frameworkFramework \newsiamremarkremRemark \newsiamremarkdefnDefinition \newsiamthmcorCorollary \newsiamthmassumAssumption \newsiamthmthmTheorem \newsiamthmpropProposition \newsiamthmlemLemma \headersMean generalization error bound of the deep learningJichang Xiao, Fengjiang Fu, and Xiaoqun Wang

Analysis of the Generalization Error of deep learning based on Randomized Quasi-Monte Carlo for Solving Linear Kolmogorov PDEs

Abstract

Deep learning algorithms have been widely used to solve linear Kolmogorov partial differential equations (PDEs) in high dimensions, where the loss function is defined as a mathematical expectation. We propose to use the randomized quasi-Monte Carlo (RQMC) method instead of the Monte Carlo (MC) method for computing the loss function. In theory, we decompose the error from empirical risk minimization (ERM) into the generalization error and the approximation error. Notably, the approximation error is independent of the sampling methods. We prove that the convergence order of the mean generalization error for the RQMC method is for arbitrarily small , while for the MC method it is for arbitrarily small . Consequently, we find that the overall error for the RQMC method is asymptotically smaller than that for the MC method as increases. Our numerical experiments show that the algorithm based on the RQMC method consistently achieves smaller relative error than that based on the MC method.

keywords:

Deep learning, Linear Kolmogorov equations, Randomized quasi-Monte Carlo, Generalization error65C30, 65D30, 65N15, 68T07

1 Introduction

Partial differential equations (PDEs) are important mathematical models to solve problems arising in science, engineering and finance. Classical numerical methods for PDEs are usually based on space partitioning, such as finite differences [40] and finite elements [6]. For high-dimensional PDEs, these methods suffer from the curse of dimensionality, which means that the computational cost grows exponentially as the dimension increases.

Recently, deep learning has achieved considerable progress. Its application to solve PDEs has attracted much attention. Based on minimizing the residual in -norm, Physics-informed Neural Networks [34] and Deep Galerkin Method [39] are proposed. Combining the Ritz method with deep learning, Deep Ritz Method [13] is proposed to solve elliptic PDEs.

In this paper, we consider the linear Kolmogorov PDE, which plays an important role in finance and physics. Beck et al. [2] first proposed a deep learning algorithm to numerically approximate the solution over a full hypercube and performed experiments to demonstrate the effectiveness of the algorithm even in high dimensions. Berner et al. [4] further developed the deep learning algorithm for solving a parametric family of high-dimensional Kolmogorov PDEs. Berner et al. [5] and Jentzen et al. [20] provided the theoretical results that the deep learning algorithm based on deep artificial neural networks can overcome the curse of dimensionality under some regularity conditions. Richter et al. [37] introduced different loss functions to enhance the robustness of the deep learning algorithm for solving Kolmogorov PDEs.

All of these deep learning-based algorithms reformulate the approximation problem into an optimization problem, where the loss function is defined as a stochastic differential equation (SDE)-based expectation. Researchers usually employ Monte Carlo (MC) methods to compute the loss function. Quasi-Monte Carlo (QMC) methods are more efficient numerical integration methods than MC methods [29]. QMC methods choose deterministic points, rather than random points, as sample points. Due to their effectiveness for integration problems, QMC methods are widely used in finance [26], statistics [14] and other problems. The applications of QMC methods in deep learning have also made some progress. Dick and Feischl [11] applied QMC methods to compress data in machine learning. Liu and Owen [24] introduced randomized QMC (RQMC) methods in stochastic gradient descent method to accelerate the convergence. Longo et al. [25] and Mishra et al. [27] trained the neural networks by QMC methods and proved that the QMC-based deep learning algorithm is more efficient than the MC-based one.

In this paper, we combine RQMC methods with deep learning for solving linear Kolmogorov PDEs, leading to the RQMC-based deep learning algorithm. To demonstrate the superiority of our proposed algorithm, we analyze how the error from the empirical risk minimization (ERM) depends on the sampling methods used to simulate training data. Similar to bias-variance decomposition, we decompose the error into the approximation error and the generalization error. The approximation error is independent of the training data. We obtain the convergence rate of mean generalization error with respect to the sample points for both MC methods and RQMC methods. We also conduct numerical experiments to compare the performance of the RQMC-based deep learning algorithm and the MC-based deep learning algorithm for solving specific linear Kolmogorov PDEs.

This paper is organised as follows. In Section 2, we introduce the minimization problem associated with the linear Kolmogorov PDEs and generalize it into a general deep learning Framework 3, we also introduce preliminary knowledge of the RQMC method and bias-variance type decomposition of the estimation error. In Section 3, we obtain the convergence rate of the mean generalization error for different sampling methods and for specific linear Kolmogorov PDEs with affine drift and diffusion. In Section 4, we implement the RQMC-based deep learning algorithm and the MC-based deep learning algorithm to solve the Black-Scholes PDEs and heat equations. Section 5 concludes the paper.

2 Preliminaries

2.1 General deep learning framework for solving linear Kolmogorov PDEs

We consider the linear Kolmogorov PDE

| (1) |

where , and . Let and be the solution of (1). The goal is to numerically approximate the endpoint solution on the hypercube . Beck et al. [2] prove that the target solves a minimization problem stated rigorously in Lemma 1.

Lemma 1.

Let , , , , let and in (1) satisfy for every that

where is the Euclidean norm and is the Hilbert-Schmidt norm. Let the function be the solution of (1) with at most polynomially growing partial derivatives. Let be a probability space with a normal filtration , be the standard -dimensional Brownian motion, be uniformly distributed and -measurable. Let be the continuous stochastic process satisfying that for every it holds -a.s.

| (2) |

For every , let be the continuous stochastic process satisfying that for every it holds -a.s.

| (3) |

We define the loss function for every .

Then there exists a unique function such that

and for every it holds that

This lemma shows that the numerical approximation problem is equivalent to the supervised learning problem for input and label with quadratic loss function. Suppose that are independent and identically distributed (i.i.d.) samples drawn from the population , then we can employ the empirical risk minimization (ERM) principle to solve this regression problem by minimizing the empirical risk

| (4) |

among the hypothesis class .

In deep learning, we use artificial neural networks as the hypothesis class.

Definition 2 (Artificial neural network).

Let , , . The artificial neural network with the activation function , the parameter bound and the structure is defined by

| (5) |

where are affine transformations, denotes the parameters in the network, is the parameter space defined by , and the activation function is applied component-wisely.

Denote the function class of all artificial neural network (5) by , and denote the restriction of on by

Remark 3.

The total number of parameters is , is equivalent to vectors on , thus is well-defined and is a compact set on . Since the composition of continuous functions remains continuous, we have . In this paper, we choose swish activation function

which could improve the performance of deep learning compared to RELU and sigmoid functions [35, 36].

Since artificial neural networks is completely determined by its parameters , it suffices to search the optimal which minimizes the empirical risk over the artificial neural networks

Deep learning can be applied to solve the linear Kolmogorov PDE (1) if we can simulate the training data .

For important cases of linear kolmogorov PDEs such as the heat equation and the Black-Scholes PDE, the SDE (2) can be solved explicitly. The closed form of depends only on the initial condition and the Brownian motion which can be simulated by

| (6) |

respectively, where are uniformly distributed on , is the cumulative distribution function of the standard normal and is the inverse applied component-wisely.

In general cases, we usually approximate numerically by Euler–Maruyama scheme. Let , the discrete process is defined by the following recursion

| (7) |

where and . We actually have an approximated learning problem with loss function

Theorem 2 in [4] shows that solving the learning problem with does indeed result in a good approximation of the target .

For the approximated learning problem, since we have for ,

| (8) |

we can simulate by uniformly distributed random variables .

[Deep learning problem with uniform input] Let , , , let be uniformly distributed on and be uniformly distributed on , denote . Assume that the input and output are given by

| (9) |

where . Let be a sequence of random variables satisfying , define the corresponding input data and output data by

| (10) |

Let , for every , define the risk and the empirical risk by

| (11) |

Let be the Banach space of continuous functions with norm defined by

Define the optimizer of risk on by

Let ,

| (12) |

assume the hypothesis class (see Definition 2). Define approximations and by

| (13) |

The deep learning problem in Framework 3 considers the input and output with specific dependence (9) on the uniform random variable . In classical learning theory [1, 10, 38], the output is usually assumed to be bounded. However, in many applications the output in (9) does not necessarily to be bounded, which means that most theoretical results in learning theory cannot be applied directly for error analysis in Section 3.

The classical ERM principle requires i.i.d. data satisfying to compute the empirical risk . In this scenario, empirical risk is actually the crude MC estimator of the risk. From the theory of QMC and RQMC methods, there are other simulation methods of the uniform data on the unit cube, thus the uniform sequence in Framework 3 does not have to be independent. If are chosen to be the scrambled digital sequence [31], then the empirical risk is the RQMC estimator of the risk .

2.2 Randomized quasi-Monte Carlo methods

Consider the approximation of an integral

MC and QMC estimators both have the form

MC methods use i.i.d. uniformly distributed sample from . Suppose has finite variance , then we have

Thus for MC estimator, the convergence rate of the expected error is . For QMC methods, the points are deterministic, which are highly uniformly distributed on . The QMC error bound is given by the Koksma-Hlawka inequality [29]

| (14) |

where is the variation of in the sense of Hardy and Krause, is the star discrepancy of the point set . Several digital sequences such as the Sobol’ sequence and the Halton sequence are designed to have low star discrepancy with . We refer to [28, 29] for the detailed constructions. For digital sequence , suppose that , Koksma-Hlawka inequality shows that the convergence rate of the approximation error is which is asymptotically better than of MC.

Since QMC points are deterministic, the corresponding estimators are not unbiased. We can use RQMC methods which randomize each point to be uniformly distributed while preserving the low discrepancy property, see [8, 31] for various randomization methods.

In this paper, we consider the scrambled digital sequence introduced in [31]. Let be the scrambled -sequence in base b, then we have the following properties:

-

(i)

Every is uniformly distributed on .

-

(ii)

The sequence is a -sequence in base with probability 1.

-

(iii)

There exists a constant such that for every and it holds that

(15)

We refer the readers to [12, 29, 31] for details of the -sequence and the scrambling methods.

2.3 Analysis of the estimation error

Under the Framework 3, we are interested in the estimation error defined by

The following lemma shows that can be expressed in terms of the loss function.

Lemma 4.

Proof 2.1.

Consider , is a quadratic function and takes the minimum at , thus equal to the coefficient of which is exactly . Thus we have

the proof completing.

In classical learning theory, there are many theoretical results which establish conditions on the sample size and the hypothesis class in order to obtain an error

with high probability for small , see [1, 5, 9, 23, 38]. Those theoretical results rely on the i.i.d. assumptions of the training data and the boundness condition of the output, thus they cannot be applied directly to research on the influence of sampling methods of . Without the i.i.d. assumption, we still have the following decomposition

In consistent with [3, 5], we refer the term as the generalization error and as the approximation error. The approximation error depends only on the function class , see [7, 16, 18, 30] for approximation property of artificial neural networks. To address the influence of sampling methods, we keep the artificial neural networks fixed and focus on the generalization error. The next lemma establishes a upper bound for the generalization error.

Proof 2.2.

By , it is trivial that

For the upper bounds, we have

where the second inequality follows from .

3 Main Results

In this section, we obtain the convergence rate with respect to the sample size of the mean generalization error for MC and RQMC methods. The mean generalization error is defined by

| (17) |

Throughout this section, we keep the hypothesis class fixed.

3.1 RQMC-based convergence rate

By Lemma 5, it suffices to obtain the convergence rate of the upper bound

| (18) |

Assume that we choose the uniform sequence in Framework 3 to be the scrambled digital sequence, then (18) equals to the mean supreme error of scrambled net quadrature rule that is

the function is defined by

| (19) |

where denotes the first components of and is the artificial neural network. In most cases, the functions are unbounded and cannot be of bounded variation in the sense of Hardy and Krause. For unbounded functions satisfying the boundary growth condition, we can still obtain the convergence rate of the mean error (or even root mean squared error), see [17, Theorem 3.1] and [33, Theorem 5.7]. These results cannot be applied directly since we need to handle with the supreme error for a function class, but it is natural to introduce the boundary growth condition for a whole function class.

For a nonempty set , denote the partial derivative by , we make a convention that . Let be an indicator function.

Definition 6 (Boundary growth condition).

Let , suppose is a class of real-valued functions defined on . We say that satisfies the boundary growth condition with constants if there exists such that for every , every subset and every it holds that

| (20) |

The next theorem establishes the error rate of mean supreme error for a function class satisfying the boundary growth condition (20).

Theorem 7.

Suppose is a class of real-valued functions defined on which satisfies the boundary growth condition (20) with constants . Suppose that is a scrambled -sequence in base , let sample size , , then we have

| (21) |

To prove Theorem 7, we need to introduce concept of the low variation extension [32, 33]. For every , let

| (22) |

be the set avoiding the boundary of with distance . The anchor point of is chosen to be such that

| (23) |

According to [32, Proposition 25], an ANOVA type decomposition of is given by

| (24) |

where denotes the point with for and for , denotes . Based on (24), the low variation extension of from to is defined by

| (25) |

For the low variation extension (25), Owen [33] proves some useful properties which are stated in the next lemma.

Lemma 8.

Suppose that is a class of real-valued functions defined on which satisfies the boundary growth condition (20) with constants . Let , and let be the set avoiding boundary defined by (22) and be the low variation extension of from to defined by (25). Then

-

(i)

for every , and , we have

-

(ii)

there exists a constant such that for every , and ,

-

(iii)

there exists a constant such that for every and ,

The next lemma states other properties of low variation extensions that are necessary to prove Theorems 7 and 17.

Lemma 9.

Under the setting of Lemma 8, suppose that are uniformly distributed on . Then

-

(i)

there exists a constant such that for every and ,

-

(ii)

there exists a constant such that for every and ,

Proof 3.1.

Define for . From of Lemma 8, we have

Taking expectations on both sides of the above inequality, then it suffices to show that for every ,

where the first inequality follows from extending the integration region to for the rest arguments when -th argument is fixed. It is easy to use the same techniques to prove that

The proof is completed.

Proof 3.2 (Proof of Theorem 7).

If the function class satisfies boundary growth condition (20) with arbitrarily small , then the error rate in Theorem 7 becomes for arbitrarily small . To obtain the error rate for the expected generalization error (17), we only need to verify that the boundary growth condition is satisfied for the specific function class defined by (19). The next lemma provides an easy way to verify the boundary growth condition for a complicated function class.

Lemma 10.

Suppose that and both satisfy the

boundary growth condition (20) with constants . Then and also satisfy the boundary growth condition with constants .

Proof 3.3.

For every subset of indices, , the partial derivatives of and are given by

We can use the above formulas to prove that the partial derivatives of and also satisfy the inequality (20) with constants .

Based on Theorem 7 and Lemma 10, we can obtain the convergence rate of the mean generalization error if the data is the scrambled digital sequence.

Theorem 11.

Proof 3.4.

Under Framework 3, the function class is the restriction of artificial neural networks on . To deal with uniform input, we define the function class

Due to the smoothness of swish activation function , is a smooth function of . The region is compact, so there exists constant such that for every subset it holds that

Hence satisfies the boundary growth condition with arbitrarily small . By Lemma 10 and the assumption on the function , the following function class

also satisfies the boundary growth condition with arbitrarily small . By Lemma 5 and Theorem 7, we find that for arbitrarily small it holds that

The proof is completed.

3.2 MC-based convergence rate

Under Framework 3, it is equivalent to directly simulate the i.i.d. data if we use MC methods to simulate i.i.d. uniform sequence . In this case, we use Rademacher complexity technique to obtain the error rate of the mean generalization error.

Definition 12 (Rademacher complexity).

Suppose are i.i.d Rademacher variables defined on the probability space with discrete distribution . Suppose that are i.i.d random samples on and take values in a metric space . Suppose is a class of real-valued borel-measurable function over ( is the Borel -field). The Rademacher complexity of a function class with respect to the random sample is defined by

The following lemmas state some useful properties of Rademacher complexity which are latter applied to bound the mean generalization error.

Lemma 13.

Lemma 14.

Under the setting of Definition 12. Suppose is a bounded measurable real-valued function over , then we have

where denotes the function class .

For the rigorous proofs of Lemmas 13 and 14, we refer the readers to [38, Lemma 26.2] and [21, Lemma5.2], respectively. Under Framework 3, the function class is the restriction of an artificial neural networks over . With reference to [21, Theorem 5.13], the next lemma gives the upper bound for the specific Rademacher complexity.

Lemma 15.

Under the setting of Definition 12. Let , , let and for . Suppose that there exists a surjective operator with image . Suppose that there exist constants and such that for all , it holds that

Then we have

Suppose that the function in Framework 3 is bounded, then we can bound the MC-based mean generalization error in terms of Rademacher complexity and obtain the desired convergence rate using Lemma 15.

Theorem 16.

Under Framework 3, suppose that for all . Suppose that are i.i.d. samples simulated from the uniform distribution on , then we have

where denotes the function class .

Proof 3.5.

By Lemma 5, we have

For some applications such as heat equations and Black-Sholes PDEs, the function is not bounded as required in Theorem 16, but the function usually satisfies the boundary growth condition (20). In this case, we can also establish the convergence rate for the MC-based mean generalization error.

Theorem 17.

Proof 3.6.

Let and let the function be the low variation extension of from to . By the triangle inequality, for every function ,

Summing up three parts, we have

Similar to the proof of Theorem 16, we have

Taking the optimal rate , the inequality becomes

The proof is completed.

Assume that we apply MC methods to simulate i.i.d. uniform data (equivalently i.i.d. data ) in Framework 3. If the function is bounded, Theorem 16 shows that the mean generalization error converges to as sample size and the convergence rate is at least . If the function merely satisfies the boundary growth condition with arbitrarily small , Theorem 17 shows that the convergence rate of the mean generalization error is at least for arbitrarily small .

3.3 Applications for linear Kolmogorov PDE with affine drift and diffusion

As discussed in Section 2.1, the numerical approximation problem of solutions to linear Kolmogorov PDEs can be reformulated as the deep learning problem satisfying Framework 3. In this section, we apply Theorems 11 and 17 to obtain the convergence rate of the mean generalization error for specific linear Kolmogorov PDEs with affine drift and diffusion. In Assumption 18 below, case and correspond to heat equations and Black-Scholes PDEs, respectively, which are two most important cases of linear Kolmogorov PDEs with affine drift and diffusion.

Assumption 18.

For the linear Kolmogorov PDE (1), suppose that the initial function has polynomially growing partial derivatives, for the drift and diffusion , we consider the following three cases

-

(i)

and , where and .

-

(ii)

and , where and .

-

(iii)

and are both affine transformations .

Let be the cumulative distribution function of the standard normal and is the inverse applied component-wisely, then we can write the function in Framework 3 as

| (28) |

where

For case , we can also solve the SDE (2) explicitly

where

denotes the -th component of , denotes -th component of and denotes -th row of . We can write the function in Framework 3 as

| (29) |

where

For case , we consider the Euler–Maruyama approximation defined by the following recursion

For affine transformations and , there exist polynomials such that

where

Then we can write the function in Framework 3 as

| (30) |

where

Lemma 19.

Proof 3.7.

For the function , since has polynomially growing partial derivatives, by chain rule, there exists constant and such that for every subset it holds that

| (31) |

For every , we have

| (32) |

Summarizing (31) and (32), we have for arbitrarily small ,

which shows that the function satisfies the boundary growth condition with arbitrarily small .

For the function , similarly there exists constant such that for every subset it holds that

| (33) |

From (33) and (32), for arbitrarily small , we have

For the function , by chain rule and the assumption on , there exists constant and such that for every subset it holds that

Same as for function , we can prove that satisfies the boundary growth condition with arbitrarily small .

Lemma 19 shows that for linear Kolmogorov PDEs satisfying Assumption 18, the corresponding functions in Framework 3 satisfy the boundary growth condition with arbitrarily small , we can apply Theorems 11 and 17 to obtain the convergence rate of the mean generalization error for different sampling methods.

Theorem 20.

Under Framework 3. Suppose that the drift function and the diffusion function in (1) satisfy Assumption 18, then

-

(i)

Suppose that is the scrambled digital sequence in base , let sample size , , then for arbitrarily small we have

-

(ii)

Suppose that are i.i.d samples simulated from the uniform distribution over , then for arbitrarily small we have

As discussed in Section 2.1, the mean estimation error from the ERM principle

can be decomposed into

The approximation error is independent of the sample , hence Theorem 20 shows that we can achieve asymptotically smaller mean estimation error as sample size if we simulate scrambled digital nets instead of i.i.d. uniform points.

4 Numerical Experiments

In this section, we conduct numerical experiments to show the potential advantages obtained by using scrambled digital nets instead of i.i.d. uniform random numbers in the deep learning algorithm for solving linear Kolmogorov PDEs. Due to the low computational cost of generating uniform samples on unit cube, we follow [4, 37] to simulate new uniform samples for each batch during training. To address the influence of the sampling methods, we ensure that other settings of the algorithms are same. The activation function of artificial neural network is chosen to be the swish function (12), and we initialize the artificial neural network by means of the Xavier initialization [15]. Moreover we add batch normalization layers [19] to enhance model robustness. For training the networks, we follow the training settings from [4]. More specifically, we use the Adam optimizer [22] with default weight decay and piece-wise constant learning rate. The detailed settings of the deep learn algorithm are given in Table 1.

To compare the performance of the deep learning algorithms based on different sampling methods, we use the relative error defined by

where is the output of the neural network after training and is the exact solution. Since the relative error cannot be computed explicitly, we approximate it via MC methods that is

| (34) |

where the sample size and are i.i.d. samples with uniform distribution on .

| Heat equation | Black-Scholes model | |

| Input | ||

| dimension | dim = 5, 20 | dim = 5, 20 |

| T | 1 | 1 |

| Network | ||

| width | 4dim | 4dim |

| depth | 6 | 6 |

| activation | swish | swish |

| norm layer | batch norm. | batch norm. |

| init | Xvaier | Xvaier |

| Training | ||

| optimizer | AdamW | AdamW |

| weight decay | 0.01 | 0.01 |

| initial learning rate | ||

| lr decay ratio | 0.4 | 0.25 |

| lr decay patience | 4000 | 4000 |

| iterations | 32000 | 32000 |

4.1 Heat equation

We first consider the following heat equation with paraboloid initial condition

| (35) |

The exact solution is given by

In our experiments, we choose and . To approximate the relative error, we choose in (34) and compute the exact solsution directly.

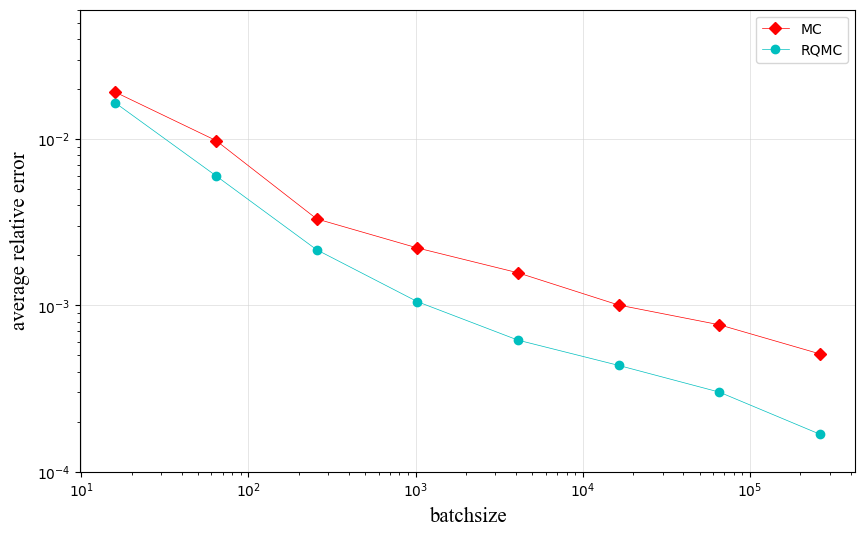

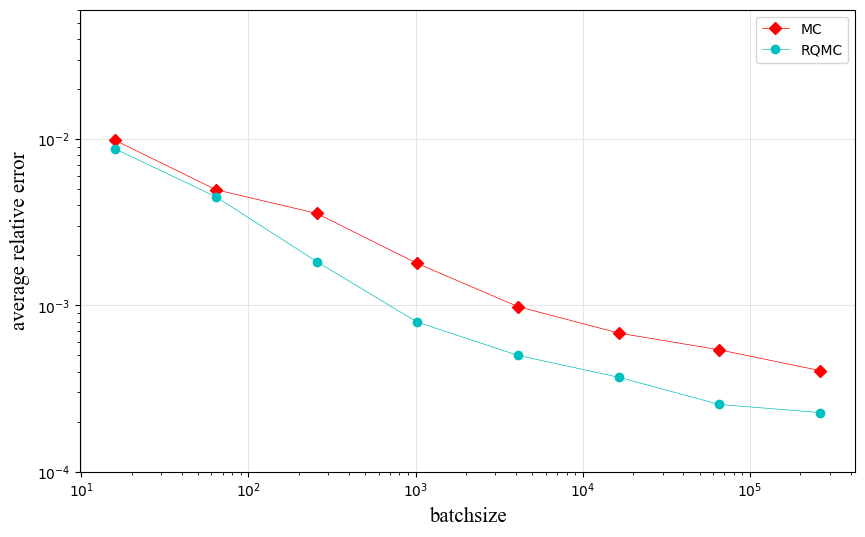

Figures 1(a) and 1(b) present the average relative error for 4 independent runs in dimensions and . Both figures demonstrate the superiority of the RQMC sampling method over the crude MC, and such superiority becomes more significant as the batchsize increases. To achieves relative error within , in dimension 5, MC-based deep learning algorithm requires batchsize while RQMC-based one only requires batchsize . In dimension 20, the advantages become slightly less impressive in the sense that MC-based deep learning algorithm requires batchsize while MC-based one requires batchsize to reach relative error within . In general, as in other applications, the superiority of RQMC methods becomes weaker in higher dimensions .

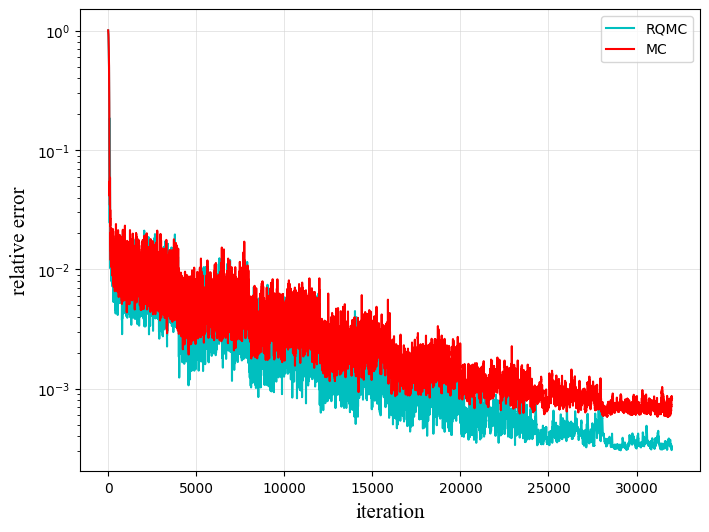

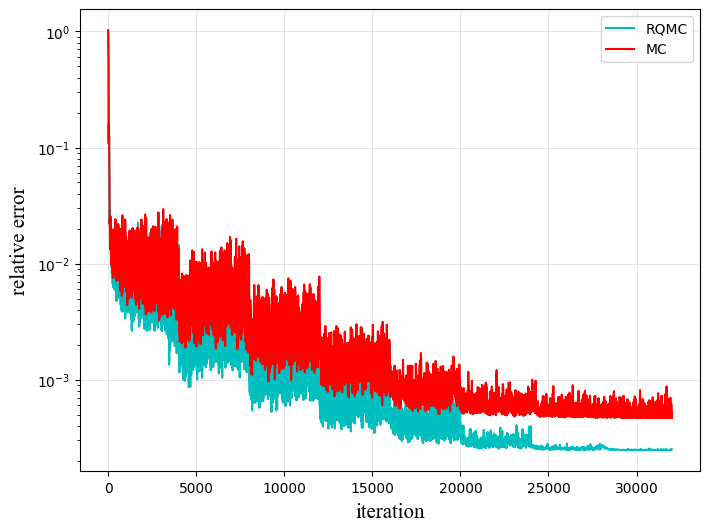

Figure 2(a) and 2(b) present the relative error during the training process of artificial neural networks with batchsize . We observe that applying RQMC sampling methods leads to a more accurate artificial neural network with smaller relative error. In , for the RQMC method, the standard deviation of the relative error over the last 100 iterations is , while it is for the MC method. In , the standard deviations of the relative error over last 100 iterations for RQMC and MC are and respectively. This suggests that the training process of the RQMC-based deep learning algorithm is more stable.

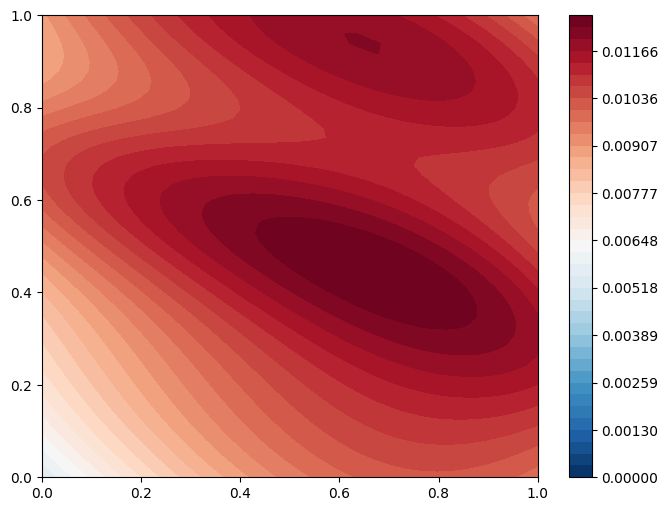

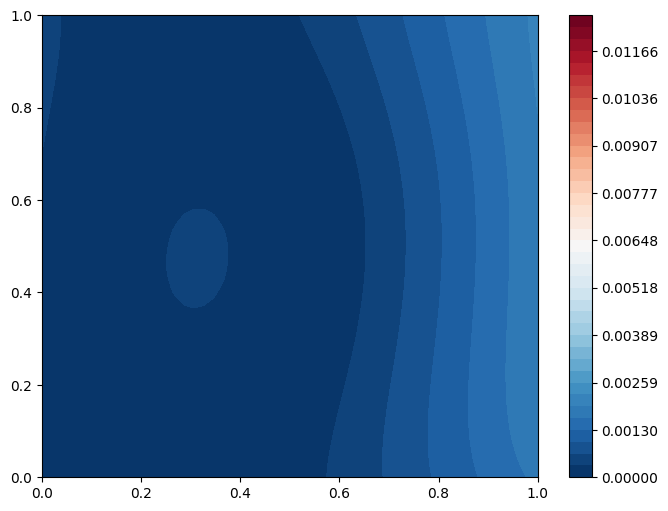

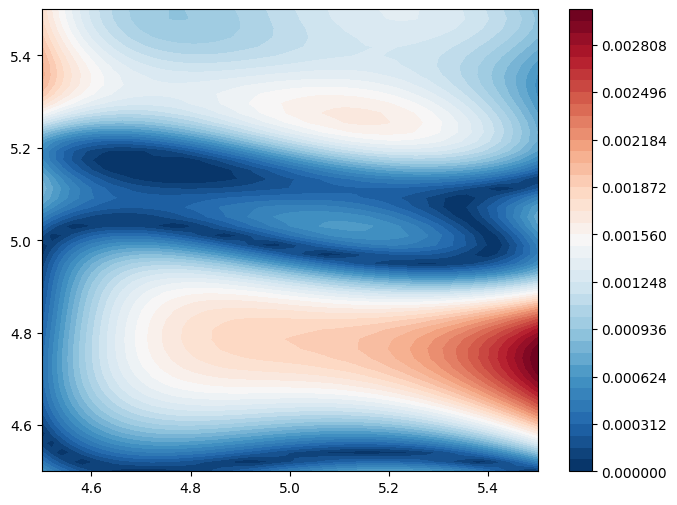

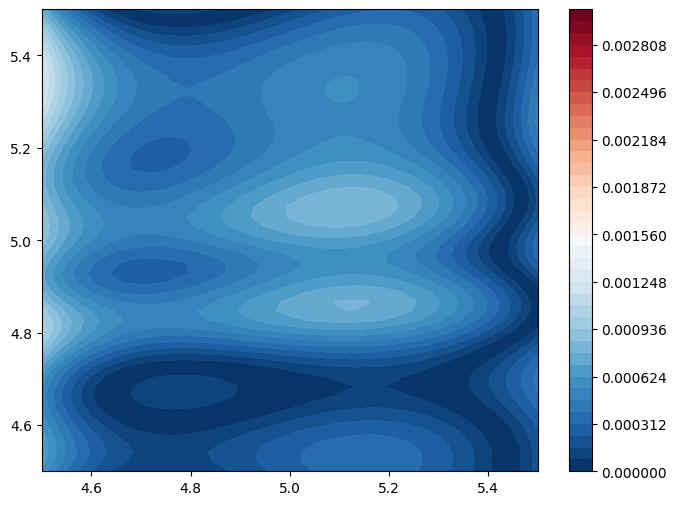

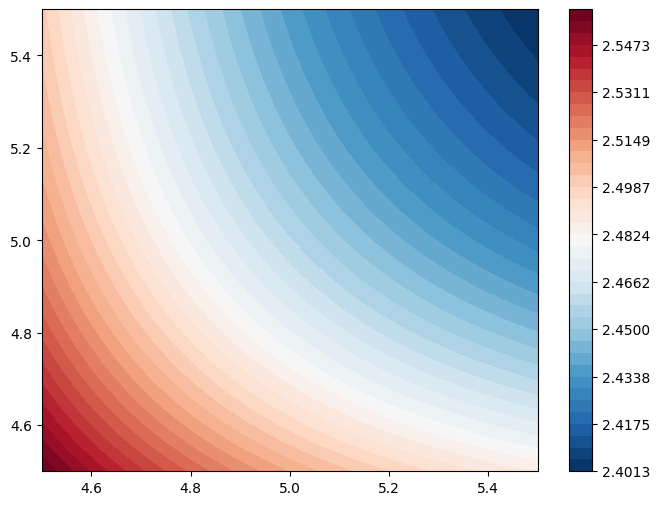

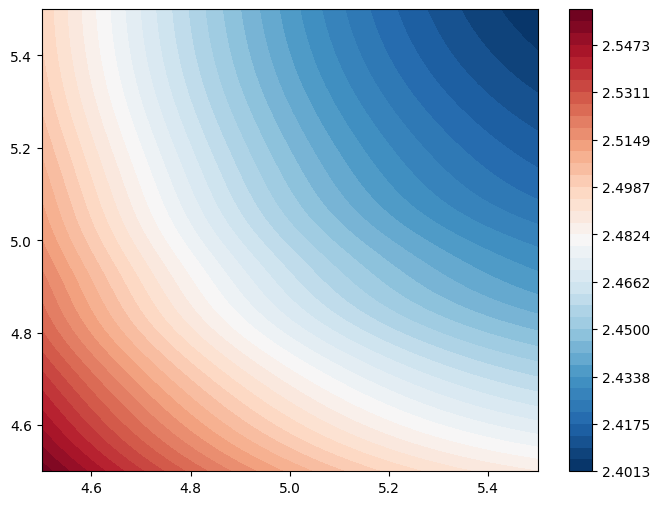

In dimension 20, we consider the projection of the exact solution and the trained neural networks on with . Comparing Figures 3(a) and 3(b), we find that the RQMC-based deep learning algorithm with batchsize achieves lower relative error across the whole region than that of MC-based one. From Figures 3(b) and 3(d), the RQMC-based deep learning algorithm does indeed numerically solve the heat equation (35) with high precision on the projection space.

4.2 Black-Scholes model

Next, we consider the Black-Scholes PDE with correlated noise (see [2, Section 3.4] and [37, Section 3.2]) defined by

| (36) |

where . For different choice of the initial functions , Black-Scholes PDEs can model the pricing problem for different types of European options. Let and the initial condition

| (37) |

Then the solution solves the problem of pricing a rainbow European put option. By Feynman-Kac formula, we know that for every it holds that

| (38) |

where

is the -th row of and is a standard -dimensional Brownian motion.

In our experiments we choose the same setting in [37, section 3.2], let , , , . Let

where and is the lower triangular matrix arsing from the Cholesky decomposition with and , . To approximate the relative error, we choose , for every sample , we approximate the exact solution via MC methods with sample size .

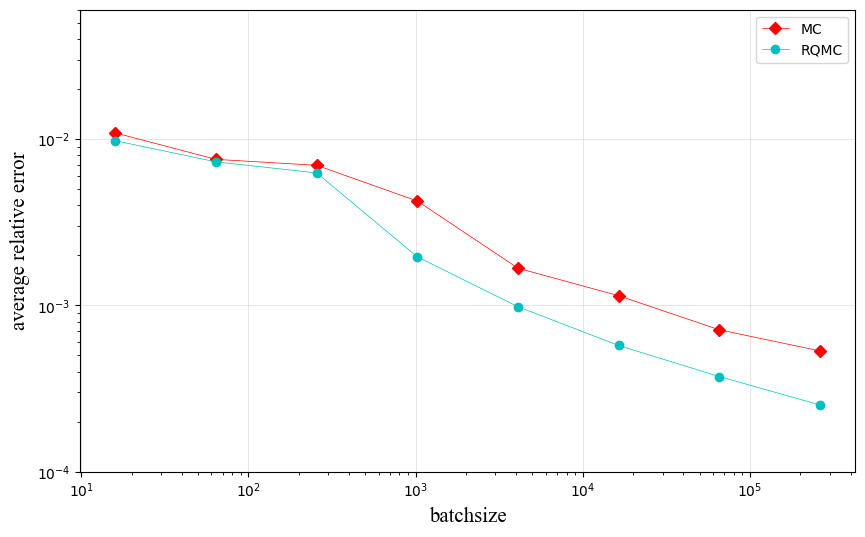

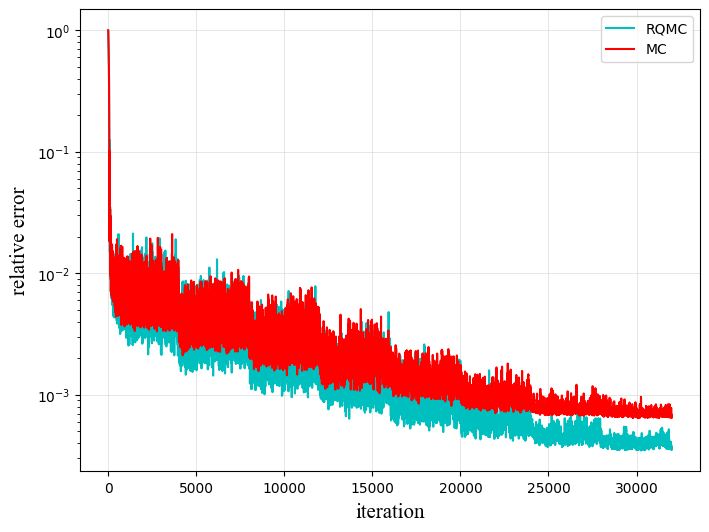

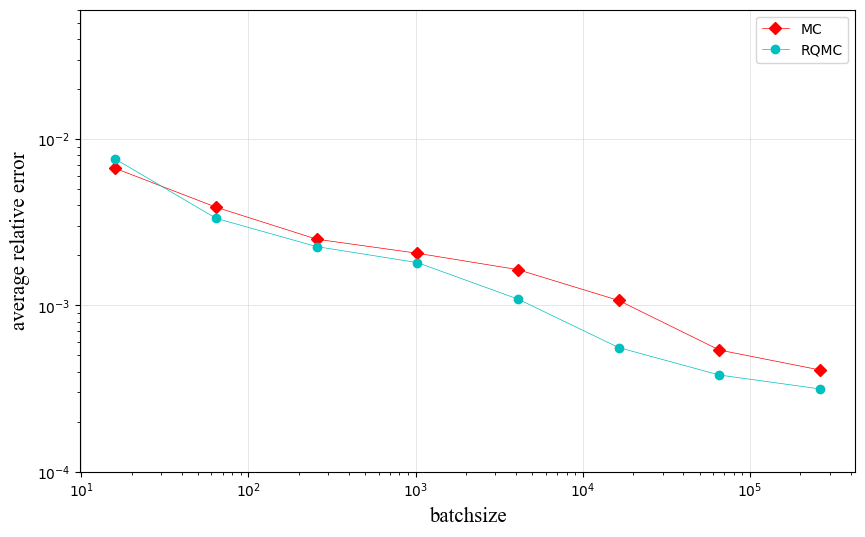

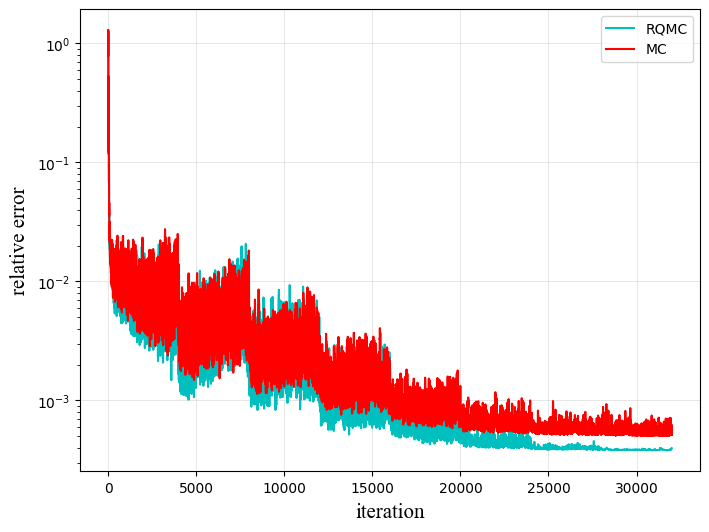

Same as the heat equation, Figure 4(a) and 4(b) present the average relative error for 4 independent runs in . Both figures demonstrate the superiority of the RQMC sampling method over the ordinary MC. In dimension 5, MC-based deep learning algorithm requires batchsize to achieve relative error while RQMC-based one only requires batchsize to achieve relative error . In dimension 20, the advantages become slightly less impressive in the sense that MC-based deep learning algorithm requires batchsize while RQMC-based one only requires batchsize to reach relative error within . Figure 5(a) and 5(b) present the relative error during a training process of artificial neural networks with batchsize . From figures, we find that applying RQMC sampling method leads to a more accurate and stable networks with smaller relative error.

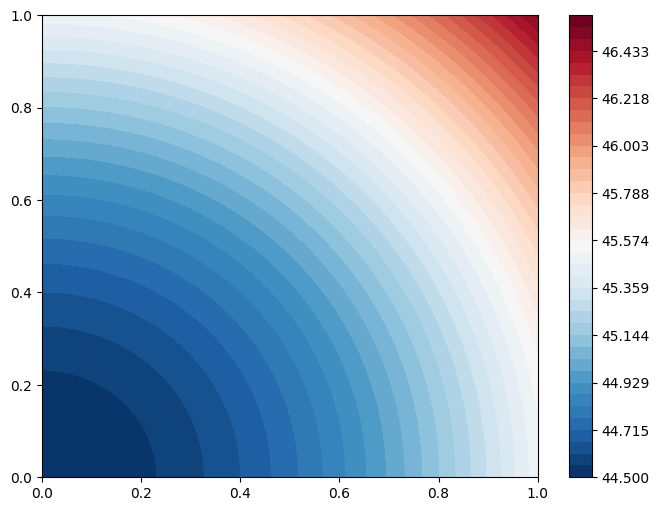

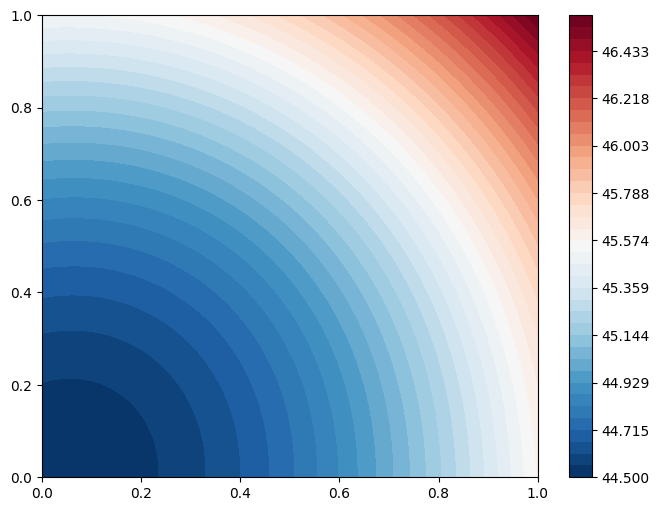

In dimension 5, we consider the projection of the exact solution and the trained neural networks on with . Comparing Figures 6(a) and 6(b), we find that the RQMC-based deep learning algorithm with batchsize achieves lower relative error than that of MC-based in most areas. From Figures 6(b) and 6(d), the RQMC-based deep learning algorithm with batchsize is highly effective in solving the Black-Scholes PDE (36) with initial condition (37) on the projection space.

5 Conclusion

The numerical approximation of solutions to linear Kolmogorov PDEs can be reformulated as a deep learning problem under Framework 3. In the general framework, the empirical loss function completely depends on the uniform data. Typically, the data are supposed i.i.d.. In this paper, we suggest that the scrambled digital sequences may be a better choice.

We decompose the error resulted from the ERM into the the generalization error and the approximation error. Since the approximation error is independent of the training data, we focus on the generalization error for different sampling strategies. For MC methods that use i.i.d. samples, we prove that the convergence rate of the mean generalization error is for arbitrarily small if function satisfies the boundary growth condition (20) for arbitrarily small constants. For RQMC methods that use the scrambled digital sequence as the uniform data, the convergence rate of the mean generalization error becomes for arbitrarily small which is asymptotically better than that of MC methods. We conduct numerical experiments to show the potential advantages obtained by replacing i.i.d. uniform data with scrambled digital sequences in the deep learning algorithm for solving linear Kolmogorov PDEs. Numerical results show that the RQMC-based deep learning algorithm outperforms the MC-based one in terms of the accuracy and robustness.

The numerical results demonstrate that we need larger batchsize to show the advantages of RQMC-based deep learning algorithm as the dimension becomes larger. One possible way to explain this phenomenon is to study on how the implied constant in the rate and depends on the dimension . There is also an apparent gap between the error from the ERM and the error from stochastic gradient descent (SDG) type algorithms such as Adam optimizer. However, the error analysis for SGD type algorithms usually relies on the convexity of the loss function, which does not actually hold for the loss function defined in Framework 3. For other deep learning algorithms for solving PDEs such as Physics-informed Neural Networks and Deep Galerkin Method, If the training data can be generated with the uniform samples on unit cube, we guess that replacing the i.i.d. uniform sample with the scrambled digital net may still improve the accuracy and efficiency of the deep learning algorithms. The theoretical error analysis and relevant numerical experiments are left as future research.

References

- [1] M. Anthony and P. L. Bartlett, Neural Network Learning: Theoretical Foundations, Cambridge University Press, 1999.

- [2] C. Beck, S. Becker, P. Grohs, N. Jaafari, and A. Jentzen, Solving the Kolmogorov PDE by means of deep learning, 2021, https://arxiv.org/abs/1806.00421.

- [3] C. Beck, A. Jentzen, and B. Kuckuck, Full error analysis for the training of deep neural networks, Infin. Dimens. Anal. Quantum Probab. Relat. Top., 25 (2022), https://doi.org/10.1142%2Fs021902572150020x.

- [4] J. Berner, M. Dablander, and P. Grohs, Numerically solving parametric families of high-dimensional Kolmogorov partial differential equations via deep learning, Adv.Neural Inf. Process. Syst, 33 (2020), pp. 16615–16627.

- [5] J. Berner, P. Grohs, and A. Jentzen, Analysis of the generalization error: Empirical risk minimization over deep artificial neural networks overcomes the curse of dimensionality in the numerical approximation of Black–Scholes partial differential equations, SIAM J. Math. Data Sci., 2 (2020), pp. 631–657, https://doi.org/10.1137/19M125649X.

- [6] D. Braess, Finite Elements: Theory, Fast Solvers, and Applications in Solid Mechanics, Cambridge University Press, 3 ed., 2007, https://doi.org/10.1017/CBO9780511618635.

- [7] M. Burger and A. Neubauer, Error bounds for approximation with neural networks, J. Approx. Theory, 112 (2001), pp. 235–250, https://doi.org/10.1006/jath.2001.3613.

- [8] R. Cranley and T. N. L. Patterson, Randomization of number theoretic methods for multiple integration, SIAM J. Numer. Anal., 13 (1976), pp. 904–914, https://doi.org/10.1137/0713071.

- [9] F. Cucker and S. Smale, On the mathematical foundations of learning, Bulletin of the American Mathematical Society, 39 (2002), pp. 1–49.

- [10] F. Cucker and D. X. Zhou, Learning Theory: An Approximation Theory Viewpoint, vol. 24, Cambridge University Press, 2007.

- [11] J. Dick and M. Feischl, A quasi-Monte Carlo data compression algorithm for machine learning, J. Complexity, 67 (2021), p. 101587.

- [12] J. Dick and F. Pillichshammer, Digital Nets and Sequences: Discrepancy Theory and Quasi–Monte Carlo Integration, Cambridge University Press, 2010.

- [13] W. E and B. Yu, The deep Ritz method: a deep learning-based numerical algorithm for solving variational problems, Commun. Math. Stat., 6 (2018), pp. 1–12, https://doi.org/10.1007/s40304-018-0127-z.

- [14] K.-T. Fang, Some applications of quasi-Monte Carlo methods in statistics, in Monte Carlo and Quasi-Monte Carlo Methods 2000: Proceedings of a Conference held at Hong Kong Baptist University, Hong Kong SAR, China, November 27–December 1, 2000, Springer, 2002, pp. 10–26.

- [15] X. Glorot and Y. Bengio, Understanding the difficulty of training deep feedforward neural networks, in Proceedings of the thirteenth international conference on artificial intelligence and statistics, JMLR Workshop and Conference Proceedings, 2010, pp. 249–256.

- [16] I. Gühring and M. Raslan, Approximation rates for neural networks with encodable weights in smoothness spaces, Neural Networks, 134 (2021), pp. 107–130, https://doi.org/10.1016/j.neunet.2020.11.010.

- [17] Z. He, Z. Zheng, and X. Wang, On the error rate of importance sampling with randomized quasi-Monte Carlo, SIAM J. Numer. Anal., 61 (2023), pp. 515–538, https://doi.org/10.1137/22M1510121.

- [18] K. Hornik, Approximation capabilities of multilayer feedforward networks, Neural Networks, 4 (1991), pp. 251–257, https://doi.org/10.1016/0893-6080(91)90009-T.

- [19] S. Ioffe and C. Szegedy, Batch normalization: Accelerating deep network training by reducing internal covariate shift, in International conference on machine learning, pmlr, 2015, pp. 448–456.

- [20] A. Jentzen, D. Salimova, and T. Welti, A proof that deep artificial neural networks overcome the curse of dimensionality in the numerical approximation of Kolmogorov partial differential equations with constant diffusion and nonlinear drift coefficients, Commun. Math. Sci., 19 (2021), pp. 1167–1205, https://doi.org/10.4310/cms.2021.v19.n5.a1.

- [21] Y. Jiao, Y. Lai, Y. Lo, Y. Wang, and Y. Yang, Error analysis of deep Ritz methods for elliptic equations, arXiv preprint arXiv:2107.14478, (2021).

- [22] D. P. Kingma and J. Ba, Adam: A method for stochastic optimization, 2017, https://arxiv.org/abs/1412.6980.

- [23] V. Koltchinskii, Oracle Inequalities in Empirical Risk Minimization and Sparse Recovery Problems: École D’Été de Probabilités de Saint-Flour XXXVIII-2008, vol. 2033, Springer Science & Business Media, 2011, https://doi.org/10.1007/978-3-642-22147-7.

- [24] S. Liu and A. B. Owen, Quasi-Monte Carlo Quasi-Newton in variational bayes, J Mach Learn Res, 22 (2021), pp. 11043–11065.

- [25] M. Longo, S. Mishra, T. K. Rusch, and C. Schwab, Higher-order quasi-Monte Carlo training of deep neural networks, SIAM J. Sci. Comput., 43 (2021), pp. A3938–A3966.

- [26] P. L’Ecuyer, Quasi-Monte Carlo methods with applications in finance, Finance Stoch., 13 (2009), pp. 307–349, https://doi.org/10.1007/s00780-009-0095-y.

- [27] S. Mishra and T. K. Rusch, Enhancing accuracy of deep learning algorithms by training with low-discrepancy sequences, SIAM J. Numer. Anal., 59 (2021), pp. 1811–1834.

- [28] H. Niederreiter, Low-discrepancy point sets obtained by digital constructions over finite fields, Czechoslovak Math. J., 42 (1992), pp. 143–166, http://eudml.org/doc/31269.

- [29] H. Niederreiter, Random Number Generation and Quasi-Monte Carlo Methods, Society for Industrial and Applied Mathematics, 1992, https://epubs.siam.org/doi/abs/10.1137/1.9781611970081.

- [30] I. Ohn and Y. Kim, Smooth function approximation by deep neural networks with general activation functions, Entropy, 21 (2019), https://doi.org/10.3390/e21070627.

- [31] A. B. Owen, Randomly permuted (t,m,s)-nets and (t, s)-sequences, in Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing, H. Niederreiter and P. J.-S. Shiue, eds., New York, NY, 1995, Springer New York, pp. 299–317, https://doi.org/10.1007/978-1-4612-2552-2_19.

- [32] A. B. Owen, Multidimensional variation for quasi-Monte Carlo, in Contemporary Multivariate Analysis And Design Of Experiments: In Celebration of Professor Kai-Tai Fang’s 65th Birthday, World Scientific, 2005, pp. 49–74.

- [33] A. B. Owen, Halton sequences avoid the origin, SIAM Rev., 48 (2006), pp. 487–503, https://doi.org/10.1137/S0036144504441573.

- [34] M. Raissi, P. Perdikaris, and G. Karniadakis, Physics-informed neural networks: A deep learning framework for solving forward and inverse problems involving nonlinear partial differential equations, J. Comput. Phys., 378 (2019), pp. 686–707, https://doi.org/10.1016/j.jcp.2018.10.045.

- [35] P. Ramachandran, B. Zoph, and Q. V. Le, Searching for activation functions, 2017, https://arxiv.org/abs/1710.05941.

- [36] A. D. Rasamoelina, F. Adjailia, and P. Sinčák, A review of activation function for artificial neural network, in 2020 IEEE 18th World Symposium on Applied Machine Intelligence and Informatics (SAMI), IEEE, 2020, pp. 281–286.

- [37] L. Richter and J. Berner, Robust SDE-based variational formulations for solving linear PDEs via deep learning, in Proceedings of the 39th International Conference on Machine Learning, K. Chaudhuri, S. Jegelka, L. Song, C. Szepesvari, G. Niu, and S. Sabato, eds., vol. 162 of Proceedings of Machine Learning Research, PMLR, 17–23 Jul 2022, pp. 18649–18666, https://proceedings.mlr.press/v162/richter22a.html.

- [38] S. Shalev-Shwartz and S. Ben-David, Understanding Machine Learning: From Theory to Algorithms, Cambridge University Press, 2014.

- [39] J. Sirignano and K. Spiliopoulos, DGM: A deep learning algorithm for solving partial differential equations, J. Comput. Phys., 375 (2018), pp. 1339–1364, https://doi.org/10.1016/j.jcp.2018.08.029.

- [40] J. W. Thomas, Numerical Partial Differential Equations: Finite Difference Methods, vol. 22, Springer Science & Business Media, 2013, https://doi.org/10.1007/978-1-4899-7278-1.