High Precision Causal Model Evaluation with Conditional Randomization

Abstract

The gold standard for causal model evaluation involves comparing model predictions with true effects estimated from randomized controlled trials (RCT). However, RCTs are not always feasible or ethical to perform. In contrast, conditionally randomized experiments based on inverse probability weighting (IPW) offer a more realistic approach but may suffer from high estimation variance. To tackle this challenge and enhance causal model evaluation in real-world conditional randomization settings, we introduce a novel low-variance estimator for causal error, dubbed as the pairs estimator. By applying the same IPW estimator to both the model and true experimental effects, our estimator effectively cancels out the variance due to IPW and achieves a smaller asymptotic variance. Empirical studies demonstrate the improved of our estimator, highlighting its potential on achieving near-RCT performance. Our method offers a simple yet powerful solution to evaluate causal inference models in conditional randomization settings without complicated modification of the IPW estimator itself, paving the way for more robust and reliable model assessments.

1 Introduction

Experimental approaches for causal model evaluation

Causal inference models aim to estimate the causal effects of treatments or interventions on outcomes of interest, given observational (sometimes experimental) data. A crucial step in developing and validating such models is to evaluate their prediction quality, that is, how well they can approximate the true treatment effects that would have been observed under different scenarios. A common approach for causal model evaluation is to launching a new randomized controlled trial (RCT) separately, which provides a reliable estimate of the true treatment effects by randomly assigning units to treatments. By comparing the RCT estimate with the prediction of the causal model, one can assess the causal error (Equation 1), a key metric to measure how well the model reflects the true effects.

Nevertheless, RCTs are not always accessible or preferable, as random manipulation of treatments might be impractical, ethically questionable, or excessively expensive. For instance, it may be impossible or inappropriate to randomly assign individuals to different lifestyles, environmental exposures, or social policies, as these may involve personal choices, preferences, or constraints that affect the willingness or ability to participate in the experiment. In such cases, causal machine learning researchers may resort to or augment their analyses with conditionally randomized designs, in which the allocation of participants into treatment and control groups is not purely random, but is instead based on a predetermined condition or factor.

Conditionally randomized experiments can vary in the level and unit of treatment assignment, such as individual, group, or setting. They also depend on different assumptions and methods to account for the potential confounding, selection, or measurement biases that arise from the lack of randomization. A common scenario is the non-random quantitative assignment paradigm (West et al., 2008), where a new set of treatment groups are selected given some quantitative covariates , via an oracle model , where is the treatment variable. For example, in sales strategy assignment, it is typical that resources are allocated towards products with higher revenue contributions, which introduces explicit confounding. A widely used method to estimate the true treatment effect in this setting is the inverse probability weighting (IPW) estimator (Rosenbaum and Rubin, 1983; Rosenbaum, 1987), which uses the propensity scores, the probability of receiving the treatment given the covariates, to weight the observed outcomes and adjust for the imbalance between the treatment groups. This IPW estimate can then be compared with the causal model prediction to evaluate the causal error.

Limitations of current approaches

Despite the popularity of the IPW estimator for conditionally randomized experiments, it suffers from several limitations that affect its reliability for causal model evaluation. (Khan and Tamer, 2010) shows that IPW may have unbounded variance when the propensity scores are imbalanced. Moreover, the it may have poor finite sample performance and high sensitivity to the specification of the propensity score model (Busso et al., 2014). Last but not the least, a surprising finding is that even the oracle IPW may be harmful for the estimation efficiency (Hahn, 1998; Hirano et al., 2003). As a consequence, the causal error estimation based on the IPW estimator may not be accurate or robust, and may lead to misleading conclusions about the causal model quality. Existing work on addressing the variance issue of the IPW estimator often involves modifying the IPW estimator itself (Crump et al., 2009; Chaudhuri and Hill, 2014; Sasaki and Ura, 2022; Busso et al., 2014; Robins et al., 2007; Lunceford and Davidian, 2004; Imbens, 2004; Liao and Rohde, 2022). However, these methods are mainly designed for treatment effect estimation rather than causal error estimation, and may introduce additional bias or complexity that may not be optimal for the purpose of causal model evaluation.

Contributions overview

We focus on causal model evaluation with conditionally randomized trials, propose a novel method for low-variance estimation of causal error (Equation 1), and demonstrate its effectiveness over current approaches by achieving near-RCT performance. Our key insight is: to estimate the causal error, we can design a simple and effective low-variance estimation procedure without improving the IPW estimator for the true treatment effect. As shown in Figure 1, denote the ground truth effect as and the treatment effect of a causal model as . Our goal to estimate the causal error with low variance. Using conditionally randomized experiments, we have an estimator of the ground truth via IPW: . Instead of improving the IPW estimator, we replace the commonly used sample mean estimator with its IPW counterpart, , having the same realizations of treatment assignments as in . This allows the variance of to be hedged by , reducing the variance of the causal error estimator . Contrary to conventional estimation strategies, the pairs estimator, as we call it, effectively reduces the variance of the causal error estimation and provides more reliable evaluations of causal model quality, both theoretically and empirically.

The rest of this paper is structured as follows. In Section 3, we formally describe our problem setting, necessary background and notations. In Section 4, we will formally define the pairs estimator for causal model evaluation, and study its theoretical properties (Proposition 1) on variance reduction. Finally, in Section 5, we will conduct simulation studies and demonstrate the effectiveness of the proposed estimation approach, highlighting its potential on achieving near-RCT performance using only conditionally randomized experimental data.

2 Related works

Alternative schemes to randomized controlled trials

There exists a number of different conditionally randomized trial schemes in the literature, for instance randomized encouragement designs (Angrist et al., 1996), non-random quantitative treatment assignment (Imbens and Rubin, 2015), and fully observational studies (Rubin, 2005). In this work, we mainly consider the non-random quantitative treatment assignment setting, where the treatment groups are determined by some known function of covariates. Nevertheless, we have an emphasized focus on using conditionally randomized trials for evaluating the quality of any given causal inference models (trained on observational data), which is a fundamental setting for many practical causal model deployment procedure.

Causal estimation methods with conditionally randomized experiments

Apart from IPW mentioned in Section 1, a number of other methods were also developed for conditionally randomized trials settings, include matching (Ho et al., 2007; Stuart, 2010; Rubin, 2006), regression adjustment (Neyman, 1923; Rubin, 1974; Lin, 2013; Wager et al., 2016), double robust methods (Robins et al., 1995; Bang and Robins, 2005; Kang and Schafer, 2007; Athey et al., 2018), and machine learning methods (Athey and Imbens, 2016; Wager and Athey, 2018; Shi et al., 2019; Chernozhukov et al., 2018). Readers can refer to (Imbens and Rubin, 2015; Morgan and Winship, 2015) for a comprehensive review. This paper, on the contrary, aims to propose a general method for causal model evaluation applicable to any causal effect estimation method, particularly the widely used IPW estimator.

Variance reduction and robustness

There has been a long standing discussion on robustness improvement (Robins et al., 1995) and variance reduction of IPW estimators. Several techniques have been proposed to address the problem of extreme or uninformative weights, including weights trimming (Crump et al., 2009; Chaudhuri and Hill, 2014; Sasaki and Ura, 2022), weights normalization (Busso et al., 2014; Robins et al., 2007; Lunceford and Davidian, 2004; Imbens, 2004), and more recently, linearly-modified IPW (Zhou and Jia, 2021), etc. These techniques aim to reduce variance but may introduce bias, complexity, or tuning parameters. Our work differs from the existing literature in that, we focus on the causal error estimation, rather than the individual treatment effect estimation. We do not improve the IPW estimator for the true treatment effect, but rather propose to apply the same IPW estimator to both the model and the true effects to hedge their variances.

3 Problem formulation

Consider the data generating distribution for the population on which the experiment is being carried over is given by , where are some (multivariate) covariates, is the outcome variable and is the treatment variable. In this paper, we only consider continuous effect outcomes. Let denote the potential outcome of the effect variable under the intervention . Without loss of generality, we assume . Then, the interventional means are given by , and , respectively. The ground truth treatment effect is then given by

Now, assume that given observational data sampled from , we have trained a causal model, denoted by , whose treatment effect is given by

Our goal is then to estimate the causal error of the model, which quantifies how well the model reflects the true effects (the closer to zero, the better):

| (1) |

In practice, will be the model output, and can be estimated easily. For example, we can sample a pool of i.i.d. subjects , and the corresponding treatment effect estimation will be given as

| (2) |

which forms the basics of many casual inference methodologies, both for potential-outcome approaches and structural causal model approaches (Rubin, 1974; Rosenbaum and Rubin, 1983; Rubin, 2005; Pearl et al., 2000). On the contrary, obtaining the ground truth effect is usually not possible without real-world experiments/interventions, due to the fundamental problem of causal inference (Imbens and Rubin, 2015). By definition, can be (hypothetically) approximated by the population mean of potential outcomes:

| (3) |

However, given a subject , only one version of the potential outcomes can be observed. Therefore, we often resort to the experimental approach, the randomized controlled trial (RCT). The RCT approach is always considered as the golden standard for treatment effect estimation, in which we would randomly assign treatments to our pool of subjects , by flipping an unbiased coin. Then the estimated treatment effect is given by:

where denotes the subset of patients that are assigned with the treatment. Together, we have the RCT estimator of the causal error:

| (4) |

However, when a randomized trial is not available, we can only deploy a conditionally randomized test assignment plan, represented by , which is a vector of Bernoulli random variables , each determines that will be revealed with probability . In practice, can be given by an treatment assignment model . This is an oracle distribution that is known and designed by the experiment designer. A subset of patients is selected given these assigment probabilities. Then, the inverse probability weighted (IPW) estimation of the treatment effect is given by

where , is created by sub-slicing with subject indices in . is the inner product, and is a vector of ones. Finally, the model causal error can be estimated as (dubbed naive estimator in this paper):

| (5) |

In practice, when the size of the subject pool is relatively small, the IPW estimated treatment effect will have high variance especially when is skewed. As a result, one will expect a very high or even unbounded variance in the estimation (Khan and Tamer, 2010; Busso et al., 2014) . The goal of this paper is then to improve model quality estimation strategy , such that it has lower variance and error rates under conditionally randomized trials.

4 Pairs estimator for causal model quality evaluation

4.1 The pairs estimator

To resolve the problems with the naive estimator for causal error in Section 3, in this section, we propose a novel yet simple estimator that will significantly improve the quality of the causal error estimation in a model-agonist way. Intuitively, when estimating , we can simply apply the same IPW estimator (with the same treatment assignment) for both the model treatment effect and the ground truth treatment effect . In this way, we anticipate that the estimators for and will become correlated; their estimation error will be canceled out and hence the overall variance is lowered. More formally, we have the following definition:

Definition 1 (Pairs estimator for causal model quality).

Assume we have a pool of i.i.d. subjects to be tested, namely , as well as a conditionally randomized treatment assignment plan, represented by , which is a vector of Bernoulli random variables , each determines that will be revealed with probability . Assume that, for a particular trial, a subset of patients are selected using these probabilities. Then, the IPW estimator of the model’s treatment effect and the ground truth treatment effect is given by

, and

, respectively. Then, the pairs estimator of causal model quality is defined as

| (6) |

We will formally show that this new estimator can effectively reduce estimation error. We will provide the full assumptions and proposition below. Note that we will assume by default that the common assumptions for conditionally randomized experiments will hold, such as non-interference/consistency/overlap, etc, even though we will not explicitly mention them for the rest of the paper.

4.2 Core assumptions for achieving variance reduction

Our main assumption is regarding the estimation error of causal models, stated as below:

Assumption A. Causal model estimation error for potential outcomes.

We assume that for each subject , the trained causal model’s potential outcome estimation can be expressed as

| (7) |

where are i.i.d. distributed random error variables with unknown variance , that is independent from and ; and is a set of deterministic function that is indexed by . This assumption is very general and models the modulation effect between the independent noise and the ground truth counterfactual. One special example would be , where the estimation error will increase (on average) as increases. In practice, dependencies between error magnitude and ground truth value could arise when the model is trained on observational data that suffers from selection bias, measurement error, omitted variable bias, etc. For the rest of paper, we write Equation 7 in its vectorized form:

where all operations are point-wise. Finally, we further require that the causal model’s counterfactual prediction should be somewhat reasonable, in the sense that . This implies that the variance of the estimation error should at least be smaller than the ground truth counterfactual.

Assumption B. Asymptotic normality of mean estimators of potential outcome variables.

111Note that this particular assumption is mainly for achieving asymptotic normality of the estimators, which is orthogonal to achieving variance reduction effect of our pairs estimator, that relies on Assumption A.Let , , , be the corresponding mean estimator of the potential outcome variables , , , . We assume that these estimators are jointly asymptotic normal, i.e.,

converge in distribution to a zero mean multivariate Gaussian. This is reasonable due to the randomization and the large samples used in experiments (Casella and Berger, 2021; Deng et al., 2018).

4.3 Theoretical results

Following our assumptions, we can derive the following theoretical result, which shows that given our assumptions described in the previous section, the pairs estimator will effectively reduce estimation variance compared to the naive estimator, .

Proposition 1 (Variance reduction effect of the pairs estimator).

With the assumptions stated in Section 4.2, we can show that our IPW estimators, and can be decomposed as

where and are random variables that depend on (or also ), and is orthogonal to , and . Furthermore, if we define the estimation error of model quality estimators as follows

then both and are asymptotically normal with zero means, and their variances satisfies

Proof: See Appendix A ∎

This result provides theoretical justifications that our simple estimator will be effective for variance reduction. In the next section, we will conduct simulation studies to empirically evaluate and validate the effectiveness proposed approach.

5 Simulation Studies

In this section, we will evaluate the performance of the proposed pairs estimator, and validate our theoretical insights via simulation studies. We will also examine the robustness and sensitivity of the pairs estimator concerning different scenarios of conditionally randomized trials, including treatment assignment mechanisms, degree of imbalance, choice of causal machine learning models, etc.

5.1 Synthetic csuite dataset with hypothetical causal model

Setting.

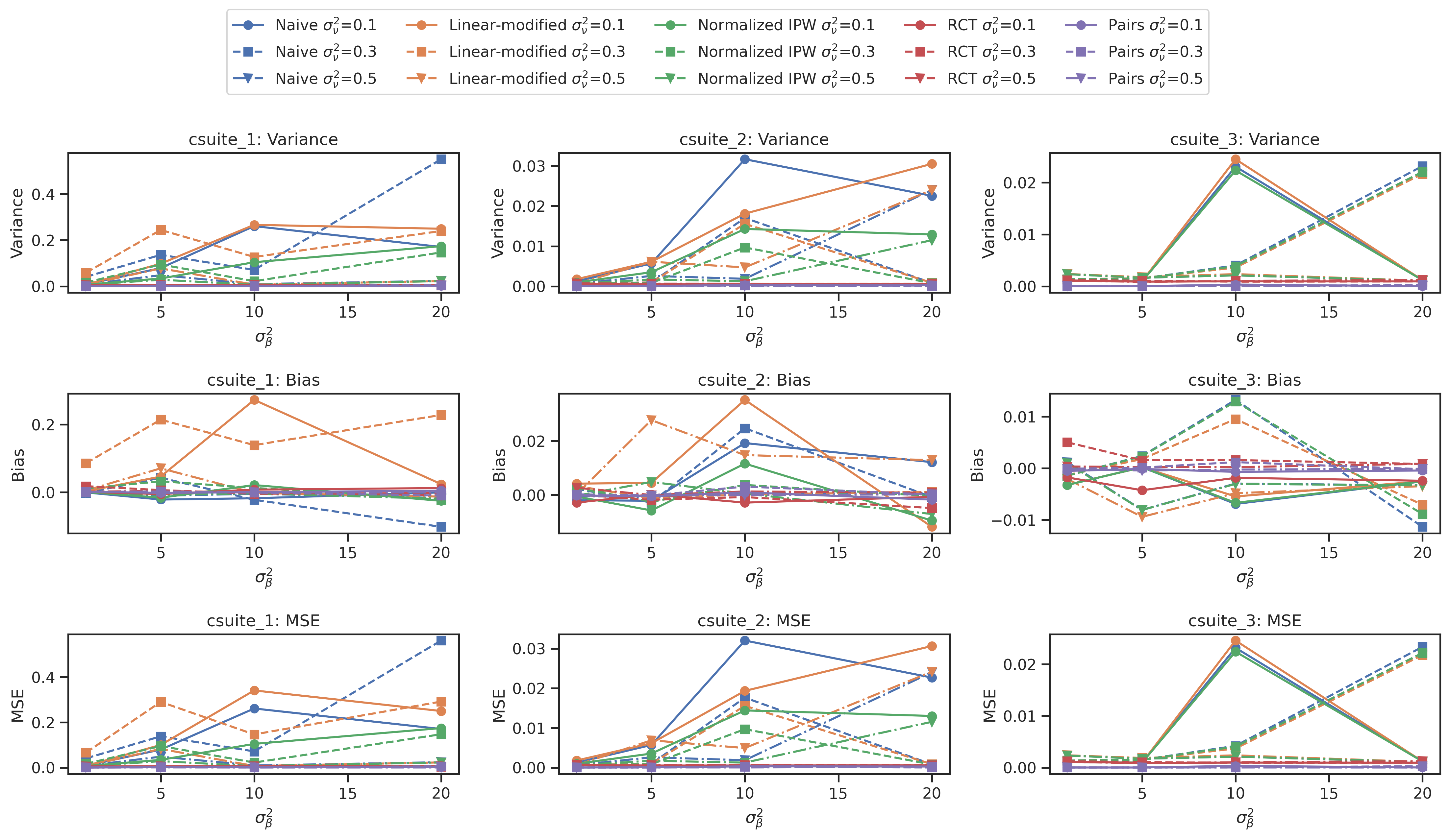

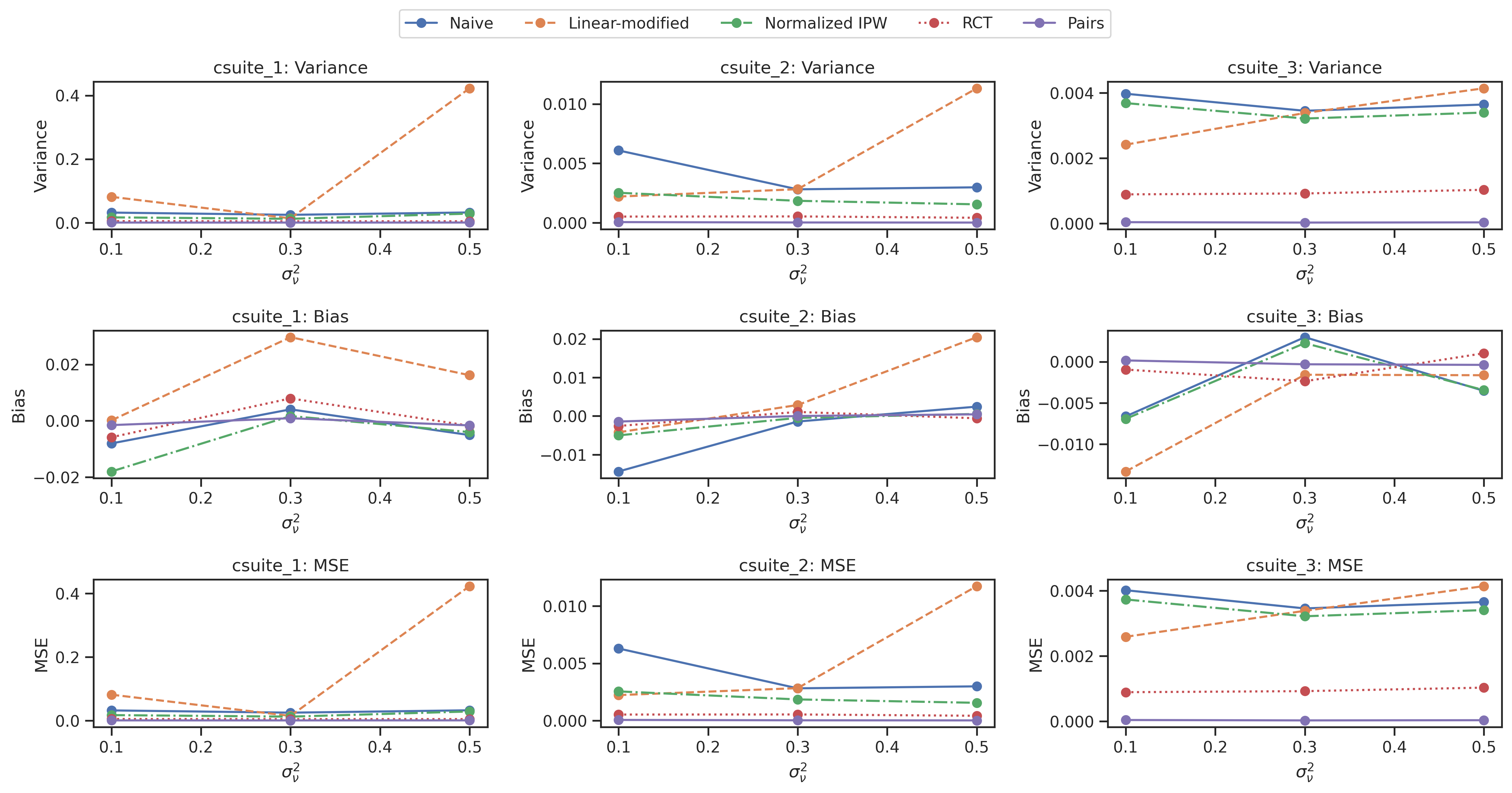

Following Geffner et al. (2022), we construct a set of synthetic datasets, designed specifically for evaluating causal inference performance, namely the csuite datasets. The data-generating process is based on structural causal models (SCMs), different levels of confounding, heterogeneity, and noise types are incorporated, by varying the strength, direction, and parameterize of the causal effects. We evaluated on three different datasets, namely csuite_1, csuite_2, and csuite_3, each with a different SCM. See Appendix B for more details. The corresponding causal model estimation is simulated using a special form of Assumption A, that is:

where are i.i.d. distributed zero-mean random variables with variance that affects the ground truth causal error. To simulate the conditionally randomized trials, we use two different schemes to generate the treatment assignment plans . The first scheme is based on a logistic regression model of the treatment assignment probability given the covariates, that is,

, where is a random vector sampled from multivariate Gaussian distributions with mean zero and variance . We vary the degree of imbalance in the treatment assignment by changing the value of . A larger implies a more imbalanced treatment assignment, as the variance of the treatment assignment probability increases. The second scheme is based on a random subsampling of the units, where the treatment assignment probability is fixed for each unit, but different units are sampled with replacement to form different treatment assignment plans. We vary the number of treatment assignment plans by changing the sample size of each subsample.

Evaluation method.

We compare the performance of the pairs estimator with the naive estimator (Equation 5), as well as the RCT estimator (Equation 4), which is the ideal benchmark for causal model evaluation. We also compare with two other baselines, by replacing the IPW component in the naive estimator (Equation 5) by its variance reduction variants. This includes the self-normalized estimator, as well as the linearly modified (LM) IPW estimator Zhou and Jia (2021), a state-of-the-art method for IPW variance reduction when the propensity score is known. We measure the performance of the estimators by the following metrics: the variance, the bias, and the MSE of the causal error estimation. See Section B.1 for detailed definitions. We compute these metrics by averaging over 100 different realizations of the treatment assignment plans for each dataset.

Results.

The results are shown in Figure 2 and Figure 3. Figure 2 shows the results for the logistic regression scheme, with different values of and . Figure 3 shows the results for the random subsampling scheme, with different . In both tables, we report the average and the standard deviation of the performance metrics of the estimators for each value of the true causal error, which is computed by the difference between the true treatment effect and the model treatment effect.

From the tables, we can see that the variance of the naive estimator quickly increases when the treatment assignment is highly imbalanced. Nevertheless, our estimator (purple) consistently outperforms the naive estimator and its variance reduction variants in all metrics (variance/bias/MSE) regardless of the value of (), and the degree of imbalance (). The pairs estimator also achieves comparable performance to the RCT estimator, the golden standard by design. The linearly-modified estimators and self-normalized estimators have a lower variance than the naive estimator, but it also introduces some bias, and their performance is sensitive to the degree of imbalance. These demonstrate the effectiveness and robustness of the proposed pairs estimator when all assumptions are met.

5.2 Synthetic counterfactual dataset with popular causal inference models

Settings.

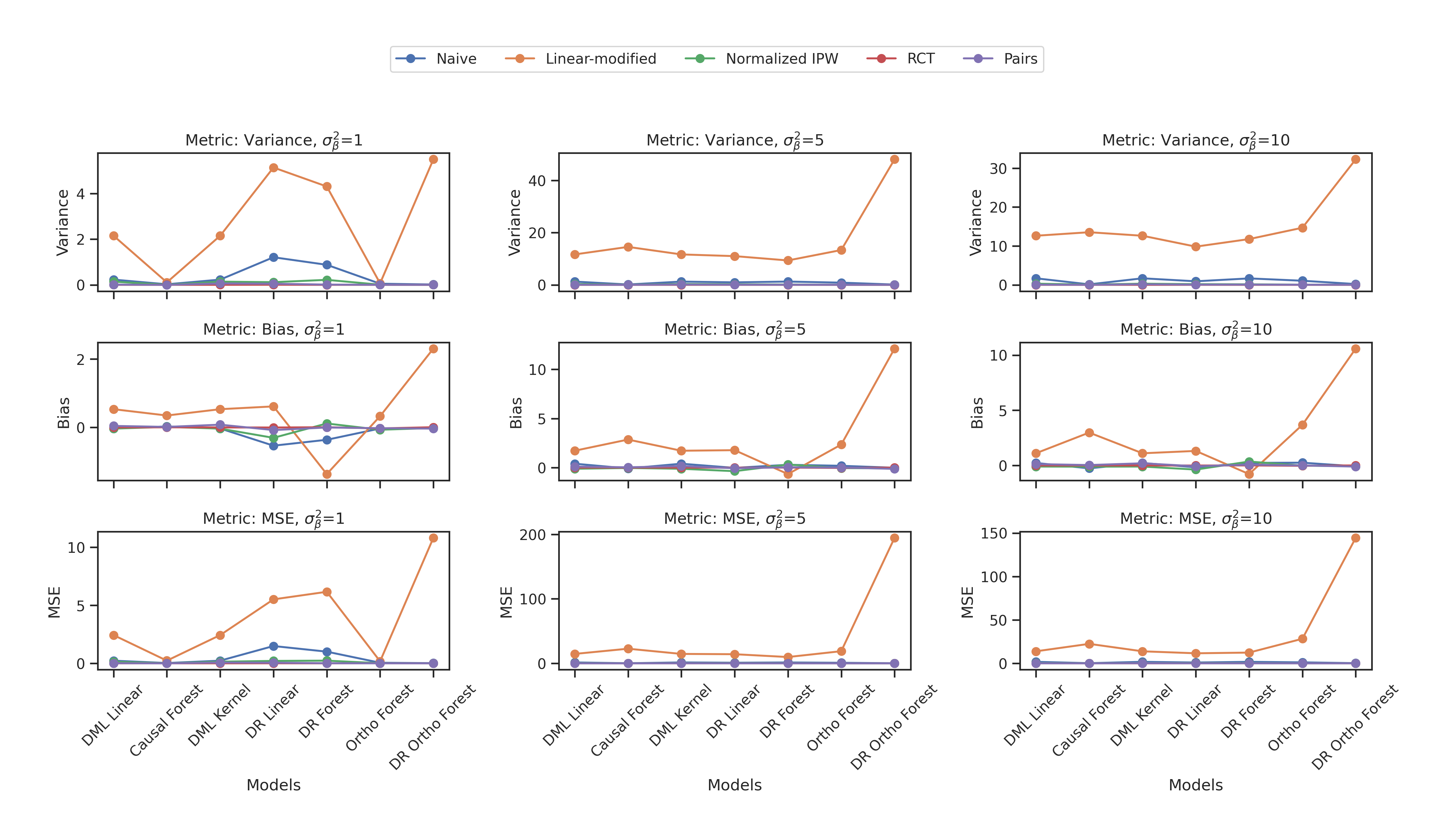

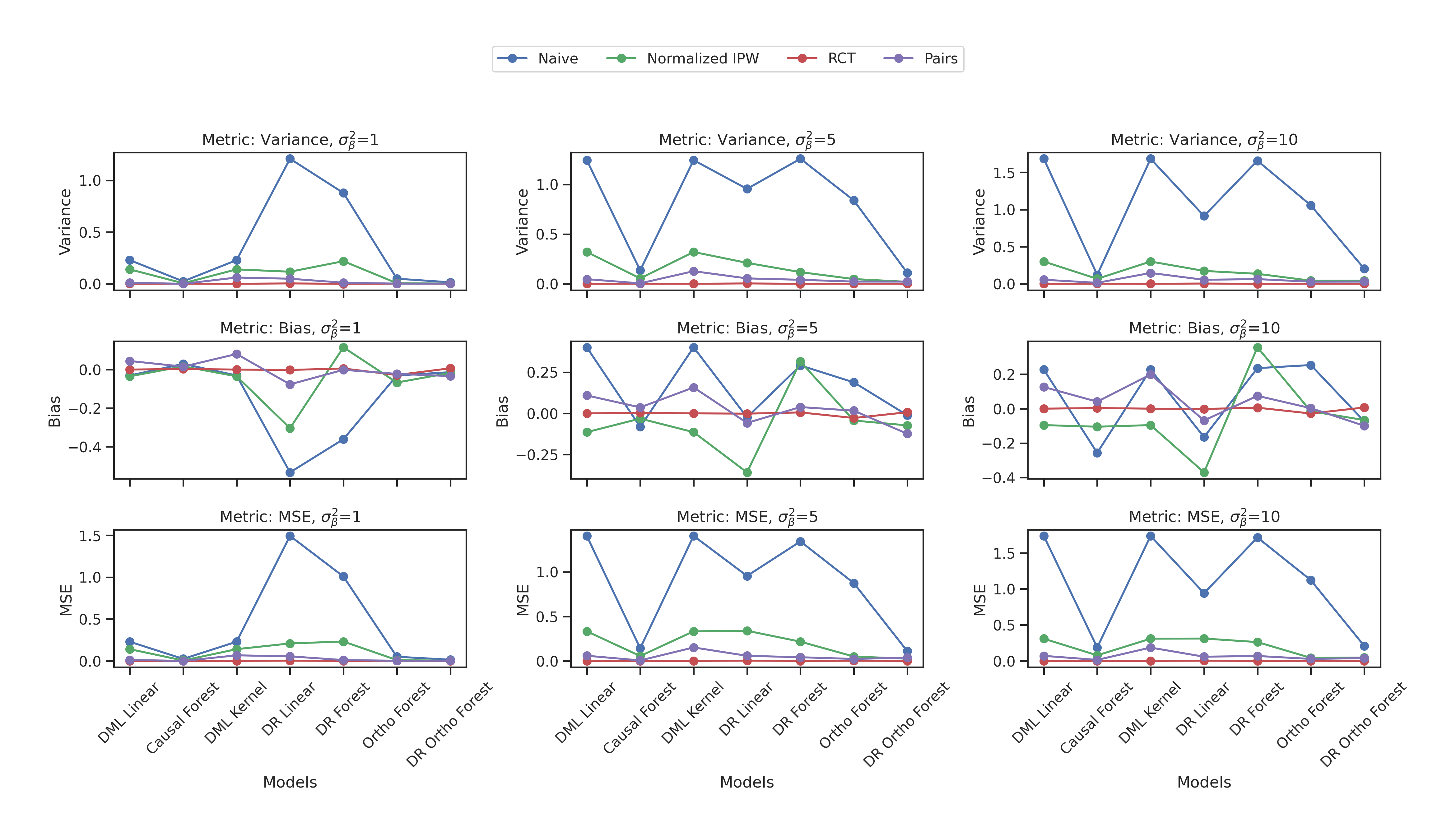

Based on Section 5.1, we now consider more realistic experimental settings, in which we apply a wide range of machine learning-based causal inference methods by training them from synthetic observational data. Thus, we expect the assumptions in Section 4.2 might not strictly hold anymore, which can be used to test the robustness of our method. We include a wide range of methods, such as linear double machine learning(Chernozhukov et al., 2018) (dubbed as DML Linear), kernel DML (DML Kernel) (Nie and Wager, 2021), causal random forest (Causal Forest) (Wager and Athey, 2018; Athey et al., 2019), linear doubly robust learning(DR Linear), forest doubly robust learning (DR Forest), orthogonal forest learning (Ortho Forest) (Oprescu et al., 2019), and doubly robust orthogonal forest (DR Ortho Forest). All methods are implemented via EconML package (Battocchi et al., 2019). See Appendix B for more details.

We mainly focus on two aspects: 1), whether the proposed estimator can still be effective on variance reduction with non-hypothetical models as in Section 5.1; 2), whether the learned causal models’ counterfactual predictions approximately follow the postulated Assumption A. Here We present the results for the first aspect, and results for the second can be found in Section 5.3.

Simulation procedure.

We repeat the same simulation procedure as in Section 5.1, but using the learned causal inference models instead of the simulated causal model. We compare the performance of the pairs estimator with the same baselines as in Section 5.1, using the same metrics and the same treatment assignment schemes. For DML Linear, DML Kernel, Causal Forest, and Ortho Forest (that does not require propensity scores), we train on 2000 observational data points generated via the following data generating process of single continuous treatment (Battocchi et al., 2019):

where is the treatment, is the confounder, is the control variable, is the effect variable, and and are some uniform distributed noise. We choose the dimensionality of and to be and , respectively. For other doubly robust-based methods, we use a discrete treatment that is sampled from a binary distribution , while keeping the others unchanged. Once models are trained on the generated observational datasets, we use the trained causal inference model to estimate the potential outcomes and the treatment effects for each unit. Then, we use the logistic regression-based treatment assignment scheme as in Section 5.1 to simulate a hypothetical conditionally randomized experiment (for both continuous treatment and binary treatment, we will assign for the treatment group and for the control group). Both our pairs estimator as well as other baselines presented in Section 5.1 will be used to estimate the causal error. This is repeated 100 times across 3 different settings for treatment assignment imbalance ().

Results.

Figure 4 222The linearly-modified baseline is not displayed for clarity reasons, see Appendix B, Figure 6 for full results. shows that using our estimator with conditionally randomized data, we achieved near-RCT performance for causal model evaluation quality across all metrics. It is also more robust to different settings of , where no significant variance change is observed. Also, we note that each causal error estimator has a different sweet-spot: for instance, the naive estimator usually consistently works very well with Causal Forest, whereas our estimator has relatively high variance and bias for DML Kernel. Nevertheless, the proposed estimator is still the most robust estimator (apart from RCT) that consistently achieves the best results across all causal models. This shows the feasibility of our method for reliable model evaluation with conditionally randomized experiments.

5.3 Validation of Assumption A in Section 4.2

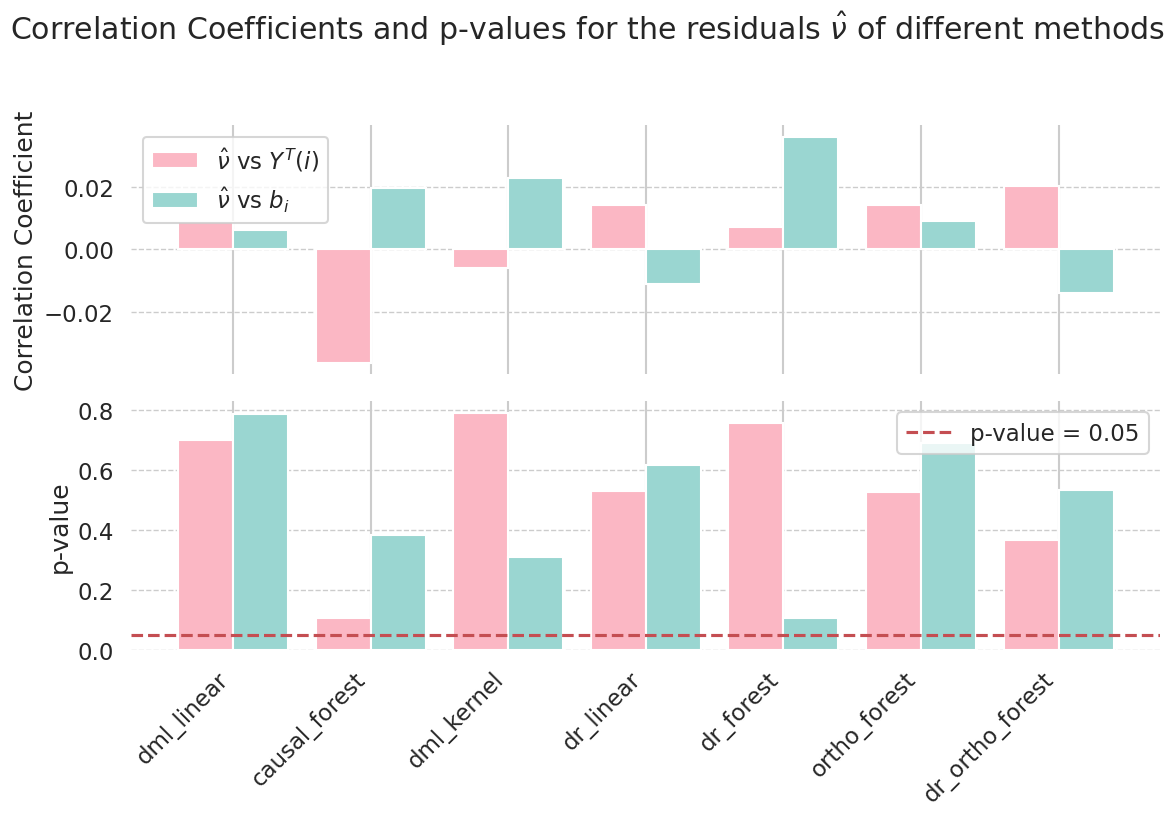

Settings

Finally, we provide experiments to validate Assumption A in Section 4.2. Specifically, we use a numerical example to check if Assumption A holds in practice for various commonly used models, including the ones considered in Section 5.2, including DML Linear, DML kernel, Causal Forest, and variations of doubly robust algorithms (DR Linear, DR forest, DR Ortho Forest). We first fit different methods using the observational data generated in Section 5.2, and obtain the counterfactual predictions from each method; Then, we parameterize the function in Equation 7 as a polynomial function and fit for the counterfactual predictions using Equation 7. Finally, we solve for the residuals in Equation 7, and test whether they are independent from and , as postulated in Assumption A.

Results

As shown in Figure 5, we calculate the Pearson correlation coefficient between and and , respectively, as shown in the upper plot; we also compute the p-values for the null hypothesis that the samples are independent. We observe that the samples have close zero correlations as well as high p-values that are unable to reject the null assumption. Hence, both results shows suggests that the independence multiplicative noise assumption is likely to be true under this setting. We have also tried other tests such as Hoeffding’s independence tests that captures non-linear dependencies, which yields similar results. This indicates that Assumption A is not overly restrictive and can be satisfied by a wide range of causal models that are popular in practical applications.

6 Conclusions

In this paper, we proposed the pairs estimator, a novel methodology for low-variance estimation of causal error in conditionally randomized trials. This approach applies the same IPW method to both the model and ground truth effects, canceling out the variance due to IPW. Remarkably, the pairs estimator can achieve near-RCT performance using conditionally randomized experiments, signifying a novel contribution for enabling more reliable and accessible model evaluation, without depending on expensive or infeasible randomized experiments. Future work may extend our method to more complex scenarios, explore alternative ways to reduce causal error estimation variance, and apply our method to other causality applications such as policy evaluation, causal discovery, and counterfactual analysis.

Acknowledgements

We thank Colleen Tyler, Maria Defante, and Lisa Parks for conversations on real-world use cases that inspired this work. We also thank Nick Pawloski, Wenbo Gong, Joe Jennings, Agrin Hilmkil and Meyer Scetbon for useful discussions and support that enables this work.

References

- Angrist et al. [1996] Joshua D Angrist, Guido W Imbens, and Donald B Rubin. Identification of causal effects using instrumental variables. Journal of the American statistical Association, 91(434):444–455, 1996.

- Athey and Imbens [2016] Susan Athey and Guido Imbens. Recursive partitioning for heterogeneous causal effects. Proceedings of the National Academy of Sciences, 113(27):7353–7360, 2016.

- Athey et al. [2018] Susan Athey, Guido W Imbens, and Stefan Wager. Approximate residual balancing: debiased inference of average treatment effects in high dimensions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(4):597–623, 2018.

- Athey et al. [2019] Susan Athey, Julie Tibshirani, and Stefan Wager. Generalized random forests. 2019.

- Bang and Robins [2005] Heejung Bang and James M Robins. Doubly robust estimation in missing data and causal inference models. Biometrics, 61(4):962–973, 2005.

- Battocchi et al. [2019] Keith Battocchi, Eleanor Dillon, Maggie Hei, Greg Lewis, Paul Oka, Miruna Oprescu, and Vasilis Syrgkanis. EconML: A Python Package for ML-Based Heterogeneous Treatment Effects Estimation. https://github.com/py-why/EconML, 2019.

- Blyth [1972] Colin R Blyth. On simpson’s paradox and the sure-thing principle. Journal of the American Statistical Association, 67(338):364–366, 1972.

- Busso et al. [2014] Matias Busso, John DiNardo, and Justin McCrary. New evidence on the finite sample properties of propensity score reweighting and matching estimators. Review of Economics and Statistics, 96(5):885–897, 2014.

- Casella and Berger [2021] George Casella and Roger L Berger. Statistical inference. Cengage Learning, 2021.

- Chaudhuri and Hill [2014] Saraswata Chaudhuri and Jonathan B Hill. Heavy tail robust estimation and inference for average treatment effects. Technical report, Working paper, 2014.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 2018.

- Crump et al. [2009] Richard K Crump, V Joseph Hotz, Guido W Imbens, and Oscar A Mitnik. Dealing with limited overlap in estimation of average treatment effects. Biometrika, 96(1):187–199, 2009.

- Deng et al. [2018] Alex Deng, Ulf Knoblich, and Jiannan Lu. Applying the delta method in metric analytics: A practical guide with novel ideas. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 233–242, 2018.

- Geffner et al. [2022] Tomas Geffner, Javier Antoran, Adam Foster, Wenbo Gong, Chao Ma, Emre Kiciman, Amit Sharma, Angus Lamb, Martin Kukla, Nick Pawlowski, et al. Deep end-to-end causal inference. arXiv preprint arXiv:2202.02195, 2022.

- Hahn [1998] Jinyong Hahn. On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, pages 315–331, 1998.

- Hirano et al. [2003] Keisuke Hirano, Guido W Imbens, and Geert Ridder. Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71(4):1161–1189, 2003.

- Ho et al. [2007] Daniel E Ho, Kosuke Imai, Gary King, and Elizabeth A Stuart. Matching as nonparametric preprocessing for reducing model dependence in parametric causal inference. Political analysis, 15(3):199–236, 2007.

- Imbens [2004] Guido W Imbens. Nonparametric estimation of average treatment effects under exogeneity: A review. Review of Economics and statistics, 86(1):4–29, 2004.

- Imbens and Rubin [2015] Guido W Imbens and Donald B Rubin. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- Kang and Schafer [2007] Joseph DY Kang and Joseph L Schafer. Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data. 2007.

- Khan and Tamer [2010] Shakeeb Khan and Elie Tamer. Irregular identification, support conditions, and inverse weight estimation. Econometrica, 78(6):2021–2042, 2010.

- Liao and Rohde [2022] Jiangang Liao and Charles Rohde. Variance reduction in the inverse probability weighted estimators for the average treatment effect using the propensity score. Biometrics, 78(2):660–667, 2022.

- Lin [2013] Winston Lin. Agnostic notes on regression adjustments to experimental data: Reexamining freedman’s critique. 2013.

- Lunceford and Davidian [2004] Jared K Lunceford and Marie Davidian. Stratification and weighting via the propensity score in estimation of causal treatment effects: a comparative study. Statistics in medicine, 23(19):2937–2960, 2004.

- Morgan and Winship [2015] Stephen L Morgan and Christopher Winship. Counterfactuals and causal inference. Cambridge University Press, 2015.

- Neyman [1923] Jersey Neyman. Sur les applications de la théorie des probabilités aux experiences agricoles: Essai des principes. Roczniki Nauk Rolniczych, 10:1–51, 1923.

- Nie and Wager [2021] Xinkun Nie and Stefan Wager. Quasi-oracle estimation of heterogeneous treatment effects. Biometrika, 108(2):299–319, 2021.

- Oprescu et al. [2019] Miruna Oprescu, Vasilis Syrgkanis, and Zhiwei Steven Wu. Orthogonal random forest for causal inference. In International Conference on Machine Learning, pages 4932–4941. PMLR, 2019.

- Pearl et al. [2000] Judea Pearl et al. Models, reasoning and inference. Cambridge, UK: CambridgeUniversityPress, 19(2), 2000.

- Robins et al. [2007] James Robins, Mariela Sued, Quanhong Lei-Gomez, and Andrea Rotnitzky. Comment: Performance of double-robust estimators when" inverse probability" weights are highly variable. Statistical Science, 22(4):544–559, 2007.

- Robins et al. [1995] James M Robins, Andrea Rotnitzky, and Lue Ping Zhao. Analysis of semiparametric regression models for repeated outcomes in the presence of missing data. Journal of the american statistical association, 90(429):106–121, 1995.

- Rosenbaum [1987] Paul R Rosenbaum. Model-based direct adjustment. Journal of the American statistical Association, 82(398):387–394, 1987.

- Rosenbaum and Rubin [1983] Paul R Rosenbaum and Donald B Rubin. The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1):41–55, 1983.

- Rubin [1974] Donald B Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of educational Psychology, 66(5):688, 1974.

- Rubin [2005] Donald B Rubin. Causal inference using potential outcomes: Design, modeling, decisions. Journal of the American Statistical Association, 100(469):322–331, 2005.

- Rubin [2006] Donald B Rubin. Matched sampling for causal effects. Cambridge University Press, 2006.

- Sasaki and Ura [2022] Yuya Sasaki and Takuya Ura. Estimation and inference for moments of ratios with robustness against large trimming bias. Econometric Theory, 38(1):66–112, 2022.

- Shi et al. [2019] Claudia Shi, David Blei, and Victor Veitch. Adapting neural networks for the estimation of treatment effects. Advances in neural information processing systems, 32, 2019.

- Stuart [2010] Elizabeth A Stuart. Matching methods for causal inference: A review and a look forward. Statistical science: a review journal of the Institute of Mathematical Statistics, 25(1):1, 2010.

- Wager and Athey [2018] Stefan Wager and Susan Athey. Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113(523):1228–1242, 2018.

- Wager et al. [2016] Stefan Wager, Wenfei Du, Jonathan Taylor, and Robert J Tibshirani. High-dimensional regression adjustments in randomized experiments. Proceedings of the National Academy of Sciences, 113(45):12673–12678, 2016.

- West et al. [2008] Stephen G West, Naihua Duan, Willo Pequegnat, Paul Gaist, Don C Des Jarlais, David Holtgrave, José Szapocznik, Martin Fishbein, Bruce Rapkin, Michael Clatts, et al. Alternatives to the randomized controlled trial. American journal of public health, 98(8):1359–1366, 2008.

- Zhou and Jia [2021] Kangjie Zhou and Jinzhu Jia. Variance reduction for causal inference. arXiv preprint arXiv:2109.05150, 2021.

Appendix A Proof of Proposition 1

Proof:

First, it is straightforward to show that the IPW estimator of the ground truth treatment effect can be re-written in terms of the population mean estimator, (Equation 3):

| (8) |

Similarly, we can derive a similar relationship for the IPW model treatment effect estimator :

| (9) |

By setting:

, Then under Assumption A, we arrive at the first conclusion of the proposition, that the estimation error of and can be further decomposed as

| (10) | ||||

| (11) |

.

Therefore, and are now given by

| (12) | ||||

| (13) |

, respectively. Their estimation error is then given by

| (14) | ||||

| (15) |

. According to delta method Casella and Berger [2021], both and are asymptotically normal with zero under Assumption B. However, their variances will differ. We proceed to compute the variances of each estimator.

First, note that can be re-written as

| (16) |

, where is the Bernoulli random variable with , and if . Without loss of generality, here we additionally assume that has zero mean to further simplify the notational complexity. The proof also holds for the non-zero mean case trivially. Therefore, note also that is independent from , we have

holds for all and all treatments and . Similarly, we have .

Therefore, it is not hard to show that , and , which implies . Thus, we have:

Since , we have

. Therefore

Since has zero mean and variance and is independent of as in Assumption A, this expression be further simplified as, according to the rules of variance of the product of independent variables:

Where the third equality is due to the fact that . Therefore, we finally conclude that the variances of the error estimators will satisfy

,

∎

Appendix B Additional details for experiment

B.1 Implementation details

Csuite dataset

The csuite dataset used in Section 5.1 is an assortment of synthetic datasets first developed by [Geffner et al., 2022], for the purpose of evaluating both causal inference and discovery algorithms. They contain datasets ranging from small to medium scale (2-12 nodes), generated through carefully constructed Bayesian networks with additive noise models. All dataset in the collection includes a training set with 2,000 samples and 1 or 2 intervention or counterfactual test sets. The intervention test sets consist of factual variables, factual values, treatment variable, treatment value, reference treatment value, and an effect variable. More specifically, our three datasets corresponds to the following datasets:

-

1.

nonlin_simpson (csuite_1): An example of Simpson’s Paradox [Blyth, 1972] using a continuous SEM. The dataset is constructed so that has the opposite sign to . Estimating the treatment effects correctly in this SEM is highly sensitive to accurate causal discovery.

The structural equations are

(17) (18) (19) (20) where and are mutually independent and independent of , is the softplus function. Constants were chosen so that each variable has a marginal variance of (approximately) 1.

-

2.

chain_lingauss (csuite_2): Simulated from the graph with linear relationship. Ensure , and have same standard deviation (1), then this turns into structural equations:

-

3.

fork_lingauss (csuite_3): Simulated from the graph with linear relationship. Turns into structural equations:

Causal model details for Section 5.2

In Section 5.2, We include a wide range of machine learning-based causal inference methods to evaluate the performance of causal error estimators. They can be roughly divided into 4 categories: double machine learning methods, doubly robust learning methods, ensemble causal methods, and orthogonal methods. All methods are implemented using EconML [Battocchi et al., 2019], as detailed below:

-

1.

DML Linear: A linear double machine learning model [Chernozhukov et al., 2018], which uses an un-regularized final stage linear model for heterogenous treatment effect. Given that it is an unregularized low dimensional final model, this class also offers confidence intervals via asymptotic normality arguments. Random forests with default settings are used for first stage estimations.

-

2.

DML Kernel: kernel DML with random Fourier feature approximations [Nie and Wager, 2021] and uns a ElasticNet regularized final model. Random forests with default settings are also used for first stage estimations. Others configs are kept as default.

-

3.

Causal Forest causal random forest (or forest DML) [Wager and Athey, 2018, Athey et al., 2019]. We set the number of estimators to 100, number of minimum samples of leaf to 10, The number of samples to use for each subsample that is used to train each tree as 0.5. The others are kept as default. For effect and outcome models, we use Lasso with cross-validation.

-

4.

DR Linear doubly robust learning with a final linear model. Regression model for is set to random forest models. The propensity model is set to a logistic regression model.

-

5.

DR Forest doubly robust learning with subsampled honest forest regressor. Regression model for is set Gradient Boosting Regressor;and the propensity model is set to a random forest classifier. For other hyperparameters we set the minimum number of samples required to be at a leaf to be 10,and the minimum weighted fraction of the sum total of weights required to be at a leaf node to be 0.1.

-

6.

Ortho Forest: orthogonal forest learning, a combination of causal forests and double machine learning that allow for controlling for a high-dimensional set of confounders, while at the same time estimating non-parametrically the heterogeneous treatment effect on a lower dimensional set of variables. We use Lasso with cross-validation as the estimator for residualizing both the treatment and the outcome at each leaf; and switch to weighted Lassos at prediction time. Readers may refer to the official documentation for more details, as well as discussions on the difference between this method and causal forest.

-

7.

DR Ortho Forest: doubly robust orthogonal forest, a variant of the Orthogonal Random Forest that uses the doubly robust moments for estimation as opposed to the DML moments. Similarly, we use logistic regression models for residualizing the treatment at each leaf for both stages; and Lasso with cross-validation for the corresponding esimators for residualizing the outcomes. At prediction time, we switch to weighted Lasso instead.

Evaluation metrics

Throughout all experiments, We measure the performance of the estimators by the following metrics: the variance, the bias, and the MSE of the causal error estimation. More concretely, with a slight abuse of notation, let denote the estimated causal error (from any estimation method). Then, the evaluation metrics are defined as:

All expectations are taken over the treatment assignment plans . In practice, we draw 100 random realizations of treatment assignments and estimate all three metrics.

B.2 Additional results

Full results for causal error estimator metrics including linearly-modified IPW