressed in Proposition 3.10., particularly the fact that it is only continuous, we expect that the first-best value function might not be smooth on the entire interval of definition . Furthermore, we suspect that, similar to the accident-free framework, there exists a point from which and its barrier coincide if for any and for any . If this were to be confirmed, we could conclude that a first-best golden parachute exists whenever , and this might also be a termination scenario, unlike the case with where the golden parachute always represents a retirement scenario. Conversely, if , we could not automatically claim the existence of a golden parachute, we would need to pay attention to the interval of the non-negative half-line that we are considering. Note that the condition for any and for any is fundamental to ensure that the face-lifted utility is a super-solution and hence a solution, considering that on the whole real line of Equation 4.3 from a certain point onwards. This is the same condition required in [44, Theorem 3.1] for . In this case, it is proved that when the marginal cost of effort at zero is null, the first-best value function never touches the barrier , thereby ruling out the existence of a first-best golden parachute.

4.1 The Karush–Kuhn–Tucker method

Proof of Theorem 4.2..

The first-best value function, as expressed in (4.2), can be further simplified when :

The optimisation with respect to the variable yields the following problem:

| (4.6) |

If , the optimisation with respect to implies that This is because for any . We can deduce that on .

On the other hand, we assume now that . Considering the reformulation of the first-best problem as shown in (4.6), we describe the function by distinguishing three distinct cases depending on which interval of the non-negative half-line we are considering. To begin, let us suppose that . It is worth noting that this interval can be empty because can be non-positive. If this is not the case, then we have that , and

We then consider the case where . It holds that and because of the definition of the two points and . Hence, is a linear function of the following form Lastly, when we have , it follows that . As a consequence,

Reviewing the computations done so far, we can deduce that on . Moreover, the first-best value function is not only continuous but also continuously differentiable since

∎

Example 4.4.

In the specific framework of the positive power utility described in Example 3.4 with , we have Additionally, let us set some , and such that and , and consider the following cost function:

The decision to consider a separate cost in the two tasks of applying effort and reducing accident risk is solely for purely analytical reasons, as it significantly simplifies the calculations, allowing us to explicitly characterise the convex dual

Under the present specification, we have that

Given this specific choice of the utility function , particularly noting that , we fall into the second scenario of Theorem 4.2.. Consequently, the first-best value function is not identically equal to its barrier , but we are unable to provide explicit formulas since and cannot be computed analytically. Setting , , and , we plot our numerical results below. Specifically, we observe that is positive, and therefore, the function is a strictly concave solution to the ODE that characterises the obstacle problem (4.3) within the interval , is affine on , and then coincides with on . It is worth noting that contrary to the results in [44], the function is not strictly concave on the whole domain of definition. Additionally, it is only continuously differentiable, as the gluing of the functions , for , , for , and , for , is only continuously differentiable. These differences arise from the fact that can be negative in our framework with accidents.

4.2 HJB approach

In order to solve the first-best version (4.1) of the contracting problem when and , we follow the general approach developed by [33, Section 4]. More precisely, we show that there is no loss of generality when the principal solves her first-best problem in maximising over the set , which we introduce later in Theorem 4.6, as opposed to optimising over such that the participation constraint is satisfied. This reduction simplifies the first-best problem to a standard stochastic control problem, making it more tractable.

To begin, let us fix a stopping time , an -predictable non-negative process and a control . For a constant , an -valued -predictable process and an -valued -measurable function , we introduce the process defined by the following SDE, for :

| (4.7) |

where denotes the -compensated random measure . Then, we introduce the set as the collection of all and defined as previously, satisfying in addition the following integrability conditions

for some , .

Remark 4.5.

Note that based on Øksendal and Sulem [39, Theorem 1.19], the Lipschitz-continuity in the -variable of the drift implies that the SDE (4.7) has a pathwise unique solution up to the random time . Furthermore, we always consider a càdlàg -modification of the process .

For any , we define the set as the collection of all quintuples , where is an –stopping time, is an -predictable non-negative process, and , that verify that

Theorem 4.6.

It holds that

Proof.

The proof follows by simply adapting the arguments in Theorem 5.2 taking into account that, for any contract and any control , the process defined as

| (4.8) |

is a –uniformly integrable -martingale (see for instance [27, Theorem I.1.42]). Here,

∎

Remark 4.7.

From the representation provided in (4.2) of the first-best value function , we immediately infer that it is non-increasing, given that the Lagrange multipliers take values in the non-positive half-line. This implies that the reward of agent is exactly given by his participation constraint . Consequently, if an optimal contract exists for the first-best contracting problem, it has the following form

where is an –stopping time, is an -predictable non-negative process and .

Theorem 4.6 reduces the complexity of the problem. This reduction simplifies the problem by associating the first-best value function with the corresponding Hamilton–Jacobi–Bellman equation, as presented in (4.3), following the classical reasoning in control theory. Our next objective is to show that the value function is the unique viscosity solution of the aforementioned equation in the class of functions that behave like at infinity. Before verifying this statement, it is necessary to prove that our value function exhibits the desired growth.

Lemma 4.8.

If and , then there exists some such that for any .

Proof.

The definition of the first-best problem straightforwardly implies that on , where . To prove the reverse bound, we first introduce the function

For any , we note that

where the second inequality is a consequence of the definition of , while the last equality follows from the concavity of . Consequently, it is sufficient to verify that there exists a constant such that

| (4.9) |

We can divide the proof into three distinct parts, depending on the specific case under consideration and the corresponding face-lifted utility . In the scenario where and , the function is given in terms of its concave conjugate introduced in (A.3). Based on its description, we can deduce that

In the first inequality, we have used the fact that for any followed by the change of variables . From the previous inequality, it becomes evident that for all . We can conclude that the inequality in (4.9) is satisfied.

When the jumps become larger, specifically in the case of and , we have that on . As the function is upper–semi-continuous since it is an infimum of an arbitrary family of continuous functions, we can deduce the existence of a constant such that for any . Nonetheless, we still need to provide a similar bound on , where is described by the concave conjugate of as given in (A.8). Its explicit formula is as follows, for any :

for some . This allows us to conclude by applying the same change of variables as we did previously.

Proof of Theorem 4.2..

First, it is important to note that the operator introduced in (4.4) is Lipschitz-continuous and non-decreasing with respect to its second variable. These properties are sufficient to say that the same techniques presented in [44, Lemma B.1] work in our setting to prove a comparison theorem for the Hamilton–Jacobi–Bellman equation (4.3) in the class of functions verifying , , for some . Furthermore, standard arguments from viscosity solution theory show that is a discontinuous viscosity solution of Equation 4.3 (the approach is similar to the one in Proposition A.11). Consequently, Lemma 4.8 allows to apply the aforementioned comparison theorem to the function , leading to the conclusion that is the unique viscosity solution, in that class of functions, and it is continuous. ∎

Proof of Theorem 4.2.-.

By assumption, there exists some such that . Since , it follows that for any due to Proposition 3.10.. Additionally, on this interval, solves Equation 4.3 because the fact that is a decreasing function implies that for any . Therefore, the comparison theorem mentioned in the proof of Theorem 4.2. allows us to conclude. ∎

5 Reduction of the second-best contracting problem

This section focuses on reducing the Stackelberg game (2.8) of the principal to a standard mixed control–stopping stochastic problem, following the approach outlined in [47], which was further developed in [19]. This reduction is possible by introducing the continuation utility of the agent as an additional state variable, and then identifying a specific class of contracts that reveal the optimal response of the agent, while ensuring no loss of generality. Before exploring further into this approach, it is essential to note that the Hamiltonian associated to the problem of the agent is defined as

| (5.1) |

Let us introduce an -valued -predictable process and an -valued -measurable function . For any given –stopping time , we define the set as the collection of efforts such that

| (5.2) |

We also need to introduce a family of processes that will be used to reformulate the admissible lump-sum payments at terminal time received by the agent. Let us fix a constant along with a non-negative -predictable process . We define the process as the solution of the following SDE, for :

| (5.3) |

Then, we introduce the set as the collection of all -valued, -predictable processes and -valued -measurable functions such that the supremum (5.2) in the definition of is attained. More precisely, we require that the set is not empty. Additionally, the following integrability conditions need to be satisfied

| (5.4) |

| (5.5) |

for some and .

Remark 5.1.

-

As pointed out in Remark 4.5, the previous SDE admits a unique strong solution . We will prove that the process represents the continuation utility of the agent given the contract , where . In particular, .

-

We highlight the fact that the non-negativity condition imposed on both the utility function and the cost function is translated into a non-negativity constraint of the continuation utility of the agent, namely for any , –a.s. This is just a consequence of a comparison theorem for BSDEs see for instance Papapantoleon, Possamaï, and Saplaouras [41, Theorem 3.25]. Additionally, the limited liability constraint implies that

Considering the previous discussion, we define the set as the collection all quadruples verifying that is an –stopping time, is an -predictable non-negative process, and . Additionally, the contract satisfies the integrability condition (2.12). With this setup, we can now proceed to formulate the reduction argument to rewrite the problem of the principal.

Theorem 5.2.

It holds that

with

| (5.6) |

The result is proved in Appendix C.

Following this result, we can now limit our study to the restricted class of contracts introduced earlier, as this restriction, for the principal, is indeed without loss of generality. Moreover, this choice allows us to reformulate the contracting problem defined by (2.8) in a more standard way, as the agent’s optimal efforts are determined by the maximisers of his Hamiltonian, and thus the problem of the agent can be easily solved. Furthermore, as already emphasised in Remark 5.1., the proof of Theorem 5.2 demonstrates that . Hence, the requirement that ensures that the participation constraint is satisfied.

5.1 The associated HJB equation

In accordance with the results from the reference paper [44] in the accident-free framework, we show that the second-best contracting problem (2.8) degenerates when . In the alternative scenario where , this degeneracy is no longer observed, and in order to characterise the solution of the Stackelberg game, we can consider the simpler mixed control–stopping problem presented in Equation 5.6. This is indeed possible based on Theorem 5.2. Therefore, by using standard techniques in stochastic control (see for instance [39]), we can introduce the following second-order integro-differential equation:

| (5.7) |

for the initial condition . Here, represents the maximal reward obtained by the principal while maintaining the utility of the agent at the level , following a notation similar to that used for the first-best problem. For any , the non-local operator is of the form

| (5.8) | ||||

where the set is the collection of all and such that

| (5.9) |

for some . Additionally, recalling that the function is introduced in Equation 5.1, we denote

Remark 5.3.

It is important to note that the integral operator is of order zero due to the fact that is a bounded measure by assumption since it represents the accident size distribution. Moreover, we have supposed that its support is contained in , for some . Consequently, there is no singularity even at infinity and the integrability condition stated in Equation 5.9 is sufficient to guarantee that the integral operator is well-defined for any function , where

Equation 5.7 should be interpreted in a weaker sense because we do not know a priori whether the value function is smooth, given that it is well-known it does not hold true in various applications. Therefore, we need to refer to an appropriate concept of viscosity solution.

5.1.1 Viscosity solutions for the integro-differential HJB equation

In this section, we introduce the notion of viscosity solution that we refer to throughout the paper since it strictly depends on the integral term appearing in Equation 5.7, especially on the regularity of the measure . For the purpose of our application, it is convenient to adopt the definition of viscosity solution from [25, Definition 2.1] (analogous to the one used by [2, Definition 2]), specifically the version derived from [25, Lemma 2.6], as we seek a solution to (5.7) that is defined on the interval rather than the entire real line.

Definition 5.4.

Let us fix . An upper–semi-continuous resp. lower–semi-continuous function is a viscosity sub-solution resp. viscosity super-solution of (5.7) on if , and for any such that , and attains a global maximum resp. global minimum at , it holds that

Additionally, we say that a locally bounded function is a viscosity solution of (5.7) on if its upper–semi-continuous envelope and its lower–semi-continuous envelope is a viscosity sub-solution and a viscosity super-solution of (5.7) on , respectively.

We can take advantage of the regularity of the integral term that characterises our Hamilton–Jacobi–Bellman equation (5.7) to provide two equivalent formulations of being a viscosity sub-solution (and consequently a viscosity super-solution). These alternative definitions will be more convenient in proving the comparison theorem for (5.7), as we will employ a standard maximum principle that invokes the notion of semi-jets instead of being formulated in terms of test functions.

Lemma 5.5.

An upper–semi-continuous function is a viscosity sub-solution of (5.7) on if and only if either of the two following conditions hold:

-

for any , it is true that

(5.10) -

for any such that attains a global maximum at , it is true that

Remark 5.6.

Proof.

It is straightforward to verify that Lemma 5.5. implies that is a viscosity sub-solution of (5.7) on . Indeed, consider such that and attains a global maximum at . Consequently, by definition, it holds that . Furthermore, we require that , and thus on . Hence, the monotonicity of the integral operator allows us to conclude since

Analogously, we can show that Lemma 5.5. implies Lemma 5.5.. Conversely, let us assume Lemma 5.5. and fix some and . By referencing Fleming and Soner [22, Lemma V.4.1] (or equivalently [25, Theorem 1.23]), it follows that there exists a -function such that , and achieves its maximum at . Moreover, we can also assume that . This implies Lemma 5.5., and thus proves the desired implication.

Finally, in order to show that Definition 5.4 implies Lemma 5.5., we consider some and . As before, we can derive the existence of a -function such that , and achieves its maximum at , where . The result in [25, Theorem 1.20] allows us to select a sequence of -functions such that, for each , for some and

Moreover, it holds that for any . We can deduce that and also have global maxima at . The latter maximum condition implies that and . Therefore,

The following equality holds:

and thus the proof immediately follows from the the monotone convergence theorem, as it implies that

∎

5.2 Characterisation of the solution to the contracting problem

As already mentioned, the second-best contracting problem degenerates when . Specifically, we can show that the reward of the principal reaches its maximum by means of a sequence of admissible contracts that offer the agent small intermediate payments and promise him a large lump-sum payment at a large retirement time. These contracts are constructed in such a way that the agent exerts maximum effort throughout their extremely long duration. However, the large discrepancy between the discount rates of the agent and the principal ensures that even the utility of the agent reaches its maximum.

The alternative scenario where is more interesting to analyse since the problem no longer degenerates. Nevertheless, it is quite challenging since the non-local nature of the Hamilton–Jacobi–Bellman equation (5.7) prevents us from replicating the regularity results presented in [44]. What we can still do is characterising the second-best value function as the unique viscosity solution (within a specific class of functions) to the aforementioned equation by applying dynamic programming principle and some other standard arguments in control theory.

Theorem 5.7.

-

If , then on . Moreover, there is no admissible contract achieving this value.

-

Let . The second-best value function is the unique continuous viscosity solution of Equation 5.7 in the class of functions such that for any , for some . Additionally, if .

The proof of Theorem 5.7. is given in Section D.1.

Proof of Theorem 5.7..

The result is obtained in two main steps. First, the fact that the second-best value function is a viscosity solution of Equation 5.7 is an immediate consequence of some standard arguments in control theory (see for instance [39]). Second, Theorem 4.2 implies that given the fact that the first-best value function is an upper bound for on their domain of definition . In Section D.2, we prove a comparison result for the integro-differential variational inequality (5.7) that immediately allows us to deduce that the second-best value function is the unique viscosity solution of Equation 5.7, and that it is continuous. Lastly, if , we can prove that , where exists as the right derivative of a continuous function. This is an immediate consequence of [44, Theorem 3.4] as the second-best value function in the accident-free setting is a viscosity super-solution of our Hamilton–Jacobi–Bellman equation (5.7). ∎

Unfortunately, we are unable to replicate the regularity results proved in the reference paper without accidents. Specifically, the fact that maximises over the set of controls that depend on the considered point prevents us from showing that whenever the second-best value function intersects its barrier , then it coincides with it forever (this is not possible even under the assumption of [44, Lemma 8.1] that is concave). Consequently, we cannot characterise the stopping region of the contracting problem. Moreover, the introduction of accidents poses another challenge stemming from the definition of the operator . The latter is described as the sum of two components: one related to the effort on the drift of the output process and the other related to the effort on the intensity of accidents. For the sake of simplicity, let us assume that the cost function is separable, specifically , for . As a result,

| (5.11) |

where

Hence, it is evident that and . To analyse the differences with the framework without accidents, we consider an open interval where the second-best value function does not coincide with its barrier , and thus solves the ODE that characterises the variational inequality (5.7). Two different scenarii can occur:

-

if the operator is positive on , then it is possible to demonstrate that is twice continuously differentiable on . Indeed, similarly to Step 2 in the proof of [44, Lemma 8.1], we can show that the aforementioned ODE is uniformly elliptic and consequently admits a classical solution (unique if initial conditions are provided). This is because Theorem 5.7. implies that is continuous, and therefore the ODE can be rewritten as

(5.12) where

(5.13) We argue that the solution coincides with on since the comparison theorem [44, Lemma B.1] can still be applied to Equation 5.12. However, we are unable to find sufficient conditions that guarantee that the operator is positive. For example, in the accident-free framework with , the fact that the value function is necessarily strictly concave implies that is positive in a right-neighbourhood of zero. In the case with accidents, this condition only implies that the operator is positive, and this is compatible with having and if the first derivative is positive for any ;

-

if the operator vanishes on , this does not necessarily imply that on , and thus the second-best value function might solve a different equation from the one that characterises its barrier . This is a pure non-linear first-order integro-differential equation. This possibility can never occur in the problem without accidents since whenever , then the value function touches or it solves the same equation but with a different initial condition.

These considerations lead us to believe that it is unlikely for our second-best value function to be more regular than continuously differentiable, especially when considering that Theorem 4.2 proves that its upper bound is only continuously differentiable when .

5.3 Numerical result

Given the impossibility of explicitly characterising the second-best value function , it is necessary to perform some numerical simulations to illustrate its behaviour and provide insights into its properties. For computational tractability, we simplify the model by assuming that accidents have a constant size, specifically equal to . Consequently, the distribution function of each accident becomes a Dirac measure. This simplification facilitates the direct calculation of the maximisers of the Hamiltonian in (5.1) and, as a result, enables the use of a finite difference approximation to solve the Hamilton–Jacobi–Bellman equation (5.7). To draw a comparison with the case analysed by [47, Figure 1], later revisited by [44, Example 3.10], we consider the scenario within the specific positive power utility setting with separable cost

We set the parameters as follows: , , and , along with and . Note that despite considering the set as bounded, fixing this bound to enables us to illustrate Sannikov’s contracting problem within the context of accidents, even though Sannikov’s problem is characterised by an unbounded . This is because this parameter choice ensures that the optimal effort remains bounded by .

Figure 4 illustrates the second-best value function and its barrier , along with the second-best value function within the accident-free framework . The latter obviously represents an upper bound for as the criterion of the principal is higher in the absence of accidents. While these two functions do not coincide over the entire half-line, it is evident that the features defining are transferred into the description of . In other words, this parameter choice leads us to infer that the agent with a small reservation utility benefits from an informational rent because the principal optimally offers him a contract that gives utility strictly higher than his participation value. Furthermore, we can notice that the second-best value function does not coincide with its barrier in a neighbourhood of zero, but then becomes equal to it, indicating the existence of a golden parachute. This suggests that if the agent’s reservation utility is higher than the point where these functions intersect, the contract terminates immediately. In such a scenario, the agent exerts no effort but receives a positive lump-sum compensation since we are considering the case where both parties are equally impatient, resulting in .