ON TECHNICAL BASES AND SURPLUS IN LIFE INSURANCE

Abstract

We revisit surplus on general life insurance contracts, represented by Markov models. We classify technical bases in terms of boundary conditions in Thiele’s equation(s), allowing more general regulations than Scandinavian-style ‘first-order/second-order’ regimes, and replacing the traditional retrospective policy value. We propose a ‘canonical’ model with three technical bases (premium, valuation, accumulation) and show how each pair of bases defines premium loadings and surplus. Along with a ‘true’ or ‘real-world’ experience basis, this expands fundamental results of Ramlau-Hansen (1988a). We conclude with two applications: lapse-supported business; and the retrospectively-oriented regime proposed by Møller & Steffensen (2007).

keywords

Counting Process, Life Insurance, Surplus, Technical Bases, Thiele’s Differential Equation

contact addresses

† Department of Actuarial Sciences, The Faculty of Business, Karabük University, Karabük, 78050, Turkey, and Institute of Applied Mathematics, Middle East Technical University, Ankara, 06800, Turkey.

‡ Research Centre for Longevity Risk, Faculty of Economics and Business, University of Amsterdam.

§ Department of Actuarial Mathematics and Statistics, Heriot-Watt University, Edinburgh EH14 4AS, UK, and the Maxwell Institute for Mathematical Sciences, UK.

Corresponding author: Angus Macdonald, A.S.Macdonald@hw.ac.uk.

1 Introduction

1.1 Motivation — Unfinished Business

Hoem introduced Markov models into life insurance mathematics (Hoem 1969, 1988) and showed how life insurance cashflows could be represented by counting processes (Hoem & Aalen 1978). These ideas were developed in several directions in the following years, see Section 1.2. We highlight two.

- (a)

-

(b)

Surplus: Emerging surplus was studied in Ramlau-Hansen (1988a), Linnemann (1993) and others. In particular the first of these studies defined the surplus process as a stochastic object and decomposed it into an expected term plus a martingale error term111This idea has been taken up recently (see Schilling et al. (2020), Jetses & Christiansen (2022)) to define a similar decomposition of surplus into its contributions from each of several risk sources. (Section 5.3).

Almost in passing, the great classical results of life insurance mathematics were extended and clarified. Hoem (1969, 1988) had generalized Thiele’s differential equation (henceforth just Thiele’s equation) to Markov models. Wolthuis (1987), Ramlau-Hansen (1988b) and Norberg (1992) in particular showed Hattendorff’s theorem (Hattendorff 1868) to have been a prescient statement of a martingale property and Lidstone’s theorem (Lidstone 1905) was given modern form by Norberg (1985).

However, this entire literature took as given a Scandinavian style of insurance regulation, in which premiums and reserves were calculated on the same first-order technical basis. The experience was then defined by a second-order technical basis which, all being well, resulted in positive surpluses. See, for example, Linnemann (1993) and Norberg (1999), or for a discrete-time version Olivieri & Pitacco (2015). Requiring valuations to use the premium basis is more restrictive than in many jurisdictions (see Section 2.4); in particular it leaves two significant gaps.

-

(a)

It rules out common approaches such as net premium and gross premium valuations on bases chosen by the valuation actuary.

-

(b)

The ability to vary the valuation basis, with considerable freedom, means that the actuary can choose when surplus will emerge, either sooner or later. This has obvious and important consequences. It is of interest to study how the choice of technical bases influences surplus, following in the footsteps of Lidstone (1905).

The example which motivated this work is the well-known result that the expected present value (EPV) of the total surplus earned in respect of a life insurance policy does not depend on the valuation basis used. It implicitly assumes that premiums, valuations and the experience rest on separate technical bases. The following, from a standard (and vintage) UK text on life insurance practice, is typical:

“The effect of changing the valuation basis is to modify the [uniform] rate of emergence of profit . The total real profit is unaffected, however, since it is a function of the premium and experience bases which cannot be affected by the valuation basis.” Fisher & Young (1965).

This proposition (when formulated more precisely) is just one of a suite of results about the incidence of surplus arising from relationships between pairs of technical bases. It is part of the third of the relationships introduced informally below labelled R1 to R3.

-

R1:

Initial surplus (strain) at inception of the policy arises from the difference between premium and valuation bases, and does not depend on the experience basis.

-

R2:

Surplus emerging during the policy term arises from the difference between the valuation and experience bases, and does not depend on the premium basis.

-

R3:

The EPV of total profit at the end of the term: (i) arises from the difference between the premium and experience bases; (ii) is equal to the EPV of the total surpluses in R1 and R2 and; (iii) does not depend on the valuation basis.

The relationships are illustrated in Figure 1. These are familiar enough to be assumed without further comment in some practice-oriented actuarial syllabuses (see the quotation above). Moreover, each relationship has an illuminating corollary, as follows.

-

R1*:

The contractual premium can be decomposed into a pure risk premium and two separate loadings for surplus: one capitalized at outset, the other emerging as premiums are paid.

-

R2*:

The EPV of the cumulative surplus at any time can be decomposed into: (a) initial surplus, plus; (b) premium loadings, plus; (c) a sum of pairs, each pair consisting of a systematic part and a martingale residual, for each source of surplus.

-

R3*:

The EPV of the total surplus is independent of the valuation basis (mentioned as R3 (iii) above).

R2 and R3* are standard in a discrete-time setting with two technical bases, see for example Olivieri & Pitacco (2015). The research-oriented literature addresses R1, R2 and R2* in the context of two technical bases, but not R1*, R3 or R3*, or the system as a whole. This leads us to the three purposes of this paper.

-

(a)

We set out to repair the gaps described above, in the setting of Markov models. That is, to describe three technical bases, the relationships R1 to R3 and their corollaries R1* to R3* in quite general terms.

-

(b)

We may say that a technical basis becomes operational by parametrizing Thiele’s equation(s). We propose then to classify technical bases in terms of the boundary conditions assumed; initial, terminal or both. This leads naturally to the relationships R1 to R3 and their corollaries, and extends to Markov models. Along the way, we suggest retiring the classical retrospective policy value, which has never found an agreed definition in general Markov models (see the Appendix).

-

(c)

We also have in mind that different terminologies (first-order, second-order versus premium, valuation, experience), techniques (net premium versus gross premium), frameworks (discrete-time versus continuous-time) and even pedagogies, can hamper communication between actuaries brought up in different traditions. We hope that this paper may help to bridge any gaps.

A study which shares some of these aims is Møller & Steffensen (2007), in particular Chapters 2 and 6. This also breaks away from Scandinavian-style regulation, but in a different way, aiming to base life insurance liabilities on retrospective considerations. They also consider the analysis of technical surplus into systematic and martingale components, R2* above, begun by Ramlau-Hansen (1988a) and since axiomatized by Schilling et al. (2020) and Jetses & Christiansen (2022). We will compare approaches in the extended example of Section 6.2.

1.2 The Literature on Thiele’s Equation, Markov Models and Surplus

The earlier history of Thiele’s equation is told in Hoem (1983) and Norberg (2004). Notably, its originator, the Danish actuary Thorvald Thiele, never published it, and it first appeared in print in Gram (1910) and Jørgensen (1913) (though it is proved en passant in deriving Lidstone’s theorem (Lidstone 1905, p.227)).

Its second phase of development began with Hoem showing that it generalized easily to Markov models in continuous time, parametrized by transition intensities, representing a wide range of possible insurance contracts, see Hoem (1969, 1988), and also Sverdrup (1965) for a notable antecedent.

Following Hoem, many papers, in particular Norberg (1985, 1990, 1991, 1992, 1995) and others (Ramlau-Hansen (1988a), Wolthuis & Hoek (1986), Wolthuis (1987), Wolthuis & Hoem (1990), Wolthuis (1992, 1994), Milbrodt (1993), Milbrodt & Stracke (1997)) pursued multiple-state models. Emergence of surplus was a major theme (Ramlau-Hansen (1988b), Linnemann (1993, 1994, 1995, 2003)) followed by distribution of bonus (Width (1986), Ramlau-Hansen (1991), Norberg (1999), Linnemann (2003, 2004)).

Hoem & Aalen (1978) were first to translate life insurance mathematics into counting process language. It was by no means adopted uniformly in all the work cited above, but its power to bring new insights was perhaps shown particularly by Ramlau-Hansen (1988a, b) on second moments and surplus, and Norberg (1991, 1992) on the rôle of filtrations as a model of information. We already mentioned Møller & Steffensen (2007) as a study that takes these ideas further, in models with more than two technical bases, see Section 6.2 below.

Most recently, research has moved towards combined models of financial risk (canonical model, Black-Scholes) and long-term insurance risk (canonical model, life insurance), though without yet arriving at any clear destination. This lies beyond our scope. For more details see, for example, Møller & Steffensen (2007).

1.3 Plan of this Paper

Section 2 introduces basic ideas in the context of the simplest life insurance contract; Thiele’s differential equation, evaluating past and future cashflows, and technical bases. These ideas form the basis of Section 3 where the Markov model is introduced, with particular attention to the counting process representation of the data, and the special rôle of the ‘true’ or ‘experience’ technical basis.

Section 4 proposes a classification of technical bases in terms of the boundary conditions satisfied in the associated Thiele’s equation. To an extent this replaces the classical retrospective policy value as a model of accumulation depleted by decremental forces; the retrospective policy value is discussed further in the Appendix. The analysis is general enough to cover a wide range of valuation methods and extends the literature beyond Scandinavian-style ‘first-order’ and ‘second-order’ technical bases.

Section 5 introduces a model for the balance sheet of a life insurer in terms of three technical bases, and analyzes the surplus arising during a contract’s term. The analysis is expressed as three relationships between pairs of technical bases, each well-known in practice, and extends the analysis of Ramlau-Hansen (1988a), Schilling et al. (2020) and Jetses & Christiansen (2022). Finally, Section 6 gives two applications; lapse-supported business and a model proposed by Møller & Steffensen (2007).

Our conclusions are in Section 7.

2 A Simple Life Insurance Model

2.1 Thiele’s Differential Equation

Before introducing the Markov model, consider the simplest life insurance policy, commencing at age , with term years. On death at time within the term a sum insured of is paid immediately, and on survival for years a maturity benefit of is paid (possibly ). Level premiums are paid continuously throughout the term at rate per year. We assume there are no lump-sum cashflows, except benefits, and ignore expenses to keep notation simple.

Suppose we are given a technical basis consisting of a force of interest and force of mortality . We suppress the initial age , so is understood to mean . Then Thiele’s differential equation (Dickson et al. 2020) is:

| (1) |

The function of time represents a fund growing at force of interest , while being added to by a continuous stream of premiums at rate per year, and decremented by a force of mortality that causes a sum insured of to be paid immediately on death, this cost to the insurer being offset by the reserve they hold.

2.2 A Model of a Life Insurance Fund: One Technical Basis

Define the discount factor allowing for survivorship as well as interest:

| (2) |

then write down the equation of value solved to determine :

| (3) |

Split this integral at any time , divide by and rearrange:

| (4) |

We can verify that the left-hand side of equation (4) is the solution of Thiele’s equation with initial boundary condition , and the right-hand side is the solution with terminal boundary condition .

We therefore have, in a single equation (3), a mathematical model of the evolution of assets and liabilities under a life insurance policy, such that:

-

(a)

there is a single technical basis for premiums, policy values and the experience;

-

(b)

the premium rate satisfies the equivalence principle;

-

(c)

no capital is required at outset ();

-

(d)

no profit remains after maturity ();

-

(e)

all policy values are solutions of Thiele’s equation; and

-

(f)

retrospective and prospective policy values are equal at all times (a kind of self-financing condition).

Norberg (1991) noted: “Thus, the traditional concept of ‘retrospective reserve’ is rather a retrospective formula for the prospective reserve ”.

2.3 A Stochastic Decomposition

We get more insight into equation (4) following Norberg (1991) by writing down the cumulative cashflow as a stochastic process and considering the information acquired by observing this process up to time (see the Appendix (e) for more details). Let be the total cashflow up to time (for example, in Section 2.2, ), and let be a discount function (for example, ). Then the value at time of all cashflows, denoted by , again splitting the integral at time , is:

| (5) |

Taking expectations conditional on , information available at time , we get:

| (6) |

We recognize the first term on the right-hand side as the accumulation of actual cashflows, and the second term as the prospective policy value. Taking expectations of equation (6) conditional on , we get:

| (7) |

If the equivalence principle holds, this is zero, and the insurance contract is, in expectation, a self-financing portfolio, in the derivative-pricing sense (see, for example, Baxter & Rennie (1996)). We see that the conventional meaning of ‘accumulation’ in life insurance mathematics is in fact an expected value conditional on , a fact to add to Norberg’s comment in Section 2.2 above.

2.4 Technical Bases and Regulations

Motivated by the above, we define a technical basis, denoted by , to be the pair . We then ask if one technical basis can serve all purposes, at all times, and answer ‘no’, as the following examples show.

-

(a)

As time passes, the interest and mortality used to calculate the contractual premium fade into historic more than current interest.

-

(b)

The valuation of past cashflows may be a matter of factual accounting; the valuation of future cashflows rarely is.

Under Scandinavian-style regulation, the first-order technical basis serves for both premiums and valuations. There is one technical basis , one premium rate, denoted by , which satisfies equation (3) under and is also the premium valued, meaning that when we write a policy value as:

| (8) |

the future premiums referred to are at rate per annum.

Under other valuation regimes this restriction on the choice of technical basis and the choice of premium valued may be lifted (see Fisher & Young (1965) for example).

-

(a)

There may be separate technical bases for premiums and valuations, which we may denote by and respectively. This may be mandatory or merely permissive.

-

(b)

Let be the premium rate under — that is, the premium rate that solves equation (3) under — and let be the corresponding premium rate under . Then we have a choice as to the premium rate actually valued — that is, the premium rate defining the cashflow in the last term in equation (8).

-

(1)

If is the premium rate valued we have a net premium valuation, and it will still be true that .

-

(2)

If is the premium rate valued we have a gross premium valuation, and in general it will no longer be the case that .

-

(3)

The rules may be still broader, however, and allow the actuary to choose a valuation premium rate different from both and ; denote this by . This means that in a policy value of the form (8) we calculate EPVs using but the premium rate valued is .

Hence we need both and to specify policy values, see Section 2.5.

-

(1)

-

(c)

In practice, the choice of valuation basis may be even wider than shown above. For example, (Fisher & Young 1965, p.269) suggests in some special cases using a policy value equal to a few years’ net premiums, perhaps accumulated at interest. In such cases, policy values need not be solutions of Thiele’s equation. In this paper, we restrict attention to policy values that are solutions of Thiele’s equation.

We summarize below how the elements of a regulatory regime may differ from the Scandinavian style.

-

(a)

Under Scandinavian-style regulations, and . Policy values are always solutions of Thiele’s equation. Everything simply follows the first-order technical basis. These constraints are so familiar to those accustomed to them that they often go unstated.

-

(b)

Under other regulatory regimes, we may have and equal to (gross premium valuation) or (net premium valuation), or neither of or (actuary’s discretion). Policy values are usually solutions of Thiele’s equation but need not be. These freedoms are so familiar to those accustomed to them that they often go unstated.

If this paper has a communications element, it consists of stating clearly what is described above as often going unstated.

In the next section, we formalize the intuitive discussion above.

2.5 Valuation Bases, Pure Premiums, and Valuation Premiums

Given an arbitrary technical basis , define the associated pure premium rate, denoted by , to be the premium rate that satisfies the equation of value under . That is, is chosen such that:

| (9) |

where and are on technical basis . Note that we are assuming, without further comment, that the equation of value under has a unique ‘sensible’ solution222In general the equation of value has many solutions (it is often a polynomial equation, for example). What we require is that it has a unique real and non-negative solution. .

Let and be the technical/valuation bases intended for the calculation of premiums, policy values and accumulations respectively. Define the contractual premium to be and the valuation pure premium to be .

The fact that is the valuation basis means that it is the basis used to calculate the EPV of future cashflows. It does not mean that the valuation pure premium is necessarily one of those future cashflows, namely the premium rate valued, see Section 2.4. Therefore we introduce an augmented technical basis consisting of the technical basis and the premium rate actually to be valued . We define , and we define a new function . The only requirement we impose is that is the pure premium rate associated with some technical basis , that is , so that the resulting policy values are solutions of Thiele’s equation. By choosing appropriately, we can specify net premium, gross premium or other valuation methods.

-

(a)

Choose and we have a gross premium valuation basis.

-

(b)

Choose and we have a net premium valuation basis.

-

(c)

Choose and ; then the valuation basis is the same as the premium basis and we have Scandinavian-style regulation.

These cases probably cover the main examples of interest. However, is arbitrary within sensible limits, and is not confined to the examples above. A case in point might be a net premium valuation basis different from the premium basis, but with a maximum premium valued equal to 90% of . Then for some contracts and .

We call the accumulation basis, and for simplicity we assume all accumulations of past cashflows accumulate the contractual premium .

Table 1 summarizes the main premium rates defined in respect of technical bases.

| Rate | Description |

|---|---|

| Pure premium rate on technical basis | |

| Valuation premium rate specified by augmented valuation basis | |

| Contractual premium rate on premium basis . |

3 Markov Models, Data and Thiele’s Equations

3.1 Definitions: Markov Models

Suppose a process takes values in a state space , labelling states representing ‘alive’, ‘ill’, ‘dead’ and so on. Define to be the state occupied by the life at time , age ; we assume is right-continuous with left-hand limits, and . Define occupancy probabilities, denoted by , as:

| (10) |

and transition intensities, denoted by , as:

| (11) |

assuming all such limits exist. The Markov assumption is present in conditioning only on , the state occupied at time , excluding any other history. Also define and the probabilities of not leaving a state are defined as:

| (12) |

3.2 Definitions: Insurance Contracts

Under a multiple-state model, insurance contracts are defined by payments of three types, namely lump sums paid immediately on a transition between states, lump sums payable upon expiry in a given state, and premiums paid continuously during a sojourn in a state. Accordingly define:

| Lump sum paid on transition from state to state | ||||

| Lump sum paid on expiry while in state | ||||

Cashflows from the insurer to the insured are positive, premiums are treated as a negative annuity, and so on. For simplicity we have made the following assumptions, all of which can be relaxed at the cost only of more notation.

-

(a)

We ignore annuity-type benefits.

-

(b)

We consider only constant benefits, but they can be made functions of time.

-

(c)

We ignore expenses.

If it helps, we can represent a contract by the collection of its parameters, denoted by , thus: . We suppress other factors such as age, term, sex and so on, that can be included as required by the context.

3.3 Representations of Multiple-State Model Data

-

(a)

A sample path of is a piecewise-constant function on , taking values in , right-continuous with left-hand limits. We call this the sample-path representation of the process.

-

(b)

Another representation generalizes the idea of the time until death of a life aged being the random variable (Bowers et al. (1997), Gerber (1990), Olivieri & Pitacco (2015), Dickson et al. (2020)). A ‘sample point’ is now a random integer , a sequence of random times and, for each random time , a pair of states called a mark, identifying a transition in the model. This is the marked point process (MPP) representation of the process.

-

(c)

A third representation is in terms of counting processes. Define to be the number of direct transitions from state to state in . Then defined as the collection , with the condition that no two processes in the collection can jump simultaneously, is a multivariate counting process.

These representations are completely equivalent, see (Jacobsen 2006, Chapter 2) for technical details. Also, they describe the data generated by the process we are modelling, not the models themselves. To see this, note that none of them mentions the intensities .

Useful with all three representations are the following indicator processes of presence in states, denoted by , for :

| (13) |

where is the usual indicator of event . means that the process is at risk of jumping out of state at time .

Each representation can also be equipped with a filtration (non-decreasing sequence of -algebras) constituting a model of information obtained by observing events over time. By an abuse of notation, let denote the filtration under any of the three representations.

3.4 Technical Bases, Pure Premiums, and Valuation Premiums

For simplicity, we assume a force of interest that is constant and the same for all states, hence we can write all discount factors as:

| (14) |

for . The definitions then follow very much along the lines of Section 2.5.

-

(a)

A technical basis for a given Markov model and contract , is a collection of force of interest and transition intensities.

-

(b)

The pure premium rates associated with the technical basis are the premium rates satisfying the equation of value:

(15) and other constraints (see below) that ensure uniqueness, and it is denoted by , with th element .

-

(c)

Exactly as in Section 2.5, for valuation the technical basis is augmented with a set of premium rates called the valuation premium rates to define the valuation basis , and we define the functions and analagously. We leave the details to the reader.

-

(d)

Given a technical basis, we require some constraints on the admissible values of the premium rates to ensure that the equation of value (15) has a unique solution. A simple example would be that level premiums are payable continuously while in state 1, and no premiums are payable otherwise. Other sensible solutions may exist, such as premiums increasing linearly over time, so we assume constraints force a choice among all such solutions of equation (15), so the function , defined above, makes sense.

3.5 Prospective Policy Values and Thiele’s Equations in a Markov Model

Assume a force of interest , and premium rates payable while in state . Hoem (1969, 1988) defined prospective policy values in state , denoted by , as (our notation):

| (16) |

Thiele’s equations for policy values are the system:

| (17) | |||||

| (18) |

where , allowing for a new policy value to be set up on a transition between states.

4 A Classification of Technical Bases

4.1 Motivation

Conventionally, technical bases have parametrized Thiele’s equations, which in turn defined policy values as solutions. Policy values were prospective or retrospective and the two were equal under ‘nice’ circumstances, see Section 2.2, which provided life insurance mathematics with a form of self-financing condition.

The awkward quantity in this scheme is the retrospective policy value. Prospective policy values have a clear purpose, in which the pooling of future stochastic risk is clearly probabilistic and defined in terms of transition intensities. Accumulations of past cashflows are also conceptually clear, and not probabilistic, but retrospective pooling of risk is expressed in probabilistic language, in terms of transition intensities — see yet again Norberg’s comment cited at the end of Section 2.2, and Section 2.3, — and, when we consider Markov models, apparently not well-defined — see the Appendix.

We sidestep this difficulty in the following sections by defining an accumulation fund to be a solution of Thiele’s equations satisfying an initial boundary condition of having value zero in every state; therefore, an original condition of no assets. The traditional retrospective policy value as used in the literature (in particular, in Ramlau-Hansen (1988a)) will often coincide with this definition, but we do not rely on that being so.

4.2 Proposed Classification of Technical Bases

Our classification of technical bases, in terms of boundary conditions satisfied by solutions of the corresponding Thiele’s equations, is set out below, and summarized in Table 2. The general idea is that two out of the premium rate, the initial boundary condition and the terminal boundary condition are fixed, and the third is to be determined. Note that every policyholder is assumed to start in state 1.

-

(a)

If the boundary conditions are satisfied, we call an accumulation basis, and the associated functions accumulation funds, alternatively policy accounts. It represents the accumulation of a fund with no initial endowment. We often use the notation and may denote the fund by .

-

(b)

If the boundary conditions , are satisfied, we call the augmented technical basis a valuation basis, and the associated functions policy values or sometimes prospective policy values. We often use the notation and . The premiums valued are , see Section 3.4.

-

(c)

If both sets of boundary conditions and are satisfied, we call a proper valuation basis, and the associated functions are again called policy values.

-

(d)

Any proper valuation basis is a candidate to be chosen as the premium basis; precisely one must be so chosen, and in that rôle it is denoted by .

-

(e)

If none of the above boundary conditions are met the technical basis defines a fund with no special name.

| Basis | Boundary Condition(s) | Name of Basis | Name, Notation of Function |

|---|---|---|---|

| None specified | Technical Basis | Fund, | |

| Accumulation Basis | Accumulation Fund, or | ||

| Policy Account, | |||

| Valuation Basis | Policy Value, | ||

| AND | Premium Basis | Policy Value, | |

| Experience Basis | Asset Share, |

The different treatment of funds at time is because of their interpretation in the balance sheet. A non-zero policy value at outset signals a movement on the liability side, either the release of surplus or a need for capital support. It is important that these are realistic and transparent because they can be created or conjured away by choosing the valuation basis. A non-zero accumulation fund, on the other hand, would (or should) represent a movement on the assets side of the balance sheet and should not be an artifact of the technical basis. This does not say that assets must be taken at market value in the balance sheet.

4.3 Canonical Examples of Valuation Bases

The examples of valuation bases for the simple life insurance model (see Section 2.5) can be restated in terms of the Markov model.

-

(a)

Valuation bases with are called gross premium valuation bases.

-

(b)

Valuation bases with are called net premium valuation bases (and must also be proper valuation bases).

-

(c)

Under Scandinavian-style regulations, the first-order technical basis defines both a gross premium and a net premium valuation basis. Most of the literature uses such a basis.

4.4 Examples

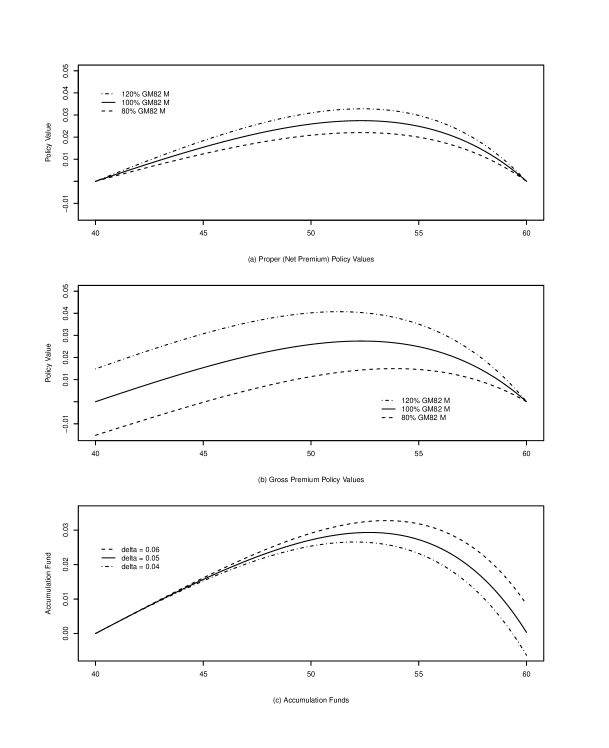

Figure 2 illustrates policy values and accumulation bases for a term insurance contract (age 40, term 20 years, sum insured $1), given a premium basis where is on the Danish GM82 Males life table. Panel (a) shows proper policy values (equivalently, net premium policy values, see Section 4.3), with both and fixed, but pure (valuation) premium varying; panel (b) shows gross premium policy values with and valuation premium fixed but varying; and panel (c) shows accumulation funds with and contractual premium fixed and varying. Essentially, Scandinavian-style regulation of liabilities admits only a fixed technical basis represented by (a), net premium valuations a choice of technical bases represented by (a), and gross premium valuations also technical bases represented by (b).

4.5 The Experience Basis, Asset Shares and Martingales

We assume the existence of a unique accumulation basis representing the actual experience and called the experience basis. It may also sometimes be called the real, asset share or martingale basis. The corresponding fund, denoted by , is called the asset share.

A precise interpretation of the statement that technical basis is ‘true’, insofar as it concerns the intensities, is that the processes defined by:

| (19) |

(see Section 3.3 for definitions of and ) are a set of orthogonal -martingales under , and is unique in this respect (this is the Doob-Meyer Decomposition under , see Andersen et al. (1993) or Fleming & Harrington (1991)).

Technical basis occupies a privileged position in the model. It is the technical basis that is assumed to generate the data. With the counting process representation, it provides a fundamental link between model and data. A technical basis with intensities estimated from the data strictly ought to be denoted by but we do not use this notation in the sequel.

4.6 A Note on Expected Values

It was assumed in Section 3 that a technical basis defines transition probabilities (see equation (10)), hence also an expected value operator, at least with respect to the transition intensities of the technical basis. Given technical basis in this section, we could define an expected value operator . For the avoidance of doubt, we do not require this degree of abstraction. All expected values in this paper are based on the technical basis , and can (loosely) be regarded as ‘true’ expectations under the ‘real world’ measure, and we use the unadorned operator throughout to mean .

4.7 A Note on Policy Accounts

An accumulation basis may be used to represent amounts credited to a policy in a policy account, which may subsequently be used as a basis for declaring bonus. See for example Ramlau-Hansen (1988a), Linnemann (2003), Møller & Steffensen (2007). Some smoothing of investment returns may be desired, and pooling of mortality risk is required, so the ‘raw’ experience is not suitable for this purpose. Other parties may be due a share of any surplus, for example shareholders or the insurer’s ‘estate’, so the full experience basis may not be appropriate either. Therefore, in what follows, we usually consider surplus with respect to an arbitrary accumulation basis .

5 Surplus

5.1 A Simple Model of a Life Insurer’s Balance Sheet

The simplest model of a life insurer’s balance sheet has one technical basis, see Section 2.2, and attains a certain level of mathematical perfection, but does not support essential features from practice, such as surplus. Most of the literature uses a model with ‘first-order’ and ‘second-order’ technical bases based on Scandinavian-style regulation. We consider a model with three technical bases, one of each type defined in Section 4.

Our model is canonical, in the sense that: (a) models with fewer technical bases lose functionality; and (b) adding more technical bases duplicates functionality.

As before, we call the three bases the premium basis, valuation (or policy value) basis and accumulation basis333In the UK, historically, life insurance regulation devolved great responsibility for solvency reporting on the individual actuary. Technical bases were not imposed, and premium rates were not regulated. See Cox & Storr-Best (1962) or Turnbull (2017) for example, for accounts of these developments., denoted by and respectively. If , we have a model of asset shares. Otherwise, we have a model with an arbitrary policy account as asset.

Figure 3 illustrates the relationships between the three technical bases. It is the same as Figure 1 except that ‘Experience Basis’ has been replaced by ‘Accumulation Basis’ since is not necessariy the same as . For example, the accumulated quantity may be a policy account (Section 4.7) which is credited with the fund rate of return less one percent.

5.2 Basic Surplus Relationship

Conventionally, given a valuation basis and an accumulation basis , surplus is generated at rate at time , during a sojourn in state , as follows. (Note we allow here just for the purposes of demonstration.) Under Thiele’s equation applied to :

| (20) |

where is the policy value, is the valuation premium rate and , see Section 3.5. Applying the parameters of to we have:

| (21) |

(recall that we assume all accumulation bases operate on the contractual premium rates ) and by subtraction of equation (20) from (21):

| (22) |

(From this point we resume the assumption of constant , hence there is no contribution to surplus from investment returns.) Thus the present value of total surplus up to time , allowing for any generated at inception can be written as:

| (23) |

We make some comments below on the functions .

- (a)

-

(b)

Given valuation basis and accumulation basis , define the EPV of surplus to time to be as follows:

(24) as in equation (23), with surplus rates defined by and .

-

(c)

The functions do not depend on any boundary conditions of Thiele’s equations, just the parameters. Therefore ‘surplus’ during the policy term is just a relative quantity that can be applied to measure the difference between any pair of technical bases of any type, not confined to an accumulation basis and a valuation basis.

5.3 Surplus and the Counting Process Representation of the Data

In a fundamental paper, Ramlau-Hansen (1988a) defined the present value of surplus based on the counting process . We have changed his notation to be consistent with ours. He assumed a constant force of interest and the same statewise premium rates under all technical bases, therefore the intensities were the only sources of surplus. He also assumed . The present value of surplus to time , denoted by , is the random variable:

| (25) |

in which policy values are on technical basis Note that the first part of this expression is obtained from the first term in equation (5) upon defining:

| (26) |

The processes and are both stochastic processes, the first defined by the difference between technical bases and , the second defined by actual cashflows and technical basis . Note in particular that .

Ramlau-Hansen (1988a) gave two expressions for in terms of model quantities and and a martingale residual. The first, modified here to allow for , was in terms of accumulated surplus:

| (27) |

-

(a)

Wolthuis & Hoem (1990) remove the assumption that both technical bases have the same force of interest . Then the rate of surplus earned includes a term .

-

(b)

We retain the assumption that both technical bases have the same constant force of interest , just to simplify expressions. We do not assume that premium rates are the same on each technical basis, we may have .

The second expression for was in terms of an accumulated fund, which we call . In Ramlau-Hansen (1988a) this was a retrospective policy value on the second-order technical basis, with initial value zero, hence consistent with our definition of accumulation fund. Define . Then:

| (28) |

(and here is not necessarily zero). The author comments: “The relation (28) is interesting because it yields an expression for in terms of , the mean of which is often interpreted as the gain obtained over when a deterministic approach to life contingencies is applied” (notation has been changed to agree with ours).

The following result ((Ramlau-Hansen 1988b, (4.3)) with not necessarily zero) will be needed later:

| (29) |

It allows us to integrate functions along sample paths allowing for jumps, if we know their statewise values, in this case .

5.4 Relationships Between Technical Bases in Multiple-state Models

We wish to demonstrate the relationships R1 to R3 between pairs of technical bases, as stated in Section 1.1. Moreover, we would like to do so for modelled rates of surplus based on an arbitrary accumulation basis . The quantities we deal with, including , are stochastic, that is -measurable, and expectations are conditional expectations given .

Relationship R1 between premium and valuation bases is straightforward (Section 5.4.1) since it is independent of any accumulation basis. In Section 5.4.2, which largely follows Ramlau-Hansen (1988a), we integrate statewise rates of earned surplus along a sample path to find relationship R2. Finally in Section 5.4.3 we find relationship R3 but show that the final profit is independent of the valuation basis only if the accumulation basis is .

5.4.1 Relationship R1: Initial Surplus: Premium and Valuation Bases

Proposition 1

Let , and define , the pure premium rates associated with , and , the valuation premium rates associated with . Then:

| (30) |

or in words, equal to (minus) the present value of premium loadings capitalized at outset.

Proof: Write initial surplus at time as:

| (31) |

Add and subtract , and from the definition of , the result follows.

Corollary 1 is slightly out of logical sequence here, since its proof calls upon Proposition 2, but we take it where it fits most naturally.

Corollary 1

Each contractual premium rate can be decomposed into:

| (32) |

in which the terms on the right-hand side are, respectively, a pure risk premium, a loading capitalized at outset and a loading falling into surplus as premiums are paid.

(Compare with Linnemann (2003), who bases loadings on a second-order basis equating to the experience basis.) The regulator may apply external constraints to ensure that and ; we do not.

Proof of Corollary 1: It is obvious that can be decomposed as in equation (32), and is the pure risk premium in state on technical basis by definition. Proposition 1 shows that a loading of is capitalized at outset. Proposition 2 will show that the loading appears in the surplus at time . .

-

(a)

For example, if the premium basis is and is a gross premium valuation basis , then so is (minus) the EPV of the premium loadings , which therefore fall into surplus at outset.

-

(b)

Or, given a net premium valuation basis , the loading , so there is no initial surplus, and all loadings fall into surplus as premiums are paid (see Proposition 2).

-

(c)

While (a) and (b) above probably cover the major examples of interest, other possibilities exist. An example was given in Section 2.5. Or, it would be possible to fix the valuation premium rates such that , so that half the premium loadings are capitalized at outset and half are not.

Everything said above, qualitative and quantitative, is independent of the accumulation basis , which is intuitively obvious because at time there has not yet been any experience.

5.4.2 Relationship R2, Surplus During the Term: Valuation and Accumulation Bases

Recall that our purpose here is to express relationship R2 for modelled surpluses given by the rates ; Ramlau-Hansen’s equation (27) did so for crude surplus .

Proposition 2

(following Ramlau-Hansen). For time , , and defining , the present value of total surplus including initial surplus is:

which can be written as:

| (33) |

Proof: Consider the derivative of :

| (34) |

Add and subtract to/from the right-hand side:

| (35) | |||||

Therefore, in terms of rates during sojourns in state :

| (36) |

We then proceed via the following steps, omitting some extensive but elementary substitutions at (b): (a) multiply throughout by ; (b) add/subtract to/from the right-hand side, and rearrange, defining ; and (c) integrate on and sum over all states , to obtain:

Now apply the result in equation (29) to integrate the middle line above:

Corollary 2

The EPV of the cumulative surplus at any time can be decomposed into: (a) initial surplus, plus; (b) premium loadings, plus; (c) a sum of pairs, each pair consisting of a systematic part and a martingale residual, for each source of surplus. Moreover, does not depend on the premium basis , once the contractual terms have been fixed.

Proof: Recall that equation (27) excluded loading surplus, but the derivation of equation (LABEL:eq:AccumSurpFinal) included it. If we include loading surplus at rate in equation (27), and substitute the result into equation (LABEL:eq:AccumSurpFinal) we have:

| (39) |

and substituting this in equation (LABEL:eq:AccumSurpFinal) and re-arranging gives the result. It is plain upon inspection that the right-hand side of equation (LABEL:eq:AccumSurpFinal) does not depend on once the contractual basis is fixed. Equation (39) shows that the same is true of the left-hand side.

Comparing equations (22) and (39), we see the latter simply displays some operations performed on the former, in the absence of interest surplus, so offers another possible derivation of equation (LABEL:eq:AccumSurpFinal). However it is obtained, we need the representation in equation (LABEL:eq:AccumSurpFinal) for relationship R3, see Section 5.4.3.

The term ‘systematic surplus’ for the penultimate term in equation (LABEL:eq:AccumSurpFinal) is from (Møller & Steffensen 2007, p.213), see Section 6.2. These authors suggest two ways to smooth the random component of total surplus from equation (LABEL:eq:AccumSurpFinal): (i) take expectations conditioning on as in Norberg (1991) (see Section 2.3); or (ii) ignore both systematic and martingale components of the surplus. Schilling et al. (2020) suggest a decomposition of total surplus (including investment surplus) into systematic and (orthogonal) martingale components of which equation (LABEL:eq:AccumSurpFinal) shows those terms due to the transition intensities. Jetses & Christiansen (2022) develop this as the ‘infinitesimal sequential updates’ (ISU) decomposition principle for surplus, avoiding difficulties associated with finite accounting periods.

5.4.3 Relationship R3, Profit: Premium and Accumulation Bases

Proposition 3

The EPV of total final surplus is minus the EPV of the difference in risk premiums arising from any difference between and , plus a martingale residual term.

Proof: Evaluate equation (39) at and take expectations.

Corollary 3

If in Proposition 3, , then the EPV of total surplus is independent of the valuation basis.

Proof: If , then in the right-hand side of equation (LABEL:eq:AccumSurpFinal) evaluated at all , and policy values are involved only through , which does not depend on the valuation basis.

If then the EPV of the total surplus is not independent of the valuation basis, because of the presence of the in the systematic surplus.

5.5 Comment on Introducing Technical Basis

It is tempting to interpret the last term (in large square brackets) in equation (36) as follows: (a) the derivative gives us the change in between jumps, which we can integrate as usual; and (b) the second term (times ) is the expected change in on a jump to state at time , so we can obtain by applying the same operations term-by-term to the right-hand side of equation (36).

However, as noted in Section 4.6, all expected values are assumed to be with respect to the ‘true’ technical basis and we are not free to interpret terms in (times ) as expectations. Hence in the step between equations (36) and (LABEL:eq:TotalSurp3) we have to swap out the terms in for terms in in order to apply equation (29).

6 Examples

6.1 Example 1: Lapse-supported Business

Lapse-supported business is a class of non-participating business mainly written in North America. The policies are whole-of-life, or endowments to a high age, depending on local practice444Valuation regulations may require a published life table to be used. If published tables cease at age 100 (for example) this dictates the design of the contract. In Canada the main contract is an endowment ceasing at age 100, confusingly called ‘Term to 100’.; we assume they are endowments to age 100, with policy term . Surrender values are as small as possible, so ignoring expenses, and assuming policy values are positive, we assume that lapses are profitable at all durations. Therefore, premium rates can be reduced by allowing for future lapses. This forms the basis of a competitive market, particularly in Canada. However, insurers are exposed to the risk of lapse rates being lower than anticipated. See Haçarız et al. (2023) for details.

-

(a)

Model: The underlying model may be represented as in Figure 4, in which the age at issue is suppressed as usual.

-

(b)

Contract: Suppose the lapse-supported contract has premium rate per year, death benefit , maturity benefit at age 100, and anticipates a surrender value of at duration . This represents an extension of the model to a time-varying benefit , which we allow without further comment. When considering alternative technical bases, the rule that level premiums are paid while in state 1, and none in states 2 or 3, will ensure that the principle of equivalence can be applied in all sensible cases to calculate pure premiums .

-

(c)

Technical Bases: A technical basis may be denoted by , with associated pure premium since premiums are payable in state 1 only. Assume that all technical bases have the same interest and mortality, so differ only in respect of lapse intensities and premium rates. Our simplest baseline setup is that the premium, valuation and accumulation bases are the same, echoing the model in Section 2.2; moreover the accumulation basis is the ‘true’ :

(40) and . Recall that by definition. Define an alternative valuation basis as follows:

(41) where . Technical basis is a proper valuation basis for the same contract assuming nil lapses and with pure premium .

-

(d)

Relationship R1: The contractual premium rate decomposes into risk premium plus loading as follows: . Since the loading is negative.

-

(e)

Relationship R3: The EPV of total surplus, where expectations are taken under , does not depend on the valuation basis, or . Both are proper valuation bases so . It is straightforward to calculate rates of surplus emerging during stays in state 1 at times , as:

(42) and:

(43) respectively. Hence, defining to be the discount factor allowing for survivorship under , integrating and re-arranging, the EPV of future premiums ‘mortgaged’ by assuming lapse-support is:

(44) (see Haçarız et al. (2023)). The first term on the right-hand side is the EPV of the lapse surpluses anticipated, while the second term adjusts for the shortfalls on actual lapses. If all and , which means that lapses and lapse surplus are anticipated to the maximum possible extent, then:

(45) which is the EPV of policy values on all lapsed policies.

The quantities in equations (44) and (45) are negative, therefore they measure a need for capital support, rather than showing surplus being released. This aspect of lapse-supported business is, of course, well-known in practice, see Society of Actuaries (1987), and may well lead to there being reserving requirements a posteriori.

We could turn this example around and define , and put , so the premium and valuation bases allow for zero lapses, and then put and where , and then is an alternative proper valuation basis allowing for lapses, for the same contract. Then the question would be whether was sufficiently prudent to allow loadings to be capitalized. It would be interesting to know if the regulator’s response to this question depended on which way it was framed. Either way, this example demonstrates freedom from a priori constraints on technical bases.

6.2 Example 2: Møller & Steffensen (2007)

Møller & Steffensen (2007) define a model life insurer’s balance sheet in which prospective policy values have been subordinated. The aim is to admit retrospective considerations to the definition of the office’s liabilities, via the conversion of recognized surplus to bonus. The authors consider a contract with term years, annual premium rate , death benefit , and maturity benefit . They define three technical bases, differing from those in Section 5.1, as follows.

-

(a)

A first-order technical basis denoted by which at time defines the maturity benefit given by the premium rate and technical reserve (see (b) below) under the equivalence principle. Thus, at time , this technical basis performs the traditional rôle of premium basis. At times it determines an entitlement to an increased maturity benefit , therefore a bonus.

-

(b)

A second-order technical basis denoted by which defines the technical reserve under Thiele’s equation, with initial boundary condition .

-

(c)

A third-order technical basis denoted by which defines the total reserve under Thiele’s equation, with initial boundary condition .

All three technical bases are associated with the same premium rate . The general idea, expressed in our notation, is of a ‘safe-side’ premium and valuation basis ; a policy account based on a somewhat less conservative accumulation basis ; and the ‘true’ accumulation basis under which the asset share builds up.

There is, in addition, a valuation basis that we call , with policy values denoted by , defined by the ‘real’ technical basis , valuation premium rate and and terminal boundary condition . Note that this boundary condition is not a contractual benefit but a solution of Thiele’s equation under technical basis above. Such a possibility exists in the quasi-stochastic setup of traditional life insurance mathematics, in which all objects are conditional expectations with respect to ; it is not obvious that it exists in a model in which must be acknowledged to be only -measureable.

The undistributed reserve at time is defined by , it being supposed that has been distributed by time , for example by being allocated to a policy account, whether or not that fact has been disclosed. A key assumption is that (p.16), which simplifies the model greatly. Some consequences of this assumption are as follows.

-

(a)

It is then evident that for all .

- (b)

-

(c)

The second-order basis drops out of certain calculations involving total profit (“ further specification of the future second order basis is redundant”, p.17). In our terms, this is Corollary 3 (Section 5.4.3), the irrelevance of the valuation basis. It is stated that “ the condition is the same as performing the equivalence principle on the total payments under the real basis” (p.17).

-

(d)

For the purposes of demonstration only, suppose that interest is the only source of surplus. Then assuming , equation (2.15) of Møller & Steffensen (2007) reduces to:

(46) Ruling out other possibilities, either on , or must change sign at least once on . So the setup cannot simply be that second-order is a uniformly ‘weaker’ accumulation basis than third-order .

It is noted that when conditional expectations are encountered based on first-order and second-order , then “ since the intensity of in the conditional expectation is not , these quantities can only be said to build on suitable imitations of the principles”, (p.27) (compare with Section 5.5, which introduces the privileged position of technical basis and its intensities).

A final feature of the model is that, in the absence of a true terminal bonus system, for example as it is known in the UK, all bonus that will be distributed must be included in by the end of the term, which must be done by choosing the technical basis to hit the target . It is said that “The second order basis is a decision variable held by the insurer that is to be chosen within certain legislative constraints and market conditions” (p.13). So the actuary still faces the classical challenge of using only reversionary bonuses to hit an asset share target.

7 Conclusions

Almost all of the literature on Thiele’s equation and surplus in life insurance uses a model inspired by Scandinavian-style regulation with two technical bases, called first-order and second-order. This is more restrictive than practice in some jurisdictions, excludes common valuation methodologies, and uses terminology that may not be universally familiar. The literature emphasizes retrospective policy values, which are uniformly familiar but, arguably, obsolete.

Our setting is Markov models, defined in Section 3. Given a particular contract, we propose: (a) a definition of ‘technical basis’ that includes interest and transition intensities (expenses and anything else can be added if desired); (b) the ‘pure’ premium rate resulting if we plug technical basis into the principle of equivalence; and (c) for technical bases classified as valuation bases (see below) the ‘valuation’ premium rate .

We then classify technical bases based on the boundary conditions that are satisfied in Thiele’s equation (Section 4). A ‘valuation basis’ satisfies the terminal boundary conditions and defines policy values. An ‘accumulation basis’ satisfies the initial boundary condition (assuming everyone starts in state 1) and defines a policy account. We have no need of the traditional retrospective policy value.

We suppose there is a ‘true’ accumulation basis denoted by and called the experience basis, which has a privileged position. Its transition intensities define the counting process martingales (Equation (19)) and therefore expected values in the model.

Our canonical model is then defined by three technical bases: premium ; valuation and accumulation (not necessarily the same as ).

Each pair of technical bases in the model defines one of the relationships R1 to R3, set out in Section 1.1. Moreover, each relationship so defined is independent of the other, third, technical basis. This set of relationships is well-known in practice (for example, Fisher & Young (1965) cited in Section 1.1) but there seems to be no coherent account of them in the technical literature. We highlight three results.

-

(a)

(Corollary 1): Each contractual premium can be written as the sum of a pure risk premium and two loadings, one capitalized and taken into surplus at inception, and one taken into surplus only as premiums are paid.

-

(b)

(Corollary 2): We show that the EPV of total surplus, including initial surplus, is independent of the valuation basis, if the accumulation basis is equal to the ‘true’ basis .

-

(c)

We define the present value of emerging surplus on accumulation basis , denoted by and show how it is related to the present value of surplus defined by Ramlau-Hansen (1988b).

Finally, in the Appendix we discuss possible definitions of retrospective policy value in Markov models, and the usefulness of the concept. Equality of prospective and retrospective policy values under restricted conditions is a mathematical result in the spirit of a self-financing portfolio. We take the more practical requirement to be for a quantity that fairly represents the assets side of the balance sheet, as the prospective policy value does for the liability side, and our candidate is the accumulation fund or policy account.

Acknowledgements

This study is part of the research programme at the Research Centre for Longevity Risk — a joint initiative of NN Group and the University of Amsterdam, with additional funding from the Dutch Government’s Public Private Partnership programme. We are grateful to Prof Dr Marcus Christiansen for comments on a draft of this paper.

Competing Interests

None.

Appendix

Retrospective Policy Values

The main features of definitions of retrospective policy values in a multiple-state model suggested in the literature are as follows.

-

(a)

Hoem (1969) defined the retrospective policy value as the limit as of the equal share per survivor of the accumulated funds accrued by a cohort of identical policies; in other words a mathematically rigorous function of actual cashflows. For the simple alive/dead model this gave:

(47) where the ‘minus’ superscript denoted the retrospective policy value. For the general multiple-state model, Hoem defined shares in the collective fund, and chose parameters such that for equation (47) held, and for .

-

(b)

Hoem (1988) started with: “Our purpose is to define as a mathematical function for which for all in for as many as possible”. There were enough degrees of freedom to assume this equality to be true by fiat for , leading to equation (47) again as the only other constraint.

Hoem also proved conditions for a first-order technical basis (in state 1) to be on the safe-side of a second-order technical basis, along the lines of Lidstone’s theorem (Norberg 1985) but including intuitive conditions on retrospective policy values. He showed that:

(48) where ‘*’ denotes the second-order technical basis and the middle equality had previously been shown to hold if .

-

(c)

Ramlau-Hansen (1988a) defined first-order and second-order technical bases, with prospective policy values denoted by and respectively and said: “let and denote the retrospective premium reserves [policy values] derived from the two valuation bases.” Moreover, a condition was imposed (initial state strongly transient, meaning no return to state 1) to ensure that , and that satisfied Thiele’s equation (Ramlau-Hansen 1988a, (3.3)). However in the sequel (see Section 5.4.2) the only properties used were: (i) the parameters of the second-order technical basis (to define surplus); and (ii) the two properties of cited above. The retrospective first-order policy value, and prospective second-order policy value, were not used at all. All the results were obtained, in our terms, using a proper valuation basis and the accumulation basis .

-

(d)

Wolthuis & Hoem (1990) took Hoem’s retrospective policy values in (a) above, expressed in matrix form:

(49) and generalized it to the form:

(50) (where is the matrix of occupancy probabilities) also compliant with Thiele’s equations (without assuming that state 1 is strongly transient). However, no particular rationale was given, except perhaps additional flexibility.

-

(e)

Norberg (1991) introduced a very general concept of policy values based on a payment function , specifying the total payments in , and a discount function , both possibly stochastic. The policy values depended on the following decomposition of the value of based on payments up to and after time :

(51) Then, given a family of sigma-algebras , not necessarily a filtration, prospective and retrospective policy values were defined respectively as:

(52) If represents full information about the past then is just the value of actual known cashflows; otherwise a coarser represents some grouping of policies defined by missing information. The prospective policy value is conventional, and satisfies Thiele’s equation, but the retrospective policy value satisfies a different differential equation, generalizing the Kolmogorov forward equations (Norberg 1991, Section 5E). These definitions do not lend themselves to the development of surplus. For all these reasons, we do not pursue these policy values further.

- (f)

Attempts to define retrospective policy values via a relationship of equality with prospective policy values seem to add little to the analysis of surplus and the real dynamics of a life insurance fund. Rather, the need is for a quantity that fairly represents the retrospective view of the assets attributed or assigned to, or accrued by, a policy or state, just as the prospective policy value represents the need to assign capital to each policy or state. The one may be most influenced by accountancy rules, the other by insurance regulations. Equality of retrospective and prospective policy values, on the other hand, is a mathematical demonstration of circumstances under which, in expectation only, the assets acquired under the natural operation of the policies will exactly meet the requirement for capital — a ‘self-financing portfolio’ condition. This is certainly of interest, but we are content simply to compare unequal supply of and demand for capital. This calls for a model of retrospective accounting that is operationally realistic, rather than mathematically ideal, and our definitions of accumulation basis and policy account have that in mind.

References

- (1)

- Andersen et al. (1993) Andersen, P. K., Borgan, Ø., Gill, R. D. & Keiding, N. (1993), Statistical Models Based on Counting Processes, Springer, New York.

- Baxter & Rennie (1996) Baxter, M. & Rennie, A. (1996), Financial Calculus, Cambridge University Press, Cambridge.

- Bowers et al. (1997) Bowers, N., Gerber, H., Hickman, J., Jones, D. & Nesbitt, C. (1997), Actuarial Mathematics, 2nd edition, Society of Actuaries, Shaumburg IL.

- Cox & Storr-Best (1962) Cox, P. R. & Storr-Best, R. H. (1962), Surplus in British Life Assurance, Cambridge University Press, Cambridge.

- Dickson et al. (2020) Dickson, D. C. M., Hardy, M. R. & Waters, H. R. (2020), Actuarial Mathematics for Life Contingent Risks, International Series on Actuarial Science, third edn, Cambridge University Press.

- Fisher & Young (1965) Fisher, H. F. & Young, J. (1965), Actuarial Practice of Life Assurance, Institute of Actuaries and Faculty of Actuaries, London and Edinburgh.

- Fleming & Harrington (1991) Fleming, T. & Harrington, D. (1991), Counting Processes and Survival Analysis, John Wiley, New York.

- Gerber (1990) Gerber, H. U. (1990), Life Insurance Mathematics, Springer, Berlin and the Swiss Association of Actuaries, Zürich.

- Gram (1910) Gram, J. P. (1910), ‘Professor Thiele som aktuar’, Dansk Forsikringsårbog 1910 pp. 26–37.

- Haçarız et al. (2023) Haçarız, O., Kleinow, T. & Macdonald, A. S. (2023), ‘Lapse-supported life insurance and adverse selection’, Submitted .

- Hattendorff (1868) Hattendorff, K. (1868), ‘Das risico bei der lebensversicherung’, Masius’ Rundschau der Versicherungen 18, 169–183.

- Helwich (2007) Helwich, M. (2007), Durational Effects and Non-smooth Semi-Markov Models in Life Insurance, PhD thesis, Universität Rostock.

- Hoem (1969) Hoem, J. M. (1969), ‘Markov chain models in life insurance’, Blätter der Deutschen Gesellschaft für Versicherungsmathematik 9, 91–107.

- Hoem (1983) Hoem, J. M. (1983), ‘The reticent trio: Some little-known early discoveries in life insurance mathematics by L. H. F. Oppermann, T. N. Thiele and J. P. Gram’, International Statistical Review 51, 213–221.

- Hoem (1988) Hoem, J. M. (1988), ‘The versatility of the Markov chain as a tool in the mathematics of life insurance’, Transactions of the 23rd International Congress of Actuaries, Helsinki S, 177–202.

- Hoem & Aalen (1978) Hoem, J. M. & Aalen, O. O. (1978), ‘Actuarial values of payment streams’, Scandinavian Actuarial Journal 1978, 38–47.

- Jacobsen (2006) Jacobsen, M. (2006), Point Process Theory and Applications: Marked Point and Piecewise Deterministic Processes, Birkhäuser, Boston.

- Jetses & Christiansen (2022) Jetses, J. & Christiansen, M. C. (2022), ‘A general surplus decomposition principle in life insurance’, Scandinavian Actuarial Journal 2022, 901–925.

- Jørgensen (1913) Jørgensen, N. R. (1913), Grundzüge einer Theorie der Lebensversicherung, Gustav Fischer, Jena.

- Lidstone (1905) Lidstone, G. J. (1905), ‘Changes to pure premium policy-values consequent upon variations in the rate of interest or the rate of mortality, or upon the introduction of the rate of discontinuance (with discussion)’, Journal of the Institute of Actuaries 39, 209–252.

- Linnemann (1993) Linnemann, P. (1993), ‘On the application of Thiele’s differential equation in life insurance’, Insurance: Mathematics and Economics 13, 63–74.

- Linnemann (1994) Linnemann, P. (1994), ‘Bonus, salary increases and real value of pensions’, Scandinavian Actuarial Journal 1994, 99–118.

- Linnemann (1995) Linnemann, P. (1995), ‘Market based valuation of guaranteed benefits of participating life insurance contracts’, Unpublished manuscript .

- Linnemann (2003) Linnemann, P. (2003), ‘An actuarial analysis of participating life insurance’, Scandinavian Actuarial Journal 2003, 153–176.

- Linnemann (2004) Linnemann, P. (2004), ‘Valuation of participating life insurance liabilities’, Scandinavian Actuarial Journal 2004, 81–104.

- Milbrodt (1993) Milbrodt, H. (1993), ‘Some remarks on actuarial payment functions’, Insurance: Mathematics and Economics 12, 127–132.

- Milbrodt & Stracke (1997) Milbrodt, H. & Stracke, A. (1997), ‘Markov models and Thiele’s integral equations for the prospective reserve’, Insurance: Mathematics and Economics 19, 187–235.

- Møller & Steffensen (2007) Møller, T. & Steffensen, M. (2007), Market-valuation Methods in Life and Pension Insurance, Cambridge University Press, Cambridge.

- Norberg (1985) Norberg, R. (1985), ‘Lidstone in the continuous case’, Scandinavian Actuarial Journal 1985, 27–32.

- Norberg (1990) Norberg, R. (1990), ‘Payment measures, interest and discounting’, Scandinavian Actuarial Journal 1990, 14–33.

- Norberg (1991) Norberg, R. (1991), ‘Reserves in life and pension insurance’, Scandinavian Actuarial Journal 1991, 3–24.

- Norberg (1992) Norberg, R. (1992), ‘Hattendorff’s theorem and Thiele’s differential equation generalized’, Scandinavian Actuarial Journal 1992, 2–14.

- Norberg (1995) Norberg, R. (1995), ‘Differential equations for moments of present values in life insurance’, Insurance: Mathematics and Economics 17, 171–180.

- Norberg (1999) Norberg, R. (1999), ‘A theory of bonus in life insurance’, Finance and Stochastics 3, 373–390.

- Norberg (2004) Norberg, R. (2004), Thiele, Thorvald Nicolai (1838–1910), in B. Sundt & J. Teugels, eds, ‘Encyclopedia of Actuarial Science’, Vol. 3, John Wiley, pp. 1671–1672.

- Olivieri & Pitacco (2015) Olivieri, A. & Pitacco, E. (2015), Introduction to Insurance Mathematics: Technical and Financial Features (second edition, Springer, Heidelberg.

- Ramlau-Hansen (1988a) Ramlau-Hansen, H. (1988a), ‘The emergence of profit in life insurance’, Insurance: Mathematics and Economics 7, 225–236.

- Ramlau-Hansen (1988b) Ramlau-Hansen, H. (1988b), ‘Hattendorff’s theorem: A Markov chain and counting process approach’, Scandinavian Actuarial Journal 1988, 143–156.

- Ramlau-Hansen (1991) Ramlau-Hansen, H. (1991), ‘Distribution of surplus in life insurance’, ASTIN Bulletin 21, 57–71.

- Schilling et al. (2020) Schilling, K., Bauer, D., Christiansen, M. C. & Kling, A. (2020), ‘Decomposing dynamic risks into risk components’, Management Science 66, 5485–6064.

- Society of Actuaries (1987) Society of Actuaries (1987), ‘Risks of lapse-supported products’, Record of the Society of Actuaries 13, 2057–2102.

- Sverdrup (1965) Sverdrup, E. (1965), ‘Estimates and test procedures in connection with stochastic models for deaths, recoveries and transfers between states of health’, Skandinavisk Aktuaritidskrift 48, 184–211.

- Turnbull (2017) Turnbull, C. (2017), A History of British Actuarial Thought, Palgrave Macmillan, Cham, Switzerland.

- Width (1986) Width, E. (1986), ‘A note on bonus theory’, Scandinavian Actuarial Journal 1986, 121–126.

- Wolthuis (1987) Wolthuis, H. (1987), ‘Hattendorff’s theorem for a continuous-time Markov model’, Scandinavian Actuarial Journal 1987, 157–175.

- Wolthuis (1992) Wolthuis, H. (1992), ‘Prospective and retrospective premium reserves’, Blätter der Deutsche Gesellschaft für Versicheringsmathematik XX, 317–327.

- Wolthuis (1994) Wolthuis, H. (1994), ‘Actuarial equivalence’, Insurance: Mathematics and Economics 15, 163–179.

- Wolthuis & Hoek (1986) Wolthuis, H. & Hoek, I. V. (1986), ‘Stochastic models for life contingencies’, Insurance: Mathematics and Economics 5, 217–254.

- Wolthuis & Hoem (1990) Wolthuis, H. & Hoem, J. M. (1990), ‘The retrospective premium reserve’, Insurance: Mathematics and Economics 9, 229–234.