ylblue \addauthorjlred

Optimal Scoring for Dynamic Information Acquisition††thanks: Part of this work was completed while Jonathan Libgober was visiting Yale University. The authors thank Dirk Bergemann, Tan Gan, Marina Halac, Jason Hartline, Nicolas Lambert, Elliot Lipnowski, Mallesh Pai, Harry Pei, Larry Samuelson, Philipp Strack and Kai Hao Yang for helpful comments and suggestions. Yingkai Li thanks Sloan Research Fellowship FG-2019-12378 for financial support.

Abstract

A principal seeks to learn about a binary state and can do so by enlisting an agent to acquire information over time using a Poisson information arrival technology. The agent learns about this state privately, and his effort choices are unobserved by the principal. The principal can reward the agent with a prize of fixed value as a function of the agent’s sequence of reports and the realized state. We identify conditions that each individually ensure that the principal cannot do better than by eliciting a single report from the agent after all information has been acquired. We also show that such a static contract is suboptimal under sufficiently strong violations of these conditions. We contrast our solution to the case where the agent acquires information “all at once;” notably, the optimal contract in the dynamic environment may provide strictly positive base rewards to the agent even if his prediction about the state is incorrect.

Keywords— Scoring rules, dynamic contracts, information acquisition, budgets, Poisson signals.

1 Introduction

This paper concerns the design of contracts to incentivize experts to acquire information for predicting a future state when doing so is costly and when this information acquisition is private. This problem may arise in a variety of situations, often when the contract designer expects to make a high-stakes decision—for instance, whether to launch a military attack in response to a perceived threat, whether to make a sizable investment, or whether to approve a risky vaccine to fight a budding pandemic. In these cases, whether a given action is best (e.g., invasion, investment, approval, respectively, for the above examples) may depend on the underlying state, which we will take as binary in this paper for simplicity. Notice that this problem features the combination of moral hazard (since the principal cannot monitor the expert’s effort) and endogenous adverse selection (since the expert’s actions generate private information).

In our model, while the agent has no direct interest in the state or the principal’s action, he can be rewarded with a prize on which (i) he places bounded value, but (ii) the principal places no intrinsic value. For example, this reward could be a recommendation or a grade, often much more valuable for early-career workers than any feasible direct payment. Alternatively, this could also reflect budget constraints on the principal, where the residual value of payments is second-order relative to the value of information. For instance, this situation applies to non-profit organizations that subject to budget constraints based on external funding in the form of grants.

Crucially, the rewards given to the expert can depend on the state of interest, where this state is unaffected by the principal’s actions. For instance, suppose the principal tasks the agent with determining whether or not the economy will be in a recession on some given date, as this may determine the relative profitability of an investment. In that case, while the principal’s investment decision would have a negligible influence on the state of the economy, rewards could still vary depending on market outcomes. Allowing the reward to depend on the state incentivizes the agent to exert effort to learn about it.

And lastly, we consider an information acquisition environment for the expert where learning takes time. Thus, the principal must provide incentives for effort to be exerted repeatedly, with possible interactions between the incentives provided at earlier times and later times. The dynamic nature of the agent’s information acquisition problem is a significant point of departure from past work on incentivizing information acquisition (e.g., Zermeno, , 2011; Li et al., , 2022), which typically assumes “all-at-once” information acquisition. But most practical information acquisition problems involve at least some dynamic elements, often taking the form of a time investment—for instance, if the expert’s task is to find a piece of evidence, and their problem is to decide if and when to give up. In such dynamic environments, additional challenges arise even for describing the agent’s incentives for acquiring costly information when rewards condition on time and choices in rich ways; hence, several existing characterizations and intuitions from the static model do not extend. A natural open question is how the principal can optimally leverage the dynamics.

Despite the challenges, we obtain insights on optimal dynamic contracts for information acquisition for a particular class of technologies in the agent’s problem. In each period, the agent decides whether to exert effort, potentially observing a signal informative of the state but incurring a flow cost. If the agent exerts effort, he may receive either a “good signal” (evidence of one state) or a “bad signal” (evidence of the other state). The arrival of signals depends on the true state and occurs at a fixed rate, which scales with the period length. Importantly, once one signal arrives, no further signals can be observed. This assumption corresponds to situations in which a single piece of evidence informs the agent about the unknown state, and the agent is searching for that specific evidence. If the agent simply rediscovers the same evidence, he will not update his belief. However, we do not assume that the evidence necessarily reveals which action would have been better with certainty (unlike, for instance, Keller et al., , 2005, which studies the analogous information acquisition technology in the continuous-time setting). As alluded to above, only the agent observes this signal. This feature reflects our goal of studying settings where agents can easily manipulate or counterfeit evidence, or when the principal must rely on expertise to interpret it.

For this class of information arrival processes, the principal learns the most if the agent works for as long as possible in the absence of evidence arrival and truthfully reports any finding once it arrives. In the following section, we will elaborate on how the principal can utilize the dynamics to incentivize the agent to work longer and describe three canonical environments where a static implementation of optimal contracts exists. Interestingly, even though the optimal contracts are static, the dynamics in effort choices still affect the design of optimal contracts.

1.1 Results and Intuition

To incentivize the agent, the principal could select an arbitrary dynamic contract, specifying rewards as a function of the realized state and the sequence of reports from the agent. Such contracts could be quite complex if rewards differ substantially depending on the sequence of reports from the agent. A simpler alternative is to wait until some terminal date and subsequently elicit reports via a scoring rule—that is, a mapping from a single report of the agent’s final belief to a reward whose amount depends on the state. We aim to characterize when scoring rules are optimal in the aforementioned dynamic settings.

Indeed, contracts requiring dynamic reports from the agent may be preferred if the principal’s goal is to learn about the evolution of beliefs over time; however, our interest is in settings where the principal is only concerned with terminal beliefs after information acquisition. Even still, one might conjecture that dynamic contracts may be necessary for optimality by allowing the principal to screen the agent using the evolution of their beliefs, thus more effectively incentivizing effort. Perhaps surprisingly, this force play little role in determining whether a single scoring rule at the terminal date is optimal.

Nevertheless, dynamic contracts may, in fact, enable the principal to strengthen incentives provided to the agent. To see why, we observe that the principal can generally provide stronger incentives to acquire information by lowering rewards in any state over which the agent assigns increasing certainty. Specifically, as the agent’s belief drifts toward one state, he becomes increasingly sure of his optimal report. Once the expected payoff from stopping exceeds the value of continued effort, he stops working once and for all. Lowering the reward in the state the agent’s belief drifts toward decreases the expected payoff from stopping, thus providing a stronger dynamic incentive to exert effort. Indeed, we show that contracts with such decreasing reward structures are optimal in general (Theorem 5) and provide sufficient conditions such that this type of dynamic contract strictly outperforms all scoring rules (Theorem 4).

We show that the optimal dynamic contract has an implementation as a scoring rule in three economically meaningful classes of information arrival:

-

1.

stationary environment (Theorem 1) where the belief does not drift in the absence of a Poisson signal;

-

2.

perfect-learning environment (Theorem 2) where the Poisson signals are fully revealing;

-

3.

single-signal environment (Theorem 3) where the belief can only jump in one direction upon receiving a Poisson signal.

In the first case, since the agent’s belief does not change over time, the optimization problem is essentially the same at every point in time. Thus, there is no need to adjust the rewards. In the latter two cases, while the previous discussion suggests the principal may wish to “reoptimize” rewards over time, doing so would lower the agent’s continuation payoff from exerting effort at earlier times, weakening their incentives. Essentially, reoptimization of rewards would redistribute the incentives of the agent from exerting effort across different periods; we show that the optimal trade-off requires no reoptimization in perfect-learning and single-signal environments. By contrast, our conditions for the strict suboptimality of scoring rules in Theorem 4 essentially boils down to a requirement that beliefs drift over time, with a sufficiently strong violation of the second and third conditions.

These results do not imply that the presence of dynamics fails to influence the form of the optimal contract. First, it need not be the case that the optimal scoring rule provides the strongest incentives at the prior, as the principal must balance incentives as the agent’s belief changes. Second, in static settings, the principal’s optimal contract only requires the agent to guess a state, providing a positive reward if the guess is correct and no reward otherwise (Li et al., , 2022); such scoring rule formats may be suboptimal in our dynamic setting even when the optimal contract has an implementation as a scoring rule. Allowing the agent to make a report that ensures strictly positive rewards in either state encourages the agent to exert effort at earlier times by increasing his continuation payoff. This modification is optimal if the rewards in both states are sufficiently low so that this option does not discourage the agent from exerting effort at later times.

Our paper focuses on settings where the principal faces a budget constraint while the agent gathers information via a (discretized) Poisson process, aligning with the applications we had in mind. Section 6 discusses the challenges and techniques for extending our results to environments where the principal can design contracts utilizing public randomization devices, where the information acquisition process may change over time, or where the principal values the reward or is only constrained by an ex-ante budget.

1.2 Related Literature

We build most directly on the literature on scoring rules. Most of this literature considers schemes for eliciting information (e.g., McCarthy, , 1956; Savage, , 1971; Lambert, , 2022).111The fact that scoring rules can condition on the state makes this literature reminiscent of work on mechanism design with ex-post verifiability (e.g., Deb and Mishra, , 2014; DeMarzo et al., , 2005). By contrast, our focus is on how to incentivize its acquisition. Several papers have studied this design problem, including Zermeno, (2011); Carroll, (2019); Li et al., (2022); Neyman et al., (2021); Hartline et al., (2023); Chen and Yu, (2021). Relative to this literature, the crucial distinction is our focus on dynamics. In particular, even though Neyman et al., (2021); Hartline et al., (2023) and Chen and Yu, (2021) have considered models where agents have a dynamic information acquisition process, all those papers make an explicit assumption that the principal can only use a static scoring rule and that the agent is only required to make a single report after the learning process ends. In contrast, the principal in our model can design dynamic contracts for monitoring the learning process and scoring the agent. In dynamic environments, Chambers and Lambert, (2021) show how to design (strictly) incentive compatible dynamic scoring rules, although these do not generally maximize the incentive for information acquisition.

The problem we build on is a dynamic mechanism design problem featuring both adverse selection and moral hazard. Much of this literature focuses on environments where the principal’s goal is to specify an allocation rule as a function of an agent’s type. Pavan et al., (2014) showed how dynamic mechanism design problems without moral hazard can (under regularity conditions) be solved using a suitably defined notion of virtual value, generalizing results tracing from Courty and Li, (2000) that derived a similar formula in a two-period model. Eso and Szentes, (2017); Garrett and Pavan, (2012) study a similar dynamic contracting problem with a single agent, but allowing both adverse selection and moral hazard; Bergemann and Strack, (2015) instead develop an analog under continuous time. Our results on the optimality of static scoring are reminiscent of other work discussing the optimality of static screening in elaborations of the sequential screening model by Courty and Li, (2000) (see, for instance, Krähmer and Strausz, , 2015; Bergemann et al., , 2020). Despite the similarity in the broader agenda of introducing realistic dynamics to otherwise canonical static settings, our problem is not nested within these frameworks. Our work examines how state-contingent rewards influence the incentives for information acquisition, an issue absent from much of this line of work.

An exception is in the literature on contracting for experimentation, which typically considers contracting problems where the possibility of success is uncertain, and where payments can depend on whether success occurs. To our knowledge, Bergemann and Hege, (1998, 2005) are among the first to study this problem, doing so under the assumption that a “success” reveals the state. This Poisson structure, which we generalize, is standard in the subsequent literature. Halac et al., (2016) consider a version of this problem with ex-ante adverse selection; while this paper allows arbitrary transfers, Guo, (2016) considers a delegation setting without transfers. McClellan, (2022) considers a related model, but where information instead takes the form of a Brownian motion and an agent who decides when to stop.

In our setting, the principal cannot extract payments from the agent and can only reward the agent with a prize for which they have no direct value. From this perspective, our contracting problem closely resembles Deb et al., (2018), considering the problem of screening forecasters when the principal can only provide incentives using a state-contingent bounded reward (see also Deb et al., , 2023; Dasgupta, , 2023). This assumption is also present in Hebert and Zhong, (2022), considering a principal-agent problem to keep an agent engaged; while similar to ours, the design problem is rather different as their principal designs an information structure instead of a payment scheme. Wong, (2023) studies a dynamic mechanism design problem with endogenous information and limited transfers, but the principal’s design problem consists of choosing a monitoring technology.

Lastly, a notable recent literature has studied single-agent problems featuring information acquisition, where the agent’s interest in the state is exogenous. Important papers on this topic include Morris and Strack, (2019); Bloedel and Zhong, (2021); Zhong, (2022); Liang et al., (2022); Che and Mierendorff, (2019). We note that such problems often have stationarity naturally embedded in them; given an arbitrary dynamic contract, there is no reason such stationarity should emerge. Partially for this reason, our approach does not require determining the agent’s exact best-response following an arbitrary dynamic contract.

2 Model

A principal contracts with an agent to acquire information about an uncertain state to be publicly revealed after time . Initially, the principal and the agent share a common prior . Our baseline model considers the case where . We assume that the set of dates at which the agent can acquire additional information is , although our results also apply to the high-frequency limit as .

At time , the principal will decide on an action based on the information acquired by the agent. After the state is revealed, the agent receives a reward to be specified by the contract the principal offers. The principal’s payoff in this game is , while the agent’s payoff is . Put differently, the principal has a maximum budget of 1 for rewarding the agent and places no value on the rewards themselves. We assume that both the principal and the agent are risk-neutral. We provide a detailed discussion of our modeling assumption in Section 2.4.

2.1 Information Acquisition

At each time , the agent can choose to exert effort or not. If the agent chooses to exert effort, the agent pays a cost of for some cost parameter . We take the information arrival process to fall into the class of single-success Poisson learning. Specifically, at any time :

-

•

if the agent exerts effort, a “good news” signal arrives with probability and a “bad news” signal arrives with probability when the state is , where and . The agent receives signal if neither nor arrives.

-

•

If the agent does not exert any effort, only signal arrives.

-

•

Once a signal or arrives, no further information can be acquired.

We refer to and as Poisson signals to distinguish them from . Note that although we refer to as “good news” and as “bad news,” we do not mean to suggest that either the principal or the agent has any intrinsic preference over these two signals, but rather do so as a way of distinguishing how we refer to states and signals. We denote the signal space for Poisson signals as and the extended signal space as . Without loss of generality, we assume that , so that the agent’s belief drifts towards state in the absence of a Poisson signal arrival. Note that in our model, while the fact that a Poisson signal arrives at most once implies that the agent’s problem ends after success arrives, it does not necessarily impose that the agent is certain of the state since signals may not be perfectly revealing.

To simplify the exposition, for any time and assuming that the agent has chosen to exert effort for all periods until , we let denote the posterior belief if no Poisson signal arrived before time (including ). Similarly, we let and denote the posterior agent’s belief when receiving Poisson signals and (respectively) exactly at time . We also refer to as the “no-information belief” of the agent at time .

There are several specifications of the model that are of particular interest:

-

•

Stationary environment: In this case, , and hence the agent’s belief absent a Poisson signal does not drift over time, i.e., for all .

-

•

Perfect-learning environment: In this case, , and hence the agent perfectly knows the state after receiving a Poisson signal, i.e, and for all .

-

•

Single-signal environment: In this case, either or . Without loss of generality, we focus on the former case, i.e., the agent’s belief drifts towards state when not receiving any Poisson signal and jumps towards state after receiving one.

Note that if , the good news signal does not reveal the state; the same observation holds for the bad news signal.

2.2 Contracting

The principal does not observe the effort choice or the signal received by the agent at any time . Instead, the principal can design contracts to reward the agent to incentivize costly information acquisition. Moreover, the designed contract must satisfy the budget constraints on rewards.

At any time , let be the message space of the agent. The history at time is denoted as . Let be the set of all possible histories at time . Before time 0, the principal commits to a reward scheme

where is the fractional reward of the agent when his history of reports is , and the realized state is . An alternative interpretation is that the principal has an indivisible reward, with denoting the probability that the agent receives the reward.222Note that although we allow randomization over the event that the agent receives the full budget, the contracts we defined above are essentially deterministic since the probability that the agent gets the full budget is a deterministic function of the history of reports. In this paper, we focus on deterministic contracts, deferring our discussion of the possibility of randomization influences the results in Section Section 6.1. The following formalizes the timeline of our model:

-

•

The principal commits to a contract ; the state is drawn according to the prior, .

-

•

At any time ,

-

–

the agent chooses whether to exert effort, and pays cost if he exerts effort;

-

–

a Poisson signal arrives with probability if the agent exerts effort and no Poisson signal has arrived before ; signal arrives otherwise;

-

–

after observing this outcome, the agent sends a message to the principal.

-

–

-

•

The principal decides on an action . The state is then publicly revealed, and the agent receives reward .

The principal’s objective is to maximize her expected payoff subject to the budget constraint.

2.3 Scoring Rules and Static Contracts

The main result of our paper is to provide sufficient conditions under which an optimal contract only requires a single, final report from the agent for the aggregated information. Using the terminology from information elicitation, a scoring rule for eliciting the agent’s subjective belief is a mapping from the posterior space and the state space to a real number; we refer to the corresponding real number output by this function as the score. A scoring rule is essentially a static contract described in our model.

Definition 1.

A dynamic contract can be implemented as a scoring rule if the message space , and for any history of reports with last message , we have for all states .

2.4 Discussion

In this section, we briefly describe some of the major assumptions of our model and what they reflect. The first assumption is that the principal has no direct preference over the transfer provided to the agent. One case where this is reasonable is if the mechanism through which the principal can reward the agent is itself non-monetary. For instance, it could be that the principal can either provide some benefit to the agent (e.g., deciding to hire them, as in Deb et al., (2018), or a promotion) or access to some special recognition (e.g., a good grade on an exam). Another is if the principal is herself budget-constrained and where the value of any residual transfer is negligible compared to the value of additional information acquisition. Similarly, it may be that while the principal designs the contract, the award itself is rigidly set by a third party (e.g., by a granting authority), implying that the principal is not the residual claimant of any reward kept from the agent.

Second, we assume that the agent privately observes the signal itself. This assumption reflects the agent’s particular expertise in evaluating evidence relative to the principal. Even in cases where signals correspond to tangible objects, however, our analysis is relevant insofar as such signals could be easily falsified or fabricated by the agent. In data analysis settings, for instance, fraud may take substantial time or effort to uncover, making it impossible to condition on this outcome.

Next, we assume that the agent can observe at most one success without assuming this success perfectly reveals the state. This assumption greatly simplifies the analysis by allowing us to view the resulting experiment’s informativeness as synonymous with the time the agent exerts effort in the absence of success. This assumption is automatically satisfied when the Poisson signals are sufficiently informative, disincentivizing the agent from exerting effort after receiving a Poisson signal given any feasible contract. In cases where signals correspond to evidence, the assumption reflects the existence of a single piece of evidence. As an example, a defense analyst may be interested in assessing a threat from some nefarious actor, with the evidence corresponding to images from the actor’s headquarters. While only one headquarters might exist, the actor’s intent may or may not be discernable from images of it. In a biomedical context, a researcher may be interested in successfully performing a particular chemical reaction as part of the experiment. In this case, while performing the reaction twice generates only negligible additional information, even perfect knowledge of the subsequent outcome only partially reveals whether a treatment based on it will be effective and worth investment.

Lastly, we take the state to be contractible. There are many channels through which contractability would emerge—for instance, if the principal’s action reveals the correct decision ex-post. This conditioning incentivizes the agent to acquire information by making their reward sensitive to the true state.

3 Preliminaries

This section illustrates optimal scoring rules for incentivizing effort. We also provide a preliminary simplification of the space of agent (effort) strategies and the set of contracts the principal needs to consider. Finally, we introduce an auxiliary static model to illustrate the central tensions in designing optimal contracts in the dynamic model.

3.1 Illustrations

To highlight some preliminary intuition regarding how the principal optimizes the agent’s contract, we first describe the performance of scoring rules that ask the agent to guess a state and provide a reward if they are correct. To obtain closed-form solutions, we describe the agent’s payoff as against such a scoring rule and further assume that there is a single source and that signals are fully revealing, i.e., . The optimality of such scoring rules in this environment will follow from our general analysis in Theorem 2; here, we illustrate the tradeoffs the principal may face when setting the agent’s rewards.

Suppose the rewards ensure that the agent will be indifferent between exerting effort and not at time , working until then. Denote the two scores the principal offers as and , the former being the selected score if no signal arrives and the latter being the score selected if the signal arrives. One can show (see Section A.5 for details) that the stopping belief is:

We note that this expression is independent of the reward . From this, we conclude that the principal should always set , as doing so relaxes the agent’s moral hazard problem as much as possible. As we shall see, this conclusion holds whenever learning is perfect. This argument yields a stopping belief of , and a stopping payoff of .

Solving for the agent’s value function, we obtain, for some constant pinned down by the agent’s payoff at the stopping belief:

We can verify that from this solution. One can also show , so that the value function is everywhere above . Thus, the agent would never shirk and choose option prior to time ; so, as long as the value function is also above , the moral hazard constraint does not bind before .

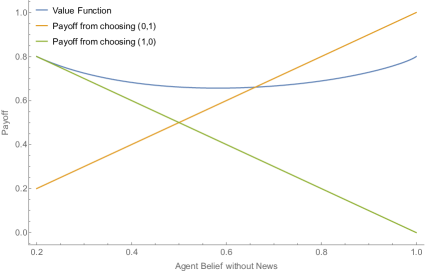

If the principal did not need to worry about the moral hazard constraint binding, then it is clear from examining the stopping belief that the principal should set . However, Figure 1 shows that if the agent is too optimistic that , then the agent prefers to never exert effort instead of exerting effort until time . As the agent’s belief increases from the stopping belief, the value function is strictly larger than the optimal payoff from stopping. Nevertheless, at some point, the value function becomes lower than the payoff under the score . In this case, the moral hazard constraint binds at the initial time.

If the agent’s payoff from exerting effort until is just below the payoff from choosing the score , then the moral hazard constraint binds, and the principal should set . Note that a decrease in lowers both the payoff from stopping immediately, as well as the value function; however, the impact on the payoff from immediately stopping is larger since the prospect of obtaining following “no news” induces the agent to work, and this does not vary with . So, if the moral hazard constraint is violated at time 0, then the principal should lower so that it binds.

So, consider how the scoring rule changes as (the initial belief that ) increases:

-

•

For , it is impossible to induce the agent to acquire any information.

-

•

There exists such that when , the optimal scoring rule involves .

-

•

There exists such that when , the optimal scoring rule involves , with the exact value pinned down by the condition that the agent is indifferent between (i) working continuously until their belief is and (ii) never working at all.

-

•

For , it is impossible to induce the agent to acquire any information.

This observation clarifies why the principal may want to (but cannot) reoptimize the scoring rule. While giving the full reward from guessing state 1 is optimal if the agent initially assigns it probability less than , for beliefs above this value, the reward from guessing state 1 must decrease. Now, even if the agent’s initial belief that is high, it will eventually decrease below with positive probability. On the other hand, offering the full reward when guessing state 1 after this time would defeat the initial purpose of starting with the lower reward—doing so would lead the agent to shirk and lie. In order to prevent this from happening, the principal must keep the initial reward low.

3.2 Stopping Strategies

We now show that one of the agent’s optimal strategies for exerting effort is a simple stopping strategy, simplifying the principal’s objective to maximization of the agent’s stopping time.

The agent can generally choose arbitrary, complex strategies for exerting effort. For example, the agent could wait for several periods before starting or randomize over such decisions. Nevertheless, we note that it is without loss for the agent to use a stopping strategy —that is, slightly overloading the notation as a stopping time under a stopping strategy, we can assume that the agent chooses to exert effort at every time , conditional on not having received any Poisson signal.

Lemma 1.

Given any contract and any best response of the agent with maximum effort length conditional on not receiving any Poisson signal,333If the agent uses randomized strategies, is the maximum effort length among all realizations. there exists a stopping strategy with that is also optimal for the agent.

Note that the maximum effort duration conditional on no Poisson signal arrival uniquely determines the information acquired by the agent. Moreover, whenever the agent works longer, the aggregated information acquired is Blackwell more informative, implying that the principal’s utility following the agent’s information acquisition is higher for any possible (principal) utility function. Therefore, Lemma 1 implies that the principal would seek to implement—and the agent would be willing to use—stopping strategies. Hence, it is without loss of generality to focus on them.

The proof for Lemma 1 is simple. Given any contract and any strategy of the agent (for instance, if the agent were potentially pausing effort for some time and resuming effort afterward), the agent does weakly better by front-loading effort to receive information earlier since this weakly increases his expected reward from the principal without increasing expected cost. Therefore, the resulting stopping strategy with the same effort length conditional on not receiving Poisson signals must also be optimal.

Principal’s objective

By restricting attention to stopping strategies, the principal’s payoff given any contract is uniquely determined by the stopping time . Moreover, regardless of the principal’s valuation function for making decisions, the principal’s expected payoff is higher when is longer. As a result, the principal’s problem simplifies to designing a contract that maximizes the stopping time subject to the budget constraint. Under this objective, the design of the optimal contracts does not depend on the details of the principal’s valuation function .

3.3 Menu Representation

As per the discussion in Section 3.2, we henceforth assume that the agent always chooses a stopping strategy for exerting effort. This observation further simplifies communication between the parties in the optimal contract. In particular, the agent need not report whether he has exerted effort in the current period. Instead, it is sufficient to incentivize the agent to truthfully report or immediately once observed, implicitly assuming that the agent indeed exerts effort in every period before the report.

We describe this menu representation for the dynamic contracts the principal might offer. The principal commits to a sequence of menu options at time ; at any time , the agent can make a one-time, irrevocable choice from the set of available menus based on his posterior belief. Lemma 2 formalizes this menu representation.

Given any reward function , let

be the agent’s expected utility given reward when his belief is . In the binary state model (i.e., ) we consider in this paper, we also represent the reward function as , where is the reward for state being and is the reward for state being .

Lemma 2 (menu representation).

Any dynamic contract implementing optimal stopping time is equivalent to a sequence of menu options where . At any time , the agent can make a one-time choice for the menu option from the subset , with the agent rewarded according to after time . Moreover, at any time , the utility of the agent with belief is maximized by picking the menu option , i.e., for any and , or for and ,

| (IC) |

Section A.1 contains the proof of Lemma 2. Note that in Eq. IC, the agent’s incentives are uni-directional in time. That is, it is sufficient to consider the incentive constraints where the agent does not prefer to deviate from a truthful report when receiving an informative signal later.

Lemma 2 dramatically simplifies the space of contracts the principal needs to consider. For example, it allows us to convert the design of the optimal contracts into a sequence of linear programs such that the sequence of menu options in the optimal contract can be computed efficiently. We provide the details of the computational methods in Section A.2.

To simplify the exposition in later sections, given the menu representation in Lemma 2 for any contract , for any time and any signal , we denote as the agent’s utility for not exerting effort in any time after when his current belief is . We also omit from the notation when it is clear from the context. Moreover, for any , we denote

as the menu option the agent would choose at time if his belief were . Let .

3.4 An Auxiliary Static Model

To further illustrate the tensions in the dynamic model, we take a slight detour by considering an auxiliary static model with binary states studied by Li et al., (2022). In Section 4, we will show how to connect this static model to our dynamic model and use this connection to prove the optimality of scoring rules in general dynamic environments. First, we review the characterizations of optimal scoring rules in the static model and their implications in this section.

Binary Effort Static Game

Consider an auxiliary static setting with binary effort. That is, the agent can choose to either not exert effort, leaving their prior belief unchanged, or exert effort and receive a signal according to signal structure where the signal space for the static setting is a measurable set. In the static model, the principal’s objective is to find a scoring rule that maximizes the expected difference in scores between exerting effort and not exerting effort, subject to a budget constraint on the scores. That is, letting be the distribution over posterior given the signal structure , the principal maximizes

subject to the constraint that for all and . Intuitively, given any cost of exerting effort in the static model, the agent is more likely to be incentivized to exert effort when the score difference is larger. In the static model, call a scoring rule optimal if it provides the maximum score increase to the agent from exerting effort.

Optimal Scoring Rules

In the static model, it turns out that optimal scoring rules fall into the class of V-shaped scoring rules. A V-shaped scoring rule has an implementation whereby the agent guesses a state and obtains some reward amount (depending on the state), provided his guess is correct. The agent receives 0 if his guess is wrong.

Definition 2 (Li et al., , 2022).

A scoring rule is V-shaped with parameters if

We say is a V-shaped scoring rule with kink at if the parameters satisfies if and if .

The terminology of the scoring rule as “V-shaped” comes from the property that the expected score is a V-shaped function. Furthermore, given any V-shaped scoring rule with kink at , the agent with prior belief is indifferent between guessing the state is either 0 or 1.

Proposition 1 (Li et al., , 2022).

In the binary effort static game, for any prior , a V-shaped scoring rule with kink at prior is optimal for all signal structures .

Proposition 1 provides an optimal solution for the static game. According to Li et al., , 2022, the V-shaped scoring rule is essentially the uniquely optimal scoring rule when the agent’s signals, received after exerting effort, are not fully revealing.

The underlying intuition for Proposition 1 is that in static environments, subject to the convexity constraint and the constraint that the expected score at the prior is a constant, V-shaped scoring rules maximize the expected score at all posteriors, thus providing the maximum incentives for the agent to exert effort. We emphasize that Proposition 1 implies that in the static model, the optimal scoring rule only depends on the prior , not on the signal structure .

Proposition 1 illustrates one of the tensions in designing optimal contracts in dynamic environments. Ideally, the principal would want to design contracts that provide the optimal incentives for the agent to exert effort at any time , since doing so would make them willing to work for the longest time possible. However, since the agent’s belief may drift over time, the scoring rules that provide the optimal incentives at time can be inconsistent with the scoring rules that are optimal for time when . The dynamic incentives of the agent further imply that the optimal incentives cannot be achieved simultaneously at every time . In Section 4, we will show that even with such tensions in the dynamic model, there are several canonical dynamic environments in which optimal contracts have an implementation as a scoring rule. We emphasize that this does not imply that the optimal scoring rules for the dynamic model necessarily coincide with the optimal scoring rules for the static model, and we will illustrate environments in which the optimal scoring rules for the dynamic model exhibit novel features in Sections 4.2 and 4.3.

4 Optimal Contracts as Scoring Rules

This section presents our main results on the implementation of the optimal contract as a static scoring rule in three canonical environments: stationary, perfect-learning and single-signal. Section 5 provides a partial converse to these results by showing that dynamic structures can be necessary to implement the optimal contract when all three conditions are violated. The main idea for the arguments in this section is to decompose the dynamic problem into multiple static problems. Specifically, we will consider a continuation game at any time where the agent only has two choices: To shirk forever or exert effort according to a specific strategy. Such continuation games essentially coincide with the static model introduced in Section 3.4. We will show that for any dynamic contract , there exists a scoring rule that provides stronger incentives for the agent to exert effort in all continuation games, which further implies that the agent has stronger incentives to exert effort for a longer duration given scoring rule in the dynamic model. Appendix B contains the missing proofs in this section.

Continuation Game

For any time , let be the continuation game between and . Specifically, the continuation game is a static game with prior belief . Moreover, the agent has binary effort in the continuation game, i.e., the agent can choose either to (a) not exert effort or (b) follow the strategy of exerting effort until time (including time ) or a Poisson signal arrives. The cost of effort in this continuation game is times the expected number of periods the agent exerts effort between and . Note that at any time in the dynamic environment, the agent has incentives to exert effort at time if there exists such that the agent has incentives to exert effort in the continuation game . For any contact with stopping time , we say is the continuation game at time for contract . In the rest of the paper, we omit the subscript of from the notation when the contract is clear from context.

In the continuation game, for , let be the probability mass function of receiving a Poisson signal at time conditional on not receiving Poisson signals before time , and let be the corresponding cumulative distribution function. Given any contract with a sequence of menu options , we refer to as the no information payoff of the agent, and

as the continuation payoff of the agent in the continuation game . We also omit in the notations if it is clear from context. In the continuation game , the agent has incentives to exert effort if the payoff difference is at least his cost of effort.

4.1 Stationary Model

The simplest case of interest is the stationary model, where the agent’s no information belief for all . In this simple case, all continuation games at any time share the same prior belief. As illustrated in Proposition 1, the optimal scoring rules for all continuation games are the same. Therefore, the tension over time does not exist. In this case, it is straightforward to show that the optimal contract has an implementation as a V-shaped scoring rule with kink at the prior , which is also the optimal scoring rule in the static model.

Theorem 1.

In the stationary model, an optimal contract can be implemented as a V-shaped scoring rule with kink prior , for any prior and signal arrival rate.

4.2 Perfect-learning Environment

Outside of the stationary model, the no information belief of the agent drifts over time, meaning that the principal cannot provide optimal incentives to the agent in every continuation game. This section focuses on the perfect-learning environment where the agent fully learns the state upon receiving a Poisson signal. We show that the optimal contract has an implementation as a scoring rule for this environment. However, since the principal’s goal is to incentivize dynamic effort choices, the particular optimal scoring rule will differ from the optimal scoring rule in the static model.

Theorem 2.

An optimal contract exists with an implementation as a V-shaped scoring rule with parameters and in the perfect-learning environment

Note that, unlike the stationary environment, although the optimal contract has an implementation as a static scoring rule, the kink of the scoring rule may not be at the prior . In particular, the kink of the scoring rule depends on the parameter , chosen to balance the agent’s incentive to exert effort at both time and the stopping time . This observation illustrates the phenomenon that, despite the optimal contract having an implementation as a scoring rule, it does not coincide with the optimal scoring rule from the static model, and the dynamics in the effort choices still affect the design of optimal contracts.

Next, we show how to identify the optimal parameter in the perfect-learning environment. We first ignore the constraint imposed by the time horizon momentarily. Given a V-shaped scoring rule with parameters and , recall that is the agent’s utility of from not exerting effort after time . Let be the optimal utility of the agent, with respect to the prior belief , from exerting effort in at least one period starting from time (including ). By the Envelope Theorem, is convex in the no information belief with its derivative between and . We let if for all . Otherwise, let and . The agent has incentives to exert effort at time given scoring rule if and only if . See Figure 2 for an illustration. In particular, the agent has incentives to exert effort at time if and only if .

Lemma 3.

Both and are weakly decreasing in .

That is, by increasing the reward for prediction state 1 correctly in the scoring rule, the agent has incentives to exert effort for longer, i.e., is smaller, but the agent has a weaker incentive to exert effort at time , i.e., is smaller. This tension illustrates an interesting dynamic effect in our model when the time horizon is sufficiently large. That is, there exist such that the agent can be incentivized to work when either the principal seeks to have the no information belief drift from (a) to or (b) to , but not when seeking to have this belief drift from to .

Let . That is, is the maximum belief of the agent that can be incentivized to exert effort given any scoring rule. Thus, we can focus on the case where . When there is a time horizon constraint for exerting effort, let if and let be the minimum parameter such that otherwise.

Proposition 2.

In the perfect-learning environment, no contract incentivizes the agent to exert effort if or . Otherwise, the optimal parameter in a V-shaped scoring rule is the maximum value below such that .

Intuitively, the optimal parameter maximizes the stopping time subject to the constraint that the agent has incentives to exert effort at time .

We illustrate the ideas behind the proof of Theorem 2. We first show that in perfect-learning environments, it is without loss of optimality to consider contracts where the menu options provide a maximum reward to the agent for receiving a bad news signal or no Poisson signal at all when the state is . Recall that is the state that the agent’s posterior belief drifts to absent a Poisson signal.

Lemma 4.

In the perfect-learning environment, for any prior and any signal arrival probabilities , there exists an optimal contract with a sequence of menu options such that for any .

Intuitively, for any contract with stopping time , we consider another dynamic contract that rewards the agent the maximum amount of following state conditional on the event that the agent receives a bad news signal at any time before or no Poisson signal until time . In the perfect-learning environment, such an event occurs with probability 1 if the state is . Therefore, whenever the state is , the agent enjoys the full increase in rewards in any continuation game for exerting effort. By contrast, the increase in the expected reward when not exerting effort in the continuation game is at most the prior probability of state times the reward increase. Thus, the agent has stronger incentives to exert effort in all continuation games given contract , which implies that contract must also be optimal in the dynamic model.

Next, we show that offering a single menu option for rewarding good news signals is also sufficient. Intuitively, the dynamic incentives of the agent imply that in any contract , the agent’s reward for receiving a good news signal must decline over time. We show that by decreasing earlier rewards to make the agent’s utility from early stopping sufficiently low and increasing later rewards to make the reward from continuing effort sufficiently high, the resulting contract has an implementation as a scoring rule, and the agent’s incentive for exerting effort increases weakly in all continuation games given the new contract. This idea is illustrated formally in the following proof.

Proof of Theorem 2.

By Lemma 4, it is without loss of optimality to focus on contract with a sequence of menu options such that for any . In addition, since signals are perfectly revealing, it is without loss to assume that and the incentive constraints imply that is weakly decreasing in .

Let be the maximum time such that an agent with no information belief weakly prefers menu option compared to . Since both and are weakly decreasing in , an agent with posterior belief weakly prefers compared to for any , and weakly prefers compared to for any . Now consider another contract that offers only two menu options, and , at every time . Contract can be implemented as a V-shaped scoring rule with parameters and . Moreover, at any time ,

-

•

if , in the continuation game , the agent’s utility for not exerting effort is the same in both contract and because the agent with no information belief will choose the same menu option . However, the agent’s utility for exerting effort is weakly higher in contract since the reward from receiving a good news signal at time weakly decreases in .

-

•

if , in the continuation game , by changing the contract from to , the decrease in agent’s utility for not exerting effort is exactly by changing the optimal menu option for no information belief from to . However, the decrease in the agent’s utility for exerting effort in is at most since the decrease in reward for receiving a good news signal is at most and it only occurs when the state is .

Therefore, given contract , the agent has stronger incentives to exert effort in all continuation games with , which implies that and hence contract is also optimal. ∎

4.3 Single-signal Environment

In this section, we consider the single-signal environment where the agent’s belief drifts towards in the absence of a Poisson signal and jumps towards when a Poisson signal arrives. In the single-signal environment, we do not assume that the signals are fully revealing.

Theorem 3.

An optimal contract with an implementation as a scoring rule exists in the single-signal environment.

Note that in the single-signal environment, although the optimal contract can be implemented as a static scoring rule, it may not be implementable as a V-shaped scoring rule when the signals are not fully revealing. Put differently, the principal may not want to simply let the agent guess the state and reward the agent only following a correct guess. By contrast, the principal may benefit from rewarding the agent even when the guess is wrong.

Consider an interpretation of the minimum reward across the two states as the “base reward” and the difference between the rewards as the “bonus reward.” From this perspective, our results indicate that it may be necessary to consider scoring rules where the base reward is strictly positive. This observation may seem counterintuitive, as providing a strictly positive base reward strictly decreases the maximum bonus reward for the agent due to the budget constraint. In principle, providing a positive base reward should lower the agent’s utility increase when correctly guessing the state and, hence, subsequently lower the agent’s incentive for exerting effort.

The correct intuition is as follows: providing a strictly positive base reward to the agent at time only decreases the agent’s incentive to exert effort at time ; however, it increases the agent’s incentive to exert effort at earlier times since the agent may expect high rewards for exerting effort, even though he might make mistakes in guessing the states after receiving (imperfectly informative) Poisson signals. This modification benefits the principal if the agent’s incentive constraint for exerting effort initially binds at time 0, but becomes slack at intermediate time . As illustrated in Figure 3 and in Section 4.2, by implementing the optimal V-shaped scoring rule, the agent’s incentive for exerting effort is binding only at the extreme time with belief and time with belief . In this case, since the signals are not perfectly revealing, there may exist a time such that . By providing an additional menu option with strictly positive base reward in the scoring rule to increase the agent’s utility at beliefs (e.g., the additional menu option illustrated in Figure 3), the agent’s incentive constraint for exerting effort at time is relaxed and the contract thus provides the agent incentives to exert effort following more extreme prior beliefs without influencing the stopping belief .

We illustrate the main ideas for Theorem 3. Note that given any (static) scoring rule, the utility of the agent from not exerting effort is a convex function of his no information belief (see Lemma 8). Therefore, to show that the optimal contract can be implemented as a scoring rule, we first show that it is without loss to focus on dynamic contracts where the is convex in .

Lemma 5.

In the single-signal environment, an optimal contract exists with the no-information utility convex in .

Intuitively, in the optimal contract, if the no-information utility is not convex, one of the following cases holds at time , the earliest time such that the utility is non-convex:

-

•

the agent’s incentive for exerting effort is slack at time . In this case, we can increase the no-information utility at time by increasing the rewards in menu option such that either (a) the incentive for exerting effort at time will bind, or (b) the no-information utility will become convex at .

-

•

the agent’s incentive for exerting effort is slack at time . In this case, the combination of the no-information utility function’s non-convexity and the contract’s incentive constraint actually implies that the agent will have a strict incentive to stop exerting effort at time . See Figure 6 in Section B.3 for an illustration.

Note that although the convexity in no-information utility function implies that the optimal contract has an implementation as a scoring rule, it does not necessarily imply that the resulting scoring rule must satisfy the ex-post budget constraint or the ex-post individual rationality constraint. For example, consider a convex no-information utility function . A simple dynamic contract that implements this no-information utility function is to offer a constant reward at time regardless of the realization of the state. However, if the principal wants to implement this utility function using a static scoring rule, by Lemma 8, the menu option for belief must be , which violates the ex post individual rationality constraint.

Primarily, a violation of the ex-post budget constraint or the individual rationality constraint emerges because the no-information utility function is too convex. In this case, we can flatten the no-information utility by decreasing the reward to the agent at earlier times. We can show that by flattening the no-information utility, the decrease in no-information utility is weakly larger than the decrease in continuation payoff in all continuation games, and hence, the agent has stronger incentives to exert effort. Figure 4 illustrates this idea, with details provided in Section B.3.

5 Optimality of Dynamic Contracts

This section shows that the optimal scoring rule must be dynamic when (i) signals are noisy and (ii) the drift is sufficiently slow. More precisely, we consider cases where both good and bad news signals can arrive with strictly positive probability if the agent exerts effort. That is, we have and . Recall that we have assumed that , meaning that “no news is bad news.” Taking the drift to be slow means that the above difference is small. Signals being noisy means that they do not reveal the state.

Let and let be the maximum time such that . Intuitively, is the maximum calendar time such that the agent can be incentivized to exert effort in any contract when the prior is .

Lemma 6.

The stopping time satisfies , given any prior , arrival rates , cost of effort , and contract that satisfies the budget constraint.

Appendix C contains this section’s missing proofs.

Theorem 4.

Given any prior , any cost of effort , and any constant , there exists such that for any and satisfying

-

•

; (sufficient-incentive)

-

•

; (noisy-signal)

-

•

, (slow-drift)

any static scoring rule is strictly suboptimal.

Theorem 4 provides sufficient conditions that necessitate the use of complex dynamic structures in the optimal contract to incentivize dynamic effort. The condition that implies that the time horizon will not be a binding constraint for the agent to exert effort. The sufficient incentive condition avoids trivial solutions by ensuring that the cost of effort is sufficiently small compared to the difference in arrival rates of the good news signal, so that the agent has incentives to exert effort for a strictly positive length of time in the optimal contract. The noisy-signal condition rules out the perfect-learning environment and the single-signal environment, and the slow-drift condition rules out the stationary environment. Moreover, the single-signal environment can also be viewed as the extreme opposite of the slow-drift condition, since the difference in arrival rates of the signals is maximal and the belief drifts to 0 quickly in the absence of a Poisson arrival.

A substantial assumption that appears harmless is that . Note that combining this with our restriction to environments where the belief absent a Poisson signal drifts towards 0, our theorem only applies to environments where the agent’s posterior belief absent a Poisson signal becomes more polarized towards the more likely states given the prior belief. This restriction ensures that the following myopic-incentive contract we define is incentive compatible for the agent.

Definition 3.

When prior , a contract with menu options is a myopic-incentive contract if and for any .

Intuitively, the sequence of menu options offered by the myopic-incentive contract is such that at any time , the agent with belief is indifferent between all menu options offered at time . See Figure 5 for an illustration. The condition that the belief absent a Poisson signal becomes increasingly polarized implies that the rewards in menu options decrease over time. This property is necessary for the constructed contract to be incentive-compatible for the agent.

Note that the construction of menu options in the myopic-incentive contract at any time resembles the V-shaped scoring rules that are optimal for the static model with prior . However, the myopic-incentive contract does not provide the optimal incentive for the agent to exert effort in all continuation games. This observation holds because, in the continuation game , the agent may receive a Poisson signal after time , when the reward for reporting the received signal decreases. Thus, the myopic-incentive contract may not always be optimal for the principal. Nonetheless, we show that when the drift of belief is sufficiently slow, the myopic-incentive contract provides incentives close to the optimal contract.

Lemma 7.

Given any prior , any cost of effort , any constant , and any , there exists such that for any and any satisfying that for all and , and

-

•

; (sufficient-incentive)

-

•

, (slow-drift)

letting be the myopic-incentive contract (Definition 3), we have .

When the drift of no information belief is sufficiently slow compared to the arrival rates of the Poisson signals, with sufficiently high probability, the agent will receive a Poisson signal before the no information belief drifts far away from his initial belief. In this case, the decrease in rewards over time in the myopic-incentive contract does not significantly weaken the agent’s incentive for exerting effort. Hence, the myopic-incentive contract is approximately optimal for the principal.

By contrast, if the principal instead uses a contract that can be implemented as a scoring rule, given stopping time in the optimal contract , this scoring rule must be close to the optimal scoring rule in the continuation game for any that is sufficiently close to in order to incentivize the agent to exert effort in continuation game . However, when the signals are noisy, as illustrated in Section A.4, such scoring rules fail to provide sufficient incentives for the agent to exert effort at time , leading to a contradiction. Intuitively,the myopic-incentive contract avoids this conflict in incentives by providing higher rewards to the agent upon receiving a bad new signal without affecting the agent’s incentive to report the acquired information truthfully. In particular, higher rewards upon Poisson signal arrivals strengthen the agent’s incentives to exert effort at any time .

General characterizations

In Lemma 7, we construct the myopic-incentive contract that is approximately optimal when the drift is slow and the belief absent a Poisson signal is polarizing. Although the stated contract is generally not fully optimal, a similar decreasing reward structure does, in fact, characterize the principal’s exact optimum.

To simplify notation, first recall that any menu option has a representation as a tuple . For any pair of menu options , we define if and . That is, if is at most in all components.

Theorem 5.

For any prior and any signal arrival rates , there exists an optimal contract with optimal stopping time and a sequence of menu options such that (1) ; (2) for all ; (3) if ; and (4) for any ,

| s.t. |

Compared to the menu representation in Lemma 2, the simplification in Theorem 5 is the optimality of providing a decreasing sequence of rewards when receiving a bad news signal in both states. Additionally, the optimal sequence of rewards for signal satisfies the condition that the contract initially maintains the maximum score for state and reduces the reward for state . This phase is followed by a decrease in the reward for state , maintaining the minimum score for state . Recall that state represents the state toward which the agent’s belief drifts absent a Poisson signal. Furthermore, the sequence of rewards following bad news signals uniquely determines the optimal contracts. In other words, given the rewards for receiving bad news signals, the rewards for receiving good news signals maximize the agent’s utility while ensuring that the agent with belief weakly prefers the menu option for signal over for all times .

However, it is worth noting that Theorem 5 does not specify the rate of reward decrease in the optimal contract, which depends on the primitives of the model. While the optimal sequence of rewards can be efficiently computed through linear programming (for details, refer to Section A.2), it may not have simple closed-form characterizations. Despite the challenges of deriving closed-form characterizations, our results in Section 4 still show that maintaining constant rewards over time is optimal in several canonical environments.

6 Extensions and Discussions

We now turn to some extensions of the main model, particularly those related to randomized contracts, non-stationary information acquisition, and ex-ante budget constraints. We show how to generalize our results and techniques to such environments. Finally, we conclude our paper and propose several open questions in Section 6.4.

6.1 Randomized Contracts

Although deterministic contracts are appealing for practical applications, in some cases, a principal could commit to randomized contracts with the help of a public randomization device. To speak to this possibility, let be a sequence of random variables with drawn from a uniform distribution in . A randomized contract is a mapping

Crucially, in randomized contracts, at any time , the history of the randomization device is publicly revealed to the agent before determining his choice of effort or the message sent to the principal. The randomization revealed before affects the agent’s incentives after time , and without it, such contracts reduce back to deterministic contracts.

Given randomized contracts, the agent’s optimal strategy need not be a simple stopping strategy. In particular, the agent may decide whether to work or not depending on the public randomization’s past realizations. The agent may also strategically delay exerting effort to wait for the realization of the public randomization. As a result, the simplified objective of maximizing the stopping time of the agent is not appropriate for randomized contracts, and we need to consider the original objective of maximizing expected payoff subject to the budget constraint.

When randomized contracts are allowed, principal objective functions could exist under which randomized contracts are beneficial. The main intuition is that at some time , the principal can randomly inflate or decrease the rewards of the agent in the menu options, setting the probability of a decrease to be much larger to preserve the agent’s dynamic incentives for truthful reporting. Then, after time , with a small probability, rewards inflate, and the agent has incentives to exert effort for longer without a Poisson signal arrival— i.e., the realized stopping time increases. Such a modification is beneficial if the principal only values extreme posterior beliefs.

To illustrate this intuition more formally, consider an environment where learning is perfect and only good news signal arrives with positive probability. By Theorem 2, under deterministic contracts, a V-shaped scoring rule with parameters and implements the optimal contract . Moreover, when the time horizon is sufficiently large, is chosen such that the agent with prior belief is indifferent between exerting effort or not, and it is easy to construct instances where . Let be the stopping time in the optimal deterministic contract, and let be the stopping belief when the agent never receives any Poisson signals.

Now, suppose the principal faces a binary decision to make at time . That is, . The payoff of the principal is for all , and ; plainly, the principal only seeks to change her action from 1 to 0 if the posterior belief is below . In this case, the principal’s benefit from acquiring information from the agent using a deterministic contract is 0. However, the following argument shows that the principal’s payoff from a randomized contract can be strictly positive. Let be the maximum number such that (1) the agent has strict incentives to exert effort until time in the absence of a Poisson signal given menu options and ; and (2) the agent can be incentivized to exert effort given menu options and when the prior belief is . Now consider the randomized contract that provides menu options and from time to , and after time , the principal offers menu options and with probability , offers menu options and with probability , and offers the same menu options and with the rest probabilities. It is easy to verify that with sufficiently small , the agent still incentives to exert effort at any time . Moreover, after time , with probability , the realized menu options are and , and the agent can be incentivized to exert effort to a time strictly larger than in the absence of a Poisson signal. Therefore, randomized contract provides a strictly positive payoff to the principal, outperforming all deterministic contracts.

6.2 Non-stationary Environments

Our model assumes that the cost of acquiring information is fixed over time, as is the mapping from states into signals when the agent exerts effort. On the other hand, many of our techniques and results do not rely on these assumptions, particularly as we focus on maximizing the incentive for the agent to exert effort. Our results extend unchanged if the cost of exerting effort is , whenever the agent has exerted effort for units of time and is a non-decreasing function. In this case, the agent’s strategy again without loss is a stopping time, and identical arguments imply that scoring rules maximize the incentive to exert effort under any of the three environments discussed.

We can similarly allow for time dependence in the informational environment. Specifically, we can allow for the arrival rates of signals at any time to depend on the amount of effort the agent has exerted until that point. That is, suppose that if the agent has exerted effort for units of time, then exerting effort produces a good news signal arrives in state with probability , and a bad news signal with probability (and no signal with complementary probability). While seemingly minor, this modification induces more richness in the set of possible terminal beliefs as a function of the effort history—for instance, if the terminal beliefs are always in the set , despite drifting over time.

Our proof techniques did not make use of the particular belief paths induced by constant arrival rates and hence extend to this case, with the minor exception that Theorem 3 requires to be weakly monotone as a function of time (a property that holds when the arrival rate is constant). Otherwise, as long as parameters stay within each environment articulated in Section 4, the proofs of these results extend unchanged.

6.3 Ex Ante Budget Constraints

In this paper, we require the principal’s budget constraint to be satisfied ex-post, and a natural extension is to relax it by considering ex-ante budget constraints. Note that in our model, we still need to impose limited liability on the agent—in other words, the reward should satisfy ex-post. Suppose the ex-ante individual rationality constraint replaces the ex-post limited liability constraint. In that case, there is no constraint on the rewards for off-path behaviors of the agent. Hence, the principal can easily implement the first best, where the agent’s total cost of effort equals the ex-ante budget, by designing contracts that punish the agent for deviation. Therefore, we focus on the model with ex-ante budget constraints and ex-post limited liability constraints.

We show that in the special case where the conditions in both perfect-learning environments and single-signal environments are satisfied, i.e., when and only , the optimal contract can also be implemented as a scoring rule. Section D.1 contains details for this claim. This observation illustrates that the optimality of static contracts extends under ex-ante budget constraints under natural assumptions. We conjecture that our result also extends when only conditions in one of the environments are satisfied, although the formal arguments for this conjecture may require additional novel ideas.

By relaxing the ex-post budget constraints, we can also apply our results to models where the principal values the rewards for the agent. In particular, when the principal values the rewards, the problem can be decoupled into two orthogonal problems: (1) maximizing the expected payoff from the decision problem subject to the ex-ante budget constraints and (2) optimizing the budgets to maximize the expected utility of the principal. Our results under ex-ante budget constraints imply that even when the principal values the rewards, the optimal contract can still be implemented as a scoring rule when only .

6.4 Conclusions

This paper has introduced a framework to consider optimal scoring rule design when the agent faces an information acquisition problem that is fundamentally dynamic. Indeed, natural stories for why information acquisition is costly involve some dynamic element—for instance, a student deciding how long to work on coming up with a proof or counterexample or researchers deciding how long to run tests to learn about a drug’s efficacy. Our assumptions on information arrival are inspired by and generalized those from past work on dynamic endogenous information acquisition; however, a fundamental difficulty in our problem was the lack of any natural structure, such as stationarity, given arbitrary dynamic contracts. Such assumptions are often critical in similar exercises. Nevertheless, we provided simple conditions such that the optimal dynamic contract is implementable by a scoring rule and explained the extent to which these conditions are necessary for this conclusion to hold.

There are many natural avenues for future work. For instance, since our goal was to optimize among dynamic contracts in a setting with dynamic moral hazard, we have neglected information arrival processes as general as those accommodated by Chambers and Lambert, (2021)—for instance, if the information the agent acquires over time relates to what information will arrive in the future. While we found the analysis under the particular class of information arrival processes considered tractable, we do not doubt that similar conclusions could emerge under different information arrival processes. Finding a richer class of tractable information arrival processes would also be necessary to allow for more of an intensive margin for experimentation relative to what we have allowed. In these cases, scoring rules may not be a natural class to consider, leading to the natural follow-up question of whether there are other simple ways of understanding how the principal may optimally leverage the dynamic nature of the problem.

Conversely, one may also be interested in these cases whether scoring rules incur significant loss relative to optimal dynamic contracts. Our goal here has been to provide a framework to study optimal contracts in dynamic settings, and we find further insights on this agenda valuable.

References

- Bergemann et al., (2020) Bergemann, D., Castro, F., and Weintraub, G. (2020). The scope of sequential screening with ex post participation constraints. Journal of Economic Theory, 188:105055.

- Bergemann and Hege, (1998) Bergemann, D. and Hege, U. (1998). Venture capital financing, moral hazard, and learning. Journal of Banking & Finance, 22:703–735.

- Bergemann and Hege, (2005) Bergemann, D. and Hege, U. (2005). The financing of innovation: Learning and stopping. RAND Journal of Economics, 36(4):719–752.

- Bergemann and Strack, (2015) Bergemann, D. and Strack, P. (2015). Dynamic revenue maximization: A continuous time approach. Journal of Economic Theory, 159(B):819–853.

- Bloedel and Zhong, (2021) Bloedel, A. and Zhong, W. (2021). The cost of optimally acquired information. Working Paper.

- Carroll, (2019) Carroll, G. (2019). Robust incentives for information acquisition. Journal of Economic Theory, 181:382–420.

- Chambers and Lambert, (2021) Chambers, C. P. and Lambert, N. S. (2021). Dynamic belief elicitation. Econometrica, 89(1):375–414.

- Che and Mierendorff, (2019) Che, Y.-k. and Mierendorff, K. (2019). Optimal dynamic allocation of attention. American Economic Review, 109(8):2993–3029.

- Chen and Yu, (2021) Chen, Y. and Yu, F.-Y. (2021). Optimal scoring rule design. Working Paper.

- Courty and Li, (2000) Courty, P. and Li, H. (2000). Sequential screening. Review of Economic Studies, 67(4):697–717.

- Dasgupta, (2023) Dasgupta, S. (2023). Optimal test design for knowledge-based screening. Working Paper.

- Deb and Mishra, (2014) Deb, R. and Mishra, D. (2014). Implementation with contingent contracts. Econometrica, 82(6):2371–2393.

- Deb et al., (2018) Deb, R., Pai, M., and Said, M. (2018). Evaluating strategic forecasters. American Economic Review, 108(10):3057–3103.

- Deb et al., (2023) Deb, R., Pai, M., and Said, M. (2023). Indirect persuasion. Working Paper.

- DeMarzo et al., (2005) DeMarzo, P., Kremer, I., and Skrzypacz, A. (2005). Bidding with securities— auctions and security design. American Economic Review, 95(4):936–959.

- Eso and Szentes, (2017) Eso, P. and Szentes, B. (2017). Dynamic contracting: An irrelevance result. Theoretical Economics, 12(1):109–139.

- Garrett and Pavan, (2012) Garrett, D. F. and Pavan, A. (2012). Managerial turnover in a changing world. Journal of Political Economy, 120(5):879–925.

- Guo, (2016) Guo, Y. (2016). Dynamic delegation of experimentation. American Economic Review, 106(8):1969–2008.

- Halac et al., (2016) Halac, M., Kartik, N., and Liu, Q. (2016). Optimal contracts for experimentation. Review of Economic Studies, 83:601–653.

- Hartline et al., (2023) Hartline, J. D., Shan, L., Li, Y., and Wu, Y. (2023). Optimal scoring rules for multi-dimensional effort. In Thirty Sixth Annual Conference on Learning Theory, pages 2624–2650.

- Hebert and Zhong, (2022) Hebert, B. and Zhong, W. (2022). Engagement maximization. Working Paper.

- Keller et al., (2005) Keller, G., Rady, S., and Cripps, M. (2005). Strategic experimentation with exponential bandits. Econometrica, 73(1):39–68.

- Krähmer and Strausz, (2015) Krähmer, D. and Strausz, R. (2015). Optimal sales contracts with withdrawal. Review of Economic Studies, 82(2):762–790.

- Lambert, (2022) Lambert, N. S. (2022). Elicitation and evaluation of statistical forecasts. revised and resubmitted at Econometrica.