Optimal Monotone Mean-Variance Problem in a Catastrophe Insurance Model

Abstract

This paper explores an optimal investment and reinsurance problem involving both ordinary and catastrophe insurance businesses. The catastrophic events are modeled as following a compound Poisson process, impacting the ordinary insurance business. The claim intensity for the ordinary insurance business is described using a Cox process with a shot-noise intensity, the jump of which is proportional to the size of the catastrophe event. This intensity increases when a catastrophe occurs and then decays over time. The insurer’s objective is to maximize their terminal wealth under the Monotone Mean-Variance (MMV) criterion. In contrast to the classical Mean-Variance (MV) criterion, the MMV criterion is monotonic across its entire domain, aligning better with fundamental economic principles. We first formulate the original MMV optimization problem as an auxiliary zero-sum game. Through solving the Hamilton-Jacobi-Bellman-Isaacs (HJBI) equation, explicit forms of the value function and optimal strategies are obtained. Additionally, we provides the efficient frontier within the MMV criterion. Several numerical examples are presented to demonstrate the practical implications of the results.

Mathematics Subject Classification (2020) 49L20 · 91G80

Keywords. Optimal reinsurance Monotone mean-variance criterion Zero-sum game Shot noise process Catastrophe insurance

1 Introduction

Large-scale disasters, especially natural catastrophes, have the potential to result in numerous injuries, fatalities, and substantial economic losses. For insurance companies, the occurrence of such catastrophic events significantly amplifies their exposure to claims within a short time. In recent times, some insurance firms have introduced specialized catastrophe insurance tailored to specific natural disasters. Therefore, the management of catastrophic risk has assumed an increasingly pivotal role within the insurance industry. In practice, insurance companies often establish a bankruptcy remote entity known as a Special Purpose Vehicle (SPV). They purchase reinsurance from the SPV through continuous premium payments. When a catastrophe occurs, the SPV partially compensates the insurance company for its losses. Simultaneously, the SPV packages and securitizes this catastrophic risk as catastrophe bonds, selling them to investors. These catastrophe bonds, whose risk depend on disaster events and often displays low correlation with financial market, become attractive risk diversification assets among investors.

Typically, optimal reinsurance problems model the insurer’s surplus process using the Cramér-Lundberg risk model. However, catastrophe insurance claims differ significantly from those in traditional insurance models. Catastrophes lead to an immediate surge in claims, and even after the event, the repercussions persist and gradually recede over time. Furthermore, the frequency of ordinary claims rises in tandem with the severity of the catastrophe(see [3] for more details). To capture this phenomenon, we employ a Cox process, to model the occurrence process of ordinary claims whose intensity is a stochastic process following a shot-noise process, which represents the occurrence and receding of the catastrophe. While this model has been applied in asset pricing (see [12], [25], [12], [24], [18], [37], [39] and [19]), it has received limited attention in the context of catastrophe insurance optimization. [17] first considered the optimal investment and reinsurance problem for the shot-noise process. They used the diffusion approximation of the shot-noise process introduced by [13] to optimize the terminal wealth under the classical MV criterion. [2] minimized the risk of unit-linked life insurance by hedging in a financial market driven by a discontinuous shot-noise process. [4] investigated the optimal investment and reinsurance problem for a Cox process. In their model, the intensity of the claim arrival process is modelled by a diffusion process. The objective was to maximize the expected exponential utility of its terminal wealth. The value function and optimal strategy were provided via the solutions to backward partial differential equations. [6] considered the self-exciting and externally-exciting contagion claim Model under the time-consistent MV criterion with a model first introduced by [14]. Therefore, existing research primarily focuses on continuous-time models or diffusion approximation models. The optimization problem of catastrophe models with pure jump settings in both the claim process and the intensity process, especially under the emerging MMV criterion, remains an under-explored topic of study.

In this paper, we address this issue by considering an insurer managing both ordinary and catastrophe insurance claims under the MMV criterion within a Black-Scholes financial market framework. The insurer faces potential claims, which fall into two categories: ordinary claims and catastrophe claims. The modeling of ordinary aggregate claims involves the use of a Cox process, wherein the intensity process takes the form of a shot noise process. Simultaneously, catastrophe claims are modeled using a compound Poisson process, sharing the same Poisson counting process as the intensity of ordinary claims. This implies that catastrophe claims and the impact of disasters occur concurrently. We make an assumption that the sizes of catastrophe claims are proportional to the effect of the catastrophe, represented as the jump of the shot noise process. Specifically, ordinary claims are expressed as:

where is a Cox process with intensity process . denotes the size of the -th claim, with the claim sizes being independent and identical distributed. The intensity process is defined as

Here, is a Poisson process with a constant intensity , and are also identically and independently distributed random variables. The shot-noise process is used to describe the occurrence and receding pattern of the catastrophes. represents the impact of the -th catastrophe, and it decays exponentially with the factor . In practice, the intensity tends to be relatively low due to the infrequent occurrence of catastrophes. We introduce a constant scale factor , thus denotes the size of the -th catastrophe claims, resulting in the aggregate catastrophe claims process:

Consequently, the total risk assumed by the insurer is given by:

Despite the successful application of the MV criterion in finance and economics, it has a notable drawback of lacking monotonicity. In other words, situations may arise where but , where represents the investor’s risk aversion parameter. To address this limitation, [31] introduced the MMV criterion, which serves as the nearest monotonic counterpart to the MV criterion. Interestingly, the MMV criterion aligns with the classical MV criterion within its domain of monotonicity. While there are relatively few studies in the literature related to the MMV optimization criterion, some researchers have ventured into this area. For example, [35] explored this criterion in a continuous-time framework, assuming that coefficients of stock prices are random as functions of a stochastic process. They focused on the discounted terminal wealth process under the MMV criterion, obtaining optimal portfolio strategies and value functions under specified coefficient conditions. In our earlier research works, [28] and [29], we delved into the MMV optimization criterion within the context of investment and reinsurance problems. Specifically, we explored this criterion in two distinct scenarios: the diffusion approximation model and the Cramér-Lundberg risk model. It is noteworthy that we made an observation regarding the optimal strategies in these two frameworks that these optimal strategies align with those derived for the classical MV problem. In a significant contribution, [34] and [36]111[36] shows that the optimal wealth processes of MMV problems are identical to that of MV problems under a certain condition which is applicable for continuous assets processes (see [16]). extended this understanding by demonstrating that for a broad class of portfolio choice problems, when risky assets are continuous semi-martingales, the optimal portfolio and value function under the classical MV criterion and the MMV criterion are equivalent, which is not the case in our present paper, since the catastrophe claim process is not continuous. To the best of our knowledge, no research has explored the optimization strategies under the MV or MMV criteria in the context of discontinuous catastrophe models.

In light of these gaps, our paper focuses on an optimal reinsurance problem encompassing both ordinary and catastrophe insurance claims, operating under the MMV criterion. This model allows the insurer to invest within a Black-Scholes financial market. To mitigate claim-related risks, the insurer has the option to purchase reinsurance for both ordinary and catastrophe insurance from SPV. For analytical simplicity, we confine the reinsurance format to proportional reinsurance. The optimal MMV problem takes the form of a max-min problem. Initially, the objective is to minimize it by selecting an alternative probability measure that is absolutely continuous (though not necessarily equivalent) with respect to the reference probability measure . Subsequently, the objective is maximized by determining the optimal insurer strategies. To facilitate this complex analysis, we adopt a procedure similar to [28] in which the alternative probability measure is replaced by its conditional expected Radon-Nikodym derivative with respect to the reference probability measure. Despite the inherent challenge of absolute continuity (not equivalence), this approach enables us to represent the conditional expected Radon-Nikodym derivative as the solution to a stochastic differential equation (see [29]). This reformulation converts the original optimal MMV problem into a two-player non-zero sum game, incorporating the conditional expected Radon-Nikodym derivative into the state processes. We leverage dynamic programming techniques to address this auxiliary problem, deriving the explicit solution to the Hamilton-Jacobi-Bellman (HJB) equation after rigorous calculations. Additionally, we provide the efficient frontier for the MMV problem involving catastrophic insurance.

The structure of the paper is organized as follows: In Section 2, we formulate the insurance model and introduce the MMV criterion. Subsequently, we transform the MMV maximization problem into an auxiliary zero-sum game problem. Employing dynamic programming, we derive the HJBI equation satisfied by the value function. In Section 3, we further solve the HJBI equation, demonstrating that the candidate value function and strategies indeed represent the optimal value function and corresponding strategies. Toward the end of this section, we provide the efficient frontier under the MMV criterion. In Section 4, we investigate the diffusion approximation model within the MMV criterion framework. Section 5 offers numerical examples and sensitivity analyses to illustrate our findings. Finally, Section 6 draws conclusions from our research.

2 Model Formulation

2.1 Insurance Model

Let be the real-world probability measure and be the surplus of an insurer, which operates both the ordinary insurance business and the catastrophe insurance business,

where is the premium rate at time . The aggregate claims of the insurer are composed of two parts, , denoting the ordinary aggregate claims, and , which represents the aggregate catastrophe claims. In the event of a catastrophe, there is an immediate surge in claims, which is characterized by the catastrophe claim process denoted as .

In traditional insurance literature, the aggregate claims process is typically assumed to follow a compound Poisson process. However, considering the impact of catastrophes, the frequency of ordinary claims should be contingent upon the occurrence of a catastrophe. The fixed intensity of the compound Poisson process is inadequate for capturing the dynamic nature of ordinary claim frequency. To address this limitation, we replace the constant intensity of with a stochastic process denoted as . Let represent the counting process for ; in this context, can be described as a doubly stochastic Poisson process, also known as a Cox process222For more details, we refer the readers to the works of [7], [1], [33], [5], [21], and [22].. .

Denote the shot noise process as follows333See [8], [9], [27], and [12].:

We employ to characterize the impact of catastrophes on the intensity of , where corresponds to the initial value, stands for the impact of the -th catastrophe, represents the total number of catastrophes occurring before time , denotes the time at which the -th catastrophe transpires, and signifies the exponential decay factor for .

Let

in which each represents the magnitude of the -th ordinary claim. Additionally, the premium rate is considered a random process, depends on the observations of within the interval . This is because the insurer has the capability to monitor the historical data of past catastrophes and evaluate their lasting effects to determine the pricing of catastrophe insurance products. At this point, is defined by

where is the intensity of , and denote the safety loadings of the insurer for ordinary claims and catastrophe claims, respectively. The integral forms of and are444We use to denote the space of positive real numbers, and to denote the space of non-negative real numbers.

and

The insurer has the option to acquire proportional reinsurance to mitigate both ordinary and catastrophic risks. We represent the safety loadings for reinsurance companies for ordinary and catastrophe claims as and , respectively. In this scenario, the managed surplus process evolves as:

where the two control variables, and , are the retention levels for ordinary claims and catastrophe claims, respectively.

We also allow the insurer to invest its wealth to a risky asset, the price of which at time is governed by a geometric Brownian motion given by

where and are constants, and represents a standard Brownian motion. The insurer is also allowed to allocate its wealth into a risk-free asset, the price of which at time follows the process:

where is a fixed interest rate. Let denote the amount that the insurer invests into the risky asset, then the insurer’s surplus process follows

| (1) |

We assume that the processes and random variables , , , and are mutually independent under the probability . Let be the completion of the -field generated by , , , and under and . By Proposition 3 of [26], the compensated random measures in probability space are given by

and

where and are distributions of and , respectively. For notational simplicity, we also denote

| (2) |

Thus, the differential equations for and can be written as

and

| (3) |

By substituting (3) into (1), the controlled surplus process of the insurer satisfies the following stochastic differential equation,

where are the control variables.

2.2 Monotone Mean-Variance Criterion

The insurer aims to choose some admissible strategies to maximize the terminal surplus under MMV criterion introduced by [31], that is,

| (4) |

where

and is a penalty function satisfying

and is an index to measure the risk aversion of the insurer. If the alternative probability measure is constrained in a subset of :

by applying the exponential martingale representation, we know that is the solution of the SDE:

| (5) |

where are some suitable process555 is an -adapted process, and for any fixed , and are -predictable processes. All of them should satisfy some integrable conditions such as Novikov’s condition. depending on the selection of (see [32] and [20] for more details). Specially, we can regard , and as control processes which have a one-to-one correspondence with .

In this paper, we do not constrain the chosen of in , hence is not necessarily positive almost surely for , and is not necessarily a standard exponential martingale. Fortunately, by using the tools of discontinuous martingale analysis in [26], [30] and [23], it can be proved that the exponential martingale representation (5) still holds and is a solution of (5) (see [29] for more details). In this case, , and can explode at the time that hits zero, but for any

, and should satisfy the following integrable condition for any integer :

| (6) |

We give the following example to illustrate this more clearly.

Example 2.1.

Let the intensity of , = 1 and define

and an alternative measure

Since is non-negative and square-integrable, and

we have . In this case,

Obviously, is not almost surely positive for . Moreover, we have

Define

then

We have . Note that on the set , we have

But for any , it satisfies the condition (6) that

2.3 Hamilton-Jacobi-Bellman-Isaacs Equation

Based on the above discussion, we now summarize the dynamics of , and below

| (7a) | ||||

| (7b) | ||||

| (7c) | ||||

and the original maximization problem is transformed to an auxiliary two-player zero-sum game as follows,

Problem.

Let

| (8) |

where represents . Player one wants to maximize with strategy over defined below and player two wants to maximize with strategy over defined below.

Notice that the starting time of Problem (4) is fixed at zero, and Problem (8) extended Problem (4) by letting the initial time become (see [28, 29] for more details). If there exist the optimal strategies and for Problem (8), then

Definition 2.1.

The strategy employed by player one is admissible if the following conditions are met: is an -adapted process, and and are -predictable processes such that (7a) is well-defined and satisfies . We denote the set of all admissible strategies as .

The strategy used by player two is admissible if the following conditions are met: is an -adapted process, and for any fixed , and are -predictable processes. These processes should satisfy the condition:

Additionally, the stochastic differential equation (7b) should have a unique solution, which is a nonnegative -adapted square integrable -martingale satisfying for . We use to represent the set of all admissible strategies .

We present the following verification theorem, whose proof closely follows the one of Theorem 2.2.2 in [38] and Theorem 3.2 in [32]:

Theorem 2.1.

(Verification Theorem) Suppose that is a function satisfying the following condition

| (9) |

where is the infinitesimal generator of given by

| (10) |

Then,

3 Value Function and Optimal Strategies

In this section, we shall first build a candidate solution to the HJBI equation (9) based on Proposition 3.1. Then We shall conduct an analysis of the optimal strategies. Subsequently, we shall demonstrate that the constructed candidate solution indeed represents the value function of Problem (4), and we will also provide its explicit form. At the end of this section, we shall present the efficient frontier for our problem. For the sake of clarity, we defer the proofs to Appendix A.

We show the main result for the optimal strategies and the value function as follows:

Theorem 3.1.

Assume the initial values , and . The value function for Problem (4) is given by

and the optimal feedback strategies are given as follows

where

and .

To achieve the aforementioned result, we employ a three-step approach. Firstly, we tackle Problem (8), and the outcomes shall be presented in Proposition 3.1. Problem (8) involves three processes, namely , , and . It is worthnoting that the insurer can only observe the surplus process and the intensity process . As serves as an auxiliary process introduced to facilitate problem-solving, it is unobservable. However, Proposition 3.1 provides expressions of the value function and the optimal strategies as functions of the auxiliary process . To remove the dependency on , we take the second step that establish a relationship between the processes and (see Lemma 3.1). Finally, in the third step, we can represent the value function and optimal strategies solely as functions of and (see Proposition 3.2).

Proposition 3.1.

For any , if there exist sufficiently smooth functions , , and satisfying the following differential equations, respectively666For any appropriate function , define as its finite difference on the spatial variable.

| (11) |

with boundry conditions , , , where

for all integrable function , then the solution to the HJB equation (9) is

| (12) |

Moreover, the corresponding optimal feedback strategies are given by

| (13) | |||||

We observe that the optimal feedback strategies (13) only depend on the auxiliary process rather than the surplus process . However is not observable in practice. To address this problem, we shall introduce a lemma which shows the relationship of and for any . Then we can rewrite the optimal feedbacks as functions that only depend on the current value of surplus process , and the initial values at time . Here is the lemma:

Lemma 3.1.

Let and be the state processes under the feedback strategies defined by (13), then for any , we have

| (14) |

Note that the process does not depend on the controls, we can easily calculate its value at any time . For simplicity, in the following context, we denote and . By substituting (14) into (12) and (13), we can rewrite the value function and the optimal strategies as follows:

Proposition 3.2.

For any , let and be the state processes under the feedback strategies defined by (13) and let and be the initial values at time , then the value function is given by

| (15) |

and the optimal strategies , and at time are given by:

| (16) |

It’s important to note that (15) and (16) also rely on . Keep in mind that is chosen as the initial time before time , implying that is, in fact, known. In conclusion, by setting the initial time of Problem (8) to be zero, and the initial values of Problem (8) to be , , and , we ultimately obtain the solution to the original Problem (4) (see Theorem 3.1). Furthermore, the optimal feedbacks in (13) solely rely on the current value of at time , making them time-consistent. However, as illustrated in (16), the strategies depend not only on but also on the values and at some time point in the past. Consequently, the optimal strategies presented in the form of (16) are precommitted.

Now, we give the explicit expressions of , , and by the following lemma.

Lemma 3.2.

Based on the above analysis and preparation, we are able to solve the HJBI equation (9). Hence, we can use the verification theorem to prove that the candidate function and the corresponding strategies are indeed the value function and the optimal strategies.

Theorem 3.2.

(Value function and optimal strategy) Assume the initial values and . The value function for Problem (8) is given by ,

| (20) |

and the equilibrium strategies are the precommitted feedback strategies

| (21) |

and

| (22) |

3.1 MMV Efficient Frontier

To simplify the notaitons, we introduce the following functions

and

where , , . Now we state the efficient frontier for the MMV criterion problem, and show the results for some special cases.

Theorem 3.3.

(Efficient Frontier) For initial values , and , letting represents , then the expected wealth process under is

Furthermore, the variance and expectation of the wealth process at time have the relationship:

| (23) |

Corollary 3.1.

The efficient frontier for the terminal wealth process is given by

Proof.

Let in (23). ∎

Corollary 3.2.

If there is no catastrophe in the model, i.e., is a constant and , then

4 Optimization Problem for the Diffusion Approximation Model

In this section, we consider the optimization problem under MMV for the diffusion approximation model. We take a parallel procedure as that of Section 2 and Section 3. In Subsection 4.1, we introduce the diffusion approximation model for the catastrophe insurance. In Subsection 4.2, we present the auxiliary problem, and by applying the dynamic programming principle, we gives the corresponding HJB equation. In Subsection 4.3, the optimal strategies and value function are obtained explicitly by solving the HJBI equation.

4.1 Diffusion Approximation of the Catastrophe Insurance

In [13], the diffusion approximation of the Cox-process driven by shot noise intensity is obtained. By Theorem 2 of [13], the diffusion approximation of the aggregate claims process and the intensity process are given by

and

where , , , and are defined by (2), and are two independent standard Brownian motions under probability .

In this section, we consider the MMV optimization problem under this diffusion approximation. Similarly, the surplus process is given by

Then the insurer’s surplus process after investment is given by

4.2 Hamilton-Jacobi-Bellman Equation

For the diffusion approximation model, the corresponding characteristic process is given by

The insurer aims to find the optimal strategies and such that for any admissible the objective function is maximized by and is minimized by , where

| (24) |

Recall that the processes , and satisfy the following SDE:

| (25a) | ||||

| (25b) | ||||

| (25c) | ||||

Definition 4.1.

We present the following verification theorem for the diffusion approximation case, the proof of which is similar to Theorem 2.1.

Theorem 4.1.

(Verification Theorem) Suppose that is a function satisfying the following condition

| (26) |

where is the infinitesimal generator of given by

| (27) | ||||

Then,

4.3 Solutions to the Diffusion Approximation Model

We take a similar procedure as that of Section 3 in this subsection. The explicit form of value functions and optimal strategies for the diffusion approximation model are also obtained. All the proofs in this section are delegated in Appendix B.

Theorem 4.2.

Assume the initial values , and . The value function for Problem (4) is given by

| (28) |

and the optimal feedback strategies are given as follows

where

To prove Theorem 4.2, we use a similar approach as in Section 3. We first find a candidate solution to the HJBI equation (26), then by Lemma 4.1 below, we provide expressions of value function and optimal strategies independent of process , only as functions of and . Finally, by setting , and , we obtain the solutions to the original problem.

Proposition 4.1.

Consider the following partial differential equations

| (29) |

with boundry conditions , , . If there exist smooth enough solutions , and for the above PDEs such that, for all and , holds, then the solution to the HJB equation (26) is of the following form:

| (30) |

Moreover, the corresponding optimal feedback strategies is given by

| (31) | |||||

The optimal strategies (31) depend on the auxiliary process , which is not able to be observed in practice. Now we give an analogue of Lemma 3.1 to show the relationship between and .

Lemma 4.1.

Let and be the state processes under the feedback strategies defined by (31), then

| (32) |

Proof.

Note that the process does not depend on the controls, by substituting (32) into (30) and (31), we can derive the optimal feedback strategies as follows:

Theorem 4.3.

Let and be the state processes under the feedback strategies defined by (13), then for any , the value function is given by

| (33) |

and the optimal strategies , and at time satisfy

Next, we give the explicit forms of the solutions to (29).

Lemma 4.2.

By far, from the above analysis and computation, we are able to find the solution of HJBI equation (26):

Theorem 4.4.

(solution of HJBI equation) Assume the initial values and . The value function related to the diffusion approximation is given by as follows,

| (35) |

and the equilibrium strategies are precommitted feedback

| (36) |

and

| (37) |

5 Numerical Examples

In this section, we assume is exponentially distributed with parameter and is exponentially distributed with parameter . Other parameters are supposed to be

-

•

months is the time horizon of planning;

-

•

is the initial time;

-

•

are the monthly expected return rate and the expected volatility of the stock, respectively;

-

•

is the monthly return of the risk-free asset;

-

•

are the wealth of the insurer and the intensity of the ordinary insurance claims at the beginning;

-

•

is the factor of risk aversion in the MMV criterion;

-

•

are the safety loading of the insurer and reinsurer for the ordinary insurance claims (catastrophe insurance claims) respectively;

-

•

are the intensity and the decay factor of the shot noise process. These two parameters mean the frequency of the occurrence of the catastrophe and the speed at which the effects of the catastrophe recede, respectively;

-

•

is the ratio of the catastrophe claims size to the catastrophe impact.

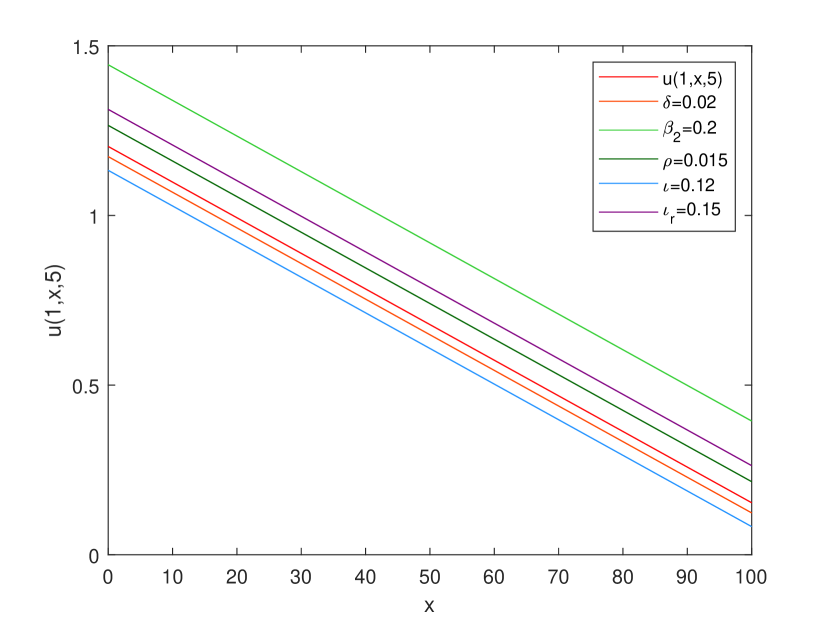

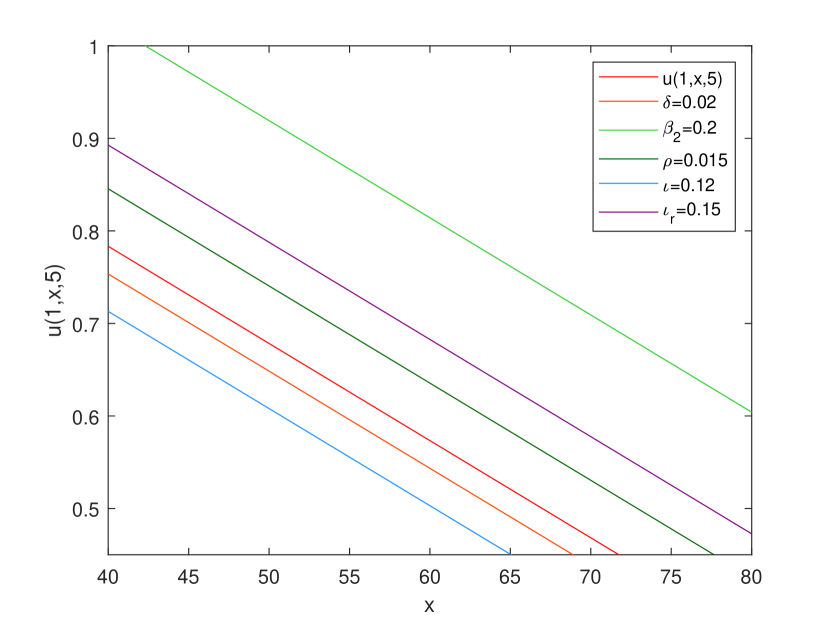

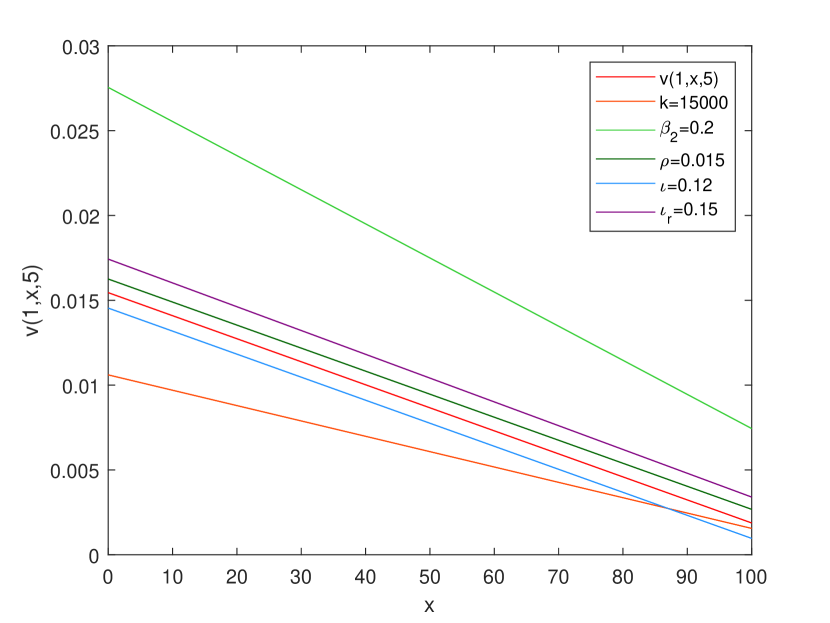

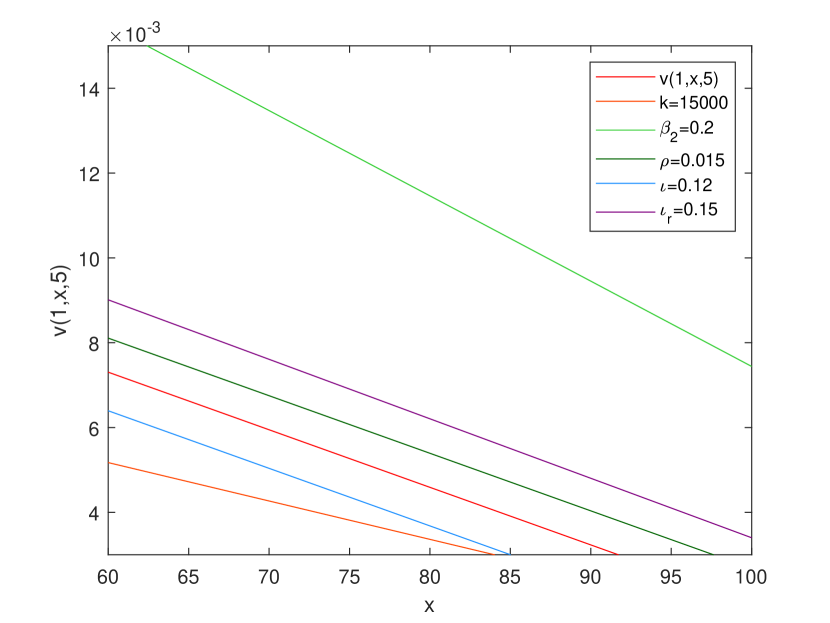

We have generated two graphs to visualize the sensitivity of the optimal strategies and , with respect to changes in catastrophe-related parameters. In Figs.1 and 2, the red lines depict the optimal strategies of ordinary claims and that of catastrophe claims as functions of the surplus under the given parameter values. Meanwhile, the other colored lines represent variations in the optimal strategies when one parameter is altered at a time.

In Fig.1, observe the green and dark green lines, which illustrate that as the frequency and intensity of catastrophes increase (indicated by larger values of or smaller values of ), the insurer adopts a more aggressive stance, leading to higher retention levels. This behavior can be attributed to the fact that with increased catastrophe frequency and intensity, the catastrophe insurance premium also rises, allowing the insurer to shoulder more risk.

In the same figure, the orange line shows that when the impact of a catastrophe fades more fast (corresponding to a larger ), the insurer adopts a more conservative approach with smaller retention levels. This is because the insurer’s ordinary insurance premium also diminishes more gradually for larger .

Fig.2 illustrates how the optimal strategy of catastrophe claims changes in response to variations in the parameters. The orange line indicates that a larger ratio results in reduced retention. Furthermore, the purple lines in both figures highlight that higher reinsurance costs lead to greater retained risks. Finally, the blue lines illustrate that increased reinsurance premium incentivize the insurer to adopt a more aggressive strategy.

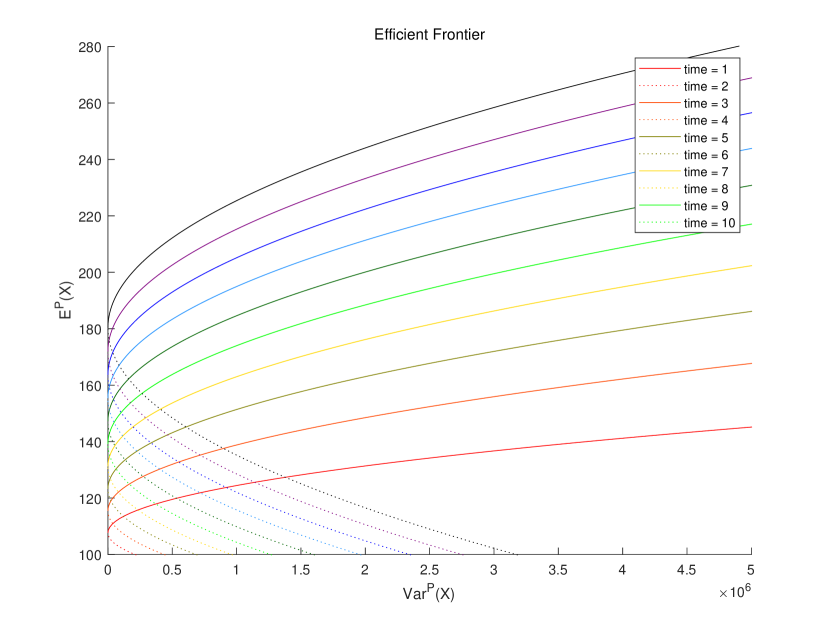

In Fig.3, we plot the efficient frontiers for this problem at different time points, where the top half of the parabolas are the efficient frontiers, from which one can clearly see that when the risk (variance) is given, the expected return becomes larger over time.

6 Conclusion

In this paper, we have studied the optimization problem of optimal investment and reinsurance for insurers facing catastrophic risks. Our study includes both jump models and diffusion approximation models, and the insurer’s primary goal is to maximize their terminal surplus under the MMV criterion. We first formulate the initial control problem as an auxiliary two-player zero-sum game, then find equilibrium solutions in explicit form through dynamic programming and solving an HJBI equation. Furthermore, we have presented the efficient frontier within the MMV criterion. Looking ahead, our future research endeavors may include: 1) integrating excess-of-loss reinsurance into the catastrophe model; 2) investigating scenarios where the insurer has access to only partial information about catastrophes, limiting their ability to design tailored premiums; 3) exploring games involving multiple insurance companies or games between insurers and SPVs; and more.

Funding: This work was supported by the National Natural Science Foundation of China 11931018 and 12271274.

Declarations

Conflict of interest: The authors have no relevant financial or non-financial interests to disclose.

References

- [1] M. S. Bartlett. The spectral analysis of point processes. Journal of the Royal Statistical Society Series B-methodological, 25(2):264–281, 1963.

- [2] J. Bi and J. Guo. Hedging unit-linked life insurance contracts in a financial market driven by shot-noise processes. Applied Stochastic Models in Business and Industry, 26(5):609–623, 2010.

- [3] P. Born and W. K. Viscusi. The catastrophic effects of natural disasters on insurance markets. Journal of Risk and Uncertainty, 33(1):55–72, 2006.

- [4] M. Brachetta and C. Ceci. Optimal proportional reinsurance and investment for stochastic factor models. Insurance: Mathematics and Economics, 87:15–33, 2019.

- [5] P. Bremaud. Point processes and queues, martingale dynamics. Journal of the American Statistical Association, 78(383):745, 1983.

- [6] J. Cao, D. Landriault, and B. Li. Optimal reinsurance-investment strategy for a dynamic contagion claim model. Insurance: Mathematics and Economics, 93:206–215, 2020.

- [7] D. R. Cox. Some statistical methods connected with series of events. Journal of the Royal Statistical Society Series B-methodological, 17(2):129–157, 1955.

- [8] D. R. Cox and V. Isham. Point Processes, volume 12. CRC Press, 1980.

- [9] D. R. Cox and V. Isham. The virtual waiting-time and related processes. Advances in Applied Probability, 18(2):558–573, 1986.

- [10] A. Dassios. Insurance, Storage and Point Processes: an Approach via Piecewise Deterministic Markov Processes. PhD thesis, 1987.

- [11] A. Dassios and P. Embrechts. Martingales and insurance risk. Communications in Statistics. Stochastic Models, 5(2):181–217, 1989.

- [12] A. Dassios and J. Jang. Pricing of catastrophe reinsurance and derivatives using the cox process with shot noise intensity. Finance and Stochastics, 7(1):73–95, 2003.

- [13] A. Dassios and J. Jang. Kalman-bucy filtering for linear systems driven by the cox process with shot noise intensity and its application to the pricing of reinsurance contracts. Journal of Applied Probability, 42(1):93–107, 2005.

- [14] A. Dassios and H. Zhao. A dynamic contagion process. Advances in applied probability, 43(3):814–846, 2011.

- [15] M. H. A. Davis. Piecewise-deterministic markov processes: A general class of non-diffusion stochastic models. Journal of the Royal Statistical Society Series B-methodological, 46(3):353–376, 1984.

- [16] F. Delbaen and W. Schachermayer. The variance-optimal martingale measure for continuous processes. Bernoulli, pages 81–105, 1996.

- [17] U. Delong and R. Gerrard. Mean-variance portfolio selection for a non-life insurance company. Mathematical Methods of Operations Research, 66(2):339–367, 2007.

- [18] M. Egami and V. R. Young. Indifference prices of structured catastrophe (CAT) bonds. Insurance: Mathematics and Economics, 42(2):771–778, 2008.

- [19] A. Eichler, G. Leobacher, and M. Szolgyenyi. Utility indifference pricing of insurance catastrophe derivatives. European Actuarial Journal, 7(2):515–534, 2017.

- [20] R. J. Elliott and T. K. Siu. Portfolio risk minimization and differential games. Nonlinear Analysis Theory Methods & Applications, 71(12):0–0, 2009.

- [21] J. Grandell. Doubly Stochastic Poisson Processes, volume 529. Springer, 2006.

- [22] J. Grandell. Aspects of Risk Theory. Springer Science & Business Media, 2012.

- [23] L. P. Hansen, T. J. Sargent, G. Turmuhambetova, and N. Williams. Robust control and model misspecification. Journal of Economic Theory, 128(1):45–90, 2006.

- [24] S. Jaimungal and T. Wang. Catastrophe options with stochastic interest rates and compound poisson losses. Insurance: Mathematics and Economics, 38(3):469–483, 2006.

- [25] J.-W. Jang and Y. Krvavych. Shot noise process and pricing of extreme insurance claims in an economic environment. Technical report, Working Paper, Actuarial Studies, UNSW, Sydrey, Australia, 2003.

- [26] J. M. Kabanov, R. Š. Lipcer, and A. Širjaev. Absolute continuity and singularity of locally absolutely continuous probability distributions. I. Mathematics of the USSR-Sbornik, 35(5):631, 1979.

- [27] C. Kluppelberg and T. Mikosch. Explosive poisson shot noise processes with applications to risk reserves. Bernoulli, 1:125–147, 1995.

- [28] B. Li and J. Guo. Optimal reinsurance and investment strategies for an insurer under monotone mean-variance criterion. RAIRO-Operations Research, 55(4):2469–2489, 2021.

- [29] B. Li, J. Guo, and L. Tian. Monotone mean-variance preference and optimal reinsurance problem for the Cramér-Lundberg risk model. Preprint.

- [30] R. Liptser and A. N. Shiryayev. Theory of Martingales, volume 49. Springer Science & Business Media, 2012.

- [31] F. Maccheroni, M. Marinacci, A. Rustichini, and M. Taboga. Portfolio selection with monotone mean-variance preferences. Mathematical Finance, 19(3):487–521, 2009.

- [32] S. Mataramvura and B. Øksendal. Risk minimizing portfolios and HJBI equations for stochastic differential games. Stochastics: An International Journal of Probability and Stochastic Processes, 80(4):317–337, 2008.

- [33] R. F. Serfozo. Conditional poisson processes. Journal of Applied Probability, pages 288–302, 1972.

- [34] M. S. Strub and D. Li. A note on monotone mean–variance preferences for continuous processes. Operations Research Letters, 48(4):397–400, 2020.

- [35] J. Trybula and D. Zawisza. Continuous-time portfolio choice under monotone mean-variance preferences-stochastic factor case. Mathematics of Operations Research, 44(3):966–987, 2019.

- [36] A. C̆Erný. Semimartingale theory of monotone mean-variance portfolio allocation. Mathematical Finance, 30(3), 2020.

- [37] A. J. Unger. Pricing index-based catastrophe bonds: Part 1: Formulation and discretization issues using a numerical PDE approach. Computers & Geosciences, 36(2):139–149, 2010.

- [38] D. W. Yeung and L. A. Petrosjan. Cooperative Stochastic Differential Games. Springer Science & Business Media, 2006.

- [39] M. Zonggang, M. Chaoqun, and X. Shisong. Pricing zero-coupon catastrophe bonds using EVT with doubly stochastic poisson arrivals. Discrete Dynamics in Nature & Society, 2017:1–14, 2017.

Appendix A Proofs of Statements in Section 3

A.1 Proof of Proposition 3.1

Proof.

We suppose that the form of solution to (9) is given as follows

| (38) |

Substituting (38) into (10) yields

| (39) |

By differentiating (39) with respect to , and and letting them equal , if holds, the minimum of (39) is attained at

Similarly, by differentiating (40) with respect to , and and letting it equals , if and hold, the maximum of (40) is attained at

By plugging , and back into (40), we obtain

By separation of variables, we get the partial differential equations (11) with the boundary conditions , and which are derived from .

∎

A.2 Proof of Lemma 3.1

A.3 Proof of Lemma 3.2

Proof.

It is easy to obtain that

| (43) |

Let us recall that satisfies

We hypothesize that it takes the following form

| (44) |

By substituting (44) into (11) and by separating the variables, we obtain the following two ordinary differential equations

The solutions are given as follows

For , we suppose it has the following form

| (45) |

Since

and

we have

∎

A.4 Proof of Theorem 3.2

Proof.

We first prove that the strategies and defined by (21) and (22) belong to and , respectively. By Theorem 13 (2) and Lemma 7 (2) of [26], the SDE (7b) has a unique solution in the class of nonnegative local martingales which we also denote by . Since is deterministic, bounded and satisfies

| (46) | |||

| (47) |

is a square integrable martingale. Consequently, .

On the other hand, since

it holds that

which proves that .

Let . We have

Since satisfies the HJBI equation, we obtain that

By letting , we obtain

A.5 Proof of Theorem 3.3

Proof.

1) and : By Feyman-Kac theorem, and are the solutions of the following PDE

with terminal values and , respectively. It is easy to obtain that

2) : To get this value, we first need to find the SDE that satisfies. By applying Itô’s lemma to , it follows that

Again by Itô’s lemma, we have

Denote by

Then satisfies

Note that is a stochastic exponential satisfying

we can define a new probability measure by

Under the probability measure , the following stochastic measure is a martingale

such that

Now the representation of under the new probability is as follows

By Feyman-Kac theorem,

is the unique probability solution of the following PDE,

| (48) |

We solve it to obtain

| (49) |

where

Therefore,

3) : We use the similar method as shown in 2). First by Itô’s lemma,

Let

Thus satisfies

and

Define a new probability measure by

The compensated Poisson process of under is given by

Moreover,

Hence the representation of under is as follows

By Feyman-Kac theorem,

is the unique probability solution of the following PDE

in other words,

where

Therefore

4) : It can also be obtained by using Feyman-Kac theorem that

| (50) |

is the unique probability solution of the following PDE

| (51) |

To solve the PDE, we suppose the form of . Recall that satisfies (48) and (49). By substituting into (51), we see satisfies

which gives

Hence,

Therefore

As a result, we obtian

Therefore

| (52) |

Since and are derived in the first part of the proof, we only need to compute the values of and .

Denote by

It follows from Theorem 10 and Theorem 11 in [26] that is a standard Brownian motion, and are the compensated compound Poisson processes with respect to and under probability measure . Thus,

and

Therefore, is a martingale under such that

By the same method in 1), we also have

As a result,

| (53) |

∎

Appendix B Proofs of Statements in Section 4

B.1 Proof of Proposition 4.1

Proof.

We suppose that the form of solution to (26) is as follows

| (54) |

If holds, we differentiate (55) with respect to , and and let them equal , respectively, then the minimum of (55) is attained at

Plugging , and back into (55) gives

| (56) |

B.2 Proof of Lemma 4.2

Proof.

It is easy to obtain that

| (57) |

For , we suppose that it has the following form

| (58) |

For , we have

The characteristic equation is given by

which has two solutions, namely,

where

If , then , and

thus

If ,

Since is a continuous function with boundary condition , we assert that for all . Factually, if , then, by its continuity, there exists a such that . In this case,

which is a contradiction. Hence

which gives

Moreover since , we have for all .

For , by integration, we have

If , we have

Hence

and

Therefore,

If , then

and

Thus can be simplified as

By integrating with respect , can be obtained as follows

To sum up, we have

where

We make the ansatz that has the following form

| (59) |

∎