SMSM References

Learning Multi-Frequency Partial Correlation Graphs

Abstract

Despite the large research effort devoted to learning dependencies between time series, the state of the art still faces a major limitation: existing methods learn partial correlations but fail to discriminate across distinct frequency bands. Motivated by many applications in which this differentiation is pivotal, we overcome this limitation by learning a block-sparse, frequency-dependent, partial correlation graph, in which layers correspond to different frequency bands, and partial correlations can occur over just a few layers. To this aim, we formulate and solve two nonconvex learning problems: the first has a closed-form solution and is suitable when there is prior knowledge about the number of partial correlations; the second hinges on an iterative solution based on successive convex approximation, and is effective for the general case where no prior knowledge is available. Numerical results on synthetic data show that the proposed methods outperform the current state of the art. Finally, the analysis of financial time series confirms that partial correlations exist only within a few frequency bands, underscoring how our methods enable the gaining of valuable insights that would be undetected without discriminating along the frequency domain.

Index Terms:

Partial correlation graph, multi-frequency, block-sparsity, nonconvex optimization.I Introduction

Learning dependencies between time series is a fundamental data-analysis task with widespread application across many domains. For instance, in finance, models for portfolio allocation and risk assessment [1] rely on the study of linear dependencies between the time series of asset returns. These dependencies may vary not only over time, but also over multiple temporal resolutions, or frequency bands, which have different importance depending on the investment horizon of the portfolio manager. Similarly, in neuroscience, fMRI scanning of the brain measures time series of neural activity in different brain regions of interest (ROIs). A large and growing body of research [2] tackles the study of the brain as a network – or better, a correlation graph – where an arc between two ROIs (nodes) is created by learning the linear dependencies of the time series associated with the two ROIs. Also in this case, such dependencies might occur at different temporal resolutions [3, 4, 5]. Consider, for example, resting-state fMRI, where although the brain is at rest, it exhibits a rich functional activity composed of fluctuations over low-frequency bands in blood oxygen level-dependent signals (see [6], and references therein). When instead the brain is subject to stimuli or performs any tasks, the related functional connectivity occurs at different frequency bands [7, 8]. Thus, the ability to capture conditional dependencies occurring at frequency bands relevant to the application context is crucial in retrieving conditional dependencies between brain regions related to different brain states, and is motivated also by other application domains, ranging from biology [9] to climatology [10].

Related works. Learning linear conditional dependencies among time series is a well-known problem in statistical learning [11, 12, 13]. Given a set of time series, the goal is to assess the dependencies between any pair of them, conditioned on the linear effects of others. These dependencies, referred to hereinafter as partial correlations, are typically represented through a partial correlation graph (PCG), where the time series are the nodes, and the partial correlations are undirected arcs. Here, the lack of an arc between two nodes indicates that the corresponding time series are linearly statistically independent, conditioned on all the possible instantaneous and lagged linear effects of the other time series. Partial correlations between time series relate to the zeros of the inverse of the cross-spectral density (CSD) matrices, as established in Theorem 2.4 in the seminal work of [14]. The information provided by the inverse CSD for time series is analogous to that provided by the precision matrix for i.i.d. random variables. This analogy has contributed to the development of techniques that generalize the results obtained for the precision matrix [15, 16, 17, 18, 19] to the time series context. Some authors propose shrinkage estimators for the CSD matrices motivated by applications in neuroscience [20, 21, 22], building upon the shrinkage framework proposed by [23] for data-driven -penalised estimation of the spectral density matrix. Another stream of research focuses on learning the PCG under sparsity constraints. Specifically, the paper in [24] studies a fixed-sample high-dimensional setting, and proposes a method related to the method of constrained -minimization for inverse matrix estimation (CLIME, [25]). Other approaches [26, 27, 28, 29] leverage the Whittle approximation (WA, [30, 31]) for Gaussian stationary processes.

Regarding these previous works, we highlight three major limitations. Firstly, existing methodologies focus on learning PCGs without the possibility of discriminating across different frequency bands, while this is important in many applications (as discussed above). Secondly, techniques based on WA might be ineffective in case of violation of Gaussianity assumption, high cross-correlation between time series, or small sample setting. As pointed out by [32] and subsequent experimental evidence [33, 34], WA leads to unreliable results in these scenarios. Thirdly, existing methods take estimated CSD matrices as input and keep them unaltered during learning. Thus, the goodness of the solution heavily depends on the accuracy of the CSD matrices estimation.

Contributions. This paper proposes methods to learn partial correlations between time series across multiple frequency bands, overcoming the three major limitations of the state of the art described above. For what concerns the first limitation, we propose the learning of a frequency-dependent PCG, where different layers correspond to different frequency bands, and where partial correlations can possibly occur only over some frequency bands. Aiming for general settings, our proposals do not rely upon WA, thus avoiding the second limitation. To overcome the third limitation, we introduce a novel methodology that jointly learns the CSD matrices and their inverses, without specifically hinging on some predefined CSD estimators. To be more specific, our proposal comprises two methods based on different assumptions. For the case where prior domain knowledge about the number of partial correlations between time series is available, we expose a problem formulation (Section V) that has a closed-form solution and builds upon theoretical results in the compressed sensing literature [35]. For the general case where such prior knowledge is not available, we formulate an optimization problem (Section VI) to jointly learn the CSD matrices and their inverses, and we devise an iterative solution of this problem based on successive convex approximation methods (SCA, [36]). In the rest of the paper, for simplicity, we dub the former method CF (for “closed-form”) and the latter method IA (for “iterative approximation”). Our methods have broad applicability as they are not limited by any particular statistical model, enabling a more general approach for learning partial correlations between time series across different frequency bands. Our experimental assessment on synthetic data (Section VII) demonstrates the superiority of our proposals over the baselines. We also present a real-world case study in the financial domain (Section VIII), confirming that in real-world time series, partial correlations might either concentrate at a certain frequency band or spread across multiple frequencies. This highlights the importance of learning block-sparse multi-frequency PCGs and shows that our methodology can help in extracting richer information from data. Overall, our proposals offer an important contribution to the field of time series analysis and have potential for applications in various domains.

Roadmap. The paper is organized as follows. Section II introduces key concepts while Section III the spectral properties of interest and their naive estimators. Next, Section IV describes the learning problem, tackled through the formulation and solution of two nonconvex problems, detailed in Sections V and VI, respectively. Then, Section VII addresses the empirical assessment of the proposed algorithms on synthetic data, while Section VIII showcases the application on financial time series. Finally, Section IX draws the conclusions.

Notation. Scalars are lowercase, , vectors are lowercase bold, , matrices are uppercase bold, , and tensors are uppercase sans serif, . The set of integers from to is denoted by , and if zero is included. The floor of is . The imaginary unit is . The conjugate of is , and the conjugate transpose is (the same for matrices). The complex signum is . is the identity matrix of size , is the matrix of ones, is the strictly lower triangular matrix of ones. The entry indexed by row and column is , is the diagonal matrix having as diagonal the vector , and , denotes the vectorization of formed by stacking the columns of into a single column vector. The set of positive definite matrices over is denoted by . The mixed norm is , where are the columns of . Additionally, the norm is the number of nonzero columns of , the norm is the Frobenious norm , is the largest singular value of , and is the element-wise infinity norm. Given a -way tensor indexed by , , and , the fiber is denoted as . The Kronecker product is . Finally, given a closed nonempty convex set , the set indicator function is defined as

II Conditional linear independence over frequency bands

In this section, we briefly recall the main results from [14] about the partial correlation between multivariate time series, expressed in the frequency domain, as they will be used later on in this paper. Consider an -variate, zero-mean, weakly-stationary process . The autocovariance function reads as the following matrix-valued function

| (1) |

with . Assuming that , the cross-spectral density function is the following matrix-valued function over :

| (2) |

with ; while we denote its inverse as . Since is Hermitian for all , also is Hermitian; furthermore, since is real-valued. Thus, we can focus only on . According to Theorem 2.4 in [14], rescaling leads to the partial spectral coherence, , where is a diagonal matrix with entries . Let us consider, w.l.o.g., and . Define , and consider the best linear prediction of and in terms of the time series in , i.e.,

| (3) | ||||

| (4) |

where ; are possible models mismatch; and is the convolution operation. Now, let us denote with the Fourier transform at frequency . From (3), applying the Fourier transform, we obtain:

| (5) | ||||

where we exploit the linearity of Fourier transform, and the convolution theorem. Similarly, from (4) we obtain:

| (6) |

The measure of linear dependence between and is , which coincides with the partial cross-spectrum [14]. From eq. (2.2) in [14], we have that iff . Given the definition of , implies no correlation between and once they have been bandpass filtered at frequency , after removing the linear effects of (for all lags ). Consequently, if , and are linearly independent conditionally on over the frequency band . This key concept leads to Definition 1 in Section IV.

III Estimation of Inverse CSD Tensor

In this section, we introduce the basic tools for the estimation of the CSD tensor and its inverse from time series data, defined below. Consider a set of time series, denoted as , where represents the number of samples in the data set and represents the number of time series. The data set comprises samples of an -variate, zero-mean, and weakly stationary process, denoted as for . Since in the finite sample setting, we denote the CSD matrix at rescaled frequency , as , and its inverse as , which we assume to exist. Similarly to Section II, and are Hermitian and symmetric; thus we focus only on positive frequencies .

Let us now introduce the CSD tensor consisting of slices of size by , where each slice represents the CSD matrix corresponding to a certain frequency. To streamline notation, hereinafter we omit the subscript in collections indexed by . An estimator of the CSD tensor is the periodogram, , defined as the discrete Fourier transform (DFT) of the sample autocovariance , defined as the collection of the matrices

for , where . Specifically, is the collection of the matrices , having entries

It is well known that the periodogram is not a consistent estimator of the CSD tensor [24]. A common remedy is to smooth it, also in high-dimensional fixed-sample settings (Theorem 3.1 in [24]). Then, we denote the smoothed periodogram by . Then, we obtain the naive estimator of the inverse CSD tensor, , such that . Finally, we have the partial spectral coherence estimator , where is a diagonal matrix with entries , [14].

IV Problem statement

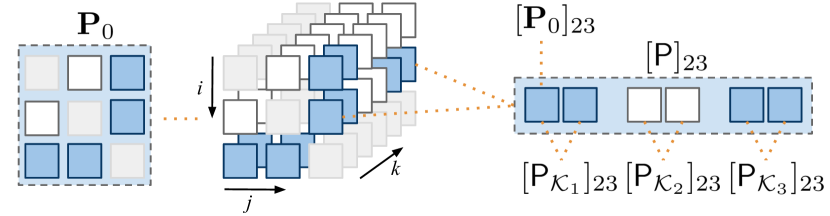

In this section, we state our learning problem, introducing the definition of multi-frequency partial correlation graph, where each layer refers to a different frequency band. Consider as input the data set mentioned above, and let us focus on the frequencies . We partition the frequency range into consecutive blocks of interest denoted as , where and . The starting frequency index of block is denoted by , and corresponds to the frequency band . We refer to the tensor collecting the inverse CSD matrices over as . Clearly, the inverse CSD tensor is equivalently given by . As a pictorial example, Figure 1 depicts the inverse CSD tensor and its components. In light of Section II, we introduce the multi-frequency partial correlation graph made of independent layers.

Definition 1 (-frequency Partial Correlation Graph).

The -frequency Partial Correlation Graph (-PCG) is a graph composed of independent layers, where the -th layer is an undirected graph associated to the frequency band , such that , and .

According to Definition 1, the presence of an arc depends on the values of within , which must be different from zero over at least one frequency component. Thus, if the arc is absent for every recovered graph , time series and are not partially correlated [14]. We say that a -PCG is block-sparse if partial correlations (i.e., arcs) exist only over some frequency bands . Then, driven by Definition 1 and the above considerations, in this work we aim to find a block-sparse graph representation associated with each frequency band in a data-driven manner, without any assumptions about the underlying statistical model. We aim to develop an approach that is robust to possible numerical fluctuations and is applicable even when . In the sequel, we formulate this problem mathematically according to two different criteria (cf. Sections V and VI, respectively), imposing block-sparsity in the estimate of the inverse CSD tensor along the frequency domain.

V The closed-form (CF) method

Let us assume that the true inverse CSD tensor is block-sparse over distinct blocks. Further, we consider the number of unique nonzero off-diagonal fibers (mode-) within each frequency band equal to for all , with . Note that, since the true inverse CSD is Hermitian, the number of nonzero off-diagonal fibers can only be even. As per Definition 1, the tensor entails a -PCG that has arc sets with cardinality , .

The rationale behind our proposal is to interpret the naive estimator (cf. Section III) as a noisy measurement of the true block-sparse inverse CSD tensor . As a consequence, if we further assume to have prior knowledge about the sparsity values , , we can cast the learning of the -PCG as a block-based signal recovery problem [35]. In particular, let us focus on a specific frequency band . We denote the flattening (a.k.a. matricization) of the true inverse CSD tensor , along the frequency interval , as . Here, each column of the matrix , i.e., with , contains the entries of the inverse CSD matrices . Thus, the block-sparsity assumption on the -PCG coincides with having only columns of to be not entirely equal to zero (cf. Definition 1). In addition, since the true inverse CSD is Hermitian, the columns of satisfy , which means that half of the information in is redundant and can be neglected in our formulation. To this end, let us consider the selection matrix , where is the vectorization of . The product retains only the columns of corresponding to the strictly lower diagonal fibers of , which contain all the information needed to learn the arc set with cardinality .

Finally, let be the flattening of the naive estimator . Then, we can cast our learning problem as the search for the -block-sparse matrix that approximates , for each ,

| (P1) | ||||

| subject to |

Problem (P1) is nonconvex due to the block-sparsity inducing constraint on the norm. Nevertheless, following the results in [35, 37], (P1) admits a closed-form (globally optimal) solution. Specifically, for each , the best -block-sparse approximation can be recovered by simply sorting the columns of according to their -norm and then retaining the top- columns. The selected columns are associated with the lower-diagonal fibers of , and are sufficient to identify the arc set with cardinality . Finally, if needed, the remaining structure of , i.e., the one associated with diagonal and upper-diagonal fibers of , can be simply obtained copying the diagonal of and taking the conjugate of , respectively. All the steps of the proposed method, named CF, are given in Algorithm 1.

Computational cost. For each block of frequencies , we compute the -norm of terms, each consisting of multiplications and additions. Therefore, these operations require flops. Afterward, we choose the top- largest terms, with a cost .

Hence, the cost for each block is .

VI The iterative approximation (IA) method

The CF method in Section V hinges on prior knowledge about the sparsity measure , which is hardly available in practical scenarios. In this section, we propose a method that does not exploit such prior information. In addition, differently from the CF method in Section V, here we do not consider the CSD tensor estimate as fixed during the learning process, but we jointly learn the CSD tensor and its inverse, which we denote as and , respectively. To this aim, since is an open set that is difficult to handle with iterative optimization methods, we first introduce an approximation of given by the closed set

| (7) |

where can be chosen sufficiently small to well approximate . Also, let be the closed set of vectorized matrices in (7). In second place, hinging on Definition 1, we notice that only the cross-interaction fibers , might yield arcs in the corresponding layer of the learned -PCG. Then, similarly to (P1), we introduce the selection matrix , , being the vectorization of the matrix . The product sets to zero the diagonal terms of the slices , and we can then enhance sparsity only over the off-diagonal fibers of . Then, to learn the -PCG, we formulate the following optimization problem:

| (P2) | ||||

| subject to |

The first term in the objective function of (P2) enforces to be the inverse of over the frequency domain. Indeed, the first term vanishes if is the inverse of . The second term of the objective in (P2) promotes block-sparsity on frequency bands (i.e., block-sparsity on the columns of , for all ), in accordance with our assumption. Here, is a regularization parameter. The inequality constraints in (P2) constrain each slice of the estimate of the CSD matrices to be close to the corresponding slice of the smoothed periodogram (cf. Section III). As a result, the matrices learned by our method can deviate from the smoothed periodogram during the learning process. The magnitude of this deviation is controlled by , which represents a tuning parameter. Finally, to ensure that the learned matrices are Hermitian and positive-definite, we optimize and over defined in (7).

Unfortunately, (P2) is nonconvex due to the presence of the bi-linear terms in the objective function. To handle its non-convexity, in the sequel, we adopt an efficient algorithmic framework based on inner convex approximation (NOVA, [38]) schemes, which can be thought as a generalization of [39]. The proposed algorithm finds a (local) solution of the original nonconvex problem (P2) by solving a sequence of strongly convex subproblems, where the original nonconvex objective is replaced by an appropriate (strongly) convex approximation, which is detailed in the sequel for our case. NOVA is suitable for distributed optimization, ensures feasibility at each iteration, and convergence to stationary points is guaranteed under mild assumptions [38].

VI-A Building the strongly convex surrogate problem

The first step of the NOVA framework entails the definition of a proper strongly convex surrogate problem, which approximates (P2) around a given point. To this aim, let us denote the bilinear function in (P2) as:

| (8) |

Then, we proceed designing a strongly convex surrogate for the nonconvex term in (8), satisfying some analytical conditions [38]. Let us define for , and let be the iterate at time . Now, taking into account the separability over and hinging on the bilinear structure of (8) (see [38]), we define the (strongly) convex surrogate function around the point :

| (9) | ||||

with . It is easy to see that the surrogate in (9) is strongly convex and satisfies

which, using the Wirtinger calculus [40] and considering that Equations 8 and 9 are real functions, guarantees first-order optimality conditions, i.e., every stationary point of in (9) is also a stationary point of the nonconvex objective function in (8). Let us now rewrite (9) and then (P2) in an equivalent form, which is more convenient for our mathematical derivations. Specifically, given two matrices and , the vectorization of their product reads as

| (10) |

Thus, using (10) in (9), and exploiting the equivalence of the element-wise infinity norm, we obtain

| (11) | ||||

Then, we conveniently rewrite the block-sparsity inducing term in the objective of (P2) as:

| (12) |

where follows from the definition of the -norm (cf. Section I), where the -th block of corresponds to the -th column of , for all ; and simply follows from the application of (10b), having introduced . Finally, using (11) and (VI-A), we apply the NOVA framework replacing the original nonconvex problem (P2) with a sequence of strongly convex subproblems that, at each iteration , read as:

| () | ||||

| subject to |

The NOVA iterative procedure then follows from computing the (unique) solution of (), i.e., and , and then smoothing it by using a diminishing stepsize rule [38]. Interestingly, the surrogate problem () is separable over and . Therefore, () can be split into two convex subproblems, one involving , the other . These two subproblems could be solved using off-the-shelf solvers for convex optimization, e.g., [41, 42]. However, this approach can be computationally demanding, especially when the size of the involved variables becomes moderately large. Thus, to reduce the overall computational burden of our algorithm, we solve the two subproblems inexactly by combining the NOVA framework [36] and the alternating direction method of multipliers (ADMM, [43]). Specifically, instead of finding the exact solutions of Problem (), we perform an inexact update by performing one ADMM iteration on the two convex subproblems involving and , respectively. The clear advantage is that the recursions of the inner ADMM are given in closed-form (cf. Algorithm 2, Sections VI-B and VI-C), and are amenable for parallel implementation, thus largely reducing the overall computation burden. Furthermore, our approach falls within the framework of inexact NOVA, whose convergence properties have been studied in [38]. In the sequel, we will provide a detailed derivation of the (single) ADMM recursion needed to solve the two subproblems.

VI-B Subproblem in

We start from the subproblem in . From (), (11), and exploiting the indicator function of (7) (useful to induce the positive definiteness of the slices ), we have to solve

| () | ||||

To deal with the non-smooth terms associated with the -norm, the indicator function, and the sum of -norms in (), we introduce three (sets of) splitting variables. The first, , handles the -norm and is defined as

| (13) |

The second, , handles the indicator function and reads as

| (14) |

The third, , , handles the sum of -norms in (), and is given by

| (15) |

Now, using (13)-(15) in (), we obtain the equivalent problem

| () | ||||

| subject to | ||||

The scaled augmented Lagrangian of () reads as [43]:

| (16) | ||||

The additional strongly convex terms in (16) have as penalty parameters , all belonging to , and as scaled dual variables the sequence of vectors , , and , with . Then, ADMM proceeds by searching a saddle point of the scaled augmented Lagrangian in (16), through the following recursions [43]:

| (S1) | ||||

Interestingly, the first, second, third, and sixth steps in (S1) can be derived in closed-form, as we show in the next paragraphs.

VI-B1 Solution for the first update

Proof.

See Appendix A. ∎

VI-B2 Solution for the second update

From (16), letting

| (18) |

the update for in (S1) reads as

| (19) |

where in (VI-B2) denotes the proximal operator of the infinity norm [43]. In particular, the result of the proximal operator in (VI-B2) can be found explicitly by hinging on the following lemma.

Lemma 2.

For any norm function on , it holds

with , , and denoting the projection operator onto the unit ball of the dual norm .

Proof.

This directly follows from Moreau decomposition [44]:

with , , and being the projection operator onto the unit ball of the dual norm . ∎

VI-B3 Solution for the third update

Here, we first derive the solution in matrix form, and then we vectorize it. From (16), letting , with being the matrix representation of , the update for in (S1) is given by

| (21) | ||||

From [44], the solution of (21) corresponds to projecting the Hermitian matrix onto , where the projection reads as

| (22) | ||||

Finally, we set

| (23) |

VI-B4 Solution for the sixth update

VI-C Subproblem in

In this case, from () and (11), we have to solve

| () |

Analogously to (), we exploit to induce positive definiteness of the slices . Now, to manage the non-smooth terms in (VI-C), we introduce two (sets of) splitting variables. The first, , is given by

| (28) |

The second, , is defined as

| (29) |

Thus, using (28) and (29) in (VI-C), we equivalently get

| () | ||||

| subject to | ||||

Considering for the moment only the equality constraints, the (scaled) augmented Lagrangian of () reads as

| (30) |

where and are penalty parameters; and are the scaled dual variables associated with the first and second equality constraints in (). Using the ADMM principle, we proceed looking for a saddle point of the augmented Lagrangian in (VI-C) that satisfies also the inequality constraints in () [43, 45]. Since (VI-C) is fully separable over , we get the recursions below for each :

| (S2) | ||||

Interestingly, the first, second, and third updates in (S2) can be evaluated in (quasi-)closed-form, as we illustrate in the sequel.

VI-C1 Solution for the first update

Starting from (VI-C), the first subproblem in (S2) reads as:

| (S2.1) |

Starting from (VI-C1), we build the related Lagrangian

| (31) |

where is the dual variable related to the inequality constraint in (VI-C1). Thus, exploiting (VI-C1), we compute jointly and by solving the Karush-Kuhn-Tucker (KKT) conditions of (VI-C1), which read as [45]:

| (32) | ||||

The first condition in (32) imposes primal optimality, while the second one is a variational inequality encompassing complementary slackness, primal and dual feasibility. From (VI-C), imposing the first condition in (32), we get

| (33) | ||||

Thus, exploiting the property of the Kronecker product in (33), and letting

| (34) |

with denoting the set of positive semidefinite block-diagonal matrices on , we obtain

| (35) | ||||

Then, we proceed as follows. First, we check whether satisfies the primal feasibility condition in (32). If it does, then we set and . On the contrary, if the primal feasibility is not satisfied, it means that we need to find as the root of the equation , which is unique since problem (VI-C1) is strongly convex, and can be efficiently found using the bisection method [46]. Finally, we set

| (36) |

VI-C2 Solution for the second update

From (VI-C), letting

| (37) |

the update for in (S2) reads as

| (38) | ||||

Hence, by resorting to Lemma 2, we obtain

| (39) |

where, similarly to Section VI-B2, is the projection operator onto the -norm ball of radius .

VI-C3 Solution for the third update

Analogously to Section VI-B3, we first derive the solution in matrix form, and then we vectorize it. From (VI-C), letting

| (40) |

with being the matrix representation of , the update for in (S2) is

| (41) | ||||

Again, following [44], the solution of (41) corresponds to projecting the Hermitian matrix onto , where the projection reads as

| (42) | ||||

Finally, we set

| (43) |

VI-D The algorithm

All the steps of the proposed iterative procedure are detailed in Algorithm 2. After the variables’ initialization (cf. lines 3-18), the algorithm proceeds exploiting the ADMM recursions (S1) and (S2) derived in the previous paragraphs (cf. lines 20-35), while also applying a diminishing step-size rule on the updates of (cf. line 23) and (cf. line 28), as required by the NOVA framework. To enable convergence with inexact updates, NOVA requires a diminishing step-size rule satisfying classical stochastic approximation conditions [38]:

Specifically, here we use the stepsize sequence [38]:

| (44) |

where as . For instance, in our experiments, we consider the pairs , and .

Stopping criteria. A suitable stopping criteria for the proposed algorithm can be obtained from the primal and dual feasibility optimality conditions [43]. We provide the complete derivation in the Supplementary Section A. The primal residuals are associated with constraints on the primal variables, whereas the dual can be derived from the stationarity conditions of the Lagrangian. As , the norms of primal and dual residuals should vanish. Hence, the stopping criterion is met when the norms of those residuals are below certain tolerances. Thus, we adopt absolute and relative tolerances, namely , for primal residuals and , for dual ones, as detailed in the Supplementary Section A.

Computational cost. The updates of the subproblems in Sections VI-B and VI-C can be run in parallel. In addition, each subproblem is further parallelizable over . With reference to Algorithm 2, computing the update in line 22 involves the inversion of in (48), i.e., inversions of matrices, costing flops. Additionally, we have block-diagonal matrix-vector multiplications, requiring flops. Afterwards, line 23 requires operations. Hence, overall we need flops for the update of in lines 22-23. Concerning line 24, the update of in (20) requires the computation of in (18), costing flops, and the projection onto the -norm ball, which is linear in the number of terms and thus costs . Therefore, the cost is . Furthermore, the update of given in (23) involves the eigedecomposition of an matrix, which costs . Next, in line 25, the updates of and are linear in the number of terms, costing flops each. Therefore, the block of lines 21-25 requires asymptotically flops.

Subsequently, the updates for and in line 27 involve the solution of the KKT conditions in (32) via the bisection method. Then, the cost depends on the number of bisection iterations, where each evaluation of (35) involves the inversion of in (34), which costs since is block-diagonal with equal blocks of size . Additionally, we have block-diagonal matrix-vector multiplications, requiring flops as above. Hence, the overall cost for evaluating (35) is . At this point, the smoothing in line 28 requires operations. Next, with regards to line 29, the update of in (39) requires computing in (37), which costs flops, and subsequently the projection onto the -norm ball, which again costs . Besides, the update of given in (43) involves the eigedecomposition of an matrix, which requires operations. Then, the updates of and in line 30 require flops each. In summary, assuming that the number of bisection iterations is small, the block of lines 26-30 asymptotically costs flops. Next, in line 33, the update of in (27) involves the computation of in (25). Now, since is diagonal, the latter computation costs flops. Finally, the update of in line 34 is linear in the number of terms, thus costing . Hence, for each , lines 32-34 have an asymptotic cost of flops.

VII Experiments on synthetic data

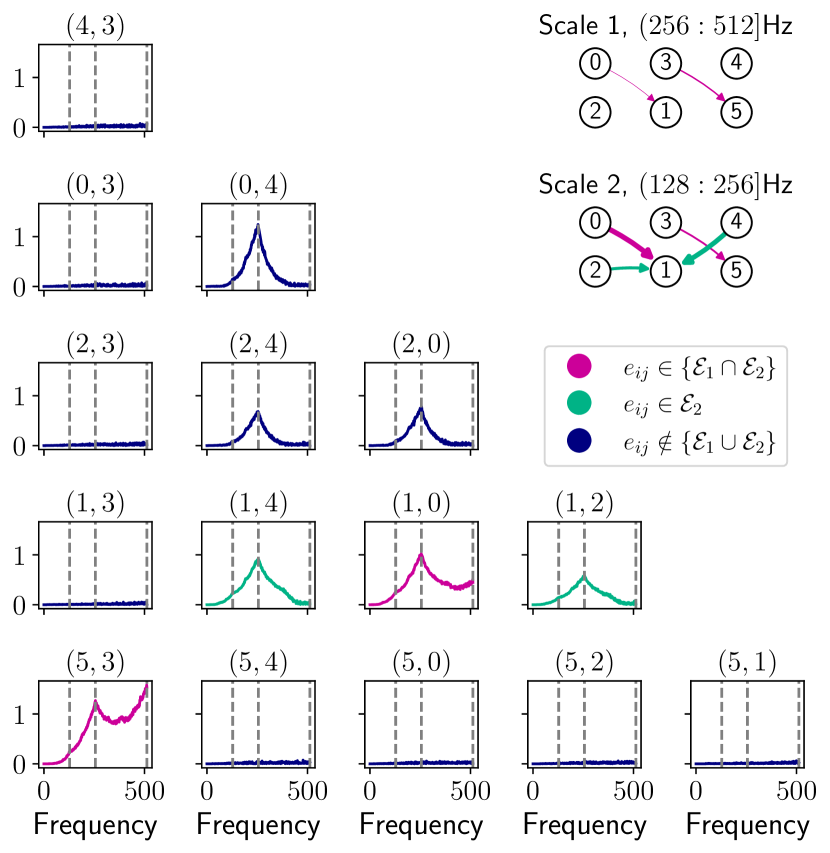

In this section, we assess and compare the performance of the proposed methods on synthetic data. To generate time series data entailing a block-sparse inverse CSD, we exploit the multiscale linear causal model proposed in [47]. Specifically, we generate data sets consisting of time series of length from a multiscale causal structure, where stationary interactions among time series occur only at two time scales, corresponding to the frequency bands Hz and Hz, respectively. Then, we use those data sets to obtain an accurate estimate of the inverse CSD tensor, from which we retrieve the -PCG where w.l.o.g. we set with equally-sized frequency blocks within the interval Hz. The cardinalities of the -PCG arc sets are .

Figure 2 depicts the multiscale causal structure together with the behavior of the strictly lower triangular part of along frequencies, where we use dashed lines to locate the splitting points of the relevant frequency bands. Since the inverse CSD tensor concerns partial correlation, we observe additional interactions that are not defined in the underlying causal structure, and which can be understood in light of the d-separation criterion [48]. For instance, the interaction between node and follows from the fact that, when we condition on the set of vertices , the latter also contains node that is a child of both and within the causal structure corresponding to the second time scale. Subsequently, the path activates, and we observe partial correlation.

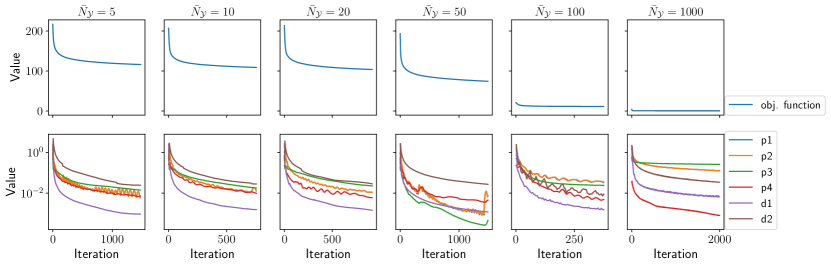

We compare our proposed methods with different baselines, including the naive estimator (cf. Sec. III) and the time series graphical LASSO algorithm in [29] (TS-GLASSO), which combines the - and -norm regularizations via (cf. eq. (41) in [29]). Here we test and . We consider two versions of the CF method: CF-nz with , where the user knows only the maximum number of non-null dependencies, and CF-fk with , where the full knowledge of is provided. In addition, we evaluate two versions of the IA method: IA-gs, which applies -norm regularization without considering distinct frequency blocks (similarly to TS-GLASSO), and IA-bs, which divides the frequency domain into blocks with starting frequencies Hz to enforce block-sparsity. To assess the quality of the learned graphs, we use the structural Hamming distance (SHD), which quantifies the number of modifications required to convert the estimated graph into the ground truth graph. The regularization strength parameter is fine-tuned within the range based on SHD, for both TS-GLASSO and IA. Furthermore, we set in (P2), and we test both strategies in lines 6-10 of Algorithm 2 for the initialization of . Convergence is determined using for both TS-GLASSO and IA. The learning process of these algorithms is stopped at iterations to manage computational time, regardless of convergence conditions. Convergence plots concerning the tested versions of our IA method are given in the Supplementary Section C, while the hyper-parameters values used in our simulations are listed in Supplementary Section B.

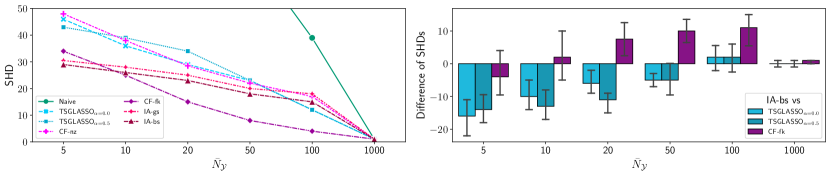

We compare the performance of the methods in three settings with varying samples availability: scarce (), medium (), and large (). For each setting, we estimate the smoothed periodogram using data sets sampled from the same causal structure. Once obtained from the learning methods, we compute the coherence for all , where is a diagonal matrix built as . The -PCG is finally obtained by normalizing between and and keeping entries greater than . We repeat this procedure times for each setting using different data sets sampled from the same causal structure.

Figure 3 shows the SHD (left) and the differences in SHD (right) between IA-bs and TS-GLASSO, as well as CF-fk, with respect to . The line plot on the left is cut at SHD for readability since the naive baseline shows SHD for . In the bar plot on the right, we omit the naive baseline for the same reason. As we can see from the line plot in Figure 3 (left), all methods outperform the naive baseline, retrieving the ground truth when . CF-fk, which has complete knowledge of , performs the best overall, followed by IA-bs and IA-gs. The superior performance of IA-gs over TS-GLASSO, despite not using block-sparsity, is due to the fact that it does not leverage WA and it can deviate from the smoothed periodogram. As increases, the gap between the IA versions and the TS-GLASSO baselines reduces, while CF-fk keeps showing considerably lower SHD. The bar plot on the right of Figure 3 highlights the benefits of using block-sparsity. Specifically, IA-bs significantly outperforms TS-GLASSO baselines for small-medium values. Then, in the large sample cases, differences vanish and are not statistically significant at the level. In addition, despite a considerable disadvantage, IA-bs does not significantly differ from CF-fk for , according to error bars. This is due to the low accuracy of the estimate of the inverse smoothed periodogram. Indeed, CF-fk receives the exact number of arcs per frequency band, and its errors are determined by the quality of the input estimate of the inverse smoothed periodogram. Thus, as the estimation improves, the performance gap between the two methods widens and then vanishes at .

VIII Application to real-world financial data

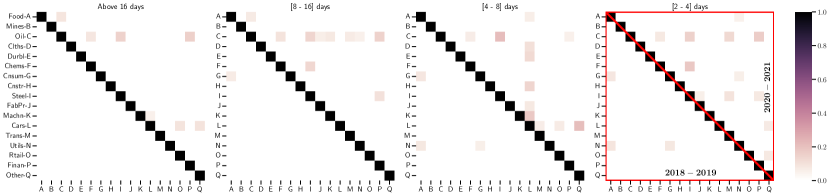

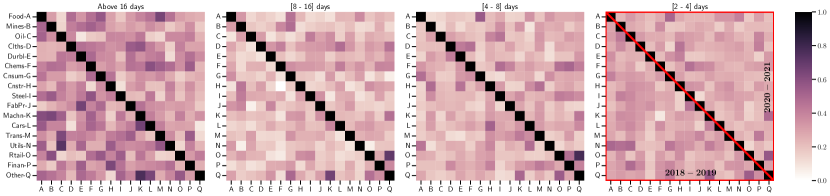

In this section, we study the partial correlations among daily returns of US industry equity portfolios from January 2018 to December 2021 (additional information in Supplementary Section D). We split the period into two parts, - and -. The first period is characterized by strong economic growth, low unemployment, and moderate inflation. However, trade tensions and geopolitical uncertainties were notable factors that influenced economic conditions during this period. The second period is characterized by a worsening macroeconomic environment, the outbreak and subsequent spread of the Covid-19 pandemic. Given the absence of prior knowledge, we apply the IA method to retrieve the -PCG associated with frequency bands, capturing interactions within , , , and above days. For example, the days block pertains to partial correlations occurring at a time resolution of consecutive days, up to a time resolution of days (i.e., roughly a business week).

Figure 4(a) illustrates the 4 layers of the block-sparse multi-frequency partial correlation graph, learned by the IA method, where each layer corresponds to a different frequency band. From Figure 4(a), we notice that over the first period (depicted in the lower triangular part of the matrices), few partial correlations occur, mainly at high-frequency bands. These dependencies are weak, and involve the food production industry (Food), businesses and industries focused on both essential and non-essential products (Cnsum), and energy services (Utils). These industries refer to segments of the economy that are relatively resistant to economic downturns and tend to remain stable during periods of economic recession or market volatility. Consequently, they are considered by investors to be defensive, meaning that they can provide stability during periods of economic uncertainty. On the contrary, during the second period (depicted in the upper triangular part of the matrices), partial correlations among portfolios are denser and spread over multiple frequency bands. These dependencies mainly relate to portfolios of energy resources (Oil); primary metal, iron and steel industries (Steel); and the automotive sector (Cars). In addition, while dependencies involving Oil occur over all frequency bands, those relating to Cars and Steel are localized within the and days time resolutions, respectively.

Our findings are justified by the economic conjuncture of the analyzed periods: the first characterized by a growing economy supported by fiscal policy, but also by the US-China trade war and increasing geopolitical uncertainties; the second by a worsening macroeconomic environment and the spread of Covid-19. In particular, the partial correlations learned over - are the signs of trade tensions, economic uncertainty, and concerns about global economic growth. These factors led investors to turn to defensive industry sectors, generating dependencies between Food, Cnsum, and Util industry portfolios. Furthermore, during the first part of 2020, the oil market crashed [49], and the natural gas market experienced its largest recorded demand decline in the history [50]. Afterward, an upward trend started, always in a scenario of economic uncertainty. Thus, the partial correlations learned over - serve as a clear indicator of the economic recession’s progression, which has been further hastened by the widespread impact of the Covid-19 pandemic.

Finally, for comparison purposes, Figure 4(b) shows that the solution obtained through the naive estimator is notably denser than the one learned by our IA method. This observation aligns with the findings presented in Section VII regarding synthetic data. In scenarios with limited samples, the naive baseline consistently returns the densest solutions and exhibits the worst SHD values. Consequently, the solution provided by the naive estimator lacks valuable insights for effectively discriminating partial correlations among time series in different market scenarios and frequency bands.

IX Conclusions

In this work, we have proposed novel methodologies to learn block-sparse multi-frequency PCGs, with the aim of discerning the frequency bands where partial correlation between time series occurs. Specifically, we devise two nonconvex methods, named CF and IA. The former has a closed-form solution and assumes prior knowledge of the number of arcs of the multi-frequency PCG over each layer. The latter jointly learns the CSD matrices and their inverses through an iterative procedure, which does not require any prior knowledge about (block-)sparsity. The IA method efficiently combines NOVA and ADMM iterations, providing a robust and highly performing recursive algorithm for learning block-sparse multi-frequency PCGs. Experimental results on synthetic data show that our proposals outperform the state of the art, thus confirming that block-sparsity regularization improves the learning of the -PCG. Interestingly, unlike methods that rely on the WA, our proposals are more robust to estimation errors when the number of available samples is scarce or modest, without sacrificing performance in large sample settings. Remarkably, the IA method performs well also with few available samples, even without knowing the measure of sparsity, thanks to its ability to deviate from the error-prone smoothed periodogram. Finally, the financial case study highlighted that learning a block-sparse multi-frequency PCG reveals valuable information about the partial correlation between time series at various frequency blocks in different market conditions, which is also supported by several economic conjectures of the analyzed periods.

Appendix A Proof of Lemma 1

From (16) and (S1), we start rearranging the term

| (45) |

to make the dependence on explicit. Specifically, let us denote the matrix form of with , and of with . At this point, the matrix form of reads as , . Analogously, , . Now, consider , ; and , . Hence, we conveniently rewrite (45) as

| (46) |

Thus, using (46) in (16), the first step of (S1) entails the minimization of (16) with respect to , which writes as:

| (47) |

Now, from (A), according to Wirtinger calculus [40], the stationarity condition follows from imposing the derivative of the objective of (A) w.r.t. equal to zero. Mathematically, this is equivalent to:

Finally, we obtain

with given by

| (48) |

where we exploited . From (48), it is easy to see that , with denoting the set of positive definite block-diagonal matrices on . Thus, the inverse of exists and can be efficiently computed in a block-wise fashion. This concludes the proof of Lemma 1.

References

- [1] H. Markowitz, “Portfolio selection,” The Journal of Finance, vol. 7, no. 1, pp. 77–91, 1952.

- [2] E. Bullmore and O. Sporns, “Complex brain networks: Graph theoretical analysis of structural and functional systems,” Nature Reviews Neuroscience, vol. 10, no. 3, pp. 186–198, 2009.

- [3] R. Salvador, J. Suckling, C. Schwarzbauer, and E. Bullmore, “Undirected graphs of frequency-dependent functional connectivity in whole brain networks,” Philosophical Transactions of the Royal Society B: Biological Sciences, vol. 360, no. 1457, pp. 937–946, 2005.

- [4] J. Jacobs, M. J. Kahana, A. D. Ekstrom, and I. Fried, “Brain oscillations control timing of single-neuron activity in humans,” Journal of Neuroscience, vol. 27, no. 14, pp. 3839–3844, 2007.

- [5] J. Ide, F. Cappabianco, F. Faria, and C.-s. R. Li, “Detrended partial cross correlation for brain connectivity analysis,” Advances in Neural Information Processing Systems, vol. 30, 2017.

- [6] M. Termenon, A. Jaillard, C. Delon-Martin, and S. Achard, “Reliability of graph analysis of resting state fMRI using test-retest dataset from the Human Connectome Project,” NeuroImage, vol. 142, pp. 172–187, 2016.

- [7] P. Ciuciu, P. Abry, and B. J. He, “Interplay between functional connectivity and scale-free dynamics in intrinsic fMRI networks,” NeuroImage, vol. 95, pp. 248–263, 2014.

- [8] J. S. Ide and R. L. Chiang-shan, “Time scale properties of task and resting-state functional connectivity: Detrended partial cross-correlation analysis,” NeuroImage, vol. 173, pp. 240–248, 2018.

- [9] M. Besserve, B. Schölkopf, N. K. Logothetis, and S. Panzeri, “Causal relationships between frequency bands of extracellular signals in visual cortex revealed by an information theoretic analysis,” Journal of Computational Neuroscience, vol. 29, no. 3, pp. 547–566, 2010.

- [10] G. Gu and R. F. Adler, “Precipitation and temperature variations on the interannual time scale: Assessing the impact of ENSO and volcanic eruptions,” Journal of Climate, vol. 24, no. 9, pp. 2258–2270, 2011.

- [11] J. Songsiri, J. Dahl, and L. Vandenberghe, “Graphical models of autoregressive processes,” in Convex optimization in signal processing and communications. Cambridge University Press, 2010.

- [12] G. T. Wilson, M. Reale, and J. Haywood, Models for dependent time series. CRC Press, 2015, vol. 139.

- [13] H. Shrivastava and U. Chajewska, “Methods for recovering conditional independence graphs: A survey,” arXiv preprint arXiv:2211.06829, 2022.

- [14] R. Dahlhaus, “Graphical interaction models for multivariate time series,” Metrika, vol. 51, no. 2, pp. 157–172, 2000.

- [15] O. Banerjee, L. El Ghaoui, and A. d’Aspremont, “Model selection through sparse maximum likelihood estimation for multivariate Gaussian or binary data,” The Journal of Machine Learning Research, vol. 9, pp. 485–516, 2008.

- [16] M. Kolar, A. P. Parikh, and E. P. Xing, “On sparse nonparametric conditional covariance selection,” in Proceedings of the 27th International Conference on Machine Learning, ser. ICML’10. Madison, WI, USA: Omnipress, 2010, p. 559–566.

- [17] S. Oh, O. Dalal, K. Khare, and B. Rajaratnam, “Optimization methods for sparse pseudo-likelihood graphical model selection,” Advances in Neural Information Processing Systems, vol. 27, 2014.

- [18] E. Belilovsky, K. Kastner, G. Varoquaux, and M. B. Blaschko, “Learning to discover sparse graphical models,” in International Conference on Machine Learning. PMLR, 2017, pp. 440–448.

- [19] G. Lugosi, J. Truszkowski, V. Velona, and P. Zwiernik, “Learning partial correlation graphs and graphical models by covariance queries.” The Journal of Machine Learning Research, vol. 22, pp. 203–1, 2021.

- [20] M. Fiecas and H. Ombao, “The generalized shrinkage estimator for the analysis of functional connectivity of brain signals,” The Annals of Applied Statistics, vol. 5, no. 2A, pp. 1102–1125, 2011.

- [21] M. Fiecas and R. von Sachs, “Data-driven shrinkage of the spectral density matrix of a high-dimensional time series,” Electronic Journal of Statistics, vol. 8, no. 2, pp. 2975–3003, 2014.

- [22] D. Schneider-Luftman and A. T. Walden, “Partial coherence estimation via spectral matrix shrinkage under quadratic loss,” IEEE Transactions on Signal Processing, vol. 64, no. 22, pp. 5767–5777, 2016.

- [23] H. Böhm and R. von Sachs, “Shrinkage estimation in the frequency domain of multivariate time series,” Journal of Multivariate Analysis, vol. 100, no. 5, pp. 913–935, 2009.

- [24] M. Fiecas, C. Leng, W. Liu, and Y. Yu, “Spectral analysis of high-dimensional time series,” Electronic Journal of Statistics, vol. 13, no. 2, pp. 4079–4101, 2019.

- [25] T. Cai, W. Liu, and X. Luo, “A constrained minimization approach to sparse precision matrix estimation,” Journal of the American Statistical Association, vol. 106, no. 494, pp. 594–607, 2011.

- [26] A. Jung, G. Hannak, and N. Goertz, “Graphical lasso based model selection for time series,” IEEE Signal Processing Letters, vol. 22, no. 10, pp. 1781–1785, 2015.

- [27] N. J. Foti, R. Nadkarni, A. Lee, and E. B. Fox, “Sparse plus low-rank graphical models of time series for functional connectivity in MEG,” in 2nd KDD Workshop on Mining and Learning from Time Series, 2016.

- [28] A. Dallakyan, R. Kim, and M. Pourahmadi, “Time series graphical lasso and sparse VAR estimation,” Computational Statistics & Data Analysis, vol. 176, p. 107557, 2022.

- [29] J. K. Tugnait, “On sparse high-dimensional graphical model learning for dependent time series,” Signal Processing, vol. 197, p. 108539, 2022.

- [30] P. Whittle, “The analysis of multiple stationary time series,” Journal of the Royal Statistical Society: Series B (Methodological), vol. 15, no. 1, pp. 125–139, 1953.

- [31] ——, “Curve and periodogram smoothing,” Journal of the Royal Statistical Society: Series B (Methodological), vol. 19, no. 1, pp. 38–47, 1957.

- [32] E. J. Hannan, “The asymptotic theory of linear time-series models,” Journal of Applied Probability, vol. 10, no. 1, pp. 130–145, 1973.

- [33] A. Contreras-Cristán, E. Gutiérrez-Peña, and S. G. Walker, “A note on Whittle’s likelihood,” Communications in Statistics - Simulation and Computation, vol. 35, no. 4, pp. 857–875, 2006.

- [34] X. Xu, Z. Li, and M. Taniguchi, “Comparison between the exact likelihood and Whittle likelihood for moving average processes,” Statistica, vol. 82, no. 1, pp. 3–13, 2022.

- [35] R. G. Baraniuk, V. Cevher, M. F. Duarte, and C. Hegde, “Model-based compressive sensing,” IEEE Transactions on Information Theory, vol. 56, no. 4, pp. 1982–2001, 2010.

- [36] G. Scutari and Y. Sun, “Parallel and distributed successive convex approximation methods for big-data optimization,” in Multi-agent Optimization. Springer, 2018, pp. 141–308.

- [37] S. Sardellitti, S. Barbarossa, and P. Di Lorenzo, “Graph topology inference based on sparsifying transform learning,” IEEE Transactions on Signal Processing, vol. 67, no. 7, pp. 1712–1727, 2019.

- [38] G. Scutari, F. Facchinei, and L. Lampariello, “Parallel and distributed methods for constrained nonconvex optimization—Part I: Theory,” IEEE Transactions on Signal Processing, vol. 65, no. 8, pp. 1929–1944, 2016.

- [39] M. Razaviyayn, M. Hong, Z.-Q. Luo, and J.-S. Pang, “Parallel successive convex approximation for nonsmooth nonconvex optimization,” Advances in Neural Information Processing Systems, vol. 27, 2014.

- [40] R. F. Fischer, Precoding and signal shaping for digital transmission. John Wiley & Sons, 2005.

- [41] M. Grant and S. Boyd, “CVX: Matlab software for disciplined convex programming, version 2.1,” 2014.

- [42] S. Diamond and S. Boyd, “CVXPY: A python-embedded modeling language for convex optimization,” The Journal of Machine Learning Research, vol. 17, no. 1, pp. 2909–2913, 2016.

- [43] S. Boyd, N. Parikh, E. Chu, B. Peleato, J. Eckstein et al., “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends® in Machine learning, vol. 3, no. 1, pp. 1–122, 2011.

- [44] N. Parikh, S. Boyd et al., “Proximal algorithms,” Foundations and trends® in Optimization, vol. 1, no. 3, pp. 127–239, 2014.

- [45] S. P. Boyd and L. Vandenberghe, Convex optimization. Cambridge, UK: Cambridge University Press, 2004.

- [46] R. L. Burden, J. D. Faires, and A. M. Burden, Numerical analysis. Cengage Learning, 2015.

- [47] G. D’Acunto, G. D. F. Morales, P. Bajardi, and F. Bonchi, “Learning multiscale non-stationary causal structures,” Transactions on Machine Learning Research, 2023.

- [48] J. Pearl, Causality. Cambridge University Press, 2009.

- [49] C. Gharib, S. Mefteh-Wali, V. Serret, and S. B. Jabeur, “Impact of COVID-19 pandemic on crude oil prices: Evidence from Econophysics approach,” Resources Policy, vol. 74, p. 102392, 2021.

- [50] IEA, “Gas (2020),” IEA, Tech. Rep., 2020. [Online]. Available: https://www.iea.org/reports/gas-2020

Learning Multi-Frequency Partial Correlation Graphs: Supplementary Material

Appendix Supplementary Section A Stopping criterion

The stopping criterion for the proposed algorithm follows from the primal and dual feasibility optimality conditions \citeSMboyd2011distributed1. For each , the primal residuals, associated with constraints on the primal variables, read as:

| (1) | ||||

from which we set , , , , , belonging to ; and .

The dual residuals can be obtained from the stationarity conditions. Specifically, , given the point , from the stationarity condition it follows that

| (2) |

and

| (3) |

From (2) we get

| (4) | ||||

In our case, denoting with a saddle point for the unaugmented Lagrangian for the subproblem in , the dual feasibility reads as

| (5) |

Hence, from (4), we have that the quantity

| (6) | ||||

can be considered as a residual for the dual feasibility condition in (5). By applying the same steps for the subproblem in , starting from (3), we get the formula for the other residual,

| (7) |

Since the expressions in (6) and (7) are specific for frequency , , also in this case we set , , both in .

As , the norms of primal and dual residuals above should vanish. According to \citeSMboyd2011distributed1, the stopping criterion is met when the norms of those residuals are below certain tolerances, constituted by an absolute and a relative term. Let us set

Hence, we define the stopping rules as composed of an absolute and a relative component. In detail, given absolute and relative tolerances, namely (i) , for primal residuals, and (ii) , for dual ones; the stopping rules read as

With regards to the values for the tolerances, they are usually set to be small, for instance .

Appendix Supplementary Section B Hyper-parameters

In Table I, we report the list of all the hyper-parameters used by the IA and TS-GLASSO algorithms to obtain the numerical results illustrated in Section VII.

| Method | init | ||||||

|---|---|---|---|---|---|---|---|

| 5 | IA-bs | 0.500 | identity | 0.50 | 0.99 | ||

| IA-gs | 0.700 | identity | 0.50 | 0.99 | |||

| 1.000 | identity | N/A | N/A | N/A | N/A | ||

| 0.700 | identity | N/A | N/A | N/A | N/A | ||

| 10 | IA-bs | 0.500 | identity | 0.50 | 0.99 | ||

| IA-gs | 0.500 | identity | 0.50 | 0.99 | |||

| 1.000 | identity | N/A | N/A | N/A | N/A | ||

| 0.500 | identity | N/A | N/A | N/A | N/A | ||

| 20 | IA-bs | 0.300 | identity | 0.50 | 0.99 | ||

| IA-gs | 0.300 | identity | 0.50 | 0.99 | |||

| 1.000 | identity | N/A | N/A | N/A | N/A | ||

| 0.300 | identity | N/A | N/A | N/A | N/A | ||

| 50 | IA-bs | 0.500 | identity | 0.99 | 0.99 | ||

| IA-gs | 0.500 | identity | 0.99 | 0.99 | |||

| 1.000 | identity | N/A | N/A | N/A | N/A | ||

| 0.070 | identity | N/A | N/A | N/A | N/A | ||

| 100 | IA-bs | 0.300 | inverse | 0.90 | 0.99 | ||

| IA-gs | 0.500 | identity | 0.99 | 0.99 | |||

| 0.100 | identity | N/A | N/A | N/A | N/A | ||

| 0.030 | identity | N/A | N/A | N/A | N/A | ||

| 1000 | IA-bs | 0.010 | inverse | 0.50 | 0.99 | ||

| IA-gs | 0.050 | inverse | 0.50 | 0.99 | |||

| 0.010 | identity | N/A | N/A | N/A | N/A | ||

| 0.001 | identity | N/A | N/A | N/A | N/A |

Appendix Supplementary Section C Empirical Convergence of the IA Method

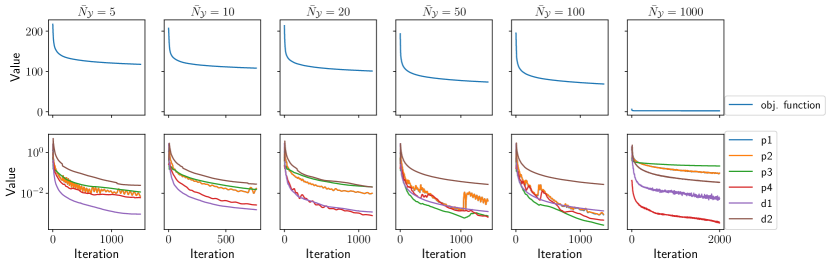

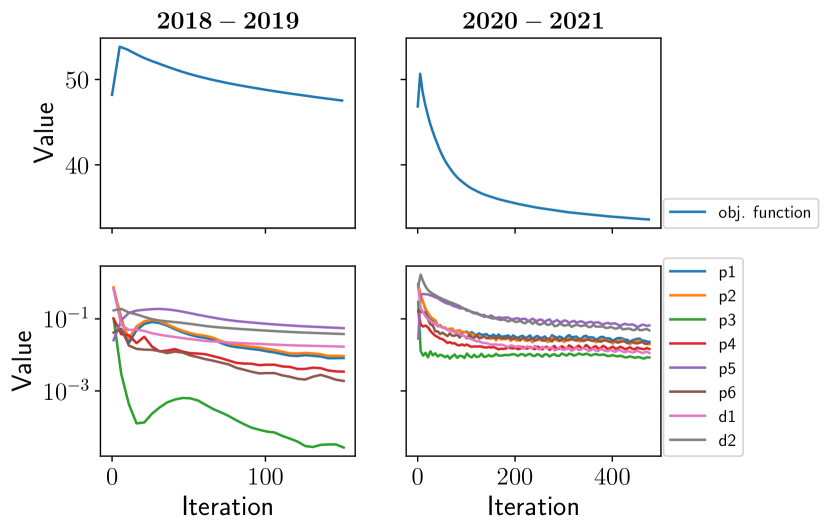

In this section we provide convergence plots regarding the proposed IA method, for both synthetic and real-world data experiments, empirically showing its convergence behavior. Specifically, Figure 1 depicts the behavior of the objective function (top row) and the norm primal and dual feasibility residuals (bottom row, on a logarithmic scale for readability reason) over the iterations for (a) IA-bs and (b) IA-gs. The columns correspond to different numbers of available samples considered in the experiments, as detailed in Section VII. The results demonstrate a consistent reduction in the objective function value throughout the optimization process, alongside the decreasing trends of the norm of primal (, , , ,, ) and dual (, ) feasibility residuals that determine the convergence of the IA method (as detailed in Supplementary Section A). In addition, Figure 1 underscores that as the sample size increases, the objective function attains lower values. Analogous observations are drawn from Figure 2, which pertains to our financial case study.

Appendix Supplementary Section D Real-world case study: data source and additional information

Daily returns were gathered from the Fama-French repository. These portfolios are made by equities traded on the NYSE, AMEX, and NASDAQ stock exchanges. Before applying the IA method, we make the time series of linear returns zero-mean. Hence, we divide the data set into two parts, - and -, consisting of and days, respectively. At this point, we estimate the smoothed periodogram corresponding to each period. Here, we use a Hanning window with a window length equal to , where . The complete list of used hyper-parameters for the IA method is provided in the IPython notebook named 2.0_real-world_case_study.ipynb, accessible from our repository. In the latter, you can also access the JAX \citeSMjax2018github implementation of our algorithms, along with the data sets and IPython notebooks for results reproduction.

MyIEEE \bibliographySMsmbibliography