\ul

Demystifying DeFi MEV Activities in Flashbots Bundle

Abstract.

Decentralized Finance, mushrooming in permissionless blockchains, has attracted a recent surge in popularity. Due to the transparency of permissionless blockchains, opportunistic traders can compete to earn revenue by extracting Miner Extractable Value (MEV), which undermines both the consensus security and efficiency of blockchain systems. The Flashbots bundle mechanism further aggravates the MEV competition because it empowers opportunistic traders with the capability of designing more sophisticated MEV extraction. In this paper, we conduct the first systematic study on DeFi MEV activities in Flashbots bundle by developing ActLifter, a novel automated tool for accurately identifying DeFi actions in transactions of each bundle, and ActCluster, a new approach that leverages iterative clustering to facilitate us to discover known/unknown DeFi MEV activities. Extensive experimental results show that ActLifter can achieve nearly 100% precision and recall in DeFi action identification, significantly outperforming state-of-the-art techniques. Moreover, with the help of ActCluster, we obtain many new observations and discover 17 new kinds of DeFi MEV activities, which occur in 53.12% of bundles but have not been reported in existing studies.

1. Introduction

Decentralized Finance (DeFi) has attracted a recent surge in popularity with more than 40B USD total locked value (def, 2020). Since transactions broadcasted in the underlying P2P network of blockchain are globally visible, opportunistic traders can strategically adjust the gas price to prioritize their transactions and earn extra revenue from DeFi, which is known as the generic term Miner Extractable Value (MEV) (Daian et al., 2020; Eskandari et al., 2019; Zhou et al., 2021c, b; Ferreira Torres et al., 2021; Qin et al., 2022; Wang et al., 2021).

MEV competition undermines both the security and efficiency of blockchain systems. First, it incentivizes financially rational validators (miners in the context of PoW) to fork the chain, thereby deteriorating the blockchain’s consensus security (Qin et al., 2022; Daian et al., 2020). Second, it aggravates network congestion (i.e., P2P network load) and chain congestion (i.e., block space usage) because opportunistic traders who compete for MEV opportunities prioritize their transactions at the cost of considerable time delay for other transactions (Daian et al., 2020).

The Flashbots organization proposed the bundle mechanism which enables opportunistic traders to design more sophisticated MEV extraction for profits, because it allows traders to submit a sequence of self-constructed and/or selected transactions as a bundle, which can even include unconfirmed transactions broadcasted on the P2P network. It was reported that compared to the vanilla Sandwich attacks, the bundle-based variants were more profitable (mba, 2021).

However, little is known about DeFi MEV activities conducted through the bundle mechanism. To demystify the status quo of DeFi MEV activities in bundles, we aim at answering the following questions, namely how prevalent are known DeFi MEV activities in bundles? Are there new DeFi MEV activities that are unreported before in bundles? If that is the case, how did they behave and how prevalent are they? What are the differences between DeFi MEV activities in bundles and other DeFi MEV activities? The answers to these questions can help researchers have an in-depth understanding of DeFi MEV activities, e.g., the features of various MEV activities and the robustness of today’s MEV mitigation techniques.

In this paper, we conduct the first systematic study on DeFi MEV activities performed through Flashbots bundle. A DeFi MEV activity usually consists of several DeFi actions, each of which refers to an interaction between a trader and an individual function provided by the contracts of DeFi applications. For example, a contract of AMM (Automated Market Maker) should support the swap DeFi action for exchanging different assets (Xu et al., 2023). A cyclic arbitrage (Wang et al., 2021) MEV activity involves multiple swap actions in different contracts of AMMs with different prices for profits.

To characterize DeFi MEV activities, we need to first recognize them according to their DeFi actions. Although existing studies (Wang et al., 2021; Qin et al., 2022, 2021a; Wang et al., 2022a; Piet et al., 2022; Wu et al., 2021; exp, 2021a; eth, 2015; Weintraub et al., 2022) examined DeFi MEV activities and their DeFi actions, they cannot conduct a systematic study on DeFi MEV activities in Flashbots bundle because they suffer from two limitations. First, the majority of them (Wang et al., 2021; Qin et al., 2022, 2021a; Wang et al., 2022a; Piet et al., 2022; exp, 2021a; Weintraub et al., 2022) focus on a few DeFi applications and could not be easily extended to cover other DeFi applications because they rely on considerable manual efforts to derive the rules for recognizing DeFi actions according to the specific events emitted by the contracts of DeFi applications and their arguments (cf. Table 1). Thus, they will miss many DeFi actions in bundles. Although DeFiRanger (Wu et al., 2021) intends to address this limitation by adopting an automated approach to recognize DeFi actions, it suffers from inaccurate recognition of DeFi actions as shown in §5.3. Second, none of them can recognize DeFi MEV activities with unknown patterns of DeFi actions.

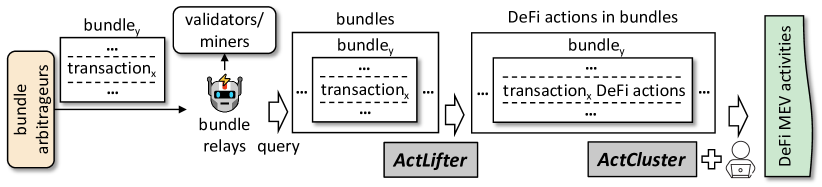

To address the aforementioned limitations, we design a new approach shown in Fig. 1 to discover known and unknown DeFi MEV activities in bundles. We first collect bundles constructed by bundle arbitrageurs via querying Flashbots’ APIs (fla, 2021a). Then, to address the first limitation, we propose ActLifter (§3), a novel automated tool for accurately identifying DeFi actions in the transactions of each bundle. ActLifter first recognizes the contracts that operate the DeFi actions, the type of the DeFi actions, and the asset transfers involved in the DeFi actions according to the captured events (§3.3), then identifies DeFi actions according to the asset transfer patterns of DeFi actions (§3.4). It is worth noting that only a one-off small amount of manual effort is needed to collect events that will be emitted while executing DeFi actions, and we provide scripts to automate the process as much as possible (§3.2).

To address the second limitation, it is inevitable to involve manual inspection to uncover new DeFi MEV activities. To reduce manual efforts, we propose ActCluster (§4), a new approach that uses representation learning (Noroozi et al., 2017) to derive distinguishable feature vectors of bundles according to DeFi actions recognized by ActLifter, and leverages iterative clustering analysis (Liu et al., 2019) and our pruning strategies to facilitate us to discover new DeFi MEV activities.

We conduct extensive experiments (§5) to evaluate the performance of ActLifter and use ActCluster to discover DeFi MEV activities from 6,641,481 bundles (from the launch of the bundle mechanism on Feb. 11, 2021 to Dec. 1, 2022). More precisely, we evaluate the effectiveness of ActLifter in identifying ten kinds of common DeFi actions and compare it with two state-of-the-art techniques, i.e., Etherscan (eth, 2015) and DeFiRanger (Wu et al., 2021). For a fair and convincing comparison with ethical consideration, we spent more than six months in collecting 1,358,122 transactions from Etherscan to mitigate potential risks or negative effects. We queried one page of Etherscan per 10 seconds, which is slower than the human click speed, and manually solved the reCAPTCHA human authentication. The experimental results show that ActLifter outperforms existing techniques and achieves nearly 100% precision and recall. Moreover, we discovered 17 new kinds of DeFi MEV activities and three known DeFi MEV activities in bundles with the help of ActCluster, which reduced at least 24.2%, 97.8% and 98.8% of manual efforts than three baseline strategies.

We further demonstrate how our approach (i.e., ActLifter and ActCluster) can enhance relays’ MEV countermeasures (§6.1), evaluate forking and reorganization (abbr. reorg) risks caused by bundle MEV activities (§6.2), and evaluate the impact of bundle MEV activities on blockchain users’ economic security (§6.3). Moreover, we discuss three feasible usages of our approach in MEV studies, supported by our experimental results and observations (§6.4).

| Methods | SW | AL | RL | LI | NM | NB | LE | BO | AI | RE |

| Qin et al. (Qin et al., 2022) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ||

| Qin et al. (Qin et al., 2021a) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | |

| Wang et al. (Wang et al., 2022a) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | |||

| Wang et al. (Wang et al., 2021) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | |

| Mev-explore (exp, 2021a) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ||

| Piet et al. (Piet et al., 2022) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | |||

| Weintraub et al. (Weintraub et al., 2022) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ||

| Etherscan (eth, 2015) | ✗ | ✗ | ✗ | |||||||

| DeFiRanger (Wu et al., 2021) | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | |||

| ActLifter |

-

•

DeFi actions. SW: Swap, AL: AddLiquidity, RL: RemoveLiquidity, LI: Liquidation, NM: NFT-Minting, NB: NFT-Burning, LE: Leverage, BO: Borrowing, AI: Airdrop, RE: Rebasing.

In summary, this work makes the following contributions.

-

•

First systematic analysis of DeFi MEV activities in bundles. To our best knowledge, our work constitutes the first effort toward a systematic analysis of DeFi MEV activities conducted through Flashbots bundle mechanism after tackling two limitations.

-

•

Novel approach for identifying DeFi actions. We propose ActLifter, a novel approach for automatically identifying DeFi actions from transactions, which outperforms existing techniques and achieves nearly 100% precision and recall.

-

•

New approach for discovering bundle MEV activities. We propose ActCluster, a new approach facilitating us to discover bundle MEV activities with much less manual efforts. In particular, it empowers us to discover 17 new kinds of DeFi MEV activities.

-

•

New applications. We demonstrate the usages of our approach (i.e., ActLifter and ActCluster), including enhancing relays’ MEV countermeasures, evaluating forking and reorg risks caused by bundle MEV activities, and evaluating the impact of bundle MEV activities on blockchain users’ economic security. Additionally, we discuss three feasible usages of our approach in MEV studies, supported by our experimental results and observations.

We refer readers to (app, 2023) for our full paper version with the appendix.

2. Background and notation

This section introduces DeFi applications and actions, Flashbots bundle, and the notations used in this paper. For the basic concepts of smart contracts, events, and ERC20/ERC721 standards, we refer readers to other helpful studies (Tikhomirov, 2017; Macrinici et al., 2018; Heimbach and Wattenhofer, 2022b). Besides, the basic concepts of representation learning can be found in Appendix I.

2.1. DeFi Applications and Actions

We focus on ten core DeFi actions of popular DeFi applications (i.e., AMM, Lending, NFT, and Rebase Token) involved in most MEV activities (Ferreira Torres et al., 2021; Qin et al., 2022; Wang et al., 2021; Wu et al., 2021; Qin et al., 2021a; Zhou et al., 2021b, c, a; Wang et al., 2022a). Each Defi action is represented in the form C.action(params), where C, action, and params refer to the smart contract implementing the DeFi action, the type and the parameters of the DeFi action, respectively.

AMM. It provides functions that allow traders to perform asset exchanges over liquidity pools automatically (Xu et al., 2023). Traders can supply or remove their assets with liquidity pools as liquidity providers, and pay a fee to liquidity providers when they exchange assets via an AMM. We focus on three core DeFi actions supported by AMMs:

-

•

A1: Swap action AMM.Swap(x1: Asset1, x2: Asset2). It performs asset exchange for a trader, which lets AMM receive x1 amount of Asset1 and send out x2 amount of Asset2.

-

•

A2: AddLiquidity action AMM.AddLiquidity(x1: Asset1, x2: Asset2, …, xn: Assetn) (n 0). It lets AMM receive n assets from a liquidity provider.

-

•

A3: RemoveLiquidity action AMM.RemoveLiquidity(x1: Asset1, x2: Asset2, …, xn: Assetn) (n 0). It lets AMM return n assets to a liquidity provider.

Lending. It provides loanable assets through collateralized deposits (Werner et al., 2021; Bartoletti et al., 2021; aav, 2020; com, 2019; mak, 2019). With a collateralized deposit, a borrower can take loanable crypto assets from Lendings. It uses two kinds of debt mechanisms (aav, 2020; com, 2019; mak, 2019), i.e., over-collateralization and under-collateralization, meaning that borrowers can deposit collateral assets with a higher (resp. lower) value than that of borrowed assets. We focus on three major DeFi actions supported by Lendings:

-

•

A4: Borrowing action Lending.Borrowing(x1: Asset1). It lets a borrower loan Asset1 from Lending with the over-collateral deposit (Wang et al., 2022a).

-

•

A5: Leverage action Lending.Leverage(x1: Asset1). It lets a borrower loan Asset1 from Lending with the under-collateral deposit (Wang et al., 2022a).

-

•

A6: Liquidation action Lending.Liquidation(x1: Asset1, x2: Asset2). It lets a trader send the debt Asset1 to Lending for repaying the debt asset and receive the collateral Asset2 from the Lending if the negative price fluctuation of the collateral asset happens (Qin et al., 2021a).

NFT (Non-Fungible Token). It provides unique tokens to represent someone’s ownership of specific crypto assets, e.g., CryptoKitties, or a physical asset, like an artwork (Das et al., 2021). Most NFT contracts follow the ERC721 standard (William et al., 2018). We focus on two major DeFi actions supported by NFT contracts:

-

•

A7: NFT-Minting action C.NFT-Minting(tokenId: Asset). It lets the NFT contract C mint an NFT with the tokenId x1.

-

•

A8: NFT-Burning action C.NFT-Burning(tokenId: Asset). It lets the NFT contract C burn an NFT with the tokenId x1.

Airdrop. The airdrop is a promotional activity for bootstrapping a cryptocurrency project by spreading awareness about the cryptocurrency project (Victor, 2020). A small amount of the cryptocurrency is sent to active users for free when they retweet the post sent by the project account. We focus on the following action:

-

•

A9: Airdrop action C.Airdrop(x1 : Asset1). It lets the contract C send out the Asset1.

Rebase Token. Rebase Token follows a continuous rebasing about the number of tokens in circulation (e.g., total supply in ERC20 standard) (Schär, 2021; Amp, 2018). For example, token holders’ balances increase or decrease automatically according to the token’s price evolution provided by price oracles (Adams et al., 2020). We focus on the following action:

-

•

A10: Rebasing action C.Rebasing(). It lets token holders’ balances in C contract automatically increase or decrease.

2.2. Flashbots bundle

The Flashbots (fla, 2021b) designed the bundle mechanism in 2021. When transactions broadcast over the P2P network, bundle arbitrageurs can observe and analyze them, and include them into bundles along with other transactions. Besides, bundle arbitrageurs can adjust the order of transactions in bundles. Bundle arbitrageurs then send bundles to trusted relays privately, such as relays of Flashbots (fla, 2021b), Eden (ede, 2021), and BloXroute (blo, 2021). The relays distribute bundles to connected miners privately. During the distribution, bundles cannot be observed by other P2P peers, until bundles are included into blocks. The connected miners will preferentially include the bundles that are the most profitable to them into the head of their mining blocks by calculating a bundle pricing formula (fla, 2021b).

Ethereum changed its consensus mechanism from PoW to PoS in September 2022 (eth, 2022). In the context of PoS, validators are selected to create new blocks and add blocks to the Ethereum blockchain, while miners do these tasks in the context of PoW. After the Merge, the Proposer-Builder Separation (PBS) (Yang et al., 2022) is introduced on Ethereum. In PBS, the role of validators is divided into builders and proposers. Specifically, builders create blocks with transactions from their mempool (Tikhomirov, 2017) and proposers submit blocks to the blockchain.

Flashbots proposed MEV-Boost (mev, 2022b) in 2022, which supports bundle mechanism in the context of PBS. In MEV-Boost, bundles are first propagated from arbitrageurs to builders privately. After creating blocks with bundles, builders submit blocks to relays privately with promising payments to proposers. Relays then distribute received blocks to connected proposers privately, and proposers finally pick the block with the most payments to submit to the blockchain. Currently, Flashbots (fla, 2021b), Eden (ede, 2021), and BloXroute (blo, 2021) maintain their builders and relays based on MEV-Boost. Besides, 68% of Ethereum blocks are created and relayed by MEV-Boost (mev, 2022b) from the starting date of MEV-Boost (Sep. 2022) to Jan. 2023 (mev, 2022c), and 77% of MEV-Boost blocks (i.e., blocks that are created and relayed by MEV-Boost) are from Flashbots (fla, 2022). Our studies shed light on DeFi MEV activities in bundles, since in both the context of PoW and PoS: i) arbitrageurs construct bundles, ii) bundles are relayed from arbitrageurs to validators/miners privately, and iii) validators/miners submit the most profitable bundles to them into the blockchain.

2.3. Notation

DeFi action. It, denoted as , represents an interaction between a trader and a function provided by DeFi applications. We focus on ten kinds of DeFi actions (A1-10 in §2.1).

DeFi actions in a transaction. A transaction can trigger the execution of multiple contracts, by invoking their functions via internal transactions. Hence, multiple DeFi actions can be operated in a transaction. We use to denote a sequence of n (n 0) DeFi actions operated in a transaction, where = [A1, A2, …, An]. Note that these DeFi actions will be executed one by one in the order.

DeFi actions in a bundle. A bundle includes a sequence of m (m 0) transactions, each of which can be signed by different accounts. These transactions will be executed one by one in the order. We use = [, , …, ] to denote all the DeFi actions involved in a bundle.

Asset transfer. Since DeFi actions involve one or more asset transfers according to their definitions (Wang et al., 2022a; Bartoletti et al., 2021; Xu et al., 2023; Schär, 2021; Victor, 2020), to identify DeFi actions, we need to recognize asset transfers and match them against asset transfer patterns of DeFi actions. We denote an asset transfer as Asset.Transfer(From, To, Value), which means From transfers Value amount of Asset to To, and we consider Asset, From, To, and Value are parameters of asset transfers. We consider two kinds of assets, i.e., crypto token and ETH, and distinguish them by the subscript of Asset. For example, Asset refers to the ETH asset and Asset refers to the token asset maintained by the contract C. We focus on ERC20 and ERC721 token assets, and our approach can be easily extended to other token assets by recognizing asset transfers from their standard events. We denote ERC721 token minting/burning as Asset.Minting/Burning(From, To, Value), meaning that the contract C mints/burns an NFT of Asset with the tokenId Value. With them, we can recognize the NFT-Minting and NFT-Burning actions.

Execution trace of a transaction. It refers to a sequence of states and opcodes executed in a transaction, denoted as (op0, s0), (op1, s1), …, (opn, sn) . Each state si is in the form of Stacki, Memoryi , where Stacki and Memoryi are the stack (Wood, 2014) variables and memory (Wood, 2014) variables, respectively. The opcode opi is defined in (Wood, 2014). For each opcode opi, the state si represents the execution environment (Wood, 2014) of opi, and the state si+1 denotes the state after executing opi.

3. ActLifter

3.1. Overview

As shown in Fig. 2, ActLifter takes in transaction execution trace and the mapping between the signature of events and the type of DeFi actions, which is constructed by a semi-automated preparation process (§3.2), and then determines DeFi actions (A1-10 in §2.1) in the transaction by two steps.

S-1 (§3.3) It first locates the emitted events in the execution trace whose signatures are in . For each event, it outputs: i) the contract that conducts the DeFi action and emits the event, ii) the corresponding type of the DeFi action in , and iii) the asset transfers involved in the DeFi action.

S-2 (§3.4) Given the information of each event (i.e., the contract, the type of DeFi action, and the asset transfers), it recognizes the corresponding DeFi action according to the asset transfer patterns (§3.4) and outputs them.

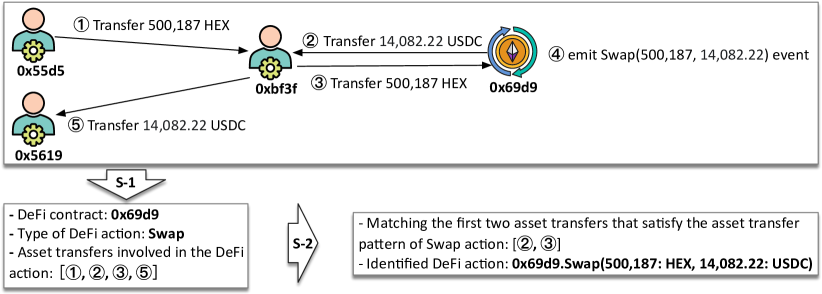

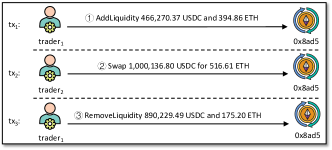

Motivating example. Fig. 3 shows how ActLifter identifies a Swap action in a transaction, where there are four asset transfers (i.e., \raisebox{-.9pt} {1}⃝, \raisebox{-.9pt} {2}⃝, \raisebox{-.9pt} {3}⃝, and \raisebox{-.9pt} {5}⃝), and the AMM 0x69d9 emits an event Swap(500,187, 14,082.22) in \raisebox{-.9pt} {4}⃝.

In S-1, ActLifter first locates the event Swap(500,187, 14,082.22) emitted in \raisebox{-.9pt} {4}⃝ whose signature is in , and then recognizes i) the contract 0x69d9 since it emits the event in \raisebox{-.9pt} {4}⃝, ii) the type of DeFi action (i.e., Swap), and iii) the four asset transfers (i.e., \raisebox{-.9pt} {1}⃝, \raisebox{-.9pt} {2}⃝, \raisebox{-.9pt} {3}⃝, and \raisebox{-.9pt} {5}⃝) since their parameters are logged in the event, i.e., 500,187 and 14082.22. The outputs of S-1 are [(0x69d9, Swap, [\raisebox{-.9pt} {1}⃝, \raisebox{-.9pt} {2}⃝, \raisebox{-.9pt} {3}⃝, \raisebox{-.9pt} {5}⃝])]. In S-2, ActLifter recognizes the Swap action 0x69d9.Swap(500,187: HEX, 14082.22: USDC) in the transaction according to the asset transfer patterns of Swap action (§3.4) (i.e., the contract 0x69d9, which operates the Swap action, receives HEX in \raisebox{-.9pt} {3}⃝ and sends out USDC in \raisebox{-.9pt} {2}⃝).

DeFiRanger (Wu et al., 2021) will report a false Swap action by pairing asset transfers in \raisebox{-.9pt} {1}⃝ and \raisebox{-.9pt} {5}⃝, because it only matches the first two asset transfers that satisfy the criteria defined in (Wu et al., 2021), i.e., one account receives and sends out different assets in two asset transfers.

3.2. Preparation

The majority of existing studies (Wang et al., 2021; Qin et al., 2022, 2021a; Wang et al., 2022a; Piet et al., 2022; exp, 2021a) use specific events to recognize DeFi actions, because smart contracts use events to notify others (e.g., users, third-party tools) about their execution (e.g., state changes) (Zhang et al., 2021). Motivated by these studies, we construct a mapping from the events to the corresponding type of DeFi actions by leveraging the event information from developers, which is scattered in different places, such as each DeFi’s official website, document, or source codes. We first develop a tool to collect the descriptions of events or the code snippets and comments of events from the websites of popular DeFi applications listed in DeFiPulse (def, 2021) and Dapp.com (dap, 2019). Then, we manually confirm the results to construct the mapping .

More precisely, if a DeFi application provides documents, we summarize the document template to extract the descriptions of events in its documents. Our tool also checks whether the extracted event indeed exists in the source codes of the DeFi. If a DeFi application does not provide documents, our tool inspects its source code to extract code snippets that define events (i.e., the keyword event representing the start of an event definition, the event’s name, and the definition of the event’s parameters) in Solidity or Vyper, the comments of events, and functions that emit events.

Two authors read the information of extracted events independently to determine whether the events correspond to DeFi actions (Appendix A uses two examples to illustrate how we determine the results.). After analyzing the collected information, they discuss and adjust results with the help of a third author to resolve conflicts for the sake of minimizing the impacts of human subjectivity.

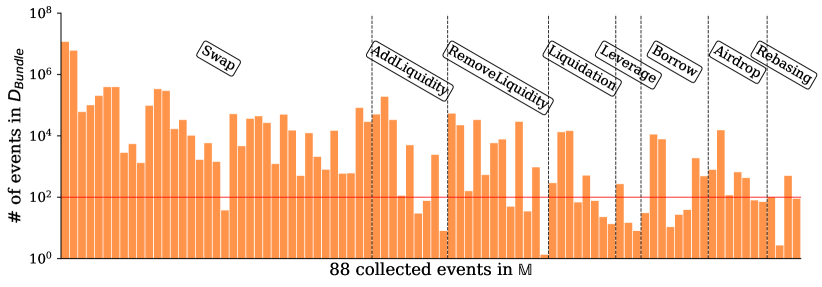

The whole procedure of manual analysis cost around 18 hours. We collect 32 and 56 events from the descriptions of events and the code snippets, and the comments of events, respectively. Specifically, we collect 37, 9, 12, 8, 3, 8, 7, and 4 different events for Swap, AddLiquidity, RemoveLiquidity, Liquidation, Leverage, Borrowing, Airdrop, and Rebasing actions, respectively. Besides, we leverage the standard Transfer event in ERC20 (Fabian and Vitalik, 2015) to recognize NFT-Minting and NFT-Burning actions, since the widely used contract templates for NFT (e.g., OpenZeppelin (Ope, 2018) and chiru-labs (chi, 2018)) emit the Transfer event during NFT minting and burning.

We further investigate the events in to estimate how much manual work we reduce compared to existing studies (Wang et al., 2021; Qin et al., 2022, 2021a; Wang et al., 2022a; Piet et al., 2022; exp, 2021a). To our best knowledge, previous studies conduct three steps to derive rules for recognizing DeFi actions: i) find out specific events that correspond to DeFi actions. ii) summarize how to recognize DeFi actions from the arguments of the events. iii) find out extra information (e.g., other events or storage variables) to assist in recognizing DeFi actions if they fail in the ii) step. For the 88 events in , we find that 41 events can be used to recognize DeFi actions according to the ii) step, and 47 events need extra manual work at the iii) step. Compared to the previous studies, we only need to find out the specific events that correspond to DeFi actions, and obviate the need of the manual efforts for the last two steps.

| Asset transfer type | Conditions |

|---|---|

| Ether transfer | |

| Token transfer | |

| ERC721 token minting | |

| ERC721 token burning |

3.3. Step S-1

Algorithm 1 presents the process of step S-1. Taking in transaction execution trace and , ActLifter first locates the emitted events whose signatures are in . Then, for each event, ActLifter identifies and outputs the information of the corresponding DeFi action, including C, action, and params (A1-10 in §2.1).

More precisely, ActLifter locates all emitted events in the trace (Line 2) by retrieving the signature and parameters of events from the execution state (i.e., Stack and Memory) of the opcodes used to log events, i.e., LOG0-4 (eth, 2021), and only keeps the events whose signatures are in (Line 3 and 4). ActLifter also records the contracts that log these events in the trace (eth, 2021; Chen et al., 2019b; Li et al., 2023; Chen et al., 2019a; He et al., 2023) (Line 5) and obtains the type of the corresponding DeFi actions from (Line 6).

Since param of a DeFi action is summarized from asset transfers involved in the DeFi action, ActLifter tracks asset transfers that are logged by the events through the function GetAssetTransfers (Line 7). These asset transfers will be used to recognize DeFi actions in S-2. We focus on recognizing four kinds of asset transfers described in §2.3, namely Ether transfer, token transfer, and ERC721 token minting/burning. Specifically, Ether can be transferred in two ways: i) the sender is a smart contract and executes the CALL opcode (Wood, 2014) by setting the recipient and the amount of transferred Ether as its parameters in the stack, ii) the sender is an externally-owned account (EOA) (Dannen, 2017) and signs a transaction with setting the recipient and the amount of transferred Ether as its parameters. Moreover, if a token transfer, or an ERC721 token minting/burning occurs, an ERC20 standard Transfer event (Fabian and Vitalik, 2015) will be emitted with the parameters of the sender, the recipient, and the amount of transferred token or the tokenId of minted/burnt ERC721 token, according to the specification of ERC20 standard (Fabian and Vitalik, 2015) and the widely used contract templates for ERC721 (e.g., OpenZeppelin (Ope, 2018) and chiru-labs (chi, 2018)).

|

Asset transfer patterns | |

|---|---|---|

| Swap | ||

| AddLiquidity | ||

| RemoveLiquidity | ||

| Leverage | ||

| Borrowing | ||

| Liquidation | ||

| NFT-Minting | ||

| NFT-Burning | ||

| Airdrop | ||

| Rebasing |

We summarize two conditions (i.e., c1 and c2) for identifying each kind of asset transfer. c1 checks whether an asset transfer occurs, e.g., a sender transfers Ether to a recipient, or a Transfer event is emitted. However, asset transfers, which do not trigger the actual transfer of assets between the sender and the recipient, can pass the check of c1 (e.g., the transferred amount of asset is zero). Thus, we use c2 to filter out such asset transfers. Table 2 lists the four types of asset transfers and their c1 and c2, which are elaborated as follows. Due to the page limit, we describe how we recognize Ether transfers as follows, and introduce the rest in Appendix B.

Ether transfer. In an Ether transfer Asset.Transfer(From, To, Value), From sends Value amount of ETH to To. Hence, c1 checks whether an Ether transfer occurs in any of the two cases: i) From is a contract and executes a CALL to transfer Value amount of Ether to To (i.e., From.CALL(To, Value)), ii) From is an EOA account and signs a transaction to send Value amount of Ether to To (i.e., TX(From, To, Value)). An Ether transfer should also satisfy both requirements in c2: i) From and To are different accounts (i.e., From To), and ii) the transferred amount Value is non-zero (i.e., Value 0). Note that there is no actual transfer of Ether between From and To if any requirement is violated.

For all asset transfers identified from the trace, we check whether they are logged by events (Line 12-14). Specifically, we check whether the event’s parameters contain the asset transfer’s parameters, since an event takes parameters of an asset transfer as its parameters to log the asset transfer. Asset transfers include four parameters, i.e., Asset, From, To, and Value. To check the first three parameters which are of the address type (sol, 2022; Chen et al., 2021; Zhao et al., 2023), we determine whether there are parameters of address type in the event, and values of the parameters are the same as the first three parameters of the asset transfer. The Value parameter denotes the amount of transferred asset, and its type is a 256-bit unsigned integer (Fabian and Vitalik, 2015; Wood, 2014). Since an event can convert Value to another type (e.g., signed integers (sol, 2022)) and use the converted one as its parameter, we also check whether absolute values of parameters in the event are the same as Value’s value.

3.4. Step S-2

Given the information (i.e., the contract that executes a DeFi action, the DeFi action’s type, and asset transfers involved in the DeFi action) collected in S-1, ActLifter determines DeFi actions according to their asset transfer patterns in S-2. Table 3 summarizes asset transfer patterns of ten DeFi actions according to their definitions (Wang et al., 2022a; Bartoletti et al., 2021; Xu et al., 2023; Schär, 2021; Victor, 2020). We explain them and describe how ActLifter leverages patterns to recognize DeFi actions as follows.

Swap. It involves two asset transfers in the transaction, where the C receives x1 amount of asset Asset1, and sends out x2 amount of another asset Asset2.

AddLiquidity/RemoveLiquidity. It involves n asset transfers in the transaction. For each asset transfer, C receives (resp. sends out) a different kind of asset Asseti, whose amount is xi.

Leverage/Borrowing. It involves one asset transfer, where C sends out x1 amount of Asset1.

Liquidation. It involves two asset transfers in the transaction, where the C receives x1 amount of Asset1, and sends out x2 amount of a different asset Asset2.

NFT-Minting/NFT-Burning. It involves an ERC721 token minting (resp. burning), where C mints (resp. burns) an NFT with the tokenId x1.

Airdrop. It involves one asset transfer, where C sends out x1 amount of Asset1.

Rebasing. Since no asset transfer is involved in the Rebasing action, for the contract C that conducts the Rebasing action, we check whether C is an ERC20 or ERC721 token contract.

Algorithm 2 presents the process of S-2. ActLifter takes in a list of C, action, and assetTransfers, and then recognizes the DeFi action (Line 4-11) according to the asset transfer patterns in Table 3. Finally, it outputs the recognized DeFi actions in a transaction (Line 14). Since different kinds of DeFi actions involve different numbers of asset transfers, we divide them into four categories as follows.

First, for AddLiquidity and RemoveLiquidity actions that require n asset transfers, we pick n asset transfers in a greedy fashion from aTs that match the patterns to recognize them (Line 6). Second, for Swap and Liquidation actions that require two asset transfers, we pick the first two asset transfers from aTs that match the patterns to recognize them (Line 8). Third, since Rebasing action does not require asset transfers, for contract C that conducts the Rebasing action, we check whether C implements standard functions defined in ERC20 or ERC721 (Fröwis et al., 2019). Fourth, for the other five DeFi actions that require one asset transfer, we pick the first asset transfer from aTs that matches the patterns to recognize them (Line 12).

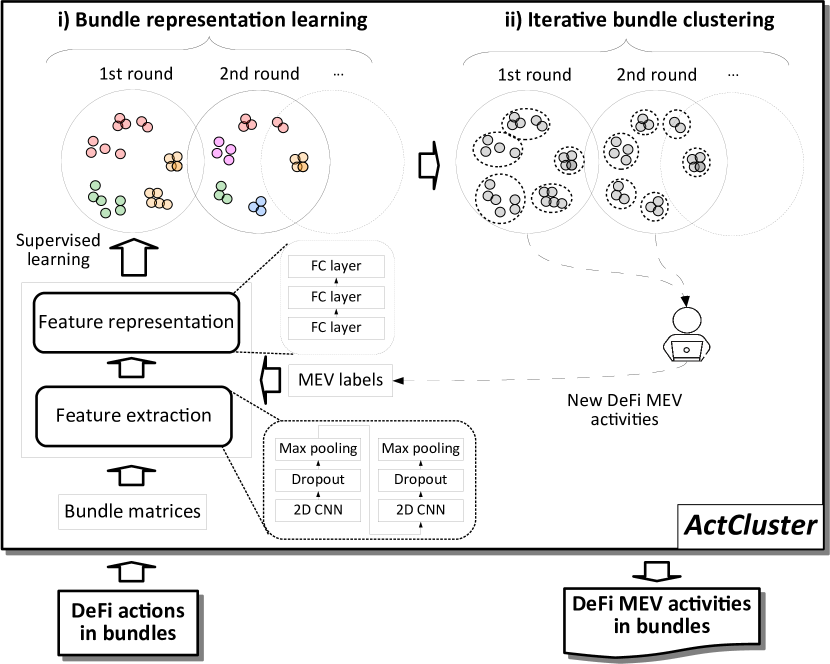

4. ActCluster

ActCluster aims at facilitating analysts to discover DeFi MEV activities in bundles, especially the unknown ones, by analyzing the semantic features involved in the sequences of DeFi actions identified by ActLifter. As shown in Fig. 4, it consists of two steps, i.e., i) bundle representation learning (§4.1), which maps the raw bundles to their feature vectors in a low-dimensional feature space, and ii) iterative bundle clustering (§4.2), which discovers new kinds of DeFi MEV activities via iteratively clustering feature vectors of bundles. We repeat the two steps by conducting representation learning with newly discovered DeFi MEV activities in the first step and conducting the iterative clustering analysis in the second step, until we cannot find new DeFi MEV activities.

The design rationale of ActCluster is fourfold. First, manual efforts in inspecting DeFi actions in bundles are required to discover new DeFi MEV activities. We cluster bundles with similar activities to minimize the manual work. Second, there is a dilemma in the setting of clustering granularity. Specifically, bigger but sparse clusters may mix bundles containing different DeFi MEV activities together, whereas smaller but denser clusters increase manual efforts in inspecting bundles sampled from each cluster. We leverage iterative clustering analysis (Liu et al., 2019) to address the dilemma, i.e., i) it gradually improves the clustering granularity to facilitate the discovery of relatively rare DeFi MEV activities. Besides, ii) it reduces the number of clusters that need to be manually inspected through bundle pruning, which iteratively excludes bundles containing known and discovered DeFi MEV activities from the bundle dataset.

Third, conventional clustering algorithms cannot be directly applied to raw bundles due to bundles’ heterogeneous format and hierarchical data structure. To tackle this problem, we employ representation learning (Bengio et al., 2013) to automatically extract distinguishable features from raw bundles with the knowledge of all known and discovered DeFi MEV activities. Unlike feature engineering, which requires rich domain-specific knowledge, representation learning is fully data-driven and task-oriented, obviating considerable manual efforts for data study. Fourth, in the first round, we conduct the representation learning with three known MEV labels collected from existing studies. Inspired by previous studies (Xie et al., 2021; Zhu et al., 2017) that improve model training’s efficiency and performance by scaling up labels and iteratively training with dynamical label updating, after each round, we extend new DeFi MEV activities to MEV labels and conduct the representation learning to improve its representation capabilities for DeFi MEV activities in bundles.

4.1. Bundle representation learning

We map bundles to low-dimensional feature vectors, based on which the dissimilarity between two bundles can be quantified by the distance between their feature vectors and thus clustering analysis of bundles can be reasonably conducted.

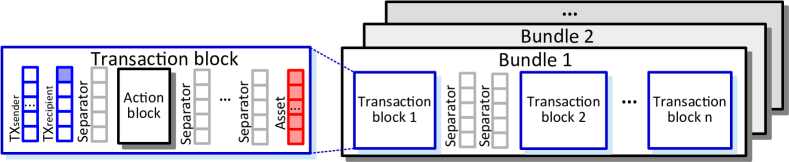

Bundle Formatting. Raw bundles are in a heterogeneous format since a bundle contains a variable number of transactions, each of which contains a variable number of DeFi actions. To facilitate the feature extraction, we express raw bundles in a unified format, i.e., a bundle matrix with a fixed shape, because bundles in the format can be directly processed by convolutional neural network (CNN) (Gu et al., 2018) in an end-to-end fashion. Considering that bundles are organized in a hierarchical structure, we construct a bundle matrix in a bottom-up manner. Specifically, we first standardize the description of DeFi actions as ten types of parameterized action blocks, corresponding to each kind of DeFi action (A1-10 in §2.3). As shown in Fig. 5, each DeFi action in a transaction will be expressed as an action block, acting as a basic element to describe this transaction. Sequentially concatenating action blocks corresponding to all DeFi actions within a transaction yields the transaction block that expresses this transaction. Recall that bundle is essentially a bunch of transactions. We construct the bundle matrix to express a bundle by combining transaction blocks corresponding to all transactions within it. We elaborate more on their constructions in Appendix F.

Feature extraction. We extract features from bundle matrices by taking advantage of a CNN. The reasons for choosing CNN are threefold: i) a bundle can be regarded as a time series because transactions within it are ordered. The temporal patterns involved in a bundle have been characterized as spatial patterns in our matrix representation of bundles. Thus, our task is suitable for CNN, which is known to be effective and efficient in extracting features from spatial patterns (Gu et al., 2018). ii) typical time series analysis models are not suitable for our tasks. First, transactions cannot be represented as tokens as the input of typical models (e.g., Bert and Transformer). Second, transactions consisting of various actions and parameters are difficult to be compactly represented as feature vectors with fixed size as the input of RNN and its variants (e.g., LSTM and GRU) without information loss. iii) CNN processes data in parallel and thus is efficient, e.g., CNN-based models even achieve state-of-the-art performance in traffic analysis tasks (Sirinam et al., 2019), where samples are represented as time series. As shown in Fig. 4, feature extraction is implemented using stacked blocks consisting of a 2D CNN layer, a dropout layer, and a max pooling layer. Such a network structure facilitates feature extraction because i) the 2D CNN layer with learnable kernels automatically captures informative features to construct feature maps, ii) the dropout layer reduces the overfitting risk, and iii) the max pooling layer downsamples feature maps to highlight the most important feature. The input is a bundle matrix, and the outputs are feature maps extracted by the last block.

Feature representation. To represent a bundle in a low-dimensional feature space, we flatten its feature maps obtained via feature extraction and process them with three stacked fully connected (FC) layers. The output of the last fully connected layer is the low-dimensional feature vector of this bundle. Models for feature extraction and feature representation are trained by leveraging supervised learning with the aid of all known MEV labels. Specifically, we construct a multi-label classifier based on multilayer perceptron (MLP) (Ruck et al., 1990) to classify bundles in the feature space. We construct the initial MEV labels by collecting three types of MEV DeFi activities from existing studies (Qin et al., 2022; Wang et al., 2021; Ferreira Torres et al., 2021; Zhou et al., 2021c), i.e., Sandwich Attack, Cyclic Arbitrage, and Liquidation. After we discover new DeFi MEV activities in the clustering analysis of each round, we extend our MEV labels with them. MLP predicts the presence/absence of each label for a bundle. Specifically, 1 (resp. 0) indicates the presence (resp. absence) of a label. We specify the output layer of MLP as a sigmoid layer so that outputs are normalized in the range of (0, 1). We choose Mean Square Error (MSE) loss (Ucar et al., 2021) to quantify the prediction error of MLP. MLP and models for feature extraction and feature representation are jointly trained by minimizing the MSE loss.

4.2. Iterative bundle clustering

Given the feature vectors of bundles, we characterize the dissimilarity between bundles with the distance between their feature vectors to facilitate the discovery of new DeFi MEV activities via bundle clustering. We test five candidate clustering algorithms, including hierarchical clustering (Xu and Wunsch, 2005), DBSCAN (Xu and Wunsch, 2005), K-means (Xu and Wunsch, 2005), Mean Shift (Xu and Wunsch, 2005), and Birch clustering (Xu and Wunsch, 2005), and finally cherry-pick DBSCAN for two reasons. First, it is more efficient than other algorithms in handling large-scale datasets in our problem. Second, DBSCAN does not need a pre-specified number of clusters.

DBSCAN is a density-based clustering algorithm. Its parameter (i.e., the maximum distance between two samples for one to be considered as the other’s neighborhood (Xu and Wunsch, 2005).) adjusts the lower bound of cluster density. A larger leads to bigger but sparse clusters, where bundles corresponding to various DeFi MEV activities may be mixed together. By contrast, a smaller results in smaller but denser clusters, enabling more fine-grained clustering analysis in favor of distinguishing different DeFi MEV activities. However, a side-effect is it substantially increases manual efforts because a smaller yields more clusters and we need to manually inspect them to verify whether they contain unseen DeFi MEV activities. To address the dilemma, we leverage the iterative clustering analysis by conducting the following steps after representation learning in each round until we cannot discover new DeFi MEV activities:

- I. Filter out bundles that only contain DeFi actions that can make up known and discovered DeFi MEV activities.

- II. Group bundles into clusters based on DBSCAN.

- III. Discover new DeFi MEV activities by sampling one bundle from each cluster and manually inspecting them to determine whether their DeFi MEV activities are new. To avoid individual bias, we involve three authors to jointly make a decision, achieving a consensus on whether a DeFi MEV activity is new.

- IV. Reduce the parameter by multiplying it by a decay factor to improve the resolution of clustering analysis.

Note that the number of bundles for clustering analysis decreases in iterations since bundles associated with discovered DeFi MEV activities are gradually filtered out. Besides, we reduce the parameter of DBSCAN in iterations yielding smaller but denser clusters. It enables us to conduct fine-grained clustering analysis for discovering bundles containing unknown DeFi MEV activities.

5. Evaluation

We implement ActLifter and ActCluster in 7,832 lines of Python code, maintain an archive Ethereum node, and conduct experiments on a server with an Intel Xeon W-1290 CPU (3.2 GHz, 10 cores), and 128 GB memory to answer four research questions. RQ1: How is the performance of ActLifter in identifying DeFi actions? RQ2: Does ActLifter outperform existing techniques with respect to identifying DeFi actions? RQ3: How many kinds of new DeFi MEV activities does ActCluster discover? RQ4: Does ActCluster outperform other methods in reducing manual efforts?

5.1. Data collection

Trace collection. We invoke the debug.traceTransaction() (deb, 2013) API of our archive Ethereum node (which is synchronized to the latest state) to get the transaction execution traces for ActLifter.

Bundle collection. Since ActCluster needs the DeFi actions identified by ActLifter in each bundle, we collect bundles and their transactions by querying the web API (fla, 2021a) provided by the Flashbots (fla, 2021b), which displays all bundles and transactions in each bundle mined in Ethereum and relayed by Flashbots. By downloading all bundles from the starting date of bundle mechanism (i.e., Feb. 11, 2021) to Dec. 1, 2022, we collect 6,641,481 bundles and 26,740,394 transactions in total and form a dataset denoted by D.

5.2. RQ1: Performance of ActLifter

In S-1 (§3.3), after locating emitted events in , ActLifter recognizes asset transfers involved in DeFi actions, if the asset transfers are logged by the events. Specifically, if an event’s parameters contain an asset transfer’s parameters, ActLifter confirms that the asset transfer is logged by the event. There are four parameters (i.e., Asset, From, To, and Value) in each asset transfer. Hence, ActLifter can choose a different number of parameters (e.g., the Value parameter or all four parameters) of an asset transfer and determine whether the parameters are in the event’s parameters. We evaluate ActLifter in terms of identifying DeFi actions with the following three configurations and manually determine the number of true positives (TP: a DeFi action is successfully identified), false positives (FP: a non-DeFi action is reported by mistake), and false negatives (FN: a DeFi action is missed) due to the lack of dataset with ground-truth.

-

•

. ActLifter chooses Value of each asset transfer and confirms whether the Value is in the event’s parameters.

-

•

. ActLifter chooses Value and Asset of each asset transfer, and confirms whether they are both in the event’s parameters.

-

•

. ActLifter chooses all four parameters of each asset transfer, and confirms whether they are all in the event’s parameters.

We also compute the precision, recall, and f-score (Olson and Delen, 2008). Since the number of transactions in D is too large ( 10 million), we sample 1,358,122 transactions from D for manual inspection and form a dataset denoted by D. To reduce unnecessary manual efforts and mitigate the potential negative effect of human subjectivity on determining TP/FP/FN, we first de-duplicate transactions having the same execution traces, because ActLifter will output identical results for them. Since the number of transactions after the trace-based de-duplication is still large ( 400,000), we further de-duplicate transactions having the same emitted event sequences (we will evaluate whether such de-duplication will cause errors in the following.). After the event-based de-duplication, 41,090 transactions are left for manual checking. Then, six authors manually check these 41,090 transactions. Once we get the TP/FP/FN results for a transaction, all de-duplicated transactions corresponding to this transaction have the same TP/FP/FN results.

Since manual inspection is labor-intensive and might cause errors, we conduct experiments to evaluate the quality of our TP/FP/FN results. First, we assess the performance of deduplication and provide the confidence level of our results. We randomly sample 1000 de-duplicated transactions from the 41,090 transactions, and find that all 1,000 transactions can be de-duplicated. Note that in relation to the total population ( 1 million), our sample size has a confidence interval of less than 0.27%, with 99.9% confidence. Second, we compute two statistical measures (i.e., Fleiss’ Kappa (Kılıç, 2015) and Krippendorff’s Alpha (Krippendorff, 2011)) to assess whether our TP/FP/FN results from different authors reach a consensus. We randomly sample 500 transactions from the 41,090 transactions, and ask all six authors to report their own results. Then, we compute the Fleiss’ Kappa and Krippendorff’s Alpha to assess the reliability of their manual results. The results are 0.9884 and 0.9948, respectively, showing that six authors come to an almost perfect agreement.

| DeFi action type | Techniques | # Identified | # TP | # FP | # FN | Precision | Recall | F-score |

|---|---|---|---|---|---|---|---|---|

| ActLifterc1 | 2,156,198 | 2,156,198 | 0 | 27,897 | 100% | 98.72% | 99.36% | |

| ActLifterc2 | 102,285 | 102,285 | 0 | 2,081,810 | 100% | 4.68% | 8.95% | |

| Swap | ActLifterc3 | 58,978 | 58,978 | 0 | 2,125,117 | 100% | 2.70% | 5.26% |

| ActLifterc1 | 8,056 | 8,056 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 45 | 45 | 0 | 8011 | 100% | 0.56% | 1.11% | |

| AddLiquidity | ActLifterc3 | 45 | 45 | 0 | 8011 | 100% | 0.56% | 1.11% |

| ActLifterc1 | 6,839 | 6,839 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 1,198 | 1,198 | 0 | 5,641 | 100% | 17,52% | 29.81% | |

| RemoveLiquidity | ActLifterc3 | 1,198 | 1,198 | 0 | 5,641 | 100% | 17.52% | 29.81% |

| ActLifterc1 | 1,635 | 1,635 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 496 | 496 | 0 | 1,139 | 100% | 30.34% | 46.56% | |

| Liquidation | ActLifterc3 | 496 | 496 | 0 | 1,139 | 100% | 30.34% | 46.55% |

| ActLifterc1 | 16,795 | 16,795 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 16,795 | 16,795 | 0 | 0 | 100% | 100% | 100% | |

| NFT-Minting | ActLifterc3 | 16,795 | 16,795 | 0 | 0 | 100% | 100% | 100% |

| ActLifterc1 | 1,308 | 1,308 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 1,308 | 1,308 | 0 | 0 | 100% | 100% | 100% | |

| NFT-Burning | ActLifterc3 | 1,308 | 1,308 | 0 | 0 | 100% | 100% | 100% |

| ActLifterc1 | 34 | 34 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 33 | 33 | 0 | 1 | 100% | 97.06% | 98.51% | |

| Leverage | ActLifterc3 | 33 | 33 | 0 | 1 | 100% | 97.06% | 98.51% |

| ActLifterc1 | 684 | 684 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 191 | 191 | 0 | 493 | 100% | 27.92% | 43.66% | |

| Borrowing | ActLifterc3 | 191 | 191 | 0 | 493 | 100% | 27.92% | 43.66% |

| ActLifterc1 | 246 | 246 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 40 | 40 | 0 | 206 | 100% | 16.26% | 27.97% | |

| Airdrop | ActLifterc3 | 40 | 40 | 0 | 206 | 100% | 16.26% | 27.97% |

| ActLifterc1 | 15 | 15 | 0 | 0 | 100% | 100% | 100% | |

| ActLifterc2 | 15 | 15 | 0 | 0 | 100% | 100% | 100% | |

| Rebasing | ActLifterc3 | 15 | 15 | 0 | 0 | 100% | 100% | 100% |

| Total | ActLifterc1 | 2,191,810 | 2,191,810 | 0 | 27,897 | 100% | 98.74% | 99.37% |

| ActLifterc2 | 122,406 | 122,406 | 0 | 2,097,301 | 100% | 5.51% | 10.45% | |

| ActLifterc3 | 79,099 | 79,099 | 0 | 2,140,608 | 100% | 3.56% | 6.88% |

Table 4 shows the performance of ActLifter in identifying ten DeFi actions with different configurations. The third column lists the number of identified DeFi actions for each DeFi action. The fourth - ninth columns list the number of TPs, FPs, and FNs, and the values of precision, recall, and f-score for each DeFi action. It shows that ActLifterc1 (i.e., ActLifter with the configuration) can effectively identify DeFi actions with nearly 100% precision and recall. However, ActLifterc1 misses 27,897 Swap actions. Manual investigation reveals that traders can receive assets from AMMs at zero cost, hence there is only one asset transfer in the transaction. Since ActLifter identifies a Swap action by matching two asset transfers (§3.4), ActLifterc1 cannot recognize the two asset transfers in transactions, and misses identifying the 27,897 Swap actions in S-2 (§3.4). Such cases count for only 1.26% (27,897/(27,897+2,191,810)) of all DeFi actions, and ActLifterc1 can achieve a 98.74% recall rate. Fig. 6 shows an example, where trader 0x777d invokes swap() of AMM 0xe967 (i.e., an AMM which supports asset exchanges between MCC and WETH tokens) in \raisebox{-.9pt} {1}⃝ in a transaction. Then AMM 0xe967 is aware of a difference of MCC between AMM 0xe967’s token balance and AMM 0xe967’s reserve variables of MCC. Please note that AMM 0xe967’s reserve variables of MCC are stored in AMM 0xe967’s contract with aiming of recording AMM 0xe967’s token balance of MCC. AMM 0xe967 considers that the difference of MCC is transferred by trader 0x777d, and trader 0x777d aims to buy WETH. Hence, AMM 0xe967 transfers WETH to trader 0x777d in \raisebox{-.9pt} {2}⃝ and emits a Swap event in \raisebox{-.9pt} {3}⃝. Since there is only one asset transfer in the transaction, ActLifterc1 considers there is no Swap action.

Unfortunately, ActLifterc2 and ActLifterc3 can only achieve 5.51% and 3.56% recall rates. Manual investigation reveals two reasons for FNs. First, for the 27,897 Swap actions missed by ActLifterc1, both ActLifterc2 and ActLifterc3 also missed the 27,897 Swap actions by the same reason. Second, ActLifterc2 and ActLifterc3 missed recognizing 2,069,419 and 2,112,711 DeFi actions, because, due to the configurations of and , the asset transfers for identifying DeFi actions are filtered out. For the example in Fig. 3, ActLifterc2 and ActLifterc3 filter out the two asset transfers in \raisebox{-.9pt} {2}⃝ and \raisebox{-.9pt} {3}⃝, because only the Value parameters of the two asset transfers (i.e., 14,082.22 and 500,187) are logged by the Swap(500,187, 14,082.22) event in \raisebox{-.9pt} {4}⃝. Hence, ActLifterc2 and ActLifterc3 can not identify the corresponding DeFi action, which is matched by the two asset transfers in \raisebox{-.9pt} {2}⃝ and \raisebox{-.9pt} {3}⃝. By contrast, ActLifterc1 can recognize asset transfers involved in DeFi actions (e.g., the two asset transfers in \raisebox{-.9pt} {2}⃝ and \raisebox{-.9pt} {3}⃝), and hence it can identify the corresponding DeFi actions. Since ActLifter with the configuration achieves nearly 100% accuracy and significantly outperforms ActLifter under the other two configurations, i.e, ActLifterc2 and ActLifterc3, we run ActLifter with the configuration for other experiments.

Insight. When DeFi developers emit events to announce DeFi actions, we find that most of them only publish the amount of transferred assets involved in DeFi actions without other parameters of asset transfers (e.g., the type of asset). It may lead to potential risks for traders in interacting with DeFis, because the same events may be triggered by DeFi actions involving different kinds of assets and thus traders will get confused or abused by adversaries.

Answer to RQ1: ActLifter can achieve nearly 100% precision and recall in identifying ten kinds of DeFi actions.

5.3. RQ2: Is ActLifter superior to others?

We compare ActLifter with three baseline methods, including two state-of-the-art techniques (i.e., Etherscan (eth, 2015) and DeFiRanger (Wu et al., 2021)), and EventLifter, a tool we developed for recognizing DeFi actions from events’ arguments, because, as mentioned in §3.2, we find 41 events whose arguments can be leveraged to recognize DeFi actions. We compare their performance in terms of identifying DeFi actions for transactions in D. Since Etherscan does not release DeFi action results in its APIs, we queried their transaction pages to obtain DeFi action results. Since DeFiRanger is also not available (Wu et al., 2021), we re-implemented its DeFi action identification approach. Note that DeFiRanger (Wu et al., 2021) only identifies AddLiquidity and RemoveLiquidity actions that supply and withdraw single asset with AMMs. For example, if an AddLiquidity action supplies two assets Asset1 and Asset2 to an AMM, DeFiRanger will identify two AddLiquidity actions that supply Asset1 and Asset2 to the AMM, respectively. We still consider that DeFiRanger identifies the true results, if their results can be combined into the true DeFi actions.

| DeFi action type | Techniques | # Identified | # TP | # FP | # FN | Precision | Recall | F-score |

|---|---|---|---|---|---|---|---|---|

| Etherscan | 1,983,869 | 1,983,869 | 0 | 200,226 | 100% | 90.83% | 95.20% | |

| DeFiRanger | 1,760,236 | 1,356,586 | 403,650 | 827,509 | 77.07% | 62.11% | 68.79% | |

| Swap | EventLifter | 102,285 | 102,285 | 0 | 2,081,810 | 100% | 4.68% | 9.16% |

| Etherscan | 4,964 | 4,964 | 0 | 3,092 | 100% | 61.62% | 76.25% | |

| DeFiRanger | 24,234 | 4,116 | 20,118 | 7,237 | 16.98% | 36.25% | 23.13% | |

| AddLiquidity | EventLifter | 45 | 45 | 0 | 8,011 | 100% | 0.56% | 1.11% |

| Etherscan | 2,629 | 2,629 | 0 | 4,210 | 100% | 38.44% | 55.53% | |

| DeFiRanger | 12,289 | 1,143 | 11,146 | 8,270 | 9.3% | 12.14% | 10.53% | |

| RemoveLiquidity | EventLifter | 1,198 | 1,198 | 0 | 5,641 | 100% | 17.52% | 29.81% |

| Etherscan | 527 | 527 | 0 | 1,108 | 100% | 32.23% | 48.75% | |

| DeFiRanger | - | - | - | - | - | - | - | |

| Liquidation | EventLifter | 496 | 496 | 0 | 1,139 | 100% | 30.34% | 46.55% |

| Etherscan | 12,532 | 12,532 | 0 | 4,263 | 100% | 74.62% | 85.46% | |

| DeFiRanger | - | - | - | - | - | - | - | |

| NFT-Minting | EventLifter | - | - | - | - | - | - | - |

| Etherscan | 1,190 | 1,190 | 0 | 118 | 100% | 90.98% | 95.28% | |

| DeFiRanger | - | - | - | - | - | - | - | |

| NFT-Burning | EventLifter | - | - | - | - | - | - | - |

| Etherscan | - | - | - | - | - | - | - | |

| DeFiRanger | - | - | - | - | - | - | - | |

| Leverage | EventLifter | 33 | 33 | 0 | 1 | 100% | 97.06% | 98.51% |

| Etherscan | 141 | 141 | 0 | 543 | 100% | 20.61% | 34.18% | |

| DeFiRanger | - | - | - | - | - | - | - | |

| Borrowing | EventLifter | 191 | 191 | 0 | 493 | 100% | 27.92% | 43.66% |

| Etherscan | - | - | - | - | - | - | - | |

| DeFiRanger | - | - | - | - | - | - | - | |

| Airdrop | EventLifter | 40 | 40 | 0 | 206 | 100% | 16.26% | 27.97% |

| Etherscan | - | - | - | - | - | - | - | |

| DeFiRanger | - | - | - | - | - | - | - | |

| Rebasing | EventLifter | 15 | 15 | 0 | 0 | 100% | 100% | 100% |

| Total | Etherscan | 2,005,852 | 2,005,852 | 0 | 213,560 | 100% | 90.38% | 94.95% |

| DeFiRanger | 1,796,759 | 1,361,845 | 434,914 | 843,016 | 75.79% | 61.77% | 68.06% | |

| EventLifter | 104,303 | 104,303 | 0 | 2,097,301 | 100% | 4.74% | 9.05% |

Table 5 shows the results of Etherscan, DeFiRanger, and EventLifter. The third - ninth columns list the number of identified DeFi actions, TPs, FPs, and FNs, and the values of precision, recall, and f-score for different kinds of DeFi actions. We next present reasons why three baseline techniques generate FP and FN cases.

Etherscan. Etherscan achieved 100% precision for the identification of 7 kinds of DeFi actions but generated incomplete results. For example, Etherscan missed identifying a Swap action in the transaction (exp, 2021b), where the trader exchanges COMP for WETH with the AMM 0xba12. Both ActLifter and DeFiRanger can correctly identify this Swap action. Since Etherscan does not disclose how they identify DeFi actions, we cannot know why Etherscan failed.

DeFiRanger. DeFiRanger led to both incomplete and inaccurate results in identifying three kinds of actions. The root causes are twofold: i) DeFiRanger identifies DeFi actions by matching ERC20 token transfers (Wu et al., 2021), and thus it cannot identify DeFi actions involving Ether transfers. ii) Heuristics, defined by DeFiRanger (Wu et al., 2021), are inaccurate. For example, DeFiRanger identifies Swap actions by only matching the first two token transfers, and in the two matched token transfers one account receives and sends out different assets. However, token transfers, which are irrelevant to DeFi actions, can also satisfy these heuristics. Hence, DeFiRanger will wrongly match the irrelevant token transfers and report wrong DeFi actions. For the example in Fig. 3, DeFiRanger identifies an incorrect Swap action by matching two irrelevant token transfers in \raisebox{-.9pt} {1}⃝ and \raisebox{-.9pt} {5}⃝.

EventLifter. EventLifter only achieved 4.74% recall rate and missed identifying 2,097,316 DeFi actions. It shows that the 41 kinds of events only count for a small proportion (i.e., 4.74%) of all emitted events whose signatures are in .

Answer to RQ2: ActLifter can significantly outperform the state-of-the-art techniques, other baseline methods, and two variants of ActLifter in identifying DeFi actions.

5.4. RQ3: DeFi MEV activities discovery

The representation learning of ActCluster leverages three initial MEV labels, i.e., Sandwich Attack, Cyclic Arbitrage, and Liquidation, to map each bundle matrix to the low-dimensional feature space in the first round (§4.1). We generate the initial MEV labels for each bundle in D by using heuristics from Qin et al. (Qin et al., 2022). As a result, 813,188, 1,334,207, and 14,263 bundles are labeled as Sandwich Attack, Cyclic Arbitrage, and Liquidation, respectively. Besides, two parameters are used in iterative bundle clustering (§4.2) of ActCluster, i.e., , which is used to adjust the lower bound of cluster density in DBSCAN (Xu and Wunsch, 2005), and , which is the delay factor of . The values of and are selected by grid search (Wang et al., 2015) with the target of minimizing required manual efforts (i.e., the amount of bundles manually inspected) to discover MEV activities. Specifically, we first make a set of candidate values for and , and then perform the iterative bundle clustering (§4.2) with each pair of parameters on a small set of (i.e., 5,000) bundles in D. Finally, we compare the amount of bundles manually inspected in iterative bundle clustering (§4.2), and determine 16 and 0.5 for and , respectively.

We train on all our data (i.e., 6,641,481 bundles in D) with MEV labels. After each round in ActCluster, we add the newly discovered MEV activities into the MEV labels, and conduct the representation learning (§4.1) of the next round with the extended MEV labels. After repeating the steps of ActCluster (§4) four rounds and analyzing 2,035 bundles manually, we discover 17 new kinds of DeFi MEV activities summarized in Table 6. We describe one as follows, and introduce the rest in Appendix E.

| DeFi MEV activity | Description | ||

|---|---|---|---|

| Swap Backrun Arbitrage |

|

||

| Liquidity Backrun Arbitrage |

|

||

| Liquidity Sandwich Arbitrage |

|

||

| Multi-layered Burger Arbitrage |

|

||

| Liquidity-swap Trade |

|

||

| Partial Cyclic Arbitrage |

|

||

| Backrun Cyclic Arbitrage |

|

||

| Hybrid Arbitrage |

|

||

| Failed Arbitrage |

|

||

| Non-cyclic Swap Trade |

|

||

| Rebasing Backrun Arbitrage |

|

||

| Airdrop-swap Trade |

|

||

| Bulk NFT-Minting |

|

||

| NFT Reforging |

|

||

| Airdrop Claiming |

|

||

| NFT-Minting-swap Trade |

|

||

| Loan-powered Arbitrage |

|

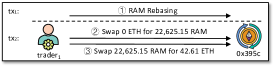

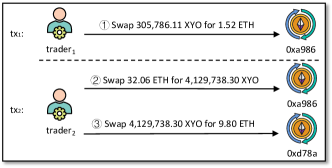

Rebasing Backrun Arbitrage (RBA). It involves two transactions in a bundle. The former executes a Rebasing action, which causes a difference between the AMM’s Rebase token balance and the AMM’s reserve variables. The Rebase token balance is stored in the contract of Rebase token, and the reserve variables are stored in the contract of AMM with recording the AMM’s Rebase token balance. The latter executes a Swap action to trade the Rebase token and obtains profits from the difference of Rebase token. For example, Fig. 7 shows the two transactions in the first bundle of the 12,147,015 block. In the first transaction, the RAM token executes a Rebasing action, and it causes the RAM token balance of the AMM 0x395c to increase by 22,625.15. However, the AMM 0x395c still uses its old RAM token balance (i.e., the reserve variables) before the Rebasing action to calculate how much the traders should pay (Adams et al., 2020). In the second transaction, after giving the trader the 22,625.15 RAM, the AMM 0x395c finds its RAM token balance does not decrease. Hence, the trader1 does not need to pay for ETH. The trader1 then swaps the 22,625.15 RAM for 42.61 ETH to earn profits of 42.61 ETH.

We also evaluate whether our results can generalize to new MEV activities. We first train our model on a small set of (i.e., 20,000) bundles in D, and then evaluate our trained model on different validation sets (Noroozi et al., 2017) (i.e., other bundle sets randomly sampled from D). It shows that our trained model achieves similar accuracy (difference ¡ 5% ) in classifying MEV labels on different validation sets. It means that our model could generalize to different sets of bundles. As new DeFi MEV activities can cause concept drift (Gama et al., 2014) in bundles (an open problem in machine learning) and might affect the accuracy of our model, Users can retrain (Gama et al., 2014) our model with new MEV activities. We evaluated the retraining cost of our model, and the result shows that it is reasonable (Appendix J).

Answer to RQ3: ActCluster empowers us to discover 17 new kinds of DeFi MEV activities in bundles. Besides, our results can generalize to new types of DeFi MEV activities.

5.5. RQ4: Is ActCluster superior to others?

To evaluate how much manual effort can be reduced by ActCluster. We compare it with three baseline strategies. It is worth noting that the three baseline strategies are selected with ablating components of ActCluster. Hence, by comparing with the three baseline strategies, we can also evaluate to which extent the components of ActCluster benefit the procedure of MEV activity discovery.

ActCluster-. It ablates the updating of labels of newly discovered MEV activities in model training of bundle representation learning (§4.1). We only conduct the representation learning (§4.1) with the initial three MEV labels (§4.1), and conduct the iterative clustering analysis by repeating the same four steps in §4.2, until we find all 17 DeFi MEV activities.

Intuitive clustering analysis. It ablates both the iterative bundle clustering (§4.2), and the updating of labels of newly discovered MEV activities in model training of bundle representation learning (§4.1). We apply the DBSCAN algorithm to all bundles in D once to find different kinds of DeFi MEV activities. Then, we sample one bundle from each cluster, and determine whether it contains new DeFi MEV activities. Since we aim to compare ActCluster with the best performance of the intuitive clustering analysis, we adjust the parameter of the DBSCAN clustering algorithm to find all 17 kinds of DeFi MEV activities.

Random sampling analysis. It ablates the whole process of ActCluster. We sample one bundle from D randomly, and determine whether it contains discovered DeFi MEV activities. If that is the case, we exclude all bundles containing the corresponding DeFi MEV activities from D. Note that the excluded bundles only contain DeFi actions that can form the corresponding DeFi MEV activities. We repeat the random sampling analysis until we find all 17 kinds of new DeFi MEV activities.

For each strategy, we record the number of bundles to be inspected for discovering all 17 kinds of new DeFi MEV activities. Our experimental results show that ActCluster-, intuitive clustering analysis, and random sampling analysis, require us to manually analyze 2,874, 108,962, and 176,255 bundles, respectively. Compared to them, ActCluster can reduce 29.2%, 98.1% and 98.8% of manual efforts for discovering DeFi MEV activities, respectively.

Answer to RQ4: ActCluster outperforms three baseline strategies in reducing manual efforts during discovering DeFi MEV activities.

6. Applications of our approach

We use three applications to demonstrate usages of our approach (i.e., ActLifter and ActCluster), including enhancing relays’ MEV countermeasures (§6.1), evaluating forking and reorg risks caused by MEV activities in bundles (§6.2), and evaluating the impact of MEV activities in bundles on blockchain users’ economic security (§6.3). Moreover, we discuss three feasible usages of our approach, supported by experimental results and observations (§6.4).

6.1. Enhancing MEV countermeasures in relays

As the most popular platforms implementing MEV countermeasures in practice (Yang et al., 2022), relays that distribute bundles to miners/validators can filter out bundles including known MEV activities (mev, 2022a) (e.g., relays (blo, 2021; MEV, 2023) block sandwich attacks). However, these relays (blo, 2021; MEV, 2023) rely on handcrafted heuristics (mev, 2021) to detect and filter out the bundles containing known MEV activities. Hence, these relays can fail to counter bundles only containing unknown MEV activities because these bundles can fail heuristics of these relays. We develop a tool named MEVHunter based on our approach to enhance relays to counter bundles containing new MEV activities. Specifically, MEVHunter takes in a bundle of transactions as input, and identifies the kinds of MEV activities (including known and our newly discovered MEV activities) exist in the bundle. For each transaction in the bundle, MEVHunter utilizes ActLifter to recognize DeFi actions in it. Besides, for each kind of MEV activity discovered by ActCluster, we summarize heuristics to identify it like others (Qin et al., 2022; Ferreira Torres et al., 2021; Weintraub et al., 2022). For each kind of MEV activity, the heuristics describe DeFi actions that a bundle arbitrageur has to perform to accomplish the corresponding MEV activity. By checking whether the DeFi actions in the bundle satisfy our summarized heuristics, MEVHunter identifies MEV activities in the bundle.

To evaluate how MEVHunter enhance MEV countermeasures in relays, we use it to inspect MEV activities for all bundles in D. The experimental results show that 31.81% (2,112,344/6,641,481) bundles contain known MEV activities (i.e., Sandwich Attach, Cyclic Arbitrage, and Liquidation), and 53.12% (3,527,655/6,641,481) bundles contain our newly discovered DeFi MEV activities. Among the 3,527,655 bundles, 3,182,363 bundles only contain new DeFi MEV activities. The experimental results indicate that, MEVHunter can enhance relays to additionally identify 3,182,363 (47.92%) bundles only containing the 17 kinds of new MEV activities. We further investigate new MEV activities in bundles, e.g., the number of contracts directly invoked by the EOA account to perform new MEV activities. Our empirical results show that new MEV activities are commonly used in bundles (cf. Appendix G for details).

Summary: Our approach can enhance MEV countermeasures in relays to discover more MEV activities in bundles, and filter out more bundles (relayed by them) containing MEV activities.

6.2. Evaluating forking and reorg risks caused by bundle MEV activities

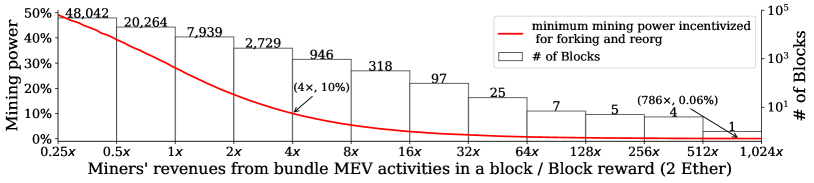

Prior studies (Daian et al., 2020; Qin et al., 2022; Liu et al., 2022; Zhou et al., 2021b) report that financially rational miners are incentivized to deliberately fork and reorganize the blockchain to gather revenues from MEV activities. Hence, we evaluate forking and reorg risks in blockchain consensus security caused by known and new MEV activities in bundles (i.e., bundle MEV activities) by measuring how many revenues miners can gather from bundle MEV activities. Our methodology for determining miners’ revenues from known and new MEV activities in bundles in D involves two steps. First, we recognize bundles containing known and new MEV activities by using MEVHunter as discussed in §6.1. Second, following methods in (Liu et al., 2022), we determine miners’ revenues from bundle MEV activities by using miners’ revenues from corresponding bundles. Miners’ revenues from bundles consist of two parts: i) gas fees for transactions in bundles, and ii) Ether transfers to miners in bundles (both of them are publicly available through the web API (fla, 2021a)). To facilitate analysis, we combine miners’ revenues from bundle MEV activities per block, and form a dataset denoted by D, because miners’ revenues from bundle MEV activities contained in the same block will cumulatively incentivize miners to fork and reorganize the blockchain. As a result, miners receive revenues from bundle MEV activities in 1,791,891 blocks. In block 14,953,916, miners received the highest revenues from bundle MEV activities as 1,584.4 Ether (792.2 times the block reward).

To further investigate how bundle MEV activities incentivize miners to fork and reorganize the blockchain, by adapting the MDP framework (Qin et al., 2022), we quantify the minimum mining power of miners incentivized to fork and reorganize the blockchain for gathering revenues in D. Specifically, the MDP framework employs a Markov Decision Process (Zhou et al., 2021b) for miners to identify whether to fork and reorganize the blockchain or not, with a given mining power on various revenues. The results are shown in Fig. 8, where each point (x, y) in the red line indicates that, miners’ revenues from bundle MEV activities in a block (which are x times the block reward) will incentive miners with no less than y mining power to fork and reorganize the blockchain for gathering the revenues. Besides, in Fig. 8, we display the distribution of miners’ revenues from bundle MEV activities in blocks in D with binning in twelve intervals. Fig. 8 shows that 1,403 blocks incentivize miners with no less than 10% mining power to fork and reorganize the blockchain. Moreover, the miners’ revenues from bundle MEV activities in block 14,953,916 can incentivize a miner with only 0.06% mining power to fork and reorganize the blockchain, highlighting the severe of forking and reorg risks caused by MEV activities in bundles.

Ethereum changed its consensus mechanism from PoW to PoS in September 2022 (eth, 2022), and the new PoS consensus mechanism is under the forking and reorg risks undertaken by validators (D’Amato et al., 2022). Besides, several studies (Neu et al., 2022; Neuder et al., 2021) propose various attacks to decrease the cost for launching forking and reorg for Ethereum blockchain. Considering that validators collect the same revenues from bundle MEV activities as miners (fla, 2021b; mev, 2022b), we believe that bundle MEV activities still endanger the consensus security in the context of PoS by incentivizing validators to fork and reorganize the blockchain.

Summary: Bundle MEV activities endanger the consensus security by incentivizing miners/validators to fork and reorganize the blockchain for gathering revenues from bundle MEV activities.

6.3. Evaluating impact of bundle MEV activities on blockchain users’ economic security

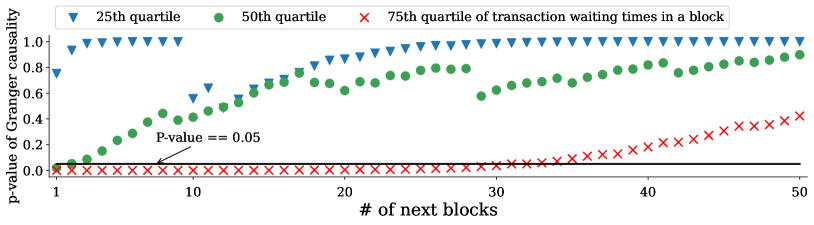

To explore the impact of bundle MEV activities on blockchain users’ economic security, we use the Granger causality test (Toda and Yamamoto, 1995; Faes et al., 2017) to examine the range of later blocks in which users’ transactions are delayed due to bundle MEV activities in prior blocks. In the context of PoW, delayed waiting time is one of the major economic security issues for users caused by MEV activities (Qin et al., 2022; Liu et al., 2022). For instance, it prolongs users’ transactions to be exposed to arbitrageurs, thereby enhancing arbitrageurs to design and engage in more profitable MEV activities (e.g., Sandwich Attack and Cyclic Arbitrage). The Granger causality test is a statistical hypothesis test to determine whether the changes in one time series cause changes in another time series, and it is widely employed in the fields of economics, political science, and epidemiology (Toda and Yamamoto, 1995; Faes et al., 2017). We capture the two parts of data examined for our Granger causality test in the following.

Transaction waiting times. We define the waiting time of a transaction as the duration that the transaction remains in mempools of miners/validators before being submitted to blockchain. To capture transaction waiting times, we utilize the three-month waiting time dataset (from Jul. 20, 2021 to Oct. 27, 2021) released by (Liu et al., 2022). Additionally, we obtained a nine-day waiting time dataset for transactions from Mar. 14, 2023 to Mar. 22, 2023 by implementing the same methods as (Liu et al., 2022) (cf. Appendix K for details). We use median values of transaction waiting times in each block to account for the variation of transaction waiting times in blocks, which is more tolerant of outliers than the mean and standard deviation (Liu et al., 2022). Finally, we combine waiting times from two time periods to form a new dataset denoted by D, which includes the 25th, 50th, and 75th quartiles of waiting times per block (where the 25th, 50th, and 75th quartiles of waiting times are sorted in ascending order).

Extractable value. Following the methods in (Liu et al., 2022), we estimate the extractable value of bundle MEV activities by using revenues of miners/validators from bundle MEV activities (§6.2). It benefits us in estimating the extractable value of bundle MEV activities even if assets in MEV activities do not have price information for calculating the extractable value (Liu et al., 2022; Qin et al., 2022). Please note that D includes waiting times for two periods. For the first period (i.e., from Jul. 20, 2021 to Oct. 27, 2021), we obtain the extractable value of bundle MEV activities in blocks by using corresponding results in D (§6.2). Moreover, to obtain the extractable value of bundle MEV activities in blocks for the second period (i.e., from Mar. 14, 2023 to Mar. 22, 2023), we first capture bundles from the web API (fla, 2021a), and then use the methods in §6.2 to obtain the extractable value of bundle MEV activities in blocks. Finally, we combine two parts of results to form a new dataset denoted by D.