Mean field optimization problems: stability results and Lagrangian discretization

Abstract.

We formulate and investigate a mean field optimization (MFO) problem over a set of probability distributions with a prescribed marginal . The cost function depends on an aggregate term, which is the expectation of with respect to a contribution function. This problem is of particular interest in the context of Lagrangian potential mean field games (MFGs) and their discretization. We provide a first-order optimality condition and prove strong duality. We investigate stability properties of the MFO problem with respect to the prescribed marginal, from both primal and dual perspectives. In our stability analysis, we propose a method for recovering an approximate solution to an MFO problem with the help of an approximate solution to an MFO with a different marginal , typically an empirical distribution. We combine this method with the stochastic Frank-Wolfe algorithm of [6] to derive a complete resolution method.

Keywords: optimization with probability measures, potential mean field games, non-atomic games, stability analysis, Frank-Wolfe algorithm.

1. Introduction

This article is dedicated to a general class of optimization problems involving probability measures with a prescribed marginal . We will refer to them as Mean Field Optimization (MFO) problems. These typically arise in multi-agent optimization problems, for which a mean-field formulation of the problem, involving the probability distribution of the decisions of the agents (rather than an enumeration of them), is not only meaningful but also provides us with convexity properties of great numerical interest.

The first ambition of our work is to provide a general framework for the formulation of such situations. For the sake of clarity, we introduce here the MFO problems investigated in this work. We refer the reader to Sec. 2.3 for a complete description of the required assumptions. Let and be two complete and separable metric spaces and let be a separable Hilbert space. Let be a closed subset of and let be a probability measure on . We consider the following problem, parametrized by :

| (Pm) |

where is a Borel measurable function and is a convex function. The admissible set is the set of all probability measures on whose marginal distribution on is . Our model allows for heterogeneity within the agents, which is modeled by some parameter . The decision variables of the agents are generically denoted by and the probability measure represents the distribution of the parameter-decision pairs of our agents. The distribution of the parameters of the agents is given by , that is why we impose that has its first marginal equal to . At an abstract level, we can interpret the term as a common good, obtained by aggregating the contributions of all the agents.

Motivation.

Our original interest for MFO problems comes from non-atomic games with a potential structure, for which finding a Nash equilibrium is equivalent to solving an MFO problem. Among these games, we have a special interest for Lagrangian Mean Field Games (MFGs), in which the agents each optimize the trajectory of some dynamical system and are parametrized by their initial condition. Problem (Pm) also arises in energy management problems, more specifically, in problems involving many small consumption (or production) units, for example electrical cars. For such problems, the common good is the total energy consumption, the parameter could model any relevant characteristic of the cars (such as their charging capacity) while the variable describes their charging profiles. Finally, let us mention that MFO problems find applications in supervised learning, more specifically in the training of neuron networks with one hidden layer: in the mean field approximation of such problems, the variable simply describes the probability distribution of the weights of the neurons [13, 24, 12]. For other applications of MFO problems in learning, we refer to [7, 13, 35] and the references therein.

Numerical approach

The numerical resolution of Problem (Pm) poses two main difficulties: the numerical manipulation of probability measures and the treatment of the marginal constraint. Let us focus on the first difficulty by supposing momentarily that is a Dirac measure located at some point , so that the problem (Pm) can simply be written as an optimization problem on . Unless is finite, is an infinite dimensional set. A first approach would consist in discretizing the set , which would preserve the convexity of the problem. This approach suffers from the curse of dimensionality, since it requires an exponential number of points with respect to the dimension of . A second approach would consist in representing the probability measure as the empirical mean of a set of points to be optimized. The clear drawback of this approach is the loss of convexity of the discretized problem; yet we mention that it proves efficient in the context of supervised learning problem [13]. In the general context of MFO problems, the Frank-Wolfe (FW) algorithm is a particularly advantageous algorithm. It produces a finitely supported approximate solution and leverages the convexity of the original problem (without using a coarse discretization of ). More specifically, it generates after iterations an -optimal solution supported by at most points.

Coming back to the case of a general marginal, we propose to discretize with an empirical measure associated with points and thus to solve:

| (P) |

This idea was already proposed in [30], in an MFG context. By the disintegration theorem, (P) is equivalent to a problem involving probability measures. A direct implementation of the FW algorithm would lead to an approximate solution possibly involving points after iterations of the algorithm. We will see that the Stochastic Frank-Wolfe algorithm, which we introduced and analyzed in [6], allows to obtain an approximate solution of (P) relying on only support points, to the price of an additional error term of order in the main convergence result. Let us mention that the Frank-Wolfe algorithm (also called conditional gradient method) was already applied to potential MFGs, see for example [16, 22, 23]. It can be seen as a generalization of the fictitious play, investigated in particular in [10, 20].

Theoretical results

At a theoretical level, we first establish a first-order necessary and sufficient optimality condition for (Pm) and an existence result, both relying on rather standard arguments. Then we perform a stability analysis of the problem with respect to the marginal . It is of course motivated by the need to understand the effect of the discretization of in the numerical approach described above. We provide a constructive method, which we call bridging method. It allows to construct an approximate solution to (Pm), given an approximate solution to the problem with a different (but close) marginal. This allows to prove that the value of problem (Pm) is Lipschitz continuous with respect to , for the Kantorovich-Rubinstein distance. Finally, we introduce a dual problem to (Pm) and prove that strong duality holds. We prove that the unique solution to the dual problem has a Hölder dependence with respect to .

Organization

In Section 2, we present some notations and results in measure theory and set-valued functions, as well as the rigorous description of the data of problem (Pm). Section 3 is dedicated to the primal problem: We provide a first-order optimality condition and an existence result. We perform in Section 4 a stability analysis for the primal problem, based on our bridging method. In Section 5, we formulate the dual problem of (Pm), we prove strong duality, and we prove the stability of the dual solution. We provide our numerical method in Section 6. We perform in Section 7 some numerical simulations for a Lagrangian MFG model taken from [18] and for a congestion problem.

2. Preliminaries

2.1. Results in measure theory

A metric space is called a Polish space if it is complete and separable. Let be a Polish space equipped with a metric , and let be a -algebra on . The Borel -algebra on is denoted by . Given any measure on , we refer to the triplet as a measure space. Measure spaces are said to be complete if for any with and for any subset of , we have . We define

Let denote the Dirac measure at point . We denote by the set of finitely supported probability measures, defined by

In particular, we call an empirical distribution if for .

The set is endowed with the narrow topology. We say that a sequence in narrowly converges to some if for any bounded and continuous function ,

The space is endowed with the Kantorovich–Rubinstein Distance,

where Lip is the set of all 1-Lipschitz continuous functions on . For any , the support of is defined by

| (2.1) |

Lemma 2.1.

Let . Let be a Borel measurable function. Assume that

Then , -a.e. Moreover, if is closed, then supp.

Proof.

The fact that , -a.e., is from [28, Thm. 1.39(a)]. Now, let be closed. Suppose that there exists such that . Since is closed, there exists an open neighborhood of such that , for all . By the definition of the support of a probability measure, we have . Therefore, , contradiction. ∎

2.2. Results about set-valued functions

In this subsection, we consider a metric space equipped with a metric , a -algebra on , and a measure on . Additionally, we fix a Polish space with a metric , and we denote the Borel -algebra on by . We call a set-valued function from to if for all , denoted by for short. The graph of is defined by

We say that has closed (non-empty) images, if for any , is closed (non-empty) in .

Let us give some definitions concerning regularity properties of set-valued functions, which are from [2, Def. 1.4.1, Def. 1.4.2, Def. 1.4.5, and Def. 8.1.1].

Definition 2.2.

Let be a set-valued function with non-empty images.

-

(1)

(Lower semi-continuity). The set-valued function is lower semi-continuous at point if for any and any sequence converging to , there exists converging to . The set-valued function is said to be lower semi-continuous if it is lower semi-continuous at each point .

-

(2)

(Upper semi-continuity). The set-valued function is upper semi-continuous at point if for any neighborhood of , there exists such that for any , we have

The set-valued function is said to be upper semi-continuous if it is upper semi-continuous at each point .

-

(3)

(Lipschitz continuity). When and are normed vector spaces, we say that is -Lipschitz continuous on , for some , if for any ,

Here denotes the closed ball in centered at with radius .

-

(4)

(Measurability). The set-valued function is measurable if the inverse image of any open subset of is measurable, i.e.,

An important property of measurable set-valued functions is the existence of measurable selections.

Theorem 2.3 (Measurable selection).

Let be a measurable set-valued function with non-empty images. Then has a measurable selection , i.e., is -measurable and for any .

Proof.

See [2, Thm. 8.1.3]. ∎

The following two lemmas will allow us to prove the measurability of some set-valued functions.

Lemma 2.4.

If is a set-valued function such that for any closed subset of , then is measurable.

Proof.

See [11, Prop. III.11]. ∎

Lemma 2.5.

Let be a complete measure space, with a positive measure such that . Then any set-valued mapping is measurable if and only if belongs to .

Proof.

See [2, Thm. 8.1.4]. ∎

2.3. Data setting and technical lemmas

Recall the MFO problem (Pm). We consider the following setting:

-

•

Two Polish spaces and their Borel -algebras: and .

-

•

A probability distribution on : .

-

•

A set-valued function with a closed graph and non-empty images. Let

-

•

The admissible set of probability measures:

where .

-

•

A separable Hilbert space: .

-

•

Two Borel measurable functions: and .

The integral in (Pm) should be interpreted in the Bochner integration sense. We refer to [14, Appx. E] for Bochner integrable functions.

Lemma 2.6.

If there exists a constant such that for any , then the function is Bochner integrable with respect to any , i.e., exists. Moreover, for any , we have

As a consequence, for any , we have

Proof.

As is separable, the function is strongly measurable. Moreover, as the constant function is Bochner integrable with respect to any , and for any , it follows from [14, Prop. E.2, Thm. E.6] that is Bochner integrable with respect to any . Therefore, we can apply [14, Prop. E.11] to obtain the first equality of this lemma. The second equality is obtained by applying twice the first one. ∎

Theorem 2.7 (Disintegration theorem).

For any , there exists a family of probability measures such that for any Borel measurable function , we have

Moreover, for a.e. , is uniquely determined.

Proof.

See [1, Thm. 5.3.1]. ∎

Remark 2.8.

It is not difficult to generalize Theorems 2.7 to functions bounded from below, by adding to a sufficient large positive constant.

3. Optimality condition

3.1. Assumptions and constants

To simplify the presentation of the assumptions and the results of the article, we introduce the following (set-valued) functions, parameterized by :

-

•

and ,

-

•

and ,

Assumption A.

The following holds:

-

(1)

The function is bounded. The function is convex and differentiable, and is Lipschitz continuous with modulus .

-

(2)

Let . Fixing any , we have:

-

•

the function is lower semi-continuous;

-

•

the set-valued function is lower semi-continuous;

-

•

the set-valued function has non-empty images.

-

•

Three useful constants below are defined, following Assumption A:

We present here a lemma following Assumption A. A similar result for the Lagrangian MFG is presented in [9, Lem. 3.4].

Lemma 3.1.

Under Assumption A, for any , the set-valued function has a closed graph.

Proof.

Let converge to some , and let converge to some . We have to prove that . First, we have , since is closed. Fix any . Since is lower semi-continuous, there exists a sequence in such that

By the lower semi-continuity of , we have

Since and , we have for any . Passing to the limit in this inequality (using the above inequalities), we deduce that . Thus, has a closed graph. ∎

In Section 5, we will consider the dual problem of (Pm). For the analysis of Section 5, Assumption A needs to be strengthened as follows:

Assumption A∗. Assumption A(1) holds true and Assumption A(2) holds true for all , where is the Fenchel conjugate of .

Remark 3.2.

Assumption A∗ is indeed stronger than Assumption A since . This inclusion is deduced from Fenchel’s relation: .

3.2. First-order-optimality condition

The following lemma plays a key role in proving the first-order optimality condition for (Pm).

Lemma 3.3.

Let Assumption A hold true. For any , we have

Here we present a proof of Lemma 3.3 for the case where has finite support, that is, . This particular case provides us with insight into the general proof, and proves beneficial for resolving the discretized problem introduced in Section 6.

Proof of Lemma 3.3 when .

Fix any . Since is bounded over , the function is bounded from below. By Lemma 2.7 and Remark 2.8, we have

where the second inequality follows from the definition of .

Let us prove the converse inequality. Let us fix . Let , let and let be such that and . For any , let . Let us define Clearly . Moreover,

The conclusion follows, moreover, minimizes over . ∎

In the general case, one has to find a measurable selection of , which requires us to prove the measurability of , which cannot be done in a direct fashion. The complete proof is given in Appendix A.

Theorem 3.4 (First-order optimality condition).

Let Assumption A(1) hold true. Let and . Consider the following three assertions:

-

(1)

The measure is a solution of problem (Pm);

-

(2)

;

-

(3)

, a.e., where is defined by the disintegration theorem.

Then, assertions (1) and (2) are equivalent. Moreover, under Assumption A(2), assertions (1), (2), and (3) are equivalent.

Proof.

Step 1. (Equivalence between and ). We first prove that . Suppose that is a solution of problem (Pm). Take an arbitrary . Then, for any , we have

where the second inequality follows from the Lipschitz-continuity of and the definition of . Therefore

Let go to . We obtain that

| (3.1) |

This implies by the definition of .

We now prove . Let hold true. We obtain (3.1) by the definition of . The convexity of implies that for any ,

Therefore, is a solution of problem (Pm).

Step 2. (Equivalence between and ). By Theorem 2.7, we have

By Lemma 3.3, we have

Therefore, assertion is equivalent to

| (3.2) |

Let hold true. It follows that , -a.e., which implies (3.2).

Let hold true. We obtain (3.2). The function is nonnegative, for a.e. , by the definition of . By (3.2), its integral is null, thus, as a consequence of Lemma 2.1, we have

| (3.3) |

Fix such that equality holds in (3.3). Consider the map . It is nonnegative, with a null integral, and is non-empty and closed. Then assertion (3) follows with Lemma 2.1. ∎

Corollary 3.5.

Proof.

This is a consequence of Theorem 3.4. ∎

The conditions in (3.4) can be interpreted as the conditions for a Nash equilibrium in an non-atomic game, in which the agents through the variable . The relation shows how results from the collective behavior of the agents, while the relation shows that the agents behave optimally, for some criterion that depends on . We will discuss some more concrete examples in Section 7.

3.3. Existence of a solution under tightness assumptions

We denote by the value of problem (Pm). We can easily deduce from Assumption A that . The following proposition demonstrates the existence of a solution to problem (Pm) under some additional assumptions.

Proposition 3.6 (Existence).

Proof.

By Prokhorov’s theorem [33, p. 43], the set is relatively compact with respect to the narrow topology. Without loss of generality, suppose that narrowly converges to some . The set is closed with respect to narrow topology by [29, Prop. 2.4]. This implies that . Let . Since is convex, we have

| (3.5) |

Since is lower semi-continuous and bounded from below by Assumption A, we deduce the following inequality from [33, Lem. 4.3]:

In inequality (3.5), letting go to infinity, by the definition of , we have

Therefore, is a solution of problem (Pm). ∎

4. Stability analysis and bridging method

In this section, we study the stability of the primal problem (Pm) with respect to its parameter . We need the following assumptions (recall the data setting introduced in Sec. 2.3).

Assumption B.

The following holds:

-

(1)

The space is a closed subset of a separable Banach space;

-

(2)

The function is continuous;

-

(3)

The set is compact for any and the set-valued function is upper semi-continuous;

-

(4)

There exists such that the set-valued function

(4.1) is -Lipschitz on .

Let and lie in . We consider the following two instances of (Pm) with and respectively:

| (P) | |||

| (P) |

Suppose that we have an (approximate) solution of problem (P), denoted by . Our goal is to propose a feasible approach for recovering an approximate solution of problem (P) from and to study the performance of this approximation. We call it the bridging method. It relies on and the solution of the optimal transport problem (OT1) stated later. To introduce (OT1), we need to define some projection operators

Recall that , , and , . The other projection operators used in this subsection are defined as:

It directly follows from the above definitions that

Now we consider the following optimal transport problem:

| (OT1) |

where . It follows from [33, Rem. 6.5] that if and lie in , then .

The following particular example will provide an intuitive understanding of our bridging method.

A particular case. Let us assume that the distributions , , and are empirical distributions with supports of size , i.e., there exists and such that

| (4.2) |

Lemma 4.1.

Proof.

This is a consequence of [26, Prop. 2.1]. ∎

Let be given by Lemma 4.1. By Assumption B(4), for any , there exists such that

| (4.4) |

In our bridging method, each is transformed to while simultaneously moving to the point for . This can be expressed as follows:

| (4.5) |

To provide a clearer formula of the construction of , we introduce the empirical distribution and the mapping , defined as:

It can be observed that and . Furthermore, we will demonstrate later in Lemma 4.2 that is a solution of another optimal transport problem (OT2). Then the approximate solution of problem (P) can be written as:

The distribution belongs to , and furthermore,

where the second line follows from the triangle inequality and the third line follows from (4.4) and Lemma 4.1. The above inequality demonstrates that the distance between the aggregates associated with and is controlled by the -distance of and .

The general case. To investigate the stability and present the bridging method in the general case, we draw inspiration from the constructions of and in the previous particular case and introduce the following:

-

•

the auxiliary optimal transport problem:

(OT2) where ;

-

•

the set-valued function ,

(4.6)

Note that problems (OT2) and (OT1) are similar in so far as the integrand of the cost function is the same, moreover, the second marginal of in (OT2) (resp. in (OT1)) must be equal to . The following lemma shows the equivalence between problems (OT1) and (OT2). We will see that the solution of (OT2) will play the role of in the particular case mentioned earlier.

Proof.

Since , by [33, Rem. 6.5], we have . The existence of solutions of problems (OT2) and (OT1) is from [33, Thm. 4.1].

Let be a solution to (OT2) and let , which is clearly an element of . By the basic properties of push-forward measures, we have that Using the relation , we obtain that . It follows that . By similar arguments, we deduce that from the relation . Therefore, , moreover,

It follows that .

On the other hand, let be a solution of (OT1). Since and have the same marginal distribution with respect to their first variable, by the Gluing lemma [33, p. 11], there exists a probability measure such that

Since , we have . From the relation , we deduce that . Thus, , moreover,

It follows that . ∎

The following two lemmas demonstrate that the set-valued function has a measurable selection, which will be denoted by . We will see that the function will fulfill the role of in the particular case discussed earlier.

Lemma 4.3.

Under Assumption B(3), let be a sequence in converging to some . Then any sequence has a convergent sub-sequence with its limit in .

Proof.

Since is upper semi-continuous, for any , there exists such that for any , we have . For , there exists such that , i.e., there exists such that

Assume now we have and for such that

Since , we can find such that . As a consequence, there exists such that

Since is compact, has a convergent sub-sequence with a limit . By the triangle inequality,

Since and are strictly increasing functions going to , we have . Therefore, is a convergent sub-sequence of with its limit . ∎

Lemma 4.4.

Under Assumption B, the set-valued function has a Borel measurable selection function . Furthermore, we have .

Proof.

We will apply Theorem 2.3 and Lemma 2.4 to prove the result. The images of are non-empty since the set-valued mapping (defined in (4.1)) is supposed to be -Lipschitz. Let us first verify that has non-empty closed images. Fix any , and assume that converges to some . It suffices to prove that , i.e., . This is true since is continuous and .

Then, let us show that is closed for any closed subset in . By (4.6), we have

If , then the conclusion is obvious. Assume that and let be a convergent sequence with its limit point . Then, it suffices to prove that . Since , there exists , for any , such that

By Lemma 4.3, the sequence has a convergent sub-sequence with its limit . Hence, . Since is closed, we have . By the triangle inequality,

By the continuity of , we have

Therefore, , and . It follows that , which implies that is closed, thus a Borel set.

Lemma 4.5.

Proof.

Step 1. (Properties of ). Since and is a Borel measurable function, we have . Observing that , it follows that . Thus, . For any , is bounded. Then,

| (4.7) |

Step 2. (Quadratic upper bound). By the Lipschitz continuity of , we have

| (4.8) |

where .

Step 3. (First-order estimate). Let us study the first-order term in (4.8). By (4.7), we have

From the relation , we deduce that

Using the previous two equalities, Lemma 4.4, and the Cauchy–Schwarz inequality, we obtain that

Step 4. (Second-order estimate). Let us study the second-order term in (4.8). Developing it and using Lemma 2.6, we obtain that

| (4.9) |

where

Fix any . Following the same argument as in step 3, we have

It follows that

Step 5. As a consequence of Steps 2-4, we deduce that

By the definition of the constant , we have . The conclusion follows. ∎

We can now state the bridging algorithm that enables us to obtain an approximate solution of (P), given an approximate solution of (P).

Remark 4.6.

We have already discussed the case where , , and are empirical distributions. We discuss now the slightly more general case where only and are empirical distributions:

This situation corresponds to the algorithm presented in Section 6. Since , by Lemma 6.5, we have , where is defined in Theorem 2.7. Then the probability distribution , obtained in general with the Gluing lemma, is given here in an explicit form:

Theorem 4.7.

Proof.

We prove (1). Fix any . Let be an -minimizer of problem (P). By Lemma 4.2, there exists such that

We deduce from Lemma 4.5 that there exists associated with such that

Since , . Combining this with the fact , we obtain that

Therefore, by the arbitrariness of . We conclude the first part of the proof by exchanging the positions of and .

5. Duality analysis

5.1. The dual problem

This section is dedicated to the duality analysis of the primal problem (Pm). In the sequel of this section, let Assumptions A∗ and B hold true. Consider the equivalent formulation of problem of (Pm),

| () |

The Lagrangian associated with () writes,

Then, the dual problem of () is,

| (5.1) |

where is the Fenchel conjugate of . For any , since is bounded over , the second term is finite. Therefore, it suffices to study (5.1) for , i.e.,

The result of Lemma 3.3 holds true for all under Assumption A∗. Applying it to the previous problem, we obtain the following equivalent dual problem:

| (Dm) |

Lemma 5.1.

The function is strongly convex with modulus . As a consequence, problem (Dm) has a unique solution, denoted by . Moreover, there exists a constant independent of such that

Proof.

Since is -Lipschitz continuous, we know that is strongly convex with modulus (i.e. is convex) (see [3, Thm. 18.15]). Let us consider as a function of while fixing any . By definition, is the infimum of a family of affine functions (with respect to , thus it is concave with respect to . Consequently, is convex with respect to . Therefore, is -strongly convex. Additionally, is both convex and closed. These properties guarantee the existence and uniqueness of the minimizer .

Since is an upper bound of , it follows that for all :

Let . As , we can derive the following inequalities:

The strong convexity of yields that

where . Combining the two above inequalities, we obtain:

where . The announced result follows, with . ∎

5.2. Strong duality

Let us now prove the strong duality principle between (Pm) and (Dm), i.e., . We will apply the Fenchel-Rockafellar theorem [27] to prove this relation.

Proposition 5.2.

Proof.

Let us consider the following optimization problem with variable in :

| (5.2) |

It is obvious that . The dual problem of (5.2) writes

| (5.3) |

By the definition of the Fenchel conjugate and the definition of , we have

Therefore, . Let us apply the Fenchel-Rockafellar theorem to (5.2). The function is convex and continuous. The function is convex and lower semi-continuous from the fact that is convex and closed. It is obvious that is non-empty. Therefore, . By the Fenchel-Rockafellar theorem [27], , thus, .

Since is non-empty, bounded, convex, and closed, and since is continuous and convex, we deduce from [8, Cor. 3.23] that problem (5.2) has a solution. Therefore, (Pm) has a solution, denoted by . Since is the solution of (Dm), by the strong duality,

On the other hand, by the definition of Fenchel’s conjugate,

Combining the previous two inequalities and the fact that , we deduce that

We obtain that from Fenchel’s relation. ∎

5.3. Stability of the dual solution

Lemma 5.3.

For any and , it holds that

Proof.

By the triangle ineqaulity,

By the definition of , we have

Let be an -minimizer of , with . By the Lipschitz continuity of , there exists such that

By the Cauchy-Schwarz inequality, we have

By the arbitrariness of , we have .

On the other hand,

By the Cauchy–Schwarz inequality and the definition of , we have that

The conclusion follows. ∎

Lemma 5.4 (Stability of the dual problem).

Proof.

According to Lemma 5.1, we know that and are smaller than . Then, by Lemma 5.3, and are -Lipschitz continuous with respect to . Hence,

| (5.6) |

where the third line is by the definition of the Kantorovich–Rubinstein distance. Since minimizes and since is -strongly convex, we have

| (5.7) |

Combining (5.6) and (5.7), we obtain that

In particular, we have . Exchanging the positions of and in (5.6), we obtain

| (5.8) |

Inequality (5.4) follows immediately and (5.5) is deduced by summing (5.6)-(5.8). ∎

5.4. Directional derivative of the value function

The value function of problem (Pm) is defined by

Our goal is to characterize the directional derivative of . Define the following function:

Proposition 5.5.

Assume that is closed for any . Then for any , we have

As a consequence, is the directional derivative of , i.e.,

Proof.

For any , let . By the strong duality, we have

From (5.6), we deduce that

| (5.9) |

On the other hand, let and be solutions of (Pm) with and respectively. Let . It is obvious that . Therefore,

By Proposition 5.2, . Since is -Lipschitz, it follows that

Recall the definition of . Combining the two inequalities above, we have

| (5.10) |

We have and . Using (5.9)-(5.10) and letting go to , we obtain that

From Lemmas 5.3-5.4, we deduce that the function is continuous in with respect to the distance . Let us define two functions from to ,

For any , observe that and . By using the same arguments as in (5.9)-(5.10), we have

We deduce that is the right derivative of at for any . By exchanging positions of and , we can prove that is the left derivative of at for any . Therefore, is differentiable at each point on and is its derivative. Since is continuous, by the fundamental theorem of calculus [28, Thm. 7.21], we have that . ∎

6. Numerical approach

We present in this section our numerical method for solving (Pm). The first step of resolution consists in discretizing . We replace it by an empirical distribution and focus next on the resolution of (P). By Theorem 4.7(1), we have

| (6.1) |

We give theoretical bounds for the minimal value of in Subsection 6.1. Then we discuss the resolution of (P) with the Frank-Wolfe algorithm in Subsection 6.2. Finally in Subsection 6.3 we propose to use a variant of the Frank-Wolfe algorithm, called Stochastic Frank-Wolfe (SFW) algorithm, introduced in [6]. This method generates a solution to (P) which is an empirical distribution.

6.1. Discretization

In view of (6.1), one should look for an empirical distribution that is as close as possible to for the -distance. This problem is commonly known as the optimal quantization problem, and for detailed information on this topic, we refer to [17]. Here, we present a slightly modified version of an optimal quantization result obtained in [25, Prop. 12]. For any subset of , we denote by the minimum radius required to cover with closed balls of radius . It is defined by

The upper box-counting dimension (or the upper Minkowski dimension) of [15, p. 41] is defined as follows:

Lemma 6.1.

Let , and let be the support of . There exists a sequence of empirical distributions on such that the following holds:

-

(1)

If , then there exists a constant such that for any ,

-

(2)

If , then there exists a constant such that for any ,

-

(3)

If , then there exists a constant such that for any ,

Proof.

This follows from the proof presented in [25, Prop. 12], with the only difference being that in the final inequality, we employ the triangle inequality for the -distance instead of the Minkowski inequality for the Wasserstein-2 distance. ∎

Remark 6.2.

If is a subset of a smooth -dimensional submanifold of a Euclidean space, then . This estimate is deduced from [15, p. 48 (i)-(ii)].

6.2. Frank-Wolfe algorithm

For general convex optimization problems, the Frank-Wolfe algorithm relies on the resolution of a sequence of linearized problems, obtained by replacing the cost function of the problem by a first-order Taylor approximation of it. In the context of problem (P), the linearized problem is of the general form:

| (6.2) |

for some .

A key observation from Lemma 3.3 is that a solution of the linearized problem, denoted by , can be obtained as in the proof of Lemma 3.3, in the simple case where is a finitely-supported probability measure: for all , find and set . Therefore, one can consider applying the Frank-Wolfe algorithm to solve (P), in which the main task is to solve (6.2).

Remark 6.3.

If we take for all , then it is easy to see that . We recover the fictitious play of [10], applied to the Lagrangian discretization of first-order MFGs.

Proof.

This is a consequence of [6, Prop. 3.4]. ∎

6.3. Stochastic Frank-Wolfe algorithm

In Algorithm 2, at each iteration, we generate the output by taking a convex combination of the previous iteration’s result and the solution of (6.2). This process requires us to add points from , for , to stock the support of solution at each iteration. As a consequence, this approach can lead to a memory overflow issue, as going to infinity. The large support of will also raise the difficulty of Step 2 in Algorithm 1, in which we will take . To address this issue, we will use the stochastic Frank-Wolfe algorithm [6] to (P). This approach will enable us to obtain an approximate empirical solution (P), and can effectively handle the large support of .

Lemma 6.5.

Let . Then lies in if and only if there exists for any such that .

Proof.

If , then . Since the push-forward operator is linear, we have that .

Conversely, let us assume that . By Theorem 2.7 and its remark, we can conclude that there exists for such that for any bounded and continuous function , we have

Applying Fubini’s theorem to the equality above, we have

This implies that . ∎

According to Lemma 6.5 and Fubini’s theorem, the discretized problem (P) is equivalent to

| (6.3) |

Problem (6.3) is the randomized relaxation of an -agent optimization problem as investigated in [6],

| (6.4) |

Problem (6.4) is equivalent to a version of problem (6.3) in which the probability measures are restricted to be Dirac measures. In particular, we can associate with each feasible element (for problem (6.4)) the tuple , which is feasible for (6.3), and the probability distribution , which is feasible for (P).

We apply the following Stochastic Frank-Wolfe algorithm, investigated in [6], to solve problems (6.3) and (6.4). Let Bern be the Bernoulli distribution with a parameter .

The interest of Algorithm 3 is that it provides an approximate solution to (6.4), and the associated empirical distribution serves as a reliable approximate solution of the problem (6.3), as demonstrated in the following lemma. Additionally, this empirical distribution has a fixed support size , which does not increase with the iteration number, making the algorithm memory-efficient.

Lemma 6.6.

in Algorithm 3, whatever the numbers , we have for any that

Proof.

This is from [6, Thm. 3.7]. ∎

Remark 6.7.

In order to obtain an approximate solution of (Pm), we combine Algorithm 3 with Algorithm 1. Let us consider the outcome of Algorithm 3 after iterations, for and for arbitrary numbers of simulations. Let . Moving on to Algorithm 1, we utilize the following inputs: , , and . The output of Algorithm 1 is denoted as , which is an element of the set . We have the following convergence result for the combination of Algorithm 1 and 3.

Proof.

7. Examples and numerical results

7.1. The traffic assignment problem

The traffic assignment problem is a non-atomic game whose potential formulation takes the form of problem (Pm). We describe it briefly in this subsection. Consider a finite set of nodes and a finite set of edges . The model is a static model that describes how the agents move on the network, taking into account their origins and destinations as well as the congestion on each arc.

We fix a subset of . Each parameter represents an origin-destination pair. Next, we denote by the set of subsets of . For each , we consider a set of possible paths connecting and , denoted . Mathematically, we simply describe a path as a subset of , so .

For the definition of the potential problem, we define . The function is defined by , where

In words, is the edge belongs to the path , 0 otherwise. Next, we fix a family of functions , parametrized by . We assume that these functions are non-decreasing and we fix a primitive for each of them. The functions are convex. Finally, we define by

With these definitions at hand, it remains to interpret the optimality conditions for the associated MFO problem. Let us consider and let . A direct calculation shows that

We can interpret as the proportion of agents using the edge . We interpret as a function that gives the travelling time on the edge in function of the congestion . So here the dual variable has a natural interpretation as a vector containing all the travelling times of the network. Finally, for any , we have

Here describes the total duration of the path . As a consequence, solving the MFO problem is equivalent to find such that for any , is supported by the optimal paths (among those connecting to ), the travel time of a path begin defined by the above relations. This notion of equilibrium is known as Wardrop equilibrium in the literature. Using the MFO setting, we recover the well-known equivalence between Wardrop equilbria and their potential formulation, see [31, Chapter 3]. We mention here that the modelling is different (but equivalent) to the standard one in which one rather describes the distribution of the agents with respect to the edges, instead of using the distribution with respect to the paths. We also note that the Frank-Wolfe algorithm is a very standard algorithm for solving those problems, see [31, Section 5.2].

7.2. Lagrangian MFGs

We propose here a class of potential Lagrangian MFGs. As before, we first formulate the potential problem, in the form of an MFO problem and interpret next the optimality conditions as a non-atomic game. There is a large amount of literature on Lagrangian MFGs, we refer the reader to [4, 5, 9, 29, 30] and the references therein. Our intention here is only to formulate a model that fits with the framework of MFO problems, we do not check the corresponding assumptions, which must be done on a case-by-case basis.

Let us fix a domain and a final time . Let be the set of all absolutely continuous functions from to . For any , we denote,

Let . Let be the distribution of the initial states of the players. We fix three functions , , and . We define by

and we define as

With these definitions of , , , , and , we have a full description of an MFO problem. Let us write the corresponding optimality conditions. Let and let . Then, , with and

For any , denote by the mapping defined by . Then is equivalently defined by

In this context, the minimization problem in (3.4) is equivalent to the following optimal control problem:

Let us note that the above problem is not convex in general. It could be solved by dynamic programming in the situation where the dimension of is moderate.

7.3. Numerical results for a competition problem with a non-renewable resource

Model

We consider a Lagrangian MFG in which the agents exploit their own stock of an exhaustible resource. The model is taken from [18]. We fix a time horizon where (the case investigated in [18] is not considered here). The state variable of a representative agent is the level of the stock of resource at any time, denoted and the control is the speed of extraction at any time, denoted . The dynamic of a given producer with an initial position is described as follows:

where , for any . We impose that , which implies that at any time.

We define the set of aggregate production, denoted as , by

The price of the resource for this representative producer depends on its extracting speed and an aggregate production ,

where is a constant. The gain of this representative producer writes,

where is a discount rate. Therefore, given an aggregate production and an initial position , we can formulate an optimal control problem associated with this representative producer,

| (7.1) |

Lemma 7.1.

Problem (7.1) has a unique solution . Moreover, , for a.e. .

Proof.

It is easy to see that is a non-empty and convex subset of . Following [28, Thm. 3.12], if converges to in sense, then there exists a subsequence of converges to a.e. As a consequence, lies in . Therefore, is closed. Furthermore, by Hölder’s inequality, we obtain that is non-empty, convex and closed in . It follows that the admissible set of problem (7.1) is non-empty, closed and convex in Hilbert space . On the other hand, the cost function is strongly convex. Then the existence of the solution of (7.1) comes from [8, Cor. 3.23] and the uniqueness is by the strong convexity of .

Let denote the distribution of the initial conditions of the producers. The aggregate production rate corresponding to is given by

Following [18], we call Nash equilibrium a solution to the fix-point problem:

| (7.2) |

Potential problem

In this paragraph, we find an optimization problem associated with the fixed point problem (7.2), which is a particular case of problem (Pm). Let us specific metric spaces and admissible sets in (Pm) associated with (7.2):

Let us define the separable Hilbert space [28, Example. 4.5(b)]:

with a scalar product,

It is easy to check that . Then, in (Pm), we set ,

Therefore, problem (Pm) associated with (7.2) writes:

| (7.3) |

Proposition 7.2.

Proof.

Let us first check that Assumption A holds true for problem (7.3). It is easy to see that Assumption A(1) and the first and the third points in Assumption A(2) are true by the continuity of and Lemma 7.1. Let us prove that is lower semi-continuous for any . This is a consequence of the claim that the set-valued function , is locally Lipschitz, i.e. Lipschitz in any compact set of . To see the local Lipschitz continuity, we fix any in . If , then we have immediately that . This implies that . On the other hand, let . We construct by the following method:

As a consequence, we have that . Therefore, by Hölder’s inequality,

This implies that . Therefore, Assumption A follows.

Numerical simulations

Let the initial measure be an exponential distribution with parameter , i.e., for all . Let us independently sample the distribution for times, denoting the samples by , and . The time space is discretized with a step size for some . Then, a totally discretized problem associated with (7.3) writes:

| (7.4) |

We apply Algorithm 3 to solve (7.4). At each iteration, the evaluation of a best-response, for each producer amounts to solve a problem of the following form:

| (7.5) |

for a given . This problem is a convex quadratic programming problem in that can be dealt with by some solvers, such as GUROBI [19].

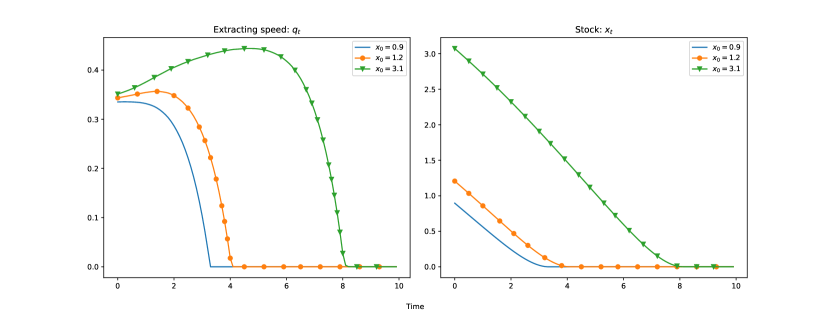

For the resolution of the problem, we chose the following parameters: , , , , , , for all . Figure 1 shows the extracting speeds and the stocks of three producers with initial stocks: 0.9, 1.2, and 3.1. From Figure 1, we see that the producers with the higher initial stock have the same extracting speed as those with a lower initial stock, at the beginning. However, as the smaller agents exhaust their resource, the larger ones progressively raise their extraction speed. Once the extraction speed reaches its maximum value, it rapidly decreases to zero. These observations are consistent with the findings of [18, Sec. 3.3].

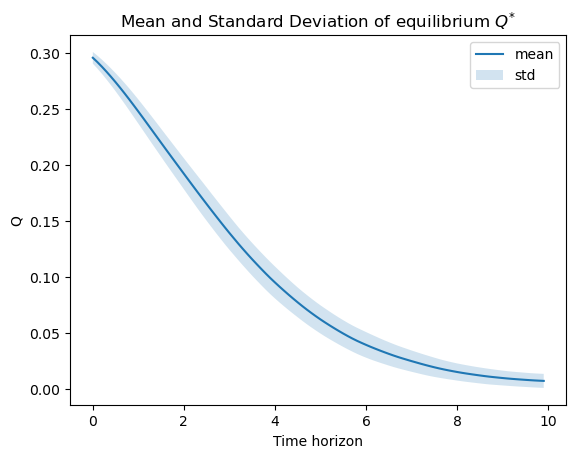

To study the error caused by sampling, we independently sample the exponential distribution for times, and group them into batches of . The empirical distribution corresponding to each batch is set as the initial distribution. Then we apply Algorithm 3 to compute corresponding to each initial distribution. In Figure 2, we show the mean and standard deviation of the results of the 100 simulations.

7.4. Numerical results for a congestion game

Model

Consider a second numerical example within the context of the minimal-time deterministic MFG. We set the following parameters: the state space is fixed as , a maximum duration is denoted by , and an upper bound for the speed is given by . In this particular example, the dynamics governing each player are characterized by the set , defined as:

The objective for the players in this example is to reach the target point as soon as possible, while simultaneously ensuring that the density at each point does not become excessively high. To quantify this, we introduce the congestion function , which is defined as follows:

Given an initial distribution , the resulting deterministic MFG problem can be expressed as follows:

| (7.6) |

where is a penalty parameter.

Regularization

Note that the congestion function does not fit to the framework studied in this article. To address this, we begin by approximating with a function that aligns with our framework. We achieve this by partitioning the interval into small, uniform subintervals: , where , and . Subsequently, we approximate as follows:

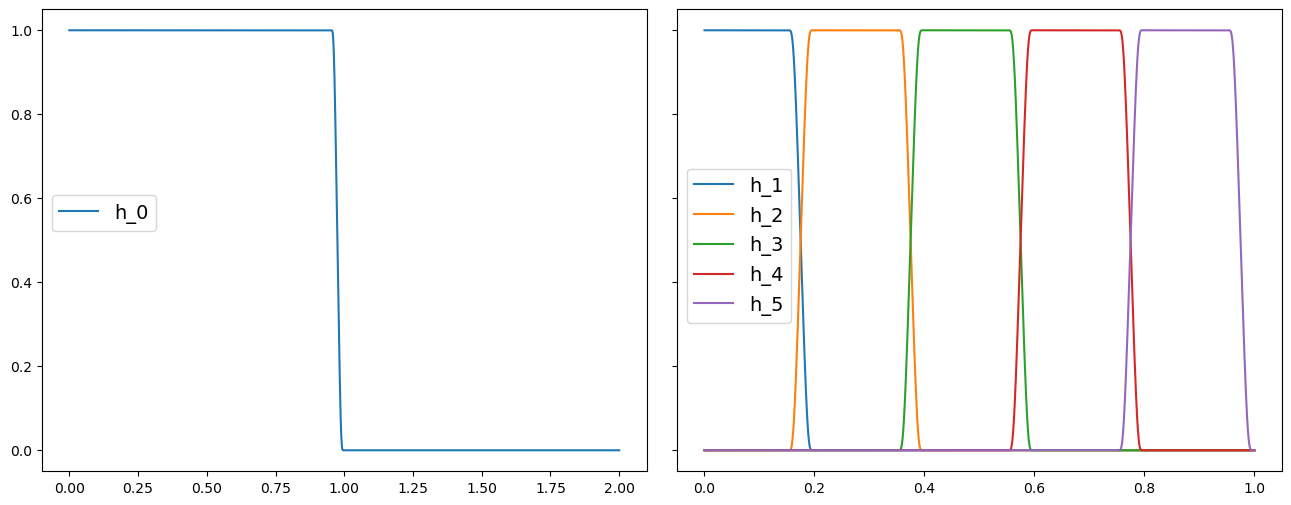

To facilitate the execution of the numerical experiments, we replace the indicator function by some smooth functions. Let be a positive integer. We introduce two smooth functions, denoted as and . These functions are parametrized by the variables and , and are defined as follows:

Then, we approximate by for , and by ,

An important property of is that , which is for any , see Figure 3.

The resulting approximated MFO problem associated with (7.6) is,

| (7.7) |

Discretization and numerical results

To proceed with our numerical experiments, we discretize the time horizon into steps, each of duration . Additionally, we discretize the initial distribution by . We formulate the fully discretized problem associated with (7.7) as follows:

| (7.8) |

Therefore, given some satisfying the constraint in (7.8), the sub-problem for player is

| (7.9) |

where . The sub-problem (7.9) is a finite-dimensional non-convex optimization problem, which is addressed by the open-source solver “scipy.optimize.minimize” [34].

Let us specify the parameters used in the numerical simulation of problem (7.7) as follows:

where “Uni” represents the uniform distribution, and the points are drawn from samples of .

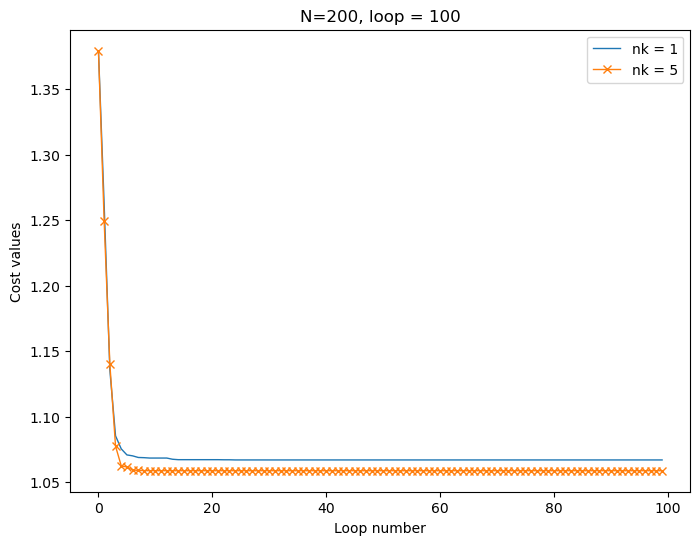

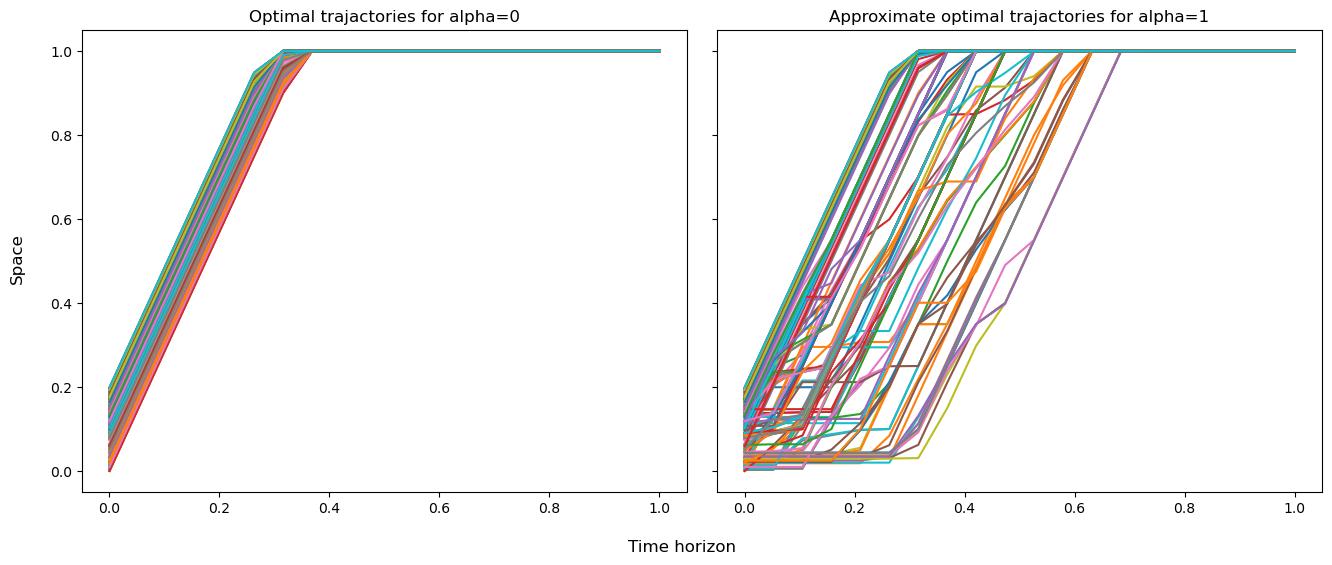

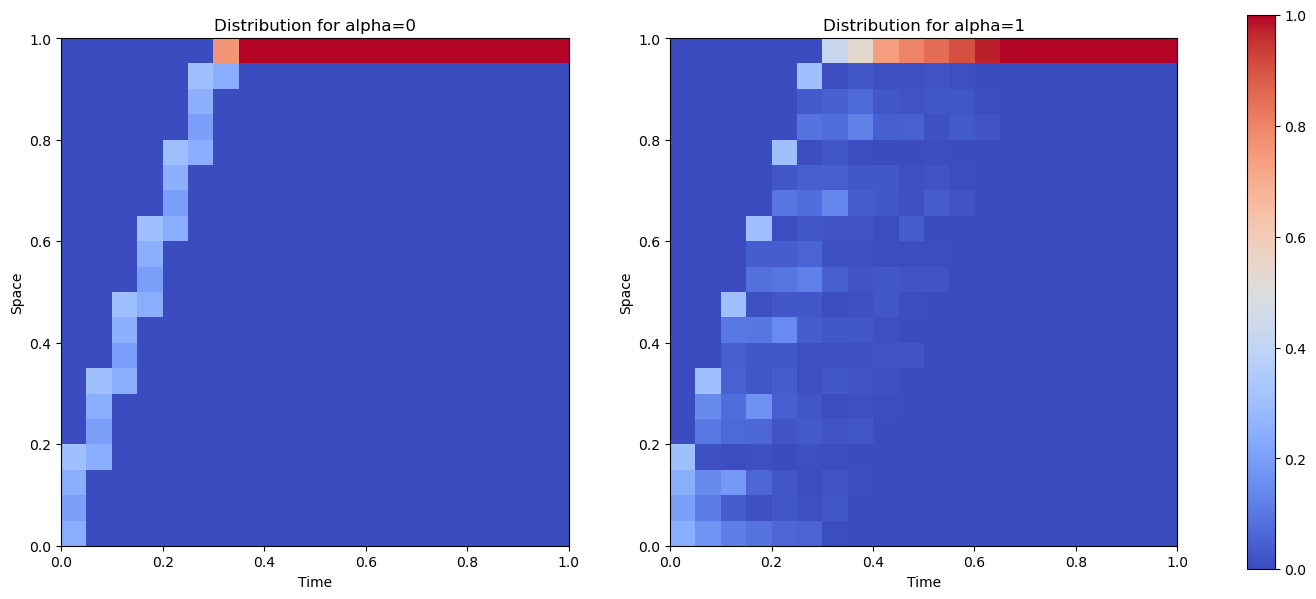

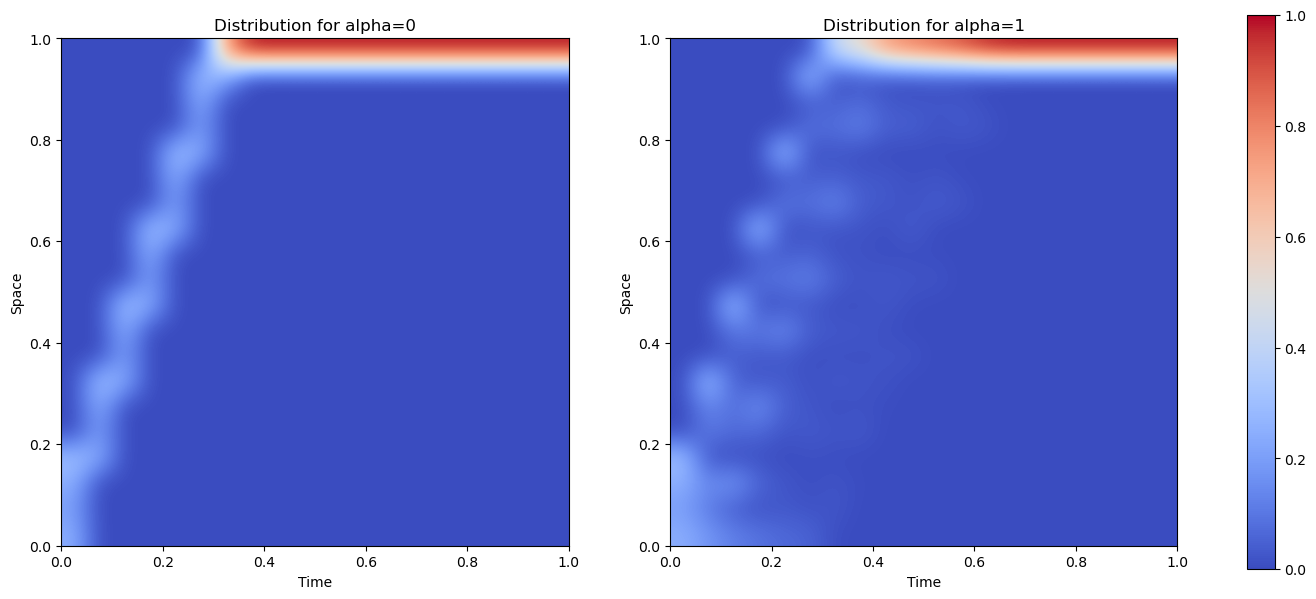

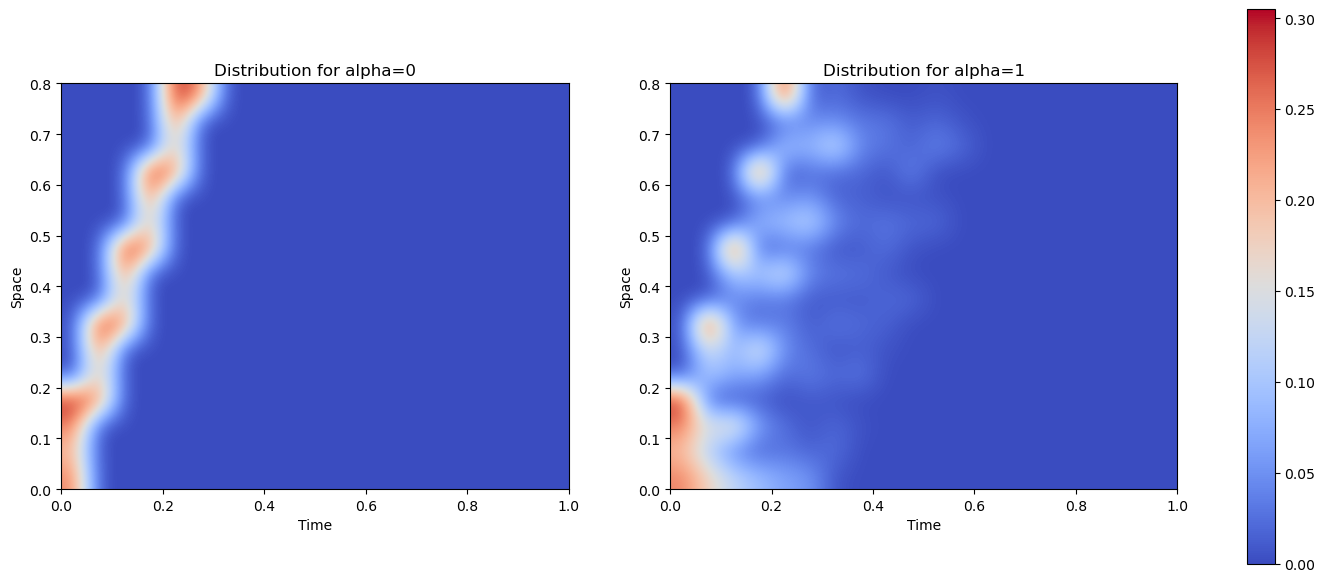

We first present in Figure 4 convergence results of Algorithm 3 for the discretized problem (7.8) in iterations, utilizing parameter settings of and . We see that in both choices, the algorithm converges to a local minimum very fast (fewer than 20 iterations). In Figure 5, we compare the optimal trajectories of for two cases: and . It is evident that, in the case of , the optimal strategy for each player is to move at the maximum speed, , as there is no penalty for density. This is depicted in the left part of Figure 5. However, when , players starting from greater initial positions choose to run at the maximum speed, whereas those with lower initial positions prefer to wait briefly to avoid congestion in density with those starting farther ahead. In Figure 6(a), we draw the agents’ state distributions at each time for both and , along with a regularized version obtained through interpolation in Figure 6(b). For a more detailed view of the density evolution before reaching the target, we further depict the restricted distributions within the spatial interval in Figure 6(c), using a distinct color scale.

Remark 7.3.

Let us underline that for this example, the optimization problems involved in the evaluation of the best-response mapping are non-convex. As mentionned above, we address them with the open-source solver scipy.optimize.minimize whose default method for tackling constrained non-linear optimization problems is the SLSQP (Sequential Least SQuares Programming) algorithm, a quasi-Newton-type algorithm. Consequently, the quality of the initial guess plays a crucial role in the resolution of sub-problems. In the context of Algorithm 3, our experience shows that at iteration , it is more efficient to initialise the evaluation of with (rather than ). We conjecture that the chance for the solver to generate a local solution is higher when initializing with .

8. Conclusion

We have provided a general framework for analyzing Mean Field Optimization problems. We have proposed a general method, based on an extension of the Frank-Wolfe algorithm for solving MFO problems, with a convergence guarantee, assuming that some best-response function can be efficiently computed (with a solver or with specific methods). Numerous extensions of the current setting could be considered. For example, one could formulate a stochastic setting with a random variable impacting all agents. In this setting the evaluation of (in the SFW algorithm) may require to use Monte-Carlo approximations, adding a new source of error in the general algorithm. One may also realize a general convergence analysis that would take into account the need to discretize the sets (in particular in the case of MFGs, where is an infinite dimension set). Finally, at a purely numerical level, we could investigate variants of the proposed method in which the distribution is discretized progressively. This would reduce the number of subproblems to solve in the early iterations of the SFW algorithm. We also mention that the SFW is robust in the following sense: at the end of iteration , if is replaced by any other point yielding a reduction of the cost function, then the general convergence properties of the SFW algorithm are preserved. This fact could motivate the design of heuristic improvements on a case-by-case basis.

Appendix A Proof of Lemma 3.3

Before proving Lemma 3.3, let us recall the definitions of the restriction of a measure and the completion of a probability space, taken from [28, Thm. 1.36].

Definition A.1 (Restriction).

Let be a Polish space, let and be two -algebras on such that , and let be a measure on . The restriction measure of on is defined as follows:

Definition A.2 (Completion).

Let be a probability space. Let be the collection of all such that there exists and in , , and . For such an , we define a function as

Then is a complete measure space. We say that is the completion of .

Sketch of the proof of Lemma 3.3.

The proof of the direction that the left-hand-side of (3.2) is greater than the right-hand-side is the same as the proof for the case that .

Let us prove the converse inequality. Let be the completion of the probability space . Fix any . By Assumption A, the set-valued function has non-empty closed images. By Lemma 3.1, Graph is closed in , thus is a -measurable set. By Lemma 2.5 and Theorem 2.3, the set-valued function is -measurable, and there exists a -measurable function such that for any ,

We define , . Since is -measurable, we have that is -measurable, see [21, Lem. 1.8]. Let be the Borel -algebra on . It is obvious that . Let us take

Then is a positive Borel measure on . Moreover, we deduce from Definitions A.1-A.2 that

Therefore, . Assume that the following two equalities hold true:

| (A.1) | ||||

| (A.2) |

By the definitions of and ,

| (A.3) |

Combining (A.1)-(A.3), we obtain that

The conclusion follows. ∎

For completing the proof of Lemma 3.3, it remains to prove equalities (A.1)-(A.2). They are deduced from Lemmas A.3-A.4:

- •

- •

Recall the definition of in the previous proof and recall that .

Lemma A.3.

Let be a Polish space. Let be a Borel measurable function. Assume that is Borel measurable. Then . As a consequence, if for some , then

Proof.

Let be any Borel set in . By the property of push-forward measure, . Since is Borel measurable, . Thus . Next, by the property of the push-forward measure,

Since is Borel measurable, we have that . As a consequence,

Therefore, for any Borel set . This concludes the first part of the proof. In the case where for some , since , it suffices to prove the conclusion for in instead of . Therefore, we can assume that . By the change-of-variable formula for push-forward measures,

Next, it follows from the equality that

Again, by the change-of-variable formula, we obtain that

The conclusion follows. ∎

Lemma A.4.

Under Assumption A, the function is upper semi-continuous for any , thus Borel measurable.

Proof.

Let . Since is bounded over , we have that for any . Fix any . Let . Let be a sequence converging to . By the lower semi-continuity of , there exists such that . Therefore,

We obtain the upper semi-continuuity of for any . Since any upper semi-continuous function defined on a metric space is the limit of a monotonically decreasing sequence of continuous functions [32, Thm. 3], we deduce that is Borel measurable. ∎

References

- [1] L. Ambrosio, N. Gigli, and G. Savaré. Gradient flows: in metric spaces and in the space of probability measures. Springer Science & Business Media, 2005.

- [2] J.-P. Aubin and Hélène Frankowska. Set-valued analysis. Springer Science & Business Media, 2009.

- [3] H.H. Bauschke and P.L. Combettes. Convex analysis and monotone operator theory in Hilbert spaces, volume 408. Springer, 2011.

- [4] J.-D. Benamou, G. Carlier, and F. Santambrogio. Variational mean field games. Active Particles, Volume 1: Advances in Theory, Models, and Applications, pages 141–171, 2017.

- [5] J.F. Bonnans, J. Gianatti, and L. Pfeiffer. A lagrangian approach for aggregative mean field games of controls with mixed and final constraints. SIAM Journal on Control and Optimization, 61(1):105–134, 2023.

- [6] J.F. Bonnans, K. Liu, N. Oudjane, L. Pfeiffer, and C. Wan. Large-scale nonconvex optimization: randomization, gap estimation, and numerical resolution. arXiv preprint, 2022.

- [7] N. Boyd, G. Schiebinger, and B. Recht. The alternating descent conditional gradient method for sparse inverse problems. SIAM Journal on Optimization, 27(2):616–639, 2017.

- [8] H. Brézis. Functional analysis, Sobolev spaces and partial differential equations, volume 2. Springer, 2011.

- [9] P. Cannarsa and R. Capuani. Existence and uniqueness for mean field games with state constraints. PDE models for multi-agent phenomena, pages 49–71, 2018.

- [10] P. Cardaliaguet and S. Hadikhanloo. Learning in mean field games: the fictitious play. ESAIM: Control, Optimisation and Calculus of Variations, 23(2):569–591, 2017.

- [11] C. Castaing and M. Valadier. Convex analysis and measurable multifunctions, volume 580. Springer, 2006.

- [12] F. Chen, Z. Ren, and S. Wang. Entropic fictitious play for mean field optimization problem. Journal of Machine Learning Research, 24(211):1–36, 2023.

- [13] L. Chizat and F. Bach. On the global convergence of gradient descent for over-parameterized models using optimal transport. Advances in neural information processing systems, 31, 2018.

- [14] D.L. Cohn. Measure theory, volume 1. Springer, 2013.

- [15] K. Falconer. Fractal geometry: mathematical foundations and applications. John Wiley & Sons, 2004.

- [16] M. Geist, J. Pérolat, M. Laurière, R. Elie, S. Perrin, O. Bachem, R. Munos, and O. Pietquin. Concave utility reinforcement learning: The mean-field game viewpoint. In Proceedings of the 21st International Conference on Autonomous Agents and Multiagent Systems, pages 489–497, 2022.

- [17] A. Gersho and R.M. Gray. Vector quantization and signal compression, volume 159. Springer Science & Business Media, 2012.

- [18] P. Graewe, U. Horst, and R. Sircar. A maximum principle approach to a deterministic mean field game of control with absorption. SIAM Journal on Control and Optimization, 60(5):3173–3190, 2022.

- [19] LLC Gurobi Optimization. Gurobi optimizer reference manual, 2018.

- [20] S. Hadikhanloo and F.J. Silva. Finite mean field games: fictitious play and convergence to a first order continuous mean field game. Journal de Mathématiques Pures et Appliquées, 132:369–397, 2019.

- [21] O. Kallenberg. Foundations of modern probability, volume 2. Springer, 1997.

- [22] P. Lavigne and L. Pfeiffer. Generalized conditional gradient and learning in potential mean field games. Applied Mathematics and Optimization, 88, 2023.

- [23] K. Liu and L. Pfeiffer. A mesh-independent method for second-order potential mean field games. ArXiv preprint, 2023.

- [24] S. Mei, A. Montanari, and P.-M. Nguyen. A mean field view of the landscape of two-layer neural networks. Proceedings of the National Academy of Sciences, 115(33):E7665–E7671, 2018.

- [25] Q. Mérigot and J.-M. Mirebeau. Minimal geodesics along volume-preserving maps, through semidiscrete optimal transport. SIAM Journal on Numerical Analysis, 54(6):3465–3492, 2016.

- [26] G. Peyré and M. Cuturi. Computational optimal transport. Foundations and Trends in Machine Learning, 11(5-6):355–607, 2019.

- [27] R.T. Rockafellar. Convex analysis, volume 11. Princeton university press, 1997.

- [28] W. Rudin. Real and complex analysis, volume 3. McGraw-Hill, 1987.

- [29] F. Santambrogio and W. Shim. A Cucker–Smale inspired deterministic mean field game with velocity interactions. SIAM Journal on Control and Optimization, 59(6):4155–4187, 2021.

- [30] C. Sarrazin. Lagrangian discretization of variational mean field games. SIAM Journal on Control and Optimization, 60(3):1365–1392, 2022.

- [31] Yosef Sheffi. Urban transportation networks, volume 6. Prentice-Hall, Englewood Cliffs, NJ, 1985.

- [32] H. Tong. Some characterizations of normal and perfectly normal spaces. Duke Math. J., pages 289–292, 1952.

- [33] C. Villani. Optimal transport: old and new, volume 338. Springer, 2009.

- [34] P. Virtanen, R. Gommers, T.E. Oliphant, M. Haberland, T. Reddy, D. Cournapeau, E. Burovski, P. Peterson, W. Weckesser, J. Bright, et al. Scipy 1.0: fundamental algorithms for scientific computing in python. Nature methods, 17(3):261–272, 2020.

- [35] M. Wang. Vanishing price of decentralization in large coordinative nonconvex optimization. SIAM Journal on Optimization, 27(3):1977–2009, 2017.