General Derivative-Free Optimization Methods under Global and Local Lipschitz Continuity of Gradients

Abstract. This paper addresses the study of derivative-free smooth optimization problems, where the gradient information on the objective function is unavailable. Two novel general derivative-free methods are proposed and developed for minimizing such functions with either global or local Lipschitz continuous gradients. The newly developed methods use gradient approximations based on finite differences, where finite difference intervals are automatically adapted to the magnitude of the exact gradients without knowing them exactly. The suggested algorithms achieve fundamental convergence results, including stationarity of accumulation points in general settings as well as global convergence with constructive convergence rates when the Kurdyka-Łojasiewicz property is imposed. The local convergence of the proposed algorithms to nonisolated local minimizers, along with their local convergence rates, is also analyzed under this property. Numerical experiences involving various convex, nonconvex, noiseless, and noisy functions demonstrate that the new methods exhibit essential advantages over other state-of-the-art methods in derivative-free optimization.

Key words: derivative-free optimization, finite differences, black-box optimization, noisy optimization, zeroth-order optimization

Mathematics Subject Classification (2020) 90C25, 90C26, 90C30, 90C56

1 Introduction

This paper addresses developing novel derivative-free methods to solve unconstrained optimization problems given in the form

| (1.1) |

where is a continuously differentiable (-smooth) function, and where only a noisy approximation of the objective function is computable. It means that the gradient information of the objective function is fully unavailable, even in the noiseless case when the noise function vanishes. These problems have received much attention with a variety of methods being developed over the years. The major developments in this vein are provided by the Nelder-Mead simplex method [31, 37], direct search methods [17, 20] and trust-region methods [13]. More recently, numerous empirical results conducted by Shi et al. in [47] show that derivative-free optimization methods based on finite differences are accurate, efficient, and in some cases superior to other state-of-the-art derivative-free optimization methods established in the literature. Meanwhile, extensive numerical comparisons in Berahas et al. [7] together with the further analysis by Scheinberg [45] also tell us that the accuracy of gradients obtained from finite differences is much higher than from randomized schemes. These empirical results suggest that the methods using finite differences have much to be recommended, and that the research in this direction should be strongly encouraged.

There are several derivative-free optimization methods in the literature that successfully employ finite differences. Kelley et al. [11, 16, 25] proposed the implicit filtering algorithm based on a finite difference approach to deal with noisy smooth box-constrained optimization problems. Berahas et al. [6, 8] developed finite difference-based line search methods for the minimization of noisy smooth functions. The approaches to compute the finite difference interval are also studied by Gill et al. [15], and recently by Moré and Wild [36] as well as by Shi et al. [46]. Although methods of this type are often used in practice to solve derivative-free smooth problems, the theoretical understanding of behavior of their iterates in general cases is rather limited in comparison with analysis of classical first-order methods. Stationarity of accumulation points is a fundamental convergence property that is achieved by many first-order methods [9, 38] and by some derivative-free optimization algorithms using the simplex-based direct method [44, Theorem 3.2], line search based on simplex derivatives [12, Chapter 9], coordinate search with difference Hessians [35, Theorem 4.2]. However, to the best of our knowledge, this property has not been established for derivative-free methods employing finite differences for general classes of smooth functions (i.e., smooth functions with global or local Lipschitz continuous gradients), even in noiseless cases. Note that the convergence properties of derivative-free methods for noisy functions studied in [8, 6] do not ensure them for noiseless functions. The reason is that the usual selection of finite difference intervals based on the noise level becomes zero, being invalid therefore in this case; see, e.g., [6, Equations (3.3), (3.4)]. The implicit filtering algorithm [11, Theorem 2.1], although achieving the stationarity for accumulation points, requires the objective function to be -smooth with rather strict conditions including the boundedness of level sets and the uniform boundedness of the inverses of Hessians. Furthermore, the convergence of the sequence of iterates to a nonisolated stationary point is also ignored in the analysis of aforementioned derivative-free optimization methods while obtained by various first-order methods [4, 26, 27, 28] under the Kurdyka-Łojasiewicz (KL) property [3, 30, 32], which is a rather mild regularity condition satisfied for the vast majority of objective functions in practice. Of course, the local convergence to nonisolated local minimizers for such derivative-free methods is still questionable.

The assumption of global Lipschitz continuity of the gradient seems to be omnipresent in derivative-free line search methods; see, e.g., [11, Theorem 2.1], [6, Assumption A1], [8, Assumption 1.1]. For general derivative-free trust-region methods, Conn et al. [13] prove global convergence results under the global Lipschitz continuity of the gradient and the Hessian of the objective function. Such properties are also employed in the proximal point method adapted to derivative-free smooth optimization problems by Hare and Lucet [18, Assumption 1]. We are not familiar with any efficient finite difference-based method considering specifically the class of smooth functions with locally Lipschitz continuous gradients, which is much broader than the class of smooth functions with globally Lipschitz continuous gradients and covers, in particular, -smooth functions. This is in contrast to the exact versions of gradient descent methods, which obtain various convergence properties including the stationarity of accumulation points for the version with backtracking stepsizes on the class of -smooth functions [9, Proposition 1.2.1] and the global convergence for the version with sufficiently small stepsizes on the class of definable -smooth functions with locally Lipschitz continuous gradients [23]. This raises the need for the design and analysis of finite difference-based methods concerning the class of smooth functions with locally Lipschitz continuous gradients, which is the best we can hope in this context since the error bounds for finite differences are not available outside this class.

Having in mind the above discussions, we propose in this paper two novel derivative-free methods for minimizing smooth functions. A general derivative-free method with constant stepsize is designed for smooth functions whose gradients are globally Lipschitzian although the exact calculation of the Lipschitz constant is not necessary. A general derivative-free method with backtracking stepsize is designed for smooth functions whose gradients are only locally Lipschitzian. Such newly developed methods are analyzed rigorously for noiseless functions, which particularly have many applications in the design of space trajectories [2], reinforcement learning [33], and other black-box optimization problems [5, 34]. For such problems, the objective functions may in fact well-behave, even being smooth, while the exact gradient information is either unavailable due to the lack of analytical forms of the objective function, or it is computationally expensive to obtain. The main ideas for our methods come mostly from the inexact reduced gradient methods (IRGM) introduced and justified in [26]. Roughly speaking, the newly developed derivative-free methods are designed as inexact gradient descent methods for smooth functions and thus inherit typical convergence properties for first-order methods including stationarity of accumulation points, global convergence under the KL property, and constructive convergence rates depending on the KL exponent. Furthermore, we establish local convergence to nonisolated local minimizers for both proposed methods under the KL property of the objective function.

Regarding numerical aspects, our methods borrow the ideas of gradient approximations from IRGM [26] and its nonsmooth extensions [27, 28], where errors are automatically adapted to the magnitude of exact gradients; see, e.g., [26, Section 6.2]. Correspondingly, the proposed derivative-free methods generate at each iteration a descent direction based on an approximate gradient associated with the largest finite difference interval. Choosing such an interval in this way allows the methods to omit rounding errors as much as possible, which makes them more efficient without knowing the noise level in advance. This selection of the finite difference interval is also completely different from the selection used in the implicit filtering algorithm [11, 16, 25], since the latter forces the finite difference interval to decrease after each iteration while ours does not. Extensive empirical results on diverse datasets including convex, nonconvex, noiseless, and noisy functions with different noise levels in different finite-dimensional spaces show that our newly developed methods usually perform better than many other state-of-the-art derivative-free methods in solving smooth problems. For the conciseness of the paper, the convergence analysis and numerical experiments involving methods coupled with quasi-Newton algorithms are not considered here but are deferred to our future research.

The rest of the paper is organized as follows. Section 2 presents some basic definitions and preliminaries used throughout the entire paper. Section 3 examines two types of approximation for gradients that cover finite differences. The main parts of our work concerning the design and convergence properties of general derivative-free methods under the global and local Lipschitz continuity of the gradient are given in Section 4 and Section 5, respectively. Local convergence of the proposed methods to nonisolated local minimizers is presented in Section 6. Numerical experiments comparing the efficiency of the proposed methods with other derivative-free methods for both noisy and noiseless functions are conducted in Section 7. Concluding remarks on the contribution of this paper together with some open questions and perspectives of our future research are given in Section 8.

2 Preliminaries

First we recall some basic notions and notation frequently used in the paper. All our considerations are given in the space with the Euclidean norm . For any , let denote the basic vector in As always, signifies the collection of natural numbers. For any and let and stand for the open and closed balls centered at with radius , respectively. When , these balls are denoted simply by and .

Recall that a mapping is Lipschitz continuous on a subset of if there exists a constant such that we have

If , the mapping is said to be globally Lipschitz continuous. The local Lipschitz continuity of on is understood as the Lipschitz continuity of this mapping on every compact subset of . The latter is equivalent to saying that for any there is a neighborhood of such that is Lipschitz continuous on , which is also equivalent to the Lipschitz continuity of on every bounded subset of . In what follows, we denote by the class of -smooth mappings that have a locally Lipschitz continuous gradient on and by the class of -smooth mappings that have a globally Lipschitz continuous gradient with the constant on the entire space.

Our convergence analysis of the numerical algorithms developed in the subsequent sections takes advantage of the following important results and notions. The first result taken from [21, Lemma A.11] presents a simple albeit very useful property of real-valued functions with Lipschitz continuous gradients.

Lemma 2.1.

Let , and let . If is differentiable on the line segment with its derivative being Lipschitz continuous on this segment with a constant , then

| (2.1) |

The second lemma established in [26, Section 3] is crucial in the convergence analysis of the general linesearch methods developed in this paper.

Lemma 2.2.

Let and be sequences in satisfying the condition

| (2.2) |

If is an accumulation point of and if the origin is an accumulation point of , then there exists an infinite set such that

| (2.3) |

Next we recall the classical results from [14, Section 8.3.1] that describe important properties of accumulation points generated by a sequence satisfying a limit condition introduced by Ostrowski [41].

Lemma 2.3.

Let be a sequence satisfying the Ostrowski condition

| (2.4) |

Then the following assertions are fulfilled:

(i) If is bounded, then the set of accumulation points of is nonempty, compact, and connected in .

(ii) If has an isolated accumulation point, then this sequence converges to it.

The version of the Kurdyka-Łojasiewicz property below is taken from Absil et al. [1, Theorem 3.4].

Definition 2.4.

Let be a differentiable function. We say that satisfies the KL property at if there exist a number , a neighborhood of , and a nondecreasing function such that the function is integrable over and we have

| (2.5) |

Remark 2.5.

If satisfies the KL property at with a neighborhood , it is clear that the same property holds for any where . It has been realized that the KL property is satisfied in broad settings. In particular, it holds at every nonstationary point of ; see [3, Lemma 2.1 and Remark 3.2(b)]. Furthermore, it is proved in the seminal paper by Łojasiewicz [32] that any analytic function satisfies the KL property at every point with for some . As demonstrated in [26, Section 2], the KL property formulated in Attouch et al. [3] is stronger than the one in Definition 2.4. Typical smooth functions that satisfy the KL property from [3], and hence the one from Definition 2.4, are smooth semialgebraic functions and also those from the more general class of functions known as definable in o-minimal structures; see [3, 4, 30]. The latter property is fulfilled, e.g., in important models arising in deep neural networks, low-rank matrix recovery, principal component analysis, and matrix completion as discussed in [10, Section 6.2].

Next we present, based on [1], some descent-type conditions ensuring the global convergence of iterates for smooth functions that satisfy the KL property.

Proposition 2.6.

Let be a -smooth function, and let the sequence of iterations satisfy the following conditions:

-

(H1)

(primary descent condition). There exists such that for sufficiently large we have

-

(H2)

(complementary descent condition). For sufficiently large , we have

If is an accumulation point of and satisfies the KL property at , then as .

When the sequence under consideration is generated by a linesearch method and satisfies some conditions stronger than (H1) and (H2) in Proposition 2.6, its convergence rates are established in [26, Proposition 2.4] under the KL property with as given below.

Proposition 2.7.

Let be a -smooth function, and let the sequences satisfy the iterative condition for all . Assume that for sufficiently large , we have and the estimates

| (2.6) |

where are some positive constants. Suppose in addition that the sequence is bounded away from i.e., there is some such that for sufficiently large , that is an accumulation point of , and that satisfies the KL property at with for some and . Then the following convergence rates are guaranteed:

-

(i)

If , then the sequence converges linearly to .

-

(ii)

If , then we have the estimate

Remark 2.8.

Observe that the two conditions in (2.6) together with the boundedness away from of yield assumptions (H1), (H2) in Proposition 2.6. Indeed, (H1) is verified by the following inequalities:

In addition, since is bounded away from , there is such that for sufficiently large . Then for such , the condition implies that by the first inequality in (2.6), and hence by the iterative procedure This also verifies (H1).

3 Global and Local Approximations of Gradients

This section is devoted to analyzing several methods for approximating gradients of a smooth function by using only information about function values that frequently appears in derivative-free optimization. Methods of this type include, in particular, finite differences [40, Section 9], the Gupal estimation [19], and gradient estimation via linear interpolation [7]. We construct two types of approximations that cover all these methods.

Definition 3.1.

Let be a -smooth function. A mapping is :

(i) A global approximation of if there is a constant such that

| (3.1) |

(ii) A local approximation of if for any bounded set and any , there is with

| (3.2) |

Remark 3.2.

We have the following observations related to Definition 3.1:

(i) If is a global approximation of , then it is also a local approximation of .

(ii) Assume that is a local approximation of and that . Then we deduce from (3.2) with and any the condition

| (3.3) |

Next we recall the two standard types of finite differences taken from [40, Section 9], which serve as typical examples of the approximations in Definition 3.1.

Forward finite difference:

| (3.4) |

Central finite difference:

| (3.5) |

Remark 3.3.

Let us now recall some results on the error bounds for the two types of finite differences that are mentioned above.

For completeness, we present a short proof showing that both types of finite differences are global approximations of when and are local approximations of when .

Proposition 3.4.

Let be a -smooth function. Then the following hold:

(i) Given and , if is Lipschitz continuous on the with the constant , then both the forward finite difference (3.4) and the central finite difference (3.5) satisfy the estimate

| (3.6) |

[Proof.] First we verify (i) for each type of the aforementioned finite difference and then employ (i) to justify (ii) and (iii) for both types.

(i) Take any and assume that is Lipschitz continuous on with the constant . Consider first the case where is given by the forward finite difference (3.4). Then for any we get by employing Lemma 2.1 that

| (3.9) |

which is clearly equivalent to

Since the latter inequality holds for all , we deduce that

which therefore verifies estimate (3.6).

Assume now that is given by the central finite difference (3.5). Employing Lemma 2.1 gives us for any the two estimates

Summing up the above estimates and using the triangle inequality, we deduce that

which implies in turn the conditions

for all . Therefore, we get

which brings us to (3.6) and thus justifies (i).

Assertion (ii) follows directly from (i). To verify (iii), take some and a bounded set , and then find such that . Defining , it is clear that is compact. Since is locally Lipschitzian, it is Lipschitz continuous on with some constant . Taking any we get that , and thus is Lipschitz continuous on with the constant . Employing finally (i), assertion (iii) is justified. The following example shows that when the local Lipschitz continuity of is replaced by merely the continuity of , the finite differences may not be local approximation of .

Example 1.

Define the univariate real-valued function by

The derivative of is calculated by

being clearly continuous on while not Lipschitz continuous around . If we suppose that is the forward finite difference approximation of from (3.4), we get that

which implies that as . It follows from (3.3) that is not a local approximation of the derivative . Supposing now that is the central finite difference approximation of , we deduce from (3.5) the expression

which also tells us that is not a local approximation of .

4 General Derivative-Free Methods for Functions

This section addresses the optimization problem (1.1) when for some . In the context of derivative-free optimization, we assume that the only information about the function value is available. This means that is not exactly computable at every , and the Lipschitz constant of is also not available. By employing gradient approximation methods that satisfy the global error bound (3.1), we propose here the general Derivative-Free method with Constant stepsize (DFC) to solve this problem with providing its convergence analysis. The DFC algorithm is described as follows.

Algorithm 1 (DFC).

Step 0.

Choose a global approximation of under condition (3.1). Select an initial point an initial sampling radius a constant a reduction factor , and scaling factors . Set

Step 1 (approximate gradient).

Find and the smallest nonnegative integer such that

Then set

Step 2 (update).

If , then and Otherwise, and

Remark 4.1.

Let us now present some observations on Algorithm 1. The first observation clarifies the existence of and in Step 1. Observation (ii) presents the ideas behind the construction of the algorithm. Observation (iii) explains the iteration updates in Step 2 while observation (iv) interprets the term “constant stepsize” in the name of our method.

(i) The procedure of finding and that satisfy Step 1 can be given as follows. Set and set

| (4.1) |

While , increase by and recalculate under (4.1). When , the existence of and in Step 1 is guaranteed. Indeed, otherwise we get a sequence with

| (4.2) |

Since the latter means that as Since is a global approximation of , for given in (3.1), we get

Letting with taking into account that , the latter inequality implies that , which is a contradiction.

(ii) Since is a global approximation of , let be a constant given in (3.1). Since is unknown, Algorithm 1 generates the sequence that approximates . Assume that in some iteration the constant is slightly larger than . Then Step 1 of Algorithm 1 provides

| (4.3) |

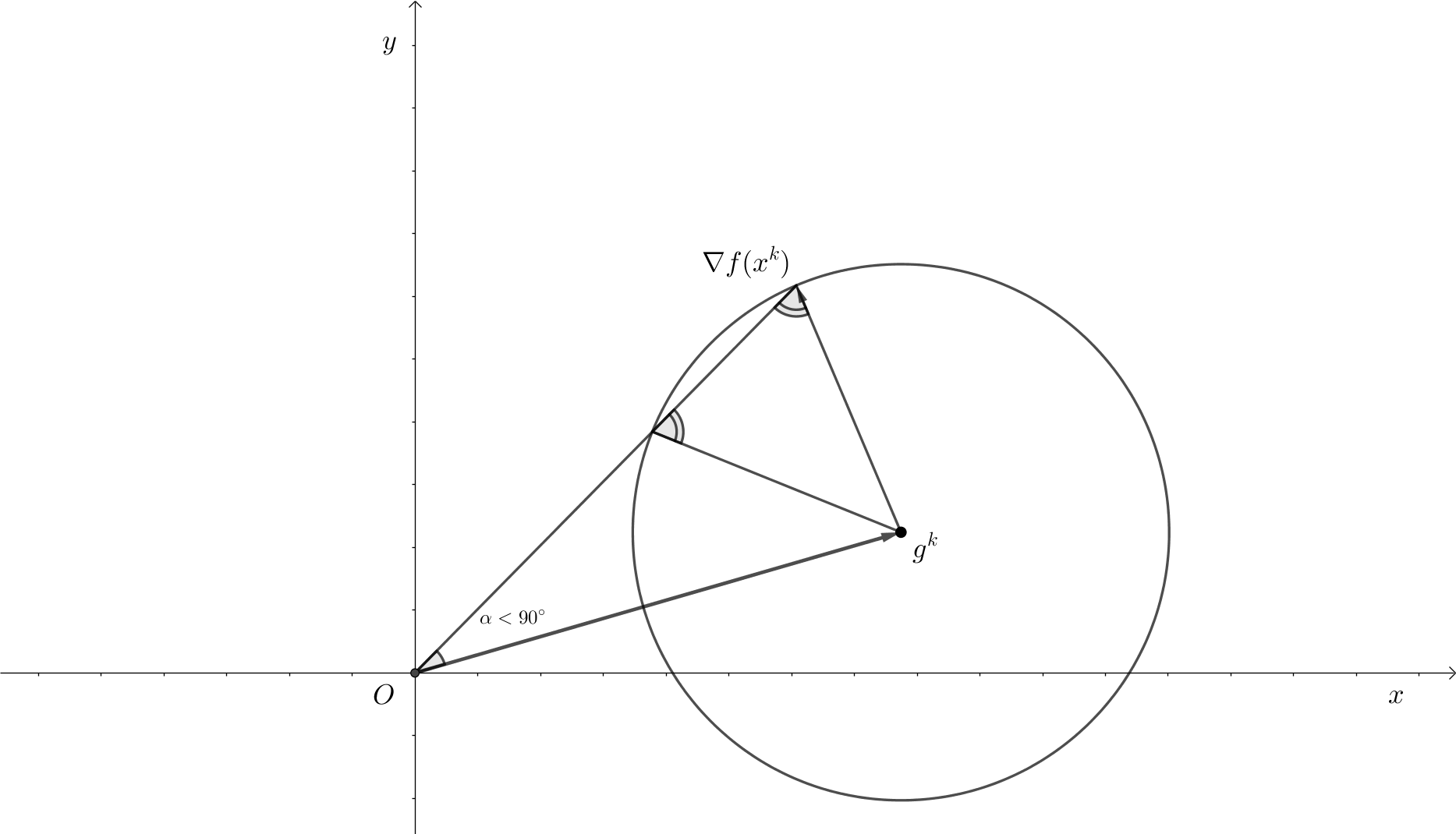

Since , the inequality above gives us which yields the angle condition as illustrated in the Figure 1 below.

Moreover, the result of [27, Theorem 3.2] about the convergence of general inexact gradient methods also tells us that the sequence satisfying the procedure and condition (4.3) achieves fundamental convergence properties. Although the Lipschitz constant of is not available in our context, it is linearly related to for some choice of ; e.g., when is obtained from finite differences, we get by Proposition 3.4 that . Thus the procedure can be replaced by

In the formulation of Algorithm 1, the constant can be chosen as an arbitrary positive number, which creates more flexibility for our method.

(iii) The condition determines whether is a good approximation for in the sense that the objective function is sufficiently decreasing when the iterate moves from to . If the condition does not hold, we increase by setting to get a better approximation for and stagnate the iterative sequence by setting .

(iv) It will be shown in Proposition 4.2 that there exists a positive number such that for sufficiently large , which also implies that for such . This explains the term “constant stepsize” in the name of our algorithm.

The next proposition verifies that the tail of the sequence generated by Algorithm 1 is constant, which is crucial in deriving the fundamental convergence properties of the algorithm.

Proposition 4.2.

Let be the sequence generated by Algorithm 1. Assume that for all . Then there exists a number such that whenever .

[Proof.] Since is a global approximation of under condition (3.1), there exists such that

| (4.4) |

Since is globally Lipschitz continuous, we also find such that is Lipschitz continuous with the constant on . Arguing by contradiction, suppose that the number asserted in the proposition does not exist. By Step 2 of Algorithm 1, this implies that for infinitely many , and hence . Therefore, there is a number such that and . Using Step 2 of Algorithm 1 together with the update , we deduce that

| (4.5) |

Combining and from Step 1 of Algorithm 1 with (4.4) and as above, we get the relationships

By the Cauchy-Schwarz inequality, the latter gives us

Combining this with Lemma 2.1 and taking into account the global Lipschitz continuity of with the constant as well as the condition as above, we get that

which clearly contradicts(4.5) and completes the proof of the proposition.

Now we are ready to establish the convergence properties of Algorithm 1.

Theorem 4.3.

Let be the sequence generated by Algorithm 1 and assume that for all Then either , or we have the assertions:

(i) The sequence converges to .

(ii) If satisfies the KL property at some accumulation point of , then .

(iii) If satisfies the KL property at some accumulation point of with for and , then the following convergence rates are guaranteed for :

If , then , , and converge linearly to , , and , respectively.

The setting of ensures the estimates

[Proof.] Since is a global approximation of under condition (3.1), there is such that

| (4.6) |

By , we find such that the gradient mapping is Lipschitz continuous with the constant on . Taking the number from Proposition 4.2 ensures that for all . This implies by Step 2 of Algorithm 1 that

| (4.7) |

which tells us that is decreasing. If , there is nothing to prove, so we assume that , which implies that is convergent. As a consequence, we get as . Then (4.7) tells us that . From Step 1 of Algorithm 1 it follows that

| (4.8) |

which implies that as . It further follows from and (4.6) that

| (4.9) |

which yields as and thus justifies (i).

To verify (ii), take any accumulation point of and assume that satisfies the KL property at . By (4.8) and (4.9), we obtain that

where . This together with (4.7) yields condition (2.6) in Proposition 2.7. By Remark 2.8(i), assumptions (H1) and (H2) in Proposition 2.6 hold. Therefore, as , which justifies (ii).

To proceed with the proof of assertion (iii) under the KL property at with , we use the iterations as in Step 2 of Algorithm 1 together with from Step 1 of Algorithm 1. This gives us for . Combining the latter with (4.7) and (4), we see that all the assumptions in Proposition 2.7 are satisfied. This verifies the convergence rates of to stated in (iii). Since is an accumulation point of , it follows from (i) that is a stationary point of , i.e., . Hence the usage of Lemma 2.1 and the decreasing property of yields

which justifies the convergence rates of to as asserted in (iii).

It remains to verify the convergence rates for . Since is Lipschitz continuous with the constant , the claimed property follows from the convergence rates for due to

This therefore completes the proof of the theorem.

5 General Derivative-free Methods for Functions

In this section, we propose and justify the novel Derivative-Free method with Backtracking stepsize (DFB) to solve the optimization problem (1.1). The main result here establishes the global convergence with convergence rates of the following algorithm, which employs gradient approximations satisfying the local error bound estimate (3.2).

Algorithm 2 (DFB).

Step 0 (initialization).

Choose a local approximation of under condition (3.2). Select an initial point and initial radius , a constant , factors , , linesearch constants , , and an initial bound . Choose a sequence of manually controlled errors such that as . Set

Step 1 (approximate gradient).

Select and the smallest nonnegative integer so that

| (5.1) |

Then set .

Step 2 (linesearch).

Set . While

| (5.2) |

set

Step 3 (stepsize and parameters update).

If , then set , , and . Otherwise, set and .

Step 4 (iteration update).

Set Increase by and go back to Step 1.

Remark 5.1.

(i) Fix any . The procedure of finding and that satisfies Step 1 of Algorithm 2 can be given as follows. Set and calculate as

| (5.3) |

While , increase by and recalculate by formula (5.3). We now show that when , this procedure stops after a finite number of steps giving us and as desired. Indeed, assuming the contrary that the procedure does not stop, we get a sequence of with

| (5.4) |

Since is a local approximation of , for any fixed the condition (3.2) with ensures the existence of a positive number such that

| (5.5) |

By , there is with for all . Combining this with (5.4) and (5.5) yields

Letting , we arrive at , which is a contradiction.

(ii) It follows directly from the construction of in Step 1 of Algorithm 2 that

| (5.6) |

To proceed further with the convergence analysis of Algorithm 2, we obtain two results of their independent interest. The first one reveals some uniformity of general linesearch procedures with respect to the selections of reference points, stepsizes, and directions.

Lemma 5.2.

Let be a function with a locally Lipschitz continuous gradient, and let . Then for any nonempty bounded set , there exists such that

[Proof.] The boundedness of gives us such that . Using the continuity of and the compactness of , we define . Since , there is such that is Lipschitz continuous with the constant on . By , we find with . Now take some and such that and . The choice of gives us by the Cauchy-Schwarz inequality that

| (5.7) |

and by using the triangle inequality that

Combining the latter with the choice of , and the construction of yields

which ensures that . The convexity of tells us that the entire line segment lies on . Remembering that is Lipschitz continuous with the constant on , we employ Lemma 2.1 by taking into account that and that (5.7). This gives us

and thus completes the proof of the lemma.

Employing the obtained lemma, we derive the next result showing that unless the stationary point is found, Algorithm 2 always makes a progress after a finite number of iterations.

Proposition 5.3.

Let and be the sequences generated by Algorithm 2, and let be such that . Then we can choose a number so that .

[Proof.] Assume on the contrary that for all . Steps 3 and 4 of Algorithm 2 give us

| (5.9) |

Therefore, for all which implies that and in Step 1 of Algorithm 2 exist for all . Since is a local approximation of , for any fixed condition (3.2) with ensures the existence of with

| (5.10) |

It follows from Lemma 5.2 with that there is some such that

| (5.11) |

Using , , and (5.9) gives us for which and . Then we get from (5.10) with taking into account that

Combining this with from (5.6) provides the estimate

which implies by the triangle inequality that

Employing the latter together with (5.11) and yields

| (5.12) |

It follows from (5.12) and the choice of parameters that

which implies in turn by Step 2 of Algorithm 2 that

By Step 3 of Algorithm 2, we conclude that , a contradiction which completes the proof. Now we are ready the establish the convergence properties of Algorithm 2.

Theorem 5.4.

Let be the sequence generated by Algorithm 2 and assume that for all Then either , or the following assertions hold:

(i) Every accumulation point of is a stationary point of .

(ii) If the sequence is bounded, then the set of accumulation points of is nonempty, compact, and connected in .

(iii) If has an isolated accumulation point, then this sequence converges to it.

[Proof.] First it follows from Steps 2 and 3 of Algorithm 2 that

| (5.13) |

which tells us that is nonincreasing. If , there is nothing to prove; so we assume that , which implies by the nonincreasing property of that . Summing up the inequalities in (5.13) over with taking into account that from the update in Step 3 of Algorithm 2 gives us

| (5.14) |

We divide the proof of (i) into two parts by showing first that the origin is an accumulation point of and then employing Lemma 2.2 to establish the stationarity of all the accumulation points of

Claim 1.

The origin is an accumulation point of the sequence .

Arguing by contradiction, suppose that there are numbers and such that

| (5.15) |

Combining this with (5.14) gives us and . The latter implies that converges to some . By taking a larger , we can assume that for all . Let be the set of all such that . It follows from Proposition 5.3 that is infinite. Hence we can take any with and get that . By Step 3 of Algorithm 2, we deduce that . Fixing some such , we get from the exit condition in Step 2 of Algorithm 2 that

| (5.16) |

The classical mean value theorem gives us such that

| (5.17) |

Combining this with (5.16) yields

which implies by dividing both sides of the inequality by that

| (5.18) |

Take some neighborhood of and . Since is a local approximation of under condition (3.2), there is such that

| (5.19) |

Since and , by taking a larger we can assume that and for all . Using this together with (5.19) and in (5.6), we get that

Combining the latter with , as , and the continuity of gives us

| (5.20) |

which yields by (5.15). It follows from (5.20), , , and for all that . Letting in (5.18) with taking into account the convergence above and (5.20) brings us to the estimate

This contradicts and . Thus the origin is an accumulation point of as claimed.

Claim 2.

Every accumulation point of is a stationary point of .

Take any accumulation point of . Using Claim 1, the second inequality in (5.14), and Lemma 2.2 tells us that there is an infinite set such that

Take a neighborhood of and . Since is a local approximation of under condition (3.2), there exists for which

| (5.21) |

Since and , we can select so that and for all . This ensures together with (5.21) that

Employing and as above, we deduce that , and hence Therefore, is a stationary point of which justifies (i).

Now we verify (ii) and (iii) simultaneously. It follows from (5.14) and for all by the choice of in Step 3 of Algorithm 2 that

which implies that . Then both assertions (ii) and (iii) follow from Lemma 2.3. The next result establishes the global convergence with convergence rates of the iterates in Algorithm 2 under the KL property and the boundedness of . We have already discussed the KL property in Remark 2.5. The boundedness of is also a standard assumption that appears in many works on gradient descent methods; see, e.g., [4, Theorem 4.1], [23, Theorem 1], and [29, Assumption 7].

Theorem 5.5.

Let be the sequence of iterates generated by Algorithm 2. Assuming that for all and that is bounded yields the assertions:

(i) If is an accumulation point of and satisfies the KL property at , then as .

(ii) If in addition to (i), the KL property at is satisfied with for some , then the following convergence rates are guaranteed:

If , then the sequence converges linearly to .

If , then we have the estimate

[Proof.] Let , and let . Since is a local approximation of satisfying condition (3.2), there exists a positive number such that

| (5.22) |

Select so that for all , which implies by (5.22) and the choice of in Step 1 of Algorithm 2 the relationships

| (5.23) |

We split the proof of the result into two parts by showing first that the sequences and are constant after a finite number of iterations and verifying then the convergence of in (i) with the rates in (ii) by using Propositions 2.6 and 2.7.

Claim 1.

There exists such that and for all

Arguing by contradiction, suppose that such a number does not exist. By the construction of and in Step 3 of Algorithm 2, we deduce that and as . Since is bounded, Lemma 5.2 allows us to find for which

| (5.24) |

Using the aforementioned properties of and , we get such that and for all . Fix such a number and then combine the condition from (5.1) with , , and (5). This gives us

which implies together with and (5.24) the estimate

and thus tells us that . Employing Step 3 of Algorithm 2 yields . Since the latter holds whenever , we conclude that the equality is satisfied for all . This contradicts the condition as and hence justifies the claimed assertion.

Claim 2.

All the assertions in (i) and (ii) are fulfilled.

From Step 2 and Step 3 of Algorithm 2, we deduce that

| (5.25) |

Defining with taken from Claim 1 gives us the equalities

| (5.26) |

Combining with (5) and from (5.1) ensures that

| (5.27) |

where . In addition, we have in (5.26), which implies together with Step 3 of Algorithm 2 the relationships

| (5.28) |

confirming the boundedness of from below. If the KL property of holds at the accumulation point of , it follows from Remark 2.8(i), (5.25), (5), and (5.28) that assumptions (H1) and (H2) in Proposition 2.6 hold. Thus as , which verifies (i).

Assume finally that the KL property at is satisfied with , and . The iterative procedure in Step 4 of Algorithm 2 together with (5.28) and from Step 1 therein tells us that for Combining this with (5.25), (5), and (5.28) verifies all the assumptions of Proposition 2.7 and therefore completes the proof of the theorem.

6 Local Convergence of General Derivative-Free Methods to Nonisolated Local Minimizers

In this section, we develop appropriate versions of both Algorithm 1 and Algorithm 2 and obtain efficient conditions that guarantee the local convergence with constructive convergence rates of these algorithms to nonisolated local minimizers.

Algorithm 3 (General derivative-free (GDF) method).

Step 0.

Choose a local approximation of under condition (3.2). Select an initial point an initial sampling radius a sequence a reduction factor and a scaling factor . Choose a sequence of manually controlled sampling radii . Set .

Step 1 (approximate gradient).

Find and the smallest nonnegative integer such that

Then set

Step 2 (update).

Choose a stepsize and set Go back to Step 1.

Similarly to Remark 5.1, the existence of in Step 1 of Algorithm 3 is guaranteed if . The result addressing the local convergence to local minimizers of Algorithm 3 is presented below.

Theorem 6.1.

Let be a -smooth function, let , and let Assume that is a local minimizer of satisfying the KL property at , and that is locally Lipschitz continuous around . Then we have the assertions:

(i) There exist positive numbers , , and such that for any initial point , an initial radius , and sequences , , and . it holds we that the iterative sequence of Algorithm 3 converges provided that for all .

(ii) If in addition the series diverges, then the sequence converges to a local minimizer of with . Moreover, the following convergence rates are guaranteed if the sequence is bounded away from , and if the KL property is satisfied with , and :

Whenever , the sequences , and converge linearly s to the points , , and , respectively.

For , we get the estimates , , and as .

[Proof.] Since satisfies the KL property at , there exist a bounded neighborhood of , a number , and a nonincreasing function such that is integrable over and

| (6.1) |

Remark 2.5 tells us that (6.1) also holds if is replaced by any with . Since is a local minimizer of and since is continuous, we can assume by shrinking if necessary that for all . Combining this with (6.1) ensures that

| (6.2) |

which implies in turn that is the only critical value of within . The local Lipschitz continuity of around gives us positive numbers and such that and is Lipschitz continuous with the constant on . Choose further and define by for with . By the right continuity of at and the continuity of at , we find such that

| (6.3) |

Since is a local approximation of under condition (3.2), we find for which

| (6.4) |

Assuming that , , , and , we now aim at verifying (i). To proceed, let us first prove the following claim.

Claim 1.

Algorithm 3 generates the well-defined iterative sequence , which stays inside .

Indeed, by for all , the existence of in Step 2 of Algorithm 3 is guaranteed in each iteration, which ensures that the iterative sequence is well-defined. To verify that , we proceed by induction. Fix and assume that for all . To show that , observe that for all by the selection of and the construction of in Algorithm 3. Since , we deduce from (6.4) and in Step 1 of Algorithm 3 that

| (6.5) |

It follows from (6.5) with , the triangle inequality, and the choice of that

| (6.7) |

Since , we deduce from the Lipschitz continuity of on that

Combining this with the update , , and (6.7) gives us

which means that . Since and is the minimum value of within , we get that . It follows from the triangle inequality and estimate (6.5) that

which implies in turn that

| (6.8) |

The Lipschitz continuity of on with the constant yields

| (6.9a) | ||||

| (6.9b) | ||||

| (6.9c) | ||||

| (6.9d) | ||||

| (6.9e) | ||||

| (6.9f) | ||||

where (6.9a) follows from Lemma 2.1, (6.9b) follows from the iterative update , (6.9c) follows from the Cauchy-Schwarz inequality, (6.9d) is deduced by from (6.5), (6.9e) follows from , and (6.9f) is deduced by from (6.8). Therefore,

| (6.10) |

As a consequence of the above, we have the inequalities

which ensure together with and (6.2) that for all . Combining the latter with (6.10) leads us to the conditions

where the second inequality follows from the nondecreasing property of Therefore, the triangle inequality gives us the relationships

where the latter inequality is a consequence of the selection and in (6.3). This means that . By induction we arrive at for all , which verifies this claim.

Claim 2.

The sequence of iterates converges to some . If in addition we have , then is a local minimizer of .

Picking any and arguing similarly to the proof of Claim 1 with taking into account that for all , we get the estimates

Passing there to the limit as yields , which tells us that converges to some point . Let now be satisfied. Since , we proceed similarly to the proof of (6.9e) in Claim 1 to show that

| (6.11) |

Combining this with the fact that for all , we deduce that

Supposing that there is with for all sufficiently large, the above inequality gives us , which is a contradiction. Therefore, is an accumulation point of , i.e., there exists an infinite set such that . As in the proof of (6.5) in Claim 1 with taking now into account, we get the estimate

Combining the latter with tells us that . Remembering that converges to , we have that as . Therefore, , i.e., is a stationary point of on . Since is the only critical value of within , we obtain that , which tells us that is a local minimizer of .

Invoke now the assumptions that the sequence is bounded away from and that the KL property (6.1) holds with and. It follows from Steps 1 and 2 of Algorithm 3 that for large . By (6.11) and the iterative procedure , we get

Arguing similarly to (6.8) with taking into account that for all , we deduce that

Therefore, the convergence rates for in (ii) are immediately obtained by applying Proposition 2.7 with observing that the KL property (6.1) also holds with , , and when is replaced by . By arguing similarly to the proof of the convergence rates in Theorem 4.3 and remembering that is Lipschitz continuous on , we verify the desired convergence rates for and in (ii) and thus complete the proof of the theorem.

Remark 6.2.

Note that the condition for all in Theorem 6.1 is a standard assumption in the convergence analysis of derivative-free optimization methods since there is no tool available to determine whether equals zero or not. Similar assumptions can also be found at [12, Section 4] and [19, Corollary 3.3]. Recently, Josz et al. [24] presented a local convergence analysis for exact momentum methods with constant stepsizes, specifically focusing on semi-algebraic functions with gradients being locally Lipschitzian everywhere. It is necessary to emphasize that this analysis does not encompass the obtained convergence properties in Theorem 6.1. Specifically, our work focuses on derivative-free methods with variable stepsizes when applied to -smooth functions satisfying the KL property. These functions have gradients that are locally Lipschitzian but only in the vicinity of local minimizers. Observe also that the local convergence result above does not follow from the one in [4, Theorem 2.10]. The latter relies on global conditions (H1) and (H2), along with the local growth condition (H4), which are not presumed in our derivative-free context and may not be satisfied within the scope of our given assumptions.

The following two consequences of Theorem 6.1 address the local convergence to local minimizers of Algorithm 1 and Algorithm 2.

Corollary 6.3.

Let be a -smooth function with a globally Lipschitz continuous gradient, let , and let . Assume that is a local minimizer of satisfying the KL property at , and that for all . Then there exist such that for any initial point , any initial sampling radius , any and other parameters listed in Algorithm 1, we have that converges to a local minimizer of with . The convergence rates as in Theorem 6.1(ii) are guaranteed if satisfies the KL property at with , , and .

[Proof.] By Theorem 6.1, there are such that for any initial point , initial radius , and sequences and , it holds that any sequence of iterates generated by Algorithm 3 exhibits the convergence properties presented in Theorem 6.1. By choosing a larger if necessary, we can assume that , where is the parameter taken from Algorithm 1.

It suffices to show that Algorithm 1 with initial point , , and the other parameters therein is a special case of Algorithm 3 with the parameters listed above, and thus Algorithm 1 enjoys the desired convergence properties. It is clear from the construction of Algorithm 1 that for all , which implies that whenever . The selection of in Step 1 of Algorithm 3 reduces to that of Algorithm 1 by choosing for all . The iterative procedure of Algorithm 1 can be rewritten as

telling us that . Proposition 4.2 guarantees that are constant for large , which ensures by Step 2 of Algorithm 1 that the stepsizes are equal to a positive constant for large . This guarantees that the sequence is bounded away from , and furthermore . All the assumptions in Theorem 6.1 are satisfied. Thus converges to some local minimizer of with , and in addition the convergence rates as in Theorem 6.1(ii) are guaranteed when satisfies the KL property at with , , and .

Corollary 6.4.

Let be a -smooth function with a locally Lipschitzian gradient, let , and let . Assume that is a local minimizer of , which satisfies the KL property at , and that for all . Then there are constants such that for any initial point , any initial sampling radius , , and the other parameters of Algorithm 2, the sequence of iterates in this algorithm converges to some local minimizer with . The convergence rates as in Theorem 6.1(ii) are guaranteed if the sequence is bounded away from , and if satisfies the KL property at with , , and .

[Proof.] By Theorem 6.1, there exist positive numbers such that for any initial point , any initial radius , and any sequences and , the sequence of iterates of Algorithm 3 exhibits the properties listed in Theorem 6.1(i,ii).

It is sufficient to verify that Algorithm 2 with initial point , , and with other parameters taken from Algorithm 2 is a special case of the general Algorithm 3, and hence it enjoys the claimed convergence properties. We see from the structure of Algorithm 2 that for all , which tells us that for all .

It follows from Step 2 of Algorithm 2 that for all . Combining this with , ensures that . Moreover, the selection of in Step 1 of Algorithm 3 also reduces to that of Algorithm 2 since as . Theorem 6.1(i) tells us that the sequence of iterates generated by Algorithm 2 converges, and thus it is bounded. By using (5.28) as in the proof of Theorem 5.5, we get that the sequence of stepsizes is bounded away from . This guarantees the condition in Theorem 6.1(ii), which verifies therefore that converges to some local minimizer of with the convergence rates as in Theorem 6.1(ii). Thus the proof is complete.

If the condition is removed, the trivial example with for all can be used to show that the iterative sequence generated by Algorithm 3 may remain at the given initial point, which is nonstationary, and thus it does not converge to any local minimizer of Even when for all but , the following example shows that may still converge to a nonstationary point, which confirms an essential role of the assumption in deriving the local optimality of in Theorem 6.1.

Example 2.

Considering the function , it is clear that its derivative is globally Lipschitz continuous, and that satisfies the KL property at the local minimizer with . Therefore, all the assumptions in Theorem 6.1 are satisfied except for . Now we consider Algorithm 3 with being chosen via the central finite difference. Then for any , we have

| (6.12) |

Let us show that for any positive numbers and , there exists an iterative sequence generated by Algorithm 3 with the initial point , with the sequence of stepsizes , and with for all such that converges to a nonstationary point of . To proceed, take any and choose . The sequence is constructed inductively as follows. For any with , we deduce from Step 1 of Algorithm 3 and (6.12) that

Choosing tells us that

Arguing by induction with the usage of ensures that the sequence of positive stepsizes constructed as above provides for all . This implies that does not converge to which is the only stationary point of . We can actually find the exact limit for to see that it is clearly not . Since for all , the iterative procedure shows that is decreasing, and thus it has a limit by taking into account its boundedness from below. Therefore,

which implies by the selection of that , i.e., It can also be observed that the assumption is not satisfied in this example since yields

7 Numerical Experiments

Here we present numerical experiments demonstrating the efficiency of our methods. This section is split into two subsections addressing different classes of problems with the usage of different algorithms.

7.1 Experiments for functions

The first subsection compares the efficiency of our DFC methods with some other well-known derivative-free methods for minimizing functions. The detailed information on the methods considered in these numerical experiments are as follows:

-

(i)

DFC-fordif, i.e., Algorithm 1 with forward finite difference.

-

(ii)

DFC-cendif, i.e., Algorithm 1 with central finite difference.

-

(iii)

FMINSEARCH, i.e., a Matlab implementation of the Nelder–Mead simplex-based method by Lagarias et al. [31].

-

(iv)

IMFIL-fordif, i.e., the implicit filtering algorithm with forward finite difference [16].

-

(v)

IMFIL-cendif, i.e., the implicit filtering algorithm with central finite difference [16].

-

(vi)

RG, i.e., a random gradient-free algorithm for smooth optimization proposed by Nesterov and Spokoiny [39].

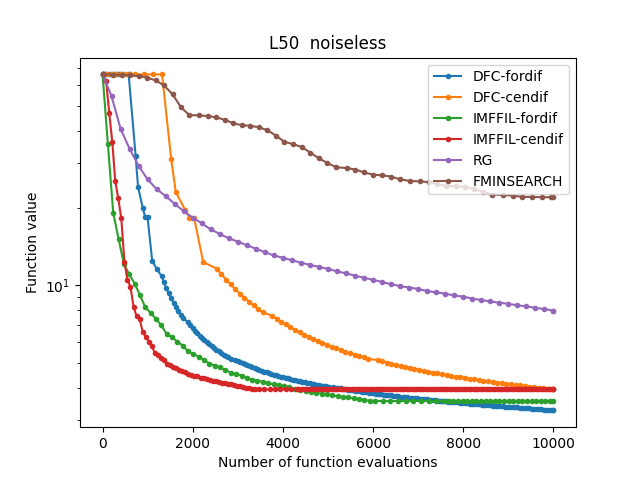

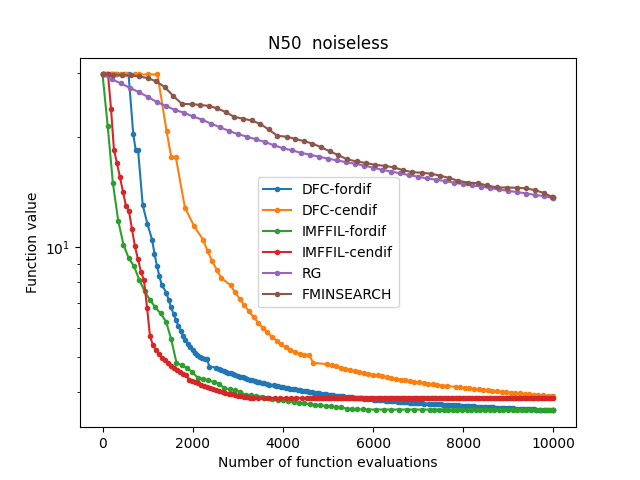

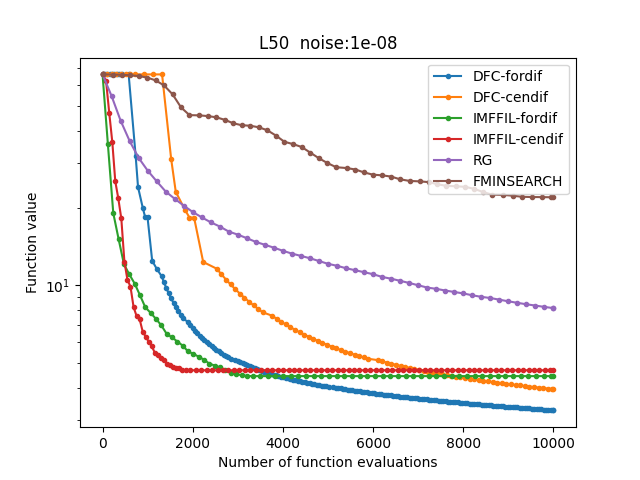

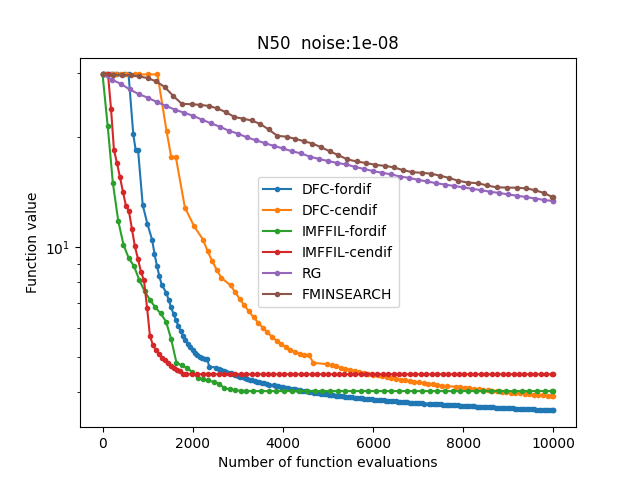

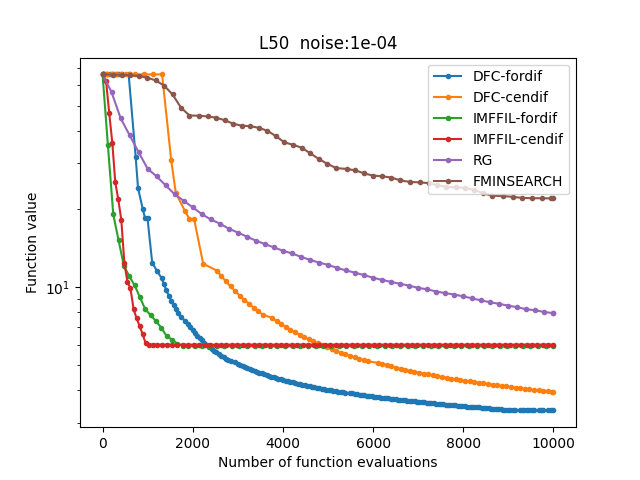

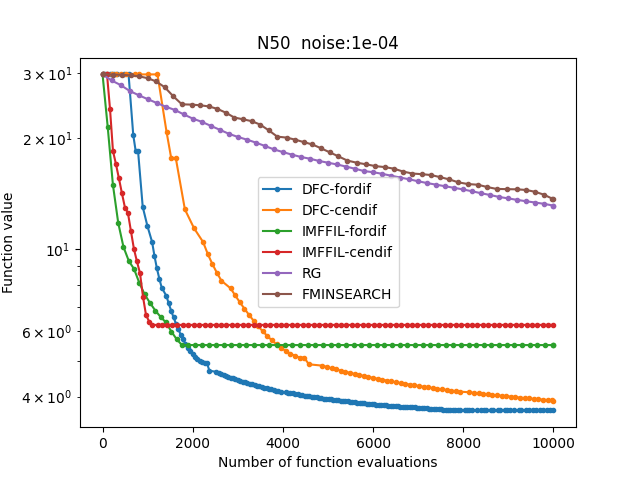

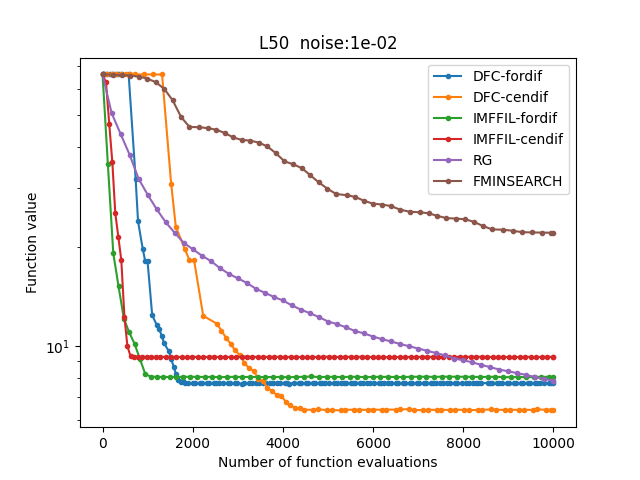

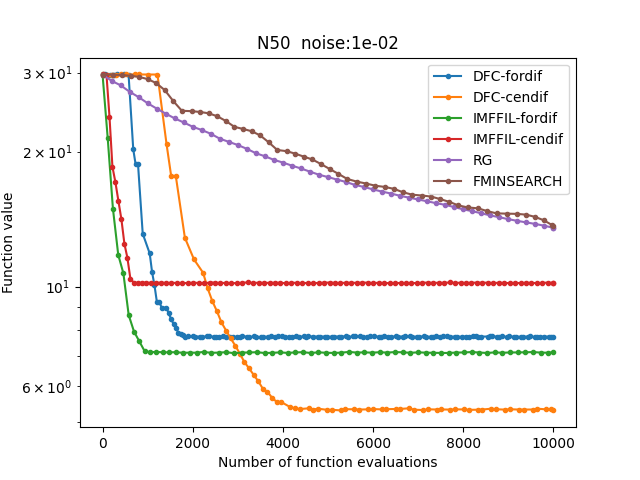

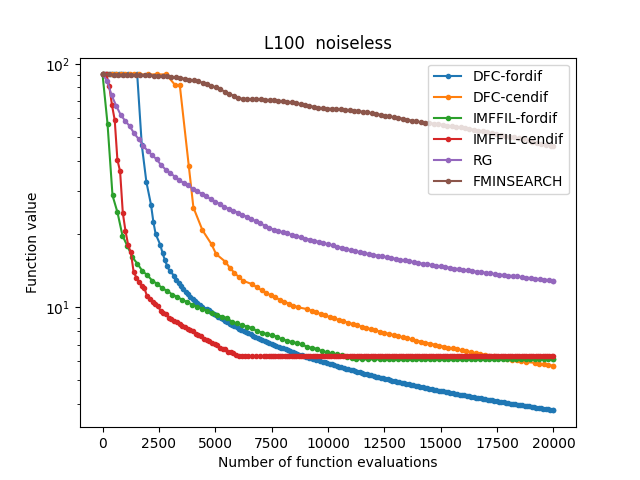

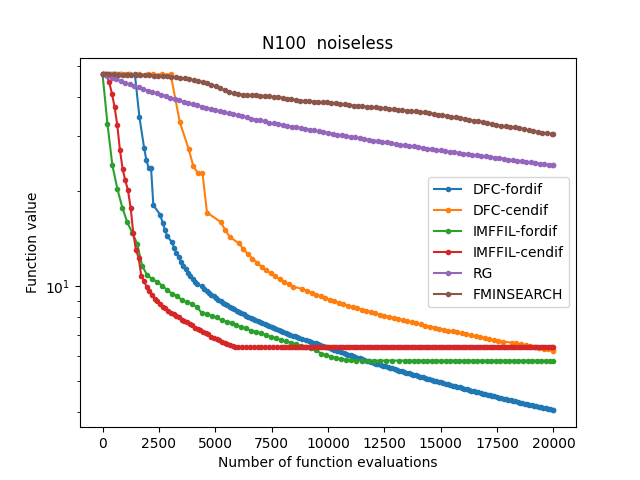

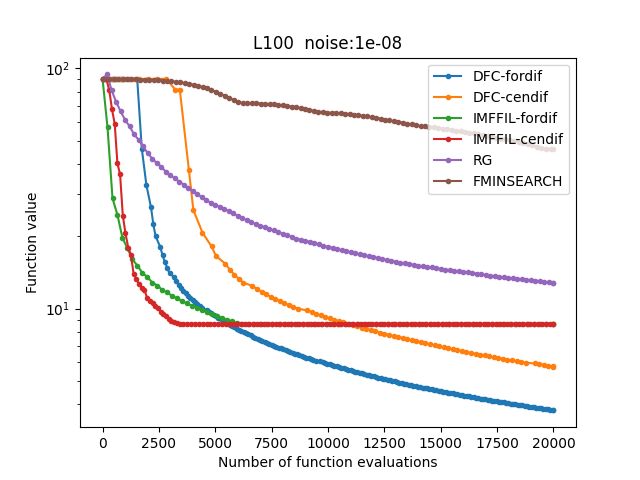

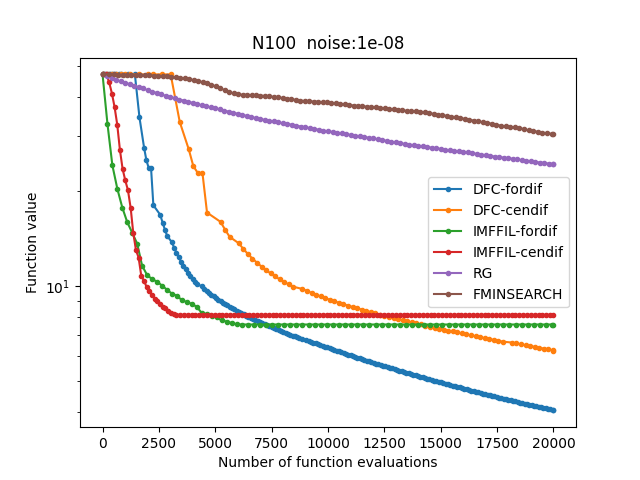

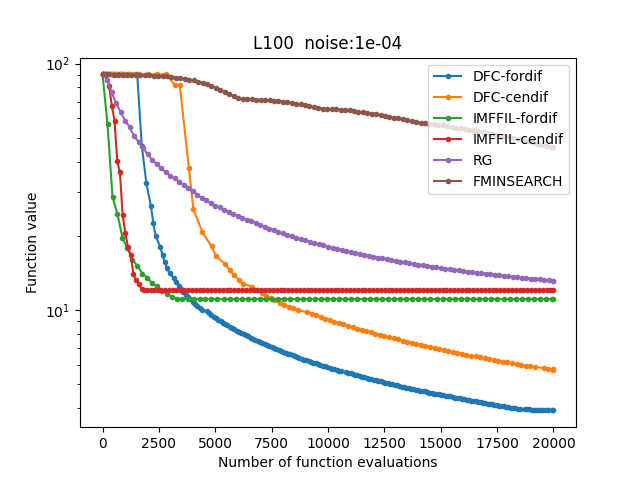

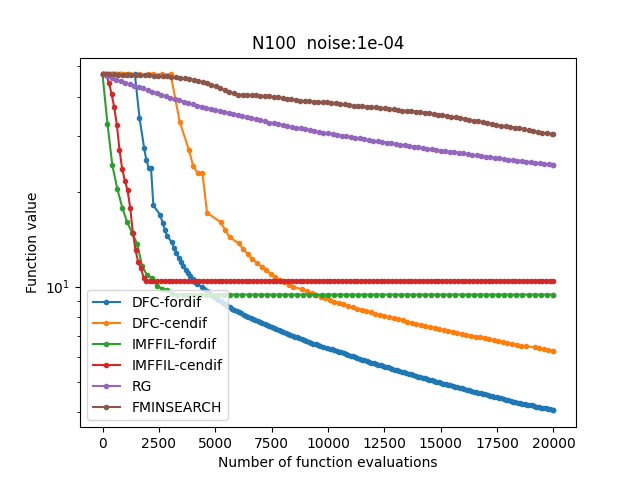

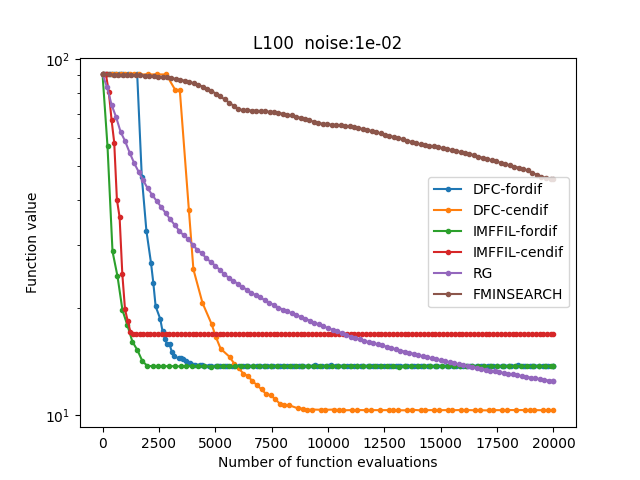

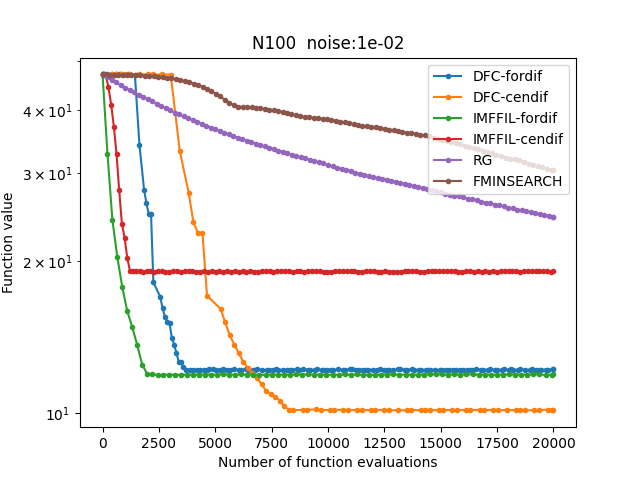

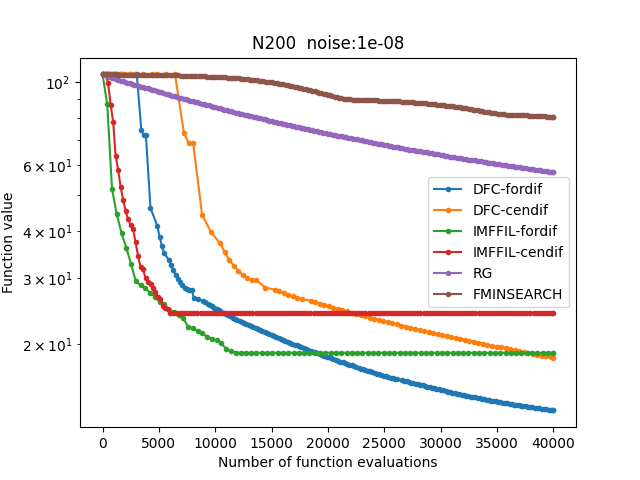

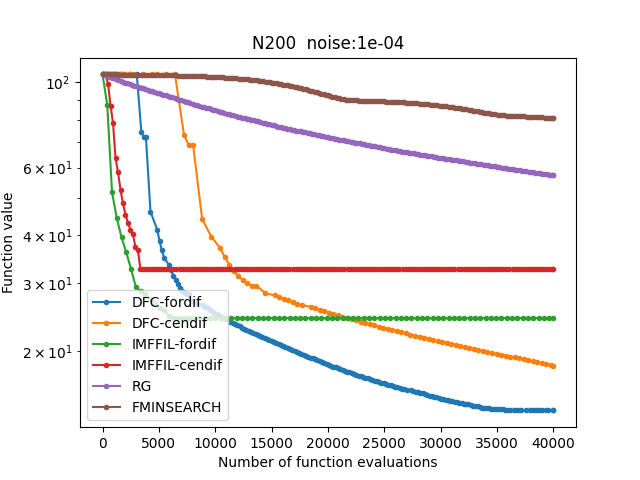

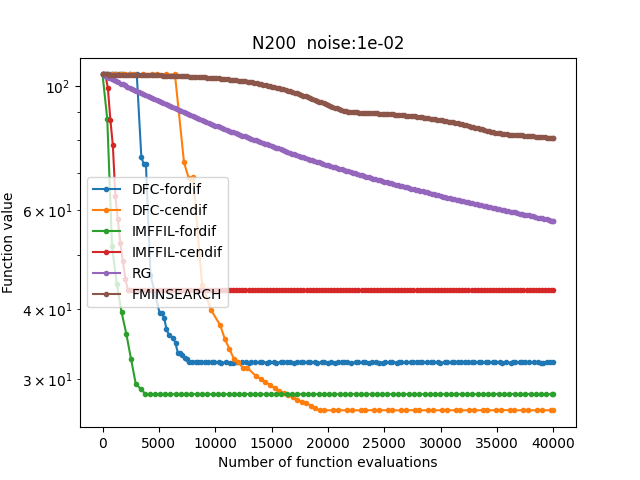

Note that the exact calculation of Lipschitz constants is not necessary for the implementation of FMINSEARCH, IMFIL, and our DFC methods while it is compulsory for RG. The solvers are tested on minimizing a noisy function , where is a uniformly distributed random variable with a given noise level , i.e., , and where the selections for are as the following.

-

1.

Least-square regression

(7.1) where is an matrix and is a vector in This problem is used for benchmarking derivative-free optimization methods in [42]. It can be seen that where is the transpose of matrix . Therefore, is Lipschitz continuous with the constant where , which is the largest singular value of the matrix .

- 2.

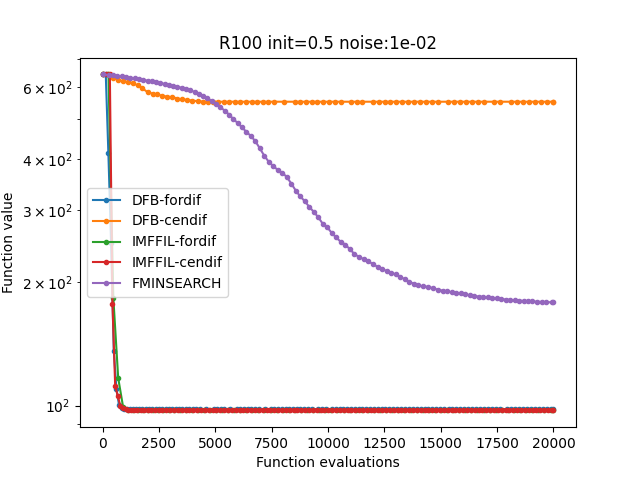

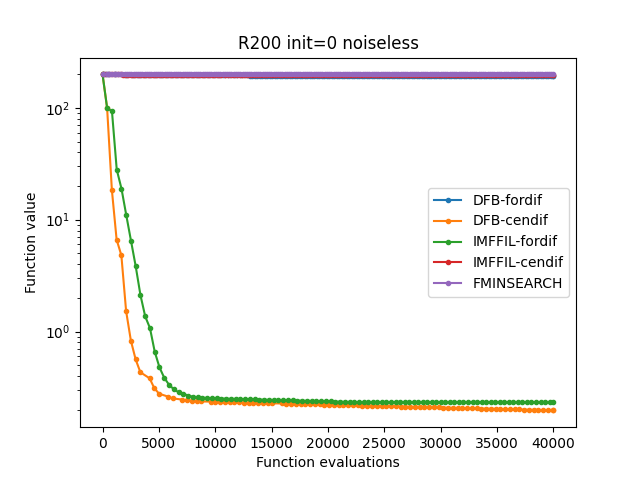

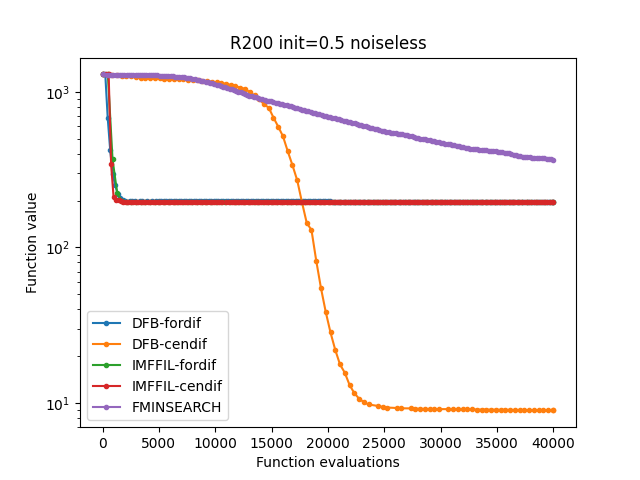

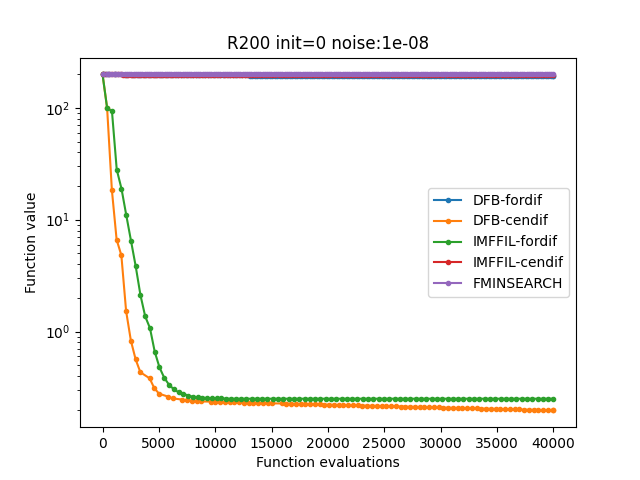

The aforementioned methods are tested on randomly generated datasets with different sizes. To be more specific, an matrix and a vector are generated randomly with i.i.d. (independent and identically distributed) standard Gaussian entries. The behavior of the methods is investigated with different dimensions and different noise levels . The noise level is considered as the noiseless case. In total, the methods are tested in 24 different problems. All the methods are executed until they reach the maximum number of function evaluations of . The results in terms of function values achieved by the methods are presented in the Figures 2–4 below, where “” stands for least square, “” stands for nonconvex image restoration, and the number after “‘” and “” is the dimension of the problem. It can be seen that all 24 out of 24 test problems admit our methods (DFC-fordif or DFC-cendif) as the best among the tested algorithms.

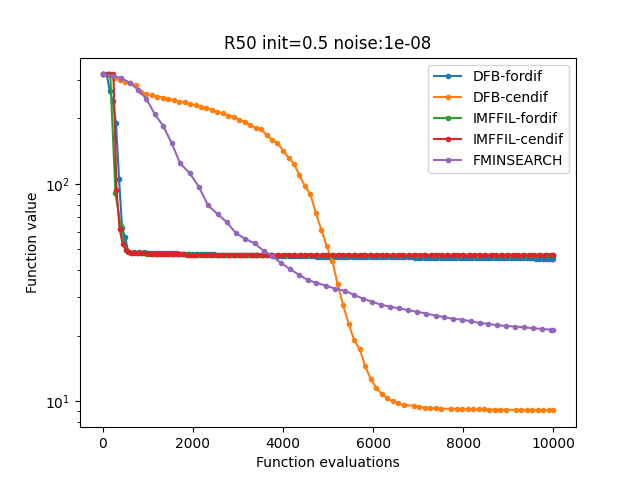

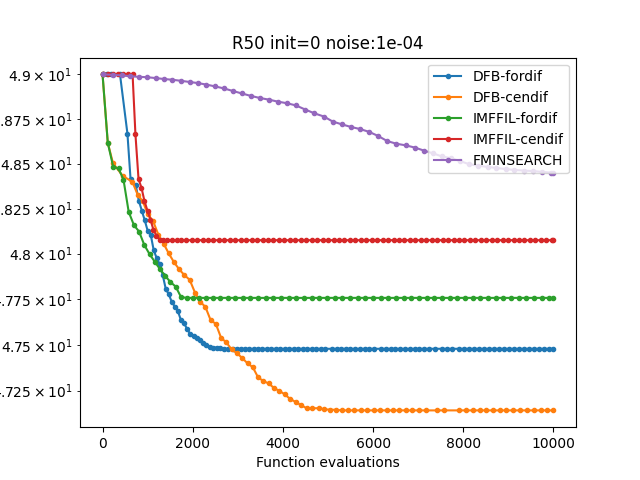

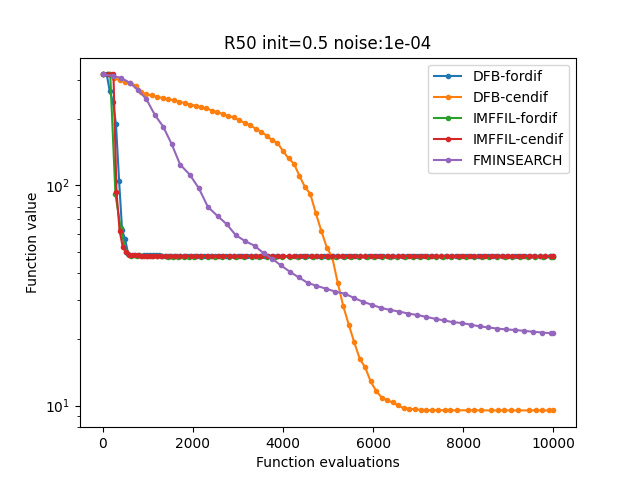

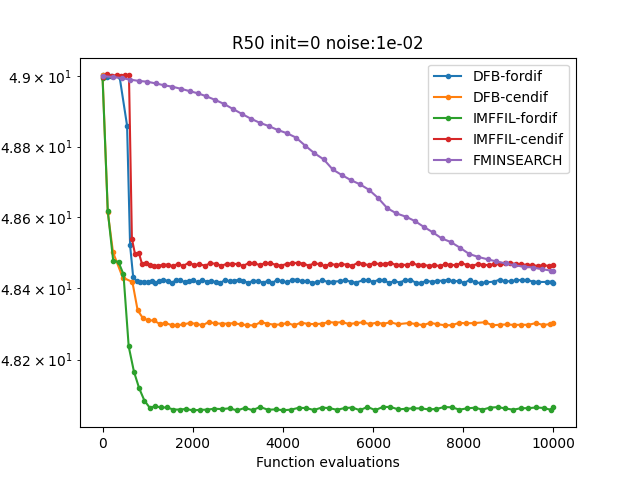

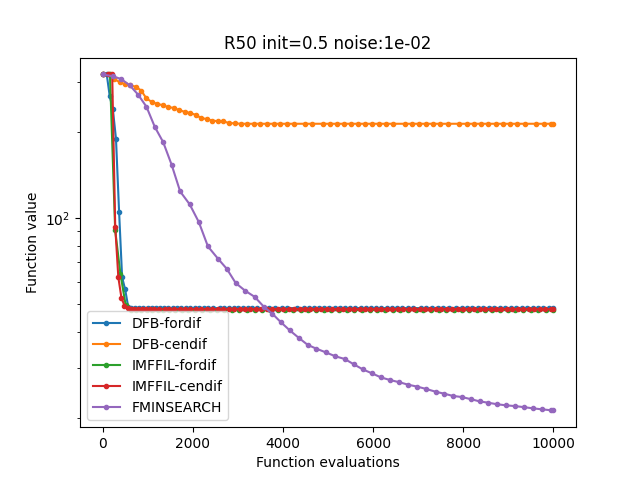

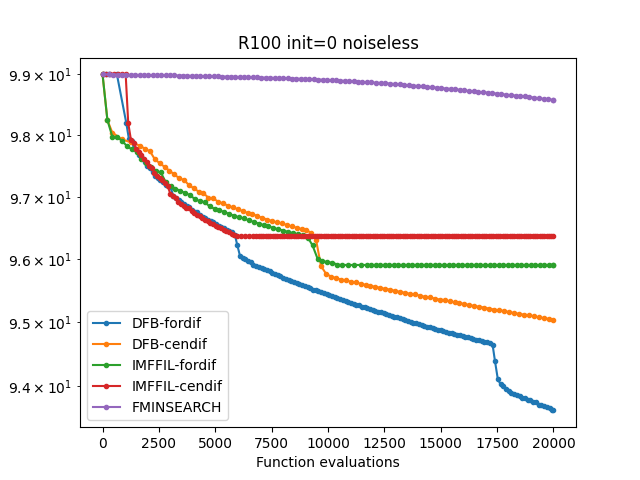

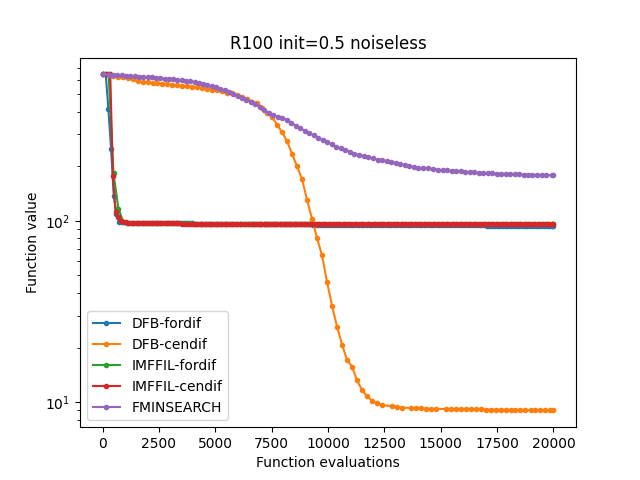

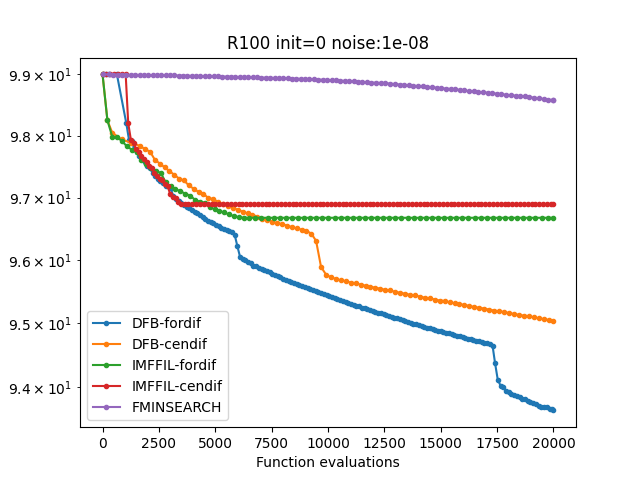

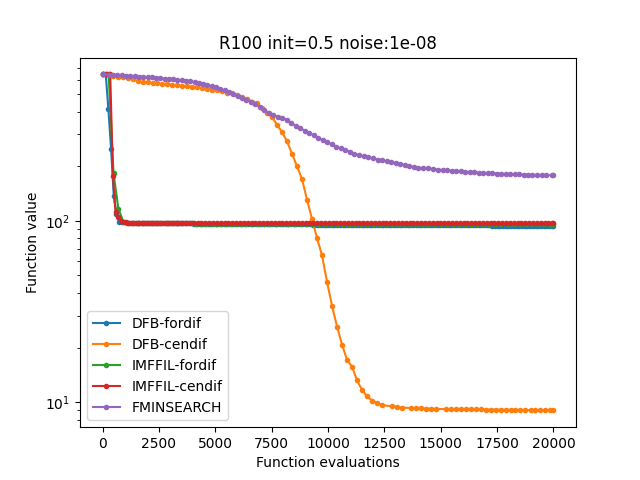

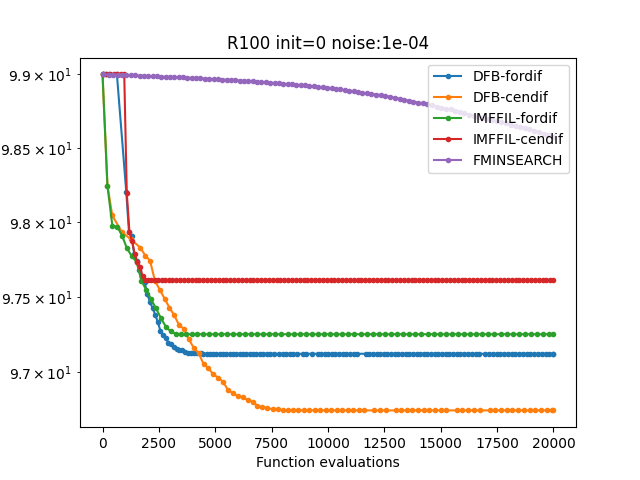

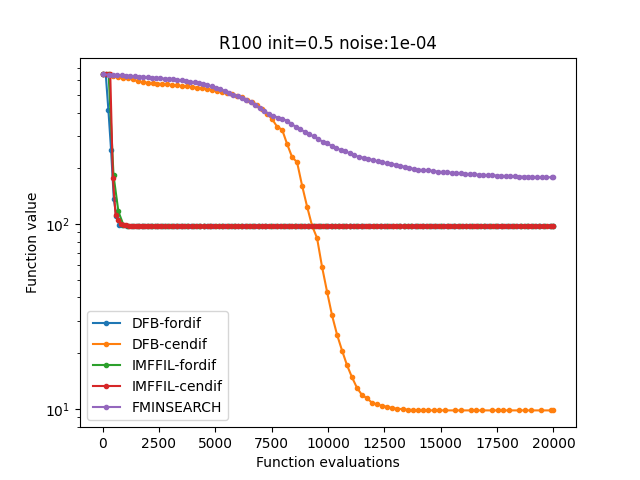

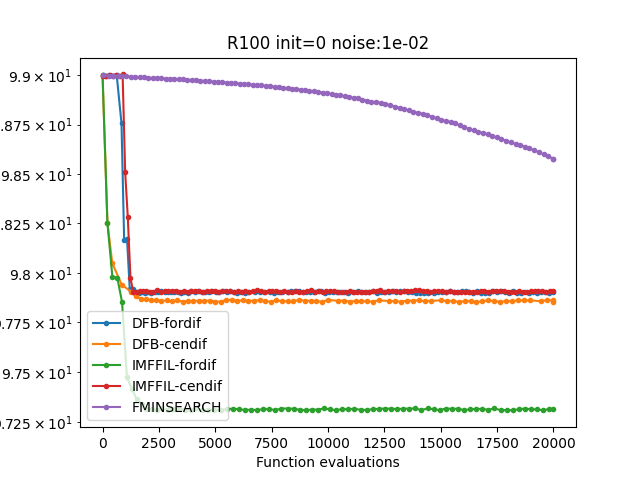

7.2 Experiments for functions

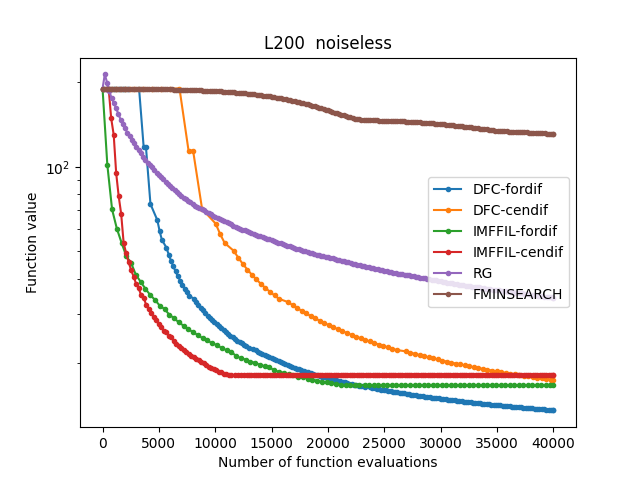

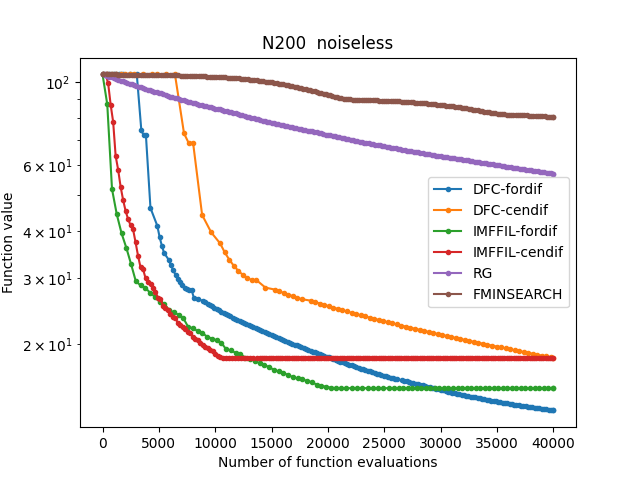

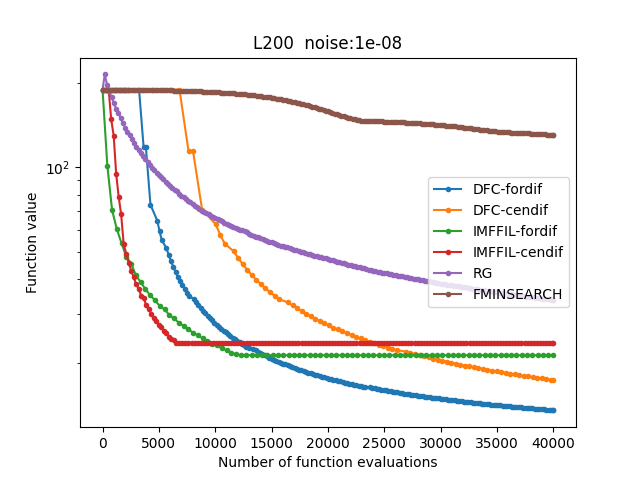

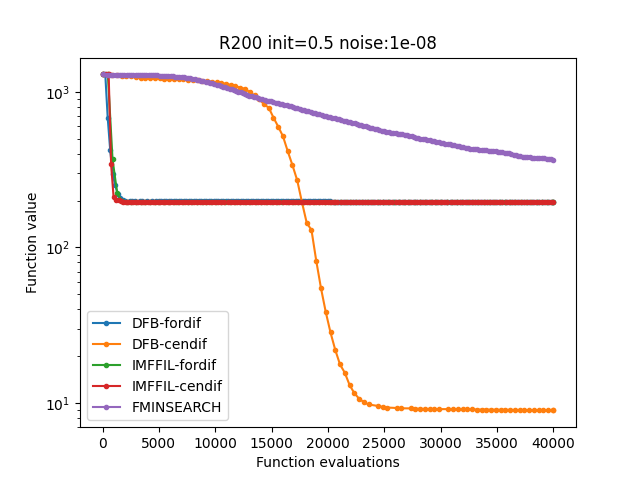

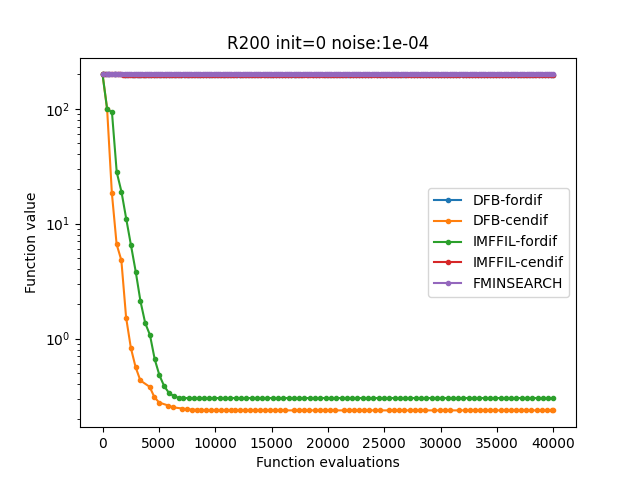

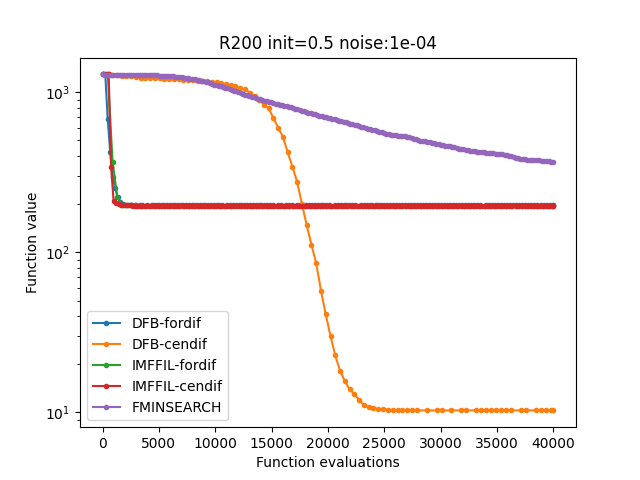

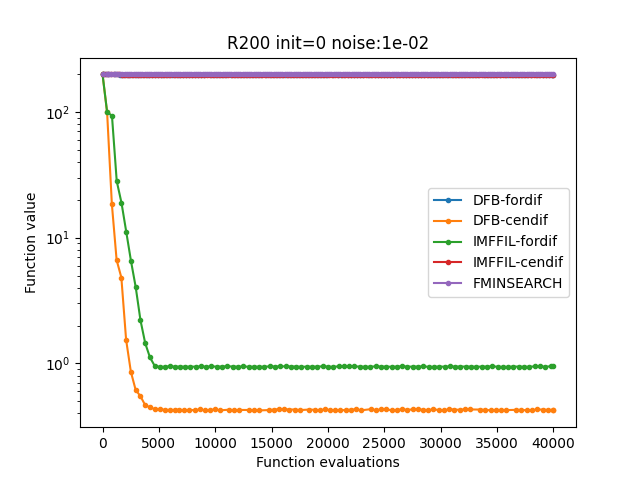

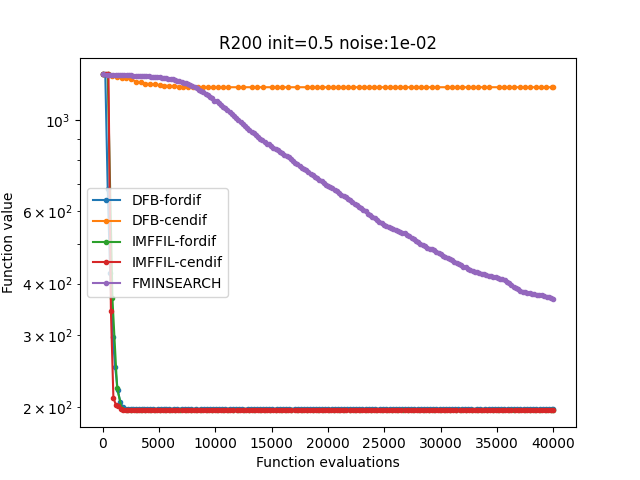

This subsection is devoted to the comparison between the efficiency of our DFB methods, i.e., Algorithm 2 and that of other state-of-the-art derivative-free methods in solving optimization problems. The methods considered in this numerical experiment are:

-

(i)

DFB-fordif, i.e., Algorithm 2 with forward finite difference.

-

(ii)

DFB-cendif, i.e., Algorithm 2 with central finite difference.

-

(iii)

FMINSEARCH, i.e., a Matlab implementation of the Nelder–Mead simplex-based method by Lagarias et al. [31].

-

(iv)

IMFIL-fordif, i.e., the implicit filtering algorithm with forward finite difference [16].

-

(v)

IMFIL-cendif, i.e., the implicit filtering algorithm with central finite difference [16].

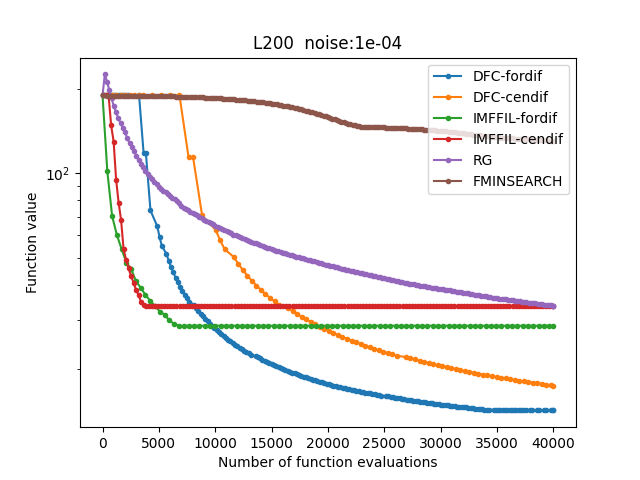

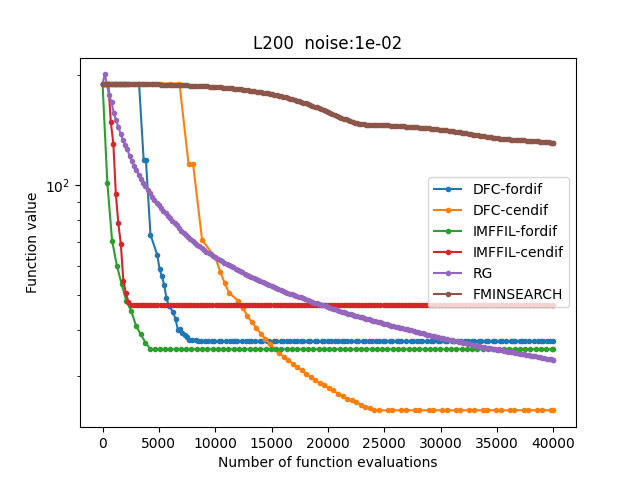

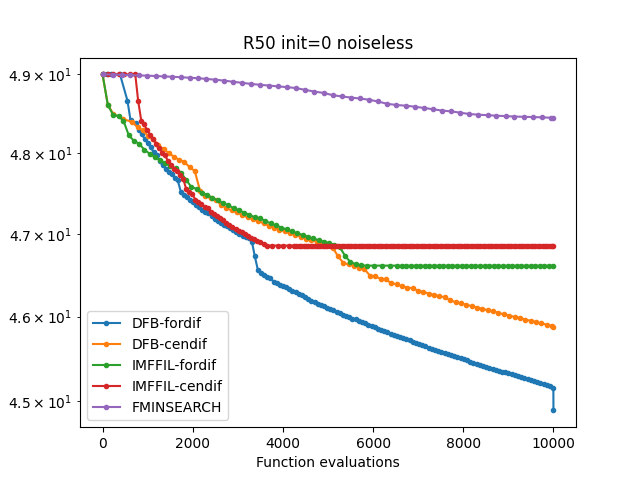

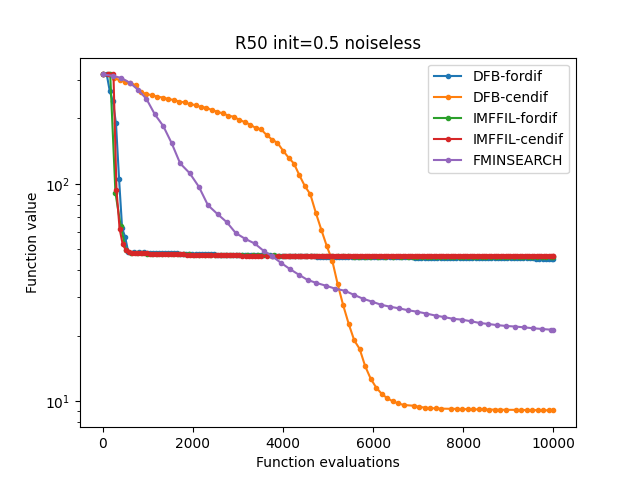

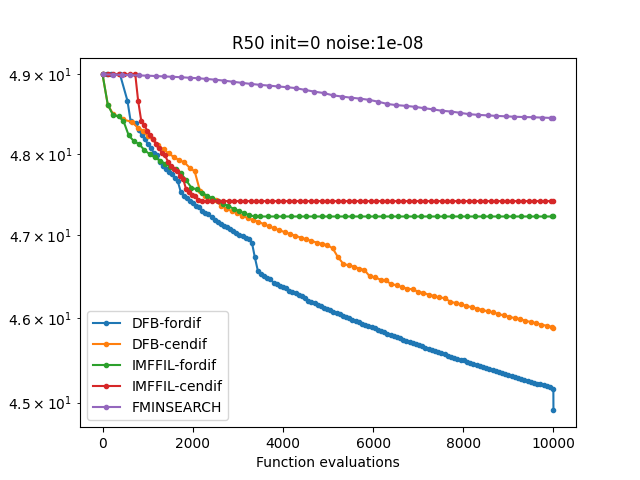

It should be mentioned that the convergence properties of the implicit filtering algorithm in [11, 16, 25] are only valid for functions under some rather strong conditions; see, e.g., [16, Assumption 3.1] and [11, Theorem 2.1, Assumption 2.1], which are not applicable to functions. However, this method is numerically tested here since its algorithm formulation does not require a Lipschitz constant of the gradient. The efficiency of all the aforementioned methods is compared in minimizing the noisy and nonconvex Rosenbrock function [22], i.e., , where

and where is a uniformly distributed random variable with a given noise level , i.e., . We investigate the behavior of the methods for different dimensions , different noise levels . The noise level is considered as the noiseless case. Since the function has different local minimizers, the methods are also tested with two different initial points which are either the zero vector or the vector containing all elements. In total, the methods are tested in 24 problems. All the methods are run until they reach the maximum number of function evaluations of . It can be seen in Figures 5–7 below that 20 problems admit our methods (DFB-fordif or DFB-cendif) as the best among tested algorithms, except for problems with the noise level

8 Concluding Remarks

This paper proposes two general derivative-free optimization methods for minimizing smooth functions. The proposed methods achieve stationary accumulation points, and under the KL property of the objective function, the global convergence with constructive convergence rates. The two newly developed algorithms cover derivative-free methods based on finite differences for and functions, where the finite difference intervals are chosen as large as possible while being automatically adapted with the exact gradients without knowing them. Our methods do not force finite difference intervals to decrease after each iteration, which omits rounding errors as much as possible and thus leads to better numerical performances in solving general convex, nonconvex, noiseless, and noisy derivative-free smooth problems in finite-dimensional spaces. In addition to the aforementioned globally convergent algorithms, we design their local versions, which locally converge to nonisolated local minimizers.

Our future research includes convergence analysis of the newly developed algorithms coupled with quasi-Newton methods for noisy smooth functions. We also intend to establish efficient conditions to ensure local and global convergence to local minimizers of iterative sequences generated by derivative-free methods for problems of nonsmooth constrained optimization.

References

- [1] P.-A. Absil, R. Mahony and B. Andrews, Convergence of the iterates of descent methods for analytic cost functions, SIAM J. Optim. 16 (2005), 531–547.

- [2] A. Addis, A. Cassioli, M. Locatelli and F. Schoen, A global optimization method for the design of space trajectories, Comput. Optim. Appl. 48 (2011), 635–652.

- [3] H. Attouch, J. Bolte, P. Redont and A. Soubeyran, Proximal alternating minimization and projection methods for nonconvex problems. An approach based on the Kurdyka-Łojasiewicz property, Math. Oper. Res. 35 (2010), 438–457.

- [4] H. Attouch, J. Bolte and B. F. Svaiter, Convergence of descent methods for semi-algebraic and tame problems: Proximal algorithms, forward-backward splitting, and regularized Gauss-Seidel methods, Math. Program. 137 (2013), 91–129.

- [5] C. Audet and W. Hare, Derivative-Free and Blackbox Optimization, Springer, Cham, Switzerland, 2017.

- [6] A. S. Berahas, R. H. Byrd and J. Nocedal, Derivative-free optimization of noisy functions via quasi-Newton methods, SIAM J. Optim. 29 (2019), 965–993.

- [7] A. S. Berahas, L. Cao, K. Choromanski and K. Scheinberg, A theoretical and empirical comparison of gradient approximations in derivative-free optimization, Found. Comput. Math. 22 (2022), 507–560.

- [8] A. S. Berahas, L. Cao and K. Scheinberg, Global convergence rate analysis of a generic linesearch algorithm with noise, SIAM J. Optim. 31 (2021), 1489–1518.

- [9] D. P. Bertsekas, Nonlinear Programming, 3rd edition, Athena Scientific, Belmont, MA, 2016.

- [10] J. Bolte and E. Pauwels, Conservative set-valued fields, automatic differentiation, stochastic gradient methods and deep learning, Math. Program. 188 (2021), 19–51.

- [11] T. D. Choi and C. T. Kelley, Superlinear convergence and implicit filtering, SIAM J. Optim. 10 (2000), 1149–1162.

- [12] A. R. Conn, K. Scheinberg and L. N. Vicente, Introduction to Derivative-Free Optimization, SIAM, Philadelphia, PA, 2009.

- [13] A. R. Conn, K. Scheinberg and L. N. Vicente, Global convergence of general derivative-free trust-region algorithms to first- and second-order critical points, SIAM J. Optim. 20 (2009), 387–415.

- [14] F. Facchinei and J.-S. Pang, Finite-Dimensional Variational Inequalities and Complementarity Problems, Vol. II, Springer, New York, 2003.

- [15] P. E. Gill, W. Murray, M. A. Saunders and M. H. Wright, Computing, forward-difference intervals for numerical optimization. SIAM J. Sci. Comput. 4 (1983), 310–321.

- [16] P. Gilmore and C. T. Kelley, An implicit filtering algorithm for optimization of functions with many local minima, SIAM J. Optim. 5 (1995), 269–285.

- [17] G. A. Gray and T. G. Kolda, Algorithm 856: Appspack 4.0: Asynchronous parallel pattern search for derivative-free optimization, ACM Trans. Math. Softw. 32 (2006), 485–507.

- [18] W. Hare and Y. Lucet, Derivative-free optimization via proximal point methods, J. Optim. Theory Appl. 160 (2014), 204–220.

- [19] W. Hare and J. Nutini, A derivative-free approximate gradient sampling algorithm for finite minimax problems, Comput. Optim. Appl. 56 (2013), 1–38.

- [20] R. Hooke and T. A. Jeeves, Direct search solution of numerical and statistical problems, J. ACM. 8 (1961), 212–229.

- [21] A. F. Izmailov and M. V. Solodov, Newton-Type Methods for Optimization and Variational Problems, Springer, New York, 2014.

- [22] M. Jamil, A literature survey of benchmark functions for global optimization problems, Int. J. Math. Model. Numer. Optim. 4 (2013), 150–194.

- [23] C. Josz, Global convergence of the gradient method for functions definable in o-minimal structures, Math. Program. 202 (2023), 355–383.

- [24] C. Josz, L. Lai and X. Li, Convergence of the momentum method for semi-algebraic functions with locally Lipschitz gradients, SIAM J. Optim. 33 (2023), 2988–3011.

- [25] C. T. Kelley, Iterative Methods for Optimization, SIAM, Philadelphia, 1999.

- [26] P. D. Khanh, B. S. Mordukhovich and D. B. Tran, Inexact reduced gradient methods in smooth nonconvex optimization, J. Optim. Theory Appl., DOI: 10.1007/s10957-023-02319-9 (2023).

- [27] P. D. Khanh, B. S. Mordukhovich and D. B. Tran, A new inexact gradient descent method with applications to nonsmooth convex optimization, arXiv:2303.08785 (2023).

- [28] P. D. Khanh, B. S. Mordukhovich, V. T. Phat and D. B. Tran, Inexact proximal methods for weakly convex functions, arXiv:2307.15596 (2023).

- [29] J. D. Lee, I. Panageas, G. Piliouras, M. Simchowitz, M. I. Jordan and B. Recht, First-order methods almost always avoid strict saddle points, Math. Program. 176 (2019), 311–337.

- [30] K. Kurdyka, On gradients of functions definable in o-minimal structures, Ann. Inst. Fourier 48 (1998), 769–783.

- [31] J. C. Lagarias, J. A. Reeds, M. H. Wright and P. E. Wright, Convergence properties of the Nelder–Mead simplex method in low dimensions, SIAM J. Optim. 9 (1998), 112–147.

- [32] S. Łojasiewicz, Ensembles Semi-Analytiques, Institut des Hautes Etudes Scientifiques, Bures-sur-Yvette, France, 1965.

- [33] D. Malik, A. Pananjady, K. Bhatia, K. Khamaru, P. Bartlett and M. Wainwright, Derivative-free methods for policy optimization: Guarantees for linear quadratic systems, J. Mach. Learn. Res. 21 (2020), 1–51.

- [34] A. L. Marsden, M. Wang, J. E. Jr. Dennis and P. Moin, Trailing-edge noise reduction using derivative-free optimization and large-eddy simulation, J. Fluid Mech. 572 (2007), 13–36.

- [35] R. Mifflin, A superlinearly convergent algorithm for minimization without evaluating derivatives, Math. Program. 9 (1975), 100–117.

- [36] J. J. Moré and S. M. Wild, Estimating derivatives of noisy simulations, ACM Trans. Math. Softw. 38 (2012), 1–21.

- [37] J. A. Nelder and R. Mead, A simplex method for function minimization, Comput. J. 7 (1965), 308–313.

- [38] Y. Nesterov, Lectures on Convex Optimization, 2nd edition, Springer, Cham, Switzerland, 2018.

- [39] Y. Nesterov and V. Spokoiny, Random gradient-free minimization of convex functions, Found. Comput. Math. 17 (2017), 527–566.

- [40] J. Nocedal and S. J. Wright, Numerical Optimization, 2nd edition. New York, 2006.

- [41] A. Ostrowski, Solution of Equations and Systems of Equations, 2nd edition, Academic Press, New York, 1966.

- [42] L. M. Rios and N. V. Sahinidis, Derivative-free optimization: a review of algorithms and comparison of software implementations, J. Glob. Optim. 56 (2013), 1247–1293.

- [43] A. Themelis, L. Stella and P. Patrinos, Forward–backward quasi-Newton methods for nonsmooth optimization problems. Comput. Optim. Appl. 67 (2017), 443–487.

- [44] P. Tseng, Fortified-descent simplicial search method: A general approach, SIAM J. Optim. 10 (1999), 269–288.

- [45] K. Scheinberg, Finite difference gradient approximation: To randomize or not?, INFORMS J. Comput. 34 (2022), 2384–2388.

- [46] H. M. Shi, Y. Xie, M. Q. Xuan and J. Nocedal, Adaptive finite-difference interval estimation for noisy derivative-free optimization, SIAM J. Sci. Comput. 44 (2022), 2302–2321.

- [47] H. M. Shi, M. Q. Xuan, F. Oztoprak and J. Nocedal, On the numerical performance of finite-difference-based methods for derivative-free optimization, Optim. Methods Softw. 38 (2023), 289–311.