An Identification-and Dimensionality-Robust Test for Instrumental Variables Models

Abstract

I propose a new identification-robust test for the structural parameter in a heteroskedastic linear instrumental variables model. The proposed test statistic is similar in spirit to a jackknife version of the K-statistic and the resulting test has exact asymptotic size so long as an auxiliary parameter can be consistently estimated. This is possible under approximate sparsity even when the number of instruments is potentially much larger than the sample size. As the number of instruments is allowed, but not required, to be large, the limiting behavior of the test statistic is difficult to examine via existing central limit theorems. Instead, I derive the asymptotic chi-squared distribution of the test statistic using a direct Gaussian approximation technique. To improve power against certain alternatives, I propose a simple combination with the sup-score statistic of Belloni et al. (2012) based on a thresholding rule. I demonstrate favorable size control andpower properties in a simulation study and apply the new methods torevisit the effect of social spillovers in movie consumption.

Keywords: Instrumental Variables, Weak Identification, High-DimensionalJEL Codes: C12, C36, C55

1 Introduction

Consider a linear instrumental variables (IV) model

| (1.1) |

where is an outcome of interest and is a vector of endogenous variables. The variable represents a vector of instrumental variables, of which a subvector of fixed dimension, , is included in the structural equation (1.1) as exogenous control. I assume that the researcher has access to independent observations of . In this setting, I propose a new test for a two-sided restriction on the structural parameter; versus . The proposed test has exact asymptotic size even when instruments are potentially high-dimensional () and arbitrarily weak.When instruments are suspected to be weak, researchers may want to test hypotheses about structural parameters using testing procedures that are robust to identification strength. These identification-robust testing procedures all require some conditions on the rate of growth of the number of instruments, , in relation to the sample size, . The tests of Anderson and Rubin (1949); Staiger and Stock (1997); Moreira (2001, 2003), and Kleibergen (2002, 2005) are shown by Andrews and Stock (2007) to control size under heteroskedasticity when . Recent tests developed in Mikusheva and Sun (2021); Crudu et al. (2021); Matsushita and Otsu (2022), and Lim et al. (2022) allow the number of instruments to be proportional to sample size, , but require that the number of instruments be large, . Moreover, while the tests proposed by Belloni et al. (2012) and Mikusheva (2023) require only for someconstant , they either rely on sample splitting or fail to incorporate first-stage information, both of which may reduce power in overidentified models.These conditions on the growth rate of can be difficult to interpret and the variety of tests available under alternate regimes may make it unclear to the researcher which test should be applied in her particular setting.111For example, consider a setting similar to that of Derenoncourt (2022) where the researcher has a dozen or so instruments and a sample size of a few hundred. The number of instruments cubed is larger than sample size, but asymptotic approximations based on seem unlikely to resemble the finite sample distribution.In contrast, the test considered in this paper is applicable in any of the settings described above. The proposed test statistic is similar in spirit to a jackknife version of the K-statistic and makes use of an auxiliary conditional slope parameter to construct first-stage estimates that are uncorrelated with the structural errors under the null hypothesis. So long as this auxiliary parameter can be consistently estimated, the proposed test statistic has a limiting chi-squared distribution with degrees of freedom equal to the number of structural parameters. The conditional slope parameter is simple to estimate with out-of-the-box methods, and consistency is achievable under approximate sparsity even when the number of instruments is much larger than the sample size. This approximate sparsity assumption is trivially satisfied when the first- and second-stage errors are homoskedastic.As the number of instruments is allowed to be larger than the sample size, traditional central limit theorems are insufficient to derive the limiting distribution of the test statistic. Instead, the limiting behavior of the test statistic is examined directly with a variation of Lindeberg’s interpolation method (Lindeberg, 1922). The direct approach allows me to characterize the limiting behavior of the test statistic in both high- and low-dimensional settings under a unified argument. I show that, in local neighborhoods of the null, the distribution of the test statistic can be uniformly approximated by the distribution of an analog statistic that replaces each observation in the expression of the test statistic with a Gaussian version that has the same mean and covariance matrix as the original. These local neighborhoods of the null are characterized by a local power index which I introduce in Section 3. An interesting feature of the direct Gaussianapproximation argument is that, while the numerator and denominator the jackknife K-statistic may both have nondegenerate distributions under weak identification, neither needs to converge on its own to a weak limit in order to characterize the limiting distribution of the jackknife K-statistic.When there is a single endogenous variable, a leading case in empirical applications, analysis of limiting behavior can be considerably simplified by taking advantage of the particular form of the test statistic.In this case I show that, under an additional regularity condition, an infeasible version of the test that could be constructed if the auxiliary parameter was known to the researcher is consistent whenever the local power index diverges. When the local power index is bounded, I examine the limiting power of the test by examining the behavior of the analog statistic. Under the alternative hypothesis the analog statistic has a nearly non-central distribution conditional on the first-stage estimates. The noncentrality parameter is proportional to the correlation between the true first-stage model and the first-stage estimates. Unfortunately, partialling out the structural parameter may introduce bias into the first-stage estimates under the alternate hypothesis. This issue is pointed out by Moreira (2001); Andrews et al. (2006), and Andrews (2016) in the context of the non-jackknife K-statistic.Against certain alternatives this bias can be particularly pronounced and the additional regularity condition needed for the consistency result may fail to hold.222This does not necessarily mean, however, that the test is not consistent.To address this, I propose a simple combination of the jackknife K-statistic with the sup-score statistic of Belloni et al. (2012) based on a thresholding rule. As with the Anderson-Rubin statistic, while the sup-score statistic does not yield efficient inference under strong identification, it does not suffer from a loss of power against any particular alternative when identification is weak (Andrews et al., 2006; Andrews, 2016). The combination test decides whether the jackknife K-test or the sup-score test should be run by comparing the value of a conditioning statistic to a predetermined cutoff value. In the approximating Gaussian regime, this conditioning statistic is marginally independent of both the jackknife K-statistic and the sup-score statistic. This allows me to show that the combination test controls size under the null without having to require that the conditioning statistic converges in distribution to a stable limit. In a simulation study, I find that taking this cutoff value to be the75th quantile of the distribution of the conditioning statistic delivers a reasonable balance of power against local and distant alternatives. Using results in Chernozhukov et al. (2017) and Belloni et al. (2018) this quantile can be simulated via a multiplier bootstrap procedure.When there are multiple endogenous variables, I cannot take advantage of the simplified form of the test statistic. Instead, I use a more involved interpolation argument that relies on strengthened moment conditions. Under these strengthened conditions I derive the limiting chi-squared distribution of the jackknife K-statistic in the larger context and propose a generalization of the thresholding test to improve power properties.I apply the proposed testing procedures to the data of Gilchrist and Sands (2016) to generate weak instrument-robust confidence intervals for the effect of social spillovers in movie consumption. Following Belloni et al. (2012), the authors’ initial analysis uses conventional heteroskedasticity-robust standard errors after estimating the first-stage via post-LASSO. The validity of this analysis depends on the structural parameter being strongly identified. Using a simple numerical demonstration, I argue that the first-stage F-statistics reported by the authors may not be reliable indicators of identification strength when LASSO is used to select instruments. The identification-robust confidence intervals generated by inverting the jackknife K-statistic are larger than those implied by the initial analysis but do not rule out the authors’ point estimates. Moreover, these confidence intervals are typically smaller than those implied by inverting the sup-score statisticin specifications for which the sup-score confidence interval is nonempty.Finally, I examine the applicability of the theoretical results in this paper through a simulation study. Tests based on the jackknife K-statistic are shown to have nearly exact size in a variety of settings. While the jackknife K-statistic may have diminished power against certain alternatives, this deficiency seems to be ameliorated by combining the jackknife K-statistic with the sup-score statistic via the thresholding test. Compared to the many-instrument tests of Mikusheva and Sun (2021) and Matsushita and Otsu (2022), the tests proposed in this paper appear to have favorable size control and power properties.The outline of this paper is as follows. Section 2 formally defines the model considered and introduces the jackknife K-statistic. Section 3 provides an overview of the Gaussian approximation approach with a single endogenous variable and characterizes the limiting behavior of the test statistic in this setting. Section 4 uses this characterization to examine the power properties of the test and introduces the combination test to address power deficiencies against certain alternatives. Section 5 extends the analyses of Sections 3 and 4 to the case of multiple endogenous variables and outlines the Gaussian approximation argument in this setting. Section 6 contains the empirical application while Section 7 provides evidence from simulation study. Proofs of the main results are deferred to Appendices A, B and C.

Notation.

For any let denote the set . I work with a sequence of probability measures on the data . To accommodate independent but not identically distributed observations, let denote the empirical expectation and denote the average expectation operator.

1.1 Prior Literature and Empirical Practice

When the first-stage F-statistic is small, standard asymptotic approximations may fail to accurately describe the finite-sample behavior of IV estimates. This was first pointed out by Nelson and Startz (1990) and Bound et al. (1995) who consider the finite-sample behavior of two-stage least squares (2SLS) in alternate settings where the IV is only weakly correlated with the endogenous variable. In a seminal paper, Staiger and Stock (1997) capture this phenomena in an asymptotic framework by considering a sequence of first-stage models that shrink to zero with the sample size. Under this framework, standard IV estimates are no longer consistent and inference procedures based on these statistics fail to control size. Because of these results, there has been a large interest in developing tests for the structural parameter that control size regardless of identification strength.To test hypotheses about the structural parameter when instruments are suspected to be weak, Staiger and Stock (1997) propose the use of the Anderson-Rubin statistic, which does not require any assumptions about identification strength to control size. Noting that the Anderson-Rubin test is inefficient in overidentified models, Moreira (2001) and Kleibergen (2002, 2005) propose the use of the (non-jackknife) K-statistic, which has a limiting null distribution that does not depend on the number of instruments. Compared to the Anderson-Rubin statistic, these tests have improved power in local neighborhoods of the null but can perform poorly against certain alternatives. To address this, Moreira (2003) and Kleibergen (2005) suggest combinations of the K-statistic and Anderson-Rubin statistic based on a conditioning statistic that is independent of them both under the null. Andrews et al. (2006) characterize the power envelope in a homoskedastic weakly identified IV model and show that the test based on theconditional likelihood ratio statistic of Moreira (2003) has nearly optimal power in this setting. When errors are heteroskedastic, Andrews (2016) proposes alternate combinations of the K-statistic and the Anderson-Rubin statistic based on a minimax regret criterion.These initial tests are developed under asymptotic frameworks that treat the number of instruments as fixed or growing slowly relative to the sample size (Han and Phillips, 2006; Newey and Windmeijer, 2009; Andrews and Stock, 2007). However, with the emergence of large datasets and more sophisticated research designs, researchers may encounter scenarios where the number of instruments may not be negligible as a ratio of sample size. A prominent example of this is in judge-design settings where the number of instruments is equal to the number of judges to whom an individual can be assigned to (Maestas et al., 2013; Sampat and Williams, 2019; Dobbie et al., 2018). Since each judge can handle only a finite number of cases the number of instruments is proportional to the sample size. Moreover, to flexibly model the first-stage, researchers may generate a large number of instruments by enriching a “small” initial set of instruments via polynomial (or other) transformations. Angrist and Krueger (1991) famously interact quarter-of-birth, state-of-birth, and year-of-birth dummies to construct a total of 180 instruments.Belloni et al. (2012) show that, when identification is strong, researchers can use a potentially high-dimensional, , set of first-stage instrument basis terms in conjunction with a LASSO or post-LASSO estimate of the first-stage. This strategy has been successfully employed in practice by Paravisini et al. (2014); Gilchrist and Sands (2016); Derenoncourt (2022), and Jou and Morgan (2023).To address these settings, there has been recent interest in developing weak instrument-robust tests under asymptotic frameworks that do not require that the ratio of instruments to sample size tends to zero. Crudu et al. (2021); Mikusheva and Sun (2021), and Matsushita and Otsu (2022) take advantage of a new central limit theorem for quadratic forms developed in Chao et al. (2012) and propose weak identification-robust tests that are valid even when the number of instruments is proportional to sample size; . Following the many instruments asymptotic framework first introduced by Bekker (1994), the analyses in these papers rely on the number of instruments diverging. When the number of instruments is fixed or diverges slowly to infinity, these asymptotic approximations may provide poor characterizations of the proposed test statistics’ finite sample distribution.Limited identification-robust testing procedures exist for the high-dimensional case, . To my knowledge, the only two options available are the sup-score test of Belloni et al. (2012) and the split-sample optimal instrument AR test developed in Mikusheva (2023). The sup-score test makes use of Gaussian approximations for maxima of high-dimensional vectors developed in Chernozhukov et al. (2013) but suffers from the same issue as the Anderson-Rubin test in that its critical value is increasing with the number of instruments. The spilt sample optimal instrument AR test splits the dataset into two parts and uses one split to estimate an optimal instrument and the other to test the null hypothesis. This may lead to a loss of power as only half of the sample is being effectively used to test the null hypothesis.Weak instrument-robust tests may be particularly interesting in high-dimensional and heteroskedastic settings because of a lack of clarity on how to pretest for identification strength. When the number of instruments is fixed and errors are homoskedastic, Stock and Yogo (2005) propose pretesting for the strength of identification via thte first-stage F-statistic. Based on their results, common practice in empirical settings has been to use standard Wald tests whenever the first-stage F-statistic exceeds 10. Lee et al. (2022) point out this recommendation is not applicable in heteroskedastic models and update the recommended F-statistic cutoff. To pretest for weak identification in the many-instruments asymptotic framework, , Mikusheva and Sun (2021) propose a new -statistic and suggest using identification-robust procedures when . When the number of instruments is larger than sample size thereis no accepted full-sample pretest for identification strength.333Mikusheva (2023) suggests a split-sample pretest in the same spirit as the split-sample optimal instrument AR test.In particular, I argue in Section 6 that first-stage F-statistics resulting from first-stage post-LASSO procedures can be misleading even if they are much larger the standard cutoff of 10.

| Asymptotic Regime | Main Tests | ||||||

|---|---|---|---|---|---|---|---|

|

|

||||||

|

|

||||||

|

|

I contribute to these literatures by proposing a new identification-robust test for the structural parameter that can work in potentially high-dimensional settings () without requiring that the number of instruments diverges. The testing procedures in this paper may be particularly applicable in intermediate cases where the number of instruments cubed may not be negligible relative to sample size but it is unclear whether asymptotic approximations based on will accurately describe finite sample behavior. Examples of such intermediate cases include the analyses of Derenoncourt (2022), where and , Paravisini et al. (2014), where and , and Gilchrist and Sands (2016), where and .In addition to the literature on weak-instrument robust testing, I contribute to a growing literature on direct gaussian approximation and interpolation techniques (Chatterjee, 2006, 2010; Pouzo, 2015; Chernozhukov et al., 2013, 2017; Celentano et al., 2020). These techniques have proven useful to approximate the behaviors of statistics in a variety of nonstandard settings, such as high-dimensional random vectors or spectral analysis of random matrices. Prior analysis of statistics via interpolation techniques has relied on the boundedness of the derivatives of these statistics with respect to individual observations. This condition does not hold in my setting as the derivative of the jackknife K-statistic with respect to terms in the denominator may be unbounded. This poses a number of technical challenges for my interpolation argument that must be overcome in order to characterize the limiting behavior of the jackknife K-statistic, particularly when . I contribute to this literature by proposing modifications of the original Lindeberg (1922) interpolation technique that can accommodate statistics with unbounded derivatives.

2 Model and Setup

Though the analysis below allows for exogenous regressors, to simplify the exposition I follow Mikusheva and Sun (2021) and assume that they have already been partialed out of both the outcome, , and the endogenous regressors, . As the controls are assumed to be of fixed dimension, this is without loss of generality.111For discussion refer to Appendix E. Along with the structural equation in (1.1), the IV model can then be written with the first stage as a system of simultaneous equations:

| (2.1) |

The researcher observes the outcome , the endogenous variable , and the instruments but neither the structural error nor the first-stage errors . The structural error is assumed to be conditional-mean independent of the instruments, . I denote as and make no assumptions about the functional form of the conditional expectation so the instruments are allowed to affect the endogenous variable in a nonlinear fashion.The random variables are assumed to be independent across observations. Observations need not be identically distributed but the errors are assumed to have a common covariance structure conditional on the instruments :

As is otherwise left unrestricted, the errors are allowed to be heteroskedastic. All results in this paper hold conditionally on a realization of the instruments so from this point forth they are treated as fixed and all expectations can be understood as conditional on the instruments.Under this setup, the researcher wishes to test a two-sided restriction on the structural parameter:

I am interested in constructing powerful tests for this null-alternate pair that are asymptotically valid under arbitrarily weak identification and with minimal restrictions on the number of instruments . To this end, define the null errors . Using these, I construct a variable, , that is a “partialed-out” version of the endogenous variable satisfying :

Each element of the nuisance parameter , for , can be interpreted as the (conditional) slope coefficient from a simple linear regression of on . Thus, if falls in some function class it can be estimated directly under by solving empirical analogs of:222Under , can be estimated directly by solving empirical analogs of where . This requires an initial estimate of , however.

I will largely work under the assumption that has an approximately sparse representation in some (growing) basis , that is where represents an approximation error that tends to zero with the sample size and is sparse in the sense that many of its coefficients are zero. This allows for nesting of the low-dimensional case, where the number of instruments is fixed, and the high dimensional case, where the number of instruments is potentially much larger than the sample size, under a unified estimation procedure. Under homoskedasticity, is a constant function and thus has a spare representation in any basis that contains a constant term.As in Chernozhukov et al. (2022), the parameter can be estimated via LASSO:

| (2.2) |

or via post-LASSO, refitting an unpenalized version of (2.2) using only the basis terms associated with nonzero coeffecients in the inital LASSO regression. The estimating procedure in (2.2) is a simple -penalized regression of against . It can be easily implemented using out-of-the-box software available on most platforms. Under standard conditions, this leads to a consistent estimate of as long as the sparsity condition where is the number of nonzero elements of and is a positive constant that depends on the moment bounds imposed. The estimation procedure is discussed in more detail in Section 3.2. With , I construct the estimated version of , for each .

2.1 Test Statistic

The test statistic is based on an arbitrary jackknife-linear estimate of the first stage,

for some “hat” matrix . The phrase “hat matrix” is borrowed from ordinary least squares (OLS) where the projection matrix, , is sometimes referred to as the hat matrix in the sense that . In practice, the hat matrix, , can be any matrix that depends only on . It is important to note that while does not depend on the observation , it may depend on through the hat matrix . This gives the test power against alternatives where .For technical reasons, I will assume that for each so that can be written as .Formally, the only structure I require on the hat matrix is a balanced-design condition described in Section 3. However, for reasons explained in Section 4 it may be optimal to introduce some regularization in estimating the first-stage models so I suggest using the deleted diagonal ridge-regression hat matrix :

| (2.3) |

where, following recommendations in Harrell (2015) and van Wieringen (2023), the penalty parameter is set so that the effective degrees of freedom of the resulting hat matrix is no more than a fraction of the sample size:

The ridge hat matrix has the benefit of being well defined even when the number of instruments is larger than the sample size.I stress, though, that the researcher may use any other hat matrix that she believes will lead to plausible first-stage estimates. Other possible choices of hat matrix include the jackknife OLS hat matrix of Angrist et al. (1999), the deleted diagonal projection matrix introduced in Chao et al. (2012) and successfully used in Kline et al. (2020); Crudu et al. (2021); Mikusheva and Sun (2021), and Matsushita and Otsu (2022), or hat matrices based on selecting instruments via some preliminary unsupervised technique such as principal component analysis (PCA). Remark 3.1 below discusses how the balanced-design condition may be verified for arbitrary choices of hat matrices.For each , define and . Collect these in the matrices

| (2.4) |

The jackknife K-statistic can then be defined

| (2.5) |

I will show that, under appropriate conditions on the hat matrix, , and moment bounds, I will show that the limiting distribution of under is . For exposition, I will largely focus on the case where , in which case the form of the test statistic simplifies to . The extension to is not immediate but is possible under strengthened moment conditions and is explored in Section 5.

3 Limiting Behavior with a Single Endogenous Variable

The limiting behavior of the test statistic is analyzed via a direct Gaussian approximation technique. When there is a single endogenous variable this approach can be considerably simplified. In this section, I detail the approach and take advantage of the simplified analysis to characterize the limiting behavior of the test statistic under local alternatives to . This direct approach has the advantage of not relying on any particular central limit theorem, which allows a great deal of flexibility in the choice of hat matrix .For each , let be jointly Gaussian random variables generated (i) independently of each other and the data and (ii) with the same mean and covariance matrix as . In addition, define .The goal will be to show that the quantiles of can be approximated by corresponding quantiles of the Gaussian statistic,

| (3.1) |

Since uncorrelated jointly Gaussian random variables are independent, under the vector is mean zero and independent of . The null distribution of conditional on any realization of is then and so its unconditional null distribution is also .

3.1 Interpolation Approach

Error arising from estimation of prevents immediate comparison of the distribution of to the distribution of . As such, I begin by considering the distribution of an infeasible statistic, , which could be constructed if were known to the researcher:

where . To show that the distribution of can be approximated by the distribution of , I adapt Lindeberg’s interpolation method, first introduced by Lindeberg (1922) in an elegant proof of the central limit theorem. This method consists of one-by-one replacment of the terms in the expression of with their Gaussian analogs, , and bounding the resulting one-step deviations.Applying the interpolation method directly on the statistics and , however, is not tractable as it requires bounding expectations of derivatives with respect to terms in the denominator. When identification is weak, the denominators of and may both be arbitrarily close to zero with positive probability. Derivatives with respect to terms in the denominators thus may not have finite expectations.Instead, I consider a different approach. For a scaling factor , introduced below, define the scaled numerators and denominators

and for any , define the decomposed statistics

Since implies and since almost surely, the events are almost surely equivalent to the events . The decomposed statistics no longer have denominators to be dealt with and are tractable for the interpolation argument. I show for any , the space of all thrice continuously differentiable functions with bounded derivatives up to the third order, that there is a fixed constant such that

| (3.2) |

where and . By taking to be a sequence of functions approximating the indicator function, , the result in (3.2) can be used to show that the cumulative distribution function (CDF) of the infeasible statistic can be approximated by the CDF of the Gaussian statistic at each point . A Glivenko-Cantelli type argument is then be applied to show the approximation holds uniformly over all points on the real line.The Lindeberg interpolation argument on the decomposed test statistics makes use of the fact that the numerator and denominator of the Gaussian test statistic are functions of quadratic forms in the random vectors and .111See Pouzo (2015) for another example of the Lindeberg interpolation method applied to approximate thedistribution of quadratic forms.Moving from approximation of expectations of smooth functions to approximation of the CDF relies on a particular anticoncentration bound on . I show that that this bound can be established under either weak or strong identification. This allows for the limiting null distribution of the test statistic under various identification regimes to be derived via a unifying argument. Additionally, even though may all have nonnegligible distributions when identification is weak, the interpolation argument does not require any of these to individually converge in distribution or probability anywhere stable. This allows for a wide range of possible hat matrices to be used in constructing the first stage estimates, . In particular, no assumption need be made on the number of instruments used to construct nor any requirement imposed that the first-stage estimates are consistent.I now detail the assumptions needed for the argument.Define and , noting and .In what comes below can be considered an arbitrary constant that may be updated upon each use but that does not depend on sample size .

Assumption 3.1 (Moment Conditions).

There is a fixed constant such that (i) , and (ii) for any such that , .

Assumption 3.2 (Balanced Design).

(i) For the following is bounded away from zero, ; (ii) ; and (iii) the following ratio is bounded away from zero: where represents the largest eigenvalue of the matrix .

Assumptions 3.1 and 3.2 allow characterization of the null distribution of .Assumption 3.1 imposes light moment conditions on the random variables and , which in turn imply restrictions on and . In particular, Assumption 3.1(i) imposes that and have finite means while Assumption 3.1(ii) bounds, both from above and away from zero, the first through sixth central moments of the random variables.Assumption 3.2(i) requires that the average second moment of the infeasible first-stage estimators be on the same order as the maximum first-stage estimator second moment. This is imposed mainly to rule out hat matrices that are all zeroes or nearly all zeros so that the effective number of observations used to test the null is growing with the sample size. Remark 3.1 below discusses how this assumption and Assumption 3.2(ii) may be verified in practice. Remark 3.2 compares this balanced design assumption to that in the many-instruments literature (Crudu et al., 2021; Mikusheva and Sun, 2021; Matsushita and Otsu, 2022; Lim et al., 2022), noting that their balanced design neither implies nor is implied by the one in this paper.Assumption 3.2(ii) requires that the maximum leverage of any observation be bounded. When is symmetric, it is automatically satisfied under Assumption 3.1(i) and the definition of .222To see this, notice that . By Assumption 3.1, is bounded from below by . Inverting this chain of inequalities yields that is bounded from above uniformly over all .The scaling factor captures both the “size” of the elements in the hat matrix and the strength of identification. If elements of the hat matrix are on the same order as a constant, one would expect under strong identification () while under weak identification ().Assumption 3.2(iii) can be viewed as a technical requirement that there be more than one “effective” instrument in the hat matrix.333In the case of a standard projection matrix (no deleted diagonal), Assumption 3.2(iii) would be satisfied whenever . This condition can be easily verified in practice by examining the eigenvalues of .In addition to characterizing the limiting distribution of under , I also examine the behavior of in local neighborhoods of the null. These local neighborhoods are characterized by the local power index , defined below, as well as an additional regularity condition that restricts the size of relative to .

Assumption 3.3 (Local Identification).

(i) The local power index is bounded, ; and (ii) .

Under , Assumption 3.3 is trivially satisfied since and . The local power index is the second moment of the scaled numerator, and is a measure of the association between the true first stage i and the first-stage estimates . In Section 4, I discuss how the strength of this association is related to the power of the test under local alternatives. Proposition 3.1 below shows that when Assumption 3.3(ii) holds, implies that the test based on the infeasible statistic is consistent.Assumption 3.3(ii) is an additional technical condition that requires that the maximum value of be on the same or lesser order than the maximum value of . Using the moment bounds in Assumption 3.1 and Assumption 3.2(ii) one can verify that Assumption 3.3(ii) is equivalent to the existence of constants such that

for all . It is always satisfied whenever is in a -neighborhood of zero in the sense that for all and some constant .In general, Assumption 3.3(ii) can be roughly interpreted as requiring the local neighborhoods of considered to be those in which the means of are of the same or lesser order than the means of .Under Assumptions 3.1, 3.2 and 3.3, I establish a main technical lemma stating that the CDF of the infeasible statistic, , can be uniformly approximated by the CDF of the Gaussian statistic, . This result does not require to have a fixed limiting distribution.

Lemma 3.1 (Infeasible Uniform Approximation).

Suppose that Assumptions 3.1, 3.2 and 3.3 hold. Then,

I additionally show that the test based on the statistic is consistent whenever the power index diverges, , and Assumption 3.3(ii) holds.

Proposition 3.1 (Consistency).

The dependence of the consistency result on Assumption 3.3(ii) is a nontrivial restriction because of the bias taken on in constructing . In particular, against certain alternatives it is possible that for all even under strong identification. This is an extreme case, however. In general, bias in does not imply a violation of Assumption 3.3(ii), which requires only that the size of be of a weakly greater order than that of . Moreover, as discussed in Remark 3.5, Proposition 3.1 does not necessarily rule out consistency when but Assumption 3.3(ii) fails.Regardless, bias taken on in constructing has consequences for the power of the test in finite samples. This is particularly true when the mean of is of a lesser order than that of as will be discussed in Section 4. To rectify this deficiency in tests based on the jackknife K-statistic, I suggest a thresholding test that decides whether to use the jackknife K-statistic or the sup-score Belloni et al. (2012) statistic based on the value of the conditioning statistic. This conditioning statistic, in turn, is based on a test statistic for the null hypothesis that for all .

3.2 Limiting Behavior of Test Statistic

The final step in characterizing the limiting behavior of the feasible test statistic is to show that the difference between the infeasible and feasible statistics is negligible. I begin with a technical lemma stating that the difference between and is asymptotically negligible whenever the differences between the scaled numerators and the scaled denominators are asymptotically negligible. Define these differences:

| N | |||

| D |

Lemma 3.2.

Suppose Assumptions 3.1, 3.2 and 3.3 hold and . Then .

While Lemma 3.2 is a simple statement, it is not obvious. In particular, showing that the difference between the infeasible and feasible statistics is negligible requires showing that is bounded in probability, where represents the scaled denominator of . In a standard analysis, this would be done by arguing that converges in distribution to a stable limit and then applying the continuous mapping theorem.444This is the approach taken by Kleibergen (2002, 2005) This approach is not applicable here as neither the scaled numerator nor the scaled denominator has a limiting distribution.Instead, I directly show that is bounded in probability by showing for any sequence . This is done by first establishing that quantiles of can be approximated by quantiles of , the scaled denominator of . If the variance of is bounded away from zero, its density can also be bounded with new bounds on Gaussian quadratic form densities from Götze et al. (2019), which yields the result. Otherwise, if , the result holds by an application of Chebyshev’s inequality and from Assumption 3.2(i).This particular anticoncentration bound for is also important in the proof of Lemma 3.1 to establish anticoncentration for the decomposed Gaussian test statistic.Lemma 3.2 allows the researcher to use alternate choices of estimators for , so long as they can verify that . Below, I verify that this condition can be satisfied for the -penalized estimation procedure proposed in (2.2). This requires a strengthened moment condition on . Given a random variable and the Orlicz (quasi-)norm is defined

Random variables with a finite Orlicz norm for some are termed -sub-exponential random variables (Gotze et al., 2021; Sambale, 2022). This class encompasses a wide range of potential distributions including all bounded and sub-Gaussian random random variables (with ), all sub-exponential random variables such as Poisson or noncentral random variables (with ), as well as random variables with “fatter” tails such as Weibull distributed random variables with shape parameter .

Assumption 3.4 (Estimation Error).

(i) There is a fixed constant such that ; (ii) The basis terms are bounded, for all ; (iii) the approximation error satisfies ; (iv) the researcher has access to an estimator of that satisfies ; (v) the following moment bounds hold

-

(va)

-

(vb)

Assumption 3.4(i) strengthens the moment condition on to require that be in the class of -sub-exponential random variables. While this condition is more restrictive than the moment condition in Assumption 3.1, as discussed above, it still allows for a wide range of potential distributions. Assumption 3.4(ii) is a standard condition in -penalized estimation. At the cost of extra notation, it can be relaxed and the sup-norm of the basis terms can be allowed to grow slowly with the sample size to accommodate bases such as normalized b-splines or wavelets. Assumption 3.4(iii) is a bound on the rate of decay ofthe approximation error, similar to the approximate sparsity condition of Belloni et al. (2012).Assumption 3.4(iv) is a high-level condition on the rate of consistency of the parameter estimate in the norm. This can be verified under approximate sparsity for both the LASSO estimator in (2.2) or post-LASSO procedures based on refitting an unpenalized version of (2.2) only using the basis terms selected in a LASSO first stage. See Belloni et al. (2012); van der Greer (2016); Tan (2017), and Chetverikov and Sørensen (2021) for references under various choices of penalty parameter. This condition allows for the dimensionality of the basis terms, , to grow near exponentially as a function of the sample size. Following the analysis of Tan (2017) one can see that, under appropriate choice of penalty parameter, this may be satisfied as long as , where the sparsity index denotes the number of nonzero elements of .Assumption 3.4(v) is a strengthening of the definition of local neighborhoods and can be interpreted similarly to Assumption 3.3(ii). Since the moment conditions in Assumption 3.4(va,vb) hold with replaced with , Assumption 3.4(v) can be interpreted as requiring that is on the same order as for all and . As with Assumption 3.3(ii), it is trivially satisfied under or, using the fact that , whenever is in a -neighborhood of zero.Under Assumptions 3.1, 3.2, 3.3 and 3.4, I establish that the difference between the infeasible and feasible statistics can be treated as negligible when the estimation procedure proposed in (2.2) is used.

Lemma 3.3.

Suppose that Assumptions 3.1, 3.3, 3.2 and 3.4 hold. Then .

Lemmas 3.1, 3.2 and 3.3 are combined for the main result, local approximation of the distribution of the feasible test statistic, , by the distribution of the Gaussian statistic, . An immediate corollary is that the limiting null distribution of is .

Theorem 3.1 (Uniform Approximation).

Suppose that Assumptions 3.1, 3.3, 3.2 and 3.4 hold. Then

Corollary 3.1 (Size Control).

Suppose that Assumptions 3.1, 3.2 and 3.4 hold. Then, under , .

If the limiting had a fixed distribution under ,Theorem 3.1 would follow immediately from Lemmas 3.1, 3.2 and 3.3, and an application of Slutsky’s lemma. However, under , there is nothing preventing the distribution of changing with the sample size. Instead I establish Theorem 3.1 directly using the fact that both and are bounded in probability and that has a density that is bounded uniformly over .While does not have a fixed distribution, examining its behavior is still tractable and allows for insight into the power properties of the jackknife K-test. In the next section, I use this result to analyze the local power of the proposed test. To improve power against certain alternatives, I suggest a combination with the sup-score statistic of Belloni et al. (2012).

Remark 3.1.

A sufficient condition for Assumption 3.2(i) is that there is some fixed quantile such that . In practice this can be verified by checking that there is some quantile such that both

| (3.3) |

are bounded away from zero. Similarly, Assumption 3.2(ii) can be verified by checking that is bounded from above.

Remark 3.2.

The balanced-design condition in Assumption 3.2(i) is neither weaker nor stronger than that in the many instruments literature (Crudu et al., 2021; Mikusheva and Sun, 2021; Matsushita and Otsu, 2022; Lim et al., 2022). These papers require that the projection matrix satisfies for some value and all . Since is idempotent, for some implies that for .555Since is idempotent, . This would not violate Assumption 3.2 if one were to take such that ; is allowed for a constant share of . Conversely, if the instruments are fixed or growslowly, it is possible to construct a projection matrix of rank where is bounded away from one for all , but “most” of the rows are zero. I view this as a theoretical edge case, however, that seems unlikely to result from real data.

Remark 3.3.

The Lindeberg interpolation method allows me to give a nearly uniform explicit bound on the Gaussian approximation error. In particular, using the bound in (3.2), I show that for any fixed value ;

where is a constant that depends only on . Lemma 3.1 makes use of the fact that the limiting statistic is bounded in probability and extends this result to show that the approximation error tends to zero uniformly over the real line. While it does not account for estimation error in , obtaining an explicit bound reflects an improvement over the original analyses of K-statistics in Kleibergen (2002, 2005). These original studies rely on continuous mapping theorems to obtain the limiting chi-squared distributions, making the rate of decay of the approximation error difficult to analyze.

Remark 3.4.

The interpolation argument relies on the fact that the first and second moments of are the same as the first and second moments of to match the first and moments of one-step deviations with Gaussian analogs. Without the jackknife form of , these one step deviations would additionally contain cross-terms such as , for . While the first moment of this cross-term is matched by the first moment of the Gaussian analog, , the second moment is not matched. This is manageable, however, so long as the terms are “small.” An example of when the terms are small is when is taken to be the OLS projection matrix, , and the number of instruments satisfies . See Appendices A and E for details.

Remark 3.5.

Proposition 3.1 does not necessarily rule out that a test based on is consistent when but Assumption 3.3(ii) fails to hold.The proof of Proposition 3.1 relies on showing that, when and Assumption 3.3(ii) holds, while and are bounded. These facts can be combined to show that for any fixed . When Assumption 3.3(ii) fails, may imply that as well, making the limiting behavior of the test difficult to analyze. There is reason to believe that this issue can be overcome, Andrews et al. (2004) show that the K-statistic of Kleibergen (2002) is consistent against fixed alternatives under strong identification. However, a full consistency result is not pursued here and left to future work.

Remark 3.6.

Approximate sparsity of may be a particularly palatableassumption in cases where the instrument set is generated by functions of a smaller initial set of instruments, as in Angrist and Krueger (1991); Paravisini et al. (2014); Gilchrist and Sands (2016), and Derenoncourt (2022). In these cases, the dimensionality of the basis, , may not need to be much larger than the dimensionality of the instruments, , to provide a good approximation of .Interestingly, if taking provides a good approximation of , the Tan (2017) result suggests that consistency of is achievable under even if is fully dense. This requirement is weaker than the requirement of the standard K-statistic.

4 Improving Power against Certain Alternatives

Using the characterization of the limiting behavior of the test statistic derived in Section 3, I analyze the local power properties of the test. Unfortunately, against certain alternatives the test statistic may have trivial power, a deficiency shared with the K-statistics of Kleibergen (2002, 2005). To combat this, I propose a simple combination with the sup-score statistic of Belloni et al. (2012) based on a thresholding rule.

4.1 Local Power Properties

In local neighborhoods of , as defined in Assumptions 3.3 and 3.4, Theorem 3.1 implies that the limiting behavior of can be analyzed by examining the behavior of the Gaussian analog statistic, . Conditional on the vector , the distribution of is nearly non-central with noncentrality parameter , :

Under local alternatives, the terms so that and , where

| (4.1) |

The numerator of suggests that power is maximized when the first-stage estimate is close to the true first stage value i. Indeed, when errors are homoskedastic is maximized by setting reflecting the classical result of Chamberlain (1987). The denominator of suggests that having first-stage estimates with low second moments may increase power. This guides the recommendation for the use of -regularization in constructing the hat matrix, .Unfortunately, estimators of i based on may not be close to i under . This is because the mean of will in general differ from i

This deficiency is inherited from the similarity of the statistic to the K-statistic.As pointed out by Moreira (2001), this need not be an issue as long as there is a fixed constant such that for all . However, in general, this will introduce bias into the first-stage estimates under . The power implications of this bias are particularly pronounced when is a constant . In this case, , and thus , will equal zero for each , and the statistic will select a direction completely at random to direct power into.111Andrews et al. (2006) and Andrews (2016) point out this deficiency in the context of the K-statistics of Kleibergen (2002, 2005).

4.2 A Simple Combination Test

To combat this loss of power for tests based on the K-statistic, a common strategy is to combine the K-statistic with the Anderson-Rubin statistic based on a conditioning statistic. While the Anderson-Rubin statistic does not have optimal power on its own, it has the benefit of directing power equally in all directions avoiding the pitfalls of the K-statistic which lacks power in certain directions. Prominent examples of such tests are the conditional likelihood ratio test of Moreira (2003), the GMM-M test of Kleibergen (2005), and the minimax regret tests of Andrews (2016). These combinations make use of the fact that the Anderson-Rubin statistic is asymptotically independent of both the K-statistic and the conditioning statistic.Unfortunately, the asymptotic validity of these tests under heteroskedasticity is based on the assumption that , which may not reasonably describe many settings discussed above. Instead, to improve the power of tests based on the jackknife K-statistic, I consider a simple combination with the sup-score statistic of Belloni et al. (2012). The test based on the sup-score statistic (4.2) is similar in spirit to the Anderson-Rubin test but controls size even when grows near exponentially as a function of the sample size.

| (4.2) |

A size test based on the sup-score statistic rejects whenever where, for iid standard normal and generated independently of the data, is the simulated multiplier bootstrap critical value:

As with the Anderson-Rubin test, tests based on the sup-score statistic may have suboptimal power properties in overidentified models as it does not incorporate first-stage information. However, the sup-score statistic does retain the benefit of directing power evenly in all directions, avoiding pitfalls of tests based on against certain alternatives.The combination test will be based on an attempt to detect whether the alternative is such that for all . When this is the case, the test based on will choose a direction completely at random to direct power into. It would then be optimal for the researcher to test the null hypothesis using the sup-score statistic. Detection of whether is based on the conditioning statistic:

| (4.3) |

Under the assumption that for all , quantiles of the conditioning statistic can be simulated analogously to the sup-score critical value.For a new set of iid standard normal and generated independently of the data, and for any , define the conditional quantile

| (4.4) |

Depending on the value of the conditioning statistic, the thresholding test decides whether the test based on or one based on should be run.

| (4.5) |

for some cutoff , which I take in the simulation study and empirical exercise to be the 75th quantile of the distribution of under the assumption that .To show that the thresholding test controls size, I compare the rejection probability to that of a Gaussian analog. In addition to , defined in (3.1), define the Gaussian analogs of and the conditioning statistic :

where, as in Section 3, are generated independently of each other and the data following a Gaussian distribution with the same mean and covariance matrix as . Since under , the statistics and are independent under the null. Similarly, the null distribution of is the same conditional on any realization of ; it is also independent of under the null. The Gaussian analog thresholding test decides whether the researcher should run a test based on or depending on the value of as in (4.5).The test statistics and are only marginally independent of the conditioning statistic under the null. This limits the ways in which the test statistics can be combined using the conditioning statistic while still controlling size. This marginal independence in the Gaussian limit is enough, however, for the asymptotic validity of the thresholding test, . To establish that the behavior of the pairs and can be approximated by the behavior of and , respectively, I rely on the following assumption:

Assumption 4.1 (Combination Conditions).

Assume that (i) there is a such that ; (ii) ; and (iii) .

Assumption 4.1(i) is a strengthening of the moment bound on similar to that of Assumption 3.4(i). As discussed, while more restrictive than the condition in Assumption 3.1, this still allows for a wide range of potential distributions for . Assumption 4.1(ii) requires that the number of observations used to test via the conditioning statistic and the number of observations used to test the null hypothesis via the sup-score test are both growing with the sample size. It can be verified by looking at the hat matrix and the instruments. Finally, Assumption 4.1(iii) is a light requirement on the number of instruments needed for the validity of the sup-score test. It allows the number of instruments to grow near exponentially as a function of sample size.

Theorem 4.1.

Suppose Assumptions 3.1, 3.2, 3.3, 3.4 and 4.1 hold. Then,

-

1.

the test based on has asymptotic size for any choice of cutoff , and

-

2.

if for all , there exist sequences and such that with probability at least ,

where denotes the probability with respect to only the variables .

The first part of Theorem 4.1 establishes the asymptotic validity of the thresholding test for any choice of cutoff . The proof of this statement follows the logic outlined above. The second part of Theorem 4.1 establishes the validity of the multiplier bootstrap procedure to approximate quantiles of the conditioning statistic. It follows directly from results in Belloni et al. (2018) after verifying that the conditions needed for error taken on from estimation of can treated as negligible under Assumption 3.4.In Section 7, I investigate the power properties of the thresholding test via simulation study. I find that combining the statistic with the sup-score statistic based on improves power against distant alternatives and helps alleviate a power decline suffered by the statistic against a particular set of alternatives.

Remark 4.1.

As mentioned by Andrews (2016) in the context of the standard K-statistic, this attempt to rectify the power deficiency via this particular conditioning statistic is not perfect. In particular, under heteroskedasticity, the means of the partialed-out endogenous variables, , may not be scaled versions of the true first stages. However, as long as , one can still expect to be related to the true fist stage i and for the test to have nontrivial power. Moreover, in light of the dependence of the consistency result in Proposition 3.1 on Assumption 3.3(ii), in the case where for all it may be particularly important to avoid using the jackknife K-statistic to test .

5 Analysis with Multiple Endogenous Variables

To analyze the limiting behavior of the test statistic when , I follow the basic idea of Section 3, which is to show that quantiles of the jackknife K-statistic can be approximated by analogous quantiles of the Gaussian statistic:

where are Gaussian with the same mean and covariance matrix as and for define , , and

As in Section 3, notice that, since uncorrelated random variables are independent, under the vector is mean zero and independent of . Conditional on any realization of the statistic then follows a distribution, and thus, its unconditional distribution is also .In addition to characterizing the local behavior of with multiple endogenous variables, I show that the thresholding test of Section 4.2 can be applied with multiple endogenous variables with a generalized conditioning statistic.

5.1 Modified Interpolation Approach

As with a single endogenous variable, error taken on from the estimation of prevents immediate comparison of to . Instead as an intermediate step consider showing that the quantiles of can be approximated by corresponding quantiles of where is an infeasible statistic:

for and defined the same way as and in (2.4), respectively, but using the true values in place of their estimates .When there are multiple endogenous variables, , I cannot take advantage of the simplified form of the test statistic to establish this approximation as in Section 3. Instead I deal directly with the test statistics themselves. Consider functions that approximate the indicators , where is arbitrary and is a scaling factor inversely proportional to the quality of the approximation but positively proportional to the derivatives of . The goal is to show, for a sequence tending to zero, that

| (5.1) |

The classical interpolation argument of Lindeberg (1922) would attempt to show (5.1) by one-by-one replacement of each pair, , in the expression of with its Gaussian analog, , and bounding of the size of each of these deviations. As mentioned in Section 3, the problem arises as the derivative of the test statistic, , with respect to terms in the denominator matrix, , may be as large as the inverse of the minimum eigenvalue of the denominator matrix. When identification is sufficiently weak, the denominator matrix will have a nonnegligible distribution and the inverse of its minimum eigenvalue may not have finite moments.To get around this, I modify the argument by considering a “data-dependent” choice of approximation parameter . This choice of approximation parameter inversely scales with the determinant of the denominator matrix and thus, since the determinant is the product of the eigenvalues, inversely scales with the minimum eigenvalue.111The determinant has the benefit of being a smooth function of elements of the matrix. This makes it nicer to work with than the minimum eigenvalue itself, which loses differentiability when the dimension of its eigenspace is larger than one. Geometrically, this approach can be thought of as “stretching out” the function in directions where the minimum eigenvalue of the denominator matrix is close to zero. Since the overall derivatives of with respect to depend on the product of derivatives with respect to the test statistic andderivatives of , which scale inversely with the approximation parameter, this adjustment of the approximation parameter allows control of the overall derivative. Details of this approach can be found in Appendix D.This approach relies on stronger moment conditions, which I detail below. These strengthened moment conditions are needed mainly needed to bound moments of the determinant of the denominator matrix. For all let , noting that . Recall also the definition of , which is equal to .

Assumption 5.1 (Moment Conditions).

Assume (i) there are constants and such that and , and (ii) .

Assumption 5.2 (Balanced Design).

(i) For any let ; then, the minimum eigenvalue of the following matrix is bounded away from zero:

(ii) ; and(iii) the following ratio is bounded away from zero: where represents the largest eigenvalue of the matrix .

Assumption 5.1(i) strengthens Assumption 3.1 to require that the random variables , and thus, by extension, are -sub-exponential. As discussed below Assumption 3.4 this is more restrictive than the finite sixth moments needed to establish Lemma 3.1 but still allows for a wide range of possible distributions. Assumption 5.1(ii) is a light regularity condition requiring that the random variables be linearly independent.Assumption 5.2(i) is a natural extension of Assumption 3.2(i) to the setting where . It requires that the average second moment of any linear combination of the first-stage estimates is proportional to the maximum second moment of the same linear combination. Assumption 5.2(ii,iii) are the same conditions as Assumption 3.2(ii,iii) and can again be implicitly thought of as requiring that the maximum leverage of any one observation be bounded and there be than two effective instruments in the hat matrix. Assumption 5.2 thus reduces to Assumption 3.2 when .

Assumption 5.3 (Local Identification).

(i) The local power index is bounded for

(ii) for all .

Lemma 5.1 (Infeasible Uniform Approximation).

Suppose that Assumptions 5.1, 5.2 and 5.3 hold. Then

5.2 Limiting Behavior of Test Statistic

Having derived the limiting behavior of the infeasible statistic, I next present a high-level condition under which estimation error taken on from estimation of can be treated as negligible. I then verify this high-level condition for the -regularized estimators proposed in (2.2). For any define the scaled differences

| N,ℓ | |||

| D,ℓ |

As long as these scaled differences tend to zero, Lemma 5.2 shows that the difference between the feasible and infeasible test statistics converges to zero:

Lemma 5.2.

Suppose that Assumptions 5.1, 5.2 and 5.3 hold and that for all . Then .

As with Lemma 3.2, while Lemma 5.2 is a simple statement, it is not immediate. In particular, establishing Lemma 5.2 requires showing that is bounded in probability, where represents a scaled version of the denominator matrix. This requires some work as the scaled denominator matrix is not required to converge in distribution to a stable limit. Instead I directly show that is bounded in probability by showing that for any sequence .To do this, I first demonstrate that it is sufficient to show that for any and fixed . I then establish the claim for an arbitrary choice of . As in Lemma 3.2 I do this by comparing the scaled quadratic form of the denominator matrix to a Gaussian analog and then establishing the corresponding result for the Gaussian analog. This corresponding result is again also useful for establishing the validity of the interpolation approach with a dynamic choice of approximation parameter.I state conditions under which holds for the -regularized estimation procedure proposed in (2.2). These conditions are equivalent to those in Assumption 3.4 but hold for each the estimation procedures.

Assumption 5.4 (Estimation Error).

(i) The basis terms are bounded, for all ; (ii) the approximation error satisfies ; (iii) the researcher has access to estimators of that satisfy for each ; and (iv) locally identified in the sense that

-

(iva)

-

(ivb)

Under Assumption 5.4 the conditions of Lemma 5.2 are satisfied. If these conditions are satisfied, Lemmas 5.1 and 5.2 can be combined to analyze the behavior of statistics in local neighborhoods of the null.

Theorem 5.1 (Uniform Approximation).

As in Lemma 3.1, the result in Theorem 5.1 does not require to have a stable limiting distribution under .

5.3 Improving Power against Certain Alternatives

As discussed in Section 4.1, tests based on the jackknife K-statistic may suffer from suboptimal power properties. These properties are particularly bad whenever for some and all . To improve power in this direction, I propose a generalization of the thresholding test in Section 4.2 based on the conditioning statistic

| (5.2) |

The conditioning statistic attempts to detect whether, for some , for all . Under the assumption that , quantiles of can be simulated by multiplier bootstrap. Let be generated iid standard normal independent of the data and for any , define the conditional bootstrap quantile:

Based on the value of the conditioning statistic the researcher can decide whether to run a test based on or a test based on the sup-score statistic .

| (5.3) |

As with Theorem 4.1, I show the asymptotic validity of the thresholding test by first establishing that quantiles of and can jointly be approximated by Gaussian analogs and then using the marginal independence of the Gaussian analog testing and conditioning statistics under the null; and under .

Theorem 5.2.

The first part of Theorem 5.2 establishes the validity of the test based on the thresholding statistic for any choice of cutoff . In practice, I recommend taking the cutoff, , to be the 75th quantile of the distribution of under the assumption that for all and . The second part of Theorem 5.2 establishes that this quantile can be simulated via the multiplier bootstrap procedure described above.

6 Empirical Application

I apply the testing procedures proposed in this paper to the data of Gilchrist and Sands (2016), who seek to determine the effect of social spillovers in movie consumption. The sample consists of all 1,671 opening weekend days111An opening weekend day is a Friday, Saturday, or Sunday of opening weekend. between January 1, 2002 and January 1, 2012. For each opening weekend, the authors observe gross ticket sales for all movies wide released in theaters in the United States.222A wide released movie is any movie that ever shows on 600 or more screens. The data are obtained through Box Office Mojo, a subsidiary of the Internet Movie Database (IMDb). To focus on movies in theaters long enough for social spillovers to be a relevant factor, the authors consider only movies that remain in theaters for at least six weeks.The outcome variables of interest are gross ticket sales of movies that opened in a given weekend in the second through sixth weeks of their run, while the endogenous variable is the gross ticket sales of a movie in its opening weekend. To control for seasonal periodicity in both the supply of and demand for movies, a vector of date controls are included. Formally, Gilchrist and Sands (2016) are interested in the parameters , from the linear IV model(s):

| (6.1) |

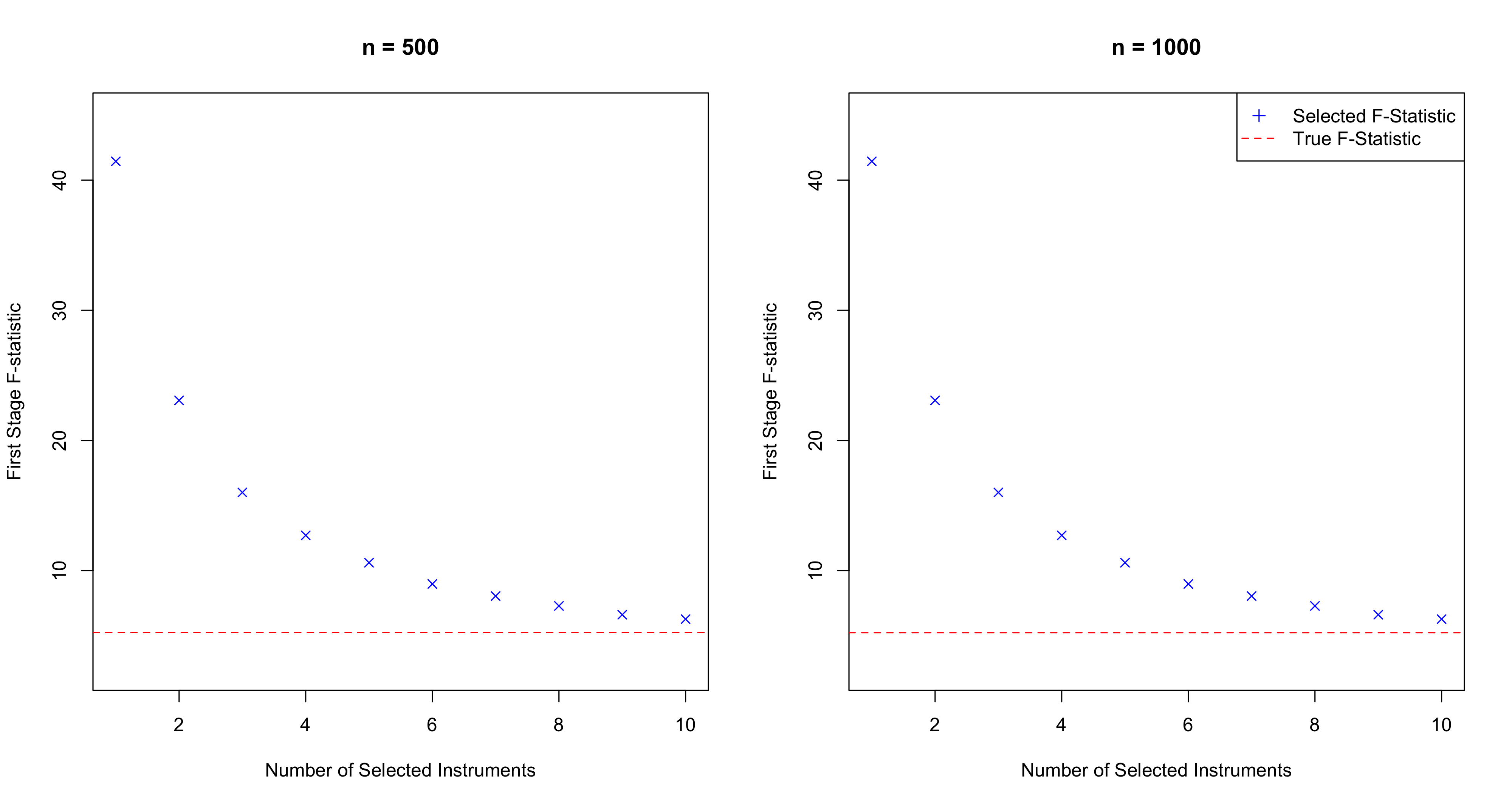

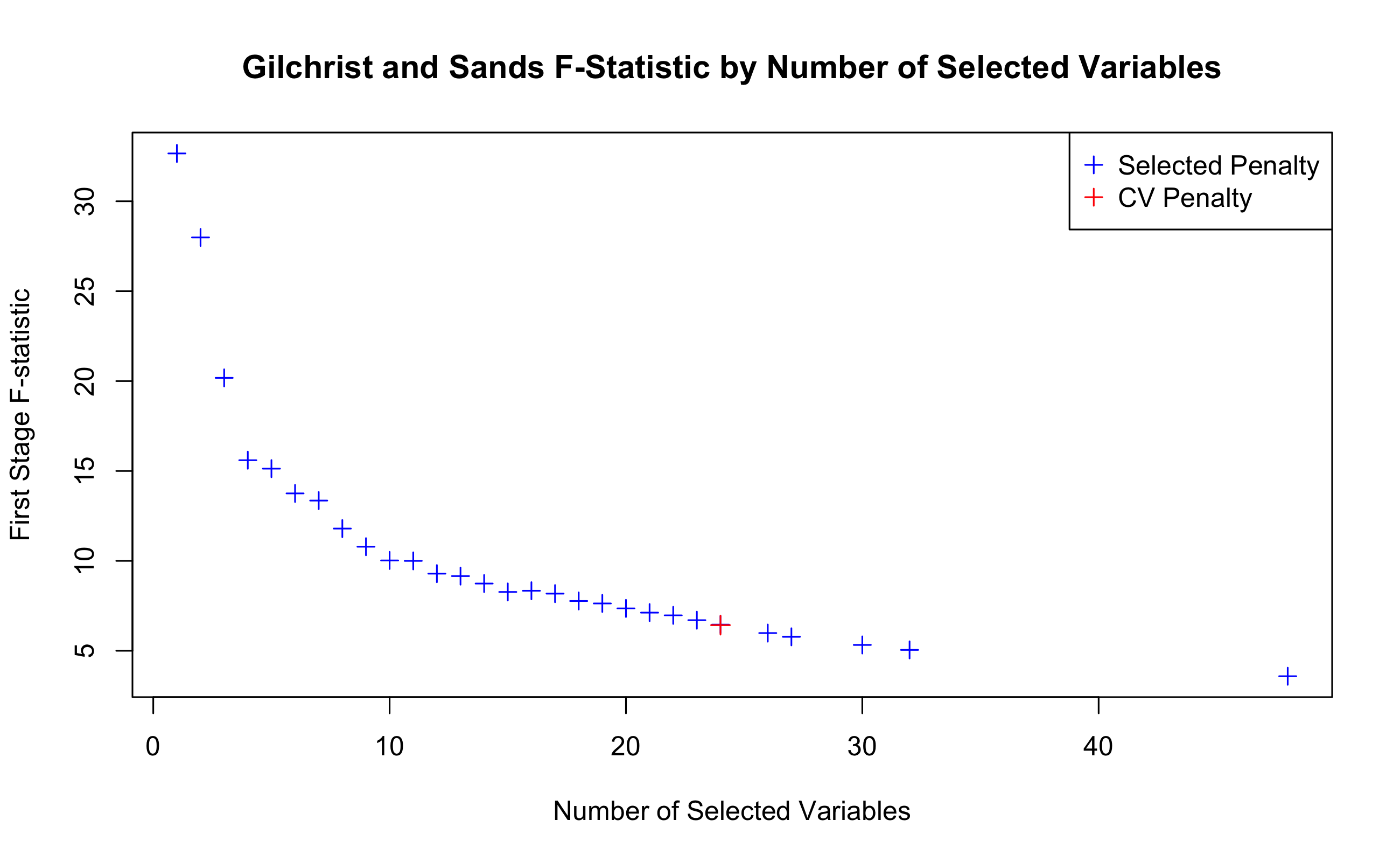

where, for , represents gross national ticket sales, after the partialing out of date controls and a constant, days after day , of movies that opened on the opening weekend of . The variable denotes the cumulative national ticket sales from the second through sixth running weekends of movies who opened in weekend , after the partialing out of date controls and a constant.The parameter represents the social spillover effect of strong opening weekend sales on sales in later weeks; more people seeing a movie on its opening weekend will mean more people telling their friends about the movie potentially leading to larger sales later on.Because movies with high first-week sales may have high sales in succeeding weeks for reasons other than word of mouth spillover effects (e.g the movie may receive positive critical reviews prerelease or be part of a previously successful franchise), the parameter cannot be plausibly recovered from ordinary least squares regression of on . To identify the structural parameter, Gilchrist and Sands (2016) employ a vector of nationally aggregated weather measures. These weather measures reflect the proportion of movie theaters experiencing a particular type of weather on a particular weekend. The measures include the proportion of movie theaters experiencing maximum temperatures in Fahrenheit bins on the interval , the proportion of movie theaters experiencing precipitation levels in 0.25 inch per hour increments on the interval , and the proportions of theaters experiencing any type of snow and of theaters experiencing any type of rain.The nationally aggregated weather conditions on opening weekend days serve as plausibly exogenous instrumental variables, affecting ticket sales in later weeks only through their effect on opening-weekend-day sales. Same-day weather conditions may also have an effect on movie ticket sales: when the weather is particularly nice, people may be more inclined to engage in outdoor activities while in poorer, weather people may choose to stay indoors and see a new movie. Putting together the nationally aggregated weather measures leaves Gilchrist and Sands (2016) with a vector of 52 instrumental variables. After the partialing out a constant and the date controls, four of these are linearly dependent. I discard these and work with the remaining 48 partialed-out instruments in my analysis.To handle the large number of instruments, the authors follow Belloni et al. (2012) and employ a post-LASSO estimate of the first stage. In their main specifications, they set the first-stage penalty parameter so that the number of instrument selected is one, two, or three. The resulting first-stage F-statistics using the selected instrument(s), 38.80, 25.86, and 20.95, respectively, seem to indicate strong identification.333Typical empirical practice is to use the Wald test when the first stage F-statistic is larger than 10. However, the first-stage F-statistic on the full set of instrumental variables is only 3.80. Moreover, since the LASSO objective is an penalized version of the OLS loss, using the variables selected by LASSO may mechanically lead to higher F-statistics even if the underlying relationship between the instruments and the endogenous variables is weak.Figure 6.1 provides evidence from a simple simulation experiment to demonstrate this. For the simulation experiment I generate an iid sample of 10 instrumental variables, from a normal distribution with a Toeplitz covariance structure, , . The endogenous variable is generated to only have a weak relationship with the instruments , where the first-stage errors are independent standard normals. From this initial set of 10 instrumental variables I generate an additional 55 technical instruments by squaring and taking all interactions between variables in the initial set. These generated instruments are correlated with the initial instruments but do not directly enter the first stage.I then set the LASSO penalty so that only a certain number of instruments are chosen and report the resulting average first stage F-statistics over one thousand simulations. As seen in Figure 6.1, these first-stage F-statistics increase significantly as the number of selected instruments decreases. While the “true” F-statistic, computed with only the 10 initial instruments directly relevant for the first stage, is only 5.234, the average F-statistic on the selected variables can be larger than 40. The persistence of this pattern between sample sizes and suggests that this is not a small-sample issue and that pretesting for weak identifications based on post-LASSO F-statistics may be problematic generally. Figure 6.2 shows how the first stage F-statistic changes with the number of LASSO-selected variables in the Gilchrist and Sands (2016) data. The pattern is similar to that seen in the Figure 6.1 simulation experiment.

Given a lack of clarity on the strength of identification, I seek to validate the results of Gilchrist and Sands (2016) using the weak identification testing procedures proposed in this paper. The setting is particularly suitable for weak IV testing using the jackknife K-statistic. With 48 instruments and a sample size of 1671, , making the tests of Moreira (2003, 2009); Kleibergen (2005), and Andrews (2016) inapplicable. On the other hand, it is unclear whether asymptotic approximations based on will accurately describe the finite-sample distribution of test statistics with 48 instruments. Moreover, since fluctuations in movie theater attendance seem to be largely driven by either particularly cold or particularly hot weather (see Figure 4 in Gilchrist and Sands (2016)), the nuisance parameter is plausibly approximately sparse.Table 6.1 compares the confidence intervals for generated by the jackknife K test to the confidence intervals generated by the sup-score test of Belloni et al. (2012) and the jackknife LM test (JLM) test of Matsushita and Otsu (2022). I form these confidence intervals by running the tests for each on a 300 point grid between zero and two and inverting the results; a point is included in the confidence interval if the test fails to reject the null that at level .For the statistic I use the choice of hat matrix in (2.3) and estimate the auxiliary parameter as in (2.2). The penalty parameter is chosen with leave-one-out cross-validation using the cv.glmnet command from the glmnet package in R (R Core Team, 2021; Friedman et al., 2010). The critical value for the sup-score statistic is simulated using 2,500 bootstrap draws. Confidence intervals based on the combination test, , are not directly reported as the pretesting procedure based on simulating the 75th quantile of as in (4.4) always suggests using the statistic.For reference, I also provide point estimates and standard errors for from Gilchrist and Sands (2016), Table 2. To facilitate comparison, these point estimates and standard errors come from a specification that uses all the instruments in the first stage of a 2SLS procedure. While the Gilchrist and Sands (2016) point estimates are always in the 95% confidence intervals generated by the and JLM tests, the confidence intervals from the identification-robust procedures are significantly wider than those generated with the 2SLS standard errors.Interestingly, the confidence intervals from inverting the jackknife K-test tend to be quite similar to the confidence intervals from the JLM test. This is surprising given the distinct forms of the and the JLM test statistics.For the parameters and , the confidence intervals generated by the sup-score statistic are empty while the sup-score confidence interval for is nearly empty. This is also the case when using the jackknife AR-statistic of Crudu et al. (2021) and Mikusheva and Sun (2021), whose confidence intervals are not reported as they are always empty. With 48 instruments and a single parameter the linear IV model in (6.1) is overidentified and as such the empty confidence intervals could be interpreted as evidence of model misspecification. For the parameter the confidence interval generated by inverting the sup-score statistic is not empty and is instead 36% larger than the confidence interval and 41% larger than the JLM confidence interval. This result suggests that the jackknife K tests and JLM tests may have better power properties than the sup-score test in this setting.

| Parameter | ||||||

|---|---|---|---|---|---|---|

| JLM |

Tables 6.2 and 6.3 repeat the analysis of Table 6.1 but with alternative instrument sets. The confidence intervals of Table 6.2 use only Fahrenheit temperature bins () while the confidence intervals of Table 6.3 include all the instruments used in Table 6.1 and all interactions between the Fahrenheit temperature bins and the other weather measures for a total of 524 instruments.444The instrument set of Table 6.3 does not include interactions between temperature bins nor interactions between other weather measures. For the most part, the confidence intervals generated by inverting the jackknife K-statistic are similar across Tables 6.1-6.3. The confidence intervals for the jackknife LM statistic however, become much narrower when using the largest set of instruments is used. Thisis interesting as the results from the test as well as the power analysis in Section 4 seem to suggest that use of the extra isntruments does not lead to better first-stage estimates. Interestingly, the JLM confidence intervals in for in Table 6.3 do not contain the point estimates for and from Gilchrist and Sands (2016). As with Table 6.1, Tables 6.2 and 6.3 do not report confidence intervals from as these always agree with the confidence intervals and do not report jackknife AR confidence intervals as these are always empty.

| Parameter | ||||||

|---|---|---|---|---|---|---|

| JLM |

| Parameter | ||||||

|---|---|---|---|---|---|---|

| JLM |

7 Simulation Study

In this simulation study, I examine the performance of tests based on the statistic and compare it with that of other tests that may be used in settings where the number of instruments is nonnegligible as a fraction of sample size. I consider a reduced-form data-generating process (DGP) similar to that of Matsushita and Otsu (2022). The outcome variable, , and endogenous variable, , are generated according to

| (7.1) |

where is a transformation of an initial set of instruments generated as described below. The value of varies depending on the strength of identification considered; for strong identification, , while under weak identification, To model heteroskedasticity, the errors are generated , and where and are generated independently of each other and other variables in the model according to a Laplace distribution with location parameter and scale parameter .111The Laplace distribution is often referred to as a “double exponential” distribution. If and are independently distributed according , then has a Laplace distribution with parameters and . If has a Laplace distribution with parameters and , then . Since the limiting distribution of the jackknife K-statistic is exact when the errors are jointly Gaussian and is known, I purposefully avoid normally distributed errors to investigate the quality of asymptotic approximations to the finite-sample behavior of the test. The parameters and control the degree of heteroskedasticity and endogeneity, respectively.

| DGP | Testing Procedure | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| A.Rbn. | JAR | JLM | ||||||||

| 200 | 10 | 0.2 | 0.3 | 0.0516 | 0.0352 | 0.0406 | 0.0406 | 0.0296 | 0.0766 | 0.0502 |

| 0.2 | 0.6 | 0.0542 | 0.0306 | 0.0442 | 0.0384 | 0.0258 | 0.0748 | 0.0400 | ||

| 0.5 | 0.3 | 0.0470 | 0.0338 | 0.0416 | 0.0418 | 0.0238 | 0.0784 | 0.0460 | ||

| 0.5 | 0.6 | 0.0506 | 0.0350 | 0.0416 | 0.0390 | 0.0280 | 0.0676 | 0.0384 | ||

| 30 | 0.2 | 0.3 | 0.0570 | 0.0124 | 0.0422 | 0.0200 | 0.0088 | 0.1000 | 0.0382 | |

| 0.2 | 0.6 | 0.0564 | 0.0126 | 0.0408 | 0.0208 | 0.0124 | 0.0962 | 0.0322 | ||

| 0.5 | 0.3 | 0.0498 | 0.0100 | 0.0366 | 0.0190 | 0.0096 | 0.1090 | 0.0318 | ||

| 0.5 | 0.6 | 0.0562 | 0.0118 | 0.0420 | 0.0216 | 0.0088 | 0.1104 | 0.0292 | ||

| 65 | 0.2 | 0.3 | 0.0542 | 0.0316 | 0.0428 | 0.0370 | 0.0314 | 0.0764 | 0.0420 | |

| 0.2 | 0.6 | 0.0532 | 0.0366 | 0.0418 | 0.0398 | 0.0250 | 0.0780 | 0.0376 | ||

| 0.5 | 0.3 | 0.0474 | 0.0308 | 0.0388 | 0.0362 | 0.0244 | 0.0748 | 0.0354 | ||

| 0.5 | 0.6 | 0.0484 | 0.0324 | 0.0366 | 0.0388 | 0.0282 | 0.0708 | 0.0402 | ||

| 500 | 10 | 0.2 | 0.3 | 0.0590 | 0.0468 | 0.0478 | 0.0516 | 0.0376 | 0.0652 | 0.0452 |

| 0.2 | 0.6 | 0.0530 | 0.0420 | 0.0460 | 0.0466 | 0.0366 | 0.0692 | 0.0434 | ||

| 0.5 | 0.3 | 0.0496 | 0.0370 | 0.0408 | 0.0368 | 0.0338 | 0.0710 | 0.0464 | ||