Optimal dividend payout with path-dependent drawdown constraint

Abstract

This paper studies an optimal dividend payout problem with drawdown constraint in a Brownian motion model, where the dividend payout rate must be no less than a fixed proportion of its historical running maximum. It is a stochastic control problem, where the admissible control depends on its past values, thus is path-dependent. The related Hamilton-Jacobi-Bellman equation turns out to be a new type of two-dimensional variational inequality with gradient constraint, which has only been studied by viscosity solution technique in the literature. In this paper, we use delicate PDE methods to obtain a strong solution. Different from the viscosity solution, based on our solution, we succeed in deriving an optimal feedback payout strategy, which is expressed in terms of two free boundaries and the running maximum surplus process. Furthermore, we have obtained many properties of the value function and the free boundaries such as the boundedness, continuity etc. Numerical examples are presented as well to verify our theoretical results and give some new but not proved financial insights.

Keywords. Optimal dividend payout; drawdown constraint; path-dependent constraint; free boundary problem; gradient constraint;

2010 Mathematics Subject Classification. 35R35; 35Q93; 91G10; 91G30; 93E20.

1 Introduction

There is no denial the fact that dividend payout policy plays a fundament role in every company’s operation of risk management. The policy of dividend payout will not only influence the actability of a company to its shareholders but also crucially affect the financial health when preparing for future adverse events. Dated back to De Finetti [13] and Gerber [19], the way to optimally payout dividends from a dynamic surplus process receives considerable investigation and remains its popularity in the areas of actuarial science and financial mathematics. The formulation of the optimal dividend payout problem considers the surplus process as the free capital to invest in an insurance portfolio and the insurer decides the optimal policy to maximize the expected totalization of future discounted dividend payouts before ruin time (i.e. the surplus process goes null or negative). It essentially reveals the fundamental balance between a good dividend compensation to the shareholders and a carefully managed surplus process to secure the position so as to avoid or delay future bankruptcy (ruin). There are miscellaneous variants in the literature on this problem concerning different modeling of the underlying surplus process (e.g., compound Poisson model in Gerber and Shiu [21], Albrecher et al. [1]; Brownian motion model in Asmussen and Taksar [7], Gerber and Shiu [20], Azcue and Muler [9]; jump-diffusion model in Delhaj [10]; stochastic profitability model in Reppen, Rochet and Soner [26]) and various types of constraint on the dividend policy (e.g. Keppo, Reppen and Soner [24] considered capital injections; one could refer to Avanzi [8] for an overview).

In this paper, we focus on an optimal dividend problem with drawdown constraint where the manager seeks for an optimal payout policy by maintaining the dividend payout rate no less than a fixed proportion of its historical running maximum. Generally speaking, a drawdown constraint is a particular type of habit-formation on the policies where the habit is formatted by setting up the reference benchmark as the running maximum of the policy history. This type of habit-formation has been extensively investigated among mathematical finance literature. For instance, Dybvig [15] first set up a infinite horizon life-time portfolio selection model with consumption ratcheting constraint where no decline is allowed in the standard living of the agent. Similar problems with ratcheting constraint over the wealth has been studied by Roche [27] and Elie and Touzi [16]. Considering the optimal consumption problem within an expected utility framework, Arun [6], Angoshtari et al. [4] and Deng et al. [14] extended the model in Dybvig [15] with drawdown constraint to allow the consumption to decrease while being no less than a fixed rate of its running maximum. Jeon et al. [23] and Albrecher et al. [2] discussed the horizon effect for the similar optimal consumption problems with either consumption ratcheting or drawdown constraint by imposing a finite time investment cycle. Recently, Angoshtari et al. [5] considered the same problem but taking the habit-formation as the exponentially weighted average of the past consumption rate. For the dividend payout problem, under both Brownian and compound Poisson types of surplus process, Albrecher et al. [1] and [2] concretely studied the optimal dividend problem with ratcheting constraint by defining the admissibility of dividend policies as non-decreasing and right continuous process. But they have only obtained viscosity solutions, so no optimal dividend payout policies were derived. Guan and Xu [22] studied the optimal dividend problem with ratcheting constraint by a PDE argument, and succeeded in deriving an optimal feedback payout strategy. Reppen et al. [26] considered the optimal dividend problem in a stochastic profitability model. They adopted the viscosity solution approach to study the problem. More recently, by adopting the viscosity solution approach Angoshtari et al. [3] imposed the drawdown constraint in the dividend payout which is similar to the setting of this paper and provided sufficient conditions on the optimality of so called “two-curve” strategies.

Technically, involving drawdown constraint into the optimal dividend problem shall lead to two-dimensional optimal control problem. Unlike classical variational inequality with function constraint (American option pricing is a typical example), the resulting Hamilton-Jacobi-Bellman (HJB) equation forms a new type of variational inequality of which a gradient constraint on the value function against the running maximum of the past dividend payout rate would be inevitably incorporated. Unlike those HJB equations with gradient constraints in portfolio selection (such as transection cost models in Dai and Yi [12], Dai et al. [11]), the operator in our HJB equation does not involve the derivatives of the value function against the running maximum of the past dividend payouts, therefore one cannot reduce the HJB equation to a one-dimensional variational inequality. This also leads to the failure of the well-known methods such as penalty method to study our HJB equation. To the authors’ knowledge, there seems no universal way to deal with such type of stochastic control problems. Albrecher et al. [2] considered the optimal dividend payout problem with ratcheting constraint and derived the HJB equations which is of the type of variational inequality we mentioned above. By discretizing the admissible set of the dividend policies into finite number of strategies, they proved for each fixed policy (dividend rate) the resulting value function is the viscosity solution to the corresponding HJB equation and the convergence of the optimal value function on the finite ratcheting strategies to the continuous case can be guaranteed in the sense of viscosity solutions. In this paper, we maintain the assumption that the underlying surplus process follows the Brownian motion model in Albrecher et al. [2] while considering the drawdown constraint which allow the dividend payout to decline over time but no less that a certain proportion of highest past dividend payout. In contrast to the viscosity solution techniques, following Guan and Xu [22], we have explored a new and more general PDE method to study the problem. Following the similar idea of discretization in Albrecher et al. [2], we disperse the parameter(running maximum of historical dividend payout) equidistantly such that a regime switching system of -states variational inequalities could be obtained. The new system of equations are a sequence of ordinary differential equations (ODEs) whose solvability can be easily resolved. Then the problem with continuous parameter can be approximated by making approach to infinity and taking the limit. By classical PDE theories, the existence and uniqueness of strong solution and its continuity with respect to the parameter can be obtained by making the uniform norm estimation on the solution of the regime switching system. Different from the linear operator in Guan and Xu [22], the operator in our HJB equation becomes non-linear, therefore many existing arguments in [22] do not work here. Compared with the viscosity solution, our solution has the advantage that, based on our solution, we can succeed in deriving an optimal feedback payout strategy, which is expressed in terms of two free boundaries arising from the HJB equation and the running maximum surplus process. Furthermore, the properties of the value function and free boundaries such as the boundedness, continuity are obtained as well.

The remainder of the paper is organized as follows. In Section 2, we formulate an optimal dividend payout problem with path-dependent drawdown constraint. Sections 3 and 4 provide explicit solutions to the boundary case and the simple case, respectively. Section 5 is devoted to the study of the complicated case. We first use delicate PDE techniques to solve the HJB equation in a proper space and then provide a complete answer the problem by a verification argument. The properties of two free boundaries are throughoutly investigated. Also, numerical examples are presented to verify our theoretical results and give some new financial insights that are not proved.

2 Model formulation

Throughout this paper, we fix a probability space satisfying the usual assumptions, along with a standard one-dimensional Brownian motion . Let denote the filtration generated by the Brownian motion, argumented with all -null sets. Let denote the set of nonnegative real numbers and the set of natural numbers. We use to denote for any (column) vector or maxtrix .

We consider a representative insurer (He) and model its surplus process by a diffusion model. Then the surplus process after paying dividends follows

| (1) |

where and are constants, standing respectively for the return rate and volatility rate of the surplus process, is the dividend payout rate of the insurer at time , which of course is an adapted process. As usual, we define the ruin time of the insurer as

with the convention that . We emphasis that the ruin time always depends on the insurer’s dividend payout strategy throughout the paper.

Given a (dividend payout) strategy , we define the corresponding running/historical maximum payout process as

Clearly it is irrational to payout dividend at a faster rate than its return rate, so we put a maximum allowed dividend payout rate such that

| (2) |

We also fix a maximum allowed drawdown proportion . A dividend payout strategy is called admissible if it is right-continuous with left-limit and satisfies

| (3) |

Given an initial value , let denote the set of all the corresponding admissible dividend payout strategies.

In this paper, we consider an optimal dividend payout problem for the insurer whose objective is to find an admissible dividend payout strategy to maximize the discounted cumulated dividend until the ruin time. Mathematically, his aim is to determine

| (4) |

where is a constant discount factor. Since and , the value function is clearly nonnegative and upper bounded by . On the other hand, if the initial surplus is , then the ruin time is 0, so we have for all .

When , the problem (4) can be easily solved by dynamic programming. Whereas when , the admissible dividend payout strategies must be non-decreasing over time, and the problem (4) becomes the so-called dividend ratcheting problem, which has been studied in Albrecher et al. [1] and [2] for different surplus models by viscosity solution technique and eventually completely solved by Guan and Xu [22] by PDE method.

Clearly, the major difficulty in solving the dividend payout problem (4) comes from the dividend payout constraint (3). Except for , the constraint is path-dependent, that is, the current and future admissible strategies depend on the whole past values. There seems no uniform way to deal with this type of stochastic control problems in the literature. In this paper, following [22], we adopt a PDE argument plus stochastic analysis method to tackle the problem (4).

3 The boundary case:

Before solving the general case, we first need to determine the boundary value since it is needed to write out the HJB equation for the problem (4). We emphasis that, for a usual optimal control or stopping problem, the boundary condition is usually trivial to obtain from the problem formulation. For instance, the value function on the boundary is usually nothing but the payoff function of an American option in an option pricing problem. But for our problem this is not the case; we cannot determine from the problem formulation immediately. Indeed, the problem itself is a stochastic control problem. This is very different from Guan and Xu [22] where the boundary value is almost trivial to obtain.

Although it is not immediately to know the optimal value , the boundary case is still relatively easy to solve, because the path-dependent constraint (3) in this case becomes path-independent. We are not only be able to give the optimal value in this case but also able to provide an explicit optimal dividend payout strategy for the problem (4).

Indeed, in the boundary case, it is easy to see that a strategy is an admissible strategy in if and only if it satisfies for all . This is because all admissible strategies are upper bounded by , and consequently the running maximum payout process remains to be a constant, i.e. , from the beginning, so the constraint set becomes time invariant. Mathematically speaking,

| (5) |

Since the above problem (3) only depends on the initial state , its HJB equation must be an ODE, therefore, one would expect to solve it completely. By contrast, in the general case, the HJB equation to (4) has an additional argument representing the running maximum, so it seems too ambitious to get an explicit value function or optimal dividend payout strategy.

3.1 Verification result for the boundary case

To get an explicit value function of the boundary problem (3), we start from the following verification result, which shows that if a function is sufficiently good (i.e., satisfying the hypothesis of Proposition (3.1)), then it is the value function of (3). We also provides an optimal dividend payout strategy for the problem (3).

The following two operators and will be used throughout this paper:

Note that, unless , in general is a nonlinear operator. This is the critical difference between our problem and that in [22] where so that is a linear operator. The nonlinearity of not only brings tremendous difficulties to our mathematical analysis, but also change the fundamental structure of the optimal strategy. We will face two free boundaries whereas there is only one in [22].

Proposition 3.1 (Verification for the boundary case)

Suppose satisfies the following ODE:

| (6) |

If both and are bounded, then is the value function of the problem (3), i.e.,

Moreover, an optimal dividend payout strategy is given by , where

| (7) |

Proof: Suppose fulfills the hypothesis of the proposition. Then for any admissible strategy in , we have

| (8) |

This together with Itô’s formula gives

Since is bounded, after integrating on and taking expectation, it follows

Because and is bounded, it follows

and since , it gives

So

This shows that is an upper bound for the value of the problem (3), namely .

If we choose the feedback dividend payout strategy as in (7), then

Also, all the above inequalities become equations, so

This together with shows that is an optimal strategy for the problem (3), and is the value function.

By the above result, we need to find a solution to (6). We provide an explict one in the next section.

Remark 3.2

The condition that is bounded can be removed from the above proposition by a standard localizing argument.

3.2 Explicit optimal value and optimal strategy

We use the following parameters throughout this paper:

Indeed, , and are, respectively, the unique positive roots for the quadratic equations:

We will use the simple fact that and frequently in our subsequent argument without claim.

Lemma 3.3

The inequality holds if and only if .

Proof:

Note that the quadratic function satisfies when and when , so is equivalent to , i.e. .

Lemma 3.4

If , we then define

If , then there is a unique positive number such that

and we define

Then satisfies (6), , and is strictly decreasing (thus is strictly concave) on . Moreover, in the second case.

We will use and defined above throughout the paper.

Proof: The estimates and can be easily deduced from the strictly monotonicity of and on . So we only need to establish the latter and satisfies (6).

Suppose . Then , and evidently and is strictly decreasing on . Since , we have

It thus yields

and

where the last equation is due to that is a root for the equation

So satisfies (6). This completes the proof for the first case .

In the rest of the proof, we assume so that .

We first prove that

| (9) |

which in particular implies . In fact, from the trivial inequality

we get

Since and are the two roots for the equations

we get from the Viete theorem that

This together with gives

which gives the desired inequality (9).

We next prove the existence of . Write

| (10) |

Since and , it follows

Thanks to , we have ; and thanks to ,

Hence, admits unique positive root in .

By the definitions of and , we have Because

we see that and are continuous at , and so are on . In particular, .

Using the same argument for the previous case, one can show that satisfies (6) on and clearly is strictly decreasing there. We now show that the same properties hold on too. Using the fact that and are the roots for the equations

one can show that

| (11) |

We now suppose that is strictly decreasing on , then since , we have on , which together with (11) implies that satisfies (6).

To show that is strictly decreasing on , we fix arbitrary and such that . Then for any , so

After rearrangement it reads

which yields

Recalling the inequality (9), we deduce

This can also be rewritten as

Since , it follows

leading to

This confirms that is strictly decreasing on .

Finally, since and are continuous and satisfies (6) on ,

we conclude that . This completes the proof.

Theorem 3.5 (Optimal value and optimal strategy in the boundary case)

Economically speaking, since one cannot increase the value of the running maximum in the boundary case, so it is fixed. In this case, one should pay dividends at the maximum rate if the market risk is relative high (i.e., ) or equivalent the maximum rate is relatively small (i.e., ). The optimal strategy does not relay on the surplus level. On the other hand, if the market risk is low (i.e., ) or equivalent the maximum rate is relatively big (i.e., ), then the optimal strategy depends on the surplus level. One should pay dividends either at the maximum rate if the surplus level is relative high (i.e., ), or at the minimum possible rate if the surplus level is relative low (i.e., ).

We now turn to the general case, which is divided into a simple case: , and the reminder complicated case: . In the former case, we will give an explicit optimal value and optimal strategy. In the latter case, the problem becomes complicated and no explicit solution or strategy is available.

4 The simple case:

We first solve the simple case: . Similar to the boundary case, we can deduce the following explicit optimal value and optimal strategy.

Theorem 4.1 (Explicit optimal value and optimal strategy in the simple case)

Suppose . Then the optimal value to the problem (4) is

and an optimal dividend payout strategy is given by , where .

Proof: If , then and by Lemma 3.3. Therefore, for any strategy , we have

Repeating the proof of Proposition 3.1 with

(8) replaced by the above inequality, one can prove the claim.

Note that the value function in the simple case is invariant with respect , i.e.,

for all .

In the rest of the paper, we deal with the more complicated case: .

5 The complicated case:

From now on we study the complicated case: , which is henceforth assumed. We will adopt a novel PDE argument plus stochastic analysis method to tackle the problem.

Our analysis consists of several parts. We start with introducing the HJB equation for the problem (4). The second step is the key of approach, where we introduce and study a regime switching system, a sequence of ODEs (where are indeed single-obstacle problems), whose solvability can be established easily by standard PDE theory. In the next step, we establish a lot of estimates for the solution of the regime switching system and construct a solution to the HJB equation of the original problem (4) from the solution of the regime switching system. Also, we propose an optimal dividend payout strategy depending on some free boundaries arising from the HJB equation. The last step is to verify that the constructed solution to the HJB equation is the value function and the proposed strategy is optimal.

We introduce the following variational inequality on :

| (13) |

It is indeed the HJB equation for our problem (4). We will show its solution is the value function of (4). The exact meaning of its solution is given as follows.

Denote and

Definition 5.1

Theorem 5.2 and Theorem 5.7 will provide a complete answer to the problem (4) in the complicated case. The former resolves the solvability issue of the HJB equation (13) and establishes some properties of its solution. The latter gives the optimal value and optimal strategy for the problem.

Theorem 5.2

This result will be proved in Section 5.3. In the rest part of this section, we let denote the unique solution to (13), given in Theorem 5.2.

To derive the optimal strategy, our initiative thinking is as follows. On one hand, we hope to pay dividend as much as possible to increase the objective in (4), the total discounted dividend payouts. But this may lead to two unfavorable results: first, it may increase the running maximum so that shrinking the set of admissible strategies given by (3) in the future and decreasing the value function; second, the ruin time may come earlier. To avoid these negative impacts, our strategy is to increase the running maximum to some higher level only when the value functions coincide at these two levels. This motives us to define the following switching region

In this region, if we increase the running maximum from to , the value function will not change. Since is non-increasing in , the complement of in , called the non-switching region, is given by

In this region, increasing the running maximum is harmful, so one should not do that; in other words, one should not pay dividends exceeding the running maximum. In particular, we have (15) holds if

It is nature to conjecture that one shall increase the running maximum only when his wealth is high enough. This motives us to define the switching boundary as follows:

| (21) |

with the convention that . Clearly it holds that if . The following result shows that the reverse statement is almost true.

Proposition 5.3

The switching boundary is positive, bounded and continuous on . The limit exits and is finite. Also, if , then for any . As a consequence, the switching and non-switching regions and are separated by :

These properties will be proved in Section 5.4.

Remark 5.4

We do not know whether belongs to or . But we have the following equivalencies:

-

•

is non-decreasing if and only if .

-

•

is non-increasing if and only if .

Indeed, we conjecture that is non-decreasing, which is consistent with numerical examples. Unfortunately, we cannot confirm this in theory unless which is proved in [22].

In order to find the optimal strategy, we define the equivalent maximum rate as

and the equivalent minimum rate as

For , the following facts can be easily verified:

-

•

;

-

•

If , then , , ;

-

•

If , then for ;

-

•

If , then ;

-

•

If , then ;

-

•

if and only if ;

-

•

if and only if .

Given a wealth level , we can increase the running maximum dividend rate to its equivalent maximum rate , which is the maximum dividend rate that will not reduce the optimal value. In particular, if , then one should not increase the running maximum dividend rate at this wealth level . Also if , then the optimal value of the problem (4) is known since .

The following result, which characterizes the equivalent maximum rate, will play a critical role in finding an optimal strategy for the problem (4).

Proposition 5.5

For each , is non-decreasing and is non-increasing on . Also, for , it holds that

| if ; | (22) | ||||

| (23) | |||||

| (24) | |||||

| (25) | |||||

| (26) | |||||

| (27) | |||||

Also,

These properties will be proved in Section 5.5. Below is an demonstration figure.

On the other hand, the objective is linear in the dividend payout, so one may expect a bang-bang dividend payout strategy: paying dividend at the maximum possible rate if the surplus is relatively high; at the minimum rate otherwise. If the marginal utility is bigger than one, then one should keep the surplus as high as possible to wait for a better future, so one should save money and pay dividend at the minimum possible rate; otherwise, at the maximum rate. The above thinking motives us to define the following minimum dividend payout region

and the maximum dividend payout region

These two regions will be separated by the following converting boundary

| (28) |

The following result characterizes the converting boundary.

Proposition 5.6

The converting boundary is continuous on , and satisfies , , and

| (29) |

Also, it separates the minimum and the maximum dividend payout regions and :

Using the above results, we now give the optimal value and the optimal strategy for the problem (4) in the complicated case as follows.

Theorem 5.7 (Optimal value and optimal strategy in the complicated case.)

For any , any admissible dividend payout strategy and any constant , through a change of measure argument, one can show that is a Brownian motion under some equivalent probability measure, so for any subset of with zero Lebesgue measure.

Applying Itô’s formula (see [25] Theorem 33 on page 81) to and then taking expectation lead to

where is the continuous part of . The mean of the stochastic integral is zero since the integrand is bounded. Applying (13), we get

Together with

we have

| (30) |

Because , , dropping the first term in the expectation and sending in above, the monotone convergence theorem gives

Since is arbitrary selected, we obtain .

We now prove the opposite inequality and show that is an optimal strategy. Thanks to the continuity of and , the right-continuity of given by (25), it is not hard to verify is an admissible strategy.

We now assume , where is a stopping time given by

Since , we have . It follows

and

It follows from (15) that

| (31) |

which, in particular, yields

By the construction of , it gives

Now applying Itô’s formula to on gives

| (32) |

Now let us consider the case , where is a stopping time defined by

We first assume . Then . So, by the construction of and (23),

By virtue of (22),

implying

If , then thanks to (27), we have , so

If , then , so the above equation also holds. Also, if , then , and thus

Because and for any , we get

Now suppose , then . It implies ; and hence

Now applying Itô’s formula to on gives

| (33) |

Finally, we assume , then . We can deduce similarly to the case to get

Combining (32), (33) and above, we obtain

| (34) |

Because is bounded and , it yields

whereas, by virtue of and , it follows

Therefore, by sending in (34) and using the dominated and monotone convergence theorems, we obtain

In view of the definition of , we conclude that , and consequently, that is an optimal dividend payout strategy.

It is left to prove Theorem 5.2, Proposition 5.3, Proposition 5.5 and Proposition 5.6. This will be a long technical journey. Before doing that, we first present our numerical study.

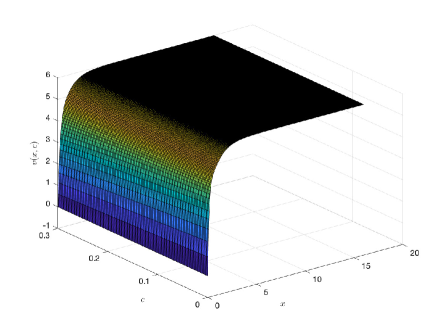

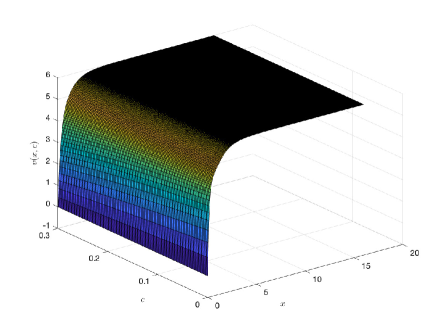

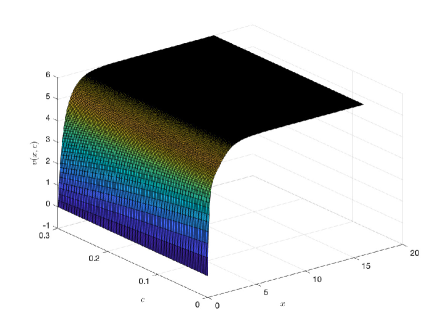

5.1 Numerical examples

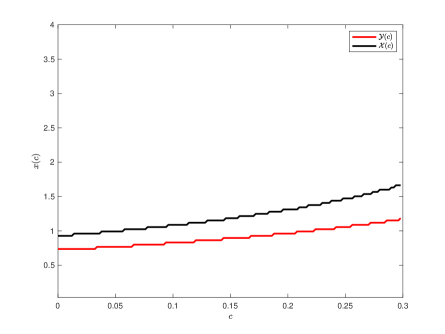

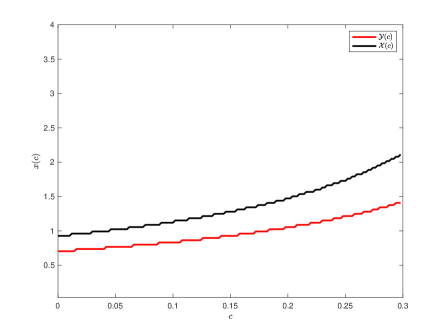

We provide here some numerical examples with parameter values , , , .

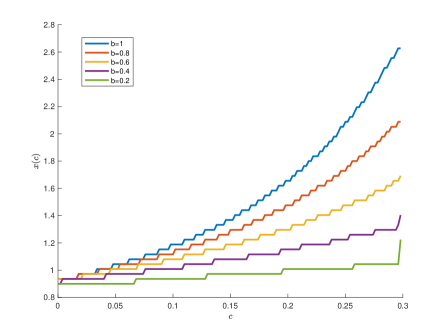

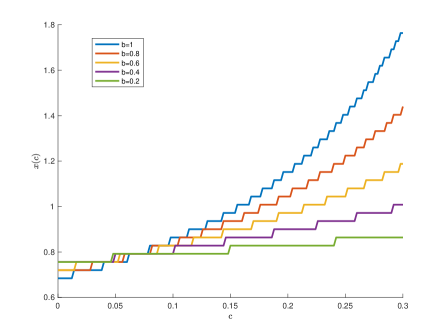

We study the impact of different values of in Figures 4-7. In each figure, the switching boundary and the converting boundary are shown in the left panel; whereas the corresponding value function is shown in the right panel. These figures are calculated by solving (35) in the next section.

We can observe from Figures 4-7 that the bigger the value of , the bigger the slopes of and . Financially speaking, a stricter drawdown constraint makes its harder to increase the maximum dividend payout rate. This is consistent with our intuition.

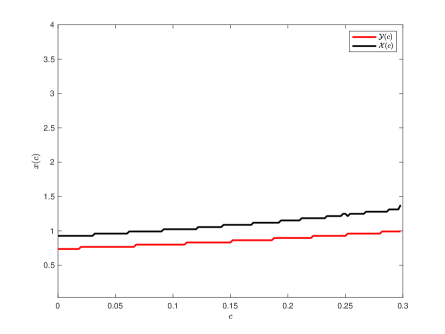

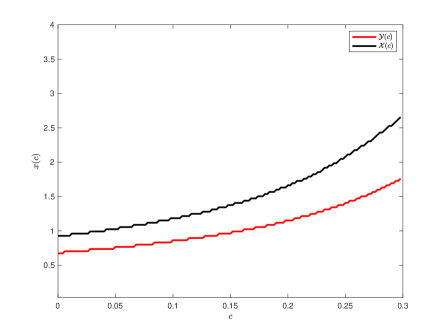

Figure 8 compares and at difference values of .

The left panel in Figure 8 shows that the bigger the value of , the bigger the value of . It means, when the drawdown constraint becomes stricter, in order to increase the maximum dividend payout rate, one has to achieve a higher surplus level. By contrast, we see from the right panel in Figure 8 that the value of is not always monotonic increasing w.r.t. .

Unfortunately, we cannot prove these phenomenons observed in above.

5.2 An approximation regime switching problem

We notice that (13) is a PDE, which is generally harder to deal with than ODEs of the same order. Following Albrecher et al. [2], we reduce it to the study of a sequence of ODEs. We use a pure differential equation methods to study it, so that a better solution will be given.

Let us explain our approach in details as follows. Since is increasing, the admissible strategy set is shrinking as the increasing of . If there are only finite discrete values for , one can treat the cases one by one backwardly: from a lager value to a smaller one. We have already done the first step where achieves its maximum that is the boundary case studied in Section 3. We can deal with the case where is fixed as a smaller value than . Since the running maximum is fixed, the HJB equation reduces to an ODE, which can be treated similarly to the boundary case studied in Section 3. By mathematical induction, we can solve the discrete value case. Once this is done, we will take a limit argument to derive the desired solution to the original HJB equation (13).

We now realize the above idea. Suppose the dividend payout rate can only take the following discrete values

with . Let , we consider the following regime switching ODE system:

| (35) |

under bounded growth condition. Here, we can think of as an approximation of .

Clearly, the system (35) can be solved recursively: for each , it is a single-obstacle ODE problem if is known. One could easily construct a numerical scheme (such as the standard penalty method in [17]) to generate the solution to (35) given is known. The free boundaries and can thereby be connected for all as shown in the previous section.

Lemma 5.8

The system (35) has a solution for any and which satisfies

| (36) | |||

| (37) |

and

| (38) |

Moreover, for each there is a free boundary point such that if and if . Also, if .

By the standard penalty method and theorem, we can prove

step by step from . By the Sobolev embedding theorem, we also have

since the process is standard (see, e.g., [18]), we omit the details.

From (35), we have

| (39) |

so the lower bound in (36) holds. Furthermore, since for , it follows that by recalling that and Lemma 3.4.

We now prove the remaining claims by mathematical induction. By Lemma 3.4, we have satisfies (36)-(38). Suppose all the desired results of the lemma hold for some (), we are going to prove they also hold if .

By the induction hypothesis, we have . It is clearly that the constant function is a super solution to (35) for , so also satisfies the upper bound in (36).

We now prove the set

is not empty. Suppose, on the contrary it was empty, then by (35) we would have on . Applying the comparison principle we can prove that under the bounded growth condition and , which would lead to , contradicting to the order (39). Therefore, is not empty, and consequently,

We next prove that

| there is no such that and . | (40) |

Suppose, on the contrary, there is some such that and . There are two cases: either there is such that

or . In the former case, since and are continuous, there is a neighborhood such that in so that

| (41) |

Whereas in the latter case, we set and the above equation still holds since .

Combining (35) and (41) yields

| (42) |

Note that both functions and attain their minimum value at , so

It implies the right hand side (RHS) of (42) is negative at . Since the RHS of (42) is continuous in , we have a.e. in if is sufficiently small. It follows that is strictly concave in , which contradicts that attains its minimum value at . Hence we have (40).

By definition, we have , so (40) leads to . By the induction hypothesis, (38) holds at , so for any . Combining these estimates we conclude

| (43) |

We next prove

| (44) |

Note that the function satisfies

| (45) |

Notice (43) implies for . It thus follows

so is another solution to (45). By the uniqueness of solution to (45), we conclude (44). Therefore, is the unique free boundary point for .

We come to prove . Since in and by the induction hypothesis, we only need to prove

| (46) |

Differentiating the equation in (35) yields

| (47) |

where Becasue and , the comparison principle leads to (46).

Finally, we prove (38) when . By (43), we know (38) also holds for . Fix any .

Applying (43), it is easy to check that the constant function is a super solution of (47) in , so (38) also holds for .

Lemma 5.9

The following variational inequality

admits a unique solution (see [28])

where

where satisfy

and

Note that , so . It follows, for ,

which means is a super solution to (35). Since , we have

By (38), we conclude .

Lemma 5.10

For each , we have

| (49) |

where is a constant independent of , and .

Proof: We can rewrite (35) as

From (48), we know the RHS is uniformly bounded, so the estimation together with (36) and (48) gives (49).

The Sobolev embedding theorem and Lemma 5.10 imply the following.

Corollary 5.11

For each , we have

| (50) |

where is a constant independent of and .

Since we will take a limit argument to constract a solution to (13) from that of (35), we first derive more properties of the solution to (35).

Define

Lemma 5.12

We have

| (51) |

where is a constant independent of and .

Proof: The lower bound comes from (35). Let be given in Lemma 5.9. Thanks to (48), we have

Let , then

namely, is a super solution to (35), so . The claim thus follows by redefining .

We use the following function in the rest of this paper:

| (52) |

It is clear that .

Lemma 5.13

We have

| (53) |

where is a constant independent of and .

Proof: Since in , we only need to prove (53) holds in Denote . The difference of the equations of and in leads to

where .

Corollary 5.11 and Lemma 5.12 imply that and are uniformly bounded independent of and , so applying the estimation, we obtain is bounded by some constant independent of and . Then the Sobolev embedding theorem shows that is also bounded and independent of and . The claim then follows.

Lemma 5.14

We have

| (54) |

where is a constant independent of and .

Proof: Since by Lemma 5.8 and in , we only need to prove that (54) holds in . By the equation of we know

where On the other hand, by the equation of in (35) and noting that , we have

Dividing the difference of the above two estimates by gives

Similarly, we can deduce

So satisfies

where the last inequality is due to (53). Moreover, because and , by the comparison principle, we have in , which gives (54) with .

5.3 Proof of Theorem 5.2

Now we are ready to prove Theorem 5.2. Fix any . Then .

For each , rewrite as if . Let be the linear interpolation function of . Lemma 5.9 and Lemma 5.12 imply is uniform Lipschitz continuous in . Apply the Arzela-Ascoli theorem, there is , and a subsequence such that, for each ,

Lemma 5.10 implies

for any ; the estimate (36) implies that is bounded in ; (51) implies that is non-increasing in . The above shows .

Furthermore, the estimate (16) comes from (51). The estimates (17)-(19) follow from (36)-(38) and (48). The estimate (20) is a consequence of (49)-(51).

We come to prove that satisfies (13). The boundary conditions are trivially satisfied. We now show

For each , by the construction of , there is such that Moreover, from Lemma 5.10 and Corollary 5.11 we also have (or its subsequence) weakly in and uniformly in for each . Let in the inequality

we get

It is only left to show the last requirement (15) in Definition 5.1. Suppose for all . For each fixed , there is a sequence such that and . So for large enough, . Since , we have . There must exist some integer such that . Thanks to Lemma 5.8, we have

It then follows from (35) that

where . The sequence has a subsequence converging to some , so that

Let , we have

So we conclude that is a solution to (13).

We now prove the uniqueness. Suppose are two solutions to the problem (13). Let where is a small constant such that

| (55) |

We come to prove

| (56) |

for any Suppose it is not true, then

Because and are bounded, tends to uniformly for all if . Hence, must attain its maximum value at a point by continuity. Without loss of generality, we may assume is the largest such that

Similarly, because , we have , and consequently,

Since is non-increasing w.r.t. , the above implies

which by the definition of the solution to (13) implies

| (57) |

On the other hand, because , we see so that is an interior maximizer. Hence, we have

which implies

where the last inequality is due to . Combining with (55) we have

contradicting (57). So we have (56), which gives by sending . The same argument gives Therefore, the solution to (13) is unique.

From now on, we let be the unique solution to the HJB equation (13) defined above. We next show is continuous in , which will complete the proof of Theorem 5.2.

5.4 Properties of the switching boundary and proof of Proposition 5.3

In this section, we establish Proposition 5.3. It will be a consequence of the below Lemmas 5.15 5.19.

Recall that

Lemma 5.15

If , then

| (60) |

and for all As a consequence, we have

| (61) |

and

Proof: Since , we have . If , then and thanks to (15),

If , then and satisfies (6), so the above equation also holds. So by (13),

| (62) |

Since attains its minimum value 0 at , it gives

Suppose . Then the RHS of (5.4) is negative at . Since it is continuous in , we have in for some small . It then follows in , which together with yields in , contradicting that is non-increasing in . Therefore, we conclude (60).

By (19) and (60) we have if and thus if Therefore, the function , defined by

satisfies

Since , we have

Since the solution of the above problem is unique, so we have in .

The estimate (61) is a consequence of (60) and the continuity of .

The last two claims come from the fact that implies for any .

Lemma 5.16

We have

| (63) |

Proof: For and , by monotonicity and , we have

It hence follows

| (64) |

by recalling that .

Comparing to (61), we conclude that .

To prove the continuity of , we need the following estimate.

Lemma 5.17

Proof: Denote

where is constructed in Lemma 5.8 with and . Suppose

for some . Then by Lemma 5.14,

for , so

i.e.

Since is non-increasing w.r.t. , we have

Let we obtain (65).

Lemma 5.18

The switching boundary is continuous in .

Proof: We first prove the right limit exits at any point , namely

| (66) |

Suppose, on the contrary, there are , and such that

Then by definition, there are two sequences and such that

| (67) |

and a decreasing sequence such that

Let

then it satisfies

| (68) |

where

Due to (20) and (16), and are bounded independent of , by the estimation we know is uniformly bounded in . On the other hand, using Lemma 5.17 and (67) we have

so it has a subsequence converges to weekly in and uniformly in . Moreover, note that is bounded in and converges to in , so it has a subsequence converges to in .

Letting in (68), we have in i.e. in However, substituting into we conclude and thus in leading to a contradiction.

In a similar way, we can prove and so that

We come to prove

Suppose, on the contrary, there are and such that

Then there is such that in note that by (60) we have in , so

then we have i.e. in Similar to above, it will lead to a contradiction.

It is left to prove

For each by the definition of and Lemma 5.15, there is such that , for all i.e. , then we have for all . So , which implies .

On the other hand, for each there is such that for all i.e. , so for all . By the continuity of , we have which implies and thus,

Lemma 5.19

The switching boundary is bounded in .

Proof: Suppose, on the contrary, there is a convergence sequence such that . Because is continuous in , we have . Let

Because and (16), we conclude that is bounded independent of . Notice,

where

By the estimation and , we know is bounded in for any , so it has a subsequence converges to some weekly in and uniformly in . Noting that

so satisfies

Since we have . Thus, there is large enough such that for . Let

where and is sufficiently small such that

Then

Since applying the comparison principle yields for . It thus follows that However, since , , leading to a contradiction.

5.5 Proof of Proposition 5.5

We now prove Proposition 5.5 in this section.

First, the monotonicity of and follows from Lemma 5.15 immediately.

To prove (22), we first assume .

-

•

If , then by Proposition 5.3, . On the other hand, it follows from definition that , leading to a contradiction.

-

•

If , then by the continuity of , we have for any , where is a sufficiently small positive constant. Consequently, by Proposition 5.3, . On the other hand, since , we have for any , so , leading to a contradiction.

Therefore, we have , namely (22) holds. Now suppose . For any , we have . The above result shows , which implies (22) since .

We now establish (23). If , then , so (23) follows from (6). If , then , so the equation (23) follows from (15).

To prove (24), we suppose and let . If for some , then , so that , which implies . But this contradicts that . Hence, , which implies . Since , we obtain from (15) that

Thanks to the continuity of , sending in above gives the desired equation (24).

To show the right-continuity property (25), since is non-decreasing w.r.t. , it suffices to prove

Let be a sequence such that and . By definition, we have , so it follows from the continuity of that which by definition implies completing the proof of (25). Similarly, one can prove (26).

We now prove (27). Since for all , we have . Now suppose . Thanks to the monotonicity of and Lemma 5.17, we have

for Since for all , we see the right hand side in the above estimate is . By sending , we get , completing the proof of (27).

The proof of Proposition 5.5 is complete.

5.6 Properties of the converting boundary

We next study the properties of the converting boundary, which is defined as

From the above definition we know when . By the continuity of and (19), we have when , so is the free boundary separating the two regions and :

Lemma 5.20

The converting boundary is continuous and positive in with .

Proof:

For any , let and . Then by the continuity of we have . Note when , so by (19) we have is non-increasing when . Then the continuity of implies is non-increasing in , so in However, substituting into we conclude and thus in leading to a contradiction. Now we established the continuity of .

Since , we obtain . If for some , then , which together with implies for sufficiently small . But this contradicts the non-increasing property of w.r.t. .

The proof is complete.

The definition of and (61) imply that for any . Since is continuous, we have . The next result Lemma 5.21, which gives a better estimate than (61), implies . As a consequence, , which implies Proposition 5.6.

Lemma 5.21

We have

| (69) |

The rest of the paper is devoted to the proof of Lemma 5.21. To this end, we first proof three technical lemmas.

Lemma 5.22

If for some , then we have

Proof: If , then by Lemma 3.4, which is strictly decreasing, so we have for .

We now prove the other case by contradiction. Suppose the conclusion is not true for some such that . Then

Due to (64) and the continuity of , we have and . By (19) we conclude for all , so the equation of in becomes

| (70) |

Then satisfies

Moreover, and for all imply . Meanwhile, combining , (17), (70) and (2)111This is the only place where we used the condition (2) throughout this paper. Indeed, this condition can be removed with more delicate analysis. We leave this to the interested readers. gives

Then applying the maximum principle yields for all So we have for all . But we just proved for all , so for all .

Taking this into (70) yields that , which contradicts that on .

In order to cover the case , we extend the lower bound 0 to a negative number . We denote by the corresponding value function when the range of is limited to . Then from the discussion above we know all of the above conclusions still apply to for all and when , so we can extend the domain of to for any without changing its value.

Lemma 5.23

Suppose for some . Suppose, in addition, if . Then there is no such that .

Proof: Suppose, on the contrary, there are such that . If , then since , we have and hence,

If , then the above holds as well since .

Let

Then the above inequality leads to

where

By Lemma 5.22, we have in so that in . Combining and and applying the strong maximum principle and the Hopf lemma, we have . However, we also have for all , so the continuity of gives , leading to a contradiction.

Lemma 5.24

Suppose for some . Suppose, in addition, if . Then there must exist such that .

Proof: Suppose, on the contrary, there is no such that for some fixed that fulfills the assumptions.

For all , let ,

Then , so .

Notice , so by the continuity of and , we have . If , then and it contradicts the assumption . If , then it contradicts the assumption that there is no such that . So we must have and both the sequences and converge to .

Because and , by Lemma 5.15, we have so that . Hence we can define

Thanks to the monotonicity of w.r.t. , we have . By (23) and (24) we have

and

So

where

Thanks to (20), we may assume , converges to uniformly in . Moreover, from Lemma 5.22 we know in , which implies the sequence converges to in On the other hand, since , and are bounded independent of , by the estimation we know is bounded in . So it has a subsequence converges to a weekly in and uniformly in . Hence satisfies

Notice

so by taking limit, it yields , which together with further implies .

By the strong maximum principle and the Hopf lemma, we have , leading to a contradiction.

Proof of Lemma 5.21:

From Lemma 5.23, Lemma 5.24, and (61), we deduce that and for any such that .

To complete the proof of Lemma 5.21, it suffices to show that for any such that .

Since for all , we get . There are only two cases.

- Case .

-

Using (22), we get Clearly , it hence follows . By the proved result, we have . Consequently,

- Case .

-

Since for any , we have by defintion. Since which is decreasing, it follows

The proof is complete.

References

- [1] Hansjorg Albrecher, Pablo Azcue, and Nora Muler. Optimal ratcheting of dividends in insurance. SIAM Journal on Control and Optimization, 58(4):1822–1845, 2020.

- [2] Hansjorg Albrecher, Pablo Azcue, and Nora Muler. Optimal ratcheting of dividends in a Brownian risk model. SIAM Journal on Financial Mathematics, 13(3):657–701, 2022.

- [3] Hansjorg Albrecher, Pablo Azcue, and Nora Muler. Optimal dividends under a drawdown constraint and a curious square-root rule. Finance and Stochastics, 27(2):341–400, 2023.

- [4] Bahman Angoshtari, Erhan Bayraktar, and Virginia R Young. Optimal dividend distribution under drawdown and ratcheting constraints on dividend rates. SIAM Journal on Financial Mathematics, 10(2):547–577, 2019.

- [5] Bahman Angoshtari, Erhan Bayraktar, and Virginia R Young. Optimal investment and consumption under a habit-formation constraint. SIAM Journal on Financial Mathematics, 13(1):321–352, 2022.

- [6] T Arun. The merton problem with a drawdown constraint on consumption. arXiv preprint arXiv:1210.5205, 2012.

- [7] Søren Asmussen and Michael Taksar. Controlled diffusion models for optimal dividend pay-out. Insurance: Mathematics and Economics, 20(1):1–15, 1997.

- [8] Benjamin Avanzi. Strategies for dividend distribution: A review. North American Actuarial Journal, 13(2):217–251, 2009.

- [9] Pablo Azcue and Nora Muler. Optimal reinsurance and dividend distribution policies in the Cramér-Lundberg model. Mathematical Finance, 15(2):261–308, 2005.

- [10] Mohamed Belhaj. Optimal dividend payments when cash reserves follow a jump-diffusion process. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 20(2):313–325, 2010.

- [11] Min Dai, Zuo Quan Xu, Xun Yu Zhou. Continuous-time Markowitz’s model with transaction costs. SIAM Journal on Financial Mathematics, 1 (2010), 96-125.

- [12] Min Dai and F. H. Yi. Finite-horizon optimal investment with transaction costs: A parabolic double obstacle problem. J. Differential Equations, 246 (2009), 1445-1469.

- [13] Bruno De Finetti. Su un’impostazione alternativa della teoria collettiva del rischio. In Transactions of the XVth international congress of Actuaries, volume 2, pages 433–443. New York, 1957.

- [14] Shuoqing Deng, Xun Li, Huyên Pham, and Xiang Yu. Optimal consumption with reference to past spending maximum. Finance and Stochastics, 26(2):217–266, 2022.

- [15] Philip H Dybvig. Dusenberry’s ratcheting of consumption: optimal dynamic consumption and investment given intolerance for any decline in standard of living. The Review of Economic Studies, 62(2):287–313, 1995.

- [16] Romuald Elie and Nizar Touzi. Optimal lifetime consumption and investment under a drawdown constraint. Finance and Stochastics, 12:299–330, 2008.

- [17] Peter A Forsyth, and Vetzal, Kenneth R Quadratic convergence for valuing American options using a penalty method. SIAM Journal on Scientific Computing, 23(6): 2095–2122, 2002.

- [18] Avner Friedman. Parabolic variational inequalities in one space dimension and smoothness of the free boundary. Journal of Functional Analysis, 18(2):151–176, 1975.

- [19] Hans U Gerber. Entscheidungskriterien für den zusammengesetzten Poisson-Prozess. PhD thesis, ETH Zurich, 1969.

- [20] Hans U Gerber and Elias SW Shiu. Optimal dividends: analysis with brownian motion. North American Actuarial Journal, 8(1):1–20, 2004.

- [21] Hans U Gerber and Elias SW Shiu. On optimal dividend strategies in the compound poisson model. North American Actuarial Journal, 10(2):76–93, 2006.

- [22] Chonghu Guan and Zuo Quan Xu. Optimal ratcheting of dividend payout under brownian motion surplus. arXiv preprint arXiv:2308.15048, 2023.

- [23] Junkee Jeon, Hyeng Keun Koo, and Yong Hyun Shin. Portfolio selection with consumption ratcheting. Journal of Economic Dynamics and Control, 92:153–182, 2018.

- [24] Jussi Keppo, A Max Reppen, and H Mete Soner. Discrete dividend payments in continuous time. Mathematics of Operations Research, 46, 3, 895-911, 2021.

- [25] Philip E Protter. Stochastic differential equations. Springer, 2005.

- [26] A Max Reppen, Jean-Charles Rochet, and H Mete Soner. Optimal dividend policies with random profitability. Mathematical Finance, 30(1):228–259, 2020.

- [27] Hervé Roche. Optimal consumption and investment strategies under wealth ratcheting. preprint, 2006.

- [28] Michael I Taksar. Optimal risk and dividend distribution control models for an insurance company. Mathematical methods of operations research, 51:1–42, 2000.