Adaptive Agents and Data Quality in Agent-Based Financial Markets

Abstract.

We present our Agent-Based Market Microstructure Simulation (ABMMS), an Agent-Based Financial Market (ABFM) that captures much of the complexity present in the US National Market System for equities (NMS). Agent-Based models are a natural choice for understanding financial markets. Financial markets feature a constrained action space that should simplify model creation, produce a wealth of data that should aid model validation, and a successful ABFM could strongly impact system design and policy development processes. Despite these advantages, ABFMs have largely remained an academic novelty. We hypothesize that two factors limit the usefulness of ABFMs. First, many ABFMs fail to capture relevant microstructure mechanisms, leading to differences in the mechanics of trading. Second, the simple agents that commonly populate ABFMs do not display the breadth of behaviors observed in human traders or the trading systems that they create. We investigate these issues through the development of ABMMS, which features a fragmented market structure, communication infrastructure with propagation delays, realistic auction mechanisms, and more. As a baseline, we populate ABMMS with simple trading agents and investigate properties of the generated data. We then compare the baseline with experimental conditions that explore the impacts of market topology or meta-reinforcement learning agents. The combination of detailed market mechanisms and adaptive agents leads to models whose generated data more accurately reproduce stylized facts observed in actual markets. These improvements increase the utility of ABFMs as tools to inform design and policy decisions.

1. Introduction

Decades of market microstructure research have shown that the mechanics of trading meaningfully impact price formation (O’hara, 1997; Madhavan, 2000; Hasbrouck, 2007). Price formation in agent-based financial markets (ABFMs) is also influenced by market microstructure, thus, ABFMs that fail to adequately capture market microstructure mechanisms present in their target systems may observe divergences in behaviors and outcomes.

The ecology of agents that populate an ABFM is just as important as the market infrastructure that mediates their interactions (LeBaron, 2001). Simple agents, such as Zero intelligence (ZI) agents (Gode and Sunder, 1993), are commonly used to understand baseline characteristics of markets (Smith et al., 2003; Farmer et al., 2005; LeBaron, 2006; Cont et al., 2010; Gould et al., 2013). However, simple agents do not exhibit the level of heterogeneity or adaptability seen in authentic market participants.

In real markets, it is common for short term trading strategies to lose effectiveness over time, a phenomenon referred to as alpha decay (Di Mascio et al., 2016). By some estimates, short term strategies take 3 to 7 months to develop and remain effective for 3 to 4 months (Schmerken, 2008). Since the average development duration is longer than the average strategy lifetime, we might expect the population of short term strategies to have a high turnover rate. This high turnover rate may be a mechanism driving non-stationary trading dynamics. It also indicates that strategy adaptation is a critical attribute of successful market participants, and that static strategies may be poorly suited for realistic ABFMs.

The use of adaptive strategies in ABFMs can promote agent specialization, leading to emergent heterogeneity. Agent heterogeneity can contribute to financial market resilience (Bookstaber et al., 2016), thus emergent heterogeneity driven by adaptive agents could improve the stability of ABFMs. Additionally, agent adaptability is critical to realize economic rationality in non-trivial ABFMs (Vives, 1993; Hammond, 1997; Marwala, 2017). Economically rational agents avoid using trading strategies that lead to financial ruin. Thus, when agents with inflexible strategies encounter unfavorable market conditions they may be forced to exit the market. Excessive attrition can lead to complete failure of a simulated market. Observed deviations from the Efficient Markets Hypothesis (Malkiel and Fama, 1970; Brown, 2011) and the rise of the Adaptive Markets Hypothesis (Lo, 2004) indicate a growing realization of the importance of agent adaptability in financial markets.

In this paper we present our Agent-Based Market Microstructure Simulation (ABMMS), an ABFM with realistic market mechanisms and agent adaptability as core design principles. We evaluate ABMMS under different configurations to determine the impacts of market fragmentation and adaptive agents on the quality of generated data. Our evaluation procedure is built using stylized facts and analytical methods developed by the econometrics, market microstructure, and ABFM communities. ABMMS is able to produce market data that mimics the form and features seen in genuine market data products. Data generated by ABMMS conforms to several stylized facts of asset prices, along with other observed properties of authentic market data, and thus may be more suitable to inform system design or policy than simpler ABFMs.

2. Related Work

2.1. Market Infrastructure in the National Market System

ABMMS aims to reproduce aspects of the US National Market System for equities (NMS), and many design decisions were based on this choice of target system. To provide the appropriate context for understanding our model, we summarize the market infrastructure present in the NMS and indicate references with additional details.

Trading in the NMS occurs in a fragmented market that consists of 16 securities exchanges, which manage several continuous double auctions (CDAs) to support trading in a set of assets (equity securities, exchange traded funds, etc). A CDA allows traders to submit orders to buy (bid) or sell (offer) at any time, and processes those orders immediately upon receipt. Orders that cannot be fulfilled instantly are collected in a Limit Order Book (LOB). Almost all CDAs prioritize order execution based on price and time, i.e. price-time priority, though some may use additional attributes. For additional details regarding CDAs or LOBs, see one or more of Smith et al. (2003); Gould et al. (2013); Abergel et al. (2016), and Friedman (2018).

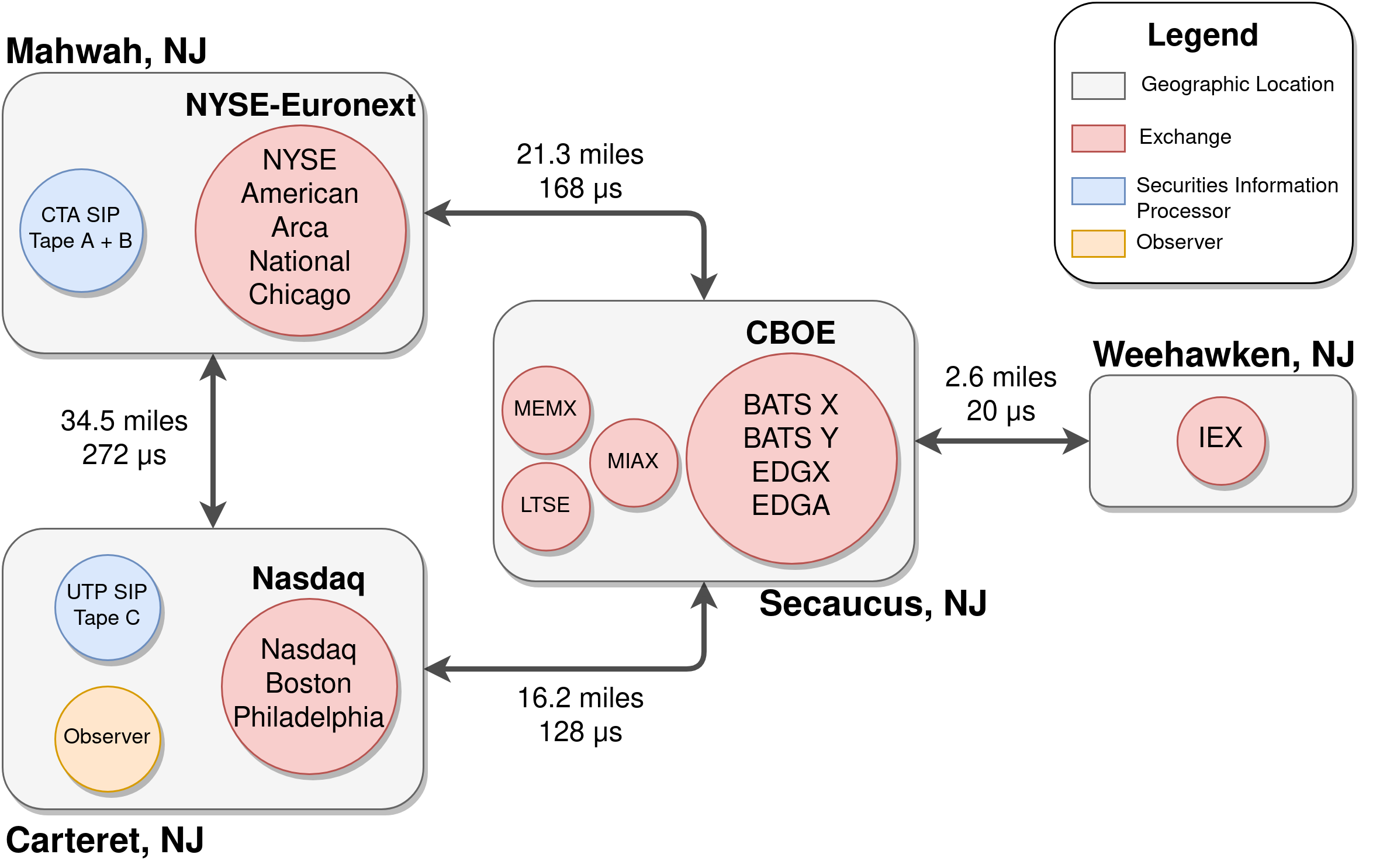

The 16 exchanges that form the NMS are housed within at least four data centers in northern New Jersey (Tivnan et al., 2020). These data centers are connected by an Communication Network (CN) that is implemented with a combination of fiber optic technology and wireless alternatives (Networks, 2021).

The use of continuous trading mechanisms causes a race to react any time new public information is released. All known communication technologies are limited by the speed of light, which guarantees the existence of propagation delays on each leg of an CN, an average of 100 s based on the current configuration of the NMS (Tivnan et al., 2020). Optimized trading algorithms on specialized hardware may only take between tens of ns to a few s to react to incoming messages. The combination of these three properties means that the propagation delays imposed by the topology and geometry of the CN can have an immense impact on trading outcomes. See Section 3 of Tivnan et al. (2020) for additional details regarding the organization of the NMS.

Beyond the mechanical details mentioned above, the regulatory environment that surrounds the NMS plays an important role in shaping the market infrastructure and agent behaviors. Readers interested in understanding key NMS regulations should refer to Appendix 3 from Tivnan et al. (2020) for an overview, or the regulation itself for details (Securities and Commission, 2005).

2.2. Market Infrastructure in Prior ABFMs

Many ABFMs implement a simple infrastructure that allows clear emphasis to be placed on specific elements, while also reducing computational costs and allowing for rapid experimentation. For example, Wah et al. (2017) study a population of heterogeneous agents trading a single asset in a single continuous double auction (CDA). The simplicity of the infrastructure places the emphasis on the heterogeneous agents, the quality of their interactions, and differences in their outcomes.

It is possible to model financial markets without agents or an explicit market microstructure. Equation Based Models (EBMs) boil down all activity to a set of mathematical equations, commonly differential equations, that describe macro-level quantities, such as asset prices (Sabzian et al., 2019). However, abstracting away these details can restrict or eliminate the possibility of emergent phenomena, greatly reducing the expressiveness of a model.

Early modeling efforts focused on simpler market architectures, such as Walrasian auctions and dealer markets (O’hara, 1997; Hasbrouck, 2007). But most modern equity markets feature a fragmented CDA with trading activity distributed across multiple locations.

Some have used ABFMs to investigate the impacts of market fragmentation, usually focusing on the simplest case involving two auctions (Wah and Wellman, 2016; Duffin and Cartlidge, 2018; Baldauf and Mollner, 2021). To simulate fragmented markets these ABFMs must account for communication latency, otherwise the fragmentation would not have a material impact on trading activity. When modeling fragmented markets, it is common to implement one or more securities information processors (SIPs) (Tivnan et al., 2017). SIPs serve as data aggregators that disseminate important signals to keep prices synchronized in a fragmented market, such as the National Best Bid and Offer (NBBO), an indicator of market wide best price.

In addition to market fragmentation, which occurs at the level of financial exchanges, some have explored ABFMs that capture the interactions that occur in multi-level markets containing many interconnected financial systems, such as equity markets, options markets (Ecca et al., 2008), brokerages, and banks (Bookstaber et al., 2018).

Speed can be a deciding factor in the competition of trading strategies, especially in market systems with continuous auction mechanisms. An often underappreciated element of this competition are response delays, the time it takes a trading strategy to ingest an incoming market message and issue an appropriate response. These response delays are often so small that they are assumed to have minimal impact on trading outcomes, and thus are not implemented in many ABFMs. However, since many aspects of the race for speed have been commoditized (e.g., colocation, wireless communication channels, specialized computing hardware, etc.) the microseconds that can be shaved via software optimization can have serious impacts (Rollins and Cliff, 2020).

There are an endless number of market infrastructure details that can impact trading processes, and should be captured in detailed models. However, in this work we focus exclusively on a stock market with detailed implementations of market fragmentation, communication infrastructure, auction mechanisms, and adaptive agents.

We applaud recent work in this area, which has attempted to address aspects of market infrastructure realism or trading agent adaptability (Jacob Leal et al., 2016; Wang and Wellman, 2017; Byrd et al., 2019; Dicks and Gebbie, 2022; Gao et al., 2022a, b), though we believe that ABMMS implements a unique set of features that is not entirely present in any existing model.

2.3. Adaptive Agents

Mechanisms for adaptive agents can be classified as active or passive (LeBaron, 2011). Active learning involves intentional change of an agent’s strategy, while passive learning occurs via the accumulation of wealth by more effective strategies over time. We direct our interest towards active learning mechanisms, due to recent advances in the field of machine learning as well as the potential relationship between active learning and economic rationality (Vives, 1993).

Active adaptive agents can feature two types of strategies, fixed or free form. Fixed strategies cover a single qualitative class of behaviors and tune a set of parameters in response to changing market conditions. Despite their ability to modify certain aspects of their behavior, such as interaction frequency or pricing beliefs, fixed strategies cannot spontaneously adopt qualitatively distinct strategies. On the other hand, free form strategies are able to implement two or more classes of behavior, and perhaps even develop new strategies on the fly. Since the behavior of fixed strategies is more constrained than their free form counterparts, they tend to be simpler to develop and understand.

2.3.1. Fixed Strategy Agents

The ZI agents introduced by Gode and Sunder (1993) were simple and broadly applicable, which lead to a proliferation of applications and sparked a vein of research that has been developed for decades. ZI Plus (ZIP) agents extend the ZI recipe by developing pricing beliefs based on the bid and offer prices that lead to trades (Cliff and Bruten, 1997; Cliff, 1997; Preist and van Tol, 1998; Cliff, 2018). The agents created by Gjerstad and Dickhaut (1998) (GD) have a similar structure to ZIP agents, they develop price belief functions based on quotes and trades. However, GD agents take actions that greedily maximise surplus, where as ZIP agents do not directly optimize profits. By covering some pathological edge cases in the GD algorithm, Modified GD (MGD) agents (Tesauro and Das, 2001) avoid excessive volatility and outperform their predecessor. The GDX strategy (Tesauro and Bredin, 2002) also builds on the pricing belief functions seen in GD agents, but accounts for future rewards via dynamic programming. This forward-looking optimization promotes longer-term strategies with more interesting behavior. Adaptive Aggressiveness (AA) agents (Vytelingum et al., 2008) combine price belief functions with an aggression function that allows them to strategically account for their “desire to trade”. Taking a slightly different approach, Assignment Adaptive (ASAD) agents (Stotter et al., 2014) use a relatively simple strategy that is less adaptive in some ways than ZIP agents, but explicitly accounts for the information contained in an agent’s submitted orders. ASAD agents can generate interesting dynamics, especially when reacting to exogenous price shocks in a homogeneous strategy space, but are generally outclassed by ZIP agents when in direct competition.

This line of research has created several relatively simple agents that combine domain knowledge with basic machine learning and optimization techniques, resulting in adaptive, but fairly restricted strategies. Through the use of more advanced machine learning techniques, removing imposed strategy structure, and allowing for greater strategy complexity, we can create agents that develop qualitatively distinct strategies.

2.3.2. Free Form Strategy Agents

Free form strategies are constructed around a behavior adaptation mechanism, commonly implemented using machine learning, that allows the agent to respond appropriately to changing market conditions.

Supervised learning techniques, in the form of imitation learning, can replicate observed patterns in order flow data (le Calvez and Cliff, 2018; Sirignano and Cont, 2019; Wray et al., 2020). However, agents built with imitation learning tend to regurgitate observed behaviors, and thus have little ability to respond to market conditions that were not observed during training or to generate new strategies. Generative Adversarial Networks (GANs) are able to create realistic looking streams of order flow in a similar manner to imitation learning based methods. GANs may be better than imitation learning at generating novel content, due to the adversarial learning mechanism, but still lack a mechanism necessary for effective generalization (Li et al., 2020).

One of the most obvious learning signals present in financial markets is profit. Profit motive is relied on as one of the fundamental forces in financial markets, and it makes intuitive sense to train trading strategies with it. Two classes of algorithms are particularly effective at deriving appropriate behavior from arbitrary reward signals: meta-heuristic search and reinforcement learning. Both meta-heuristic search (Subramanian et al., 2006; Hu et al., 2015) and reinforcement learning (Schvartzman and Wellman, 2009; Deng et al., 2016) have been applied repeatedly, and with varying degrees of success, to the learning of trading strategies.

Many traditional applications of meta-heuristic search and reinforcement learning focused on narrowly defined problems, and did not emphasize the ability to adapt to dynamic environments. The rise of meta-learning, commonly described as learning to learn, has greatly improved the ability of machine learning models to learn from, and adapt to, more broadly defined problems (Hospedales et al., 2020). Trading agents developed using meta-learning techniques, such a hierarchical reinforcement learning (Talla Kuate, 2016) or meta-learned evolutionary strategies (Sorensen et al., 2020), often learn more quickly, display higher peak performance, and handle new market conditions more gracefully than agents developed with traditional techniques.

2.4. Model Examination

For an ABFM to be useful to policy makers and system designers, it must satisfy three properties. First, the model must align with the system that it is intended to influence. Second, the model must provide useful insights into that target system. Third, the model must garner a certain amount of trust from policy makers and designers.

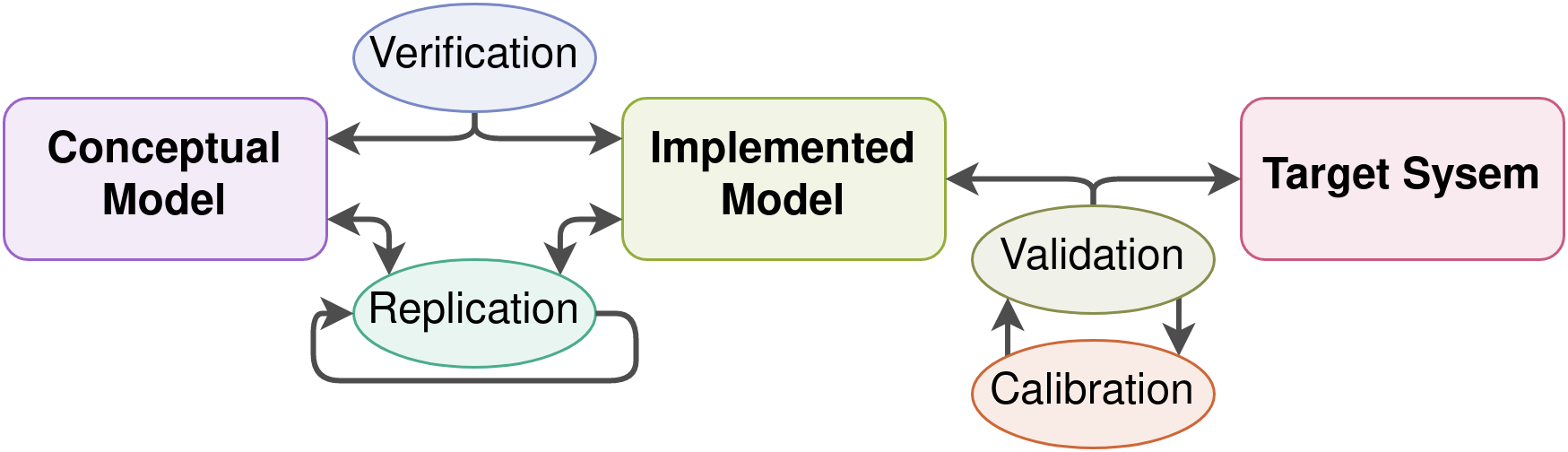

Figure 1 summarizes the model development pipeline, including ABFM development, which is driven by four processes that ensure quality and consistency: verification, validation, calibration, and replication (Xiang et al., 2005; Rand and Wilensky, 2006; Arifin and Madey, 2015). During verification, an implemented model is compared and contrasted with a conceptual model. Good software testing and debugging are core verification tasks, though visual inspection of model outputs and other similar actions also play a role. Validation compares an implemented model with the target system via iterative calibration, which involves tuning free model parameters so that data generated by the model resembles data from the target system. Comprehensive validation and verification, along with clear communication, establish a baseline level of trust in a model. Replication, which is a collection of tasks ranging from running code provided by the creators of a model to complete re-implementation, can further bolster the reputation of a model. The primary goal of replication is to ensure that the outputs of the model display the advertised properties, and are not the result of spurious factors.

Model validation can be driven by data collected from the target system, stylized facts that have been developed based on quantitative observation of the target system, or other forms of distilled knowledge. In most cases, this decision is based on data availability. For example, it is prohibitively costly to obtain high frequency data from all of the exchanges in the NMS. Like many who have come before us (Ghoulmie et al., 2005; Bookstaber et al., 2016; McGroarty et al., 2019), we validate our model using stylized facts of asset price time series (Cont, 2001), order book metrics (Paddrik et al., 2017), and dislocations (Tivnan et al., 2020), instead of depth-of-book data.

3. Methods

3.1. Market Infrastructure in ABMMS

We developed ABMMS, a highly configurable ABFM that targets the US National Market System for equities (NMS), to investigate the impacts of market microstructure and adaptive agents. ABMMS emphasizes the explicit representation of many market microstructure elements, starting with a realistic communication network (CN). The CN consists of a queue of in-flight messages and a topology that those messages travel over. The topology is an undirected graph with weighted edges, where nodes are data centers, edges are communication channels, and edge weights are deterministic propagation delays. Messages are routed based on the shortest weighted path, identified via Dijkstra’s algorithm. Exponential noise with a mean of 5 s is added to the propagation delay to simulate latency jitter and other stochastic delays.

Figure 2 shows the default configuration for ABMMS, which is derived from the state of the NMS in early 2021 and adopts the propagation delays presented by Tivnan et al. (2020). ABMMS uses a discrete-event scheduler to process messages passed between agents via the CN, capturing the temporal heterogeneity of market events and agent response times. Messages are processed sequentially based on the time they should arrive at their recipient, resulting in a dynamic step size for the simulation clock. Exchanges are distributed across the nodes of the CN, where each exchange manages a CDA for each actively traded stock. All CDAs in ABMMS prioritize the execution of orders based on price, visibility, and time, with ties broken randomly. Each Exchange implements a fee schedule that includes market access fees, also known as maker-taker fees, which incentivize liquidity demand or supply depending on the configuration. The default configuration of ABMMS includes a pair of SIPs that construct and disseminate NBBOs, LULD bands, and TAQ feeds. See Appendix A for an in depth description of ABMMS following the Overview, Design concepts, Details (ODD) protocol (Grimm et al., 2006; Grimm et al., 2010; Grimm et al., 2020).

When compared with previous ABFMs, ABMMS implements several market elements that are usually abstracted away, and have never been investigated simultaneously in a single model. Specifically, CDAs to facilitate trading, multiple assets traded simultaneously, market fragmentation in excess of two exchanges, SIPs that issue NBBOs as well as LULD bands, trade-through protection, common order modifiers (hidden, immediate-or-cancel, all-or-nothing, inter-market sweep), and market access fees. There is an expectation of emergent phenomena in ABFMs, thus the inclusion of these additional details may have non-trivial impacts on market dynamics, especially if leveraged strategically by a learning agent.

3.2. Traders

We developed our adaptive trading agent using meta-reinforcement learning (Duan et al., 2016; Wang et al., 2016). Meta-reinforcement learning is better able to adapt to dynamic environments than traditional reinforcement learning, and financial markets are extraordinarily dynamic. One mechanism that causes meta-reinforcement learning to foster adaptability is the use of effective experimentation processes. Meta-reinforcement learning agents are able to actively investigate the state of their environment and incorporate that information into their decision process (Dasgupta et al., 2019).

Given the importance of agent adaptability and heterogeneity discussed earlier, one approach to developing reinforcement learning traders might populate a simulation entirely with such reinforcement learning traders in order to develop a population of co-adapted strategies. However, multi-agent reinforcement learning is unstable (Buşoniu et al., 2010). With each agent adapting in real time, the optimal strategy for all agents becomes a moving goal that is difficult to approach. Instead, we focus on the impact of a single reinforcement learning agent in simulations otherwise populated with simple agents. For this purpose we select ZIP agents, since they have a long history of effective applications in ABFMs and have not been clearly bested by another simple strategy (Rollins and Cliff, 2020).

We develop our ZIP traders based on the reference implementation provided by Cliff (2018), with one minor deviation. The original implementation of ZIP traders uses an exogenous stream of limit prices as a basis for the pricing beliefs of each agent. We replace this exogenous input with random limit prices drawn from a truncated normal distribution that is parameterized based on the current Limit Up-Limit Down (LULD) bands and is updated each time new LULD bands are issued (details in Appendix A.11.4).

3.3. Stylized Facts

The econometrics community has been developing stylized facts that capture various features of data generated by financial markets since the mid 90’s, if not earlier (Pagan, 1996; Cont, 2001; Bouchaud et al., 2002; Potters and Bouchaud, 2003; Sewell, 2011). Stylized facts are statistical properties that are observed across a broad range of assets, markets, and time periods. Stylized facts are qualitative and trade off precision in favor of generality, thus there can be exceptions. However, through the combination of many stylized facts, it becomes possible to identify data that has been generated by authentic trading processes.

We focus on the eleven stylized facts outlined by Cont (2001), since they are relatively simple to test for with moderate amounts of data. However, three facts (#1: Absence of Linear Auto-correlation, #4: Aggregational Gaussianity, and #11: Asymmetry in Time Scales) require long periods of coarse grained data that can be costly to generate with high fidelity models. We eschew the three problematic facts, and rely on the remaining eight to validate ABMMS.

The stylized facts described by Cont (2001) are exclusively concerned with properties of asset price time series. However, ABMMS produces much more information than asset price time series. In particular, we have access to a complete depth-of-book feed, thus metrics that investigate limit order book properties (Bouchaud et al., 2002; Potters and Bouchaud, 2003; Sewell, 2011; Paddrik et al., 2017) could also help to quantify the impacts of our meta-reinforcement learning trader.

4. Results

To ensure that our tests for stylized facts are effective, we calibrate them on historical price data. We source minute resolution data from Alpha Vantage (Inc., 2021a) for 30 US stocks: AAPL, AXP, BA, CAT, CSCO, CVX, DD, DIS, GE, GS, HD, IBM, INTC, JNJ, JPM, KO, MCD, MMM, MRK, MSFT, NKE, PFE, PG, RTX, TRV, UNH, V, VZ, WMT, and XOM. The data for most symbols covers two years of trading, roughly from April 2019 through February 2021. RTX was formed as the result of a merger in 2020, and thus has truncated data coverage from April 2020 through May 2021 (roughly 14 months). Alpha Vantage derives their data from SIP feeds and aggregates to minute resolution, with open, high, low, close, and volume features. The data is adjusted to account for splits and dividends. See the Alpha Vantage documentation for more details (Inc., 2021b).

| Stylized Fact | Free Parameters | Best Parameter Values | Pass Rate |

|---|---|---|---|

| #2: Heavy Tailed Returns | Window Size | max(len(returns) // 1000, 30) | 29 / 30 |

| #3: Asymmetry of Returns | Window Size | max(len(returns) // 1000, 390) | 10 / 30 |

| #5: Intermittency of Returns | Window Size | max(len(returns) // 60, 100) | 29 / 30 |

| #6: Volatility Clustering | Lag Count | 5000 | 30 / 30 |

| #7: Heavy Tailed Conditional Returns | Window Size | max(len(returns) // 1000, 30) | 29 / 30 |

| #8: Slow Decay of Return Autocorrelation | Lag Count | 100 or 10000 | 21 / 30 |

| #9: Leverage Effect | R Value Threshold, P Value Threshold | None, None | 25 / 30 |

| #10: Volume/Volatility Correlation | R Value Threshold, P Value Threshold | None, None | 12 / 30 |

We calibrate our tests for stylized facts by optimizing free parameters to improve their detection rate. This relies on the assumption that the selected stylized facts should be expected in these stocks and during this time period. However, stylized facts are not without exceptions and market dynamics may have qualitatively changed since the early 2000’s. Table 1 summarizes the results of our stylized fact calibration, with the main take-away being that facts #3 and #10 were difficult to reliably detect. Due to this lack of consistency, we rely on the remaining six stylized facts (#2 and #5 through #9) when validating ABMMS.

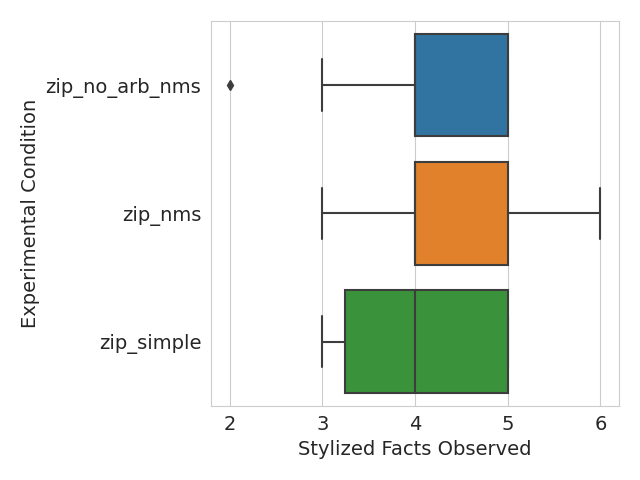

To provide the appropriate context for interpreting the impact of a learning agent, we select three control configurations. In zip_simple, we use a single exchange, a single SIP, and 30 ZIP traders, all of which are located at the Carteret node of the CN. The zip_nms configuration features a relatively complete representation of the NMS, with 16 exchanges distributed across the four nodes of the CN, a SIP located in Mahwah, and a SIP located in Carteret. This condition is populated with 29 ZIP traders that are randomly distributed and one Arbitrage trader located at Secaucus. The final condition, zip_no_arb_nms, is identical to zip_nms except that it replaces the Arbitrage trader with a ZIP trader. Between these three configurations we can isolate the impacts of market infrastructure differences and understand some of the effects of market fragmentation. The experimental condition is identical to zip_nms, but replaces the Arbitrage trader with a Reinforcement Learning trader.

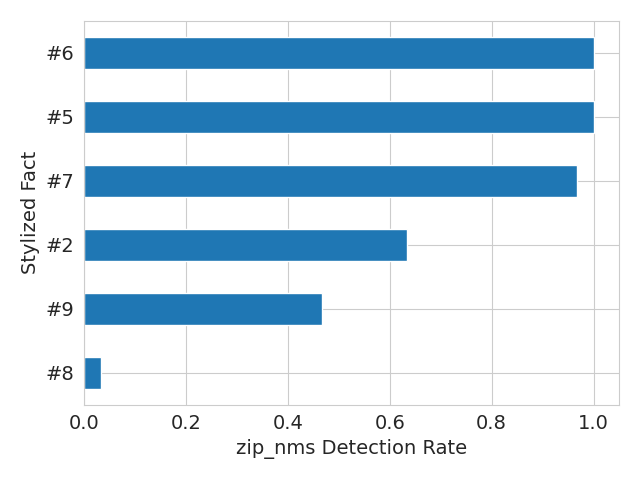

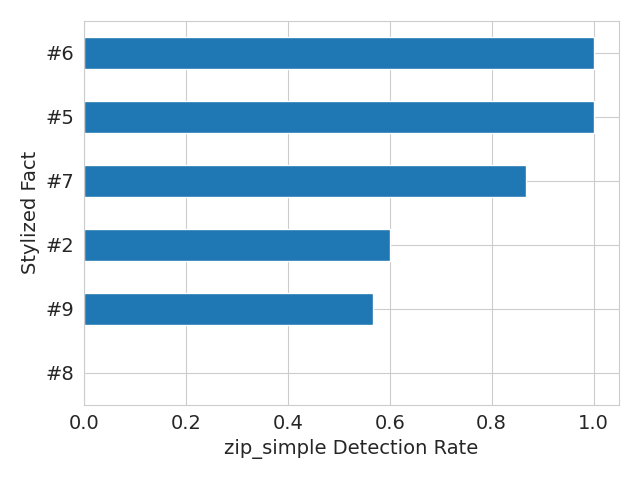

We collect data from 30 independent trials for each condition, where a single trial covers five trading days. Figure 3 shows the ability of data generated by each condition to display the six stylized facts that were selected based on the calibration discussed above. All of the baseline configurations display roughly four of the six stylized facts. The two conditions with NMS-inspired market infrastructure, zip_nms and zip_no_arb_nms, had a slight advantage over zip_simple, but that difference was not statistically significant.

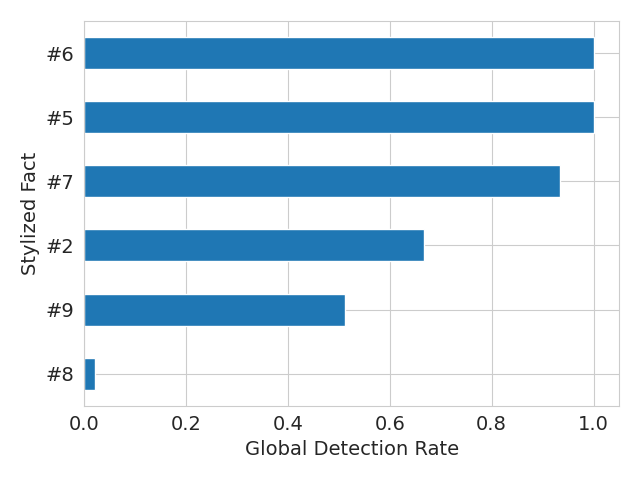

Figure 4 displays the detection rate of each stylized fact, across all trials and by experimental condition. Facts #5 and #6 had a perfect detection rate, facts #2, #7, and #9 were detected in more than 50% of trials, and fact #8 was detected in less than 10% of trials. The two conditions with NMS-inspired infrastructure were more likely to display fact #2 and less likely to display fact #9 than the condition with simple infrastructure. Additionally, the condition with simple infrastructure was unable to produce a single trial that displayed fact #8, whereas the NMS-inspired conditions both produced a single trial that did.

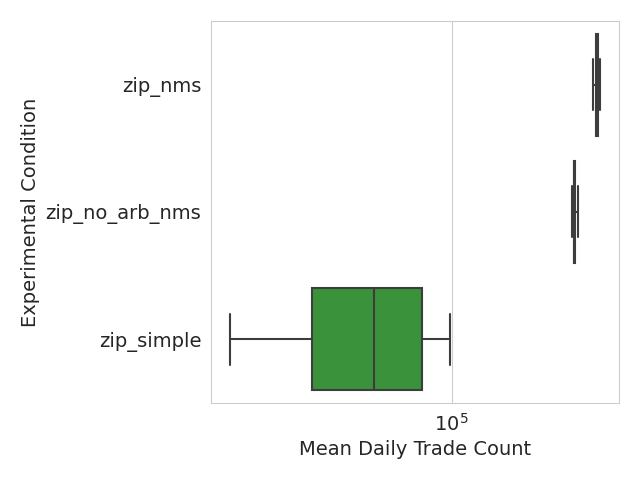

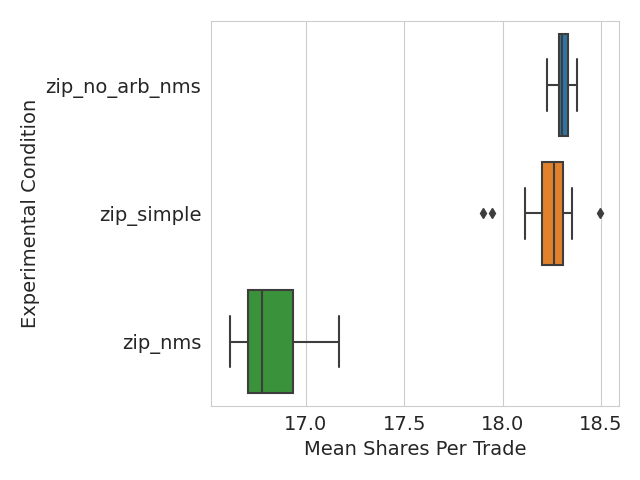

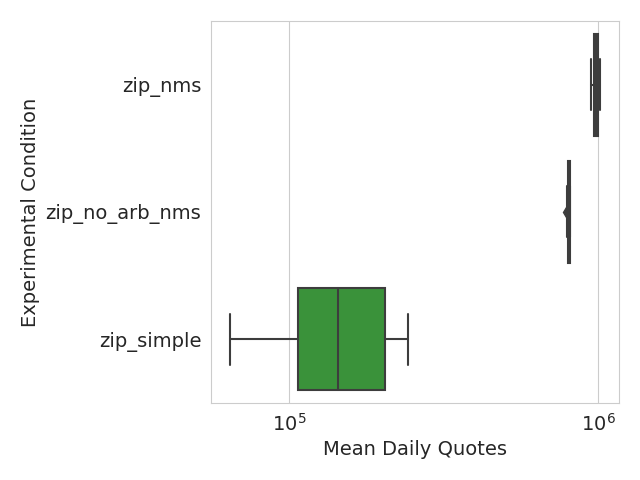

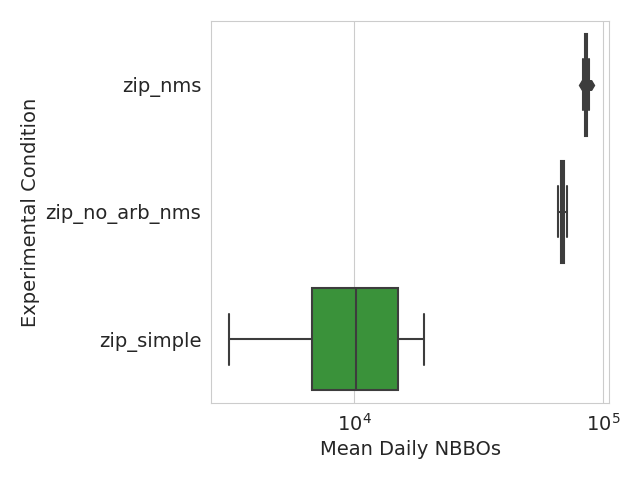

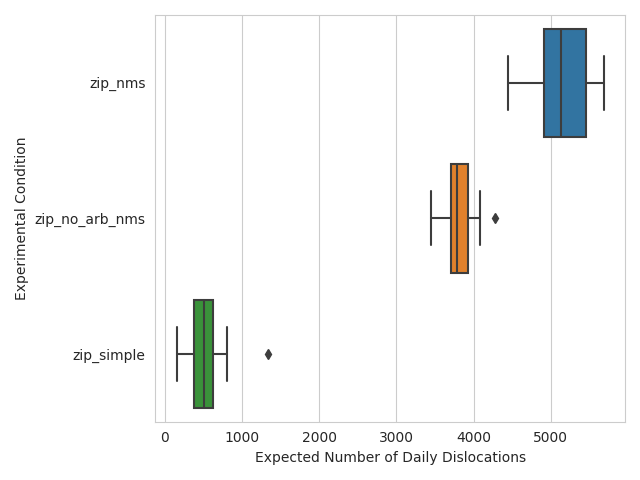

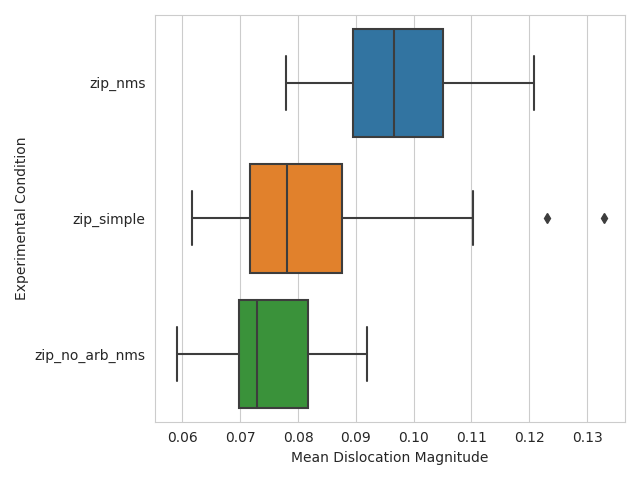

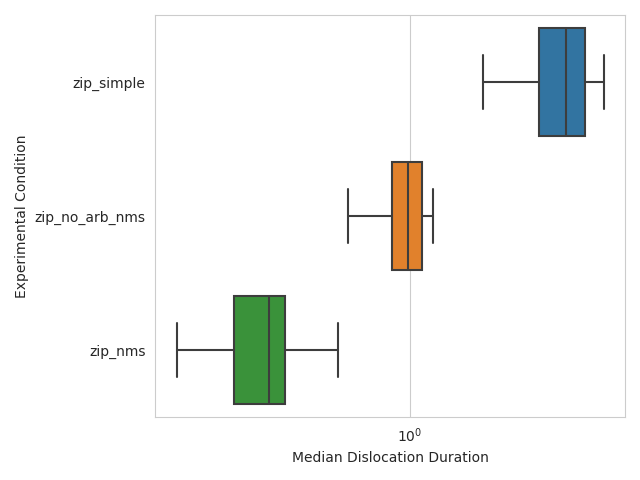

The stylized facts developed by Cont (2001) are exclusively concerned with properties of asset price time series. However, there is a wealth of additional information that is produced by real markets, and by ABMMS. Figure 5 investigates differences between the experimental conditions using daily occurrences of trades, quotes, and NBBOs. Market fragmentation and the arbitrage trader both have non-trivial impacts on all of these statistics, but market fragmentation has a much larger effect. Figure 6 summarizes the occurrence of dislocations, as discussed in Tivnan et al. (2020), in ABMMS. The zip_simple condition generates roughly an order of magnitude less dislocations than the conditions with NMS-inspired infrastructure, but those dislocations tend to be longer. The arbitrage trader appears to cause an increase in the mean dislocation magnitude, but also a large decrease in dislocation duration.

5. Discussion and Conclusion

The fact that dislocations occur in ABMMS, and can be directly measured in the same way as the NMS, is an advance in ABFM infrastructure. Tivnan et al. (2020) indicates that dislocations in the NMS tend to have a median duration between and seconds, which is roughly 3 orders of magnitude smaller than the median duration displayed by the different configurations of ABMMS. This is likely caused by the relatively small number of trading agents simulated, and may also indicate that we need representative strategies that characteristically operate at higher frequencies.

There are three major directions that this work could be extended. First, we investigated the impacts of a single learning agent to avoid development difficulties that can be encountered when multiple learning agents interact, however future work should tackle these issues and develop populations of heterogeneous learning agents. Second, we captured many important mechanisms in our implementation of ABMMS, but the NMS is an extremely complicated system and there are bound to be details that we have abstracted away. Enumerating and implementing these additional mechanisms will improve the accuracy of future models, and open additional strategies for learning agents to explore. Third, we chose to exclusively implement an equities market. However, real equity markets are linked with several financial systems, including lending systems and options markets. Extending ABMMS to account for any of these additional financial systems could enrich the produced results. Beyond these direct extensions, our implementation and calibration of tests for stylized facts indicates a need to revisit some common stylized facts, which may be more difficult to identify, or may not be displayed in the same ways as previously observed.

Financial market policy has been shaped largely by public comments (Securities and Commission, 2021a), recent events (Securities and Commission, 2010), and live pilots (Securities and Commission, 2021b). However, each of these influences is problematic in its own way. Public comments can be subjective or self serving, recent events only help retrospectively, and live pilots impose costs on exchanges (Michaels and Osipovich, 2020). There have been a few successful applications of ABFMs to policy evaluation (Soramäki et al., 2006; Darley, 2007; Haldane and May, 2011; Laine, 2015; Bookstaber et al., 2016; Collver Jr., 2017; Bookstaber et al., 2018), but additional efforts could increase the amount of policy informed by ABFMs and avoid the noted issues associated with other policy influencing mechanisms.

We do not openly provide the source code for our agents, models, and analysis due to concerns about potential malicious use. We will consider sharing all or part of the source code on a case by case basis. Please contact the authors if interested. Finally, to facilitate peer review and some degree of transparency, we provide all of the model outputs from experimental runs used to create the figures and analysis of this paper (Van Oort, 2021).

Acknowledgements

We thank Thayer Alshaabi, David Dewhurst, Matthew Koehler, and John Ring for their insightful discussion and suggestions. Some computations were performed on the Vermont Advanced Computing Core, supported in part by NSF award No. OAC-1827314.

References

- (1)

- Abergel et al. (2016) Frédéric Abergel, Marouane Anane, Anirban Chakraborti, Aymen Jedidi, and Ioane Muni Toke. 2016. Limit order books. Cambridge University Press.

- Arifin and Madey (2015) SM Niaz Arifin and Gregory R Madey. 2015. Verification, Validation, and Replication Methods for Agent-Based Modeling and Simulation: Lessons Learned the Hard Way! In Concepts and Methodologies for Modeling and Simulation. Springer, 217–242.

- Baldauf and Mollner (2021) Markus Baldauf and Joshua Mollner. 2021. Trading in fragmented markets. Journal of Financial and Quantitative Analysis 56, 1 (2 2021), 93–121.

- Bookstaber et al. (2016) Richard Bookstaber, Michael D Foley, and Brian F Tivnan. 2016. Toward an understanding of market resilience: market liquidity and heterogeneity in the investor decision cycle. Journal of Economic Interaction and Coordination 11, 2 (2016), 205–227.

- Bookstaber et al. (2018) Richard Bookstaber, Mark Paddrik, and Brian Tivnan. 2018. An agent-based model for financial vulnerability. Journal of Economic Interaction and Coordination 13, 2 (2018), 433–466.

- Bouchaud et al. (2002) Jean-Philippe Bouchaud, Marc Mézard, and Marc Potters. 2002. Statistical properties of stock order books: empirical results and models. Quantitative finance 2 (2002), 251–256.

- Brown (2011) Stephen J Brown. 2011. The efficient markets hypothesis: The demise of the demon of chance? Accounting & Finance 51, 1 (2011), 79–95.

- Buşoniu et al. (2010) Lucian Buşoniu, Robert Babuška, and Bart De Schutter. 2010. Multi-agent reinforcement learning: An overview. Innovations in multi-agent systems and applications-1 (2010), 183–221.

- Byrd et al. (2019) David Byrd, Maria Hybinette, and Tucker Hybinette Balch. 2019. Abides: Towards high-fidelity market simulation for ai research. arXiv preprint arXiv:1904.12066 (2019).

- Cliff (1997) Dave Cliff. 1997. Minimal-intelligence agents for bargaining behaviors in market-based environments. Hewlett-Packard Labs Technical Reports (1997).

- Cliff (2018) Dave Cliff. 2018. BSE: A Minimal Simulation of a Limit-Order-Book Stock Exchange. Proceedings of the 30th European Modeling and Simulation Symposium (EMSS 2018) (2018), 194–203.

- Cliff and Bruten (1997) Dave Cliff and Janet Bruten. 1997. Zero is Not Enough: On The Lower Limit of Agent Intelligence For Continuous Double Auction Markets. Hewlett-Packard Labs Technical Reports (1997).

- Collver Jr. (2017) Charles D. Collver Jr. 2017. An application of agent-based modeling to market structure policy: the case of the U.S. Tick Size Pilot Program and market maker profitability. https://www.sec.gov/marketstructure/research/increasing-the-mpi-combined.pdf

- Cont (2001) Rama Cont. 2001. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 1 (2001), 223–236.

- Cont et al. (2010) Rama Cont, Sasha Stoikov, and Rishi Talreja. 2010. A stochastic model for order book dynamics. Operations research 58, 3 (2010), 549–563.

- Darley (2007) Vincent Darley. 2007. A NASDAQ market simulation: insights on a major market from the science of complex adaptive systems. Vol. 1. World Scientific.

- Dasgupta et al. (2019) Ishita Dasgupta, Jane Wang, Silvia Chiappa, Jovana Mitrovic, Pedro Ortega, David Raposo, Edward Hughes, Peter Battaglia, Matthew Botvinick, and Zeb Kurth-Nelson. 2019. Causal reasoning from meta-reinforcement learning. arXiv preprint arXiv:1901.08162 (2019).

- Deng et al. (2016) Yue Deng, Feng Bao, Youyong Kong, Zhiquan Ren, and Qionghai Dai. 2016. Deep direct reinforcement learning for financial signal representation and trading. IEEE transactions on neural networks and learning systems 28, 3 (2016), 653–664.

- Dewhurst et al. (2019) David Rushing Dewhurst, Colin M Van Oort, John H Ring IV, Tyler J Gray, Christopher M Danforth, and Brian F Tivnan. 2019. Scaling of inefficiencies in the US equity markets: Evidence from three market indices and more than 2900 securities. arXiv preprint arXiv:1902.04691 (2019).

- Di Mascio et al. (2016) Rick Di Mascio, Anton Lines, and Narayan Y Naik. 2016. Alpha decay. SFS Finance Cavalcade (2016).

- Dicks and Gebbie (2022) Matthew Dicks and Tim Gebbie. 2022. A simple learning agent interacting with an agent-based market model. arXiv preprint arXiv:2208.10434 (2022).

- Duan et al. (2016) Yan Duan, John Schulman, Xi Chen, Peter L Bartlett, Ilya Sutskever, and Pieter Abbeel. 2016. Rl 2: Fast reinforcement learning via slow reinforcement learning. arXiv preprint arXiv:1611.02779 (2016).

- Duffin and Cartlidge (2018) Matthew Duffin and John Cartlidge. 2018. Agent-based model exploration of latency arbitrage in fragmented financial markets. In 2018 IEEE Symposium Series on Computational Intelligence (SSCI). IEEE, 2312–2320.

- Ecca et al. (2008) Sabrina Ecca, Michele Marchesi, and Alessio Setzu. 2008. Modeling and simulation of an artificial stock option market. Computational Economics 32 (2008), 37–53.

- Espeholt et al. (2018) Lasse Espeholt, Hubert Soyer, Remi Munos, Karen Simonyan, Vlad Mnih, Tom Ward, Yotam Doron, Vlad Firoiu, Tim Harley, Iain Dunning, et al. 2018. Impala: Scalable distributed deep-rl with importance weighted actor-learner architectures. In International Conference on Machine Learning. ICML, 1407–1416.

- Farmer et al. (2005) J Doyne Farmer, Paolo Patelli, and Ilija I Zovko. 2005. The predictive power of zero intelligence in financial markets. Proceedings of the National Academy of Sciences 102, 6 (2005), 2254–2259.

- Friedman (2018) Daniel Friedman. 2018. The double auction market institution: A survey. In The Double Auction Market Institutions, Theories, and Evidence. Routledge, 3–26.

- Gao et al. (2022a) Kang Gao, Perukrishnen Vytelingum, Stephen Weston, Wayne Luk, and Ce Guo. 2022a. High-frequency financial market simulation and flash crash scenarios analysis: an agent-based modelling approach. arXiv preprint arXiv:2208.13654 (2022).

- Gao et al. (2022b) Kang Gao, Perukrishnen Vytelingum, Stephen Weston, Wayne Luk, and Ce Guo. 2022b. Understanding intra-day price formation process by agent-based financial market simulation: calibrating the extended chiarella model. arXiv preprint arXiv:2208.14207 (2022).

- Ghoulmie et al. (2005) Francois Ghoulmie, Rama Cont, and Jean-Pierre Nadal. 2005. Heterogeneity and feedback in an agent-based market model. Journal of Physics: condensed matter 17, 14 (2005), S1259.

- Gjerstad and Dickhaut (1998) Steven Gjerstad and John Dickhaut. 1998. Price formation in double auctions. Games and economic behavior 22, 1 (1998), 1–29.

- Gode and Sunder (1993) Dhananjay K Gode and Shyam Sunder. 1993. Allocative efficiency of markets with zero-intelligence traders: Market as a partial substitute for individual rationality. Journal of political economy 101, 1 (1993), 119–137.

- Gould et al. (2013) Martin D Gould, Mason A Porter, Stacy Williams, Mark McDonald, Daniel J Fenn, and Sam D Howison. 2013. Limit order books. Quantitative Finance 13, 11 (2013), 1709–1742.

- Grimm et al. (2006) Volker Grimm, Uta Berger, Finn Bastiansen, Sigrunn Eliassen, Vincent Ginot, Jarl Giske, John Goss-Custard, Tamara Grand, Simone K Heinz, Geir Huse, et al. 2006. A standard protocol for describing individual-based and agent-based models. Ecological modelling 198, 1-2 (2006), 115–126.

- Grimm et al. (2010) Volker Grimm, Uta Berger, Donald L DeAngelis, J Gary Polhill, Jarl Giske, and Steven F Railsback. 2010. The ODD protocol: a review and first update. Ecological modelling 221, 23 (2010), 2760–2768.

- Grimm et al. (2020) Volker Grimm, Steven F Railsback, Christian E Vincenot, Uta Berger, Cara Gallagher, Donald L DeAngelis, Bruce Edmonds, Jiaqi Ge, Jarl Giske, Juergen Groeneveld, et al. 2020. The ODD protocol for describing agent-based and other simulation models: A second update to improve clarity, replication, and structural realism. Journal of Artificial Societies and Social Simulation 23, 2 (2020).

- Haldane and May (2011) Andrew G Haldane and Robert M May. 2011. Systemic risk in banking ecosystems. Nature 469, 7330 (2011), 351–355.

- Hammond (1997) Peter J Hammond. 1997. Rationality in economics. Rivista internazionale di scienze sociali 105, 3 (1997), 247–288.

- Hasbrouck (2007) Joel Hasbrouck. 2007. Empirical market microstructure: The institutions, economics, and econometrics of securities trading. Oxford University Press.

- Hochreiter and Schmidhuber (1997) Sepp Hochreiter and Jürgen Schmidhuber. 1997. Long short-term memory. Neural computation 9, 8 (1997), 1735–1780.

- Hospedales et al. (2020) Timothy Hospedales, Antreas Antoniou, Paul Micaelli, and Amos Storkey. 2020. Meta-learning in neural networks: A survey. arXiv preprint arXiv:2004.05439 (2020).

- Hu et al. (2015) Yong Hu, Kang Liu, Xiangzhou Zhang, Lijun Su, EWT Ngai, and Mei Liu. 2015. Application of evolutionary computation for rule discovery in stock algorithmic trading: A literature review. Applied Soft Computing 36 (2015), 534–551.

- Inc. (2021a) Alpha Vantage Inc. 2021a. Alpha Vantage. https://www.alphavantage.co/

- Inc. (2021b) Alpha Vantage Inc. 2021b. Alpha Vantage API Documentation: Intraday (Extended History). https://www.alphavantage.co/documentation/#intraday

- Jacob Leal et al. (2016) Sandrine Jacob Leal, Mauro Napoletano, Andrea Roventini, and Giorgio Fagiolo. 2016. Rock around the clock: An agent-based model of low-and high-frequency trading. Journal of Evolutionary Economics 26 (2016), 49–76.

- Laine (2015) Tatu Laine. 2015. Quantitative analysis of financial market infrastructures: further perspectives on financial stability. (2015).

- le Calvez and Cliff (2018) Arthur le Calvez and Dave Cliff. 2018. Deep learning can replicate adaptive traders in a limit-order-book financial market. In 2018 IEEE Symposium Series on Computational Intelligence (SSCI). IEEE, 1876–1883.

- LeBaron (2001) Blake LeBaron. 2001. A builder’s guide to agent-based financial markets. Quantitative finance 1 (2001), 254–261.

- LeBaron (2006) Blake LeBaron. 2006. Agent-based computational finance. Handbook of computational economics 2 (2006), 1187–1233.

- LeBaron (2011) Blake LeBaron. 2011. Active and passive learning in agent-based financial markets. Eastern Economic Journal 37, 1 (2011), 35–43.

- Li et al. (2020) Junyi Li, Xintong Wang, Yaoyang Lin, Arunesh Sinha, and Michael Wellman. 2020. Generating realistic stock market order streams. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 34. AAAI, 727–734.

- Liang et al. (2017) Eric Liang, Richard Liaw, Philipp Moritz, Robert Nishihara, Roy Fox, Ken Goldberg, Joseph E Gonzalez, Michael I Jordan, and Ion Stoica. 2017. RLlib: Abstractions for Distributed Reinforcement Learning. arXiv preprint arXiv:1712.09381 (2017).

- Lo (2004) Andrew W Lo. 2004. The adaptive markets hypothesis. The Journal of Portfolio Management 30, 5 (2004), 15–29.

- Madhavan (2000) Ananth Madhavan. 2000. Market microstructure: A survey. Journal of financial markets 3, 3 (2000), 205–258.

- Malkiel and Fama (1970) Burton G Malkiel and Eugene F Fama. 1970. Efficient capital markets: A review of theory and empirical work. The journal of Finance 25, 2 (1970), 383–417.

- Marwala (2017) Tshilidzi Marwala. 2017. Rational Choice and Artificial Intelligence. arXiv preprint arXiv:1703.10098 (2017).

- McGroarty et al. (2019) Frank McGroarty, Ash Booth, Enrico Gerding, and VL Raju Chinthalapati. 2019. High frequency trading strategies, market fragility and price spikes: an agent based model perspective. Annals of Operations Research 282, 1 (2019), 217–244.

- Michaels and Osipovich (2020) Dave Michaels and Alexander Osipovich. 2020. Appeals Court Rules for Stock Exchanges in Fee Fight With SEC. https://www.wsj.com/articles/appeals-court-rules-for-stock-exchanges-in-fee-fight-with-sec-11592322391

- Networks (2021) Anova Financial Networks. 2021. Low Latency Financial Connectivity. https://anovanetworks.com

- O’hara (1997) Maureen O’hara. 1997. Market microstructure theory. Wiley.

- Paddrik et al. (2017) Mark Paddrik, Roy Hayes, William Scherer, and Peter Beling. 2017. Effects of limit order book information level on market stability metrics. Journal of Economic Interaction and Coordination 12, 2 (2017), 221–247.

- Pagan (1996) Adrian Pagan. 1996. The econometrics of financial markets. Journal of empirical finance 3, 1 (1996), 15–102.

- Potters and Bouchaud (2003) Marc Potters and Jean-Philippe Bouchaud. 2003. More statistical properties of order books and price impact. Physica A: Statistical Mechanics and its Applications 324, 1-2 (2003), 133–140.

- Preist and van Tol (1998) Chris Preist and Maarten van Tol. 1998. Adaptive agents in a persistent shout double auction. In Proceedings of the first international conference on Information and computation economies. ACM, 11–18.

- Rand and Wilensky (2006) William Rand and Uri Wilensky. 2006. Verification and validation through replication: A case study using Axelrod and Hammond’s ethnocentrism model. North American Association for Computational Social and Organization Sciences (NAACSOS) (2006), 1–6.

- Rollins and Cliff (2020) Michael Rollins and Dave Cliff. 2020. Which Trading Agent is Best? Using a Threaded Parallel Simulation of a Financial Market Changes the Pecking-Order. arXiv preprint arXiv:2009.06905 (2020).

- Sabzian et al. (2019) Hossein Sabzian, Mohammad Ali Shafia, Ali Maleki, Seyeed Mostapha Seyeed Hashemi, Ali Baghaei, and Hossein Gharib. 2019. Theories and practice of agent based modeling: Some practical implications for economic planners. arXiv preprint arXiv:1901.08932 (2019).

- Schmerken (2008) Ivy Schmerken. 2008. Quants Demand More Efficient Alpha Generation Technology Platform. https://web.archive.org/web/20110718225953/http://www.wallstreetandtech.com/asset-management/showArticle.jhtml?articleID=208808533 Accessed 2021-03-16.

- Schvartzman and Wellman (2009) L Julian Schvartzman and Michael P Wellman. 2009. Stronger CDA strategies through empirical game-theoretic analysis and reinforcement learning. In Proceedings of The 8th International Conference on Autonomous Agents and Multiagent Systems-Volume 1. International Foundation for Autonomous Agents and Multiagent Systems, 249–256.

- Securities and Commission (2005) US Securities and Exchanges Commission. 2005. Regulation National Market System. (2005). https://www.sec.gov/rules/final/34-51808.pdf

- Securities and Commission (2010) U.S. Securities and Exchanges Commission. 2010. Findings Regarding The Market Events of May 6, 2010. https://www.sec.gov/files/marketevents-report.pdf

- Securities and Commission (2021a) U.S. Securities and Exchanges Commission. 2021a. How to Submit Comments. https://www.sec.gov/rules/submitcomments.htm

- Securities and Commission (2021b) U.S. Securities and Exchanges Commission. 2021b. Tick Size Pilot Program. https://www.sec.gov/ticksizepilot

- Sewell (2011) Martin Sewell. 2011. Characterization of financial time series. Rn 11, 01 (2011), 01.

- Sirignano and Cont (2019) Justin Sirignano and Rama Cont. 2019. Universal features of price formation in financial markets: perspectives from deep learning. Quantitative Finance 19, 9 (2019), 1449–1459.

- Smith et al. (2003) Eric Smith, J Doyne Farmer, László Gillemot, and Supriya Krishnamurthy. 2003. Statistical theory of the continuous double auction. Quantitative finance 3 (2003), 481–514.

- Soramäki et al. (2006) Kimmo Soramäki, Morten L Bech, Jeffrey Arnold, Robert J Glass, and Walter E Beyeler. 2006. The Topology of Interbank Payment Flows. Federal Reserve Bank of New York: Staff Reports (2006).

- Sorensen et al. (2020) Erik Sorensen, Ryan Ozzello, Rachael Rogan, Ethan Baker, Nate Parks, and Wei Hu. 2020. Meta-Learning of Evolutionary Strategy for Stock Trading. Journal of Data Analysis and Information Processing 8, 2 (2020), 86–98.

- Stotter et al. (2014) Steve Stotter, John Cartlidge, and Dave Cliff. 2014. Behavioural investigations of financial trading agents using Exchange Portal (ExPo). In Transactions on Computational Collective Intelligence XVII. Springer, 22–45.

- Subramanian et al. (2006) Harish Subramanian, Subramanian Ramamoorthy, Peter Stone, and Benjamin J Kuipers. 2006. Designing safe, profitable automated stock trading agents using evolutionary algorithms. In Proceedings of the 8th annual conference on Genetic and evolutionary computation. ACM, 1777–1784.

- Talla Kuate (2016) Rodrigue Talla Kuate. 2016. Hierarchical reinforcement learning for trading agents. Ph.D. Dissertation. Aston University.

- Tesauro and Bredin (2002) Gerald Tesauro and Jonathan L Bredin. 2002. Strategic sequential bidding in auctions using dynamic programming. In Proceedings of the first international joint conference on Autonomous agents and multiagent systems: part 2. International Foundation for Autonomous Agents and Multiagent Systems, 591–598.

- Tesauro and Das (2001) Gerald Tesauro and Rajarshi Das. 2001. High-performance bidding agents for the continuous double auction. In Proceedings of the 3rd ACM Conference on Electronic Commerce. ACM, 206–209.

- Tivnan et al. (2020) Brian F Tivnan, David Rushing Dewhurst, Colin M Van Oort, John H Ring IV, Tyler J Gray, Brendan F Tivnan, Matthew TK Koehler, Matthew T McMahon, David M Slater, Jason G Veneman, et al. 2020. Fragmentation and inefficiencies in US equity markets: Evidence from the Dow 30. PloS one 15, 1 (2020), e0226968.

- Tivnan et al. (2017) Brian F Tivnan, Matthew TK Koehler, David Slater, Jason Veneman, and Brendan F Tivnan. 2017. Towards a model of the US stock market: How important is the securities information processor?. In 2017 Winter Simulation Conference (WSC). IEEE, 1181–1192.

- Van Oort (2018) Colin M. Van Oort. 2018. Market Efficiency in US Stock Markets: A Study of the Dow 30 and the S&P 30. Graduate College Dissertations and Theses (2018).

- Van Oort (2021) Colin M. Van Oort. 2021. Agent Based Market Microstructure Simulation. https://gitlab.com/computational-finance-lab/abmms Accessed 2021/04/20.

- Vives (1993) Xavier Vives. 1993. How fast do rational agents learn? The Review of Economic Studies 60, 2 (1993), 329–347.

- Vytelingum et al. (2008) Perukrishnen Vytelingum, Dave Cliff, and Nicholas R Jennings. 2008. Strategic bidding in continuous double auctions. Artificial Intelligence 172, 14 (2008), 1700–1729.

- Wah and Wellman (2016) Elaine Wah and Michael P Wellman. 2016. Latency arbitrage in fragmented markets: A strategic agent-based analysis. Algorithmic Finance 5, 3-4 (2016), 69–93.

- Wah et al. (2017) Elaine Wah, Mason Wright, and Michael P Wellman. 2017. Welfare effects of market making in continuous double auctions. Journal of Artificial Intelligence Research 59 (2017), 613–650.

- Wang et al. (2016) Jane X Wang, Zeb Kurth-Nelson, Dhruva Tirumala, Hubert Soyer, Joel Z Leibo, Remi Munos, Charles Blundell, Dharshan Kumaran, and Matt Botvinick. 2016. Learning to reinforcement learn. arXiv preprint arXiv:1611.05763 (2016).

- Wang and Wellman (2017) Xintong Wang and Michael Paul Wellman. 2017. Spoofing the limit order book: An agent-based model. In Workshops at the Thirty-First AAAI Conference on Artificial Intelligence.

- Wray et al. (2020) Aaron Wray, Matthew Meades, and Dave Cliff. 2020. Automated Creation of a High-Performing Algorithmic Trader via Deep Learning on Level-2 Limit Order Book Data. In 2020 IEEE Symposium Series on Computational Intelligence (SSCI). IEEE, 1067–1074.

- Xiang et al. (2005) Xiaorong Xiang, Ryan Kennedy, Gregory Madey, and Steve Cabaniss. 2005. Verification and validation of agent-based scientific simulation models. In Agent-directed simulation conference, Vol. 47. The European Modeling and Simulation Symposium, 55.

Appendix A ODD Protocol for ABMMS

Below we describe ABMMS following the Overview, Design concepts, Details (ODD) protocol (Grimm et al., 2006; Grimm et al., 2010; Grimm et al., 2020).

A.1. Purpose

The immediate goal of ABMMS is to evaluate the impact of market microstructure details and adaptive agents on the quality of data generated by an agent based financial market (ABFM). Phrased more explicitly, “Does the combination of detailed market mechanisms and adaptive learning agents create synergistic effects that improve the level of realism of data generated by an ABFM?” Beyond that, ABMMS is intended as a tool to evaluate the impacts of policy and design decisions in the US National Market System for equities (NMS). ABMMS primarily targets the NMS, but is designed to simulate arbitrary market configurations to allow for the investigation of a broad range of counterfactual scenarios.

A.2. Patterns

We evaluate ABMMS by its ability to reproduce the following patterns:

A.2.1. Stylized Facts of Asset Prices

ABMMS should produce asset price time series that satisfy stylized facts proposed by Cont (2001) and others. Replicating all of the 11 stylized facts proposed by Cont (2001) is difficult, especially considering the volume of data that is required to evaluate facts #1, #4, and #11, so we aim to replicate at least 4. Additionally, we found that facts #3 and #10 were difficult to detect when calibrating our stylized fact tests on real data. Therefore, replicating 4 stylized facts should be considered acceptable and replicating 6 stylized facts should be considered desirable.

A.2.2. Profits of Learning Agents

Simple agents may have positive or negative profits depending largely on the market conditions that they experience and random chance. However, learning agents should have positive expected profits, otherwise economic rationality would demand that they cease participation. This does not require that an agent have positive profit in any particular time window, or even over the entirety of a particular simulation run, only that an agent nets positive profit in the long run.

A.2.3. Daily Trading Activity

Financial markets tend to feature a smile shaped activity density curve at the trading day time scale. The start of the trading day features a burst of trading activity, which decays as the day goes on, as well as a ramp up of activity as the day reaches its close. There is no mechanism to generate such an activity curve when an ABFM is populated entirely with ZI or ZIP agents, beyond engineering such activity patterns into their trading behavior. However, when learning agents are introduced one possible mechanism for generating this activity distribution comes with them, and that is the opportunity cost associated with the market closure between trading days. To test for this pattern we can construct activity histograms for each trading day, with bins covering 10 second intervals, then test if the bins in the first and last 5 minutes of the trading day feature significantly more activity than other bins.

A.2.4. Dislocations

Tivnan et al. (2020) describe the occurrence of quote dislocations in the NMS. Since ABMMS is intended to model the NMS, we expect to observe similar quote dislocations in the data generated by it. The quote dislocations observed in ABMMS should have similar distributions of attributes to what was observed in the NMS. On average, stocks in the NMS can exhibit daily dislocation counts that fall anywhere between roughly 3000 and 16000, for thinly traded members of the Russell 3000 and members of the Dow 30 respectively (Dewhurst et al., 2019). When accounting for time of day, the occurrence distribution should have a smile-like shape, where more dislocations occur near the open and close of a trading day. Additionally, the duration distribution should be heavy tailed, with a tail reaching towards longer duration, and a mean between and s. The distribution of dislocation magnitudes should be heavy tailed, possibly a power law, with a greater frequency of small magnitude dislocations and an exceptionally long tail (Van Oort, 2018).

A.3. Entities

ABMMS features the following:

-

•

Simulation Driver: Orchestrates the execution of the simulation and manages global variables.

-

•

Communication Network (CN): Mediates interactions between agents.

-

•

Agent: An actor in the simulation. Agent classes can have heterogeneous roles and incentives. All agents share a set of common state variables that cover general information.

-

–

Exchange: Manage auctions that facilitate stock trading.

-

–

Securities Information Processor (SIP): Provides a signal to synchronize prices across a fragmented marketplace.

-

*

Limit Up-Limit Down Queue: Tracks historical trades in a time window to aid in calculating LULD bands.

-

*

-

–

Trader: Buys and sells financial instruments.

-

*

Zero Intelligence (ZI): Based on the agents developed by Gode and Sunder (1993), all trading decisions are selected randomly. One deviation is that we do not implement separate buyer and seller agents. Instead, each time a ZI agent is able to trade it randomly selects whether to act as a buyer or seller.

-

*

Minimum Intelligence (MI): Similar to ZI agents, but the width of the random price distribution is based on the spread of the NBBO, and orders are always sent to the exchange that holds the appropriate side of the NBBO.

-

*

ZI Plus (ZIP): Based on the agents developed by Cliff and Bruten (1997). Takes trading actions that are nearly as random as ZI agents, except that prices are determined by a belief function that is updated based on orders that result in trades.

-

*

Arbitrage: Attempts to profit by uncrossing distributed markets that are crossed.

-

*

Reinforcement Learning (RL): Learns a trading strategy via meta-reinforcement learning, leading to a more adaptive and free form strategy.

-

*

-

–

Observer: An aggregator that constructs consolidated data products.

-

–

-

•

Message: Information sent from one agent to another. All messages feature the same header information, while the body content varies based on the message type.

-

–

Add: A bid (buy interest) or offer (sell interest) has been added to an order book.

-

–

Modify (Mod): Shares have been removed from an order book without execution.

-

–

Trade: Shares have been removed from an order book due to execution.

-

–

Quote: The best bid or best offer at an exchange have updated.

-

–

National Best Bid and Offer (NBBO): The best bid or best offer across all exchanges in a market system have updated.

-

–

Limit Up-Limit Down (LULD) Bands: Range of valid trading prices for an asset.

-

–

Request: Traders may submit an add or mod request to an exchange. Requests may be rejected if they are malformed.

-

–

Receipt: Exchanges indicate the status of a request via a receipt that is sent exclusively to the sender of the request.

-

–

Trigger: Schedules the occurrence of a discrete event, such as a trade or an auction. Usually sent from an agent to itself, though this is not explicitly enforced.

-

–

SIP Message: Trade and Quote messages that pass through a SIP.

-

–

CNs represent the communication infrastructure through which all other agents interact. The core of an CN is the topology of the communication infrastructure, which is represented as an undirected graph. The nodes of the topology represent physical locations, and edges represent communication pathways between locations. Edges are weighted to represent a deterministic propagation delay associated with sending a message across that edge. An exponential random variable is added to the deterministic propagation delay, simulating other aspects of electronic communication systems, such as queuing delays or packet loss. All messages sent via the CN are subjected to a minimum delay, which primarily impacts messages sent between agents located at the same node. The state variables for CNs are summarized in Table S2.

Exchanges facilitate the trade of assets by matching buyers and sellers via an auction mechanism. The auction mechanism is implemented by the combination of an order book, which accumulates market state, and a matching engine, which matches incoming orders against those resting in the order book. Trading in multiple assets can be supported through the use of multiple independent order books. Exchanges may use transaction fees, also called market access fees or maker-taker fees, to monetize their activity. The state variables for exchanges are summarized in Table S4.

SIPs act as a synchronization mechanism by aggregating information across a fragmented market system and disseminating indicators. A SIP constructs several signals, including the national best bid and offer (NBBO), limit up-limit down (LULD) band indicators, as well as a trade and quote (TAQ) for each asset it is responsible for. The state variables for SIPs are summarized in Table S6. Each SIP tracks historical trades over a small time window in order to implement the Limit Up-Limit Down (LULD) mechanism. These trades are stored in a LULD Queue, which aids in the calculation of LULD bands. The state variables for LULD Queues are summarized in Table S7.

Traders buy, sell, and hold financial instruments by interacting with other traders via an exchange. Each trader tracks the state of its holdings, the amount of each traded asset, plus cash, that it possesses. Additionally, each trader implements a strategy for placing bids and offers. The state variables for Traders are summarized in Tables S8–S11.

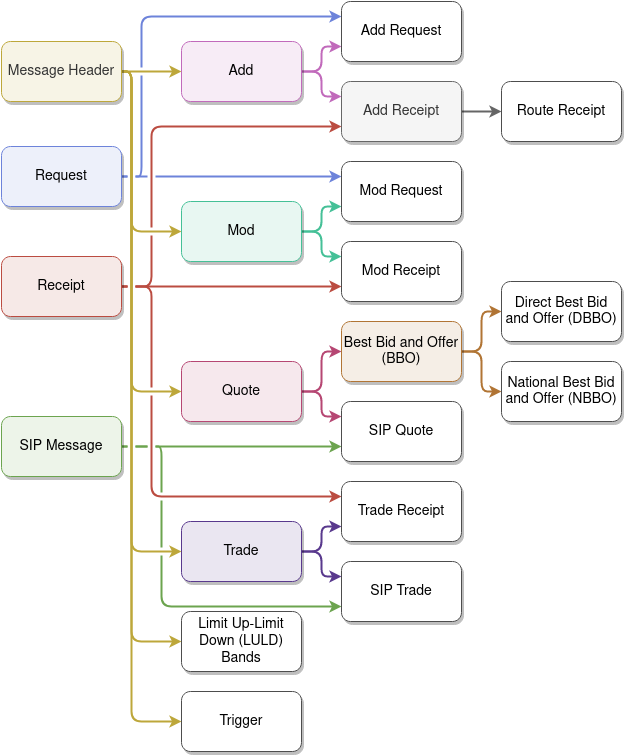

ABMMS implements a variety of message types, whose relationships are summarized in Figure S1. The state variables for each message type are summarized in Tables S12–S20.

A.4. State Variables

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Global Clock | Timestamp, dynamic; s | Time keeper for the simulation. |

| Simulation Start | Timestamp, static; s | The Global Clock is set to this at the start of the simulation. |

| Simulation End Time | Timestamp, static; s | The simulation is terminated if the Global Clock reaches or passes this. |

| Communication Network | CN, static | Communication infrastructure that mediates agent interactions. See Table S2 for more details. |

| Agents | List[Agent], static | Agents that populate this simulation. See Table S3 and related Tables for more details. |

| Trading Symbols | List[String], static | Identifiers for the stocks that will be traded in this simulation. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Topology | Undirected Graph, static | Nodes represent physical locations that other agents might inhabit. Edges represent communication channels between locations. Weights on edges indicate the magnitude of deterministic propagation delays associated with communication along each edge. |

| Minimum Delay | Integer, static; s | The minimum delay imposed on all communications. Primarily impacts messages passed between agents located at the same node in the CN. |

| Mean Delay Noise | Float, static; s | Scale parameter for an exponential random variable that is used to create stochastic communication delays. |

| Message Queue | Sorted Queue, dynamic | Contains the messages that have been sent into the CN, but not yet arrived. Always sorted such that the first element of the queue is the next message that will arrive at its destination. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Identifier | String, static | A unique identifier, or name, that is used to refer to this agent. |

| Location | Categorical, static | A node in the CN where this agent is located. |

| Clock | Timestamp, dynamic; s | A local clock. A copy of the global simulation clock by default. |

| Trading Symbols | List[String], static | Identifiers of stocks that this agent may interact with. |

| Subscribers | List[Agent], dynamic | Agents subscribed to the broadcast feed of this agent. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Agent State Variables | N/A | See Table S3 for more details. |

| Order Books | Dict[String, Order Book], static | Mapping from Trading Symbols to their associated Order books (Table S5). |

| Matching Engine | Matching Engine, static | Strategy for matching incoming orders with resting orders. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Trading Symbol | String, static | Orders are managed for this trading symbol. |

| Bid Priority | Ordering Function, static | Defines an ordering for the execution priority of bids. |

| Bids | List[Add Request], dynamic | List of Bid Requests that have been accepted, but not executed. Sorted according to Bid Priority. |

| Offer Priority | Ordering Function, static | Defines an ordering for the execution priority of offers. |

| Offers | List[Add Request], dynamic | List of Offer Requests that have been accepted, but not executed. Sorted according to Offer Priority. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Agent State Variables | N/A | See Table S3 for more details. |

| LULD Queues | Dict[String, LULD Queue], static | Map from trading symbols to LULD Queues. One LULD Queue for each trading symbol that this SIP is responsible for. See Table S7 for more details. |

| Round Lot Size | Integer, static; shares of stock | How many shares must be associated with a quote for it to be considered a round lot, and thus eligible for inclusion in the NBBO. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Trading Symbol | String, static | LULD bands are managed for this trading symbol. |

| LULD Reference Price | Integer, static | Initial reference price for the LULD bands. |

| LULD Window | Timedelta, static; s | Length of the time window used to select recent trades. |

| LULD Percentage | Float, static; percent | Half the width of the LULD bands as a fraction of the reference price. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Agent State Variables | N/A | See Table S3 for more details. |

| Holdings | Dict[String, Integer or Float], dynamic; Shares of stock or $0.0001 | Mapping from asset identifiers to possessed asset quantities. |

| Pending Orders | Dict[Integer, Message], dynamic | Mapping from order identifiers to orders that have been submitted to an exchange and have an unknown status. |

| Active Orders | Dict[Integer, Message], dynamic | Mapping from order identifiers to orders that have been placed into an order book on an exchange. |

| NBBOs | Dict[String, NBBO], dynamic | Mapping from trading symbols to the current NBBO for that trading symbol. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Trader State Variables | N/A | See Table S8 for more details. |

| Maximum Limit Prices | Dict[String, Integer], dynamic; $0.01 | Maximum prices for submitted limit orders, one for each traded stock. |

| Minimum Limit Prices | Dict[String, Integer], dynamic; $0.01 | Minimum prices for submitted limit orders, one for each traded stock. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Trader State Variables | N/A | See Table S8 for more details. |

| Profit Margins | Dict[String, List[Float]], dynamic | Mapping from trading symbols to pairs of profit margins, one for bids and one for offers. |

| Limit Prices | Dict[String, Integer], dynamic | Mapping from trading symbols to the worst price that the agent is willing to transact at. |

| Target Prices | Dict[String, List[Integer]], dynamic | Mapping from trading symbols to target prices used to update the profit margins. |

| Momentum Values | Dict[String, Float], dynamic | Mapping from trading symbols to current momentum values. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Trader State Variables | N/A | See Table S8 for more details. |

| DBBOs | Dict[String, DBBO], dynamic | Mapping from Trading Symbols to their current Direct Best Bid and Offer (DBBO). |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message ID | Integer, static | Identifier associated with this message. |

| Related ID | Integer, static | Optional identifier of a related message. |

| Sender ID | String, static | Identifier of the agent that sent the message. |

| Recipient ID | String, static | Identifier of the intended recipient. |

| Send Time | Timestamp, static; s | When the message was sent. |

| Receive Time | Timestamp, static; s | When the message will be received. |

| Trading Symbol | String, static | Indicates what Trading Symbol this message is associated with. |

| Random | Float, static | Value drawn from a distribution. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Sequence Number | Integer, static | Identifier applied by an exchange to indicate the processing order of requests. |

| Order Type | Categorical, static | Limit, market, or midpoint order. |

| Side | Categorical, static | Bid or offer. |

| Shares | Integer, static | Quantity of shares to be bought or sold. |

| Limit Price | Integer, static; $0.01 | Highest acceptable bid price, or lowest acceptable offer price. |

| All or Nothing | Boolean, static | Indicates that this order should execute in its entirety, or not at all. |

| Hidden | Boolean, static | Indicates that this order should not be displayed if placed in an order book. |

| ISO | Boolean, static | Indicates that this order is part of an inter-market sweep, and that standard execution price protections are waived. |

| Time in Force | Duration, static; s | Amount of time that this order should rest in a limit order book before it is cancelled by the exchange. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Sequence Number | Integer, static | The Sequence Number of a resting order. |

| Side | Categorical, static | The Side (bid or offer) of the resting order. |

| Shares to Remove | Integer, static | Quantity of shares to be removed from the resting order. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Price | Integer, static; $0.01 | Execution price of the trade. |

| Shares | Integer, static | Quantity of shares exchanged. |

| Triggering Side | Categorical, static | Side of the active order. |

| ISO | Boolean, static | Whether the active order was an Inter-market Sweep. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Bid Price | Integer, static; $0.01 | Highest price among bids in an order book. |

| Bid Shares | Integer, static | Quantity of shares associated with the highest priced bid. |

| Offer Price | Integer, static; $0.01 | Lowest price among offers in an order book. |

| Offer Shares | Integer, static | Quantity of shares associated with the lowest priced offer. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Quote | N/A | See Table S16 for details. |

| Bid Exchange | String, static | Identifier of the exchange that holds the National Best Bid. |

| Offer Exchange | String, static | Identifier of the exchange that holds the National Best Offer. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Upper Band | Integer, static | Highest eligible trade price. |

| Lower Band | Integer, static | Lowest eligible trade price. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Success | Boolean, static | Indicates whether a request was successful or not. |

| Reason | String, static | Optional error message indicating why a request failed. |

| Variable Name | Variable Type and Units | Meaning |

|---|---|---|

| Message Header | N/A | See Table S12 for details. |

| Trigger Event | Categorical, static | What event should be triggered, Auction or Trade. |

A.5. Scales

The minimum observable time increment of ABMMS is 1 s, though the simulation “step size” is variable and based on scheduled events. The model is usually run in segments of 1 trading day (6.5 hours), 5 trading days (1 trading week), or 20 trading days (1 trading month). Spatial relationships are not explicitly represented, though they appear implicitly in the CN, where propagation delays are estimated based on properties of fiber optic communication technology and geographic locations of real world data centers (Tivnan et al., 2020). The round lot size is 100 shares, and is used to filter quotes when constructing an NBBO, but odd lots are not restricted. The minimum tick size for prices of quotes is $0.01, trades can occur in $0.001 increments, and maker-taker fees are in increments of $0.0001.

All scales present in ABMMS are selected with the intent to model the NMS as closely as possible. The round lot size and minimum price increments are directly taken from regulation and documentation of NMS participants. The most subjective choice is the minimum time increment of 1 s, which allows for accurate modeling of most trading processes. However, if agent response times were to be accurately modeled, a smaller minimum increment (i.e. 1 ns) may be needed, since exchanges and some high frequency trading strategies may have faster response times than 1 s.

A.6. Process overview

ABMMS is event-driven, with discrete events occurring in fine-grained, but discrete time. To initiate a simulation, a start method is called for each agent, allowing it to perform setup actions at run time and schedule initial trading actions. The results of these start methods form the seed of the event-driven simulation, where messages are processed in increasing order of time of receipt. Each agent has its own strategies for how it reacts to particular message types, but generally all state variables are updated asynchronously. The only variable that is updated synchronously is the global clock, which is shared by all agents in a simulation. The existence of a single global clock removes the possibility of clock synchronization issues, which is a prevalent and difficult problem in distributed high frequency systems. Events are processed sequentially until there are no remaining events to process or the simulation termination time is reached.

All agents in ABMMS respond to messages, which indicate state changes in other agents or that a scheduled discrete event should occur.

Agent behaviors fall into one of two classes: planned and reactive. Planned behaviors are triggered by a message sent from the agent to itself, with the intent of performing a certain action at a specific time. For example, an agent may decide that it would like to submit an order to an exchange in five minutes, and schedule this planned action using a trigger message.

Reactive behaviors are triggered by messages sent to the agent from elsewhere in the system. For example, suppose an arbitrage trader receives a new quote from an exchange that indicates a crossed market state. The arbitrage trader then reacts by sending orders to the two exchanges involved in the cross, intending to be the counterparty to the bid at one exchange and the offer at another.

A.6.1. CN Processes