Regularized Linear Regression for Binary Classification

Abstract

Regularized linear regression is a promising approach for binary classification problems in which the training set has noisy labels since the regularization term can help to avoid interpolating the mislabeled data points. In this paper we provide a systematic study of the effects of the regularization strength on the performance of linear classifiers that are trained to solve binary classification problems by minimizing a regularized least-squares objective. We consider the over-parametrized regime and assume that the classes are generated from a Gaussian Mixture Model (GMM) where a fraction of the training data is mislabeled. Under these assumptions, we rigorously analyze the classification errors resulting from the application of ridge, , and regression. In particular, we demonstrate that ridge regression invariably improves the classification error. We prove that regularization induces sparsity and observe that in many cases one can sparsify the solution by up to two orders of magnitude without any considerable loss of performance, even though the GMM has no underlying sparsity structure. For regularization we show that, for large enough regularization strength, the optimal weights concentrate around two values of opposite sign. We observe that in many cases the corresponding "compression" of each weight to a single bit leads to very little loss in performance. These latter observations can have significant practical ramifications.

1 INTRODUCTION

As the usage of machine learning models becomes more prevalent, the need for efficiently storing these models and for guaranteeing their performance in the face of noisy training data becomes increasingly vital. With the advent of LLMs, which are comprised of many billions of weights, the necessity for reliable compression schemes becomes ever more critical. Thus, the question is raised, are there methods that allow us to compress the weights of a deep neural net without compromising a lot on the performance? In this paper, we would like to take baby steps towards addressing this question via the analysis of the toy problem of regularized linear regression for binary classification. Regularization can be used to avoid fitting corrupted data, thereby improving performance, as well as to favor solutions with desired properties, such as sparsity or compressibility. Through theory, intuitive arguments, and numerical simulations, we demonstrate that regularization can help the generalization performance on noise-corrupted data sets, as well as reduce the number of model parameters by orders of magnitude without significant loss in performance.

2 RELATED WORKS AND OUR CONTRIBUTION

There has been a recent surge of results in binary classification that provide a sharp analysis of a variety of methods tailored to different models (see, e.g., Thrampoulidis et al., (2018, 2020); Huang, (2017); Candès and Sur, (2018); Sur and Candès, (2019); Kammoun and Alouini, (2020); Salehi et al., (2019); Taheri et al., (2020); Deng et al., (2019); Montanari et al., 2019a ; Mignacco et al., 2020b ; Lolas, (2020) and the references therein). These works typically pose the over-parameterized binary classification problem as an optimization problem and employ either the Convex Gaussian Min-max Theorem (CGMT) Thrampoulidis et al., 2015b ; Thrampoulidis et al., (2018); Stojnic, (2013); Gordon, (1985); Loureiro et al., (2021) or the Approximate Message Passing (AMP) (see, e.g, Donoho et al., (2009); Bayati and Montanari, (2011); Javanmard and Montanari, (2013)) approach to obtain formulas for the generalization error that involve solutions to a system of non-linear equations (in a small number of variables) that often do not admit closed-form expressions. These results follow a long line of work that deals with obtaining sharp high-dimensional asymptotics for convex optimization-based estimators. Most of the papers referred to above use some form of linear, logistic, or max-margin optimization. Most relevant to the scope of the present work are those that study binary classification through the lens of regularized linear regression which we highlight below.

Loureiro et al., (2021) explores both binary and multi-class classification using an arbitrary convex loss and quadratic regularizer. Since our focus is on the effects of regularization, such as sparsification and compression, we instead study quadratic loss and arbitrary regularizer. They demonstrate how to reduce the analysis of the generalization error to finding fixed points of a low-dimensional system of equations using AMP. We should remark that we currently do not know how to use the CGMT framework to analyze the multi-class setting, a topic that is worthy of investigation in its own right—see e.g., Thrampoulidis et al., (2020) for an attempt in this direction.

Mignacco et al., 2020a uses Gaussian comparison inequalities to analyze the binary classification error for arbitrary loss functions with regularization. The main differences between our works are:

The loss considered in Mignacco et al., 2020a is of the form , whereas ours is , as we aim to study performance of the regression-based approaches to classification.

We introduce corruption to the labels and analyze how it affects the generalization error. This seems more natural to do because one of the main reasons for explicit regularization is finding solutions that do not interpolate the data.

We consider arbitrary separable convex regularizers and, in particular, show that regularization allows one to find sparse classifiers and regularization can lead to -bit compression of the solution. For simplicity, we have focused on quadratic loss so that we could highlight the effect of the regularizer.

In the case of regularization we reduce the number of scalar parameters to find the generalization error from six in Mignacco et al., 2020a to two. Furthermore, in the regime of strong regularization, i.e., , we find a closed form expression for the generalization error and use it to conclude that an arbitrary corruption rate can be annihilated with large enough regularization strength.

Other works have studied corruption in the labels. Most notably Chatterji and Long, (2021) analyzes the performance of the max-margin algorithm for binary classification of linearly separable data in the presence of corruption in the labels.

3 PRELIMINARIES

3.1 Gaussian Mixture Model

We consider a binary classification problem with two classes, where for class the feature vector is drawn at random from , with the mean and the covariance matrix, and where the label is chosen as for and for . How well a linear classifier performs depends on how "close" the mean vectors and are and what the structure of the covariance matrices is. In the sequel, we will largely assume that the covariances are isotropic (). For the means, we will assume that their matching components are drawn iid from zero mean standard normal distributions with cross-correlation . The cross-correlation allows one to control the distance between the cluster centers. For example, this means that for large , and .

For simplicity of exposition, we treat only the case of equal class sizes in this paper, but it is straightforward to apply the same techniques to the case of unbalanced classes. What we mean by equal classes is that the number of training data points for each class is (for a total of training points) and that the probability of drawing an element from each class, in order to determine the generalization error, is . In all our subsequent analysis we will assume that we are in the over-parametrized regime, i.e., (often . Finally, we will assume that a fraction of the training dataset is mislabeled.

We will consider a linear classifier given by a weight vector . In other words for a given feature vector , we will declare that belongs to class 1 if and to class 2 if . It is then straightforward to show the following result.

Lemma 1.

Given a weight vector , and assuming the feature vectors are equally likely to be drawn from class 1 or class 2, the corresponding generalization error for the Gaussian mixture model with means and and covariance matrices is given by

| (1) |

where is the integral of the tail of the standard normal distribution.

The goal of this paper is to compute and characterize the generalization error of linear regression using different regularizers for the linear binary classifier with Gaussian mixture model. As can be seen from Lemma 1, this requires us to characterize the four quantities

In fact, in much of the subsequent analysis, we shall assume , which implies we need to characterize only the following three quantities

| (2) |

Since the data model that we are considering is a Gaussian mixture, we shall make use of the Convex Gaussian Min-Max Theorem (CGMT) (Thrampoulidis et al., 2015b ), which is a tight and extended version of a classical Gaussian comparison inequality (Gordon, (1985)).

3.2 Convex Gaussian Min-Max Theorem

The CGMT framework has been developed to analyze the properties of the solutions to non-smooth regularized convex optimization problems and has been successfully applied to characterize the precise performance in numerous applications such as -estimators, generalized lasso, massive MIMO, phase retrieval, regularized logistic regression, adversarial training, max-margin classifiers, distributionally robust regression, and others (see Stojnic, (2013); Thrampoulidis et al., (2018); Salehi et al., (2019); Thrampoulidis et al., 2015a ; Abbasi et al., (2019); Salehi et al., (2018); Miolane and Montanari, (2021); Taheri et al., (2021); Aubin et al., (2020); Javanmard and Soltanolkotabi, (2022); Montanari et al., 2019b ; Salehi et al., (2020); Aolaritei et al., (2023). In this framework, a given so-called primary optimization (PO) problem, is associated with a simplified auxiliary optimization (AO) problem from which properties of the optimal solution can be tightly inferred. Specifically, the (PO) and (AO) problems are defined as follows:

| (PO) | ||||

| (AO) |

where and . Denoting any optimal minimizers of (PO) and (AO) as and , respectively, CGMT states:

Theorem 1 (CGMT Thrampoulidis et al., (2018)).

Let , be convex compact sets, be continuous and convex-concave on , and, and all have entries iid standard normal. Let be an arbitrary open subset of and . Denote by and the optimal costs of (PO) and (AO) respectively when is minimized over . If there exist constants such that , and , (converge in probability), then .

Let be a convex function. For and the Moreau envelope of function (Moreau, (1965)) is defined as

We call a convex separable, when for convex .

3.3 Optimal solutions with oracle access to

We need to introduce the following two definitions before proceeding further:

Definition 1.

We say that is -sparse if it has at most non-zero entries

Definition 2.

We say that is a -bit vector if each of its entries is equal to , for some

In the over-parametrized regime, since , it is not possible to reliably estimate the means and (this is further confounded when the labels have errors). Nonetheless, it is useful to see what the optimal linear classifiers would look like when one has oracle access to the means. We will do this for the general case, as well as for the -sparse and -bit classifiers.

Lemma 2.

1. The overall optimal classifier is , which has performance

2. The optimal -bit classifier is , which has performance

3. The optimal -sparse classifier is obtained from taking the coordinates of with the largest magnitude and zeroing out the rest

3.4 Regularized linear regression in the presence of corruption in labels

It is natural to use regularized linear regression for classification when not all labels are reliable. As mentioned earlier, stands for the corruption rate, meaning that labels within each class are corrupt. Let be an arbitrary convex regularizer and be the regularization strength. The present paper is concerned with analyzing the case of the linear regression applied to GMM (cf. 3.1) with means and and covariance . After reordering the training data so that the first columns of the data matrix correspond to the points from the first class, our analysis reduces to the following optimization problem:

| (3) |

Where the entries of are i.i.d. , encodes the means corresponding to each class, encodes the training labels.

3.5 Approach and intuition behind it

As mentioned earlier, we are interested in computing the inner products and the norm (2). We focus on the over-parametrized high-dimensional regime where is fixed and . In this regime, we show that the quantities in (2) concentrate and we determine their asymptotic values. Moreover, in the cases of and regularization, we do the same for the sparsity and compression rates, respectively.

To do so, we will employ the CGMT framework. This starts by using the Fenchel dual of the quadratic loss to rewrite (3) in the following min-max form:

Applying CGMT and explicitly performing the maximization over in the (AO), we obtain:

| (4) |

where we have used the following notation

It is insightful to examine each term in (4) as it provides some explanation of the phenomenona observed in the simulations.

The sum of the second and the third terms encourages the minimizer to align with . As seen earlier, the oracle-based optimal is . Thus, it is these two terms that encourage to approach the oracle-based optimal. Note that the extra term has of the variance of and represents the effects of the variance in the training data from the GMM. The second and third terms represent fitting the correctly labeled data.

The fourth term encourages to align with the arbitrary Gaussian vector . This represents the minimizer’s attempt to interpolate the corrupted labels, as it vanishes when .

The first term makes partly align with a random direction and is independent of . It represents the fact that the problem is over-parametrized.

The last term is the regularization term.

Ideally, we would like the minimizer to minimize the second and third terms and to ignore the first and fourth ones. We now provide some intuition as to why the regularization term helps with this. Due to the equivalence of norms, our argument applies to any norm , and so, for simplicity, we shall focus on and .

Due to the existence of the regularizer, the minimizer would like to minimize the terms in (4) with as small a as possible. This is much easier to do for the second and third terms, since the squared norm of the vectors and is , than it is for the fourth term where the squared norm of the vector is . Thus, the minimizer will reduce the second and third terms at the expense of the fourth one. In other words, the regularization term encourages the regressor to interpolate the correctly labeled data, at the expense of the corrupted labels, which improves performance and is what we hoped it would do. In fact, the larger is, the stronger the incentive to ignore the mislabeled data.

4 MAIN RESULTS

In this section we provide rigorous results along some remarks which will help to gain more insights on the general problem.

4.1 Precise results

The reader can find a theorem describing the generalization error for an arbitrary convex regularizer below.

Theorem 2 (Master theorem).

The generalization error resulting from the application of the linear regression with a separable convex regularizer , with ’s being identical and regularization strength to the Gaussian mixture model with means and covariance is equal to

for and defined by the scalar optimization

where the expectation is taken over and

Next, we proceed to provide some specialized results for prominent regularizers. In the case of , it turns out that from Theorem 2 takes form of for some (see Appendix). This allows for an easier way of characterising the desired generalization error than the one suggested by Theorem 2.

Theorem 3 ( regularization).

The generalization error resulting from the application of the ridge regression with regularization strength to the Gaussian mixture model with means and covariance is equal to

where are defined by the following two-dimensional convex optimization problem:

with

For regularization, one can find the sparsity rate in addition to analyzing performance.

Theorem 4 ( regularization).

The generalization error resulting from the application of the regularized regression with regularization strength to the Gaussian mixture model with means and covariance is equal to

for and defined by the optimization:

where

Furthermore, the corresponding solution is -sparse

Finally, in the case of we were also able to calculate the compression rate.

Theorem 5 ( regularization).

The generalization error resulting from the application of the regularized regression with regularization strength to the Gaussian mixture model with means and covariance is

for and defined by the optimization:

where

Moreover, of the weights are equal to , of the weights are equal to , and all others weights lie in between, where

4.2 Explicit approximations for large

While the theorems above accurately describe the generalization errors, they are not as explicit as one might wish. To overcome this, we show for large enough, the first term of (4) is negligible compared to . This suggests dropping that term completely from the (AO). Leaving the technical details for the Appendix, we summarize the implications of this approximation in the remarks below. In Section 6 we will observe that these approximations do work well when is large.

Remark 1.

The following approximation for the generalization error takes place in the case of the ridge regression if :

Remark 2.

Assume that . Then the following approximation can be made:

Note that the -function applied to the argument above is a negligibly small number for big enough . Thus, informally, this remark can be stated as follows: if the problem is high-dimensional and is small enough, the negative effects of any corruption rate can be completely eliminated via ridge regression with a sufficiently large regularization strength.

Remark 3.

Dropping the first term of (4) in the case of the -regularized regression and assuming that is large enough, one can show that unless is close to , where is defined via

Moreover, it turns out that the optimal scalars , , and are such that holds with high probability. This suggests that regularization tries to kill all the components of apart from the ones corresponding to the top entries of where the latter can be regarded as an approximation to . This is similar to the description of the optimal sparse classifier from Lemma 2. Thus, for large enough , the regularizer tries to find as sparse a solution as possible that aligns itself with the top entries of .

Remark 4.

Assuming that is large enough, the following approximation can be made for the found from the -regularized regression:

Where and are defined by the optimization:

for

Since all entries of have the same magnitude and since (1) is unaffected by a scaling of , this implies that we can replace by without any loss of performance. Thus each component of the optimal can be encoded by a single bit.

5 A COMPRESSION SCHEME

As discussed in Remark 4, -regularization with large can be used for -bit compression via . One might wonder whether using the same compression scheme for an arbitrary -regularized solution would still retain good performance. Turns out that this scheme does succeed for and in the small noise () and large regime. For , this is discussed in Remark 3. For , as discussed in Section 3.5, the corresponding strives to align with . This makes approximate which, according to Lemma 2, is the optimal -bit classifier.

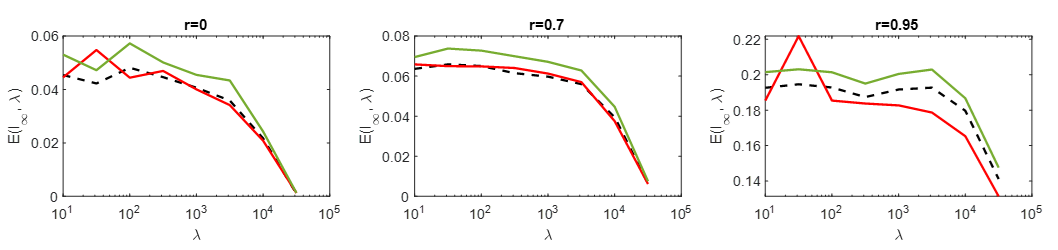

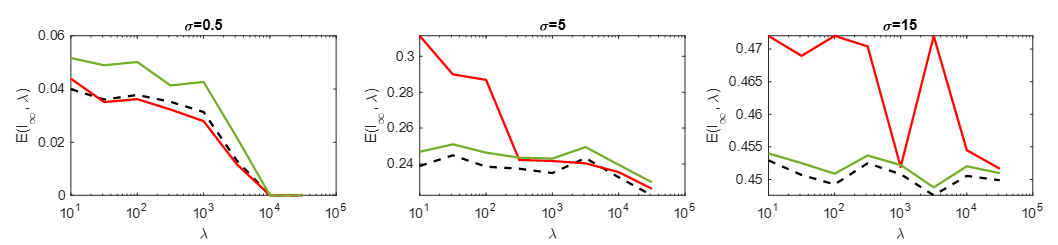

6 NUMERICAL RESULTS

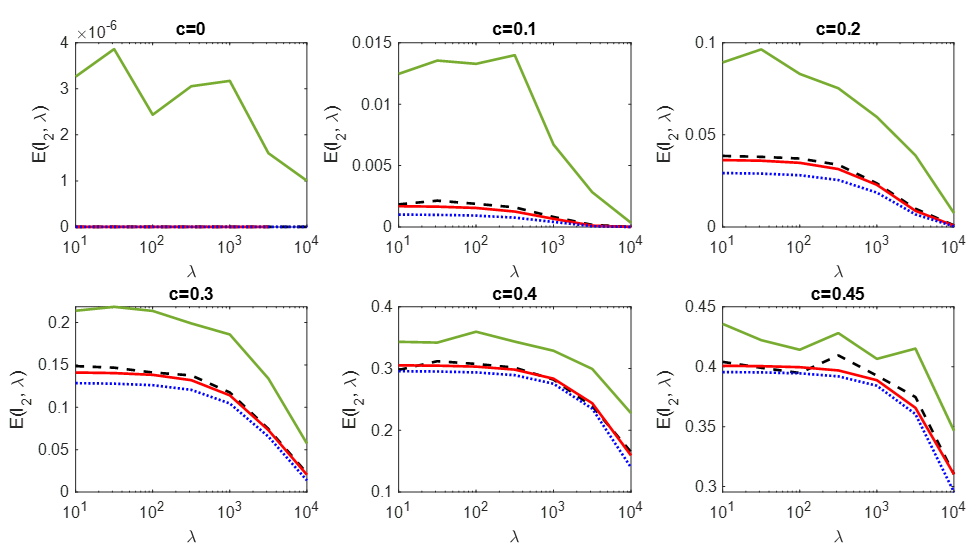

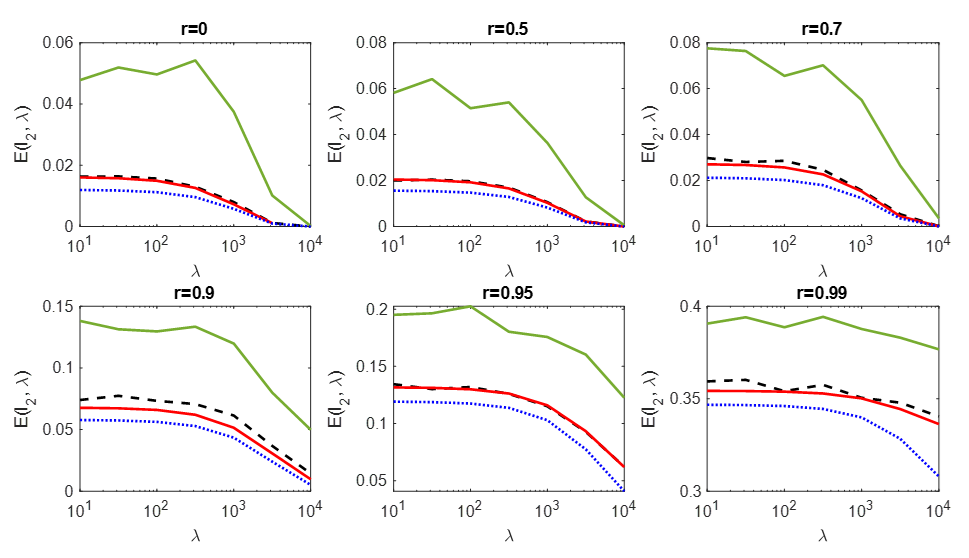

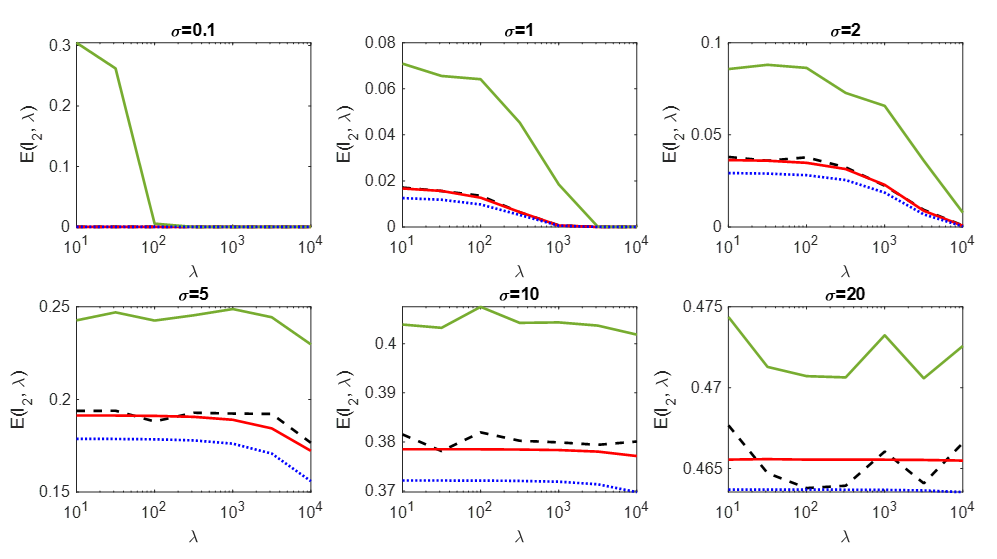

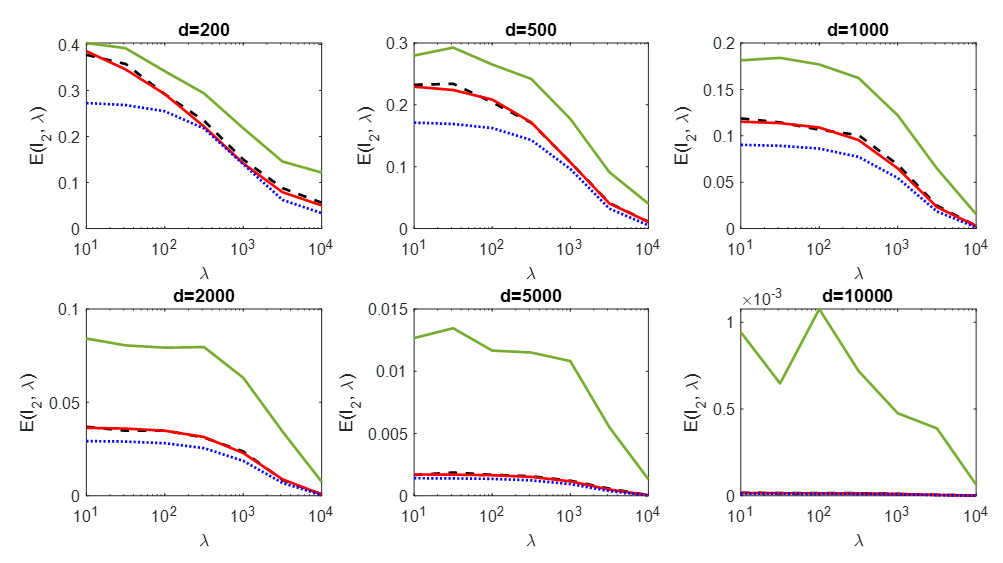

To showcase our results, we performed extensive simulations using synthetic data produced according to the assumptions described in the previous sections. We generated points equiprobably from two distributions and , where the corresponding components of the were iid standard normal with cross-correlation , and with labels and respectively, a fraction of those which were subsequently corrupted. Making use of the MATLAB™ CVX package (Grant and Boyd, (2008, 2014)), we trained classifiers that minimize the , and regression objectives for this data. We simulated the generalization error of these classifiers, and compared it to the expressions obtained in theorems 3, 4, and 5 (cf. Fig.1, Fig.2, Fig.3). Moreover, we have also plotted the predicted sparsity and compression rate for the and cases. In the following figures, we took the nominal values as a starting point. Then, to analyze the effects of these parameters independently, we vary exactly one parameter per experiment while keeping the others fixed. In the subsections below, we go over the plots and interpret their results.

6.1 Ridge regression

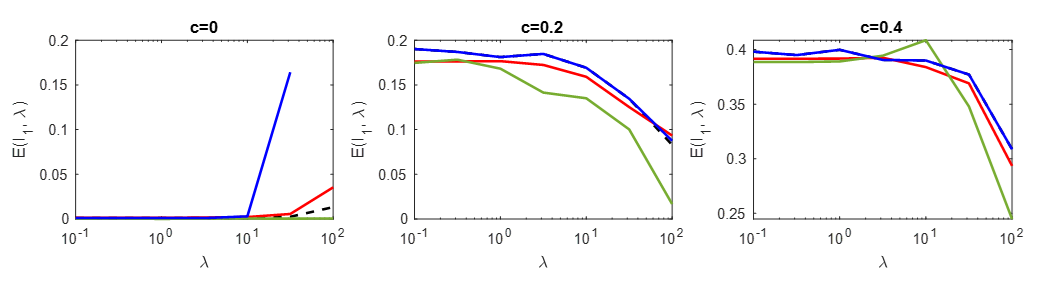

For the ridge regression, we examined the effects of on the generalization error in Fig. 1. As expected, the generalization error improves as the regularization strength increases. The , simulated directly by solving ridge regression, and the prediction for it derived from Theorem 3 match very closely. Moreover, the closed-form approximation formulated in Section 4.2 follows the true closely for large values of . In addition, it appears to be a lower bound for the generalization error for all , though we leave proving this to future work. Finally, in light of Section 5, we also considered the sign of the solution as a possible classifier. It turns out one does not lose much in performance by compressing each weight to a single bit. Furthermore, it is evident that increasing either of increases the classification error and, on the opposite, increasing , decreases it.

6.2 regularization

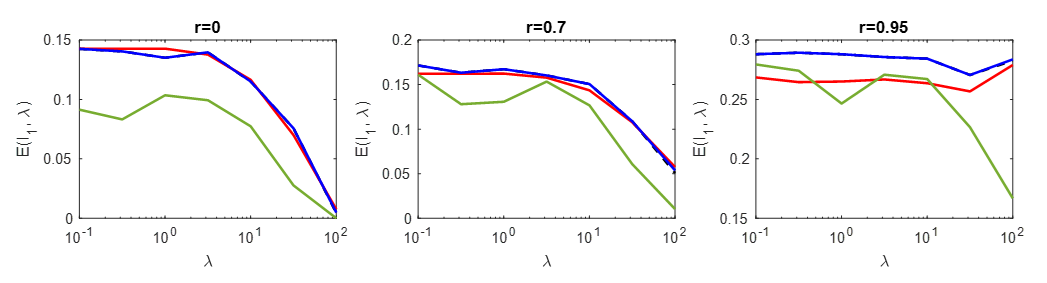

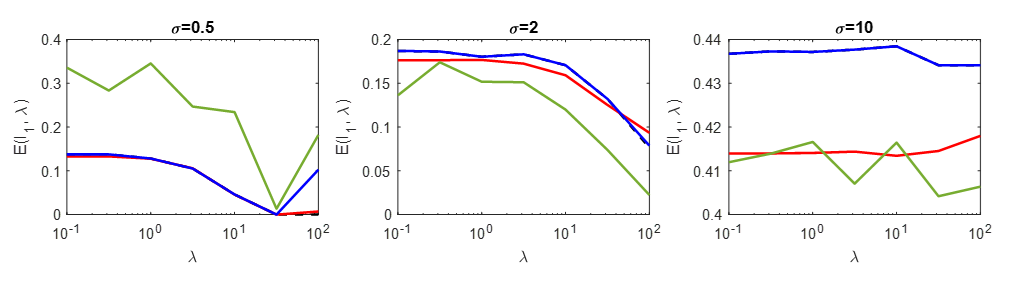

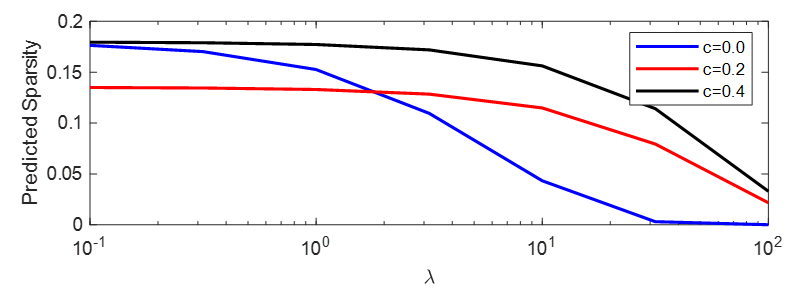

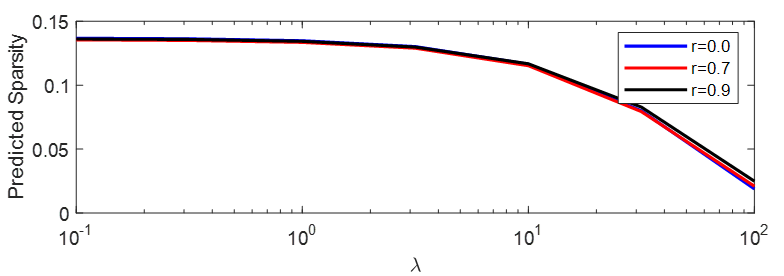

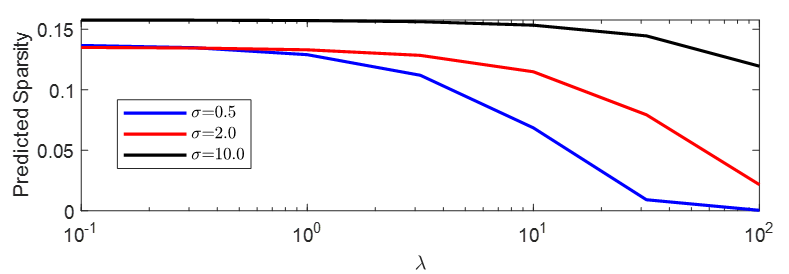

Similar to the previous section, in Fig. 2 we compared the simulated error to the error predicted by Theorem 4 and observed a close match. The solution has many entries that are very close to zero, but are not exactly equal to it because of small-scale numerical inaccuracies, and so we sparsified this solution according to the rate suggested by Theorem 4. We observed that this does affect the performance. Finally, we also compress the solution down to bit. The effects of changing on the generalization error are similar to what was observed in the ridge regression case. Interestingly, changing these parameters has different impacts on the theoretical prediction for the sparsity rate. Fig. 4 proposes the sparsity rate does not change much with , whereas increasing leads to difficulty in sparsifying. Also note that we obtain sparsity rates close to zero as we increase . Pairing the observations from Figs. 2 and 4, we see that one can attain a good generalization error with an extremely sparse estimator. For instance, when , we get an -sparse estimator (in an ambient dimension of 2000) with a generalization error of as little as . This is despite the fact that the underlying GMM model had no inherent sparsity structure.

6.3 regularization

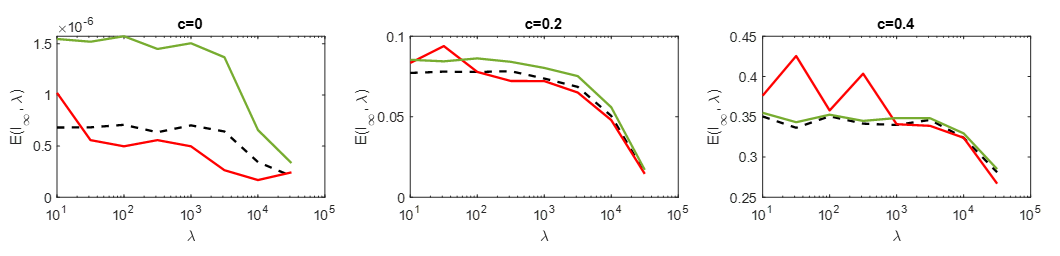

Repeating the same procedure as before, we verified that the predicted error matches the simulated error, as can be seen in Fig. 3. Moreover, we checked the same for the compression rate (cf. Fig. 5). It is noteworthy that the -bit estimator follows the simulated error closely. Analyzing the compression rate, it is evident that no matter how corrupt the labels are (larger ), one can still take the one-bit estimator and not lose out much on performance. The same could also be said about the angle between the means represented by .

7 CONCLUSION

In this work we considered the problem of binary classification with corrupt labels through the lens of regularized linear regression. We used CGMT to derive sharp results for the generalization error for a general convex separable regularizer . Both theoretically, and through simulations, we showed that regularization helps the generalization performance. We calculated the sparsity rate for the case and the compression rate for the case and validated the theoretical findings numerically. These evaluations suggest that good sparse classifiers and good one-bit classifiers often exist, even when the underlying GMM has no inherent sparsity structure, and even in the presence of high rates of label corruption. Possible future directions include extending this work to the case of multi-class classification and to other regularizers and loss functions.

References

- Abbasi et al., (2019) Abbasi, E., Salehi, F., and Hassibi, B. (2019). Performance analysis of convex data detection in mimo. In ICASSP 2019-2019 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 4554–4558. IEEE.

- Aolaritei et al., (2023) Aolaritei, L., Shafieezadeh-Abadeh, S., and Dörfler, F. (2023). The performance of wasserstein distributionally robust m-estimators in high dimensions. arXiv:2206.13269.

- Aubin et al., (2020) Aubin, B., Krzakala, F., Lu, Y., and Zdeborová, L. (2020). Generalization error in high-dimensional perceptrons: Approaching bayes error with convex optimization. Advances in Neural Information Processing Systems, 33:12199–12210.

- Bayati and Montanari, (2011) Bayati, M. and Montanari, A. (2011). The dynamics of message passing on dense graphs, with applications to compressed sensing. IEEE Transactions on Information Theory, 57(2):764–785.

- Candès and Sur, (2018) Candès, E. J. and Sur, P. (2018). The phase transition for the existence of the maximum likelihood estimate in high-dimensional logistic regression. arXiv preprint arXiv:1804.09753.

- Chatterji and Long, (2021) Chatterji, N. S. and Long, P. M. (2021). Finite-sample analysis of interpolating linear classifiers in the overparameterized regime. The Journal of Machine Learning Research, 22(1):5721–5750.

- Deng et al., (2019) Deng, Z., Kammoun, A., and Thrampoulidis, C. (2019). A model of double descent for high-dimensional binary linear classification. arXiv preprint arXiv:1911.05822.

- Donoho et al., (2009) Donoho, D. L., Maleki, A., and Montanari, A. (2009). Message-passing algorithms for compressed sensing. Proceedings of the National Academy of Sciences, 106(45):18914–18919.

- Gordon, (1985) Gordon, Y. (1985). Some inequalities for gaussian processes and applications. Israel Journal of Mathematics, 50:265–289.

- Grant and Boyd, (2008) Grant, M. and Boyd, S. (2008). Graph implementations for nonsmooth convex programs. In Blondel, V., Boyd, S., and Kimura, H., editors, Recent Advances in Learning and Control, Lecture Notes in Control and Information Sciences, pages 95–110. Springer-Verlag Limited.

- Grant and Boyd, (2014) Grant, M. and Boyd, S. (2014). CVX: Matlab software for disciplined convex programming, version 2.1.

- Huang, (2017) Huang, H. (2017). Asymptotic behavior of support vector machine for spiked population model. Journal of Machine Learning Research, 18(1):1472–1492.

- Javanmard and Montanari, (2013) Javanmard, A. and Montanari, A. (2013). State evolution for general approximate message passing algorithms, with applications to spatial coupling. Information and Inference: A Journal of the IMA, 2(2):115–144.

- Javanmard and Soltanolkotabi, (2022) Javanmard, A. and Soltanolkotabi, M. (2022). Precise statistical analysis of classification accuracies for adversarial training. The Annals of Statistics, 50(4):2127–2156.

- Kammoun and Alouini, (2020) Kammoun, A. and Alouini, M.-S. (2020). On the precise error analysis of support vector machines. arXiv preprint arXiv:2003.12972.

- Lolas, (2020) Lolas, P. (2020). Regularization in high-dimensional regression and classification via random matrix theory. arXiv preprint arXiv:2003.13723.

- Loureiro et al., (2021) Loureiro, B., Sicuro, G., Gerbelot, C., Pacco, A., Krzakala, F., and Zdeborová, L. (2021). Learning gaussian mixtures with generalized linear models: Precise asymptotics in high-dimensions. Advances in Neural Information Processing Systems, 34:10144–10157.

- (18) Mignacco, F., Krzakala, F., Lu, Y., Urbani, P., and Zdeborova, L. (2020a). The role of regularization in classification of high-dimensional noisy Gaussian mixture. In III, H. D. and Singh, A., editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 6874–6883. PMLR.

- (19) Mignacco, F., Krzakala, F., Lu, Y. M., , and Zdeborová, L. (2020b). The role of regularization in classification of high-dimensional noisy gaussian mixture. arXiv preprint arXiv:2002.11544.

- Miolane and Montanari, (2021) Miolane, L. and Montanari, A. (2021). The distribution of the lasso: Uniform control over sparse balls and adaptive parameter tuning. The Annals of Statistics, 49(4):2313–2335.

- (21) Montanari, A., Ruan, F., Sohn, Y., and Yan, J. (2019a). The generalization error of max-margin linear classifiers: High-dimensional asymptotics in the overparametrized regime. arXiv preprint arXiv:1911.01544.

- (22) Montanari, A., Ruan, F., Sohn, Y., and Yan, J. (2019b). The generalization error of max-margin linear classifiers: High-dimensional asymptotics in the overparametrized regime. arXiv preprint arXiv:1911.01544.

- Moreau, (1965) Moreau, J.-J. (1965). Proximité et dualité dans un espace hilbertien. Bulletin de la Société mathématique de France, 93:273–299.

- Salehi et al., (2018) Salehi, F., Abbasi, E., and Hassibi, B. (2018). A precise analysis of phasemax in phase retrieval. In 2018 IEEE International Symposium on Information Theory (ISIT), pages 976–980. IEEE.

- Salehi et al., (2019) Salehi, F., Abbasi, E., and Hassibi, B. (2019). The impact of regularization on high-dimensional logistic regression. Advances in Neural Information Processing Systems, 32.

- Salehi et al., (2020) Salehi, F., Abbasi, E., and Hassibi, B. (2020). The performance analysis of generalized margin maximizers on separable data. In International conference on machine learning, pages 8417–8426. PMLR.

- Stojnic, (2013) Stojnic, M. (2013). A framework to characterize performance of lasso algorithms. arXiv preprint arXiv:1303.7291.

- Sur and Candès, (2019) Sur, P. and Candès, E. J. (2019). A modern maximum-likelihood theory for high-dimensional logistic regression. Proceedings of the National Academy of Sciences, 116(29):14516–14525.

- Taheri et al., (2020) Taheri, H., Pedarsani, R., and Thrampoulidis, C. (2020). Sharp asymptotics and optimal performance for inference in binary models. Proceedings of Machine Learning Research, pages 3739–3749.

- Taheri et al., (2021) Taheri, H., Pedarsani, R., and Thrampoulidis, C. (2021). Fundamental limits of ridge-regularized empirical risk minimization in high dimensions. In International Conference on Artificial Intelligence and Statistics, pages 2773–2781. PMLR.

- (31) Thrampoulidis, C., Abbasi, E., and Hassibi, B. (2015a). Lasso with non-linear measurements is equivalent to one with linear measurements. Advances in Neural Information Processing Systems, 28.

- Thrampoulidis et al., (2018) Thrampoulidis, C., Abbasi, E., and Hassibi, B. (2018). Precise error analysis of regularized -estimators in high dimensions. IEEE Transactions on Information Theory, 64(8):5592–5628.

- (33) Thrampoulidis, C., Oymak, S., and Hassibi, B. (2015b). Regularized linear regression: A precise analysis of the estimation error. In Conference on Learning Theory, pages 1683–1709. PMLR.

- Thrampoulidis et al., (2020) Thrampoulidis, C., Oymak, S., and Soltanolkotabi, M. (2020). Theoretical insights into multiclass classification: A high-dimensional asymptotic view. Advances in Neural Information Processing Systems, 33:8907–8920.

Appendix A USEFUL TECHNICAL RESULTS

The following results will be of use for proving the theorems. We will invoke them multiple times without referring to them explicitly:

An expectation formula. Let . Then .

Proof.

Denote .

∎

A square root trick. The following equality holds for any :

Proof.

Differentiate the objective from the right hand side by :

We conclude that is minimized at . The value the objective takes at this point is

∎

Appendix B PROOFS OF THE LEMMAS

B.1 Proof of Lemma 1

Proof.

By definition,

Rewrite for and for . Note that and . We obtain:

Since and we have:

∎

B.2 Proof of Lemma 2

Proof.

Note that, since the model for the data distribution is symmetric w.r.t. the transformation , the equality has to hold for the optimal from each of the parts (1)-(3) of the lemma. One therefore has:

Now let us proceed to proving each of the points (1)-(3) separately:

1. Note that for any satisfying the symmetry condition it holds that

2. Assuming that and is a - bit vector we have

3. If is a - sparse vector such that , then

where is obtained from taking the coordinates of with the largest magnitude and zeroing out the rest.

∎

Appendix C PROOFS OF THE MAIN RESULTS

C.1 Proof of Theorem 2

Proof.

As discussed in Section 3.4, the proof reduces to analyzing the following optimization problem:

We rewrite it as a min-max problem to enable invocation of CGMT:

Applying CGMT yields the following AO:

Performing optimization over leads to:

| (5) |

Substituting for the norm of we obtain:

Recall that by definition . We then have and therefore

Noting that and using the square root trick we arrive to:

Writing the Fenchel dual for each of and we get:

Open up as . The objective above can be rewritten as:

We will recover the optimal now. Since the first part of the expression above is independent of , we will put it aside for a time being and look only at the second one:

| (6) |

The expression above is equal to the following by definition of the Moreau envelope:

We will simplify the objective further. Notice that also by definition . This equality can be plugged in into the corresponding part of the objective:

Recall that and are i.i.d Gaussian by assumption. Therefore, we have the following equality asymptotically when , where :

Note that we can take because our model for the data is symmetric w.r.t to the substitution . Thus, the expression above simplifies into:

Note also that

Putting all derivations above together, we are left with the following optimization problem:

Denoting , we arrive to the desired result:

∎

C.2 Proof of Theorem 3

Proof.

Taking the derivative by of the expression above and setting it to we get:

Since , we arrive at:

We conclude from the identity above that belongs in the span of and . Moreover, since this identity is invariant under the transformation , we also conclude that . Put together, this implies that can be written as . Now return to the equation (5) derived the proof of Theorem 2 and specify it to the case :

Performing optimization over we obtain:

| (7) |

Denote:

It is straightforward to open up each term from the objective above in terms of and :

Plugging these into equation (7), we get the desired objective:

Using Lemma 1 we also derive:

∎

C.3 Proof of Theorem 4

Proof.

Using Fenchel duality and introducing yields the following expression:

Due to the symmetry to the transformation , we have leading to the following optimization problem:

Solving for we get:

Where

The optimization would then be

Now we will plug in and calculate each term. The first term concentrates to

Similarly, we have for and :

For and we get:

Denoting

Putting the results together, we arrive at the following objective:

To calculate the sparsity rate, we analyze the probability of attaining non-zero values which is equivalent to the occurrence of the event :

A straightforward calculation of integrals yields and therefore . Subsequently, the solution is -sparse, where . ∎

C.4 Proof of Theorem 5

Proof.

Starting from equation (C.1) again, we introduce the regularization term as a constraint using a new variable :

Using Fenchel duality and introducing yields the following expression:

Due to the same symmetry as in the proof of the previous theorem, it holds that and the objective turns into

Now we can take derivative w.r.t and find the optimal solution,

We note that and thus

Then plugging in the previous expression,

Let . Using the assumptions on we model the randomness coming from by a single :

After finding we plug its value into the original optimization

It remains to express and in terms of the scalars. For we have

For inner product we observe the following concentration phenomenon:

Thus we have:

Therefore:

The optimization problem turns into:

Performing the optimization over we get the final expression:

Considering the expression for , it can also be seen that

∎

C.5 Calculating the generalization error

Proof.

As an attentive reader might have noticed, we omitted derivations for the expressions for the generalization error from the proofs of Theorems 2, 4, 5. The purpose of this subsection is filling in this gap.

Applying Lemma 1 and using that holds for the optimal from each of Theorems 2, 4, 5, we have . Thus, our goal is to determine the values of and . The former is immediate, as . The latter is less trivial but still straightforward; by definition,

and

We derive

Putting the equalities above together yields

∎

Appendix D DERIVATIONS BEHIND THE REMARKS

Recall from Section 3.4 that the problem is equivalent to analyzing the following:

| (8) |

To gain more insight, we would like to apply a unitary transformation , such that

To explain why it exists, note that the desired matrix equality is guaranteed by the following two vector equalities:

Due to the defining property of a unitary operator, such a unitary exists if and only if it would preserve all pairwise dot products between the vectors it is defined on. It is easy to see that all the coordinates of the vectors in the image of are chosen so that this would indeed be true.

Apply to the term under the norm in the equation (8). We have:

| (9) |

Since has the same distribution as , it can be written as , where for each and has its entries . Also denoting , and , we transform (9) into the following:

Applying CGMT to the objective above in the same way as in the proof of Theorem 2 yields:

| (10) |

D.1 Derivations behind Remark 1

Specifying equation (10) to the case of we get:

| (11) |

Note that if . Thus, the term is dominated by the regularization term, which is why we can drop it in this regime. After doing so, we get the following objective:

We claim that can be written in the form . Indeed, belongs in the span of and because all terms of (11) but the last one depend only on the projections of onto these directions and the last term is does not increase if all other directions are dropped from . Note also that because (11) is invariant under the transformation . Hence, .

To calculate the generalization error, note that and . Since we deemed the effect of the first term in (11) negligible, we can set , as this parameter does not play any role. The error then equals to the following:

D.2 Derivations behind Remark 2

Assume and note that

Plugging in the expressions for and from the previous remark, we have

Denoting , we derive

Since , the last term in the denominator can be neglected and the expression can be approximated as

D.3 Derivations behind Remark 3

In this section we present the optimal values of and which are used in the statement of Remark 3 and show that indeed the optimal attains the value except when . Let us consider the following optimization which comes from the equation (10):

For large enough , in a similar argument to the ridge regression case, we can neglect the first term because it is dominated by the regularization term, which yields:

Now we introduce through taking the Fenchel Dual of the square terms:

Rearranging the order of optimization to find the optimal w:

The optimization over reduces to:

Therefore the solution would be:

Note that plugging in results in adding the following constraint:

Or overall,

Which is equivalent to:

Denote

Using the preceding discussion, the optimization can be written as:

Furthermore, using the assumptions on , one can observe:

where and stands for equality in distribution.

Denote . Then the equivalent optimization would be:

We know that concentrates to for i.i.d. standard Gaussians (cf. Gumbel distribution for Gaussian random variables). Then, using a Lagrange multiplier:

Convexity in and concavity in all other variables allow us to swap min and max:

Note that

To do the quadratic optimization, we calculate the Schur Complement:

γ_1 = - γ_2 =: γγ, βηηγ, βη

D.4 Derivations behind Remark 4

Similar to the previous section, we present an approach through which, can be calculated efficiently. By taking to be large enough, we can drop the first term which in turn yields:

Adding a new variable for we obtain:

Introducing through Fenchel Dual and changing the order of optimization we derive the following objective:

It is straightforward to see that . So, the optimization would be

Let . Optimizing over yields:

In a manner similar to the previous section we note:

with . Denoting, This result entails the following objective:

We leverage the fact that for iid standard Gaussians , . To write the optimization in a more tractable format, we use a Lagrange multiplier to bring in the constraint:

It can be seen that we arrive at an objective which is essentially the same as the one in the previous section, but with being replaced by . Therefore we can use the results from before and derive the final optimization for :

We note that . Having found the , we therefore obtain:

Appendix E SOLVING THE SCALARIZED AO NUMERICALLY

Having simplified a high-dimensional optimization problem to a low-dimensional, i.e. one having 2-3 variables, the task of solving the scalarized optimization remains. Since the objective from the conclusion of Theorem 3 is a convex minimization problem, it could be handled directly using CVX. However, this is not the case for Theorems 4 and 5, where one must deal with a . Since there are no packages available for solving problems numerically, we needed to adapt different approaches. For Theorem 4, we conducted a grid search over and for each we performed maximization over and using MATLAB fmincon. Alternatively, doing a grid search over all variables is also a feasible approach, which may not work effectively when the number of variables and the number of points in the grid increase. Nevertheless, this is what we used for simulating Theorem 5, which turned out to work well in practice for variables and a grid with points.