Enhancing Asset Allocation in the Fixed Income Universe: A Synthetic Dataset Approach for Robust Portfolio Construction

Generating Realistic Synthetic Datasets for Improved Asset Allocation in the Fixed Income Universe

Improved Data Generation for Enhanced Asset Allocation: A Synthetic Dataset Approach for the Fixed Income Universe

Abstract.

We present a novel process for generating synthetic datasets tailored to assess asset allocation methods and construct portfolios within the fixed income universe. Our approach begins by enhancing the CorrGAN model (Marti, 2020) to generate synthetic correlation matrices. Subsequently, we propose an Encoder-Decoder model that samples additional data conditioned on a given correlation matrix. The resulting synthetic dataset facilitates in-depth analyses of asset allocation methods across diverse asset universes. Additionally, we provide a case study that exemplifies the use of the synthetic dataset to improve portfolios constructed within a simulation-based asset allocation process.

1. Introduction

When applying asset allocation methods in practice, a crucial challenge arises due to limited and biased empirical datasets. Conventional approaches to constructing portfolios solely on historical data often suffer from overfitting and neglect the potential market scenarios that could have occurred but did not (Lopez de Prado, 2019). To address this problem and enhance the performance of asset allocation methods during out-of-sample periods, the utilization of synthetic financial datasets has emerged as a promising solution.

Recent literature provides examples where synthetic correlation matrices were used to assess asset allocation methods in simulation-based frameworks (Lopez de Prado, 2016a; Papenbrock et al., 2021; Marti et al., 2021). However, limitations arise when applying these methods in more complex scenarios, especially when dealing with financial assets that exhibit diverse characteristics or when practitioners have objective functions and constraints that are more intricate than those of simple minimum variance portfolios. In our paper, we analyze the fixed income universe, comprising assets with varying volatility levels, where a frequent optimization goal is maximizing yield within specified risk constraints. To perform a comprehensive simulation-based assessment of asset allocation methods within this universe, it is necessary to not only have realistic correlation matrices but also other attributes, particularly volatilities and yield data that is coherent with the matrices. This necessitates the use of more advanced models for data sampling.

We propose a two-step process for generating a synthetic dataset tailored specifically to assess and fine-tune asset allocation within the fixed income universe. First, we employ a generative adversarial network to sample realistic correlation matrices, capturing the interdependencies among assets. Then, we generate additional characteristics of the assets conditional on the matrices, including volatilities, expected returns, and forward returns data, using a proprietary Encoder-Decoder model. We hypothesize that the synthetic dataset, with its reduced reliance on historical data, can address the limitations of empirical datasets and improve the performance of asset allocation methods during out-of-sample periods. Our analysis indicates that the generative models provide a more diverse dataset that extrapolates distributions into plausible areas and mitigates outliers, decreasing dependency on historical events with low future probability.

We also present a case study to showcase the practical application and potential benefits of the synthetic dataset. Our findings indicate that the synthetic dataset enables investors to construct more robust portfolios.

In summary, our research contributes to addressing the challenges posed by limited and biased empirical datasets in fixed income asset allocation. By introducing a novel process for generating a tailored synthetic dataset and demonstrating its benefits through a case study, we provide valuable insights for practitioners and researchers in the field.

2. Related Work

Asset allocation methods aim to distribute funds across different investments to optimize return and manage risk. Lopez de Prado introduced two asset allocation methods, Hierarchical Risk Parity (Lopez de Prado, 2016a) and Nested Clustered Optimization (Lopez de Prado, 2016b), and to indicate their superior performance over more traditional frameworks used a Monte Carlo approach based on synthetic correlation and associated covariance matrices. The matrices were formed using multivariate normal distributions with additional random shocks in the former paper and imposed correlated blocks in the latter article. While the performed tests provided convincing arguments supporting the introduced techniques, the synthetic data was drawn from relatively simple processes and may not be suited for more advanced simulations and tests.

A more sophisticated method of sampling synthetic correlation matrices was proposed by Papenbrock et al. (Papenbrock et al., 2021) who employed a multi-objective evolutionary algorithm. The generated dataset was used to compare the performance of asset allocation methods in a simulation-based framework. The authors also applied SHAP framework (Lundberg and Lee, 2017) to find which characteristics of correlation matrices could provide intuitive explanations of what asset allocation method to use. The approach provided realistic synthetic correlation matrices that exhibited many characteristics of empirically observed ones but the algorithm was designed to optimize for the characteristics, and as a result, it might have omitted features that were not specifically included in the objective functions.

Generative Adversarial Networks (GANs) (Goodfellow et al., 2020) have gained popularity in the financial domain for generating synthetic datasets. GANs consist of a generator and a discriminator network, where the generator generates new data samples resembling the training data, and the discriminator distinguishes between real and fake samples. GANs have been applied in various finance-related studies, such as generating time-series data for trading strategy calibration (Koshiyama et al., 2021), addressing imbalanced classes in actuarial datasets (Ngwenduna and Mbuvha, 2021), and hedging (Kim, 2021).

Marti (Marti, 2020) introduced a GAN model based on the DCGAN architecture (Radford et al., 2015) to generate synthetic correlation matrices. (Marti et al., 2021) extended the model to condition sampled data on market regimes and conducted experiments to assess distributions of outcomes for selected asset allocation strategies. The framework learns a number of characteristics of the empirical correlation matrices in an unsupervised manner and provides high-quality data samples. The generated matrices are visually undiscernible to empirical matrices which was supported by results of an online poll in which users could guess whether depicted correlation matrices are real or fake.

(Mariani et al., 2019) and (Lu and Yi, 2022) proposed alternative approaches to generating synthetic data for portfolio construction based on GAN models that learn a joint probability distribution of assets’ future price trends based on historical time series. The authors indicate that portfolios constructed using simulations derived from the GANs outperform traditional asset allocation methods. While the approach of optimizing portfolios across time-series simulations is promising and may potentially provide a more comprehensive environment to assess asset allocation methods than using correlation matrices, the papers provided examples with a low number of assets. Also, given that the testing of correlations across the simulations is limited, it is not clear whether the independency structure of the synthetic data exhibits all of the characteristics found in empirical datasets and listed in (Marti et al., 2021).

Synthetic data from generative models can also be valuable in assessing portfolio risk, simulating extreme events, and testing the robustness of models to different scenarios. Flaig and Junike (Flaig and Junike, 2022) employed GAN architecture to create an economic scenario generator for calculating market risk in insurance companies. In a separate publication (Flaig and Junike, 2023), the authors presented methods for further validating their model, assessing the alignment of dependencies between risk factors, and measuring model overfitting to empirical data. (Cont et al., 2022) introduced the Tail-GAN model, focusing on generating tail risk scenarios for user-specified trading strategies. The model utilized a bespoke loss function to accurately capture the tail risk of benchmark portfolios based on common risk measures such as Value-at-Risk and Expected Shortfall.

In the later sections of our paper, we present a case study that utilizes the concept of tracking error volatility (TEV) which measures the standard deviation of a portfolio’s returns relative to its benchmark (Roll, 1992). Given the diverse characteristics of fixed income assets, investors can construct portfolios that are significantly different from their benchmarks. TEV serves as a simple measure of relative risk, particularly relevant to portfolio managers who have a mandate to outperform a benchmark within strict risk limits.

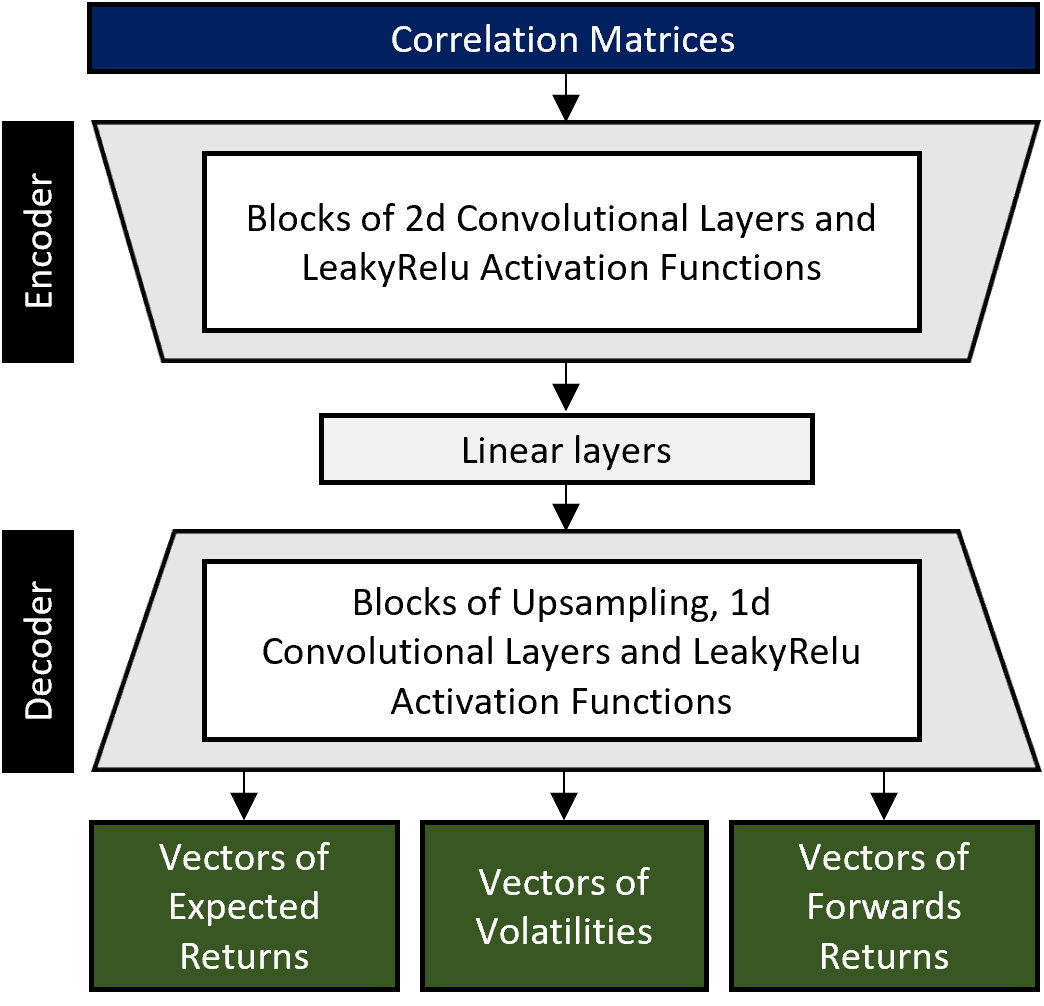

3. Generating synthetic data

We propose a process to generate synthetic data that consists of two parts:

-

(1)

A generative adversarial network (GAN) model that samples synthetic correlation matrices.

-

(2)

An Encoder-Decoder model that provides additional data vectors (asset volatilities, expected returns, and forward realized returns) conditionally on a given correlation matrix.

The GAN model in 1) is supposed to provide information on market structure and current market conditions. The Encoder-Decoder network in 2) uses correlation matrices as input data and generates any additional information that may be required.

| mean correl | eigen gini |

|

|

|

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std | Mean | Std | Mean | Std | Mean | Std | Mean | Std | Mean | Std | |||||||||

| Empirical | ||||||||||||||||||||

| Training Period | 0.231 | 0.063 | 0.855 | 0.011 | 0.716 | 0.118 | 0.751 | 0.071 | 2.335 | 0.389 | 1.952 | 0.093 | ||||||||

| Testing Period | 0.284 | 0.079 | 0.862 | 0.019 | 0.717 | 0.102 | 0.697 | 0.079 | 2.227 | 0.396 | 1.965 | 0.112 | ||||||||

| Generated | ||||||||||||||||||||

| DCGAN | 0.222 | 0.038 | 1.044 | 0.031 | 0.670 | 0.098 | 0.728 | 0.077 | 3.306 | 0.288 | 2.154 | 0.068 | ||||||||

| WGAN | 0.230 | 0.070 | 0.976 | 0.064 | 0.697 | 0.115 | 0.742 | 0.073 | 3.225 | 0.303 | 2.032 | 0.081 | ||||||||

Our analysis is based on a time-series dataset spanning from April 2007 to October 2022. This dataset includes 68 financial assets, representing 28 currencies and 40 investable fixed income indices. The fixed income indices cover various types of treasury, corporate, government-related, and securitized bonds in developed countries across North America, Europe, Asia, as well as emerging market countries. The selection of the financial instruments aims to reflect a broad spectrum of building blocks, suitable for constructing a well-diversified global fixed income investment product. Although all selected fixed income indices are FX-hedged to USD, our case study allows to open FX positions by taking long or short positions directly on the currencies. For each asset, we collected two main time-series from Bloomberg terminal – a total return index and a series of expected returns based on assets’ yields, adjusted to account for the yield that an investor could have obtained by hedging FX risk to USD with forward contracts. The generative models were trained on a transformed form of the dataset that consists of the following four components for each day in the analyzed period: correlation matrix based on 52 weekly returns, vector of volatilities based on 52 weekly returns, vector of 1-year expected returns and vector of 1-month forward realized returns.

The dataset is divided into a training period from April 2007 to March 2017 and a testing period from May 2017 to October 2022. The testing period covered a significant drawdown that the fixed income universe experienced in 2022 when both, interest rates increased and credit spreads widened. The rare combination of positively correlated interest rates and spreads accompanied by high volatility provides an interesting testing environment for any asset allocation strategy seeking to minimize risk.

3.1. Generative Adversarial Network

The GAN model developed for the analysis takes a random vector and outputs a correlation matrix that exhibits characteristics found in empirically observed correlation matrices. The architecture of the model follows the methodology described in (Marti, 2020) but introduces several enhancements:

-

•

The model is converted to a Wasserstein GAN model following an approach described in (Gulrajani et al., 2017). Without the change, the network in some configurations of hyperparameters failed to converge or exhibited mode collapse (Goodfellow, 2016). The most common reason for the issues was that the discriminator was learning too quickly which did not allow the generator to improve. The change has also improved the characteristics of generated correlation matrices across the tests that were conducted.

-

•

In many hyperparameter configurations, the generated correlation matrices exhibited a “checkerboard artifact” described in (Odena et al., 2016) and (Aitken et al., 2017). The issue may occur when there is an overlap between filters of transposed convolutional layers and consequently, some pixels (or correlation coefficients in this case) receive less focus in the learning process. To address this issue, in the generator network, we reduced the use of transposed convolutional layers and instead favored convolutional and upsampling layers with nearest-neighbor interpolation.

-

•

The empirical correlation matrices used for training were not sorted using a hierarchical clustering algorithm; instead, they maintained a consistent asset order. While (Marti, 2020) suggested sorting the matrices to emphasize the hierarchical structure of financial markets, in our experiments we noticed that the GAN model can learn characteristics of the empirical dataset without reordering the empirical dataset.

We evaluate the GAN model by comparing the characteristics of the generated correlation matrices with empirical ones. Two variants of the GAN model are assessed: ”DCGAN,” the original model based on (Marti, 2020), and ”WGAN,” the enhanced model proposed in this section. We sampled 64,000 correlation matrices for both models and used metrics suggested in (Papenbrock et al., 2021) for assessment:

-

•

mean correl – average correlation coefficient across matrices

-

•

eigen gini – Gini coefficient of matrices’ eigenvalues

-

•

coph corr – cophenetic correlation between the original correlation distance matrix and the cophenetic matrix of the hierarchical clustering algorithm (using single or ward linkage). This is a proxy that measures how hierarchical correlation matrices are. The correlation distance is measured as

-

•

perron frob sum neg – measures the sum of negative entries of the first eigenvector.

-

•

power eigen values – power exponent of correlation matrices’ eigenvalue distribution

As shown in Table 1, most WGAN metrics closely resemble those of empirical matrices. Notable distinctions emerge mainly in the ”perron frob sum neg” values, which signify a higher prevalence of negative elements within the eigenvector corresponding to the largest eigenvalue. Additionally, Gini coefficients and power exponents of eigenvalues exhibit higher averages compared to the empirical dataset. All WGAN variant’s mean metrics are closer to those of the empirical training dataset compared to the DCGAN model. While some of the differences between models are not large, it is worth noting that training the DCGAN model necessitated hyperparameter calibration and multiple training trials to achieve successful convergence and avoid the mode collapse issue.

The higher performance of the WGAN model can be also illustrated by comparing the diagonals of the matrices - the average diagonal element of WGAN’s matrices is 0.9992 whereas for DCGAN the average is 0.9719. While the original CorrGAN model (Marti, 2020) was trained on a different dataset, the author noted an average diagonal element of 0.998.

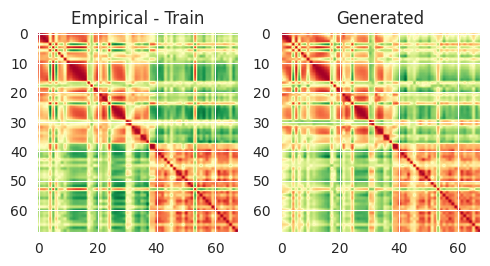

Similarly to (Marti, 2020), our generated correlation matrices are difficult to be visually discerned from empirical correlation matrices as illustrated in Figure 1.

3.2. Encoder-Decoder network for additional asset characteristics

The Encoder-Decoder model generates additional asset attributes from a correlation matrix, including volatilities, expected returns, and 1-month forward returns. The additional attributes should reflect the market conditions that a correlation matrix corresponds to.

The encoder takes a correlation matrix as input and deconstructs it using a block of 2D convolutional layers with LeakyReLU activation functions and dropout layers. The output is then compressed using linear layers. The decoder consists of three parallel blocks, each comprising linear, 1D convolutional, and upsampling layers with LeakyReLU activation functions. The model outputs three vectors representing volatilities, expected returns, and 1-month forward returns of the underlying assets. Notably, the values in these generated vectors maintain the same order of assets as the input correlation matrix.

| Mean | Std Dev | Skew | Kurtosis | |

|---|---|---|---|---|

| Volatilities | ||||

| Empirical Train | 7.098% | 5.475% | 1.447 | 2.807 |

| Generated | 7.391% | 5.482% | 1.246 | 2.048 |

| Empirical Test | 6.309% | 5.278% | 2.873 | 19.890 |

| 1-Year Expected Returns | ||||

| Empirical Train | 3.053% | 3.297% | 4.613 | 96.076 |

| Generated | 2.937% | 3.000% | 3.073 | 35.917 |

| Empirical Test | 2.397% | 3.828% | 6.857 | 107.077 |

| 4-Week Forward Returns | ||||

| Empirical Train | 0.251% | 2.537% | -0.758 | 10.601 |

| Generated | 0.223% | 2.372% | 0.053 | 6.026 |

| Empirical Test | -0.029% | 2.497% | 0.693 | 59.745 |

During training, the model employs a loss function that consists of three Mean Squared Error (MSE) components to compare the generated three vectors with the original empirical dataset. Training is conducted using only empirical correlation matrices and the final model is evaluated by comparing distributions of the synthetic and empirical additional vectors.

The model acts as a deterministic ”translator” that converts a correlation matrix into additional data vectors, without introducing additional randomness. The diversity in the output stems from the variety of generated correlation matrices.

For the further parts of the analysis, we created a “synthetic” dataset by sampling 64,000 correlation matrices from the GAN model and corresponding vectors of volatilities, expected returns and forward returns from the Encoder-Decoder model.

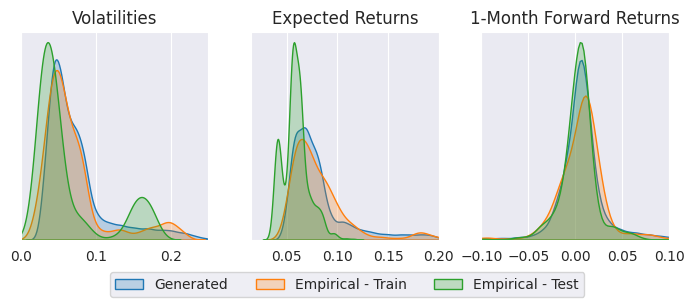

Table 2 compares the main statistics of the vectors in the synthetic and empirical datasets. The Encoder-Decoder model effectively captures the distributions of the additional data vectors, with means similar to the empirical vectors used in training. The other three moments are moderately less pronounced which is caused by the model mitigating outliers that are present in the empirical dataset. The kurtosis of forward returns is lower in the generated dataset, but still reflects fat tails in the underlying assets’ returns. The generated vectors are relatively different from the empirical dataset in the testing period. However, considering that the Encoder-Decoder model did not directly target these metrics in the training process, such discrepancies were expected.

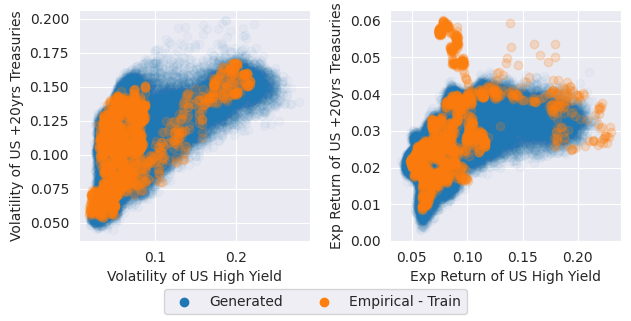

In Figure 3, we compare the distributions of the empirical and synthetic vectors for a selected asset, US High Yield, which is one of the most volatile fixed income indexes in the dataset. Some discrepancies are observed between the two datasets - notably, the Encoder-Decoder model smooths out rough sections in the empirical dataset’s distributions, leading to more monotonic shapes.

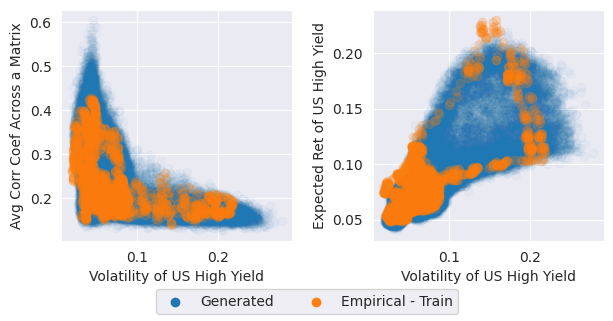

Figures 4 and 5 demonstrate that the Encoder-Decoder network learns the relationships across components for a single asset and dependencies between different assets’ components. The model shows the ability to extrapolate relationships, as evident in the second scatterplot of Figure 4, where expected returns and volatilities extend into a less represented region. Although this area was not extensively covered in the empirical data, it is plausible that the asset may exhibit volatilities and expected returns within that region in the future. Overall, a visual assessment of the components across the entire dataset reveals consistent conditioning of the additional vectors by the correlation matrices for all assets.

4. Case Study

Let’s consider an investor who aims to build a portfolio that outperforms a chosen benchmark over the long-term, while maintaining low tracking error volatility (TEV; measured as the standard deviation of the portfolio’s returns relative to the benchmark). Once the initial investment is made, the portfolio allocations are not adjusted. To construct the portfolio, the study employs an approach that searches for optimal asset weights across simulations using either empirical or synthetic datasets. We hypothesize that portfolios constructed using the synthetic dataset would outperform portfolios based only on the empirical dataset in an out-of-sample period.

| #Obs |

|

|

|

t-stat | p-value |

|

|

|

|

|||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |||||||||||||||||||||

| FR Sims | ||||||||||||||||||||||||||||||

| Empirical | 335 | 74.6 | 46.6 | 0.684 | 0.106 | 0.713 | 0.943 | |||||||||||||||||||||||

| Synthetic | 335 | 69.3 | 47.7 | 0.751 | -13.77 | <0.01% | 0.214 | 0.779 | 1.028 | 81.2% | ||||||||||||||||||||

| Combined | 335 | 68.9 | 47.7 | 0.758 | -14.85 | <0.01% | 0.202 | 0.784 | 1.050 | 84.5% | ||||||||||||||||||||

| MV Sims | ||||||||||||||||||||||||||||||

| Empirical | 335 | 76.2 | 44.5 | 0.640 | 0.096 | 0.683 | 0.990 | |||||||||||||||||||||||

| Synthetic | 335 | 74.9 | 46.4 | 0.661 | -9.52 | <0.01% | 0.203 | 0.680 | 1.036 | 73.1% | ||||||||||||||||||||

| Combined | 335 | 75.0 | 46.3 | 0.661 | -9.54 | <0.01% | 0.190 | 0.680 | 1.035 | 73.1% |

The simulation-based asset allocation method can be described with the following process. We have an matrix that represents n simulation returns for each of the m assets. corresponds to a returns vector of the benchmark, which is one of the columns in the matrix, and is the returns vector of the portfolio, which is obtained by multiplying the matrix of assets’ simulation returns () by , the vector of portfolio weights: . The optimization problem can be defined as:

| (1) |

subject to:

,

where and represent the average expected returns of the portfolio and benchmark across simulations and is an additional excess return target. As a result, the optimizer aims to minimize the 1-month deviations of the portfolio from the benchmark, reducing the tracking error volatility, while ensuring that the expected return is on average higher than or equal to a specified target above benchmark’s expected return. The portfolio must be also fully invested, and there are limitations on FX positions within the range of -5% to 5%.

Simulated returns () and expected returns are derived from three different datasets: the empirical dataset (”Empirical” variant), the synthetic dataset (”Synthetic” variant), or a combination of both (”Combined” variant). The simulated returns were also drawn from two different methods:

-

•

”FR Sims” – the 1-month forward returns vectors were directly sourced from the empirical dataset or generated using the Encoder-Decoder model discussed earlier. This yielded 2,610 forward return sets from the empirical dataset and 64,000 from the synthetic dataset

-

•

“MV Sims” – returns were generated by drawing from a multivariate normal distribution, with covariance matrices based on correlation matrices and volatility vectors from either the empirical or generated datasets. In this approach, multiple simulations were performed per covariance matrix, resulting in 26,100 simulations using the empirical dataset and 640,000 simulations using the synthetic dataset

The ”FR Sims” option was expected to more effectively incorporate the skewed distributions of assets’ returns, resulting in portfolios with on average lower TEVs.

To determine if portfolios constructed using simulations based on synthetic datasets outperform, we conducted a series of experiments. These involved constructing portfolios with the described method and evaluating their performance through backtests conducted over the testing period from May 2017 to October 2022. The backtests were performed for each of the 40 fixed income indices analyzed, with varying excess expected return targets ranging from 20 to 100 bps in 10 bps increments. Instances, where the optimizer failed to converge, were excluded from the analysis. This typically occurred when the portfolio’s benchmark was a high-yielding asset and there were insufficient other assets in the dataset with expected returns meeting the excess return target. Consequently, in total, 335 examples were used in the analysis in both the ”FR Sims” and ”MV Sims” configurations.

The primary metric used to assess the results was the ratio of expected returns in excess of the benchmark’s returns to tracking error volatility. This metric directly aligns with the objectives targeted by the optimizer and serves as an indicator of the expected information ratio in the long term.

Table 4 presents the results of the case study. The variants utilizing the synthetic dataset (”Synthetic” and ”Combined”) demonstrated lower TEVs and higher average excess expected returns compared to the ”Empirical” variant. This difference was particularly notable in the ”FR Sims” options, where the TEVs of the ”Synthetic” and ”Combined” variants were 5 bps lower than that of the ”Empirical” variant. The combination of lower TEVs and slightly higher excess expected returns led to a significant increase in the excess expected returns to TEV ratios. In the ”MV Sims” options, the differences were more subtle, with the TEV being only about 1 bps lower and excess expected returns approximately 1 bps higher for the ”Synthetic” and ”Combined” variants compared to the ”Empirical” variant. The improvements in the excess expected returns to TEV ratios were confirmed by one-sided t-tests, which yielded p-values lower than 1%. Notably, the ”Combined” variants exhibited higher t-stats than the ”Synthetic” variants in both the ”FR Sims” and ”MV Sims” options, suggesting that augmenting the empirical dataset may offer more benefits to practitioners than solely replacing it with a synthetic dataset.

5. Conclusion

In this work, we proposed a process to generate synthetic data for analyses of asset allocation methods in the fixed income universe. The data generation process was divided into two stages: firstly, we generated correlation matrices with an enhanced CorrGAN (Marti, 2020) model and then we sampled additional assets attributes (volatilities, expected returns and forward returns) with an Encoder-Decoder model introduced in this paper. The generated dataset exhibited characteristics of the empirical dataset and preserved relationships between the generated matrices and the additional attributes. Importantly, the generative models also demonstrated their capability in mitigating outliers, reducing reliance on historical events with low future probability, and extrapolating data into probable areas that were sparsely represented in the empirical dataset. In the case study we also illustrated that utilizing the synthetic dataset led to the construction of better-performing portfolios.

Future research endeavors could explore additional modifications to the GAN and Encoder-Decoder model, such as conditioning them on external factors to improve the performance of asset allocation methods in specific market regimes. Additionally, further investigations can focus on expanding the application of synthetic datasets to other asset classes and considering different practitioner requirements. For example, in an equities universe, the model could incorporate valuation metrics alongside volatility metrics to evaluate asset allocation methods with a value-bias.

By introducing this approach to synthetic data generation and demonstrating its practical benefits, we aim to encourage practitioners and researchers to embrace synthetic datasets as a valuable tool for improving asset allocation in the fixed income universe, as well as exploring their potential applications addressing diverse requirements of asset allocators.

References

- (1)

- Aitken et al. (2017) Andrew Aitken, Christian Ledig, Lucas Theis, Jose Caballero, Zehan Wang, and Wenzhe Shi. 2017. Checkerboard artifact free sub-pixel convolution: A note on sub-pixel convolution, resize convolution and convolution resize. arXiv preprint arXiv:1707.02937 (2017).

- Cont et al. (2022) Rama Cont, Mihai Cucuringu, Renyuan Xu, and Chao Zhang. 2022. Tail-gan: Nonparametric scenario generation for tail risk estimation. arXiv preprint arXiv:2203.01664 (2022).

- Flaig and Junike (2022) Solveig Flaig and Gero Junike. 2022. Scenario generation for market risk models using generative neural networks. Risks 10, 11 (2022), 199.

- Flaig and Junike (2023) Solveig Flaig and Gero Junike. 2023. Validation of machine learning based scenario generators. arXiv preprint arXiv:2301.12719 (2023).

- Goodfellow (2016) Ian Goodfellow. 2016. Nips 2016 tutorial: Generative adversarial networks. arXiv preprint arXiv:1701.00160 (2016).

- Goodfellow et al. (2020) Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. 2020. Generative adversarial networks. Commun. ACM 63, 11 (2020), 139–144.

- Gulrajani et al. (2017) Ishaan Gulrajani, Faruk Ahmed, Martin Arjovsky, Vincent Dumoulin, and Aaron C Courville. 2017. Improved training of wasserstein gans. Advances in neural information processing systems 30 (2017).

- Kim (2021) Hyunsu Kim. 2021. Deep hedging, generative adversarial networks, and beyond. arXiv preprint arXiv:2103.03913 (2021).

- Koshiyama et al. (2021) Adriano Koshiyama, Nick Firoozye, and Philip Treleaven. 2021. Generative adversarial networks for financial trading strategies fine-tuning and combination. Quantitative Finance 21, 5 (2021), 797–813.

- Lopez de Prado (2016a) Marcos Lopez de Prado. 2016a. Building diversified portfolios that outperform out-of-sample. Journal of Portfolio Management (2016).

- Lopez de Prado (2016b) Marcos Lopez de Prado. 2016b. A robust estimator of the efficient frontier. Available at SSRN 3469961 (2016).

- Lopez de Prado (2019) Marcos Lopez de Prado. 2019. Tactical investment algorithms. Available at SSRN 3459866 (2019).

- Lu and Yi (2022) Jun Lu and Shao Yi. 2022. Autoencoding Conditional GAN for Portfolio Allocation Diversification. arXiv preprint arXiv:2207.05701 (2022).

- Lundberg and Lee (2017) Scott M Lundberg and Su-In Lee. 2017. A unified approach to interpreting model predictions. Advances in neural information processing systems 30 (2017).

- Mariani et al. (2019) Giovanni Mariani, Yada Zhu, Jianbo Li, Florian Scheidegger, Roxana Istrate, Costas Bekas, and A Cristiano I Malossi. 2019. Pagan: Portfolio analysis with generative adversarial networks. arXiv preprint arXiv:1909.10578 (2019).

- Marti (2020) Gautier Marti. 2020. Corrgan: Sampling realistic financial correlation matrices using generative adversarial networks. In ICASSP 2020-2020 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP). IEEE, 8459–8463.

- Marti et al. (2021) Gautier Marti, Victor Goubet, and Frank Nielsen. 2021. cCorrGAN: Conditional correlation GAN for learning empirical conditional distributions in the elliptope. In Geometric Science of Information: 5th International Conference, GSI 2021, Paris, France, July 21–23, 2021, Proceedings 5. Springer, 613–620.

- Ngwenduna and Mbuvha (2021) Kwanda Sydwell Ngwenduna and Rendani Mbuvha. 2021. Alleviating class imbalance in actuarial applications using generative adversarial networks. Risks 9, 3 (2021), 49.

- Odena et al. (2016) Augustus Odena, Vincent Dumoulin, and Chris Olah. 2016. Deconvolution and checkerboard artifacts. Distill 1, 10 (2016), e3.

- Papenbrock et al. (2021) Jochen Papenbrock, Peter Schwendner, Markus Jaeger, and Stephan Krügel. 2021. Matrix evolutions: synthetic correlations and explainable machine learning for constructing robust investment portfolios. Jochen Papenbrock, Peter Schwendner, Markus Jaeger and Stephan Krügel The Journal of Financial Data Science Spring (2021).

- Radford et al. (2015) Alec Radford, Luke Metz, and Soumith Chintala. 2015. Unsupervised representation learning with deep convolutional generative adversarial networks. arXiv preprint arXiv:1511.06434 (2015).

- Roll (1992) Richard Roll. 1992. A mean/variance analysis of tracking error. The Journal of Portfolio Management 18, 4 (1992), 13–22.