Inference for Rank-Rank Regressions

Abstract

Slope coefficients in rank-rank regressions are popular measures of intergenerational mobility, for instance in regressions of a child’s income rank on their parent’s income rank. In this paper, we first point out that commonly used variance estimators such as the homoskedastic or robust variance estimators do not consistently estimate the asymptotic variance of the OLS estimator in a rank-rank regression. We show that the probability limits of these estimators may be too large or too small depending on the shape of the copula of child and parent incomes. Second, we derive a general asymptotic theory for rank-rank regressions and provide a consistent estimator of the OLS estimator’s asymptotic variance. We then extend the asymptotic theory to other regressions involving ranks that have been used in empirical work. Finally, we apply our new inference methods to three empirical studies. We find that the confidence intervals based on estimators of the correct variance may sometimes be substantially shorter and sometimes substantially longer than those based on commonly used variance estimators. The differences in confidence intervals concern economically meaningful values of mobility and thus lead to different conclusions when comparing mobility in U.S. commuting zones with mobility in other countries.

1 Introduction

Regressions involving ranks are popular in empirical work in economics. A prominent example is a rank-rank regression for measuring the persistence in socioeconomic status across generations. Dahl and DeLeire (2008) and Chetty et al. (2014) have been influential in promoting this approach and a vast and fast-growing empirical literature is using such and related regressions for the study of intergenerational mobility in different socioeconomic outcomes, countries, regions, and time periods.111The recent surveys by Deutscher and Mazumder (2023) and Mogstad and Torsvik (2023) provide numerous examples and references. The resulting measures are important inputs to broader political and public debates about inequality, the importance of the family and the neighborhood into which children are born, and opportunities for children to grow out of poverty (Mogstad and Torsvik (2023)). Besides intergenerational mobility, regressions involving ranks have also been used in a range of other areas in economics such as education (e.g., Chetty et al. (2011), Murphy and Weinhardt (2020), Carneiro et al. (2023)), crime (e.g., Sharkey and Torrats-Espinosa (2017)), or migration (e.g., Ward (2022b)).

In its simplest form, a rank-rank regression in the intergenerational mobility literature consists of performing two steps: first, rank a child’s and their parent’s socioeconomic status (say, income) in their respective distributions and, second, run a regression of the child’s rank on a constant and the parent’s rank. The slope coefficient in this regression is then interpreted as a relative measure of intergenerational mobility. A small value of the slope indicates low dependence of the child’s position in their income distribution on the parent’s position in their income distribution, and thus high mobility.

In this paper, we develop an asymptotic theory for the OLS estimator of such rank-rank regressions and other regressions involving ranks. First, we demonstrate that the homoskedastic and Eicker-White variance estimators, which in empirical work involving rank-rank regressions are often employed to compute standard errors and confidence intervals, are not consistent in the context of rank-rank regressions. In fact, we show that the probability limits of these variance estimators may be too large or too small relative to the true asymptotic variance, depending on the shape of the copula of the two variables to be ranked. As a consequence, inference based on these commonly used variance estimators may be conservative or fail to satisfy coverage criteria.

Second, we derive the asymptotic distribution of the OLS estimator in a general rank-rank regression with covariates and without assumptions on whether the distributions of the dependent and independent variables are continuous or not. In the special case in which the distributions are continuous and there are no covariates, the OLS estimator is equal to Spearman’s rank correlation, and our limiting distribution coincides with that derived by Hoeffding (1948) for Spearman’s rank correlation. In the more general case in which at least one of the distributions is not continuous (e.g., because of zero incomes or top-coding) or covariates are present, the OLS estimator is not equal to Spearman’s rank correlation anymore and Hoeffding’s results do not apply. Importantly, in the case of non-continuous distributions, the estimand and the estimator’s asymptotic distribution are both sensitive to how ties are handled.

Third, we extend the asymptotic theory to other regressions involving ranks. For example, in the empirical literature studying intergenerational mobility, rank-rank regressions are sometimes run separately in different regions of a country, for instance in commuting zones within the U.S., but the ranks are computed in the national distribution rather than within the regions (e.g., as in Chetty et al. (2014), Acciari et al. (2022), Corak (2020)). This type of regression yields rank-rank slopes for each commuting zone with ranks defined on a common scale. We cover such clustered rank-rank regressions. Two further extensions treat the case in which the regression involves a general, non-ranked, outcome variable and a ranked regressor (e.g., as in Chetty et al. (2011), Murphy and Weinhardt (2020)) and the case in which the regression involves a ranked outcome and a general, non-ranked regressor (e.g., as in Sharkey and Torrats-Espinosa (2017)). For all these extensions, we derive the asymptotic distribution of the OLS estimator.

Fourth, for each of the regression models involving ranks, we propose a consistent estimator of the true asymptotic variance of the OLS estimator. Software implementations of these are provided in the R package csranks, which is available on CRAN. A Stata command is under development.

Finally, we discuss three empirical applications in which we compare inference methods based on our new variance estimators to those based on the commonly used variance estimators. In a simulation experiment calibrated to data analyzed by Chetty et al. (2014, 2018); Chetty and Hendren (2018), we study intergenerational mobility in commuting zones in the U.S.. We find that our (correct) standard errors may be substantially larger or smaller than those computed using the homoskedastic or Eicker-White variance estimators. For some of the commuting zones, the latter standard errors may be up to 60% too large or up to 20% too small. The differences in standard errors translate into economically meaningful differences in confidence intervals. For instance, we find that mobility in several commuting zones in California are significantly different from those in Italy and Canada according to our inference method. In contrast, the homoskedastic and Eicker-White variance estimators lead to confidence intervals that are conservative and include the mobility values of Italy and Canada. Similarly, there are commuting zones in California whose mobility is not significantly different from those in Norway and Canada according to our inference method, but the homoskedastic variance is too small and leads to confidence intervals that do not include Norway’s and Canada’s mobility values. Such comparisons of mobility across regions and countries are common in the literature. To avoid misled conclusions, it may therefore be important to conduct inference based on estimators of the correct variance.

We also apply our inference methods to Ward (2022a), who studies intergenerational mobility in terms of occupational status using PSID data. In this application, the confidence intervals based on our new variance estimators are similar to those based on commonly used variance estimators, except on a small subsample of parent-child cohort pairs in which the homoskedastic variance estimator leads to conservative inference.

In a re-analysis of Camerer et al. (2016), who study the replicability of lab experiments, we find large differences in our new confidence intervals compared to those based on commonly used variance estimators. For instance, confidence intervals based on the homoskedastic variance estimator may be up to about twice as large as our new confidence intervals. In one specification, the underlying regressor is a binary variable leading to a large number of ties. Depending on how these ties are handled, we find confidence intervals based on the homoskedastic or Eicker-White variance estimators to be substantially smaller or larger that the confidence intervals produced by our method.

Our theoretical results are relatively easy to derive. In fact, all of them follow from an application of the U-statistics theory, as originally developed in Hoeffding (1948) and comprehensively reviewed in Serfling (2002). Alternatively, given that our estimation problem is semiparametric, we could derive the same results using Newey (1994) and the empirical process theory. In addition, instead of letting the controls enter the rank-rank regression in a separately additive fashion, we could consider a more flexible specification, where the slope coefficient of the rank-rank regression depends on the controls nonparametrically. For such a model, we would be able to obtain the asymptotic distribution results using the theory of influence function adjustments, as developed in Chernozhukov et al. (2022), or other semiparametric techniques. However, we focus on the simple, linear rank regressions as they seem to be most relevant for empirical work.

Our paper contributes to the general literature on nonparametric rank statistics. Since the literature is large, we provide here only some key references, referring an interested reader, for example, to a recent review Chatterjee (2023). As mentioned above, Hoeffding (1948) derived the asymptotic distribution for Spearman’s rank correlation in the case of continuous distributions. Nes̆lehova (2007) obtained a meaningful extension of the same coefficient for a specific way of handling ranks to the non-continuous case, with the extension satisfying several intuitive axioms that any measure of concordance measure between random variables should satisfy. Mesfioui and Quessy (2010) extended the results of Nes̆lehova (2007) to cover the case of more than two variables. Genest et al. (2013) studied the problem of estimating Spearman’s rank correlation in the multivariate case with discontinuities. Ornstein and Lyhagen (2016) derived the asymptotic normality result and the asymptotic variance formula for the Spearman’s rank correlation for variables with finite support. We note here that these extensions are, although relevant, quite different from our work. In particular, we study the OLS estimator in a regression involving ranks, which coincides with the Spearman’s rank correlation only in the special case of the rank-rank regression when the marginal distributions are continuous and there are no covariates. Otherwise, our estimands and estimators differ from those in the papers listed here.

Our work is also related to Klein et al. (2020) and Mogstad et al. (2023), who also proposed inference methods involving ranks, but the key difference is that they focused on inference on ranks of population parameters whereas we consider inference on features of the distribution of ranked observations.

The paper is organized as follows. In the next section, we show that commonly used OLS variance estimators are not consistent in the context of rank-rank regressions. In Section 3, we derive a general asymptotic theory for rank-rank regressions. In Section 4, we provide three extensions, covering other regressions involving ranks which have been used in empirical work. In Section 5, we present three empirical applications. The appendix contains additional theoretical results and all proofs.

2 Motivation

In this section, we show that commonly used inference methods in rank-rank regressions are not valid, even in the simplest case when the underlying variables are continuously distributed and there are no covariates. In addition, we illustrate how the presence of pointmasses changes the inference problem.

2.1 Rank-Rank Regressions With Continuous Marginal Distributions

To motivate our analysis in this paper, consider a child’s income and their parent’s income . Suppose we are interested in measuring intergenerational mobility in these incomes by running a rank-rank regression of the child’s income rank on a constant and the parent’s income rank. The slope coefficient from this regression reflects the persistence of the two generations’ positions in their respective income distributions. A small value of the slope indicates low persistence and thus high mobility.

To simplify the discussion we start with the simplest possible rank-rank regression in which there are no covariates and the two income distributions are continuous. Let be the joint distribution of and let and be the corresponding marginals. Given an i.i.d. sample from , we run the rank-rank regression as follows. First, compute the child’s income rank and the parent’s income rank , where and denote the empirical cdfs of and . Then, run a regression of on a constant and . The OLS estimator of the slope parameter can then be written as the sample covariance of and divided by the sample variance of :

where and are sample averages of and , respectively. Inference is then performed by computing standard errors and confidence intervals based on the usual variance formulas for the OLS estimator. Popular choices in the intergenerational mobility literature are the homoskedastic and robust variance formulas,

where for all and . The estimator is sometimes used when regression errors are believed to be homoskedastic whereas is robust to heteroskedasticity and is often referred to as the Eicker-White estimator.

The OLS estimator is also often interpreted as Spearman’s rank correlation,

| (1) |

Indeed, given that the marginal distributions and are both assumed to be continuous, we have

| (2) |

with probability one.222To see this, note that by continuity of the distributions, with probability one there are no ties in the data and is just a reordering of . Thus, the OLS estimator of the rank-rank regression and Spearman’s rank correlation are numerically identical in finite samples. As a result, they must have the same asymptotic properties, which we now discuss.

First, it is well known that the probability limit of is

| (3) |

with denoting the copula of the pair . Second, Hoeffding (1948) showed that

where

| (4) |

and

| (5) | ||||

| (6) |

The main goal of this subsection is to point out that the OLS variance estimators and , which are commonly used in applied work, are not consistently estimating the true asymptotic variance . In consequence, inference based on these variance estimators may be misleading.

To show that the estimators and are not consistent for , we first derive probability limits for both estimators. To do so, define

The following lemma provides the probability limits.

Lemma 1.

Let be an i.i.d. sample from a distribution with continuous marginals. Then

| (7) |

and

| (8) |

The proof of this result, as well as of all other results presented in this paper, can be found in Appendix C.

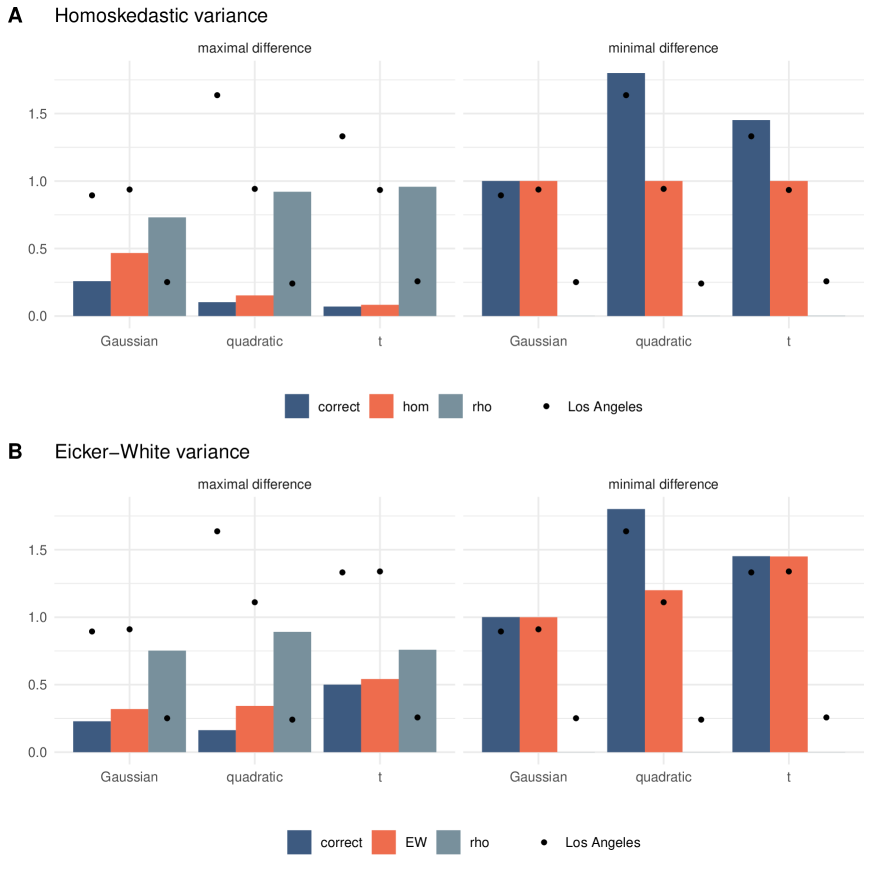

An important special case of this lemma occurs when and are independent, in which case and both probability limits are equal to the correct variance, . In general, however, the three variances are different. In fact, and can each be larger or smaller than the correct variance . Appendix A.1 shows that all three variances depend on the joint distribution only through its copula . Therefore, whether and by how much the variances are larger or smaller depends on the shape of the copula of child and parent incomes. To illustrate this point we compare the three variances in three simple parametric families of copulas.

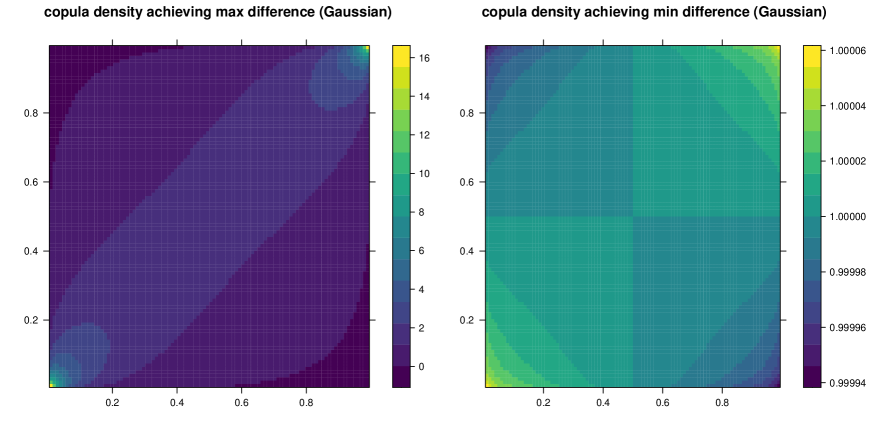

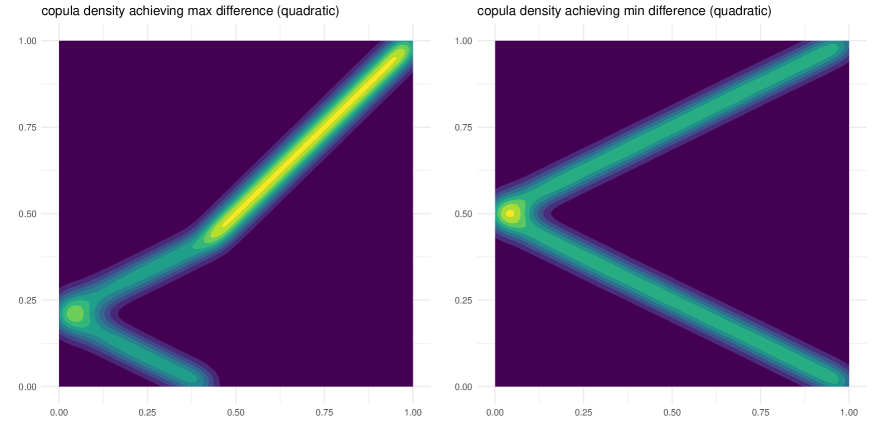

Specifically, we compute the minimal and maximal differences and over three families of copulas: the Gaussian, the Student-t (“t”), and a “quadratic” copula. In all cases, we optimize over the parameters of the copulas so as to find the largest and smallest difference in variances. Details of the specifications and solutions of the optimization problems can be found in Appendix A.2.

Panels A and B in Figure 1 show the variances achieving the minimal and maximal differences for the homoskedastic (“hom”) and the Eicker-White (“EW”) variances within the different families of copulas. They also display the rank correlation of the copulas that achieve the optima. The optimal copulas achieving these bounds are shown in Figures 14–16 in Appendix A.2. Within the t and the quadratic families, the correct variance may be substantially larger than the hom and EW variances, up to about 70% larger. Within the Gaussian family this is not possible, but the correct variance may be significantly smaller than the other two, almost half as large. Within the quadratic and the t families, the correct variance may also be smaller than the other two, but to a lesser extent than in the Gaussian family.

Interestingly, the minimal difference in variances is achieved for copulas that have rank correlation close to zero whereas the maximal differences occur for copulas with high rank correlation. To show that substantial differences in variances occur not only for very small or very large rank correlations, the graphs also indicate the value of the three different variances for the copula that matches the rank correlation of child and parent incomes in Los Angeles, one of the commuting zones that we further analyze in Section 5.1. In the data by Chetty et al. (2022a), Los Angeles has a rank correlation of . Since individual-level incomes are not publicly available, we do not know the true copula of incomes in Los Angeles. The dots in Figure 1 indicate the values of the correct, the hom, and the EW variances if the copula were Gaussian, t, or quadratic. If it were Gaussian, the hom and EW variances would be slightly larger than the correct one. If it were quadratic, however, the hom and EW variances would both be substantially smaller than the correct variance. Finally, in the t family, the hom variance would be substantially smaller than the correct variance, but the EW variance would be about the same as the correct one.

The variances , , and are all bounded, and so mutual differences between them are bounded as well. This is not true for ratios, however. The following lemma shows that if we do not restrict the distributions , the ratios and can both be arbitrarily large. To emphasize the dependence of the variances on the joint distribution of , we use the notation , , and .

Lemma 2.

There exists a sequence of distributions on with continuous marginals such that and as .

An implication of this lemma is that the two variances and can be larger than the correct variance by arbitrarily large factors. As the proof of the lemma reveals, the divergence occurs under sequences of copulas approaching perfect dependence so that both variances tend to zero, but the correct variance converges to zero at a faster rate than the variances and .333The copulas leading to large ratios of the variances are not the same as those leading to large differences between the variances. The large differences in Figure 1 are achieved when at least one of the variances is far from zero whereas large ratios are achieved when both are close to zero. This explains why larger ratios than those implied by Figure 1 are possible.

Given the result in Lemma 2, the next interesting question is how small the variances and can be relative to the true variance . The following lemma provides a partial answer to this question in the case of .

Lemma 3.

There exists a constant such that for all distributions on with continuous marginals.

By this lemma, the ratio is bounded away from zero, so that can be smaller than only by a factor that is bounded from below by the constant .444We do not know whether a version of Lemma 3 holds for the EW variance but we would be surprised if that were not the case. However, it is important to emphasize that this constant may be rather small. In particular, we have already seen in Figure 1 that for simple well-known classes of copulas, like the t copula, the hom variance may be substantially smaller than the correct variance. In the empirical applications of Section 5, we also find that the hom variance may be substantially smaller than the correct variance.

In conclusion, this subsection has shown that commonly used formulas for the estimation of asymptotic variances, and thus also for standard errors, do not yield the correct asymptotic variance of the OLS estimator in a rank-rank regression. In particular, the homoskedastic and the Eicker-White standard errors may be too small or too large depending on the shape of the copula of the income distribution. In consequence, confidence intervals may be too short or too wide, possibly leading to under-coverage or conservative inference.

2.2 Rank-Rank Regressions With Noncontinuous Marginal Distributions

The well-established asymptotic theory for Spearman’s rank correlation described in the previous subsection crucially depends on the assumption that both marginals of the distribution are continuous. In empirical applications of rank-rank regressions, however, pointmasses are common. For instance, incomes may be top-coded, there may be pointmasses at zero or negative incomes (e.g. as in Chetty and Hendren (2018)). In fact, one of the commonly cited (Deutscher and Mazumder (2023), Mogstad and Torsvik (2023)) advantages of studying the rank-rank relationship over other approaches such as estimating intergenerational elasticities is that the rank-based approach is applicable in the presence of zero incomes. In addition, income measurements may be rounded, or ranks may be computed from discrete measures other than income (e.g., occupational status as in Ward (2022a) or human capital as in de la Croix and Goni (2022)). In such cases, pointmasses in the income distribution create ties in the ranks and their presence changes inference in the rank-rank regression in at least three important ways: (i) the interpretation of the estimand in the rank-rank regression changes, (ii) the estimand changes with the way in which ties are handled, and (iii) the statistical properties of the OLS estimator change with the way ties are handled. We now illustrate each of these three points in more detail.

First, in the presence of pointmasses, the OLS estimator of the rank-rank regression is not equal to Spearman’s rank correlation and its probability limit cannot be interpreted as a rank correlation anymore. This is because the ratio of standard deviations in (2) is not necessarily equal to one. The OLS estimator therefore estimates a scaled version of the rank correlation, which may be scaled upwards or downwards depending on the relative location and magnitudes of pointmasses in the distributions of and . In particular, the slope coefficient of the rank-rank regression may lie outside of the interval and cannot be interpreted as a correlation. Researchers should therefore be careful about whether they want to estimate Spearman’s rank correlation or the rank-rank slope, and potentially adjust the rank-rank slope by the ratio of standard deviations.

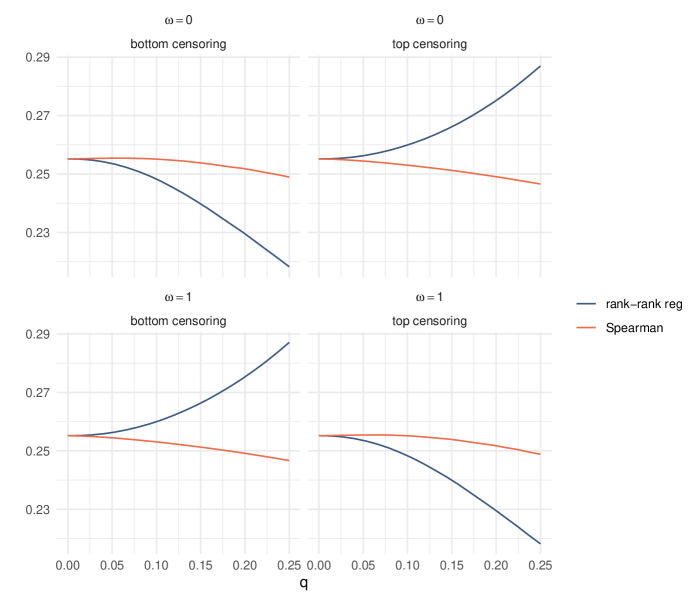

The first row of Figure 2 illustrates this point. It is based on the (continuous) joint distribution of child and parent incomes which we calibrated to data from Los Angeles (see Section 5.1). We introduce more and more zero (“bottom censoring”) or top-coded (“top censoring”) parental incomes into the distribution and then show how Spearman’s rank correlation (“Spearman”) and the rank-rank slope (“rank-rank reg”) change. The first graph (“bottom censoring”) shows the two estimands when all parental incomes up to the -th quantile are set to zero, while the second graph (“top censoring”) shows the same quantities when all parental incomes above the -th quantile are set equal to the income at that quantile. At there is no censoring and the joint distribution of incomes is continuous, so the rank correlation and rank-rank slope are equal. With more censoring (larger ), the joint distribution features larger pointmasses and the two estimands diverge. Without censoring, the rank-rank slope is equal to while with 25% top-censoring, the rank-rank slope takes a value of . Among the ranking of all 709 CZs that we analyze, this change in mobility corresponds to Los Angeles moving from 59th place to 134th place. This is a substantial change in mobility. Of course, 25% of the sample being censored is an extreme case, but we see significant sensitivity of the rank-rank slope with respect to even for smaller values. In addition, discreteness stemming from sources other than censoring may have similarly substantial impacts on the estimand.

While for top-censoring, the rank-rank slope increases with , for bottom-censoring it decreases with .

Second, in the presence of pointmasses in the distribution , different ways of handling ties in the ranks lead to different estimands (i.e., the rank-rank slopes).555Ranks are defined as in (9) below, where is a parameter governing how ties are handled. The second row in Figure 2 illustrates this point. It shows the same graphs as the first row, but for a different definition of the rank. The rank correlation is almost the same for the two definitions of the rank, but the rank-rank slope substantially changes. Handling ties differently () than in the first row of figures () means that Los Angeles’ mobility measure drops from without censoring to with 25% top-censoring. This change in mobility corresponds to Los Angeles moving from 59th place up to 20th place in the ranking of all 709 CZs.

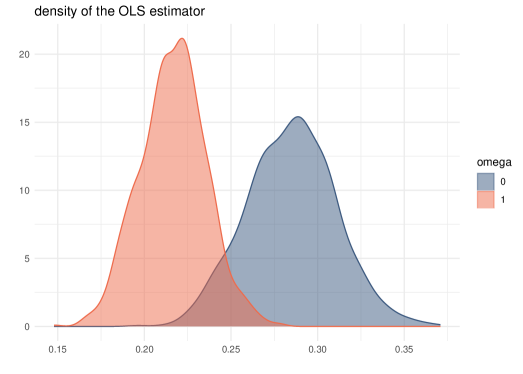

Third, the way in which ties are handled also impacts the statistical properties of the OLS estimator of the rank-rank slope. Figure 3 illustrates this point by showing the estimated distribution of the estimator for the two different definitions of the ranks for and . To create this graph, we simulated 10,000 samples of size 2,000 from the income distribution calibrated to data from Los Angeles with 25% top-coding and the Gaussian copula. In Figure 2, we have already seen how the estimand changes depending on whether or . In Figure 3, we see this reflected in the different means of the two distributions of the estimator. In addition, however, the variance of the two estimators is also different. If ties are handled by setting , the variance is larger compared to the estimator’s variance when .

2.3 Summary

The previous arguments can be summarized as follows:

-

1.

Hoeffding (1948)’s derivation of the asymptotic distribution of Spearman’s rank correlation yields the correct asymptotic distribution of the OLS estimator of the slope in a rank-rank regression in the special case with continuous marginal distributions of and and without covariates.

-

2.

Commonly used variance estimators for OLS regressions do not estimate this asymptotic variance. They may be too small or too large depending on the shape of the copula of the pair .

-

3.

When at least one of the two marginal distributions of and is not continuous or when there are covariates in the regression, then Hoeffding’s theory does not apply. Importantly, in the noncontinuous case, the rank-rank regression estimand, the OLS estimator, and its asymptotic distribution are all sensitive to the specific way in which ties are handled.

The next section develops a general, unifying asymptotic theory for coefficients in a rank-rank regression that allows for any definition of the rank, for continuous or noncontinuous distributions, and for the presence of covariates.

3 Inference for Rank-Rank Regressions

3.1 Asymptotic Normality Result

In this section, we develop the asymptotic theory for the OLS estimator of a rank-rank regression. The results apply to continuous and non-continuous distributions . To deal with potential ties, we consider a more general definition of the rank, in fact a class of ranks, indexed by a parameter . Different definitions of the rank differ in the way in which they handle ties, but they are all equivalent in the absence of ties.

For a fixed, user-specified , let , , and

For an i.i.d. sample from , we then define the rank of as , where

| (9) |

is an estimator of . This definition of the rank is such that an individual with a large value of is assigned a large rank. If is continuous, then the probability of a tie among is zero and the rank is the same for all values of . If is not continuous, then different choices of lead to definitions of the rank that handle ties differently. For instance, if then and tied individuals are assigned the largest possible rank. If , then is the mid-rank as defined in Hoeffding (1948), which assigns to tied individuals the average of the smallest and largest possible ranks. Finally, leads to a definition of the rank that assigns to tied individuals the smallest possible rank. Table 1 illustrates the different definitions of ranks in an example with ties. The quantities , , and their estimators are defined analogously for . We assume that is the same value in and , so that ranks are defined consistently for both variables and . Throughout the paper, this value of is fixed and chosen by the researcher, so it does not appear as argument or index anywhere.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 3 | 4 | 7 | 7 | 10 | 11 | 15 | 15 | 15 | 15 | |

| smallest rank: for | 0.1 | 0.2 | 0.3 | 0.3 | 0.5 | 0.6 | 0.7 | 0.7 | 0.7 | 0.7 |

| mid-rank: for | 0.1 | 0.2 | 0.35 | 0.35 | 0.5 | 0.6 | 0.85 | 0.85 | 0.85 | 0.85 |

| largest rank: for | 0.1 | 0.2 | 0.4 | 0.4 | 0.5 | 0.6 | 1 | 1 | 1 | 1 |

We consider the following regression model:

| (10) |

where is a -dimensional vector of covariates, is noise, and , are regression coefficients to be estimated. As already indicated in Section 2.2, the interpretation of depends on whether the marginal distributions of and are continuous and, if at least one of them is not, how ties are handled. However, in the model (10) there is one additional reason complicating the interpretation of , namely the presence of covariates: even if and have continuous marginal distributions, in the presence of covariates that are correlated with , cannot be interpreted as a rank correlation and, in particular, does not have to lie in the interval .666This can be seen by writing as the covariance of residuals from partialling out from the two ranks divided by the variance of one of the two residuals. Then, this ratio is not equal to the correlation of the ranks after partialling out because the standard deviations of the two residuals are not necessarily equal.

Letting be an i.i.d. sample from the distribution of the triplet , we study the properties of the following OLS estimator of the vector of parameters :

| (11) |

To derive the asymptotic normality of , we introduce the projection of onto the covariates:

| (12) |

where is a random variable representing the projection residual, and is a vector of parameters. Consider the following regularity conditions:

Assumption 1.

is an i.i.d. sample from the distribution of .

Assumption 2.

The vector satisfies and the matrix is non-singular.

Assumption 3.

The random variable is such that .

These are standard regularity conditions underlying typical regression analysis. Assumption 3 requires that the rank can not be represented as a linear combination of covariates. Importantly, our regularity conditions do not require and to be continuously distributed.

Under these conditions, we have the following asymptotic normality result.

Theorem 1.

As already mentioned above, the proof of this result, as well as of all other results presented in this paper, can be found in Appendix C. In fact, Theorem 1 follows from a more general result, which we state in Appendix B (Theorem 5). The more general result shows joint asymptotic normality for and ,

and provides an explicit formula for . The joint asymptotic distribution for and is useful for empirical work in the intergenerational mobility literature. Suppose there are no covariates so only contains a constant. Besides the rank-rank slope, another popular measure of intergenerational mobility (Deutscher and Mazumder (2023)) is the expected income rank of a child given that their parent’s income rank is equal to some given value :

With the asymptotic joint distribution above, it is straightforward to compute standard errors and confidence intervals for .

Theorem 1 has the following interpretation. If we knew the population ranks and , we would simply estimate and by an OLS regression of on and . The asymptotic variance of such an estimator for would be given by , which is the familiar OLS variance formula. Without knowing the population ranks, however, we have to plugin their estimators, and the extra terms in the asymptotic variance, represented by and , provide the adjustments necessary to take into account the noise coming from estimated ranks. Importantly, the estimation error in the ranks is of the same order of magnitude as that in the OLS estimator with known ranks. Therefore, the estimation error in the ranks does not become negligible in large samples, not even in the limit as the sample size grows to infinity.

The derivation of the asymptotic normality result uses standard techniques from the U-statistic theory. To see this consider the case without covariates so that only contains a constant. Then, the OLS estimator of the slope can be written as

It is easy to show that the denominator converges in probability to . The numerator is a U-statistic because it is an average of terms involving and , which themselves are sample averages. Under the above assumptions one can then verify the standard conditions for such a U-statistic to be asymptotically normal (e.g., Serfling (2002)).

Remark (Comparing the variance formulas in (4) and (13)).

When both and are continuous random variables and contains only a constant, the asymptotic variance formula in (13) reduces to the classical Hoeffding variance formula in (4). Indeed, replacing and by and respectively, we can assume without loss of generality that both and are random variables, in which case in (5) reduces to

Similarly, in (6) reduces to . Hence, the variance in (4) simplifies to , where

| (14) |

and it is straightforward to verify that coincides with up to an additive constant whenever and contains only a constant.

Remark (Asymptotic variance in the non-continuous case).

The asymptotic normality result in Theorem 1 holds for both continuous and noncontinuous distributions of and . In the presence of pointmasses in at least one of the distributions of and , although implicitly, the asymptotic variance of the OLS estimator derived in Theorem 1 depends on . Therefore, different ways of handling ties through different choices of may affect not only the estimand and the estimator, but also the value of the asymptotic variance, as we have already seen in the discussion of Figure 3.

3.2 Consistent Estimation of the Asymptotic Variance

In this subsection, we propose an estimator of the asymptotic variance appearing in the asymptotic normality result in Theorem 1 and show that it is consistent. In particular, we consider the following plug-in estimator:

where is an empirical analog of , , and

for all . The following lemma shows that this simple plug-in estimator is consistent without any additional assumptions.

Theorem 1 and Lemma 4 give the correct way to perform inference in rank-rank regressions. For example, a asymptotic confidence interval for can be constructed using the standard formula

where is the number such that . Standard hypothesis testing can be performed analogously.

Remark (Bootstrapping the distribution of ).

In addition, to performing inference on via a consistent estimator of the asymptotic variance in Lemma 4, one can also perform inference by bootstrapping the distribution of . Indeed, to show bootstrap validity, observe that is a smooth functional (Hadamard differentiable), and our estimator takes the plug-in form, . Therefore, given that the empirical distribution function satisfies Donsker’s theorem, it follows from Theorem 3.1 in Fang and Santos (2019) that the distribution of , where is the estimator obtained on a bootstrap sample, consistently estimates that of ; see also Bickel and Freedman (1981) for the original result on bootstrapping von Mises functionals.

4 Inference for Other Regressions Involving Ranks

Motivated by regressions that have been used in empirical work, especially in the intergenerational mobility literature, we provide three extensions of the asymptotic normality result in Theorem 1. In particular, we consider (i) a rank-rank regression with clusters, where ranks are computed in the national distributions rather than in the cluster-specific distributions, (ii) a regression of a general outcome on the rank , and (iii) a regression of the rank on a covariate . For brevity of the paper, we keep the discussions of each extension relatively short.

4.1 Rank-Rank Regressions With Clusters

In this subsection, we consider a population (e.g., the U.S.) that is divided into subpopulations or “clusters” (e.g., commuting zones). We are interested in running rank-rank regressions separately within each cluster. The ranks, however, are computed from the distribution of the entire population (e.g., the U.S.). Such regressions have become particularly popular since the influential work by Chetty et al. (2014) for studying regional mobility, where the scale of the mobility measure is fixed by the national distribution. The survey by Deutscher and Mazumder (2023) provides more examples of empirical work running such regressions, for instance Corak (2020) and Acciari et al. (2022).

Specifically, we consider the model

| (15) |

where is an observed random variable taking values in to indicate the cluster to which an individual belongs. The quadruple has distribution , and we continue to denote marginal distributions of and by and . The quantities , , , and are also as previously defined, so that , for instance, is the rank of in the entire population, not the rank within a cluster. So, in the model (15), the coefficients and are cluster-specific, but the ranks and are not. In consequence, cannot be interpreted as the rank correlation within the cluster . Instead, in the intergenerational mobility literature, the rank-rank slope is interpreted as a relative measure of mobility in a region , where its scale is fixed by the national population. Unlike the rank-rank slope in the model without clusters, (10), the slopes do not only depend on the copula of and in a cluster, but also on the marginal distributions of and in the cluster. To see this note that adding a fixed amount to every child and parent income in a cluster does not change the ranking of children and parents within the cluster, but it may change the ranking of these individuals in their national income distributions. In conclusion, the may then also change.

We now introduce a first-stage projection equation similar to the one in (12), except that the coefficients are cluster-specific:

| (16) |

Let be an i.i.d. sample from the distribution of . Ranks are computed using all observations, i.e. with as in (9) and () the (left-limit of the) empirical cdf of . The computation of the rank is analogous.

First, notice that an OLS regression of on all regressors, i.e. and , produces estimates of that can be written as:

| (17) |

Therefore, can be computed by an OLS regression of on and using only observations from cluster . Similarly, can be computed by an OLS regression of on using only observations from cluster . Note however, as explained above, that the ranks and are computed using observations of and from all clusters and thus the OLS estimators across clusters are not independent.

Assumption 4.

is a random sample from the distribution of .

Assumption 5.

The vector is such that and, for all , the matrix is non-singular.

Assumption 6.

The random variable is such that for all .

As in the previous section, note that our assumptions do not require the marginal distributions and to be continuous. In addition, we introduce an assumption about the number and size of the clusters:

Assumption 7.

The number of clusters is a finite constant and for all .

Observe that if the number of clusters were to increase together with the sample size , with the number of units within each cluster being of the same order, the extra noise coming from estimated ranks would be asymptotically negligible, and the standard OLS variance formula would be applicable. The new result below applies to the case with a fixed number of clusters so that the estimation error in the ranks is not negligible even in large samples. This scenario seems reasonable, for instance, in our empirical application in which a cluster is a commuting zone within a U.S. state because each of these states contains only a small number of commuting zones relative to the sample size.

Under these four assumptions, we have the following extension of Theorem 1.

Theorem 2.

In Appendix B, we provide a joint asymptotic normality result for all regression coefficients. Letting , , , and , the appendix shows that

| (18) |

and provides an explicit formula for . From this result, one can then easily calculate the asymptotic distribution of linear combinations of parameters. For instance, similarly as in the rank-rank regression without clusters, a popular measure of intergenerational mobility (Deutscher and Mazumder (2023)) is the expected rank of a child with parents at a given income rank ,

| (19) |

The asymptotic distribution in (18) allows us to construct a confidence interval for for a specific commuting zone or simultaneous confidence sets across all commuting zones.

An estimator of the asymptotic variance is

where

for all and . One can prove consistency of this estimator using the same arguments as those in the proof of Lemma 4.

4.2 Regression of a General Outcome on a Rank

In this subsection, we consider a regression model with a general outcome as the dependent variable and a rank as the regressor:

| (20) |

Such a regression has been used, for instance, by Chetty et al. (2014) to study the association of child outcomes like college attendance or teenage pregnancy with the parent’s income rank. Another example is Chetty et al. (2011) in which wages are regressed on the rank of a test score.

For the above regression, the OLS estimator takes the form

| (21) |

The following theorem derives asymptotic normality for .

Theorem 3.

4.3 Regression of a Rank on a General Regressor

In this subsection, we consider a regression model with the rank as a dependent variable and a general regressor:

| (22) |

where, for brevity of notations, we let the vector to absorb the regressor . An example of such a regression in applied work is Sharkey and Torrats-Espinosa (2017) who regress the income rank on the crime rate.

Denote by the -th element of and by the vector of all elements of except the -th. The projection of onto for any now takes the following form:

| (23) |

where are -dimensional vectors of parameters. For this model, the OLS estimator takes the following form:

| (24) |

We then have the following result.

Theorem 4.

The theorem shows, in particular, that for the -th element of , we have

where

and, like above, a consistent estimator of the asymptotic variance can be obtained by the plugin method, analogously to our discussion in Section 3.

5 Empirical Applications

We illustrate our new inference methods through three empirical applications: (i) estimating intergenerational income mobility for neighborhoods in the U.S., (ii) estimating intergenerational mobility in terms of occupational status, and (iii) studying the determinants of replicability of laboratory experiments.

5.1 Intergenerational Mobility in the U.S. – Income

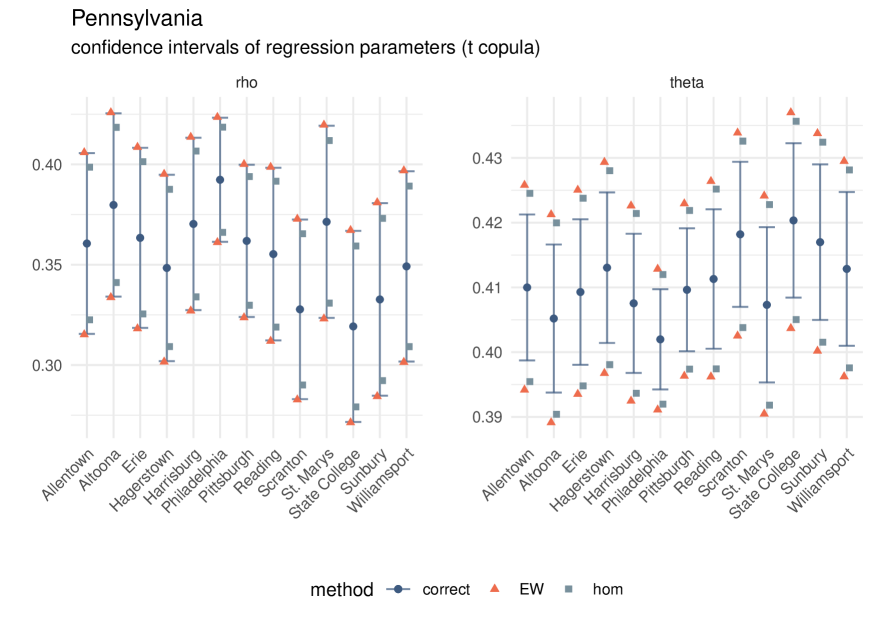

In this section, we apply our new inference methods to the analysis of intergenerational mobility in U.S. commuting zones (CZs) as in Chetty et al. (2014, 2018); Chetty and Hendren (2018). Since the micro-data are not publicly available, we design a simulation experiment calibrated to the available information about commuting zones’ income distributions.

Suppose we are interested in learning about mobility in CZs of California. A local politician in a given CZ of the state may be interested in estimating mobility in their own CZ. In that case, she might run a rank-rank regression as in (10) using only data from that particular CZ. Importantly, ranks for children and parents are therefore computed in their respective distributions within that CZ. Second, a state-level politician may want to learn about mobility in all CZs of their state and perhaps compare mobility across CZs. In that case, she might want to run a rank-rank regression with clusters as in (15), where ranks are computed in the distribution of the whole state.

We apply our new inference methods to both types of regressions on simulated data, where the data-generating process has been calibrated to information from the CZs in California, and compare the results to methods using the homoskedastic and Eicker-White variance estimators. Subsequently, we show that the results from California are not special in the sense that similar results are found in other U.S. states.

In both types of regressions, the CZ-specific regressions of the form (10) and the regression with clusters as in (15), contains only a constant. Both regressions produce rank-rank slopes for each CZ . In addition, we compute the expected income rank of a child with parents at the -th rank, as defined in (19).

Data.

From Chetty et al. (2022b), we obtain information about the CZ-specific marginal income distributions for 709 CZs.777The information on the marginal income distributions is missing for some CZs, so we do not analyze all 741 CZs contained in the dataset by Chetty et al. (2022a). Specifically, we obtain the CZ-specific mean and median for 2011-12 for child family income of children in the 1980-82 birth cohorts and the CZ-specific mean and median for 1996-2000 for the parent family income. In addition, we obtain CZ population sizes from the 2000 census. From Chetty et al. (2022a), we obtain estimates of for two values and for each CZ together with their standard errors.

Calibration.

First, we calibrate a CZ-specific copula for children’s and parents’ income. To this end, for each CZ , we use the two estimates of for and to solve for the implied estimate of the rank-rank slope . We then consider two copula families, the normal and the t copulas. For each family we find the copula that matches the observed rank correlation .

Second, we calibrate CZ-specific marginal distributions for children’s and parents’ income. For each CZ we fit a log-normal distribution that matches the observed CZ-specific mean and median incomes for children. Similarly, we fit a log-normal distribution that matches the observed CZ-specific mean and median incomes for parents.

Finally, we calibrate CZ-specific sample sizes proportional to the observed CZ population sizes.888We define a minimum () and maximum () sample size. Among all CZs in the U.S., the one with the smallest (largest) populations size is assigned (). All other CZs are assigned a sample size between these two, proportional to their population size.

Simulation Exercise.

We draw Monte Carlo samples for each CZ. On each Monte Carlo sample, we estimate the two parameters of interest, and . For each, we compute three types of standard errors: the correct standard errors from Theorem 5 or Theorem 6, respectively, the OLS standard error assuming homoskedasticity of the regression errors (“hom”), and the Eicker-White (“EW”) standard error. In the rank-rank regression with clusters, the hom and EW standard errors for , are computed based on the residuals from CZ .999An alternative approach would be to pool the residuals from all CZs to estimate the residual variance, similar to the regression in (15). The results from this approach are similar to those without pooling residuals and are not shown here. Ranks are defined as in (9) with .

Results.

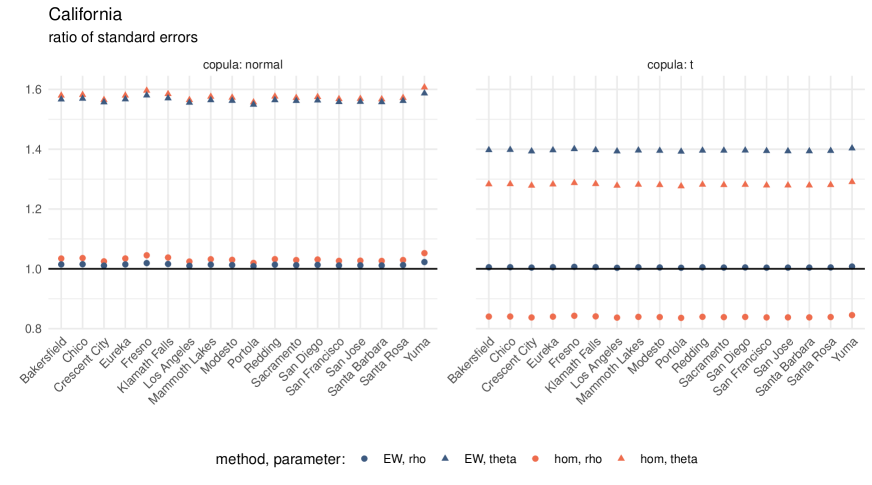

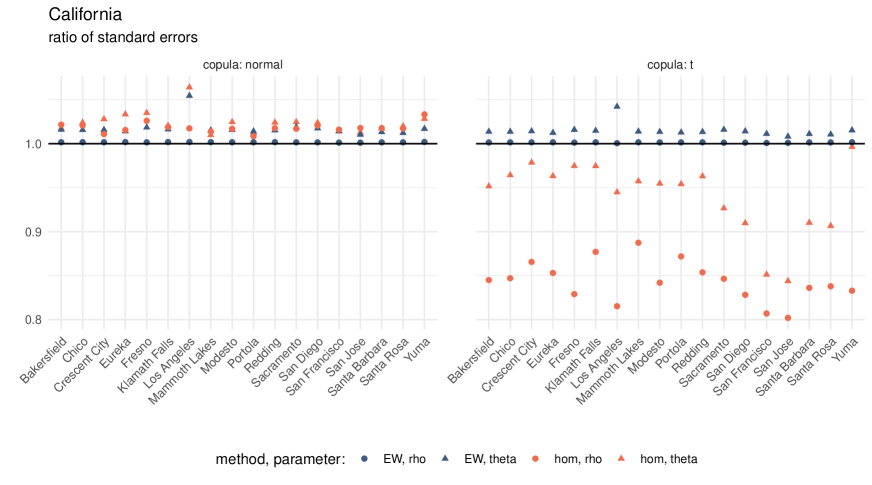

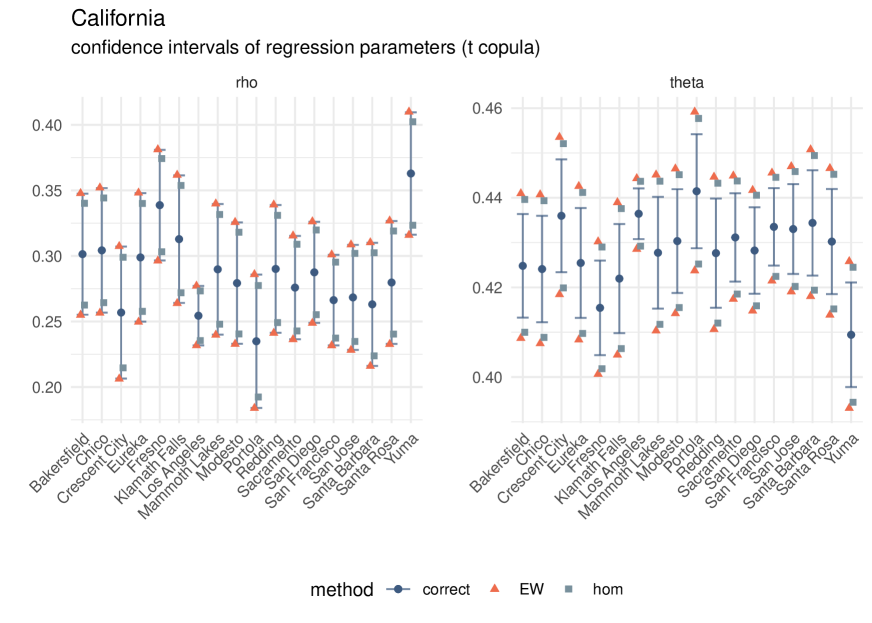

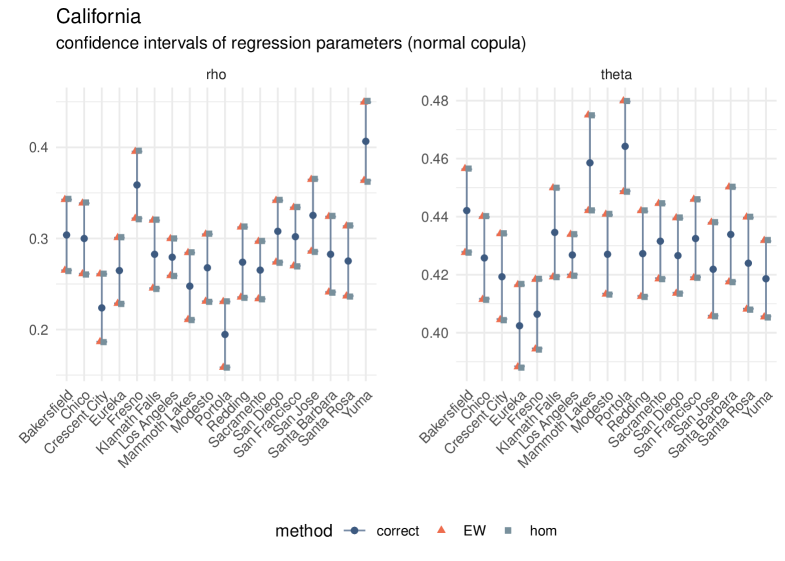

Figures 4 and 5 show the ratios of the hom and EW standard errors divided by the correct standard error. A ratio above (below) one means that the hom or EW standard error is larger (smaller) than the correct one.

For the normal copula, the hom and EW standard errors are larger than the correct one in all CZs. In the separate rank-rank regressions, for the rank-rank slope , the ratio of standard errors is close to one, but for the expected income rank , the ratios are close to 1.6, i.e. the hom and EW standard errors are about 60% too large. For the rank-rank regression with clusters, the ratios are all fairly close to one except for in Los Angeles, where the hom and EW standard errors are slightly over 5% too large.

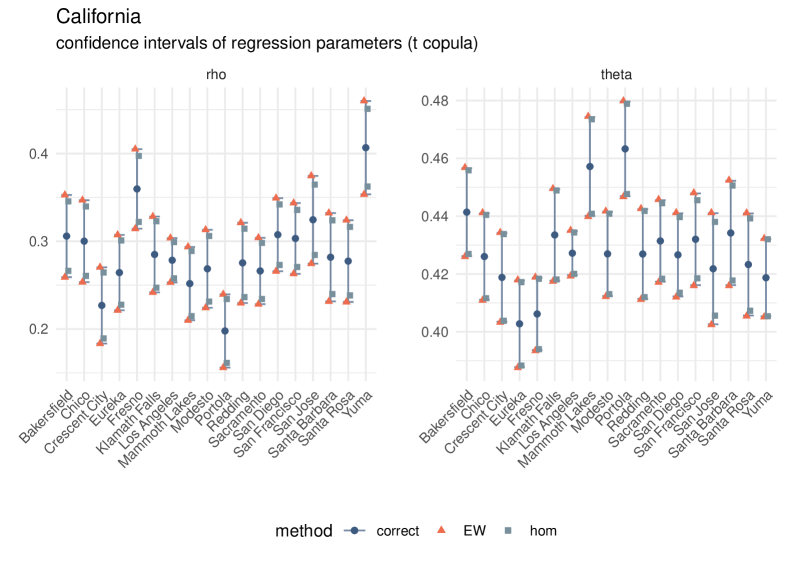

For the t copula, on the other hand, the hom standard error for the rank-rank slope may be substantially (around 20%) smaller than the correct one. The hom standard error for the expected income rank may be around 30% too large in the separate rank-rank regressions, but up to 10% too small in the rank-rank regressions with clusters. The EW standard error may also be substantially too large (about 40% too large in the separate regressions), but is never too small.

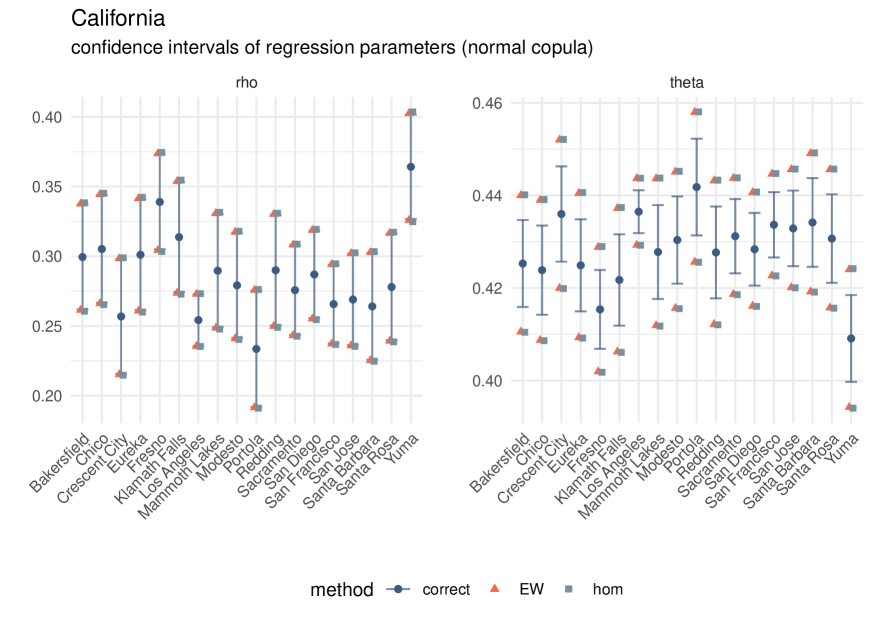

The differences in standard errors translate into differences in confidence intervals. Figures 6 and 7 show 95% marginal confidence intervals for the mobility estimates based on the normal and the t copulas. Figures 17 and 18 in the Appendix show the corresponding figures for the rank-rank regression with clusters.

For the normal copula, confidence intervals for the rank-rank slope are similar across the three methods. For the expected income rank, however, the confidence intervals based on hom and EW variance estimators are substantially longer than those based on the correct variance estimator, and thus lead to conservative inference. The difference in length of the hom and EW compared to the correct confidence intervals is economically meaningful in the sense that the hom and EW confidence intervals include meaningful values of mobility that the correct intervals exclude. For instance, the hom and EW confidence intervals for Modesto, San Jose, Santa Rosa, and Santa Barbara all include Italy’s (Acciari et al. (2022) report a value of 0.445) and Canada’s (Corak (2020) reports a value of 0.444) values of mobility, but the correct intervals are shorter and exclude Italy’s and Canada’s values. Similarly, Cresent City’s hom and EW confidence intervals include Australia’s value of mobility (Deutscher and Mazumder (2023) report a value of 0.45), but the correct interval is shorter and does not include Australia’s value.

For the t copula, the hom confidence intervals for the rank-rank slope are too small while the EW confidence intervals are almost identical to the correct ones. The difference in length of the hom and the correct confidence intervals is economically meaningful in the sense that the hom confidence intervals exclude meaningful values of mobility that the correct intervals include. For instance, the hom confidence intervals for Redding and Mammoth Lakes imply that mobility in these two CZs is significantly different from that in Germany (Bratberg et al. (2017) report a rank-rank slope of 0.245) and Canada (Corak (2020) report a rank-rank slope of 0.242) while the correct confidence intervals are longer and include Germany’s and Canada’s values of mobility. Similarly, Santa Barbara’s hom confidence interval implies that mobility in this CZ is significantly different from that in Norway (Bratberg et al. (2017) report a rank-rank slope of 0.223) and Italy (Acciari et al. (2022) report a rank-rank slope of 0.220), but the correct confidence interval includes Norway’s and Italy’s values of mobility.

Comparisons of mobility across countries are common in the literature (Deutscher and Mazumder (2023)) and the above discussion shows that our new confidence intervals may lead to different conclusions than those based on commonly used variance estimators.

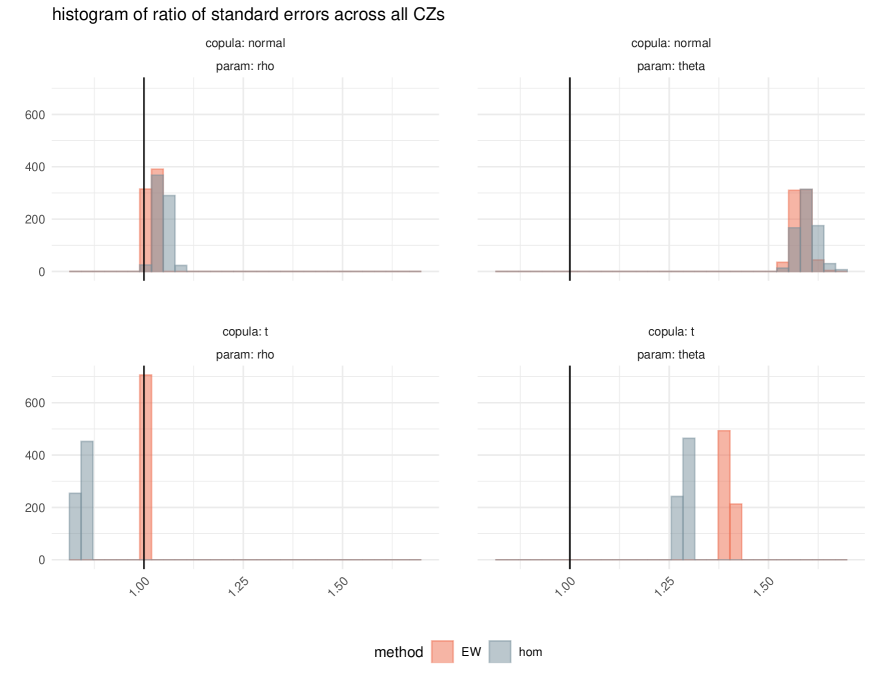

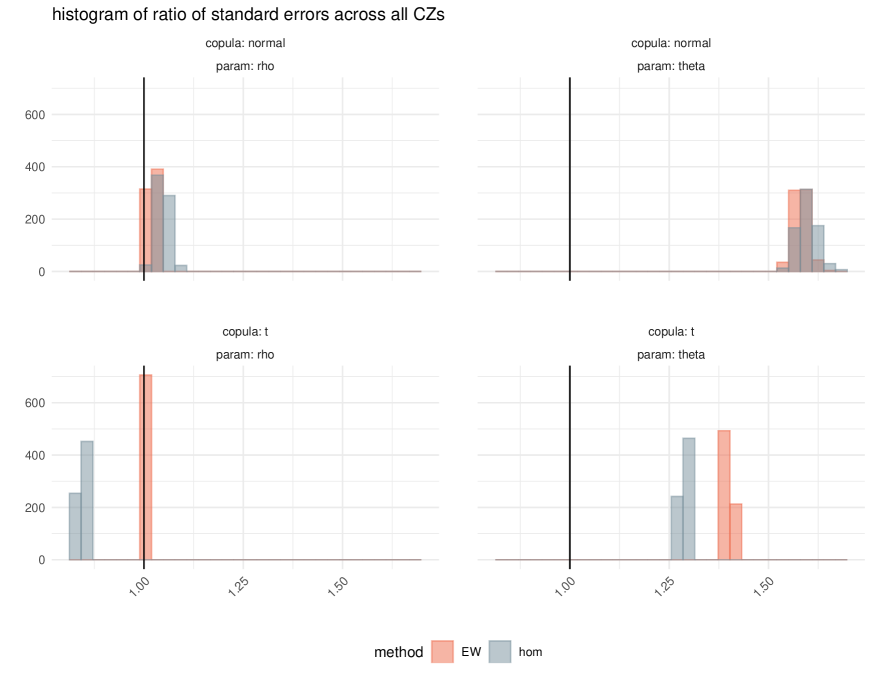

We now turn to the set of all 709 CZs. For the separate rank-rank regressions, Figure 8 shows the histogram of ratios of standard errors across all CZs. Figure 19 in the Appendix shows the corresponding figure for the rank-rank regression with clusters. Both figures illustrate that the results for California are not special. In particular, as in California, most ratios for the normal copula and the expected income rank parameter take values around 1.6, so that most hom and EW standard errors are about 60% too large. Similarly, as in California, most hom standard errors for the t copula and the rank-rank slope are about 20% too small.

5.2 Intergenerational Mobility in the U.S. – Occupational Status

In this section, we analyze intergenerational mobility in the U.S. as in Song et al. (2020) and Ward (2022a), who measure mobility by the rank-rank relationship between fathers’ and sons’ occupational status. We focus on cohorts covered by the PSID dataset used in Ward (2022a).

Data.

We use the PSID dataset from Ward (2022a), including his construction of the Song score (not his “adjusted” Song score), the measure of occupational status.

Econometric Specification.

Our analysis deviates somewhat from that of Ward (2022a). To obtain a rank-rank regression model as in (10), we modify Ward’s regression in three ways. First, we run a rank-rank regression separately for each subpopulation of father-son pairs within which he computes ranks, i.e. within father-son birth cohort combinations. We remove father-son cohorts with fewer than 20 observations. Second, we do not use sample weights. Third, we do not average ranks over time. These three modifications to Ward (2022a)’s regression specification allow us to interpret the regression slopes as rank-rank regression slopes and the model fits into (10).101010Since the occupational status measure is a discrete random variable, the rank-rank slope we estimate is not a rank correlation (see Section 2.2). We estimate the rank-rank regression with and without the covariates used by Ward (2022a). Ranks are defined as in (9) with .

Results.

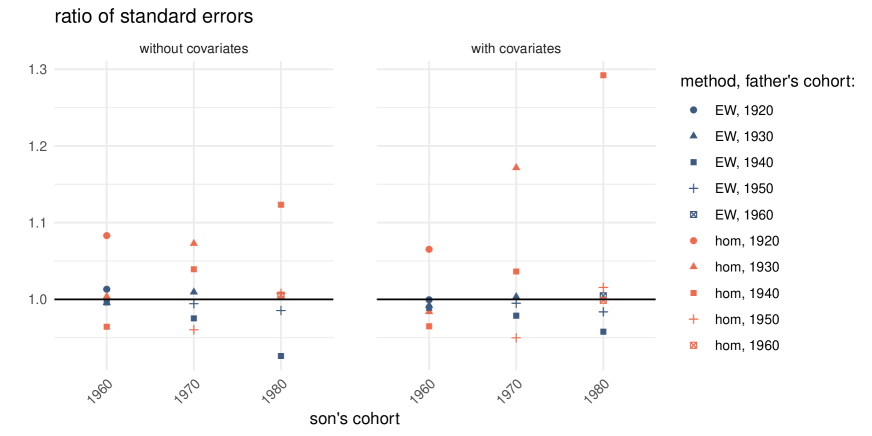

For the different father-son cohorts, Figure 9 shows the ratios of the hom and EW standard errors divided by the correct standard error. A ratio above (below) one means that the hom or EW standard error is larger (smaller) than the correct one. The left (right) panel reports ratios for the rank-rank regression without (with) covariates.

Some of the hom and EW standard errors are too small relative to the correct one, many are close to the correct one, but a few are substantially larger than the correct one. For instance, for the 1940-1980 father-son cohort, the hom standard error is up to 30% larger than the correct one.

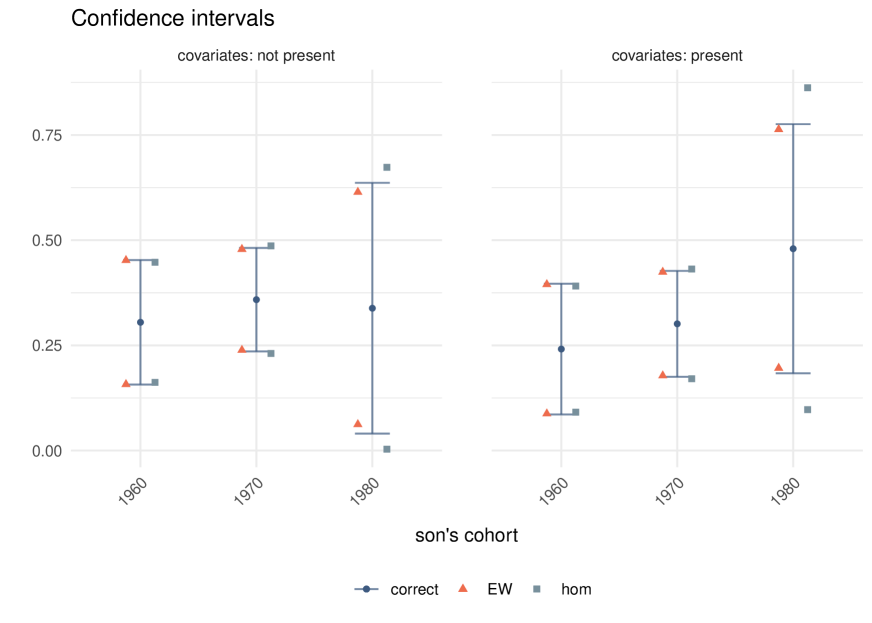

The differences in standard errors translate into differences in confidence intervals for the rank-rank slope. Figure 10 shows 95% marginal confidence intervals for the rank-rank slope. Most hom and EW confidence intervals are similar to the correct confidence interval, but for the son’s cohort of 1980 we see some differences: the hom confidence sets are longer than the correct ones and lead to somewhat conservative inference.

5.3 Replication of Laboratory Experiments in Economics

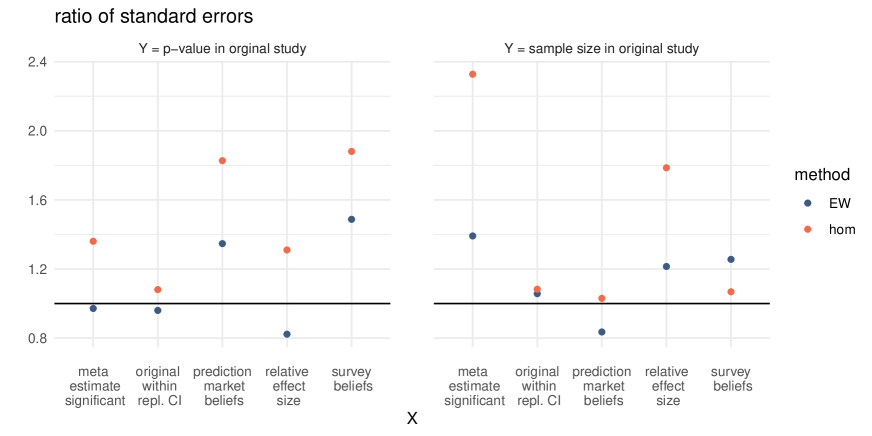

In this section, we reanalyze Camerer et al. (2016) who replicated 18 laboratory experiments published in the American Economic Review and the Quarterly Journal of Economics between 2011 and 2014. Among other aspects the authors investigate how sample size and p-value in the original study relate to measures of replicability of the study. They report Spearman’s rank correlations together with indicators of these correlation’s significance (see their Figure 3).

Data.

We use the original dataset made available through the Experimental Economics Replication Project Forsell et al. (2016).

Econometric Specification.

We estimate rank-rank regressions as in (10), where only contains a constant. As in Camerer et al. (2016), we consider two different variables to play the role of in the rank-rank regression: the sample size or the p-value in the original sample. Similarly, different variables are considered for : five different measures of replicability of the study. For more information on these variables, see Camerer et al. (2016). Ranks are defined as in (9) with .

Results.

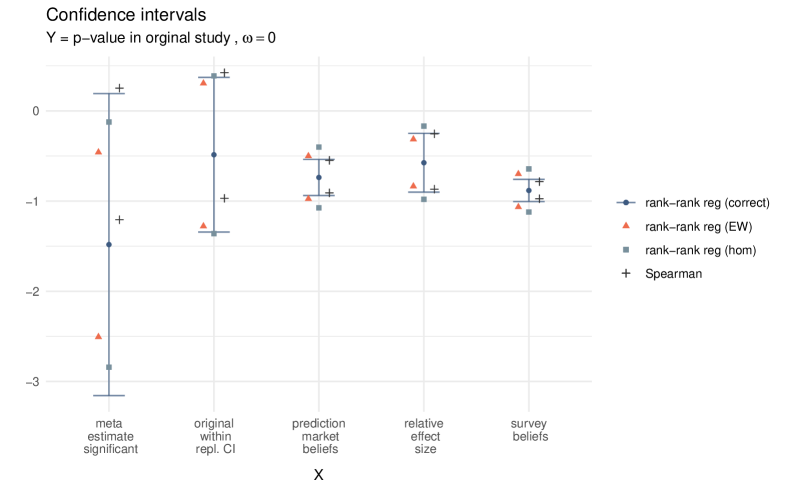

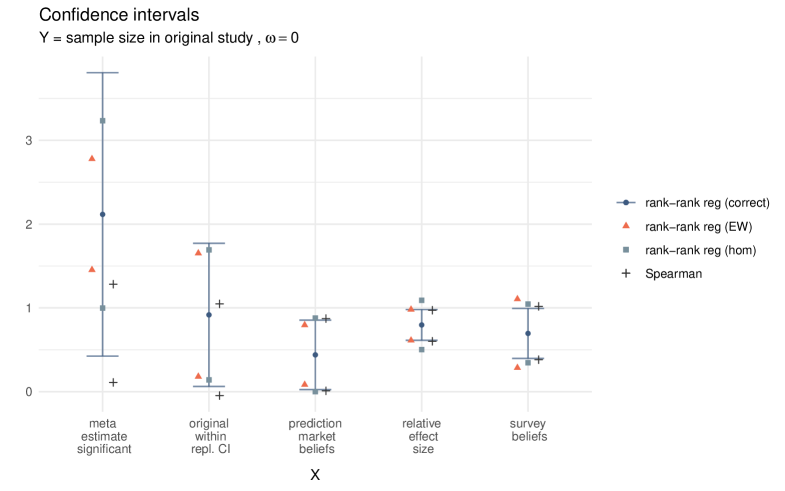

Figure 11 shows the ratios of the hom and EW standard errors divided by the correct standard error. A ratio above (below) one means that the hom or EW standard error is larger (smaller) than the correct one. The left (right) panel reports ratios for the rank-rank regression with being the p-value (sample size) in the original study.

Some of the hom and EW standard errors are close to, some are slightly smaller than but several are substantially larger than the correct standard errors. For instance, the hom standard error is about 2.5 times as large as the correct standard error for the measure “meta estimate significant” when is the sample size in the original study. Several of the other hom standard errors are about twice as large as the correct one. The EW standard errors tend to be smaller than the hom standard errors, but may still be substantially larger than the correct one. Several of them are about 50% too large.

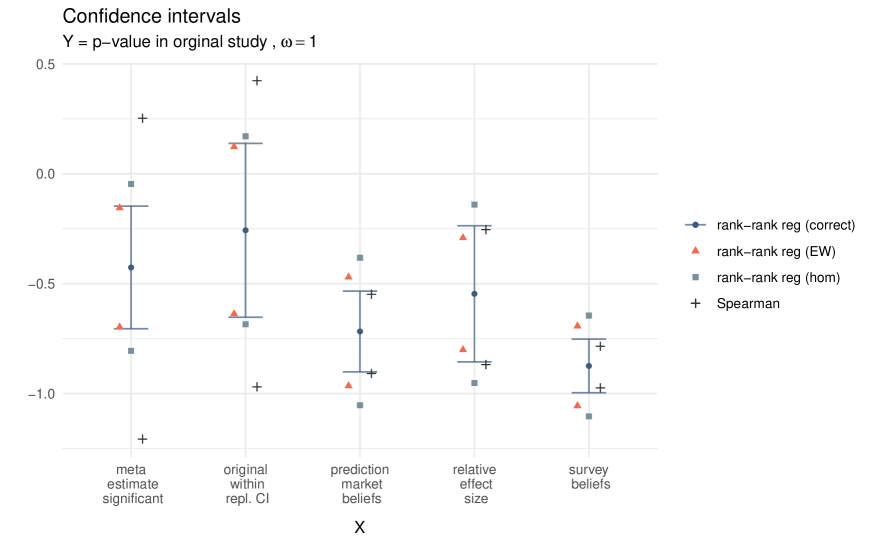

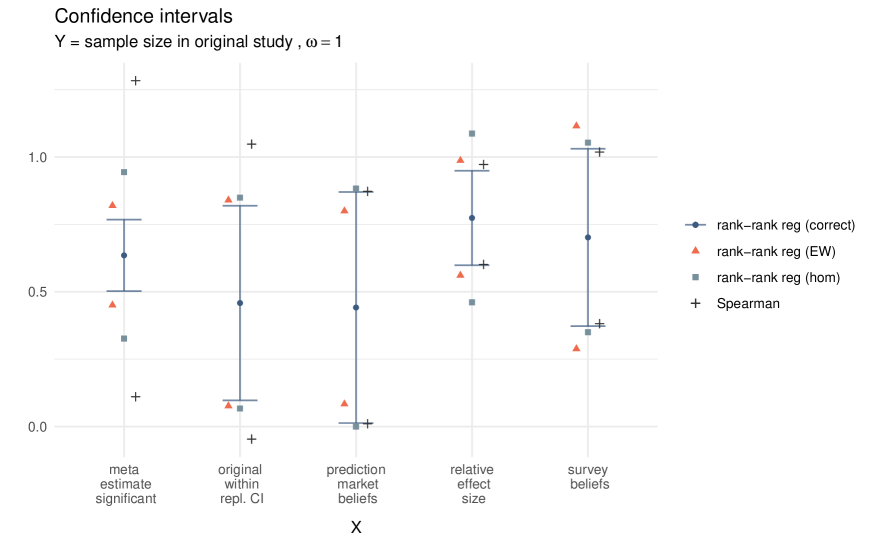

The differences in standard errors translate into differences in confidence intervals for the rank-rank slope. Figures 12 and 13 show 95% marginal confidence intervals for the rank-rank slope for the two different outcomes. In several cases, the hom confidence interval is substantially larger than the correct confidence interval. For instance, when is the sample size in the original study and is the measure “meta estimate significant”, the hom confidence interval is about twice as long as the correct one. The EW confidence interval is also too long, but to a lesser extent.

Figures 21 and 22 in the Appendix show the confidence sets when ties are handled differently, i.e. . In that case, several of the hom and EW confidence intervals are substantially shorter than the correct ones. The confidence intervals are more sensitive to the choice of how ties are handled when has fewer support points. The differences are largest for the measure “meta estimate significant”, which is a binary variable. The figures also show the confidence intervals for Spearman’s rank correlation based on Hoeffding’s theory that assumes and have continuous marginal distributions (i.e., based on the asymptotic variance in (4)). These intervals are centered at a different value than the intervals for the rank-rank slope, illustrating the fact that pointmasses in the distributions of and/or imply that the rank-rank slope is not equal to Spearman’s rank correlation. In addition, the confidence intervals for Spearman’s rank correlation are not valid in the presence of pointmasses.

References

- (1)

- Acciari et al. (2022) Acciari, P., A. Polo, and G. L. Violante (2022): “And Yet It Moves: Intergenerational Mobility in Italy,” American Economic Journal: Applied Economics, 14, 118–63.

- Bickel and Freedman (1981) Bickel, P., and D. Freedman (1981): “Some asymptotic theory for the bootstrap,” Annals of Statistics, 9, 1196–1217.

- Borkowf (2002) Borkowf, C. B. (2002): “Computing the nonnull asymptotic variance and the asymptotic relative efficiency of Spearman’s rank correlation,” Computational Statistics & Data Analysis, 39, 271–286.

- Bratberg et al. (2017) Bratberg, E., J. Davis, B. Mazumder, M. Nybom, D. D. Schnitzlein, and K. Vaage (2017): “A Comparison of Intergenerational Mobility Curves in Germany, Norway, Sweden, and the US,” The Scandinavian Journal of Economics, 119, 72–101.

- Camerer et al. (2016) Camerer, C. F., A. Dreber, E. Forsell et al. (2016): “Evaluating replicability of laboratory experiments in economics,” Science, 351, 1433–1436.

- Carneiro et al. (2023) Carneiro, P., Y. Cruz Aguayo, F. Salvati, and N. Schady (2023): “The effect of classroom rank on learning throughout elementary school: experimental evidence from Ecuador,” Working Paper CWP19/23, CeMMAP.

- Chatterjee (2023) Chatterjee, S. (2023): “A survey of some recent developments in measures of association,” arXiv:2211.04702.

- Chernozhukov et al. (2022) Chernozhukov, V., J. Escanciano, H. Ichimura, W. Newey, and J. Robins (2022): “Locally robust semiparametric estimation,” Econometrica, 90, 1501–1535.

- Chetty et al. (2022a) Chetty, R., J. Friedman, N. Hendren, M. R. Jones, and S. R. Porter (2022a): “Replication Data for: The Opportunity Atlas: Mapping the Childhood Roots of Social Mobility,” https://doi.org/10.7910/DVN/NKCQM1.

- Chetty et al. (2018) Chetty, R., J. N. Friedman, N. Hendren, M. R. Jones, and S. R. Porter (2018): “The Opportunity Atlas: Mapping the Childhood Roots of Social Mobility,” Working Paper 25147, NBER.

- Chetty et al. (2011) Chetty, R., J. N. Friedman, N. Hilger, E. Saez, D. W. Schanzenbach, and D. Yagan (2011): “How Does Your Kindergarten Classroom Affect Your Earnings? Evidence from Project Star,” The Quarterly Journal of Economics, 126, 1593–1660.

- Chetty and Hendren (2018) Chetty, R., and N. Hendren (2018): “The Impacts of Neighborhoods on Intergenerational Mobility I: Childhood Exposure Effects,” The Quarterly Journal of Economics, 133, 1107–1162.

- Chetty et al. (2014) Chetty, R., N. Hendren, P. Kline, and E. Saez (2014): “Where is the land of Opportunity? The Geography of Intergenerational Mobility in the United States,” The Quarterly Journal of Economics, 129, 1553.

- Chetty et al. (2022b) (2022b): “Replication Data for: Where is the Land of Opportunity? The Geography of Intergenerational Mobility in the United States,” https://doi.org/10.7910/DVN/NALG3E.

- Corak (2020) Corak, M. (2020): “The Canadian Geography of Intergenerational Income Mobility,” The Economic Journal, 130, 2134–2174.

- de la Croix and Goni (2022) de la Croix, D., and M. Goni (2022): “Nepotism vs. Intergenerational Transmission of Human Capital in Academia (1088–1800),” discussion paper.

- Dahl and DeLeire (2008) Dahl, M., and T. DeLeire (2008): “The Association between Children’s Earnings and Fathers’ Lifetime Earnings: Estimates Using Administrative Data,” Discussion Paper 1342-08, Institute for Research on Poverty.

- Deutscher and Mazumder (2023) Deutscher, N., and B. Mazumder (2023): “Measuring Intergenerational Income Mobility: A Synthesis of Approaches,” Journal of Economic Literature, 61, 988–1036.

- Dudley (2002) Dudley, R. M. (2002): Real Analysis and Probability, Cambridge Studies in Advanced Mathematics: Cambridge University Press, 2nd edition.

- Dudley (2014) (2014): Uniform Central Limit Theorems: Cambridge University Press, Cambridge.

- Fang and Santos (2019) Fang, Z., and A. Santos (2019): “Inference on directionally differentiable functions,” Review of Economc Studies, 86, 377–412.

- Forsell et al. (2016) Forsell, E., M. Johannesson, C. Camerer et al. (2016): “Experimental Economics Replication Project,” osf.io/bzm54, Jun.

- Genest et al. (2013) Genest, C., J. Nes̆lehova, and B. Rémillard (2013): “On the estimation of Spearman’s rho and related tests of independence for possibly discontinuous multivariate data,” Journal of Multivariate Analysis, 98, 214–228.

- Hoeffding (1948) Hoeffding, W. (1948): “A Class of Statistics with Asymptotically Normal Distribution,” The Annals of Mathematical Statistics, 19, 293 – 325.

- Klein et al. (2020) Klein, M., T. Wright, and J. Wieczorek (2020): “A joint confidence region for an overall ranking of populations,” Journal of the Royal Statistical Society: Series C (Applied Statistics), 69, 589–606.

- Mesfioui and Quessy (2010) Mesfioui, M., and J.-F. Quessy (2010): “Concordance measures for multivariate non-continuous random vectors,” Journal of Multivariate Analysis, 101, 2398–2410.

- Mogstad et al. (2023) Mogstad, M., J. P. Romano, A. M. Shaikh, and D. Wilhelm (2023): “Inference for Ranks with Applications to Mobility across Neighbourhoods and Academic Achievement across Countries,” The Review of Economic Studies, forthcoming.

- Mogstad and Torsvik (2023) Mogstad, M., and G. Torsvik (2023): “Family background, neighborhoods, and intergenerational mobility,” in Handbook of the Economics of the Family, Volume 1 ed. by Lundberg, S., and Voena, A. Volume 1 of Handbook of the Economics of the Family: North-Holland, Chap. 6, 327–387.

- Murphy and Weinhardt (2020) Murphy, R., and F. Weinhardt (2020): “Top of the Class: The Importance of Ordinal Rank,” The Review of Economic Studies, 87, 2777–2826.

- Nes̆lehova (2007) Nes̆lehova, J. (2007): “On rank correlation measures for non-continuous random variables,” Journal of Multivariate Analysis, 98, 544–567.

- Newey (1994) Newey, W. (1994): “The asymptotic variance of semiparametric estimators,” Econometrica, 62, 1349–1382.

- Ornstein and Lyhagen (2016) Ornstein, P., and J. Lyhagen (2016): “Asymptotic properties of Spearman’s rank correlation for variables with finite support,” PLOS one, 11, 1–7.

- Serfling (2002) Serfling, R. J. (2002): Approximation Theorems of Mathematical Statistics: John Wiley & Sons, Inc.

- Sharkey and Torrats-Espinosa (2017) Sharkey, P., and G. Torrats-Espinosa (2017): “The effect of violent crime on economic mobility,” Journal of Urban Economics, 102, 22–33.

- Song et al. (2020) Song, X., C. G. Massey, K. A. Rolf, J. P. Ferrie, J. L. Rothbaum, and Y. Xie (2020): “Long-term decline in intergenerational mobility in the United States since the 1850s,” Proceedings of the National Academy of Sciences, 117, 251–258.

- Ward (2022a) Ward, Z. (2022a): “Intergenerational Mobility in American History: Accounting for Race and Measurement Error,” American Economic Review, forthcoming.

- Ward (2022b) (2022b): “Internal Migration, Education, and Intergenerational Mobility,” Journal of Human Resources, 57, 1981–2011.

Supplementary Appendix (For Online Publication)

Appendix A Differences in Asymptotic Variances

A.1 Asymptotic Variances as Functionals of the Copula

Under the assumption that is continuous, all three asymptotic variances analyzed in Section 2 can be written as functionals of the copula . First, one can use results in Borkowf (2002) to show that

| (25) |

where

Second, since , the homoskedastic asymptotic variance of the OLS estimator can be written as

| (26) |

Finally, noticing that

it is clear that

is a functional of . Interestingly, all three variances depend on , and only on .

A.2 Optimizing the Difference in Variances Within Families of Copulas

This section provides details on the calculations of the maximal and minimal differences of variances presented in Figure 1. Specifically, we want to minimize and maximize the difference for . As shown in Appendix A.1, both variances depend on the copula of , and only on . To make this dependence explicit, we write and . Consider the maximization problem first. We want to solve

| (27) |

where is a family of copulas. We consider three families, the Gaussian family, the (Student-)t family, and one with quadratic dependence.

Denote by the bivariate Gaussian copula with correlation (both variances are equal to one, means are equal to zero). The Gaussian family is then defined as

Let denote a (Student-)t copula with one degree of freedom and dependence parameter . Then, the t family we consider is

Finally, consider the following “quadratic” data-generating process. , , where . Denote by the joint distribution of and by the copula of . Then, the quadratic family we consider is defined as

We want to solve (27) with being replaced by each of the three families as well as the corresponding minimization problem. These are optimization problems in the scalar parameter , which we solve by simulation combined with a grid search. First, we define an equi-distant grid of of size 200. For each parameter value on this grid, we then draw samples of size from the bivariate copula in with that parameter. Then, we compute the value of the objective function in (27) for each of these draws and then average over all Monte Carlo samples. Denote the maximizer on the grid leading to the largest value of the objective function by . The left graph of panel A in Figure 1 then plots the magnitude of (“correct”), of (“hom”) and the rank correlation of the copula in the given parametric family.

The black dots are computed as follows. In the data from Section 5.1, Los Angeles has a rank correlation of . For each of the parametric families, we can then find the parameter value so that the copula from that parametric family has a rank correlation equal to . Besides the value of , the dots then show the values of and for .

The right graph in panel A of Figure 1 plots the quantities for the copula that solves the minimization problem corresponding to (27). Panel B of the figure shows the corresponding graphs for the optimization problems with .

Figures 14–16 show the copulas that achieve the maximum and minimum of within the three families of copulas. The corresponding graphs for the EW variance look very similar and are not shown here.

Appendix B Asymptotic Theory for All Regression Coefficients

B.1 Rank-Rank Regressions

In this section, we present the asymptotic theory for all coefficients in the rank-rank regression model studied in Section 3:

| (28) |

where we had already introduced the equation projecting onto the other regressors in :

| (29) |

To study the asymptotic behavior of the coefficients , we now also introduce some additional projections. Let denote an element of and by the vector of all elements of except the -th. We now introduce the projection of onto and the remaining regressors : for any, ,

| (30) |

where are scalar constants and are -dimensional vectors of constants.

Assumption 8.

For , the random variable is such that .

Consider the OLS estimator in (11):

| (31) |

With the additional assumption and notation, one can derive the following joint asymptotic normality result:

Theorem 5.

B.2 Rank-Rank Regressions With Clusters

In this section, we present the asymptotic theory for all coefficients in the rank-rank regression model with clusters studied in Section 4.1:

| (32) |

where we had already introduced the equation projecting onto the other regressors in :

| (33) |

To study the asymptotic behavior of the coefficients , we now also introduce some additional projections. Let denote an element of and by the vector of all elements of except the -th. We now introduce the projection of onto and the remaining regressors : for any, ,

| (34) |

where are scalar constants and are -dimensional vectors of constants.

Assumption 9.

For and , the random variable is such that .

Consider the OLS estimator in (17):

| (35) |

With the additional assumption and notation, one can derive the following joint asymptotic normality result:

Theorem 6.

Theorem 2 already shows the asymptotic variance of . Similarly, for the -th component of , denoted by , we have

where

B.3 Regression of a General Outcome on a Rank

In this section, we present the asymptotic theory for all coefficients in the rank-rank regression model studied in Section 4.2:

| (36) |

with the projection equations (29) and (30). Consider the OLS estimator in (21):

| (37) |

Let , , , and be defined as in Theorem 3. For , further define ,

and

Finally, let .

With the additional notation, one can derive the following joint asymptotic normality result:

Theorem 7.

Theorem 3 already shows the asymptotic variance of . Similarly, for the -th component of we have

where

Appendix C Proofs

C.1 Proofs for Section 2

Define the sample counterpart to :

Before proving Lemma 1, we state and prove the following auxiliary lemma.

Lemma 5.

Let , , be an i.i.d. sample from a distribution with continuous marginals. Then for .

Proof.

Define , , and . Similarly, define , , and . Also, let . Note that by the Glivenko-Cantelli theorem (e.g., Theorem 1.3 in Dudley (2014)), . We will use this bound, as well as the elementary identity , several times without referring to them explicitly.

First, consider

Using the law of large numbers, we have

Furthermore,

Therefore, we have shown . Analogously, .

Second, consider

Here,

and so

since , . Also, by an analogous argument, . In addition,

by the law of large numbers and the bounds , , and .

Third, consider

Using the elementary identity , we have

Then, continue the proof similarly as for .

Finally, consider

Then, continue the proof similarly as for . ∎

Proof of Lemma 1.

Proof of Lemma 2.

Let be a constant and let be the cdf of a pair of random variables such that

Then

and

Hence, given that if and only if , the function in (14) satisfies

and

Therefore, given that by the discussion in a remark after Theorem 1, it follows that

On the other hand, by Lemma 1,

In addition, tedious algebra shows that

Thus, by Lemma 1,

Combining these bounds, we obtain that and as , yielding the asserted claim. ∎

Proof of Lemma 3.

Let be any distribution with continuous marginals and let be a pair of random variables with distribution . Letting and denote the corresponding marginal distributions, it follows that and are both random variables. Also, , where is the copula of . In addition, .

Consider first the case . By Lemma 1,

On the other hand, by (4),

| (38) | |||

| (39) |

Here, observe that

Thus, the expression in (38) is equal to

To bound (39), we claim that

| (40) |

Indeed, if , then

and so (40) follows. On the other hand, if , then

and so (40) follows as well, yielding the claim. Thus,

and, similarly,

Hence, the expression in (39) is bounded from above by

Therefore, , and so is bounded below from zero.

In turn, the case can be treated similarly. The asserted claim follows. ∎

C.2 Proofs for Section 3

The proof of Theorem 1 relies on a few auxiliary results, which are presented below. As in the main text, throughout this appendix, is fixed and the same in the definitions of , , , and .

Proof of Theorem 1.

By the Frisch-Waugh-Lovell theorem, the estimator in (11) can alternatively be written as

| (41) |

where

| (42) |

is the OLS estimator of a regression of on . Therefore, using and replacing in the numerator of (41) by ,

| (43) |

Thus, by Assumption 3 and Lemmas 9 and 10,

| (44) |

Consider the numerator. Define for all and

for all . Also, define , where the sum is over all six permutations of the triplet , for all . Note that is a symmetric function satisfying whenever . Moreover, let be the set of triplets in such that all three elements are the same, be the set of triplet in such that two out of three elements are the same, and be the set of triplet in such that all three elements are different. It is then easy to check that for all ,

and so

Therefore,

where the last line follows from the Lemma on p. 206 of Serfling (2002), whose application is justified since by Assumption 2. Furthermore, the results on p. 188 of Serfling (2002) imply that the U-statistic can be projected onto the basic observations. To compute the projection, note that, for ,

Denoting , we thus have , and so

Therefore, the central limit theorem (e.g., Theorem 9.5.6 in Dudley (2002)) implies that the numerator of (44) is asymptotically normal with mean zero and variance . By Lemma 9, the denominator of (44) converges in probability to , so that Slutsky’s lemma yields the asserted claim. ∎

Proof of Lemma 4.

First, we prove that

| (45) |

To do so, observe that

by Assumption 2. Hence, it follows from Lemma 11 that (45) holds if

| (46) |

In turn, by the triangle inequality, , where

We bound these three terms in turn.

Regarding , we have and by Assumption 2. Also,

by Lemma 7, Theorems 1 and 5 and Assumption 2. In addition,

Regarding , we have by the triangle inequality that

where

Also,

under Assumption 2 by Lemma 8 and the triangle inequality. In addition, for all , denote

Then

by Theorems 1 and 5 and Assumption 2;

by Lemmas 6 and 7 and Assumption 2;

by Assumption 2. Hence, by Lemma 12,

Combining presented bounds gives .

Lemma 6.

Under Assumption 2, we have .

Proof.

Lemma 7.

We have and .

Proof.

By the Glivenko-Cantelli theorem (e.g., Theorem 1.3 in Dudley (2014)), . Also, by the Glivenko-Cantelli theorem applied to ’s instead of ’s, . The first claim thus follows. The second claim follows from the same argument. ∎

Lemma 8.

Proof.

Lemma 9.

Under Assumption 2, we have

Proof.

Lemma 10.

Under Assumption 2, we have

Proof.

Lemma 11.

For any vectors and , we have

Proof.

We have

by the Cauchy-Schwarz inequality. Also,

by the triangle inequality. Combining these bounds gives the asserted claim. ∎

Lemma 12.

For any vectors , , , and , we have

Proof.

For all , we have

Hence,

by the triangle inequality. Applying the Cauchy-Schwarz inequality to each term on the right-hand side of this bound yields the asserted claim. ∎

C.3 Proofs for Section 4

C.3.1 Proofs for Section 4.1

Proof of Theorem 2.