Path-dependent PDEs for volatility derivatives

Abstract.

We regard options on VIX and Realised Variance as solutions to path-dependent partial differential equations (PDEs) in a continuous stochastic volatility model. The modeling assumption specifies that the instantaneous variance is a function of a multidimensional Gaussian Volterra process; this includes a large class of models suggested for the purpose of VIX option pricing, either rough, or not, or mixed. We unveil the path-dependence of those volatility derivatives and, under a regularity hypothesis on the payoff function, we prove the well-posedness of the associated PDE. The latter is of heat type, because of the Gaussian assumption, and the terminal condition is also path-dependent. Furthermore, formulae for the greeks are provided, the implied volatility is shown to satisfy a quasi-linear path-dependent PDE and, in Markovian models, finite-dimensional pricing PDEs are obtained for VIX options.

Key words and phrases:

VIX options, path-dependent PDE, implied volatility, rough volatility2020 Mathematics Subject Classification:

60G22, 35K10, 91G201. Introduction

In a continuous time model, VIX and Realised Variance (RV) both boil down to time-averages of the stochastic volatility of the asset. Prices of derivatives on these underlyings are represented as expectations, hence their numerical evaluation naturally leans towards Monte Carlo methods. The extensive literature dedicated to simulation schemes—which covers their design, numerical implementation, and convergence analysis—bears witness to the omnipresence of this approach, especially for volatility derivatives. As an alternative, this paper proposes to view option prices on volatility derivatives such as the VIX as solutions to a path-dependent PDE (PPDE). Before getting into more details, we should first explore the motivation behind this class of financial assets. Readers who wish to get down to business may directly jump to Section 1.2.

1.1. Background

Volatility derivatives are used both as risk management and speculation tools to get a direct exposure to an index or a stock’s volatility. Although this class has attracted attention as a whole, VIX derivatives became some of the most liquid instruments on the financial markets. The CBOE Volatility Index (VIX) measures the 30-day forward-looking volatility of the S&P500 index (SPX); more precisely, it represents a log-contract on the SPX, approximately replicated with a weighted sum of quoted Calls and Puts. In an idealised stochastic volatility model , we have by Itô’s formula

| (1.1) |

where is the 30-day window and represents the forward variance curve. The structural links between VIX and SPX, visible from the computation above, require a consistent model for able to jointly calibrate options on both underlyings simultaneously. This central issue is a driving force of research on volatility and has proven particularly challenging to resolve. Since the introduction of VIX options in 2006, massive efforts were produced by the community to design models and numerical methods up to the task.

Bergomi [13] and Gatheral [29] rapidly argued for multifactor models (Ornstein-Uhlenbeck and CEV respectively), before jump models tackled the problem. We will gently leap over this stream of research as we are concerned here with continuous and particularly rough volatility models. Let us mention that robust statistical estimators and significant empirical evidence [14, 20, 21, 28, 35, 56] confirmed the original thesis that log-volatility trajectories indeed have low regularity [30]. Evidence from options data can also be found in [7, 23, 33, 49]. More relevant to this paper’s premise, a variety of simulation schemes were developped around and away from the traditional Euler scheme, including the hybrid scheme [9, 44], a tree formulation [36], Markovian multifactor approximations [1, 3, 6] and quantization [15]. When it comes to pricing VIX options, these models also went through the Monte Carlo pipe [17, 31, 37, 38, 50]. Indeed, rough volatility has not been generous on alternatives: a few asymptotic results [4, 25, 39, 41] and a weak expansion [18] are the only contenders to the best of our knowledge.

Widening our scope a little, we observe that signature-based models led to a semi-closed formula for VIX [22]. When the variance is a semimartingale with linear drift, one can write as a function of only, which leads to a standard type of pricing PDE. The authors of [5, 26, 42, 47] exploited this property to derive fast pricing techniques and small-parameter expansions in Heston type of models. Similarly, under the assumption that the variance curve is of the form with a semimartingale, Buehler [19] proved an HJM condition for the variance curve which takes the form of a PDE. This is again the case in the Heston model. Unfortunately, the non-Markovianity of the (quadratic) rough Heston model prevents both these ideas to be applied there. Recently, several multifactor models, dubbed quintic [2], S-M-2F-QHyp [49] and 4-factor path-dependent volatility [34], claimed that simple transformations of Markovian dynamics were sufficient to capture the joint calibration. The first two, in particular, model the volatility as transformations of Ornstein-Uhlenbeck (OU) processes, similarly to what Bergomi originally proposed in [12, 13]. This further motivates us to model the squared volatility as a generic function of a multidimensional Gaussian Volterra process , such as a fractional Brownian motion or an OU process. Our framework thus encompasses many of the models presented above, in particular the family of Bergomi models which can be of multifactor, rough or mixed type or any combination of the aforementioned (see Examples 2.2 and 2.3). Suitable and more stringent conditions should allow to generalise our results to a broader class of processes including solutions to stochastic Volterra equations. However, none of the above-mentioned models would benefit from this extension (not even the quadratic rough Heston model) hence we refrain from doing so.

1.2. Path-dependent PDEs

Even though options with path-dependent payoffs are known since the work of Dupire [24] to satisfy PPDEs, they were, to the best of our knowledge, never formulated in the context of variance options. The case of rough volatility, more recent, was initiated by the functional Itô formula derived in [54], and the PDE aspect was further developped in [16, 55]. The insight of the former authors is that, contrary to the Markovian case, if is a Gaussian Volterra process then the conditional expectation not only depends on the past trajectory but also on the “forward curve” . This infinite-dimensional path encodes all the necessary information to recover the Markov property in the space of continuous paths . The functional Itô formula is then established for processes of the type where , and involves Fréchet derivatives in . This choice of state space seems natural but has a notable drawback: for rough volatility purposes the kernel , which is also the direction of the pathwise derivative, is not bounded on and hence does not belong to . This singularity has to be circumvented via an approximation argument, as described in [54], which imposes stringent conditions on and its derivatives. Thus, the derivative is not of Fréchet type but is the limit of a sequence of Fréchet derivatives. We also note for completeness that the functional Itô formula was actually proved for a much larger class of Volterra processes.

1.3. Contributions

In this work, we are interested in option prices of the form , where is a volatility derivative (think as in (1.1)) and . Our contributions are threefold:

-

1/

We show that such a price has the Markovian representation , for a map ; see Proposition 3.1;

-

2/

Under the additional assumption that and are three times differentiable with suitable growth conditions (which include the square root for ), we prove that the map is of class with appropriate regularity and growth estimates, which implies that it is the unique classical solution to a path-dependent PDE in this class; see Theorem 4.6.

-

3/

We observe that the total implied variance (equivalently the implied volatility) satisfies a quasi-linear path-dependent PDE; see Theorem 5.1.

The first point is different than the case where the payoff is a function of because involves the trajectory up to a time as well as a conditional expectation with respect to . The second contribution relies on the general result [16, Proposition 2.14] which grants well-posedness of the PPDE provided some conditions on are met. Our task thus consists in studying the Fréchet differentiability of , as well as regularity and growth of its derivatives. The conditions themselves depend on the singularity of the kernel and require enough smoothness so that the approximation argument holds. We obtain a Cauchy problem of the form

where is (the limit of) a Fréchet derivative and has a semi-closed form as an integral over . This infinite-dimensional analogue of the heat equation has the advantage of being linear parabolic, with an explicit terminal condition. Much effort has been dedicated to faster pricing of VIX options and even greater to the simulation of fractional processes but, meanwhile, PPDE schemes are still in their infancy (the literature consists in three papers [40, 51, 53] which all rely on inserting a discretisation of the path in a neural network). Provided the path is encoded in an efficient way, this alternative viewpoint serves as the theoretical groundwork for new numerical schemes that spit out the whole implied volatility surface and the greeks without relying on simulation or Monte Carlo. Signature kernel methods [52] appear to be strong candidates as they combine a tailored encoding of the path through its signature, an efficient numerical computation and convergence guarantees; for those reasons we will apply them to this problem in an incoming work [46].

Implied volatilities are the unitless equivalent to option prices which enable practitioners to compare financial products with different features. It is obtained by inverting the Black-Scholes formula which is not an easily tractable technique. Our third contribution consists in retrieving two quasi-linear path-dependent PDEs satisfied by the total implied variance and the implied volatility. This PDE representation was not known for volatility derivatives and is one of very few pre-asymptotic results in the literature. The computation is inspired by [11] where uniqueness and asymptotic expressions are also established.

Besides numerical schemes, PPDEs may therefore find other applications in asymptotic analysis and they were already instrumental in obtaining weak rates of convergence for rough volatility models in [16]. Analogously to the finite-dimensional theory, the PPDEs offer additional tools for the analysis of complex volatility derivatives and their dynamics. On the more fundamental side, several open questions are worthy of interest, such as: Can we relax the assumption to bare convexity, in particular to show that the Call price is in ? Is there a maximum principle of the type as for the finite-dimensional heat equation? These are left for future research.

Finally, we observe in Section 6 that, in Markovian models, if the volatility derivative does not depend on the trajectory on (e.g. which only acts on ) then neither does the option price. This leads to finite-dimensional PDEs displayed in Corollary 6.2 and implemented for the pricing of VIX options in a two-factor Bergomi model where is an OU process. The rapidity and efficiency of this approach appoints it as an alternative to Monte Carlo methods, especially if one yearns for prices with respect to initial conditions, time to maturity, or for financial greeks.

1.4. Organisation of the paper

The rest of the paper is arranged as follows. Section 2 introduces the model and some notations. In Section 3 we develop and prove our first result, the Markovian representation of the option price. The path-dependent PDE is presented in Section 4, followed by some additional results on the greeks, and preceded by the definitions of the pathwise derivatives and the subspace of of interest. We derive the PPDE for the implied volatility in Section 5, discuss the Markovian case in Section 6 and, finally, the proof of the main result is gathered in Section 7.

2. Framework

2.1. The model

Let us fix a filtered probability space as well as two finite times and two intervals and . The conditional expectation with respect to the filtration will be denoted, for all , as . Let be a square-integrable matrix-valued kernel such that for and is finite, and let be a -dimensional Brownian motion for some . We introduce the Gaussian Volterra process

| (2.1) |

with mean , a deterministic continuous path, and covariance structure

We make the standing assumption that is a continuous stochastic process. This condition is directly linked to the behaviour around zero of the function and can be checked easily using Kolmogorov’s or Fernique’s continuity criterion, see [32, Lemma 2.3] for the latter. All the kernels presented in Example 2.2 do satisfy this condition.

Definition (2.1) is slightly more general than what is usually found in the literature where . In this case, the Gaussian process has memory of the past until an arbitrary fixed time . However, when pricing an option at time (the moment the option is issued), one can have information about what happened before and this is precisely what the function contains. Mathematically, can be interpreted as , which is -measurable if one extends the Brownian motion to the negative half-line. This is similar in spirit to the original fractional Brownian motion of Mandelbrot and Van Ness [43], as well as the Brownian semistationary processes which allow to decouple roughness from long-time memory [10]. In dimension one, with the choice of kernel , the “Hurst” parameter determines the roughness while controls the memory properties.

Let . The variance derivatives we will look at are encompassed by this general definition:

| (2.2) |

and is a nice enough function. This includes forward variance models as introduced by Bergomi [12], see also Example 2.3. The subset of on which is non-zero plays an important role so we name this support . The following example illustrates this.

Example 2.1 (Derivatives).

We consider a continuous time stochastic volatility model with no interest rate defined by the SDE .

-

•

Letting (with corresponding to one month) and for (hence ) yields . For , the conditional expectation corresponds to the price at time of a VIX future if and a VIX Call if with .

-

•

If one sets then is the realised variance and . For , the random variable corresponds to the price at time of a variance swap if and a Call on realised variance if

We can also give examples of popular models covered by our setup.

Example 2.2 (Kernels).

The following types of one-dimensional kernels account for most of the models found in the literature. One can build matrix-valued kernels by taking those as entries. For :

- •

-

•

Power-law: corresponds to the class of rough volatility models for and long-memory fractional volatility models for . Here hence Kolmogorov’s continuity theorem implies that the trajectories of (a modification of) are almost -Hölder continuous.

-

•

Shifted power-law: yields a semimartingale path-dependent model whenever and extends the range of the Hurst exponent to . We refer to [2] for more details.

-

•

Gamma: , for and , leads to a rough volatility model with an exponential damping and the same continuity properties as above.

-

•

FBM: and recovers the fractional Brownian motion of Mandelbrot and Van Ness [43], which also has almost -Hölder continuous paths. This binds us to consider random initial conditions; an alternative is to represent the fBM on an interval with and an intricate kernel, see for instance [45, Section 5.1.3].

-

•

Log-fBM: , where , and . For , the associated process has the same continuity property as in the power-law case, however this log-modulation includes the case which also induces a continuous process [8].

When the power-law is present, the constant is usually set to .

Example 2.3 (Volatility functions).

Different choices of non-linearity have been proposed, as the introduction witnesses. All of them can be multiplied by an initial curve to match the forward variance curve. Let denote the stochastic exponential .

-

•

One-factor (rough) Bergomi model: , for .

-

•

Multi-factor (rough) Bergomi model:

(2.3) where and so that . Note that, for , and are correlated if the kernel matrix is not diagonal.

-

•

A variety of models are studied by Rømer [49], including the two-factor rough Bergomi model, the two-factor hyperbolic model which consists in replacing by in (2.3), and a two-factor model that uses both hyperbolic and quadratic transformations. The details of the latter are shown in [49, Eqs (45)-(48)].

- •

2.2. Notations

The notation corresponds to the Euclidean norm in and Frobenius norm in . Let be the space of càdlàg paths, we recall and introduce the following:

For and , , and with a slight abuse of notation, we will write instead of , implying that for all . Let denote the set of functions continuous under . In the remainder, the time horizon will correspond to the maturity of the derivatives, which are then stochastic processes on . Meanwhile, the underlying Gaussian process is defined on , hence its trajectories live in .

3. The Markovian representation

For a function , the main protagonist of this paper is the stochastic process which represents the price of the volatility derivative under a risk-neutral measure. For all , one of the central ideas behind the functional Itô formula of [54] is to split in two parts:

| (3.1) |

where is an -measurable process while is independent of for all . It is clear that in the Brownian motion case , this decomposition boils down to . For and two paths , their concatenated path reads . For , the continuous path

will play an important role, as can be seen directly from our first main result.

Proposition 3.1.

Let and be measurable functions. There exists a measurable map such that

This map will be referred to as the option price or the value function.

Remark 3.2.

In the VIX case we have for all , in other words the option price does not depend on the past , but depends on a path that runs after the maturity . On the other hand, the RV option corresponds to .

Proof.

We recall that

which features two convoluted conditionings at and .

We first take a look at . For , , while for , as in (3.1). Since is independent of and is -measurable, there exist two measurable functions and such that

| (3.2) |

Let and , then we can define explicitly . Note that has a Gaussian distribution with zero mean and variance . Hence, for ,

| (3.3) |

where is the density function of if is non-degenerate. Furthermore, we clearly have

| (3.4) |

We turn to the second conditioning with respect to . We decompose the path , for all :

| (3.5) |

where . Since is independent of , there exists a measurable map such that we can write options on under our stochastic volatility model as

| (3.6) | ||||

almost surely, where we expressed as in (3.2). For all and , this map is defined explicitly as

| (3.7) |

which serves as the definition of and concludes the proof. ∎

Remark 3.3.

In the VIX case () we have and in the RV case () we have .

In addition to Proposition 3.1, one can give an insightful peak on the path-dependence structure of . For and , let us define

| (3.8) |

Notice that, for all , and therefore . By fixing the trajectory for some , Equation (3.7) yields

| (3.9) |

The role of the shift is made more precise here. We observe that hence . Pricing at time without including in the model comes down to computing and ignoring all the information that occured before . Introducing this shift provides a more coherent theory across all times.

The representation (3.9) allows to describe a type of time invariance for the option price. Let us write to highlight the dependence in the terminal time and the time interval. It is common for solutions to PDEs on to have the property . A similar phenomenon takes place in our setting under the assumption that is of convolution type.

Corollary 3.4.

Let and assume there exists such that for all . Then for all and measurable functions and , we have

where is the support of and if .

Remark 3.5.

For both VIX and Realised Variance, corresponds precisely to the interval of interest for an option of maturity . In financial terms, this invariance property means one can translate the price at time of an option of maturity to the price at time of an option of maturity , provided one shifts the path accordingly.

Proof.

4. The path-dependent pricing PDE

Proposition 3.1 confirms the natural intuition that options on variance, whether realised or VIX, are functions of a path. Thus the associated pricing PDE is of path-dependent type as we will see in this section. We apply the setting of [16, Section 2.2], itself adapted from [54].

4.1. The pathwise derivatives

Let us define the right time derivative

for all , provided the limit exists. We also define the Fréchet derivative with respect to , which is a linear operator on :

| (4.1) |

If it exists, it is equal to the Gateaux derivative

| (4.2) |

The second derivative , defined similarly, is a bilinear operator on and its evaluation is denoted , for all . We say that if , and exist and are continuous on , that is: for all , is continuous under for all

If is an -valued path (like ) with being the (-valued) th column then, by a mild abuse of notation, we define

which are analogous to the gradient and the trace, respectively. The solution space is adapted to the singularity of the kernel , hence we start with describing the latter.

Assumption 4.1.

For any , exists and there exist and such that

This assumption includes most kernels found in the literature, in particular those presented in Example 2.2, moreover it does not impose any condition on the structure but only on the speed of the explosion in the diagonal.

Definition 4.2.

We say that , with , if there exists an extension of in , still denoted as , a growth order and a modulus of continuity function such that: for any , and with supports contained in , the following hold:

-

(i)

for any such that ,

(4.3) (4.4) -

(ii)

for any other such that ,

(4.5) (4.6) -

(iii)

For any , and are continuous.

This definition is applied from [16, Definition 2.8], itself borrowed from [54, Definition 2.4], where we allow the exponential growth bounds with respect to because is finite for any Gaussian process and [39, Lemma 6.13]. The introduction of the parameter touches upon a technical specifity of the singular kernel case. Setting ensures that the decaying factors and on the right hand side balances the explosion of quantified in Assumption 4.1. Notice that in the regular case one can choose ; in the rough case , we will show that the value functional defined in (3.7) belongs to with .

We then extend the domain of the pathwise derivative by approximation near the diagonal. For , we introduce the truncated kernel

and the notations and . For , the spatial derivatives are defined as limits of Fréchet derivatives

| (4.7) | ||||

| (4.8) |

4.2. The main result

This section presents the main result, namely a well-posed PPDE satisfied by the option price. In order to state it, we introduce the assumptions needed on the functions and .

Definition 4.3.

-

(i)

We say that a function has polynomial growth if there exist such that . For , we write if is times continuously differentiable and and all its derivatives have polynomial growth.

-

(ii)

We say that a function has exponential growth if there exist such that . For , we write if is times continuously differentiable and and all its derivatives have exponential growth.

-

(iii)

We say that a function has exponential decay if there exist such that . For , we write if is times continuously differentiable and and all its derivatives have exponential decay. Moreover, we denote .

Assumption 4.4.

-

(i)

The map belongs to , with the growth constants .

-

(iia)

If , the map belongs to , with the growth constants .

-

(iib)

If , the map belongs to , with the growth constants .

Remark 4.5.

Under the additional assumption of exponential decay, our setup includes payoffs of the type for any . In particular, is crucial to study VIX futures and options.

Theorem 4.6.

Remark 4.7.

Several remarks are in order.

-

(1)

This PDE is not homogeneous in time because of the direction . However, in the case of convolution kernels, Corollary 3.4 recovers a certain time invariance property.

-

(2)

The derivative operator itself is of (path-dependent) heat type, already derived in [54, Theorem 4.1], and common to all PPDEs linked to a Gaussian Volterra process. The novelty is the path-dependent nature of the terminal condition. It exhibits an extra layer, the function , which is a simple Riemann integral and can be learned offline. Indeed, functionals of a path are known to be well approximated by linear maps of their signature, in which case the learning phase does not rely on a fixed discretisation grid, which means that one can evaluate the learned functional on a different time grid than the one it was trained on.

-

(3)

The vertical derivative of Dupire morally corresponds to (4.2) where is frozen on and is constant. Hence the PPDE (4.9) boils down to the functional PDE introduced in [24, 48] in the Brownian motion case where . Rigorously speaking, the two notions of derivatives differ as they are not defined on the same spaces.

-

(4)

The assumption that and are three times continuously differentiable is made for convenience but can be relaxed to two times differentiable with an -Hölder continuous second derivative for any .

-

(5)

From a financial point of view, an important question remains. Say one solves the PPDE and knows the functional , then which path should one use to compute the right price? If one is looking for the price at time then one should input to recover . Naturally, is not observed but it can be inferred from the forward variance, which is the derivative of the variance swap. Let us consider VIX derivatives in the rough Bergomi model, which means and . The forward variance is given by

In particular, at , we have which is only attainable for a non-constant curve if is also not constant.

Proof of Theorem 4.6.

The main computational part of the proof is postponed to Section 7 for clarity, and is summarised in the following lemma.

A straightforward application of Theorem 4.6 is the martingale representation derived from the functional Itô formula.

Proof.

The uniqueness of the martingale representation entails that it is equivalent to the Clark-Ocone formula [45, Proposition 1.3.14], in particular we have where denotes the Malliavin derivative. From a financial viewpoint, the martingale representation naturally lends itself to hedging formulae, see [27, Proposition 2.2]. It also shows that a market where the two following assets are traded is complete: the variance derivative with payoff and an asset with dynamics , with a Brownian motion correlated to . In practical terms, they would correspond to the S&P 500 and an option on the VIX or on the realised variance.

For completeness, we provide a more explicit expression of the pathwise derivatives at play in this section. The proof can be found in Section 7.3. For any , let and be the gradient and Hessian matrix respectively. For any , we also define for clarity and coherence

Remark 4.11.

Again, a parallel can be drawn with Malliavin calculus as we have

where and are respectively the first and second Malliavin derivatives.

5. The implied volatility counterpart

Inspired by [11], we derive a path-dependent PDE for the implied volatility of the volatility derivatives we considered so far. In this paper, Berestycki, Busca and Florent considered the implied volatility in a (Markovian) stochastic volatility model, which yields a pricing PDE on . Even in this simpler setting, well-posedness was a highly challenging task therefore we do not intend to pursue such a goal here, since the solution theory of our PPDEs remains limited.

Let be the Black-Scholes price at time of a Call option with spot , volatility , maturity , strike and with zero interest rates. The Black-Scholes formula gives

Let be the price of the traded future at time : the VIX future is , for days, while the variance swap gives (for different , see Example 2.1). Note that if were a traded asset (e.g. a stock price) then it would be a martingale and . We assume, as it is the case for both the VIX future and the variance swap, that the payoff belongs to such that is a particular case of Theorem 4.6 and solves the path-dependent PDE

Let us define the reduced variable , which hence solves for all

| (5.1) |

where denotes the Euclidean norm in . We notice that the Call price can be written as

| (5.2) |

since is independent of , see Equation (3.5) and below. We do not know at this point how to exploit the regularising property of the expectation to relax the assumption . Because of the non-differentiability of the function , this map is not covered by Theorem 4.6, hence we will make this a standing assumption, from now on and in Theorem 5.1. The future price is a true martingale, by integrability of , thus the implied volatility of the variance derivative is defined as the unique non-negative solution to

The main difference with [11] is that the future price also depends on which brings more intricate dependencies. Although some asymptotic results for implied volatility of VIX exist, the main result of this section is to the best of our knowledge the first theoretical result that holds at any time and without involving .

Theorem 5.1.

We assume that the functional defined in (5.2) belongs to for some . For all , the total implied variance is a solution of the PPDE

| (5.3) |

where represents the Euclidean norm in and for all we denote and .

Remark 5.2.

Letting , this is equivalent to the PPDE for the implied volatility

Setting , i.e. , we are left with Clearly both PPDEs, for and , are well-posed in the sense that is a classical solution. As mentioned above, whether this system of PDEs has a unique solution was already a hard problem in the Markovian case and is out of scope of this article.

Proof.

The proof follows [11, Section 3.1], only with more details. Let us introduce the reduced variables and and define the unit volatility Black-Scholes price

We observe that and solves the initial value problem

| (5.4) |

The implied volatility can be defined via this reduced approach to

| (5.5) |

We write for conciseness and the total implied variance . Through the informal chain rule formula applied to , we can define the derivatives for . Indeed, all the derivatives of and are already well-defined and , hence the derivatives of are uniquely determined by:

where we recall that and are -valued. It turns out these are also the derivatives of interest from (5.5), yielding the expression

| (5.6) | ||||

We use the relation from (5.4) and the PPDE (5.1) to get

Furthermore, we plug the classical relations of the Black-Scholes greeks

in (5.6) to obtain

This simplifies further when observing that

Since the left-hand-side is equal to zero we reach the PPDE for the total implied variance

which is precisely the claim. ∎

6. Path but no past in the Markovian case

This subsection explores the particular case of VIX options, technically speaking the case , which simplifies considerably in Markovian models. The latter corresponds to the first bullet point in Example 2.2 with the exponential kernel where , and the matrix exponential is understood componentwise, that is . Hence, setting for all with , is an Ornstein-Uhlenbeck process solution to the SDE and . Under the assumption that the payoff does not look into , the option price at time is only a function of and (Proposition 6.1), therefore no path-dependent lift is necessary and this price is recovered as the solution of a finite-dimensional PDE (Corollary 6.2). Although similar in spirit to [5, 26, 42, 47] for the Heston model, the present case involves an additional non-linearity which prevents from computing explicitly. After the theoretical results, numerical illustrations complete the picture.

Proposition 6.1.

Let and be measurable functions and . There exists a measurable map such that

Proof.

We simply have to notice that for all , . Then, Equation (3.6) reads

where is independent of . Therefore there exists a map such that almost surely. This map is defined for all and as

| (6.1) |

which concludes the proof. ∎

Classical results of Feynman-Kac type asserts that this pricing function satisfies a finite-dimensional backward Kolmogorov PDE starring the generator of the OU process. However, we can also retrieve it from the PPDE, thereby exploiting the Markov property of the OU process. First compare (3.7) and (6.1) and notice that, for all ,

| (6.2) |

From the terminal condition of the PPDE (4.9) we immediately recover the terminal condition of the PDE (6.4). Let and . Recall that and let us look carefully at the derivatives:

| (6.3) | ||||

The PPDE (4.9) holds for any , in particular for any . Therefore we obtain

Combined with the terminal condition, this entails both existence and uniqueness of the PDE.

Corollary 6.2.

Remark 6.3.

Remark 6.4.

The results of this section still hold if one replaces with a different semimartingale, however the Gaussian case has the advantage that is given in integral form because is Gaussian. For non-Gaussian processes, this function and hence the terminal condition are in general computable only by Monte Carlo.

6.1. Numerical example

Let us specify a model under which we will illustrate the option prices given by the PDE method. Let , for all , and , we define the traingular matrices and :

This yields

In the original Bergomi models [12, 13], the volatility is a function of albeit with , while more modern versions such as in [49] consider a weighted sum of nonlinear functionals of and , with and . In this section we will consider the latter. Then following Example 2.3 we define

where we set for simplicity and . Note that the correlation is not visible here, but acts in the PDE through the matrix . If we had picked then would also be present in . We are concerned with VIX options hence we set where is the 30 days window. For pricing a Call with strike we set and recall that .

For computing the terminal condition, we observe that and let such that we have

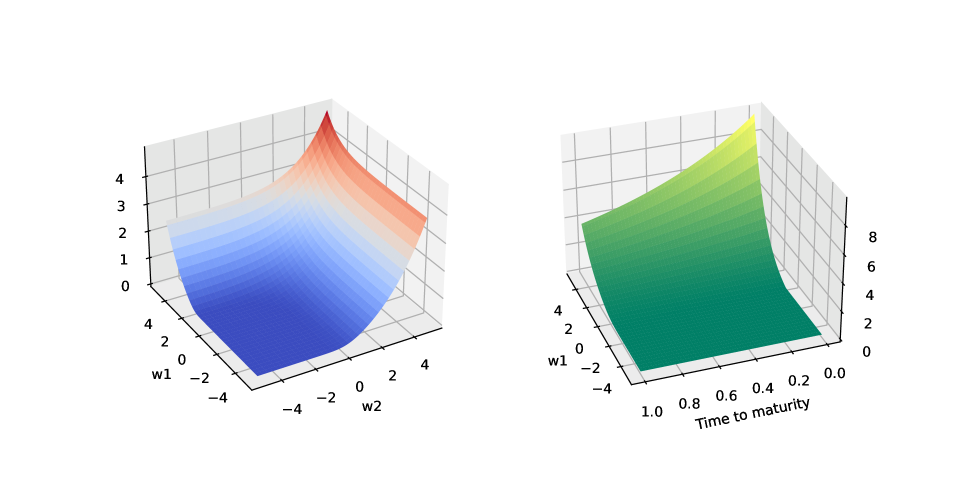

This function is then integrated between and using Simpson’s rule. We propagate this terminal condition through time via an explicit finite-difference scheme on a two-dimensional grid. The choice of boundary conditions requires more thought. By the form of the function it is apparent that the option price should vanish as and both tend to ; it is however unclear how the price shall behave in other limits and with respect to the interaction between and when the problem is not symmetric. The pronounced convex shape of the solution (see Figure 1) seems unfit for Dirichlet or Neumann conditions but invites us to move one order further and impose that the second derivative is zero at the boundary. This latter choice indeed brings the most consistency. Furthermore, for the sets of parameters that we experienced with, the best stability is achieved when choosing the number of time steps and the number of points on one slice of the grid to be equal. The complexity of the algorithm is thus . Better stability and convergence could be achieved with an implicit or Crank-Nicolson method; we leave this more thorough analysis for future research.

In this particular example, the conditional expectation can be expressed analytically therefore Monte Carlo schemes are rather straightforward; one simply needs an integration step to recover the payoff. This method has the advantage of computing at almost no cost option prices with new payoff functions since one can reuse the same simulated trajectories, while the PDE method requires to start over. On the other hand, modifying the initial condition entails simulating new paths while the PDE method outputs a price for every spatial point on the grid. The initial condition of the OU process does not have an obvious financial interpretation. Nevertheless, we recall point (5) of Remark 4.7 which details how, in the one-dimensional case, one can recover (and hence ) from the forward variance curve. In addition, the PDE scheme offers prices for all times to maturity on the grid as well as derivatives which can be leveraged to compute greeks.

We set the following parameters: , , with time steps and a grid of size with points in each dimension. We compute a Call price with strike . To illustrate our results, we present in Figure 1 slices of the solution to the pricing PDE, one with fixed time and one with fixed .

6.2. Implied volatility

The dimension reduction also applies to the implied volatility PPDE investigated in Section 5. Recalling the definitions of and from this section, let , , and . Define to be the VIX implied volatility in this setting, that is the unique solution to . By identification we deduce that and similarly we define the implied variance . From the PPDE (5.3) and the relations between the derivatives that we computed in (6.3) we infer that the implied variance solves for all the PDE

where stands for the Euclidean norm in and for both we denote and .

7. Proofs of Section 4

7.1. Useful estimates

The derivation, growth and regularity estimates of the partial derivatives of hinge on recurrent estimates, summarised in Lemmas 7.1 and 7.4 below.

Lemma 7.1.

In particular,

Remark 7.3.

Proof.

Throughout the proof, constants can change from line to line.

(1) Thanks to the exponential growth of and the Gaussianity of , we have, for all ,

| (7.6) |

where . In the other case , hence the exponential growth of yields (7.1).

(2) In the case , by the polynomial growth of and Jensen’s inequality

which yields (7.2) by applying (7.1). If then

The first term is identical to the case . For the second one, we set , use the exponential decay property and exploit Jensen’s inequality with the concavity of the logarithm to obtain

| (7.7) | ||||

where is a continuous Gaussian process and thus the expectation on the last line is bounded by [39, Lemma 6.13]. This concludes the proof of (7.2).

(3) By Taylor’s theorem with integral remainder, we have

| (7.8) |

Notice that , and for all , . Hence, by Cauchy-Schwarz and Jensen’s inequalities and (7.1),

which yields (7.3).

(4) By Taylor’s theorem with integral remainder, we have

| (7.9) |

For all , Jensen’s inequality yields

where we used (7.3) to conclude. As , the polynomial growth entails for all ,

Note that . In the case , the exponential decay assumption allows to derive the following bound with the same arguments as (7.7) for any :

In virtue of this inequality and (7.2), we get . The claim (7.4) follows after an application of Cauchy-Schwarz inequality to the norm of (7.9).

(5) We consider two time points and, similarly as above, using Taylor’s theorem, Jensen and Cauchy-Schwarz inequalities,

| (7.10) |

Exploiting BDG inequality and Assumption 4.1 we have

where is a constant that changes from inequality to inequality. In the case we use that is decreasing and hence . If then since is continuously differentiable.

Lemma 7.4.

Let and assume that satisfies Assumption 4.4 (iia) if and (iib) if . Let , , and for any define . Then we have

| (7.11) |

In particular, this holds for .

7.2. Proof of Lemma 4.8

In order to prove that , we need to check that the first and second Fréchet derivatives exist and satisfy the three items of Definition 4.2. The latter are proved in Lemmas 7.5 and 7.6 for the first and second derivatives respectively.

Lemma 7.5.

Proof.

Let , and . By a mild abuse of notation we will write instead of in the remainder of this proof. Recall that, by the definition of the Fréchet derivative (4.1), we need to prove the convergence

We write

where is defined as in Lemma 7.4. We consider

| (7.13) | ||||

By Cauchy-Schwarz inequality and the bound (7.1) there is such that . Hence, Cauchy-Schwarz inequality yields

which tends to zero as goes to zero thanks to the limit (7.11) applied to . Regarding the first term of (7.13), first notice that is bounded by the growth assumption of and the bound (7.2). We have

with and . Hence Cauchy-Schwarz and Jensen’s inequalities yield

which goes to zero as goes to zero by (7.3) and proves (7.12).

(i) Let be supported on from now on. By Cauchy-Schwarz and Jensen’s inequalities, as well as estimates (7.2) and (7.1), we have

where the constants are independent of and can change from line to line. This proves (4.3) with .

Lemma 7.6.

Proof.

Let , and . By a mild abuse of notation we will write instead of in the remainder of this proof. We aim at proving a similar type of convergence as in the proof of Lemma 7.5. Let us start with the observation that

We then consider the difference of the first term with the first term of (7.14)

where we used Cauchy-Schwarz inequality, estimate (7.1) and are independent of . The analysis performed in (7.13) and below applies similarly here and proves that this quantity is . Turning to the second term we have

By Cauchy-Schwarz and Jensen’s inequalities we obtain

where the first expectation is bounded by , for some , in virtue of (7.4). Applying Cauchy-Schwarz inequality twice yields

which uniform bound over goes to zero as goes to zero, by (7.1). Thus . Before tackling , we notice that

Applying Cauchy-Schwarz and Jensen’s inequalities again yield

where the first term is bounded thanks to (7.2) and

and this goes to zero, uniformly in , by (7.4). This proves the convergence of the second term and hence concludes the first part of the proof.

(i) Let be supported on for some . Then Hölder’s and Jensen’s inequalities combined with Estimates (7.1) and (7.2) show

| (7.15) | ||||

for some independent of . Similarly,

for some independent of , where we used again (7.1) and (7.2) to conclude. This proves that (4.4) is satisfied with .

(ii) We look at the regularity of (7.14) with and start with the first term. We split it in three and apply Hölder’s inequality:

where we concluded using Jensen’s inequality in the same way as in (7.15) as well as all the estimates of Lemma 7.1. Similarly, for the second term we apply Cauchy-Schwarz inequality

where we again used Lemma 7.1 to conclude. This proves that satisfies (4.6) with and .

7.3. Proof of Proposition 4.10

We remind the reader that derivatives in the singular direction of are defined in (4.7) as the limits of the derivatives with the truncated kernel . Let and .

We name the right-hand side of (4.12). By linearity of the Fréchet derivative, Cauchy-Schwarz and Jensen’s inequalities, we have

Estimates (7.2) and (7.1) ensure that the expectations are uniformly bounded. Moreover, we note that and are different only on hence we have

| (7.16) |

and, with , Assumption 4.1 yields

| (7.17) | ||||

where the constant depends on and may change from line to line. Therefore, coming back to (7.16), we obtain

which tends to zero as goes to zero.

We call the right-hand side of (4.13). Once more by linearity of the Fréchet derivative, we have

Let and note that , which allows us to use Hölder’s inequality as

Using Jensen’s inequality, estimates (7.2) and (7.1) yield

On the one hand, Assumption 4.1 entails

where we used . On the other hand, reasoning as in (7.17) we get

which tends to zero with . The same computations show that also goes to zero because is also bounded.

For the third term, we apply Hölder’s inequality followed by Jensen’s and Cauchy-Schwarz:

The expectations are again bounded thanks to (7.2) and (7.1). For the integral we will use that and . Once again we leverage on Assumption 4.1 and (7.16) to obtain

where the constant may change from line to line. This proves that tends to zero as does and, since converges with the same arguments, this concludes the proof. ∎

References

- [1] E. Abi Jaber and O. El Euch, Multifactor approximation of rough volatility models, SIAM Journal on Financial Mathematics, 10 (2019), pp. 309–349.

- [2] E. Abi Jaber, C. Illand, and S. Li, Joint spx-vix calibration with gaussian polynomial volatility models: deep pricing with quantization hints, arXiv preprint arXiv:2212.08297, (2022).

- [3] A. Alfonsi and A. Kebaier, Approximation of stochastic Volterra equations with kernels of completely monotone type, Mathematics of Computation, (2023).

- [4] E. Alos, D. García-Lorite, and A. Muguruza, On smile properties of volatility derivatives and exotic products: understanding the VIX skew, SIAM Journal on Financial Mathematics, 13 (2022), pp. 32–69.

- [5] A. Barletta, E. Nicolato, and S. Pagliarani, The short-time behavior of VIX-implied volatilities in a multifactor stochastic volatility framework, Mathematical Finance, 29 (2019), pp. 928–966.

- [6] C. Bayer and S. Breneis, Markovian approximations of stochastic Volterra equations with the fractional kernel, Quantitative Finance, 23 (2023), pp. 53–70.

- [7] C. Bayer, P. Friz, and J. Gatheral, Pricing under rough volatility, Quantitative Finance, 16 (2016), pp. 887–904.

- [8] C. Bayer, F. A. Harang, and P. Pigato, Log-modulated rough stochastic volatility models, SIAM Journal on Financial Mathematics, 12 (2021), pp. 1257–1284.

- [9] M. Bennedsen, A. Lunde, and M. S. Pakkanen, Hybrid scheme for Brownian semistationary processes, Finance and Stochastics, 21 (2017), pp. 931–965.

- [10] , Decoupling the short-and long-term behavior of stochastic volatility, Journal of Financial Econometrics, 20 (2022), pp. 961–1006.

- [11] H. Berestycki, J. Busca, and I. Florent, Computing the implied volatility in stochastic volatility models, Communications on Pure and Applied Mathematics: A Journal Issued by the Courant Institute of Mathematical Sciences, 57 (2004), pp. 1352–1373.

- [12] L. Bergomi, Smile dynamics II, Risk, (2005).

- [13] , Smile dynamics III, Risk, (2008).

- [14] A. E. Bolko, K. Christensen, M. S. Pakkanen, and B. Veliyev, A GMM approach to estimate the roughness of stochastic volatility, Journal of Econometrics, (2022).

- [15] O. Bonesini, G. Callegaro, and A. Jacquier, Functional quantization of rough volatility and applications to the VIX, arXiv preprint arXiv:2104.04233, (2021).

- [16] O. Bonesini, A. Jacquier, and A. Pannier, Rough volatility, path-dependent PDEs and weak rates of convergence, arXiv preprint arXiv:2304.03042, (2023).

- [17] F. Bourgey and S. De Marco, Multilevel Monte Carlo simulation for VIX options in the rough Bergomi model, arXiv preprint arXiv:2105.05356, (2021).

- [18] F. Bourgey, S. De Marco, and E. Gobet, Weak approximations and VIX option price expansions in forward variance curve models, Quantitative Finance, 23 (2023), pp. 1259–1283.

- [19] H. Buehler, Consistent variance curve models, Finance and Stochastics, 10 (2006), pp. 178–203.

- [20] C. Chong, M. Hoffmann, Y. Liu, M. Rosenbaum, and G. Szymanski, Statistical inference for rough volatility: Central limit theorems, arXiv preprint arXiv:2210.01216, (2022).

- [21] , Statistical inference for rough volatility: Minimax theory, arXiv preprint arXiv:2210.01214, (2022).

- [22] C. Cuchiero, G. Gazzani, J. Möller, and S. Svaluto-Ferro, Joint calibration to SPX and VIX options with signature-based models, arXiv preprint arXiv:2301.13235, (2023).

- [23] J. Delemotte, S. D. Marco, and F. Segonne, Yet another analysis of the SP500 at-the-money skew: Crossover of different power-law behaviours, Available at SSRN 4428407, (2023).

- [24] B. Dupire, Functional Itô calculus, Quantitative Finance, 19 (2019), pp. 721–729.

- [25] M. Forde, S. Gerhold, and B. Smith, Small-time VIX smile and the stationary distribution for the rough Heston model, 2021.

- [26] J.-P. Fouque and Y. F. Saporito, Heston stochastic vol-of-vol model for joint calibration of VIX and S&P 500 options, Quantitative Finance, 18 (2018), pp. 1003–1016.

- [27] M. Fukasawa, B. Horvath, and P. Tankov, Hedging under rough volatility, arXiv preprint arXiv:2105.04073, (2021).

- [28] M. Fukasawa, T. Takabatake, and R. Westphal, Consistent estimation for fractional stochastic volatility model under high-frequency asymptotics, Mathematical Finance, 32 (2022), pp. 1086–1132.

- [29] J. Gatheral, Consistent modeling of SPX and VIX options, in Bachelier congress, vol. 37, 2008, pp. 39–51.

- [30] J. Gatheral, T. Jaisson, and M. Rosenbaum, Volatility is rough, Quantitative finance, 18 (2018), pp. 933–949.

- [31] J. Gatheral, P. Jusselin, and M. Rosenbaum, The quadratic rough Heston model and the joint S&P 500/VIX smile calibration problem, arXiv preprint arXiv:2001.01789, (2020).

- [32] A. Gulisashvili, Time-inhomogeneous Gaussian stochastic volatility models: Large deviations and super roughness, Stochastic Processes and their Applications, 139 (2021), pp. 37–79.

- [33] J. Guyon and M. El Amrani, Does the term-structure of equity at-the-money skew really follow a power law?, Available at SSRN 4174538, (2022).

- [34] J. Guyon and J. Lekeufack, Volatility is (mostly) path-dependent, Quantitative Finance, 23 (2023), pp. 1221–1258.

- [35] X. Han and A. Schied, Estimating the roughness exponent of stochastic volatility from discrete observations of the realized variance, arXiv preprint arXiv:2307.02582, (2023).

- [36] B. Horvath, A. Jacquier, and A. Muguruza, Functional central limit theorems for rough volatility, arXiv preprint arXiv:1711.03078, (2017).

- [37] B. Horvath, A. Jacquier, and P. Tankov, Volatility options in rough volatility models, SIAM Journal on Financial Mathematics, 11 (2020), pp. 437–469.

- [38] A. Jacquier, C. Martini, and A. Muguruza, On VIX futures in the rough Bergomi model, Quantitative Finance, 18 (2018), pp. 45–61.

- [39] A. Jacquier, A. Muguruza, and A. Pannier, Rough multifactor volatility for SPX and VIX options, arXiv preprint arXiv:2112.14310. Forthcoming in Advances in Applied Probability, (2021).

- [40] A. Jacquier and M. Oumgari, Deep curve-dependent PDEs for affine rough volatility, SIAM Journal on Financial Mathematics, 14 (2023), pp. 353–382.

- [41] C. Lacombe, A. Muguruza, and H. Stone, Asymptotics for volatility derivatives in multi-factor rough volatility models, Mathematics and Financial Economics, 15 (2021), pp. 545–577.

- [42] Y.-N. Lin and C.-H. Chang, VIX option pricing, Journal of Futures Markets: Futures, Options, and Other Derivative Products, 29 (2009), pp. 523–543.

- [43] B. B. Mandelbrot and J. W. Van Ness, Fractional Brownian motions, fractional noises and applications, SIAM review, 10 (1968), pp. 422–437.

- [44] R. McCrickerd and M. S. Pakkanen, Turbocharging Monte Carlo pricing for the rough Bergomi model, Quantitative Finance, 18 (2018), pp. 1877–1886.

- [45] D. Nualart, The Malliavin calculus and related topics, vol. 1995, Springer, 2006.

- [46] A. Pannier and C. Salvi, Learning path-dependent PDEs with signature kernels, In preparation.

- [47] A. Papanicolaou and R. Sircar, A regime-switching Heston model for VIX and S&P 500 implied volatilities, Quantitative Finance, 14 (2014), pp. 1811–1827.

- [48] S. Peng and F. Wang, BSDE, path-dependent PDE and nonlinear Feynman-Kac formula, Science China Mathematics, 59 (2016), pp. 19–36.

- [49] S. E. Rømer, Empirical analysis of rough and classical stochastic volatility models to the SPX and VIX markets, Quantitative Finance, 22 (2022), pp. 1805–1838.

- [50] M. Rosenbaum and J. Zhang, Deep calibration of the quadratic rough Heston model, arXiv preprint arXiv:2107.01611, (2021).

- [51] M. Sabate-Vidales, D. Šiška, and L. Szpruch, Solving path dependent PDEs with LSTM networks and path signatures, arXiv preprint arXiv:2011.10630, (2020).

- [52] C. Salvi, T. Cass, J. Foster, T. Lyons, and W. Yang, The signature kernel is the solution of a Goursat PDE, SIAM Journal on Mathematics of Data Science, 3 (2021), pp. 873–899.

- [53] Y. F. Saporito and Z. Zhang, Path-dependent deep Galerkin method: A neural network approach to solve path-dependent partial differential equations, SIAM Journal on Financial Mathematics, 12 (2021), pp. 912–940.

- [54] F. Viens and J. Zhang, A martingale approach for fractional Brownian motions and related path-dependent PDEs, The Annals of Applied Probability, 29 (2019), pp. 3489–3540.

- [55] H. Wang, J. Yong, and J. Zhang, Path dependent Feynman–Kac formula for forward backward stochastic Volterra integral equations, Annales de l’Institut Henri Poincaré: Probabilités et Statistiques, 58 (2022), pp. 603–638.

- [56] P. Wu, J.-F. Muzy, and E. Bacry, From rough to multifractal volatility: The log s-fbm model, Physica A: Statistical Mechanics and its Applications, 604 (2022), p. 127919.