GMM-lev estimation and individual heterogeneity: Monte Carlo evidence and empirical applications††thanks: We are grateful to the participants at the International Panel Data Conference for their helpful comments. Special thanks to Alok Bhargava, Maurice Bun, Jacques Mairesse, Patrick Sevestre. We thank Annapaola Zenato for her initial help with the research.

Abstract

We introduce a new estimator, CRE-GMM, which exploits the correlated random effects (CRE) approach within the generalised method of moments (GMM), specifically applied to level equations, GMM-lev. It has the advantage of estimating the effect of measurable time-invariant covariates using all available information. This is not possible with GMM-dif, applied to the equations of each period transformed into first differences, while GMM-sys uses little information as it adds the equation in levels for only one period. The GMM-lev, by implying a two-component error term containing individual heterogeneity and shock, exposes the explanatory variables to possible double endogeneity. For example, the estimation of actual persistence could suffer from bias if instruments were correlated with the unit-specific error component. The CRE-GMM deals with double endogeneity, captures initial conditions and enhance inference. Monte Carlo simulations for different panel types and under different double endogeneity assumptions show the advantage of our approach. The empirical applications on production and R&D contribute to clarify the advantages of using CRE-GMM.

Keywords: Dynamic Panel Data Models; GMM-lev; Individual heterogeneity. Correlated Random Effects.

JEL classification: C13, C15, C23, D20, O30

1 Introduction

The generalized method of moments (GMM) is widely used in applied economic research to estimate linear dynamic panel data models, mainly as GMM-dif (model in first differences instrumented by lagged levels, [11]) and GMM-sys (which adds model in levels to the model in first differences and uses lagged first differences to instrument, [12, 25]).

We investigate the effect of exploiting uniquely the model in levels explicitly combined with the [73]’s idea of "Correlated Random Effects" (CRE) in a unified framework. Our approach addresses unobserved heterogeneity and dynamic panel estimation simultaneously. Instruments will be defined as lagged first differences or levels according to the presence or absence of correlation between the explanatory variables and individual heterogeneity; lags’ selection will depend on the classification of the explanatory variables as exogenous, predetermined and endogenous in terms of correlation with the idiosyncratic shock. We show that the [73]’s approach is useful to handle this “double” endogeneity of the explanatory variables arising from two sources. The first source of endogeneity (endogeneity because of heterogeneity) emerges from the correlation between the covariates and unobservable individual-specific characteristics, while the second source (standard endogeneity) depends on the correlation of the covariates with the idiosyncratic shocks. Hence, we propose the Correlated Random Effects generalized method of moments on levels, the CRE-GMM estimation, which combines two methods to deal with both unobserved individual-specific effects (handled by the [73]’s approach) and dynamic panel data model estimation challenges (handled by the GMM-lev method). We consider alternative settings: macro panels (small N and long T, for example N=25 and T=40), multilevel panels (the number of groups is high relative to the number of observations per group, for example N=100 and T=20), and longitudinal panels (N greatly larger than T, for example, N=1000 and T=10).

The first aim of our CRE-GMM method is to maintain the levels of the equation of interest as they allow for estimating the effects of measurable time-invariant explanatory variables while considering the role of unmeasurable individual heterogeneity. Indeed, time invariant variables are lost when first differencing the data. For example, on macro panels, we cannot estimate the effects on emissions of measurable institutional features driving time-invariant heterogeneity while controlling for country-specific unobserved heterogeneity with first differences to avoid omitted variable bias [42]. [63] discusses the interpretations and identification of within-unit and cross-sectional variation in panel data models and shows that using only within variation, as in [2], leads to incorrect conclusions about null effects of democracy on GDP. On longitudinal panels we cannot study innovative investments as a function of measurable individual characteristics (e.g., size, sector, market power) that are of great interest to researchers. To obtain unbiased effects, it is necessary to consider unobservable factors like management quality, ownership motivation, and cost of capital (further discussion is [39]). In fields like education, psychologyl, sociology, and political science, standard approaches involve multilevel, multidimensional, or hierarchical models. While the fixed effects specification controls for correlations between lower-level predictors and higher-level residuals through within or first-differencing transformations, it cannot estimate the effects of higher-level, time-invariant, variables (time-invariant variables). Unfortunately, this approach models out higher-level variables, rendering any correlations with covariates irrelevant, and it does not address the source of endogeneity, which can itself be of interest [38, 35, 52, 55]. A recent discussion from the economic perspective is in [69, 98].

Our second research aim tackles a common challenge in applied empirical studies. When using the GMM-lev estimator for dynamic panel data models, we often observe a high estimated autoregressive parameter, akin to the upward-biased pooled OLS estimation, ignoring individual heterogeneity. This implies that neglecting or failing to capture individual heterogeneity results in a mix of “spurious” persistence (due to unobserved unit-specific permanent characteristics) and “true" persistence (causal effect of past realizations on the current realization of the dependent variable) [51, 78, 19]. An illustrative example from innovation literature highlights the difficulty of estimating the causal effect of past R&D activities on current R&D investment due to the path-dependent nature of technical changes [14]. Spurious persistence, a product of uncontrolled individual heterogeneity, significantly impacts the innovation process [80].

An important issue in the estimation of level dynamic panel data models with unit-effects is whether it is possible to remove the unobservable individual heterogeneity from the model, or from the regressors, or from any variable that may be used as an instrument [57]. Our CRE-GMM approach explicitly extends the estimated equation of interest to capture the initial endowment of each unit which is measured by pre-sample realisations of the variables of the model. Hence, it is able to deal with a mix of units whose differences are not captured uniquely by the initial observation of the dependent variable, but by a set of observations of the variables concurring to the dynamic process.

In our extended level regressions, we treat individual heterogeneity as random. In the words of [75], while fixed effects models may be appropriate in cases in which a population is sampled exhaustively (e.g., data from geographic regions over time) or in which it is desired to predict individual behaviour (e.g., the probability that a given individual in a sample will default on a loan), random effects models are more consistent with [41]’s view that the “population” consists of an infinity of decisions made by individuals who are different from each other and who may change their behaviours over time.

Our approach can be related to the static model using an instrumental variables approach to deal with endogeneity due to the correlation of the individual heterogeneity with some of time-varying and time-invariant explanatory variables [46]. [62] extend [46] to dynamic models by proposing a two-stage GMM estimation in which at the first stage a GMM-dif is used to estimate the role of time-varying covariates, while at the second stage a GMM-lev can be used to estimate the effects of measurable time-invariant covariates. In both approaches, all the explanatory variables are assumed to be strictly exogenous with respect to the idiosyncratic error term. [12] consider a dynamic panel data model with individual effects assumed to be random and equations in levels. [84] extend the correlated random effects approach to linear static panel data models in which both the individual heterogeneity and the idiosyncratic shocks are correlated with time-varying explanatory variables, and implement instrumental variables approaches. Indeed, our CRE-GMM approach could also be used to estimate static models that need instrumental variables estimation for endogeneity together with consideration of the correlation of regressors with individual heterogeneity;111Internal instruments have the advantage that they are readily available while external instruments need to be carefully selected. Fundamental to our paper is also [30] investigating GMM-dif, GMM-lev, GMM-sys supposing predetermined possibly correlated with individual heterogeneity. For GMM-lev and GMM-sys the leading term of the bias is strongly affected by the magnitude of the individual effects as well by any correlation of the regressor and the effect.

Our work is also related to [81, 82, 54, 53, 5] who use quasi-likelihood estimator of the conditional mean approach [32, 73] applied to dynamic panel data models. [81, 82] assume random cross-sectional effects and have regressors that include lagged values of the dependent variable and may include other explanatory variables that are exogenous to the time-varying error component but may be correlated with unobserved time-invariant components. Initial conditions do not matter if the model is first augmented with an appropriate control function. The feasible GLS iteration produces a quasi maximum-likelihood (QML) estimator of the augmented model that is consistent and asymptotically normal as increases while is fixed, regardless of initial conditions, log-likelihood misspecification or conditional heteroskedasticity. [54] show that a properly specified QML estimator that uses the approaches from [73, 32] to condition the unobserved effects and initial values on the observed strictly exogenous covariates is asymptotically unbiased if whether is fixed or . [53] extends the analysis by comparing the feasible GLS for the conditional mean approach of [73] and the linear difference approach treating initial values as random variables and as fixed constants. [5] show that a correlated random effects estimation in levels may achieve substantial efficiency gains relative to estimation from data in differences. Among sociologists, [3, 71, 72] consider likelihood-based estimation of panel data under fixed- and large- settings.

Other related works are [93, 94, 83] discussing how the Mundlak1978’s approach can be used to handle the initial conditions problem and the likelihood function in dynamic non-linear unobserved effects panel data models. [17, 16] uses the [73]’s device in panels where there is a factor error structure correlated with the regressors. Levels are used instead of differencing, as differencing the data tends to remove useful information and is ineffective in removing the individual effects.

In contrast to the studies cited above, we would like to relax the exogeneity assumption of the explanatory variables other than the lagged dependent variable. In other words, we would like to better understand the role of endogenenity due to heterogeneity (the correlation between the explanatory variables and individual characteristics) and the role of endogeneity due to the correlation of the explanatory variables with the idiosyncratic shock that varies between units and over time. In many applications, the explanatory variables are affected by both of the two sources of endogeneity.

Finally, our research extends the literature focused on the comparative analysis of GMM estimation on dynamic panel data models [47, 48, 49, 50, 30, 31, 57, 59, 58, 4, 56].

The paper is organized as follows. Section 2 introduces the model and Section 3 presents the Correlated Random Effects GMM-lev estimation (CRE-GMM) and its motivations for the applied researcher. Section 4 presents the Monte Carlo experiment and the results from our simulations. Section 5 reports two empirical examples of our approach. Section 6 concludes. Details and further results of our approach are in the Appendix A

2 The model

We consider a general dynamic model, able to capture many phenomenon like country/regional growth or unemployment, temporal sequence of students’ performance into classes nested within schools, firms’ productivity, corporate financial choices, investment in R&D. In a nutshell, lags of the explanatory variables characterize many economic and sociological behaviours. The standard uni-equational linear dynamic model is defined as an ARDL(1,0) or partial adjustment model (PAM):

| (1) |

where is a vector of measurable explanatory variables changing with and , and is a vector of measurable time-invariant explanatory variables changing only with .

The lagged dependent variables, , avoids omitted variables and the assumption implies stability respectively weakly-stationary.

The error term is where represents the individual-specific unobserved effects randomly drawn along with the observed covariates. captures unobserved heterogeneity, possibly correlated with and and by construction with . The component represents the idiosyncratic errors. The indvidual heterogeneity is uncorrelated with the random noise, i.e. ; we will however relax this assumption in some of our Monte Carlo simulations.

The error components and are sometimes referred to as "permanent" and "transitory" components. To be poetic, [36] referred to the fixed part of the model as the "immutable constant of the universe" (the unique constant term, ), to as the "lasting characteristic of the individual" (the individual effects), and to as the "fleeting aberration of the moment" (the idiosyncratic shocks). Units are all different from one another in fundamental unmeasured ways. Particularly in behavioural sciences, individual differences are the norm rather than the exception, and the individual effects capture an additive linear combination of all unit-specific time-invariant omitted variables (such as the institutional and demographic specificities of the country; the cultural background of the people’s family of origin; the ability, intelligence, enthusiasm, willingness to take risks, motivation, work ethic of the students; the type of company ownership and management involvement) that can capture the differences of each individual relative to the benchmark.

The assumptions regarding the idiosyncratic shock are:

-

1.

and , with , errors are uncorrelated across units;

-

2.

and with , errors are serially uncorrelated over time;

The easiest way to ensure validity of assumption (1) is to assume that . Adding time dummies aims to explicitly capture, within the fleeting aberration of the moment , each period-specific factor of aggregate influence on micro units. Examples are the business cycle, macroeconomic events, neighbourhood effects, herd behaviour and social norms. If not accounted for, these unobservable common factors may generate a weak form cross-sectional dependence.222For an overview over cross-sectional dependence, see [34]. Another simple way to account for common correlated effects is to use cross-sectional demeaned data as in [71, 5]. In case of a more complex structure strong cross-sectional dependence can be an outcome. A prominent example is the interactive fixed effects models, , where indicates factors and individual-specific loadings, strong cross-sectional dependence. To account for strong cross-sectional dependence, regressions are augmented with cross-section averages [79] or principal components [17].

To guarantee the assumption 2. of non-autocorrelation, which underlies the appropriate setting of the moment conditions exploited by the GMM, the dynamics of equation (1) can be extended. For example, we might consider an ARDL(1,1) and the corresponding equilibrium correction model (ECM):

| (2) |

The absence of autocorrelation of errors also goes hand in hand with the non-rejection of the restrictions and . In this case, a static model is obtained, for which the GMM approach is nevertheless interesting as it provides "internal" instruments (information within the model), thus avoiding the difficulties of finding good "external" instruments.

3 The CRE-GMM estimation

One of the aims of our Correlated Random Effects GMM-lev estimation method (CRE-GMM) is to keep equation (1) in levels as they allow estimating the effects of measurable time-invariant explanatory variables, , while also considering the role of unmeasurable individual heterogeneity which, if omitted, would generate upward bias of the autoregressive parameter (and bias of all other parameters through the smearing effect). The individual effects capture an additive and linear combination of all time-invariant unit-specific unobservable variables. They capture the differences of each individual with respect to the benchmark . The GMM-dif [6, 7, 11, 12, 4] could solve the upward bias due to endogeneity because of heterogeneity, but it does not allow estimating the parameters associated with the measurable time-invariant variables . This problem also affects the GMM-sys [12, 25], at least in terms of efficiency, as most of the equations are first-differenced while the level equation is only retained for non-redundant moment conditions, actually for only one more period per panel unit.

Another reason why the GMM-lev is an attractive alternative to the GMM-dif estimator is that its performance does not deteriorate for approaching unity [24]. The closer the autoregressive parameter is to one, the weaker would be the relation between lagged levels and first difference variables. On the other hand, in GMM-lev, a large autoregressive parameter implies a strong link between lagged first differences and level variables [21]. Hence we suppose to get more informative and relevant estimations from the GMM-lev than from the GMM-dif and GMM-sys.

The addition of Correlated Random Effects to equation (1) can be analysed by exploiting the recursive substitutions for in equation (1) [23, 57, 75]:

| (3) |

where and covers the pre-sample and sample periods. The dependent variable can be separated into four components. The first component, is the term that depends on the initial observations, , and influences the behaviour of any estimators as long as is finite; its effect does not vanish, and affects each subsequent period when the time dimension is short. Instead, its relevance decreases when is large, under the condition of weak stationarity . The effect of the initial conditions does not vanish with when is close to unity. The starting values may be seen as representing the initial individual endowments. Particularly in longitudinal panels where is rather small and asymptotic concerns , the effects of the initial conditions are not asymptotically diminishing, and hence the assumptions on initial observations play an important role in determining the properties of the various estimators proposed in the literature, like GMM-sys and GMM-lev. [43] argues that in estimating an AR(1) model on panel data it is fairly common to disregard the potentially informative role of the distribution of initial conditions for the estimation of the autoregressive parameter . This practice is understandable because misspecification of the distribution of would result in the inconsistency of the resultant estimator. Perhaps because of this concern, efficiency in dynamic panel literature has been discussed in the framework where was assumed to be ancillary for the parameter of interest. He shows that the marginal information contained in the initial condition is substantially even when is relatively large, and the efficiency gain tends to be larger for close to one, as the coefficient of indicates that the importance of initial condition in is an increasing function of .

The second term, , is a modified intercept that depends on the unit-specific unobservable effects, and possibly on observable individual characteristics, ; individual effects and the autocorrelation coefficient interact to determine the long run means of the series, constant for each individual . The third term, , is a component depending on current and past values of , and related to the dynamics of the model Finally, the last term is a moving average of the disturbances .

It is reasonable to assume that the process driving has been in process sufficiently long in the pre-sample period, such that . Then Equation 3 can be re-formulated as:

| (4) |

This implies that it is impossible to estimate models with finite time dimension (even if were 40 periods). Instead, we truncate the dynamics of explanatory variables at some lags, say in a Partial Adjustment Model (PAM) or in an Error Correction Model (ECM); hence we omit in equation (1).

The individual effects can thus be considered as random and interpreted in terms of the past histories of each individual in the panel prior to the time when estimates begin, and these past histories are functions of the stochastic variables, omitted because of the lag truncation in and .333Take the example in [75] in which with , cross-sectionally and serially unrelated. For (the set of indices for which is observed, with used to specify the dynamics chosen much less than ), the j-order autocorrelation is . It follows that and are correlated, , with a correlation depending on how close to the beginning of the sample period the observation on is taken. This introduces additional “” parameters in equation (1) capturing the relationship between the individual effects and the observed past values of the explanatory variables ; the greater the greater is the signal to noise ratio on one side, but the greater the dependence between and on the other side (especially for near the beginning of the observation period). Further useful insights are in footnote 7 of [22].

As there is no good reason to treat the initial observation differently from subsequent observations or from unobserved previous values, let us suppose that the temporal observations can be split as:

| pre-sampleestimation sample | ||

The starting values computed by exploiting the observations may be seen as representing the initial individual endowments on each unit . Hence we can express equation (3) as:

| (5) |

where includes the observations used in the estimation sample, , while includes the observations of the pre-sample period used to proxy initial conditions, .

Lag truncation leads to omission of observations over time. The observations of and in those time periods can represent the individual endowments of each unit .444The lag length of the ARDL(p,q) should be selected in such a way as to imply uncorrelated errors. The individual effects can be then written as:

| (6) |

where and , and is the pre-sample period. To put it differently, we calculate the averages of the explanatory variables for the periods to capture permanent components, and then implement the estimations over the periods .

In equation (3) we suppose that the unobserved individual effects/initial conditions can be estimated from the history of observations of the explanatory variables entering our equation of interest. Using values dated before the estimation sample to compute proxies for the unobserved heterogeneity avoids correlation with any subsequent shock in the equation of interest. This has the distinct advantage of producing weakly exogenous (pre-determined) regressors as the measurement of individual effects is based exclusively on pre-sample information. For example, using the average innovative activity carried out by firms in the pre-estimation period makes it possible to capture unobservable differences in accumulated knowledge, returns to scale and cost of R&D not affected by endogeneity [29]. For stationary stochastic processes, such as ARs, the pre-sample mean is a more informed estimate of the steady state solution than the first sample observation. Averages condense past informations and therefore are better suited to represent the initial conditions in comparison to first observations in a sample. A further advantage is that they mitigate possible large variations in the time series and measurement errors (being divided by , the statistical averaging effect is achieved). In contrast, the single initial observation can be strongly influenced by the short-term cyclical position of the variables and/or the occurrence of random shocks. Indeed, the use of the individual’s time series mean ([73]’s approach) is more restrictive than using each observed variable at all the different time periods for each unit , and , as in the [32]’s approach. However, the simulation results in [54] suggest that to deal with the incidental parameters issues arising from the presence of individual-specific effects,555In a longitudinal, short , panel, asymptotic theory relies on and as so too does the number of individual effects to estimate. This is the incidental-parameters problem [76, 64, 70]. following the [73]’s suggestion to condition on the time series average of individual’s observed regressors performs better than conditioning on each observed variable at all different time periods as suggested by [32]. The averages tend to perform better when the temporal dimension is large (possibly larger than ). For small () the two approaches can lead to asymptotically unbiased inference, with the [73]’s approach yielding the smaller bias and RMSE.

Our idea to capture initial conditions is sufficiently general and encompasses several other specifications of the initial values considered in the literature as special cases. We are close to [23] suggesting to use as the equation determining the initial observations. [6] show (in their Table 1) the sensitivity of maximum likelihood estimators to four alternative assumptions about initial conditions. At one extreme, it can be assumed that the initial observations are fixed constants specified independently of the parameters of the model; under this specification there are no unit-specific effects at the initial period which considerably simplifies the analysis.666However, as pointed out by [74], unless there is a specific argument in favour of treating as fixed, in general such an assumption is not justified and can lead to biased estimates. Alternatively, the initial values can be assumed to be random draws from a distribution with a common mean: where is assumed to be independent of and . Once again, the starting value and the equilibrium level are independent. At the other extreme, the initial endowment affects the level, , and the initial observation is no different from any other observations (an assumption close to our assumption).

A drawback of our approach is the requirement of a sufficient number of pre-sample observations for each unit . In the case of unbalanced panel data, the initial conditions of the units entering the sample after (and thus with no observations available in the pre-sample period) could be proxied by the averages computed for other units available in the pre-sample and characterised by “similar” initial endowments; for example, we could use individual averages of firms characterised by the same size, within the same industry, localized in the same geographical zone, and with other cluster-level characteristics. Our approach is also valid under the condition that the and parameters of equation (6) do not vary across otherwise we will have the incidental parameters problem; however, the correlated random effects approach does not lead to incidental-parameter bias when and are of comparable dimension [15].

3.1 The CRE-GMM estimation - advantages

Based on [73] idea, the CRE approach models the relationship between , and the lagged dependent variable . An attractive assumption of (6) is that the individual specific effect is decomposed into a systematic component depending on the individual specific mean of the regressors, and , and the remaining unsystematic component treated as an additional random term, . In the words of [20], the endogeneity due to correlation between lower-level predictors, , and higher-level part of residuals, , occurs so regularly, alongside consideration of the [45]’s specification test. The fixed effects solution which circumvents this problem by controlling out all differences between higher-level units brings to a very limited model, being unable to estimate the effects of higher-lever variables, . The random effects estimation used in a formulation similar to that originally proposed by [73] which partitions the effect of lower-level covariates into two parts, treats endogeneity as a substantive phenomenon which occurs when a given lower-level variable with different within and between processes is assumed to have a single homogeneous effect. A well-specified random effects model can be used to achieve everything that the fixed effects models achieve, and much more besides.

As an example, firm-specific technical efficiency and economies of scale are between effects, while technological changes over time are within effects. Permanent unemployment is a between measure, while temporary unemployment is a within measure. When studying the birth weight of newborns [1], weight may be more related to maternal smoking behaviour than smoking cessation. When studying the impact of GDP () on democracy (), a fixed-effects estimation yields a single parameter. This leads to the counter-intuitive finding that GDP has no relationship with democratization [2]. Unobserved factors unique to each country, related to historical, cultural, and political factors, can affect democracy levels. These factors play a role in pushing countries to higher or lower democracy levels. Ignoring the "between" cluster effects can lead to incorrect inferences when "within" cluster data show no GDP-democracy relationship. In psychological research, the ecological fallacy arises from confounding within and between group differences [85].

Augmenting the dynamic panel data regression with the systematic part of the individual effects yields a model representation that includes the random and fixed effect specifications as special cases:

| (8) |

In our random effects framework, initial conditions give rise to a “between’ equation” (6), which captures sample variation across units, while the “within” estimated parameters of equation (8) captures the sample variation within each unit over time.777A similar idea in the maximum likelihood framework is in [66]. The RE estimator under the hypothesis of exogenous is investigated also by [54, 53].

The CRE-GMM approach based on equation (8) has the following advantages:

-

1.

It avoids the omission/inability to capture individual heterogeneity and the mixture of “spurious” (past/state dependence) persistence, due to the serial correlation generated by the unobserved permanent , and “true” (path/behavioural) persistence, measured by ) which is the causal effect of past values of the dependent variables on its current realization.

-

2.

The inclusion of individual averages avoids bias from omitted variables and the “endogeneity bias due to heterogeneity”. In general, it is a rather difficult hypothesis to rule out a statistical dependence between the individual specific effects and the explanatory variables. The GMM-lev estimation applied to equation (8) extended in a [73]’s fashion treats the endogeneity as a substantive phenomenon without necessarily requiring instrumental variables estimation for such an endogeneity.

-

3.

Instead of using (erroneously?) a single weighted average of the within and between effects of the covariates , we keep the partition and assess whether the between effect is relevant and thus cannot be neglected as in fixed effects/first-differences estimations. Hence, we simultaneously estimate the within effect (effect of unit-specific temporary deviations from the period averages of ) and the between effect (effect of permanent differences between individuals in ).

-

4.

Obtaining the within estimate of each while controlling for systematic differences in the levels of the covariates across results in a more convincing analysis. We can estimate coefficients on time-constant variables while reproducing the fixed effects estimates of the time-varying variables, [96, 97, 89, 90].

-

5.

A causal interpretation to the coefficients of can be given only if meaning that is uncorrelated with once the time-varying covariates are controlled for. This assumption is too strong in many applications, but one still might want to include time-constant covariates [95]. If is correlated with individual heterogeneity, the effect of time-invariant observable variables can be identified in the spirit of [46] who use, as instruments, both the within and between transformations of the components of uncorrelated with individual heterogeneity. In our CRE-GMM approach, we directly add to the model the individual averages of to capture the individual heterogeneity (see further discussion in Section 3.2). Equation (6) could also be extended to include measurable time-invariant variables correlated with individual heterogeneity.

-

6.

Indeed, equation (8) allows for the variable addition, or regression based, robust version of the [45] test on for individual effects uncorrelated with covariates [10]; this test can be implemented also for sub-sets of covariates. This version avoids computational problems and can be robust, avoiding the severe size distortion on inference after using the non-robust Hausman [40].

-

7.

We have greater variability, due to the combination of the variation across cross-sectional units (between) with the variation over time (within), and more informative data. As a results, we could achieve more efficient estimations and mitigate multicollinearity problems, particularly in the weighting matrix used by the GMM to handle the moment conditions.

3.2 The CRE-GMM estimation - moment conditions

The moment conditions exploited to estimate equation (8) in levels must tackle the endogeneity of the lagged dependent variable and the possible double endogeneity of the variables:

The lagged dependent variable includes the unobservable , hence, by definition, it is endogenous because of the individual heterogeneity; considering the shock component , the lagged dependent variable is predetermined, meaning uncorrelated with . The variables could be (?) correlated with both the individual heterogeneity and the shock . Indeed, a variable in could be predetermined instead than strictly exogenous, meaning influenced by past values of the dependent variable (correlated with past shocks); for example, in a model explaining wages of workers, a change in of the dependent variable wages could determine becoming member of a union in hence producing a change in one of the explanatory variables [91]). Often the dynamic model in equation (8) could be affected by omitted regressors correlated with , measurement errors in , simultaneity, thus producing endogeneity of the variables.

When the model is first-differenced, as in GMM-dif, the moment conditions are based on the levels of and . The comparison of our moment conditions and those of GMM-dif is in Table 1. When exploiting the equations in levels, as in GMM-sys, the usual approach to tackle correlation with the individual heterogeneity included in the error term, is to exploit the moment conditions based on the first-differenced variables and . Compared with GMM-sys, where the equations in levels are added only for the non-redundant period with respect to the periods already exploited by the GMM-dif, our approach in principle uses all the moment conditions available for the level-equations, not just the non-redundant ones. However, it has to be considered that panels often have moderate and long , and that applied econometricians tend to use in practice less than the total number of available instruments when that number (which depends on ) is judged to be not small enough relative to the cross-sectional sample size. To combine this practice with a more structured lag selection, we follow the suggestion of [99, 30] to use fewer IVs that potentially available for GMM-lev in the matrix,888The instrument matrix has full column rank if and . i.e. to restrict the moment conditions to lags from to . The selected lags are valid to deal with predetermined and endogenous explanatory variables in the equation in levels.

| Classification | Method | ||

|---|---|---|---|

| GMM-dif | CRE-GMM-CRE-GMM5 | ||

| Correlat. | |||

| Predet. | |||

| CRE-GMM and CRE-GMM3 | |||

| additional MCs: | |||

| GMM-dif | CRE-GMM-CRE-GMM2 | ||

| Correlat. | |||

| Predet. | |||

| Endog. | |||

| CRE-GMM-CRE-GMM1 | |||

| additional MCs: | |||

| GMM-dif | CRE-GMM3-CRE-GMM5 | ||

| Uncorrelat. | |||

| Predet. | |||

| Endog. | |||

| CRE-GMM3-CRE-GMM4 | |||

| additional MCs: | |||

In all the methods CRE-GMM-CRE-GMM5 we implemented, and in the three CRE-GMM-CRE-GMM2 estimations, we assume that , and by definition , are correlated with the individual heterogeneity, . In the three CRE-GMM3-CRE-GMM5 estimations we suppose that is uncorrelated with the individual heterogeneity, . GMM-style lags of the explanatory variables in levels are valid instruments for the untransformed equation (in levels) only if they are uncorrelated with the unit-specific error component, while the first set of CRE-GMM-CRE-GMM2 estimations uses first-differenced instruments, as suggested by [25]. We explore each of these identification strategies in estimation by comparing the use of lagged first-differenced and lagged levels of as instruments for the equation in levels (respectively, CRE-GMM-CRE-GMM2 and CRE-GMM3-CRE-GMM5). Using IVs in levels could increase the correlation between endogenous variables and IVs, hence the efficiency of the CRE-GMM approach.999The lagged dependent variable is always estimated with lagged first-differences of as is correlated with the individual heterogeneity by definition. Robustness checks about the use of lagged levels of as instruments do not show any improvement in the results.

The inclusion of unit-specific averages in equation (8) allows the comparison of the two sets of estimations, CRE-GMM-CRE-GMM2 and CRE-GMM3-CRE-GMM5, as it explicitly models the individual endogeneity which is hence removed from the error term, making valid the IVs in levels. Additionally, it helps when there is no guarantee that the first-differenced instruments for the untransformed model are uncorrelated with the unit-specific error component. For example, [67] examine the adoption of fuel-efficient precalciner kilns in the cement industry and have a region-specific term that affects all cement plants in the same geographic region. The first-differences are valid instruments only under the case that the region-specific effect is constant over time, a process that could arise in practice due to state-level differences, for example in unionization policies or tax rates. However, the region-specific term could evolve according to a finite moving-average process of order , a possibility arising if construction projects take multiple periods to complete, but there are no spillovers from one construction project to future projects. In such a setting, T-period lags of the endogenous regressors are valid instruments if . The region-specific term could also evolve according to an autoregressive process if construction projects have positive spillovers on future projects, so that the effect of a positive region shock diminishes over time but never fully dies out. Lagged regressors taken from the period are valid instruments if they are orthogonal to the region-specific term in and the entire series of shocks in .

With regard to the assumptions concerning individual averages, let us compare three alternative cases: the pre-sample individual averages and are exogenous (cases CRE-GMM and CRE-GMM3); only individual averages of are exogenous (cases CRE-GMM1 and CRE-GMM4); the pre-sample individual averages of and are endogenous (cases CRE-GMM2 and CRE-GMM5). In Section 4 we discuss the simulated results with and without instrumenting the proxies for the initial conditions. Individual averages supposed to be endogenous are instrumented by the same suitable lags used to instrument the explanatory variables of the model, and .101010The idea behind these comparisons is to understand what happen when we use suspect moment conditions. [37] suggests that, in finite samples, the addition of a slightly endogenous but highly relevant instruments can reduce estimator variance by far more than bias is increased. Instrumenting the averages obtained from the pre-sample with the lags of the variables in the estimating sample resembles the orthogonal forward deviations suggested by [12].111111In [4] for fixed the IV estimators in orthogonal deviations and first-differences are both consistent, whereas as increases the former remains consistent but the latter is inconsistent. Using past observations has its antecedent in the work of [33] considering the use of long lags in regressors.

An interesting aspect that emerges from comparing CRE-GMM-CRE-GMM1 and CRE-GMM3-CRE-GMM4 estimations with CRE-GMM2 and CRE-GMM5 estimations is whether individual characteristics have evolved over time. If agents maintain their personal characteristics unchanged over time, then it clearly follows that and and the moment conditions under CRE-GMM-CRE-GMM1 and CRE-GMM3-CRE-GMM4 and not valid. If, instead, the behaviour of the agents evolves over time or, even better, if there is a structural and status change in individual characteristics such that with and for but with and for , hence the moment conditions used in CRE-GMM-CRE-GMM1 and CRE-GMM3-CRE-GMM4 are valid.121212We have that and by definition, as the individual averages are computed by exploiting the pre-estimation period . In other terms, we are explicitly modelling the mean-stationarity assumption implying that the deviations of and from the initial conditions are uncorrelated with the levels of the initial conditions, and the “new” realisations of and for are not informative for the individual heterogeneity . Comparing estimates CRE-GMM2 and CRE-GMM5 with CRE-GMM-CRE-GMM1 and CRE-GMM3-CRE-GMM4 can add information regarding the behaviour of individuals.

As discussed in [86], the validity of the equations in levels added to GMM-sys is based on whether individuals have achieved their steady state before the study period. Otherwise, the initial distance from the steady state may be greater the higher the individual effect (on which the steady state depends) and this produces, in the early periods of the study, a correlation between the first-differenced and the error term, . Suppose that we would like to estimate production functions, in which may capture the effect of technical efficiency and unobserved managerial practices. The mean-stationarity assumption makes it difficult to deal with a mix of companies in which the youngest, still far from their steady state compared to more mature companies, can grow faster at the beginning of the sample period. Note that an implication of lack of stationarity in mean is that the data in first differences will generally depend on individual effects, making invalid the IVs for GMM-lev [5]. In short panels, steady state assumptions about initial observations are also critical since estimators that impose them lose consistency if the assumptions fail. Moreover, there are relevant applied situations in which a stable process approximates the dynamics of data well, and yet there are theoretical or empirical grounds to believe that the distribution of initial observations does not coincide with the steady state distribution of the process.

For example, educational experience has an effect on the earnings structure that is not crudely captured by years of schooling (a between effect), but also depends on on-the-job training (a within effect). During the early stages of their careers, workers may accept lower earnings because they expect that more experience will develop the skills needed to compensate them for higher future earnings [44]. In these examples, the individual average of working experience added to the equation of interest (our CRE-GMM approach) can help in capturing the heterogeneous different starting points of the workers.

Another example are growth models [27]: assuming that the means of the series, whilst differing across units, are constant through time could be implausible for e.g. per capita GDP.131313The inclusion of the time dummies allows for common long-run growth in per capita GDP, consistent with common technical progress. However, if the process has been generating the per capita GDP series for long enough, prior to the estimation sample, any influence of the true start-up conditions would be negligible and . Our CRE-GMM can help in capturing the country-specific initial conditions and the validity of the above assumptions.

[56] generate the dynamic panel data with periods () where the starting value is from , and then take the last periods as their sample. By doing so, the initial value in the estimation is close to the steady state. They also use the first period of the simulated data as the initial observation in the estimation sample (so that and the process is away from its steady state). For the case, the GMM-sys has a larger bias; this is consistent with the theoretical prediction because the system GMM estimate requires that initial observations are uncorrelated with the individual effects, which is satisfied if the process has started a long time ago.

4 Results

4.1 Monte Carlo simulations

To asses the performance of our proposed estimator, we employ a Monte Carlo simulation with the following DGP based on an ARDL(1,1) model:

| (9) | ||||

An ARDL(1,0) model is obtained from Equation (9) if . The error term is composed into an individual effect and an idiosyncratic shock .

The parameters and control the degree of endogeneity by specifying the correlation between , the individual effects, and the random noise . sets the correlation between the individual effects and the error .141414Note, when , then the variance of the idiosyncratic shock is lower than the variance of the individual heterogeneity. For a more detailed discussion see Equation (A5) in the Appendix A.1. Further details on the setup of Monte Carlo simulations are in Appendix A.1.

As a baseline we estimate the Pooled Ordinary Least Squares (POLS), the Random Effects (RE) and the Fixed Effects (FE) estimators on model (9). Under the assumption that is uncorrelated with the idiosyncratic shock () the POLS, RE and FE estimates serve as benchmarks for the consistent estimate of the parameter. The upper bound is provided by the POLS, affected by omitted heterogeneity bias, and the RE which assumes there is no correlation between the regressors and the individual effects (). The lower bound is the FE which eliminates the influence of any time-invariant variable from the model by exploiting the within-transformation of the data, , where . The FE estimator would produce a consistent estimate of the autoregressive parameter for , as the [77]’s bias disappears.

We then estimate two correlated random effects models. For the first one, named CRE1, we add only the individual average of the lagged dependent variable. For the second one, named CRE2, the individual average of the explanatory variable are also added. If the explanatory variable is uncorrelated with the idiosyncratic shock, but (and obviously ) are correlated with , then the difference in the estimates obtained by CRE1 and CRE2 to the baseline estimators should provide an idea of the bias due to the correlation with the individual heterogeneity.

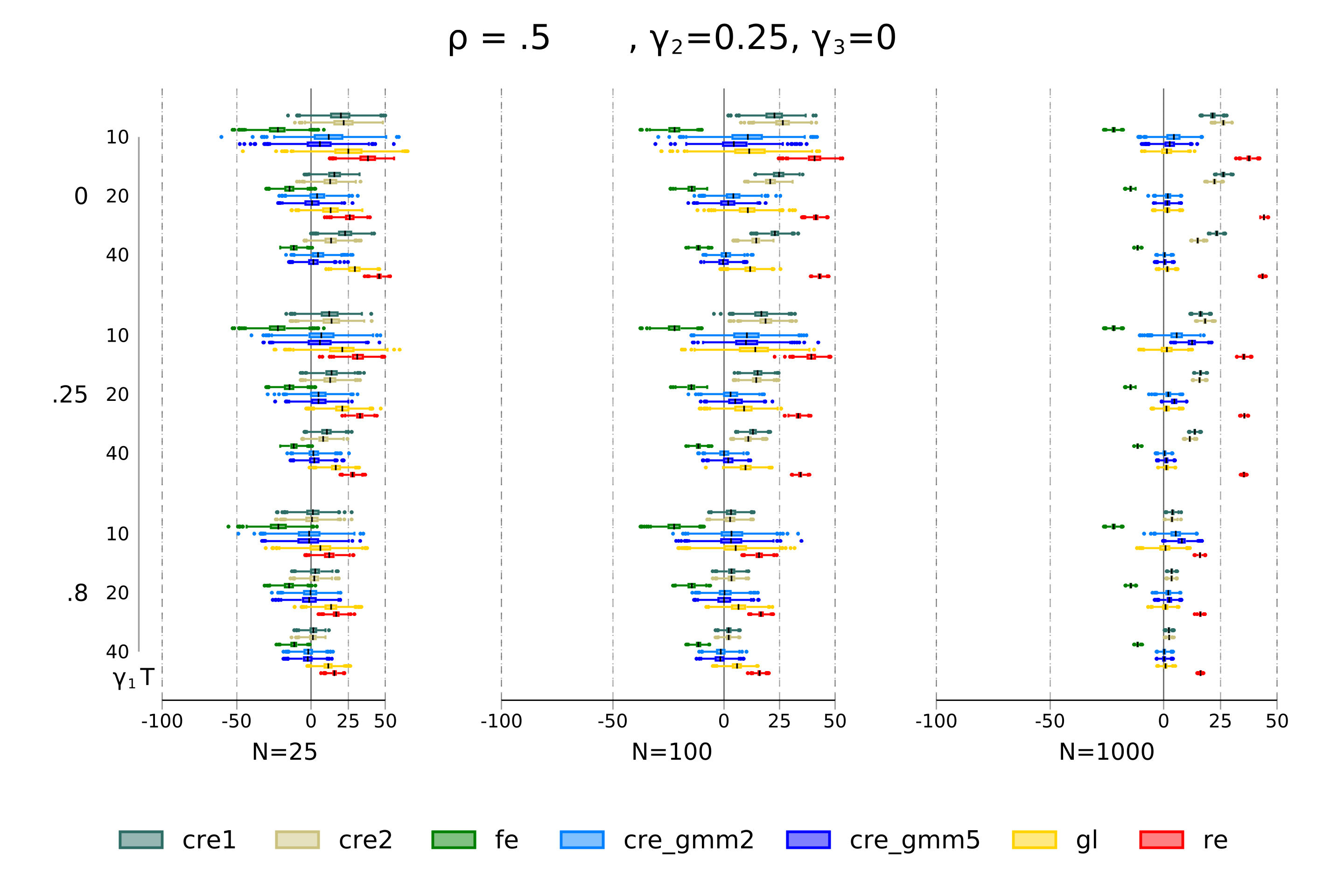

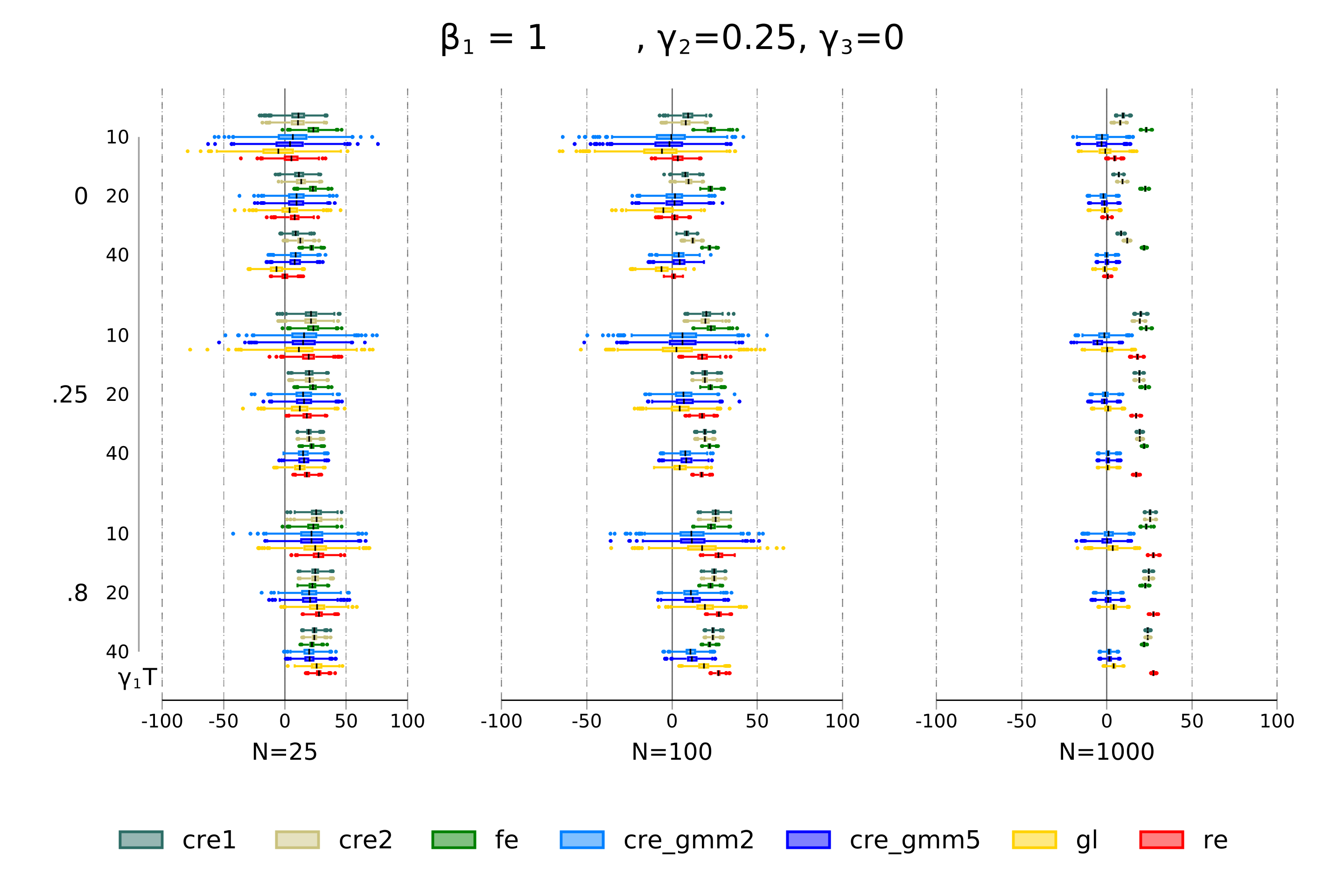

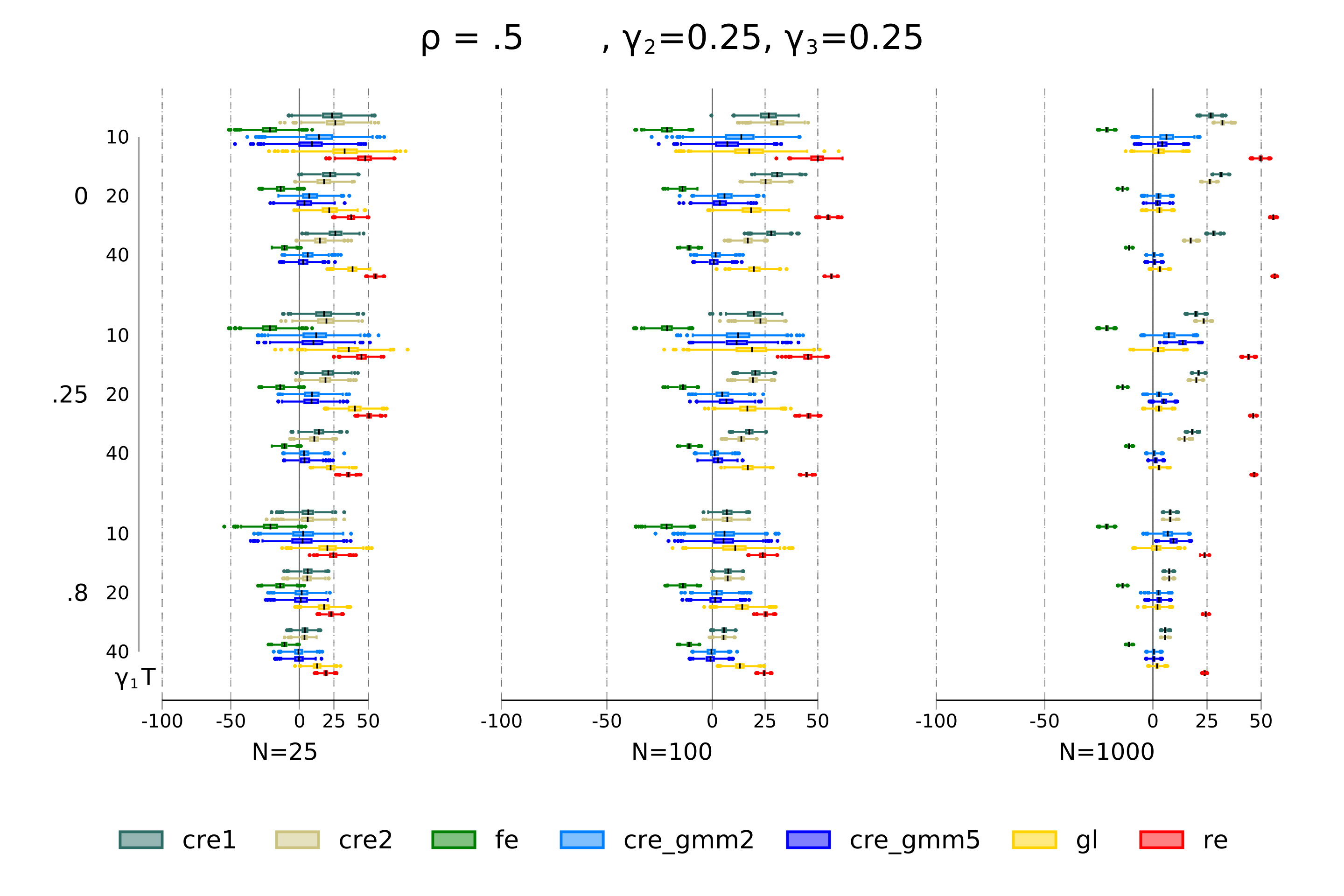

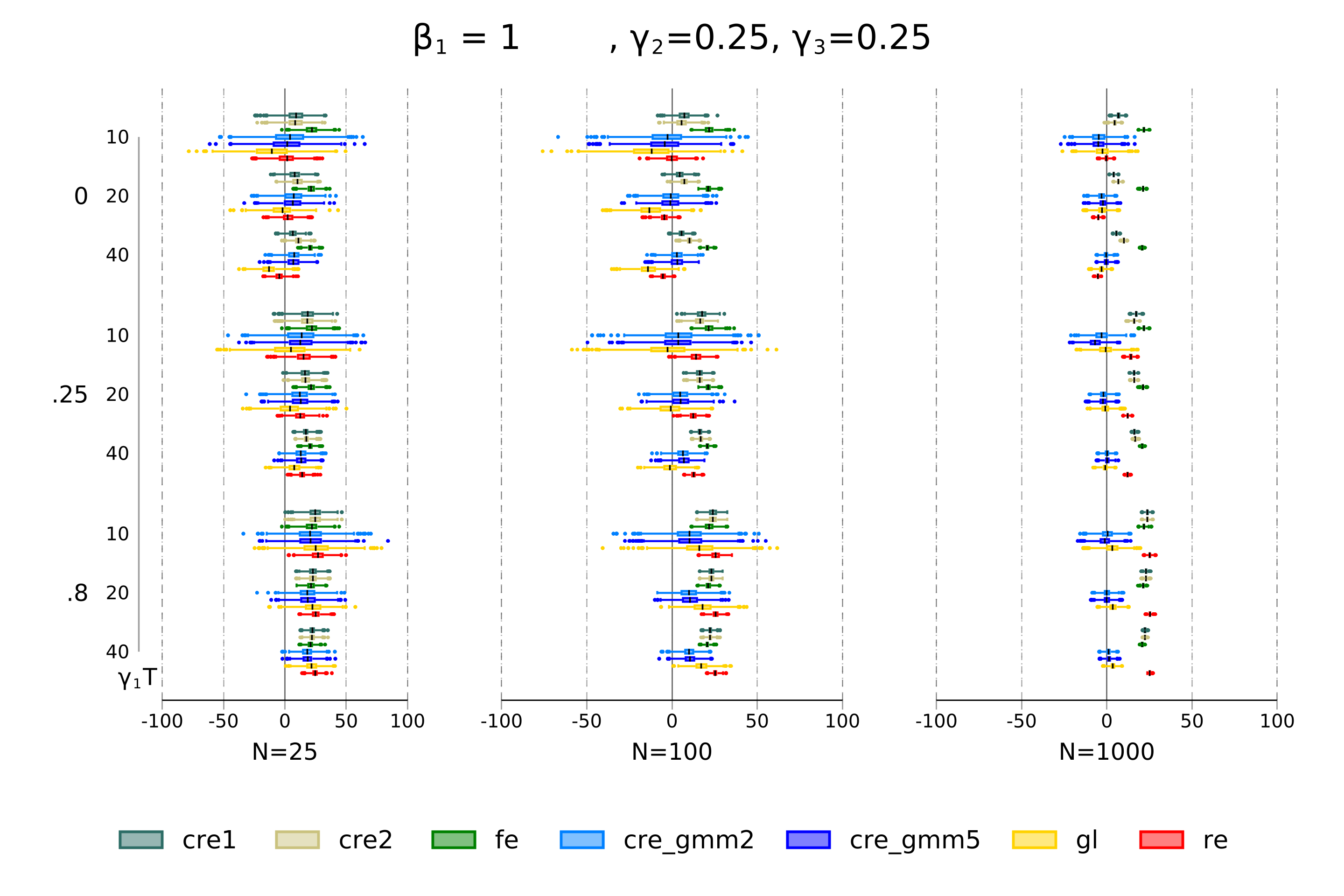

Finally, we apply the standard GMM-lev (named GL) estimation to equation (9), and we implement the six CRE-GMM estimations, presented in Table 1, on the dynamic model (9) extended to include, as additional explanatory variables, the individual averages of both and computed in the pre-sample period.151515In the ECM specification we add the individual averages of both and . The parameters for the simulation are set as follows: we fix , and . and are varied between 0, 0.25 and 0.8, while . With respect to the dimension of the cross-sections and time periods, we focus on three combinations of N and T: longitudinal panel (), macro panels (), and multilevel panels ().161616Results with , , and yield 288 combinations and with different variances as shown in Table A1 in the Appendix, Section A.1, produces 1152 experiments. We present the results for variances defined by equations (A5) and (A7). Equations (A4) and (A6) and alternative combinations of equations in Table A1 of the Appendix A.1 produce similar results. All our simulations are repeated 1000 times and are done in Stata. Estimation are done with the community contributed command xtdpdgmm [61].

4.2 Monte Carlo results

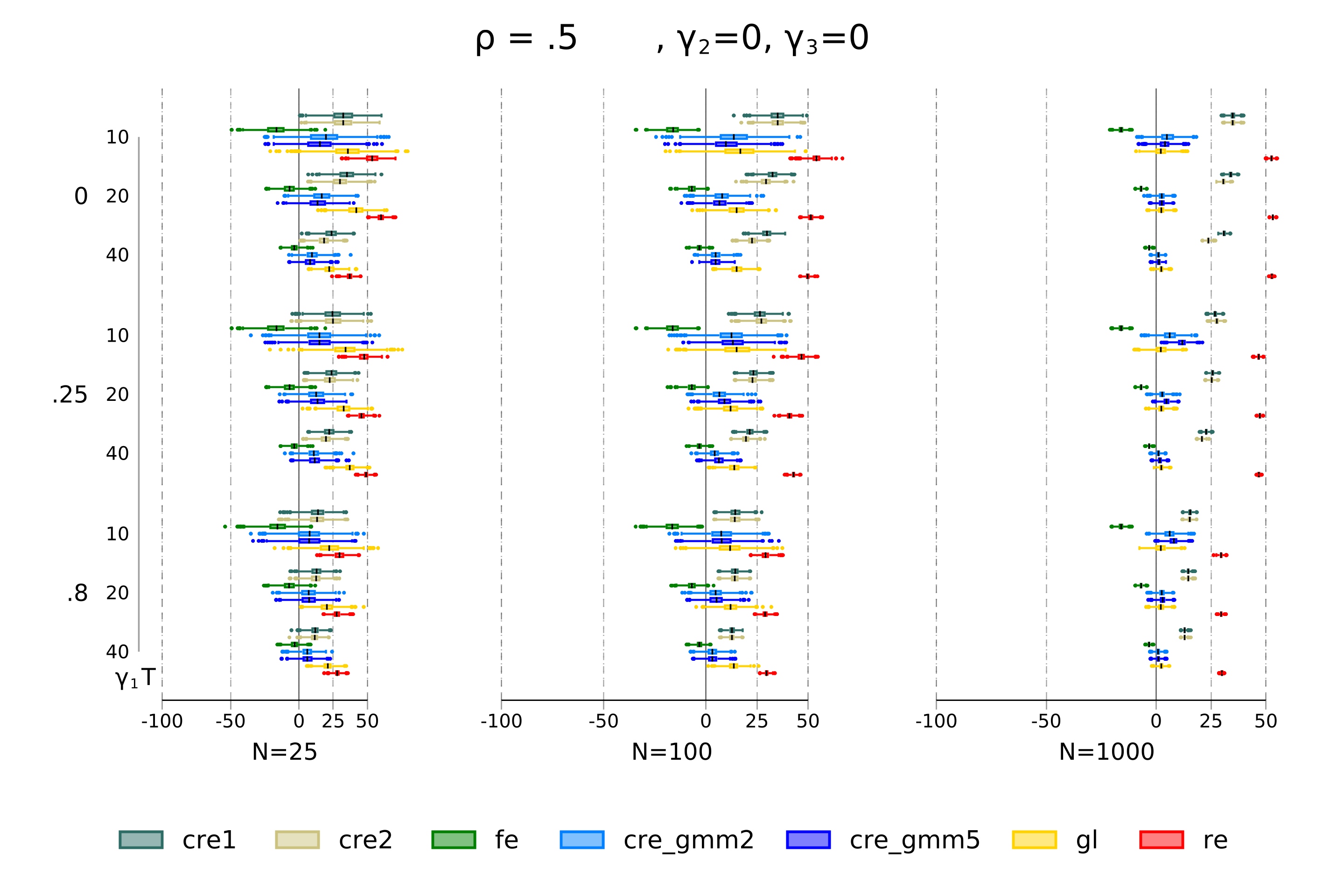

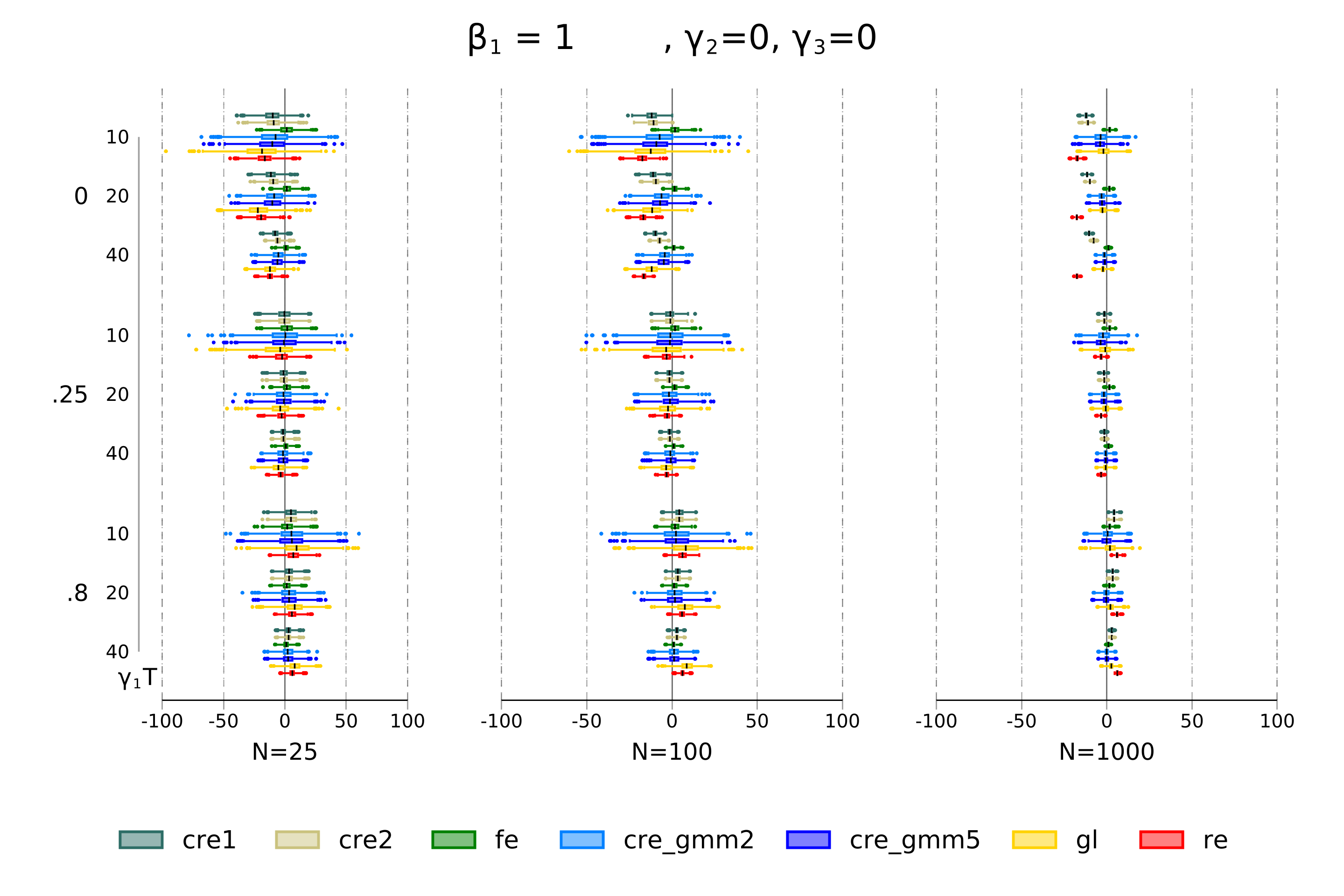

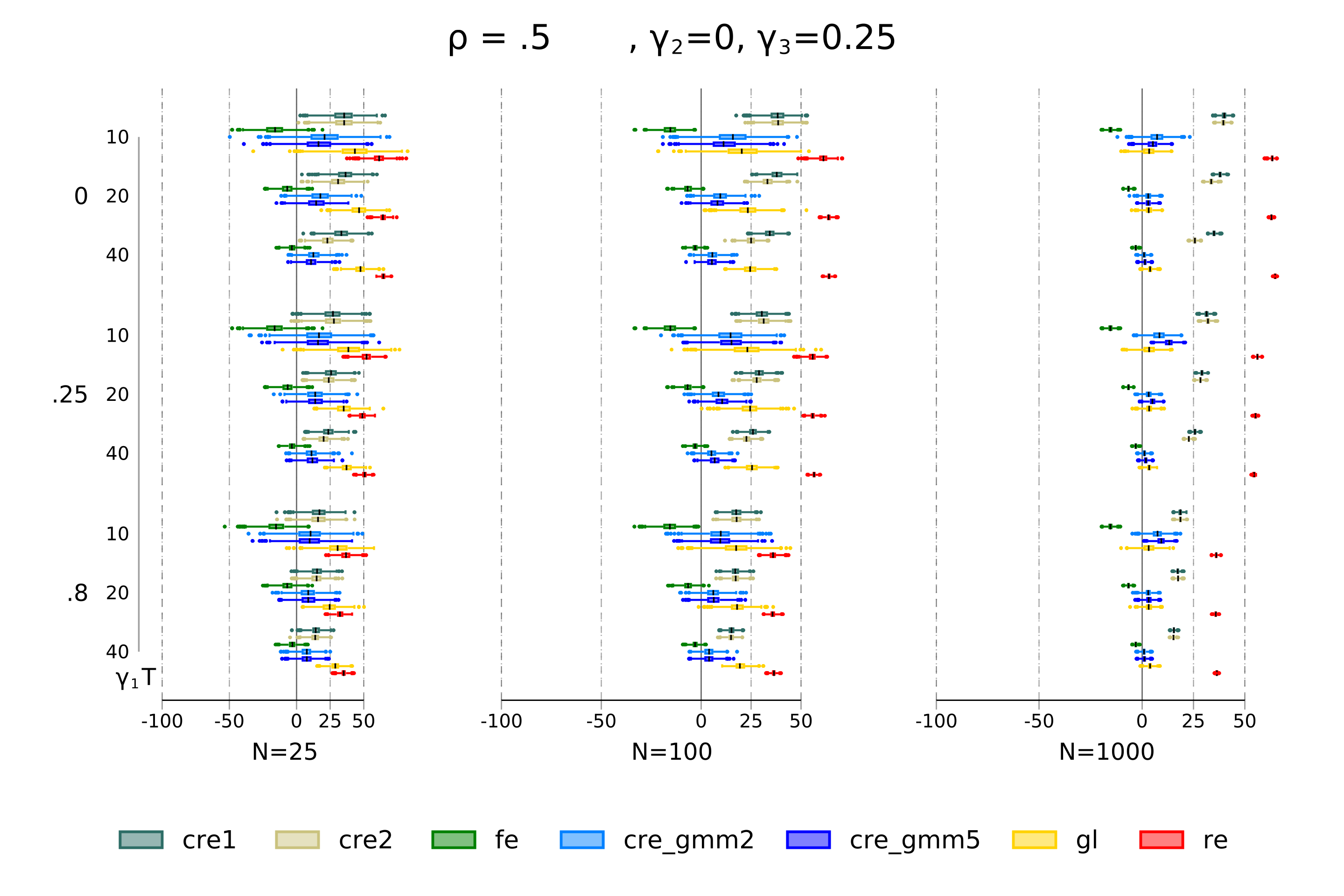

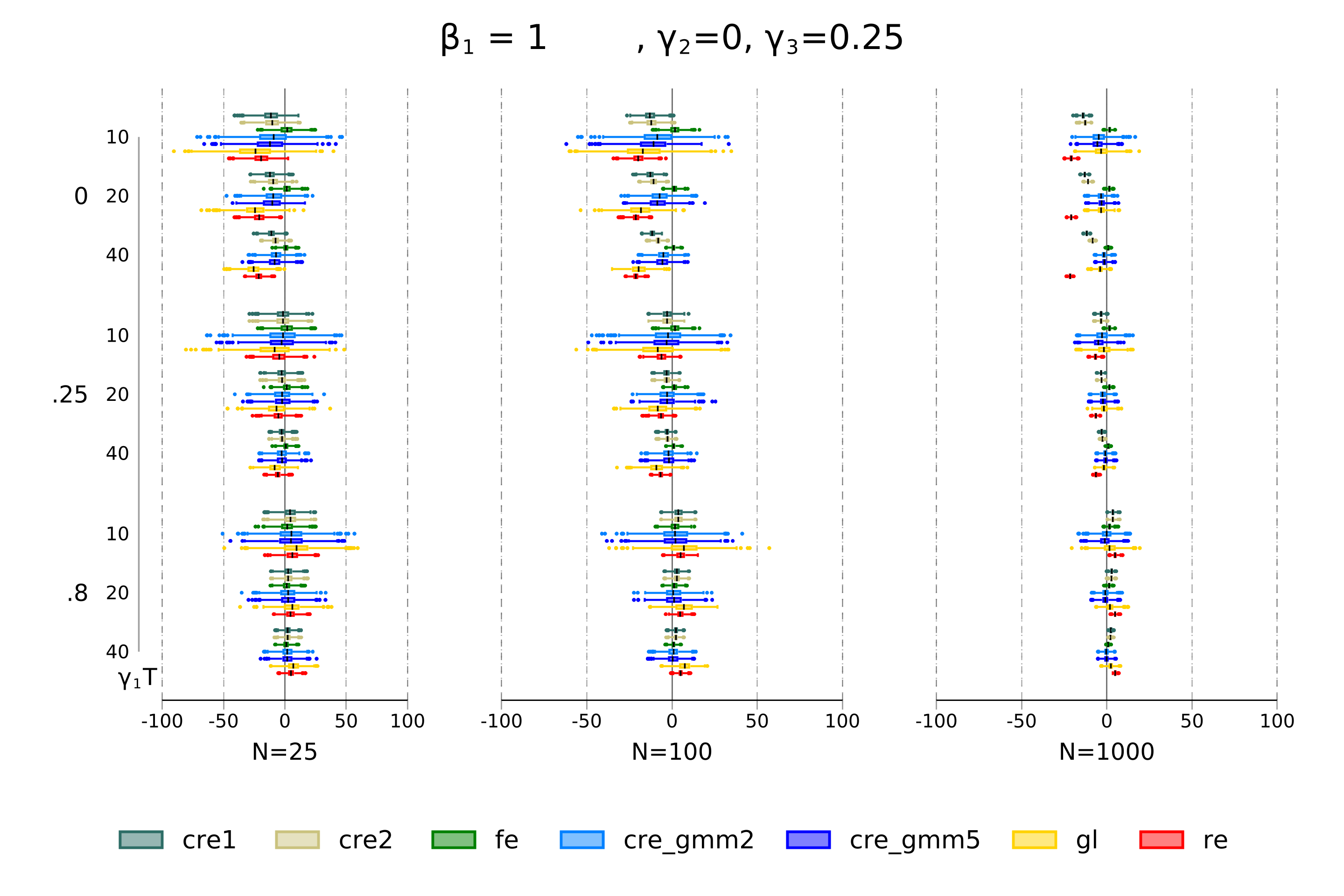

The results for the PAM model are presented in Tables 2-7 and report the average bias and the root mean square error estimates for the RE, FE, CRE1, CRE2, GL, CRE-GMM-CRE-GMM5 estimators of and . The model is specified as an ARDL(1,0) where the variable follows an autoregressive process with ; true and are 0.5 and 1, respectively.171717The ECM results, with equal to 1 and equal to 0.5, are in Section A.4 of the Appendix.

When there is no correlation with the idiosyncratic shock, , estimates from CRE1 and CRE2 are aligned between those from FE and RE. CRE1 and CRE2 eliminate, from the weighted average of between and within variability produced by RE, the between variability, captured by the individual averages. The correlation with individual effects, measured by individual averages, is unavoidable for the lagged dependent variable, generating the well-known interval for consistent dynamic estimates, with RE providing the upper bound benchmark and FE providing the lower benchmark. Since we do not have problems of standard endogenity, GMM-lev (GL) and the set of CRE-GMM estimators should provide similar estimates. This is in general true for longitudinal panels, while for multilevel and macro panels CRE-GMM is less biased and more efficient, particularly when we use levels of as instruments (CRE-GMM3-CRE-GMM5).

The presence of standard endogeneity, , produces a bias in the estimates increasing with the parameter capturing the correlation between and . The bias is greatly reduced by IVs in CRE-GMM framework: using first-differences or levels as IVs does not alter the results (there is a tendency to prefer levels for ), since we do not have correlation with individual heterogeneity. Instrumenting individual averages is usually preferable in terms of reduction of bias and standard errors in longitudinal panels. Under the case, the bias in the FE estimates for is reduced when we implement IVs approaches: we have 0.231 (FE), -0.010 (GL) and -0.029 (CRE-GMM5) in the longitudinal panel; 0.219 (FE), -0.068 (GL) and 0.082 (CRE-GMM5) in macro panel; 0.226 (FE), -0.051 (GL) and 0.013 (CRE-GMM) in the multilevel panel. The parameter is moderately affected by endogeneity of : the biases are -0.110 (FE), 0.006 (GL) and 0.013 (CRE-GMM5) in the longitudinal panel; -0.058 (FE), 0.146 (GL) and 0.009 (CRE-GMM5) in the macro panel; -0.073 (FE), 0.053 (GL) and 0.009 (CRE-GMM5) in the multilevel panel.

When there is endogeneity due to heterogeneity, , the parameter bias in GL increases from 0.011 (longitudinal) to 0.060 (multilevel) to 0.186 (macro). The best approach seems to be CRE-GMM2, with IVs in first-differences, presenting a bias going from 0.031 (longitudinal) to 0.032 (multilevel) and 0.054 (macro), and an apparently better disentangling of true (path) and spurious (state) dependence. The CRE-GMM2 approach is also beneficial for the parameter. The bias increases as increases going from -0.009 to 0.019 (GL, longitudinal), -0.027 to 0.078 (GL, multilevel), -0.052 to 0.081 (GL, macro); on the opposite, the increase in the bias is smaller or null for CRE-GMM2, moving from -0.016 to 0.026 (longitudinal), from 0.031 to 0.030 (multilevel), from -0.014 to 0.016 (macro). Also CRE-GMM5, with the IVs in levels, work well, indicating that the inclusion of individual averages is able to capture the impact of individual heterogeneity correlated with .

When there is endogeneity from both sources and , meaning that the correlation with the idiosyncratic shock prevails over the endogeneity due to heterogeneity, CRE-GMM2 works well in longitudinal panels for both and , while in multilevel/macro panels also CRE-GMM5 has a good performance, particularly for the parameter. Good performance of CRE-GMM5 for in multilevel/macro and in longitudinal panels, and of CRE-GMM2 for in longitudinal and in multilevel/macro is obtained when the correlation with individual heterogeneity prevails over the correlation with the idiosyncratic shocks, . The bias of the parameter is 0.003 (GL) and 0.027 (CRE-GMM2) in longitudinal; 0.033 (GL) and 0.001 (CRE-GMM5) in multilevel; 0.057 (GL) and -0.011 (CRE-GMM5) in macro panel. The bias of the parameter is 0.036 (GL) and 0.000 (CRE-GMM5) in longitudinal; 0.194 (GL) and 0.111 (CRE-GMM2) in multilevel; 0.260 (GL) and 0.198 (CRE-GMM2) in macro panel.

The advantage of our approach over GL is even more evident for large and (multilevel panels) and (macro panels) for both and parameters. Having a longer improves the possibility to compute better the initial conditions and the CRE-GMM approach is less affected by the spurious persistence (note that for long the FE tends towards the true parameter for ). When individual heterogeneity matters and is correlated with the variable, our approach once again outperforms the GL and is in line with FE. Standard endogeneity produces bias in the FE estimates, at least for , while our method is less affected. With the two sources of endogeneity, the bias of the CRE-GMM approach is in general lower than that of GL. The moment conditions based on the pre-sample individual average of , if exploited, does not affect the results; the moment conditions based on the pre-sample individual average of does the same only as increases and both and .

Longitudinal panel , . Parameter RE FE CRE1 CRE2 GL CRE-GMM CRE-GMM1 CRE-GMM2 CRE-GMM3 CRE-GMM4 CRE-GMM5 bias 0.263 -0.080 0.175 0.175 0.011 0.054 0.027 0.026 0.044 0.018 0.019 ese 0.004 0.007 0.007 0.007 0.018 0.013 0.019 0.022 0.014 0.017 0.017 bias 0.354 -0.038 0.161 0.195 0.050 0.108 0.070 0.070 0.081 0.039 0.042 ese 0.005 0.005 0.009 0.009 0.031 0.013 0.023 0.029 0.014 0.022 0.020 bias 0.188 -0.110 0.108 0.131 0.006 0.052 0.022 0.021 0.038 0.017 0.013 ese 0.007 0.007 0.009 0.007 0.018 0.014 0.020 0.023 0.014 0.018 0.018 bias 0.323 -0.057 0.129 0.163 0.048 0.109 0.069 0.070 0.080 0.037 0.040 ese 0.006 0.005 0.009 0.009 0.031 0.013 0.022 0.030 0.014 0.021 0.019 bias -0.002 -0.138 -0.043 -0.018 -0.001 0.049 0.009 0.007 0.022 -0.002 0.000 ese 0.006 0.004 0.006 0.007 0.018 0.014 0.021 0.025 0.015 0.017 0.017 bias 0.225 -0.084 0.051 0.082 0.046 0.117 0.067 0.067 0.080 0.030 0.036 ese 0.007 0.004 0.007 0.008 0.032 0.014 0.025 0.034 0.015 0.024 0.021 bias 0.233 -0.080 0.134 0.138 0.011 0.060 0.054 0.031 0.067 0.061 0.059 ese 0.004 0.007 0.006 0.006 0.019 0.012 0.014 0.020 0.013 0.013 0.013 bias 0.326 -0.038 0.136 0.168 0.056 0.107 0.109 0.077 0.095 0.104 0.092 ese 0.004 0.005 0.008 0.008 0.031 0.011 0.012 0.025 0.012 0.012 0.014 bias 0.148 -0.078 0.077 0.076 0.010 0.043 0.042 0.030 0.047 0.040 0.040 ese 0.004 0.007 0.006 0.006 0.017 0.012 0.012 0.016 0.013 0.013 0.013 bias 0.238 -0.038 0.099 0.118 0.052 0.085 0.087 0.068 0.091 0.077 0.073 ese 0.003 0.005 0.006 0.006 0.028 0.010 0.012 0.019 0.011 0.011 0.013 bias 0.176 -0.110 0.081 0.091 0.006 0.062 0.054 0.028 0.072 0.064 0.062 ese 0.005 0.007 0.007 0.006 0.018 0.013 0.014 0.021 0.013 0.013 0.014 bias 0.300 -0.057 0.105 0.136 0.052 0.110 0.110 0.076 0.097 0.107 0.094 ese 0.004 0.005 0.008 0.008 0.032 0.012 0.012 0.027 0.012 0.012 0.015 bias 0.022 -0.138 -0.044 -0.029 -0.004 0.067 0.049 0.013 0.076 0.072 0.071 ese 0.005 0.004 0.005 0.006 0.019 0.014 0.016 0.025 0.014 0.015 0.015 bias 0.221 -0.084 0.034 0.062 0.042 0.119 0.116 0.072 0.101 0.117 0.104 ese 0.006 0.004 0.006 0.007 0.030 0.013 0.013 0.029 0.013 0.013 0.016 bias 0.080 -0.110 0.020 0.018 0.003 0.043 0.043 0.027 0.047 0.040 0.040 ese 0.004 0.007 0.005 0.005 0.017 0.013 0.013 0.017 0.013 0.014 0.014 bias 0.212 -0.057 0.070 0.088 0.046 0.088 0.090 0.068 0.095 0.078 0.075 ese 0.003 0.005 0.006 0.006 0.029 0.010 0.012 0.020 0.011 0.011 0.013

Macro panel , . Parameter RE FE CRE1 CRE2 GL CRE-GMM CRE-GMM1 CRE-GMM2 CRE-GMM3 CRE-GMM4 CRE-GMM5 bias 0.185 -0.017 0.118 0.091 0.112 0.049 0.049 0.048 0.042 0.041 0.041 ese 0.015 0.018 0.029 0.027 0.028 0.029 0.029 0.029 0.027 0.027 0.027 bias 0.399 -0.008 0.193 0.122 0.337 0.072 0.071 0.071 0.057 0.056 0.056 ese 0.009 0.012 0.037 0.030 0.023 0.029 0.029 0.029 0.026 0.026 0.026 bias 0.229 -0.058 0.114 0.067 0.146 0.025 0.025 0.024 0.010 0.009 0.009 ese 0.013 0.017 0.034 0.030 0.029 0.031 0.031 0.031 0.027 0.027 0.028 bias 0.388 -0.028 0.180 0.104 0.323 0.056 0.055 0.055 0.039 0.038 0.038 ese 0.009 0.012 0.039 0.031 0.022 0.029 0.029 0.029 0.026 0.026 0.026 bias 0.113 -0.109 0.041 -0.001 0.047 -0.038 -0.039 -0.039 -0.050 -0.050 -0.050 ese 0.016 0.012 0.031 0.027 0.025 0.025 0.025 0.025 0.023 0.023 0.023 bias 0.381 -0.061 0.153 0.072 0.329 0.026 0.025 0.025 0.009 0.009 0.009 ese 0.017 0.010 0.044 0.032 0.023 0.028 0.028 0.027 0.025 0.025 0.025 bias 0.246 -0.017 0.110 0.097 0.186 0.055 0.054 0.054 0.063 0.060 0.057 ese 0.012 0.018 0.028 0.027 0.025 0.030 0.030 0.030 0.029 0.030 0.030 bias 0.355 -0.008 0.155 0.115 0.323 0.069 0.068 0.068 0.066 0.068 0.068 ese 0.009 0.012 0.032 0.028 0.019 0.027 0.027 0.027 0.026 0.027 0.027 bias 0.140 -0.017 0.059 0.057 0.105 0.031 0.030 0.030 0.045 0.038 0.031 ese 0.012 0.019 0.020 0.020 0.022 0.026 0.026 0.026 0.025 0.026 0.027 bias 0.249 -0.008 0.100 0.089 0.236 0.053 0.053 0.052 0.066 0.058 0.051 ese 0.008 0.013 0.022 0.021 0.016 0.023 0.023 0.023 0.022 0.023 0.023 bias 0.139 -0.058 0.053 0.041 0.083 0.010 0.010 0.009 0.015 0.013 0.012 ese 0.013 0.017 0.025 0.024 0.026 0.027 0.027 0.027 0.026 0.026 0.026 bias 0.345 -0.028 0.137 0.096 0.314 0.051 0.050 0.050 0.048 0.050 0.049 ese 0.009 0.012 0.031 0.027 0.018 0.026 0.026 0.026 0.025 0.026 0.026 bias 0.103 -0.108 0.005 -0.011 0.047 -0.043 -0.044 -0.044 -0.031 -0.034 -0.036 ese 0.012 0.012 0.024 0.023 0.022 0.023 0.023 0.023 0.023 0.023 0.023 bias 0.289 -0.060 0.098 0.059 0.250 0.017 0.017 0.016 0.018 0.019 0.017 ese 0.015 0.010 0.033 0.027 0.022 0.025 0.025 0.025 0.024 0.025 0.025 bias 0.079 -0.058 0.008 0.006 0.057 -0.009 -0.009 -0.010 0.002 -0.003 -0.011 ese 0.012 0.017 0.018 0.018 0.022 0.024 0.024 0.024 0.023 0.024 0.025 bias 0.221 -0.028 0.078 0.067 0.206 0.034 0.034 0.033 0.048 0.040 0.033 ese 0.008 0.012 0.021 0.021 0.017 0.022 0.022 0.022 0.022 0.023 0.023

Multilevel panel , . Parameter RE FE CRE1 CRE2 GL CRE-GMM CRE-GMM1 CRE-GMM2 CRE-GMM3 CRE-GMM4 CRE-GMM5 bias 0.257 -0.035 0.163 0.147 0.075 0.039 0.038 0.038 0.035 0.034 0.033 ese 0.009 0.014 0.018 0.018 0.030 0.025 0.025 0.027 0.025 0.025 0.025 bias 0.395 -0.016 0.217 0.186 0.231 0.067 0.065 0.066 0.051 0.050 0.049 ese 0.010 0.010 0.023 0.019 0.036 0.023 0.023 0.026 0.024 0.024 0.024 bias 0.207 -0.073 0.123 0.104 0.053 0.021 0.020 0.020 0.011 0.010 0.009 ese 0.009 0.013 0.018 0.019 0.029 0.025 0.025 0.026 0.025 0.026 0.026 bias 0.357 -0.036 0.186 0.165 0.195 0.056 0.054 0.055 0.039 0.038 0.037 ese 0.015 0.010 0.026 0.020 0.038 0.024 0.024 0.026 0.024 0.024 0.024 bias 0.054 -0.117 0.008 0.018 -0.001 -0.021 -0.023 -0.024 -0.031 -0.032 -0.032 ese 0.020 0.009 0.020 0.019 0.027 0.023 0.023 0.025 0.023 0.023 0.023 bias 0.316 -0.067 0.116 0.110 0.220 0.044 0.042 0.043 0.023 0.022 0.022 ese 0.019 0.008 0.026 0.025 0.039 0.025 0.025 0.029 0.025 0.026 0.026 bias 0.205 -0.035 0.117 0.114 0.060 0.035 0.034 0.032 0.059 0.048 0.046 ese 0.009 0.015 0.016 0.016 0.028 0.024 0.024 0.025 0.024 0.025 0.024 bias 0.342 -0.017 0.173 0.162 0.215 0.062 0.061 0.059 0.077 0.067 0.066 ese 0.008 0.010 0.019 0.016 0.033 0.022 0.022 0.024 0.022 0.023 0.023 bias 0.145 -0.035 0.071 0.070 0.060 0.026 0.025 0.024 0.049 0.029 0.025 ese 0.009 0.015 0.013 0.013 0.024 0.023 0.023 0.023 0.023 0.024 0.024 bias 0.250 -0.016 0.117 0.117 0.197 0.052 0.050 0.048 0.086 0.051 0.048 ese 0.006 0.010 0.013 0.013 0.025 0.019 0.020 0.020 0.019 0.021 0.021 bias 0.167 -0.073 0.076 0.073 0.044 0.017 0.016 0.015 0.042 0.028 0.026 ese 0.009 0.013 0.015 0.015 0.029 0.023 0.023 0.025 0.024 0.024 0.024 bias 0.338 -0.036 0.152 0.147 0.235 0.058 0.058 0.056 0.073 0.062 0.060 ese 0.009 0.010 0.021 0.017 0.035 0.022 0.023 0.025 0.023 0.024 0.024 bias 0.066 -0.117 -0.009 0.003 -0.002 -0.019 -0.020 -0.024 0.015 -0.000 -0.004 ese 0.015 0.009 0.016 0.015 0.027 0.020 0.020 0.023 0.021 0.023 0.022 bias 0.259 -0.067 0.076 0.087 0.182 0.039 0.039 0.036 0.056 0.045 0.043 ese 0.014 0.008 0.020 0.021 0.037 0.022 0.022 0.025 0.023 0.024 0.024 bias 0.083 -0.073 0.017 0.017 0.033 0.004 0.004 0.003 0.026 0.005 0.001 ese 0.008 0.013 0.012 0.012 0.025 0.022 0.022 0.022 0.022 0.024 0.023 bias 0.228 -0.036 0.093 0.095 0.186 0.042 0.040 0.039 0.079 0.041 0.037 ese 0.006 0.010 0.014 0.013 0.026 0.019 0.020 0.020 0.019 0.021 0.021

Longitudinal panel , . Parameter RE FE CRE1 CRE2 GL CRE-GMM CRE-GMM1 CRE-GMM2 CRE-GMM3 CRE-GMM4 CRE-GMM5 bias -0.174 0.017 -0.122 -0.112 -0.019 -0.069 -0.036 -0.035 -0.113 -0.048 -0.040 ese 0.014 0.012 0.013 0.013 0.050 0.044 0.047 0.052 0.041 0.045 0.044 bias -0.167 0.008 -0.083 -0.108 -0.097 -0.145 -0.096 -0.090 -0.208 -0.103 -0.088 ese 0.010 0.007 0.010 0.011 0.068 0.038 0.048 0.050 0.038 0.047 0.042 bias 0.046 0.231 0.096 0.078 -0.010 -0.082 -0.031 -0.028 -0.111 -0.033 -0.029 ese 0.015 0.011 0.015 0.013 0.055 0.049 0.054 0.056 0.047 0.052 0.051 bias -0.084 0.088 0.002 -0.021 -0.098 -0.162 -0.102 -0.095 -0.217 -0.100 -0.088 ese 0.011 0.007 0.010 0.011 0.070 0.040 0.050 0.052 0.040 0.051 0.045 bias 0.396 0.465 0.416 0.401 0.016 -0.089 -0.002 0.000 -0.072 0.014 0.011 ese 0.009 0.007 0.008 0.009 0.053 0.051 0.056 0.056 0.049 0.052 0.052 bias 0.091 0.223 0.163 0.147 -0.102 -0.201 -0.114 -0.108 -0.238 -0.088 -0.085 ese 0.009 0.006 0.008 0.009 0.072 0.046 0.059 0.060 0.048 0.057 0.052 bias -0.034 0.017 -0.014 -0.015 -0.009 -0.025 0.000 -0.019 0.005 -0.033 -0.035 ese 0.013 0.012 0.012 0.012 0.050 0.042 0.048 0.051 0.040 0.043 0.043 bias -0.078 0.008 -0.030 -0.051 -0.087 -0.105 -0.074 -0.072 -0.114 -0.102 -0.100 ese 0.010 0.007 0.008 0.009 0.068 0.035 0.042 0.045 0.032 0.033 0.032 bias 0.060 0.017 0.042 0.042 0.019 0.014 0.013 0.005 0.079 -0.003 -0.002 ese 0.012 0.012 0.011 0.011 0.047 0.039 0.043 0.044 0.038 0.041 0.042 bias 0.013 0.008 0.015 0.006 -0.040 -0.048 -0.042 -0.038 -0.036 -0.049 -0.053 ese 0.009 0.007 0.007 0.008 0.056 0.029 0.032 0.034 0.030 0.030 0.030 bias 0.179 0.231 0.200 0.193 0.003 -0.041 -0.008 -0.016 -0.017 -0.052 -0.053 ese 0.013 0.011 0.012 0.012 0.053 0.046 0.051 0.053 0.045 0.047 0.047 bias 0.008 0.088 0.055 0.036 -0.089 -0.121 -0.088 -0.079 -0.127 -0.119 -0.114 ese 0.010 0.007 0.008 0.009 0.070 0.037 0.043 0.046 0.034 0.035 0.035 bias 0.463 0.464 0.468 0.463 0.032 -0.074 -0.018 0.007 -0.086 -0.089 -0.091 ese 0.008 0.007 0.008 0.008 0.053 0.050 0.054 0.055 0.052 0.052 0.052 bias 0.171 0.223 0.205 0.194 -0.080 -0.160 -0.116 -0.089 -0.157 -0.157 -0.150 ese 0.008 0.006 0.007 0.007 0.069 0.042 0.048 0.054 0.040 0.041 0.041 bias 0.273 0.231 0.254 0.254 0.036 0.012 0.016 0.011 0.085 -0.002 0.000 ese 0.011 0.011 0.011 0.011 0.051 0.043 0.046 0.048 0.043 0.046 0.047 bias 0.103 0.088 0.100 0.093 -0.035 -0.058 -0.050 -0.041 -0.046 -0.056 -0.060 ese 0.008 0.007 0.007 0.008 0.062 0.032 0.033 0.037 0.033 0.032 0.032

Macro panel , . Parameter RE FE CRE1 CRE2 GL CRE-GMM CRE-GMM1 CRE-GMM2 CRE-GMM3 CRE-GMM4 CRE-GMM5 bias -0.121 0.010 -0.078 -0.058 -0.121 -0.057 -0.056 -0.055 -0.065 -0.064 -0.063 ese 0.038 0.031 0.038 0.037 0.069 0.064 0.064 0.065 0.065 0.065 0.066 bias -0.262 0.004 -0.128 -0.078 -0.368 -0.083 -0.082 -0.081 -0.087 -0.086 -0.084 ese 0.035 0.019 0.036 0.029 0.061 0.049 0.049 0.049 0.051 0.051 0.051 bias -0.000 0.219 0.087 0.127 -0.068 0.086 0.086 0.087 0.080 0.081 0.082 ese 0.042 0.030 0.043 0.039 0.077 0.069 0.070 0.070 0.070 0.070 0.070 bias -0.206 0.085 -0.061 -0.005 -0.336 -0.024 -0.023 -0.022 -0.026 -0.025 -0.024 ese 0.037 0.019 0.039 0.031 0.062 0.051 0.051 0.051 0.053 0.053 0.053 bias 0.265 0.460 0.329 0.371 0.175 0.305 0.306 0.306 0.310 0.310 0.310 ese 0.038 0.022 0.040 0.034 0.065 0.057 0.057 0.057 0.057 0.057 0.057 bias -0.114 0.220 0.058 0.123 -0.318 0.079 0.080 0.081 0.082 0.083 0.084 ese 0.041 0.016 0.043 0.031 0.068 0.052 0.051 0.051 0.052 0.051 0.051 bias -0.033 0.010 -0.013 -0.011 -0.052 -0.017 -0.016 -0.016 -0.013 -0.013 -0.014 ese 0.036 0.031 0.033 0.033 0.073 0.063 0.063 0.063 0.062 0.062 0.063 bias -0.144 0.005 -0.062 -0.045 -0.242 -0.053 -0.053 -0.052 -0.054 -0.053 -0.052 ese 0.031 0.019 0.028 0.025 0.057 0.044 0.045 0.045 0.044 0.044 0.044 bias 0.061 0.010 0.029 0.029 0.081 0.025 0.025 0.026 0.035 0.031 0.026 ese 0.034 0.033 0.033 0.033 0.062 0.059 0.060 0.060 0.061 0.061 0.061 bias -0.014 0.005 -0.004 -0.004 -0.050 -0.010 -0.010 -0.010 -0.012 -0.011 -0.010 ese 0.026 0.020 0.022 0.022 0.052 0.040 0.040 0.041 0.040 0.041 0.041 bias 0.180 0.220 0.196 0.198 0.122 0.150 0.151 0.151 0.154 0.154 0.155 ese 0.036 0.030 0.034 0.033 0.071 0.063 0.064 0.064 0.062 0.062 0.062 bias -0.075 0.085 0.014 0.032 -0.200 0.010 0.011 0.012 0.011 0.011 0.012 ese 0.033 0.020 0.030 0.026 0.062 0.046 0.046 0.046 0.046 0.046 0.047 bias 0.408 0.461 0.433 0.437 0.307 0.366 0.366 0.366 0.363 0.364 0.365 ese 0.032 0.022 0.028 0.027 0.060 0.050 0.050 0.050 0.049 0.049 0.049 bias 0.059 0.221 0.148 0.166 -0.094 0.122 0.123 0.123 0.122 0.122 0.123 ese 0.034 0.017 0.030 0.026 0.063 0.045 0.045 0.045 0.044 0.044 0.044 bias 0.275 0.220 0.241 0.241 0.260 0.197 0.198 0.198 0.207 0.205 0.201 ese 0.034 0.033 0.033 0.033 0.064 0.061 0.061 0.061 0.061 0.062 0.061 bias 0.069 0.085 0.078 0.078 0.017 0.056 0.056 0.057 0.054 0.055 0.056 ese 0.026 0.020 0.023 0.022 0.052 0.041 0.041 0.041 0.041 0.041 0.041

Multilevel panel , . Parameter RE FE CRE1 CRE2 GL CRE-GMM CRE-GMM1 CRE-GMM2 CRE-GMM3 CRE-GMM4 CRE-GMM5 bias -0.171 0.015 -0.111 -0.095 -0.119 -0.064 -0.062 -0.060 -0.075 -0.073 -0.070 ese 0.030 0.024 0.031 0.030 0.079 0.070 0.070 0.070 0.072 0.072 0.072 bias -0.255 0.007 -0.143 -0.120 -0.367 -0.106 -0.103 -0.101 -0.107 -0.104 -0.101 ese 0.027 0.015 0.027 0.023 0.084 0.055 0.055 0.055 0.056 0.056 0.055 bias 0.015 0.226 0.078 0.098 -0.051 0.010 0.012 0.014 0.009 0.011 0.013 ese 0.031 0.023 0.031 0.030 0.086 0.075 0.075 0.075 0.077 0.077 0.077 bias -0.173 0.087 -0.062 -0.047 -0.322 -0.078 -0.074 -0.072 -0.074 -0.071 -0.068 ese 0.030 0.015 0.029 0.025 0.091 0.059 0.059 0.059 0.060 0.060 0.060 bias 0.329 0.463 0.365 0.356 0.106 0.156 0.159 0.160 0.171 0.173 0.174 ese 0.027 0.016 0.026 0.027 0.081 0.070 0.070 0.070 0.069 0.069 0.069 bias -0.030 0.222 0.100 0.102 -0.382 -0.035 -0.032 -0.030 -0.018 -0.016 -0.014 ese 0.028 0.012 0.026 0.027 0.102 0.065 0.065 0.065 0.065 0.065 0.065 bias -0.029 0.015 -0.014 -0.014 -0.027 -0.016 -0.015 -0.014 0.003 -0.007 -0.009 ese 0.027 0.024 0.026 0.026 0.075 0.068 0.069 0.069 0.069 0.070 0.070 bias -0.136 0.007 -0.068 -0.064 -0.259 -0.068 -0.066 -0.064 -0.074 -0.070 -0.068 ese 0.023 0.015 0.021 0.020 0.078 0.051 0.051 0.051 0.051 0.051 0.051 bias 0.060 0.015 0.034 0.034 0.078 0.016 0.016 0.016 0.057 0.025 0.018 ese 0.025 0.024 0.024 0.024 0.070 0.066 0.067 0.067 0.066 0.069 0.069 bias -0.015 0.007 -0.003 -0.005 -0.098 -0.026 -0.025 -0.025 -0.034 -0.029 -0.026 ese 0.019 0.015 0.017 0.017 0.066 0.048 0.048 0.048 0.049 0.048 0.048 bias 0.175 0.226 0.193 0.194 0.048 0.068 0.069 0.069 0.080 0.076 0.073 ese 0.027 0.024 0.026 0.026 0.082 0.072 0.073 0.074 0.075 0.075 0.075 bias -0.065 0.087 0.011 0.010 -0.289 -0.048 -0.046 -0.044 -0.052 -0.047 -0.045 ese 0.025 0.015 0.023 0.021 0.089 0.056 0.056 0.056 0.056 0.056 0.056 bias 0.427 0.463 0.444 0.437 0.180 0.207 0.208 0.211 0.182 0.194 0.196 ese 0.021 0.015 0.018 0.019 0.077 0.064 0.064 0.064 0.066 0.066 0.065 bias 0.099 0.222 0.169 0.160 -0.222 0.012 0.014 0.017 0.002 0.011 0.013 ese 0.023 0.012 0.018 0.020 0.093 0.057 0.057 0.057 0.056 0.057 0.056 bias 0.275 0.226 0.247 0.247 0.194 0.112 0.112 0.111 0.154 0.129 0.120 ese 0.024 0.023 0.023 0.023 0.076 0.069 0.070 0.070 0.070 0.070 0.070 bias 0.070 0.087 0.080 0.078 -0.068 0.009 0.009 0.010 -0.003 0.007 0.011 ese 0.019 0.015 0.017 0.017 0.069 0.049 0.049 0.050 0.051 0.050 0.050

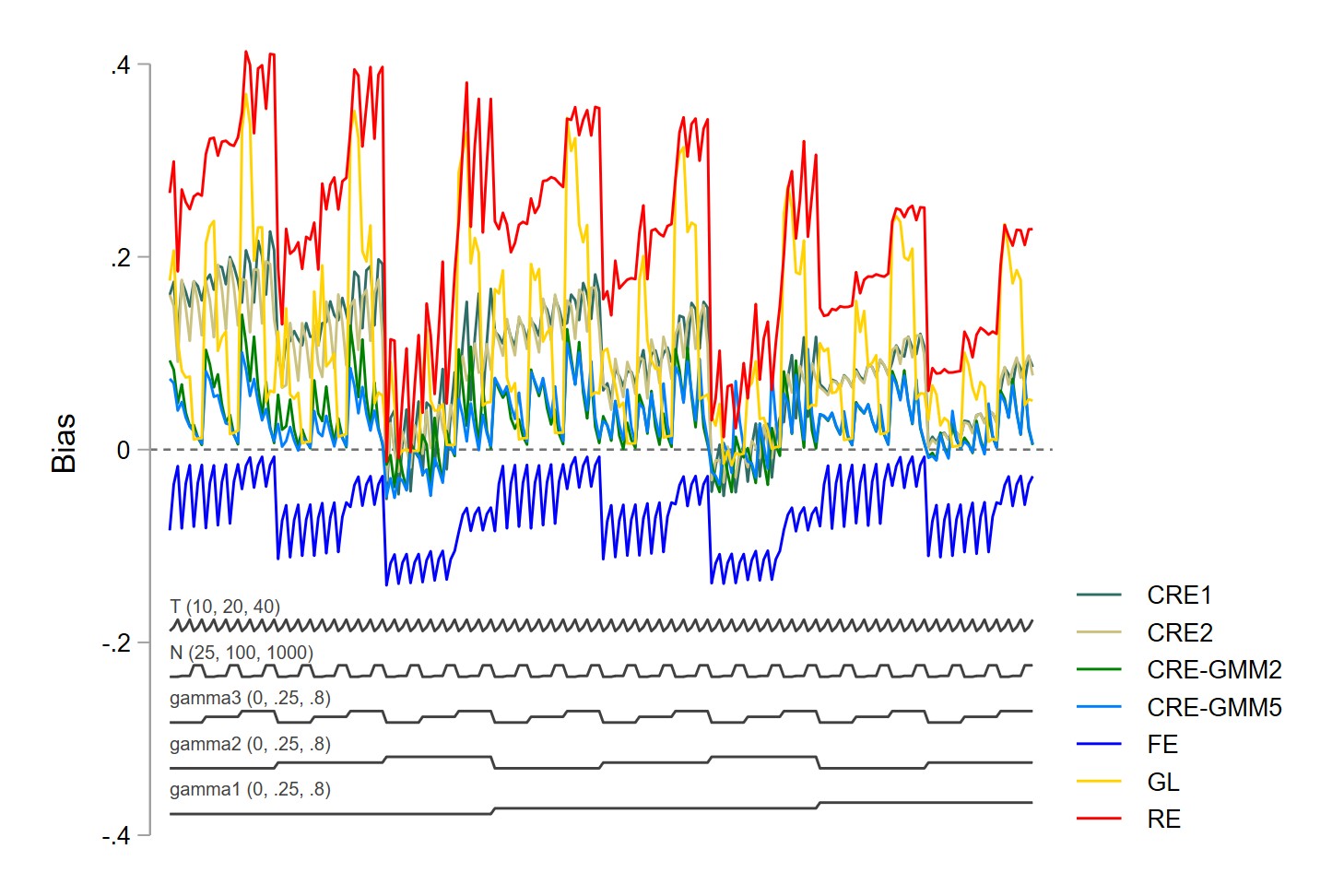

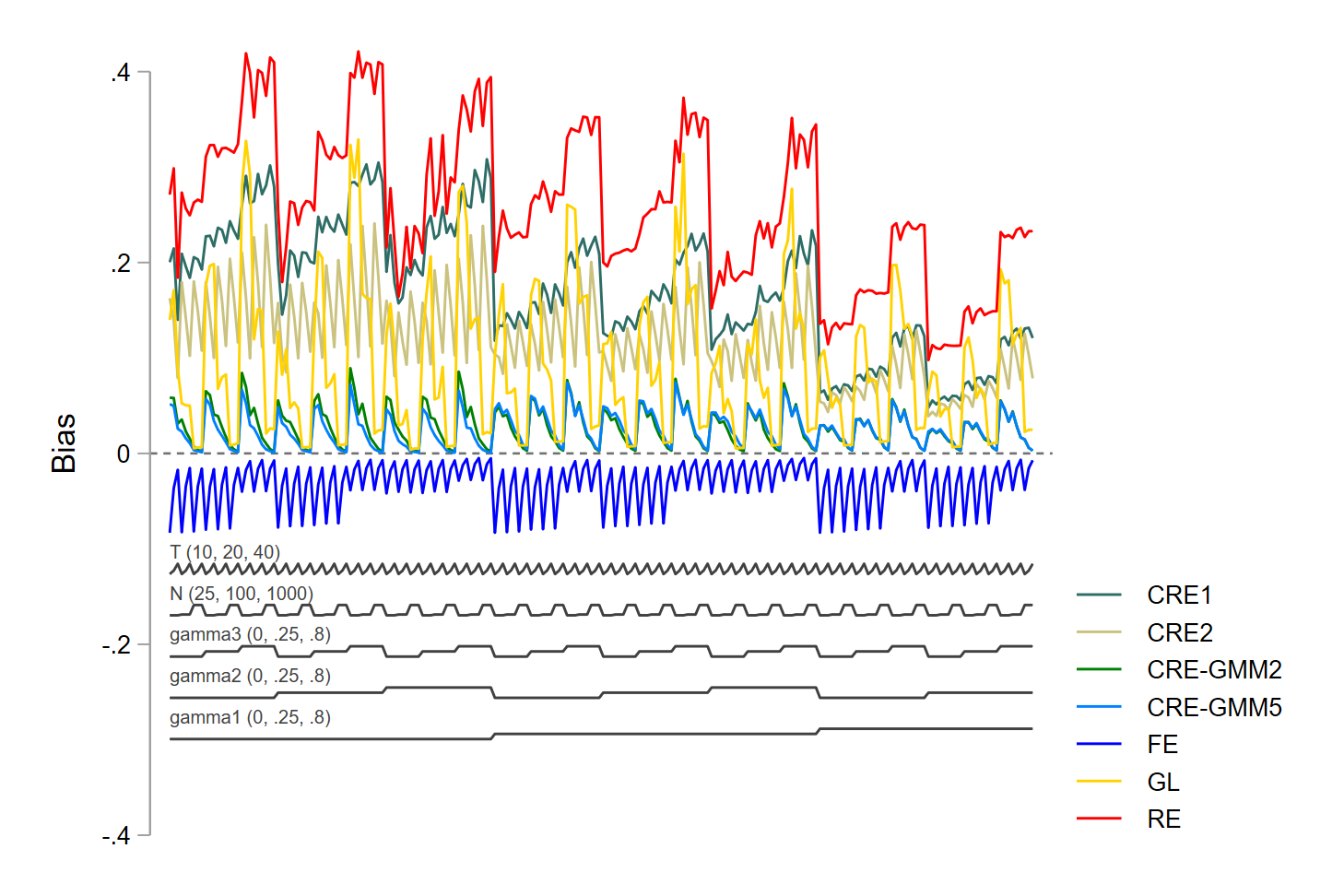

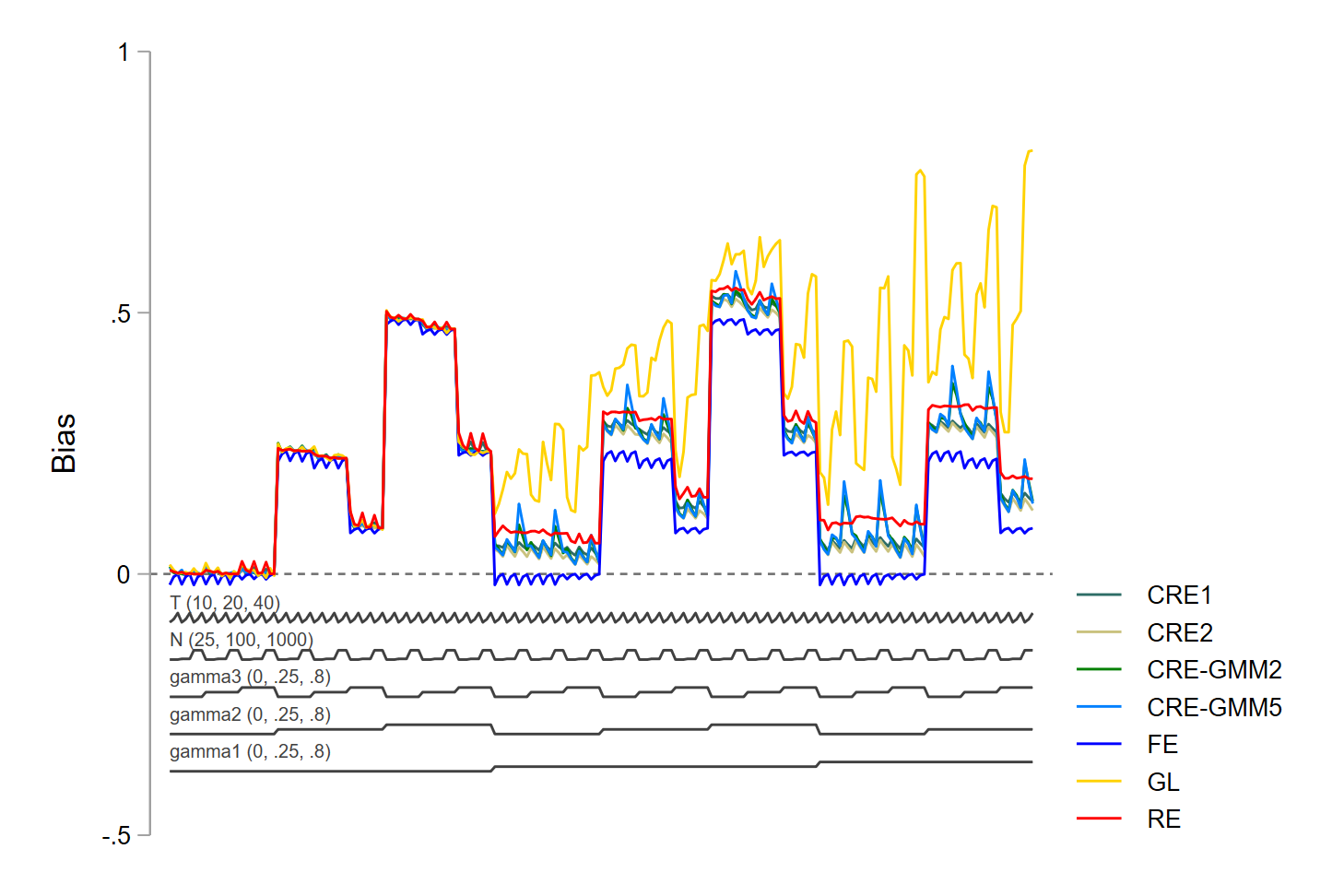

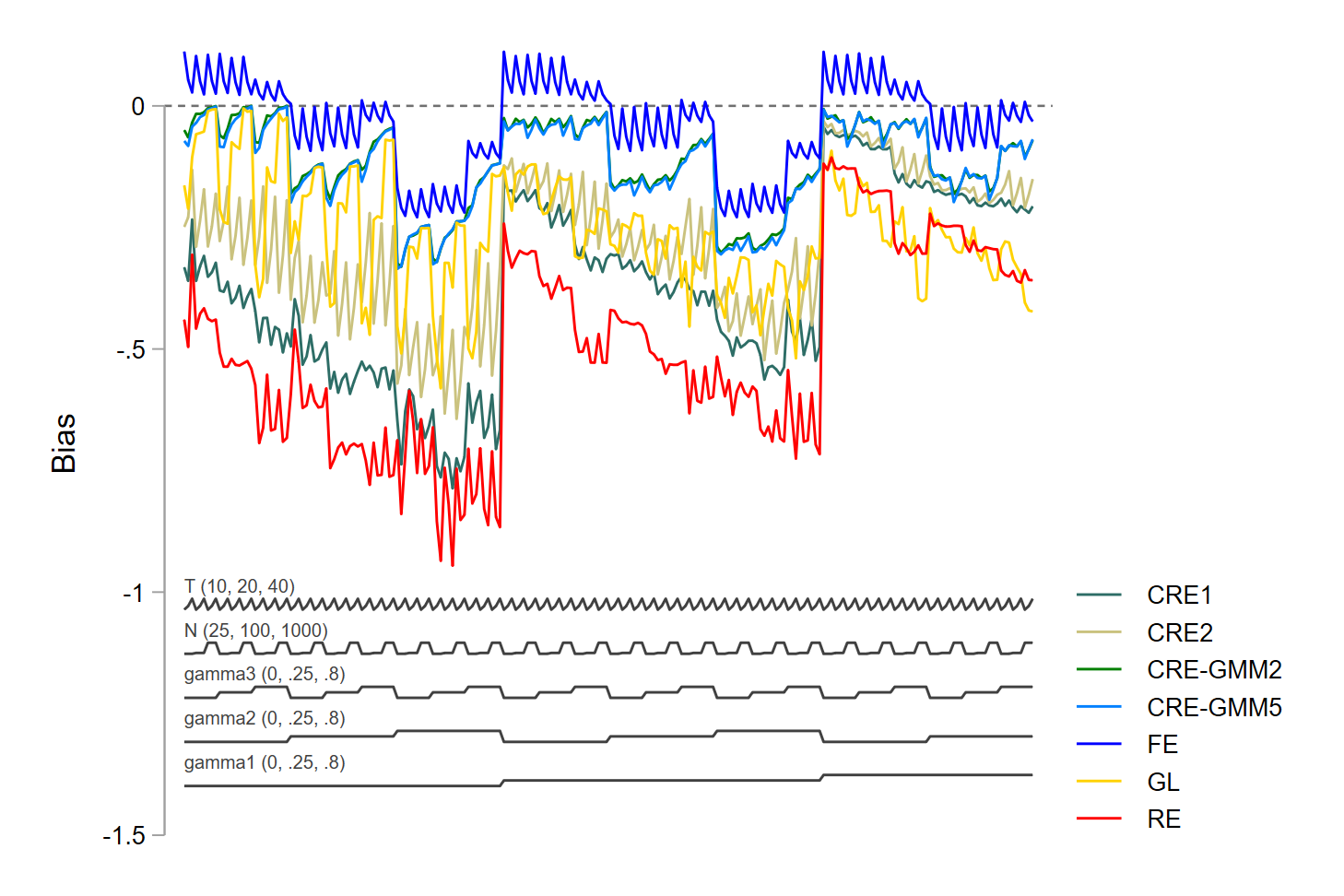

Figures 1-2 shows the role of alternative values for , the endogeneity due to heterogeneity, under alternative panel’s settings and the case, where is the variance of individual heterogeneity, , and is the variance of the shocks . Figures 3-4 shows how results change when the variance of individual heterogeneity is higher than the variance of the shocks, . Figures 5-6 and Figures 7-8 compare the cases and when standard endogeneity, due to the correlation between and the idiosyncratic shocks through , is added to the endogeneity due to heterogeneity. To extend the picture of results provided by the Tables, where , in the Figures we present the case of .

Boxplot for bias of with .

and are on the horizontal axis.

Boxplot for bias of with .

and are on the horizontal axis.

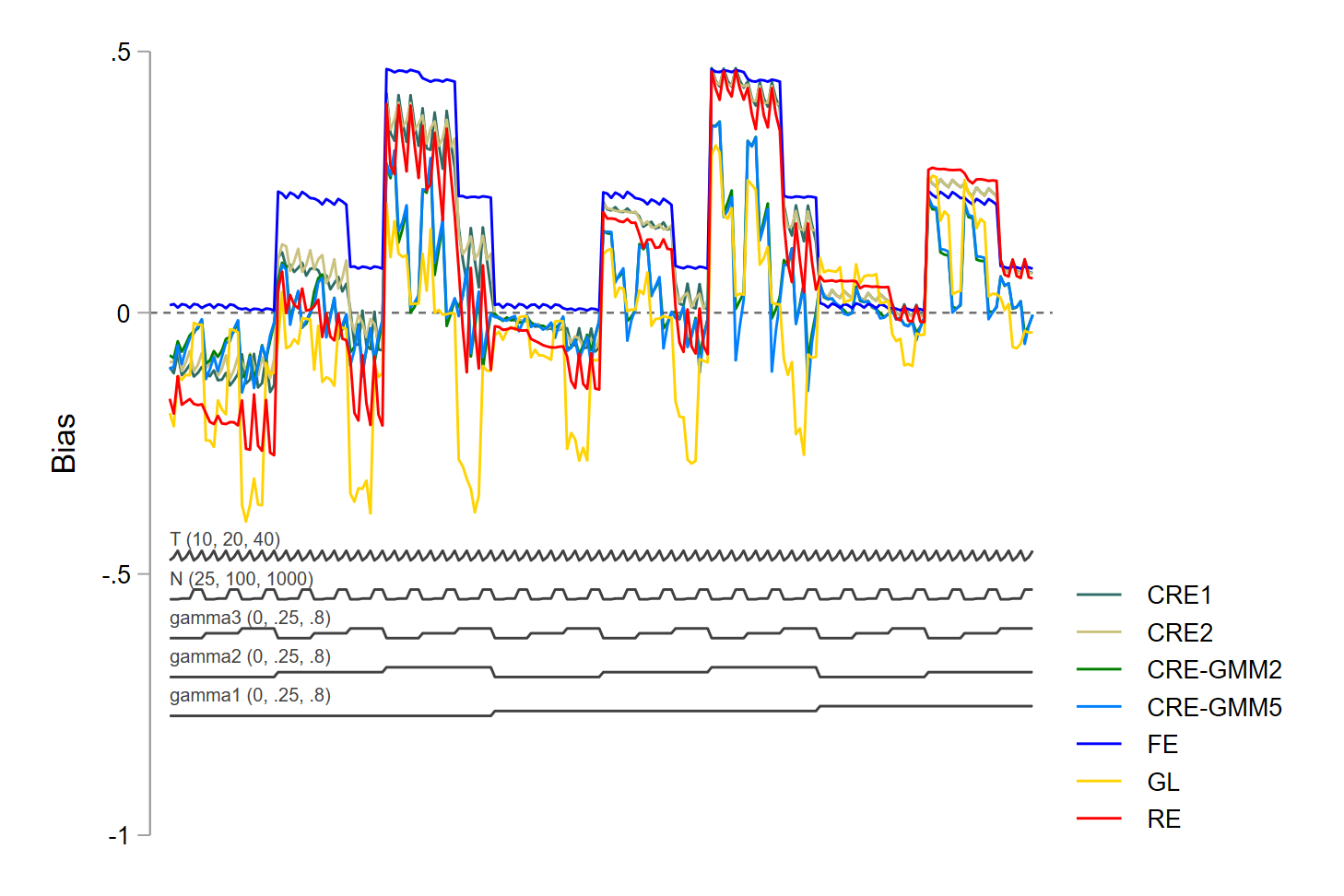

Boxplot for bias of with and higher variation in than error component , .

and are on the horizontal axis.

Boxplot for bias of with and higher variation in than error component , .

and are on the horizontal axis.

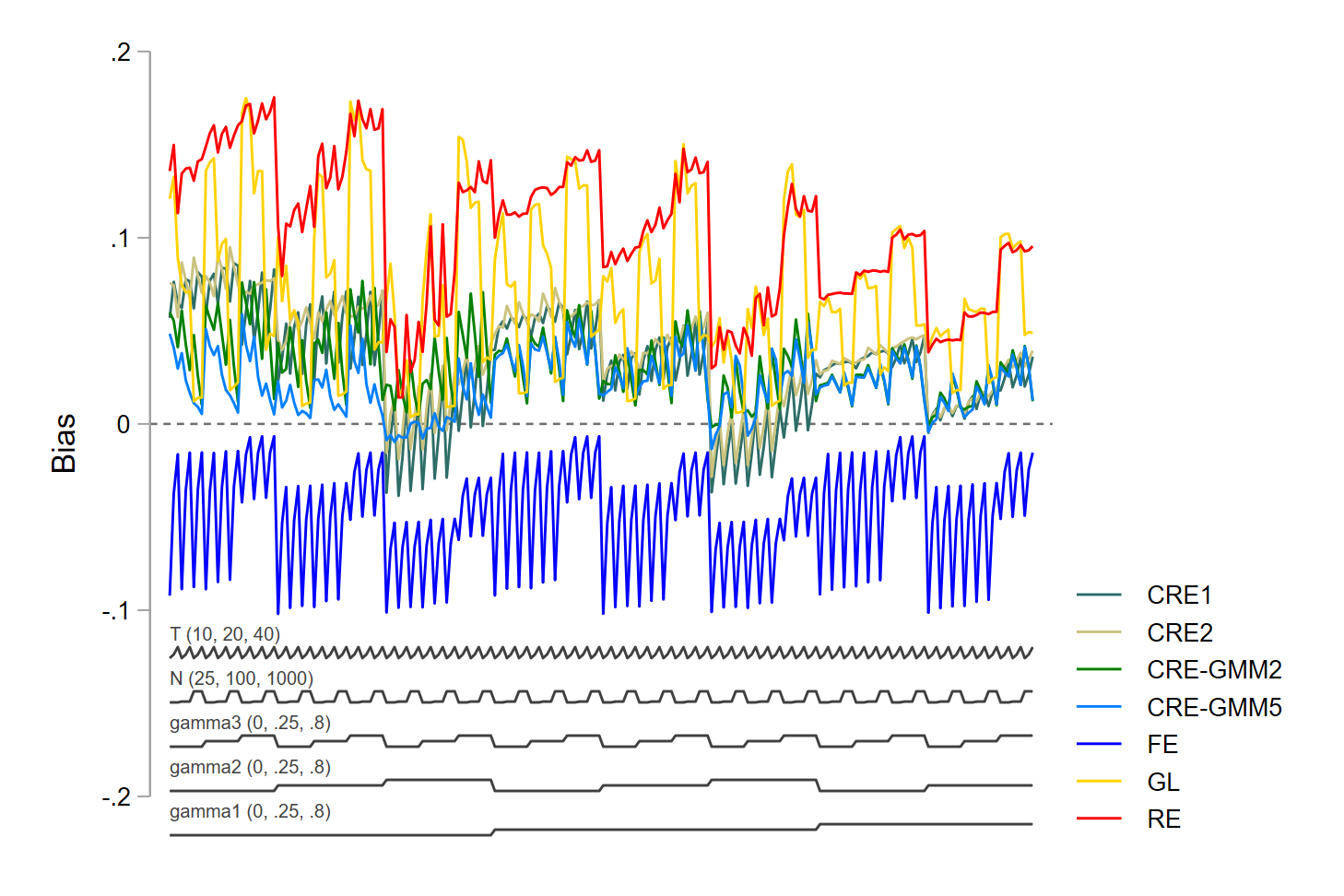

Boxplot for bias of with correlation between and error , .

and are on the horizontal axis.

Boxplot for bias of with correlation between and error , .

and are on the horizontal axis.

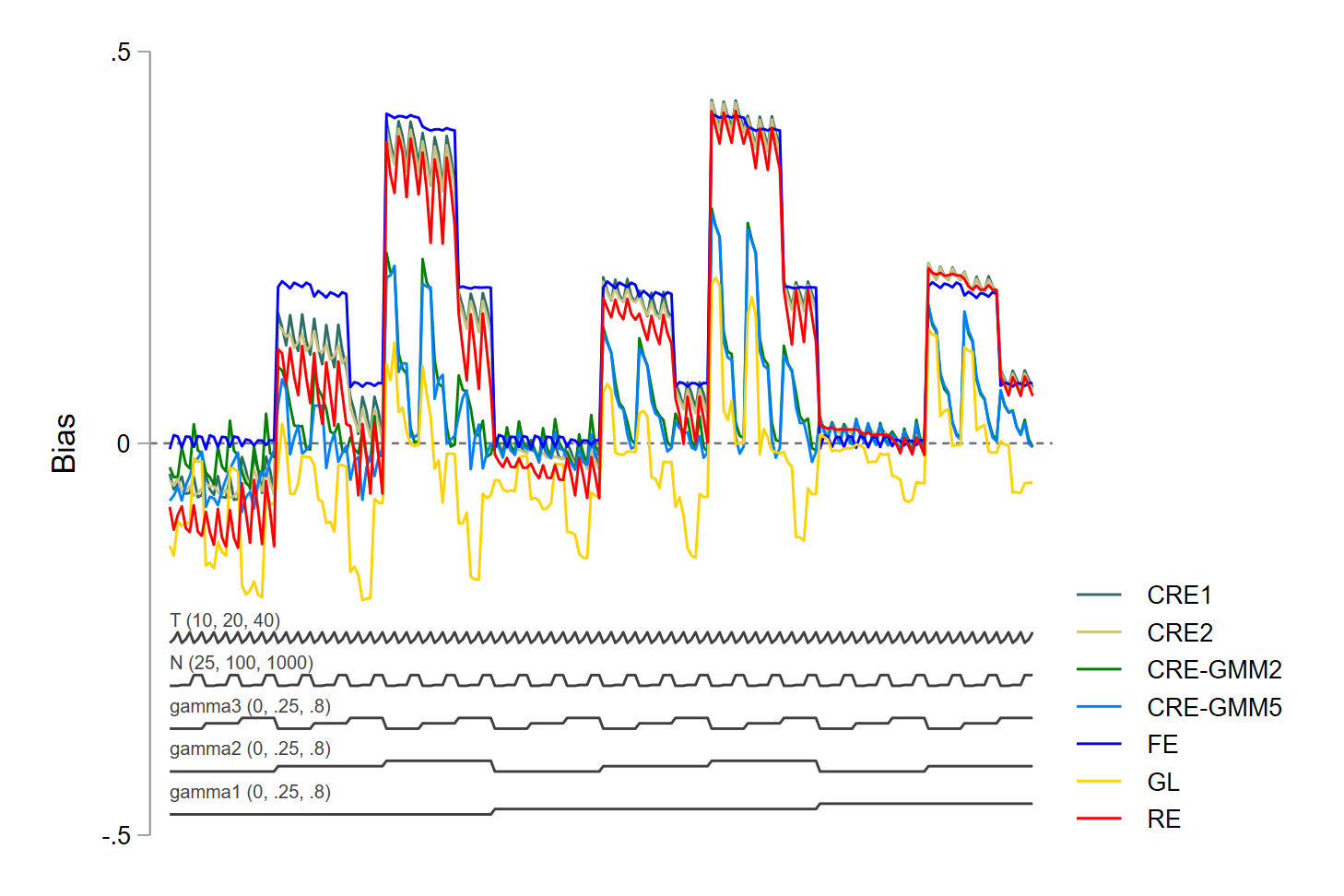

Boxplot for bias of with correlation between and error , , and higher variation in than error component , .

and are on the horizontal axis.

Boxplot for bias of with correlation between and error , , and higher variation in than error component , .

and are on the horizontal axis.

Figures 9 and 10 present the bias for and in form of a nestloop plot [87] which allows for a straightforward comparison across parametrisations.181818The plots are produced using siman suite in Stata [68]. The different parametrisations are on the horizontal axis. The different lines represent the different methods. If in longitudinal panels, CRE-GMM2 is better when and CRE-GMM5 when , this difference disappears as . Figures 11 and 12 show the bias when the autoregressive parameter is equal to 0.8.191919The detailed results are in Tables A2-A7 of Appendix A.3. The level equations (CRE-GMM3-CRE-GMM5) deal better with the persistence, and exploiting the additional moment conditions based on the pre-sample average of and reduces the bias particularly in the presence of both sources of endogeneity.

Bias for across different specifications. Parameters shown on horizontal axis.

Bias for across different specifications. Parameters shown on horizontal axis.

Bias for across different specifications. Parameters shown on horizontal axis.

Bias for across different specifications. Parameters shown on horizontal axis.

5 Empirical applications

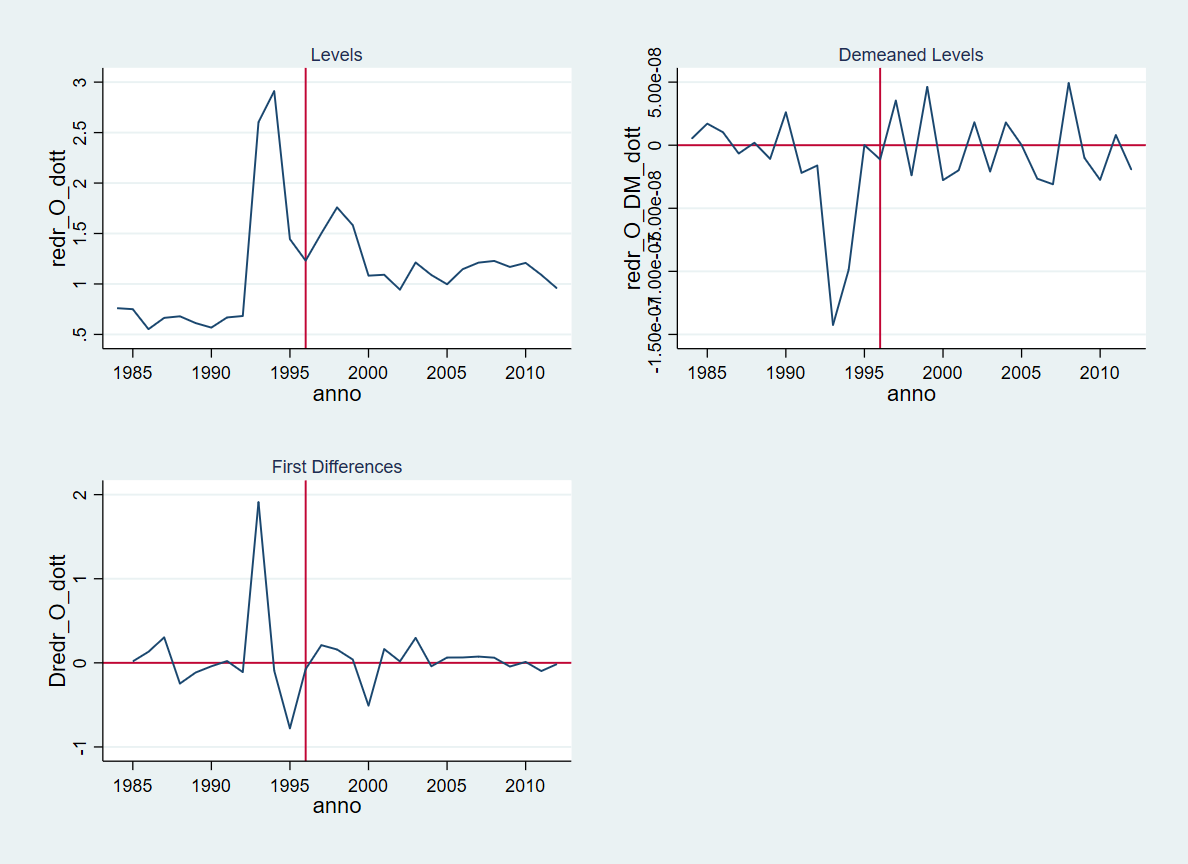

In this section we showcase our estimator on two examples. The first one investigates a specific shape of the production function and the role of net capital and employment on final output on a balanced panel. The second example exploits an unbalanced panel to study an important IO topic concerning the evaluation of the persistence of R&D activity. The role of accumulated knowledge has to be assessed inside a model that considers, in addition to the unit-and time-varying explanatory variables , also a list of time-invariant unit-specific measurable explanatory variables which are very important to capture the role of firm-specific market power.

5.1 Production functions estimation

We use the dataset in [26] to estimate a Cobb-Douglas production function in a sample of 509 US manufacturing firms observed through an eight-year period from 1982 to 1989. This dataset is the equivalent of the UK data used by [11] and successively largely analysed by the literature on dynamic panel data models. We estimate the following model:

where is the logarithm of sales, is the logarithm of employment, is the log of net capital stock, captures time effect and is firms’ heterogeneity..

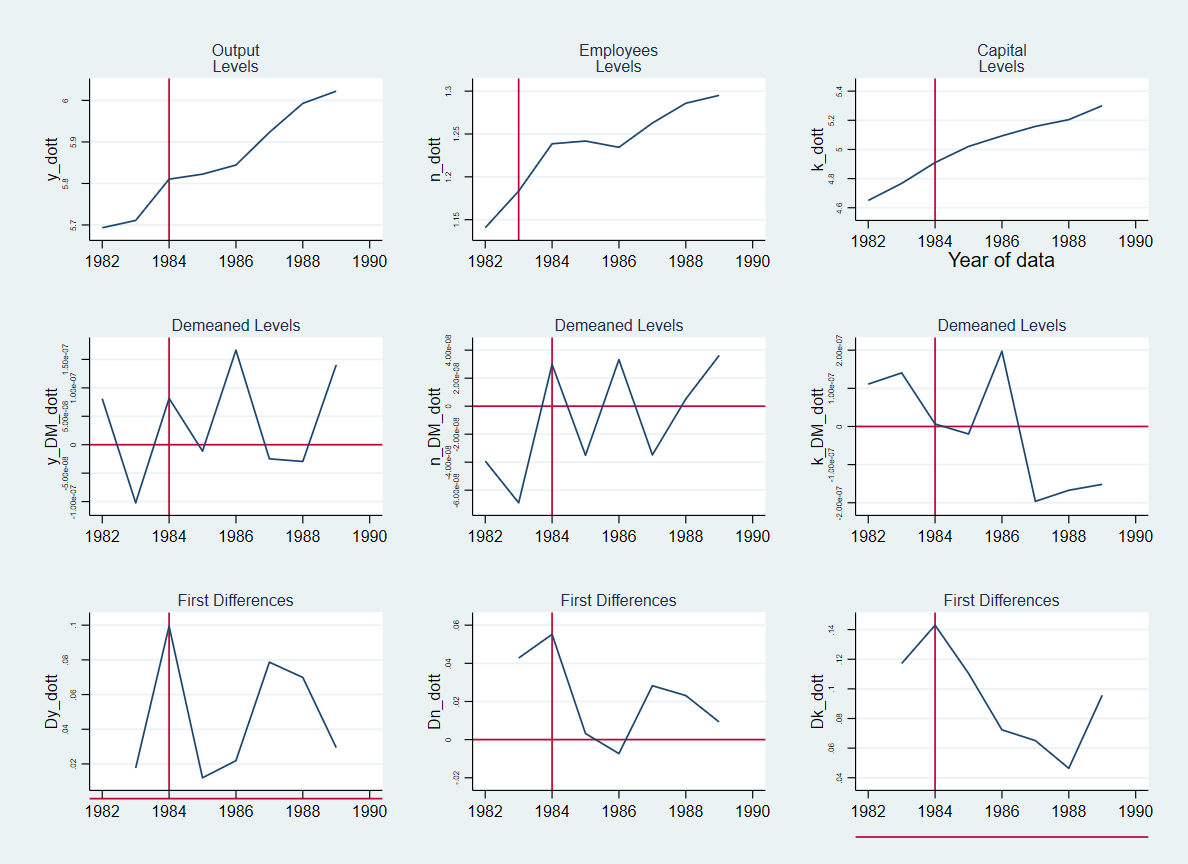

According to the ARDL(1,1,1) model, we need the individual averages of the lagged dependent variable , the current and lagged employment and net capital, , , and ; the period is short, so we selected years 1982-83 as the pre-sample period used to compute the individual averages, and the remaining years 1984-1989 to estimate the model. Table 8 compares the characteristics of the dependent variable in terms of variability over the entire period and the two sub-samples.

| Period | 1982-1989 | 1982-83 | 1984-89 |

|---|---|---|---|

| Between variability | 98.22% | 99.70% | 98.87% |

| Within variability | 1.78% | 0.30% | 1.13% |

| common to all the units | (0.31%) | (0%) | (0.17%) |

| unit-specific | (1.47%) | (0.30%) | (0.95%) |

The total variability of the dependent variable is dominated by the variation over the units, with the within variability being mostly firm-specific. Common factors like the business cycle and inflation, which may have the same influence across companies, play a marginal role when explaining within variability.

Figure 13 (and Dickey-Fuller tests not reported) confirms the persistence already noticed by [26]. Such high persistency leads to the potential weak IVs issue for GMM-dif. Both output and employment present a period of stagnation between 1984 and 1986, which could potentially underline the effects of the oil crisis following the Iranian Revolution in 1979, causing a global recession which influenced the US over the period 1980-1982. The average log output steeply increased over time, especially from 1986. Employment had rapid growth from the beginning period until 1984, starting to rise again in a consistent way from 1986. Besides, capital presents an increasing linear trend from 1982 until the last year considered.

| RE | FE | CRE1 | CRE2 | GL | CRE-GMM2 | CRE-GMM5 | MLtd | ML | QML | |

| L.y | 0.930*** | 0.378*** | 0.935*** | 0.864*** | 0.667*** | 0.694*** | 0.667*** | 0.928*** | 0.604*** | 0.546*** |

| (0.0094) | (0.0281) | (0.0114) | (0.0175) | (0.0466) | (0.0514) | (0.0491) | (0.0132) | (0.0483) | (0.0757) | |

| n | 0.454*** | 0.460*** | 0.453*** | 0.438*** | 0.459*** | 0.688*** | 0.779*** | 0.369*** | 0.520*** | 0.411*** |

| (0.0303) | (0.0325) | (0.0302) | (0.0338) | (0.1249) | (0.1630) | (0.1749) | (0.1127) | (0.0534) | (0.0426 | |

| L.n | -0.406*** | -0.004 | -0.406*** | -0.301*** | -0.232* | -0.360*** | -0.453*** | -0.335*** | -0.114** | -0.072 |

| (0.0316) | (0.0368) | (0.0315) | (0.0368) | (0.1265) | (0.1355) | (0.1571) | (0.0529) | (0.0544) | (0.0602) | |

| k | 0.238*** | 0.200*** | 0.235*** | 0.177*** | 0.573*** | 0.400** | 0.383** | 0.219* | 0.093* | 0.182*** |

| (0.0373) | (0.0377) | (0.0379) | (0.0431) | (0.1309) | (0.1955) | (0.1649) | (0.1205) | (0.0547) | (0.05489) | |

| L.k | -0.216*** | -0.125*** | -0.211*** | -0.222*** | -0.464*** | -0.460*** | -0.420*** | -0.204*** | -0.145*** | -0.177*** |

| (0.0361) | (0.0277) | (0.0371) | (0.0345) | (0.1162) | (0.1329) | (0.1252) | (0.0577) | (0.0370) | 0.0530 | |

| -0.007 | 0.079*** | 0.061 | 0.087 | |||||||

| (0.0084) | (0.0175) | (0.0630) | (0.0598) | |||||||

| 0.026 | -0.165* | -0.090 | ||||||||

| (0.0278) | (0.0961) | (0.0748) | ||||||||

| -0.129*** | -0.105** | -0.101** | ||||||||

| (0.0185) | (0.0446) | (0.0485) | ||||||||

| 0.067*** | 0.215* | 0.143* | ||||||||

| (0.0256) | (0.1213) | (0.0820) | ||||||||

| 0.001 | 0.022 | 0.006 | ||||||||

| (0.0113) | (0.0487) | (0.0261) | ||||||||

| NT | 3054 | 3054 | 3054 | 3054 | 3054 | 3054 | 3054 | 3054 | 3054 | 3054 |

| N | 509 | 509 | 509 | 509 | 509 | 509 | 509 | 509 | 509 | 509 |

| 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | |

| ar1 pval. | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||

| ar2 pval. | 0.29 | 0.80 | 0.65 | 0.53 | 0.83 | 0.62 | ||||

| ar3 pval. | 0.35 | 0.98 | 0.92 | 0.59 | 0.98 | 0.83 | ||||

| Hausman pval. | 0.417 | 0.000 | 0.000 | 0.007 | 0.034 | |||||

| Time dummies pval. | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

Table 9 presents the regression results. The RE estimation can be seen as an upper bound, while the FE is a lower bound on the behavioural persistency . This means that consistent estimates would be characterized by an autoregressive parameter falling inside . In addition, the discrepancy between RE and FE underlines the presence of firm-specific effects correlated with the explanatory variables and corroborated by CRE1 and CRE2. Such heterogeneity is time-invariant and captures firm-specific characteristics, like the CEO’s innate abilities or unique features of their products. This sample represents a suitable environment for our CRE-GMM estimator also because individual heterogeneity could be subject to potential changes over time, losing their constancy and intrinsic features. For instance, the overall CEO’s ability remains invariant over time until the industry does not hire a new manager. Hence we compare the standard GMM-lev estimation (GL) with the GMM-lev augmented with CRE where instruments are chosen according to the results obtained in our simulations (CRE-GMM2 and CRE-GMM5).