Perturbation-based Analysis of Compositional Data

Abstract

Existing statistical methods for compositional data analysis are inadequate for many modern applications for two reasons. First, modern compositional datasets, for example in microbiome research, display traits such as high-dimensionality and sparsity that are poorly modelled with traditional approaches. Second, assessing – in an unbiased way – how summary statistics of a composition (e.g., racial diversity) affect a response variable is not straightforward. In this work, we propose a framework based on hypothetical data perturbations that addresses both issues. Unlike existing methods for compositional data, we do not transform the data and instead use perturbations to define interpretable statistical functionals on the compositions themselves, which we call average perturbation effects. These average perturbation effects, which can be employed in many applications, naturally account for confounding that biases frequently used marginal dependence analyses. We show how average perturbation effects can be estimated efficiently by deriving a perturbation-dependent reparametrization and applying semiparametric estimation techniques. We analyze the proposed estimators empirically on simulated data and demonstrate advantages over existing techniques on US census and microbiome data. For all proposed estimators, we provide confidence intervals with uniform asymptotic coverage guarantees.

Keywords: compositional data, causality, perturbation, feature importance, diversity effects, nonparametrics

1 Introduction

Compositional data, that is, measurements consisting of parts of a whole, appear in many scientific disciplines, for example, rock compositions in geology, green house gases in the atmosphere, species compositions in ecology and racial or gender distributions in social sciences. The defining property of such data is that they only capture information relative to the unknown whole and hence do not contain any information on the absolute sizes. Depending on the application, the absolute information either might not be of interest (e.g., when analyzing racial or gender distributions) or might not be easily accessible with existing measuring techniques (e.g., in ecology). Mathematically, a -coordinate composition can – without loss of information – be normalized such that it is represented as a point on the -dimensional simplex

It is well-known that many conventional statistical procedures become invalid when applied to compositional data. For example, already Pearson (1897) drew attention to the fact that correlations between individual compositional components can be spurious due to the sum-to-one constraint. Much work has gone into constructing new procedures for adjusting the correlation measure for compositional components, e.g., by transforming the data with log-ratio transforms (Aitchison, 1982). An instructive viewpoint is to see these approaches not as adjusting the correlation measure but rather as creating new target parameters (e.g., the correlation between log-ratios) that have meaningful interpretations in compositional data.

We adopt this point of view and develop a framework which uses hypothetical perturbations of the data to construct meaningful target parameters. Specifically, we consider a setting where we observe an outcome of interest and an associated compositional predictor . Our goal is to construct functionals of the conditional distribution given that are useful when analyzing compositional data. To illustrate this, we consider two examples in which existing approaches are insufficient.

Example 1 (Effects of presence or absence of microbes).

Consider the problem of determining whether the presence or absence of certain microbes in the human gut is affecting a disease. Microbial abundances are commonly measured using genetic sequencing (e.g., targeted amplicon or shotgun metagenomic sequencing) which in most cases only measures the composition and not the absolute abundances. Assume we have measurements from a cohort of patients, where for each patient the relative abundance of all microbes in their gut and a disease indicator has been recorded. While estimating causal effects in such a setting is often too ambitious, one could hope to screen for relevant microbes that could then be considered for follow-up randomized studies. One possible approach (e.g., Hu et al., 2021) would be to consider a fixed microbe and then compare the distributions

for example, with an independence test or by regressing on . It is well-known that this type of marginal dependence analysis can be misleading if dependencies exist between the individual components. As an example, assume the disease indicator is generated by

that is, the absence of increases while the absence of decreases the probability of having the disease. In a numerical simulation of this generative model with dependence between and , the effect of is instead estimated to decrease the probability of disease as shown in Table 1. If did not live on the simplex, we could adjust for the dependence in the remaining coordinates by considering conditional dependencies of the form . However, due to the simplex constraint completely determines , so the conditional independence always holds. In the Table 1, we also provide the results from applying the compositional knockout effect to which we introduce in Section 2.2.

| Example 1 | ||

|---|---|---|

| method | estimate | 95%-CI |

| OLS of on | ||

| using rf | ||

| Example 2 | ||

|---|---|---|

| method | estimate | 95%-CI |

| OLS of Y on | ||

| using rf | ||

Example 2 (Effects of increased diversity).

Consider the problem of determining the effect of an increase in diversity of on the response . Such a question is of immediate interest in many applied fields, e.g. when investigating whether more racially diverse university programs improve educational outcomes (Antonio et al., 2004) or whether increased income equality boosts economic output (Shin, 2012). The prevalent approach is to summarize diversity via a one-dimensional summary statistic (e.g., the Gini coefficient, generalized entropy or Gini-Simpson index) and analyze the correlation between and . As in Example 1 this type of marginal dependence analysis is potentially misleading in practice. In Table 1 we illustrate this on a specific numeric example, where the true causal effect is positive, but the marginal method leads to a negative effect of diversity (details are provided in Section S4.1 of the supplementary material). To avoid this, one would again like to adjust for the remaining dependence within to avoid the confounding biases. However, since depends on all of existing adjustment approaches are not applicable. The compositional diversity effect (with Gini-speed) which we introduce in Section 2.2 appropriately adjust for the confounding as shown in Table 1. A more in-depth example in which the marginal approach is misleading is given in Section 4.2 where we estimate the effect of racial diversity on income on grouped real data. Unlike in Example 1, the problem of not being able to adjust with existing techniques is not solely due to the simplex-constraint and similarly appears for summary statistics of unconstrained Euclidean data. Our perturbation-based framework can also be extended to those settings, but as the use of this type of analysis is particularly prevalent in compositional data applications we restrict our attention to this setting.

In this work, we propose a procedure that accounts for potential confounding within . The main idea is to introduce a new target parameter via a hypothetical perturbation of the data. More concretely, a perturbation is a function which for each point describes a path along which the point should be changed. For example, in Example 1 when considering the first microbe (i.e., ), we could consider a binary perturbation satisfying for all that and , where scales the inputs to have sum one. A target parameter that captures the desired adjusted effect is then given by

In Example 2, an increase in the diversity of can be expressed as a perturbation that pushes every point in to a more diverse point. Formally, using the center of the simplex (i.e., ) as the most diverse point, we define for all and all the perturbation

We can then interpret for a small as slightly increasing the diversity of the point . With this notion of an increase in diversity, a target parameter that captures the desired adjusted effect is given by

which quantifies how on average the conditional expectation of given is affected by small increases in diversity. A key strength of using perturbations to define target parameters is that it makes them easy to communicate, interpret and discuss with practitioners. From our experience, practitioners often have a good understanding of what perturbation they are interested in and formalizing them mathematically as above is straight-forward. Even though the target parameters and have a clear causal motivation, it is important to stress that they are purely (observational) statistical quantities. To connect them to causal effects requires standard causal assumptions and potentially adjustments to the estimators, which we discuss in Section 2.3.

While the target parameters and may seem simple at first sight, they can be challenging to estimate directly as they depend on estimating the conditional expectation which due the simplex structure is generally a complex functional. We therefore propose an approach that reparametrizes the compositional vector via a bijection to a vector in such a way that the perturbation only changes in the new parametrization. To make this more concrete, assume that the structural causal model (SCM) (e.g., Pearl, 2009) given in Figure 1 (left) generates the data (the causal terminology is used only to provide a more intuitive introduction). Given a perturbation that we are interested in, we now propose to construct a bijection that maps to such that if we intervene on by setting it to this corresponds to an intervention in an SCM over the variables on alone (see Figure 1 (right)). Hence, if we are able to construct such a reparametrization, then we have successfully reduced our problem to a setting in which standard adjustment works, that is, using any existing method to estimate the effect of on that adjusts for results in an unbiased estimate of the causal effect. Given a perturbation , we provide a general recipe to construct the reparametrization . We furthermore propose several explicit perturbations (including their corresponding reparametrizations) and suggest efficient estimators of the perturbation-based target parameters using semiparametric theory based on the -reparametrization.

(a) SCM on -scale (b) SCM on -scale

The remainder of the paper is structured as follows. In Section 1.1 we discuss existing methods for compositional data analysis and how our approach contributes to this research. Section 1.2 collects the mathematical notation used throughout this work. Our perturbation-based framework is introduced in Section 2. In Section 2.1, we provide a way to construct interpretable perturbations based on suitably choosing the endpoint, direction and speed of the perturbation. We also provide a general construction for the aforementioned and for a wide range of perturbations. We end the section by discussing how to adapt our proposals to general geometries on the simplex including those employed by many current methods in compositional data analysis. In Section 2.2 we highlight and name some of the perturbation effects that we believe are most useful for practitioners and provide some examples of how and when these effects should be applied. In Section 3, we discuss how to estimate the parameters of interest based on semiparametric theory using two different methods that represent a trade-off between generality and robustness. Our semiparametric estimators and perturbation effects are then illustrated on both simulated data and two real-world applications in Section 4. Finally, we present the theoretical guarantees of our estimates in Section 5.

1.1 Relation to existing compositional data analysis approaches

Compositional data analysis has a long history dating back to Pearson (1897). The most prevalent class of methods is based on the seminal paper by Aitchison (1982) which introduces the log-ratio approach. In its most basic form it consists of transforming the simplex data via the additive, centered or isometric log-ratio transforms (Aitchison, 1982; Egozcue et al., 2003) and then performing the statistical analysis in the transformed space. By considering ratios instead of compositional coordinates it avoids the common pitfalls of spurious correlations that occur by comparing coordinates. Our approach is not based on log-ratios, but it is possible to construct perturbations from this perspective (see Section 2.1.3). Furthermore, some of the perturbation effects that we highlight as interpretable overlap with effects that can also be deduced from the log-ratio perspective. Most prominently, we consider a class of compositional feature influence measures for which a certain member (multiplicative speed, see Example 3) corresponds to the compositional feature influence which has been previously proposed by Huang et al. (2023). It also corresponds to one of the coefficients in a log-contrast model (Aitchison and Bacon-Shone, 1984) if the conditional mean lies in the log-contrast model class. Our perturbation-based framework, however, has a fundamentally different starting point and allows for the construction of perturbations that are not related to the log-ratio approach.

The idea of transforming compositional data via the log-ratio transform to a simpler sample space has been applied successfully in many applications, however we believe its indirect use of the data is restrictive. This is best illustrated by the so-called zero-problem that occurs because the log-ratio approach, in general, cannot be applied in settings with too many zeros. This problem has sparked a large body of research developing various types of zero-imputation schemes (e.g., Martín-Fernández et al., 2000, 2003, 2015; Palarea-Albaladejo and Martín-Fernández, 2008; Lubbe et al., 2021) that can be used before applying the log-ratio approach. Other approaches advocate the use of different transformations, for example power-transformations (Greenacre, 2009) or spherical transformations (Scealy and Welsh, 2011; Li and Ahn, 2022). While many of these approaches are sensible in specific applications, we believe that it is generally preferable to modify the statistical procedure to fit the data rather than vice versa. Greenacre et al. (2023) provide an overview of current state-of-the-art compositional data analysis and highlights some of the shortcomings in existing transformation-based approaches. In contrast to these methods, our perturbation-based framework works directly with the compositional data and defines the target parameter from this perspective. In the presence of zeros, perturbations that directly incorporate or omit zeros can be selected based on the application. Furthermore, we can construct perturbation effects that directly capture the effect of setting certain components to zero.

1.2 Notation

We use superscripts to index coordinates of a vector throughout, that is, for we write for the th coordinate of and denote by the th canonical unit vector in . For all , we define . For a real-valued function with , we denote by the partial derivative of with respect to the coordinate and the gradient (vector of partial derivatives) of is denoted by . When differentiating a function of a single variable at a boundary point of the domain, we only consider the one-sided limit. For and , we define . Lastly, we define , the (simplex) closure operator, with the additional convention that for we have .

2 Target parameters via perturbations

For a response and a compositional predictor , we seek to summarize the effect of on the expectation of under a pre-specified change of . We specify this change via perturbations.

Definition 1 (perturbations).

Let be such that for all it holds that . We call a function a perturbation if it satisfies for all that . For all we define the -domain and endpoint of (if it exists) by

respectively. We furthermore say that

-

(a)

is a binary perturbation if for all it holds that , i.e. , and

-

(b)

is a directional perturbation if for all there exists with and exists. We further define the direction and speed of the perturbation for all by

respectively.

Binary perturbations describe discrete changes that move each point to a specific endpoint, that is, they capture the difference between (doing nothing) and (applying the perturbation). An example of this is setting the first component of to . Directional perturbations describe ‘local’ changes to , that is, differences in (doing nothing) and for some small (moving slightly along the perturbation path). We later focus on the derivative of the perturbation at as this captures the rate of change of directional perturbations at the initial point. As we only intend to use this initial derivative, it suffices to consider perturbations of the form

| (1) |

We will discuss how to construct perturbations with interpretable directions and speeds in Section 2.1.2. Choosing to have the direction and speed parametrized by the -norm is an arbitrary choice that turns out to be convenient on the simplex. In this work, we only consider binary and directional perturbations but other classes of perturbations could be of interest too. Perturbations can also be defined on more general sample spaces than simplices and many of the perturbation-related concepts described here can be readily extended to these settings.

Using the two types of perturbations, we can define informative summary statistics that capture the effect of the perturbations on the response. We do this by using contrasts of the perturbation, similar to how causal effects are defined via contrasts of interventions in the causal inference literature. Formally, we define the following target parameters associated with each type of perturbation.

Definition 2 (average perturbation effects).

Let , let be random variables and define . Then, for a binary perturbation , if is identified on and , we define the average (binary) perturbation effect by

Furthermore, for a directional perturbation , if for all it holds that is differentiable on the simplex(see Section S1 for a precise definition) at , we define the average (directional) perturbation effect by

We showcase different potential applications for both types of perturbation effect in the numerical experiments in Section 4. For binary perturbations, the denominator is included to scale the effect by the probability that the perturbation does not change . This is not required but in many cases provides a more meaningful parameter if one is interested in how the perturbation affects points on the simplex that are not yet at their endpoint. While both target parameters have obvious similarities to causal effects, they are a priori only (observational) statistical quantities. In particular, they are identifiable from the observational distribution as long as the conditions in Definition 2 are satisfied. We discuss the assumptions required for causal conclusions in Section 2.3.

Direct estimation of both target parameters relies on estimating the regression function and taking averages (see Section 3). An alternative estimation procedure for the effect of a binary perturbation can be derived from noting that, if and , then

Therefore, we can write

| (2) |

which is an expression more amenable to analysis by semiparametric theory and thus allows us to construct efficient estimators. If we are willing to assume that is constant when and equal to, say , then

and furthermore

so is the coefficient of in a partially linear model of on and .

It would be convenient to also phrase the average directional perturbation effect as a quantity that is similarly amenable to semiparametric analysis and permits us to impose a partially linear model. To motivate the upcoming condition, we consider what happens when takes values in . In that case, we can write

We now want to isolate the change of in the direction into a real-valued variable while keeping the remainder of the ‘information’ in in an additional variable . For a reparametrization of into , we define the reparametrized as . Then, in order for the reparametrization to separate the ’information’ appropriately, we require

to equal , that is,

This derivation is only morally correct when ( is not defined in the usual sense for simplex-valued functions) and to make it formally correct one needs to apply techniques from differential geometry. The proof of the following result can be found in Section S2.1 of the supplementary material.

Proposition 1 (derivative-isolating).

Consider the setting of Definition 2. Let be a set and a family of subsets of . Suppose that is a bijection and a directional perturbation such that for all it holds that . Suppose that for all and all , we have

| (3) |

Then, defining and , the average perturbation effect satisfies

| (4) |

We say that is derivative-isolating if it satisfies (3).

From this result it follows that if we are able to find a derivative-isolating reparametrization (we describe how to find such reparametrizations for certain perturbations in Section 2.1.2) the average directional perturbation effect can be expressed as an average partial derivative of a conditional expectation (4) – a quantity that has been previously studied using semiparametric theory (Newey and Stoker, 1993). It can either be estimated nonparametrically or by assuming a partially linear model, that is, assuming that there exists a parameter and a function such that

| (5) |

Details on the different estimation approaches are discussed in Section 3.

Remark 1 (zero speeds).

While we do not allow in the definition of derivative-isolating reparametrizations, it is clear from the definition of that such points do not contribute to the perturbation effect. We can therefore allow for such points if we appropriately adapt the estimates. In Section S3.2 of the supplementary material, we describe how to modify the estimation procedures introduced in Section 3 to allow for valid estimation even when with positive probability.

2.1 Perturbations on the simplex

We now turn to the construction of perturbations on the simplex. For binary perturbations, we only need to specify the endpoint of the perturbation, while for directional perturbations it suffices to choose a direction and a speed to construct a perturbation of the form (1). For a fixed endpoint there is a canonical (potentially geometry-dependent) choice of direction that is given by the straight line from a point to its endpoint. The choice of speed is, however, more subtle and it should be selected in a way that provides a clear interpretation. We propose two general approaches for selecting speeds: (a) by directly specifying an interpretable speed and (b) by starting from a summary statistic and assuming it satisfies a partially linear model as in (5) with being the summary statistic. For both approaches, Proposition 2 provides – under additional assumptions – explicit derivative-isolating reparametrizations, which can then be used for efficient estimation.

In the remainder of this section, we discuss interpretable simplex endpoints in Section 2.1.1, provide details on the selection of directions and speed together with the construction of derivative-isolating reparametrizations in Section 2.1.2 and finally in Section 2.1.3 discuss how one could construct directional perturbations that respect a different geometry than the Euclidean one. The perturbations introduced here are used in Section 2.2 to construct specific target parameters based on potential applications. The more applied reader may jump directly to that section and skip the more technical discussion on perturbations here.

2.1.1 Endpoints in the simplex

As formally defined in Definition 1, an endpoint function , if it exists, determines where the perturbation ends when is increased as much as possible. The simplest type of endpoint function on the simplex is a constant function, that is, there exists a fixed point such that for all it holds that . For example, we can choose the fixed endpoint , which corresponds to a vertex on the simplex and hence a perturbation with this endpoint moves proportions from the other coordinate into the th one. A further example, is to use the center of the simplex, i.e. . As alluded to in the introduction, perturbations with as the endpoint can be seen as perturbing observations in the direction of equal distribution and hence capture a notion of diversity. For later reference, we call all perturbation with endpoint function centering perturbations.

A second type of endpoint function, that can be non-constant, is given by mapping each to amalgamations on the simplex. An amalgamation is a well-studied operation (e.g., Aitchison, 2003) which consist of merging parts of the compositional components into others. Formally, we define the -amalgamation operator for all by

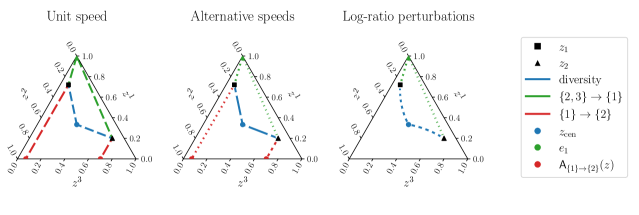

The -amalgamation has the effect of setting components in to , scaling up the components in such that the subcomposition in remains fixed (i.e., ) and leaving the remaining components fixed. We call all perturbations with endpoint function amalgamating perturbations. An important class of amalgamating perturbations are those where and so that , i.e. perturbations that push towards a vertex of the simplex. Amalgamations, however, do not need to have fixed endpoints but allow for more general endpoints that can also depend on the initial point. Several perturbations on are visualized in Figure 2 below.

2.1.2 Directions, speeds and derivative-isolating reparametrizations

When constructing directional perturbations it is sufficient to consider perturbations that are parametrized by their direction and speed as

An endpoint function gives rise to a canonical direction defined for all by

| (6) |

that is, for each we define the unit vector in the direction of the straight line from to the endpoint. Throughout this section, to avoid zero speeds, we restrict the domain of the perturbations to but as discussed in Remark 1 the target parameters and estimates can be easily extended to settings where zero speeds are allowed. In Section 2.1.3 we describe how working in other geometries can lead to different notions of direction. Taking the direction in (6) as given, we now want to select a speed that leads to an interpretable average directional perturbation effect and then construct a derivative-isolating reparametrization for the resulting perturbation in order to efficiently estimate the effect. We propose two approaches: (a) starting directly from a speed that satisfies some regularity conditions and (b) starting from a one-dimensional summary statistic, for which a partially linear model as in (5) can be assumed, and then constructing a corresponding speed. In both cases, the construction of a derivative-isolating reparametrization is similar.

As a fundamental building block for the general construction below, we consider a perturbation with unit-speed and direction , that is, for all with and all we define

Intuitively, a derivative-isolating reparametrization for should isolate changes along the direction from changes due to varying directions. We therefore consider the reparametrization defined for all by , where is formally defined in Proposition 2. The inverse of this reparametrization is , so

and hence is derivative-isolating for . Since these type of unit-speed perturbations may not always be easy to interpret, we extend this basic construction to start from either a given interpretable speed or a summary statistic. The proof of the following result is given in Section S2.2 of the supplementary material.

Proposition 2.

For , let be an endpoint function satisfying for all that . Denote by the set of endpoints and define for all and all the sets and . Finally, define the unit speed reparametrization for all by and with the canonical endpoint direction defined in (6). Then the following approaches lead to perturbations with corresponding derivative-isolating reparametrizations.

-

(a)

(Speed) Let be a given speed function. For all define for all by and let denote a solution to

(7) Then, the reparametrization defined for all by is derivative-isolating for the perturbation and any other perturbation with the same speed and direction.

-

(b)

(Summary statistic) Let be a given summary statistic. For all define for all by and assume that is differentiable and strictly decreasing. Then, the reparametrization defined for all by is derivative-isolating for the perturbation , where the speed is defined for all as

and any other perturbation with the same speed and direction.

Part (a) starts from a given speed and finds a corresponding derivative-isolating reparametrization by solving the differential equation in (7). Part (b) starts from a one-dimensional summary statistic, which is assumed to be smoothly decreasing in the distance from to the endpoint. Using the statistic as one component in a derivative-isolating reparametrization, the result provides the speed of the perturbation that is being parametrized. We illustrate the use of Proposition 2 by constructing several directional perturbations.

Example 3 (Feature influence).

Suppose we are interested in the effect of increasing the value of a particular component of . We can investigate the effect of such a change by means of a -amalgamating perturbation, that is, a perturbation which satisfies for all that . While for some purposes it may be perfectly reasonable to use a constant speed , in other settings this speed can be unintuitive. For example, if we imagine the observed as being generated from an unobserved on an absolute scale by , it might be more natural to consider which speeds are induced on the simplex from hypothetical changes to . A first attempt might be to consider the speed resulting from adding a constant to , however, since

this speed is not scale-invariant for , that is, the speed when considering the counts and for may differ. This means that the speed on the simplex would depend on the unobserved quantity so the perturbation is ill-defined. Instead, we can consider the speed resulting from multiplying by (so that corresponds to no change) which yields a well-defined perturbation on the simplex since this operation is scale-invariant. More formally, letting denote the Hadamard (point-wise) product, the resulting speed is

which is scale-invariant and therefore meaningful to consider on the simplex. On the simplex, this corresponds to the speed

which we call multiplicative speed. To find a corresponding derivative-isolating reparametrization we apply Proposition 2 (a). Since for all it holds that and , we have that (defined in Proposition 2) does not depend on and is of the form

Hence, solving (7) amounts to solving

which has solutions of the form for . For simplicity, we choose and note that as , we have

We can therefore conclude (dropping the constant endpoint from the reparametrization) that

is a derivative-isolating reparametrization for the -amalgamating perturbation with multiplicative speed.

Example 4 (Amalgamation influence).

We can extend the considerations of Example 3 to more general amalgamating perturbations. For disjoint , consider an -amalgamating perturbation. Suppose as before that for some on an absolute scale. We can omit components of and that are not in from the analysis as these do not change under the perturbation so we suppose now that . The multiplicative operation described in Example 3 can be generalized by letting and considering

which similarly corresponds to a well-defined perturbation on the simplex. Computing the speed, we obtain that

We can use this speed even when resulting in the general multiplicative speed

| (8) |

Using Proposition 2 (a) as in Example 3, we further obtain that

is a derivative-isolating reparametrization for with multiplicative speed.

Example 5 (Diversity with Gini-speed).

Suppose we are interested in the effect of diversifying . We can investigate such an effect by using a centering directional perturbation, that is, a perturbation which satisfies for all that . As every element of as defined in Proposition 2 is of the form for a direction , we instead drop the endpoint from the set and use instead. In contrast to the Examples 3 and 4 it is not as obvious how to choose an interpretable speed. We therefore start from a summary statistic and apply Proposition 2 (b) to derive the corresponding speed and derivative-isolating reparametrization. For econometricians a natural choice of diversity measure might be the Gini coefficient. The Gini coefficient is defined for all by

| (9) |

Using , we can express this as

Hence, defining for all the strictly decreasing and differentiable function ( is defined in Proposition 2) for all by

we have that . Applying Proposition 2 (b), we conclude that

is a derivative-isolating reparametrization for perturbations with direction and speed given by

| (10) |

Similar arguments could be applied to other popular measures of diversity such as the Shannon entropy or the Gini–Simpson index.

2.1.3 Perturbations arising from alternative simplex geometries

When constructing the directional perturbations in Section 2.1.2, we considered (Euclidean) straight lines to the endpoint to construct directions, that is, . While we believe that this is natural in many applications, one could also imagine starting from alternative geometries on the simplex and construct other types of directions. We illustrate how this would work for the Aitchison geometry and show that it provides an interesting connection to the log-ratio based literature. The Aitchison geometry is a popular alternative geometry that goes back to the work of Aitchison (1982) who proposed to analyze the interior of the simplex by transforming to a subset of Euclidean space and applying conventional methods to the transformed data. A popular variant of this transformation is the centered log-ratio transform (CLR) defined for all by

This transformation maps the interior of to the subspace of given by . The inverse CLR is defined for all by

or more simply as where is applied componentwise. The inverse of the transform can in fact be defined on all of rather than just the range of the -function as is clear from the definition. The -transformation induces what is called the Aitchison geometry (Egozcue and Pawlowsky-Glahn, 2006) on the simplex. The Aitchison geometry induces a different notion of direction than the Euclidean notion considered above and, in particular, the direction of the line connecting to an endpoint may differ from the direction in (6) (see, for example, Figure 2). However, as is a bijection on the open simplex, we can just as well consider perturbations on directly and use arguments similar to those in Proposition 2 but now for the perturbation on the log-ratio scale. We illustrate this procedure in the following two examples and discuss connections to the centering and amalgamating perturbations defined above.

Example 6 (Diversity in the Aitchison geometry).

Suppose we are interested in the effect of diversifying . As in Example 5, we can think of such effects as moving towards the center , but now using the Aitchison geometry this corresponds to moving towards along a straight line in CLR-space. This line transformed back to the simplex can be written as

Therefore, computing the diversifying direction in the Aitchison geometry amounts to differentiating the expression above at and normalizing. Applying the chain rule, this yields

which can be normalized to a unit -norm vector. The direction of this derivative can be vastly different from the centering direction used in Example 5. To obtain a derivative-isolating reparametrization, we can instead define a unit-speed perturbation on the log-ratio scale, , and find a reparametrization on this scale. It can be shown that on the log-ratio scale, a derivative-isolating reparametrization is given by and and we can transform these to reparametrizations of by composing with the -transform.

Example 7 (Feature influence in the Aitchison geometry).

Suppose, as in Example 3, we are interested in the effect of increasing the value of a particular component of . For we have a natural notion of increasing inherited from , namely adding to . The derivative of the resulting perturbation on the simplex is for all given by

It is straight-forward to check that the speed and direction of this perturbation match exactly the multiplicative perturbation derived in Example 3. One can therefore view an additive log-ratio perturbation as a multiplicative speed perturbation.

2.2 Perturbation effects on the simplex

To make the discussion more concrete, we now provide several explicit perturbation effects on the simplex using the perturbations constructed in Section 2.1. We motivate each perturbation effect with an example application to showcase potential use cases. A list summarizing all proposed perturbation effects together with their respective derivative-isolating reparametrizations that are used for efficient estimation is provided in Table 2. We encourage practitioners to develop further application-specific perturbations that optimally target the research question they are interested in.

2.2.1 Effects of changes in individual components

As a first example we consider perturbation effects that capture how a response is associated with changes in individual components. These types of effects are, for example, useful as a variable selection tool in compositional data. In Section 4.3, we illustrate this for a human gut microbiome study. For each study participant the body mass index (BMI) and their gut microbiome composition are measured. We then wants to determine for which microbes a high abundance is associated with a high BMI. The simplex constraint implies that for all coordinates the conditional independence

| (11) |

is trivially satisfied and feature importance or influence measures based on (11) are meaningless. Intuitively, this stems from the fact that changing a single component always requires a change in at least some of the remaining components. We therefore propose – for a fixed component – to consider perturbations that increase the th component while decreasing all remaining components proportionally. We define the compositional feature influence for the th feature or simply as for any directional perturbation with endpoint . To that end, we already considered these perturbations in Example 3 where we proposed two possible speeds leading to slightly different interpretations of the average perturbation effects: is the perturbation that moves at a constant (unit) speed towards the vertex and is the perturbation that moves at what we call multiplicative speed (see Example 3 for more intuition on these speeds). has previously been proposed by Huang et al. (2023), however without an efficient estimation procedure. Huang et al. (2023) also prove that when a log-contrast regression model is well-specified the th coefficient in the model is equal to . A crucial difference between unit speed and multiplicative speed perturbations is how they account for observations with . As the multiplicative speed is in this case such points do not contribute to , however, they do contribute to .

In datasets with many zeros, which is common for example in microbiome data, it can also be interesting to focus only on the effect of zeros in individual components. This can be achieved by considering a binary perturbation given by and . We call the resulting average binary perturbation effect the compositional knock-out effect for the th feature, or for short. The allows for a straightforward analysis of zeros in compositional data, which has been a long-standing problem with many existing approaches.

2.2.2 Effects of changes in diversity

As a second example we consider perturbation effects that capture how a response is associated with increases in diversity. Such effects are often relevant in social sciences and econometrics, e.g., when considering racial or income distributions. As we outlined in the introduction, it can be misleading to only model summary statistics of diversity and ignore the remaining compositional structure as this structure can confound the relationship between the diversity measure and the response. Instead, we propose to consider the effect of directional perturbations that push towards (the centering perturbations defined in Section 2.1.1) and call for such perturbations a compositional diversity influence (). We denote the effect by if the perturbation has unit speed and by if the perturbation was constructed as in Example 5 such that is equal to the negative Gini coefficient. The construction in Example 5 can be adapted to many popular diversity measures and hence allows practitioners to use their favorite diversity summary statistics. In Section 4.2, we use data from the US census to analyze the effect of racial diversity on income and show how avoids the confounding caused by naively including the Gini coefficient in a regression.

We do not define a binary centering perturbation here as it requires a positive probability of observing , which is rarely the case.

2.2.3 Effects of amalgamations

As a third example we consider perturbation effects that capture the influence of general amalgamations. As an example, consider a study where data is collected on how individuals spend their time each day (e.g., hours spent sleeping, eating, working, doing sports, etc.) as well as a response variable (e.g., general happiness). Assume now that we want to use this data to investigate the relationship between time spent on sports and happiness. As above, we are again interested in effect of an individual component, so we might consider estimating a . However, this would capture the effect of increasing time spent on sports while all other activities are down-scaled proportionally. For example, time spent sleeping and eating would both be decreased if time doing sports is increased which is not realistic. To address this, we can instead consider a general -amalgamating perturbation (as defined in Section 2.1.1), where and corresponds to activities which are reduced to make increased time for sports. Perturbing in this fashion keeps the components in fixed (e.g., eating and drinking) while down-scaling the activities in . We call directional perturbation effects of this form compositional amalgamation influences, or for short. As with the , we use subscripts to denote the speed of the perturbation, so we have and (see Example 4).

Analogously, we could be interested in the effect of removing particular activities (e.g. gambling) entirely and spending the time on desirable activities (e.g. sports) while fixing time spent on a third group of activities (e.g. eating, sleeping). We can capture this effect using a binary amalgamating perturbation . We call the resulting average binary perturbation effect for an -compositional amalgamation effect, or for short.

| Effect of changes in | Target | Speed | Endpoint | |

|---|---|---|---|---|

| individual components | ||||

| binary | ||||

| diversity | ||||

| see (10) | , see (9) | |||

| amalgamations | ||||

| binary |

2.3 Perturbations as causal quantities

Perturbations are a priori non-causal quantities and should not be confused with (causal) interventions. To make this distinction clear, we now discuss how our perturbation framework can be used for causal inference. Causal models (Pearl, 2009; Rubin, 2005) provide a mathematical framework for modeling changes to the data generating mechanism – often called interventions. In contrast to an (observational) statistical model, which assumes a single observational distribution that generated the data, a causal model additionally postulates the existence of a collection of interventional distributions that describe the data generating mechanism under hypothetical interventions. The power of causal models is that they allow specification of rigorous mathematical conditions under which (parts of) the interventional distributions can be identified (or computed) from the observational distribution. Unlike interventions, perturbations describe hypothetical changes to the predictor space (in this work , but the same ideas hold more generally) and not to the data-generating mechanism. To make this more precise and show how to use perturbations for causal inference, we use the structural causal model (SCM) framework (Pearl, 2009; Bongers et al., 2021). Similar considerations, however, also apply with the potential outcome framework.

As an example, consider the SCM over the variables given by

where and are measurable functions and are jointly independent noise terms with expectation zero. The SCM generates a distribution over which is called the observational distribution. Intervening corresponds to changing individual structural assignments while keeping everything else fixed such that the modified SCM again induces a distribution – called the interventional distribution. The example SCM is a commonly assumed causal structure in which the predictor causally precedes the response but is confounded by .

Assume now we observe data generated by and are interested in understanding how causally affects . One target parameter might be to consider the expected value of under an intervention that sets to a fixed value, using do-notation (Pearl, 2009), this can be expressed as . For larger the full causal relation might be too ambitious of a goal, and it may be more tractable to look at the effect of individual components. Since the vector is compositional, one needs to be careful when expressing summary interventions. Perturbations provide a solution to this as they allow us to express sensible ways of changing the predictors. More specifically, let be a perturbation as defined in Definition 1. Then, for all , consider the intervention , which in replaces the -structural assignment by . In a similar way as to how we previously used the conditional expectation of under the perturbation, we can now use the expected value of under the perturbation-induced intervention, i.e., . Here, we only consider interventions on the entire compositional vector , which means that it is not possible to model how causal effects propagate within the composition itself. The corresponding causal versions of the target parameters in Definition 2 are then the causal average binary perturbation effect

and the causal average directional perturbation effect

Unlike their non-causal versions, the causal average perturbation effects may not be identifiable from the observational distribution. Therefore, to estimate them, we need to make additional causal assumptions. For example, we may assume the variable were generated by an SCM with the same causal structure as . In that case, if is observed, the expectation of under perturbation induced interventions on can be expressed as

| (12) |

and hence is identifiable. The formula in (12) is a special case of the adjustment formula (e.g., Pearl, 2009), but other ways of identifying this effect also exist (e.g., propensity score matching). It is easy to adapt the estimators proposed in this work to such settings by conditioning on additional confounding covariates . In particular, starting from the reparametrization into one only needs to add additional observed confounders alongside . This is for example done in the numerical experiment in Section 4.2.

Finally, let us shortly discuss under which assumptions the causal and non-causal average perturbation effects coincide. Obviously, one sufficient condition is to assume that

| (13) |

Such a condition holds by definition whenever is an exogenous variable (i.e., does not depend on other variables in its structural assignment) but can also hold more generally. A common assumption to ensure (13) is to assume that and are not confounded, that is, and have no common causes (this is known as ignorability in the potential outcome framework). In the SCM this would for example mean that does not exist or either or do not depend on . In many cases, this is not satisfied and one should instead carefully argue for which causal assumptions are reasonable and adjust the estimation accordingly, e.g., by conditioning on additional covariates as in (12).

3 Estimating perturbation effects

In this section, we describe how to estimate and test hypotheses about the target parameters and . We will not explicitly restrict ourselves to any one perturbation as the approaches described are agnostic to this choice. However, we will assume that any directional perturbation comes with a derivative-isolating reparametrization and for any binary perturbation we define and . This allows us to transform our estimation problem from a compositional data problem where we observe i.i.d. copies of to a generic problem with observations of with and , where our interest lies in the relationship between and when controlling for . We only present an overview of the different estimators in this section and postpone a detailed description of the algorithms and theory to Section 5.

3.1 Efficient estimation using semiparametric theory

We now give a brief introduction to semiparametric estimation of statistical functionals and, in particular, we describe how naive plug-in estimation of target parameters based on nonparametric methods rarely leads to efficient tests and how to remedy this. This perspective is not new and goes back to at least Pfanzagl (1982) with several more recent monographs and reviews (Bickel et al., 1993; Tsiatis, 2006; Chernozhukov et al., 2018; Kennedy, 2023). For illustration, we focus on the estimation of , that is, the estimation of

where . A naive approach, which is known as plug-in estimation, is to estimate by first learning a differentiable estimate of using all observations and then computing

While such an estimate can be consistent, it is rarely asymptotically Gaussian, which invalidates standard asymptotic inference. Using the corresponding plug-in estimate of the asymptotic variance, given by

| (14) |

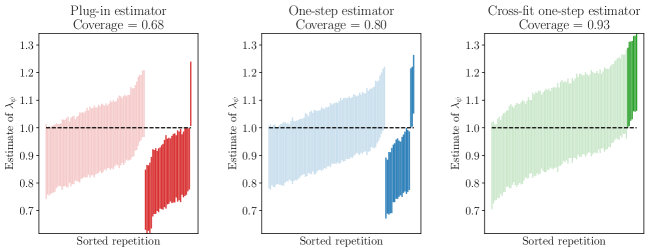

hence does not provide valid inference (see Figure 3 (left)) as the confidence intervals can be biased or too narrow.

There are two main issues with this estimate; (a) repeated usage of the same data for both the estimation of and the computation of the target (double-dipping) and (b) estimation bias inherited from the bias in . Issue (a) can be resolved by splitting the dataset into two parts of roughly equal size and using the first half to compute and the second part to compute . To increase finite-sample performance of this splitting procedure, one can swap the roles of the two halves and average the resulting estimates. This procedure is known as cross-fitting. Sometimes it is preferable to split in more than two folds to increase the sample size in the estimation of and to derandomize the resulting estimate. Issue (b) is more complicated to resolve and requires the machinery of semiparametric theory. One well-established approach is to start from the plug-in estimator and derive a bias-correction, known as a one-step correction, that can be added to the plug-in estimator and weakens the conditions under which the estimator is asymptotically Gaussian. The one-step correction can be found by computing the influence function of the target parameter, which can be thought of as analogous to a derivative when the target parameter is viewed as a function defined on a space of distributions. For more details on this general procedure, see e.g. Kennedy (2023). It can be shown that these bias-corrected estimators are asymptotically efficient, meaning that, at least asymptotically, they have the smallest possible variance of any estimator. Influence functions have already been computed for the target parameters and that we estimate here and we will describe the details of these estimates in the following sections. Figure 3 contains an illustration of the coverage of confidence intervals resulting from target parameter and variance estimates from the different methods mentioned above.

3.2 Efficient estimation of perturbation effects

In this section, we present our proposals for estimating perturbation effects. We postpone the theoretical analysis and a detailed description of cross-fitting to Section 5 and only provide a high-level overview here. All the presented estimators involve regressions that can be performed by arbitrary (sufficiently powerful) regression methods.

3.2.1 Nonparametric estimation of the binary perturbation effect

Consider a binary perturbation with corresponding perturbation effect and recall from the arguments of Section 2 that with and , we have that

The denominator and are both easy to estimate efficiently using their empirical counterparts (the one-step correction term is for these quantities). The term in the numerator is trickier and is related to the notion of average predictive effects (e.g., Robins et al., 1994; Chernozhukov et al., 2018; Kennedy, 2023) that has been analyzed extensively in the causal inference literature. The one-step corrected estimator for is related to the augmented inverse propensity weighted (AIPW) estimator and is given by

where is an estimator of and is an estimator of the propensity score . An efficient estimator for is thus

| (15) |

A full algorithm is given in Algorithm 2. It is worth noting that this estimator is sensitive to the estimation of the propensity score which can be difficult when the dimension of is large or the relationship between and is complicated (see Section S3.1 of the supplementary material for an illustration of this).

3.2.2 Nonparametric estimation of the directional perturbation effect

Consider a directional perturbation with a derivative-isolating reparametrization and the corresponding perturbation effect . By the arguments in Section 2, setting and , we have that

This quantity is another well-known target of inference; the average partial effect (Newey and Stoker, 1993; Chernozhukov et al., 2022; Klyne and Shah, 2023). The one-step corrected estimator in this setting is given by

| (16) |

where is a differentiable estimator of and is an estimate of the conditional score function of given , that is, an estimate of the function where denotes the conditional density of given . A full algorithm for the estimation is given in Algorithm 1 below. Both the estimation of with computable derivative and can be challenging and we show in Section 4 that the overall estimator (16) is sensitive to both estimates (see Section S3.1 of the supplementary material for an illustration of this).

For the estimation of we require that the estimator is differentiable and with computable derivatives (which additionally need to approximate the true derivative at a sufficiently fast rate). This excludes the direct use of many popular machine learning methods such as random forests or boosted trees. One solution is to start from a potentially non-differentiable pilot estimate of and smooth it to get a differentiable estimate for which derivatives can be computed. Such a procedure based on kernel-smoothing has been proposed by Klyne and Shah (2023). Here, we use an alternative smoothing method which uses random forests and local polynomials. A full description of our smoothing method is provided in Section S3.3 of the supplementary material. Finally, for the estimation of , we follow the proposal in Klyne and Shah (2023) and assume a location-scale model. This requires the estimation of the conditional mean and variance of given (referred to as in Algorithm 1). Further details on the location-scale based estimate of is given in Section S3.4 of the supplement.

3.2.3 Partially linear estimation of perturbation effects

While the estimators in the previous sections make only mild assumption on the data generating model, they rely on accurate estimates of quantities that may be difficult to estimate, such as derivatives of densities and regression functions. One way to avoid these complicated estimations is by additionally assuming a partially linear model. For both binary and directional perturbations (with a derivative-isolating reparametrization), we can assume a partially linear model on and , that is, the existence of and such that

| (17) |

With this assumption, is exactly equal to the perturbation effect. Efficient estimation of in a partially linear model is a well-studied problem (e.g., Robinson, 1988; Chernozhukov et al., 2018) and one estimator (sometimes referred to as the partialling out estimator) is given by

| (18) |

where is an estimator of and is an estimator of . A full algorithm is given in Algorithm 3. In contrast to the estimators from the previous sections, this estimator only relies on estimating two conditional mean functions. This comes at the expense of assuming that there is no interaction effect between and on and that the effect of is linear on . Even when these assumptions are not satisfied, the estimator may still provide a reasonable estimate of the effect of on and we found in our experiments that the estimator is more robust to errors in the estimation of the nuisance functions than the estimators above. In fact, one can show that the quantity is minimized by the population version of the partially linear model estimate, so one can think of the partially linear model as a ‘best approximation’ to a generic nonparametric model (see Proposition S1 in Section S3.1.3 of the supplementary material for a proof of this fact).

4 Numerical experiments

We now present three numerical experiments illustrating the usage and performance of our methods. In Section 4.1 we investigate the performance of the semiparametric estimators discussed in Section 3. In Section 4.2 we analyze the effect of diversity on income based on grouped data from the 1994 US census. In Section 4.3 we investigate variable influence (importance) measures for the prediction of BMI from gut microbiome data. The code for all of our experiments is available at https://github.com/ARLundborg/PerturbationCoDa. For all regressions we use the scikit-learn package (Pedregosa et al., 2011) except for the -penalized log-contrast regression in Section 4.3 where we used the c-lasso package (Simpson et al., 2021).

4.1 Semiparametric estimators

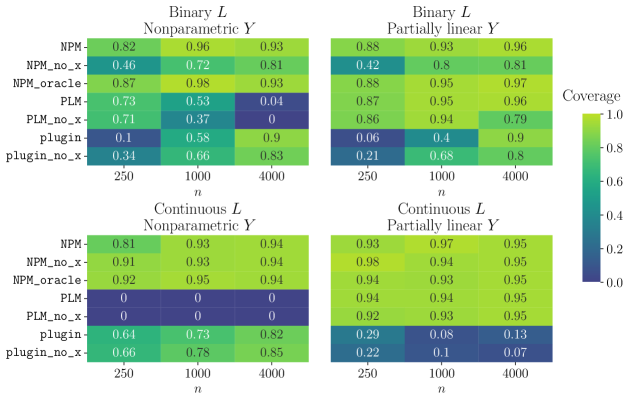

In this section we investigate the performance of the semiparametric estimators outlined in Section 3 with as a simplex-valued random variable. More specifically, we compare the different approaches of estimating

from i.i.d. data . For both types of average perturbation effects we consider the following seven types of estimators.

- •

-

•

NPM_no_x: The same estimators as NPM but without cross-fitting.

-

•

NPM_oracle: The same estimators as NPM including cross-fitting but using the true nuisance functions for the one-step-correction (propensity score in the binary case and conditional score function in the directional case). This is an oracle as the true nuisance functions are unknown in practice.

- •

-

•

PLM_no_x: The same estimators as PLM but without cross-fitting.

- •

-

•

plugin_no_x: The same estimators as plugin but without cross-fitting.

The variance of the NPM and PLM estimates is computed based on the provided algorithms for the NPM and PLM methods while the variance for the plugin is estimated using an estimator akin to the one given in (14). Each estimator above is itself based on multiple of the regression estimates , , and and NPM and NPM_no_x additionally on the score estimate . For the regression estimates, we use a -fold cross-validation based estimator which for each fit selects among the following three models: a simple model that predicts the mean of the outcome (or the proportion of each class for binary classification), a random forest with trees with trees grown to a maximum depth of and a random forest with trees and no depth restriction. For the score estimator we use the location-scale based estimator described in Section S3.4 of the supplement, that uses the same -fold cross-validated regression estimator for the location and scale nuisance regressions.

We consider four data generating models each with varying sample size and predictor dimension . In all settings, we let be uniformly distributed on , denote by the population median of and the variance of and define . We then consider the following four generative models

-

•

Binary with partially linear :

-

•

Binary with nonparametric :

-

•

Continuous with partially linear :

-

•

Continuous with nonparametric :

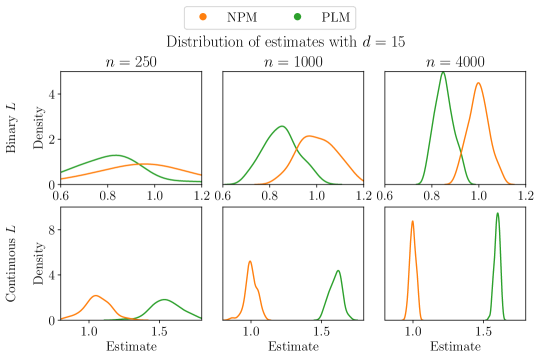

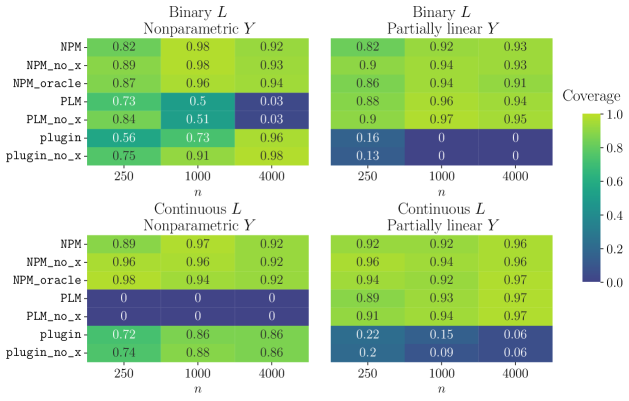

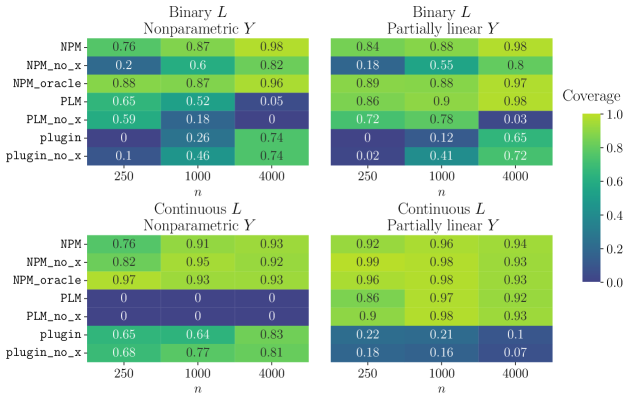

The noise variables , , and are all sampled independently (and independent of ). The true value of in the binary settings and in the continuous settings is . For each setting we simulate data and compute an estimate with a corresponding asymptotic confidence interval using each of the methods described above. We repeat the experiment times and compute coverage rates of the confidence intervals for in Figure 4 while coverage rates for and are reported in Section S4.2 of the supplementary material.

In all settings we see that the partially linear model works well when it is well-specified but can fail when the partially linear assumption is violated. We see that the plugin estimator generally performs worse than the one-step estimator but this disparity is reduced for large . In many cases cross-fitting is not a necessity, however, in some settings cross-fitting does positively impact the performance of the tests, e.g. for and binary . In the cases where cross-fitting is not necessary, it does not seem to negatively impact the performance of the test.

4.2 Compositional confounding in relationship between income and race

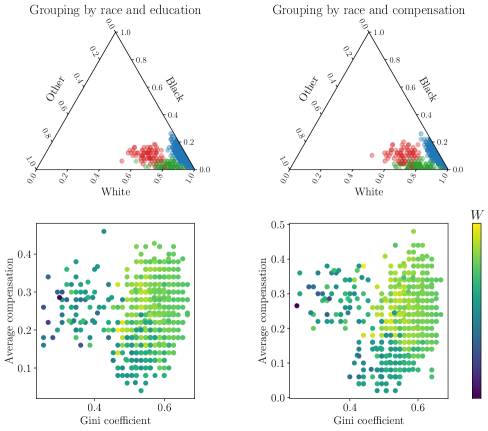

In this section we provide an example based on real data that illustrates how failing to adjust for compositional confounding can lead to incorrect conclusions about effects of compositional variables. We consider the ‘Adult’ dataset available from the UCI machine learning repository (Becker and Kohavi, 1996). This dataset is based on an extract from the 1994 US Census database and consists of data on 48,842 individuals. The response variable in the data, compensation, is a binary variable where and encode whether an individual makes below or above 50,000 USD per year, respectively. Additionally, we consider the demographic features age (numeric, between 17 and 90), education (categorical, with 16 categories), sex (binary, encoding male and female) and race (categorical, with categories ’White’, ’Black’ and ’Other’).

We now use this individual-level data to construct community-level datasets by artificially grouping individuals together. This allows us to construct settings, where there is a known dependence between the racial diversity of the communities and the response variable. As we show below, this illustrates the potential pitfalls of ignoring compositional structure in the data and how the approach based on perturbations solves these issues. More specifically, we group all individual-level observations into groups of around individuals. We then create a new response variable by averaging the individual-level compensation in each group. Similarly, we create a predictor variable by averaging age and sex and selecting the majority class of the categorical variable education (breaking ties randomly). Finally, we create a compositional predictor by computing the proportions of ‘White’, ‘Black’ and ‘Other’ individuals in each group. To ensure, a (partially) known effect of increased racial diversity on compensation, we construct three categories of groups (0, 1 and 2). We construct these categories in two different ways:

-

•

Grouping by race and education: Groups in category 1 are sampled to be similarly diverse and with lower educational levels than the total population and category 2 groups are sampled to be more diverse and with higher educational levels than the total population. The groups in category 0 consist of groups constructed randomly from the remaining individuals.

-

•

Grouping by race and compensation: Groups in category 1 are sampled to be similarly diverse and with lower average compensation than the total population and category 2 groups are sampled to be more diverse and with higher average compensation than the total population. The groups in category 0 consist of groups constructed randomly from the remaining individuals.

We then sample groups from each category, using a weighted sampling approach described in detail in Section S4.3 of the supplementary material. This results in observations with in category , in category and in category when grouping on education and in category , in category and in category when grouping on compensation. For each type of grouping the racial composition for the resulting groups is illustrated in the top half of Figure 5. In both cases we expect that – by construction – there is a positive effect of increased diversity on compensation (for the grouping by race and education this is because education is positively associated with compensation).

Bottom: Plot of average compensation per group () against Gini coefficient colored by the value of ( takes values in a -dimensional subset of ). Depending on the color the dependence between and the Gini coefficient changes.

Based on the two constructed community-level datasets, we now compare a naive approach that neglects the simplex structure and is applied in the literature (e.g. Richard (2000); Richard et al. (2007); Lu et al. (2015); Paarlberg et al. (2018)) with the perturbation-based approach. The naive approach summarizes racial diversity in a single measure, here we use minus the Gini coefficient as in Example 5, for which large values correspond to high diversity, and estimate associations between this measure and the average compensation . We call the method that regresses on linearly naive_diversity. This estimator can easily be adapted to also adjust for the additional covariates , the racial composition or both under a partially linear model assumption. The point estimates together with asymptotic confidence intervals (based on an efficient partialling out estimator like the estimator in (3)) are provided in Table 3. The naive estimator that conditions either on the empty set or on both result in significant negative effects which by construction of the datasets is incorrect. Furthermore, additionally conditioning on , leads to an ill-conditioned estimator as is now a perfect predictor of the diversity measure. This is also visible in the large resulting confidence intervals. While we here constructed the groups in a way to highlight how compositional confounding can be misleading, we believe that this type of confounding is likely also present in real-world settings as groupings are often confounded (e.g., educational levels may well be correlated with race and average compensation in actual communities).

These pitfalls can be avoided with a perturbation-based analysis. In this setting, we propose to apply with and without conditioning on the additional covariates . The results are also shown in Table 3. As desired one gets significant positive effects with this method as it is adapted to the simplex. Interestingly, for that adjusts for the effect disappears for the grouping based on education. This is expected because the association between diversity and compensation was constructed based on education which is also part of .

| Method | Grouping on education | Grouping on compensation | ||

|---|---|---|---|---|

| Estimate | CI | Estimate | CI | |

| naive_diversity | ||||

4.3 Variable influence measures when predicting BMI from gut microbiome

In this section, we analyze the ‘American Gut’ (McDonald et al., 2018) dataset which contains a collection of microbiome measurements and metadata from over 10,000 human participants. We use the pre-processed version used in Bien et al. (2021) (available at https://github.com/jacobbien/trac-reproducible/tree/main/AmericanGut). Our focus is on the relationship between body mass index (BMI) and gut microbiome composition at the species-level and our primary goal is to determine which species are important for predicting BMI. We consider the subset of individuals from the United States with BMI between 15 and 40, height between 145 and 220 cm and age above 16 years. To reduce the dimensionality of the microbiome composition (i.e., the number of species), we perform an initial variable screening and only include species that appear in at least of the observations and where the mean abundance is greater than (this is after scaling the absolute counts by the total number of reads for each observation). The resulting dataset consists of 4,581 observations of measurements and the relative abundances of microbial species .

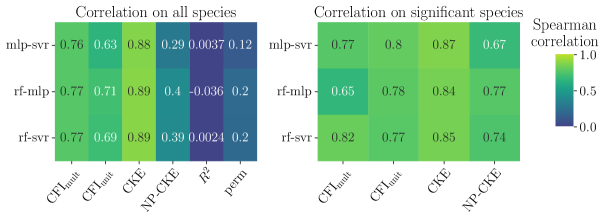

We begin by evaluating, how sensitive the proposed perturbation effect estimates are with respect to the employed nuisance function estimators. To this end, we consider three different regression methods: random forest (rf), neural network (mlp) and kernelized support vector regression using an RBF kernel (svr). Each of the regressions is combined with a grid-search cross-validation to automatically tune the hyperparameters of each method. For each of the three regression methods and all the species we then compute , and using the estimator based on a partially linear model and the using the nonparametric estimator. As baselines, we additionally compute a nonparametric (Williamson et al., 2021) and permutation importance (Breiman, 2001). Figure 6 shows the Spearman correlation between the estimates from the different regression methods.

While the average perturbation effect estimates which are specifically tailored to the compositional setting are consistent across different regression methods, the permutation and measures are – unsurprisingly – not. The population version of the nonparametric is always , so the estimates are essentially mean zero random noise that depends on the estimator. For the permutation measure the inconsistency comes the fact that the permuted data inherently leave the support of the simplex, making the resulting influence measure highly dependent on how the regression methods extrapolate. Unfortunately, due to a lack of alternatives, it is still common to use these types feature importance or influence measures in microbiome science (e.g., Marcos-Zambrano et al., 2021). Furthermore, the results show that the nonparametric estimator of the CKE is less well-behaved than the other estimators based on the partially linear model. One reason for this could be that dividing by the propensity score estimator results in a more unstable estimate, particularly when the propensity score is poorly estimated.

Next, we empirically demonstrate that simply ignoring the simplex constraint is not an option. To this end we consider a standard approach for estimating effects of coordinates for unconstrained Euclidean data. More specifically, we compare the proposed (with estimator based on the partially linear model) with a similar estimator but based on the partially linear model in which the parameter is unidentified due to the simplex constraint. For both methods we use a regression estimator that uses cross-validation to select the best estimator out of a linear regression, random forest and support vector regression. As expected the results from the estimator that ignores the simplex structure are meaningless; for example, , a proxy for the variance explained by the linear effect, is larger than for all species. In contrast, for these values lie between and .

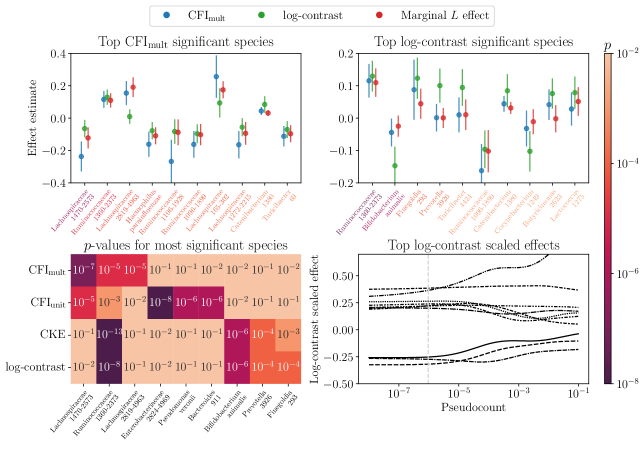

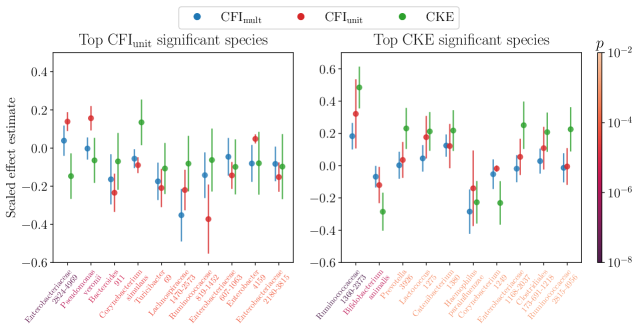

We now analyze different types of average perturbation effects and compare them with the commonly used log-contrast based analysis. We fit both a standard log-contrast regression and an -penalized log-contrast regression and then use the coefficients as feature influences. Since the log-contrast model is only defined on the open simplex, that is, it does not permit zeros in the data, one usually adds a ‘pseudocount’ to each observation before rescaling to the simplex. We follow a standard recommendation and use the minimum non-zero observation of divided by (this is not required for the perturbation-based measures). To investigate how the log-contrast approach compares to the perturbation-based approach, we plot the most significant hits using (with random forests as regression method) and a log-contrast regression model in the top row of Figure 7. These are comparable quantities since is equal to the th coefficient in a log-contrast model when it is correctly specified and no zeros are present. We omit plotting the -penalized log-contrast estimates as these are broadly similar to the standard log-contrast estimates in this example. We also plot a marginal effect of which corresponds to predicting using OLS on and correcting for the presence of zeros as we mention in Remark 1. The results with corresponding -confidence intervals are given in the top row of Figure 7; top most significant species sorted according to significance of (left) and according to log-contrast coefficients (right).

While the effects overlap for some of the features, there are also significant differences. To further illustrate these differences, we present the -values from , , and the log-contrast method for several species in the bottom left of Figure 7. From these -values, we can see that the log-contrast and are highly correlated and appear to be selecting similar species. This is despite the fact that the log-contrast model is supposed to model the continuous effect of each species. The similarities to the hence indicates (likely due to the pseudocounts) that the log-contrast coefficients are instead capturing the effects of presence and absence of species. To further investigate this, for different values of pseudocounts we plot log-contrast estimates (scaled by the standard deviation of ) in the bottom right of Figure 7. This further highlights the dependence of the log-contrast coefficients on the used pseudocount. The fact that the perturbation-based effects explicitly account for zeros and allow us to distinguish between continuous effects (e.g., or ) and presence/absence effects are an important feature of the perturbation-based approach. In Section S4.4 of the supplementary material we provide an additional plot like the top row of Figure 7 which illustrates the significant hits of and when compared to estimates using .

5 Theoretical analysis of estimators

In this section we prove asymptotic normality uniformly over large classes of distributions for each of the three estimation methods described in Section 3; nonparametric estimation of , nonparametric estimation of and by means of estimating in the partially linear model (17). These results are derived using standard proof techniques from the semiparametric literature and likely exist individually in similar form elsewhere (e.g., Klyne and Shah, 2023; Chernozhukov et al., 2018). We do not claim that any of the derived asymptotic results are novel or surprising but include them for completeness and to motivate the precise form of the estimators and their corresponding variance estimates.

We start from a given perturbation and a corresponding reparametrization which reparametrizes into and assume that satisfy (2) if is a binary perturbation and that is derivative-isolating if is a directional perturbation. Our goal is now to use the estimation procedures discussed in Section 3 to estimate the average perturbation effects (i.e., or ) consistently and construct asymptotically valid confidence intervals for the estimates. To construct asymptotically valid confidence intervals, we estimate both the target parameter and its variance and then show that the resulting standardized estimators are asymptotically normal with a uniform convergence rate over the class of possible distributions of the data. Distributionally uniform results are desirable here as they ensure uniform coverage guarantees of the confidence intervals. The following result shows uniform asymptotic normality of each of the three estimation procedures.

Theorem 1 (Uniform asymptotic normality).

Let denote a class of distributions of and assume we are in one of the following settings.

- (a)

- (b)

- (c)

Then, letting denote the cumulative distribution function of the standard normal distribution, it holds that

The result is proven in Section S5 of the supplementary material. In the following three sections, we go over each of the settings (a), (b) and (c) individually and provide the required assumptions and detailed algorithms for the target parameter and variance. For the remainder of this section, we omit -subscripts for simplicity and use the following notation to help us express the uniformly asymptotic results rigorously. Let denote a family of sequences of random variables indexed by . For a nonnegative sequence we write if for all it holds that

that is, converges to in probability uniformly over . We also write if for all there exist and such that

that is, is bounded in probability for large . When we write conditional expectations given a fitted regression function we mean a conditional expectation given the random variables used to fit and any additional randomness involved in the fitting.

5.1 Nonparametric estimation for directional effects