Consumption Smoothing in Metropolis:

Evidence from the Working-class Households

in Prewar Tokyo

Abstract

I analyze the risk-coping behaviors among factory worker households in early 20th-century Tokyo. I digitize a unique daily longitudinal survey dataset on household budgets to examine the extent to which consumption is affected by idiosyncratic shocks. I find that while the households were so vulnerable that the shocks impacted their consumption levels, the income elasticity for food consumption is relatively low in the short-run perspective. The result from mechanism analysis suggests that credit purchases with local retailers played a role in smoothing short-run food consumption. The event-study analysis using the adverse health shock as the idiosyncratic income shock confirms the robustness of the results. I also find evidence that the misassignment of payday in data aggregation results in a systematic attenuation bias due to measurement error.

Keywords:

consumption smoothing;

credit purchases;

daily budget data;

local retailers;

measurement error;

risk-coping strategy;

risk-sharing

JEL Codes: E21; N35

PRELIMINARY

1 Introduction

Economic theory illustrates the mechanism behind the smoothing of consumption in complete markets (Arrow and Debreu 1954). A series of empirical studies have tested the smoothness of consumption among households in various economies under systematic empirical specification. Evidence shows that markets in contemporary developing countries are often imperfect.111 The early representative literature includes, for example, Townsend (1994), Townsend (1995), Ravallion and Chaudhuri (1997), Grimard (1997), and Fafchamps and Lund (2003). Morduch (1999), Townsend (1995), and Dercon (2004) provide a review of the earlier studies. Attanasio and Pistaferri (2016) and Meyer and Sullivan (2023) provide recent discussions. The households are vulnerable to risk, and the idiosyncratic shocks impact the levels of their consumption because risks are not fully insured in the markets. Therefore, consumption smoothing is an essential agenda for mitigating poverty, especially in developing economies.222Smoothness of consumption is also an important factor in accumulating human capital. For example, Foster (1995) shows that children’s growth patterns are influenced by the inefficiency of the credit markets using the floods of 1988 in Bangladesh as a shock. Rose (1999) investigates the relationship between consumption smoothing and excess losses of girls, revealing that the favorable rainfall shocks in early life increased the survival probabilities of the girls in rural India. Gertler and Gruber (2002) also offers evidence that the smoothing of consumption against health shocks is fairly imperfect in Indonesia.

Historical economies offer experimental environments to investigate the means and degrees of consumption smoothing under less developed societies. Lessons from historical institutions in developed economies shall provide meaningful insights for today’s developing economies. Despite this advantage, little has been known about historical consumption smoothing behaviors, partially because of the lack of data on longitudinal household budgets. This study is the first to digitize a unique daily longitudinal budget survey on working-class households conducted in Tokyo around 1919 and employed systematic econometric methods to explore the consumption behaviors among factory worker households in a representative manufacturing area. The result shows that the full insurance hypothesis is strongly rejected for overall consumption expenditure. The estimated income elasticity is close to that for the rural households in southern India around 1980. This means that the factory worker households in historical metropolis suffered certain consumption losses when they faced idiosyncratic adverse income shocks. However, I also found evidence that while expenses on dispensable categories are likely to be cut in response to the idiosyncratic shocks, expenses on indispensable consumption categories are partially smoothed in the short-run. Mechanism analyses provide suggestive evidence that credit purchases in the local economy played an important role in mitigating adverse idiosyncratic shocks to smooth the consumption.

The first contribution of this study is to offer the first case study of a metropolis in a past developing economy. Urbanization is now a general phenomenon in the world, and the shares of urban population in many developing countries, especially in East Asia, are reaching a similar level to the developed countries (Henderson and Turner 2020). This fact raises the need for a deeper understanding of consumption behavior among urban working households in the process of economic development. Despite this, there is still little evidence for the urban worker households in this literature. While Townsend (1995) offers the results for Bangkok in Thailand between 1975 and 1990, a large part of the existing studies focused on the rural economies (Townsend 1994; Ravallion and Chaudhuri 1997; Gertler and Gruber 2002).333Recent field experimental studies also focus on the village economies (Comola and Prina 2023; Macours et al. 2022). A few exceptional studies provide case studies on the middle-sized contemporary economies (Skoufias and Quisumbing 2005; Aguila et al. 2017). In historical context, Ogasawara (2024) analyzes the factory workers’ households in Osaka City around 1920, which was roughly half the size of Tokyo City (Online Appendix Table A.1). This study focused on a set of homogeneous households in a representative manufacturing area in Tokyo, which provides an ideal empirical setting for testing the risk-sharing behaviors in the target economy.444This setting systematically mitigates bias in estimating income elasticity under the standard risk-sharing regressions due to the heterogeneity in the risk preferences (Schulhofer-Wohl 2011; Mazzocco and Saini 2012). I found suggestive evidence of consumption smoothing using credit transactions with local retailers among working-class households in a historical metropolis.

Macroeconomics literature has investigated the theoretical mechanisms behind the false rejections of the null of the risk-sharing hypothesis. An important factor disturbing the valid statistical inference is measurement error in aggregate data (Cochrane 1991; Nelson 1994; Dynarski et al. 1997; Gervais and Klein 2010). This study reveals a specific generating process of systematic measurement errors in the aggregated income and expenditure series in the survey dataset. In my empirical setting, the factory workers had two paydays in a month: one was set in the middle and the other at the end of the month. Hence, the panel dataset based on the calendar months leads to a substantial mismatch between the timing of earnings and expenses.555If payday is set soon after the initial date in a certain time cell, it does not cause a mismatch in income and expenditure. However, when payday is set just before the initial date in the cell, it leads to measurement errors because the consumption schedule in that cell shall based on the earnings in the previous cell. In other words, this way of matching assumes that the households in a certain cell make their consumption schedule based on “future” earnings. This assumption is unrealistic, particularly in the historical setting. I found that the aggregation ignoring this mechanism causes false rejections in most consumption subcategories due to the attenuation bias. This evidence shows the importance of reflecting the timing of paydays in the aggregation and invokes careful reviews of the existing results based on the aggregate budget dataset, a typical format widely used previously.

The second contribution is to add a new analytical perspective to economic history studies. How working-class households overcame their economic hardships during industrialization has attracted wider attention in economic history. The previous studies have focused on the temporary income sources used to deal with income losses in the late 19th to the early 20th century Britain, showing that working-class households had used a variety of risk-coping institutions.666 Horrell and Oxley (2000) found the important roles of the labor supply adjustments among family members in coping with the income losses of the head in working-class households in late 19th-century Britain. Scott and Walker (2012) also found that interwar British working-class households had access to various institutions such as clothing clubs, hire-purchase, contractural savings, and insurance. The households with less earnings were likely to use credit-based institutions like clubs and hire-purchase, whereas those with higher earnings could use the savings institutions. Kiesling (1996) and Boyer (1997) focused on the risk-coping behaviors among the cotton workers households in Lancashire during the recession due to Civil War. Another strand of literature in financial history provided supply-side (lender-side) evidence on the functions of the micro-financial institutions for the workers (O’Connell and Reid 2005). Weights of evidence from these studies have revealed the roles of historical financial institutions and labor supply adjustments in compensating income losses. However, there is little evidence of how those risk-coping strategies contributed to smooth household consumption. In addition, the previous studies have utilized the cross-sectional variations in income to estimate the elasticities for the temporary income sources.777For example, Horrell and Oxley (2000) and James and Suto (2011) consider the deviations of actual earnings from the predicted earnings to sort out the shocks. While Scott and Walker (2012) considers the smoothness of expenditure rather than income based on the deviation from the mean expenditure, their analyses employed the cross-sectional variations in the pooled cross-sectional sample. This means that the estimated elasticity shows the mean tendency that the households with lower (higher) income were more (less) likely to use a specific risk-coping strategy.888In other words, the elasticity is derived from the observations across different households with different income levels. However, since risk-coping is a concept about the dynamic behavior of a specific household, comparing the different time cells is natural to evaluate the roles of the risk-coping strategies. This study implements the stylized econometric analysis of panel data to systematically investigate the households’ smoothing mechanisms to offer comparable estimates.

Another historical contribution is adding micro-level evidence on the consumers’ behaviors during industrialization. Francks (2009) provides a comprehensive view of the long-run consumption history in Japan from the Edo era to the twentieth century.999There are several business history studies analyzing the relationship between consumption and production. A representative work is Gordon (2013), who investigated the expansion of the sewing machine from many aspects, including the production, distribution, and gender social norms in Japan. However, these studies have little interest in the households’ risk-coping behaviors. This study employs a different analytical view by focusing on short-run behaviors.101010There are a few studies focusing on the relationships between household chores and consumption behaviors in interwar households (Tanimoto 2011, 2012). Looking into the extent and how the local society could ensure the households’ consumption provides valuable insights into the consumption history literature.

The rest of this paper is organized as follows. Section 2 overviews the Japanese economy around the First World War (WWI) and reviews Tsukisima, the target area in my analysis. I also summarize the financial institutions that were accessible to working-class households. Section 3 introduces the documents used to construct my panel dataset and discusses the sample characteristics. Section 4 summarizes the empirical strategies and results. Section 5 overviews the credit purchases in the local economy. Section 6 concludes.

2 Historical Background

2.1 Japanese Economy around the First World War

Japan had the foundations of an industrial nation by WWI. Between 1885 and 1915, real GNP grew annually by 2.6%, while population increased at 1.1%.111111Miyamoto (2008, pp. 60; 64) summarizes that economic growth is faster than population growth, implying that modern economic growth had started in this period as defined by Simon Kuznets. In 1915, the percentage of the employed population in the primary, secondary, and tertiary industries were 63%, 20%, and 18%, respectively. Based on domestic genuine production, however, these industries accounted for just under 30%, over 30%, and approximately 40%, respectively.

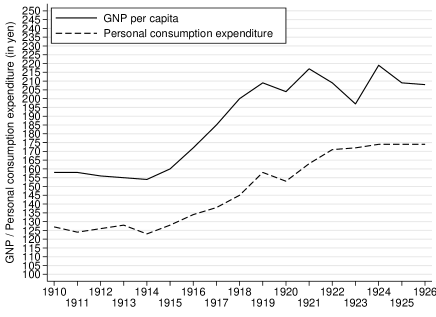

Soon after the outbreak of WWI, exports from European countries declined. Japan increased exports to the Asian market on behalf of those European countries and exported munitions and foodstuffs to the European Allies, leading to a current account surplus. Given the declines in the export capacity of the European countries, import substitution had progressed (Nakamura and Odaka 1989, p. 10). This expands the domestic market and leads to a rise in the machinery, metal, and chemical sectors. A worldwide shortage of ships also stimulated the development of shipbuilding, which proliferated as a leading industry. Development of shipbuilding industry stimulated demand for the machinery and steel industries (Sawai and Tanimoto 2016, p. 250). Through this process of heavy and chemical industrialization, the total number of enterprises increased.121212Year-on-year growth in the number of incorporated firms was 17.8% in 1918, 22.3% in 1919, and 13.5% in 1920. These are indeed the top three years of the 34 years from after the Russo-Japanese War to 1940 (Nakamura and Odaka 1989, p. 22). Figure 1 shows that the GNP growth from 1915-19 was 11.5% in nominal terms (4.4% in real terms), the highest growth throughout the 1910s and 1920s.

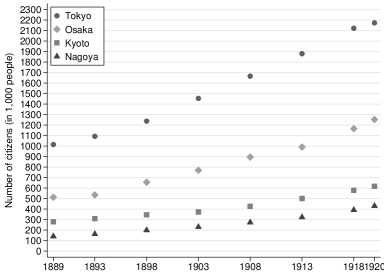

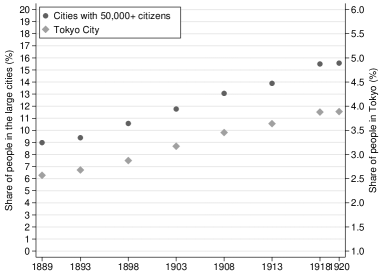

This rapid industrialization impacted the Japanese economy in many ways. Due to export-led economic growth, large inflows of gold increased domestic currency balances, causing prices to soar (Nakamura and Odaka 1989, p. 21). Although wages began to rise around 1916 as a response to rising prices and labor demand due to the increased number of firms, wage increases failed to keep pace with soaring prices. By the end of the war, the number of labor disputes grew sharply, and the labor movement flourished (Nakamura and Odaka 1989, p. 23). Furthermore, the rise of business accelerated urbanization as the rural population moved to cities in search of job opportunities (Nakamura and Odaka 1989, p. 22). The share of large cities (with people of 50,000 or more) as a percentage of the total population was less than 10% in 1889 but increased to nearly 16% in 1920 (Online Appendix Figure A.1a). The growth rate was exceptionally high during the WWI period, indicating that structural changes through the war accelerated the rise of the urban population. Urbanization has increased public investment in large cities, especially in construction investment in social capital such as roads and water supply systems (Nakamura 1971, pp. 142; 147).

Exports in the 1920s were lower than before because of the yen’s appreciation against the real exchange rate due to the accumulation of domestic and foreign species during WWI (Sawai and Tanimoto 2016, p. 253). Since the current account deficit was settled through the disbursement of foreign species owned by the government and the Bank of Japan, there was no reduction in the domestic money supply despite the sizeable current account deficit. This resulted in the domestic prices, especially nontradable goods prices, being kept high (Sawai and Tanimoto 2016, p. 254). The first half of the 1920s saw a temporary decline in industrial investment as the capital investment boom of the WWI period came to a halt under declining demand.131313On the other hand, construction investment by the private sector, including electric power and private railways, increased (Nakamura 1971, p. 145).

Note: This figure shows the gross national product per capita (solid line) and personal consumption expenditure (dashed line) between 1910 and 1926. The prices are deflated using the CPI in 1934-1935 price.

Sources: Created by the author using Ohkawa et. al. (1974, p. 237).

As described, there were short-term business cycles, such as the boom caused by WWI and the subsequent recession. However, taken as a whole, Japan achieved a high economic growth rate relative to other countries in the early 20th century and before WWII (Nakamura 1971, pp. 2–5). As shown in Figure 1, the growth rates of personal consumption expenditure were particularly high during and immediately after WWI, with average growth rates reaching 112% in 1915-19 and 118% in 1920-24.141414Total consumption as a percentage of the GNP remained above 80%. This level is indeed not apparent among other countries (Kuznets 1962). Importantly, however, the growth rate of real personal consumption per capita was also high: from 1875 to 1939, the average growth rate of personal consumption was 1.36%, and personal consumption never turned negative except during the Russo-Japanese War period. This was a high level even by international standards (Nakamura 1971, p. 27). Given the rapid urbanization, it is therefore necessary to focus on the consumption behavior of urban households when considering the Japanese economy at that time. However, progress has yet to be made in analyzing the consumption behavior (Nakamura 1971, pp. 30–31).

2.2 Tsukishima: A Representative Manufacturing Area

The population in Tokyo City has been growing since the end of the 19th century, and industrialization due to WWI spurred its growth. Tokyo City’s population share increased from 2.5% in 1889 to approximately 4% by 1920.151515In 1920, there were more than 10,000 municipalities in Japan, suggesting how huge Tokyo was in Japan. Compared to other large cities, Tokyo was still large: there was a difference of about 1 million between Tokyo and Osaka, the second largest city by population. Online Appendix Figure A.1a summarizes the trends in the number of people in the top five cities between 1889 and 1920. Throughout the 1910s, the percentage of industrial and commercial workers increased in Tokyo City, building the city as a gigantic commercial and industrial place (Tanimoto 2002, p. 8). In fact, Column 1 of Panel A in Table 1 shows that nearly half of the male workers worked in the industrial sector as of 1920 in Tokyo.

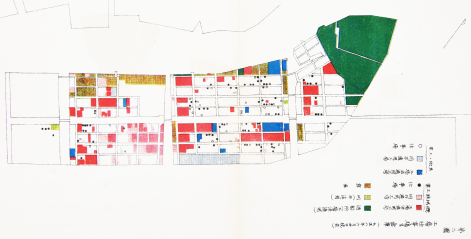

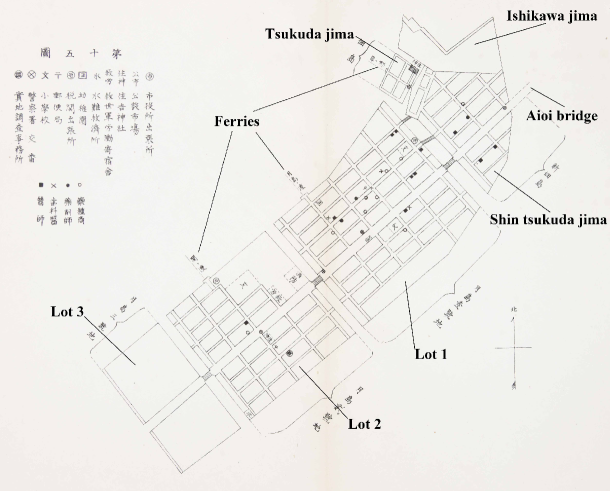

Notes: The name in each lattice indicates the administrative ward in Tokyo. The gray ward indicates the Kyobashi Ward and an island in the Kyobashi Ward indicates Tsukishima. The border surrounded by Asakusa, Honjyo, Nihonbashi, and Fukagawa wards includes the Sumida River. The borders of each ward are based on the administrative district in 1920. Geographical coordinate system is based on JGD2000/(B, L).

Source: Created by the author using the official shapefile (Ministry of Land, Infrastructure, Transport and Tourism, database).

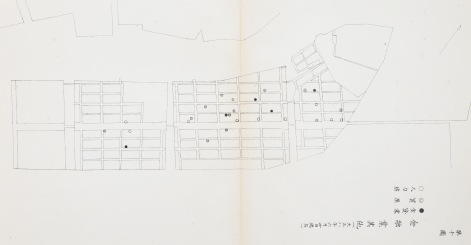

Notes: Blocks in green and light green indicate the shipyards. Blocks in red and pink indicate the factories in the machinery sector. Blocks in blue and light blue indicate the factories in the other manufacturing sectors. Blocks in brown are the warehouses. Small circles colored in black and white show the workplaces in the machinery sector and the other manufacturing sectors, respectively.

Source: Department of Health, Ministry of the Interior 1923c, second map. The tone was adjusted by the author using Adobe Photoshop 24.7.0.

The subject of this paper is Tsukishima, an industrial area located southeast of Kyobashi Ward in Tokyo (Figure 2).161616The base of the island was reclaimed during the Edo and Meiji periods from a delta at the mouth of the Sumida River. Online Appendix A.3 summarizes the development history of Tsukishima in detail. Column (2) of Panel A in Table 1 shows that Kyobashi had an industrial composition similar to that of Tokyo City in 1920. Column (3) confirms that Tsukishima is a representative industrial area in the city; approximately 68% of male workers were employed in the manufacturing sector. In the same year, there were 214 factories on this island, and approximately 80% of them belonged to the machinery and related sectors. (Department of Health, Ministry of the Interior 1923a, pp 385–389).171717According to the census of 1920, the number of workers in the metal and machinery equipment manufacturing industry was the highest in the entire city of Tokyo (%) compared to other industries. The same tendency was observed in Kyobashi Ward (%). Although similar statistics are not available for Tsukishima, this supports the evidence that Kyobashi was not an area with a unique industrial pattern (Statistics Bureau of the Cabinet 1929c, pp. 85–86; 108–109)). Figure 3 shows the spatial distribution of factories in Tsukishima as of June 30, 1918. Tsukishima had many machine factories and shipyards, and the workers’ residences were clustered there.181818For example, a representative shipbuilding plant was located on Ishikawajima island north of Tsukishima (Figure 3). Ships were strongly influenced by the import substitution that was underway at the beginning of the 20th century, and domestic production of ships was progressing (Section 2.1). The production of a hydraulic 80-ton hardened crane by Ishikawajima Shipyard in 1917 is an example of the domestic output of a production good that had previously relied on imports (Nakamura and Odaka 1989, pp. 10; 32). The focus of this study is the consumption behavior of these worker households in the industrial sector.

| Panel A: Industrial structure | |||

|---|---|---|---|

| Name of survey | (1) 1920 Population census | (2) 1920 Population census | (3) 1920 Population census |

| Survey area | Tokyo City | Kyobashi Ward | Tsukishima |

| Survey subject | Complete survey | Complete survey | Complete survey |

| Survey month and year | October 1920 | October 1920 | October 1920 |

| Agriculture | 1.0 | 0.6 | 0.4 |

| Fisheries | 0.1 | 0.3 | 0.8 |

| Mining | 0.4 | 0.4 | 0.8 |

| Manufacturing | 44.5 | 45.2 | 67.7 |

| Commerce | 32.4 | 34.0 | 16.9 |

| Transport | 7.6 | 10.2 | 6.1 |

| Public service and professions | 11.3 | 10.2 | 4.6 |

| Housework | 0.3 | 0.1 | 0.2 |

| Other industry | 2.4 | 2.0 | 2.5 |

| Panel B: Demographic structure | |||

| Name of survey | (1) 1920 Population census | (2) 1920 Population census | (3) 1920 Population census |

| Survey area | Tokyo City | Kyobashi Ward | Tsukishima |

| Survey subject | Complete survey | Complete survey | Complete survey |

| Survey month and year | October 1920 | October 1920 | October 1920 |

| Average household size (in person) | 4.6 | 4.7 | 4.3 |

| Share of married males (%) | 38 | 36 | 40 |

| Sex ratio (males/females) | 1.2 | 1.2 | 1.3 |

| 0–13 years | 1.1 | 1.1 | 1.1 |

| 14–19 years | 1.5 | 1.7 | 2.2 |

| 20–29 years | 1.3 | 1.4 | 1.6 |

| 30–39 years | 1.2 | 1.2 | 1.3 |

| 40–49 years | 1.2 | 1.2 | 1.3 |

| 50–59 years | 1.1 | 1.1 | 1.2 |

| 60+ | 0.8 | 0.8 | 0.9 |

| Average age of males | 25.3 | 25.3 | 25.1 |

Notes:

Panel A: This panel summarizes the industrial structures based on the occupations of male workers measured in the 1920 population census. Each share is calculated as the number of males worked as regular workers in each sector divided by the total number of male workers (in percentage). All the figures do not include the number of unemployed (mugyō sha) males.

Panel B: The average household size is the number of people divided by the number of households. The share of married males is the number of married males living with/without spouses divided by the total number of males (in percentage). The average age of males is calculated using the tables for population by age group reported in the census. Since the tables are open-ended, the class for over 60 years old is rounded as following the range of the former category (i.e., 50–59). All the figures in this panel do not include a small number of quasi-households (jyun setai), which include the person, such as the students in dormitories and the patients in hospitals.

The figures for Tsukishima listed in column 3 of both panels are based on the total sum of statistics of all the blocks (chōme) in Tsukishima (i.e., from Tsukudajima to Tsukishima dōri jyūni chōme).

Sources: Columns 1 and 2 of Panel A use the Statistics Bureau of the Cabinet (1929c, pp. 18–19). Columns 1 and 2 of Panel B use the Statistics Bureau of the Cabinet (1929c, pp. 38–43); Tokyo City Office (1922b, pp. 2–3; 42–46). Column 3 of Panel A uses the Tokyo City Office (1922c, pp. 42–47). Column 3 of Panel B uses the Tokyo City Office (1922a, pp. 26–31); Tokyo City Office (1922b, pp. 2–3; 42–46).

To look more closely at the characteristics of working-class households in Tsukishima, Panel B in Table 1 summarizes the population and occupational statistics from the census. First, the average household size in Tsukishima is , similar but slightly smaller than the values of and in Tokyo City and Kyobashi Ward, respectively. The percentage of the married male population is %, which is in the similar range of the figures of Tokyo City (%) and Kyobashi Ward (%). The average age of men in Tsukishima is , slightly lower than the figures for Tokyo and Kyobashi. While the sex ratio by age group in Tsukishima shows a similar trend to that of Tokyo and Kyobashi, the ratios for the – and – age bins are higher than those. Overall, these statistics reflect the fact that Tsukishima is a typical industrial area and many young male workers were employed there. The slightly smaller household size in Tsukishima can be attributed to the relatively large number of young factory worker households compared to other areas. Given that the percentage of married men is slightly higher in Tsukishima, some of these worker households in their early 20s might had been couples before they started raising children.

Finally, I briefly overview the lives of the factory workers’ households in Tsukishima. Factories and workers’ residences were scattered throughout the island.191919Tsukishima is composed of Ishikawajima island at the northern end, the adjacent Tsukudajima and Shin-tsukudajima islands, and the rectangular Lots 1–3 in the south (Online Appendix Figure A.3). Specifically, factories and worker residences were scattered throughout Shin-tsukudajima and Lots 1 and 2, whereas Lot 3, a relatively new reclaimed site completed in 1913, was undeveloped. The factory workers had lived in similar tenements and used the commercial stores and restaurants in the central lot.202020Online Appendix A.4 summarizes the housing in Tsukishima in detail using a housing survey. Regarding the stores, there were 209 stores selling daily necessities, 109 selling clothing, 74 selling tools, and 120 selling food, drink, and entertainment. There were also ten bathhouses (Department of Health, Ministry of the Interior 1923a, pp. 41–47). There were two postal offices, 13 pawnshops, and five moneylenders, and those were scattered throughout the island (Online Appendix Figure A.2). As for medical personnel, there were eight doctors, four dentists, eight obstetricians, and 14 drug stores. The main routes to the mainland were the wooden Aioi Bridge (Aioi bashi) and three ferries (watashi bune).212121See Online Appendix Figure A.3 for these routes. The average daily total number of people using the ferries in 1918 was reported to be , accounting for more than twice as many people as the Tsukishima population.222222See Department of Health, Ministry of the Interior (1923a, p. 30). The number of people and households of Tsukishima at the end of December 1918 is reported to be and , respectively (National Police Agency 1920a, pp. 50–51). These descriptions illustrate Tsukishima as a busy machine industry area during the industrialization.

2.3 Risk-Coping Institutions

Working-class households had been exposed to several risks that led to losses of income at that time. Generally, social insurance, such as health, accident, and unemployment insurance, can help mitigate the idiosyncratic income shocks on the workers.232323Gertler and Gruber (2002) shows the impacts of illness on consumption smoothing behavior in early 1990s Indonesia and argues the importance of public support for the illness. Kantor and Fishback (1996) show that the installation of workers’ compensation reduced the precautionary savings in the interwar U.S. Gruber (1997) provides evidence that unemployment insurance smooths individual consumption as the case of the U.S. from 1968–1987. However, comprehensive social insurance systems did not exist in the early 1920s in Japan. The former health insurance was enacted in 1927 and unemployment insurance had not been established throughout the prewar period. Therefore, the workers had basically no public support for their illness, injuries, and joblessness. Instead, they might have used private financial institutions to deal with the idiosyncratic risks.

Several financial institutions were indeed available for working-class households. A representative savings institution for households was the postal savings (yūbin chokin). In Tokyo City, roughly million people had postal savings accounts, covering approximately % of the entire citizens in 1920 (Online Appendix Table A.2). The average savings amount per capita in Kyobashi Ward was yen (Tokyo City Office 1921, pp. 892–893), which is less than one month’s earnings of the skilled-factory workers (Section 3.2). Savings bank (chochiku ginkō) is another famous savings institution among the working class in the 1910s (Ito and Saito 2019, pp. 79–81). The number of people with savings accounts was roughly million, accounting for approximately % of total people in Tokyo (Online Appendix Table A.2). However, % of all the depositors were the commerce and miscellaneous workers, and the manufacturing sector shared only % in Kyobashi Ward (Online Appendix Table A.3). As described by the Tokyo Institute for Municipal Research, savings bank was a savings institution designed for lower-income workers than factory workers (Tokyo Institute for Municipal Research 1925b, p. 81). This is consistent with the fact that Tsukishima did not have any savings bank branches, while there were two postal offices (Section 2.2). Although another savings institution was the mutual loan association (mujin), it had been used among small business owners and merchants for running their businesses (see Online Appendix A.2 for details).242424Generally, the ordinary bank in prewar Japan was the institution for providing large loans to businesses. There was no bank in Tsukishima, as workers did not borrow money from banks to make ends meet. The official report states that “a commercial bank is not necessary in a laboring area such as this Tsukishima, and even for large entrepreneurs such as factory owners, there is no particular need to establish a bank for their business transactions, and transactions with banks in other areas are sufficient” (Department of Health, Ministry of the Interior 1923a, p. 48).

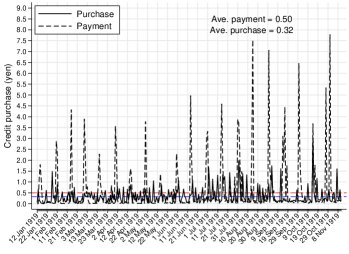

There also be a few lending institutions. Credit purchases (kakegai) in retail shops were the most popular institution. Although the systematic statistics on credit purchases are unavailable, the THBS households often used credit purchases in various retail shops for rice, fish, vegetables, firewood, and charcoal.252525Cooperative societies were also available for worker households to buy daily commodities, albeit they were not lending institutions. There were 26 cooperative societies in Tokyo prefecture in 1924, of which 23 were organized by the citizens and workers (Central Federation of Industrial Associations 1925, p. 57–59). However, while the two largest societies had roughly members, the others were generally small societies with less than 100 members. This figure accounts for only a few percentage points in the workers in the city, given that the number of male workers was more than 768 thousand. Most of the THBS households had not used the cooperatives. I will describe this institution in detail in Section 5. Pawnshop was the popular lending institution among low-income households who might face certain credit constraints.262626Lenders did not need to screen the borrower’s credit, and the borrowers did not worry about incurring heavy debt as the main articles were inexpensive clothes (Shibuya and Shojiro 1982). In addition, the interest rates were regulated by the Pawnbroker Regulation Act of 1895, and the average redemption rate was substantially high under the lower interest rates. The accessibilities were higher than the other lending institutions:272727The number of pawnshops in Tokyo were in 1918 and in 1919, respectively. The total number of cases was and each year. These figures are more than three times greater than the entire population in Tokyo City. as described, there were pawnshops in Tsukishima, more than twice the large number of moneylenders. However, the core users of the pawnshops were the low-income working-class households rather than the factory workers (Tokyo City Social Affairs Bureau 1921, p. 9). According to the statistics on the pawnshop users in Tokyo prefecture in 1923, the most representative users were the day laborers and workers classified as “miscellaneous”, accounting for % of all users. In contrast, those for agriculture, commerce, and manufacturing sectors were only , , and %, respectively (Tokyo Institute for Municipal Research 1926, p. 25). The inexpensive article means that pawnshops were used to deal with very short-run necessities only. Among the pawnshops of Kyobashi, for example, the average amount per case was yen which accounts for % of the monthly earnings of the THBS households. This means that the average redemption rate was substantially high: among pawnshops in Kyobashi, it was approximately % in 1920 ( cases/ cases) (Tokyo City Office 1922b, pp. 888–889). While the pawnshops were the famous lending institutions, they might not offer a sufficient amount of temporary income.

Other lending institutions are money lenders (kinsen kashitsuke gyō) and credit unions (shinyō kumiai). Generally, moneylenders were used by business owners with very high-interest rates (Shibuya 2000, pp. 184; 248). Similarly, the coverage of the credit unions was substantially low, say a few percentage points of the male workers in the manufacturing sector (Online Appendix A.2). Informal gifts may be another type of risk-coping institution, although systematic statistics are not available. A household survey on the 185 factory-worker households in Tokyo suggests that the share of average monthly gifts in total income was approximately % in November 1922 (Social Affairs Division 1925, pp. 58-59). Although this means that the gifts comprised a few percentage points of the monthly income, whether these informal income transfers had functioned as mutual aid is unclear.

To summarize, while there were several institutions, the available institutions for the factory-workers were few in the practical sense. For savings institutions, the postal savings might have been the best available devices for Tsukishima workers. Regarding lending institutions, credit purchase is the plausible device among factory workers. Although pawnshops were the most accessible financial institutions, they might not provide sufficient money as the articles were usually inexpensive. The factory workers in Tsukishima might have combined these risk-coping devices to deal with the idiosyncratic income shocks.

3 Data

This section offers a set of descriptive analyses to understand the characteristics of the data used in the study. I give an overview of the Tsukishima Survey in Section 3.1. I then utilize the statistics from the complete surveys in Section 3.2 to assess the representativeness of the sample households. In Section 3.3, I explain my data aggregation method to overcome the potential measurement error issue. The variables used, the trend in income and expenditure, and variations in idiosyncratic shocks are introduced in Section 3.4.

3.1 Tsukishima Household Budget Survey

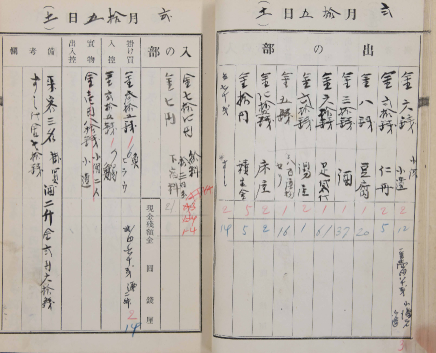

The Tsukishima Survey was the first urban social survey conducted in Japan by the Ministry of Home Affairs around 1919. The purpose was to investigate the status of the lives of urban worker households amid the rapid progression of industrialization throughout WWI. It was designed as a field survey consisting of multiple survey items on the worker households, and the household budget survey (hereafter THBS) included in.282828Online Appendix B.1 summarizes detailed information abour the Tsukishima Survey. The THBS was the first household survey in Japan to use the budget book method and is considered the prototype for subsequent household surveys in Japan (Sekiya 1970, p. 43). The Ministry of Interior published a report on the Tsukishima Survey in 1921, which contains some aggregated information on the target households. However, the main interest of this current study is the variations in the consumption and income in each household, meaning that household-level budget information is required.

Fortunately, the household budget book (kinsendeiri hikaechō) gathered in the THBS is preserved in the archives of the Ohara Institute of Social Research (hereafter, OISR).292929The author is permitted to access the materials related to the Tsukishima Survey by the OISR: Archives of the Tsukishima Survey (THBS, unreleased). While most of the sources are unreleased, the official reports of the survey published by the Ministry of Home Affairs are included in the archives of Gonda Yasunosuke at the OISR and are available to the public (The OISR, Archives of Gonda Yasunosuke (7-2; 7-3; 7-4)). These budget books were transferred to the OISR by Iwasaburo Takano, who was responsible for the Tsukishima Survey as a member of the 7th Section of the Health and Hygiene Research Committee of the Ministry of Home Affairs and became the first director of the OISR.303030Iwasaburo Takano was a professor at Tokyo Imperial University and a specialist in social statistics and social policy. He emphasized gathering statistics about workers through social surveys and is known as a researcher who significantly contributed to the formation of social survey methodology in Japan. His contribution to the Tsukishima Survey is summarized in detail in the Online Appendix B.1.

I corrected and digitized all the 40 THBS budget books for the factory worker households that were included in the official report of the Tsukishima Survey.313131The archives of the OISR also reserve several other household budget books of factory worker households. However, these budget books are generally in poor record keeping. Therefore, I do not use these incomplete books in this study. The characteristics of the remaining household budget books are summarized in detail in the Online Appendix B.5. During the study period, each household recorded their income and expenses daily in a budget book. Notably, a survey office was set up in Tsukishima, where a few surveyors lived and were closely connected with the survey households. Furthermore, weekly administrative meetings were held to discuss the progress of the survey (Miyoshi 1980, p. 38). This confirms that the information in these budget books is reliable and that the THBS budget dataset ensures a quality that allows quantitative analysis.323232Online Appendix B.1 provides finder details on how the Tsukishima Survey had been conducted carefully as a social survey project of Takano.

3.2 Sample Characteristics

Analytical Sample

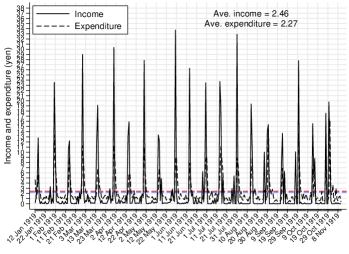

I use the semi-monthly and monthly panel datasets for my baseline analyses.333333The (semi-)month cells are defined based on the timing of paydays as I will explain in Section 3.3. Therefore, a (semi-)month cell reflects the outcome of the household’s consumption behaviors given a certain amount of income. The daily panels are unavailable to analyze the relationships between income and expenditures because most of the daily income cells take zero values (Figure 4a). Among the 40 THBS households, there are five cross-sectional units in the semi-monthly and monthly data. The estimation strategy used for testing consumption smoothing and risk-coping behaviors requires the panel structures (Section 4). Thus, I excluded these five cross-sectional units, leaving 35 THBS households.343434These cross-sectional units are generated from the households with roughly one-month observation in the budget survey. Although these cross-sectional units are useful for descriptive purposes, the identification in the estimation strategy used in the analysis requires within variations in each unit. Next, a household with incomplete income information, which is necessary data for my analysis, is removed. I also exclude a household for which no information on payments to the credit purchases was recorded. Finally, I excluded the small number of budget books created at both edges of the survey periods to aggregate the daily to semi-monthly dataset that I will explain in detail in the next section (Section 3.3). Consequently, my THBS sample includes 33 households with panel structures from 12th January to 11th November 1919. Online Appendix B.3 presents the finer details of the original data structure and trimming.

Before analyzing the representatives of the THBS sample, I assess the potential selection bias due to attrition of the units. The panel units with shorter (longer) time-series observations might have different preferences on the consumption than those with longer (shorter) time-series observations. In other words, the households with shorter panels should have similar family size characteristics to those with more extended panels. To test this potential issue, I regressed an indicator variable for the shorter panel units on the family size variables using the THBS sample. Online Appendix Table B.2 summarizes the results. All the estimated coefficients on the covariates are close to zero and statistically insignificant, and this result is robust to changing the thresholds. The Wald statistics support the null results, which are robust to using different thresholds such as first quantile, median, and third quantile. This result supports the evidence that the family structure, representing the household’s preference, is independent of the unbalancedness in my analytical sample.

Representativeness

| Panel A: Manufacturing sector | ||||

|---|---|---|---|---|

| Name of survey | (1) 1919 Statistics of | (2) 1920 Tsukishima Factory | (3) The THBS | |

| National Police Agency | Survey | |||

| Survey area | Tsukishima | Tsukishima | Tsukishima | |

| Survey month and year | December 1919 | November 1920 | 1919 | |

| Survey subject | All factories with | All factories with # of | 33 households | |

| # of workers | workers | workers | ||

| Textile | 0.2 | 2.9 | 0.0 | 0 |

| Machinery | 87.4 | 85.3 | 91.8 | 93.9 |

| Chemical | 1.1 | 5.9 | 5.5 | 0 |

| Food | 1.2 | 1.5 | 0.0 | 3.0 |

| Miscellaneous | 10.2 | 4.4 | 2.7 | 3.0 |

| Observations | workers | 68 factories | 146 factories | 33 heads |

| Panel B: Family structure | ||||

| Name of survey | (1) 1920 Population | (2) 1919 Statistics of | (3) The THBS | |

| Census | National Police Agency | |||

| Survey area | Tsukishima | Tsukishima | Tsukishima | |

| Survey month and year | October 1920 | December 1919 | 1919 | |

| Survey subject | Complete survey | Complete survey | 33 households | |

| Average household size | 4.3 | 4.3 | 4.3 | |

| Sex ratio | 1.3 | 1.2 | 1.2 | |

| Household size (% share) | ||||

| 1 | 6.0 | – | 0 | |

| 2 | 16.7 (18.7) | – | 15.2 | |

| 3–5 | 50.8 (57.1) | – | 57.6 | |

| 6–8 | 21.5 (24.2) | – | 27.3 | |

| 9+ | 4.9 | – | 0 | |

| Pearson statistic -value | – | – | 0.948 | |

| Panel C: Monthly earnings | ||||

| Name of survey | (1) The THBS | (2) Manufacturing Census | ||

| Survey area | Tsukishima | Tokyo City | ||

| Survey/equivalent year | 1919 | 1919 | ||

| Survey subject | THBS heads | Male factory workers | ||

| (Ave. age: 33.2) | in machinery factories | |||

| (Age range: 30-40) | ||||

| Average monthly earnings | 52.7 | 55.0 | ||

| 95%CI [48.0, 57.4] | ||||

Notes: Panel A: Column 1 shows the share of factory workers to the total factory workers in each sector (in percentage). The number of factory workers includes female and male factory workers in the 68 factories, with 15 workers and more. Column 2 indicates the share of factories to the total number of factories in each sector by factory size (in percentage). Column 3 summarizes the manufacturing sectors for the heads of the THBS. The definition of classification in the Statistics of the National Police Agency (column 1) is used in columns 2 and 3. Following this definition, several “woodworking” factories measured in the Tsukishima Factory Survey are included in the machinery sector in column 2, as it consists of shipbuilding and wooden pattern factories. The report also supports that the wooden patterns are used in the casting process and shall be regarded as one of the machinery sector (Department of Health, Ministry of the Interior 1923a, pp. 388–389).

Panel B: The first and second rows in columns 1 and 2 show the average household size and sex ratio measured in the 1920 Population Census and Statistics of the National Police Agency of 1919, respectively. The third to eighth rows in columns 1 and 3 show household size distributions in the census and the THBS sample, respectively. The figures in parentheses in Column (1) are the percentage share for family size bins between 2 and 8 people. The ninth row in column 3 shows the -value from the Pearson test for the equality of the household size distributions between 2 and 8 people. The share in each household size bin measured in the census is used as the theoretical probability in calculating the test statistic (Online Appendix B.5).

Panel C: Column 1 lists the average monthly earnings of the THBS heads calculated using the adjusted monthly panel dataset. Gaussian-based 95% confidence interval (CI) using bootstrap standard error is reported in the brackets. Column 2 shows the average monthly wage of the male factory workers in the skilled age range (30-40 years old) in machinery factories in Tokyo City. This figure is calculated using the average monthly wage and average monthly ancillary wage measured in the manufacturing censuses. All the wage statistics are deflated using the CPI for cities provided by Ohkawa et al. (1967, p. 255). Online Appendix B.6 summarizes the finer details of the process of this wage estimation.

Sources: Panel A: Column 1 uses the National Police Agency (1920b, p. 236). Column 2 uses the Department of Health, Ministry of the Interior (1923a, p. 385–386). Column 3 uses the Department of Health, Ministry of the Interior (1923a, p. 154). Panel B: Column 1 uses the Tokyo City Office (1922a, pp. 26–31; 262–283); Tokyo City Office (1922b, pp. 2–3; 42–46). Column 2 uses the National Police Agency (1920b, p. 53). The figures in column 3 are calculated by the author using the THBS dataset. Panel C: Column 1 uses the THBS dataset. Column 2 uses the Tokyo City Statistics Division (1926a, pp. 16; 244–245); Tokyo City Office (1921, pp. 726–757).

By using the manufacturing and population censuses, I first assess the representativeness of the THBS sample in Tsukishima.

Panel A of Table 2 summarizes the share of male workers in the manufacturing industry by sector. Statistics of the National Police Agency (hereafter SNPA) focusing on factories with more than or equal to 15 workers show that roughly 90% of male workers had been engaged in the machinery sector in 1919 (column 1). Column 2 summarizes the statistics in the manufacturing census conducted in the Tsukishima Factory Survey. The proportion of machine factories is % in larger factories and % in smaller factories. Thus, both columns indicate that most of the male workers in Tsukishima worked in the machinery sector.353535 I have confirmed that the paternal occupational statistics for the primary school students in Tsukishima provide materially similar results. Online Appendix A.5 summarizes the analysis using a survey of primary school students. In column 3, I confirm that the THBS heads’ occupations show a similar proportion: % worked in the machinery sector. In fact, the report states that “It is not too much to say that most of the industry in Tsukishima is machinery. Therefore, to describe the labor situation in Tsukishima, it is sufficient to describe its machinery industry” (Department of Health, Ministry of the Interior 1923a, p. 389). Figure 3 illustrating many machinery factories supports this statement for Tsukishima. For the other sectors, the THBS includes a few heads who worked in food and miscellaneous sectors, and the proportions are similar to those listed in column 2.

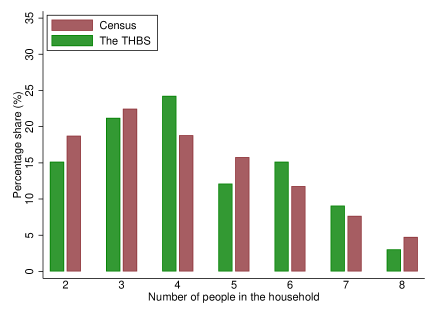

Panel B of Table 2 summarizes the family structure. The average household sizes are identical in the Population Census ( in column 1), SNPA ( in column 2), and THBS ( in column 3). In addition, the sex ratio is similar across the surveys (–). The number of people in the THBS households ranges from 2 to 8, meaning the THBS sample does not include single or very large households.363636The share of single and vary large (9+ people) households was roughly % (Column 1 of Table B). This supports the evidence that focusing on the family households with 2–8 people covers most of the households in Tsukishima. In other words, the THBS mainly focuses on the consumption behavior in couples and households with a few children. For this household size range, the Pearson test does not reject the null of equality in the household size distributions with -value = . This means that the THBS sample reasonably approximates the distribution of family households in Tsukishima. This confirms the validity of the statement in the report that the THBS households can be “regarded as representative of the family form in Tsukishima” (Department of Health, Ministry of the Interior 1923a, p. 145). Online Appendix B.5 illustrates the household size distributions in finer detail.

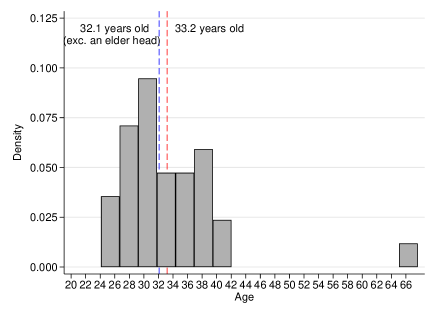

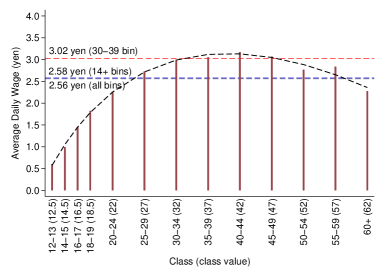

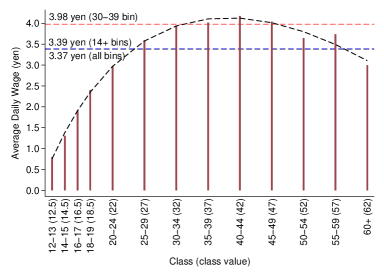

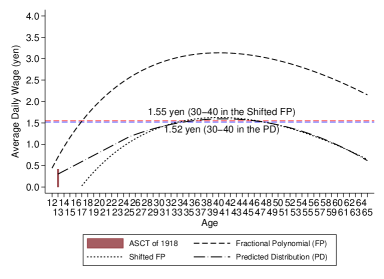

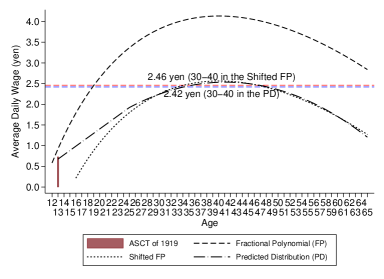

The official report of the Tsukishima Survey suggests that roughly nine out of ten factory workers in the skilled-age range were classified as skilled workers. Roughly six of those skilled workers were employed in the middle- to large-scale factories, and three worked in small-scale factories.373737Online Appendix A.5 summarizes this in detail using the complete survey on the primary school students in 4th to 6th grades in Tsukishima. Given this fact in Tsukishima, the THBS was designed to investigate the budgets in skilled workers’ households.383838The finer details in the background of this survey design are summarized in Online Appendix B.1. Shortly, Iwasaburo Takano, a survey director, regarded that the skilled workers in the modern industrial sector will constitute the core of the labor force, labor movement, and citizens. The average THBS head’s age is 33, which is indeed in the skilled workers’ representative age range of the 30s in the machinery factories (Kitazawa 1924).393939Specific occupations are not available for most heads because they usually list “factory workers” in the occupation section. However, sub-categories available at a few heads indicate lathe operator and finisher, the typical skilled workers in machinery factories. Online Appendix A.6 summarizes the works in the machinery factories in Tsukishima. Column 1 of Panel C in Table 2 indicates that the average monthly earning of the THBS heads is yen. In Column 2, I calculated the average monthly earning of male machinery factory workers in the skilled-age range using the manufacturing censuses for the entire city, which shows only yen higher earnings (i.e., ) than the THBS heads’ earnings.404040Shortly, this figure is calculated using the average daily wage of male factory workers aged 30-40 and average annual working days measured in the manufacturing censuses. Online Appendix B.6 provides the finer details of the calculation steps. The average wages for the male factory workers had an inverted-U-shaped distribution with respect to age, taking the greatest figure in the 30s (Online Appendix Figure B.7). This is a similar life-cycle pattern to the factory workers observed in late 19th century England (Horrell and Oxley 2000, p. 42). This provides evidence that the monthly earnings of the THBS heads and skilled workers’ households in Tsukishima are materially similar. Therefore, the THBS households can be useful in inferring the mean tendency of those households.

3.3 Aggregation

Measurement Error

income and expenditure

net income

income and expenditure

net income

by Different Time-series Frequencies

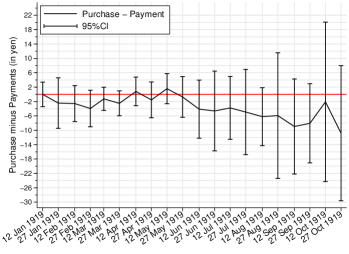

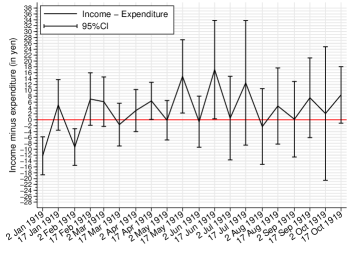

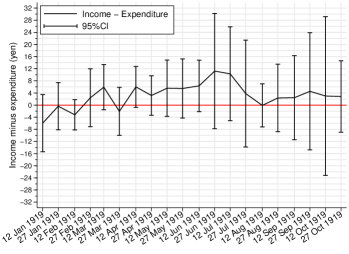

Note: Figure 4a, 4c, and 4e illustrate the time-series plots of the average daily, semi-monthly, and unadjusted semi-monthly income and expenditure, respectively. Figure 4b, 4d, and 4f illustrate the time-series plots of the average daily, semi-monthly, and unadjusted semi-monthly income minus expenditure. Figures 4a and 4b shows the daily data between 12th January and 11th November 1919. The (adjusted) semi-monthly series defines the 12-26th for the first and 27-11th for the second half. Thus, Figures 4c and 4d show the semi-monthly series calculated using the daily data between 12th January and 11th Novemeber 1919. The unadjusted semi-monthly series uses the 15th of each month as a threshold. Figures 4e and 4f show the unadjusted semi-monthly series calculated using the daily data between 15th January and 31st October 1919.

Source: Created by the author using the THBS sample.

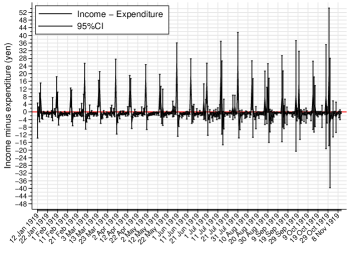

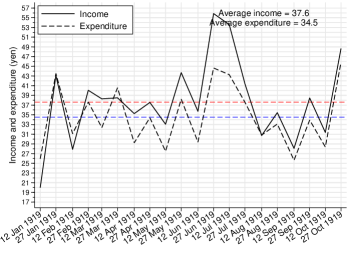

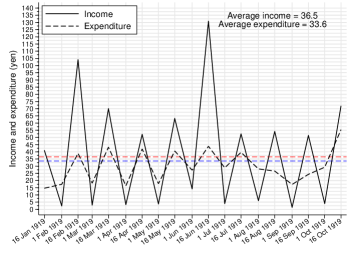

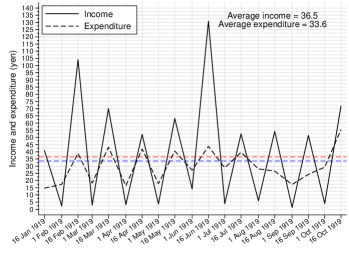

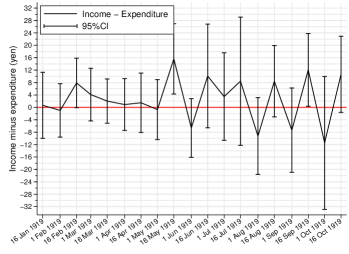

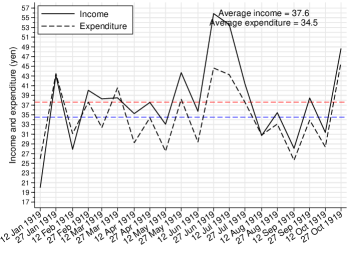

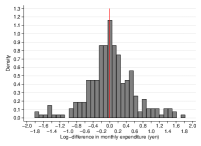

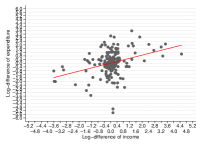

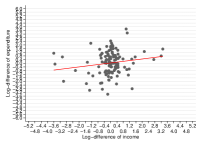

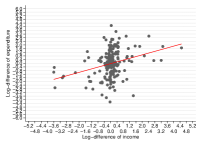

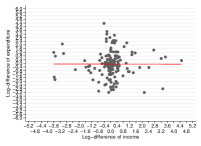

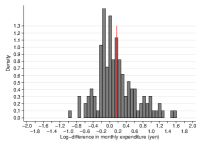

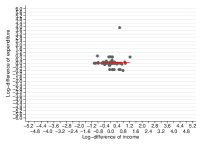

It is necessary to summarize the daily budget information into a more extended time range because household needs a set of time to smooth their consumption given a realiszed amount of income. To explore the reasonable way to aggregate the THBS dataset, I first overview the daily time series on the total income and expenditure. Figure 4a shows that the head’s income had been paid twice monthly: the semi-monthly wages were paid on the middle (14–16th) and last day (30th or 31st).414141The head’s income was the dominant way in earnings because the breadwinner households had been typical at that time (Panel B in Table 3). Importantly, Figure 4a indicates that the households expensed much of their income just on the payday and spent the rest of the payment little by little until the next payday. In other words, the expenditures had never clearly increased just before the paydays. This means that the households had made their consumption decisions (schedules until the next payday) based on the income they obtained. Notice that the calendar (semi-)monthly aggregation can not reflect this household behavior because the calendar (semi-)month does not place the payday at the beginning of its cell.424242For example, a calendar semi-month cell in January, say the cell from 1st to 14th, starts on the 1st but its payday is set on the 14th. This assumes that the aggregate consumption in this semi-month cell is based on the earnings at the end of its cell. This is clearly an unrealistic assumption. Another source of measurement error is the shift of the payday: the payday for the latter half of a month was sometimes set on the first date of the following month. Although this shift did not occur frequently, the calendar month cell shall contain a substantial noise from the shift as it leads to the cells including more (three paydays) and fewer (one payday) payments than normal. Nelson (1994) suggests that this sort of mismatching in the timing of income and expenditure tends to induce the type II error in the test of consumption smoothing.

Adjustment

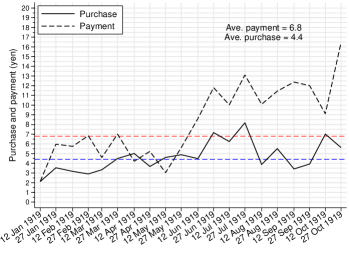

To match income and expenditure data precisely, I first consider aggregating the daily data into semi-monthly series. Specifically, I aggregate the daily observations between the 12th and 26th for the first half and those between the 27th and 11th of the next month for the second half.434343This means that the number of days included in a semi-month ranges from 13 to 16. Note that this heterogeneity in the number of days over different semi-months is a cross-sectional constant. Thus, these differences are entirely captured using the semi-month fixed effects in the regression. This range is based on the fact that almost all of the paydays in the second half of a month measured in the THBS dataset, are 27th–31st.444444Note that I do not use the definition of semi-month starting from the 2nd (to the 16th) in each month because this way of stratification places the payday at the end of each semi-month cell. Online Appendix B.7 provides the evidence that while the definition using 2nd in each month as the threshold provides an improved series in income, the expenditure can not chase the income in the right way because the expenses measured under this definition are based on the income in the previous semi-month cell. Again, I confirmed that my preferred definition using the 12th in each month as the threshold offers a clean series of income and expenditure.

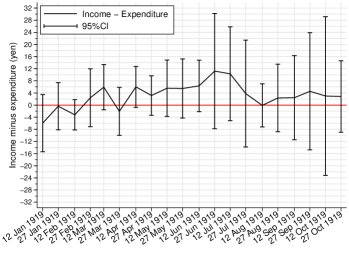

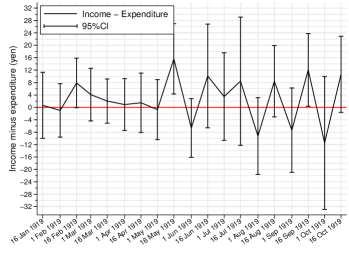

Figure 4c shows the time-series plots of the income and expenditure from this adjusted semi-monthly panel dataset, whereas Figure 4e illustrates the unadjusted (calender) semi-monthly series using the 15th of each month as the threshold of the semi-month. Clearly, Figure 4e provides very rough measures of both income and expenditure due to the measurement errors from the misadjustment of paydays. The most significant improvement in Figure 4c is that the expenditure can chase the income in each month, reflecting the households’ consumption behaviors based on their income measured in the exact timing. Given the improvements in both income and expenditure measures, the net income series shows a much smoother trend in Figure 4d, which are not available under the unadjusted definition (Figure 4f). In Section 4.1, I will demonstrate how these measurement errors in the unadjusted dataset attenuate the estimates.454545Note that the monthly aggregation is still useful for calculating the average monthly income because those shifts do not influence the total amount of incomes. For this reason, I use the monthly average figure in Panel C of Table 2 for comparison.

3.4 Data Description

Variables

The THBS budget book has two primary sections: expenditure and income. I digitized records in each category following the categorization used in the official report of the Tsukishima Survey. Panel A of Table 3 lists the subcategories for expenditures: food, housing, utilities, furniture, clothes, education, medical, entertainment, transportation, gifts, and miscellaneous. These variables are used to test the smoothness of these consumptions. I consider five net income categories: net savings, net insurance, net borrowing, net credit purchase, and net gifts to investigate the risk-coping strategies. Net variables are defined as the income minus expenditure in each category; for example, net savings refers to the difference between the withdrawal amount and deposits to savings. I also consider the sales of miscellaneous goods and labor earnings from the family members except for the head to test the contribution of the asset sales and intrahousehold labor-supply adjustments. Panel B of Table 3 summarizes these variables.464646Online Appendix B.9 presents the results for the panel unit root tests. The null hypothesis of unit roots in all the panels is rejected at the conventional level for all these variables.

It is important to take into account the possibility of changes in preferences that may occur as a result of alterations in family size (Jappelli and Pistaferri 2017).474747In village economies, landholding and asset stocks such as livestock and grain may also be correlated with the household’s risk-coping behaviors (e.g., Udry 1994, 1995). Since this study analyzes urban factory workers’ households, the roles of these assets can be discarded. Fortunately, the archives of the Tsukishima Survey include the sheets documenting the changes in household composition (Kazoku idō hyō).484848The Ohara Institute for Social Research, Archives of the Tsukishima Survey (THBS, unreleased). I found that the size of households had been stable over time: one household experienced changes in the number of family members due to the birth of a son during the sample periods. This supports the evidence that the preference shifts had rarely occurred among the THBS households. Although family size is included in all regressions to be conservative, it has little effect on the results.494949The family size variable shall be omitted in several regressions due to the near-perfect multi-collinearity in the fixed-effects models given its small within variations. Although the number of family members in different age bins is available from the THBS, those family composition variables are also time-constant and are absorbed by the household fixed effect. Panel C of Table 3 shows the summary statistics on the family size variable.

| Panel A: Variables for testing consumption smoothing (in yen) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Semi-monthly Panel Dataset | Adj. Monthly Panel Dataset | |||||||

| Level | Log | Level | Log | |||||

| Mean | Obs. | Mean | Obs. | Mean | Obs. | Mean | Obs. | |

| Total expenditure | 34.5 | 289 | 3.4 | 289 | 61.1 | 162 | 4.0 | 162 |

| Food | 10.9 | 289 | 2.3 | 270 | 19.5 | 162 | 2.8 | 152 |

| Housing | 2.7 | 289 | 1.6 | 134 | 4.9 | 162 | 1.8 | 118 |

| Utilities | 1.2 | 289 | -0.1 | 232 | 2.2 | 162 | 0.5 | 147 |

| Furniture | 0.4 | 289 | -1.6 | 177 | 0.7 | 162 | -1.2 | 126 |

| Clothes | 2.8 | 289 | 0.3 | 248 | 5.0 | 162 | 1.0 | 148 |

| Education | 0.7 | 289 | -0.6 | 201 | 1.3 | 162 | -0.2 | 135 |

| Medical | 1.7 | 289 | 0.2 | 269 | 3.0 | 162 | 0.7 | 152 |

| Entertainment | 1.4 | 289 | -0.1 | 255 | 2.5 | 162 | 0.5 | 150 |

| Transportation | 0.4 | 289 | -1.3 | 195 | 0.8 | 162 | -0.9 | 125 |

| Gift | 3.1 | 289 | 0.5 | 243 | 5.6 | 162 | 1.2 | 148 |

| Miscellaneous | 0.5 | 289 | -1.3 | 222 | 0.9 | 162 | -0.9 | 140 |

| Disposable income | 37.6 | 289 | 3.5 | 278 | 67.3 | 162 | 4.1 | 159 |

| Panel B: Variables for testing risk-coping mechanisms (in yen) | ||||||||

| Semi-monthly Panel Dataset | Adj. Monthly Panel Dataset | |||||||

| Mean | Std. Dev. | Obs. | Mean | Std. Dev. | Obs. | |||

| Panel B-1: Savings, insurance, borrowing, and gifts | ||||||||

| Net savings | -0.01 | 3.97 | 289 | -0.02 | 5.52 | 162 | ||

| Net insurance | -0.03 | 6.67 | 289 | -0.05 | 8.97 | 162 | ||

| Net borrowing | 0.31 | 5.03 | 289 | 0.61 | 7.32 | 162 | ||

| Net credit purchase | -2.47 | 11.33 | 289 | -4.67 | 19.38 | 162 | ||

| Net gifts | -2.04 | 6.11 | 289 | -3.56 | 9.20 | 162 | ||

| Panel B-2: Labor supply adjustments & sales of miscellaneous assets | ||||||||

| Other family member’s earning | 3.74 | 6.11 | 289 | 6.72 | 14.79 | 162 | ||

| Sales of assets | 0.02 | 0.12 | 289 | 0.04 | 0.15 | 162 | ||

| Panel B-3: Income variable | ||||||||

| Head’s earning | 29.43 | 18.11 | 289 | 52.70 | 30.30 | 162 | ||

| Panel C: Family size (people) | ||||||||

| Semi-monthly panel dataset | ||||||||

| Mean | Std. dev. | Min | Max | Obs. | ||||

| Number of family members | 4.3 | 1.6 | 2.0 | 8.0 | 289 | |||

| Panel D: Health shocks | ||||||||

| Semi-monthly panel dataset | ||||||||

| Mean | Std. dev. | Min | Max | Obs. | ||||

| Number of days with illness (head) | 0.1 | 0.8 | 0 | 11 | 254 | |||

| Number of days with illness | 0.2 | 1.7 | 0 | 16 | 254 | |||

| (the other family members) | ||||||||

Notes:

Panel A: The summary statistics of the variables used to test the consumption smoothing for the 33-panel units in the semi-monthly and adjusted monthly panel datasets are shown in this panel. Disposable income is the total income minus tax payments.

Panel B: This panel shows the summary statistics of the variables used to test the risk-coping strategies for the 33-panel units in the semi-monthly and adjusted monthly panel datasets. Each net income variable is defined as the difference between income and expenses. “Net savings” refers to the difference between the amount withdrawn and the total deposits. “Net insurance” refers to the amount received from insurance minus the expenses paid for insurance. “Net borrowing” refers to the amount of borrowing minus the debt payments. “Net credit purchase” refers to the amount of credit purchases minus credit redeemed. “Net gifts” refer to the total received amounts, including both pecuniary and non-pecuniary gifts, minus the payments for gifts. “Other family member’s earnings” refers to the total income earned by all family members except for the head of the household. “Sales of assets” includes the sale of daily miscellaneous goods such as newspapers and empty bottles.

Panel C: The summary statistics of the family size variable for the 33-panel units in the semi-monthly panel dataset are listed. The statistics for the adjusted monthly panel dataset are not reported because they are materially similar to those for the semi-monthly panels.

Panel D: The summary statistics of the number of days with illness for family members are listed. Since both are lagged variables, the initial time period in all the units is omitted. Similarly, a household with two semi-month observations is excluded. Similarly, .

Sources: Created by the author from the THBS sample.

Trend

Next, I overview the time-series figures to evaluate the representativeness of my THBS dataset. Figure 4c shows a weak increasing trend in the average income. This is consistent with the macroeconomic trend in the nominal income during this period. This trend in earnings was, however, offset by the steep inflation under the expansions after the war (Section 2.1). In Figure 4d, the deviation of expenditure from income in January must capture the expenses on the goods for the New Year events. The gaps in June to the first half of July may reflect the payments of bonuses. The humps in March may reflect the preparation for the new fiscal and academic year from April, meaning that the increased income in this month may suggest a higher proportion of temporary income from withdrawals and loans. These support the evidence that the budget data from the THBS households can capture the macroeconomic trends.

Idiosyncratic Shocks

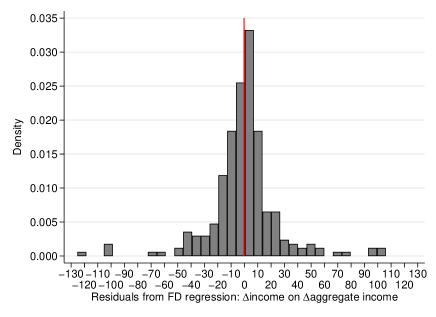

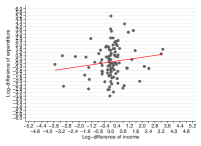

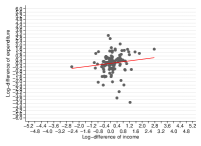

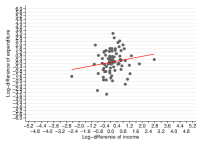

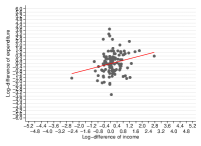

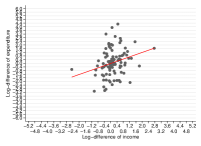

Online Appendix Figure B.11 illustrates the residuals from the regression in the first difference in semi-monthly income on the first difference in aggregate semi-monthly income.505050Let be the number of households in semi-month in the year 1919. For household in semi-month cell, the residual is then defined as , where and is the estimated coefficient. I used the semi-monthly panel dataset to overview the entire distribution of the idiosyncratic shocks because the daily panels include a set of consecutive cells with no income. While the residuals satisfy the zero-average property, they occasionally take large negative and positive values, suggesting that the workers had experienced idiosyncratic income shocks in some cells. Regardless of favorable or adverse shocks, these cells that deviated from mean tendency are helpful in investigating how those households coped with the idiosyncratic shocks. Despite this, it is helpful to focus on the illness as it is the least predictable shock (Gertler and Gruber 2002). Although joblessness is another shock, the THBS heads rarely changed their occupation during the survey period as they are the skilled workers who were less likely to move to other jobs.515151Another possibility is that the THBS heads who changed their jobs might have been omitted from the survey. However, I confirmed that the households with longer and shorter time-series observations have similar family characteristics (Online Appendix B.3). Thus, this omission does not lead to selection bias in terms of the potential vulnerabilities to the idiosyncratic risk. In contrast, fortunately, the illness among the THBS family is documented systematically. As explained in Section 2.3, the comprehensive health insurance system was unavailable then. Moreover, the sanitary conditions in the cities were low, leading to higher mortality rates.525252See Schneider and Ogasawara (2018) for the overviews on the sanitary conditions in interwar Japan. The official report indeed mentioned the fact that the workers in the machinery factories in Tsukishima had faced the risk of diseases (Department of Health, Ministry of the Interior 1923a, p. 14).

Considering this, I first provide the overall results from the specification using the changes in earnings as the idiosyncratic income shock in Sections 4.1 and 4.2. I then consider the structure behind the adverse income shocks using the heads’ temporary illness to investigate the households’ consumption and risk-coping behaviors in Section 4.3. Panel D of Table 3 shows the summary statistics on the health shock variables used.

Risk Preferences

This study investigates consumption smoothing behaviors among homogeneous households, say the skilled factory workers’ households in the machinery sector in Tsukishima. This empirical setting is useful because the different attitudes toward risks among households may lead to bias in the standard risk-sharing regressions. Following Schulhofer-Wohl (2011), I tested whether the earnings of the heads who worked in a few specific factories or sectors showed different responses to the aggregate shocks. Specifically, I consider the heads who worked in large-scale or governmental factories to have potentially different risk preferences because those workers might have lower risk tolerance than those who worked in smaller enterprises. I confirmed that the sensitivities to the aggregate shocks are materially similar in both groups in the statistical sense.535353By using the fixed-effect model with one-way error component, the heads’ earnings are regressed on the aggregate consumption, its interaction term with respect to the indicator variable for the large-scale and government factories, and family size variable. The results are unchanged if I trim the semi-months with the smaller number of cross-sectional observations. This result is unchanged if I assume that a few heads who worked in the smithing factory or in the non-machinery sectors had different risk preferences.545454The skilled workers in the smithing sector might be a business owner (Online Appendix A.6). Similarly, the workers in the non-machinery sectors in Tsukishima, a representative machinery production area, might have had a different, presumably higher, risk-tolerance. This supports the evidence that conditional on the household fixed effects, it is plausible to assume that the THBS households shared similar risk preferences. Online Appendix B.10 summarizes the finer details of this analysis.

4 Empirical Analysis

4.1 Consumption Smoothing

Estimation Strategy

I consider a linear fixed-effects model designed to test the consumption smoothing.555555Another empirical specification used to test the consumption smoothing is the first-difference model, including the aggregate consumption to capture the macroeconomic shocks in the economy (Mace 1991). In other words, this alternative model requires the interpretation of the estimated coefficient on the aggregate measure of consumption. Although the consumption of the THBS households may capture the macroeconomic trend in the consumption (Section 3.3), those households do not cover entire households in the target economy, Tsukishima, which shall disturb the interpretation of the coefficient on the aggregate consumption. To be conservative, therefore, I use the two-way fixed-effects model to control for the macroeconomic shocks (Cochrane 1991; Ravallion and Chaudhuri 1997). Online Appendix C.1 provides the conceptual framework and the derivation of my empirical specification. For household in time , the reduced form equation is characterized as follows:

| (1) |

where is consumption, is disposable income, is the family size control, is the household fixed effect, is the semi-month fixed effect, and is a random error term. The household fixed effect captures the time-constant unobservable factors such as permanent income and consumption preference. The time-fixed effect effectively removes the unobservable macroeconomic shocks and trends described in Section 3.4. The estimate of suggests income elasticity, which can range from zero for perfect insurance to one for the absence of insurance. The cluster-robust variance-covariance matrix estimator is used to deal with heteroskedasticity and serial dependency (Arellano 1987).

Results

| (1) Semi-monthly Panels | (2) Adj. Monthly Panels | (3) Unadj. Monthly Panels | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Disposable income | Obs. | Disposable income | Obs. | Disposable income | Obs. | ||||

| Coef. | Std. error | Coef. | Std. error | Coef. | Std. error | ||||

| Total consumption | 0.358 | [0.033]*** | 278 | 0.548 | [0.065]*** | 159 | 0.261 | [0.054]*** | 144 |

| Food | 0.136 | [0.030]*** | 259 | 0.436 | [0.088]*** | 149 | 0.100 | [0.072] | 135 |

| Housing | 0.099 | [0.415] | 134 | 0.291 | [0.243] | 118 | -0.263 | [0.167] | 126 |

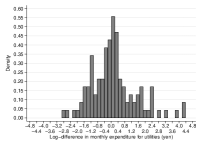

| Utilities | -0.003 | [0.138] | 223 | 0.431 | [0.149]*** | 144 | 0.197 | [0.333] | 133 |

| Furniture | 0.426 | [0.223]* | 169 | 0.943 | [0.335]*** | 123 | 0.250 | [0.339] | 114 |

| Clothes | 0.378 | [0.190]* | 238 | 0.374 | [0.324] | 145 | 0.806 | [0.262]*** | 135 |

| Education | 0.070 | [0.092] | 194 | 0.337 | [0.212] | 133 | 0.093 | [0.213] | 125 |

| Medical expenses | 0.039 | [0.066] | 258 | 0.498 | [0.196]** | 149 | -0.128 | [0.094] | 135 |

| Entertainment expenses | 0.355 | [0.109]*** | 244 | 0.484 | [0.148]*** | 147 | -0.049 | [0.199] | 134 |

| Transportation | 0.278 | [0.110]** | 187 | 0.635 | [0.190]*** | 124 | 0.362 | [0.290] | 117 |

| Gift | 0.523 | [0.106]*** | 234 | 0.599 | [0.115]*** | 146 | 0.622 | [0.305]* | 133 |

| Miscellaneous | -0.076 | [0.147] | 214 | 0.549 | [0.184]*** | 137 | 0.246 | [0.267] | 129 |

***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. Standard errors in brackets are clustered at the household level.

Notes: This table shows the results of equation 1: the regressions of the 11 measures of log-transformed consumption on log-transformed disposable income as well as on the family size control, household-fixed effect, and time-fixed effect. Columns 1, 2, and 3 show the results for the semi-monthly, adjusted monthly, and unadjusted monthly panel datasets, respectively. The estimated coefficients on log-transformed disposable income are listed in the column named “Coef.”.

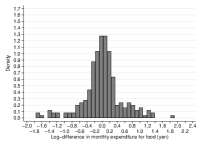

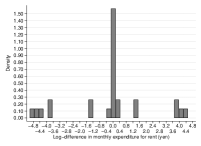

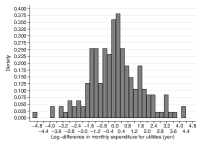

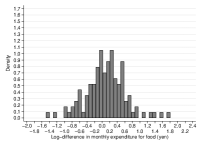

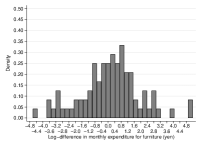

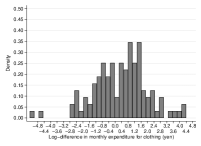

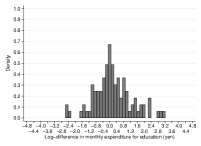

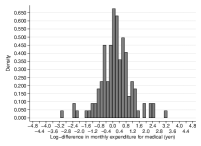

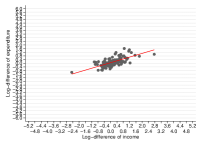

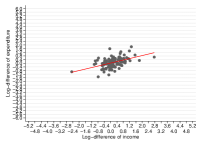

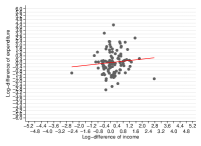

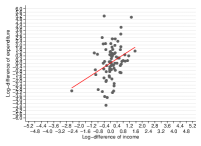

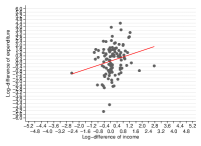

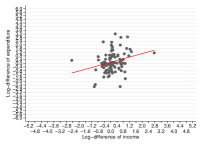

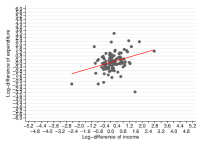

Column (1) of Table 4 presents the results from the semi-monthly panel dataset. In the total consumption, the estimated coefficient is . This means that a one percentage point decrease in disposable income decreases the total expenditure by percentage point, suggesting that the factory worker households could not thoroughly smooth their consumptions. Among the subcategories, the food, furniture, clothes, entertainment, transportation, and gifts expenditures are not well-insured. This implies that the households are likely to cut off (increase) their expenses on these categories when they face adverse (favorable) income shocks. The estimates suggest that the expenses on furniture and clothes are relatively sensitive to the shocks ( and , respectively). This is consistent with the fact that both categories are luxury categories. Similarly, the estimate for gifts shows a large magnitude () because the expenses on the other households are essentially optional. The estimates for the entertainment and transportation expenses are slightly smaller but statistically significant ( and ). This also makes sense, given that these expenses are related to family travel and theatergoing.565656The workers can enter their factories by walking in Tsukishima. Thus, the costs of commuting to the factory are not usually documented in the budget books. Importantly, the estimate for food categories is statistically significant but much smaller (). This implies that the households might have had some means to deal with idiosyncratic shocks to smooth their expenses on food. I will return to this point later.

Next, I present the results for the adjusted monthly panel dataset in Column (2) to see whether the income elasticities changed in monthly frequency, a longer span than the semi-monthly frequency. Not surprisingly, the adjusted monthly series yields greater estimates than the semi-monthly series. The estimate for total consumption is now , which is roughly times greater than that from the semi-monthly panel data. Generally, the panels with short-run time bins are more likely to be influenced by unexpected shocks in consumption, which tends to attenuate the income elasticity (Nelson 1994). In this case, however, the estimates for the adjusted monthly panels are greater than those for the semi-monthly panels across almost all subcategories. The clothes category alone shows a similar but statistically insignificant estimate. This may reflect the cases in which the workers bought their work clothes for the new season. Although such a replacement of work clothes has not occurred frequently (i.e., semi-monthly), this means that the clothes category includes both luxury and necessary items, which may increase the standard error of the estimate.