Provably Efficient High-Dimensional Bandit Learning with Batched Feedbacks

Abstract

We study high-dimensional multi-armed contextual bandits with batched feedback where the steps of online interactions are divided into batches. In specific, each batch collects data according to a policy that depends on previous batches and the rewards are revealed only at the end of the batch. Such a feedback structure is popular in applications such as personalized medicine and online advertisement, where the online data often do not arrive in a fully serial manner. We consider high-dimensional and linear settings where the reward function of the bandit model admits either a sparse or low-rank structure and ask how small a number of batches are needed for a comparable performance with fully dynamic data in which . For these settings, we design a provably sample-efficient algorithm which achieves a regret in the sparse case and regret in the low-rank case, using only batches. Here and are the sparsity and rank of the reward parameter in sparse and low-rank cases, respectively, and omits logarithmic factors involving the feature dimensions. In other words, our algorithm achieves regret bounds comparable to those in fully sequential setting with only batches. Our algorithm features a novel batch allocation method that adjusts the batch sizes according to the estimation accuracy within each batch and cumulative regret. Furthermore, we also conduct experiments with synthetic and real-world data to validate our theory.

1 Introduction

With the growing availability of user-specific data and the increasing demand for personalized service, high-dimensional contextual bandits have received tremendous attention in various industries, including healthcare (Ameko et al., 2020), individual content recommendations (Li et al., 2010), dynamic pricing (Qiang and Bayati, 2016; Fan et al., 2023+), and talent searching (Geyik et al., 2018). Furthermore, data dimensions are rapidly increasing in the era of big data. For example, patients’ information in healthcare includes thousands of components, such as medical history records, clinical test results, and biomarker profiles. Sometimes, this information has to be framed into a low-rank matrix model, like X-ray images and genetic biomarker profiles. These problems are generally high-dimensional but often represented by parameters with sparse structures, such as vectors with low effective dimensions or matrices with low ranks.

In the face of high-dimensional data, traditional sequential bandits encounter a problem of inefficiency and unrealistic feedback acquisition. Because the feedback may not be revealed instantly, making optimizations under high dimensions consumes significant time and resources. For example, in clinical trials, it takes a period to judge the effectiveness of treatments. Still, new patients usually need to be treated urgently and cannot wait for the previous patient to finish the trial. Similarly, in individual music recommendations, a vast number of users log in simultaneously and are impatient, so the system must interact with them simultaneously. Additionally, there are some applications where feedback is naturally divided into batches, such as in vaccine treatment, where vaccines are allocated into batches according to demand, and each batch corresponds to the vaccine given to people in each period.

Motivated by these problems, we study high-dimensional contextual bandits with batched feedback, formulated as high-dimensional linear contextual bandits or low-rank matrix bandits with sparse parameters, respectively. “Batched feedback” means that feedback is not revealed instantly; instead, they are divided into several batches, and rewards in the same batch are revealed simultaneously at the end of the batch. Hence, the agent’s knowledge is only updated once per batch. For the batched bandit problem, the agent needs to decide how to allocate rounds of interactions into batches and how to take actions in each batch.

Our problem involves three coupled challenges – (a) the exploration-exploitation tradeoff, (b) batched feedback, and (c) estimation in high-dimensional statistical models. Challenge (a) arises from the need to balance gathering enough samples to estimate the model accurately with the need to choose greedily based on the limited information available, known as the exploration-exploitation tradeoff. More importantly, since our feedback is divided into batches, we have to balance exploration and exploitation even before observing the contexts (data in the next batch). Challenge (b) is unique to our problem since we need to design the batch allocation policy so that the order of the expected regret will not be much affected by the batched feedback, thus making the decision process more challenging than the standard LASSO bandit. Finally, learning the reward functions for high-dimensional covariates naturally involves Challenge (c).

To address these challenges, we propose a novel algorithm that incorporates three key components: (a) a batch allocation policy that uses gradually decelerated-increasing batches, (b) an exploration strategy that employs -decay forced sampling and arm-elimination, and (c) high-dimensional estimation techniques such as LASSO and nuclear-norm regularization. Specifically, for (a), we propose a novel technique that guarantees sufficient i.i.d. samples for estimation convergence and develop an analysis to demonstrate that the regret bound under batched scenarios almost matches that under sequential ones. Our approach is based on the intuition that our estimations become more accurate as time passes so that the updating frequency can be reduced. Additionally, as the convergence rate of estimations slows down, the growth rate of batch sizes should be decelerated accordingly. For (b), we introduce -decay forced sampling due to the lack of knowledge about the actions at the beginning, so more importance should be attached to exploration. As more knowledge is obtained, the proportion of exploration decays. Moreover, arm elimination excludes poorly performing (sub-optimal) actions and identifies the optimal policy. For (c), under high-dimensional linear contextual bandits, the estimator will converge if a constant fraction of the non-i.i.d. sample set is i.i.d., as proved in Bastani and Bayati (2015). In the low-rank matrix bandit scenario, to the best of our knowledge, we first establish a tail inequality for a low-rank estimator with a subset of enough i.i.d. samples. Notably, the proof is significantly different and novel compared with the one for the LASSO estimator (Bastani and Bayati, 2015), where we show matrix concentration inequalities.

We theoretically demonstrate that for the sparse cases with users and covariate dimensions, only batches are sufficient to achieve a regret. Notably, the batched bandit algorithm achieves nearly the same order of regret bounds as the sequential one (LASSO bandit with ), which means that our algorithm attains a desired bound in the batched version. For a low-rank case with users and matrix dimensions, the algorithm can guarantee the regret bound on the order of with only batches. Notably, we believe that our work is the first in a low-rank matrix setting that bounds the expected reward by the logarithmic dependence both on the sample size and on the covariate matrix dimension.

1.1 Main Contributions

Our contributions are three-fold.

-

•

For high-dimensional linear bandits, we propose a computationally efficient algorithm that is based on a novel batch allocation policy. Our algorithm adjusts each batch’s length according to the estimation error’s convergence rate. Additionally, we show that our policy ensures sufficient i.i.d. samples during the estimation process. Our algorithm guarantees a regret bound of , where is the number of effective dimensions and is the total number of users. This bound almost matches that in the sequential case ( (Bastani and Bayati, 2015)).

-

•

When extending to the low-rank matrix bandit problem, we incorporate the batch allocation policy into the algorithm. Furthermore, we demonstrate that the low-rank estimator will converge if a constant fraction of the samples are independently and identically distributed. In terms of regret bounds, the algorithm guarantees an regret bound, where is the upper bound of the effective matrix rank and is the dimension of the matrix. To the best of our knowledge, this is the first bound that achieves a logarithmic square dependence on both the sample size and the matrix dimensions.

-

•

We conduct experiments on synthetic and real datasets to validate the performance of our algorithms. Particularly, we compare our algorithm under certain batches with the sequential version (). Our results show that the performance of our algorithms nearly approximates the sequential one.

1.2 Related Work

Our research on batched high-dimensional bandit problems is built upon the fields of contextual bandits, high-dimensional statistics, and batched literature. This section will provide a brief overview of these three areas.

The contextual bandit problem is characterized by the exploration-exploitation tradeoff, which arises from the bandit feedback setting where only the feedback from the chosen decision is accessible to the agent. There are two main approaches to address the tradeoff. The first approach is to explore and exploit simultaneously by comparing the confidence bounds for all the policies, which are represented by UCB-type algorithms (Auer, 2002; Dani et al., 2008; Rusmevichientong and Tsitsiklis, 2010; Abbasi-Yadkori, 2013; Deshpande and Montanari, 2012). The second approach is to arrange pure-exploration steps, which was first proposed by Goldenshluger and Zeevi (2013). They introduce a forced sampling method to generate enough i.i.d. samples and prove that the OLS bandit algorithm attains a regret bound logarithmically dependent on the sample size. However, their algorithm does not efficiently apply to high-dimensional settings.

In terms of high-dimensional contextual linear bandits, following the i.i.d. covariate setting and the approaches in Goldenshluger and Zeevi (2013), Bastani and Bayati (2015) propose the LASSO bandit under the sparsity condition . With a tighter regret analysis and convergence on LASSO estimators, their algorithm achieves a poly-logarithmic dependence on the sample size and covariate dimension: . Additionally, by adopting techniques from LASSO bandit and using the MCP method, Wang et al. (2018) propose a -decay sampling method. The regret bound yielded by their G-MCP-Bandit algorithm is optimal on the sample size and covariate dimension .

Following LASSO bandit, much bandit literature has focused on the exploration-free version of high-dimensional contextual linear bandits. By requiring more diversity for the covariate distribution (relaxed symmetry condition), Ariu et al. (2020); Oh et al. (2021) neither proceed with exploration nor require knowledge of the sparsity parameter without the marginal condition. Thus, their algorithms are parameter-free. Furthermore, Bastani et al. (2021) propose the Greedy-First algorithm that determines whether the greedy policy fails with a hypothesis test on the covariates and rewards. Additionally, there is an emerging body of literature on high-dimensional contextual linear bandit problems that propose algorithms to tackle various scenarios (Kim and Paik, 2019; Hao et al., 2020; Oh et al., 2021; Ariu et al., 2022). Further effort has been made to investigate the challenges in sparse linear Markov decision process (MDP) by (Hao et al., 2021).

In low-rank matrix scenarios, significant progress has been made recently. In statistics, Negahban and Wainwright (2011) derive estimation error bounds for the trace regression model under nuclear norm penalization. Then, Fan et al. (2021) analyze the robust low-rank matrix recovery for heavy-tailed data by developing a robust quadratic loss function. When utilizing the low-rank structure in the bandit problem, Jun et al. (2019) and its generalization Lu et al. (2021) propose online computation algorithms that bound the expected regret with , where omits poly-logarithmic factors of the covariate matrix dimension , matrix rank , and sample size . Additionally, Li et al. (2022) provide a novel analysis technique by applying the matrix Bernstein inequality. However, due to some gaps, their approach cannot lead to regret depending logarithmically on . In this paper, we introduce the statistical analysis of low-rank estimators and prove the convergence result for non-i.i.d. samples. With more rigorous analysis, we achieve an expected regret of .

Ultimately, our work is related to batched settings for high-dimensional sparse linear contextual bandits (Ren and Zhou, 2020). The field of bandits and Markov decision processes with batched feedback has been rapidly developing in recent years (Perchet et al., 2016; Gao et al., 2019; Han et al., 2020; Wang et al., 2021; Karbasi et al., 2021) due to their broad applications in real-world problems. Specifically, Wang and Cheng (2020) study batched high-dimensional sparse bandits with similar settings to our work. However, they set the batch size as fixed, so the regret bound is multiplied by the batch size number. In contrast, we design a fine-grained grid according to the estimation error bound. Meanwhile, Kalkanli and Ozgur (2021) propose batched Thompson sampling for the multi-armed bandit (MAB) via a dynamic batch allocation. To the best of our knowledge, our algorithm is the first to attain a regret bound in almost the same order as the LASSO bandit algorithm.

1.3 Notation

For any integer , let be the set . For any vector and index subset , denote by the vector composed of nonzero elements of and by the index set of nonzero entries of . For any data matrix , let refer to its sample covariance matrix. For any subset , let represent . For , denote and by and respectively. Additionally, let and represent positive real numbers and positive integers, and refer to the set of positive semidefinite matrices of size d by d. For any real-valued random variable , we claim that it is -subgaussian if for every , which implies that and .

For matrix models, use to denote the space of -by- real matrices. For any matrix , define and to be its operator norm, nuclear norm, Frobenius norm, the sum of the absolute matrix values and elementwise max norm respectively. The vectorized version of is denoted as , where is the column of . Let denote the -by- matrix constructed by , where is the column of . For any time index subset , let be the submatrix whose rows are for all the . Given two matrices , we use to denote the matrix inner product , where is the trace operator.

2 Preliminaries

This section will describe the standard problem formulation of contextual bandits for high-dimensional linear models with batched feedback.

2.1 Contextual Bandit

Consider an arrival process with time steps. At each step , a new user (such as a patient) arrives, and the agent observes the covariate vector containing all available personal information (such as medical records, clinical test reports, and other useful observations). The observed sequence of covariates is drawn i.i.d. from an unknown distribution over a deterministic set . The agent then has access to arms and aims to optimize the total reward produced during the process. Let be the chosen arm at time . If the agent selects action , she will receive the reward .

The agent’s policy is denoted as , where depends on the user’s covariate and the information that the agent attains before the current batch. To benchmark the performance of policy , we introduce the optimal policy , which attains the highest reward given the true parameters. Performance of the policy is measured by the notion of regret, which is defined as the cumulative expected suboptimality compared with the best policy:

| (2.1) |

The goal is to find the policy that minimizes the cumulative regret up to time .

2.2 Linear Models

Suppose that each arm has an unknown parameter . If we choose arm at time , the reward is generated as

where the noise is a -subgaussian variable. Then, we consider two linear models: the high-dimensional sparse model and the low-rank matrix model.

High-Dimensional Sparse Model. The reward for arm pulled at time is formulated as

Now we have the dataset , where the rows of design matrix are the vectors and treatment arm and the components of response vector are the rewards (for all ). We also denote the noise vector by . By putting ’s as a long vector , and appropriately expanding by padding zero according to the treatment arms, and still denoting the rearranged matrix as , we can write the model as . Thus, for a regularization parameter , the LASSO estimator (Tibshirani, 1996) is determined by solving

| (2.2) |

Low-Rank Matrix Model. The reward for arm pulled at time satisfies

where is the true coefficient matrix. Given the sequence of covariate matrices and the rewards , we can represent this model in a more compact form by defining the observation operator with elements and writing

where and are the -dimensional vectors with components and , respectively. Generally, the parameter matrices are low-rank or well approximated by a low-rank matrix. Hence, we estimate by solving

| (2.3) |

where is a regularization parameter. The sum of its singular values gives the nuclear norm of :

2.3 Batched Feedback Structure

The concept of batching refers to dividing time sequences into groups. During each batch, the agent interacts with a group of users simultaneously. Once all the decisions in this group have been made, the feedback belonging to the same batch is revealed. To illustrate this interaction protocol, we present Figure 1, where the total time steps are divided into batches by the agent before the interaction starts, and the rewards are revealed at each division point . The division points are called grid with (batch is composed of time steps to ). Note that if , the size of each batch is , and the bandit becomes fully sequential. If , at the beginning of each batch, the agent needs to specify policies for the batch without observing contexts. The agent makes decisions only according to the feedback from previous batches. To achieve the final goal of maximizing the expected cumulative reward , the agent faces two tasks before the process. One task is to decide how to divide the feedback into batches, called the batch allocation policy. The other task is to specify how to take action in each batch.

3 Algorithm

In this section, we propose algorithms to overcome three online learning and decision-making challenges: the exploration-exploitation tradeoff, batched feedback, and high-dimensional estimation with non-i.i.d. data. These challenges are coupled together for the following reasons.

The first challenge, the exploration-exploitation tradeoff, arises from the fact that the agent can only observe the reward corresponding to the chosen arm . Hence, it is likely to mistake suboptimal arms for the optimal choice with limited samples. Because the greedy decision-making can lead to suboptimal decisions, we need enough i.i.d. samples to guarantee the convergence of estimators for each arm . On the other hand, excessive forced samples (collected with a random exploration) can also sacrifice cumulative regret as they don’t use collected data to make decisions, particularly when the estimation becomes more accurate. Additionally, at the beginning of each batch , the agent must allocate the exploration and exploitation for time steps before observing the covariates , making the tradeoff more difficult. The second challenge, batched feedbacks, occurs because in batch , the rewards are not available to the agent until the decision is made for time step . Therefore, for the covariates , the agent have to make decisions according to the estimates , where represents the data collected in the first batches for arms . The third challenge is high-dimensional estimations based on non-i.i.d. data, which requires a carefully designed algorithm and analysis to achieve the desired convergence result.

We employ several techniques to address the challenges faced in this problem. The first challenge is overcome by using forced sampling and arm elimination. To balance the exploration and exploitation, we introduce the -decay forced sampling method to obtain i.i.d. samples via random explorations (Wang et al., 2018), which not only ensures sufficient i.i.d. samples but also gradually reduces the proportion of forced sampling. For arm elimination, we use a two-stage sampling procedure that leverages the gap between optimal and suboptimal arms (as defined in Assumption 4.3), thus increasing the chances of selecting the optimal arm. The second challenge is addressed by using a fixed batch allocation policy where the batch sizes satisfy a specific equation. This policy is formulated based on two intuitions: firstly, we want the batch size to adapt to changes in estimation accuracy; secondly, we aim to roughly balance the regret incurred in each batch and achieve a logarithmic dependence on the batch number , as we will illustrate below. Finally, the third challenge is addressed by using LASSO or nuclear-norm regularized regression. We defer the analysis to 4.

3.1 Batched High-Dimensional Sparse Bandit Algorithm

For batched high-dimensional linear bandits, we propose the batched high-dimensional sparse bandit algorithm, which is called the batched sparse bandit for simplicity. For convenience, we denote whole-sample and forced-sample (obtained from random explorations) sets for arm up to the end of batch by and , respectively. Let and be estimators trained on and .

The execution of the batched sparse bandit: Before the arrival process, given the number of users and batches , the agent designs the grid and initializes the parameters. Then, in each batch , the decisions are made only based on the estimators in the previous batches. For each time step in the current batch, a user comes with an observable covariate vector . After recording the user’s covariate , the agent draws a binary random variable , where with probability , for a given . There are two situations:

-

•

If , the agent will randomly implement a decision with equal probability. Then, she will update the forced-sample dataset by including (as the reward is temporarily unobserved but will be updated when available).

-

•

If , the agent will execute the two-stage decision procedure in Algorithm 2. In the first stage, she will construct a decision candidate set containing the arms yielding rewards (with the forced-sample estimators ) within of the maximum possible value. If the set has only one component, this component will become the optimal decision; otherwise, the precise stage will proceed based on the whole-sample estimators . The agent will select the arm that generates the highest reward in the decision candidate set .

Then, the agent updates the whole-sample dataset by appending the datapoint . When all the selections in batch are completed, she will observe the user’s response to the decision and fill the reward in the corresponding datapoints for all in batch . Meanwhile, the agent will update the regularization parameter , forced-sample estimators and whole-sample estimators via LASSO for , based on the sample sets and . The detailed procedure is presented in Algorithm 1.

Batch Allocation Policy: Our grid design is motivated by two intuitions - (a) the batch size should be adjusted according to the estimation accuracy; (b) the batch size can adjust the regret of each batch so that the cumulative regret has a logarithmic dependence on the batch number. From (a), we will find from Proposition 5.5 that the estimation error at the end of batch is bounded by , so the regret at time step in batch attains the bound (as we will show in appendix). To balance the regret for each batch, we incorporate the term into the batch size. From (b), only if the expected regret in batch is bounded by an order of can the cumulative regret (controlled by an integral ) be bounded by a polynomial of . Hence, the regret will be finally bounded by a polynomial of , which almost equals the regret bound under the sequential setting (Bastani and Bayati, 2015). Suppose the number of batches . The grid is as follows:

| (3.1) | ||||

where is a predetermined parameter satisfying that , and is an absolue constant. The setting of is to get feedback more frequently at the beginning.

-decay Forced Sampling Method: To ensure enough i.i.d. samples by the online learning and arm-selection process, we adopt the -decay forced sampling method from Wang et al. (2018), where random selections are made with decreasing probability . This decreasing probability is applied to avoid exploring too much to control the cumulative regret. Furthermore, it will be presented in Lemma C.8 that the -decay forced sampling method guarantees sufficient forced samples (on the logarithmic dependence on sample sizes) to ensure the performance of estimation.

Two-Stage Sampling Procedure: The procedure in Algorithm 2 is introduced from Bastani and Bayati (2015). The screening stage determines a preliminary set of decisions by eliminating the sub-optimal arms based on the forced-sample estimators. The radius of the preliminary set is to ensure that the sub-optimal arms are excluded and the optimal arm is included. Then, in the precise stage, we determine the arm that yields the best-estimated reward according to the whole-sample estimators.

3.2 Batched Low-Rank Bandit Algorithm

Now we propose the batched low-rank bandit algorithm for low-rank matrix models defined in 2.2. Accordingly, we define the whole-sample estimator as and the forced-sample estimator as , and choose the grid identically to (3.1). Then we can obtain the batched low-bank bandit for trace regression by only changing the parameters into matrix forms in Algorithm 1 and updating the regularization parameter by . Thus, for conciseness, we do not repeat the pseudocode of the algorithm here. Additionally, since the grid choice remains the same, the upper and lower bounds of forced-sample sizes up to time step are still on the order of (by Lemma C.8). The performance of the policy will be discussed in the following section.

4 Theoretical Results

4.1 High-Dimensional Sparse Bandit

Before illustrating the theorem, we will show four technical assumptions necessary for the theoretical analysis of the expected cumulative regret. We adapt the standard assumptions in the high-dimensional linear bandit literature such as Bastani and Bayati (2015), Wang et al. (2018) and Wang and Cheng (2020).

Assumption 4.1 (Parameter set).

There exist positive constants , and , such that for any and , we have , and .

The first assumption is proposed by Rusmevichientong and Tsitsiklis (2010) to guarantee that the observed covariate vector is in the bounded subspace , and the arm parameters are bounded and sparse. According to the Hölder inequality , we have . Thus, the expected regret at any time step is at most .

Assumption 4.2 (Margin condition).

There exists a constant such that for and , we have .

This assumption is known as the margin condition for the -class classification problem and is adapted to linear bandit models in Bastani and Bayati (2015). In this assumption, the probability that the covariate vector approximates a decision boundary hyperplane is bounded. Therefore, given a user’s covariate vector, the decisions are appropriately separated based on their rewards. Otherwise, it is likely to pull the wrong arm since there may exist two arms whose rewards are too close.

Assumption 4.3 (Arm optimality).

There exists two mutually exclusive sets and which make up the arm set , with the suboptimal set and the optimal set , where parameter and is a positive constant satisfying that .

Following from Goldenshluger and Zeevi (2013) and Bastani and Bayati (2015), this assumption requires that the suboptimal and optimal sets make up . For any optimal arm , there exists a region with positive measure such that for any covariate , the corresponding reward is strictly optimal. For the suboptimal arm , for any covariate , the expected reward is strictly smaller than the best possible expected reward. Additionally, Assumption 4.2 and Assumption 4.3 are related in the way that when the margin condition holds and the parameter is small enough, the arm optimality holds (i.e., for any arm , it belongs to either or ). Particularly, we can demonstrate that this assumption holds whenever Assumption 4.2 holds and the probability of falling into the margin is small enough. For details, we refer readers to Lemma D.1.

Assumption 4.4 (Compatibility condition).

There exists a constant such that, for each , we have , where we define

and for each , , where the region and .

Note that for arms , the region is exactly defined in Assumption 4.3. The compatibility condition (or restricted eigenvalue condition) is necessary for the consistency of high-dimensional estimators (Candes et al., 2007; Bickel et al., 2009; Negahban et al., 2012; Bühlmann and Van De Geer, 2011; Wang et al., 2018; Fan et al., 2020). As the covariance matrix is the conditional expectation of the Hessian matrix for the loss function in (2.2), this condition requires that the loss function is locally strongly convex in a cone subspace. In low-dimensional settings, this condition means that loss functions are strongly convex near the true parameter. Nevertheless, the strong convexity is inappropriate for high-dimension settings since the covariate dimensions significantly outweigh sample sizes. To illustrate the above four assumptions, a simple example is provided in Bastani and Bayati (2015).

Following the batched sparse bandit algorithm, the expected cumulative regret upper bound can be established in the theorem below.

Theorem 4.5 (Total Regret).

Theorem 4.5 first demonstrates that the expected cumulative regret of the batched sparse bandit over time steps is upper-bounded by within a factor of , thus matching the regret bound achieved by the sequential version (Bastani and Bayati, 2015), within a factor of . Therefore, the batched sparse bandit successfully balances the regrets in each batch with the grid choice. Nevertheless, the batched sparse bandit and LASSO bandit both do not meet the lower bound , which is a natural extension from the lower bound in the low-dimensional setting (Goldenshluger and Zeevi, 2013).

Now we briefly introduce the proof techniques. To begin with, since our algorithm ensures enough i.i.d. samples in both forced-sample and whole-sample sets, we will obtain the convergence result for the forced-sample and whole-sample estimators by the LASSO tail inequality for non-i.i.d. data and the batch allocation policy. Then, we divide the total sample size into three groups and bound the regret in each group. Eventually, with our batch allocation policy, the cumulative expected regret is upper bounded by . For more details, see 5 for a proof sketch and Appendix A.3 for the detailed proof.

4.2 Batched Low-Rank Bandit

Before introducing the assumptions for the low-rank bandit, we adopt the concept of decomposability and subspaces from Wainwright (2019), which is crucial for the compatibility condition in the matrix form. Consider any matrix and denote its row and column spaces as and . Given a positive integer , we let and denote the -dimensional subspaces of vectors. Then the two subspaces of matrices can be defined as

| (4.1) | ||||

| (4.2) |

where and denote the subspaces orthogonal to and . By taking the orthogonal complement of (4.2), we can define the subspace , which is a strict superset of . Additionally, it is easy to verify that the nuclear norm is decomposable with respect to the given pair of subspaces defined in (4.1) and (4.2):

for any pair of matrices and .

For arm , suppose that the target matrix has a low-rank structure , and write it in the SVD factored form , where the first entries of the diagonal matrix are the nonzero singular values of , and the first columns of the orthonormal matrices and are the left and right singular vectors of . Let and be the -dimensional subspaces spanned by the column vectors of and respectively, thus yielding the pair of subspaces . Now we state the assumptions for the low-rank matrix bandit, which are adapted from the high-dimensional linear bandit and Wainwright (2019).

Assumption 4.6 (Parameter set).

The dimensions and the rank constraint parameter . There exist positive constants , , , such that for any and , we have , , .

This assumption ensures that the covariate and the parameter are in bounded subspaces. The bounds on and in Li et al. (2022) imply this assumption. According to the matrix Hölder inequality (Baumgartner, 2011), for any time , holds. However, the regret at any time step is upper bounded by .

Assumption 4.7 (Margin condition).

There exists a such that for and , we have .

Assumption 4.8 (Arm optimality).

There exists two mutually exclusive sets and that include all arms for some positive constant , with suboptimal set and optimal set , where parameter and is a positive constant satisfying that . In other words, for optimal arms , we define

| (4.3) |

Assumptions 4.7 and 4.8 are directly extended from the corresponding assumptions for the high-dimensional linear setting.

Assumption 4.9 (Compatibility condition).

Consider the pair of subspaces defined above. There exists a constant such that, for each , we have , where we define

| (4.4) |

and , where the region and for each .

For arms , the region is exactly defined in Assumption 4.8. This assumption, adapted from the compatibility condition for linear estimation, is closely related to the restricted strong convexity for matrix estimation (Equation (10.17) in Wainwright (2019)). This condition also ensures the diversity of training samples so that the low-rank estimation will converge.

We also have the regret upper bound for the batched low-rank bandit in the following theorem. Recall that the agent’s decision and the optimal policy at time are and , respectively. The expected cumulative regret at the time

is bounded by the following theorem.

Theorem 4.10 (Total regret).

Theorem 4.10 indicates that the expected cumulative regret of the batched low-rank bandit over time steps is upper-bounded by . To the best of our knowledge, this is the first regret bound for low-rank linear bandits, outperforming previous algorithms for low-rank bandit problems in both and . The analysis of this theorem directly follows the proof of Theorem 4.5. We present the details of proving the bound in Appendix B.

5 Proof Sketch

Although we adopt the main structure of the proof in Bastani and Bayati (2015), we highlight our technical novelty from three perspectives: first, since the batched setting significantly decreases the frequency of updating parameters, we design the grid iteration (3.1) to counteract the influence of batched feedbacks and bound the regret in batch on the order of ; second, we demonstrate that for general batch allocation policies (not restricted to our grid selection), there are sufficient i.i.d. samples in the whole-sample set. Notably, we demonstrate in Proposition 5.3 that this conclusion holds for a general grid choice by utilizing the tricks of keeping the second half of batches and bounding the summations with integrations; third, for the low-rank bandit, we prove a convergence result for non-i.i.d. data in Lemma C.1. The difficulty lies in coping with the matrices and operator norms. Hence, we prove a convergence result for Matrix Sub-Gaussian Series and adopt matrix Bernstein inequality from Tropp (2011).

The contents of this section are organized as follows. To begin with, we present abridged technical proofs for the batched sparse bandit in four parts: in 5.1, we adopt the LASSO tail inequality for non-i.i.d. data from Bastani and Bayati (2015) to provide a basic convergence guarantee; in 5.2, we obtain the convergence result for forced-sample estimators; in 5.3, we construct an i.i.d. subset and demonstrate the convergence for whole-sample estimators; in 5.4, we ultimately get the regret upper bound.

5.1 A LASSO Tail Inequality For Non-i.i.d. Data

Since general convergence guarantees do not apply to this setting, we adopt the tail inequality for non-i.i.d. data from Bastani and Bayati (2015), which facilitates the proof of the following convergence properties. First of all, a general conclusion for the LASSO estimator for the non-i.i.d. sample will be proved. Specifically, we consider the design matrix whose rows are bounded random vectors (i.e., for all ), the response vector and the noise vector , and describe their relationships with the linear model

It is assumed that . For any subset , let be the submatrix of whose rows are for each . Recalling the notation in 1.3, we define the terms , , and similarly for any subset . Trained on samples in (which are not required to be i.i.d.), a LASSO estimator is obtained for any :

Now suppose that there exists some unknown subset comprised of i.i.d. samples which are subject to a distribution . We define and assume that for a constant . Bastani and Bayati (2015) demonstrates in the following lemma that if the size of an i.i.d. sample is large enough to make up a constant fraction of the samples in , a convergence guarantee will be proved for the LASSO estimator trained on non-i.i.d. samples in . The result is shown as follows.

Lemma 5.1 (LASSO Tail Inequality For Non-i.i.d. Data).

For any , if , , , and , then the following tail inequality holds:

where and .

The proof of this lemma can be seen in Appendix EC.2 of Bastani and Bayati (2015), from which we know that generating sufficient i.i.d samples is necessary for the convergence of the LASSO estimator. Then, we will show in the following two subsections that the -decay and arm elimination methods guarantee the number of i.i.d. samples.

5.2 Estimator From Forced Samples Up To Batch

Proposition 5.2.

Although the forced samples are i.i.d., we cannot directly utilize the LASSO tail inequality for i.i.d. data. Since the compatibility condition in Assumption 4.4 holds for the conditional covariance instead of , we define as the i.i.d. sample set from . By invoking Lemma C.1 with and defined above, the convergence result follows. The detailed proof is given in Appendix A.1.

5.3 Estimator From Whole Samples Up To Batch

Consider a general grid choice :

where is a predetermined function. In this subsection, we will explore what kind of conditions for a general grid choice will ensure the tail inequality for the whole-sample estimators of optimal arms .

The challenge lies in the fact that simply invoking Lemma 5.1 with and is not applicable due to the limited number of i.i.d. samples in , which is far from sufficient for the requirement of Lemma 5.1. To resolve this, we will construct an i.i.d. sample set with the sample size in the same order of .

In Algorithm 1, when random sampling is not conducted, the agent follows a two-step decision procedure to determine the optimal decision. The first step involves determining whether an arm is in the decision candidate set based on the performance of its forced-sample estimator. According to Proposition 5.2, this estimator will not be far from its true parameter value. We denote as the event in which the forced-sample estimators in batch are within a given distance of their true parameters:

Using Proposition 5.2, if , we have . Moreover, conditioning on event , for any , we can verify the following inequality:

In other words, if event happens for , in the first step, the agent will only choose arm , which is the optimal arm. To bound the total number of time steps up to batch when holds, and the agent selects the optimal arm via the two-step sampling procedure, we define for and :

where . The difference between defined in this paper and in Bastani and Bayati (2015) is that we need to divide the summation by batches. The represents the size of a subset where the forced sampling is not executed, the covariate belongs to optimal set , and the forced-sample estimator for the past batches approaches the true one with a given distance. We also denote the sample set as , and we will show in Appendix A.2.2 that the samples in are i.i.d. (given distribution ). Thus, denotes the number of a type of i.i.d. samples in the whole-sample set up to batch . Eventually, knowing that is a martingale, we can bound the value of for each in the following proposition.

Proposition 5.3.

Suppose and the grid satisfies that is non-decreasing, for all for some constant and . When , where , for any , we have

This proposition implies that it suffices to require that the recursive grid function is non-decreasing and the growth rate does not exceed exponential growth (). The proof of Proposition 5.3 is provided in Appendix A.2.1. This proposition indicates that, with high probability, the actual i.i.d. sample size for decision in will be of the order of instead of . Ensuring the number of is more challenging than in the case of Lemma EC.14 in Bastani and Bayati (2015) for two reasons. Firstly, our estimators are not updated until the end of each batch, and secondly, the forced-sampling time steps are not predetermined. Forced sampling may occur at each time step with a decreasing probability. Additionally, there is a discrepancy between the proof of Proposition 5.4 and Proposition 5 in Wang et al. (2018). When lower-bounding the probability of for each time step in batch , the latter directly lower-bounds and by their values of and at the final time step . This step is questionable as cannot be lower-bounded by for . To overcome this challenge, we introduce a new half-control technique that bound the summations of the remaining part of batches through integration.

Coming back to our specific grid in (3.1), we demonstrate in Appendix A.2.2 that this grid satisfies the conditions in Proposition 5.4 that show the following result.

Proposition 5.4.

Under Algorithm 1, if , , then for , we have

5.4 Cumulative Regret up to Time

Finally, with our convergence results, we divide the time steps, up to time , into three groups to provide an upper bound for each group. Specifically, we define and partition the three groups are as follows.

-

1.

Time steps in batch (initialization) or forced sample .

-

2.

Time steps out of forced-sample set in batch when event does not hold.

-

3.

Time steps out of forced-sample set in batches when event holds.

Note that the three groups collectively cover all time steps. The cumulative expected regret at time in the first group is bounded by , as the reward cannot be controlled in the initial stage (the first batches) and forced-sampling time steps. The regrets in these groups are bounded by (as stated in Assumption 4.1).

In the second group, the cumulative expected regret at time is upper-bounded by , as event occurs with a high probability according to Proposition 5.2. Therefore, we can assume the worst cases for the time steps in this group.

In the third group, the cumulative expected regret is bounded by . As event holds, the agent uses the forced-sampling estimator to choose the estimated best arm, and we can use Proposition 5.4 without worrying that the chosen arm may not be the true optimal arm. Thus, the agent will choose the optimal arm when the agent does not sample randomly. Using Proposition 5.5 for all time steps in this group, we can bound the expected regret in this group. By combining the cumulative regret for all three groups, Theorem 4.5 follows. The detailed proof is presented in Appendix A.3.

6 Empirical Results

In this section, we will evaluate the performance of the batched sparse bandit and the batched low-rank bandit by examining how their cumulative regret is affected by different factors such as time steps, batch number, data dimensions, and the size of the decision set.

In the high-dimensional sparse setting (6.1), we will compare the performance of our batched bandit algorithm to the LASSO bandit algorithm using both synthetic data and real-world datasets. This evaluation is based on the formulations outlined in Bastani and Bayati (2015). In the low-rank setting (6.2), we will conduct experiments on synthetic data to compare the performance of our batched bandits.

6.1 High-Dimensional Bandit

6.1.1 Synthetic Data

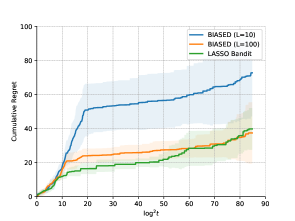

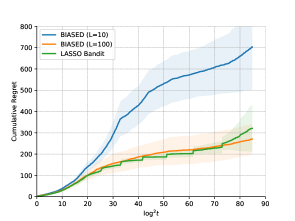

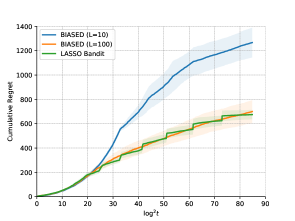

Dataset. Consider three cases for arm number , data dimension and sparsity parameter : (1) ; (2) ; (3) . In these cases, we benchmark the performance of the Batched hIgh-dimensionAl SparsE banDit (BIASED) under batches and to the LASSO bandit (Bastani and Bayati, 2015) (with ). Moreover, to validate the influence of the covariate dimension on the cumulative regret for BIASED, we fix and plot the regret with . In each scenario, the true parameter for each is a sparse vector, where only randomly chosen components are nonzero. These values are sampled from a uniform distribution on . At each time , a user covariate is independently drawn from a Gaussian distribution and truncated within . Then, the noise variance is .

Algorithm Inputs. Given the time periods , to validate the robustness of our algorithm with respect to different batch numbers , we choose the size of the first batch and consider two batch numbers by using two different grid parameters according to (3.1): 1) To obtain , we choose ; 2) To obtain , we choose . For the other input parameters, we select the initialized regularization parameters , the -decay forced sampling parameter (consistent with the value in Theorem 4.5). For LASSO bandit, we choose the forced sampling parameter . For both bandits, the arm optimality parameter in scenarios (1) and (2), and in scenario (3). Conclusively, the choice for the tuning parameters is basically consistent with Bastani and Bayati (2015).

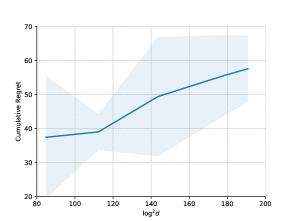

Results. The performance of BIASED is compared with the LASSO bandit in Figure 3 under and batches, respectively. The horizontal axis is set to to examine the order of the upper bound with respect to . The results, averaged over trials and have confidence intervals, validate that the regret bound is of the order . Additionally, Figures 3(a)-3(c) demonstrate that BIASED is robust to the choice of parameters , , and . Although a smaller batch size of yields a higher regret than , both regret bounds are in the same order. Finally, Figure 3(d) shows that the cumulative regret at time depends on the dimension with .

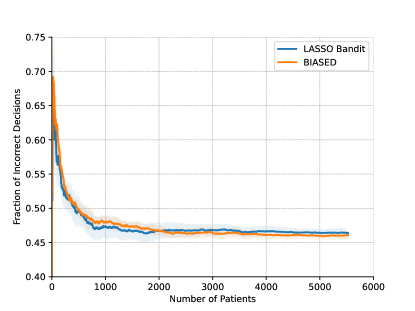

6.1.2 Warfarin Dosing

Dataset. In the first experiment on real data, we apply our algorithm to a precision medicine problem called warfarin dosage (Consortium, 2009), where physicians decide the optimal warfarin dosage for arriving patients. In the dataset 111https://github.com/chuchro3/Warfarin/tree/master/data, patients carry individual covariates of dimension , including demographic, diagnosis, previous diagnoses, medications, and genetic information.

Bandit Formulation and Hyperparameters. According to Bastani and Bayati (2015), the problem is formulated as follows. The correct dosage is divided into three levels: low, medium and high. Since the correct dose is given but concealed, the reward is if the chosen arm is the patient’s correct dose. Otherwise, the reward is . For the hyperparameters, we set the initialized regularization parameters , and the arm optimality parameter . For BIASED, the batch number , the grid parameter , the size of the first batch and -decay forced sampling parameter . For LASSO bandit, the forced sampling parameter .

Results. In Figure 4, we compare the fraction of incorrect dosages between BIASED and LASSO bandit averaging over trails. We note that the batched bandit nearly exhibits the same performance as the sequential bandit (LASSO bandit).

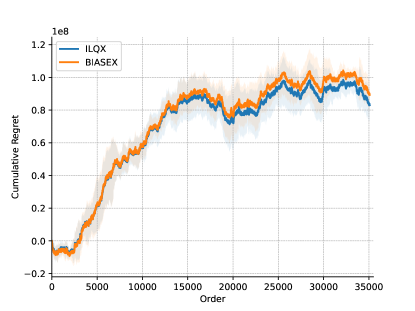

6.1.3 Dynamic Pricing in Retail Data

Dynamic pricing problems with unknown demands (Besbes and Zeevi, 2009) can be modeled with a batched linear contextual bandit. Following Xu and Bastani (2021), we use a publicly available dataset of customized orders from meal delivery companies 222https://datahack.analyticsvidhya.com/contest/genpact-machine-learning-hackathon-1/. We select a subset containing orders from the same city during the same period. The information on each order includes meal categories, cuisines, base prices and promotions. For each order , the decision is the price (a continuous variable falling in a range of ). The demand is modeled as a linear function of the contexts (of dimension ) and the price (Ban and Keskin, 2021):

The goal is to maximize the revenue , which is known as the reward function. In the algorithm, we make parameter estimations , and determine the price . When selecting the price greedily, we let be the truncated maximizer of the estimated revenue function, i.e., . Then, we measure the performance by the regret , where we define (where the and are the true demand and price given in the dataset), and . Note that since the true parameters are unknown, the demand corresponding to the price was predicted using the estimation of the whole training set. We adapt the exploration strategy for dynamic pricing in Ban and Keskin (2021) to the batched sparse bandit, which is named BIASEX and shown in Algorithm 3. The details can be found in Appendix E.

To compare the performance of BIASEX, we ran the algorithm with batches and compared it with ILQX, the LASSO-based pricing algorithm used in Ban and Keskin (2021). Each curve was averaged over trials, and the results are shown in Figure 5. Our batched algorithm performed comparably to the baseline algorithm, demonstrating its effectiveness in solving batched dynamic pricing problems with unknown demands.

6.2 Low-Rank Bandit

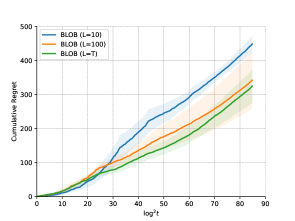

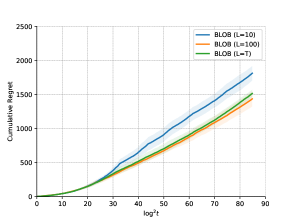

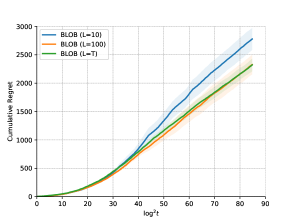

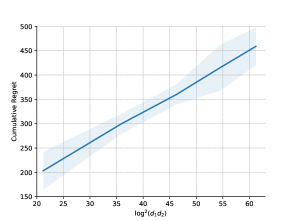

Dataset. We run the simulation for different arm numbers , matrix row numbers and column numbers (assume that row and column numbers are the same ) and rank values : (1) ; (2) ; (3) . In the three scenarios, we compare the performance of the Batched LOw-rank Bandit (BLOB) among different batches: , and (i.e., the sequential version). Then, by fixing , we plot as in the graph to validate the order of regret bound on matrix dimensions. The true matrix parameter is a diagonal matrix with only nonzero components. The user covariate is a by matrix independently drawn from a Gaussian distribution and truncated between .

Algorithm Inputs. Given time steps , we choose to obtain , and choose to derive . In all scenarios, the number of the first batch is . The initialized regularization parameters are chosen as . Since the -decay sampling parameter , let . For all the cases, the arm optimality parameter is set as . The parameter selections are according to Theorem 4.10 and follow the choices for the synthetic data in high-dimensional bandits.

Results. The curves of the regret bound are shown in Figure 6. From Figures 6(a)-6(c), we validate that the upper bound is on the order of and robust with respect to and . Furthermore, Figure 6(d) verifies that the dependence of the cumulative regret at time on the dimension is .

7 Conclusions

This paper presents two algorithms dealing with the batched version of online learning and the decision-making process in high-dimensional and low-rank matrix data, respectively. We propose a predetermined grid selection to reduce the influence of the batched setting and successfully approximate the regret bound in batched versions to the one in sequential versions. The regret bounds for both proposed algorithms are proved to be in the number of sample sizes via at least batches. Particularly for low-rank versions, our algorithm first achieves the regret bound with the polynomial logarithmic dependence on both sample sizes and matrix dimensions. In conclusion, the proposed algorithms both maintain high time efficiency and achieve regret bounds close to sequential ones. Finally, the experiments based on synthetic and real data validate that the batched sparse bandit and the batched low-rank bandit perform favorably.

We end by discussing some limitations of the batched sparse bandit and the batched low-rank bandit. First of all, our grid selections are not adaptive and flexible enough to adjust to the performance in previous batches. Second, as mentioned in Bastani and Bayati (2015), the forced sampling method applied by our algorithms may bring irreversible consequences. Take medical decision-making as an example, where making decisions randomly sacrifices the patients’ health and causes medical tangle. In those cases, it is more appropriate to avoid pure exploration. For example, UCB Auer (2002) explores within the range of confidence sets. For another example, Bastani et al. (2021) proposes a greedy-first algorithm to avoid exploration as much as possible.

References

- Abbasi-Yadkori (2013) Abbasi-Yadkori, Y. (2013). Online learning for linearly parametrized control problems.

- Alon and Spencer (2016) Alon, N. and Spencer, J. H. (2016). The probabilistic method. John Wiley & Sons.

- Ameko et al. (2020) Ameko, M. K., Beltzer, M. L., Cai, L., Boukhechba, M., Teachman, B. A. and Barnes, L. E. (2020). Offline contextual multi-armed bandits for mobile health interventions: A case study on emotion regulation. In Fourteenth ACM Conference on Recommender Systems.

- Ariu et al. (2020) Ariu, K., Abe, K. and Proutière, A. (2020). Thresholded lasso bandit. arXiv preprint arXiv:2010.11994.

- Ariu et al. (2022) Ariu, K., Abe, K. and Proutière, A. (2022). Thresholded lasso bandit. In International Conference on Machine Learning. PMLR.

- Auer (2002) Auer, P. (2002). Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3 397–422.

- Ban and Keskin (2021) Ban, G.-Y. and Keskin, N. B. (2021). Personalized dynamic pricing with machine learning: High-dimensional features and heterogeneous elasticity. Management Science, 67 5549–5568.

- Bastani and Bayati (2015) Bastani, H. and Bayati, M. (2015). Online decision-making with high-dimensional covariates. Forthcoming in Operations Research.

- Bastani et al. (2021) Bastani, H., Bayati, M. and Khosravi, K. (2021). Mostly exploration-free algorithms for contextual bandits. Management Science, 67 1329–1349.

- Baumgartner (2011) Baumgartner, B. (2011). An inequality for the trace of matrix products, using absolute values. arXiv preprint arXiv:1106.6189.

- Besbes and Zeevi (2009) Besbes, O. and Zeevi, A. (2009). Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations research, 57 1407–1420.

- Bickel et al. (2009) Bickel, P. J., Ritov, Y., Tsybakov, A. B. et al. (2009). Simultaneous analysis of lasso and dantzig selector. The Annals of statistics, 37 1705–1732.

- Bühlmann and Van De Geer (2011) Bühlmann, P. and Van De Geer, S. (2011). Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media.

- Candes et al. (2007) Candes, E., Tao, T. et al. (2007). The dantzig selector: Statistical estimation when p is much larger than n. The annals of Statistics, 35 2313–2351.

- Consortium (2009) Consortium, I. W. P. (2009). Estimation of the warfarin dose with clinical and pharmacogenetic data. New England Journal of Medicine, 360 753–764.

- Dani et al. (2008) Dani, V., Hayes, T. P. and Kakade, S. M. (2008). Stochastic linear optimization under bandit feedback.

- Deshpande and Montanari (2012) Deshpande, Y. and Montanari, A. (2012). Linear bandits in high dimension and recommendation systems. In 2012 50th Annual Allerton Conference on Communication, Control, and Computing (Allerton). IEEE.

- Fan et al. (2023+) Fan, J., Guo, Y. and Yu, M. (2023+). Policy optimization using semiparametric models for dynamic pricing. Journal of the American Statistical Association 1–29.

- Fan et al. (2020) Fan, J., Li, R., Zhang, C.-H. and Zou, H. (2020). Statistical foundations of data science. CRC press.

- Fan et al. (2021) Fan, J., Wang, W. and Zhu, Z. (2021). A shrinkage principle for heavy-tailed data: High-dimensional robust low-rank matrix recovery. Annals of statistics, 49 1239–1266.

- Gao et al. (2019) Gao, Z., Han, Y., Ren, Z. and Zhou, Z. (2019). Batched multi-armed bandits problem. Advances in Neural Information Processing Systems, 32.

- Geyik et al. (2018) Geyik, S. C., Dialani, V., Meng, M. and Smith, R. (2018). In-session personalization for talent search. In Proceedings of the 27th ACM International Conference on Information and Knowledge Management.

- Goldenshluger and Zeevi (2013) Goldenshluger, A. and Zeevi, A. (2013). A linear response bandit problem. Stochastic Systems, 3 230–261.

- Han et al. (2020) Han, Y., Zhou, Z., Zhou, Z., Blanchet, J., Glynn, P. W. and Ye, Y. (2020). Sequential batch learning in finite-action linear contextual bandits. arXiv preprint arXiv:2004.06321.

- Hao et al. (2021) Hao, B., Lattimore, T., Szepesvári, C. and Wang, M. (2021). Online sparse reinforcement learning. In International Conference on Artificial Intelligence and Statistics. PMLR.

- Hao et al. (2020) Hao, B., Lattimore, T. and Wang, M. (2020). High-dimensional sparse linear bandits. Advances in Neural Information Processing Systems, 33 10753–10763.

- Jun et al. (2019) Jun, K.-S., Willett, R., Wright, S. and Nowak, R. (2019). Bilinear bandits with low-rank structure. In International Conference on Machine Learning. PMLR.

- Kalkanli and Ozgur (2021) Kalkanli, C. and Ozgur, A. (2021). Batched thompson sampling. Advances in Neural Information Processing Systems, 34 29984–29994.

- Karbasi et al. (2021) Karbasi, A., Mirrokni, V. and Shadravan, M. (2021). Parallelizing thompson sampling. Advances in Neural Information Processing Systems, 34.

- Kim and Paik (2019) Kim, G.-S. and Paik, M. C. (2019). Doubly-robust lasso bandit. Advances in Neural Information Processing Systems, 32.

- Li et al. (2010) Li, L., Chu, W., Langford, J. and Schapire, R. E. (2010). A contextual-bandit approach to personalized news article recommendation. In Proceedings of the 19th international conference on World wide web.

- Li et al. (2022) Li, W., Barik, A. and Honorio, J. (2022). A simple unified framework for high dimensional bandit problems. In International Conference on Machine Learning. PMLR.

- Lu et al. (2021) Lu, Y., Meisami, A. and Tewari, A. (2021). Low-rank generalized linear bandit problems. In International Conference on Artificial Intelligence and Statistics. PMLR.

- Negahban and Wainwright (2011) Negahban, S. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, 39 1069–1097.

- Negahban et al. (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J., Yu, B. et al. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical science, 27 538–557.

- Oh et al. (2021) Oh, M.-h., Iyengar, G. and Zeevi, A. (2021). Sparsity-agnostic lasso bandit. In International Conference on Machine Learning. PMLR.

- Perchet et al. (2016) Perchet, V., Rigollet, P., Chassang, S. and Snowberg, E. (2016). Batched bandit problems. The Annals of Statistics 660–681.

- Qiang and Bayati (2016) Qiang, S. and Bayati, M. (2016). Dynamic pricing with demand covariates. Available at SSRN 2765257.

- Ren and Zhou (2020) Ren, Z. and Zhou, Z. (2020). Dynamic batch learning in high-dimensional sparse linear contextual bandits. arXiv preprint arXiv:2008.11918.

- Rivasplata (2012) Rivasplata, O. (2012). Subgaussian random variables: An expository note. Internet publication, PDF, 5.

- Rusmevichientong and Tsitsiklis (2010) Rusmevichientong, P. and Tsitsiklis, J. N. (2010). Linearly parameterized bandits. Mathematics of Operations Research, 35 395–411.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58 267–288.

- Tropp (2011) Tropp, J. (2011). Freedman’s inequality for matrix martingales. Electronic Communications in Probability, 16 262–270.

- Wainwright (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, vol. 48. Cambridge University Press.

- Wang and Cheng (2020) Wang, C.-H. and Cheng, G. (2020). Online batch decision-making with high-dimensional covariates. In Internaxtional Conference on Artificial Intelligence and Statistics. PMLR.

- Wang et al. (2021) Wang, T., Zhou, D. and Gu, Q. (2021). Provably efficient reinforcement learning with linear function approximation under adaptivity constraints. Advances in Neural Information Processing Systems, 34.

- Wang et al. (2018) Wang, X., Wei, M. M. and Yao, T. (2018). Online learning and decision-making under generalized linear model with high-dimensional data. arXiv preprint arXiv:1812.02962.

- Xu and Bastani (2021) Xu, K. and Bastani, H. (2021). Learning across bandits in high dimension via robust statistics. arXiv preprint arXiv:2112.14233.

Appendix A Proof of Theorem 4.5

We restate Theorem 4.5 and list the specific choices of the parameters as follows.

Theorem A.1 (Restatement of Theorem 4.5).

In this section, to demonstrate Theorem 4.5, we first show the convergence of random-sample estimators and whole-sample estimators in A.1 and A.2 respectively. Then, we bound the cumulative regret with the convergence results in A.3.

A.1 Convergence of Random-Sample Estimators

The convergence inequality of random-sample estimators is stated in Proposition 5.2. The proof does not follow from Lemma 5.1 directly, since according to Assumption 4.4, we have only assumed that the compatibility condition holds for rather than . We denote the forced-sample size for arm up to batch by and the sub-sample set as . We will solve this problem by showing that is a set of i.i.d. samples from , and applying Lemma 5.1.

Proof of Proposition 5.2.

To begin with, we will prove that is a set of i.i.d. samples from . For each , is drawn randomly from and therefore with probability at least , , i.e., . Additionally, are independent for different values of , since the original sequence is i.i.d., each , is an i.i.d. sample of .

Furthermore, define the event

Then, by invoking Lemma C.10 we have

| (A.1) |

Suppose that holds, since and , we have . Thus by combining Lemma 5.1 and C.9, and by , , , and , we know that

where the first inequality is deduced by using , and the second inequality is due to . Finally, by invoking (A.1), we obtain the following result

Therefore, we conclude the proof of Proposition 5.2. ∎

A.2 Convergence of Whole-Sample Estimators

To demonstrate the convergence of whole-sample estimators, we first show in A.2.2 that sufficient i.i.d. samples are guaranteed in the sample set for each optimal arm . Then, we invoke Lemma 5.1 to attain the tail inequality for whole-sample estimators in A.2.3.

A.2.1 A General Form

Proof of Proposition 5.3.

Recall in 5.3 that we define as

To begin with, for each optimal arm , we will prove that if , the arm will definitely be chosen, and furthermore the components of are i.i.d.(with distribution ). For any , since and holds, we have

which means that

As a result, the agent will only select arm at the first step. Additionally, since only relies on samples in , the is independent of . Therefore, random variables are i.i.d. samples from . Now, since the presence of each in or not in is simply rejection sampling, in is distributed i.i.d. from . Therefore, we have which counts a part of i.i.d. samples of the whole-sample set up to batch . Moreover, for the reason that

and that covariates are generated randomly, we know that is a martingale with , we can use to bound the value of with Azuma’s inequality:

So we further get:

| (A.2) |

Then, we can express as follows:

where the last equality comes from the fact that is independent of and that is independent of . Additionally, by invoking Proposition 5.2 with for all arms in , we have .

Then, let , where . If , we have

where the first inequality hold since is an increasing function and , and the second inequality uses .

If , we write that

Then, the can be lower bounded by

| (A.3) |

By invoking Lemma F.5, it follows that

which is taking back into (A.3) to obtain that

| (A.4) |

where the last inequality is due to . Similar to Lemma F.5, we have

By taking the result above back into (A.4), we get

| (A.5) |

where the second inequality is by applying , and the last inequality is due to . Eventually, we obtain the desired inequality by combining (A.2) and (A.5). ∎

A.2.2 Proof of Corollary 5.4

A.2.3 Proof of Proposition 5.5

Proof of Proposition 5.5.

Since

Applying Proposition 5.4, we have

Let , , . Since , and , we have satisfies . Therefore, we can apply Lemma 5.1 with to obtain the following result:

where the last inequality is deduced by using and . Taking

we get

where the choice of implies . Hence, we conclude the proof of Proposition 5.5. ∎

A.3 Bounding the Cumulative Regret

Proof of Theorem 4.5.

Recall that the cumulative regret up to time , batch is divided into three groups:

| (A.6) |

In the sequel, we will bound the regrets in each group separately.

Regrets in Group 1.

We bound as

From Lemma C.9, we find that if , , and , the following inequality can be obtained:

which indicates that

| (A.7) |

Thus we have

By combining the inequality above and (A.7), we get

| (A.8) |

Regrets in Group 2.

From Proposition 5.2, we have

which implies that

Therefore, can be bounded as follows:

| (A.9) |

where the third equality comes from the grid structure:

Regrets in Group 3.

Without loss of generality, at time in batch (), it is assumed that arm is true optimal arm. Then, we can bound the regret as follows:

| (A.10) |

Let denote the event for that at time the true reward of arm is at least less than that of arm , which means that , for . Then we have the following bound:

| (A.11) | ||||

| (A.12) |

We bound the term in (A.12) as follows:

where the last inequality comes from Assumption 4.2.

Now we consider the term in (A.11), which can be bounded as follows:

By applying Hölder’s inequality to the right hand side of the last inequality above, we get

| (A.13) |

Then, from Proposition 5.5, we have the following inequality:

| (A.14) |

By combining (A.13) and (A.14) and setting , we obtain:

Then, the following result can be deduced:

where .

We find that the upper bound of time in the same batch is equal. Therefore, we bound the third part of the regret as follows:

We continue to compute that

| (A.15) |

where and .

Appendix B Proof of Theorem 4.10

The following theorem is the restatement of Theorem 4.10 with details about the constants.

Theorem B.1 (Restatement of Theorem 4.10).

The proof of Theorem 4.10 is composed of three subsections: in B.1 and B.2, we demonstrate the convergence of random-sample estimators and whole-sample estimators, respectively; in B.3, the cumulative regret is decomposed into several parts and upper-bounded seperately.

Estimator from forced samples up to batch : By combining Lemma C.1 and Lemma C.8, we will obtain the tail inequality for forced-sample estimator . The proof is presented in Appendix B.1.

Proposition B.2.

Estimator from whole samples up to batch : To show the performance of the whole-sample estimator , we start by proving that enough number of i.i.d. data in whole samples is guaranteed. We also define the event that the forced-sample estimator at batch is within a given distance of its true parameter:

According to Proposition B.2, if , we have . Moreover, for and , we define

where . Now we know that is a martingale, and the same proof of Proposition 5.4 constructs its bound: if , , then for , we have

| (B.1) |

Now, we will show the convergence of the whole-sample estimators. The proof is presented in Appendix B.2.

Proposition B.3.

Cumulative regret up to time : Eventually, we will divide all time steps into three groups in the same way as 5.4. We will bound the regrets in each group by applying convergence inequalities for forced-sample and whole-sample estimators in Proposition B.2 and B.3. The full proof of Theorem 4.10 refers to the process of proving Theorem 4.5 in Appendix A.3. The details are presented in Appendix B.2.

B.1 Convergence of Random-Sample Estimators

Proof of Proposition B.2.

We know from the proof of Proposition 5.2 that is a set of i.i.d. samples from for arm . Since , , we can invoke Lemma C.9 to obtain

| (B.2) |

Moreover, since and

, we have . Then, by applying Lemma C.1 and Lemma C.10 to (B.2), with , , and , it follows that

where the last inequality is deduced since and . Hence, we finifsh the proof of Proposition B.2. ∎

B.2 Convergence of Whole-Sample Estimators

B.3 Bounding the Cumulative Regret

Proof of Theorem 4.10.

We can divide the cumulative regret into three parts in the same way as (A.3). In the sequel, we bound the regrets in each group.

Regret for the first group:

From Lemma C.9, we know that if , , and , the following inequality can be obtained:

| (B.3) |

Thus, refering to (A.3), we can bound the regret of the first group as

| (B.4) |

Regret for the second group:

From Proposition B.2, we know that

Therefore, can be bounded as follows:

| (B.5) |

where the third equality comes from the grid structure (3.1).

Regret for the third group:

Define . Then, similar to the decomposition in (A.11) and (A.12), the regret at time can be bounded as

| (B.6) | ||||

| (B.7) |

The term (B.7) can be bounded by Assumption 4.7:

| (B.8) |

Correspondingly, the term (B.6) is bounded by

| (B.9) |

Then, we derive from Proposition B.3 that

which is applied to (B.3) by setting :

| (B.10) |

Combining (B.8) and (B.3), we obtain that

where . Then, we accumulate the regret in this group:

| (B.11) |

where and .

Appendix C Proof of the Supporting Lemmas

C.1 A Tail Inequality for Low-Rank Matrix

This subsection provides a demonstration of a tail inequality for the low-rank matrix model. The inequality is stated in Lemma C.1. We summarize the key steps as follows. First, we demonstrate in Appendix C.1.1 that when the covariance matrix of satisfies the compatibility condition and holds, the nuclear norm of is bounded. To establish these conditions, we prove in Appendix C.1.2 that satisfies the compatibility condition with high probability by showing that is small with high probability and that meets the compatibility condition. Finally, in Appendix C.1.3, we show that occurs with high probability by using the matrix subgaussian series and the matrix Bernstein Concentration.

The novel concentration result for non-i.i.d. data here, which is obtained by adopting the matrix Bernstein inequality and deriving an inequality for matrix subgaussian series (Lemma F.3). These techniques differ from the prior low-rank bandit literature, particularly from Li et al. (2022). Although they proved a similar result for low-rank bandits, their work doesn’t directly utilize inequalities for matrix series in Lemma C.4, leading to exploration time steps of when is large. Therefore, their regret bound has a dependence of instead of . In our work, we consider a non-i.i.d. data set with an unknown subset consisting of i.i.d. samples. We assume that , where . Then, denoting by , we present the following result.

Lemma C.1 (A Tail Inequality for Non-i.i.d. Data).

If , for any , , , and , the following tail inequality holds:

where , .

C.1.1 A General Tail Inequality

Given a sample set (not necessarily i.i.d.) of size , we first consider a general convex loss function with the nuclear norm regularization. We aim to determine under what conditions the estimation error will be bounded.

Lemma C.2.

Proof.

To begin with, we use the optimality of :

| (C.1) |

Taking the second order Tailor expansion of into (C.1), we deduce that

Applying Hölder’s inequality for Schatten norms to the leftmost term of the equation above, it follows that

| (C.2) |

If event holds true, (C.2) can be written as

| (C.3) |

Additionally, by invoking Lemma C.3 we have

| (C.4) |

Furthermore, if in (4.9), it follows that

| (C.5) |

where the second inequality is derived since any matrix has rank at most (Wainwright, 2019), and the last inequality is by applying (C.4). Then by combining (C.5) and (C.3), we finally get

thus we prove that

Thus, the proof is accomplished. ∎

Then, we demonstrate that by properly choosing the regularization weight , the error vector is in special cone in the following lemma.

Lemma C.3.

This lemma is adopted from Proposition in Wainwright (2019). For the completeness of the theory, we present the proof here.

Proof.

The argument starts with the function given by

| (C.8) |

By the convexity of , we know that

| (C.9) |

where the second inequality is by applying the matrix Hölder inequality for spectrum norms, and the last inequality is deduced by conditioning on in (C.6) and the triangle inequality.

Additionally, we have

| (C.10) |

where the second inequality is by the triangle inequality, and the last is because of the decomposability of subspaces . Taking (C.1.1) and (C.1.1) back into (C.8), we obtain that

| (C.11) |

Since the optimality of implies that , we obtain from (C.1.1) that

which completes the proof. ∎

In the next two sections, we will prove that and event holds with a high probability separately.

C.1.2 Compatibility Condition for Non-i.i.d. Samples

Recall the whole set , the i.i.d. subset and the corresponding covariance matrices and . In this part, we will show that is small with high probability in the beginning so that we can prove with high probability. Afterwards, we finally prove that with high probability.

Lemma C.4.

Given i.i.d. samples such that satisfy for all , then when , we have

where , , and .

Proof.

Since

we know that

Moreover, we obtain the following bound

where the first inequality uses Jenssen inequality, and the equality is deduced since matrix is positive semi-definite and for any positive semi-definite matrix , we have . Hence, it follows that

Then, by invoking Lemma F.2 with and , we get

Taking , we can find and , which completes the proof. ∎

Lemma C.5.

There exists an i.i.d. sample set in a non-i.i.d. set . Suppose for some and , then .

Proof.

Since , for any matrix in (C.7), we have . Then, using , we deduce that

| (C.12) |

where we denote as . In addition, by the matrix inequalities, it is deduced that

| (C.13) |

where the second inequality is by applying (C.4) and the reason for the last inequality is that . We obtain from (C.12) and (C.13) that

| (C.14) |

Thus the following result is obvious:

| (C.15) |

which completes the proof. ∎

Lemma C.6.

Suppose that for some . If , we have

where .

C.1.3 Probability of

Given the observations from the matrix regression model in 2.2, recall the loss function . Then the event is given by

Lemma C.7.

Suppose Assumption 4.6 holds and define . Then, we have

Proof.

Since for all , we get the following bounds

Hence, we can invoke Lemma F.3 with and to derive that for all ,

which finishes the proof. ∎

C.1.4 Proof of Lemma C.1

Proof.

Firstly, since and , we get . Using Lemma C.6, it holds that

| (C.16) |

where . Then from Lemma C.7,

| (C.17) |

where . Take (C.16) and (C.17) back into Lemma C.2 and let and . Then, it follows that

| (C.18) |

Now let and choose , where . This choice guarantees that . Then taking the selections back into (C.1.4) yields the final result:

Finally, we finish the proof of Lemma C.1. ∎

C.2 Bounds about the Forced Samples

In this section, we focus on bounding the size of the forced sample. Lemma C.8 and Lemma C.9 are adopted from Proposition 2 and Lemma EC.8 of Wang et al. (2018). For the sake of completeness and clarity, the full proof is presented here.

Lemma C.8 (Proposition 2 of Wang et al. (2018)).

Let , and . Then, for arm , under the -decay forced sampling method, with probability at least , the size of forced sample up to time is bounded by

Proof.

Via the -decay forced sampling method, the system randomly draws arm at time with the probability of , where denotes the number of arms. Therefore, at time , the expected total number of time steps at which arm were randomly sampled is

When , it follows that

| (C.19) |

The function is decreasing in , so can be bounded from both sides for any :

Since , we plug from to into the above inequality respectively and sum them up:

| (C.20) |

From (C.19) and (C.20), the can be bounded as follows:

| (C.21) |

Because , it is regarded as the summation of bounded i.i.d. random variables. We can connect and with the Chernoff bound:

| (C.22) |

Using the upper and lower bounds provided in (C.21), the in (C.22) can be relaxed:

| (C.23) |

When , and , the right-hand size of (C.23) can be simplified as

Therefore, we conclude the proof. ∎

Lemma C.9 (Lemma EC.8 of Wang et al. (2018)).

Proof.

From Lemma C.8, we have

| (C.24) |

According to Assumption 4.3, for , there exists a region such that . Therefore, the expected number of will be lower bounded by:

| (C.25) |

where the last inequality comes from (C.21). Because indicates , we simplify (C.25) as follows:

| (C.26) |

Applying the Chernoff inequality to , we obtain:

Using (C.26), we deduce that:

| (C.27) |