2 Formulation of the optimal stopping problems

We begin with some necessary notation. For the sake of consistency, we shall follow the same notation used in Gapeev and Shiryaev ([5]).

1.

Given a probability space , let the measure be defined, for any , as

| (2.1) |

|

|

|

where is a random variable taking values in with and . Let the measure be defined as and let the measure be defined as .

Suppose that we observe a process whose dynamics are given by the solution to the SDE in (1.1). With the exception of Section 5, we shall assume throughout the present paper that the signal-to-noise ratio, defined as

| (2.2) |

|

|

|

is non-constant. We shall also assume that Assumption 2.1 below holds throughout the sequel.

Assumption 2.1.

Let be a domain in .

(1). The functions and are continuously differentiable in . Further, for any , .

(2).

For either or , the SDE (1.1) admits a unique solution in . Moreover, strictly increases to almost surely as .

Part (1) of Assumption 2.1 offers a slight generalization of the work of Gapeev and Shirayev ([5]), where is assumed to be .

Part (2) of Assumption 2.1 will be invoked to guarantee that the likelihood ratio will either tend to infinity or tend to 0 when the waiting time tends toward infinity.

2.

Being based upon the continuous observation of , the problem is to sequentially test the two

hypotheses and with minimal loss where

|

|

|

We achieve this task by considering a sequential decision rule

, where is a stopping time of the observation process (i.e. a stopping time with respect to the natural filtration for ) and is an -measurable function taking values in . After we stop observing the process at time , the decision function delineates which hypothesis should be accepted: if , we accept and if , we accept The set of all admissible decisions can be written as

|

|

|

Our objective now is to find the optimal which minimizes the risk function

| (2.3) |

|

|

|

where and is a given constant. In the above equation, the combination

is the probability of wrong detection and the term is the expected waiting time.

3. As in [5, 10], we solve the equivalent optimal stopping problem which arises after performing an appropriate change of measure to the observed process .

A key observation in both [5] and [10] is that

the optimal decision at time satisfies

| (2.4) |

|

|

|

where the likelihood ratio is defined as

| (2.5) |

|

|

|

The form of the optimal decision in (2.4) results from minimizing the probability of false detection given by (2.3). The class of admissible decisions reduces to

|

|

|

The set S is thus to be interpreted as the subset of D for which (2.4) holds. The expression in (2.4) enables us to rewrite the risk function in (2.3) as

| (2.6) |

|

|

|

The nonlinear Wiener sequential testing problem may now be formulated as the following optimal stopping problem (OSP).

OSP 1: Find a such that

| (2.7) |

|

|

|

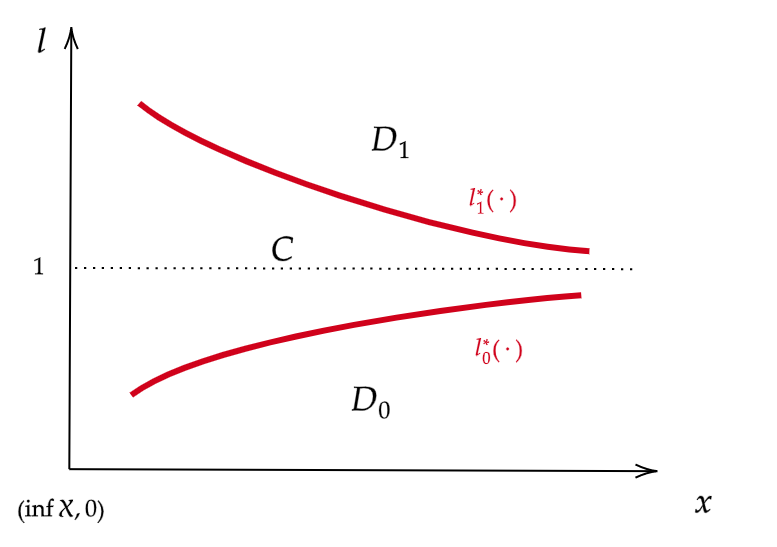

As noted in Section 1, the optimal stopping problem in (2.7) was first solved by Gapeev and Shiryaev ([5]). It is proven (see Lemma 3.1 therein) that the optimal stopping time for this optimal stopping problem satisfies

| (2.8) |

|

|

|

for some appropriate functions independent of . We refer the reader to [5] for further details.

4. With the above preparation in hand, we turn to the formulation of the minimax Wiener sequential testing problem. The objective of the minimax formulation is to minimize the performance functional in the worst case scenario of all prior distributions . This leads to the following optimal stopping problem.

OSP 2: Find a such that

| (2.9) |

|

|

|

In the above equality, the “worst case scenario” for corresponds to taking the supremum (over all ) of .

5. In order to solve the optimal stopping problem in (2.9)

by the saddle point property, we will need to find an optimal couple satisfying, for any and ,

| (2.10) |

|

|

|

The first inequality in (2.10) states that is the least favorable priori distribution given the stopping time . The second inequality in (2.10) asserts that is the solution for the optimal stopping problem with initial value . By (2.8), it follows that

|

|

|

where and are determined by the optimal stopping boundary in (2.7).

This paper’s key result for the minimax Wiener sequential testing problem, given by Theorem 4.1, is that there exists a which is the least favorable distribution for the stopping time . However, before embarking on this problem, we must first return to the nonlinear Wiener sequential testing problem in (2.7).

5 The case of constant SNR

In all of the previous sections, we have assumed that the signal-to-noise ratio

|

|

|

is non-constant. We will now assume, for all , that the signal-to-noise ratio is constant and equal to . We proceed to consider the minimax Wiener sequential testing problem in (2.9) under the assumption of constant SNR. Trivially, Assumption 3.1 and Assumption 3.2 from Section 3 are now irrelevant.

In order to derive the form of the least favorable distribution, we will consider a generalized performance functional defined as

|

|

|

where is a smooth running cost function of the likelihood ratio.

When , the performance functional reduces to the performance functional in (2.3).

In the setting of constant SNR, the likelihood ratio process (as defined in (3.3)) is a strong Markov process. The optimal decision for the optimal stopping problem can then be determined entirely by the likelihood ratio process .

In order to minimize the probability of false detection, we select the decision as in (2.4). Moreover, note that , and are all independent of . This leads us to formulate the following performance functional independent of and

|

|

|

The minimax Wiener sequential testing problem

in this case then reduces to the following optimal stopping problem.

OSP 3: Given , find a such that

| (5.1) |

|

|

|

We proceed to solve the optimal stopping problem in (5.1). We break up the solution into two intermediate steps.

(1) Optimal strategy. Suppose, for some , that the initial value of is . We would then seek to find the optimal stopping time for the following optimal stopping problem

| (5.2) |

|

|

|

The candidate optimal stopping time to be verified is the stopping time .

Using standard tools from the theory of optimal stopping for diffusions (see [10]), the form of can be found from the following free-boundary problem

| (5.3) |

|

|

|

where

|

|

|

We proceed by defining the function

|

|

|

which is the solution to

|

|

|

It is straightforward to see that if , we have, for some ,

|

|

|

The boundary conditions then become

|

|

|

from which the explicit value of can be identified for given and . If on , we may then apply Itô’s formula. The stopping time defined by

|

|

|

will then be optimal.

(2) Verification of least favorable distribution. To verify that is optimal for the optimal stopping problem in (5.1), it is equivalent to check that, for all , the following inequality holds

|

|

|

Lengthy but straightforward calculations yield

|

|

|

We then have that is the maximum point of if and only if

| (5.4) |

|

|

|

Note that, for ,

|

|

|

For ,

|

|

|

By the mean-value theorem, there exists a such that (5.4) holds. Theorem 5.1 below then immediately follows.

Theorem 5.1.

Suppose the following free-boundary problem

|

|

|

admits a solution . Then solving (5.4) is a least favorable distribution and the stopping time is optimal for the optimal stopping problem in (5.1).

5.1 The Case where both SNR and are constant

We now examine the special case where both SNR and are constant. In this case, we can explicitly find a closed form solution for the least favorable distribution.

Proposition 5.2 (Symmetric case when SNR is a constant).

Suppose the following free-boundary problem

|

|

|

admits a solution . If for any , then is a least favorable distribution and the first exit time of from is optimal for the optimal stopping problem in (5.1). When is constant, the free boundary problem admits a solution and is the least favorable distribution.

Proof.

We begin by verifying that (5.4) holds for in the symmetric case. We claim that

Recall that is the solution to the optimal stopping problem

|

|

|

We have

| (5.5) |

|

|

|

Since the probability law of the likelihood ratio process under is same as the probability law of under the measure ,

|

|

|

We then have that , which indicates that . Plugging the equality into (5.4) with , we see that

|

|

|

This says that is the least favorable distribution.

When is constant, Peskir and Shiryaev [10, p. 290] prove that the free boundary problem has a unique solution. We may thus conclude that is the least favorable distribution in the case of constant SNR and constant . This completes the proof.

Acknowledgements Philip A. Ernst gratefully acknowledges support from the Army Research Office (ARO-YIP-71636-MA), the National Science Foundation (DMS-2311306), the Office of Naval Research (N00014-21-1-2672), and the Royal Society Wolfson Fellowship (RSWFR2222005). Hongwei Mei gratefully acknowledges support the Simons Foundation’s Travel Support for Mathematicians Program (No. 00002835).

References

-

[1]

-

[2]

Ernst, P.A., Peskir, G., & Zhou, Q. (2020). Optimal real-time detection of a drifting Brownian coordinate. The Annals of Applied Probability, 30(3), 1032–1065.

-

[3]

Ferreyra, G., & Sundar, P. (2000). Comparison of solutions of stochastic equations and applications. Stochastic Analysis and Applications, 18(2), 211–229.

-

[4]

Gapeev, P.V., & Peskir, G. (2004). The Wiener sequential testing problem with finite horizon. Stochastics and Stochastic Reports, 76(1), 59–75.

-

[5]

Gapeev, P.V., & Shiryaev, A.N. (2011). On the sequential testing problem for some diffusion processes. Stochastics, 83(4-6), 519–535.

-

[6]

Johnson, P. & Peskir, G. (2018). Sequential testing problems for Bessel processes. Transactions of the American Mathematical Society, 370(3), 2085–2113.

-

[7]

Johnson, P., Pedersen, J.L., Peskir, G., & Zucca, C. (2022). Detecting the presence of a random drift in Brownian motion. Stochastic Processes and their Applications, 50, 1068–1090.

-

[8]

Karatzas, I., & Shreve, S. E. (1998). Brownian Motion and Stochastic Calculus. Springer.

-

[9]

Lehmann, E.L. (1959)

Testing Statistical Hypotheses. John Wiley & Sons.

-

[10]

Peskir, G. & Shiryaev, A.N. (2006).

Optimal Stopping and Free-Boundary Problems. Lectures in

Mathematics, ETH Zürich, Birkhäuser.

-

[11]

Shiryaev, A.N. (1978). Optimal

Stopping Rules. Springer-Verlag.

-

[12]

Wald, A. (1948). Sequential Analysis. Wiley.

Appendix A Appendix: Proof of Theorem 3.3

The purpose of this appendix is to prove Theorem 3.3 from Section 3. We need only prove the theorem under Assumption 3.1 as the proof of Theorem 3.3 under Assumption 3.2 is completely symmetric. For the sake of convenience, in the sequel, we shall omit the superscript 0 in or .

We begin with the proof of Statement (I) of Theorem 3.3. For ease of exposition, we shall split the proof into several intermediate steps.

(1) Time-change.

Let us define by

|

|

|

Note that is strictly increasing and is uniquely defined. Let

and

It is straightforward to see that

Employing Itô’s formula, we obtain

| (A.1) |

|

|

|

where is a standard Brownian motion under the measure by its Lévy characterization.

Then the optimal stopping problem in (3.7) is equivalent to

| (A.2) |

|

|

|

where , , is the set of stopping times of , and the subscript under stands for the initial value of . Since is an exponential martingale, almost surely as . For simplicity, we write and . The infinitesimal generator of is given by

|

|

|

We proceed to study the optimal stopping problem in (A.2), which has the same optimal stopping boundary as the optimal stopping problem in (3.7). We begin with Lemma A.1 below.

Lemma A.1.

The following three statements hold:

(1) The random variable is exponentially distributed with mean 1 under .

(2) It follows that

| (A.3) |

|

|

|

(3) Let

|

|

|

Then for any ,

converges to 0 uniformly in as .

Proof.

(1). Note that

|

|

|

The right-hand side is exponentially distributed with mean 1.

(2). Equation (A.3) holds by a straightforward calculation from statement (1).

(3). Note that . It follows that

|

|

|

Given any , it immediately follows that as . Further note that is increasing with respect to . This yields uniform convergence on any finite interval .

(2) Optimal stopping time. We fix and consider the optimal stopping problem

| (A.4) |

|

|

|

By the Feller property of the process , it is easy to see that, for all , is a continuous function of . Employing Lemma A.1, we have

| (A.5) |

|

|

|

The above implies that is a Cauchy sequence in for any finite open subset . We now let . By Statement (3) in Lemma A.1, is also a continuous function and, for any ,

converges to uniformly on .

We now wish to find the optimal stopping time for using the sequence of optimal stopping times for . To this end, we write

|

|

|

We also write

|

|

|

Further, let us denote

|

|

|

with . For any triple with , we have that, for ,

|

|

|

This means that increases as either increases or decreases.

Let almost surely. Employing the Snell envelope (see, for example, [10, Theorem 2.2]), we have that

|

|

|

is a martingale. We proceed by writing

| (A.6) |

|

|

|

where we have used the fact that As both and , the last equality in (A.6) tends to

|

|

|

Invoking the finiteness of , we conclude that is an optimal stopping time.

We now wish to verify that coincides with . Recalling Statement (3) in Lemma A.1, we proceed to calculate

|

|

|

Note that almost surely and that is bounded and converges to for any fixed as .

Letting both and , we have . This means that almost surely and thus almost surely.

(4) Optimal stopping boundary. We now turn to a study of the properties of the optimal stopping boundary. We begin with Lemma A.2 below.

Lemma A.2.

The following two statements hold.

(1). For each fixed , is concave on .

(2). If and , .

Proof.

(1) For each fixed , is linear with respect to the initial value . Further, and are concave with respect to and is concave on . The desired result then follows.

(2)

Note that is increasing on . Since is increasing with respect to and , the result holds by invoking the comparison of the solutions of stochastic differential equations in [3, Theorem 1].

We continue with Proposition A.3 below.

Proposition A.3.

The line belongs to the continuation region . It then follows that .

Proof.

Recall that . Employing the change-of-variable formula for and invoking the optional sampling theorem, we have

|

|

|

where is the local time of on the curve , i.e.

|

|

|

We now define

|

|

|

where and .

We claim that there exists and (independent of ) such that, for ,

| (A.7) |

|

|

|

Assuming the claim in (A.7) holds, we would then have that for any ,

|

|

|

For small values of , since , . This means that the line belongs to the continuation region . Now all that remains is to prove (A.7) as claimed. However, the proof of (A.7) is exactly the same as that of (8.6) in [2], and is thus omitted. This completes the proof.

The stopping region is divided into two separate parts:

and .

Recall the definition of in (3.8). The monotonicity of the optimal stopping boundary is now proven in Proposition A.4 below.

Proposition A.4.

The optimal stopping boundary is increasing in . The optimal stopping boundary is decreasing in .

Proof.

Note that for , we have

|

|

|

By the monotonicity of , we have that . This means that is decreasing.

If , then for all . The optimal stopping problem of interest then becomes

|

|

|

Since on , instantaneous stopping

is optimal. Note that on is concave and, for , . Then for any such that , we have that , i.e. . Together with the definition of , we have that if , then the pairs (with and ) belong to as well. Therefore, must be increasing. This concludes the proof.

We have now finished the proof of Statement (I) of Theorem 3.3. We now continue with the proof of Statement (II) of Theorem 3.3.

(3) Probabilistic regularity of the optimal stopping boundary. We need only show Statement (II) of Theorem 3.3 for the case , as the proof for all other cases is completely identical. Recall that

| (A.8) |

|

|

|

For some , let

| (A.9) |

|

|

|

and

|

|

|

Note that is continuous and strictly increasing. Itô’s formula then implies that

| (A.10) |

|

|

|

By the monotonicity of , for any , it is straightforward to see that belongs to if and . It then follows from (A.10) that, for any ,

| (A.11) |

|

|

|

For any , we have that for small , there exists such that . We may thus write

|

|

|

Noting that if and with , it follows that

| (A.12) |

|

|

|

We now combine (A.11) and (A.12). Since was assumed to be arbitrary, it follows that, for any ,

. This yields probabilistic regularity of the optimal stopping boundary, as desired.

We finish the Appendix with the proof of Statement (III) of Theorem 3.3.

It is straightforward to note that

|

|

|

where is the optimal stopping time for the optimal stopping problem in (2.7) with initial value .

This completes the proof of Theorem 3.3.